News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

cjgaddy

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Honestabe13, so you know, only 'ADMIN' (not Mods) can Ban a poster.

AZN publishes their Partnering Brochure each MAY. Why do you think it wouldn't be easy for them to change it (ie, remove Peregrine) when they updated & issued the new Brochure PDF for 5-2017?

5-2017: AZN’s 5-2017 “Partnering For Scientific Leadership” Brochure

https://www.astrazeneca.com/content/dam/az/PDF/2017/2017_18_AZ_BD%20&%20Partnering%20Brochure_FINAL.pdf

MORE: https://www.astrazeneca.com/our-focus-areas/oncology.html

Large Ownership now ~13.9mm shares, 31.0% of 45mm O/S. (Ronin/SW, E.Cap/Dart, Institutions)

7-14-17/13D: Group Ronin Trading/SWInvest (John Stafford III+Stephen White) acquires 8.8% stake (3,952,446sh.) in PPHM http://tinyurl.com/y7ezqvm9

...3,801,139 COMMON - 8.4% of 45,069,188 common O/S at 7-10-17 (total beneficial=3,952,446 if Pref. conv. x1.19 to Common, 8.8%)

...127,099 PREFERRED – 7.7% of 1,647,760 preferred O/S at 1-31-17

......As a Group, ie, “people that share the furtherance of a common objective/concerted action”; 13D’s are reserved for ACTIVE INVESTORS who may be “interested in agitating for some kind of a change at the company”.

...7-13-17: Ronin/SW-Invest Letter to Stockholders; PPHM Comments http://tinyurl.com/ybr8ycbp - Ronin nominates Gregory Sargen, Brian Scanlan, Saiid Zarrabian for election to PPHM's board at next ASM ~10-12-17.

- - - - - - - - - - -

10-30-15: Kenneth Dart (Eastern Capital) acquires 9.6% stake (4,300,992sh.) in PPHM http://tinyurl.com/y95yskck

...3,777,183 COMMON - 8.4% of 45,069,188 common O/S at 7-10-17 (total beneficial=4,300,992 if Pref. conv. x1.19 to Common, 9.6%)

...440,000 PREFERRED - 26.7% of 1,647,760 preferred O/S at 1-31-17

- - - - - - - - - - - - - - -

Plus, INSTITUTIONS a/o 3-31-17: 5,690,888sh. = 12.6% (of 45mm) http://www.nasdaq.com/symbol/pphm/institutional-holdings

TOP5:

Kennedy Capital Mgt. 1,247,224 +164,952

Tappan Street Partners 914,304 +914,304

Vanguard Group 882,964 +267,438

Blackrock (Larry Fink, CEO) 855,455 +177,856

Renaissance Technologies 439,673 +6,259

AZN lists the AZN-PPHM "Partnership" on their 5-2017 brochure. So, is AZN "unbelievable" too, Peregr?

5-2017: AZN’s 5-2017 “Partnering For Scientific Leadership” Brochure

https://www.astrazeneca.com/content/dam/az/PDF/2017/2017_18_AZ_BD%20&%20Partnering%20Brochure_FINAL.pdf

MORE: https://www.astrazeneca.com/our-focus-areas/oncology.html

PPHM’s 10K Notes re: Avid FY18 & Beyond (FY18 Guidance announced 7-14-17: $50-55mm - http://tinyurl.com/yb4wulvu )

From 4-30-17 10K iss. 7-14-17 - http://tinyurl.com/ycxu4l5n

Pg.2: “With respect to our CDMO business, FY17 was a record year for revenues, topping $57mm, a 30% revenue growth over FY16 FY. While we are pleased at the continued yr-over-yr revenue growth, we have also recently seen unanticipated decreases in mfg. demand from our largest customer [Halozyme] and a recent regulatory filing delay from our 2nd largest customer which will have some impact on our ability to grow the revenues from our CDMO business in FY18 and could impact our ability to achieve overall profitability by q/e July 31, 2018. However, we believe this to be temporary delay in revenue growth during FY18 and have recently secured 4 new customers and are continuing to focus on securing addl. customer business in order to better diversify our customer base. Our goal is to maintain profitability for Avid over the short term while positioning the business for long-term growth and attracting the resources necessary to continue to advance our promising research and development efforts.”

Pg.3: “FY18 Key Objectives - Our CDMO Business

* Expand our mfg. capacity through the installation & validation of two 2,000L single-use bioreactors in our Myford Facility to support the anticipated needs of a current customer

* Continue to diversify our customer base by securing addl. customers to support our future revenue growth beyond FY18.”

Pg.31: “We have been developing and mfg. biologics since 1993 in our Franklin biomfg. facility (the “Franklin Facility”) located at our current headquarters in Tustin and formed Avid in 2002 to offer these services to 3rd-party customers using. In March 2016, we expanded our mfg. capacity through the launch of our Myford biomfg. facility (“Myford Facility”), which doubled our mfg. capacity. The 42,000sf facility, which is our 2nd biomfg. facility, can accommodate single-use bioreactors up to the 2,000-liter mfg. scale. The Myford Facility was designed to accommodate a fully disposable biomfg. process for products in late stage clinical dev. to commercial. To date, Myford Facility has been utilized to complete a number of process validation runs for our 3rd-party customers, which may lead to future commercial production, and has supported the process validation of our internal product, bavituximab. The Myford Facility is located adjacent to our Franklin Facility. As we look to expand our CDMO business, in Feb. 2017, we leased an addl. 42,000sf of vacant warehouse space within the same building as our existing Myford Facility. The proximity of this space will allow us to utilize existing mfg. infrastructure that we believe should enhance our mfg. efficiencies and reduce the overall cost and timeframe to construct a 3rd biomfg. facility. Although we previously anticipated that the new mfg. facility would be constructed and ready for mfg. activities by mid-calendar year 2018, due to unanticipated changes in and/or timing of customer demand (as discussed above), we have decided to defer construction of this 3rd facility until demand from existing or potential new customers is expected to exceed the current mfg. capacity at our Franklin Facility & Myford Facility. Additionally, commencement of construction is also subject to our ability to raise sufficient addl. capital to support this expansion effort. As a result, we presently do not expect to commence construction of this 3rd facility prior to April 30, 2018.”

Pg33: “Excluding any future potential new business, we expect Avid revs for FY18 to slightly decline vs. FY17. Part of this decline is due to lower anticipated commitments from Halozyme (our largest customer) based on their most recent committed forecast (covering the 3 qtrs ending March 2018), which amount is expected to be partially offset by $10mm revenue that was expected to be recognized in FY17, but has been shifted to FY18 due to a delay in shipping product that was complete and ready for shipment as of fye 4-30-17.”

= = = = = = = = = = = = = = = = = = = = = = =

AVID BIOSERVICES, Inc. (Peregrine's Mfg. Subsidiary): http://www.avidbio.com

7-14-17: PPHM's Revs & Burns By Qtr Table, FY'07/Q1 thru FY'17/Q4 (q/e 4-30-17): http://tinyurl.com/yb4wulvu (since 5-2006: Avid=$231.2mm, Total=$257.8mm, incl.Govt)

......Avid FY18 (fye 4-30-18) revs guidance: $50-55mm; committed backlog=$58mm. Recently Leased +42,000sf in same bldg. as MYFORD for future expansion."

7-14-17: Avid Scientists develop “Antibody Discovery & Characterization Platform” http://tinyurl.com/ycr3erft

...S.King: “through which we can generate antibodies against virtually any target. These capabilities are state-of-the-art and meant for rapid screening for high affinity antibodies as drug candidates.”

5-2017: Avid II (Myford) adds 2 MilliporeSigma Mobius 2,000L single-use bioreactors; total mfg. capacity now ">11,000L". http://tinyurl.com/ky7bmu4

5-10-17: Halozyme comments on Avid II(Myford) expansion in their 3-31-17/10Q pub. 5-9-17: http://tinyurl.com/mrl34uk

..."validation of the new facility is scheduled to end in Q2/2017… Once this new facility is approved, it will become the primary source for Roche of bulk rHuPH20.”

NCI Scientist Speaking “PS” 10-2-17 at AACR/Immunotherapy Conf. in WashDC. Traces back to same author’s 6-1-17 Mol.Cell article with basically the same name. Interesting: Both the Lead+Senior authors (NCI) list MSKCC in their work declarations.

Oct1-4 2017: “AACR’s Tumor Immunology & Immunotherapy Conf.”, Boston

http://www.aacr.org/Meetings/Pages/MeetingDetail.aspx?EventItemID=122

Pgm: http://www.aacr.org/Meetings/Pages/MeetingDetail.aspx?EventItemID=122&DetailItemID=651

10-2-17 3:45-5:30pm: Plenary Session 4: A Systems Approach to Immuno-Oncology

“Long-Lived Disruption of Inflammation Stems from the Catch-and-Release of Cytokines Mediated by Surface Phosphatidylserine in Tumors”, Gregoire Altan-Bonnet, NCI, Bethesda

G. Altan-Bonnet profile: https://ccr.cancer.gov/Cancer-and-Inflammation-Program/gr%C3%A9goire-altan-bonnet

- - - - -

Related Pub. 6-1-17/MolCell: “Catch & Release of Cytokines Mediated by Tumor Phosphatidylserine Converts Transient Exposure into Long-Lived Inflammation”, Senior Author: Gregoire Altan-Bonnet **

https://www.ncbi.nlm.nih.gov/pubmed/28575659

NCI Followup PR: “Cancer cells with more PS on their surfaces could be more vulnerable to these treatments because they will maintain high IFNy levels in the surrounding tissue.”

https://ccr.cancer.gov/news/article/catch-and-release-a-weak-point-on-cancer-cells

**INTERESTING: Memorial Sloan Kettering CC (MSKCC) is listed in the author-info. section for both Dr. G.Altan-Bonnet and the lead author, J. Oyler-Yaniv.

COMPLETED BAVI PH.1/2 TRIALS ARCHIVED From iBox 7-16-17

Now linked to from within iBox for perpetuity: http://investorshub.advfn.com/boards/show_ibox.aspx?boardid=2076

BAVITUXIMAB SOLID CANCERS PHASE1+2 TRIALS:

==> PR=Partial-Resp(30-99% Red.), SD=Stable-Disease(29% Red.-19% Incr.), OR=Obj-Resp(PR+CR)

6-2012: FTM's charts of MOS Data from CtlArms(chemo) of Comp.Trials for 1NSCLC 2NSCLC PANCRE trials http://tinyurl.com/757plm7

11-25-11: Comp. of Bavi+Chemo vs. Avastin & Chemo-Only in 3 completed Ph.2 single-arm trials (ABC/2 & NSCLC): http://tinyurl.com/79b3jcj

O. 6th IST Trial: Bavi+Ipilimumab(Yervoy) vs. Adv.Melanoma (Ph1b, random, open-label, 2arms, n=24)

Protocol (UTSW): http://www.clinicaltrials.gov/ct2/show/NCT01984255 (PI: Dr. Arthur Frankel - see "Researching for Cures" http://youtu.be/0zLAxjFny5Q )

UTSW's listing: http://www.utsouthwestern.edu/research/fact/detail.html?studyid=STU%20102013-007

…Note: Ipilimumab = BMS’s “Yervoy” (anti-CTLA-4) http://www.yervoy.com

...12-10-15: “Due to newly-appr. therapies & chgs in SOC [ex: Keytruda/Opdivo: less-side-effects], enrollment recently stopped by UTSW.” http://tinyurl.com/jkp885g

...4-23-14: Bavi+Yervoy IST trial initiated: http://tinyurl.com/km7krcm ;

N. 5th IST Trial (Bavi+Capecitabine+RAD) vs. Rectal Cancer (Ph1, open-label, 1arm, n=18)

Protocol: http://www.clinicaltrials.gov/ct2/show/NCT01634685

...Note: Capecitabine (prodrug of 5-FU) = Roche/Genentech's Xeloda - see http://www.xeloda.com

...11-1-15/RadiationOncology – prelim. results/8 evaluables http://tinyurl.com/q3wey2b

…...”Of the 7 pts that proceeded to surgery, 1 demonstrated a pathologic complete response.”

...7-16-12: IST (Rectal) initiated at UTSW (PI=Jeffrey Meyer), ~18 patients - http://tinyurl.com/cr29l6k

M. Tumor Imaging & Dosimetry trial of I124-PGN650 (FH-Bavi) in Adv. Solid Tumors (Ph0, open-label, 1arm, n=12)

Protocol: http://clinicaltrials.gov/ct2/show/NCT01632696

..."I124-PGN650 is the Fab end of PS-targeting mab PGN635 (FH-Bavi) joined to the PET imaging radioisotope iodine-124, a new approach to imaging cancer."

5-1-15: Interim Results/8pts (Jrnl Nuclear Med, vol56 suppl#3) http://jnm.snmjournals.org/content/56/supplement_3/1033

…”124I-PGN650 is safe and results in acceptable dosimetry and needs further optimization as an imaging agent based on the level of increased tumor uptake on PET/CT”

...6-28-12: Trial added to Trials.gov, 1st site "recruiting" (Wash.UnivSM/St.Louis)

…4-3-12: Peregrine Launches PS-Targeting Clinical Imaging Pgm (AACR'12 #2452) http://tinyurl.com/7p7jovt & http://tinyurl.com/7yrwqm7

L. 4th IST Trial (Bavi+Cabazitaxel vs. 2nd-Line PROSTATE(CRPC) Cancer, open-label Ph.1B/IIA) *CANCELLED due to chg. in SOC Drugs*

Protocol: http://clinicaltrials.gov/show/NCT01335204 (CRPC=Castration-Resistant Prostate Cancer)

...Note: Cabazitaxel = Sanofi-Aventis' Jevtana - see http://www.jevtana.com

...3-12-13: CRPC IST cancelled (Slow-Enroll/2 New SOC Drugs): http://tinyurl.com/c48osut

...5-25-11: IST (Prostate) initiated at UCI -> moved ot Med.Univ.SCar (PI: Michael Lilly), ~31 patients - http://tinyurl.com/3mtvdvl

K. 3rd IST Trial (Bavi+PemCarbo vs. Frontline NSCLC, open-label Ph.1B, n=25)

Protocol: http://clinicaltrials.gov/ct2/show/NCT01323062

…10-30-14: Interim data n=23, MSTO’14: MOS=12.2mos (hist-ctl ~10mos), PFS=4.8mos, ORR=35% http://tinyurl.com/mll62c6

...9-9-14: Stage IV NSCLC IST Enrollment complete. http://tinyurl.com/ktrfswj

...4-2012: Clinicaltrials.gov shows 2nd site added: Univ. of Pittsburg (PI=Liza Villaruz, MD)

...4-2-12 AACR'12: "5pts. to-date, 3 have PR's" http://tinyurl.com/7yrwqm7 (see #1744)

...3-8-11: IST (NSCLC) initiated at UNC (PI= J.Grilley-Olson), ~25 patients - http://tinyurl.com/6b926ku

J. 2nd IST Trial (Bavi+Paclitaxel(Taxol) vs. Her2- Met. Breast Cancer, open-label Ph.1, n=14)

Protocol: http://clinicaltrials.gov/ct2/show/NCT01288261

...3-31-15/A.Stopeck article(Ph1 data) “Cancer-Medicine” N=13: PFS=7.3mos, ORR=85%, 2 CR's http://tinyurl.com/nm5oog4

…6-3-13: ASCO’13/interim data, n=14: ORR=85%, 2 CR’s (15%) http://tinyurl.com/kq3uv4e

...4-29-13: Enrollment complete. http://tinyurl.com/cqrup9e

...4-3-12 AACR'12: "5pts. to-date, 2 CR's, 1 PR" http://tinyurl.com/7yrwqm7 (see #4404)

...1-19-11: IST (Her2- MBC) initiated at Arizona CC (PI=A.Stopeck), ~14 patients - http://tinyurl.com/5t7zomn

I. Phase II Bavi+GEM vs. Front-Line Adv. PANCREATIC (randomized, unblinded, n=70)

Protocol: http://www.clinicaltrials.gov/ct2/show/NCT01272791 (15 U.S. + 4 Ukraine = 19 as of 6-7-2012)

…1-22-13: FTM's post of 13 Ph3 Gem+Treatment Pancreatic Trials ('02-'13) - Mean MOS: GEM=6.4mos., GEM+TR=7.3mos. http://tinyurl.com/al99hx9

......Another FTM Pancreatic Phase3 trials table showing HR's, P-Values, and ORR% stats: http://tinyurl.com/btzkw4l

…6-3-13 ASCO’13/final data: n=70, Ctl=>Bavi MOS 5.2=>5.6mos, ORR 13%=>28% HR=.75 http://tinyurl.com/kq3uv4e

......Promising ‘immuno-indicative’ 1yr SURVIVAL results: GEM-Only(n=31): 0%, Bavi+GEM(n=32): 24.5% - see: http://tinyurl.com/lz5yg4f

...2-13-13 Topline Data: “Bavi+Gem resulted in more than a doubling of ORR” http://tinyurl.com/aqny7ny

...6-25-12: Enrollment complete. http://tinyurl.com/72tvnfj

...6-20-12: Early data (cutoff=6/6/12 bavi=15 ctl=17) presented at AACR Pancreatic Conf. http://tinyurl.com/77m9fw2

...1-5-11: U.S. Ph.2 randomized trial initiated http://tinyurl.com/26hnuzv "up to 70 front-line patients at ~10 clinical sites."

H. 1st Investigator-Sponsored (IST) Ph.I/II Trial (Bavi+Sorafenib vs. Liver Cancer/HCC, open-label, n=9+38=47)

...Note: Sorafenib = Onyx/Bayer's Nexavar - see http://www.nexavar.com

Protocol: http://clinicaltrials.gov/ct2/show/NCT01264705 UTSW: http://tinyurl.com/mwdc2ql (5 sites: 3/UTSW, Parkland-Hosp, Dallas/VA, PI=Dr. Adam Yopp)

...3-25-15: Dr.Adam.Yopp(UTSW) Oral-pres./SSO (Liver-IST/Ph2-data) http://tinyurl.com/opkh5qy N=38(79%HepC, ECOG/0=34%): MTTP=6.7mos, MOS=6.1, MDSS=8.7, DCR=58%

...1-16-15 ASCO Gastro-Symposium: Ph.2 data/n=38 (Adam Yopp), “These clinical outcomes of TTP=6.7/DCR=58%/PFS=4mo are quite encouraging…” http://tinyurl.com/m9uz9mo

...11-8-14 SITC'14: Ph.2 Correlative Studies data (biopsies B4/After) on 6pts, incl. KOL Dimitry Gabrilovich’s comments: http://tinyurl.com/pchzr6h

...9-9-14 Enrollment complete. http://tinyurl.com/ktrfswj (ph2=38 Ph1=9)

...4-4-12 AACR'12: Dr. Adam Yopp, "promising safety profile to-date" http://tinyurl.com/7yrwqm7 (see #5591)

...Feb'12-Sep'14 10+ times: CEO Steve King hints of future ex-US partner-driven Bavi+Sorafenib/LIVER trial in Asia-Pacific: http://tinyurl.com/nkaxtcc

......Articles & Data describe Liver Cancer challenges in Asian populations: http://tinyurl.com/7z7o8j9 & http://tinyurl.com/7z99cy4

...12-1-10: PPHM's 1st IST (Liver Cancer) initiated at UTSW, ~56 patients - http://tinyurl.com/3xd3e6c

…Per S.King, 5-18-10/R&R, "We've had a lot of interest in running clinical trials with the compound from investigators who have either had prior experience with the drug or would like to study the drug in various settings. Potential IST indications include all the major solid tumor types. Of particular interest is Liver Cancer, in which we have a natural tie-in with our HCV program, Ovarian Cancer & Pancreatic Cancer, also very nicely supported by the prior data."

G. Phase IIb Bavi+PC vs. Front-Line NSCLC (randomized, unblinded, 'confirmatory', n=86)

Protocol: http://clinicaltrials.gov/ct2/show/NCT01160601 (17 U.S. + 9 India + 2 RepGA + 7 RussianFED + 5 Ukraine = 40 as of 8-12-11)

...Also listed in: India's CTRI registry http://tinyurl.com/ljg7aad and WHO's registry http://tinyurl.com/kcp4z89

...6-27-13: Bavi+CP MOS>14mos (“with < 60% of survival events”) http://tinyurl.com/pmcgsgp

…”with less than 60% of survival events, while the Bavi+CP arm currently demonstrates a MOS > 14mos, there was not a meaningful enough diff. in survival between the 2 arms that would support the advancement of this combination. Full results will be presented at a future sci. meeting or thru pub.”

...5-7-13: FTM's Table of 20 prev. Ph.3 Trials in 1st-Line NSCLC (ctl=CP), MOS & HR results (Note Avastin improved CP-Only by 19%): http://tinyurl.com/cho7o29

...3-9-12: Topline ORR & PFS Data (Bavi+PC vs.PC-only) http://tinyurl.com/7m9r6ya

…...LOCAL reads: ORR/32%-31% PFS/5.8-4.6mos , CENTRAL reads: ORR/25%-23% PFS/6.7-6.4mos

...12-6-11 Prelim. Data (n=86, 100% Stage IV's) => ORR=39%, PC/alone=25%: http://tinyurl.com/7ph4tty

......Comp. vs. Avastin+PC/Ph3/n=417(74% Stage IV's): ORR=35% (Sandler/E4599/2006 http://www.nejm.org/doi/pdf/10.1056/NEJMoa061884 )

...9-8-11: Enrollment complete. http://tinyurl.com/3vv9zfx

...7-14-11/CC: Enrollment was taking longer than expected; have amended protocol; expanding to 30+ sites, expect enroll. comp. "in coming weeks", interim data by Yr-end'11. http://tinyurl.com/6k6y2as

…7-14-10/CC, J.Shan (VP/Clin+RegAffairs): "This trial is intended to confirm in a randomized setting the results from our Ph.2 signal-seeking NSCLC trial which showed 43% ORR, more than double the generally accepted chemo ORR of under 20% in numerous publications. Favorable results could then lead to an end of Ph.2 meeting with the FDA, with possibly a pivotal Ph/3 trial for front-line lung cancer, our 2nd potential regulatory pathway for bavituximab."

...7-14-10: U.S. Ph.2b randomized trial initiated http://tinyurl.com/27kxksl

……up to 86 front-line patients at ~20 clinical sites; goal: enrollment comp. by mid'11.

F. LEAD IND: Phase IIb Bavi+Doce vs. 2nd-Line NSCLC (randomized, double-blinded, placebo-ctl'd, n=120, 'registrational')

Protocol: http://clinicaltrials.gov/ct2/show/NCT01138163 (24 U.S. + 15 India + 2 RepGA + 7 RussianFED + 5 Ukraine = 53 as of 8-12-11)

Enrolled Oct2010 - Oct2011 at 40 global sites (per J.Shan 9-7-12 webcast (http://tinyurl.com/8cn87la )

8-2012: Compare Bavi+Doce's MOS=11.7mos (Bavi/3mg) to the 4 Curr-Approved 2Line/NSCLC Drugs http://tinyurl.com/cgnkvpa

• Taxotere/docetaxel => MOS=6.3mos (meta-analysis of 5 trials, 865 pts)

• Altima/pemetrexed => No diff. vs. Docetaxel (Ph.3 non-inferiority vs. Doce, 571 pts)

• Tarceva/erlotinib => MOS=5.3mos (TITAN Ph.III n=424 trial - see http://tinyurl.com/8w8lo93 )

• Iressa/gefitinib => "Iressa does not improve OS"

2-19-16/Clin-Lung-Cancer-Jrnl: Ph2 Final Data, Dr. David Gerber et al http://tinyurl.com/z5a7fwu

9-8-15: CMS SETTLEMENT EXECUTED (CSM pays PPHM only $600k for their “breach of contract, negligence & constructive fraud”, due to “limitation of liability contract clauses”) http://tinyurl.com/pemub47 (10Q/pg.17)

6-23-14: PPHM files Opposition to CSM’s Motion For Partial Summary Judgment - excerpts: http://tinyurl.com/q8xwd4v

. . .Declaration of Joseph Shan (VP/Clin+RegAffairs): http://tinyurl.com/kdgllxn

. . .Declaration of Jeffery Masten (VP/Quality): http://tinyurl.com/oru9p5q #6: “up to 25%" of CTL had 1mg, and “up to 25%" of 1mg had CTL(DoceOnly).

3-28-14: Peregrine files 1st Amended Complaint vs. CSM (13pgs) http://tinyurl.com/lsgf5lz

...Pg6: ”[as of 4-15-10], CSM had already secretly & unilaterally swapped the A & B arms so that those patients that were randomized in the A arm (CTL) and supposed to receive placebo treatments, were actually receiving 1MG Bavi treatments, and vice-versa. Peregrine’s Fall’12 investigation revealed that CSM committed other labeling & distribution errors affecting the A & B arms above & beyond the swap of the A& B arms noted above.”

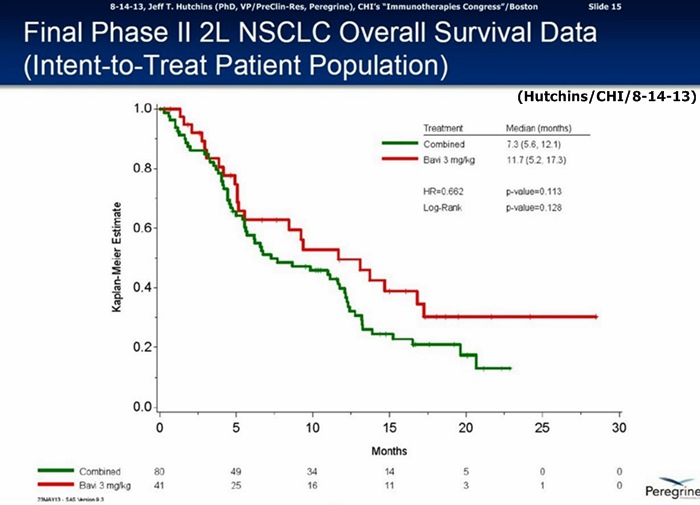

6-3-13/ASCO’13: Final Data Ph.II 2L/NSCLC http://tinyurl.com/my8qxw7

…60% improvement in MOS: Bavi/3mg=11.7mos. vs. 7.3mos. for CTL-arm(combined Bavi/1mg + DoxyOnly arms), HR=.662, P=.113

5-20-13: FDA Approves Bavituximab Ph.III Design for 2L/NSCLC; 600-pt trial to begin by y/e’13 http://tinyurl.com/n3dxtm6

...S.King: “We will now focus on starting the Ph.III trial while continuing ongoing partnering discussions.”

…R.Garnick: “This was a highly collaborative effort with the FDA; this trial, when combined with Bavi’s supporting data to date, could be sufficient to support a future BLA submission."

2-19-13: Topline Data Update from 2nd-Line NSCLC Trial after data discrepancies review http://tinyurl.com/ansqcea

…60% improvement in MOS: 3mg=11.7mos. vs. 7.3mos. for CTL-arm(combined 1mg & Doxy+placebo arms), HR=.73, p=.217

6-5-13: FTM's table of MOS data in 15 prior Doxy 2nd-Line NSCLC trials (Bavi's 60% MOS Improvement is Tops) http://tinyurl.com/m886ctb

1-25-13: MLV's George Zavoico recaps 2ndLine/NSCLC data errors & current status of PPHM's review http://tinyurl.com/b9u4pk8

...GZ: "This means that patients randomized into the high dose arm were administered Bavi correctly, whereas some of the patients in the placebo arm were administered low dose Bavi and some in the low dose Bavi arm were administered placebo. More importantly, the findings suggested that the MOS of 13.1 mos. in the high dose arm was likely to be valid. Even by historical measures, this is a remarkable result, since docetaxel's product insert lists the MOS of NSCLC patients receiving this widely used drug as 2nd-Line therapy in 2 trials as 5.7 & 7.5 mos. In effect, adding Bavi doubled the MOS. In our view, this was an extraordinary stroke of luck. If the high dose arm had been affected by the coding discrepancy, Peregrine would have been in a completely different & unfortunate position… Moreover, Peregrine must determine how best to present its case to the FDA. Will the historical controls be sufficient to justify moving Bavi into a Phase III pivotal trial, or will Peregrine have to pool the results of the placebo & low-dose arms and use that as a comparator to argue for moving ahead? A simple average of the placebo & low-dose arms results in a new control MOS of about 8.4 mos., still several months less than that of the high dose arm. This quick analysis results in about a 5-mo. survival advantage, a substantial prolongation for patients with second-line NSCLC and likely to justify moving Bavi into a pivotal Phase III trial in 2013, in our view."

1-7-13 PPHM PR - Review Update: "discrepancies are isolated to the placebo and 1 mg/kg arms; no evidence of discrepancies in the 3 mg/kg arm… Peregrine is taking a very conservative approach toward analyzing the results by combining the placebo & 1mg/kg arms into one treatment arm (control arm), and comparing to the 3mg/kg arm. This analysis indicates that the 3 mg/kg arm continues to show favorable TRR's, PFS, and OS over the new combined control arm. Peregrine expects to announce more detailed results from the analysis in the near term when it is completed." http://tinyurl.com/asup54d

9-24-12: Major Discrepancies found in 2nd-Line NSCLC Ph.2B Treatment Group Coding by Indep. 3rd-Party Vendor CMS/FargoND http://tinyurl.com/8r9zcqy

…"Investors should not rely on clinical data that the company disclosed on or before Sept. 7, 2012 from its Ph.2 Bavi trial in patients with 2nd-Line NSCLC or any presentations or other documents related to this Ph.2 trial."

9-24-12: Peregrine sues CSM Over Bavi Ph.2B 2nd-Line NSCLC Clinical Trial Mix-Up http://tinyurl.com/8fpgngu

…CSM = Clinical Supplies Management Inc., Fargo ND http://www.csmondemand.com

...1-17-13: Peregrine's lawsuit against CSM for "breach of contract & negligence" SERVED http://tinyurl.com/a7zrgys

…9-10-12 CEO Steve King, QtlyCC ( http://tinyurl.com/8nkwrml )

……"These are truly remarkable results (statistically doubling MOS) that are not only great for the pgm… but also great news for the NSCLC patients in the trial…"

…9-10-12 Robert Garnick (Head/Reg), QtlyCC ( http://tinyurl.com/8nkwrml )

……"The NSCLC data we announced 9-7-12 has far exceeded our expectations, and I hope that you're as excited as I am with bavituximab's potential. I feel strongly that Peregrine should be recognized for having the corporate courage to conduct the rigorous, randomized placebo-controlled Phase II trial that provided these robust data and that provide the basis for us to plan for a pivotal Phase III program."

...9-7-12: PPHM Press Release about Dr. Gerber's plenary at ASTRO/Thoracic/Chicago: http://tinyurl.com/96wrrso

…"The interim data showed a statistically significant improvement in OS (Hazard Ratio 0.524, p-value .0154) and a doubling of MOS (11.1/13.1mos. vs. 5.6mos.) in the Bavituximab-containing arms compared to the [Docetaxel] ctl-arm."

......VP Joe Shan's 15min. Webcast & Slideshow recapping Dr. David Gerber's 9-7-12 ASTRO/Chicago Plenary: http://tinyurl.com/96wrrso

…8-15-12 CEO Steve King, Wedbush/NYC ( http://tinyurl.com/8mhrtld )

......"As we're sitting here today, we have still not reached the # of events for MOS in either of the Bavituximab arms - and, in fact, we still have patients that are on treatments." Q&A: "it's going to be a very positive MOS result, it's just a matter now of magnitude."

…7-16-12 CEO Steve King, QtlyCC ( http://tinyurl.com/cs7spbz )

......"The strength of this 2nd-Line NSCLC data (esp. MOS trends) in this large area of high unmet medical need has also sparked a surge in partnering discussions that has included over 15 in-person partnering meetings since that time with major players in oncology, with all discussions ongoing and addl. parties showing interest. Our goal for the program is to position ourselves, along with a potential partner, to initiate Ph3 by mid-2013, which means an EOP2 meeting by yr-end'12. It would be ideal to have a partner on board to participate in the EOP2 meeting, and we have communicated this to interested parties and they agree."

…7-16-12 Robert Garnick (Head/Reg), QtlyCC ( http://tinyurl.com/cs7spbz )

……"We've been working very hard and very actively on the next steps in our Bavi 2nd-Line NSCLC pgm, given the favorable data that we've seen. As you can imagine, with data like this, there are many things that we need to consider. One consideration is that, should the data continue to trend the way it is, particularly in survival, this opens a door for potential discussions around a pathway for Accelerated Approval. At this point, all options are being considered, with Peregrine working towards the most efficient path forward from a regulatory standpoint." Q&A: "…all in all, I think the data is extremely compelling and I think it makes a really good case. Certainly, I think, I've seen a lot of Ph2 & Ph3 data, and this is as compelling Ph2 data as I've ever seen. So, I'm very comfortable proposing a meeting with the FDA for Q4'12."

…7-12-12 CEO Steve King, JMP-Conf/NYC ( http://tinyurl.com/csdclwb )

……"Re: 2nd-Line/NSCLC trial, the most thrilling thing is the fact that, even though we'd reached MOS for the ctl-arm(Doce) at end of Apr'12 of LESS THAN 6MOS, the majority of patients are still alive (today) in both Bavi arms, and we expect that to continue for some period of time still. Ph3 planning is underway already; our goal is to start this Ph3 by mid'13, meaning an EOP2 meeting with the FDA in Q4'12; our goal is to bring a partner on board, ideally in time for that EOP2 meeting, certainly before the beg. of the Ph3 trial."

…5-21-12: TopLine data n=117 for Bavi/3mg+Doce arm: ORR=17.9%/PFS=4.5mos (vs. CTL 7.9%/3mos) http://tinyurl.com/73aeyxj

......Importantly, MOS for CTL-arm "< 6 mos", but not yet reached in both Bavi arms.

...10-6-11: Enrollment complete. http://tinyurl.com/3m9re39

...7-14-11/CC: Enrollment was taking longer than expected; have amended protocol; expanding to ~45 sites, expect enroll. comp. "early in Q4/2011", data unblinding 1H'12. http://tinyurl.com/6k6y2as

…3-17-10/Roth, CEO S.King: "We refer to this trial as a Registrational Phase II Study, because we believe that if we have results anywhere near approaching what we saw in the earlier [India] study, it could be a conduit for Accelerated Approval."

...6-4-10: Ph.2b randomized reg. trial Open for enrollment: http://tinyurl.com/25v22qk

……"up to 120 refractory patients at ~30 clinical sites; goal: fully-enroll by mid'11, topline data by y/e'11."

1st 5 COMPLETED BAVI CANCER TRIALS:

These 5 completed Ph.1 & Ph.2 Bavituximab Cancer Trials archived to: http://tinyurl.com/72dnkfg

1. Ph.1A Bavi/Mono vs. Solid Cancers (USA n=26, 6/2005-6/2009)

2. Ph.1B Bavi+Chemo vs. Solid Cancers (India n=12, 11/2006-5/2007)

3. Ph.2 Bavi+Doce/BREAST/Refractory (RepGA n=46, 1/2008-5/2009): ORR=61%(Her2+=86%), PFS=7.4mos, MOS=20.7mos *

4. Ph.2 Bavi+PC/BREAST/Frontline (India n=46, 8/2008-9/2009): ORR=74%(Her2+=100%), PFS=6.9mos, MOS=23.2mos %

5. Ph.2 Bavi+PC/NSCLC/Frontline (India n=49, 6/2008-10/2009): ORR=43%, PFS=6.1mos, MOS=12.4mos #

......* BAVI+DOCE/Refract-MBC N=46: Compare *MOS=20.7mos to 11.4mos for Doce/alone (Nabholtz/JCO1999 Ph3/n=203 http://tinyurl.com/3rxqqtk )

......% BAVI+PC/FrontLine-MBC N=46: Compare %MOS=23.2mos to 16.0mos for P+C/alone (Loesch/JCO2002 Ph2/n=95 http://tinyurl.com/6wazs9p )

......# BAVI+PC/Frontline-NSCLC N=49: Compare #MOS=12.4mos to P+C/alone=10.3, Avastin+PC=12.3 (E4599/n=434), achieved using less Chemo (175-v-200 & AUC5-v-AUC6), treating 16% (8/49) more-difficult Squamous in Bavi trial (excluded totally from E4599), and treating higher % of sicker ECOG1 pts than in E4599 (96%-v-60%). See 6-15-11/PR http://tinyurl.com/3fcz5ok , ASCO'10 http://tinyurl.com/2g5cqof , and a discussion of differentiating factors between patient demographics & baselines treated in the 2 trials: http://tinyurl.com/6k5uuf7 .

BAVI HEPC TRIALS (2005-2011) ARCHIVED From iBox 7-16-17

Now linked to from within iBox for perpetuity: http://investorshub.advfn.com/boards/show_ibox.aspx?boardid=2076

4 COMPLETED BAVITUXIMAB HEP-C PHASE1+2 TRIALS (2005-2011):

9-9-11: PPHM is positioning Bavi as potential Interferon replacement in HCV cocktails: http://tinyurl.com/3novgzk

12-2011: Nature Medicine article lists Peregrine among 11 co's dev. interferon-free treatments for HCV: http://tinyurl.com/87ltkmt

7-2011: Nature Biotechnology article quotes Dr. Thorpe on Bavi's goal to elim. IFN-A: http://tinyurl.com/3n8qluq

D. Phase II Bavi+Riba vs. Frontline-HEPC (randomized, open-label):

Protocol (init=1-2011): http://clinicaltrials.gov/ct2/show/NCT01273948

12-29-11: HCV Ph.2 Trial Update http://tinyurl.com/coq2969

……SK: " this is a good time to seek partners for the antiviral pgm. which has shown promise in this study."

9-26-11: Enrollment Complete in Bavi+Riba/HCV trial http://tinyurl.com/3j9bba8

1-10-11: Bavi+Ribavirin/HepC Ph.2 trial initiated http://tinyurl.com/4uz97tv

......"~66 patients with previously untreated genotype-1 chronic HCV, 1 of 3 arms (.3Bavi+R / 3.0Bavi+R / PEGIFN+R) for 12 wks, testing for safety & antiviral activity."

C. Phase 1B HCV-HIV Co-Infected's Mono Repeat-Dose Trial:

Protocol (init=7-2007): http://clinicaltrials.gov/ct/show/NCT00503347

…4-2-11: Ph.1B trial data presented at EASL-2011/Berlin on 4-2-11 http://tinyurl.com/3mmwy5d

…1-31-11: Enrollment Complete in HCV-HIV trial http://tinyurl.com/4tagpz2

...7-10-07: Enrollment begins at St.Michaels (Peter Ho Mem. Clinic, NJ) http://tinyurl.com/2g7rdp

......Ascending dose levels of Bavi weekly for 8 wks; ~24 pts; designed to assess Safety & PK, but "HCV & HIV viral titers & other biomarkers will be evaluated".

...5-17-07: New Clinical Protocol filed with FDA: http://tinyurl.com/2lpacm

These 2 completed Ph.1 Bavituximab Hep-C Trials archived to: http://tinyurl.com/27f58fc

1. Phase 1A Bavi/Mono Single-Dose HCV Trial: (init=8-2005 comp=2-2006 n=30)

2. Phase 1B Bavi/Mono Repeat-Dose HCV Trial: (init=6-2006 comp=1-2007 n=24)

COTARA & ANTI-VEGF/2C3 PGMS ARCHIVED From iBox 7-16-17

Now linked to from within iBox for perpetuity: http://investorshub.advfn.com/boards/show_ibox.aspx?boardid=2076

TUMOR NECROSIS THERAPY (TNT/COTARA/VEA's) NEWS:

Highlights of Cotara/GBM Trials History 1998-2009: http://tinyurl.com/y8fyl2r

12-5-12: FDA OK's Ph3 Pivotal Trial Design for Cotara/GBM (single-infustion, dual catheters) http://tinyurl.com/czjy6mf

…SK: "We can now escalate our business development activities to secure a partnership, recognizing the great interest by companies in drug candidates within the orphan and rare disease space."

5-3-10: PPHM Licenses TNT rights in "Certain APEC Countries" to STASON(Stonsa Biopharm) http://tinyurl.com/29x433b

Stonsa's website: http://stonsabio.com

...Harry Fan/CEO/Stason, "This agreement represents a unique opportunity to acquire a novel, cutting-edge pharmaceutical technology package and bring innovative & promising treatments to millions of cancer patients in Asia & the Pacific Rim. We will also continue developing new applications & bioproducts based on TNT technologies to complement Peregrine's activities in the glioblastoma arena and will aggressively pursue new, diverse biotechnology markets. To advance these efforts, a new spin-off biopharmaceutical company (Stonsa Biopharm Inc.) headed by Dr. Eugene Mechetner will be formed which will focus on commercializing TNT technologies."

7-20-11: Dr. Missag Parseghian now VP/R&D at Stonsa Biopharm; pub's article in Jrnl/Chromatography http://tinyurl.com/m3c69w

…6-2010: More on PPHM-Stason Collab., "TNT For Tumors", Lloyd Dunla, Drug Disc. News http://tinyurl.com/28vmkzm

…5-27-10: Stonsa's CEO Dr. Eugene Mechetner presents TNT at Taiwanese Bio-Seminar http://tinyurl.com/29r7one

...12-16-10: "Stason Inks Deal to use Lonza's GS Gene Expression System with TNT Antibody Platform" http://tinyurl.com/2dzz4b5

7-1-09 Eur. Patent #1638989 for 'In-Line Labeling' (used in Cotara GBM trials) & JNM Article: http://tinyurl.com/mlgz8p

India (expanded Jan'10 to U.S.) Cotara/Brain Ph.2 Trial (40 patients, 1st relapse):

India's DCGI protocol (init=7-2007): http://clinicaltrials.gov/ct2/show/NCT00677716

7-2011 BRIT (India Radiolabelling co.) says: "(Cotara) Ph2 completed; another order is expected from Peregrine to enable them to go ahead with Ph3" http://tinyurl.com/43vb4ax

10-11-11: SIRO Clinpharm is Peregrine's Indian CRO for GBM/Cotara Ph.2 Trial: http://tinyurl.com/3eobdca

6-3-11 ASCO'11: Dr. William Shapiro (Barrow) presents Cotara N=41 Data http://tinyurl.com/3g7oz55

…"Interim MOS=8.8mos(38wks); we are eager to meet with the FDA in Q4'11 to determine the optimal registration pathway for Cotara."

...NOTE: In 12-12-2011 QtlyCC, S.King reported MOS at 9.3 mos., up from in "interim" 8.8mos reported at ASCO'11. http://tinyurl.com/75rfwrv

…Dr. Shapiro's Cotara Poster #2035 (PDF & Images) http://tinyurl.com/3wetx5r

5-19-11: ASCO'11 preview; Dr. Vladimir Evilevitch (ex-Novartis) hired as Med.Dir. "to execute Cotara Reg&Clin. strategy" http://tinyurl.com/3av4red

12-20-10: Treatment Complete in Cotara/GMB Ph.2 Trial http://tinyurl.com/2844wrq

…J.Shan: "We expect top-line data by mid-year 2011 and plan to meet with the FDA to define the optimal registration pathway for Cotara."

10-18-10: Interim Ph.2 update (n=14) at CNS'10: http://tinyurl.com/349kvca

...PI Dr. Deepak Gupta, ”MOS of 86 weeks far exceeded our expectations in this very difficult to treat patient pop. where treatment options are few and rarely extend med.survival beyond 6mos."

…Roth's Joe Pantginis: "Physicians know how long these patients are expected to survive on avg. and that's why these data are very, very promising. Because there is a huge unmet medical need for new treatments for this type of brain cancer, Peregrine may seek an accelerated approval that could avoid lengthy Phase III clinical trials."

...Link to Dr. Gupta's CNS'10 Poster (6pg PDF): http://tinyurl.com/26b8sp9

...6-3-10/ASCO: Cotara/Ph.2 Trial 75% enrolled; 3 more U.S. sites added: http://tinyurl.com/33z8ggo

...1-28-10 U.S. site (Barrow/Phoenix) added formerly India-Only Ph.2 trial: http://tinyurl.com/yk565jy

…Per 3-11-10 QtlyCC, VP/ClinAffairs J.Shan said also exp. UPenn & Univ. of S.Car. http://tinyurl.com/yl4befh

…9-2-09 Interim Ph.2 data (10 pts) presented at AANS Annual Mtg/Boston: http://tinyurl.com/mxzbzm

……P.I. Dr. A.K. Mahapatra: "Most importantly, Cotara has demonstrated promising signs of efficacy."

...8-2-07 1st Patient Dosed in Indian Cotara/Brain Ph.2 Trial: http://tinyurl.com/296mcj

...The obvious desire is to compare Cotara vs. SOC Temodar for GBM therapy: http://tinyurl.com/yttt99

USA Cotara/Brain 'Dosimetry & Dose Confirmation Trial' (originally funded by NABTT):

U.S.A. Cotara Brain Cancer trial protocol (added 8-14-07): http://clinicaltrials.gov/show/NCT00509301

6-6-10/ASCO: Final Results of Cotara/GBM Ph.1/Dosimetry trial (n=12): http://tinyurl.com/24qjxxh

......"Final data confirm Cotara's targeting capabilities, delivering 300-fold higher radiation levels to the tumor than to normal organs."

...2-11-10: "Current Cancer Therapy Reviews" article on Cotara/GMB http://tinyurl.com/yg2on8f

......the cases of "2 patients who have survived more than 9 years" are also reviewed.

...12-2-09: U.S. Trial Enrollment Complete http://tinyurl.com/yez7lzd

...6-16-09: Cotara/Brain Oral-Pres. at SNM Annual Meeting http://tinyurl.com/lmhkw2

......Dr. Sui Shen (U-Alabama), "With a mean dose ratio showing 300-fold greater delivery of radiation to the tumor as compared to other organs, Cotara represents a potentially valuable new therapy for GBM patients."

…9-23-08: Article in Cleveland paper - comments by P.I. Dr. Andrew Sloan (Case Western/CLEV) http://tinyurl.com/3mkmas

...5-31-08: Cotara USA Ph.1B data presented at ASCO/2008: http://tinyurl.com/68apro

...8-29-05: NABTT Initiates Cotara/Brain Trial (28 patients/4 sites): http://tinyurl.com/9w3cr

...Orig. NABTT protocol, "6-2007, completed": http://www.clinicaltrials.gov/ct/show/NCT00128635

...The Phil (Marfuta) Bannister Story (NABTT Cotara/GBM patient #1, diag. 2-4-06): http://tinyurl.com/24gkml

......4-22-10: Phil reports on YASG that his GBM was misdiagnosed; he has a GrIII Oligodendroglioma, which carries a MLE of 12yrs! http://tinyurl.com/23mhboa

Previous USA Cotara/Brain Ph.1-2 Trials, completed in 2003:

...Slides showing correlation between Cotara dosage levels and MST vs. Temodar(curr.SOC): http://tinyurl.com/26s265

...4-27-08 update: The Jerod Swan Cotara/Brain Success Story (10 years after diag.): http://tinyurl.com/68ofsv

...5-22-07 update: The Freddie Sanford Cotara/Brain Success Story (7 years after diag.): http://tinyurl.com/2du2e5

...6-1-05: Cotara w/CED Brain Delivery pub. in Neurosurgery Jrnl: http://tinyurl.com/anmaa

..."Cotara Holds Promise for Treating Brain Cancer - P1/P2 Data Suggests Extended Survival in a Number of Patients"

PRIOR COTARA/GBM PH.3 FDA NEGOTIATIONS (2 INFUSIONS, SINGLE-CATHETER)

…12-13-01: FDA OK's Ph3 Design for Cotara/GBM (2 doses, single interstitial catheter) http://tinyurl.com/a7m3xjw

…7-1-02: Peregrine Provides Update on Status of Cotara Phase III http://tinyurl.com/bac9rtr

......"Peregrine FDA have been in close consultation regarding the Cotara Ph3 trial. Peregrine is confident that the Ph3 will adequately address all regulatory, drug safety & efficacy requirements for such a large multi-national trial."

…11-19-02: Peregrine Provides Update on Status of Cotara Phase III http://tinyurl.com/a4mw5yj

......ELegere: "Although many issues have been finalized, there are several important issues that remain to be negotiated prior to Ph3 approval. We will request an expedited meeting with the FDA so we can clarify & finalize the remaining issues…"

…11-25-02: Peregrine Receives Orphan Drug Designation for Cotara in Europe http://tinyurl.com/b7wr9at

…2-24-03: Peregrine Receives FDA Approval for its Cotara Phase III Registration Trial Design for GBM http://tinyurl.com/bjowgh6

......"Peregrine has received approval from the FDA to start its Cotara Ph3 registration clinical study in GBM."

TNT3 (Vivatuxin) Lung Cancer Approval/Launch in China:

...Shanghai MediPharm Biotech's TNT/China website: http://www.vivatuxin.com

...8-2010 Profile of Shanghai MediPharm Biotech by WallStreetResearch (Alan Stone): http://tinyurl.com/2fn3nvk

...3-2010: New Vivatuxin+MicrowaveAblation NSCLC trial (n=2000) http://tinyurl.com/2ccghvr

...1-16-07: Medipharm Launches TNT in China for Lung Cancer http://tinyurl.com/ttlne

...6-19-02: TNT Interim Lung Data from China: http://tinyurl.com/ggcba & http://tinyurl.com/em6da

Peregrine v. CTL Lawsuit - Settled 6-19-09:

...6-19-09: Form 8-K, Peregrine & CTL Settle: http://tinyurl.com/mhgcg7

...3-29-07 CTL countersues PPHM over TNT/China licensing dispute: http://tinyurl.com/39k8sx

...3-30-07 PPHM comments on CTL's 3-29-07 countersuit: http://tinyurl.com/33xzzq

...1-12-07: New China Subsidiary; Suit Filed Against Cancer Therapeutics Labs (CTL) http://tinyurl.com/y4vzbj

Eur. Licensee Merck-KGaA's TNT/Cytokine Fusion Protein Ph.1 Trial:

...4-3-12: NHS-IL2-LT (EMD 521873) poster at AACR'12 http://tinyurl.com/7bm4lpx

...4-2009: 2nd SELECTIKINE Ph.1 trial added: SELECTIKINE+RAD/NSCLC: http://tinyurl.com/pzl9j8

...5-2007: 2nd SELECTIKINE Ph.1 site added, Univ. of Lausanne, Switz: http://tinyurl.com/2l933s

...Ph.1 Trial Protocol (Merck KGaA/Germany, PI=Dr. R.Stupp): http://tinyurl.com/2f4u2t

...2-22-07: TNT-based European Cancer Trial initiated by 'Licensee': http://tinyurl.com/2zcjqr

...Clearly, it's Merck-KGaA's 'SELECTIKINE' (NHS-IL2-LT/EMD521873): http://tinyurl.com/yud7pw

VEAs:

...5-1-08 Dr. Missag Parseghian (Dir/R&D) presents VEAs at PEGS/2008: http://tinyurl.com/66onj2

AFFITECH-PPHM Collab: Fully-Human Mabs, Anti-PS & Anti-VEGF/2C3

• AT001 is Fully-Human 2C3 = R84 = PGN311

• AT004 is Fully-Human BAVI=PGN635=1N11

• AT005 is the Duke-PPHM-HIV candidate PGN632=11.31

4-28-09 Affitech comments on PGN635 & PGN632 presented at AACR'09: http://tinyurl.com/cxkcb4

...All Affitech Press Releases: http://www.affitech.com/investors-news/press-releases-english

ANTI-ANGIOGENESIS AGENT '2C3' [Fhu: R84=At001] ANTI-VEGF MAB:

8-20-12: 1st patient dosed in R84 (AT001) Ph.1 "Various Cancers" Trial in Russia/CIS http://tinyurl.com/8ahaw3l

3-12-12 Affitech's Board rec's S/H's approve Trans Nova's buyout offer (7.85mm Euros for rem. 60%) http://tinyurl.com/6qwh4zb

6-16-11: Affitech partners with IBC Generium for R84 dev. in Russia/CIS http://tinyurl.com/6hezkux

…Affitech rec. $2.5mmEURO from IBC; PPHM re-invests $1.6mm payment into "further advancement of R84."

5-26-11 Affitech update on R84 progress: "trial matl. mfg. (by Avid)" http://tinyurl.com/3hu5nqe

4-28-11: Affitech's Annual SHM (32pg. PDF) - much on R84 progress/plans: http://tinyurl.com/3h47nqa

..Affitech's 12-31-10 10-K iss. 4-28-11 - much info on R84 as well: http://tinyurl.com/3dcnefa

…$1mm milestone to PPHM for pre-clin-pkg forthcoming? Also, Avid "1st-GMP-Mfg" => http://tinyurl.com/3hc6bw9

4-28-11: Affitech signs with UTSW/Dr. Rolf Brekken for further AT001/R84 research: http://tinyurl.com/4ybh2l2

...Dr. Rolf Brekken's research at UTSW: http://www4.utsouthwestern.edu/brekkenlab/research.htm

2-18-11 Interview with Affitech CEO Dr. Martin Welschof discusses R84 Progress/Plans http://tinyurl.com/5rhmlog

Nov/Dec'10: Affitech Reiterates R84 (FH-2C3) Dev. Project Plans http://tinyurl.com/2fhyzxz

9-30-10: PPHM & Affitech Amend 7-2009 R84 Licensing Agreement http://tinyurl.com/2cn77c2

…following Affitech/NTS+ Collab for dev. in Russia/Brazil. Also, Avid gets contract to mfg. R84 for clinical studies.

8-6-10/PLoS: PPHM-Brekken/UTSW/Affitech article on pre-clin. R84=AT001 (Fhu 2C3): http://tinyurl.com/2unp4j3

…"Extended r84 therapy controls tumor growth without induction of toxicity"

6-30-10: NTS-Plus to run 2C3/R84 clinical trial(s) in Russia: http://tinyurl.com/26hhln4

…"AT001/r84 differs from Avastin in a number of ways… more selective… may have a better side effect profile."

4-21-10: Affitech sub-licenses Anti-VEGF mabs (incl. R84) to Russian partner NTS-Plus: http://tinyurl.com/29tzen9

11-3-09/PLoS: R.Brekken (PPHM SRB) on R84, increases "immune cell infiltration" in Breast Cancer: http://tinyurl.com/y8ooxah

7-22-09: Peregrine Licenses Anti-VEGF mabs (incl. R84) to Affitech: http://tinyurl.com/n67v57

6-30-09: R.Brekken article in Mol-Cancer-Ther on 2C3/R84+Avastin vs. Breast Cancer: http://tinyurl.com/mqv5ol

12-11-08: Dr. Brekken (PPHM SRB) presents F.H. 2C3 (R84/PGN311) at TX Breast-Cancer Conf. http://tinyurl.com/63utya

11-3-07: Dr. Brekken presents 'R84' (F.H. 2C3, aka PGN311) data at IBC-Conf: http://tinyurl.com/yp459d

4-16-07 AACR2007: Brekken [PPHM SRB] presents fully-human 2C3 ('R3') http://tinyurl.com/2udkgr

"The anti-tumor activity of 2C3, which only blocks VEGFR2 compared favorably to that of Avastin, which blocks both VEGFR1+2"

2-14-05: Humanized 2C3 Pre-Clin. data presented at "Anti-Angio. Symposium" http://tinyurl.com/85qy3

2-10-05: VEGF Pioneer Dr. Donald Senger joins PPHM's SRB to assist with 2C3 pgm: http://tinyurl.com/yul72w

OTHER PEREGRINE DRUG CANDIDATES:

5-6-12: Dr. Phil Thorpe's poster on PGN632 vs. AMD/CNV at ARVO-2012/FtLaud http://tinyurl.com/6q6kuwa

1-9-07 PR: VTA Microbubbles as Contrast Agents (AACR/CCR article) http://tinyurl.com/v7mf9 & http://tinyurl.com/w4pe9

9-26-06: VTA+Combo Patent Granted; Expands VTA Licensing Opportunities http://tinyurl.com/er4hh & http://tinyurl.com/ry5a4

8-25-05: PPHM Licenses Conjugated Anti-PSMA VTA Technolody to Medarex: http://tinyurl.com/dv6rt

"These types of deals should add considerable value to the company as our partners move their VTA dev. programs forward."

4-19-05: VEGF121/rGel presented at AACR (50% Survival vs. Prostate Cancer): http://tinyurl.com/8gazv

###SUPG moving VEGF121/rGel (lic. from PPHM) fwd. via Targa/Rosenblum: http://tinyurl.com/ylevod

...Rosenblum 11-15-06, "Ph.I human trials of VEGF121/rGel are expected to open shortly at M.D.A."

How do I convert iBox formatting back to “posting” format? I need to archive a bunch of really old stuff to iHub posts and then link to them in iBox with something like:

“ARCHIVE of OLD Trials: http://investorshub.advfn.com/boards/read_msg.aspx?message_id=15555408 “

Is there a tool to allow me to CONVERT already marked-up iBox text like this to “iHub Post Suitable” format that retains the original BOLDS and ITALICS etc and the highlighted URL’s?

EXAMPLE – say this is in iBox:

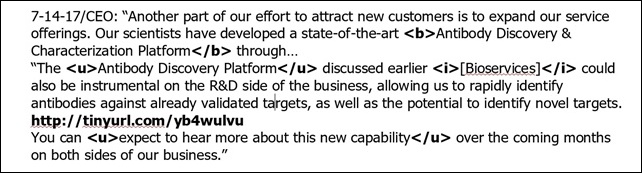

7-14-17/CEO: “Another part of our effort to attract new customers is to expand our service offerings. Our scientists have developed a state-of-the-art Antibody Discovery & Characterization Platform through…

“The Antibody Discovery Platform discussed earlier [Bioservices] could also be instrumental on the R&D side of the business, allowing us to rapidly identify antibodies against already validated targets, as well as the potential to identify novel targets.

http://tinyurl.com/yb4wulvu

You can expect to hear more about this new capability over the coming months on both sides of our business.”

I want to somehow convert this to the following, so I can then create a new iHub post that retains the original markups and urls as in this:

Once I have this, I can then easily copy/paste to a new “Archive iBox” post that looks exactly like the iBox stuff did.

I need a tool to do this. I can’t be unique!!!

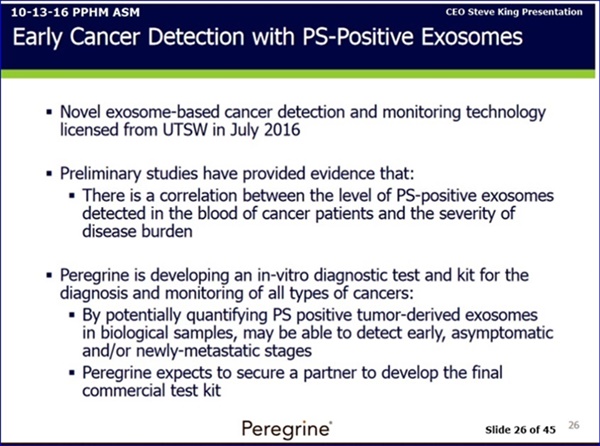

7-14-17: Updates on the PS Exosomes Diagnostic Platform – from the Q4/FY17 earnings PR, the CC, and the 10K...

7-14-17/CEO Steve King: “On the R&D side, we are pleased to report that the company continues to make progress with its PS-targeting Exosome Diagnostic Technology that is designed to detect & monitor cancer. Our scientists have successfully optimized the assay and we are currently preparing to generate addl. data, testing the diagnostic with an expanded set of human samples. Such data will be important to partnering discussions and we’ll keep you posted on progress. http://tinyurl.com/yb4wulvu

- - - - - - - - - -

**6-22-17: Nature/BJoC article, Dr. Alan Schroit/UTSW etal: "Detection of PS+ Exosomes for the Diagnosis of Early-Stage Breast & Pancreatic [Using Betabody KL15C]" http://tinyurl.com/ycrx9672 <= This article has not been PR’d or mentioned as yet by PPHM, to my knowledge.

**2-9-17/PR: PS+ Exosomes Proof-of-Concept Data (N=44, Ovarian, Dr. Alan Schroit/UTSW etal) pub. 1-22-17 in OncoTarget http://tinyurl.com/jhv57ua

From the 7-14-17 PR: http://tinyurl.com/yb4wulvu

PS EXOSOME TECHNOLOGY HIGHLIGHTS:

The company continues to make progress with its PS exosome diagnostic technology that is designed to detect and monitor cancer. The assay has been successfully optimized and we are currently preparing to generate addl. data by testing human samples. Such data will be important to partnering discussions.

4-30-17 10-K pub. 7-14-17 pg.6: http://tinyurl.com/ycxu4l5n

Exosome Technology

We licensed from UTSWMC in July 2016, proprietary Exosome-Based Cancer Diagnostic Technology, with the goal of developing an optimized test for further clinical testing in collaboration with a potential partner. The platform is based on the diagnostic potential of tumor derived exosomes, which are small vesicles from tumor cells that are released into the blood as tumors grow. Tumor derived exosomes have PS on their surface as a potentially detectable marker. It is believed that even small tumors begin to release PS-positive exosomes and thus the ability to detect these exosomes in the blood may be an indicator of the presence of a tumor. In the study published by Oncotarget [1-22-17: http://tinyurl.com/yb4wulvu ], plasma samples from 34 patients with ovarian tumors and 10 healthy subjects were analyzed for the presence of PS-expressing exosomes in a blinded test. Results demonstrated that those patients with malignant ovarian cancer displayed significantly higher blood PS exosome levels than those with benign tumors (median 0.237 vs. -0.027, p=0.0001) and the malignant and benign groups displayed significantly higher blood PS exosome levels than the healthy subjects (median 0.237 vs -0.158, p < 0.0001 and -0.027 vs -0.158, p=0.0002, respectively).

.

.

= = = = = = = = = = = = = = = = = = = = = = = = = = =

PPHM’s Exosomes Diag. Platform (incl. 6-22-2017 NATURE/BJC article)

...Known POC Data Summary (see below):

1-22-17/OncoTarget: Ovarian – senior author Alan Schroit (UTSW/PPHM SAB)

6-22-17/Nature(BJC): Breast & Pancreatic – senior author Alan Schroit (UTSW/PPHM SAB) *Using Betabody KL15C*

PPHM’s PS+ EXOSOME-BASED CANCER DETECTION & MONITORING TECHNOLOGY ("Liquid Biopsy") – Reverse Chron. History

...Excellent Exosome (aka microparticles, microvesicles) info: http://www.exosome-rna.com

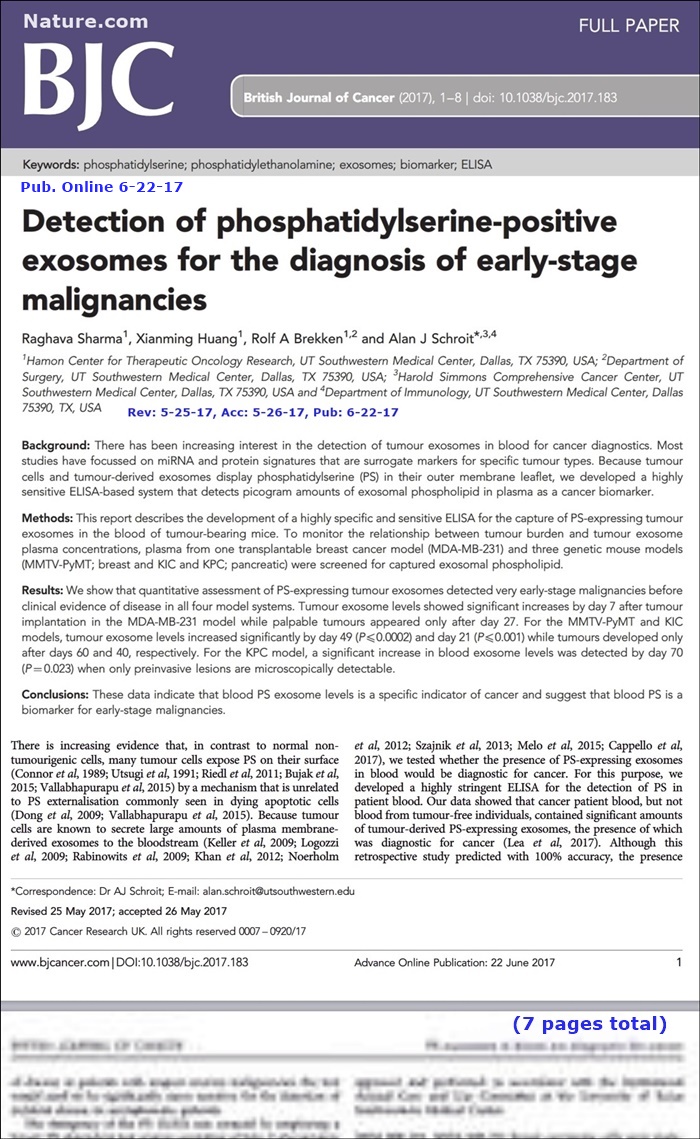

6-22-17: Nature (British Jrnl of Cancer): ”Detection of Phosphatidylserine-Positive Exosomes for the Diagnosis of Early-Stage Malignancies [Using Betabody KL15C]”

Raghava Sharma, Xianming Huang, Rolf A Brekken (PPHM SAB), Alan J Schroit

….Dr. Schroit: PPHM SAB, UTSW profile: http://tinyurl.com/yaqnvcvq ; pubs: http://tinyurl.com/lqbd8kt

https://www.nature.com/bjc/journal/vaop/ncurrent/pdf/bjc2017183a.pdf

ABSTRACT

Background: There has been increasing interest in the detection of tumor exosomes in blood for cancer diagnostics. Most studies have focused on miRNA and protein signatures that are surrogate markers for specific tumor types. Because tumor cells and tumor-derived exosomes display phosphatidylserine (PS) in their outer membrane leaflet, we developed a highly sensitive ELISA-based system that detects picogram amounts of exosomal phospholipid in plasma as a cancer biomarker.

Methods: This report describes the development of a highly specific and sensitive ELISA for the capture of PS-expressing tumor exosomes in the blood of tumor-bearing mice. To monitor the relationship between tumor burden & tumor exosome plasma concentrations, plasma from one transplantable breast cancer model (MDA-MB-231) and 3 genetic mouse models (MMTV-PyMT; breast and KIC and KPC; pancreatic) were screened for captured exosomal phospholipid.

Results: We show that quantitative assessment of PS-expressing tumor exosomes detected very early-stage malignancies before clinical evidence of disease in all 4 model systems. tumor exosome levels showed significant increases by day 7 after tumor implantation in the MDA-MB-231 model while palpable tumors appeared only after day 27. For the MMTV-PyMT and KIC models, tumor exosome levels increased significantly by day 49 (P<=0.0002) and day 21 (P<=0.001) while tumors developed only after days 60 & 40, respectively. For the KPC model, a significant increase in blood exosome levels was detected by day 70 (P=0.023) when only preinvasive lesions are microscopically detectable.

Conclusions: These data indicate that blood PS exosome levels is a specific indicator of cancer and suggest that blood PS is a biomarker for early-stage malignancies.

- - - - -

Addl. article info (Fig.1) extracted by Bamboozler762 6-23-17 iHub #300359 http://investorshub.advfn.com/boards/read_msg.aspx?message_id=132436726

Fig1: Schematic diagram of betabody, KL15C

- - - - - - - - - -

Note: BETABODIES (Clipped/Nicked B2GPI - ex: KL15, “2nd-gen. PS-Targeting”) - bind to PS directly, are smaller in size (100 vs. 250KDa) and have a longer serum half-life (~5days) than natural antibodies (Bavi=~1day) – see http://tinyurl.com/khopa3d …2/17/15: UTSW/PPHM’s BetaBodies patent#8,956,616 Awarded(Granted) http://tinyurl.com/p75uyfu

Fig.1: Schematic diagram of betabody, KL15C

Domains 1 & 5 of the plasma PS-binding protein, B2GP1, were genetically fused to the C-terminus of the CH3 domains of the Fc fragment of human IgG1. A Gly4Ser linker was inserted between the CH3 domains and domains 1 and 5 of B2GP1. The recombinant betabody was expressed as a dimer.

- - - - - - - - - -

...Glimpse of beg. of 7pg. 6-22-17 BJC article: http://www.readcube.com/articles/10.1038/bjc.2017.183

2-23-17/StockNewsUnion.com: “What Next For Peregrine Pharmaceuticals After Exosomes Proof of Concept?”

Peregrine has said that its sight is on developing the technology into an optimized diagnostic platform for clinical testing of cancer. To reach that goal, Peregrine said it is seeking strategic partners to help it develop & commercialize the platform. Those partners would be expected to inject money into the project for an equity stake in PPHM or a cut of revenue from the sale of the platform. There are several large pharmaceutical companies developing their own ovarian cancer diagnostic systems are in need of such technology, so PPHM could pitch to them to join its exosomes-based diagnostic efforts.

POTENTIAL PARTNERS:

* AstraZeneca plc (NYSE:AZN https://www.astrazeneca.com - http://finance.yahoo.com/quote/AZN MktCap=$72B)

* Tesaro Inc. (NASDAQ:TSRO http://www.tesarobio.com - http://finance.yahoo.com/quote/TSRO MktCap=$9.5B)

* Clovis Oncology Inc. (NASDAQ:CLVS http://clovisoncology.com - http://finance.yahoo.com/quote/CLVS MktCap=$2.6B)

...are some of the major pharma brands that could be a fit for PPHM. The pharma giants are at various stages in the development of their ovarian cancer assets.”

http://stocknewsunion.com/what-next-for-peregrine-pharmaceuticals-nasdaqpphm-after-proof-of-concept/2043/

2-9-17/PR: ”Recent Publication Highlights Proof-of-Concept Data Supporting the Diagnostic Potential of Phosphatidylserine-Positive Exosomes in Ovarian Cancer”

http://ir.peregrineinc.com/releasedetail.cfm?ReleaseID=1011223

TUSTIN, Feb. 9, 2017: Peregrine Pharmaceuticals, Inc. (NASDAQ:PPHM/PPHMP), a biopharmaceutical company committed to improving patient lives by manufacturing high quality products for biotechnology and pharmaceutical companies and advancing its proprietary R&D pipeline, today announced the publication of positive proof-of-concept data for a novel exosome-based cancer detection platform. Results of the study, conducted at University of Texas (UT) Southwestern Medical Center, showed researchers were able to distinguish between healthy subjects and patients with ovarian tumors based on the levels of exosomes containing phosphatidylserine (PS) found in their plasma. Furthermore, analysis of the PS-positive exosome levels allowed researchers to distinguish between malignant and benign tumors. These data were recently published online by the peer-reviewed journal, Oncotarget, in a paper titled, "Detection of Phosphatidylserine-Positive Exosomes as a Diagnostic Marker for Ovarian Malignancies: A Proof-Of-Concept Study."

Peregrine is currently advancing the proprietary exosome-based cancer diagnostic technology, licensed from UT Southwestern Medical Center in July 2016 [7-14-16: http://tinyurl.com/zszd4fj ], with the goal of developing an optimized test for further clinical testing. As part of these efforts, the company is in the process of seeking a strategic partner for collaboration on developing and commercializing the technology. The platform is based on the diagnostic potential of tumor exosomes, which are small vesicles from tumor cells that are released into the blood as tumors grow. Tumor derived exosomes have PS on their surface as a detectable marker. It is believed that even small tumors begin to release PS-positive exosomes and thus the ability to detect these exosomes in the blood may be an indicator of the presence of a tumor.

In the study published by Oncotarget [1-22-17 FULL article: http://tinyurl.com/hlc68tq ], plasma samples from 34 patients with ovarian tumors and 10 healthy subjects were analyzed for the presence of PS-expressing exosomes in a blinded test. Results demonstrated that those patients with malignant ovarian cancer displayed significantly higher blood PS exosome levels than those with benign tumors (median 0.237 vs. -0.027, p=0.0001) and the malignant and benign groups displayed significantly higher blood PS exosome levels than the healthy subjects (median 0.237 vs -0.158, p < 0.0001 and -0.027 vs -0.158, p=0.0002, respectively).

"These initial proof-of-concept results are encouraging as they appear to support the underlying concept that the measurement of PS-positive exosome levels in blood could be a simple way to detect and monitor cancer. While the work is still early, we think these data serve as an important first step in highlighting the diagnostic potential of this platform," said Steven W. King, President and CEO of Peregrine. "This type of diagnostic technology is particularly important in an area such as ovarian cancer, in which screening options are limited and the ability to detect the disease at an early stage is inadequate. We look forward to continuing to explore the potential of the technology platform in ovarian as well as other types of cancer."

"There is a significant and growing interest in the healthcare industry around the ability to detect cancer and monitor its progression with more readily accessible blood tests. With this area being one of the fastest growing segments of the oncology diagnostics market, we believe that our exosome-based technology represents a significant product development and licensing opportunity," stated Stephen Worsley, VP of Business Development at Peregrine. "Based on the fact that PS is a marker associated with a broad range of cancer types, we believe our platform has potential applications in several solid tumors beyond ovarian cancer. With that in mind, we look forward to aligning with a partner to help explore the potential of this promising technology."

- - - - - - - - - - - - -

1-22-17/OncoTarget Article: PS-Exosomes: PPHM SAB’r Dr. Alan Schroit: Proof-of-Concept Datasupports the “high diagnostic power” of PS-Positive Exosomes in Ovarian Malignancies. ...Basically, Dr. Schroit (cell membrane guru) & his UTSW team used a variant of fully-human Bavi (1N11) to detect the PS on the exosomes…

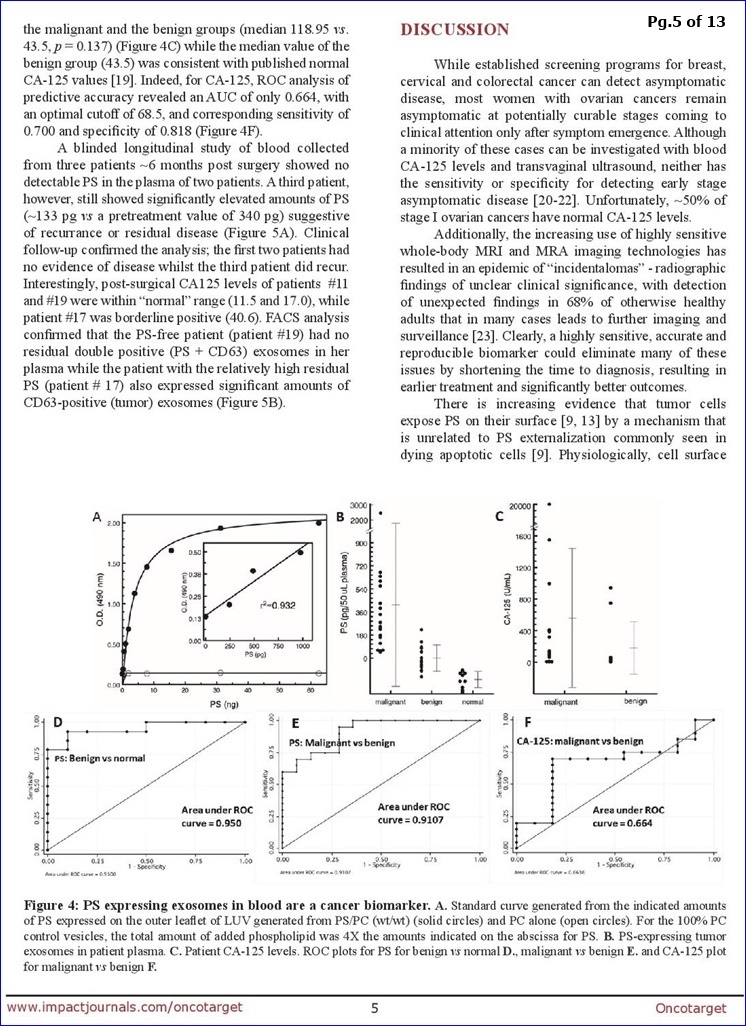

FROM PG.8: “The data summarized in Fig. 4 [N=44] show that quantification of PS-exosomes in blood distinguishes, with 100% accuracy, healthy tumor-free individuals from patients with ovarian malignancies.”

1-22-17 Oncotarget:

“Detection of Phosphatidylserine-Positive Exosomes as a Diagnostic Marker for Ovarian Malignancies: A Proof of Concept Study”

Lea J 1, Sharma R 2, Yang F 2, Zhu H 1, Ward ES 3,4, Alan J. Schroit (PPHM SAB, UTSW Profile: http://tinyurl.com/yaqnvcvq ) 1,3

1 Harold Simmons Comprehensive CC, UTSW-MC/Dallas

2 Hamon Center for Therapeutic Oncology Res., UTSW-MC/Dallas

3 Dept of Immunology, UTSW-MC/Dallas

4 Dept of Molecular & Cellular Medicine, Texas A&M Univ. Health Science Ctr

https://www.ncbi.nlm.nih.gov/pubmed/28122335 Rec.1-4-17, Acc.1-11-17, Pub.1-22-17

ABSTRACT:

There are no suitable screening modalities for ovarian carcinomas (OC) and repeated imaging and CA-125 levels are often needed to triage equivocal ovarian masses. Definitive diagnosis of malignancy, however, can only be established by histologic confirmation. Thus, the ability to detect OC at early stages is low, and most cases are diagnosed as advanced disease. Since tumor cells expose phosphatidylserine (PS) on their plasma membrane, we predicted that tumors might secrete PS-positive exosomes into the bloodstream that could be a surrogate biomarker for cancer. To address this, we developed a highly stringent ELISA that detects picogram quantities of PS in patient plasma. Blinded plasma from 34 suspect ovarian cancer patients and 10 healthy subjects were analyzed for the presence of PS-expressing vesicles. The nonparametric Wilcoxon rank sum test showed the malignant group had significantly higher PS values than the benign group (median 0.237 vs. -0.027, p=0.0001) and the malignant & benign groups had significantly higher PS values than the healthy group (median 0.237 vs -0.158, p<0.0001 and -0.027 vs -0.158, p=0.0002, respectively). ROC analysis of the predictive accuracy of PS-expressing exosomes/vesicles in predicting malignant against normal, benign against normal & malignant against benign revealed AUCs of 1.0, 0.95 and 0.911, respectively. This study provides proof-of-concept data that supports the high diagnostic power of PS detection in the blood of women with suspect ovarian malignancies.

FULL ARTICLE (13pgs):

HTML: http://www.impactjournals.com/oncotarget/index.php?journal=oncotarget&page=article&op=view&path%5B%5D=14795&path%5B%5D=47251

PDF: http://www.impactjournals.com/oncotarget/index.php?journal=oncotarget&page=article&op=download&path%5B%5D=14795&path%5B%5D=47248

EXCERPTS FROM 1-22-17 ONCOTARGET ARTICLE:

**From DISCUSSION (pg. 8): “The data summarized in Fig. 4 show that quantification of PS-exosomes in blood distinguishes, with 100% accuracy, healthy tumor-free individuals from patients with ovarian malignancies… In summary, this study provides proof-of-concept data that supports the high diagnostic power of PS-expressing tumor exosome detection in blood from women with suspect ovarian malignancies. Ultimately, these studies could lead to earlier stage diagnosis, substantial cost savings, reduced patient exposure to radiation and invasive procedures, and improved clinical outcomes. The assay might also find utility in patients with radiographic abnormalities, even before clinical detection. Indeed, an accurate biomarker predicting the likelihood of malignancy would be extremely beneficial to such a population since they often face long periods of anxiety and uncertainty inherent to a “wait & watch” approach. Finally, if PS-exosome diagnostics are confirmed in a large study to be an accurate and reproducible biomarker of ovarian malignancies, the assay could be applied to the early detection of other visceral malignancies."

**From METHODS (pg.9): “Expression of an engineered tetravalent antibody for PS-detection Monoclonal 1N11 is a human IgG1^ that binds PS through the PS-specific plasma protein B2GP1. A tetravalent variant of 1N11 (1N11-T), with 4 binding sites per molecule was designed to generate a high avidity PS binding agent (Fig.1).”

……...[NOTE: 1N11 is Fully-Human Bavituximab (aka PGN635=AT004), B2GPI-dep. Binding]

**From FINANCIAL SUPPORT (pg.11): “Supported by Cancer Prevention & Res. Inst. of TX (CPRIT) Grant #RP110441, and a Simmons CC Support Grant 5P30 CA142543.”

**EDITORIAL NOTE (pg.11): “This paper has been accepted based in part on peer-review conducted by another journal and the authors’ response & revisions as well as expedited peer-review in Oncotarget."

.

PDF EXCERPTS 1-22-17/OncoTarget/A.Schroit/PPHM-Exosomes (5 pgs of the 13):

NOTE/2-10-17: Exosomes-RNA.com posted the news of the 2-9-17 PPHM Exosomes POC PR...

http://www.exosome-rna.com/proof-of-concept-data-for-a-novel-exosome-based-cancer-detection-platform-published/

10-13-16/ASM REPORT BY ATTENDEE COPPER888: “...I think there is a shift on how the company execs and BOD view the business. As mentioned by multiple posters, SK said that they are still looking to hit a "homerun" with Bavi. But I think that they are now doing that in a framework of risk avoidance, and profitability as their primary goals. With every initiative mentioned, SK would talk about partnering in the next sentence. Exosome testing with a partner; potential of exploring the utility of Beta Bodies - would "advance aggressively with a partner"; If Sunrise data warrants a small study to confirm, they would "partner the next step", etc. I think that for good or bad...the new company directive is the march toward profitability. He also said that the company is worth multiples of its current market cap and that they want to delay the RS as much as they can. "I am focused on getting the Share price over a dollar" He mentioned that there may be many events between now and April that may get us there...” http://tinyurl.com/jx7ouay

9-8-16/CC J.Hutchins PREPARED: “1st, an an update on our PS Exosome Program. As we announced in July, we executed a licensing agreement with UT Southwestern Medical Center for a novel exosome technology designed to detect PS-positive exosomes in a patient blood sample. It is our belief that this technology can provide clinicians with detection & monitoring information regarding the presence and the prevalence of cancer. Preliminary indep. studies have demonstrated that the levels of PS-positive exosomes present in the blood of cancer patients are higher than levels found in the blood of healthy volunteers. Furthermore, study findings also suggest that there is a correlation between the level of PS positive exosomes detected in the blood of cancer patients and the severity and extent of their disease burden. Given our in-house expertise in PS targeting, we believe that we are uniquely qualified to advance this technology. We believe there are significant opportunities to use this technology as both a complementary tool in bavituximab's ongoing development as well as more broadly as the basis for a novel cancer detection & monitoring test kit that will be the focus of partnering efforts. It is our goal to develop, optimize and validate a functional screening assay capable of detecting PS positive exosomes in a blood sample and to initiate partnering discussions for commercialization of the pgm in 2017. We are on track to achieve this goal and we look forward to providing further updates.” http://tinyurl.com/jydtkoy

9-8-16-PR/FY17Q1: “Peregrine in-licensed a novel exosome technology from UTSW that has potential for cancer detection and monitoring applications. This technology aligns directly with the company's expertise, its proprietary PS-targeting platform and the bavituximab dev. program. As such, there are opportunities to use this technology as both a complementary tool in bavituximab's ongoing development, as well as more broadly as the basis for novel cancer detection & monitoring tests that can be the focus of partnering efforts.” http://tinyurl.com/jydtkoy

7-14-16/PR: Peregrine Licenses Exosome-based technology from UTSW (Inventors: Alan Schroit/Philip Thorpe) http://tinyurl.com/zszd4fj

...“relates to assays that are able to detect small amts of PS+ Exosomes in a patient's blood sample as a way to detect cancer at a very early stage of development.”

VP JEFF HUTCHINS: “We are excited to enter into this licensing agreement with our long-term collaborators at UTSW. This technology offers a promising product development opportunity and aligns directly with the company's expertise with our proprietary PS-targeting platform and our longstanding CDMO capabilities around the development, qualification, and validation of in vitro analytical assays. As such, there are significant opportunities to use this technology as both a complementary tool in bavituximab's ongoing development, as well as more broadly as the basis for novel cancer detection & monitoring tests that can be the focus of partnering efforts. It is important to note that this dev. program will require minimal capital investment and has the potential to create significant value over the next 18mos., including potential partnering opportunities. As a result, we feel that today's licensing deal provides yet another important driver in our ongoing efforts to achieve profitability."

7-14-16/CC S.King PREPARED: “...In addition to bavituximab program which continues to have tremendous potential value, the company announced earlier today that it has licensed-in a Novel PS Exosome Technology, with the potential to detect & monitor cancer at an early stage through a simple blood test [ 7-14-16: http://tinyurl.com/zszd4fj ]. I recognize that some of you might think this theme is contrary to controlling spending as we move toward profitability, but in fact we believe that given our already existing knowledge base in Targeting PS and our already available infrastructure for developing & validating tests, that so a very modest capital investment we can quickly reach proof-of-concept with a goal of partnering this technology, which could then bring in addl. revenue, with another potential upside of the technology being that it can possibly be useful in the continued dev. of bavituximab. Jeff will talk more about this during his prepared remarks. Given the strategy of R&D targeted toward early partnering, will allow the company to continue its R&D activities with significant upside coming from partnering as we move to our profitability.” http://tinyurl.com/h8eqtg5

7-14-16/CC J.Hutchins PREPARED: “I'm very happy to be able to discuss a number of exciting developments in our preclinical group. First, as Steve discussed, we have executed the licensing agreement with UT Southwestern Medical Center, for novel exosome technology [ 7-14-16: http://tinyurl.com/zszd4fj ]. While many of you are familiar with exosomes, I’ll provide a brief overview for those who are not. Exosomes are cell-secreted vesicles, or mini-cells if you will, that are present in nearly all bodily fluids, including blood. Likewise, tumor-derived exosomes represent small pieces of tumor cells that are released into the blood as tumors grow. As well, these tumor-derived exosomes have Phosphatidylserine or PS on their surface as a marker and can also contain DNA, RNA and proteins as markers of malignant disease. It is believed that even small tumors begin to release PS-positive exosomes, and thus the ability to detect these exosomes in the blood may be an indicator of presence or progression of a tumor. The licensed technology is designed to detect & monitor PS-positive exosomes in a patient's blood sample, providing clinicians with detection & monitoring information regarding the presence & prevalence of cancer. These exosomes have PS flipped to the outside of the surface and demonstrate immunosuppressive activity, just as we find with tumor cells. Preliminary studies have demonstrated that the levels of PS-positive exosomes present in the blood of cancer patients are higher than levels found in the blood of healthy volunteers. Furthermore, study findings also suggest that there is a correlation between the level of PS-positive exosomes that are detected in the blood of cancer patients and the severity or extent of their disease burden. Given our in-house expertise in PS-targeting, we believe that we are uniquely qualified to advance this technology. As Steve stated, there are significant opportunities to use this technology as both a complimentary tool in bavituximab's ongoing development, which Joe will address later, as well as more broadly as the basis for a novel cancer detection & monitoring test kit that will be the focus of our partnering efforts. It is our goal to develop, optimize, and validate a functional detection & monitoring assay capable of detecting PS-positive exosomes from a simple blood sample, and, given the company's extensive experience in developing assays of this type, we do not anticipate the need for added personnel or any specialized equipment for this project. Once we have successfully validated this assay, we plan to establish proof-of-concept through an efficient preclinical & clinical testing program. We have no intention of conducting further development work beyond the proof-of-concept stage. Rather, we expect to initiate partnering discussions for commercialization of this program in 2017. We're very excited to begin this work on this new program and we'll have more details to offer in the coming months.”

...SUMMARY: “And lastly, we've in-licensed a new exosome technology for a minimal cost that leverages our existing in-house expertise and provides us with another opportunity for us to create value to product development. Together, we believe the strategy will provide success, as it will allow us to focus the majority of our resources on achieving our primary corporate goal, future sustainable profitability within 24mos. At same time, we will focus our R&D efforts on small early stage trials and development of the exosome technology in an effort to attract partners. We believe this strategy will allow us to build near-term revenues through Avid, while maintaining the potential for significant addl. value creation associated with our R&D efforts.” http://tinyurl.com/h8eqtg5

7-14-16/CC J.Shan PREPARED: “I'd first like to comment on our new exosome program. One of the most exciting aspects of this technology is the potential synergy that it offers with our bavituximab clinical dev. program. Through our ongoing work with bavituximab, we have gained significant understanding of PS-mediated immuno-suppression in cancer. The availability of the PS specific biomarker, which can be implemented in our planned future bavituximab clinical trials, aligns nicely with our refocused bavituximab dev. strategy aimed at generating the most meaningful data possible from small, early stage clinical trials to support partnering efforts. We are very anxious to bring this new technology to Peregrine and we look forward to the value it brings to our bavituximab program.” http://tinyurl.com/h8eqtg5

7-14-16/CC Q&A/Pantginis – SK: “(On the Exosome pgm), …it fits right in; we’re not having to hire addl. people, we’re not having to bring in addl. equipment. This really fits in with everything we are doing on both studying PS, as well as on the assay development side of the business. We think it’s actually going to be complementary. There are other technologies out there looking at exosomes; they're are all taking a very different approach to what we’re doing and we actually think they could be very complementary to each other. We also see a need, even as interest in exosomes begins to pick up, to actually utilize this in conjunction with other things that are in development.” http://tinyurl.com/h8eqtg5