But we now know the SISP failed and no offers were received for a restructuring or reorganization...so it moved to liquidation...and the results of that have been completely, and specifically, disclosed.

This is one of the chief statements being touted to support the position that shares ultimately have no value. However, it forever continues to stop short of acknowledging that the Retained Bidder(s) acquired post-SISP were of precisely the same nature, that is to say STRATEGIC BUYERS, as would have arisen if it occurred during the initial SISP.

In other words, the result produced was precisely the same as had it occurred during the initial SISP. Because these are CCAA proceedings, PwC is not beholden to their own chosen language and process, such that there is necessarily some extremely rigid legal mandate they must abide by in the event a buyer is not produced within any initial SISP. This is one of the fundamental purposes of the CCAA, that it provides maximum flexibility. If a stragetic buyer is not produced during a SISP, but one is produced at a later stage, this will be viewed as a positive result and successful exercise by the Canadian court, in order to benefit all of the Petitioner's stakeholders.

Indeed, that is the entire point and intent of these proceedings.

The strategic buyers are Visolis and LCY Chemical Corp. At the time of their Letter Of Intent For Investment in BioAmber, they did not yet have their joint venture in place. They only indicated to PwC they were "setting up a NewCo". This explains much of the vague language PwC uses in many subsequent documents, including the APA.

Consider the following from Appendix D in the Sixth Monitor's Report, titled "Visolis Transaction APA (Unredacted):

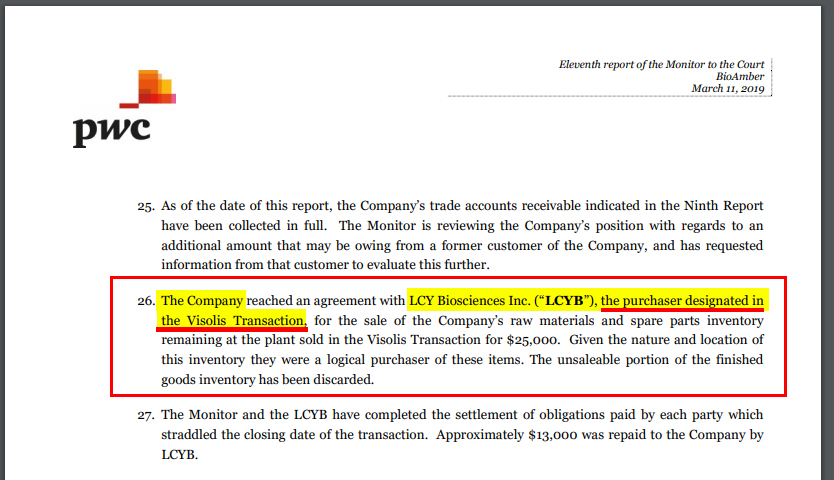

And now, a full six months later, from the 11th Monitor's Report:

Two things jump right out:

1. PwC says "The Company" reached an agreement, versus "PwC" reaching an agreement. This, of course, is because BioAmber Inc., BioAmber Sarnia, and BioAmber Canada, together designated as "The Company" (by PwC's own definition), remains intact, with PwC acting on the behalf of BioAmber and making material decisions, i.e. functioning as a surrogate in the absence of a board of directors.

2. PwC now defines the designated Purchaser as LCY Biosciences Inc., aka ("LCYB"). This, of course, is because the joint venture between Visolis and LCY Chemical is now complete.

Visolis plans to license proprietary technology to LCY Biosciences Inc., as indicated in their Letter Of Intent of Investment In BioAmber, "Apart from Succinic acid, we intend to product other higher value products with significantly higher margins at the Sarnia facility via licensing certain Visolis proprietary technology to NewCo." Visolis further states the role of LCY Chemical Corp.; "LCY's exstensive sales and operations in China can significantly accelerate adoption of [LCY Biosciences] Succinic acid."

Now, this begs the ultimate question:

Why would a buyer go through all of the trouble to explain the intentions and purpose of using purchased assets? In a straight liquidation of assets a Purchaser is under zero obligation to explain their intentions; they merely exchange funds for goods and each go their separate way.

The answer is because Visolis and LCY Chemical Corp. (LCY Chemical Corp. which is now owned by the collosal giant KKR), and having created the joint venture LCY Biosciences Inc. "LCYB", is (collectively) a strategic buyer whereby some material transaction of BioAmber Inc.'s shares must now occur.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.