News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

sumisu

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

I just finished reading this article and it's scary.

"But we can't eat oil. A nation might have the financial means to buy energy or be blessed with energy resources within its borders, but if superbugs wipe out much of its cereal and other commodity crops and its livestock, its people will go hungry."

"Here's the problem with superbugs: you can't kill them with standard-issue antibiotics. They spread like wildfire through monoculture crops and livestock yards and kill with indiscriminate alacrity.

The only solution, poor as it is, is to kill every animal that might be infected--tens of millions or hundreds of millions in the case of African swine fever."

Ironically I have not directly had antibiotics for years other than in the food that I might be consuming!

Thanks

PS: My personal antibiotic is chicken noodle soup loaded with hot pepper. I will develop a vegetarian alternative with noodles.

Peak Oil Review: 15 April 2019

By Tom Whipple, Steve Andrews, originally published by Peak-Oil.org

https://www.resilience.org/stories/2019-04-15/peak-oil-review-15-april-2019/

Quote of the Week

“Shale companies from Texas to North Dakota have been managing their wells to maximize short-term oil production. That has long-term consequences for the future of the American energy boom. By front-loading the wells to boost early oil output, many companies have been able to accelerate growth. But these newer wells peter out more quickly, so companies have to drill new ones sooner to sustain their production. In effect, frackers have jumped on a treadmill and ratcheted up the speed, becoming ever more dependent on new capital to keep oil production humming, even as Wall Street is becoming more skeptical of funding the industry.” Rebecca Elliot, The Wall Street Journal (4/8)

1. Oil and the Global Economy

Oil prices continued to creep up last week closing out at $71.55 in London and $63.89 in New York, making the sixth consecutive week of gains. If you have been watching your gas pumps lately, you have noted that regular is up 30 cents a gallon in the last month to average $2.83 in the US. In California, however, regular is just about $4 a gallon and is going for $4.62 in one county.

The now familiar situations in Venezuela and Iran have been joined by upheavals in Libya and Algeria as places where oil exports could fall substantially. On the bearish side is news that there may be a settlement to the US-China trade war and a new IMF forecast that cuts global growth for 2019 down by 0.2 percentage points to 3.3 percent. The IMF sums up the oil situation by saying: “Upside risks to [oil] prices in the short term include geopolitical events in the Middle East, civil unrest in Venezuela, a tougher US stance against Iran and Venezuela, and slower-than-expected US production growth. Downside risks include stronger-than-expected US production and noncompliance among OPEC and non-OPEC countries. Trade tensions and other risks to global growth can also further affect global activity and its prospects, in turn reducing oil demand.”

The Wall Street Journal ran a very significant story last week pointing out that shale oil drillers in the US have been managing their wells to maximize short-term production in a way that will have long-term consequences for future production. “By front-loading the wells to boost early oil output, many companies have been able to accelerate growth. But these newer wells peter out more quickly, so companies have to drill new ones.”

This paradigm is in contrast with what Exxon and Chevron plan to do in the Permian in the next few years. “You don’t try to grow production fast,” Chevron Chief Executive Mike Wirth said in a recent interview. “You really look at the entire life cycle of the asset.” The story notes that the growth of shale oil already has begun to slow. U.S. production fell slightly to 11.87 million b/d in January, from 11.96 million in December, after rising steadily for much of last year. The next few months should give us a good idea of whether forecasts of a 1.4 million b/d increase in US oil production this year have a chance of coming true.

The OPEC Production Cut: The future of the OPEC+ production cut is coming into question with the 32 percent increase in oil prices this year to circa $72 a barrel coupled with the expectation that less oil will be coming from Venezuela and Iran and possibly from Libya and Algeria. Even the likelihood that there will be a significant increase in US shale oil production this year is coming into question. The current OPEC+ agreement to cut 1.2 million b/d for six months expires at the end of June.

OPEC’s monthly oil market report which came out last week estimates that the cartel’s production in March was down to 30.2 million b/d, 534,000 b/d lower than in February. Last month was the cartel’s lowest production since February 2015. Saudi production was down by 324,000 b/d for the month to less than 10 million b/d. OPEC says that Venezuela’s production was down by 289,000 b/d during March although this number is at the high end of estimates as to what happened to Venezuelan output in March.

Moscow has never been enthusiastic about the current production agreement and has been slow to make cuts, citing technical reasons. In the last few weeks, there have been official hints that the production cut will end on June 30th. The Saudi energy minister said last week that it was premature to tell whether a consensus existed among OPEC and its allies to extend oil supply cuts, but a meeting next month would make the decision. The minister added that “I don’t think we will need (to do more) … the market is on its way toward balance. We have done a lot more than others.”

US policies targeting Iran and Venezuela have introduced a new level of uncertainty for OPEC as the producer group struggles to predict global supply and demand. Some Saudis are saying that OPEC will act after it sees what the Trump administration does about the waivers which currently allow some Iranian exports to its best customers.

US Shale Oil Production: The most important news of the week was Chevron’s purchase of Anadarko Petroleum for $33 billion. The combined company is set to become the leading operator in the Permian Basin. In recent years, small and midsize oil-and-gas companies such as Anadarko have performed poorly and are facing investor pressure to slow growth and deliver more profits and cash flow. Chevron’s move says the firm believes that large integrated companies can make a profit from whatever remains of the shale oil boom where smaller producers have failed.

The EIA remains optimistic about the future of US crude production which it now expects to increase by 1.43 million b/d in 2019 to average 12.39 million b/d. This is an increase from the EIA’s last forecast of a 1.35 million b/d increase this year.

There are several reasons to question the EIA’s forecasts. Last week, North Dakota reported production of 1.355 million b/d during February, down from 1.403 million in January. Bad weather this winter slowed fracking operations, and well completions were down to 59 in February from 113 in December and 92 in January. Fracking in sub-zero temperatures is not possible. The rig count in the basin currently is three below the January count, and the state government says that “gas capture, workforce availability, and competition with the Permian and Anadarko shale oil plays for capital continue to limit drilling rig count in the state.” North Dakota is having problems with more natural gas coming to the surface than can be piped away, so that the percent flared in February climbed to 19.2 percent. State policy is that only 12 percent of total production is allowed to be flared.

If a 1.4 million b/d increase in US shale oil production happens this year, the increase will have to come from the Permian Basin as the other shale oil regions are growing slowly and give indications of approaching a peak. April’s Permian crude production is expected to reach 4.177 million b/d, according to Energy Information Administration, up 8,000 b/d from March while the April natural gas output will increase to 14,075 million cf/d from March’s 13,859 million cf/d. The price gap between Permian Basin oil and gas will continue to widen as steady demand for crude continues to overwhelm oversupplied natural gas markets, an analysis by S&P Global Platts showed last week. Permian natural gas prices have fallen to record lows as planned maintenance on transmission lines strands gas, forcing some regional gas processing plants to flare.

As the smaller and middle-sized drillers in the Permian say they are reducing capital expenditures, any large increase is likely to come from Exxon and Chevron who are talking about substantial increases in profitable production where smaller companies have failed. The large companies, however, say they plan to move very slowly to ensure that they extract all the oil possible and not front-load production so that more oil comes out in the first month and then tails off quickly resulting in less production during the lifetime of the well than expected. How well these plans come out would seem to be the key to the future of the US shale oil industry and maybe even the global oil industry itself.

2. The Middle East & North Africa

Iran: Tehran’s oil exports have recovered close to prior levels, supported by robust demand from China and South Korea, according to data from shipping sources and provisional tanker tracking data. Shipments from Iran grew 12 percent to 1.70 million b/d in March, the highest since October, as buyers scrambled to import more oil before US sanctions waivers expire in early May. Exports could fall this summer if the US tightens its sanctions on Iran crude purchases from the eight countries given special treatment.

India imported about 5 percent more oil from Iran in the last fiscal year through March as companies raised purchases ahead of US sanctions. However, Indian refiners are holding back from ordering Iranian crude for loading in May waiting to see if Washington will extend the waivers. Companies that continue to do business with Iran, including oil purchases allowed under US waivers, will have to be careful in their dealings with Tehran after the US designated the Islamic Revolutionary Guard Corps a terrorist group. Most importers of Iranian oil do far more business with the US than with Iran and fear that their trade could be damaged if they become involved with some Iranian firm run by the Revolutionary Guard.

Iraq: The Basra Provincial Council has voted to hold a referendum on creating a new federal region, as anger over a dysfunctional government in Baghdad continues. If past efforts to turn Basra into a distinct region are any indication, there will be many obstacles to gaining some form of home rule as the Kurds have. There will be no support from the federal government to hold a vote, and the problem of convincing over half the population to vote “yes.” Basra is the oil hub of Iraq with much of the oil and the export terminal. Should some form of limited independence emerge, still more controversy is likely.

Saudi Arabia: Saudi Arabia’s crude production slumped to the lowest in two years as the Kingdom cut output to boost prices. The country’s rate of compliance with the OPEC+ production cut agreement reached 153 percent according to the IEA. The Saudi cut, coupled with a sharp drop in production in Venezuela under the weight of sanctions and a string of blackouts, helped reduce global oil supply by 340,000 bpd in March.

Saudi Aramco is set to raise $12 billion with its first international bond issue after receiving more than $100 billion in orders, a record-breaking vote of confidence in the prospects for the giant oil company. A bond issue is a safer form of investment in an oil company in a nation that can turn a larger share of profits into tax revenues should the need arise. The question now is whether the Saudis will continue with the plan to sell a 5 percent equity interest in Aramco or continue to issue bonds to raise the capital needed to diversify the economy.

The government denied last week that recent claims the Kingdom would sell its oil in currencies other than the dollar are accurate. The statement follows reports that Riyadh was considering switching from the dollar to other currencies in its oil trade in response to anti-OPEC legislation plans in the US Congress. Reuters reported last week that the switch to other currencies had been discussed in senior Saudi circles and that it had also been shared with US government officials. The Saudis fear the possibility that they could be involved in US litigation for as long as OPEC lasts.

The Saudis could begin natural gas exports in five to six years and have already started talks with neighboring Gulf Arab states about building natural gas pipelines to friendly countries in the Persian Gulf. The Saudis claim that large quantities of natural gas have been found in the Red Sea.

Libya: The National Oil Corporation said last week it is discussing ways to keep national crude production stable despite fighting between the country’s two main rival forces. For now, oil production and exports remain unaffected despite the fighting, but the recent escalation in violence has raised the risk of oil supply outages. The CEO of the oil company says that Libya’s oil and gas exports are facing the most significant threat since 2011 given the scale of the fighting. “Unless the problem is solved very quickly, I am afraid this will affect our operations, and soon we will not be able to produce oil or gas.”

Days before General Haftar launched an offensive to seize the capital and attempt to unite the divided country under his rule, Saudi Arabia promised tens of millions of dollars to help pay for the operation, according to senior advisers to the Saudi government. Should Haftar succeed in taking Tripoli, he will still face many opponents across the country who will likely look to sabotaging oil production as their best option.

3. China

BP is set to become the latest international oil company to quit drilling for shale gas in China because of poor exploration drilling results. In 2016, BP and China National Petroleum Corporation signed a production sharing contract for shale gas exploration, development, and production in the Sichuan Basin in southwestern China. Later in 2016, BP signed a second PSC deal with CNPC for shale gas exploration. However, poor results are now making BP withdraw from the projects. Every few months Beijing announces a renewed effort to exploit shale oil and gas, but so far there have been no significant results.

Those worried about the climate will be unhappy to learn that China is set to produce an additional 100 million tons of coal this year according to Wang Hongqiao, vice president of China National Coal Association. “Coal demand for power generation in China will increase, but the growth rate of general coal consumption will slow down,” Wang said. Imports of thermal coal are due to slip by 11 percent from last year due to increased domestic production. China produced 4 billion tons of coal in 2018, according to the National Bureau of Statistics but also added 194 million tons in mine capacity that year, despite promising to cut excess capacity for the sector.

China’s economic transformation over the last 40 years has driven its demand for forest products, and it is now the world’s largest importer of wood. It is also the largest exporter — turning much of the wood it imports into products headed to Home Depots and Ikeas around the world.

Since China began restricting commercial logging in its forests two decades ago, it has increasingly turned to Russia, importing vast amounts of wood in 2017 to satisfy the needs of its construction companies and furniture manufacturers. This situation is leading to a backlash in Russia where environmentalists are starting to complain that China is taking too much of the Siberian forests. Protests have erupted in many cities, and members of Russia’s parliament have assailed governmental officials for ignoring the environmental damage in Siberia and the Far East.

Chinese demand is also stripping forests elsewhere — from Peru to Papua New Guinea, Mozambique to Myanmar. In the Solomon Islands, the current pace of logging by Chinese companies could exhaust the country’s rain forests by 2036. In Indonesia, activists warn that illegal logging by local Chinese partners threatens one of the last strongholds for orangutans on the island of Borneo.

4. Russia

Shell pulled out of a project to build a Russian liquefied natural gas plant partly because Gazprom suddenly added another partner with links to President Vladimir Putin. After three years of work on the Baltic Coast project, Shell discovered that Gazprom was bringing in a company linked to Arkady Rotenberg, who is on a US sanctions blacklist. The sudden change in the line-up of partners was one of the key factors contributing to Shell’s Wednesday announcement that it was pulling out of the project.

Belarus is threatening to suspend transit of Russian crude to Europe via the Druzhba Pipeline in an attempt to pressure Moscow amid deepening economic disagreements between the two countries. Russia exports more than 1 million b/d of crude to Europe through Druzhba, including to Germany, Poland, the Czech Republic, Slovakia, and Hungary.

European refiners are paying the price for the sanctions on Venezuela and Iran as they try to find replacements for the sour crude Washington has blocked from the global market. To make matters worse, OPEC members have cut sour crude output as part of their deal with allied producers to boost oil prices, and a new refinery designed to run on sour oil has just started up in Turkey. So far Moscow is the primary beneficiary of the sour oil shortage as prices for the grades are increasing.

5. Nigeria

The International Monetary Fund (IMF) has advised Nigeria and other countries still subsidizing fuel for domestic consumption to stop doing so. The IMF said fuel subsidy removal would help boost revenue and improve on local infrastructure development. IMF wants Nigeria to remove the subsidy due to the lack of funds for infrastructure reforms and other social services. Nigeria has among the lowest tax to GDP ratios in the world. The fund also noted that Nigeria’s Excess Crude Account, which takes in revenue during times of high oil prices and pays out when prices are low, was not achieving the goals for which it was set up.

Petroleum Minister Kachikwu said the average production cost for a barrel of oil in Nigeria has declined to just $23 a barrel and that oil companies are aiming to reduce this further, to $15 a barrel. Some 226 companies have bid for a contract to manage the 176 gas flaring sites in Nigeria. The government wants to stop gas flaring in the country by the year 2020 as the wasteful practice is losing billions, but it will take a substantial investment in new pipelines and natural gas utilization facilities to make any progress. Given past experience, it is doubtful if the government’s goal will be met.

More than 50 percent of Nigeria’s oil and gas blocks remain untapped as gas shortages persist in the country. Out of 390 oil blocks in the country, 211 are yet to be allocated by the Federal Government. With many other countries making efforts to increase their oil and gas production, industry experts are concerned about the lack of new oil-licensing rounds in Nigeria since 2008.

6. Venezuela

Venezuela’s oil output sank to a new low last month due to US sanctions and blackouts. OPEC reported last week that Venezuela pumped 960,000 b/d in March. This number was published by Caracas and may be an exaggeration of production. Of more importance is the status of the four crude oil upgraders which normally process some 700,000 b/d of heavy oil so that it can be refined or exported.

While power has been mostly restored for at least part of the day in Caracas, much of the country where Venezuela’s industry is located is receiving power for less than 12 hours a day. As of the last report, only two of the four heavy oil upgraders have resumed operations, and together they are processing less than 300,000 b/d. The two other upgraders appear to have been out of service for over a month. If the operators are unable to get the upgraders back into service, Venezuela’s oil production and exports should be substantially lower in April.

Washington continued its crusade against the Maduro government last week by slapping more sanctions on shipping companies transporting oil from Venezuela. The US blacklisted four companies with nine ships for carrying oil some of which went to Cuba.

Venezuela’s government has signed an agreement with Russia under which the iron, steel, mining and agriculture industries will receive Russian investment and other participation. This agreement is nonsense as the press is reporting that only a small part of the country’s industrial concerns is working.

7. The Briefs (selections from the press – date of article in Peak Oil News is in parentheses – see more here: news.peak-oil.org)

Norway, Western Europe’s biggest petroleum producer, is falling out of love with oil. To the dismay of the nation’s powerful oil industry and its worker unions, the opposition Labor Party over the weekend decided to withdraw its support for oil exploration offshore the sensitive Lofoten islands in Norway’s Arctic, creating a solid majority in parliament to keep the area off limits for drilling. The dramatic shift by Norway’s biggest party is a significant blow to the support the oil industry has enjoyed and could signal that the Scandinavian nation is coming closer to the end of an era that made it one of the world’s most affluent. Oil companies led by state-controlled Equinor ASA, the biggest Norwegian producer, have said that gaining access to an estimated 1 to 3 billion barrels of oil offshore Lofoten is key if the country wants to maintain production as resources are being depleted. (4/10)

In Sudan, President Omar al-Bashir, who has ruled since 1989, was toppled from power by the military on Thursday and placed under “heavy guard”, following months of protests against the government and its handling of a severe economic crisis in the country. After South Sudan’s secession from Sudan, the two countries have been mutually dependent on oil revenues, because the south has 75 percent of the oil reserves, while the north has the only current transport route for the oil to international markets.

South Sudan’s information minister told reporters in Juba, the capital, that the country will provide 30,000 b/d to state-owned lender Export-Import Bank of China to help fund South Sudan’s largest infrastructure project, which is being funded by Beijing. The amount has tripled from the 10,000 b/d it provided to China in February. South Sudan, which produces around 170,000 barrels of oil per day, gained its independence from Sudan in 2011 after years of civil war which saw China supply Sudan with arms and financing in spite of allegations of human rights abuses. (4/9)

The future of Algeria’s oil industry was called into question earlier this week as its political crisis took hold, and now its future is even more suspect, as its state-run oil company, Sonatrach, will once again find itself under the microscope as old corruption investigations are reopened and as the date is set for presidential elections after President Bouteflika stepped down earlier this month. (4/12)

Algeria again: The oil patch is reeling from a political crisis in Algeria that first saw Exxon halt its prospective shale ambitions in the country and has now spread to major trading houses and far beyond its borders. (4/10)

New “Arab spring”? From a Western point of view, the removal of president Bashir of Sudan, after several weeks of mass protests in Khartoum and other cities, is in line with the exit of Algeria’s long-time leader Abdelaziz Bouteflika. Optimism in the press, especially in the West, over both developments seem to be based on emotions and not on facts. As the Arab Spring has shown, don’t ever count out the existing power structures of the respective regimes, and specifically the armed forces. The Egyptian revolution was the first example, shortly after the ‘democratic revolution’ the military took over and reinstated the status quo. (4/12)

In Papua New Guinea, ExxonMobil, France’s Total, and Australia’s Oil Search have signed a gas agreement with the government, outlining the fiscal terms for a new liquefied natural gas (LNG) project in the Pacific island, estimated to cost $13 billion and thought to double Papua New Guinea’s LNG exports from the Exxon-operated PNG LNG plan. (4/10)

In Argentina, oil production from shale in Vaca Muerta is expected to reach 200,000 b/d by the end of 2021, said Ryan Carbrey, senior vice president of Rystad Energy. The play produced 78,000 b/d in February, up 70 percent year on year. (4/10)

Mexico’s government will open retail gasoline stations controlled by the army if retailers do not decrease fuel prices, President Andres Manuel Lopez Obrador said last week. CIF Eastern Mexico RBOB gasoline prices have averaged Peso 9.71/liter so far in April, down slightly from the October average of Peso 10.04/l. But according to the Mexican government, retail profit margins for regular gasoline have increased by 55 percent since October, as retailers have absorbed tax cuts without passing on the savings to customers. (4/10)

The US oil rig count grew by two to 833, while the active gas rig count dropped by five to 189, according to Baker Hughes, a GE Company. This brings the nation’s total to 1,022 rigs – 14 higher than one year ago when the rig count was 1,008. (4/13)

New data from the US EIA revealed that demand skyrocketed to 9.8 million b/d last week. The estimate is approximately 700,000 b/d more than the previous week and 550,000 b/d more than the first week of April in 2018. Many market analysts expect the estimate to be revised downward when EIA releases final demand figures for April later this year, but the high estimate likely signals that 2019 could bring the highest gasoline demand rates ever recorded by EIA — potentially as early as this summer. (4/13)

Rotten oil? Exxon Mobil is the latest company to raise concerns that a stockpile of US government crude is tainted with poisonous gas. The American energy giant said some of the oil it purchased last year from the Energy Department’s Strategic Petroleum Reserve, or SPR, contained “extremely high levels” of hydrogen sulfide, up to 250 times higher than government safety standards allow. (4/13)

In the GOM: Shell has sold its 22 percent interest in the Anadarko-operated Caesar-Tonga field in the US section of the Gulf of Mexico to Israeli Delek Group for US$965 million. The divestment report comes on the heels of Shell’s entry into China’s shale gas industry via a joint exploration project with the country’s largest refiner and main shale gas player, Sinopec. The exploration will take place in the eastern Chinese province of Shandong where Sinopec’s shale operations are. (4/12)

Pipeline rules bruhaha: President Trump has signed an executive order seeking to limit states’ powers in the approval or rejection of new oil and gas pipeline projects. The signing was scheduled for a trip to Texas yesterday, and expectations are that opponents of new oil and gas infrastructure will challenge it in court. Some lawyers have noted the states’ powers to grant or refuse permits for federal infrastructure projects are stipulated in federal law and a presidential order cannot trump this. (4/11)

New at Interior: The Senate on Thursday voted to confirm David Bernhardt, a former lobbyist for the oil and agribusiness industries, as secretary of the interior. The confirmation of Mr. Bernhardt to his new post coincided with calls from more than a dozen Democrats and government watchdogs for formal investigations into his past conduct. (4/12)

US natural gas-fired combined-cycle capacity overtook coal-fired capacity in 2018, the US Energy Information Administration reported on Wednesday. In the United States, natural gas-fired combined-cycle capacity has increased for years, finally overtaking coal-fired capacity, which has seen a steady decline over the last decade. (4/11)

The US’s 2019 coal production of 684.1 million tons will likely be 9.2 percent lower than the 753.7 million tons produced in 2018, while 2020 production is estimated at 640.1 million tons, the EIA said in its April Short-Term Energy Outlook. The 684.1 million tons expected in 2019 would be the lowest production since 670.16 million tons was produced in 1978. (4/10)

Car guys’ nightmare: As the Trump administration prepares to drastically weaken Obama-era rules restricting vehicle pollution, nervous automakers are devising a strategy to handle their worst-case scenario: a divided American auto market, with some states following President Trump’s weakened rules while at least one-third of the market sticks with the tougher ones. The new rules would all but eliminate the Obama-era restrictions, essentially freezing standards at about 37 miles per gallon, compared to 54.5 miles per gallon required by the current rules. (4/11)

EV batteries: Ford Motor Company is teaming up with Solid Power to develop all solid-state batteries (ASSB) for next-generation electric vehicles. The announced partnership will focus on further developing ASSBs toward automotive requirements. Solid Power’s solid-state technology combines a cathode, metallic lithium anode, and an inorganic solid electrolyte layer. Solid-state batteries offer improved energy capacity and safety as compared to current industry-standard lithium-ion batteries. (4/12)

Global sales of plug-in electric vehicles fell by 21 percent in February month on month, led by a sharp fall in China due to seasonal factors and ahead of the government cutting subsidies for EVs in March. (4/9)

EV ultra-chargers: An Australian company, Tritium, makes chargers that can add more than 215 miles to an EV’s range in just ten minutes. Companies around the world are developing such superchargers that can “fill up” an EV battery in a matter of minutes, but there is one problem: they can’t be deployed because battery makers have yet to make their product capable of withstanding the supercharge. (4/8)

New biofuel: For centuries the world has agonized over its relationship with waste – by burying it, burning it, flushing it. But entrepreneurs at Fulcrum BioEnergy are now trying to turn it into jet fuel. Organic material like banana peels will be put into a vessel to decompose under pressure and heat, in a similar process to the creation of fossil fuels over hundreds of millions of years. The Californian start-up is investing $280m in a plant near Reno, Nevada, that, once fully operational, is expected to produce 10m gallons of renewable “syncrude” [synthetic crude] a year from organic material that would otherwise go to waste. (4/8)

An Achilles heel of RE: While proponents argue that solar and wind are already cost competitive with oil and gas, that’s not true in extreme winter weather. Critics of the Green New Deal proposed by Congresswoman Alexandria Ocasio-Cortez have used the opportunity to point at the shortcomings of solar and wind in extreme weather conditions as an argument against a Green New Deal. (4/11)

UK’s move to RE: The UK’s Department for Business, Energy & Industrial Strategy has set out its aim to increase renewables generation 75% from 2018 levels by 2035, with the expectation that there will be a gradual decline in gas-fired generation. The department forecast renewables production to rise to 211 TWh by 2035. This 211 TWh also represents 58% of total electricity supplied in the UK in 2035. (4/12)

South Africa is facing an energy crisis. The once distinguished national public energy provider, Eskom, has been driven to the point of collapse by “years of corruption, incompetence and political meddling”. Under the Presidency of Jacob Zuma, Eskom went from making a billion Rand profit in 2008 to making a 2.3 billion Rand loss. The Eskom crisis has only depressed an already strained economy. This critical situation has left Cyril Ramaphosa, the presidential incumbent, in an uncomfortable position. To address South Africa’s myriad problems, Ramaphosa must garner support and reform a party filled with discredited Zuma loyalists. (4/11)

London clampdown: The Ultra-Low Emission Zone (ULEZ) has come into force in central London. Drivers of older, more polluting vehicles are being charged to enter the congestion zone area at any time. However, the Federation of Small Businesses said many small firms were “very worried about the future of their businesses” as a result of the “additional cost burden”. Most vehicles which are not compliant will have to pay £12.50 for entering the area each day, in addition to the congestion charge. (4/8)

Shipping speed limit? France’s delegation to the International Maritime Organization has proposed mandatory slow steaming as a means of cutting the shipping industry’s greenhouse gas emissions. France is suggesting that speed limits differentiated by shipping sector should be implemented “as soon as possible.” Reducing a ship’s speed to the level at which it has maximum fuel efficiency reduces its bunker fuel consumption and emissions. (4/11)

Shell’s carbon offsets: Royal Dutch Shell is launching a $300m forestry program in an attempt to reduce its emissions, at a time when an increasing number of oil companies are investing in carbon offset plans to comply with climate goals. The energy company will spend $300m over the next three years on projects to store carbon, including large forests in the Netherlands and Spain, and will start offering motorists the option of purchasing carbon offsets when they buy petrol or diesel at the pump. (4/10)

Peak Oil Review: 8 April 2019

By Tom Whipple, Steve Andrews, originally published by Peak-Oil.org

https://www.resilience.org/stories/2019-04-08/peak-oil-review-8-april-2019/

Quote of the Week

““Fast [nuclear] reactors are less safe, less secure and more proliferation-prone than light-water reactors. The US Department of Energy should not be asking taxpayers to spend billions on this dangerous reactor.” Ed Lyman, senior scientist with the Union of Concerned Scientists

1. Oil and the Global Economy

London’s oil prices broke through the $70 a barrel barrier last week to close at $70.34. New York futures were some $7 behind to close at $63. Oil prices gained around 30 percent in the first quarter with London and New York posting their best quarterly performance in the last ten years. Behind the unexpected surge in oil prices – US gasoline is up 50 cents a gallon – are the US sanctions on Iran and Venezuela and the OPEC+ production cut. The restraints on production joined with stronger-than-expected demand for oil products to produce the price increase.

Although the IMF is saying that the clouds of a global economic slowdown are gathering, for now the forces pushing prices higher have the upper hand. Last week what could be the beginning of a civil war broke out in Libya threatening the country’s 1 million b/d oil production. Heavy rains are flooding the region where most of Iran’s oil is produced – likely reducing output in the immediate future. Finally, Venezuela is moving towards a total societal collapse with the likelihood of much lower oil exports in the coming weeks.

Then we have indications that the rapid growth of US shale oil production may be slowing as Wall Street holds back on pouring still more money into a money-losing industry. This situation could change if oil prices return to levels of ten years ago or if the Sino/US trade dispute is settled. In sum, the global oil situation is more volatile than usual with many uncertainties ahead.

The OPEC Production Cut: The cartel’s production in March fell to its lowest level since February 2015, as Saudi Arabia cut more than it had pledged under the output deal and Venezuela continued to contend with the US sanctions and a series of power blackouts. There is an unusually large disagreement between Reuters and Platts, with the former estimating that OPEC’s production fell by 280,000 b/d last month and Platts suggesting it was 570,000 b/d. Much of this disagreement seems to be over how much oil Caracas was able to export between power outages that stopped exports for about a week last month. Iraqi exports were down by about 100,000 b/d due to bad weather at its export terminal.

The rate of compliance from the eleven OPEC members bound by the pact—with Iran, Venezuela, and Libya exempted—also suggests that the Saudis and their Arab Gulf partners are deepening the cuts in order to drive prices higher.

Various OPEC ministers have been suggesting during the last few weeks that the production cut needs to be extended when the cartel+ meets in June. Russia has been saying it sees no need for an extension, and with oil prices back above $70 a barrel, it is difficult to make a case for extending the cuts. Should production in Venezuela and Libya fall dramatically in the next two months the loss of exports from these two countries could be larger than the OPEC+ cuts.

US Shale Oil Production: Average daily crude oil production slipped during January for the first time in nearly six months, according to an EIA monthly report, which was based on better information than the weekly production estimates. January oil production for the US averaged 11.871 million b/d for January—down from 11.961 million b/d in December of last year. The January production decline, a falling-off in oil well productivity, a drop in the rig count, and reports that Wall Street is going to slow financing for shale oil drillers who consistently lose money all suggest that change is coming.

US crude production surged in 2018, with overall production rising by 1.7 million b/d to a record 10.9 million. That was the biggest year-over-year increase in output, according to EIA data going back to 1859. The 2018 surge led to optimistic predictions that large increases would continue for the next few years. Financial writers are now suggesting that rapid growth in US shale oil production will soon shift to a plateau, putting more pressure on the OPEC+ consortium to increase output in June.

Even the ever-optimistic EIA trimmed its 2019 production forecast from 12.4 million b/d to 12.3 million. Morgan Stanley also cut its projection for this year by 100,000 b/d due to well “productivity improvements slowing, the rig count rolling over” and guidance from exploration and production companies.

In response to the demands of investors, the small drillers have been cutting spending in response to years of losses. Although Exxon and Chevron are expanding in the Permian Basin, independent companies are not. While the major oil companies plan to spend about 16 percent more on US drilling and completions in 2019 versus last year, the independent exploration and production companies are expected to cut spending by around 11 percent.

Lower amounts of oil are also being delivered per well, slowing the rate of output growth. In the Permian Basin, per-well productivity is projected to fall by about 6 percent this month compared with a year ago, according to the EIA. This development likely reflects an inevitable reduction in the number of productive sweet spots which is forcing drillers to less profitable locations. The course of this trend and oil prices will determine just how much longer shale oil production in the US remains viable.

Another sign of trouble ahead is the drop in the value of merger and acquisitions deals in the US. In the first quarter, the value of these deals plunged 93 percent to a 10-year low as investors began insisting that shale oil producers start to show profits rather than just increased production.

Colorado’s legislature passed a sweeping overhaul of the state’s oil and natural gas laws, giving local governments more power to regulate drilling. The bill, which passed the state Senate amid intense industry opposition, now heads to the desk of the governor, a longstanding proponent of tightening public health and safety standards around oil and gas development. Much of the shale boom in Colorado is concentrated in the relatively dense suburbs north of Denver, which means, unlike the fracking in West Texas and North Dakota, drillers often bump up against homes, businesses, and schools.

Natural gas prices fell into record negative numbers in the Permian basin last week. Natural gas in West Texas is produced as a byproduct. This dynamic helps explain how natural gas prices at the Waha hub in West Texas can fall to a negative $3.38 per million BTUs as producers are paying others to take the gas away. In North Dakota, excess gas is flared despite restrictions, but Texas is imposing stiffer controls.

2. The Middle East & North Africa

Iran: Khuzestan province in southwestern Iran was hit by the worst flooding in 70 years last week. About 1,900 cities and towns have been affected, and some 100,000 people were evacuated to shelters. The province is the center of Iran’s oil industry which has undoubtedly been interrupted by the flooding putting still more pressure on the government which is having trouble coping with the US sanctions.

After a meeting with the Iraqi prime minister last week, President Rouhani said he is ready to expand gas and electricity trade with Baghdad and develop a plan to connect their railroad systems.

Washington’s sanctions waivers which allow eight countries to import oil from Iran are due to expire in six weeks. Oil prices are once again on the rise, as they were six months ago when the Trump administration buckled under the pressure of $80 oil and granted the waivers. Three of the eight countries with waivers have reduced their imports of Iranian crude to zero, and the US says it is not planning to extend them. In the last three months, however, oil prices have been climbing rapidly – partly due to the new US sanctions on Venezuela — with oil prices already in the low $70’s and likely will be higher in a month or so. This situation may force Washington to extend the waivers or face still higher oil prices.

Iraq: Oil exports fell to an average of 3.377 million b/d in March, the Oil Ministry said on Monday, as poor weather interrupted loadings. February loadings were 3.62 million b/d. The severe weather also forced a cut in production at some oilfields including Majnoon, where output declined in mid-March by 140,000 b/d from 240,000 b/d earlier in the month. Basra is close to Iran which currently is suffering from severe flooding so Iraq’s problem may continue into early April.

Iraqi Prime Minister al-Mahdi and Kurdistan‘s Prime Minister Barzani ignored a request to sign pleadings in the court case aimed at settling the long-standing oil dispute between the two governments. Observers say this is a sign that neither side is eager to have Iraq’s highest court decide on their disagreement over the division of oil revenues.

Saudi Arabia: In anticipation of its $10 billion international bond sale, Aramco was forced to issue its first public financial statement since the firm was nationalized nearly 40 years ago. Last year Aramco had earnings of $224 billion and said it has oil and gas reserves of 257 billion barrels which could last for 50 years at the current rate of production. The big surprise in the prospectus was the revelation that the giant Ghawar oil field is only able to produce 3.8 million b/d rather than the 5.8 million b/d that the EIA said it could produce last year.

The news sparked a debate as to whether Saudi production is starting to decline. During a presentation in Washington in 2004 Aramco tried to debunk the “peak oil” supply theories of the late US oil banker Matt Simmons by claiming the field was pumping more than 5 million b/d. The new maximum production rate for Ghawar means that the Permian in the US, which produced 4.1 million b/d last month, is already the world’s largest oil production basin.

Saudi Arabia is threatening to sell its oil in currencies other than the dollar if Washington passes a bill exposing OPEC members to US antitrust lawsuits. The chances of the US bill known as NOPEC coming into force are slim, and Saudi Arabia would be unlikely to follow through on their threat. Should the Saudis abandon the dollar, it would undermine its status as the world’s primary reserve currency, reduce Washington’s clout in global trade, and weaken its ability to enforce sanctions on nation states.

Libya: The political situation underwent a sea change last week when General Haftar, who controls eastern and southern Libya, ordered his troops to march on Tripoli to oust the UN-backed government and take over the country. Heavy fighting is taking place south of Tripoli and militias from Misrata are moving to support the government. The US is moving an unspecified number of troops somewhere in the area and foreigners are evacuating the capital.

When the order to attack Tripoli was given, the UN secretary-general was in Libya trying to broker a solution to the split government by organizing a conference scheduled for next week. This effort now is dead. Many Libyans distrust Haftar who they see as a potential dictator.

Libya has been split for five years between a UN-backed government in Tripoli and rival government in the east under the control of General Haftar. The Tripoli government is protected by an array of militias including a particularly strong one in Misrata. Haftar has been supported by Egypt, the UAE, and Russia.

An important question is what happens to oil production if the fighting is prolonged. Libya recently increased production to over 1 million b/d which could be threatened by a civil war. It was Haftar’s forces who recently moved on the Sharara 315,000 b/d oilfield and restored production there.

3. China

President Trump said last week that the US and China are hoping to reach a trade deal in the next four weeks, though he failed to announce a much-anticipated summit with Xi Jinping. Mr. Trump and his trade team say negotiations are in their final stages, but caution that daunting issues remain—including when to lift punitive tariffs against Chinese imports, protection of US intellectual property and enforcement of the pact’s provisions. There are “major issues left,” US Trade Representative Robert Lighthizer said. “We’re certainly making more progress than we would have thought when we started.”

Chinese factory activity unexpectedly grew in March for the first time in four months, suggesting that the government’s stimulus measures may be starting to take hold. If sustained, the improvement in business conditions could indicate that manufacturing is on a path to recovery, easing fears that China could slip into a sharper economic downturn. But analysts remained cautious, citing seasonal distortions due to the long Lunar New Year break in February.

China’s three state oil and gas companies plan to increase their spending on oil and gas by 20 percent this year, bringing the total to some $74 billion for the first time in five years. Some observers are skeptical that plowing this much money into aging oil fields will pay off with much of a production increase.

China will be able to build six to eight nuclear reactors a year once the approval process gets back to normal according to the chairman of the China National Nuclear Corporation. “That should be enough to meet our country’s 2030 development plans.” China did not approve any new projects in the wake of Japan’s Fukushima disaster until it permitted the construction of two new reactor complexes in southeast China earlier this year.

4. Russia

Moscow’s oil output declined to 11.298 million b/d last month, missing the target set under OPEC+ deal to cut oil production. The March output was down by around 112,000 b/d from the October 2018 level, the baseline of the global deal; however, Russia had pledged to cut its oil output by 228,000 b/d from the October level. Energy Minister Novak said last week that the country’s oil production in April would be in line with the OPEC+ deal.

Rosneft, the largest oil producer in the country, plans to develop an Arctic cluster of oil fields over the next five years. These plans fit President Putin’s ambitions to develop Arctic oil and gas resources and adjacent regions, as well as the Northern Sea Route to the Far East. Russia’s Arctic oil development has stalled in recent years due to the western sanctions that have had international majors, including ExxonMobil, pull out of some exploration projects in Russia.

5. Nigeria

Exxon Mobil may sell the oil and gas fields it holds in Nigeria and has commenced talks on the sales as it focuses on US shale and the new field offshore Guyana, industry and banking sources told Reuters. The potential sales are expected to include stakes in onshore and offshore oil fields and could raise as much as $3 billion. The development followed a statement from the Nigerian National Petroleum Corporation that it would no longer sign off any gas project without plans for stopping natural gas flaring.

Exxon declined to comment on the development, adding that the oil company, which is one of the largest oil and gas producers in Nigeria with 106 operating platforms, is producing about 225,000 b/d in the country.

Petroleum Minister Emmanuel Ibe Kachikwu admitted that reducing oil production to the quota assigned by OPEC is a challenge because of the start of production at the Egina offshore oil field with a capacity of 150,000 b/d.

The petroleum minister has tasked local Nigerian operators to step up their investments and take over operations from international oil companies, especially as many are already considering divesting and charting new paths. The minister emphasized the need to double oil production to 4 million b/d as against the current output of between 1.9 to 2 million b/d. According to the minister, changes in the global oil and gas industry are presently challenging the exploration and investment strategies as oil is fast becoming a degenerating asset with alternative sources of energy taking over.

6. Venezuela

President Maduro announced 30 days of electricity rationing after a third blackout hit the struggling the country early last week. Maduro said rolling blackouts would help the government deal with the power failures that have also affected water supply and communications.

Reuters says that PDVSA was able to keep exports near 1 million b/d in March despite power outages that halted pumps at the main export terminal for at least six full days. The company was able to offset the power failures by loading mainly very large tankers bound for Asia and the company already had the oil to be exported in storage. Venezuela at one time was shipping close to 3 million b/d and still appears to have the ability to load 1 million b/d in three weeks of pumping.

A more severe problem in the weeks ahead is the status of the four crude upgraders which convert the very heavy Orinoco oil into a transportable and marketable crude. The four upgraders have a combined capacity of 700,000 b/d and are mostly operated jointly with the help of partners from the US, Russia, France, and Norway. A large percentage of Venezuela’s crude exports is coming from these facilities as the rest of the country’s oil production is crumbling due to lack of maintenance.

Two of the upgraders have been out of service since the March 7th blackout while the other two stopped production after the March 25 blackout. Work continues on cleaning up the mess when the power goes off unexpectedly. Three of the upgraders may be back in partial operation later this month, but one is expected to be out of service indefinitely. One source told Reuters that PDVSA has canceled all shipments of upgraded crude during April. If this is true, and Venezuela does not have much marketable crude in storage, exports could plummet this month pushing oil prices much higher.

Vice President Pence announced that the US is adding 34 PDVSA owned or operated vessels to the sanctions list. The sanctions not only target the PDVSA vessels but also two firms that transport Venezuela crude oil to Cuba. Pence said that this may not be the final addition to the sanctions list as the US mulls even more sanctions, this time targeting the financial sector.

7. The Briefs (selections from the press – date of article in Peak Oil News is in parentheses – see more here: news.peak-oil.org)

EU oil Co’s to electricity: European oil companies have started to address what they worry may one day be an existential threat to their business — the end of a century of oil demand growth in a low carbon world. The emergence of the electric vehicle and demand among investors and consumers for cleaner energy to limit climate change has pushed the European side of Big Oil to take baby steps towards refocusing their businesses from oil production and refining to electricity via natural gas and renewables. (4/4)

Saudi Aramco made $111 billion in net income last year, according to rating agency Moody’s Investors Service, making the oil and gas firm the most profitable company in the world. Moody’s and Fitch Ratings published snapshots of Aramco’s financials on Monday as they rated the oil firm ahead of a $10 billion Aramco bond sale expected as soon as this week. (4/1)

Egypt will remove subsidies on most energy products by June 15 it told the International Monetary Fund in a January letter released as part of a review of Cairo’s three-year, $12 billion loan program with the lender. Removing the subsidies will mean increasing the price to consumers of gasoline, diesel, kerosene and fuel oil, which are now at 85-90 percent of their international cost. (4/6)

Tanzania’s government will start this month talks with major international firms to define the commercial terms for a deepwater liquefied natural gas project off the coast of the east African country expected to be worth $30 billion. Major international companies have been exploring for gas offshore Tanzania and have found sufficient quantities for a potential LNG plant. (4/5)

Ecuador loses again: The Supreme Court of Canada dismissed claims attempting to force Chevron Corp’s Canadian unit to pay a $9.5 billion judgment handed down in Ecuador against the US oil major over pollution in the Andean country. Residents of Ecuador’s Lago Agrio region have been trying to force Chevron to pay for water and soil contamination caused from 1964 to 1992 by Texaco, which Chevron acquired in 2001. The villagers obtained a judgment against Chevron in Ecuador in 2011. But the company has no assets in the country. (4/5)

In Colombia, state-run oil company Ecopetrol and Exxon Mobil have each signed joint contracts with Spain’s Repsol to explore for oil in offshore blocks in the Caribbean. Colombia recently modified contractual terms for offshore exploration and launched a permanent bidding process to boost its long-stagnant oil sector. Companies including Shell, Noble, and Parex have since signed on to operate new blocks. The two contracts will generate some $700 million in investment. (4/4)

In Canada, the stubborn, sharp rise in heavy crude prices may finally falter later this year, when swelling output overwhelms a pipeline system that will be lacking a key project producers had counted on, according to Deloitte. Western Canadian Select crude prices have more than doubled since the end of November, buoyed by the Alberta government’s output limits for drillers in the province. (4/4)

The US oil rig count increased last week by 15 to 831, up from 808 rigs one year ago, according to GE’s Baker Hughes. Active gas rigs climbed by four to 194, bringing the total rig count to 1,025. The following states added rigs: Texas (8) West Virginia (4) New Mexico (3) Alaska (2) Colorado (2) North Dakota (1). Among the major basins, the Permian saw the most gains as it added eight rigs while the Marcellus added another three. (4/6)

Total weekly US crude and product exports should be consistently outpacing imports starting in 2020. Thanks to hydraulic fracturing and horizontal drilling, crude production has boomed 140 percent over the past decade. During 2018, for instance, output rose nearly 25 percent, even more impressive since domestic prices (WTI) had fallen 23 percent to $46 per barrel by the end of December. (4/5)

SPR debate: US Congress should debate whether to reduce the emergency crude oil stored in the Strategic Petroleum Reserve (SPR) because America’s oil production boom has diminished its reliance on imports, US Secretary of Energy Perry said at a Senate hearing on Tuesday. The Strategic Petroleum Reserve is a US Government complex of four sites with deep underground storage caverns created in salt domes along the Texas and Louisiana Gulf Coasts. As of March 29, 2019, the SPR held a total of 649.1 million barrels of crude oil. (4/4)

Keystone pipeline…again: President Trump on Friday signed a new permission for TransCanada Corp to build the long-delayed Keystone pipeline for imports of Canadian oil, replacing his previous permits in a fresh attempt to get around the blocking of the $8 billion project by a court in Montana. (4/6)

In Colorado, new legislation changing regulation of the oil and gas industry is arguably much weaker than a public referendum from last year that would have imposed state-wide setback distances. The law in question only grants localities the ability to set their own, rather than state-wide setbacks. Moreover, there will be a lengthy rulemaking process, so any fallout for the industry won’t be immediate. Some localities in favor of drilling may not impose limits at all…While Wall Street has grown more skeptical of the shale industry in general, Colorado-focused drillers have been particularly hit. (4/5)

CA’s oil off-ramp: The shale revolution that has transformed the US oil and gas industry has completely passed California by. Not that long ago, California was the second most important US oil-producing state. Since peaking in 1985, however, output has plunged almost 60 percent to 460,000 b/d. This collapse is made even more discouraging by the fact that total US crude oil production has been soaring to record heights. The inevitable result of plummeting production amid high consumption is that California is forced to import 70 percent of the oil that it needs. With the collapse of Alaska’s production, foreign sources now supply almost 60 percent of California’s crude oil, compared to just 15 percent 20 years ago. (4/4)

In Ohio, Royal Dutch Shell is on track to revitalize the Rust Belt by building the first major factory in the region since 1992. The massive polyethylene plastics plant being constructed along the Ohio River 30 miles outside of Pittsburgh will cover a whopping 386 acres. The estimated price tag of $6 to $10 billion (with a $1.6 billion package in reduced taxes over 25 years granted to Shell by the state of Pennsylvania) makes the factory one of the most significant industrial projects ever developed in the area. (4/3)

California is escalating its battle with the Trump administration over cars and climate change, filing suit Friday to demand that two federal agencies release data they used to justify a rollback of auto emissions standards. The lawsuit by the state Air Resources Board says the Trump administration failed to show it met requirements to take meaningful input from state officials while it crafted a new proposal to ease emissions standards. (4/6)

MPG vs. vehicle type: Does the higher occupancy of SUVs compensate for their higher energy consumption per vehicle distance when considering energy consumption per occupant distance? Barely. The results from a recent study are shown in the table below (4/3):

EVs in NC: Duke Energy is proposing a $76-million initiative to spur EV adoption across the state of North Carolina—the largest investment in electric vehicle infrastructure yet in the southeastern US. In a filing with the North Carolina Utilities Commission, Duke Energy outlined its program that will provide incentives to customers. It will also lead to a statewide network of fast-charging stations to meet growing demand.

US weekly coal production was estimated to be 10.5 million tons for the week ended March 30, down 6.6 percent from the previous week and down 26.3 percent from the year-ago week, US EIA data showed Thursday. This was the fifth week in a row of decreases from the year-ago week. (4/5)

German coal shutdown: President Frank-Walter Steinmeier received on Wednesday the symbolic ‘last piece of black coal,’ marking the end of Germany’s two centuries of hard black coal production, while the country struggles to keep up with European peers in curbing emissions. Germany closed its last black coal mine in December 2018. In January this year, Germany became the latest important European economy to lay out a plan to phase out coal-fired power generation. (4/4)

Nuclear power appeals as being a source of reliable electricity without causing greenhouse gas emissions. But new reactors are so expensive that in many countries they are unable to compete with cheap gas and coal or renewable energy sources. If new nuclear plants are to play any significant role in curbing future emissions in developed economies, their costs are going to have to come down a long way. That is the argument underlying the recent upsurge in interest in new nuclear technologies, including small modular reactors (SMRs). (4/5)

The rapidly dropping cost of renewable energy has upended energy economics in recent years, with new solar and wind plants now significantly cheaper than coal power. But new research shows another significant change is afoot: The cost of batteries has been declining so rapidly that renewables plus battery storage are now cheaper than even natural gas plants in many applications, according to a new report by Bloomberg New Energy Finance. BNEF reports that electricity prices for onshore wind, solar PV and offshore wind have fallen by 49 percent, 84 percent, and 56 percent respectively since 2010. Costs for lithium-ion battery storage have dropped 76 percent since 2012 — and plunged 35 percent in the past year. (4/5)

Nuke $ overrun news: The flagship of the Trump administration’s advanced nuclear power research program could cost about 40 percent more than a government official estimated earlier this year, a US Department of Energy document shows. Energy Secretary Rick Perry has tried to breathe life into the country’s nuclear power industry, which is suffering in the face of competition from plants burning cheap natural gas as well as falling costs for wind and solar power. Perry announced the versatile test reactor, or VTR, in late February, saying it was a “key step to implementing President Trump’s direction to revitalize and expand the US nuclear industry,” and critical for national security. (4/5)

RE & batteries: Billionaires are spending more on renewable energy, storage, and battery technology. A group of them even set up a $1-billion fund, Breakthrough Energy Ventures, to encourage research in these areas, aiming “to make sure that everyone on the planet can enjoy a good standard of living, including basic electricity, healthy food, comfortable buildings, and convenient transportation, without contributing to climate change.” One big reason for this is that there is more technology to invest in. (4/2)

Corn production: A new study finds that environmental damage caused by corn production results in 4,300 premature deaths annually in the United States, representing a monetized cost of $39 billion. The paper, published in Nature Sustainability, presents how researchers have estimated for the first time the health damages caused by corn production using detailed information on pollution emissions, pollution transport by wind, and human exposure to increased air pollution levels. (4/2)

India’s polluted air: According to an independent study by the International Institute for Applied Systems Analysis (IIASA) and the Council on Energy, Environment, and Water (CEEW), more than 674 million Indian citizens are likely to breathe air with high concentrations of PM 2.5 in 2030 even if India were to comply with its existing pollution control policies and regulations. (4/1)

In Germany, a top Volkswagen group executive said that the group alone is responsible for around 2 percent of global carbon emissions, about the same amount that Germany emits. It’s almost one percent for cars and one percent for trucks. Germany, in comparison, accounts for nearly 2.2 percent of C02 emissions. (4/4)

British Columbia-based Carbon Engineering has shown that it can extract CO2 cost-effectively. It has now been boosted by $68 million in new investment from Chevron, Occidental and coal giant BHP. But climate campaigners are worried that the technology will be used to extract even more oil. (4/4)

Canada is warming twice as fast as the rest of the world, a landmark government report has found, warning that drastic action is the only way to avoid catastrophic outcomes. The report, released late on Monday by Environment and Climate Change Canada, paints a grim picture of Canada’s future, in which deadly heatwaves and heavy rainstorms become a common occurrence. (4/3)

Peak Oil Review 1 April 2019

By Tom Whipple, Steve Andrews, originally published by Peak-Oil.org

April 1, 2019

https://www.resilience.org/stories/2019-04-01/peak-oil-review-1-april-2019/

Quote of the Week

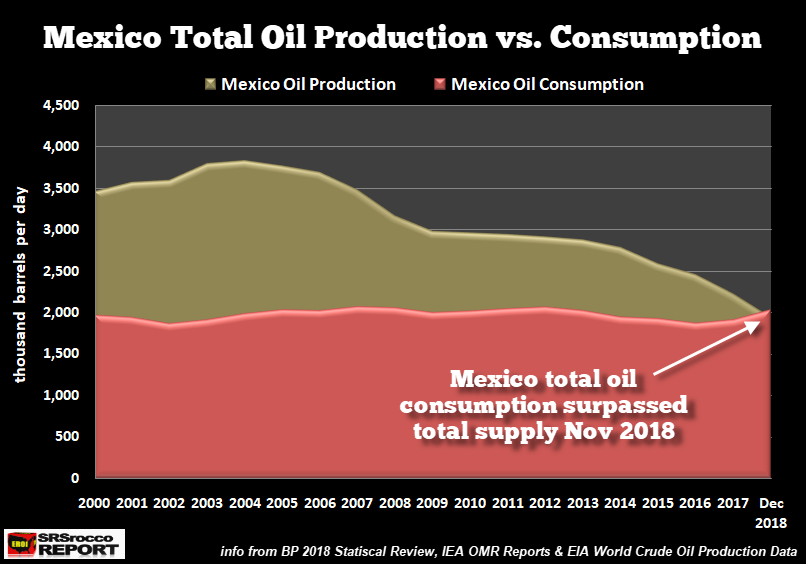

“In just a little more than a year, Mexico’s net oil exports fell from 314,000 barrels per day to net imports of 90,000 barrels per day in December 2018…I find it strange that this has not yet been mentioned in the news as it is a very critical factor for the future of Mexico.” Steve St. Angelo, oil industry commentator

Graphic of the Week

World demand growth for key materials vs. GDP and population growth

1. Oil and the Global Economy

Prices have climbed steadily for the last three months closing on Friday above $60 a barrel in New York and $67 in London. The combination of slowing US shale oil drilling and the Venezuela, Iran, and the OPEC+ situations continue to outweigh the bad economic news that may someday lower demand. The situation in Venezuela gets worse every day, and it seems likely that the country will see a significant drop in production and exports during March.

On Friday, the EIA reported that the average daily US crude production slipped during January for the first time in nearly six months falling to 11.871 million b/d from 11.961 in December. This number is likely to be more accurate than the weekly estimates that are based more on trends than actual production numbers. Given the severe weather across North Dakota during the last two months, it seems unlikely there will be an increase in Bakken production until spring.

The US oil rig count continues to slide, falling from 885 on January 1st to 816 last week. This situation suggests that we may not see another 1.8 million b/d gain in shale oil production like happened in 2018 despite all the hype about the smarter and wealthier international oil companies taking over the Permian Basin from smaller, less efficient, drillers.

U.S. and Brent crude oil futures touched a new high for the year this week. While the price increase is underpinned by the fundamentals of the oil market, optimism is increasing that a settlement of the US-China trade dispute is in the offing and that the prospects for a recession later this year are receding.

It should be noted, however, that along with higher crude prices, US gasoline prices have been increasing at a steady pace – up 28 cents a gallon in the last month. Prices on the US West Coast are already over $3 a gallon and Michigan, Illinois and Pennsylvania are in the vicinity of $2.80. While nobody is forecasting a return to $4 a gallon gasoline in the US in the immediate future, California is already at $3.61 for regular and is approaching the point where discretionary driving starts to slow.

The OPEC Production Cut: Saudi Arabia is having a hard time convincing Russia to stay much longer in an OPEC+ pact cutting oil supply, and Moscow may agree only to a three-month extension. Russian Energy Minister Novak told the Saudis last month that he is under pressure to end the cuts but would agree to extend the cuts to the end of September. Moscow has always been skeptical of the cuts, given that the collapse of Venezuela amounts to nearly the same thing without harming the major oil exporters. Last November, Russia agreed to go along with the deal but warned that it would not be able to cut 50,000-60,000 b/d until spring. This situation left the Saudis and the other Gulf Arabs to shoulder the bulk of the cut.

In the meantime, President Trump, worried about the price of gasoline during next year’s presidential election, is calling for higher OPEC production.

US Shale Oil Production: The International Energy Agency recently forecast that a “second” shale revolution was on the horizon. The next wave would drive US oil output to “19.6 million b/d by 2024 up from 15.5 million b/d in 2018,” and higher crude exports are expected. The forecast was published just before the CERA Week 2019 conference last month and caused “ecstatic dialogues about the viability and future direction of the industry. US production is expected to account for 70% of the total increase in global output capacity by 2024, while total exports of crude and refined products should reach 9 million bpd, surpassing rivals Russia and Saudi Arabia.

The Agency probably made this optimistic forecast based on the growth of US shale oil production in recent years without giving much concern to recent developments or the economics of shale oil. There is increasing evidence that the financers of the 10-year-old shale oil boom are becoming tired of the billions of dollars that they have lost as for most producers it still costs more to find and extract shale oil than the product selling price. Although there have been “efficiencies” in producing shale oil in recent years, a large number of drillers are still losing money even with oil now selling for $60 a barrel.

The next issue is whether there is enough oil left to extract at affordable prices. This issue seems to be focusing on the Permian Basin as the other shale basins have not been growing rapidly in the last two years despite all sorts of expensive “new technology” and procedures being applied. As some of these are rather new ways of extracting oil, we will not know for a couple of years whether they increase the amount of oil ultimately recovered from a given well or just extract it faster. Some geologists who have looked closely at the Permian doubt that the large amount of oil that the Geologic Survey says can be found in the basin will ever be produced economically.

The last issue is the growing presence of the international oil companies in the Permian Basin. These companies have very large cash flows and can even afford to produce shale oil from the Permian at a loss provided they can make up the difference between the well and the retail gas pump. If there is oil that can be produced economically in the Permian Basin even by the international oil company standards, then production there might be able to grow. If the affordable oil is not there, then there may not be much of a “second” shale oil revolution in the immediate future.

Last week two South Korean refiners canceled the delivery of U.S crude oil cargoes saying they were concerned about the quality of the crude. There is a massive pipeline network carrying crude oil from US shale oil fields to the Gulf Coast ports. While passing through many pipelines, oil can get contaminated with oil residue, heavy metals, pipe cleaning agents, and a group of compounds called oxygenates. The latter can be especially troublesome to refiners. If contamination of US shale oil proves to be endemic, we could see demand drop.

2. The Middle East & North Africa

Iran: Renewal of the US sanctions waivers which affect Iranian sales to India, China, South Korea, Taiwan, and Japan is the subject of much debate in Washington. The National Security Council staff does not want to extend the waivers, while the State Department believes such an action would do more harm than good. Iran’s exports seem to be down by about a million b/d since before the sanctions were announced and some believe that as much as another million b/d could be cut from Tehran’s exports if its major customers stop all imports. Japanese refineries have already halted imports of Iranian oil after buying 15.3 million barrels between January and March in anticipation that the US sanction waiver will not be renewed.

Over the years, Iran has become expert in evading US sanctions though what Washington describes as a vast network operating in Turkey and the UAE which helps the Iranians to continue exporting oil and receiving payments. Among the techniques Tehran uses is transferring oil at sea from Iranian tankers to those of foreign registration and issuing forged export certificates attesting that the cargoes originated in Iraq.

Torrential rains have plagued Iran in the last few weeks with 26 of 31 provinces issuing flood threats. Particularly hard hit was Khuzestan Province which produces some 70 percent of Iran’s oil and almost all of its natural gas.

The loss of revenue from the sanctions is starting to have an impact on Iran’s foreign policy. Projects Iran promised to help Syria’s ailing economy have been postponed. The Trump administration says the strains show that the sanctions are effective. However, other observers doubt constrained oil sales will ever have much effect on passions loose in the Middle East.

Iraq: Iraq’s total oil production fell by about 70,000 b/d in February as the government began cutting output to comply with the OPEC+ agreement. The federal government and the KRG together produced some 4.83 million b/d, down from an estimated 4.90 million b/d in January.

Security forces at the Alaas field in northern Iraq have thwarted an attack by Islamic State militants, killing and injuring several attackers. This attack is the latest by the terrorist group on the same oil field after it was driven out of the area in 2017. While Baghdad celebrated the defeat of Islamic State after the battle for Mosul, some military experts warned that not all militants were destroyed in the push and that the group will sooner or later resurface.

Saudi Arabia: An underfunded budget is forcing the Saudis to push for oil prices of at least $70 per barrel this year, even though US shale oil producers could benefit, and Riyadh’s share of global crude markets might be further eroded. Riyadh cut exports to its primary customers in March and April despite refiners asking for more of its oil. The move defies President Trump’s demands that OPEC help to reduce prices while he toughens sanctions on oil producers Iran and Venezuela.

The long-awaited Saudi Aramco acquisition of Saudi Basic Industries Corporation (SABIC) took place last week. Aramco has acquired a 70 percent stake in SABIC, with an estimated value of $69.1 billion. The deal would join Saudi Arabia’s two largest companies and give the Saudi sovereign-wealth fund, SABIC’s current owner, roughly the same amount of money it had expected from an initial public offering for Aramco. This money will supply part of the capital that Prince Mohammed needs to diversify the Saudi economy. Saudi Aramco plans to issue a $10 billion bond this week start the funding of the SABIC purchase. The bond would be the first-ever debt issuance by the Saudi Arabian Oil Co.

US Energy Secretary Perry has approved six secret authorizations by companies to sell nuclear power technology and assistance to Saudi Arabia. The Trump administration has quietly pursued a deal to sharing US nuclear power technology with the Saudis, who plan to build at least two nuclear power plants. Several countries including the United States, South Korea, and Russia are competing for that deal, and the winners are expected to be announced later this year.

Libya: Oil workers at Sharara oilfield, which recently re-opened after a three-month occupation by militant workers, have demanded a salary increase of 67 percent as they try to return oil production at the field to its normal 315,000 b/d production.

3. China

Profits at large Chinese industrial companies fell at the fastest pace in almost a decade in the first two months of 2019 in the latest sign of a slowdown for the Chinese economy. Industrial profits fell 14 percent year-on-year, figures from the National Bureau of Statistics showed, the largest drop recorded since May 2009. Earnings in the auto industry tumbled 42 percent year-on-year for January and February.

Uncertainty caused by the US-China trade war, as well as a government crackdown on China’s high levels of corporate debt, led the country’s economic growth to fall to its slowest annual rate in almost three decades in 2018. The fall in industrial profits comes despite a series of fiscal and monetary stimulus measures put in place since July to shore up growth. The possibility that China’s economy is headed for a steep downturn is a significant factor in keeping a lid on oil prices.

China’s largest state-run oil majors, China Petroleum & Chemical (SINOPEC), China National Petroleum Corporation (CNPC), and China National Offshore Oil Corporation (CNOOC) have announced plans to spend billions in the next few years to increase oil output. Many observers are saying this effort will be a massive waste of money as China has few opportunities to open new oil fields and that increases in capital expenditures attempting to rejuvenate aging oil fields is unlikely to pay off.