News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Dragon Lady

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

STEM CELLS ARE DRUGS according the United Stated FDA, and are REGULATED AS SUCH- and to say otherwise IMO. is grossly in error.

The FDA on its own govt run website also says there is only ONE "FDA approved stem cell treatment/procedure" meaning ANY OTHERS would be illegal IMO, and apparently that of the FDA (unless they are under clinical trial protocols, according to the FDA website itself)

http://www.fda.gov/ForConsumers/ConsumerUpdates/ucm286155.htm

THAT is the FDA WARNING TO CONSUMERS about "un-regulated" so called stem cell "treatments"

http://www.ipscell.com/2014/12/breaking-new-fda-draft-guidance-views-fat-stem-cells-as-drugs/

"Breaking: New FDA Draft Guidance Views Fat Stem Cells As Drugs"

http://www.ipscell.com/2014/12/new-interview-with-fda-on-key-stem-cell-regulatory-issues-its-own-research/

"For example, in 2012-2013 there were numerous Warning Letters issued, but none in 2014 related to stem cells to my knowledge. It certainly seems that the problem of stem cell clinics is not going away so that’s not the explanation so less FDA action. If anything there are dramatically more of such clinics in the US now than in past years. Why is CBER not taking action?

FDA: As discussed above, CBER is actively working to develop guidance on the issues relating to SVF and other unapproved stem cell-based products. These guidances will offer necessary clarification with regard to HCT/P regulations.

As you know, FDA cannot comment on any potential actions or open investigations."

http://www.nature.com/news/fda-s-claims-over-stem-cells-upheld-1.11082

"FDA’s claims over stem cells upheld

Drug watchdog wins right to regulate controversial therapies."

http://www.the-scientist.com/?articles.view/articleNo/39108/title/Judges-Side-with-FDA-on-Stem-Cells/

"A US federal appeals court maintains that stem cells proliferated in a lab must be regulated as a drug."

Also, "stem cells are NATURAL", LOL !!! What? PLUTONIUM is "natural" too, LOL !! SO is oil and uranium and ultraviolet radiation and protons and alpha particles and 10,000 other poisonous or carcinogenic substances just as simple examples. What does it even mean to make a claim that something is "natural"????? EVERYTHING on planet earth is "made" or consists of the elements of the periodic table- and is therefor "natural", LOL !!!

Here's some famous cases of what were claimed to be "legal" so called "stem cell treatments" - well, the end result was a tad bit different according to the regulatory agencies involved in the end (what as the claim- that people are "very happy with the results", LOL???? WHAT "people"???? Who and where- who are these "people"?????):

Possible new ALL, ALL TIME LOW here soon it seems???

Bid/Ask both collapsed all into the .004s again now

0.0041 / 0.0049 (50800 x 504000)

Bid only .0041, HOLY COW !! LOADED still 10 to 1 to the Ask/Sell-side

All, all time low is .004 and it's a fraction, 1/100th of a cent off that now on the Bid, wowza??

In the next day or two- this might see the .003's for the first time in company history IMO- another "new record" for the books. Wow !

So the market cap is now barely holding $3 million lousy bucks against company debt/obligations of at least $11 MILLION known of as of last 10-Q (we don't even know the effects of the large lawsuit they just lost/settled for $1.7 MILLION approx that we know of- there's gonna be attorney costs and expenses on top of all that)

When that new 10-Q comes out in a few weeks- I'll do the "3 minute" read version first be looking for the following:

1) New O/S share count (aka how much more mass dilution has occurred?)

2) Cash on hand- how low is it? ($79K total bucks left previously, cash broke for all intents and purposes)

3) If any new toxic, floorless convertible debt deals were inked since the last 10-Q and if so, for how much and with what hedge lending firms

4) Have they made more draw-downs on the Magna dilution credit-line and if so for how much and when and how many shares have they issued to Magna

5) How many more dilution shares were paid-out since the last 10-Q for things like dilution lender convertible debt settlements, paying common bills like "accounts payable" etc

6) Any details on how the legal settlement of approx $1.7 MILLION is to be paid and how they expect to pay it, where they'll get the cash or is it dilution shares, etc

Those will be the "highlights" I'll be looking for when that SEC filing gets released. Should be very "telling" IMO.

My .0041 or so CENTS worth

.0044 DOWN 20%, HOLY COW !!! What happened??????

0.00440.0011 (-20.00%)

Real-Time Best Bid & Ask

0.0044 / 0.005 (11000 x 470000)]

That's thee OTC itself- it's bleeding red looks like to me?????? But, is this the "going big" thingy? I really can't "get it"??? .10 or .15 CENTS "SOON", no???????????????? The "vet thingy alone is like a $25 MILLION biz real "soon" cause they could supposedly do a "$1 MILLION mailer" thingy and some phone calls using a "ten person phone center" with like ONE PERSON handling it all, LOL !!!! No? Is that not working out yet or something? Any charts or graphs to show EXACTLY how the $25 MILLION revenues thing is going to "work", like EXACTLY? I'd sure like to see those? Fascinating IMO.

This sure is awfully, awfully close to the now all, all, all time LOW of .004 CENTS made almost exactly 2 months ago- about May 18th, 2015. It touched that new low twice. 2 months almost to the day- like maybe a dilution conversion "cycle"- timing thing seems to me maybe? Like when they (BHRT) perhaps make cash "draw requests" from ole Magna maybe or when the hedge firm convertible debt lenders like to convert- sorta on a "cycle" type of timing?

Pretty good volume already today- so this is taking a pretty solid beating in here looks like by the ole dilution MM's?? Wow.

My .0044 or so CENTS worth

Bid and Ask just DROPPED AGAIN?? HOLY COW !! .0047 only on Bid?????

0.0047 / 0.005 (250000 x 240000)

Wow!! ONLY the .004's again? But it was GOING BIG "soon", no?? What happened exactly? The .10 CENTS, no .15 CENTS "soon" thingy ?? Is this part of all that happening? Not sure I can see it here? Confusing?

Or, is this part of the "send out a $1 MILLION mailer" and then set up "10 people with phones in a call center" and get like $25 MILLION in "revenue" in like a real short time, using ONE PERSON cause "people will pay for their pets" thingy ? Is that what's happening now? Is there a chart or graphs and real numbers and all to actually show how that "works" exactly? I'd love to see the details- if that's what's really happening here? Cause the common share price just doesn't quite seem to match all that yet?????????

I mean- solid Bid back in the .004's again? Wow? Holy cow- how is that possible if the market cap is gonna be like $1 BILLION, no it was $2 BILLION "projected" by end of 2015, and now it's passing mid July already???? The real market cap in reality is about 734 million shares X .0049 = $3.6 MILLION lousy bucks (against immediate obligations/debts of like $11 MILLION) - so I guess I'm not totally "getting it" when or how exactly this $2 BILLION market cap thingy happens in a few short months from now, LOL ????

http://www.sec.gov/Archives/edgar/data/1388319/000114544315000630/bioheart_10q.htm

From the most recent 10-Q SEC filing:

PAGE 11:

" GOING CONCERN MATTERS

The accompanying unaudited condensed financial statements have been prepared on a going concern basis, which contemplates the realization of assets and the satisfaction of liabilities in the normal course of business. As shown in the accompanying unaudited condensed financial statements, during three months ended March 31, 2015, the Company incurred an operating loss of $1,048,217 and used $384,251 in cash for operating activities. As of March 31, 2015, the Company had a working capital deficit (current liabilities in excess of current assets) of approximately $11.0 million. These factors among others may indicate that the Company will be unable to continue as a going concern for a reasonable period of time.

The Company’s existence is dependent upon management’s ability to develop profitable operations and to obtain additional funding sources. There can be no assurance that the Company’s financing efforts will result in profitable operations or the resolution of the Company’s liquidity problems. The accompanying statements do not include any adjustments that might result should the Company be unable to continue as a going concern."

PAGE 25:

"Our Ability to Continue as a Going Concern

Our independent registered public accounting firm has issued its report dated March 16, 2015, in connection with the audit of our financial statements as of December 31, 2014, that included an explanatory paragraph describing the existence of conditions that raise substantial doubt about our ability to continue as a going concern and Note 2 to the unaudited financial statements for the period ended March 31, 2015 also describes the existence of conditions that raise substantial doubt about our ability to continue as a going concern."

PAGE 33:

"At March 31, 2015, we had cash and cash equivalents totaling $70,974. However our working capital deficit as of such date was approximately $11 million. Our independent registered public accounting firm has issued its report dated March 16, 2015 in connection with the audit of our financial statements as of December 31, 2014 that included an explanatory paragraph describing the existence of conditions that raise substantial doubt about our ability to continue as a going concern and Note 2 of our unaudited financial statement for the quarter ended March 31, 2015 addresses the issue of our ability to continue as a going concern."

I mean- that's a whole lot of "GOING CONCERN WARNINGS" and a little ole wee bit of cash is seems to me, to do a "ONE PERSON $1 MILLION mailer" thingy or be a "$2 BILLION market cap SOON" and all??? NO?? Not sure I "get it"?? Makes no sense to me?????

My .0049 or so cents worth

Hit the $4's again this AM, UH OH????????????????

Is this the "big institutions" are "accumulating" thingy or is it "big institutions" that really like sorta somehow are "stealth buying" where they "know how to keep the price down" while secretly "accumulating" huge amounts of shares while not "alerting others", LOL !!!

Not quite sure I'm "seeing it" or "getting it" here???

Looks like a classic ole warrant laced, weak, dilution SECONDARY playing out to me?? Personally, I've seen it Soooo many time before on these dilution micro-cap plays. Just shorting and selling by the very hedge firms and underwriters who buy and pitch and then unload these weak financing deals, coupled with NO TRIAL(S) starting to date, and no prospect of a product or revenues for years to come. The Nasdaq is home of the BIG BOY pro shorts- they're merciless. The concept that "getting off the OTC" was somehow a free ride to "stability" and a certain price increase never made any sense to me personally? The Nas is where serious shorting got perfected to a fine art/science and HFT (high frequency) and automated trading and share-crusher hedge firms were invented and make their livings IMO.

This is just a cash poor, no product, highly speculative "single micro sized trial data", high dilution bio-play getting run through the classic hedge firm and short crushing machine IMO. Not much more complicated than that to me?

Meanwhile- ISSUE MORE "PR" about whatever- mice "studies" and "conferences" and "presentations" and a "patent" a blah, blah, blah. Not going to cut it IMO. Without major trial data (and it better be a raving success)- this is going to be under huge downside pressures IMO. Phase II is where most small bio-techs get tripped up- and these guys can't even get their key trials started yet (what was the initial promises- late 2014 and a warrant free $62 million secondary? Now it's passing mid 2015 and they got a very weak warrant laced secondary - that no one knows what it even "netted" to the company, as they WILL NOT STATE IT?) , let alone how long will it take to know if their phase II data and results (IF they ever manage to start the thing, let alone fund it anywhere near to completion w/o massive more dilution needed) are any trial results even going to be any good when they face the magnitudes tougher Phase II "control arm" studies and scrutiny.

Tough sledding in here IMO- at least for now. But oh, those "C" level guys are gonna get their piles of options "reset" with the stroke of a pen- so they can sell and unload a pile into any future potential price blip spike, like their key insider did last time this spent about 30 seconds at $12 bucks and change- before its mass collapse now right back down to sub $5 BUCKS. Not bad how one can time those "pre-planned" sales to sell-off right into a near perfect price spike blip??? No wonder the top brass want a pile of options all locked and loaded and ready to go, aka "in the money" when they need um. Great gig IMO, if one can get it. Still very OTC-ish to me- like did they ever really leave penny-ville?

My $5 bucks or so worth

Ask now maxed at .0054 this AM, Bid trying to hold .005 Uh oh?????

0.0051 / 0.0054 (10000 x 423464)

(.0055 is NOT "up" or "green" 5% as is showing? That was yesterday's closing price? The stock is FLAT to down on open? There's a data feed error on the I-hub price display looks like? The OTC site has it flat at .0055 open, with the Ask and Bid now dropped to .0054 and .0051, aka RED?)

That's CDEL with a large block sitting on the Ask at only .0054

All stacked to the Ask/Sell-side again. Looking pretty weak in here IMO.

Is this the "it's going BIG" thingy or the "it's being accumulated" thingy right now? Or is this the $million dollar "mailer" thingy and then a "call center of 10 people" thingy that makes like $25 MILLION in revenues real quick like with ONE PERSON???? I don't get it? Or, is this the .10 cents a share "soon", no it was .15 cents "soon", no a $1 BILLION market cap "soon" thing all playing out right now? I guess I just don't "see it"???????? Very confusing to me- how that all supposedly "works" exactly?????

BMAK is on the Bid way down at .004 with their "hard floor" support share block- so that Bid is barely holding the .005's at this point IMO- looks like CDEL has the temporary floor block (10K shares as usual) parked at .0049 for now, meaning this looks likely to head at some point back into the .004's here soon, IMO.

If any of these dilution MMs let go in here with a large sell block or big ole convertible debt "conversion"- looks to me like the bottom might fall out pretty quick. That new all, all, all time recently made low is .004 and that's right where BMAK is parked for now w/ a lot of Bids now showing in the .004s today, and they're time stamped and updated- so they're real as of this AM.

The last big down tranche took it to .004, so who knows where the next new low will be made on a high volume down leg??

It's a certainty IMO that shares (from numerous floorless, convertible debt deals coming due all through this summer and into the fall) have had at least some shares converted in this .0045 to .005 range, which at a 45% or 47% discount (see 10-K or 10-Q for Asher, KBM worldwide, Daniel James, Fourth Man, Vis Vires group etc "financing" deals) - then with those share discounts it'd mean that shares, 10's of MILLIONS of shares likely to me, have already been issued out in the .0025 to .003 or per share or less range.

That's a lot of cheap priced dilution share overhang that will go to the Ask, sell block side IMO. More continual down, selling pressure I think.

It's a classic "death spiral" playing out looks like to me- that's what the SEC and other firms (Bloomberg finance for example) call these "floorless convertible debt" dilution scenarios as they "play out"- spiraling down in a never ending sell-side scenario of ever increasing dilution shares needing to be issued to pay the convertible debt lenders (oh and that's not even considering that Magna is in the picture big time now as a BHRT lender- and they'd also have 10's and 10's of MILLIONS of shares to sell- just see the past 10-Q and 10-K and how many 10's of MILLIONS of share have already been issued to Magna for "financing")

Tough sledding in here IMO.

http://www.sec.gov/answers/convertibles.htm

Quote from thee SEC itself:

" Because a market price based conversion formula can lead to dramatic stock price reductions and corresponding negative effects on both the company and its shareholders, convertible security financings with market price based conversion ratios have colloquially been called "floorless", "toxic," "death spiral," and "ratchet" convertibles."

https://en.wikipedia.org/wiki/Death_spiral_financing

http://www.bloomberg.com/news/articles/2015-03-12/josh-sason-made-millions-from-penny-stock-financing

http://www.bloombergview.com/articles/2015-03-12/death-spiral-convertible-financier-has-a-lot-of-fun

Quote BS, "LOL..Where's the 0.004 prediction????????" WHAT??????

What????????????

There was NO ".004 prediction" made or stated???? WHEN and WHERE?

There was a FACTUAL STATEMENT that the Bid, the BID had re-entered the .004's today (that's ANY value from .004 to .0049), which it did- hitting .0047 during the day's trading. THAT was a "statement" that was made, NOT a "prediction"- two totally different concepts/realities.

The Bid also FACTUALLY was "thin" in the .005's again today and the Ask was stacked heavily to the sell-side in volume- with legit Level II Bids IN THE .004's being shown by several MM's. Again, a FACT, not a "prediction".

Green? The Bid never left the low .005's which is all one can/would get for their shares if they wanted to/needed to sell um. Call it "green", makes no difference to me, LOL !!!

It's a 1/2 CENT stock again and showing weakness INTO THE .004's on the Bid. Just FACTS and not "predictions". What's it LOST in a matter of the most recent week or so (you know, the "going big SOON" thingy)- about 30% or so, DOWN, RED, really in a matter of only a few trading days, LOL !!! Yeah, that's real "green" alright????????????

Quote LOL , "Uh-oh??? the ask and price are going up"

WHAT? NO. The Ask actually just DROPPED from .0056 to .0055 and got loaded w/ some more sell-side shares?

0.0052 / 0.0055 (10000 x 466711)

There's nothing "going up", LOL !!

That's both BMAK AND CDEL sitting hard on that Ask- loaded to the gills today. The Bid is thin and actually showed the .004's today and is thin all the way into the .004's right now?????

It's not "going up"- it's going essentially nowhere? It's head-locked in a MM "bracket" right at about 1/2 CENTS.

No "price is going up"??????? Where?

Bid DROPPED into the .004's again, UH OH??????????????????

Bid showing only .0047 right now? How can that be? Is that the "going big soon" thingy or the .10 CENTS, no wait, .15 CENTS a share thingy part?? I'm confused I guess- I mean how can it be SUB 1/2 CENT when it's going to be .15 CENTS "soon" as is the "claim"??????????????

Is the $MILLION dollar "mailer thingy" started yet, the one person thing where a "franchise" is created out of the thin air just by sending out some "mailers" and a few phone calls afterward, LOL !!!! When exactly does that thing start and where are they gonna get the 1 $MILLION they DO NOT HAVE so they can send out those amazing "mailings" things- to make the easy $25 MILLION in revenue as is the claim made prior here? Any details more on how EXACTLY that "works" (well, besides the 10 people working a phone call center thingy, after the ONE PERSON does this $MILLION dollar "mailer" thing LOL !!)

Or, is this the part where those who bought for less than .02 then have the MM's somehow convert their shares back into cash money and then maybe like Maxim comes along and "gives" BHRT like $10 MILLION or something- is that what's happening right now? Again, I'm sorta confused I guess on how all these things are "working out" as explained here prior?

IS THIS THOSE THINGS HAPPENING - right now, is that part of the Bid going SUB 1/2 CENT? Is that it????????????

I'm just not clear yet I guess on all the details of how those thingys work and all????????????? Like makes NO SENSE IMO, NONE. Total nonsense IMO. WHY if it was going to .10, no .15 CENTS "soon", no wait- a $1 BILLION market cap, no it was $2 BILLION market cap, then WHY IS IT ONLY sub 1/2 CENT NOW with a market cap of barely $4 million lousy bucks????????? It's supposed to be at like this $2 BILLION market cap in a matter of a few months according to all that was stated??

I don't think I'm getting it I guess?? Confusing to me?????

Quote BS LOL !!, "OCAT Powerhouse Parkinson's Disease Patent. Michael J. Fox is working on this one. "

What? Michael J. Fox "works" on Parkinson's related patents? He's a scientist or something, really, LOL !!! Michael J. Fox's name appears on some OCAT "patent"??????? WHERE? WHERE IS THAT EXACTLY, LOL ???????????

WHERE is there ONE WORD from the Michael J. Fox FOUNDATION (for which he RAISES FUNDS and acts as the figure head and a director)- where is there ONE IOTA OF PROOF that the Fox Foundation has ONE THING, ANYTHING to do with OCAT? WHERE is that published as a fact? Where?

Total nonsense IMO. There's no proof of any connection between the Fox Foundation and OCAT that I've ever seen or read? NONE???????

Kinda RED again? Is this the "patent effect" thingy or is it the "big institutions" doing more "big buying" thingy?

NOT sure I'm "getting it"? How a stock sits near or on its new 52 WEEK LOWS when all this supposed net "big buying" and all is occurring?

Seems to be a stock that's going nowhere and now trades BELOW where it did on the OTC penny markets? What exactly explains all that, LOL !!!

Looks to me like the market just panned um again.

But hey, WHEN YA GOT NO BIG PHASE II ACTUALLY HAPPENING AS PROMISED (not late 2014, but now mid JULY 2015 and GOOSE EGG, NO TRIAL(s) and NO $62 million secondary, but a lousy $30 mil or less, warrant laced secondary in reality) - I mean when ya got that "going for ya"- just ISSUE MORE "PR" about things like "lupus in mice" (when one sees "mice" or "animal studies" - translation is like $200 MILLION to maybe a $BILLION more needed and probably 10 years MINIMUM IMO) or issue a "patent" PR or a "conference" PR- just issue them ole "PRs" till the cows come home- when those ole "big trials" are sitting in the location labeled PARKED.

It's dead money in here IMO. Not seeing it? They missed big on the secondary- and at the pace it took um to pull of a micro sized phase I (what, FIVE YEARS) and now as late as they are on the phase II trial(s)- this is 3 years on the "fast track" and more like 5 YEARS reality minimum IMO, to even know if they "have it" or are just another phase II bust like most of these turn out to be.

My $5 bucks and small change worth

Bid BARELY holding the ole .005 line, Ask massively stacked to the sell-side

0.0051 / 0.0056 (10000 x 400000)

That's 40 to 1 to the Ask/sell again. CDEL and BMAK are both parked hard on the Ask now- back on "their game" in full swing looks like. Must be a conversion or a "draw request" in the works looks like to me?

4000 shares posted as opening trade (not even on the open, but late)- that's a big ole $25 bucks or so worth, LOL ! Looks like those retail buyers just aren't quite beating the ole door down to get these "cheap" shares even at 1/2 CENT??? Why? I wonder why that is?

I mean, is this the "going big" part or is it the "it's gonna be HUGE" part, no? LOL???

I think I'm confused? When exactly is that .10 CENTS, no wait- it was .15 CENTS a share thingy gonna happen exactly, the "soon" prediction- oh wait, or was it the $1 BILLION market cap, no the $2 BILLION market cap thingy, "soon" really?

You know- the thingy where they (I guess, cause it makes no sense to me personally) but where they just take a $MILLION they DO NOT HAVE and do a ONE PERSON (LOL !!) ole "mailer thingy" and then a couple of "sales calls" from a "phone bank of 10 callers" and like generate $25 MILLION in sales, just like that, LOL !!

Is that all happening now? I'm not sure I'm "getting it" I guess? WHEN does that all happen exactly? Is there like some charts and tables with DETAILS IN RED highlights and actual DATES and facts as to when EXACTLY that part all will supposedly happen and how exactly it "works" and all? I'd sure like to see those details, really !!

Looks like it's 1/2 CENT in here now, and the next big sell/dump conversion by some convertible debt holder IMO takes it a lot lower than the new recent low of .004, I think. It hit that .004 low from a 1 CENT starting point. 1/2 CENT is the new "base" IMO and there's been shares certainly converted in this range- with discounts of 45% to 47% on um (see any recent 10-K or 10-Q filing Asher, KBM Worldwide, Vis Vires group, Daniel James, Fourth Man convertible debt hedge loan deals- all steeply discounted)- so there's gotta be shares issued in the .0025 to .003 range now IMO, maybe even a tad lower.

Looking pretty weak here to me- just dilution piling on to more dilution that I can see.

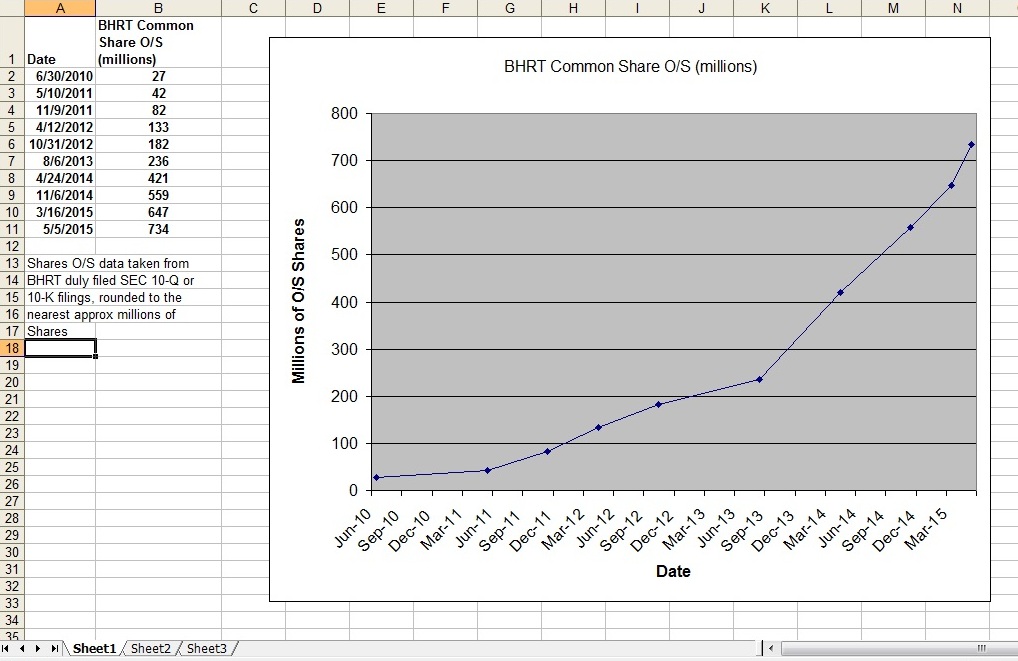

What's the "dilution picture" look like? Well, here's a simple graph showing dilution and then the corresponding massive common share price declines- seem to correlate pretty 1 to 1 IMO??

And then what's the common share price done- as that mass dilution has been flooding the market for years now- and actually accelerating (going more vertical on the graph) - increasing recently and continually (NOT decreasing as was claimed?)-

That's the "picture" as I see it as of now- pretty clear to me personally. Essentially never ending mass common share dilution, and lots of it, has consequences, seems to me?

.0052, ONE HALF CENT on very high volumes, LOL !! "GOING BIG"???????????

Is it "going big"

Are they getting out of the "human stuff" thingy and "doing the vet" thingy supposedly, LOL !!

Is ONE PERSON just gonna do a "mail list" thingy (who even does mailings anymore, LOL ???) and then make an imaginary near instant $25 MILLION?? WHAT DOES AMAZON PAY TO ACQUIRE ONE, ONE NEW CUSTOMER? (like maybe $150 OR MORE per customer, LOL !! Not a little "mailing" thingy) Amazon also just happened to have built probably the world's most sophisticated server farms and computer networks on planet earth- so good that they now rent out space on it to the who's who of businesses on planet earth- and NO, they did not do it with ONE EMPLOYEE, LOL !!

WHAT happened to .10 CENTS, no it was .15 CENTS "soon" and then a $1 BILLION market cap, no it was a $2 BILLION market cap by end of year, LOL !!! It's mid July- and the market cap is collapsing like a lead boat anchor hitting bottom??????????

WHY is it not "going big" as was stated so many times here? Why? Is this the ONE PERSON new "franchise thingy" where they just take a $MILLION (which they DO NOT HAVE, LOL !!!) and just sound out some "mailers" and then use the ole "phone call sellers" and in like 6 months get $MILLIONS in sales, LOL LOL !!!!!!!!!!!!! What? HOW does that "work" exactly??? Why doesn't every biz just "take a $MILLION" and then just "do some mailing" and shazam, in like 6 months they'd all have this imaginary supposed $25 MILLION in sales, LOL !!!!!!!!! Why not, why doesn't EVERY biz just do that then- sounds like the easiest money a biz could ever make- well, all except the part about it DOES NOT WORK and one has to have a "product" to actually SELL that people or other businesses NEED and WANT, LOL !!!!!!

.0052 on HIGH VOLUME and it's "going big" alright, DOWN BIG looks like to me????

Quote LOL BS, "$25 Billion Companies Started in a Garage

"

Bioheart isn't a "start up"???????????? What? They've been in business for about 15 YEARS NOW, LOL !!!! And in that time they've NEVER, EVER, EVER produced so much as ONE CENT of ROI or ONE CENT of a profit.

Microsoft in a "garage", LOL !!! Microsoft was PROFITABLE FROM ALMOST DAY ONE and then attracted mega-bucks in high quality venture investment.

Youtube a "garage" - same thing. Once the "template" of Youtube was designed (and the insiders had their own scratch in the game maxing out credit cards and mortgaging homes or whatever) they went on to attract THEE WHO'S WHO OF MENLO PARK VENTURE financing. THEE finest investment money one can attract- before being bought-out by Google. And NO, they did not have ONE "employee" when they ramped- not even close. Neither did Microsoft or Facebook or Google or any other mega company of today- they hired and hired quickly as their ramps were the largest and fastest in business world history.

Sequoia Capital, LOL !!! Probably THEE finest and most "connected" venture money in existence (the who's who of Menlo Park "drive")- and they CHOSE Youtube AND Google, LOL !! And NO, they were not ONE PERSON operations.

http://blogs.wsj.com/venturecapital/2010/03/18/finally-heres-what-youtubes-investors-made-in-sale-to-google/

The "smart" money venture firms PICK WINNERS- just the way it is. NEVER were their investments ever penny stock money losers, ever. NEVER has happened.

LOL, Bid/Ask BOTH collapsed to the .005's again !! Uh oh?????

Wait, this is the "going big" thingy I guess? No, the "huge" thing, at 1/2 CENT, LOL !!!

Oh, and now using ONE PERSON they'll just "start a franchise" like Amazon or whatever, LOL !!!! (Amazon has 1000's of employees and $BILLIONS in capital, LOL) - but ole 1/2 CENT BHRT with ONE PERSON will just "do an e-commerce" type thingy (selling WHAT to WHO, WHO KNOWS LOL ?????) and then just kaboom- like in 6 months they get like $10 or no, $20, or no $50 MILLION in "revenue" just like that- just cause they set up an imagined ONE PERSON "franchise" whatever????

HOW EXACTLY DOES THAT WORK, LOL ?????? HOW? Oh, using an "Amazon model", LOL !!!!! Right on??????

Makes NO SENSE TO ME (well except the 1/2 CENT dilution selling part) -but this imaginary vet "franchise" ONE PERSON thingy, no way IMO. NONE. Past lotto odds if not impossible. WHY did Stemlogix, the BHRT "vet division" of which Comella was CEO, WHY DID IT NEVEV MAKE $MILLIONS or ever amount to anything???? WHY? WHY???

http://www.marketwired.com/press-release/bioheart-partnership-with-stemlogix-leads-first-us-combination-regenerative-medicine-1733056.htm

http://globenewswire.com/news-release/2012/03/22/471364/249904/en/Bioheart-Labs-and-Stemlogix-Veterinary-Products-Featured-in-Media.html

WHY did none of that ever generate $MILLIONS?????? WHY???? IT all went nowhere? Why is that???/

Now, using ONE PERSON some "vet franchise thingy" is supposedly gonna rapidly generate $MILLIONS using a "Amazon e-commerce model", LOL !!!!!!!!!!!!!!!!!!

Right on????? Not seeing it?? I see 1/2 CENT again today - SOLID RED, LOL !! Right back where it was a week ago. Why is that? What happened to "going big" and "huge", LOL ??? Makes ZERO sense to me?

Quote LOL, "Big days and weeks ahead.

There's plenty of DD out there that proves any negativity wrong.

This is going to be a huge company! "

Was TODAY and the past several days of MASS PRICE COLLAPSE and DECLINES back to the .006's (it hit the .005's today on the low) - is this all part of this supposed "big days and weeks ahead" thingy?

Is a 6/10th OF ONE CENT common share price and almost no cash-on-hand (see any recent SEC filed 10-K or 10-Q) - is that part of this supposed "this is going to be a HUGE company" thingy stuff?

Not really seeing it or getting it IMO? NOT AT ALL??? Makes ZERO sense to me personally? The collapsing common share price and market cap versus their large amount of debt, their amount of constant use of common share dilution for everything from paying common bills to near continual use of toxic convertible debt financing deals (AND a Magna dilution "credit line" facility for survival cash), their own numerous GOING CONCERN warnings laced all through their own SEC filings, their near total lack of any cash-on-hand at any given time and all the rest of the realities just a don't "jive" with this whole "it's going big" thingy stuff IMO??? NOPE?

Makes no sense that I can see, LOL !! None.

.0061 and BMAK is BACK and that ole Ask DROPS to .0065 and Bid just collapsed to .0061, LOL !!!

Is this the "going big" thingy happening again? When's the "it's going to 10 CENTS, no 15 CENTS "soon"" part gonna happen? EXACTLY WHEN, LOL????

.0061 RED, DOWN 12% plus

0.0062 / 0.0065 (290000 x 290000)

CDEL and BMAK running the ole "brackets" now- they've got it headlocked on the Bid/Ask, with 10K share bottomless blocks. Yepper, same old pattern of all of 2015 from what I've observed?

Again, I'm just a tad confused as to when EXACTLY the "it's going big, it's going to be huge" thingy exactly will be happening? Is there like an exact date- it was stated by END OF THIS YEAR it would have a $1 BILLION, no $2 BILLION market cap and it's already passing mid July of 2015. Not much time left- when will this "going big" thingy and all these imaginary prices per share and vast market cap "projections" be met, EXACTLY? When?

I'm not seeing it- I see .0061 RIGHT NOW, today? DOWN in the SUB PENNY range and going nowhere? The new all, all, all time LOW of .004 was made very recently- and I don't see a single uptrend in place in all of 2015, or even in the past 1 YEAR from a technical/chart stand point? WHY? WHY is that?????? WHEN IS IT "going big" and WHEN is the 15 CENTS a share thing going to happen- WHEN EXACTLY and WHY?

Makes no sense to me, NONE?????

Uh oh, Bid DROPPED to .006's and 900K shares on the Ask/Sell-side and BMAK just slid down on that ole Ask, parking a 10K share block @ .007

Looks to me like that's it then, .007 just got "set" as the ole "hard cap" once again by BMAK. It doesn't look to be "going big" here IMO??? Nope, LOL !! Looks like it's staying at SUB PENNY status for now at least IMO- looking at that Level II stack as of right now.

0.0064 / 0.0065 (15000 x 900000)

That's a 60 to 1 Ask/Sell-side stack there- not looking good IMO. Ask just dropped back to the ole .006's with a big ole block for sale. And now BMAK just slid right back on down that ole Ask and is sitting in position #2, one level off that 900K share block showing. Yep, BMAK IS BACK.

Not sure what part of the "going big" thingy this is? Doesn't make a lot of sense to me personally? Doesn't look to really be "going anywhere" that I can see? When exactly does this "going big" thingy happen again?

Is this the "it's going to 10 CENTS" part? Oh wait, no it's 15 CENTS I think was the last price "prediction"??? Is that happening right now - cause it looks like 6/10ths of ONE CENT to me? I'm not seeing that 10 or 15 CENTS thingy???? Is this the "market cap is going to be $1 BILLION or no, $2 BILLION "soon" thingy???? When exactly does that happen again?

Is this Maxim creating a $10 million deal by converting those who bought under .02 and somehow making those shares turn into money/cash- something like that? Is this cause "Cassell introduced" um and all, LOL !!!! When exactly did Maxim "start working with BHRT", what page of wht SEC filing is that on- cause I've searched and searched and sure can't find it??? Where is that stated by the company- that they're now "working with Maxim" and that "Maxim is providing financing" to Bioheart? Is there a "PR" thingy or ANY SEC filing about that being true? I'm confused I guess- where is "Maxim" in all this- and aren't they like "converting those who paid under .02 into cash financing"- isn't that how it was stated it all "works" I think? Something like that, LOL ????

When EXACTLY will the "Maxim doing an offering" thingy take place- is there a date given? I'd sure like to know?

Wow, sure looks like 6/10ths of ONE CENT to me- I just don't see or find any of this other "stuff" happening as stated here? What am I missing?

$5.12 SOLID RED??? Oops? What happened??

Is this the "big institutional" buyers thingy happening AGAIN? OR is this those big "stealth buyers" who really buy and keep the price going DOWN as they supposedly BUY BIG, LOL !!!!

HOW does a stock go LOWER when supposed LARGE NET "BUYING" is taking place- I still can't understand exactly how that all supposedly "works"???

Is this ole Blackrock like buying their supposed 5 million or whatever it's supposed to be? OR is this the Cowen effect thingy happening?

Looks like it can barely hold a lousy $5 bucks a share to me- it's RED right on my screen? Why? Why is that is all this "big buying" stuff is happening?

Sure makes no sense to me? Looks like NET SELLING to me, and it's sitting near its brand new 52 WEEK LOW of $4.88 and has literally gone NOWHERE (well maybe DOWN) in years, and has lost big from $7.50 a share recently to now only about $5 a share???? Why is that with "big buying" from "institutions" supposedly happening? HOW CAN THAT BE, LOL ???

WHY does it trade today BELOW where it traded on the OTC? Why?

Bid solid in the .006's still, on a whopping 9K shares traded, LOL !!

Is this the "going big" thingy happening??

0.0067 / 0.007 (11000 x 36428)

9K shares = approx $58 bucks traded in over 30 minutes !! Looks like a HUGE rush of retail buyers just piling in to get these sub ONE PENNY shares, LOL !!! Nope? Why not? If this is "going to be huge" - then WHERE are the buyers when it's not even .007 CENTS right now? Where are they?

At $58 bucks traded, that's nearly ill-liquid IMO. Meaning if one wanted to sell more than maybe $500 bucks worth or say a $thousand worth, that Bid is going to drop and drop hard as far as I can see? CDEL has their "bid support" ole 10K share block parked way down at .006, meaning IMO that's the "floor" price for now- those MM's aren't gonna pay more than that if one wanted to sell a chunk, not that I can see on that Level II stack.

So it's really about a .006 CENT stock still looks like to me. And the volumes have been very low end of last week and sub anemic this AM? Why? Why is that if this is "going big" and all?

Makes ZERO SENSE to me? I don't get it? Where's the big buyers and buy orders piling in to get those "cheap shares" as has been stated so many times here? I don't see it happening? Why? Why is that? WHERE ARE THE BUYERS FOR SHARES selling at .007 or less?

Quote LOL BS, "Quote " the company is going to be huge"

The revenue from Vetbiologics over the next 24 months will be over $15m in 10k for 2017. They need to sell the IP or license it etc. The real money is in animals. People will line up to pay $5k for a SCT"

WHAT????????????????????

A supposed $15 MILLION by 2017, LOL !!!!! Based on what made up numbers? WHERE does this imaginary exact $15 million come from and why by some 10-K in 2017, LOL!!!!

WHAT WAS THE SO CALLED "Vetbiologics" ole "revenue" as of the last 10-Q filing?????????????? Where does "Vetbiologics" even actually exist- as in number of employees and what EXACT "products/services/therapies" do they offer and sell as of right now, today etc?

Other than a powerpoint slide or two and a name and a website that would take about 2 hours to put together- WHAT EXACTLY comprises this so called "Vetbiologics" thingy? BHRT didn't even list any "revenues" as being broken-out and attributed to "Vetbiologics" last Qtr, IN THE 10-Q, NOT THAT I EVER READ OR SAW?????????????

"Vetbiologics" used to be "Stemlogixs" (the old "Stemlogix" web link began to re-direct to "Vetbiologics" fairly recently per my clicking on it?) and had an address of a RESIDENTIAL HOUSE, LOL !!!! How "big" an operation does one think that actually is or was, LOL !!!!

And this is all supposedly going to ramp up to $15 MILLION in annual revenue in a period of 1.5 yrs or so, LOL !!! Really? BASED ON WHAT? HOW? HOW is that exactly going to happen- when BHRT finished the last qtr with what, like $79K TOTAL CASH to their name (BHRT has put a grand total of less than $60K into the stem cell "clinic" thingy per the last filed 10-Q and is taking a loss on that as of that filing?) , so BHRT with $79K cash-on-hand, something like that- see the 10-Q filing is going to make a $15 MILLION annual revenue vet biz now too? Really? Again, WHAT REVENUES were from "Vetbiologics" and where does one even go to get a "Vetbiologics" product or so called "treatment" etc? WHERE?

http://www.sunbiz.org/scripts/ficidet.exe?action=DETREG&docnum=G14000079143&rdocnum=G14000079143

So that's the Florida Secretary of State site for ALL registered businesses- and it shows that "Vet Biologics" wasn't even "created" as a fictitious business name entity until July 31, 2014, just about 1 yr ago now. It was came into being at exactly the time that Comella became involved in a lawsuit being named the defendant by Stemlogix.

https://www.clerk-17th-flcourts.org/Clerkwebsite/BCCOC2/OdysseyPA/CaseSummary.aspx?CaseID=NzE1NTQxMA%3d%3d-YfCzOBpRAXo%3d&hidSearchType=party_case&DisplayCitation=no&CaseNumber=CACE13024037&SearchType=

http://search.sunbiz.org/Inquiry/CorporationSearch/GetDocument?aggregateId=flal-l10000061738-8f1560a3-97a1-448b-b02f-17e79a596386&transactionId=l10000061738-9654a935-2e8c-4eee-b373-5261237e9fee&formatType=PDF

THAT is the 2014 "Stemlogix LLC" filing above- and one will notice that Comella was named a "Mgr" of the LLC in 2014. THAT WAS the ole "vet division/partnership" thingy (LOL !!) of ole Bioheart in the past- and the address was literally some residential house. Comella even had herself listed in her resume and other places as being the "CEO OF Stemlogix" etc. So then she apparently gets sued by um- and suddenly "Vet Biologics" is created by nothing more than a fictitious name filing and a couple of web pages being slapped up. HOW is that a $15 MILLION business? HOW LONG DID STEMLOGIX ALREADY EXIST and why then did it not do $15 MILLION in business already???? T

The Florida Secretary of State shows that "Stemlogix" the former "Vet" division or sub company (whatever one wants to call it) has existed since 2010 and it's NEVER done even $1 MILLION in "revenue" that I'm aware of- not even a fraction of that, but now out of the thin air- this "Vet Biologics" is supposedly going to ramp to $15 MILLION in a yr or two, LOL !!!! REALLY? HOW, HOW EXACTLY IS THAT GOING TO HAPPEN??????

http://www.marketwired.com/press-release/bioheart-partnership-with-stemlogix-leads-first-us-combination-regenerative-medicine-1733056.htm

There is ONE PR claiming that Bioheart and "Stemlogix" were "Partners" clear back in 2012- so WHERE was all the "revenues" the supposed $MILLIONS from that "vet" thingy they did? WHERE? Why did it NEVER HAPPEN THEN but is supposedly going to suddenly happen now????????????

http://globenewswire.com/news-release/2012/03/22/471364/249904/en/Bioheart-Labs-and-Stemlogix-Veterinary-Products-Featured-in-Media.html

There's another great sounding "PR" about Stemlogix/BHRT and why did that never amount to any $MILLIONS in supposed "revenues"?????? Why?

http://www.bioheartinc.com/AboutUs/Management/KristinComella

RIGHT THERE - it says that Comella was "was co-founder and Chief Executive Officer of Stemlogix, LLC for veterinary medicine. "

So WHY DID THIS "vet thingy" then NEVER MAKE ANY MONEY and was shown on the Florida Secretary of State filings as being run out of a residential HOUSE? Why no $15 MILLION in imaginary "revenues" when it's been in business for like 5 yrs now- and Comella was CEO of it prior?? WHY, LOL !!

Makes ZERO sense to me?? None? Now an imaginary supposed $15 MILLION in "revenue" when the essential same entity (The Stemloxix web link on Google now does an auto-redirect to "Vetbiologics" a tiny website that can literally be slapped up in an afternoon IMO, I know I could build it in a few hours) - why did it never do these supposed $MILLIONs in "revenues" for the past 3 or 4 years then ? Why? Totally makes no sense, none IMO?

Quote LOL BS, "They've we've working with them since Cassel financial introduced them in late 2013.

"

What???????????????

NO, NO THEY HAVE NOT????????????????????

WHAT PAGE of WHAT SEC FILING shows that BHRT has EVER been "working with" or "financed by" or has ANY "working relationship" with so called "Maxim", LOL ????????????????????????????

BHRT is being financing by various hedge fund convertible debt lenders but Maxim IS NOT ONE OF THEM. BHRT is "working with" Asher, KBM Worldwide, Daniel James, Fourth Man, Vis Vires Group, Magna etc but NOT "Maxim" group, LOL !!!!!!!!!!!!!!!!!

NOWHERE in any SEC filing going back to 2013 is the Maxim group ever named and it has ZERO to do with supposed Cassel "introducing them", LOL !!!!!!!!!!!!!!!!!!!!!

Quote LOL, "My apologies. Here is Bioheart listed as a 'Spotlight Company' in Maxim's "JULY OF 2015" report:"

They don't even have the share price correct, LOL!!! AND the market cap is totally incorrect too, LOL !! That's some "report"??? What's the accuracy rating of ole "Maxim's" vast predictive powers on their little "spotlight company" charts/tables or whatever - when they can't even get the share price and market cap correct?

They list the share price as ONE CENT on July 7th, 2015?????? NEVER HAPPENED- not even close. They list the market cap on the same day as $6 million dollars, LOL, nope again.

On July 7th 2015, BHRT traded between .0065 and .007 max. The market cap at most on that day would have been 734 million shares x .0065 = approx. $4.7 million, NOT $6 million.

Nothing like a bunch of incorrect info on some "spotlight company" um "report" from ole Maxim. Again, WHAT IS THEIR ACCURACY RATING AT EVER BEING CORRECT IN THE FUTURE PRICE "predictions"??? What does being a "spotlight company" at ole Maxim even mean????? If the don't state their accuracy rating- then what difference does the little "report" thingy make in the end???

Further- WHAT does being on some Maxim "report" that list 100's of companies- have to do with the supposed "implication" that "Maxim" is supposedly going to "invest" in BHRT or whatever, LOL !!!! Maxim isn't "invested" in the vast majority of the companies on that "list" (if any of them?) - not even close. So what difference does it make?

A "list" that means little to nothing IMO. Just a typical "coverage" sheet- with a bunch of penny stocks on it, big whoop. What did the 2014 Maxim "lists" ever amount to? As pointed out prior- BHRT stock has declined at least 50% to more like 65% since those Maxim "lists" were published in 2014 naming it a "spotlight company", LOL !! So what was that worth in the end? DID THEY "INVEST" in BRHT since 2014? NO?? Why not then??????

All I need to know- "lists" don't mean much to me personally. Little to no value IMO. Almost always wrong- no better than a wild guess at best IMO.

Quote LOL, "You might be on to something with Maxim Group. Bioheart was listed by them as a "Spotlight Company" in their June 2014 and September 2014 'Coverage Universe' reports. "

What???? It's NOW JULY OF 2015 and the stock would have ONLY LOST about what, 50% or MORE since June of 2014 and Sept of 2014, LOL !!!

Sounds like when ole "Maxim" does a "Spotlight" then big ole price declines soon follow?

WHAT does some penny "spotlight company" coverage blah blah have to do with anything? It probably means Maxim was unloading some shares for someone IMO. How has it helped the common share price or the company- it's been in mass, total decline in the past yr, losing 65% on a one yr chart and hitting it's brand new recent all, all, all time lows of .004 cents. SUB ONE CENT now for nearly all of 2015???? That must of been some "spotlight"??

"Maxim", LOL - right on???

Bioheart doesn't even own all of U.S. Stem Cell whatever AND is taking losses on it, big whoop, LOL !!!!

THIS is supposedly gonna be their big ole "revenue" generator and fund some large phase III trial(s) or whatever, LOL !! Really? Doesn't look like it to me- and besides, how do they "sell" and Bioheart "products" there when their OWN 10-K says they HAVE NO APPROVED PRODUCTS and CARRY NO PRODUCT LIABILITY INSURANCE for the very reason that they HAVE NO APPROVED PRODUCTS TO SELL? HOW DOES THAT "work" exactly? It's a contradiction between their own SEC filings and these little "web sites" and the "clinic" thingy??? Makes ZERO sense to me, NONE.

From the latest filed 10-Q, PAGE 12:

"Investment is comprised of a 33% ownership of U.S. Stem Cell Clinic, LLC, accounted for using the equity method of accounting. The initial investment in 2014 and 2015 of cash and expenses paid on U.S. Stem Cell Clinic, LLC’s behalf was in aggregate of $54,714. The Company’s 33% income earned by U.S. Stem Cell Clinic, LLC of $3,966 for the three months ended March 31, 2015 (inception to date loss of $5,151) was recorded as other income/expense in the Company’s Statement of Operations in the appropriate periods and increased the carrying value of the investment to $49,563."

Their big "grand plan" clinic thingy - and they only own a whopping 33% of it AND have sunk a big ole $54,714 bucks into it, LOL !!! My local dentist or doc's office has about 5X that investment in it. AND they're taking a loss on the "big revenue generator" per the claims made here, LOL !!!

Last filed 10-K, PAGE 32:

"We do not currently have product liability insurance because none of our product candidates has yet been approved for commercialization. While we plan to seek product liability insurance coverage if any of our product candidates are sold commercially, we cannot assure you that we will be able to obtain product liability insurance on commercially acceptable terms, if at all, or that we will be able to maintain such insurance at a reasonable cost or in sufficient amounts to protect against potential losses.

Claims may be made by consumers, healthcare providers, third party strategic collaborators or others selling our products if one of our products or product candidates causes, or appears to have caused, an injury. We may be subject to claims against us even if an alleged injury is due to the actions of others. For example, we rely on the expertise of physicians, nurses and other associated medical personnel to perform the medical procedures and processes related to our product candidates. If these medical personnel are not properly trained or are negligent in using our product candidates, the therapeutic effect of our product candidates may be diminished or the patient may suffer injury, which may subject us to liability. In addition, an injury resulting from the activities of our suppliers may serve as a basis for a claim against us.

32

We do not intend to promote, or to in any way support or encourage the promotion of, our product candidates for off-label or otherwise unapproved uses. However, if our product candidates are approved by the FDA or similar foreign regulatory authorities, we cannot prevent a physician from using them for any off-label applications. If injury to a patient results from such an inappropriate use, we may become involved in a product liability suit, which will likely be expensive to defend.

"

SO WHAT DO THEY "sell" at the ole "clinic" thingy- when their own 10-K says THEY HAVE NO APPROVED PRODUCTS, CARRY NO LIABILITY INSURANCE and DO NOT INTEND TO "PROMOTE" OR SELL ANY UN-APPROVED PRODUCTS OF THEIRS?

IF, nothing they have is "approved" per their own SEC statements, AND they say they WILL NOT SELL ANYTHING THAT IS NOT APPROVED- then how are they "selling" supposed "products/treatments" at their "clinic" thingy? HOW? It's mutually exclusive language per their own SEC filing- they're contradicting themselves per my reading of their own pretty plain language, LOL !!!

HOW does that 10-K statement make ANY sense in relation to the claims that the "clinic" thingy is SELLING PRODUCTS and "treatments" as made by Bioheart??? HOW IS THAT POSSIBLE?

MAKES ZERO SENSE TO ME, NONE. They're contradicting their own SEC filings from one line to the next IMO. Plain English to me.

I'm not your "bro" and never will be.

WHAT is on the "website" supposedly? MOST of the website is very dated/out of date, LOL !!!

Makes no sense. None. What is "it" and where is "it" on what website? The link is bad- doesn't work, LOL !!

LOL quote, "There are a number of clinical application presently and legitimately being provided to patients utilizing both their products and knowledge base. This activity is growing rapidly, and with their combined subsidiaries BHRT is generating the revenue required to move forward with trials to ultimately acquire the approvals needed for their premier products. The Grand Slam. "

WHAT????????????

Where is all this spelled out in a SEC 10-Q or 10-K??????

What EXACT "products" are they offering and where (especially "legitimately" which IMO would be in 100% contradiction to their own duly filed SEC documents?)

BHRT is "generating revenue required to move forward with trials to ultimately acquire the approvals needed for their premier products"????

Again, WHAT SEC FILING IS THAT IN? Their losses from operations last qtr were larger than the prior year over year? Where is "revenue" resulting in smaller losses, let alone generation of any cash/positive cash flows even remotely close to being enough to supposedly fund a large phase III or similar set of clinical trials? If that was true- then why in late 2014 and early 2015 has the company done "toxic" dilutive financing deals with Magna (both a convertible debt "note" AND a dilutive credit line) and then done FIVE floorless convertible debt deals in Jan/Feb of 2015 and April of 2015 with Vis Vires group, KBM World wide, Daniel James, Fourth Man etc (SEE last 10-Q and prior 10-K filings)??? WHY would they do those highly dilutive financing deals at the worst of terms- if they were supposedly generating cash internally as claimed? Why? "revenue" DOES NOT = free cash flows or profits, not by a long shot.

http://www.sec.gov/Archives/edgar/data/1388319/000114544315000378/bioheart_10k.htm

From the BHRT 10-K filing, PAGE 32:

"We do not currently have product liability insurance because none of our product candidates has yet been approved for commercialization. While we plan to seek product liability insurance coverage if any of our product candidates are sold commercially, we cannot assure you that we will be able to obtain product liability insurance on commercially acceptable terms, if at all, or that we will be able to maintain such insurance at a reasonable cost or in sufficient amounts to protect against potential losses."

"We do not intend to promote, or to in any way support or encourage the promotion of, our product candidates for off-label or otherwise unapproved uses. However, if our product candidates are approved by the FDA or similar foreign regulatory authorities, we cannot prevent a physician from using them for any off-label applications. If injury to a patient results from such an inappropriate use, we may become involved in a product liability suit, which will likely be expensive to defend."

SO WHAT EXACTLY DO THEY "sell legitimately" then?????? Says RIGHT THERE IN PLAIN ENGLISH in their duly filed 10-K, they CARRY NO PRODUCT LIABILITY INSURANCE AS THEY HAVE NO SALABLE OR APPROVED PRODUCTS???? So which is it? Sounds pretty risky to me- if they're selling un-approved drugs and carry no product liability too boot?????

Latest SEC filed 10-Q, PAGE 11:

"NOTE 2 — GOING CONCERN MATTERS

The accompanying unaudited condensed financial statements have been prepared on a going concern basis, which contemplates the realization of assets and the satisfaction of liabilities in the normal course of business. As shown in the accompanying unaudited condensed financial statements, during three months ended March 31, 2015, the Company incurred an operating loss of $1,048,217 and used $384,251 in cash for operating activities. As of March 31, 2015, the Company had a working capital deficit (current liabilities in excess of current assets) of approximately $11.0 million. These factors among others may indicate that the Company will be unable to continue as a going concern for a reasonable period of time."

Same 10-Q, PAGE 33:

"At March 31, 2015, we had cash and cash equivalents totaling $70,974. However our working capital deficit as of such date was approximately $11 million. Our independent registered public accounting firm has issued its report dated March 16, 2015 in connection with the audit of our financial statements as of December 31, 2014 that included an explanatory paragraph describing the existence of conditions that raise substantial doubt about our ability to continue as a going concern and Note 2 of our unaudited financial statement for the quarter ended March 31, 2015 addresses the issue of our ability to continue as a going concern."

SO THEY ARE SUPPOSEDLY "going to" or "about to" FUND A LARGE CLINICAL TRAIL(S) when they just ended their prior qtr with $70,974 TOTAL DOLLARS to their name, against $11 MILLION in debts, LOL !!!!!!!!!!! REALLY? Where's this thing about "revenues are going to fund trials" thingy- WHAT PAGE EXACTLY OF A SEC FILING IS THAT PART ON? Cause the reality of that statement above, FROM THEIR MOST RECENT 10-Q, totally negates that reality? It's impossible to claim they are "close to funding a phase 3 clinical trial" and have them be a "GOING CONCERN" and have $79K lousy bucks left in their bank account at end of a qtr, a qtr in which they borrowed heavily using dilution funding too boot, LOL !! Two mutually exclusive realities IMO, anyway one wants to slice it?????

SAME 10-Q, PAGE 24:

"Subsequent financing

On April 13, 2015, the Company entered into a Securities Purchase Agreement with Vis Vires Group, Inc. (“Vis”), for the sale of an 8% convertible note in the principal amount of $33,000 (the “Note”).

The Note bears interest at the rate of 8% per annum. All interest and principal must be repaid on January 16, 2016. The Note is convertible into common stock, at Vis’s option, at a 45% discount to the average of the three lowest closing bid prices of the common stock during the 10 trading day period prior to conversion. In the event the Company prepays the Note in full, the Company is required to pay off all principal, interest and any other amounts owed multiplied by (i) 140% if prepaid during the period commencing on the closing date through 179 days thereafter. After the expiration of 180 days following the date of the Note, the Company has no right of prepayment.

On April 27, 2015, the Company entered into a Securities Purchase Agreement with Daniel James Management, Inc., for the sale of an 9.5% convertible note in the principal amount of $25,000 (the “Note”).

The Note bears interest at the rate of 9.5% per annum. All interest and principal must be repaid on April 26, 2016. The Note is convertible into common stock, at Asher’s option, at a 47% discount to the lowest daily closing trading price of the common stock during the 10 trading day period prior to conversion. In the event the Company prepays the Note in full, the Company is required to pay off all principal at 150%, interest and any other amounts."

SAME 10-Q, PAGE 19:

"During the three months ended March 31, 2015, the Company issued an aggregate of 4,783,568 shares of its common stock in the amount of $41,782 for the settlement of outstanding accounts payable and accrued expenses. In connection with the issuance of the shares the Company recognized a gain on settlement of accounts payable and accrued expenses in the amount of $41,507 (see Note 5).

During the three months ended March 31, 2015, the Company issued 6,650,000 shares of common stock in settlement of litigation. In connection with the issuances, the Company recognized a loss in the amount of $59,850, which is included in the marketing, general and administration expense in the Statement of Operations (see Note 12).

During the three months ended March 31, 2015, the Company issued an aggregate of 40,704,366 shares of its common stock for the conversion of $231,727 of notes payable and related accrued interest. Upon conversion of the notes, the Company recorded an adjustment to the derivative liability in the amount of $230,999 (see Note 13).

During the three months ended March 31, 2015, the Company issued an aggregate of 35,520,249 shares of common stock in exchange for $283,578 under the stock purchase agreement with Magna Equities II, LLC (see Note 6), and issued an aggregate of 1,443,656 shares of common stock in exchange for $16,270. In connection with the stock sale, the Company issued an aggregate of 1,443,656 warrants to purchase the Company’s common stock (see Note 11)."

WHY would a company supposedly "close" to being able to supposedly being able to fund or pay for its own large, expensive clinical trials supposedly "due to revenues"- WHY would they be paying common bills such as "accounts payable" in common shares of stock, as well as, be continually issuing 10's and 10's of MILLIONS of shares of stock to all kinds of people/firms to pay their bills due, as they DO NOT HAVE THE CASH TO PAY THEIR BILLS as shown in those 10-Q filing statements above? WHY OR HOW WOULD THAT BE?

Quote:

"and with their combined subsidiaries BHRT is generating the revenue required to move forward with trials to ultimately acquire the approvals needed for their premier products."

So if ONE IOTA of that was reality- then WHY are they doing floorless convertible debt deals (aka "toxic" - that's what the SEC calls um)- WHY are they doing financing deals with 45% and 47% share discounts as recently as April of 2015, for pittances of $25K and $33K AND tapping a Magna dilution credit line at the same time AND paying out 10's and 10's of MILLIONS of shares of common stock (massive dilution) to pay their bills? WHY ?? HOW is the claim they're about to fund some clinical trials possible- when they are for all intents and purposes CASH BROKE or very close to CASH BROKE at any given time per their own SEC filings, their own auditor's GOING CONCERN WARNINGS, their own mgt's GOING CONCERN WARNINGS, their own SEC filing CASH ON HAND statements, etc?

Makes ZERO sense to me- the "claims" being made make no sense and don't match the reality of the company's own SEC filings in any way, shape or form that I can see? None???

Quote BS LOL, "Retail shorts still in denial"

What??????

1) There is almost ZERO "retail" open short interest in this stock, LOL!!

2) IF one was short this stock- THEY are the only ones who've been making money on it. It'd DOWN approx 99% since it began trading public. It's DOWN from a high of about $12.50 on a one yr chart. It's DOWN approx 50% on a short term chart- from $7.50 approx 60 days ago to barely $5 and change today with a very recent new 52 WEEK LOW of $4.88, LOL !!! A shorts dream come true. It would be LONGS IN DENIAL based on all the pertinent FACTS and actual reality???????????

3) If ANYONE is "short" this stock to any large degree- it's 100% most likely a) The UNDERWRITERS and b) THE HEDGE FIRMS THEY SOLD THE SECONDARY TO such as Blackrock thee hedge fund and c) The book-running firms such as COWEN who just issued the "buy" rating today- a very common "sign" of a firm looking to unload a lot of shares FOR THEIR OWN POSITIONS or "clients" of theirs (aka hedge firms and similar). Those are the "usual suspect" likely short candidates. Oh, and any "pro" as in professional Nasdaq hedge fund or similar "pro" short trading desk- who live off of weak, barely $5 per share, cash poor, highly speculative, low float, easy target SHORT CANDIDATES, GOLDEN SHORTS such as OCAT presents right now. NO PRODUCTS, NO REVENUES, HIGH DILUTION, LOW CASH, NO PROSPECT OF REVENUE OR PRODUCTS FOR YEARS if EVER, etc GOLDEN SHORT TARGET PAINTED IN BRIGHT RED IMO.

LONGS are in "denial" if anyone, LOL !!! Pull up a 3 month, 6 month, 1 yr, 2 yr, 3 yr, 5 yr chart- it's a LOSER or DEAD MONEY if there ever was one, LOL !! What would any short supposedly "be in denial" about- they and the insiders who sell n dump share for self enrichment are about the only ones who've made any real bank off this stock???

The statement makes ZERO sense? None.

"Jefferies LLC and Cowen and Company, LLC are acting as joint bookrunners for the offering. Raymond James & Associates, Inc. is acting as co-manager for the offering."

http://www.streetinsider.com/Corporate+News/Ocata+Therapeutics+(OCAT)+Prices+5.5M+Common+Stock+Offering+at+$5.50Share/10658009.html

SHAZAM, well whata ya know, eh? Holy cow- I'm soooo surprised. You mean COWEN was/is involved intimately in the ole secondary offering and now their un-biased "analyst" just happens to issue a big ole positive "recommend" on lil ole OCAT, LOL !! Dang, I can't hardly believe it, LOL !

AND THERE YOU HAVE IT- why "Cowen" of all firms suddenly issue their favorable "coverage" for ole OCAT. THEY have scratch "in the game".

COWEN ran book on the offering- they have shares to unload. It's as OLD AS TIME ITSELF on Wall Street for a firm involved in needing to "unload" shares- so pull a magic rabbit "analyst buy rating" out of the proverbial hat, perfectly timed with THEIR OWN NEEDS to "move shares" in the very stock they just happen to be "covering" !!

NOoooo "conflict of interest" there, NOoooooooo, LOL !!!! Ole "Boris the analyst" for ole Cowen, right on cue post the secondary. And one wonders why no one had ever heard from this "analyst" prior- regarding ole OCAT or ACTC?????

Right on !

Quote BS LOL, "However I agree it was kept at $0.0055 to allow the majority of the float to be purchased by the penny movers being that they have found that it is much easier to buy the float than the way they did in the past which was to promote and buy into the promotion.

MAXM is almost ready. I expect a press release after the next 10q announcing a $7-10m offering etc."

WHAT???????????????? WHAT DOES THAT EVEN MEAN, LOL !!!!

.0055 what? The new all, all, all time LOW is .004 and it did a LOT of volume at .004 AND at .0045 AND at .005, so what's special about supposed .0055, LOL !!!! What? MAKES NO SENSE IMO????

"it was kept at .0055" to "allow the majority"??? WHO is the "majority" - WHAT DOES THAT MEAN????? And so the "penny movers"??????? WHAT? WHO are so called "penny movers"????????? Because "they", THEY WHO? WHO ARE "THEY", LOL !!! So that the mystery "they" could supposedly " buy the float" WHAT, LOL!!!! "the way they did in the past"?? What? "they" who and in what "past" did "they" do whatever "they" supposedly do, LOL !!! And the ole "promote" thingy- WHAT DOES THAT MEAN? "buy into the promotion", LOL !!!!! WHO? WHO buys into what supposed "promotion" and why? Why do "they" supposedly "buy into a promotion" and WHAT is a "promotion" supposed to even be or mean? WHERE IS THERE PROOF OF ANY OF THIS?

Who, what, where, when and why? WHO is "they" - what's the name of these people or firms or whatever "they" supposedly even are????? Give exact details of ONE instance in the past of "they" doing what "they" do and EXACT details of what a "promotion" is and when it occurred and where it's shown to be documented and who paid for it and all the rest? ONE EXAMPLE? WHERE and WHEN with backing data to prove it? "they", LOL !!!!

AND, now back to the ole "Maxim" is going to blah, blah, blah WHAT? WHY? Now it's a "Maxim offering"?????? OFFERING OF WHAT? What are they going to "offer" and how and why and who's gonna put up the $7 to $10 MILLION for a 6/10ths of ONE CENT, CASH POOR, DEBT LADEN nano-cap???????? What? Who other an a dilution, convertible debt lender with infinite down-side protection, LOL !!! And WHY is MAXIM supposedly going to finance this company when Manga already has financing in place as does Daniel James and Asher And Vis Vires and Fourth Man and KBM Worldwide and who knows now- until the 10-Q is released, LOL !!! WHY is Maxim of all people going to supposedly lend or inject $10 MILLION or whatever into this company? BASED ON WHAT PROOF? An MM symbol that's sitting out on the Level II, RIGHT THIS MOMENT, LOL !!!!!!!!!!!!!! Really? And why then now after the next 10-Q, LOL !!! I thought this Maxim thingy was already happening- just like the 10 cents, no 15 cents, no $1 BILLION market cap, no $2 BILLION market cap, LOL !!!!!

Makes NO SENSE TO ME, NONE?????????? Pulled form the thin air IMO? Who are "they" anyway? WHAT DOES THAT EVEN MEAN? Maxim, LOL !!!! Right on?

Some SELLING/DUMPING OFF into a blip of strength already, UH OH??????

First sign of a few percent blip and it's got some pretty decent SELLING going on, on volume???

As another post stated- WHAT "credible" so called "analyst" puts out a price target "prediction" of an over 500% increase to take place in a one yr or less period of time and is supposed to be taken seriously? What brand of crystal ball does this "Boris" the stock analyst use and what's his historical accuracy rating on these vast and glorious incredible price appreciation targets, LOL !!!!

Just do the match on what $35 a share = in market cap and it's laughable at this stage for a cash poor micro cap that can't even get it's key trial(s) out of the parking spot yet.

Real question is- did Cowen BUY or PARTICIPATE IN ANY OF THE SECONDARY OFFERING- and therein would lie a very "key" piece of "data" IMO (an old saying, "there lies the rub"). All one would need to know IMO. If I was a betting man, I'd put some bank on it that COWEN has a piece of the action in this secondary one way or another. And thus SHAZAM, a vast price target "analyst" prediction just pops out from ole "COWEN" and their "Boris the analyst" the vast predictor of stock prices.

My $5 bucks and small change worth

Quote, "New here. I have been researching their technology, and am having trouble finding efficacy data on their treatments."

ALL information about the company is in their duly file SEC 10-K (annual) and 10-Q (quarterly) reports. IMO, that is the ONLY place one should look for reliable information about the company- not using "PR" or similar info as it often changes later because it is subject to the "safe harbor" and protection of the "forward looking" disclaimer info one will find attached to the bottom of every "PR" type statement issued.

ALL BHRT (Bioheart) SEC filings ever made are located in the SEC, U.S. govt Securities and Exchange system website database known as "EDGAR":

http://www.sec.gov/cgi-bin/browse-edgar?action=getcompany&CIK=0001388319&owner=exclude&count=40&hidefilings=0

That is EVERY SEC filing ever made by Bioheart.

For example, a "PR" style release regarding something about "South Africa" was made- but if one reads the later filed SEC document, they will find that for all intents and purposes, it appears that this "South Africa" thingy never actually really sorta-kinda never occurred and has never been mentioned or spoken about since.

10-Q filing, PAGE 23 (POST the "PR" on ole "South Africa", which in the subsequent 10-K was never mentioned again, as one example)

http://www.sec.gov/Archives/edgar/data/1388319/000114544314001305/d31740.htm

""We announced a joint venture in South Africa and the facilities called “South African Stem Cell Institute” were successfully opened in September, 2014 with the intention to retain a 49% ownership of the new entity. As of September 31, 2014, however, there was no formal legal entity established and no formal operating agreement for this joint venture. In additional the Company has not yet incurred any material expenses associated with this venture. Management has concluded that as of September 31, 2014 this announcement is not material to the Company’s financial statements."

LIKE IT NEVER REALLY HAPPENED- despite the "PR" that was cited. LOL WHAT??? SO, "it" the ole "South Africa" thingy supposedly "had" a "grand opening" and supposedly "treated patients" blah, blah according to "PR", but then that pesky ole SEC filing comes along and says IT WAS NEVER EVEN A LEGAL ENTITY and NO MATERIAL EFFECT to the company occurred, LOL!!! HOW CAN THAT BE??????? Google "Dr Walter Bell" of South Africa and there is NOTHING said on his site about Bioheart or working with Bioheart or offering Bioeheart supposed "treatments" etc. Google shows only ONE "Dr Walter Bell" in all of South Africa and he's in a tiny, two doctor "clinic" that appears to be run out of a sort of converted "house" off of some small side street- one can view it in Google maps. That's just one example I did per my own research.

OR this one was another "PR CLASSIC" IMO- the ole "Global Stem Cells Group" ole "agreement" thingy - complete with "videos" (one could see them on Youtube, both Bioheart and Global Stem Cells Group mgt appeared on them together) made about the big "partnership" and lots of "PR" about how it would "expand BHRT globally" I think it said like to a "global worldwide network of physicians" - something like that, LOL !!! and a blah, blah, blah. Some stock and warrants were handed out if memory serves me:

http://finance.yahoo.com/news/bioheart-announces-agreement-global-stem-131629865.html

Well, I don't think that even lasted ONE YEAR and then the ole SEC filing ole "reality" version came out once again:

http://www.sec.gov/Archives/edgar/data/1388319/000114544315000378/bioheart_10k.htm

SEC filed 10-K, PAGE 11:

"We previously partnered with the Global Stem Cell Group to market and make available our AdipoCell adipose derived stem cell therapies to all doctors across the U.S. and in foreign markets. On November 26, 2014, we terminated our relationship with Global Stem Cell Group."

TERMINATED????????? What? All that great sounding ole "PR" and the whole thing just sorta was another "kaput" and went nowhere and amounted to a big ole GOOSE EGG as far as I can tell? But boy, the initial "PR" sure sounded great, no? It did IMO.

As far as "efficacy" - again, the SEC filings are the only reliable source of data/information IMO.

http://www.sec.gov/Archives/edgar/data/1388319/000114544314000356/d31044-10k.htm

Example: Bioheart filed annual report 10-K PAGE 31:

"Our product candidates may never be commercialized due to unacceptable side effects and increased mortality that may be associated with such product candidates.

Possible side effects of our product candidates may be serious and life-threatening.

A number of participants in our clinical trials of MyoCell have experienced serious adverse events potentially attributable to MyoCell, including six patient deaths and 18 patients experiencing irregular heartbeats. A serious adverse event is generally an event that results in significant medical consequences, such as hospitalization, disability or death, and must be reported to the FDA. The occurrence of any unacceptable serious adverse events during or after preclinical and clinical testing of our product candidates could temporarily delay or negate the possibility of regulatory approval of our product candidates and adversely affect our business. Both our trials and independent trials have reported the occurrence of irregular heartbeats in treated patients, a significant risk to patient safety. We and our competitors have also, at times, suspended trials studying the effects of myoblasts, at least temporarily, to assess the risk of irregular heartbeats, and it has been reported that one of our competitors studying the effect of myoblast implantation prematurely discontinued a study because of the high incidence of irregular heartbeats. While we believe irregular heartbeats may be manageable with the use of certain prophylactic measures including an ICD, and antiarrhythmic drug therapy, these risk management techniques may not prove to sufficiently reduce the risk of unacceptable side effects."

One will notice that these FDA level trials have never progressed since- since approx 2009, over SIX YEARS AGO NOW (BHRT states for "lack of funding" in many subsequent SEC filings). SIX YEARS ago approx- and no progress since.

Or, same 10-K, PAGE 40:

"Risks Related to Our Intellectual Property

We hold limited patent and other intellectual property rights, and our success will be dependent in large part on safeguarding our existing intellectual property rights and obtaining patent and other proprietary protection for our product candidates.

We hold limited patent rights in our product candidates. Our MyoCath product candidate is protected by a patent, expiring in September 2017, in which we have an irrevocable co-exclusive license. Our MyoCell product candidate is no longer protected by patents, which means that competitors will be free to sell products that incorporate the same or similar technologies that are used in MyoCell without infringing our patent rights. As a result, MyoCell, if approved for use, may be vulnerable to competition in the form of products that use the same or similar technologies. We have previously licensed certain patents and patent applications relating to our MyoCell product candidate. These licenses have all lapsed as of the date of this report, although we have had discussions with the relevant licensor regarding a potential reinstatement of our rights in such licenses."

Reading SEC filings is critical IMO if one wants as "true and accurate" a picture of what's going on at any public traded company IMO.

My .0065 or so CENTS worth (the present Bid, which is the max one would get for their shares right now then)

0.0065 / 0.007 (120000 x 170000)

Quote BS LOL, "Target PPS $35.00 Top Ranked Cowens & company Analsyt Boris Peaker rates OCAT OUTPERFORM with 1 year target PPS $35.00. YMB "

What? ANY ACCURACY RATING INFO ON HOW OFTEN OLE "Boris" is ever CORRECT in his vast "predictions" and ole "price targets"?????????????????? What makes this analyst "Boris" supposedly "top ranked", LOL !