News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Koan

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Nah.

BioAmber was liquidated - they weren't purchased - so the NOLs are worthless - no one can use them.

Since there was a asset liquidation - the NOLs really are worthless and can't be used by anyone.

Nah.

It is in a stragetic buyer's favor (which is what the SISP sought to produce), to acquire a target company in a "liquidation sale process" scenario. This provides certain benefits, e.g. certain tax and confidentiality benefits to name the obvious ones, that would not otherwise be present if acquiring a target company under a SISP.

It's about value creation.

While it is tempting to think about this entire process with BioAmber in the fashion of a barnyard auction -- because after all, thinking of BioAmber's restructuring in such a manner requires the least amount of brainpower -- there are far too many complicated aspects involved to treat of this situation with a mere cursory glance.

Shares are safe.

Nah.

The SISP is not a "transaction". It is a process. This would be evidenced by what it is called, i.e. "Sale and Investor Solicitation Process".

Next.

And the restructuring is almost complete. It has resulted in an empty shell with $80+M of debt that the company with no operations cannot pay. The completion of the proceedings will restructure BioAmber into oblivion when the remaining unpaid debt and the equity are discharged by the judge.

BioAmber filed for Chapter 11 restructuring to facilitate the orderly sale and/or restructuring of the company that was already planned long in advance. This was not a forced sale of assets, BioAmber was not caught by surprise, and there is no court order anywhere, in the US or Canada, citing any forced sale of any kind whatsover.

Chapter 11 was subsequently dismissed, terminated, and moved to the even more flexible CCAA with Chapter 15 recognition order. Under CCAA, Stay of Proceedings can continue indefinitely and provides the most leeway in terms of a Plan Of Arrangement or restructuring.

PwC, as court appointed monitor via the Canadian Superior Court, provides updates and speaks to topics that are within their legal purview. Shares are with BioAmber Inc.; PwC has made no explicit statement regarding the plan for shares; e.g. using only words such as "anticipate" in regards to future transactions.

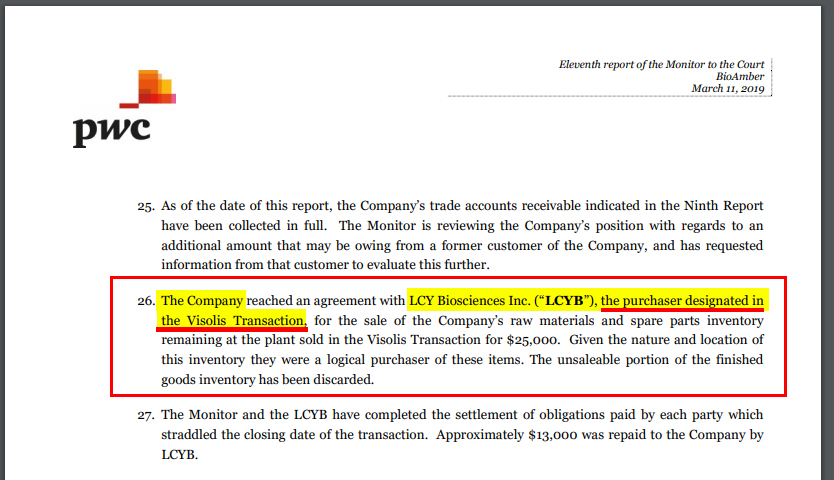

Shares are safe.

Nah.

The entire purpose of Chapter 15 is to collaborate with other countries on a single beneficial outcome. It is not a disjointed or separate process.

Nah.

Chapter 15 is a foreign main proceeding (versus a nonmain) with the CCAA in the driver's seat. The US courts are rubber stamping the restructuring plan occurring within the context of the CCAA.

For every piece of DD that has been posted there is an equal amount not posted. A lot of smart people are on this and have chosen not to give away their hard work for free; there is enough information from PwC and elsewhere that strongly indicates shares are safe.

As has already been stated, this is a complex restructuring under the CCAA.

Shares are safe.

And yet, it's updated.

And this:

Nah.

The NOLs absolutely have value when the business continues as a going concern.

That is why profitable companies don't run around and buy up distressed companies only for tax benefits. It's illegal. They have no interest in continuing the business. In that hypothetical instance they would only be interested in what essentially would be free money. Basically, paying a few dollars to take advantage of the losses of another business, to then not have to pay taxes for their own business.

So, they obviously can't do that.

However, in this case, LCY Biosciences "LCYB" is going to continue the business, (namely the production of bio-based succinic acid) - see "Letter of Intent for Investment in BioAmber Inc." from the Monitor's Sixth Report), such that BioAmber's NOLs will retain their value and can be utilized for tax benefits.

"Secret" is something not known to exist, i.e. it is hidden. Therein lies the inherent definition of "secret".

"Not publicly disclosed" is something known to exist, but not specifically divulged.

For example, the LCY Letter affirming the Letter Of Intent For Investment In BioAmber is not a secret. It exists, however, it has not been publicly disclosed.

Regulation FD is limited in its use and Rule 10b-5 must be in connection with the purchase or sale of any security.

Given the context of the CCAA with a Stay of Proceedings in Canada and Chapter 15 Recognition Order rendered by the Delaware court in the US, coupled with the fact that PwC is not buying or selling shares of BioAmber, neither of these two regulations and rules apply.

Yes, there have been many arguments from authority.

Unconvincing.

Actual court documents and at-length explanations connected to Bioamber citing specific SEC "regs" and laws that would demonstrate said understanding is notably absent.

The synonymous rebuttal is simply this:

People who understand the history of BioAmber and the subsequent restructuring process know the shares are safe.

Nah.

Two notable things not disclosed, among many others:

1. The letter from LCY Chemical affirming the Visolis Letter Of Intent for Investment In BioAmber

2. The "Transaction Process" as referenced by PwC in the Request For Binding Offers

Also, let's not forget the most obvious, written in bold right on PwC's website:

"FOR EFFICIENCY AND CONFIDENTIALITY PURPOSES, THE MONITOR CANNOT RESPOND TO THE MANY QUESTIONS SUBMITTED BY BIOAMBER'S SHAREHOLDERS." - PwC

Even the concept, "Everything is disclosed" would require the belief that this entire process has been 100% transparent, which it has not. However, since it is ongoing, it is possible that transparency will exist, albeit over a longer period of time, such that some answers and information will come to light at future date.

Shares are safe.

Under normal circumstances.

There is a grand canyon of difference between "secret" and "not publicly disclosed".

Correction ... Debtors no longer have legal representation.

The Joint Venture Is Now Complete

But we now know the SISP failed and no offers were received for a restructuring or reorganization...so it moved to liquidation...and the results of that have been completely, and specifically, disclosed.

What precisely is the totality of BioAmber Inc.'s liabilities? The remaining liabilities will be discharged and the common shares cancelled.

This question has never been answered, or even close to answered, from those claiming shares will be cancelled.

In fact, the entire premise that shares will be cancelled hinges on and relies on this single unsupported hypothesis; namely that BioAmber Inc. has liabilities (of unknown X amount), that said liabilities will not be satisfied, and that as a result they will be discharged.

In order for this argument and line of reasoning to bridge the gap between only so much air to one that is convincing, one must support their position with actual numbers and, ideally numbers and documents, i.e. empirical evidence.

FINRA already contacted US counsel back in OCTOBER, over 4 MONTHS AGO.

"The Monitor's U.S. counsel has also responded to queries from FINRA regarding the progress of the CCAA proceedings and the results of the sale process."

- Marc Duchesne

BLG

Borden Ladner Gervais

November 2, 2018

KKR Expands Renewable Energy Portfolio

Acquiring BioAmber fits in perfectly with KKR's renewable energy acquisitions.

https://www.businesswire.com/news/home/20190304005504/en/KKR-Expands-Renewable-Energy-Portfolio-Investment-NextEra

Yes.

Great news!

The Chapter 11 was dismissed to allow a restructuring plan under the CCAA, which is recognized as a foreign main proceeding by the Chapter 15 recognition Order rendered by the Delaware court.

The Canadian subsidiaries are the main center of business, namely BioAmber Sarnia Inc. BioAmber Canada Inc. is the other subsidiary. The bulk of liabilities are with BioAmber Sarnia. The patents, trade secrets, and other IP are held with BioAmber Inc.

The US parent company is BioAmber Inc., over which PwC has little or limited purview, and for which they either cannot or refuse to make direct, absolute or definitive statements.

FINRA has already made inquires themselves as far back as October. PwC saying they contacted FINRA in the Tenth Report is redundant and only for the purposes of disseminating information that is within their purview, i.e. the CCAA proceedings.

This is in reference from the Tenth Report to what PwC informed the courts the Company owed at the outset of the CCAA proceedings.

PwC did not break it down per company. As per PwC's definition of "Company" (with a capital "C"), it necessarily includes all three entities, the two Canadian subsidiaries and the US Parent; i.e. BioAmber Canada, BioAmber Sarnia, and BioAmber Inc.

Most of the liabilities are with BioAmber Sarnia.

Well then this is what it will all come down to, as the Motion for Extension filings shows Section 4 and 5 of the CCAA -- if PwC made sufficient arrangements with secured and unsecured creditors within the CCAA process, when it goes to Delaware there will be nothing for the US court to expunge and, therefore no need to cancel shares.

In other words, in order for shares to be cancelled by the US Courts, the creditors must not be satisfied, but if they have made these arrangements, again under sections 4 and 5 of the CCAA as indicated in the Motions, (which may include longer term agreements), the US courts will only have to sign off and there will be no need to cancel equity.

This is the part that is unclear and continues to be unexplained:

"But the CCAA should close soon. At that point, the US Bankruptcy Court will discharge the remaining unpaid liabilities"

FINRA has already inquired themselves in October about the CCAA proceedings. The tenth report does not indicate when FINRA correspondence occurred. FINRA is aware and has been aware of these proceedings for over 3 months, including after the closing of the Visolis Transaction.

What specific creditors or entities are impaired from the company BioAmber Inc., and by what amounts?

There has been a lot of discussion on the impairment and relief of two other companies, i.e. BioAmber Sarnia Inc. and BioAmber Canada Inc., however, the shares are not with those companies.

As the shares are with BioAmber Inc., how much debt remains with that company?

This is a cross-border case involving three companies. Two Canadian companies and one US Company. PwC was appointed Monitor by the court under CCAA that is recognized as a "foreign main proceeding" by the Chapter 15 Order rendered by the Delaware court.

It is clear by all of the court documents to date, the service lists, the Monitor's reports, that BioAmber Inc. is not within PwC's legal purview.

The Notice to Creditors from PwC only includes BioAmber Sarnia and BioAmber Canada.

The current Service List provided by PwC does not include the US Attorneys representing BioAmber Inc., namely Laura Davis Jones and Colin R. Robinson of Pachulski Stang Ziehl & Jones LLP.

The question is, how much debt does each of the three companies have independently of each other, BioAmber Canada, BioAmber Sarnia, and BioAmber Inc.?

Additionally, what security interests (if any) does any given creditor from the subsidiary companies, i.e. BioAmber Sarnia or BioAmber Canada have over BioAmber Inc.?

And finally, what debt and/or security interests will remain (if any) with BioAmber Inc. upon the closing of the CCAA proceedings?

It's these types of complicated and messy questions for which there is a reluctance to answer.

PwC Made The Following Statement:

PwC defines the "Company" (where capitalized) in all of its reports, including the Tenth Report, as follows:

From the Tenth Report, here is #16, the "No transactions..." statement:

![]()

Now, this statement written out in long form (using only PwC's own definitions contained within the same document), reads exactly as follows:

"No transactions involving the shares of BioAmber Canada Inc. and BioAmber Sarnia Inc. and BioAmber Inc. or BioAmber Canada Inc. or BioAmber Sarnia Inc. have occurred nor are anticipated. The monitor does not anticipate that the shares of BioAmber Canada Inc. and BioAmber Sarnia Inc. and BioAmber Inc. or BioAmber Canada Inc. or BioAmber Sarnia Inc. have any net realizable value for creditors."

Quite the mouthful and...

Of course they don't have any value! Shareholders don't own shares in BioAmber Canada Inc. or BioAmber Sarnia Inc. PwC attached the subsidiaries via their own definition to BioAmber Inc.(the only company in which shareholders own shares), such that the statement will be true insofar as we do not own shares in the subsidiaries!

At no time has PwC separated out BioAmber Inc. in singularity and made a statement about the outcome of shares in BioAmber Inc.

Period.

One likely reason is that PwC is making every effort to maintain Confidentiality Agreements while at the same time only speaking within the context of what they are legally required and that is "within the Monitor's purview", as they also stated precisely that in the Tenth Report.

Yes!

This is an example of the word games that are necessary when one is attempting to make true statements while simultaneously not making certain information public.

The subsidiaries of BioAmber Inc. are BioAmber Sarnia and BioAmber Canada.

BioAmber Sarnia and BioAmber Canada are Canadian companies. BioAmber Inc. is a US Company.

WORD GAMES | PwC, The 10th Report

In contracts and legal agreements, words have meaning. Credit card agreements, home loans, Operating Agreements -- they are written with words that are structured in such a way as to form the foundation of each party's responsibility. The courts make judgements on such agreements on the basis of what is inside the four corners of those documents. Some words might have a variety of interpretations, but there are other words which are non-interpretable and stand the test of time. The most common of these types of words are coordinating connectors, and two of the most relied upon are "and" and "or".

Coordinating Connectors -- "AND" versus "OR":

A conjunction is a compound statement formed by joining two statements with the connector "and".

A disjunction is a compound statement formed by joining two statements with the connector "or".

A conjunction is true if and only if both of its combined parts are true.

A disjunction is true if at least one of its combined parts is true.

Consider the following two statements:

Statement 1: The ball is blue and green.

Statement 2: The ball is blue or green.

The ball is blue.

Therefore:

Statement 1 = false

Statement 2 = true

Given that, below are four statements made by PwC in their Tenth Monitor's report in regards to the shares of BioAmber. It is worth noting that shareholders own shares in BioAmber Inc. Shareholders do not own shares in BioAmber Sarnia (a subsidiary), or BioAmber Canada (a subsidiary).

Here are the four statements made by PwC in the 10th Report:

Statement 1: [The Visolis Transaction] did not include the shares of Bioamber Inc. or any of the Company's subsidiaries, nor did it include the cash, accounts receivable or inventory of the Company.

Statement 2: No transactions involving the shares of the Company or its subsidiaries have occurred nor are anticipated.

Statement 3: The Monitor does not anticipate that the shares of the Company or its subsidiaries have any net realizable value for creditors.

Statement 4: The Monitor does not believe that holders of equity interests or equity claims of the Company, including shareholders of the Company, will realize any value in the CCAA Proceedings on account of their claims or interests.

So, let's break the compound statement Statement 2 into its parts. Remember, all of these statements are disjunctions (uses the connector "or") and it only requires one of its parts to be true in order for the entire statement to be true.

Part A: No transactions involving the shares of the Company have occurred nor are anticipated.

Part B: No transactions involving the shares of its subsidiaries have occurred nor are anticipated.

Again, in order for the entire statement to be true we only need one of those parts to be true. Well, Part B will always be true! Part A can either be true or false (it doesn't matter), and the entire statement will still be true.

All of the reactions to PwC's statements in the Tenth Report are in response to only Part A, as if that was the entire, singular and non-compound statement by itself. But it wasn't a singular statement. It was a compound statement and necessarily includes Part B, i.e. the subsidiaries. Again, Part A can be true or false (it doesn't matter), as long as Part B is true the entire statement will be true.

Part B is true.

It is my contention that PwC purposely included the subsidiaries in each of their carefully constructed compound statements in order to make the entire statement true. If they omitted the part in regards to the subsidiaries, or used the conjunction "and", then the statements would be false.

The same is true in regards to "equity interests or equity claims" compound statement.

Consider the following statement, if written like this:

"The Monitor does not believe that holders of equity interest and equity claims, including shareholders of the Company, will realize any value in the CCAA Proceedings on account of their claims and interests."

Completely different statement when the word "and" is substituted for the word "or". And this has drastic legal implications and meaning and this is what lawyers do for a living.

Do not think for one second that PwC's lawyers did not scour this document ten times over. They constructed these statements extremely carefully, they made them only in the context of their "purview" and with the additional awareness of third-party online reports. In other words, they are aware there are a lot of eyeballs on this report.

To conclude, the Tenth Monitor's report is the ultimate non-answer. To this date, PwC has not made a direct statement on the outcome of the shares of BioAmber Inc. For whatever reason, they continue to play word games and construct vague, indirect, and compound statements. Additionally, language such as "anticipate" and "believe" is exceedingly difficult to take seriously and only begs more questions.

There is not one single direct statement in the Monitor's Tenth report that definitively, without qualification or interpretation, details the outcome of the shares of BioAmber Inc.