News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

ChuckBits

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Rory the "word smith".

*

al·le·vi·ate

verb <-- (how ironic! It's a "verb")

past tense: alleviated; past participle: alleviated

make (suffering, deficiency, or a problem) less severe.

"he couldn't prevent her pain, only alleviate it"

*

Kind of like when someone is dying from cancer and in excruciating pain:

The doctor prescribed fentanyl to alleviate the pain...

Or

...management has alleviated substantial doubt about the Company’s ability to continue as a going concern.

Exactly. "2023" This confirms Melvin has created an AI time travel app!

I guess nobody else caught the date Melvin intends to file the annual?

Simple Riddle: Why does Melvin always file an extension?

Answer: Because he can.

I'm thinking the same. I believe the big catalyst will be the release of the "Time Travel App". If you look closely at the late notice report, the "hint" will be right there.

I stand corrected.

I agree, thanks again.

Thanks for that. I don't think I've ever seen a Q or Annual filed on a weekend or holiday? Are you saying if an alternative filer uploaded a report thru OTCIQ on a Saturday, we would see it on OTC Markets?

Leap year makes due date March 30th, Saturday, so bumped to Monday, April 1st... April Fools Day!

Not correct. Reports can not be filed on weekends or holidays. Since the due date of March 30th is a Saturday, it gets moved to Monday April 1st. Therefore, "if" an extension is filed, the due date becomes Monday April 15th.

I've said more than once I don't hold millions of shares like you & others claim to, and if ya'all do, that's fine. But money is money and the amount, small or large, is relevant to the individual.

Also, in case you didn't notice, I haven't made a negative post since my last beat-down weeks ago. I now know that only happy, shiny, positive, xanax posts are permitted on this board. There was nothing negative about GDVM in tonight's post either. I was simply breaking your balls regarding your silly "chart analysis" and based on the level of name-calling and anger your expressing, maybe "you" need help?

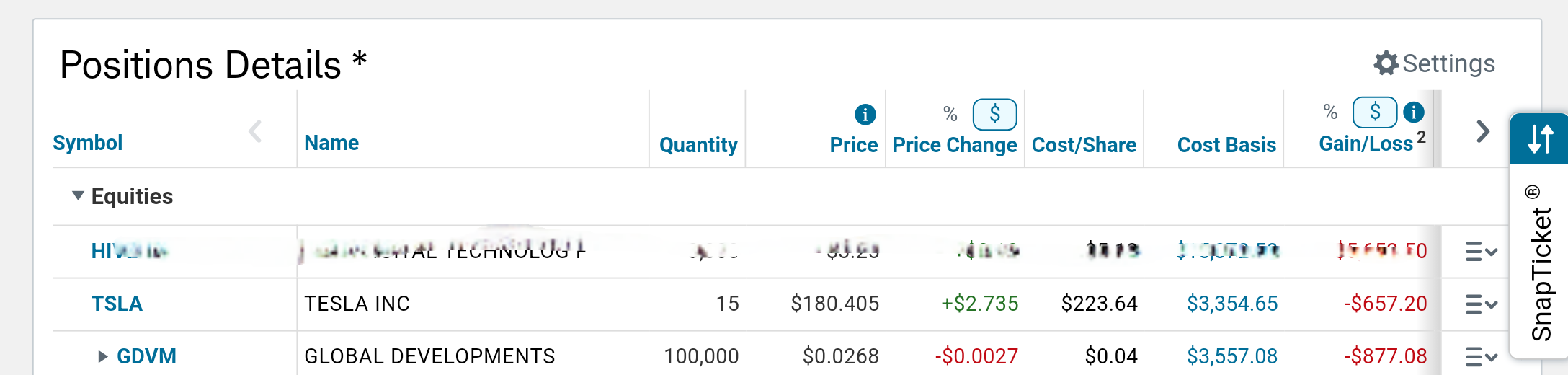

Anyway, the excerpt below is from my wife's Roth account thru Schwab. The "price" shown (PPS) is today's closing price. I started close to .06 cents pps.

Now get some rest.

Lol. I still have all my shares and I don't care that we're not above .03, yet. I don't expect much until some of the things we've all been expecting start to come to fruition. Hopefully this starts with the annual report.

You're the knucklehead who made the adament prediction based on a "chart signal", and then instantly snapped into a tough-guy bully when other peeps suggested to chill a bit, just like you snapped tonight!

Where's your confession "you" f'ed up & was wrong?

Lighten up

Who cares, we're above .03 now! There's NO stopping us!

Wasn't even thinking about "April 1st"! Could be a "fun day"...

PS I've been to an incredible number of concerts and yes, I'm still rocking!

Leap year so "day 90" is March 30, a Saturday. Do due date is Monday, April 1st. "If" an extension is filed, then Monday April 15th.

This is the one question I asked my accountant 20+ years ago before I hired him:

What is the sum of 2 + 2?

His answer:

.

.

.

.

"Whatever you want it to be"

OTC = 6.95

Schwab (from buying out TDA), but I haven't been trading it...

C'mon, I replied with a thumbs up 👍.

(And my last attempt at humor was political and we know how that went so I'll try to refrain from humor too)

Geeze, Sorry it bothers you that I have yet to sell any shares, & my pps is still above where we're trading. And the "sarcastic" post you replied to was for someone who posted only hate, i.e. silly name-calling. I tried to say earlier today I'll shut up & play along but people keep poking me. What would you do?

I've been on iHub for 10 years and have never experienced a board anything like this one...

PS Have a nice day

This is a really meaningful, useful, & well thought post too. So I'll reply with something to match your intelligence:

I'm rubber, you're glue, whatever you say bounces off of me and sticks to you.

I never intended & didn't think I was ripping on the company but since you & some others took it that way I'll need to accept it & drop it. Shutting up now, thanks.

Thanks for taking the time to make a thought out, detailed post. I don't want to dwell on this since it obviously annoys people so I'll just say I disagree with the significance of the "you know what risk", & I AM NOT saying it should be there. I do believe that it is holding back the stock's performance and will be very happy when it's gone.

Thanks for re-re-iterating what I said, in case you didn't understand:

No longer "seeking a merger", but "merged". Right? Like a year ago. WTF am I missing? So you're saying the shell risk risk will come OFF tomorrow & the stupid ticker will change too, right? Keep it up & I will too.

I'm sorry you interpreted my comment as ripping the company and I did NOT say or imply GDVM is a "shell". My bad if I wasn't clear but I can't help being honest. I simply "tried" to say the following:

1) The company profile/description has not changed. They updated 1 thing to say "they have merged", from "seeking a merger". The primary objective remains the same, which is good.

2) They have previously declared 25 employees. "If" this is new to the OTCM profile, fine, but it has been declared in other otc filings. And as I said, the number makes sense considering 4 locations.

3) Finally, the shell "RISK", not "shell". The "No Shell" as been declared by Melvin since day 1. Obviously OTCM doesn't take anyone's word alone. The subject has been discussed many times here, perhaps while you were on sabbatical? The concensus is an annual audit will be required to remove the shell risk tag. I think many are expecting, or at least hoping an audit will be included with annual report, likely to come mid-April.

I knew OTC labeled it as a shell risk when I first bought shares in May. I am not the one calling it a shell, OTCM is calling it shell risk. I was hoping it would have been resolved before year end but accepted the need to wait. I'm sure I don't hold as many shares as most here claim but I have only added since May.

Would you not agree the stock can/will do so much better when that label is removed? Again, sorry I poked you. Hope this post is more clear?

Thanks for keeping it real...

1) Ok, "seeking a merger" to "merged". Should have said that a year ago, right? The rest is unchanged.

2) I'm certain I've seen "25 employees" months ago. Perhaps on the VeeMost website? At the time I thought "seems a bit of a stretch", but when you factor in 4 locations, it's reasonable. The number is simply a correction. If anyone really thinks they just QUINTUBBLED their workforce, clearly a PR is a day or 2 away, agree?

3) SHELL RISK = NO is a deja vu topic and Melvin has declared this since day 1. The issue is he can "say" whatever he wants, but obviously it needs to be proven!

I'm not bashing! At least the profile is being looked at and corrected but I see no "fundamental changes".

Peace out

Timing of your reply was missed by me, sorry, wasn't looking to "push you". Did you look at the company description in the GDVM "main notes, dd, links" area? (The stuff that "mods post")

Did you see my post 5 minutes ago?

The profile was simply "re-verified" by Melvin. The company description is exactly the same (look at it on the iHub DD/notes/links area), 25 employees is the same, as is his claim to "no shell". Nothing has changed...

You recognize humor 😄. Glad I didn't need to post the "next chart" I prepared just in case there was a "dump", uptrend is way more fun...

We're acquiring Nvidia! That's awesome!

Nobody's made a political post since Dolphins' respectful post regarding the matter about a day & a half ago. So keeping up with the latest standard of name-calling, whose being the idiots now?

Happy Presidents Day! Let's get to the "root causes" of the shell risk like Kamala Harris did to solve the immigration disaster!

"Pink disclosure annual report" along with an audit or whatever is needed to remove the shell risk. Sorry for mix-up...

No, currently in YAWN cycle...

Bro, I thought we covered this, like yesterday. So when you say "soon", do you mean like "Elon Musk will colonize Mars soon", like in the next 100 years? Or, like "if I don't find a bathroom soon, I'm gonna shit my pants"?

The next report, not "Q4", but "annual 10K", shouldn't be expected until mid APRIL.

Quote:

I think clowns are the ones who invest in a company then trash talk it. Sell the stock, or average down. It’s simple.

Well, that's your opinion, which is valid, and since this is an "opinion board", you're free to express it. I have averaged down from .055-.06 'ish to about .035. I don't have unlimited funds & there haven't really been opportunities for me to take any "profits". I also did the "smack the ask" thing recently at .019. You know, the thing that gets the momo going. How's that working for me?

My whiney, negative posts come after I read stuff like "very bullish", "great earnings coming soon", "Cisco Gold imminent", etc. I'm sorry but that makes me lose it!

Are you a sports fan by any chance? Suppose your NFL team is 2-10, your 5 year veteran quarterback sucks & just threw his 4th interception of the game. Do you yell at the people giving him shit & complaining, tell them to be patient and then go buy another of his jerseys & say "give him more time"? Or do you say "man, this guy sucks" & "the coach sucks too, replace them"?

PS, I don't plan on going anywhere until the 10K which better include an audit & remove the shell risk.

Cheers