News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

SFSecurity

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Hi Toofuzzy, Too right, you are!

It's a battle between hands off versus regulation thinking without finding a middle ground, alas.

Part of the problem with the FED is the thinking that it should provide guidance but not interfere too much in the day to day operations of the financial sector and that it is almost strictly hands off when it comes to some of the issues you raised. As far as I can tell the feeling around the FED is that issues like infrastructure are not in their purview even though they greatly affect the economy as a whole.

There were a couple of things that President Dwight D. Eisenhower that really helped the US economy, the primary one being the building of the US Interstate Highway system. If one looks at that alongside the economies metrics of the period one can see their intertwining as part of the "good old days" often referred to by our parents.

Now the pendulum has swung back to the "hands off, less regulation is best" school of thinking given Trump (even though he wants to spend big on infrastructure) and the current Congress so I'd be on the watch for the consequences that result, much like what happened a few years after the elimination of Glass-Steagall Act under Bill Clinton in 1999.

We'll see what happens, but, like Californians, we need to be prepared for the next major storm.

Best,

Allen

Hi Tom, Yes, quite interesting, and thanks for the pointer but, in my view the commentary about it is even more interesting, such as:

Walter Palmer

Researcher, Writer, Speaker: sustainable alternative fuels and climate; consultant

Danielle DiMartino Booth, I didn't read the whole article; I'm not a finance nerd. But the evident opening assumptions make a non-expert wonder: Most of us assume that national reserve banks should be busy at providing as much fiscal and monetary stability as possible -- within the bounds of the tools available. But the reserve banks don't control the private banking industry and they don't set banking regulation policy. The Fed may have reacted well, or not so well to the 2008 crisis--great discussion; go ahead and have it--but the Fed did not create or control a US banking industry that took itself, of its own delusional and pathologically greedy accord deep into the many and varied ways of selling unsecured credit as 'investment.' Look to the captain(s) of the ship (bank boards and executives) and the people who control their license (here's that word:) government, in order to prevent a recurrence. But look at what is happening now: with the new administration in power, the banks are right back at it; lobbying the government to rip all of the controls off of Wall Street. Steve Denning wrote a piece for Forbes two years ago pointing out how pathetically the (very necessary) financial services sector serves the larger economy: it is yanking literally hundreds of billions of dollars out of GDP and yet wants MORE. You can beat up on the stodgy, and (intellectually) conservative ways of a bureaucratic cornerstone; and you can suggest that academics' lack of 'real business' experience rendered them shortsighted, but let me ask this: As between the stuffy academics and economic theorists on one side, and multi-million-salaried commercial bankers on the other, who was actually looking farthest and most responsibly at the potential pitfalls of US banking practice in the period leading up to the 2008 tummy upset?

Hi Clive, Oh dear, it is so embarrassing to see ones typos highlighted by being quoted. Oh, well, goes with the territory I guess.

Anyway, thanks for your very informative post. I would love to see a copy of your spreadsheet, if you would. Please send it to: 60e20f21@opayq.com if you would.

I find it very useful to see how others approach a common issue because we all bring somewhat different perspectives based on our experience and the environment we live in. Can you imagine having the perspective of Lawrence of Arabia? I sure can't but I love getting it explained as it may give me a clue as to how to deal with a situation I now face, like where the market might go, in either direction, and how best to respond.

Anyway, I have a question about how you have approached the issue of a changing market. You say:

inflation adjusted US share price only (S&P500 index) monthly values as input (ignores dividends and cash interest on the basis that they broadly offset inflation).

Hi Tom, I just ran CCL from 1/2010 to 2/2017 and got 6.725% per year without dividends. Including dividends I got 8.313% per year.

B&H would have gotten 8.068% if you include dividends.

Best,

Allen

Hi AIM1979, Get drunk to kill the pain, eh?

Best,

Allen

Hi Gang, I came across something I had not heard about before, the S&P Global Luxury Index. It does not seem to have a symbol it can be tracked with but it can be seen at: http://us.spindices.com/indices/equity/sp-global-luxury-index#

In looking at it it hit its high point sometime in June of 2014 and it has been relatively steady in the high 1900 - very low 2000 range for the last bit.

The S&P Global Luxury Index is comprised of 80 of the largest publicly-traded companies engaged in the production or distribution of luxury goods or the provision of luxury services that meet specific investibility requirements.

If the wealthy aren't spend all that much perhaps they've been advice that the bull market is getting long in the tooth so they should watch their spending. Does this make any sense?Daimler AG DAI Consumer Discretionary

Diageo Plc DGE Consumer Staples

LVMH-Moet Vuitton MC Consumer Discretionary

NIKE Inc B NKE Consumer Discretionary

Richemont, Cie Financiere A Br CFR Consumer Discretionary

Bayer Motoren Werke AG (BMW) BMW Consumer Discretionary

Tesla Motors Inc TSLA Consumer Discretionary

Carnival Corp CCL Consumer Discretionary

Pernod-Ricard RI Consumer Staples

Las Vegas Sands LVS Consumer Discretionary

Hi Gang, Sometimes I think I'm all fumble fingers. I'm not exactly sure exactly how or when it happened but the year/month/week/day calculation was s#$%ed up when I was checking a possible position last night. Since the formula and how it works is a bit complex I'll just send new copies to all who want them. Drop me a note at: 60e20f21@opayq.com

Be sure to remember your Valentine tomorrow!

Allen

Hi cklow, If you like I'll review what you have. Send it to: 60e20f21@opayq.com

A point to remember is that AIM depends on volatility and if there is not enough and in a specific time period B&H could very well do better.

I just ran the dates that Toofuzzy suggested (1/2000 - 1/2013) for SPY and it does beat B&H and if you go to 12/2013 AIM beats the pants off of B&H with a ~64% gain versus ~32% B%H. This is using $20,000 position, 50% cash for AIM and a minimum sale of $1000 and 30% starting shares for buy/sell and 0% sell safe. Yeah, I know that the minimum share sell at 30% is way above the 5-10% that most refer to and in the book but if you use that you get ~3% less return for the period.

They both beat the S&P 500 over the 1/2000 - 12/2013 frame. AIM is 3.66%/year over the 13.917 years while B%H is 2.03% and the S&P 500 was 1.74%/year, starting at $1454.60 on 1/3/2000 and ending at $1848.46 on 12/2/2013.

If you go back to 1/2000 to 1/2013 then AIM beats the pant off of both B&H and the S&P 500 itself with ~44% over the 13 years. B&H is only 7.26% and the S&P 500 itself is 7.43% over the same time period. These translate into 2.85%/year for AIM, 0.54% for B&H and 0.55% for the S&P 500 itself.

AIM just beats inflation for the period which was somewhere between 2.35%/year and 2.42%/year, depending on the online calculator you use.

What all this goes to show is that backtesting is not always a reliable way of evaluating what position to get into for the long term.

Best,

Allen

Hi Toofuzzy, You're right. I meant to say bear market.

Best,

Allen

Hi Gang, what does everyone think about the $100/year for the Premium access to Investor's hub. Is it worth it?

Thanks,

Allen

Hi Gang, First of all I found a couple of minor errors in my modified AIM spreadsheet. Cell K8 should be =VLOOKUP(J9,V3:W6,2,FALSE), not V2.

Another thing is that one needs to enter the proper interval in cell G11 by hand to match J9, years, months, weeks, or days; otherwise you might get confused when you set J9 for calculation of the return over the interval you are studying.

Also in W3 it should be =W4*5, not 7 as there are only 5 days in a trading week.

Next, I've been looking at the volatility of various possible positions, especially ETFs/ETNs. Typically the 1x versions have much less volatility than bare stocks because of the diversity of their holdings. The 2x and 3x have more, TQQQ, as one example, has ~8% change up in price in the last 10 days, beta of 3.76 and SQQQ a change, down, of ~7% and a beta of 3.14. However, we know there is more risk in the leveraged ETFs/ETNs than the non-leveraged ones, like QQQ with a change up of ~2.4% in the last 10 days and a beta of 1.19.

Okay, why look at this? Because AIM looks for volatility to make money, as shown in the chart on page 64 of the 4th edition where there is a drop of 60% in three months followed by rise of 250% in the next three months. Only in a market crash do we get that down volatility, except when a company files for bankruptcy like VNR, and I've not seen that kind up in that short of time frame anywhere. Perhaps I've overlooked some but it is quite rare if it exists at all.

This chart is one of the limitations of Lichello's book, so I've been puzzling over what to do about this and have not come up with any good solution yet, perhaps there is none.

I've been looking at this with 50% cash, a range down from $10 down to $4.80 over 52 weeks and back up to $14 over 92 weeks, $0.10/week. I've been playing with the minimum share sale and the minimum $ amount which seems to work best around $900-$1000. At that amount one does not run out of cash as readily and it cuts the cost of trading.

What I do find is that Tom's use of 0% for the sell safe is quite a bit of help compared to the default of 10% but with the default 10% buy you still run out of money after 49 weeks. However, if you raise the buy safe to 15% you don't run out of money but you drop the return 5%. If you raise the minimum shares from 5% to 20% you raise the return ~2% and the optimal seems to be about 25%, which gets you ~5% more return over the same 146 week period than Tom's approach, almost 3 years, which gives you about 14% per year return better than the S&P 500 typically. However, 25% minimum stock sale is much more than the typical 5% or 10% usually called for. Maybe using LD-AIM is a better approach but I've not tried that.

However, the rate of change is still more than typical for most non-leveraged ETFs/ETNs.

Anyway, it seems that keeping our powder dry for the next while makes sense given the typical curve of the market, longer time up and shorter time down. Plus, using orcroft's, or other mechanisms, to delay buying during the slide down will put us in the best position to ride out the next bull market.

Best,

Allen

Welcome back, macprogrammer! I'm curious how you use AIM with options. Could you please explain?

Thanks,

Allen

Hi Firebird400, Sorry, not true: https://en.wikipedia.org/wiki/Percentage

Then there is this:

This is down the page at http://www.wikihow.com/Calculate-Percentage-IncreaseWhat is 250 as a percentage?

wikiHow Contributor

This completely depends on what the total is. 250 could be 100%. If it's out of 500,

then it's half, so 50%. If you drank 250ml of water out of a 500ml glass, you

drank half the water.

Hi Gang, As a goof I bought the book by Clem Chambers, the person who created the web site where this board is located that's a book form of his pay to view blog, "Be Rich - How to make 25% a year investing sensibly in shares - A real time demonstration." The introduction is quite funny in parts.

However, my question is, who is Tom Winnifrith? He is listed as "The sheriff of AIM" on a page plugging the newsletters at https://newsletters.advfn.com.

Best,

Allen

Hi Firebird400, Actually 50% of 100 is 50, not 25, which is 25%. So a 50% loss recovery requires a 100% gain. It's 50 + 50 which equals 100, the starting point.

Speaking of odd, 100% is usually represented as 1.00 as a multiplier, but if you multiply 50 by 1.00 the answer is still only 50! Yes, it is the amount you need to add to the baseline but..., one has to us 2.00 as the multiplier to get to 100 as a result of the equation; however, the result is only a 100% gain!

It is these type of conventions that sometimes make even simple math confusing. Calculus? Fergetit.

Best,

Allen

Hi Gang, Math can be so odd. From a base of 100 the DOW/stock market went up about 332% before the crash of '29 ending, roughly, in the middle of '33 at about 36. So an up of 332% is less than an 89% decline. In fact the low point is roughly 64% down from the baseline calculated the way I do. Calculated the way the online calculator does it it take a move up of about 278% to equal a baseline of 100

This one of the reasons I calculate a percentage down from the starting point rather than from an end point that is up 120% of the endpoint - (20% up) - to get to the baseline.

100 -20% = 80 the way I calculate it rather than 84 * 120% = 100 that the online calculator TooFuzzy created says.

After all 20% up from 100 equals 120, or 20 points, so why shouldn't 20% down equal 80, down the same 20 points as the amount up?

I think the way it calculates the down point is too soon. Granted, 20% down calculated this way is a significant correction, but then so is 20% up and ETFs only rarely move this much. This is why tighter buy/sell safe is needed, like Tom uses, 0% up and 10% down which makes sense when combined with a minimum shares to sell of 5%. This get you a buy at 87% of the current price and a sell at 105% of the current price, a total range about 18%, much more reasonable than a range of 40%, or 36%, of current price.

It also delays a buy more than a sell so we capture profits sooner and catch a lower dip.

Best,

Allen

Hi Firebird400, Thanks for the complete update. It helps my thinking going forward.

I noticed a tidbit in the paper this morning that might be worth looking into. Apparently when Pres. Trump dings a company its stock takes a bit of a dive. Haven't been following which companies have been his target. Have any of you noticed? And have the downturns been at all significant such that it might be worth a ride?

Best,

Allen

Hi Gang, Interesting article in today's SF Chronicle from the Houston Chronicle about Trump's travel ban straining Mideast oil ties. In essence it says it potentially creates problems with America exporting oil drilling, and such, gear as well as employee problems.

http://www.houstonchronicle.com/business/article/Travel-ban-frays-big-oil-ties-in-Middle-East-10895411.php?cmpid=gsa-chron-result

If this turns out to be true we might expect that oil prices will go up so we might want to see if oil is at a low point compared to the future and buy come positions for the forthcoming rise to allow some cash accumulation with sales dow the road a bit.

Best,

Allen

Thanks, Tom. SLW has already slid below my sell point and way below my next sell point so we'll see.

Frankly SLW kind of annoyed me as Canada changed the rules on taxation and I had 15% withheld in one account and 25% in the other of the dividends. I don't know, but I assume I'll get credit for that on my US taxes. We'll see.

Best,

Allen

Thanks, Ray, for the tip but I finally, sort of, found the problem with my hosts file. I had flailed around with it several times with no real progress but this time I went back to an older version and it now works. Now I need to figure out why it was a problem, and that is a problem in itself as there are 15,000+ lines to compare.

I think I got some malware a while back while visiting a web site that had been compromised that injected things into the hosts file but did not affect anything else given the various protections I have in place. No matter how many protections one has in place they are always a bit behind because they have to find the problems and update their scanning files to the new risks. Even heuristic approaches need updating for new hacks when some clever nut figures out a new hack.

Oh, well. Computers save us so much time, don't they?

Best,

Allen

Hi Gang, Got a sale of SLW at $21.75 but it went up to $22.13 and after market to $22.15. Missed out on $120. D$%^. The price of AIM advice was $21.56 and I looked at the volatility and set it a bit higher. Oh, well, could have gone higher but who knew.

Best,

Allen

Hi Firebird400, Truly bizarre! Yahoo f*&^s up again. The downloaded data from ca.finance.yahoo.com does not match that displayed on the page which is why I got different results than you did. When I scrolled through page I saw what you said, but when I downloaded it again I got the same results as before.

BTW, I still can't get to the US Yahoo finance page, no matter what browser I use and I have not been able to figure out why.

Best,

Allen

Hi Toofuzzy, Running as an "actual program" on a cellphone is a bit more complicated. What you have to do is save the page as "*.htm" and I'm not sure how that is done on the phone. However, one can save it to your computer and then import it into your phone and putting a link on one of your screens to the "*.htm" file. On my BlackBerry that's easy.

Best,

Allen

Hi Firebird400, You said CFBK but I don't find any data matching yours.

This what I got downloading it from ca.finance.yahoo.com and sorting it. (I still can't figure out why I can't get to the US version.)Date Open High Low Close Volume Adj Close

12/23/1999 16.875 16.875 16.500 16.750 1100 59.617

6/15/2004 16.000 18.000 16.000 16.210 3500 65.730

11/24/2003 15.870 16.180 15.480 16.140 900 64.610

12/31/2003 14.690 16.090 14.690 16.090 200 64.410

3/6/2000 15.875 16.000 15.875 16.000 500 56.948

12/22/1999 16.000 16.000 16.000 16.000 0 56.948

6/14/2004 13.660 16.500 13.130 15.990 3900 64.838

2/28/2000 15.938 15.938 15.938 15.938 100 56.725

11/21/2003 15.760 15.890 15.760 15.890 200 63.609

1/2/2004 16.100 16.100 15.810 15.880 100 63.569

3/3/2000 15.125 15.875 15.125 15.875 200 56.503

11/20/2003 15.590 15.850 15.000 15.800 1200 63.249

3/2/2000 15.750 15.750 15.750 15.750 0 56.058

3/1/2000 15.875 16.125 15.125 15.750 2200 56.058

2/29/2000 15.875 15.875 15.750 15.750 200 56.058

2/24/2000 15.750 16.125 15.750 15.750 1300 56.058

Hi Toofuzzy, Just open the web page in the browser (I use Firefox) on your phone and save it in bookmarks. I did that and it works just fine.

http://web.archive.org/web/20120609073103id_/http://www.aim-users.com/calculator.htm

Best,

Allen

Toofuzzy, It seems, unless they go bankrupt, it probably doesn't matter all that much when you buy as we "know" that oil is going to go up in price, but we don't "know" when that will happen, alas.

Best,

Allen

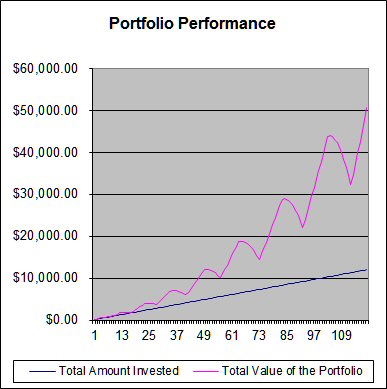

Hi Tom, Very pretty picture, indeed and 35% over 14 months is most excellent. Can't beat that with a stick.

BTW, what program is the top chart from?

Best,

Allen

Hi AIM1979, Yep, that is almost exactly what I do. I call it AIMCalc.htm. That is an HTML (Hypertext Markup Language) file. From what Toofuzzy has said in the past I thought it was an *.exe, *.py or some such file so in thinking about it and trying various possibilities I never got it to work that way but as a *.htm file it runs just fine.

Best,

Allen

Hi AIM1979, I don't read JavaScript so converting a combo of HTML and JavaScript to a stand alone program is beyond me, alas.

Best,

Allen

Hi Toofuzzy, What I mean is that it runs as an HTML file in my browser, Firefox. I do not go to the online calculator or anywhere on the Internet.

As to trying different extensions, way too many to try, over 1000 the last time I looked.

Could you send me a copy of what you have? Perhaps then I can put together a little sticky that outlines how to do it step by step.

Best,

Allen

Hi Toofuzzy, Yes, it is running as a web page. I never was able to get it to run as a program.

What extension does your file have? (name.???)

Best,

Allen

Thanks CanRay, I was thinking that it had to be some sort of computer program language since Toofuzzy has kept mentioning that he saved it to e-mail. I never thought to do it as a web page. Works great as a web page.

Best,

Allen

Hi lostcowboy, Got the same Google message as not being available in my country.

Best,

Allen

Hi Tom, Sorry, I haven't studied it in depth yet so whatever I say may well be in error. If you'd like a copy to exam, drop me a line at 60e20f21@opayq.com and it's yours.

Best,

Allen

Hey lostcowboy, It's okay. Money will do that to a person. ;O

Best,

Allen

Hi lostcowboy, All I got was:

Sorry! This content is not available in your country yet.

We're working to bring the content you love to more countries as quickly as possible.

Please check back again soon.

Hi Hedgebunny, Yeah, way overbought. Starting on the first of February, 2009, if the DOW was simply keeping up with inflation, the $7062.93 DOW would now be worth about $7945.76. no where near the nearly $20,000 of today.

Best,

Allen

Hi Toofuzzy, Thanks for the compliment but I haven't been around all that long, I just am used to researching things and finding things in hidden corners as an information security analyst.

One day I was at work consulting for a medical company, and doing my usual analysis of networks I came across ALL the records for the employees of a well known men's store, wages, credit card numbers, birth dates, medical histories, and on and on, all in plain sight unencrypted. The head of the security section had no, I mean NO clue it was sitting where it could be read by anyone at the medical company and outsiders if they did a very minimal hack. I wrote up my report and gave it to him. Then, a couple of months later I was meeting with a Vice President and the division head to discuss a further project and I asked how it was going on my previous report, It turned out that the security head had not told them about the results of my testing. Anyway, my point is that I've always had a nose for finding things and then, when it was ethical, keeping copies for my own reference. I kept nothing from that medical company. I even obfuscated the critical parts of the images in my report.

Best,

Allen

Okay Gang, I told ya'll that I had been serious sick starting a couple of years ago and only recently have I gotten some small portion of my brain capability and memory back. Well..., this discussion of Syncrovest and Twinvest tickled those few brain cells that hadn't gone on vacation and I remembered that I had downloaded copies of both but had had a problem opening them as they seemed to have been password protected and I stopped trying to look into the formulas.

If my memory serves me correctly I downloaded them from something connected to lostcowboy in some way that I don't recall nor do I recall where it was on the net, alas, so I can't point you to that repository. However, I saved copies. At some point I must have figured out how to open them as they don't seem to be password protected now.

So, if you would like copies of all the versions of both that I have, drop me a line at 60e20f21@opayq.com and they are yours.

Now, the differences between Syncrovest and Twinvest. It appears that Twinvest is primarily and update to Syncrovest and the results are that Twinvest does not go into negative territory after a few months - below amount of investment cash - whereas Syncrovest does. Also Twinvest gets better returns than Syncrovest. See the two images from the two spreadsheets below.

SYNCROVEST

TWINVEST

But the real winner is a modification of Twinvest labeled Twinvest Combo done by who knows, I sure don't.

All the same time frames and prices. WOW!!

Anyway, all the variations on Twinvest are on tabs of a single spreadsheet.

Best,

Allen

Hi Toofuzzy, Post #760 in SIG does not exist. However the formulas for Syncrovest are in post #73 - http://investorshub.advfn.com/boards/read_msg.aspx?message_id=309558 which you posted for lostcowboy back in 2002!

To make it easy here it is:

Lostcowboy asked me to post this explanation of Syncrovest.

Syncrovest: A simple explanation of how it works.(By the book)

1)Decide how much to invest = PLANNED INVESTMENT

(ex $100/month or $500/quarter)

2)Invest 3/4 of PLANNED INVESTMENT = BASE INVESTMENT

(ex $75)

3)Each month AVERAGE COST/CURRENT PRICE = MULTIPLYER

4)MULTIPLYER * BASE INVESTMENT = INVESTMENT 1 (that month)

(This is first gear)

AND if MULTIPLYER is > 1 THEN step 5

5)(MULTIPLYER - 1) * CASH RESERVE = INVESTMENT 2 (that month)

(This is second gear)(it is an additional investment to INVESTMENT 1)Do not invest more than 50% of remaining CASH RESERVE.

6)When INVESTMENT = 1/2 or less of PLANNED INVESTMENT use MULTIPLYER * PLANNED INVESTMENT (instead of Base Investment)You have made a 50% profit at this point.(You now use third gear)

7)When Using PLANNED INVESTMENT if INVESTMENT 1/2 or less of PLANNED INVESTMENT then SELL EVERYTHING

8)Start over with PLANNED INVESTMENT * MULTIPLYER and new AVERAGE COST.(This is fourth gear). You will now have lots of cash from the CASH RESERVE to invest on any future price drop.

When your investment is again < 50% of PLANNED INVESTMENT sell everything again and start with a new AVERAGE PRICE.

In practice when you have a sale you would sell everything but your FIRST periodic investment($100).(why sell it just to immediatly buy it back).

If SYNCROVEST is suitable it would be best in a retirement fund invested in a No Load mutual fund. Otherwise the broker fees and taxes could be substantial.

I hope this is the clearest and most concise description of SYNCROVEST ever written.

Still

Toofuzzy