News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

cjgaddy

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Reposting; I missed Swim’s add of 45k Common since 8-30-17, per today’s Ronin/SW PR and the 14A followup.

= = = = = = = = = =RONIN/SWInvest 13D DETAIL TRANS:

10-10-17/14A(Ronin’s PR) COMMON ONLY: http://tinyurl.com/ybvkjd3e

This Ronin/SWIM PR has a section at the bottom giving updated ownership figures. It shows that SWIM added 45,000sh. of Common since the last 14A dated 8-29-17, taking SWIM from 655,000 to 700,000. This results in Ronin/SW Group total beneficial ownership moving from 3,979,699 to 4,024,699 (8.9% of 45,096,081 common outstanding as of 8-25-17).

Was waiting on the next PPHM/Ronin/Shareholders to update, but I think it's time to add SITC'17 regardless...

See:

Nov8-12 2017: “(SITC) Society for Immunotherapy of Cancer 32nd Annual Meeting”, Natl-Harbor MD

http://investorshub.advfn.com/boards/manage_msg.asp?message_id=134756056

KNOWN UPCOMING:

Sep25-28/Avid(booth #918): Informa’s BPI’17: BioProcess Intl. Conf. & Exhibition, Boston https://lifesciences.knect365.com/bioprocessinternational

Oct2/NCI Scientist Gregoire Altan-Bonnet(MSKCC ties), AACR’s Tumor Immunotherapy Conf., Boston http://tinyurl.com/y74v76go

...“Long-Lived Disruption of Inflammation Stems from the Catch-and-Release of Cytokines Mediated by Surface Phosphatidylserine in Tumors”

Oct6/Avid(booth): LakePharma Protein Eng. Symposium, So.SanFran http://tinyurl.com/ya6yvetk

~Oct12(??based on 2016): Peregrine's Annual Shareholder’s Meeting (2016 attendee reports: http://tinyurl.com/jx7ouay )

Nov8-12: 32th Annual SITC’17, Natl-Harbor MD http://tinyurl.com/ybfm75wj

...1. PPHM-PrecisionMed: “Results of Epigenetic-Based Quantitative PCR Assisted Immune Cell Counting Analysis in Bavi SUNRISE Trial Subgroup”

...2. MSKCC-PPHM: “PS-Targeting In Combo w/Rad+Immune Checkpoint Blockade Promotes Anti-Tumor Activity in Mouse B16 Melanoma”

Dec11-15/Avid Booth #311: KNect365’s Antibody Eng. & Therapeutics Conf., SanDiego https://lifesciences.knect365.com/antibody-engineering-therapeutics

~Dec11: FY'18Q2 (qe 10-31-17) Financials & Conf. Call - http://ir.peregrineinc.com/events.cfm

Jan18-22 2018: Phacilitate’s Immunotherapy World Forum, Miami http://www.immunotherapyforum.com

...Jan18 12:30-12:45, Joe Shan(VP/Reg+Clin): “Turning up the Heat: PS-Targeting Antibodies Modulate the Tumor Microenvironment & Enhance Checkpoint Blockade”

Re: Eastern/Dart 9-29-17 Form4: Maybe, but he’s been under 10% for a few months now, so how could that be what triggered it now?

Also, the box X’d says, “if no longer subject to Section 16.”, but then also says, “Form 4 or Form 5 obligations may continue.” Is that maybe a diff. between 5% and 10% requirements?

Finally, another strange thing about this “3. Date of Earliest Trans: 9/11/2017.”

The whole thing is weird (to ME)!

= = = = = = = = = = = = = = = = =

9-29-17 Form4 Eastern/Dart:

https://www.sec.gov/Archives/edgar/data/704562/000140840817000032/xslF345X03/ecl_pphmform4092017.xml

10-30-15: Kenneth Dart (Eastern Capital) acquires 9.5% (presently) stake (4,300,992sh.) in PPHM http://tinyurl.com/y95yskck

...3,777,183 COMMON – 8.4% of 45,096,081 common O/S at 8-25-17 (total beneficial=4,300,992 if Pref. conv. x1.19 to Common, 9.5%)

...440,000 PREFERRED – 26.7% of 1,647,760 preferred O/S at 1-31-17

…...9-29-17/Form4: http://tinyurl.com/y9oadloa ???

8-2016: One 5% Stockholder: Eastern Capital Limited (Kenneth Dart), Grand Cayman Islands

...from Form14A ASM Proxy http://tinyurl.com/ybu8nr7l

8-2016: “The info. set forth herein is based solely on a Schd. 13G/A filed 11-2-15 by Eastern Capital Ltd. The number of beneficial shares owned (30,106,945sh.) includes 3,666,667 shares of common stock that could be acquired upon conversion of the 440,000 shares of Series E Preferred Stock held by Eastern Capital.”

11-2-15/E.Cap 13G & Form3: http://tinyurl.com/pexs62e & http://tinyurl.com/ns2s9p6

Thx/PM: "This same joint PPHM+MSKCC TITLED poster was presented..."

Huts, Eastern(K.Dart)’s 3,777,183 COMMON (8.4%) matches what I posted in my latest “Large Ownership Summary(34.8%)” update, except that he also owns 440,000sh. of PREFERRED.

See: http://investorshub.advfn.com/boards/read_msg.aspx?message_id=134685455

PS: I do wish you had posted the LINK to that info (as always).

#1: 10-30-15: Kenneth Dart (Eastern Capital) acquires 9.5% stake (4,300,992sh.) in PPHM http://tinyurl.com/y95yskck

...3,777,183 COMMON – 8.4% of 45,096,081 common O/S at 8-25-17 (total beneficial=4,300,992 if Pref. conv. x1.19 to Common, 9.5%)

...440,000 PREFERRED – 26.7% of 1,647,760 preferred O/S at 1-31-17

2nd SITC’17(Nov8-12) Title: Joint MSKCC(Wolchok Lab)+PPHM

Nov8-12 2017: “(SITC) Society for Immunotherapy of Cancer 32nd Annual Meeting”, Natl-Harbor MD

”The premier destination for scientific exchange, education, and networking in the Cancer Immunotherapy Field”

SITC = The Society for Immunotherapy of Cancer http://www.sitcancer.org

SITC 2017 Meeting: http://www.sitcancer.org/2017/home

Abstracts: http://www.sitcancer.org/2017/abstracts All abstracts submitted to the SITC 32nd Annual Meeting will be published in the Journal for ImmunoTherapy of Cancer (JITC), the official journal of SITC. Regular abstracts will be published on Tuesday, Nov. 7 and LBA's will be published on Dec. 7.

= = = = =So far:

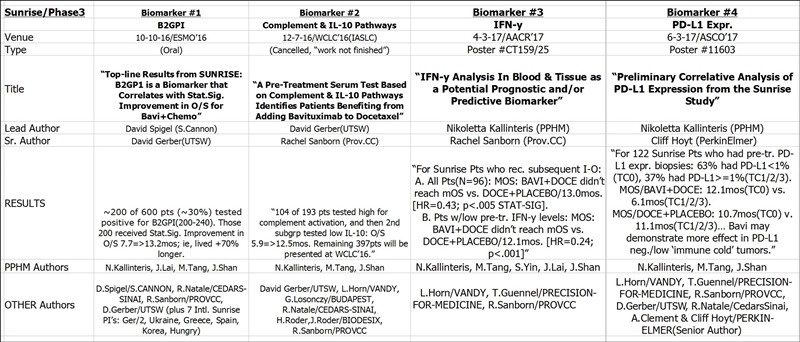

1. “Results of Epigenetic-Based Quantitative PCR Assisted Immune Cell Counting Analysis in Bavituximab SUNRISE Trial Subgroup”

https://www.sitcancer.org/2017/abstracts/titles/biomarkers-immune-monitoring

Nikoletta L. Kallinteris 1, Thomas O. Kleen 2, Min Tang 1, Shen Yin 1, Tobi Guennel 3, Jennifer Lai 1, Victor Nowakowski 2, Steven Olek 2, Steve King 1, Joseph S. Shan 1

1 Peregrine Pharmaceuticals

2 Epiontis GmbH, Berlin, Germany

3 Precision Medicine, Frederick MD

2. “Phosphatidylserine Targeting Antibody In Combination With Tumor Radiation & Immune Checkpoint Blockade Promotes Anti-Tumor Activity in Mouse B16 Melanoma”

https://www.sitcancer.org/2017/abstracts/titles/combination-therapy

Sadna Budhu 1, Rachel Giese 1, Olivier De Henau 1, Roberta Zappasodi 1, Luis Felipe Campesato 1, Aditi Gupta 1, Christopher Barker 1, Bruce Freimark 2, Jedd D. Wolchok 1, Taha Merghoub 1

1 Memorial Sloan Kettering Cancer Center, NYC

2 Peregrine Pharmaceuticals, Inc.

...NOTE: This same joint PPHM+MSKCC poster was presented 11-11-16 at SITC’16 (http://tinyurl.com/js3fca4 ) and 4-2-17 at AACR’17 (http://tinyurl.com/lxlltd6 ).

= = = = = = = = = =

Peregrine began working w/Mem-Sloan-Kettering(Jedd Wolchok Lab) in Jul'15 (2 known studies a/o 4-2017: #1/Bavi+PD1+Rad, #2/Bavi+”ACT”) to investigate “Novel PS-Targeting Immunotherapy Combos”. See: http://tinyurl.com/lxlltd6

Known Upcoming Events, Large-Shareholders(35%), RONIN-PPHM HISTORY: updated 9-17-17 with PPHM’s 9-11-17 announcement that Roger J. Lias, 57, will become Avid’s President and join PPHM’s BOD eff. 9-25-17.

NOTE: RONIN/SWIM’s 8-29-17 PRELIM. Proxy Statement (14A) and PPHM’s 8-28-17 Amended 10-K were added previously – see below...

KNOWN UPCOMING:

Sep25-28/Avid Booth #918: Informa’s BPI’17: BioProcess Intl. Conf. & Exhibition, Boston https://lifesciences.knect365.com/bioprocessinternational

Oct2/NCI Scientist Gregoire Altan-Bonnet(MSKCC ties), AACR’s Tumor Immunotherapy Conf., Boston http://tinyurl.com/y74v76go

...“Long-Lived Disruption of Inflammation Stems from the Catch-and-Release of Cytokines Mediated by Surface Phosphatidylserine in Tumors”

~Oct12(??based on 2016): Peregrine's Annual Shareholder’s Meeting (2016 attendee reports: http://tinyurl.com/jx7ouay )

Dec11-15/Avid Booth #311: KNect365’s Antibody Eng. & Therapeutics Conf., SanDiego https://lifesciences.knect365.com/antibody-engineering-therapeutics

~Dec11: FY'18Q2 (qe 10-31-17) Financials & Conf. Call - http://ir.peregrineinc.com/events.cfm

Jan20-22 2018: Phacilitate’s Immunotherapy World Forum, Miami http://www.immunotherapyforum.com

...Jan18 12:30-12:45, Joe Shan(VP/Reg+Clin): “Turning up the Heat: PS-Targeting Antibodies Modulate the Tumor Microenvironment & Enhance Checkpoint Blockade”

= = = = = = = = = = = = = = = = = = = = = = = = = = = = = = =

7-20-17: Large Ownership Summary(34.8%), RONIN Letters/PPHM Comments

Large Ownership now ~15.8mm shares, 34.9% of 45,096,081 O/S at 9-6-17. (Ronin+SW/Stafford+White, Eastern Cap./K.Dart, Institutions incl. Tappan’s 8-14-17/13G)

#1: 10-30-15: Kenneth Dart (Eastern Capital) acquires 9.5% stake (4,300,992sh.) in PPHM http://tinyurl.com/y95yskck

...3,777,183 COMMON – 8.4% of 45,096,081 common O/S at 8-25-17 (total beneficial=4,300,992 if Pref. conv. x1.19 to Common, 9.5%)

...440,000 PREFERRED – 26.7% of 1,647,760 preferred O/S at 1-31-17

#2: 7-14-17/13D: Group Ronin Trading/SWInvest (John Stafford III+Stephen White) acquires 8.8% stake (3,979,699sh.) in PPHM http://tinyurl.com/y7ezqvm9

...3,828,391 COMMON – 8.5% of 45,096,081 common O/S at 8-25-17 (total beneficial=3,979,699 if Pref. conv. x1.19 to Common, 8.8%)

...127,099 PREFERRED – 7.7% of 1,647,760 preferred O/S at 1-31-17

NOTE: ALL historical common #’s adjusted for the 1:7 R/S eff. 7-10-17.

RONIN/SW 13D SUMMARY:

13D TransDates COMMON-CHG PREF-CHG ENDING-COMMON ENDING-PREF.

3-2-17 1/20/17-3/1/17 +2,947,425 +51,364 2,947,425 51,364 http://tinyurl.com/jr42u23

3-10-17 3/2/17-3/9/17 +433,509 +25,661 3,380,934 77,025 http://tinyurl.com/ydxra96u

4-17-17 3/28/17-4/10/17 0 +23,334 3,380,934 100,359 http://tinyurl.com/lanjddc

5-19-17 5/1/17-5/17/17 0 +23,140 3,380,934 123,499 http://tinyurl.com/mgnn92x

6-20-17 3/10/17-6/16/17 +378,170 0 3,759,105 123,499 http://tinyurl.com/y76q5rqu

6-29-17 6/21/17 +7,143 0 3,766,248 123,499 http://tinyurl.com/y9sp8bfv

7-14-17 6/29/17-7/7/17 +34,891 +3,600 3,801,139 127,099 http://tinyurl.com/ybra4s69

8-29-17 8/4/17-8/15/17 +27,252 0 3,828,391 127,099 http://tinyurl.com/yay55u3p (14A)

SPLITOUT 13D GROUP into Ronin(John Stafford III) and SW-Partners(Stephen White):

Ronin Trading (Stafford) 3,173,391 115,299

SW-Partners (White) 655,000 11,800

See Ronin/SWIM 13D’s Details Below.

- - - - - - - - - - - - - - -

Plus, INSTITUTIONS a/o 6-30-17: 7,476,857sh. = 16.6% <=incl. Tappan’s 8-14-17/13G,

...and KennedyCAP corrected 9,758,459=>1,394,066(Nasdaq R/S error)

...15,198,818 +(1,394,066-9,758,459) + (2,298,684-1,656,252) = 7,476,857

http://www.nasdaq.com/symbol/pphm/institutional-holdings

TOP7:

Tappan St. Partners 2,298,684 +1,384,380 <=per 8-14-17/13G(see below**)

Kennedy Capital Mgt. 1,394,066 +146,842

Vanguard Group 1,029,755 +146,791

Blackrock (Larry Fink) 806,022 -49,433

Renaissance Technologies 481,160 +41,487

Geode Capital Mgt. 225,679 +20,319

Bandera Partners 203,004 New

**8-14-17/13G: Tappan Street (Prasad Phatak) http://tinyurl.com/ybgqp9uq

2 Funds + P.Phatak’s personal shares:

...Partners LLC, Tappan St. Fund L.P. 1,540,000

...Tappan St. Partners Ideas Fund L.P. 691,577

...Prasad Phatak (Principle Owner) 67,107 Total TAPPAN: 2,298,684 (5.1%)

Note: Tappan Inst. Holdings a/o 3-31-17 was: 914,304, 1,656,252 at 6-30-17.

9-11-17 Qtly CC-Transcript, PR(Fin’s Q1FY18/qe7-31-17), Avid Revs History Table

=> Total Revs May06-Jul17: $258.3mm/Avid + $24.1mm/Govt + $2.4mm/Lic. = $284.9mm.

Cash at 7-31-17: $37.3mm (Op. Cash Burn for q/e 7-31-17 was $78k – see below).

As of Sept. 6, 2017, there were 45,096,081 shares outstanding. (10Q 7-31-17 iss. 9-11-17 http://tinyurl.com/ycbzp4zn )

...NOTE: PPHM shares were 1:7 Reverse Split eff. 7-10-17 (315mm/$.606=>45mm/$4.24) http://tinyurl.com/ycohqn6j

This large post has 4 sections:

I. 9-11-17 Q1/FY18 Qtly. Earnings Conf. Call TRANSCRIPT (q/e 7-31-17)

II. 9-11-17 PPHM Press Release: Q1/FY18 Earnings & Developments

III. A link to “O/S Shares & ATM Sales History – 2006-curr.” (http://tinyurl.com/ybjgm425 )

IV. Updated Table of Avid Revenues By Quarter (May’06-Current)

…Recall: Peregrine’s FY runs May-Apr, so FY’18 = May’17-Apr’18.

((( Orig. transcript from SeekingAlpha.com [http://tinyurl.com/yd3zp6gu ], with numerous corrections made. )))

Link to webcast replay: http://ir.peregrineinc.com/events.cfm => http://edge.media-server.com/m/p/h72967p8

FULL TRANSCRIPT… 9-11-17 FY’18/Q1 Earnings Conf. Call (q/e 7-31-17) (King/Lias/Lytle)

WELCOME & FWD-LOOKING STATEMENTS: Tim Brons, Vida Strategic Partners (IR) http://www.peregrineinc.com

CEO STEVE KING – OPENING COMMENTS:

Thanks to all of you who have dialed in and all of you who are participating via webcast today. I would actually like to start with a moment of silence in respect to those that died in the 9/11 terrorist attacks and for those that have been affected by the recent hurricanes.

Over the past year and a half, following the negative results from our Phase III SUNRISE trial, we have seen the company change from an R&D-focused business that has been running a contract dev. & mfg. organization, or CDMO, on the side to a CDMO business that has been running R&D on the side. I am very proud that we have been able to grow our CDMO business, Avid Bioservices, from an internal support operation to a full service CDMO that now manufactures bulk drug substance for products that are approved and marketed in over 18 countries by leading biopharma companies. The company was recently recognized as a leading CDMO by Life Science Leader and received multiple 2017 Contract Mfg. Leadership Awards for Quality, Reliability, Capabilities, Expertise, and Compatibility. Avid has an outstanding regulatory inspection history and state-of-the-art cGMP mfg. Facilities. This growth did not happen by accident. It is the result of the dedication, selflessness, and intense effort by the Avid and Peregrine employees that have been involved in the business, which has always been the secret of our success and will continue to be in the future.

We have two very different businesses, CDMO and R&D, within Peregrine with different investment and growth strategies and the two efforts need to be separated so that each has a better opportunity for success. From a business standpoint, we want to ensure the success of Avid which represents a relatively lower-risk business that can be grown over the coming years to create significant stockholder value. In the meantime, we also want to find the best strategic options for advancing the bavituximab and PS-Exosome diagnostic programs, which will require significant short-term investments, which by the very nature of R&D is relatively high risk and capital intensive.

The appointment of Dr. Roger Lias as president of Avid Bioservices [9-11-17: http://tinyurl.com/yd3eh3uv ] and his appointment to Peregrine's Board of Directors marks an important next step in this transition. Roger is a highly experienced executive with a long track record of success in the CDMO industry, and was an ideal candidate for the position. We have a successful commercial CDMO business, and we look forward to taking Avid to the next level under Roger's leadership. Naturally, job one will be a smooth transition to ensure we continue to support our existing clients, while simultaneously working to attract new clients as we look to grow the business on multiple fronts.

As we focus on the success of the CDMO business, we have been evaluating the best options for divesting our R&D assets. The goal being to find a partner that will make a significant short-term investment in the bavituximab program in order to validate the subset analysis from the Phase III SUNRISE trial and build on recent data from our collaborators. The subset analysis, which supports the combination of bavituximab with checkpoint inhibitors, is compelling but needs further clinical validation. This data, combined with findings from our collaborators at Memorial Sloan Kettering Cancer Center (MSKCC – See 4-14-17: http://tinyurl.com/lxlltd6 ) supporting combinations with cellular therapies including CAR-T and the ongoing trials from our partners at the National Comprehensive Cancer Network (NCCN), all as outlined in our earnings release, have bolstered our belief that our bavituximab program can be successfully advanced in the right hands. However, there is still much work to be done to realize this value. For this reason, we have concluded that in order to best position Peregrine’s R&D assets for successful development, they should be advanced by a partner with the appropriate expertise and ample resources to invest in the necessary clinical trials. To that end, we have been working diligently towards the transformation of the overall business to becoming a pure-play CDMO, while assessing the best strategic options for the R&D assets that would allow stockholders to directly see the future value from their continued developments. By partnering and eliminating future R&D expenditures, we believe we are best positioning Avid for future growth. Through reinvestment and expansion, we believe we will attract new customers and extend current contracts that will help position Avid as a leading U.S. CDMO. We are moving forward expeditiously with strategic discussions as we recognize the need to move quickly both from the R&D & CDMO standpoints. We hope to bring this process to completion over the coming months and will update you on our progress.

----------NCCN:

[NCCN Bavituximab Trials Announced 9-6-16 http://tinyurl.com/gutgwb5

...#1: Ph1/HepC-Related Hepatocellular(Liver) (Bavi+RAD+Bayer’s Nexavar=Sorafenib), MOFFITT CC (N=18)

. . . . . . .PI: Jessica Frakes, MD https://clinicaltrials.gov/ct2/show/NCT02989870 <=Recruiting 3-27-17

...#2: Ph2/Newly Diag. Glioblastoma (Bavi+RAD+Merck’s Temodar), MASS-GEN. & DANA FARBER (N=36)

. . . . . . .PI: Elizabeth Gerstner, MD https://clinicaltrials.gov/ct2/show/NCT0313991 <=Recruiting 6-16-17, 1stDose=9/7/17

...#3: Ph2/Progressive Squamous Head+Neck (Bavi+Merck’s Keytruda), JOHNS-HOPKINS(Sidney Kimmel CC)

. . . . . . .PI: Ranee Mehra, MD https://clinicaltrials.gov/ct2/show/XXXXX - See Dr. R.Mehra Jan'17/IFN-y Biomarker: http://tinyurl.com/h8gzkww

Now back to Avid. We have continued to see lots of activity on the CDMO front, including Q1 revs of $27mm. And while we are projecting a relatively flat revenue year, based on the decreased FY’18 forecasts from our 2 largest customers, we do believe this decrease will be temporary and expect that Avid will continue to thrive despite lower revenue from these 2 clients in the short term. There could still be a revenue upside this year as our new customers continue to move towards GMP mfg. and the potential to bring on even more new customers. In addition to our business dev. efforts, we have also continued to make critical investments in our CDMO facilities to ensure that we offer the most state-of-the-art systems. During the quarter, we installed 2 new 2,000L bioreactors in the Myford facility and we have already secured commitments for this capacity. Due to its modular design, there’s a potential to install addl. bioreactors in our Myford facility which will allow us to grow the business in the future. In addition, we continue to evaluate options to expand Avid’s offerings in order to meet even more needs for our existing & prospective clients. I would now like to turn the call over to Roger for a few words on his joining the company and future directions, and we will then turn the call over to Paul Lytle for a discussion of financial highlights for the qtr and for the remainder of the FY.

ROGER LIAS (President/Avid eff. 9-25-17):

...9-11-17/PR: Dr. Lias hired as Avid’s President (also to join BOD): http://ir.peregrineinc.com/releasedetail.cfm?ReleaseID=1039872

Thanks, Steve, and good afternoon, everyone. I’d first like to say that I’m absolutely delighted to be able to join the Avid Bioservices team at what is a very exciting time for the company. It’s clear that the broad biologics market remains robust and there is undoubtedly very strong demand for high-quality contract dev. & mfg. services to support the dev. and launch of a wide range of important therapeutic biological products. Based on my personal long experience in this field, stretching way back to the formative perhaps market-making years at Celltech Biologics, which is now Lonza, and at companies such as Diosynth, KBI BioPharma, Cytovance Biologics, and Eden Biodesign, I very strongly believe that the building blocks are mostly in place here at Avid to support growth & transition to a world-leading CDMO. I’ve had the opportunity to look at Avid recently both as a competitor over the years and even more recently as a consultant supporting a very well funded company on the East Coast that has selected, I’m pleased to say, Avid as its preferred mfg. for a very interesting and potentially lifesaving product that should move rapidly to commercialization. The decision-making process for this company was multifaceted. The quality and capabilities go without saying, and ultimately the decision to come to Avid came down to the employees, the people, the flexible and creative approach, and the ability to meet timelines. And it’s interesting that Avid beat out most major contract anufacturers to win this project, and I was certainly duly impressed. In many ways, Avid is in a very unusual position relative to its peer contract manufacturers based on the somewhat unorthodox way in which the company has evolved. An exemplary 12-year track record in releasing commercial batches is very unusual and coupled with almost 25 years of overall experience in biologics, process development, and manufacture, this represents a truly tremendous platform from which to grow the company.

There’s clearly work to be done, however. Over the shorter term, I believe we clearly need to diversify the client base and to continue to grow the order book and revenue backlog. I believe that as part of this effort, Avid’s market visibility & reach needs to be dramatically increased. The new Myford mfg. facility represents a tremendous opportunity and obviously needs to be filled as a priority, and I’m pleased to see progress in that direction already. I believe that Avid’s earlier stage process dev. and process sciences capabilities need to be strengthened, both in support of mfg. operations and to create a stronger pipeline of future mfg. projects and addl. revenue stream. Stepping back and taking the longer view, there’s clearly exciting opportunities for considerable growth, both organically and potentially via mergers and acquisitions. Clearly I believe the available Myford II expansion space provides opportunities to add additional commercial drug substance manufacturing to the type already installed, but we should also examine opportunities to potentially add earlier discovery services to feed the process development and subsequent mfg. pipeline and potentially latest stage drug product mfg. services that will fill and finish a product. I believe strongly that we also need to be ready to look beyond antibodies and recombinant proteins and to take advantage of growing market demand for newer classes of products such as viral vectors and vaccines. These support exciting new therapeutic advantages in gene, cellular and immunotherapies, antibody-drug conjugates, and bio multi-specific antibody products. Each of these has specific technical and operational challenges that will need to be carefully addressed, but the opportunities are significant and I believe the timing is very good. So in closing, I’m very much looking forward to getting started and I believe that the future looks very bright for the broad biologics market and for Avid Bioservices in particular. I’m very much looking forward to taking Avid to the next level and to reporting on progress during future calls. And with that, I’d hand over to Paul who will cover the quarterly results in more detail.

PAUL LYTLE (CFO): [7-31-17 10Q iss. 9-11-17: http://tinyurl.com/ycbzp4zn ]

I’ll now discuss our financial results for Q1/FY18, starting with revenue. As a backdrop, our revenue guidance for FY’18 is expected to be $50-55mm, of which we recognized $27mm during Q1. This included $10mm in revenue that shifted from Q4 of FY’17 to Q1 due to a customer requested shipping delay. This represents an increase in revenue of 383% vs. $5.6 million that we reported during the same prior year period. While we had an excellent quarter, we have also seen decreases in mfg. from our 2 largest customers. As a result, we saw revenue backlog decline to ~$33mm at the end of the current qtr. As we look ahead, adding new customers and diversifying our customer base will be extremely important to growing revenue. This is the key reason we have hired a President of Avid solely focused on our CDMO business and someone who is highly connected to the bio-mfg. industry. Let me shift gears now to discuss our gross margins on contract mfg.. During Q1, our gross margins declined to 24% mostly due to a higher percentage of revenue related to pass through charges, such as raw materials, that are recorded to revenue at cost plus a nominal mark-up. This is relatively standard for our industry. During Q1, 38% of our revenue was related to pass through charges vs. 20% in the same prior year qtr, thereby lowering the overall gross margin. In addition, we saw lower capacity utilization during the current qtr in addition to unavailable capacity while we installed and validated two 2,000 liter bioreactors which are now operational. This also impacted our gross margins for Q1 vs. the same prior year period. Now turning to R&D, we are continuing our commitment to reduce R&D spending. In FY17 [May’16-Apr’17], we reported a 52% decline in R&D expenses and we have continued this trend into Q1/FY18, achieving a 57% reduction in R&D expenses. Based on our plan to pursue strategic alternatives for our R&D assets, we expect R&D expenses to decline at least 50% overall this year, and it could be a greater percentage decline depending on the timing of any potential transaction around the R&D assets. In summary, the increase in mfg. Revenue, combined with a decrease in R&D spending, has translated into a reduction in our net loss by 89% to $1.2mm for Q1 vs. a net loss of $11mm for the same prior year period.

Q&A: [beg. 16:16]

1. George Zavoico – (FBR & Co.): http://www.fbr.com

GZ: ”Hi, everyone. Good afternoon. And Roger welcome to Peregrine. I have a question for you. The revenue & client customer base, it’s kind of choppy, kind of up & down as you’ve seen and as Peregrine has seen lately. What in your view do you see as the critical mass that you need in terms of customer base to sort of eliminate some of that choppiness in terms of number of customers and volumes? In other words, what’s your goal, what’s your objective to get to that point?”

Roger Lias: Yes, I think the key thing is to look – we’re very well positioned to given the track record and obviously the available capacity to potentially bring in later phase clients and to technology transfer in programs that can go straight into commercial mfg., and clearly that’s a major objective. While the 2 current commercial clients are sort of somewhat soft in their forecast at the moment, if we can get more similar clients into the Myford facility, clearly that’s going to do a good job of smoothing these revenue flows. We’re fortunate in many ways, even though at times it seems that the commercial mfg. side of things can be heavy lifting and hard work, it’s a lot more choppy & lumpy if you rely entirely on process dev. and clinical stage projects. I do believe we need more of those as well in order to keep the funnel full for pipeline and to keep feeding manufacturing. But, I think if we could, over the shorter term, get in at least 2 more commercial clients and to fill the Myford I facility, I think we’ll see a much smoother revenue flow.

GZ: ”You mentioned some of the aspects of that that you really were attracted to, to be able to take this position. Could you expand on that a little bit? What do you see as a differentiating factor for Avid compared to some of its competitors? Is there going to be a cost benefit, an advantage, efficiency? What do you see as the key advantages of going with Avid vs. competitors?

Roger Lias: That’s a very good question. Differentiation in the, let’s call it the 2,000L single-use bioreactor space is getting tougher & tougher. There were more & more competitive players out there offering on paper at least similar capacity. I think for me, certainly with respect to the particular program that I was assisting with, what was really very impressive was the people, and I have to say that. It was the ability to think creatively out of the box to provide sort of exemplary feedback and that’s a difficult thing to lay out on paper, but once you get potential clients inside the door, I think the team really shines. On top of that, with the program I was involved in I haven’t had the chance to look too carefully at pricing yet, but I think there’s some potential, let’s say, just to increase margins based on pricing. I think Avid is a long way away from being one of the more expensive players out there, which I think is good news, I think it gives us a lot of upside. The available capacity in that long regulatory track record of releasing commercial batches should not be underestimated. There are many, many, I guess I’d call them peer contract manufacturers, who are only just now getting to that stage of their first FDA inspection, and in my view, we should play that for all it’s worth. So I think there’s, from a client perspective, a tremendous opportunity to gain both capacity & expertise at actually pretty reasonable value terms.

GZ: ”And as I recall and correct me if I’m wrong, it’s mostly been bulk mfg. and not so much fill+finish. Do you have any plans to do that?”

Roger Lias: I can’t say we have plans at this point. And again, forgive me as it’s early and I haven’t even had the chance to really discuss this too much with the rest of the team at this point. I do, however, believe that sort of forward integration into drug product manufacture fill+finish is potentially valuable. We have the space to do it. I certainly wouldn’t recommend jumping in heavily into very large scale or anything like that to start off with. It’s a different business; it’s further down the value chain, but nevertheless, we could certainly support clinical fills to support those drug substance clients that are in the clinic, and I think that’s potentially a very good way to start at relatively low investment.

GZ: ”Okay. Roger, welcome and good luck in meeting objectives. I also have a question for Steve regarding bavituximab, because you barely touched on it in your prepared remarks. Could you remind me of what are some of the near-term milestones? Are you going to be presenting anything at SITC’17 [Nov8-12 2017 Natl-Harbor MD], for example, or any other medical conferences?”

Steve King: So for bavituximab, we have a few things on the horizon. Obviously, we recently announced that the NCCN studies are starting to kickoff and one of those I think that’s particularly important is a combination with Keytruda in Head & Neck cancer. Clearly the data, the subset analysis from the SUNRISE trial really supports moving these kind of combinations forward, naturally where we feel that the focus of the program should be in moving forward. In addition, we have other investigators who have expressed interest in running studies that we hopefully would be able to start over the near term with other combinations with the checkpoint inhibitors in actually new indications. And so, those are some of the milestones. Absolutely, you’ll continue to see data coming out at conferences like SITC and AACR and a series of other conferences highlighting both the potential of bavi in combination with checkpoint inhibitors and combinations with cellular therapies such as CAR-T and other cellular therapies that are emerging. I think importantly from the standpoint of finding the right partner for the program, it’s really important that it is a living program and that it is active and that we’re continuing to garner the sort of interest we are from key opinion leaders and from others who really want to see the program advancing and do think it could potentially be a perfect fit with these I/O combinations. So yes, I think you’ll see lots of information coming out. And again, hopefully we’re able to find that right partner here over the short term that will really be able to not just oversee these studies but really boost the program, because it’s very important that we find a partner that’s willing to invest significant dollars upfront here in advancing the program, because we need to really illustrate the proof of concept that the subset analysis from the SUNRISE study is valid. I think that’s an important first step. And then actually move it very quickly toward commercialization because, of course with any drug you get closer & closer rather to your patent expiry and even though those can be extended, there’s a real sense of urgency to see the program move forward very quickly toward those later stage clinical trials. So yes, I look forward to updating on all fronts; the science front, clinical front, as well as the partnering front as we move into the last part of this year.

GZ: ”Okay, thanks. Look forward to seeing those – the new data. Thank you very much.”

MR. KING’S CLOSING COMMENTS:

I’d like to thank you all again for participating in today’s phone call. As always, I want to thank our stockholders for their continued support. And I would like to especially thank our patients, their families, and the investigators that are participating in our bavituximab clinical trials. With that, we will conclude the call.

= = = = = = = = = = = = = = = = = = = = = = = = = = = = = == = = =

9-11-17/PR: Peregrine Pharmaceuticals Reports Financial Results for Q1/FY2018 and Recent Developments

* Avid Bioservices Records Revenues of $27 Million in Q1/FY2018

* Roger Lias, PhD, Appointed President of Avid Bioservices as Company Continues Transition to a CDMO Focused Business

* Supported by Recent Positive Data, Company is Pursuing Strategic Options for its Research and Development Assets

http://ir.peregrineinc.com/releasedetail.cfm?ReleaseID=1039958

TUSTIN, Sept. 11, 2017: Peregrine Pharmaceuticals, Inc. (NASDAQ:PPHM/PPHMP), a biopharmaceutical company committed to improving patient lives by manufacturing high quality products for biotechnology and pharmaceutical companies and through its proprietary R&D pipeline, today announced financial results for the first quarter of fiscal year (FY) 2018 ended July 31, 2017, and provided an update on its contract manufacturing operations, research and development programs, and other corporate highlights.

Highlights Since April 30, 2017

"We have been working diligently toward the transformation from an R&D focused business to a business dedicated to a contract development and manufacturing organization or CDMO. The appointment of Roger Lias, PhD, as President of our CDMO subsidiary, Avid Bioservices, and his appointment to Peregrine's board of directors marks an important next step in this transition [9-11-17/PR: http://tinyurl.com/yd3eh3uv ]. Roger is a highly experienced executive with a long track record of success in the CDMO industry, and was an ideal candidate for the position," stated Steven W. King, President and CEO officer of Peregrine. "We have built a successful commercial CDMO business with an excellent regulatory track record and we look forward to taking Avid to the next level under Roger's leadership. Naturally, job one will be a smooth transition to ensure we continue to support our existing clients while simultaneously working to attract new clients as we look to grow the business on multiple fronts."

Avid Bioservices was established as Peregrine's internal biologics manufacturing and development group, and began formal operations in January 2002. Avid has grown from an internal support operation to a full service CDMO that manufactures bulk drug substance for products that are approved and marketed in over 18 countries by leading biopharma companies. Avid was recently recognized as a leading CDMO by Life Science Leader as a recipient of multiple 2017 Contract Manufacturing Leadership Awards for Quality, Reliability, Capabilities, Expertise and Compatibility. Avid has an outstanding regulatory inspection history and state-of-the-art cGMP manufacturing facilities. Mr. King has been president of Avid since its formation in addition to his role as president and CEO of Peregrine Pharmaceuticals since 2003.

Mr. King continued, "As we focus on the CDMO business, we have been evaluating the best option for divesting our R&D assets through licensing or asset sale. The goal being to find a partner that will make a significant short term investment in the bavituximab program in order to validate the subset analysis from the Phase III SUNRISE trial. The subset analysis, which supports the combination of bavituximab with checkpoint inhibitors, is compelling but needs further clinical validation. These data, combined with findings from our collaborators at Memorial Sloan Kettering Cancer Center (MSKCC – See 4-14-17: http://tinyurl.com/lxlltd6 ) supporting combination with cellular therapy and the ongoing trials from our partners at the National Comprehensive Cancer Network (NCCN), have bolstered our drive to find a suitable partner for advancing the bavituximab and PS-exosome diagnostic programs. We are moving forward expeditiously as we recognize the need to move quickly from the R&D standpoint, as well as the establishment of a pure play CDMO with no R&D expenses. We hope to bring this process to completion over the coming months and will update you on our progress."

Avid Bioservices Highlights

"Avid had a strong first quarter, recognizing revenue of $27 million," stated Paul Lytle, CFO of Peregrine. "When combined with a 57% decrease in R&D spending and a moderate decrease in SG&A, our net loss for the quarter decreased 89% to $1.2 million. During this transition year where we have seen a lower manufacturing demand from our top two customers, we are still expecting to generate between $50 and $55 million in revenue while we continue to focus on securing new customers and diversifying our customer base as we have added four new customers this calendar year thus far."

* The company is providing manufacturing revenue guidance for the full FY 2018 of $50-55 million.

* Avid's current manufacturing revenue backlog is $33 million, representing estimated future manufacturing revenue to be recognized under committed contracts. Most of the backlog is expected to be recognized during the remainder of FY 2018.

Research & Development Highlights

ASCO Highlights:

Peregrine researchers presented additional supportive data demonstrating that patients in the bavituximab containing arm who had low baseline PD-L1 expression on tumor cells (i.e., patients typically with poorer response to PD-1/PD-L1 checkpoint inhibitors) lived significantly longer than patients with high baseline PD-L1 expression. [6-3-17: http://tinyurl.com/y93upatl ]

ESMO Highlights:

Clinical investigators and Peregrine researchers presented the final clinical results from the company's Phase III SUNRISE trial of bavituximab in patients with previously treated locally advanced or metastatic non-squamous non-small cell lung cancer. As previously reported, study results demonstrated that the addition of bavituximab to docetaxel did not result in improvement of the study's primary endpoint of overall survival in the intent-to-treat population. However, a subgroup analysis on the final dataset demonstrated that for bavituximab plus docetaxel patients who received subsequent immunotherapy, the median overall survival was not yet reached. This compared to a median overall survival of 12.6 months for patients who received placebo plus docetaxel, and subsequent immunotherapy [HR = 0.46; p = 0.006]. [9-9-17: http://tinyurl.com/yb9kjutp ]

NCCN Highlights:

The three clinical trials under the collaboration with the NCCN are advancing as planned.

* Massachusetts General Hospital Cancer Center—Phase I/II Clinical Trial of Bavituximab with Radiation and Temozolomide for Patients with Newly Diagnosed Glioblastoma. Patient dosing was initiated in September 2017.

* Moffitt Cancer Center—A Phase I Trial of Sorafenib and Bavituximab Plus Stereotactic Body Radiation Therapy for Unresectable Hepatitis C Associated Hepatocellular Carcinoma. This trial is open for enrollment.

* The Sidney Kimmel Comprehensive Cancer Center at Johns Hopkins—Phase II Study of Pembrolizumab and Bavituximab for Progressive Recurrent/Metastatic Squamous Cell Carcinoma of the Head and Neck. This trial is expected to be initiated by the end of the calendar year 2017.

PS Exosome Technology Highlights:

The company continues to make progress with its PS exosome diagnostic technology that is designed to detect and monitor cancer. The assay has been successfully optimized and we are evaluating options to license, partner, or sell this technology. [7-15-17: http://tinyurl.com/yd3n5kbk ]

Financial Highlights and Results

Contract manufacturing revenue from Avid's clinical and commercial biomanufacturing services was $27,077,000 for the first quarter of FY 2018 compared to $5,609,000 for the first quarter of FY 2017. This represents total revenue growth of 383% for FY 2018 compared to the same prior year period. It is important to note that the $27 million included the shipment of $10 million in product, which was held over from the fourth quarter of 2017 due to delays in shipping at the customer's request. The first quarter increase was primarily attributed to an increase in demand for contract manufacturing services associated with process validation activities in addition to the greater number of manufacturing runs shipped during the quarter.

Total costs and expenses for the first quarter of FY 2018 were $28,306,000, compared to $16,691,000 for the first quarter of FY 2017. Research and development expenses decreased 57% to $3,645,000, compared to $8,569,000 for the first quarter of FY 2017.

Cost of contract manufacturing increased to $20,448,000 in the first quarter of FY 2018 compared to $3,062,000 for the first quarter of FY 2017. This increase is primarily due to an increase in the cost of contract manufacturing associated with higher reported revenue. Also contributing to this increase and impacting gross margins for the period was idle capacity due to lower demand and unavailable capacity during the installation of the new 2,000 liter bioreactors combined with a higher percentage of revenue related to pass through charges, such as raw materials, that are recorded as revenue at cost plus a nominal mark-up, thereby lowering the overall gross margin. During the current quarter, 38% of our revenue was related to pass-through charges versus 20% in the same prior year quarter. For the first quarter of FY 2018, selling, general and administrative expenses decreased to $4,213,000 compared to $5,060,000 for FY 2017. Peregrine's consolidated net loss attributable to common stockholders was $2,647,000 or $0.06 per share, for the first quarter of FY 2018, compared to a net loss attributable to common stockholders of $12,437,000, or $0.36 per share, for the same prior year quarter. Peregrine reported $37,256,000 in cash and cash equivalents as of July 31, 2017, compared to $46,799,000 at fiscal year ended April 30, 2017.

More detailed financial information and analysis may be found in Peregrine's Quarterly Report on Form 10-Q, which will be filed with the Securities and Exchange Commission today.

[ https://www.sec.gov/Archives/edgar/data/704562/000168316817002343/peregrine_10q-073117.htm ]

CONFERENCE CALL: Peregrine will host a conference call and webcast this afternoon, Sept. 11, 2017, at 4:30PM EDT (1:30PM PDT). To listen to the conference call, please dial (877) 312-5443 or (253) 237-1126 and request the Peregrine Pharmaceuticals conference call. To listen to the live webcast, or access the archived webcast, please visit: http://ir.peregrineinc.com/events.cfm .

About Peregrine Pharmaceuticals, Inc.

Peregrine Pharmaceuticals, Inc. is a biopharmaceutical company committed to improving the lives of patients by delivering high quality pharmaceutical products through its contract development and manufacturing organization (CDMO) services and through its proprietary R&D pipeline. Peregrine's in-house CDMO services, including cGMP manufacturing and development capabilities, are provided through its wholly-owned subsidiary Avid Bioservices, Inc. (http://www.avidbio.com ), which provides development and biomanufacturing services for both Peregrine and third-party customers. The company is also working to evaluate its lead immunotherapy candidate, bavituximab, in combination with immune stimulating therapies for the treatment of various cancers, and developing its proprietary exosome technology for the detection and monitoring of cancer. For more information, please visit http://www.peregrineinc.com .

About Avid Bioservices

Avid Bioservices provides a comprehensive range of process development, high quality cGMP clinical and commercial manufacturing services for the biotechnology and biopharmaceutical industries. With over 15 years of experience producing monoclonal antibodies and recombinant proteins in batch, fed-batch and perfusion modes, Avid's services include cGMP clinical and commercial product manufacturing, purification, bulk packaging, stability testing and regulatory strategy, submission and support. The company also provides a variety of process development activities, including cell line development and optimization, cell culture and feed optimization, analytical methods development and product characterization. For more information about Avid, please visit http://www.avidbio.com .

Safe Harbor *snip*

CONTACTS:

• Stephanie Diaz (Investors) Vida Strategic Partners 415-675-7401 sdiaz@vidasp.com

• Tim Brons (Media) Vida Strategic Partners 415-675-7402 tbrons@vidasp.com

PEREGRINE PHARMACEUTICALS, INC.

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS AND COMPREHENSIVE LOSS (UNAUDITED)

THREE MONTHS ENDED

JULY 31,

2017 2016

Contract manufacturing revenue $ 27,077,000 $ 5,609,000

COSTS AND EXPENSES:

Cost of contract manufacturing 20,448,000 3,062,000

Research and development 3,645,000 8,569,000

Selling, general and administrative 4,213,000 5,060,000

Total costs and expenses 28,306,000 16,691,000

LOSS FROM OPERATIONS (1,229,000 ) (11,082,000 )

OTHER INCOME (EXPENSE):

Interest and other income 27,000 25,000

Interest and other expense (3,000 ) —

NET LOSS $ (1,205,000 ) $ (11,057,000 )

COMPREHENSIVE LOSS $ (1,205,000 ) $ (11,057,000 )

Series E preferred stock accumulated dividends (1,442,000 ) (1,380,000 )

NET LOSS ATTRIBUTABLE TO COMMON STOCKHOLDERS

$ (2,647,000 ) $(12,437,000)

WEIGHTED AVERAGE COMMON SHARES OUTSTANDING

Basic and diluted (1) 44,773,727 34,227,870

BASIC AND DILUTED LOSS PER COMMON SHARE (1) $ (0.06 ) $ (0.36 )

(1) All share and per share amounts of our common stock for all periods presented have been retroactively adjusted to reflect the one-for-seven reverse stock split of our issued and outstanding common stock, which took effect with the opening of trading on July 10, 2017.

PEREGRINE PHARMACEUTICALS, INC.

CONDENSED CONSOLIDATED BALANCE SHEETS

JULY 31, 2017 APRIL 30,

2017 Unaudited

ASSETS

CURRENT ASSETS:

Cash and cash equivalents $ 37,256,000 $ 46,799,000

Trade and other receivables 7,884,000 7,742,000

Inventories 24,235,000 33,099,000

Prepaid expenses 1,388,000 1,460,000

Total current assets 70,763,000 89,100,000

Property and equipment, net 24,399,000 23,674,000

Restricted cash 1,150,000 1,150,000

Other assets 3,963,000 4,188,000

TOTAL ASSETS $ 100,275,000 $ 118,112,000

LIABILITIES AND STOCKHOLDERS' EQUITY

CURRENT LIABILITIES:

Accounts payable $ 4,013,000 $ 5,779,000

Accrued clinical trial and related fees 4,812,000 4,558,000

Accrued payroll and related costs 4,844,000 6,084,000

Deferred revenue 13,433,000 28,500,000

Customer deposits 14,322,000 17,017,000

Other current liabilities 963,000 993,000

Total current liabilities 42,387,000 62,931,000

Deferred rent, less current portion 1,880,000 1,599,000

Commitments and contingencies

STOCKHOLDERS' EQUITY (1):

Preferred stock—$0.001 par value; authorized 5,000,000 shares; 1,647,760 issued and outstanding at July 31, 2017 and April 30, 2017, respectively 2,000 2,000

Common stock—$0.001 par value; authorized 500,000,000 shares; 45,094,154 and 44,014,040 issued and outstanding at July 31, 2017 and April 30, 2017, respectively 45,000 44,000

Additional paid-in capital 594,482,000 590,971,000

Accumulated deficit (538,521,000 ) (537,435,000 )

Total stockholders' equity 56,008,000 53,582,000

TOTAL LIABILITIES AND STOCKHOLDERS' EQUITY $ 100,275,000 $ 118,112,000

(1) All share and per share amounts of our common stock for all periods presented have been retroactively adjusted to reflect the 1:7 reverse stock split of our issued and outstanding common stock, which took effect with the opening of trading on July 10, 2017.

- - - - - - - -

From 10-Q header: “As of Sept. 6, 2017, there were 45,096,081 shares outstanding.”

- - - - - - - - - - - - - - - - -

Latest 10K 4-30-17 iss. 7-14-17 http://tinyurl.com/ycxu4l5n PR: http://tinyurl.com/yb4wulvu (Cash 4-30-17=$46.8mm); Amended 8-25-17: http://tinyurl.com/yb5jq7vc

Latest 10Q 7-31-17 iss. 9-11-17 http://tinyurl.com/ycbzp4zn PR: http://ir.peregrineinc.com/releasedetail.cfm?ReleaseID=1039958 (Cash 7-31-17=$37.3mm)

ALL SEC filings for PPHM: http://tinyurl.com/6d4jw8

9-11-17: O/S Shares & ATM Sales History (’06–curr.) http://tinyurl.com/ybjgm425

**NOTES:

1. PPHM shares were 1:7 Reverse Split eff. 7-10-17 (~315mm/$.606=>~45mm/$4.24) http://tinyurl.com/ycohqn6j

2. Per the 4-30-10 10-K (pub. 7-14-17), ALL ATM Agreements have been fully used – none remain (F-20 & F-28). If any new ATM’s are opened (and reported via Form 424B5), they go against the $67mm remaining on the orig. $150mm shelf filed via the S-3 filed 4-23-14. 10K: http://tinyurl.com/ycxu4l5n

3. The last ATM sales made (a/o the 7-31-17 10Q iss 9-11-17) were these: • Sold 5/1/17-6/30/17: $4,307,000gr./1,051,258sh. = $4.10/sh.

= = = = = = = = = = = = = = = = = = = = = = = = = = = =

Updated PPHM REVS-BY-QTR TABLE, now thru FY18'Q1(qe 7-31-17), per the 10-Q ( http://tinyurl.com/ycbzp4zn ) issued 9-11-17.

• Total Revs since May’06: ($258.3mm/Avid + $24.1mm/Govt + $2.5mm/Lic.) = $284.9mm

• 9-11-17: FY'18 (May'17-Apr'18) Avid revs guidance $50-55mm (committed B/L=$33mm). **

• Deferred-Revs at 7-31-17 total $15.1mm, DOWN from $28.5mm at 4-30-17.

• Cust.Deposits at 7-31-17 total $2.7mm, DOWN from $17.0mm at 4-30-17.

• Inventories at 7-31-17 total $24.2mm, DOWN from $33.1mm at 4-30-17.

• Avid’s Gross-Profit over last 4 qtrs: $23.5mm on revs of $79.1mm (GP%=29.7)

• Recall, Avid Rev$ from Gov’t DTRA Contract work (6/30/08 – 4/15/11, totaling $24.15mm), went into GOVT-REVS, not AVID-REVS, in the Financials.

**4-30-17 10K/p.33: “Excluding any future potential new business, we expect Avid revs for FY18 [$50-55mm guidance] to slightly decline vs. FY17. Part of this decline is due to lower anticipated commitments from Halozyme (our largest customer) based on their most recent committed forecast (covering the 3 qtrs ending March 2018), which amount is expected to be partially offset by $10mm revenue that was expected to be recognized in FY17, but has been shifted to FY18 due to a delay in shipping product that was complete & ready for shipment as of fye 4-30-17. http://tinyurl.com/ycxu4l5n

Avid’s website: http://www.avidbio.com

AVID PROFITABILITY (GROSS*) BY QTR:

QTR Avid-Rev$ CostofMfg$ Gross-Profit$ GP%

FY13Q1 7-31-12 4,135,000 2,024,000 2,111,000 51%

FY13Q2 10-31-12 6,061,000 3,703,000 2,358,000 39%

FY13Q3 1-31-13 6,961,000 3,651,000 3,310,000 47%

FY13Q4 4-30-13 4,176,000 3,217,000 959,000 23%

FY14Q1 7-31-13 4,581,000 2,670,000 1,911,000 42%

FY14Q2 10-31-13 7,354,000 4,195,000 3,159,000 43%

FY14Q3 1-31-14 3,885,000 2,416,000 1,469,000 38%

FY14Q4 4-30-14 6,474,000 3,829,000 2,645,000 41%

FY15Q1 7-31-14 5,496,000 3,583,000 1,913,000 35%

FY15Q2 10-31-14 6,263,000 4,139,000 2,124,000 34%

FY15Q3 1-31-15 5,677,000 3,113,000 2,564,000 45%

FY15Q4 4-30-15 9,308,000 4,758,000 4,550,000 49%

FY16Q1 7-31-15 9,379,000 4,608,000 4,771,000 51%

FY16Q2 10-31-15 9,523,000 4,741,000 4,782,000 50%

FY16Q3 1-31-16 6,672,000 3,896,000 2,776,000 42%

FY16Q4 4-30-16 18,783,000 9,721,000 9,062,000 48%

FY17Q1 7-31-16 5,609,000 3,062,000 2,547,000 45%

FY17Q2 10-31-16 23,370,000 15,441,000 7,929,000 34%

FY17Q3 1-31-17 10,747,000 7,974,000 2,773,000 26%

FY17Q4 4-30-17 17,904,000 11,782,000 6,122,000 34%

FY18Q1 7-31-17 27,077,000 20,448,000 6,629,000 24%

FY13 TOTAL: 21,333,000 12,595,000 8,738,000 41%*

FY14 TOTAL: 22,294,000 13,110,000 9,184,000 41%*

FY15 TOTAL: 26,744,000 15,393,000 11,151,000 42%*

FY16 TOTAL: 44,357,000 22,966,000 21,391,000 48%*

FY17 TOTAL: 57,630,000 38,259,000 19,371,000 34%*

*Avid Net-Profit (ie, incl. Selling, G&A) not split out from PPHM-Corp. in the financials.

.

PPHM REVENUES (in thousands) DEFERRED

-------REVENUES------- REVENUES INVEN-

Quarter Avid Govt Lic. TOTAL Avid Govt TORIES

FY07Q1 7-31-06 398 0 23 421 317 0 971

FY07Q2 10-31-06 636 0 48 684 1388 0 1899

FY07Q3 1-31-07 347 0 16 363 2202 0 1325

FY07Q4 4-30-07 2111 0 129 2240 1060 0 1916

FY08Q1 7-31-07 1621 0 4 1625 1820 0 2363

FY08Q2 10-31-07 1863 0 29 1892 1338 0 3500

FY08Q3 1-31-08 1662 0 13 1675 1434 0 2394

FY08Q4 4-30-08 751 0 150 901 2196 0 2900

FY09Q1 7-31-08 1193 324 0 1517 4021 980 4628

FY09Q2 10-31-08 983 958 0 1941 6472 1701 6700

FY09Q3 1-31-09 5778 1048 0 6826 4805 3262 5547

FY09Q4 4-30-09 5009 2683 175 7867 3776 3871 4707

FY10Q1 7-31-09 2070 4671 9 6750 5755 2332 6177

FY10Q2 10-31-09 5308 1510 78 6896 4260 3989 5850

FY10Q3 1-31-10 2945 6854 78 9877 3052 76 3861

FY10Q4 4-30-10 2881 1461 78 4420 2406 78 3123

FY11Q1 7-31-10 983 2111 115 3209 3719 47 4692

FY11Q2 10-31-10 3627 966 78 4671 2447 35 3555

FY11Q3 1-31-11 1922 882 79 2883 4300 40 3915

FY11Q4 4-30-11 1970 681 78 2729 5617 0 5284

FY12Q1 7-31-11 5439 0 216 5655 4145 0 4481

FY12Q2 10-31-11 4154 0 78 4232 2012 0 3178

FY12Q3 1-31-12 3203 0 78 3281 2552 0 2722

FY12Q4 4-30-12 1987 0 78 2065 3651 0 3611

FY13Q1 7-31-12 4135 0 116 4251 6056 0 5744

FY13Q2 10-31-12 6061 0 78 6139 6221 0 5426

FY13Q3 1-31-13 6961 0 78 7039 5061 0 4635

FY13Q4 4-30-13 4176 0 78 4254 4171 0 4339

FY14Q1 7-31-13 4581 0 107 4688 4164 0 5679

FY14Q2 10-31-13 7354 0 0 7354 3468 0 4033

FY14Q3 1-31-14 3885 0 0 3885 4329 0 5224

FY14Q4 4-30-14 6474 0 0 6474 5241 0 5530

FY15Q1 7-31-14 5496 0 0 5496 4670 0 5998

FY15Q2 10-31-14 6263 0 37 6300 3612 0 5379

FY15Q3 1-31-15 5677 0 0 5677 5752 0 6148

FY15Q4 4-30-15 9308 0 0 9308 6630 0 6148

FY16Q1 7-31-15 9379 0 292 9671 8291 0 10457

FY16Q2 10-31-15 9523 0 0 9523 9688 0 12554

FY16Q3 1-31-16 6672 0 37 6709 15418 0 15189

FY16Q4 4-30-16 18783 0 0 18783 15418 0 15189

FY17Q1 7-31-16 5609 0 0 5609 21531 0 25274

FY17Q2 10-31-16 23370 0 0 23370 21531 0 25274

FY17Q3 1-31-17 10747 0 0 10747 26367 0 33829

FY17Q4 4-30-17 17904 0 0 17904 28500 0 33099

FY18Q1 7-31-17 27077 0 0 27077 13433 0 24235

Totals: 258276 24149 2453 284878 <=since5/1/2006

.

TOTAL REV’s BY YEAR (Avid+Gov’t+Lic):

FY04 4-30-04 3,314 …Avid(CMO)= 3,039 (Avid-Revs don’t incl. Govt-SVCS)

FY05 4-30-05 4,959 …Avid(CMO)= 4,684

FY06 4-30-06 3,193 …Avid(CMO)= 3,005

FY07 4-30-07 3,708 …Avid(CMO)= 3,492

FY08 4-30-08 6,093 …Avid(CMO)= 5,897

FY09 4-30-09 18,151 …Avid(CMO)= 12,963

FY10 4-30-10 27,943 …Avid(CMO)= 13,204

FY11 4-30-11 13,492 …Avid(CMO)= 8,502

FY12 4-30-12 15,233 …Avid(CMO)= 14,783

FY13 4-30-13 21,683 …Avid(CMO)= 21,333

FY14 4-30-14 22,401 …Avid(CMO)= 22,294

FY15 4-30-15 26,781 …Avid(CMO)= 26,744

FY16 4-30-16 44,686 …Avid(CMO)= 44,357

FY17 4-30-17 57,630 …Avid(CMO)= 57,630

...Total Gov’t Revs from 7-2008 inception thru FY11Q1(Apr’11): $24.15mm

.

PPHM’S QTLY. NET LOSS BY QTR:

FY08Q1 7-31-07 4,656,000

FY08Q2 10-31-07 6,207,000

FY08Q3 1-31-08 6,154,000

FY08Q4 4-30-08 6,159,000

FY09Q1 7-31-08 5,086,000

FY09Q2 10-31-08 4,497,000

FY09Q3 1-31-09 3,332,000

FY09Q4 4-30-09 3,609,000

FY10Q1 7-31-09 2,428,000

FY10Q2 10-31-09 2,787,000

FY10Q3 1-31-10 1,538,000

FY10Q4 4-30-10 7,741,000

FY11Q1 7-31-10 7,695,000

FY11Q2 10-31-10 7,513,000

FY11Q3 1-31-11 8,929,000

FY11Q4 4-30-11 10,014,000

FY12Q1 7-31-11 8,092,000

FY12Q2 10-31-11 12,055,000

FY12Q3 1-31-12 11,090,000

FY12Q4 4-30-12 10,882,000

FY13Q1 7-31-12 7,664,000

FY13Q2 10-31-12 8,753,000

FY13Q3 1-31-13 4,914,000

FY13Q4 4-30-13 8,449,000

FY14Q1 7-31-13 7,600,000

FY14Q2 10-31-13 7,790,000

FY14Q3 1-31-14 9,724,000

FY14Q4 4-30-14 10,248,000

FY15Q1 7-31-14 13,129,000

FY15Q2 10-31-14 12,100,000

FY15Q3 1-31-15 12,994,000

FY15Q4 4-30-15 12,135,000

FY16Q1 7-31-15 13,723,000

FY16Q2 10-31-15 13,198,000

FY16Q3 1-31-16 16,847,000

FY16Q4 4-30-16 11,884,000

FY17Q1 7-31-16 11,057,000

FY17Q2 10-31-16 4,056,000

FY17Q3 1-31-17 7,774,000

FY17Q4 4-30-17 5,272,000

FY18Q1 7-31-17 1,205,000

= = = = = = = =

OPER. CASH BURNS* BY QTR(FROM THE 10-Q/K’S):

FY10Q1 7-31-09 2,024,000 (from 10Q pg.25)

FY10Q2 10-31-09 2,351,000 (Q1+Q2: 4,375,000 pg.28)

FY10Q3 1-31-10 1,158,000 (Q1+Q2+Q3: 5,533,000 pg.30)

FY10Q4 4-30-10 6,375,000 (FY’10: 11,908,000 10K pg.58)

FY11Q1 7-31-10 6,567,000 (from 10Q pg.24)

FY11Q2 10-31-10 6,167,000 (Q1+Q2: $12,734,000 pg.25)

FY11Q3 1-31-11 7,736,000 (Q1+Q2+Q3: $20,470,000 pg.26)

FY11Q4 4-30-11 8,961,000 (FY’11: 29,431,000 10K pg.54)

FY12Q1 7-31-11 6,984,000 (from 10Q pg.25)

FY12Q2 10-31-11 11,668,000 (Q1+Q2: 18,652,000 pg.25)

FY12Q3 1-31-12 8,490,000 (Q1+Q2+Q3: 27,142,000 pg.25)

FY12Q4 4-30-12 11,265,000 (FY’12: 38,407,000 10K pg.55)

FY13Q1 7-31-12 6,742,000 (from 10Q pg.21)

FY13Q2 10-31-12 6,162,000 (Q1+Q2: 12,904,000 pg.23)

FY13Q3 1-31-13 3,597,000 (Q1+Q2+Q3: 16,501,000 pg.23)

FY13Q4 4-30-13 7,053,000 (FY’13: 23,554,000 10K pg.60)

FY14Q1 7-31-13 5,750,000 (from 10Q pg.23)

FY14Q2 10-31-13 5,834,000 (Q1+Q2: 11,584,000 10Q pg.24)

FY14Q3 1-31-14 7,875,000 (Q1+Q2+Q3: 19,459,000 10Q pg.26)

FY14Q4 4-30-14 8,706,000 (FY’14: 28,165,000 10K pg.55)

FY15Q1 7-31-14 11,076,000 (from 10Q pg.23)

FY15Q2 10-31-14 9,947,000 (Q1+Q2: 21,023,000 10Q pg.25)

FY15Q3 1-31-15 11,116,000 (Q1+Q2+Q3: 32,139,000 10Q pg.26)

FY15Q4 4-30-15 10,474,000 (FY’15: 42,613,000 10K pg.54)

FY16Q1 7-31-15 12,306,000 (from 10Q pg.25)

FY16Q2 10-31-15 11,701,000 (Q1+Q2: 24,007,000 10Q pg.26)

FY16Q3 1-31-16 15,086,000 (Q1+Q2+Q3: 39,093,000 10Q pg.27)

FY16Q4 4-30-16 10,112,000 (FY'16: 49,205,000 10K pg.39)

FY17Q1 7-31-16 9,607,000 (from 10Q pg.22)

FY17Q2 10-31-16 2,565,000 (Q1+Q2: 12,172,000 10Q pg.24)

FY17Q3 1-31-17 6,274,000 (Q1+Q2+Q3: 18,446,000 10Q pg.24)

FY17Q4 4-30-17 3,886,000 (FY'17: 22,332,000 10K pg.40)

FY18Q1 7-31-17 78,000 (from 10Q pg.23)

FY’09 total Op-Burn: $14,715,000

FY’10 total Op-Burn: $11,908,000

FY’11 total Op-Burn: $29,431,000

FY’12 total Op-Burn: $38,407,000

FY’13 total Op-Burn: $23,554,000

FY’14 total Op-Burn: $28,165,000

FY’15 total Op-Burn: $42,613,000

FY’16 total Op-Burn: $49,205,000

FY’17 total Op-Burn: $22,332,000

Period Halozyme Cust-A Other-Custs

FYE 4-30-14 91% 1% 8%

FYE 4-30-15 79% 12% 9%

FYE 4-30-16 69% 26% 5%

Q/E 7-31-16 65% 29% 6%

Q/E 10-31-16 77% 10% 13%

Q/E 1-31-17 29% 56% 15%

FYE 4-30-17 58% 26% 16%

Q/E 7-31-17 78% 16% 16%

O/S Shares & ATM Sales History (’06–curr.)

Shares O/S as of 9-6-17: 45,096,081

**NOTES:

1. PPHM shares were 1:7 Reverse Split eff. 7-10-17 (~315mm/$.606=>~45mm/$4.24) http://tinyurl.com/ycohqn6j

2. Per the 4-30-10 10-K (iss. 7-14-17), ALL ATM Agreements had been fully used – none remained (F-20 & F-28). If any new ATM’s are opened (and reported via Form 424B5), they go against the $67mm remaining on the orig. $150mm shelf filed via the S-3 filed 4-23-14. 10K: http://tinyurl.com/ycxu4l5n

-------

NOTE: the 7-31-17 10Q (iss. 9-11-17 http://tinyurl.com/ycbzp4zn ) confirmed this: NO ATM SALES OCCURRED AFTER THOSE REPORTED IN THE “SUBSEQUENT EVENTS” SECTION OF THE 4-30-17 10K (iss. 7-14-17) – these were the last ATM’s sold:

• Sold 5/1/17-6/30/17: $4,307,000gr. / 7,358,806(1,051,258 post/RS)= $.59/sh.($4.10/sh. Post/RS)

PPHM - O/S Shares History (’06–curr.)

4-30-06 35,876,438

1-31-07 39,222,440

4-30-07 39,222,440

7-6-07 45,233,123

7-31-07 45,242,123

10-31-07 45,242,123

1-31-08 45,242,123

4-30-08 45,242,123

7-31-08 45,242,123

10-31-08 45,242,123

1-31-09 45,242,123

4-30-09 45,537,711

7-10-09 47,392,883

7-31-09 47,393,783

**NOTE: PPHM shares were 1:5 Reverse Split eff. 10-19-09 (~237mm/$.64=>~47.4mm/$3.20) http://tinyurl.com/ykuw588

10-31-09 48,869,563 +1,475,780

1-31-10 50,903,404 +2,033,841

4-30-10 53,094,894 +2,191,490

6-21-10 54,388,917 +1,294,023 (6-22-10 ATM/mlv Form424)

7-9-10 55,069,449 +475,987 (4-30-10 10K iss. 7-14-10)

7-31-10 55,784,955 +715,506

10-31-10 59,220,742 +3,435,787

11-30-10 63,932,353 +4,711,611 (10-31-10 10Q iss. 12-9-10)

12-15-10 64,404,097 +471,744 (12-17-10 S-3: $75M Shelf Reg.)

1-31-11 66,813,419 +2,409,322

2-28-11 67,885,811 +1,072,392 (1-31-11 10Q iss. 3-11-11)

4-30-11 69,837,142 +1,951,331

7-8-11 71,069,858 +1,232,716 (4-30-11 10K iss. 7-14-11)

8-22-11 72,704,647 +1,634,789 (Proxy iss. 8-26-11)

8-31-11 73,284,016 +579,369 (424B5 iss. 9-2-11)

9-8-11 79,536,268 +6,252,252 (Roth Sale to 3 Inst’s @ $1.11/sh.)

10-31-11 82,638,201 +3,101,933

12-9-11 86,788,817 +4,150,616 (10-31-11 10Q iss. 12-12-11)

1-31-12 93,146,226 +6,357,409

2-29-12 98,873,172 +5,726,946 (1-31-12 10Q iss. 3-9-12)

4-30-12 101,421,365 +2,548,193

7-13-12 104,174,056 +2,752,691 (4-30-12 10K iss. 7-16-12)

7-31-12 104,178,431 +4,375 (7-31-12 10Q iss. 9-10-12)

8-16-12 104,191,176 +12,745 (prelim. proxy 14A http://tinyurl.com/c48bvof )

9-7-12 104,191,176 nochg (7-31-12 10Q iss. 9-10-12)

10-31-12 123,310,188 +19,119,012

12-7-12 132,539,783 +9,229,595 (10-31-12 10Q iss. 12-10-12)

1-31-13 133,770,614 +1,230,831

3-12-13 137,110,758 +3,340,144 (1-31-13 10Q iss. 3-12-13)

4-30-13 143,768,946 +6,658,188 (4-30-13 10K iss. 7-11-13)

7-5-13 151,602,765 +7,833,819 (4-30-13 10K iss. 7-11-13)

7-31-13 153,506,811 +1,904,046

9-5-13 156,461,114 +2,954,303 (7-31-13 10K iss. 9-9-13)

10-31-13 160,248,742 +3,781,628

12-6-13 160,325,891 +77,149 (10-31-13 10K iss. 12-10-13)

1-31-14 176,453,261 +16,127,370

3-3-14 176,481,054 +27,793 (1-31-14 10Q iss. 3-7-14)

4-30-14: 178,871,164 +2,390,110

7-7-14: 179,209,458 +338,294 (4-30-14 10-K cover page, iss. 7-14-14)

7-31-14: 179,216,032 +6,574 (7-31-14 10Q iss. 9-9-14)

8-22-14: 179,226,424 +10,392 (8-28-14 Proxy/Def14A)

9-5-14: 179,505,424 +279,000 (7-31-14 10Q iss. 9-9-14)

10-31-14: 182,000,583 +2,495,159 (10-31-14 10Q iss. 12-10-14)

12-5-14: 182,081,234 +80,651 (10-31-14 10Q cover pg., iss. 12-10-14)

12-19-14: 182,081,234 -0- (12-23-14 S-3)

1-31-15: 184,244,698 +2,163,464 (1-31-15 10Q iss. 3-12-15)

3-12-15: 188,332,872 +4,088,174 (“ “ “)

4-30-15: 193,346,627 +5,013,755 (4-30-15 10-K iss. 7-14-15)

7-10-15: 199,934,918 +6,588,291 (4-30-15 10-K/cover-pg, iss. 7-14-15)

7-31-15: 200,983,948 +1,049,030 (7-31-15 10Q iss. 9-9-15)

9-4-15: 202,124,031 +1,140,083 (“ “ “)

10-31-15: 225,824,551 +23,700,520 (10-31-15 10Q iss. 12-10-15)<=Incl. 18.5mm sh. Dart/EastCAP @1.08

12-9-15: 229,701,808 +3,877,257 (10-31-15 10Q iss. 12-10-15)

1-31-16: 232,231,242 +2,529,434 (1-31-16 10Q iss. 3-9-16)

3-8-16: 233,738,426 +1,507,184 (“ “ “)

4-30-16: 236,930,485 +3,192,059 (4-30-16 10K iss. 7-14-16)

7-11-16: 241,456,721 +4,526,236 (“ “ “)

7-31-16: 241,456,721 -0- (7-31-16 10Q iss. 9-8-16)

9-2-16: 242,381,850 +925,129 (“ “ “)

10-31-16: 251,765,279 +9,383,429 (10-31-16 10Q iss. 12-12-16)

12-8-16: 257,141,534 +5,376,255 (“ “ “)

1-31-17: 271,068,464 +13,926,930 (1-31-17 10Q iss. 3-13-17)

3-10-17: 297,709,478 +26,641,014 (“ “ “)

4-30-17: 44,014,040(x7)=308,098,280 +10,388,802 (4-30-17 10K iss. 7-14-17)

7-10-17: 1:7 R/S (~315mm/$.606=>~45mm/$4.24) http://tinyurl.com/ycohqn6j

7-10-17: 45,069,188 +1,055,148 (“ “ “)

7-31-16: 45,094,154 +24,966 (7-31-17 10Q iss. 9-11-17)

8-25-17: 45,096,081 +1,927 (8-25-17 Amended 10K http://tinyurl.com/yb5jq7vc )

9-6-17: 45,096,081 nochg (7-31-17 10Q iss. 9-11-17)

= = = = = = = = = = = = = = = = = =

ATM Sales Summary (3/2009–9/11/2017). Also, PPHM O/S Shares History Table (’06–curr.) at the bottom of this post. At 9-6-17, common shares O/S = 45,096,081sh. (recall, 1:7 R/S was eff. 7-10-17)

ATM = “At-The-Market Sales Issuance”

-------

The 7-31-17 10Q (iss. 9-11-17 http://tinyurl.com/ycbzp4zn ) confirmed that NO ATM SALES OCCURRED AFTER THOSE REPORTED IN THE “SUBSEQUENT EVENTS” SECTION OF THE 4-30-17 10K (iss. 7-14-17) – these were the last ATM’s sold:

• Sold 5/1/17-6/30/17: $4,307,000gr. / 7,358,806(1,051,258 post/RS)= $.59/sh.($4.10/sh. Post/RS)

I. WM-SMITH 3-2009:

• $7.5mm ATM/Wm.SMITH 3-26-09: $7,500,000gr. / 2,150,759sh. = $3.49/sh. (commiss: 3%)

• $25mm ATM/Wm.SMITH 7-14-09: $25,000,000gr. / 7,569,314sh. = $3.30/sh. (commiss: 3%/1st$15mm, then 2%)

*Total Raised via WmSmith ATM Sales thru 7-31-10:

. . .Before 7-10-17 1:7RS: $32,500,000gr. / 9,720,073sh. = $3.34/sh.

. . .After 7-10-17 1:7RS: $32,500,000gr. / 1,388,582sh. = $23.41/sh.

II. MLV 6-2010: http://www.mlvco.com

$15mm ATM/MLV 6-22-10 (commiss: 2%) Form424: http://tinyurl.com/24txkxb

• Sold 6/22/10–10/31/10: $6,840,000gr. / 4,031,018sh. = $1.70/sh.

• Sold 11/1/10–11/30/10: $7,407,000gr. / 4,711,611sh. = $1.57/sh.

• Sold 12/1/10–1/31/11: $753,000gr. / 471,744sh. = $1.60/sh.

*Total Raised via MLV June’10 ATM Sales thru 1-31-11:

. . .Before 7-10-17 1:7RS: $15,000,000gr. / 9,214,373 = $1.63/sh.

. . .After 7-10-17 1:7RS: $15,000,000gr. / 1,316,339 = $11.40/sh.

III. MLV 12-2010: “Dec’10 AMI Agreement” http://www.mlvco.com

$75mm ATM/MLV 12-29-10 (commiss: max=5%) Form8K: http://tinyurl.com/2a6w76g

(pursuant to $75mm S-3 Shelf Reg. filed 12-17-10: http://tinyurl.com/2469b2d )

• Sold 12/29/10-1/31/11: $6,460,000gr. / 2,385,862sh. = $2.71/sh.

• Sold 2/1/11-2/28/11: $2,358,000gr. / 998,142sh. = $2.36/sh.

• Sold 3/1/11-4/30/11: $4,470,000gr. / 1,840,487sh. = $2.43/sh.

• Sold 5/1/11-7/31/11: $3,713,000gr. / 1,912,576sh. = $1.94/sh.

• Sold 8/1/11-10/31/11: $5,582,000gr. / 4,727,840sh. = $1.18/sh.

• Sold 9-2-12 Roth Direct: $6,940,000gr./ 6,252,252sh. = $1.11/sh.

• Sold 11/1/11-1/31/12: $10,961,000gr. / 10,308,025sh. = $1.06/sh.

• Sold 2/1/12-2/29/12: $5,871,000gr. / 5,726,946sh. = $1.03/sh.

• Sold 3/1/12-4/30/12: $1,263,000gr. / 2,198,543sh. = $.57/sh.

• Sold 5/1/12-6/30/12: $1,496,000gr. / 2,752,691sh. = $.54/sh.

• Sold 7/1/12-9/26/12: none**

• Sold 9/27/12-10/31/12: $16,719,000gr./ 18,557,928 = $.90/sh.

• Sold 11/1/12-11/30/12: $7,296,000gr./ 9,220,313 = $.79

• Sold 12/1/12-1/31/13: $1,540,000gr./ 1,131,282 = $1.36

• Sold 2/1/13-3/12/13: $330,000gr./ 201,154 = $1.64

*Total Raised via MLV Dec’10 ATM Sales thru 3-12-2013:

. . .Before 7-10-17 1:7RS: $75,000,000gr. / 68,214,041 = $1.10sh.

. . .After 7-10-17 1:7RS: $75,000,000gr. / 9,744,863 = $7.70sh.

IV. MLV 12-2012: “Dec’12 AMI Agreement” http://www.mlvco.com

$75mm ATM/MLV 12-29-12 (commiss: max=5%) Form8K: http://tinyurl.com/2a6w76g

(pursuant to $75mm S-3 Shelf Reg. filed 3-9-12: http://tinyurl.com/7dl7pjm )

• Sold 2/1/13-3/12/13: $4,475,000gr. / 3,132,402sh. = $1.43/sh.

• Sold 3/13/13-4/30/13: $8,897,000gr. / 6,188,273sh. = $1.44/sh.

• Sold 5/1/13-7/11/13: $12,729,000gr. / 7,927,016sh. = $1.61/sh.

• Sold 7/12/13-7/31/13: $2,468,000gr. / 1,690,864sh. = $1.46/sh.

• Sold 8/1/13-9/9/13: $4,372,000gr. / 3,057,431sh. = $1.43/sh.

• Sold 9/10/13-10/31/13: $4,708,000gr. / 3,262,958sh. = $1.44/sh.

• Sold 11/1/13-12/6/13: NONE – see 10Q note below.

• Sold 12/7/13-1/31/14: $28,130,000gr. / 16,045,717sh. = $1.75/sh.

• Sold 2/1/14-4/30/14: $3,017,000gr. / 1,543,383sh. = $1.95/sh.

• Sold 5/1/14-7/31/14: $425,000gr. / 226,700sh. = $1.92/sh.

• Sold 8/1/14-10/31/14: $3,891,000gr. / 2,494,835sh. = $1.56/sh.

• Sold 11/1/14-1/31/15: $1,878,000gr. / 1,261,825sh. = $1.49/sh.

*Total Raised via MLV Dec’12 ATM Sales thru 10-31-2014:

. . .Before 7-10-17 1:7RS: $75,000,000gr. / 46,831,404 = $1.60sh.

. . .After 7-10-17 1:7RS: $75,000,000gr. / 6,690,200 = $1.21sh.

V. MLV 6-2014: “Jun’14 AMI Agreement – up to $25mm” http://www.mlvco.com

Form 424B5 filed 6-13-15: http://tinyurl.com/ycxje6pj

• Sold 11/1/14-1/31/15: $1,193,000gr. / 869,504sh. = $1.43/sh.

• Sold 2/1/15-3/12/15: $6,204,000gr. / 4,354,954sh. = $1.44/sh.

• Sold 3/13/15-4/30/15: $6,147,000gr. / 4,457,299sh. = $1.38/sh.

• Sold 5/1/15-7/14/15: $8,896,000gr. / 6,534,400sh. = $1.36/sh.

• Sold 7/15/15-7/31/15: $1,270,000gr. / 1,003,830sh. = $1.27/sh.

• Sold 8/1/15-9/9/15: $1,290,000gr. / 1,091,508sh. = $1.18/sh.

*Total Raised via MLV Jun’14 ATM Sales thru 9-9-2015:

. . .Before 7-10-17 1:7RS: $25,000,000gr. / 18,311,495 = $1.37/sh.

. . .After 7-10-17 1:7RS: $25,000,000gr. / 2,615,928 = $9.56/sh.

VI. MLV 8-2015: “Aug’15 AMI Agreement – up to $30mm” http://www.mlvco.com

Form 424B5 filed 8-7-15: http://tinyurl.com/oc53ugn

• Sold 8/7/15-9/9/15: $892,000gr. / 1,091,000sh. = $1.18/sh.

• Sold 9/10/15-10/31/15: $4,294,000gr. / 4,059,478sh. = $1.06/sh.

• Sold 11/1/15-12/10/15: $2,261,000gr. / 1,939,413sh. = $1.17/sh.

• Sold 12/11/15-1/31/16: *NO ATM SALES*, per 1-31-16 10Q iss. 3-9-16

• Sold 2/2/16-4/30/16: *NO ATM SALES*, per 4-30-16 10Q iss. 7-14-16

• Sold 5/1/16-7/14/16: $937,000gr. / 1,876,918sh. = $.50/sh.

• Sold 7/15/16-9/8/16: *NO ATM SALES*, per 7-31-16 10Q iss. 9-8-16

• Sold 9/9/16-10/31/16: $2,513,000gr. / 6,432,439sh. = $.39/sh.

• Sold 11/1/16-12/12/16: $1,174,000gr. / 3,788,346sh. = $.31/sh.

• Sold 12/13/16-1/31/17: $3,404,000gr. / 11,069,646sh. = $.31/sh.

• Sold 2/1/17-3/13/17: $7,335,000gr. / 15,308,300sh. = $.48/sh.

• Sold 3/14/17-4/30/17: $2,883,000gr. / 4,486,182 = $.64/sh.

• Sold 5/1/17-6/30/17: $4,307,000gr. / 7,358,806 = $0.59/sh.

. . .Before 7-10-17 1:7RS: $30,000,000gr. / 57,072,288 = $.53/sh.

. . .After 7-10-17 1:7RS: $30,000,000gr. / 8,153,184 = $3.68/sh.

VII. NOBLE 8-2015: “Aug’15 Eq.Dist. Agreement – up to $20mm” http://www.noblelsp.com

Form 424B5 filed 8-7-15: http://tinyurl.com/yazonjyw

• Sold 11/1/15-12/10/16: $2,371,000gr. / 1,925,844sh. = $1.23/sh.

• Sold 12/11/15-1/31/16: $2,857,000gr. / 2,529,434sh. = $1.13/sh.

• Sold 2/1/16-4/30/16: $1,741,000gr. / 4,017,010sh. = $.43/sh.

• Sold 5/1/16-7/14/16: $1,233,000gr. / 2,649,318sh. = $.47/sh.

• Sold 7/15/16-9/8/16: *NO ATM SALES*, per 7-31-16 10Q iss. 9-8-16

• Sold 9/9/16-10/31/16: $1,283,000gr. / 2,988,086sh. = $.43/sh.

• Sold 11/1/16-12/12/16: $496,000gr. / 1,587,909sh. = $.31/sh.

• Sold 12/13/16-1/31/17: $904,000gr. / 2,857,284sh. = $.32/sh.

• Sold 2/1/17-3/13/17: $6,006,000gr. / 11,273,296sh. = $.53/sh.

• Sold 3/14/17-4/30/17: $3,109,000gr. / 4,896,376sh. = $.63/sh.

. . .Before 7-10-17 1:7RS:$20,000,000gr. / 34,724,557 = $.58/sh.

. . .After 7-10-17 1:7RS:$20,000,000gr. / 4,960,651 = $4.03/sh.

TOTAL ALL A-T-M SALES – INCEPTION (3-2009) THRU 6-30-2017:

. . .Before 7-10-17 1:7RS: => $272,500,000gr. / 244,088,231sh. = $1.12/sh.

. . .After 7-10-17 1:7RS: => $272,500,000gr. / 34,869,747sh. = $7.81/sh.

= = = = = = = = = = = = = = = = = =

O/S WARRANTS & STOCK-OPTIONS A/O 7-31-2017 (10Q pgs. 13-14):

• WARRANTS: As of 7-31-17, warrants to purchase 39,040 shares at an exercise price of $17.29 were outstanding and are exercisable thru Aug30 2018. These warrants were issued in FY’13 in connection with the Aug.2012 [Oxford] loan agreement, which was paid in full Sept.2012.

• STOCK OPTIONS OUTSTANDING A/O 7-31-17: 4,022,136 shares at a wgt.avg. exercise price of $8.73.

- - - - - - - - - - - - - - - - -

Latest 10K 4-30-17 iss. 7-14-17 http://tinyurl.com/ycxu4l5n PR: http://ir.peregrineinc.com/releasedetail.cfm?ReleaseID=1033237 (Cash 4-30-17=$46.8mm)

Latest 10Q 7-31-17 iss. 9-11-17 http://tinyurl.com/ycbzp4zn PR: http://ir.peregrineinc.com/releasedetail.cfm?ReleaseID=1039958 (Cash 7-31-17=$37.3mm)

ALL SEC filings for PPHM: http://tinyurl.com/6d4jw8

10-13-16 ASM Voting Results: http://tinyurl.com/ycrrrb43

= = = = = = = = = = =PREFERRED STOCK:

2-5-14: PPHM Announces Public Offering of 10.5% Series E Convertible Preferred Stock http://tinyurl.com/lkxsna6

...2-11-14: PPHM Raises net $16.2mm selling 700k Preferred Shares with 10.5% div. at $25/sh, convertible to common at $3/sh http://tinyurl.com/jwmsnsk (8-K)

...6/14/14-7/14/13: PPHM Raises net $9.5mm selling 400k Preferred Shares with 10.5% div. at $25/sh, convertible to common at $3/sh http://tinyurl.com/mhva3k3 (4-30-14 10-K pg. F-34; $20mm gross remaining)

PREFERRED SHARES:

4-30-15 10K/p.F26: On 6-13-14, we entered into an At Market Issuance Sales Agreement with MLV, pursuant to which we may issue & sell shares of our Series E Preferred Stock through MLV, as agent, for gross proceeds of up to $30,000,000, in registered transactions from our Jan2014 Shelf. During FY’2015, we sold 799,764 shares of our Series E Preferred Stock at mkt prices for gross $19,205,000 before deducting commissions/costs of $1,002,000. As of 4-30-15, gross proceeds of up to $10,795,000 remained available under the Series E AMI Agreement.

NOTE: One of the holders of Preferred is KENNETH DART (EASTERN CAPITAL), who in a 2-13-15 SG14G ( http://tinyurl.com/k4nsfuu ) reported their 240,000sh. Preferred holdings as 2,000,000 common shares (SHARED VOTING POWER: 9,921,760,% OF CLASS REPRESENTED: 5.4%).

“which has a liquidation preference of $25.00/sh. and a conversion price of $3.00/sh.” 2,000,000 / 240,000 = 8.333

10Q: http://tinyurl.com/j2u2bjk

**7-31-16 10Q(iss. 9-8-16): 8/1/16-9/8/16, we sold 68,910sh. for gross=$1,601,000; a/o 9-8-16, $9,134,000 remained available.

**7-31-17 10Q(iss. 9-11-17): Preferred stock O/S at 7-31-17: 1,647,760

Known Upcoming Events, Large-Shareholders(35%), RONIN-PPHM HISTORY: updated 9-6-17 with PPHM announcing that Q1’FY18(q/e 7-31-17) 10Q/CC will be on Monday 9-11-17/after-hrs. Also, 9-9-17/ESMO’17 (SUNRISE Final Data) added to Known Events.

NOTE: RONIN/SWIM’s 8-29-17 PRELIM. Proxy Statement (14A) and PPHM’s 8-28-17 Amended 10-K were added previously – see below...

KNOWN UPCOMING:

Sep11/AfterHrs: FY'18Q1 (qe 7-31-17) Financials & Conf. Call http://ir.peregrineinc.com/releasedetail.cfm?ReleaseID=1039405

Sep8-12/ESMO’17(Madrid), PPHM Booth #257: Final SUNRISE Ph3 Data http://tinyurl.com/yb9kjutp

...Sep9 1:15pm Poster #1364P: “Final Clinical Results from SUNRISE: A Ph3 Trial of Bavi+Doce/Prev. Treated IIIb/IV NSCLC”. In an exploratory analysis of OS for pts who received subsequent ICI, mOS was not reached.

Sep25-28/Avid Booth #918: Informa’s BPI’17: BioProcess Intl. Conf. & Exhibition, Boston https://lifesciences.knect365.com/bioprocessinternational

Oct2/NCI Scientist Gregoire Altan-Bonnet(MSKCC ties), AACR’s Tumor Immunotherapy Conf., Boston http://tinyurl.com/y74v76go

...“Long-Lived Disruption of Inflammation Stems from the Catch-and-Release of Cytokines Mediated by Surface Phosphatidylserine in Tumors”

~Oct12: Peregrine's Annual Shareholder’s Meeting (2016 attendee reports: http://tinyurl.com/jx7ouay )

Dec11-15/Avid Booth #311: KNect365’s Antibody Eng. & Therapeutics Conf., SanDiego https://lifesciences.knect365.com/antibody-engineering-therapeutics

~Dec11: FY'18Q2 (qe 10-31-17) Financials & Conf. Call - http://ir.peregrineinc.com/events.cfm

Jan20-22 2018: Phacilitate’s Immunotherapy World Forum, Miami http://www.immunotherapyforum.com

...Jan18 12:30-12:45, Joe Shan(VP/Reg+Clin): “Turning up the Heat: PS-Targeting Antibodies Modulate the Tumor Microenvironment & Enhance Checkpoint Blockade”