News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

cjgaddy

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

COMPLETED BAVI PH.1/2 TRIALS ARCHIVED FROM iBox 7-16-17, and updated 2-3-18.

Now linked to from within iBox for perpetuity: http://investorshub.advfn.com/boards/show_ibox.aspx?boardid=2076

BAVITUXIMAB SOLID CANCERS PHASE1+2 TRIALS:

==> PR=Partial-Resp(30-99% Red.), SD=Stable-Disease(29% Red.-19% Incr.), OR=Obj-Resp(PR+CR)

6-2012: FTM's charts of MOS Data from CtlArms(chemo) of Comp.Trials for 1NSCLC 2NSCLC PANCRE trials http://tinyurl.com/757plm7

11-25-11: Comp. of Bavi+Chemo vs. Avastin & Chemo-Only in 3 completed Ph.2 single-arm trials (ABC/2 & NSCLC): http://tinyurl.com/79b3jcj

O. 6th IST Trial: Bavi+Ipilimumab(Yervoy) vs. Adv.Melanoma (Ph1b, random, open-label, 2arms, n: 24=>3)

Protocol (UTSW): http://www.clinicaltrials.gov/ct2/show/NCT01984255 (PI: Dr. Arthur Frankel - see "Researching for Cures" http://youtu.be/0zLAxjFny5Q )

UTSW's listing: http://www.utsouthwestern.edu/research/fact/detail.html?studyid=STU%20102013-007

…Note: Ipilimumab = BMS’s “Yervoy” (anti-CTLA-4) http://www.yervoy.com

...11-10-15: UTSW chgd. ClinicalTrials to NO LONGER RECRUITING, Actual-Pts: 3

...12-10-15: “Due to newly-appr. therapies & chgs in SOC [ex: Keytruda/Opdivo: less-side-effects], enrollment recently stopped by UTSW.”; http://tinyurl.com/jkp885g

...4-23-14: Bavi+Yervoy IST trial initiated: http://tinyurl.com/km7krcm

N. 5th IST Trial (Bavi+Capecitabine+RAD) vs. Rectal Cancer (Ph1, open-label, 1arm, n=18)

Protocol: http://www.clinicaltrials.gov/ct2/show/NCT01634685

...Note: Capecitabine (prodrug of 5-FU) = Roche/Genentech's Xeloda - see http://www.xeloda.com

...7-31-17/Jrnl-Clin-Oncol(UTSW): Phase I update http://www.redjournal.org/article/S0360-3016(15)01602-8/fulltext

“There is interest in improving the tumoricidal effects of preoperative radiotherapy for rectal carcinoma by studying new radiosensitizers. The safety & toxicity profile of these combination regimens needs rigorous clinical evaluation. The primary objective of this study was to evaluate the toxicity of combining bavituximab, an antibody that targets exposed phosphatidylserine, with capecitabine, and radiation therapy. Patients with stage II/III rectal adenocarcinoma were enrolled on a phase I study combining radiation therapy, capecitabine, and bavituximab. A std. 3+3 trial designed was used. In general, bavituximab was safe & well tolerated in combination with radiation therapy & capecitabine in the treatment of rectal adenocarcinoma. To date, there are 8 evaluable patients, 3 at each of the 1st two dose levels and 2 at the 3rd and highest dose level. One patient at the highest dose level experienced a grade III infusion reaction related to the bavituximab. Of the 7 patients who have proceeded to surgery, 1 patient's tumor demonstrated a pathologic complete response. Bavituximab is safe in combination with capecitabine & radiation therapy at the doses selected for the study. Further clinical investigation would be necessary to better define the efficacy of this combination… Trial enrollment continues at the 3 mg/kg dose level. Toxicities have been relatively mild to date...”

...11-1-15/RadiationOncology – prelim. results/8 evaluables http://tinyurl.com/q3wey2b

…...”Of the 7 pts that proceeded to surgery, 1 demonstrated a pathologic complete response.”

...7-16-12: IST (Rectal) initiated at UTSW (PI=Jeffrey Meyer), ~18 patients - http://tinyurl.com/cr29l6k

M. Tumor Imaging & Dosimetry trial of I124-PGN650 (FH-Bavi) in Adv. Solid Tumors (Ph0, open-label, 1arm, n: 12=>11)

Protocol: http://clinicaltrials.gov/ct2/show/NCT01632696

..."I124-PGN650 is the Fab end of PS-targeting mab PGN635 (FH-Bavi) joined to the PET imaging radioisotope iodine-124, a new approach to imaging cancer."

...10-2017/Mol-Imag: Results of Human Testing (n=11) of 124I-PGN650 PET Imaging http://tinyurl.com/y9ofyu8o

...”Tumor targeting in Pts was less than prev. observed in animal studies… tumor uptake was quite low & not sufficient for clinical studies.”

...5-1-15: Interim Results/8pts (Jrnl Nuclear Med, vol56 suppl#3) http://jnm.snmjournals.org/content/56/supplement_3/1033

…”124I-PGN650 is safe and results in acceptable dosimetry and needs further optimization as an imaging agent based on the level of increased tumor uptake on PET/CT”

...6-28-12: Trial added to Trials.gov, 1st site "recruiting" (Wash.UnivSM/St.Louis)

…4-3-12: Peregrine Launches PS-Targeting Clinical Imaging Pgm (AACR'12 #2452) http://tinyurl.com/7p7jovt & http://tinyurl.com/7yrwqm7

L. 4th IST Trial (Bavi+Cabazitaxel vs. 2nd-Line PROSTATE(CRPC) Cancer, open-label Ph.1B/IIA) *CANCELLED due to chg. in SOC Drugs*

Protocol: http://clinicaltrials.gov/show/NCT01335204 (CRPC=Castration-Resistant Prostate Cancer)

...Note: Cabazitaxel = Sanofi-Aventis' Jevtana - see http://www.jevtana.com

...3-12-13: CRPC IST cancelled (Slow-Enroll/2 New SOC Drugs): http://tinyurl.com/c48osut

...5-25-11: IST (Prostate) initiated at UCI -> moved ot Med.Univ.SCar (PI: Michael Lilly), ~31 patients - http://tinyurl.com/3mtvdvl

K. 3rd IST Trial (Bavi+PemCarbo vs. Frontline NSCLC, open-label Ph.1B, n=25)

Protocol: http://clinicaltrials.gov/ct2/show/NCT01323062

…10-30-14: Interim data n=23, MSTO’14: MOS=12.2mos (hist-ctl ~10mos), PFS=4.8mos, ORR=35% http://tinyurl.com/mll62c6

...9-9-14: Stage IV NSCLC IST Enrollment complete. http://tinyurl.com/ktrfswj

...4-2012: Clinicaltrials.gov shows 2nd site added: Univ. of Pittsburg (PI=Liza Villaruz, MD)

...4-2-12 AACR'12: "5pts. to-date, 3 have PR's" http://tinyurl.com/7yrwqm7 (see #1744)

...3-8-11: IST (NSCLC) initiated at UNC (PI= J.Grilley-Olson), ~25 patients - http://tinyurl.com/6b926ku

J. 2nd IST Trial (Bavi+Paclitaxel(Taxol) vs. Her2- Met. Breast Cancer, open-label Ph.1, n=14)

Protocol: http://clinicaltrials.gov/ct2/show/NCT01288261

...3-31-15/A.Stopeck article(Ph1 data) “Cancer-Medicine” N=13: PFS=7.3mos, ORR=85%, 2 CR's http://tinyurl.com/nm5oog4

…6-3-13: ASCO’13/interim data, n=14: ORR=85%, 2 CR’s (15%) http://tinyurl.com/kq3uv4e

...4-29-13: Enrollment complete. http://tinyurl.com/cqrup9e

...4-3-12 AACR'12: "5pts. to-date, 2 CR's, 1 PR" http://tinyurl.com/7yrwqm7 (see #4404)

...1-19-11: IST (Her2- MBC) initiated at Arizona CC (PI=A.Stopeck), ~14 patients - http://tinyurl.com/5t7zomn

I. Phase II Bavi+GEM vs. Front-Line Adv. PANCREATIC (randomized, unblinded, n=70)

Protocol: http://www.clinicaltrials.gov/ct2/show/NCT01272791 (15 U.S. + 4 Ukraine = 19 as of 6-7-2012)

…1-22-13: FTM's post of 13 Ph3 Gem+Treatment Pancreatic Trials ('02-'13) - Mean MOS: GEM=6.4mos., GEM+TR=7.3mos. http://tinyurl.com/al99hx9

......Another FTM Pancreatic Phase3 trials table showing HR's, P-Values, and ORR% stats: http://tinyurl.com/btzkw4l

…6-3-13 ASCO’13/final data: n=70, Ctl=>Bavi MOS 5.2=>5.6mos, ORR 13%=>28% HR=.75 http://tinyurl.com/kq3uv4e

......Promising ‘immuno-indicative’ 1yr SURVIVAL results: GEM-Only(n=31): 0%, Bavi+GEM(n=32): 24.5% - see: http://tinyurl.com/lz5yg4f

...2-13-13 Topline Data: “Bavi+Gem resulted in more than a doubling of ORR” http://tinyurl.com/aqny7ny

...6-25-12: Enrollment complete. http://tinyurl.com/72tvnfj

...6-20-12: Early data (cutoff=6/6/12 bavi=15 ctl=17) presented at AACR Pancreatic Conf. http://tinyurl.com/77m9fw2

...1-5-11: U.S. Ph.2 randomized trial initiated http://tinyurl.com/26hnuzv "up to 70 front-line patients at ~10 clinical sites."

H. 1st Investigator-Sponsored (IST) Ph.I/II Trial (Bavi+Sorafenib vs. Liver Cancer/HCC, open-label, n=9+38=47)

...Note: Sorafenib = Onyx/Bayer's Nexavar - see http://www.nexavar.com

Protocol: http://clinicaltrials.gov/ct2/show/NCT01264705 UTSW: http://tinyurl.com/mwdc2ql (5 sites: 3/UTSW, Parkland-Hosp, Dallas/VA, PI=Dr. Adam Yopp)

...3-25-15: Dr.Adam.Yopp(UTSW) Oral-pres./SSO (Liver-IST/Ph2-data) http://tinyurl.com/opkh5qy N=38(79%HepC, ECOG/0=34%): MTTP=6.7mos, MOS=6.1, MDSS=8.7, DCR=58%

...1-16-15 ASCO Gastro-Symposium: Ph.2 data/n=38 (Adam Yopp), “These clinical outcomes of TTP=6.7/DCR=58%/PFS=4mo are quite encouraging…” http://tinyurl.com/m9uz9mo

...11-8-14 SITC'14: Ph.2 Correlative Studies data (biopsies B4/After) on 6pts, incl. KOL Dimitry Gabrilovich’s comments: http://tinyurl.com/pchzr6h

...9-9-14 Enrollment complete. http://tinyurl.com/ktrfswj (ph2=38 Ph1=9)

...4-4-12 AACR'12: Dr. Adam Yopp, "promising safety profile to-date" http://tinyurl.com/7yrwqm7 (see #5591)

...Feb'12-Sep'14 10+ times: CEO Steve King hints of future ex-US partner-driven Bavi+Sorafenib/LIVER trial in Asia-Pacific: http://tinyurl.com/nkaxtcc

......Articles & Data describe Liver Cancer challenges in Asian populations: http://tinyurl.com/7z7o8j9 & http://tinyurl.com/7z99cy4

...12-1-10: PPHM's 1st IST (Liver Cancer) initiated at UTSW, ~56 patients - http://tinyurl.com/3xd3e6c

…Per S.King, 5-18-10/R&R, "We've had a lot of interest in running clinical trials with the compound from investigators who have either had prior experience with the drug or would like to study the drug in various settings. Potential IST indications include all the major solid tumor types. Of particular interest is Liver Cancer, in which we have a natural tie-in with our HCV program, Ovarian Cancer & Pancreatic Cancer, also very nicely supported by the prior data."

G. Phase IIb Bavi+PC vs. Front-Line NSCLC (randomized, unblinded, 'confirmatory', n=86)

Protocol: http://clinicaltrials.gov/ct2/show/NCT01160601 (17 U.S. + 9 India + 2 RepGA + 7 RussianFED + 5 Ukraine = 40 as of 8-12-11)

...Also listed in: India's CTRI registry http://tinyurl.com/ljg7aad and WHO's registry http://tinyurl.com/kcp4z89

...6-27-13: Bavi+CP MOS>14mos (“with < 60% of survival events”) http://tinyurl.com/pmcgsgp

…”with less than 60% of survival events, while the Bavi+CP arm currently demonstrates a MOS > 14mos, there was not a meaningful enough diff. in survival between the 2 arms that would support the advancement of this combination. Full results will be presented at a future sci. meeting or thru pub.”

...5-7-13: FTM's Table of 20 prev. Ph.3 Trials in 1st-Line NSCLC (ctl=CP), MOS & HR results (Note Avastin improved CP-Only by 19%): http://tinyurl.com/cho7o29

...3-9-12: Topline ORR & PFS Data (Bavi+PC vs.PC-only) http://tinyurl.com/7m9r6ya

…...LOCAL reads: ORR/32%-31% PFS/5.8-4.6mos , CENTRAL reads: ORR/25%-23% PFS/6.7-6.4mos

...12-6-11 Prelim. Data (n=86, 100% Stage IV's) => ORR=39%, PC/alone=25%: http://tinyurl.com/7ph4tty

......Comp. vs. Avastin+PC/Ph3/n=417(74% Stage IV's): ORR=35% (Sandler/E4599/2006 http://www.nejm.org/doi/pdf/10.1056/NEJMoa061884 )

...9-8-11: Enrollment complete. http://tinyurl.com/3vv9zfx

...7-14-11/CC: Enrollment was taking longer than expected; have amended protocol; expanding to 30+ sites, expect enroll. comp. "in coming weeks", interim data by Yr-end'11. http://tinyurl.com/6k6y2as

…7-14-10/CC, J.Shan (VP/Clin+RegAffairs): "This trial is intended to confirm in a randomized setting the results from our Ph.2 signal-seeking NSCLC trial which showed 43% ORR, more than double the generally accepted chemo ORR of under 20% in numerous publications. Favorable results could then lead to an end of Ph.2 meeting with the FDA, with possibly a pivotal Ph/3 trial for front-line lung cancer, our 2nd potential regulatory pathway for bavituximab."

...7-14-10: U.S. Ph.2b randomized trial initiated http://tinyurl.com/27kxksl

……up to 86 front-line patients at ~20 clinical sites; goal: enrollment comp. by mid'11.

F. LEAD IND: Phase IIb Bavi+Doce vs. 2nd-Line NSCLC (randomized, double-blinded, placebo-ctl'd, n=120, 'registrational')

Protocol: http://clinicaltrials.gov/ct2/show/NCT01138163 (24 U.S. + 15 India + 2 RepGA + 7 RussianFED + 5 Ukraine = 53 as of 8-12-11)

Enrolled Oct2010 - Oct2011 at 40 global sites (per J.Shan 9-7-12 webcast (http://tinyurl.com/8cn87la )

8-2012: Compare Bavi+Doce's MOS=11.7mos (Bavi/3mg) to the 4 Curr-Approved 2Line/NSCLC Drugs http://tinyurl.com/cgnkvpa

• Taxotere/docetaxel => MOS=6.3mos (meta-analysis of 5 trials, 865 pts)

• Altima/pemetrexed => No diff. vs. Docetaxel (Ph.3 non-inferiority vs. Doce, 571 pts)

• Tarceva/erlotinib => MOS=5.3mos (TITAN Ph.III n=424 trial - see http://tinyurl.com/8w8lo93 )

• Iressa/gefitinib => "Iressa does not improve OS"

2-19-16/Clin-Lung-Cancer-Jrnl: Ph2 Final Data, Dr. David Gerber et al http://tinyurl.com/z5a7fwu

9-8-15: CMS SETTLEMENT EXECUTED (CSM pays PPHM only $600k for their “breach of contract, negligence & constructive fraud”, due to “limitation of liability contract clauses”) http://tinyurl.com/pemub47 (10Q/pg.17)

6-23-14: PPHM files Opposition to CSM’s Motion For Partial Summary Judgment - excerpts: http://tinyurl.com/q8xwd4v

. . .Declaration of Joseph Shan (VP/Clin+RegAffairs): http://tinyurl.com/kdgllxn

. . .Declaration of Jeffery Masten (VP/Quality): http://tinyurl.com/oru9p5q #6: “up to 25%" of CTL had 1mg, and “up to 25%" of 1mg had CTL(DoceOnly).

3-28-14: Peregrine files 1st Amended Complaint vs. CSM (13pgs) http://tinyurl.com/lsgf5lz

...Pg6: ”[as of 4-15-10], CSM had already secretly & unilaterally swapped the A & B arms so that those patients that were randomized in the A arm (CTL) and supposed to receive placebo treatments, were actually receiving 1MG Bavi treatments, and vice-versa. Peregrine’s Fall’12 investigation revealed that CSM committed other labeling & distribution errors affecting the A & B arms above & beyond the swap of the A& B arms noted above.”

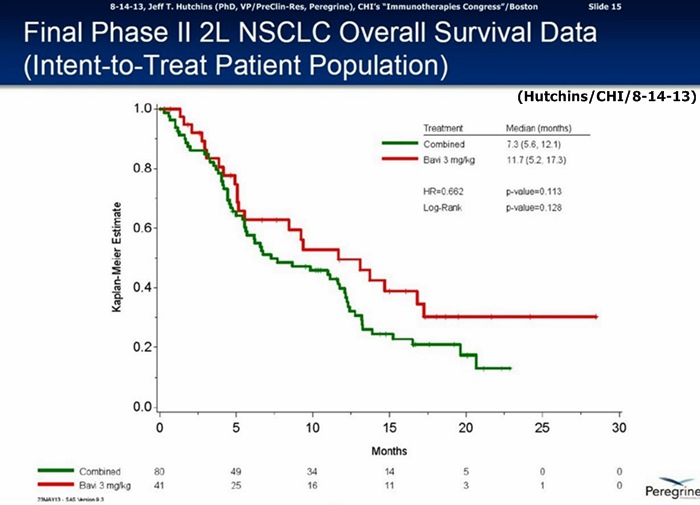

6-3-13/ASCO’13: Final Data Ph.II 2L/NSCLC http://tinyurl.com/my8qxw7

…60% improvement in MOS: Bavi/3mg=11.7mos. vs. 7.3mos. for CTL-arm(combined Bavi/1mg + DoxyOnly arms), HR=.662, P=.113

5-20-13: FDA Approves Bavituximab Ph.III Design for 2L/NSCLC; 600-pt trial to begin by y/e’13 http://tinyurl.com/n3dxtm6

...S.King: “We will now focus on starting the Ph.III trial while continuing ongoing partnering discussions.”

…R.Garnick: “This was a highly collaborative effort with the FDA; this trial, when combined with Bavi’s supporting data to date, could be sufficient to support a future BLA submission."

2-19-13: Topline Data Update from 2nd-Line NSCLC Trial after data discrepancies review http://tinyurl.com/ansqcea

…60% improvement in MOS: 3mg=11.7mos. vs. 7.3mos. for CTL-arm(combined 1mg & Doxy+placebo arms), HR=.73, p=.217

6-5-13: FTM's table of MOS data in 15 prior Doxy 2nd-Line NSCLC trials (Bavi's 60% MOS Improvement is Tops) http://tinyurl.com/m886ctb

1-25-13: MLV's George Zavoico recaps 2ndLine/NSCLC data errors & current status of PPHM's review http://tinyurl.com/b9u4pk8

...GZ: "This means that patients randomized into the high dose arm were administered Bavi correctly, whereas some of the patients in the placebo arm were administered low dose Bavi and some in the low dose Bavi arm were administered placebo. More importantly, the findings suggested that the MOS of 13.1 mos. in the high dose arm was likely to be valid. Even by historical measures, this is a remarkable result, since docetaxel's product insert lists the MOS of NSCLC patients receiving this widely used drug as 2nd-Line therapy in 2 trials as 5.7 & 7.5 mos. In effect, adding Bavi doubled the MOS. In our view, this was an extraordinary stroke of luck. If the high dose arm had been affected by the coding discrepancy, Peregrine would have been in a completely different & unfortunate position… Moreover, Peregrine must determine how best to present its case to the FDA. Will the historical controls be sufficient to justify moving Bavi into a Phase III pivotal trial, or will Peregrine have to pool the results of the placebo & low-dose arms and use that as a comparator to argue for moving ahead? A simple average of the placebo & low-dose arms results in a new control MOS of about 8.4 mos., still several months less than that of the high dose arm. This quick analysis results in about a 5-mo. survival advantage, a substantial prolongation for patients with second-line NSCLC and likely to justify moving Bavi into a pivotal Phase III trial in 2013, in our view."

1-7-13 PPHM PR - Review Update: "discrepancies are isolated to the placebo and 1 mg/kg arms; no evidence of discrepancies in the 3 mg/kg arm… Peregrine is taking a very conservative approach toward analyzing the results by combining the placebo & 1mg/kg arms into one treatment arm (control arm), and comparing to the 3mg/kg arm. This analysis indicates that the 3 mg/kg arm continues to show favorable TRR's, PFS, and OS over the new combined control arm. Peregrine expects to announce more detailed results from the analysis in the near term when it is completed." http://tinyurl.com/asup54d

9-24-12: Major Discrepancies found in 2nd-Line NSCLC Ph.2B Treatment Group Coding by Indep. 3rd-Party Vendor CMS/FargoND http://tinyurl.com/8r9zcqy

…"Investors should not rely on clinical data that the company disclosed on or before Sept. 7, 2012 from its Ph.2 Bavi trial in patients with 2nd-Line NSCLC or any presentations or other documents related to this Ph.2 trial."

9-24-12: Peregrine sues CSM Over Bavi Ph.2B 2nd-Line NSCLC Clinical Trial Mix-Up http://tinyurl.com/8fpgngu

…CSM = Clinical Supplies Management Inc., Fargo ND http://www.csmondemand.com

...1-17-13: Peregrine's lawsuit against CSM for "breach of contract & negligence" SERVED http://tinyurl.com/a7zrgys

…9-10-12 CEO Steve King, QtlyCC ( http://tinyurl.com/8nkwrml )

……"These are truly remarkable results (statistically doubling MOS) that are not only great for the pgm… but also great news for the NSCLC patients in the trial…"

…9-10-12 Robert Garnick (Head/Reg), QtlyCC ( http://tinyurl.com/8nkwrml )

……"The NSCLC data we announced 9-7-12 has far exceeded our expectations, and I hope that you're as excited as I am with bavituximab's potential. I feel strongly that Peregrine should be recognized for having the corporate courage to conduct the rigorous, randomized placebo-controlled Phase II trial that provided these robust data and that provide the basis for us to plan for a pivotal Phase III program."

...9-7-12: PPHM Press Release about Dr. Gerber's plenary at ASTRO/Thoracic/Chicago: http://tinyurl.com/96wrrso

…"The interim data showed a statistically significant improvement in OS (Hazard Ratio 0.524, p-value .0154) and a doubling of MOS (11.1/13.1mos. vs. 5.6mos.) in the Bavituximab-containing arms compared to the [Docetaxel] ctl-arm."

......VP Joe Shan's 15min. Webcast & Slideshow recapping Dr. David Gerber's 9-7-12 ASTRO/Chicago Plenary: http://tinyurl.com/96wrrso

…8-15-12 CEO Steve King, Wedbush/NYC ( http://tinyurl.com/8mhrtld )

......"As we're sitting here today, we have still not reached the # of events for MOS in either of the Bavituximab arms - and, in fact, we still have patients that are on treatments." Q&A: "it's going to be a very positive MOS result, it's just a matter now of magnitude."

…7-16-12 CEO Steve King, QtlyCC ( http://tinyurl.com/cs7spbz )

......"The strength of this 2nd-Line NSCLC data (esp. MOS trends) in this large area of high unmet medical need has also sparked a surge in partnering discussions that has included over 15 in-person partnering meetings since that time with major players in oncology, with all discussions ongoing and addl. parties showing interest. Our goal for the program is to position ourselves, along with a potential partner, to initiate Ph3 by mid-2013, which means an EOP2 meeting by yr-end'12. It would be ideal to have a partner on board to participate in the EOP2 meeting, and we have communicated this to interested parties and they agree."

…7-16-12 Robert Garnick (Head/Reg), QtlyCC ( http://tinyurl.com/cs7spbz )

……"We've been working very hard and very actively on the next steps in our Bavi 2nd-Line NSCLC pgm, given the favorable data that we've seen. As you can imagine, with data like this, there are many things that we need to consider. One consideration is that, should the data continue to trend the way it is, particularly in survival, this opens a door for potential discussions around a pathway for Accelerated Approval. At this point, all options are being considered, with Peregrine working towards the most efficient path forward from a regulatory standpoint." Q&A: "…all in all, I think the data is extremely compelling and I think it makes a really good case. Certainly, I think, I've seen a lot of Ph2 & Ph3 data, and this is as compelling Ph2 data as I've ever seen. So, I'm very comfortable proposing a meeting with the FDA for Q4'12."

…7-12-12 CEO Steve King, JMP-Conf/NYC ( http://tinyurl.com/csdclwb )

……"Re: 2nd-Line/NSCLC trial, the most thrilling thing is the fact that, even though we'd reached MOS for the ctl-arm(Doce) at end of Apr'12 of LESS THAN 6MOS, the majority of patients are still alive (today) in both Bavi arms, and we expect that to continue for some period of time still. Ph3 planning is underway already; our goal is to start this Ph3 by mid'13, meaning an EOP2 meeting with the FDA in Q4'12; our goal is to bring a partner on board, ideally in time for that EOP2 meeting, certainly before the beg. of the Ph3 trial."

…5-21-12: TopLine data n=117 for Bavi/3mg+Doce arm: ORR=17.9%/PFS=4.5mos (vs. CTL 7.9%/3mos) http://tinyurl.com/73aeyxj

......Importantly, MOS for CTL-arm "< 6 mos", but not yet reached in both Bavi arms.

...10-6-11: Enrollment complete. http://tinyurl.com/3m9re39

...7-14-11/CC: Enrollment was taking longer than expected; have amended protocol; expanding to ~45 sites, expect enroll. comp. "early in Q4/2011", data unblinding 1H'12. http://tinyurl.com/6k6y2as

…3-17-10/Roth, CEO S.King: "We refer to this trial as a Registrational Phase II Study, because we believe that if we have results anywhere near approaching what we saw in the earlier [India] study, it could be a conduit for Accelerated Approval."

...6-4-10: Ph.2b randomized reg. trial Open for enrollment: http://tinyurl.com/25v22qk

……"up to 120 refractory patients at ~30 clinical sites; goal: fully-enroll by mid'11, topline data by y/e'11."

1st 5 COMPLETED BAVI CANCER TRIALS:

These 5 completed Ph.1 & Ph.2 Bavituximab Cancer Trials archived to: http://tinyurl.com/72dnkfg

1. Ph.1A Bavi/Mono vs. Solid Cancers (USA n=26, 6/2005-6/2009)

2. Ph.1B Bavi+Chemo vs. Solid Cancers (India n=12, 11/2006-5/2007)

3. Ph.2 Bavi+Doce/BREAST/Refractory (RepGA n=46, 1/2008-5/2009): ORR=61%(Her2+=86%), PFS=7.4mos, MOS=20.7mos *

4. Ph.2 Bavi+PC/BREAST/Frontline (India n=46, 8/2008-9/2009): ORR=74%(Her2+=100%), PFS=6.9mos, MOS=23.2mos %

5. Ph.2 Bavi+PC/NSCLC/Frontline (India n=49, 6/2008-10/2009): ORR=43%, PFS=6.1mos, MOS=12.4mos #

......* BAVI+DOCE/Refract-MBC N=46: Compare *MOS=20.7mos to 11.4mos for Doce/alone (Nabholtz/JCO1999 Ph3/n=203 http://tinyurl.com/3rxqqtk )

......% BAVI+PC/FrontLine-MBC N=46: Compare %MOS=23.2mos to 16.0mos for P+C/alone (Loesch/JCO2002 Ph2/n=95 http://tinyurl.com/6wazs9p )

......# BAVI+PC/Frontline-NSCLC N=49: Compare #MOS=12.4mos to P+C/alone=10.3, Avastin+PC=12.3 (E4599/n=434), achieved using less Chemo (175-v-200 & AUC5-v-AUC6), treating 16% (8/49) more-difficult Squamous in Bavi trial (excluded totally from E4599), and treating higher % of sicker ECOG1 pts than in E4599 (96%-v-60%). See 6-15-11/PR http://tinyurl.com/3fcz5ok , ASCO'10 http://tinyurl.com/2g5cqof , and a discussion of differentiating factors between patient demographics & baselines treated in the 2 trials: http://tinyurl.com/6k5uuf7 .

EMAIL ADDY you PM'd doesn't work: RESEND pls.

DELETE

5 Events Added to AvidBio.com (March-Sept)

Mar 19–22 2018 - BioProcess Intl. West Conf., SanFran

Mar 19–22 2018 - DCAT Week, NYC

Jun 4–7 2018 - BIO Intl. Convention, Boston

Aug 13–17 2018 - The Bioprocessing Summit, Boston

Sep 4–7 2018 - BioProcess Intl. Conf. & Exhibition, Boston

https://avidbio.com = > http://ir.avidbio.com/events.cfm

= = = = = = = = =

EARLIER R.LIAS PRESENTATIONS:

1-29-18/Roger Lias: NobleCon14, Ft.Laud. - Webcast Replay: https://tinyurl.com/yanwk9yo

...Slide4/2:26 COMPLETED KEY ELEMENTS OF TRANSITION: “...We are currently seeking to monetize the R&D assets, the remainder, some residual value we believe, and we hope to have news on that front very soon, and obviously that represents potential upside for stockholders over the short term.”

...Slide15/10:13 NEAR-TERM PLANS FOR GROWING THE BUSINESS: “...We are expanding our sales & marketing. As I mentioned before, we haven’t been, for several years really, selling at all; there hasn’t been a need for it. So suddenly we’ve had to take that on, and I’m pleased to report that we’re already showing, really, tremendous progress in that area, and I hope we’ll have some announcements soon about several new clients.”

1-18-18: ASM2017 (@Myford Facility) - Roger Lias’ Slideshow & Attendee Reports https://tinyurl.com/yca6enbr PROXY/14A: https://tinyurl.com/y7qprpg9

1-8-18/Roger Lias: EBD's Biotech Showcase 2018 (parallel w/JPM Conf.), SanFran - Slideshow: https://tinyurl.com/ya6tgxxa

12-11-17: Qtly. Conf. Call (Lias/Lytle) Transcript https://tinyurl.com/ybycb2s6

...Dr. Lias, "the company is undergoing a broad-scale transformation, the goals of which are to shift complete focus to the Avid Bioservices CDMO business and the complete divestiture of all of Peregrine's legacy R&D assets, which include bavituximab."

FULL HISTORY of PPHM-Ronin PR’s, Letters, 13-D’s, Form4’s, Proxy’s, etc: https://tinyurl.com/ycb3fpfm

1-29-18/NobleCon14: Roger Lias Presentation Webcast Link (20mins/24 Slides)

Jan29 2018: “NobleCon14 – Noble Financial’s 14th Annual Inv. Conf.”, Ft.Laud.

Conf. website: http://nobleconference.com

11:30amET: Roger J. Lias, PhD: Corporate presentation

WEBCAST Link - 20mins/24 Slides:

http://noble.mediasite.com/mediasite/Play/a4bbd41fda0d41ab9be7504f2a8eb7901d

http://ir.avidbio.com/events.cfm

Slide4 “Completed Key Elements of Transition”

2:26/RL: “...We are currently seeking to monetize the R&D assets, the remainder, some residual value we believe, and we hope to have news on that front very soon, and obviously that represents potential upside for stockholders over the short term.”

Slide15 “Near-term Plans for Growing the Business”

10:13/RL: “...We are expanding our sales & marketing. As I mentioned before, we haven’t been, for several years really, selling at all; there hasn’t been a need for it. So suddenly we’ve had to take that on, and I’m pleased to report that we’re already showing, really, tremendous progress in that area, and I hope we’ll have some announcements soon about several new clients.”

= = = = = = = = =EARLIER R.LIAS PRESENTATIONS:

1-18-18: ASM2017 (@Myford Facility) - Roger Lias’ Slideshow & Attendee Reports https://tinyurl.com/yca6enbr PROXY/14A: https://tinyurl.com/y7qprpg9

1-8-18/Roger Lias: EBD's Biotech Showcase 2018 (parallel w/JPM Conf.), SanFran - Slideshow: https://tinyurl.com/ya6tgxxa

12-11-17: Qtly. Conf. Call (Lias/Lytle) Transcript https://tinyurl.com/ybycb2s6

...Dr. Lias, "the company is undergoing a broad-scale transformation, the goals of which are to shift complete focus to the Avid Bioservices CDMO business and the complete divestiture of all of Peregrine's legacy R&D assets, which include bavituximab."

FULL HISTORY of PPHM-Ronin PR’s, Letters, 13-D’s, Form4’s, Proxy’s, etc: https://tinyurl.com/ycb3fpfm

CEO Roger Lias 11:30amET/NobleCon14: VIDEO TOMORROW

Jan29 2018: “NobleCon14 – Noble Financial’s 14th Annual Inv. Conf.”, Ft.Laud.

Conf. website: http://nobleconference.com

11:30amET: Roger J. Lias, PhD: Corporate presentation

Delayed Webcast (24hrs later):

=> http://noble.mediasite.com/mediasite/Play/a4bbd41fda0d41ab9be7504f2a8eb7901d

http://ir.avidbio.com/events.cfm

Received by DovePress Sept. 6, 2017

Pub. 1-23-18/DovePress: “Antibody Targeting of Phosphatidylserine for the Detection & Immunotherapy of Cancer”

Rec: 9-6-17, Acc: 10-27-17, Pub: 1-23-18 (14 pgs.)

Olivier Belzile 1 Xianming Huang 2,3 Jian Gong 2,3 Jay Carlson 2,3 Alan J Schroit 1 Rolf A Brekken 1 Bruce Freimark 2,3

1 Hamon Center for Therapeutic Oncology Res.s, UTSW/MC/Dallas

2 Dept of Preclinical Res., Peregrine Pharm.

3 Dept of Antibody Discovery, Peregrine Pharm.

https://investorshub.advfn.com/boards/read_msg.aspx?message_id=137906812

Updated w/Table3, History of Bavi Human Cancer Trials

1-23-18: New Dovepress article by UTSW+PPHM on PS-Targeting immunotherapy for cancer, concluding that, “targeting exposed PS in the tumor microenvironment may be a novel approach to enhance immune responses to cancer”. Gives a history of PS-Targeting (Bavituximab), both pre-clinical studies and human trials to date. For SUNRISE, for Results (Table 3), it says, “Manuscript in preparation”.

1-23-18/DovePress: “Antibody Targeting of Phosphatidylserine for the Detection & Immunotherapy of Cancer”

Rec: 9-6-17, Acc: 10-27-17, Pub: 1-23-18 (14 pgs.)

Olivier Belzile 1 Xianming Huang 2,3 Jian Gong 2,3 Jay Carlson 2,3 Alan J Schroit 1 Rolf A Brekken 1 Bruce Freimark 2,3

1 Hamon Center for Therapeutic Oncology Res.s, UTSW/MC/Dallas

2 Dept of Preclinical Res., Peregrine Pharm.

3 Dept of Antibody Discovery, Peregrine Pharm.

https://www.dovepress.com/antibody-targeting-of-phosphatidylserine-for-the-detection-and-immunot-peer-reviewed-article-ITT

ABSTRACT:

Phosphatidylserine (PS) is a negatively charged phospholipid in all eukaryotic cells that is actively sequestered to the inner leaflet of the cell membrane. Exposure of PS on apoptotic cells is a normal physiological process that triggers their rapid removal by phagocytic engulfment under noninflammatory conditions via receptors primarily expressed on immune cells. PS is aberrantly exposed in the tumor microenvironment and contributes to the overall immunosuppressive signals that antagonize the development of local and systemic antitumor immune responses. PS-mediated immunosuppression in the tumor microenvironment is further exacerbated by chemotherapy & radiation treatments that result in increased levels of PS on dying cells & necrotic tissue.

Antibodies targeting PS localize to tumors and block PS-mediated immunosuppression.

Targeting exposed PS in the tumor microenvironment may be a novel approach to enhance immune responses to cancer.

LINK TO FULL PDF (14pgs): https://www.dovepress.com/getfile.php?fileID=40225

CONCLUSION:

PS is well-recognized as a cell surface marker of apoptotic cells which provides signals to specific receptors for noninflammatory efferocytosis by phagocytes. The same signals are usurped in the tumor microenvironment by the exposure of PS on tumor blood vessel endothelium and tumor cells, contributing to immunosuppression and tolerance of tumor growth. Specific receptors that bind PS, including TIMs and TAMs, on immune cells and tumors, trigger these immunosuppressive pathways. The uptake of PS-targeting antibodies by tumors is readily demonstrated in preclinical models and initial clinical studies. Multiple preclinical studies serve as proof of concept that the antibody-mediated blockade of PS in tumors can reactivate innate & adaptive immune responses in the tumor microenvironment. A combination of PS-targeting antibodies with approved immune activating therapies such as chemotherapy, radiation, and immune checkpoint inhibitors (including antibodies targeting CTLA-4, PD-1, and PD-L1) and with novel therapies such as oncolytic viruses has the potential to treat a variety of different tumor types. These data support clinical trial evaluation of the PS-targeting antibody, bavituximab, in multiple oncology indications.

ACKNOWLEDGMENTS

We acknowledge the Dept’s of Clinical & Regulatory Affairs and Process Sciences at Peregrine Pharmaceuticals, for current insight on the clinical development of bavituximab and for providing antibodies for preclinical studies. We also thank Steve King for helpful technical discussions and support of preclinical studies and Dave Primm for editorial assistance.

1-18-18/2017 ASM: Roger Lias’ Slideshow & Attendee Reports

...Attendee Reports are after the Slides. I will update & re-post as more come in over the next few days. Thanks N40K for your addl. feedback – hopefully more to come.

1-18-2018: Avid Bioservices’ 2017 Annual Shareholder’s Mtg http://ir.avidbio.com/events.cfm

…10amPT at Avid’s Myford Facility, 14191 Myford Rd, Tustin, CA 72780 MAP: https://tinyurl.com/y9kpqesd

Webcast https://edge.media-server.com/m6/p/ij9i8ypx

PROXY/14A: https://tinyurl.com/y7qprpg9 VotingRecDate=11-27-17

CEO Roger Lias’ ASM Presentation Slides (1-18-18):

ATTENDEE REPORTS (2017 ASM 1-18-18):

By: Hawkfan1 (Michael) 1-18-18 9:41pmET #322974

https://investorshub.advfn.com/boards/read_msg.aspx?message_id=137796412

Here are some of my notes taken at the ASM. They are very brief paraphrases, since I never took shorthand in school.

As usual, Brandon Cox was the first to take the microphone with a long list of questions, that at least this shareholder very much appreciated.

Q. You are burning $3-4mm/qtr, with no cash and no back log. How do you plan to raise capital?

A. Your estimate of our burn rate is in the right ball park. We do have $33mm in backlog, but that is quite conservative. Most companies recognize all of an order when it is placed, but traditionally, PPHM has only recognized backlog as work orders for that order are placed. But clearly, we need more capital. We must eliminate the 'going concern' clause. While it may not be ideal for a small biotech, it is probably something they can live with. But for a manufacturing company, it is a death knell. Customers need to know that you are going to be around for the long term.

Q. How dilutive will it be?

A. We don't know yet. We don't know how much we will need yet.

Q. Is anyone from the old management team working to help sell the R&D technology?

A. Yes, Shelly. And others are working as consultants.

Q. Most CDMO's are private companies. Are there any plans to take the company private?

A. Not currently. (He did mention, kind of jokingly, that it would be nice).

Q. Who are the major institutional investors?

A. Still Ronan, Tappan, and Eastern Capital.

Q. Will they be involved in the capital raise?

A. Hopefully.

Q. What is the cost of being a public company?

A. About $2-3mm/year.

Q. As a strictly mfg. company, do we really need 7 board members?

A. Right now, the experience that they all bring is extremely helpfull. Down the road, maybe not.

Q. How much cash do we currently have?

A. $27.7mm. (Not quite sure I got this right, but I think that $10mm was in customer deposits). [NOTE: the $27.7mm is a/o 10-31-17, the last 10-Q (Deposits were $13.1mm): https://tinyurl.com/ybycb2s6 ]

Q. Will Avid expand beyond the earthquake prone Tustin area?

A. It could be done relatively easily. Down the road, it will be evaluated.

Then Brandon relinquished the mike and North40k gave a long and impassioned commentary about various trials and people (such as Dr. Wolchok) that the company should contact about Bavituximab. He mentioned Wolchok's comment that his next trial "depends on the company".

Dr. Lias stated that Dr. Wolchok has not contacted the company. He mentioned that an associate of Dr. Wolchok had said that it will be 18 mos. before the next trial proceeds. (This was met with incredulity from several shareholders in attendance).

Dr. Lias stated that they have numerous discussions regarding CAR-T, but there was no interest. In some other discussions, they found our technology interesting, but then said "prove it in a trial".

N40k then asked if the recent Halozyme trial failure would affect Avid. It will not.

Brandon Cox then resumed his questioning. He asked a question regarding the IP patent clock, which I previously reported. For continuity, Dr. Lias's answer was that as patents start to expire, and a BP realizes that it will take about $70mm and 3-4 years to bring a product to market, a 5-year patent life is not that exciting to them.

Q. How much Bavi do we have in storage?

A. Enough for a couple of small trials, nothing big.

Q. Client #1 is Halozyme. We don't know the name of client #2, but are they gone for good?

A. No, but I don't expect them to be hugely successful. They will be years down the road.

Q. Question regarding the interest in the Exosome test kit.

A. Not much commercial interest.

Q. Are you trying to sell the IP in bits and pieces or as a package deal?

A. While a package deal would be ideal, not gonna happen.

Then Greg got up and asked about the process of sell the IP. Dr. Lias commented that there was not much interest. The previous board has talked to everyone - it is not a secret - just not much interest.

Then N40k asked the board to contact Precision for Medicine, which concluded the Q&A.

Again, this is very roughly paraphrased from my notes. Other members that were in attendance, please correct anything that I may have inadvertently gotten wrong.

As I decided to take the tour, I was not able to talk to the board members one on one after the meeting.

BY: HAWKFAN1 (MICHAEL)

... 1-18-18 7:54pmET #322954 (INITIAL POST)

https://investorshub.advfn.com/boards/read_msg.aspx?message_id=137794640

Dr. Lias comment about the lack of interest in the IP by BP was in response to a question by Brandon Cox about the declining IP clock. His example was that if BP knows that it will take about $70M and 3-4 years of trials to get a drug to market, then a 5-year patent life is just not that exciting to them. This doesn't address the question of getting a patent extension, however. If this is true, then Dr. Lias needs to be made aware of it.

FU #323010:

Just a few more general impressions from the meeting today. Like the rest of you, I was very disappointed in the approach to marketing the IP. On the one hand, Dr. Lias said that there were on-going discussions that he could not talk about, but he continually down played any expectation that we would receive much value for it. It was almost like they have already given up and have a 'Hey, we tried, but nobody is interested' attitude. They certainly didn't spell out any detailed marketing plan.

On the CDMO front, they generally impressed me as qualified, and will probably do a fine job, but I almost choked when Lias said that Tracy Kinjersky "hit the ground running". Hopefully, she will not emulate Mary Boyd.

The tour of the Myford facility was as impressive as ever. The 2 new 2000L reactors are installed, tested and ready to go, but have not yet been used in production. Someone asked how many employees we have now and we were told about 200, of which 30 something (I don't remember the exact number) are in production. I asked, if only 30 something are in production, what do the others do? I was told quality control, testing, etc., which I would consider as part of production. This brought the number up to about 75. Unfortunately, we were interrupted, and I wasn't able to pursue this breakdown any further.

It seems reasonable to me that we can get to $200mm in sales, but it will be at least 2-3 years down the road. They already have space in the Myford building to build out a duplicate of the existing facility, except that I believe it will use all 2000L reactors. But this space is still raw warehouse space, and will take a minimum of a year to build. And they won't start building it until they have reached significant profits from the exiting facility. So it all hinges on how fast they can attract new clients.

FU#323064:

re: How many in meeting? I didn't actually count, but I was going to guess that there were probably about 20 shareholders, and we were matched, if not outnumbered, by company employees. My impression was that it was a bit smaller attendance by shareholders than in years past.

By: Holotawoopas 1/18/18 4:49pmET #322902

https://investorshub.advfn.com/boards/read_msg.aspx?message_id=137790910

For those who have pinned their hopes on the value of the IP it is time to mourn your loss and move on as there was nothing concrete about any potential monetizing extrapolated at the ASM. N40 gave a valiant effort to plead the case of value of the IP but IMO it fell on deaf ears! The CEO said no BP interest has been received!

FU#322909:

The CEO stated that the biggest down fall to monetizing the IP has nothing to do with leverage but has everything to do with patent expiration!!!

By: Eb0783 1/18/18 1:45pmET #322864

https://investorshub.advfn.com/boards/read_msg.aspx?message_id=137783413

ASM votes: #1 all re-elected, #2 for 36.4mm, #3 for 15.2 v. against 3.6, #4 1 year

FU#322879:

Per Lias, there is no formal process, group, or investment bank in place to sell the IP.

FU#322934:

Lias said he wasn't a patent expert when made those comments about short patent life being an issue. It was obvious he wasn't aware that patents could be extended due to years lost in development. Some of us took that short patent life excuse with a grain of salt.

FU#323063:

re: How many in meeting? I counted about 40 at the start of the meeting. I would guess 50%-60% were shareholders. That is about normal from my experience. I remember counting 40 & 50 in previous ASMs.

FU#323066:

The thing is, if they are really not having a process, group, or IB in place to evaluate/sell our IP, they don't have to spend anything to do it. At the very least, give the task to some IB or 3rd party expert on contingency: you can keep 50% of whatever you can sell it for. (You lawyers often take cases on the same basis and accept 30, 40, 50% quite often). I said that to Lias after the meeting, with Ziebell & Lytle standing there - no comment from them. I find their stance on this incredulous, if true!

By: Djohn 1-19-18 2:18pmET #323067

https://investorshub.advfn.com/boards/read_msg.aspx?message_id=137818937

MY THOUGHTS AFTER THE ASM: I missed the fancy danish, the cream cheese and bagels also missed the fancy hotel backdrop making me think we were on the verge of something astronomical. What did not miss was my thoughts of how many shares had to be sold to pay for me to bite on my bagel, sip on my fine coffee while looking at a beautiful swimming pool at a posh hotel.

It’s amazing what can be done with a couple of cases of bottled water, one pot of coffee and a room with chairs. That alone convinced me our new leadership is serious about how they spend the shareholders money!

For me the ASM went as I expected. It just confirmed to me that we are no longer chasing a dream. We no longer have a questionable cast of characters spending our money diluting our shares. It’s pretty easy, we are a manufacturing company now with basic straight forward business model. We have people in place who are qualified to grow this business and IMO recoup the total amount I invested in PPHM maybe even more.

I have given up the dream! I will awake daily and put on a BaviDermCQ patch. I will develop a 12-step program to wean myself from astronomical thoughts. One of those steps will be to not visit this board as often. Another step will be to fully investigate the members of the BOD in any company I ever invest in again. One other will be to take full responsibility for my investment decisions and accept how they turn out.

I bugged out right after the ASM ended and didn’t stick around for the tour of Avid. I had a flight to catch. Only one flight I could get to make it home that day. Maybe some of you there could gather more insight in talking with BOD or management during the tour. I went on the Avid tour last year and was impressed with the facilities.

FWIW This is what I gathered and is my opinion about the current situation. I saw a group of highly qualified individuals both on the new BOD and new leadership for Avid. These individuals are try to make lemonade out of lemons. Face it folks, after years and years of being told we had a bag of diamonds but we ended up with a bag of lemons! I am not saying that PS/Bavi/IP is worthless. Nobody really knows! Yet! but because the leadership of legacy PPHM did not do the correct things to prove it’s worth, we are left with an IP in shambles. After spending several hundreds of millions they left us with no value for the IP and the only way to prove value of the IP is to spend many more millions. ( A Bag of Lemons) Basically, after Sunrise failure the PPHM leadership decided to spend millions more to search around in the bag of lemons to see if they could just one diamond. We can all speculate on why legacy PPHM leadership continued down their path.

Fact to me is last year PPHM had two things. An R&D division with the IP and faced with spending millions more to prove some worth with low chance of success, even lower based on past successes. A CDMO business that with the right leadership and direction could become a nice profitable business in a few years. The chance of success with CDMO is very high IMO and I think valued much higher than R&D portion.

I think Ronin saw the CDMO business as a good development opportunity and took it. Real business people made real business decisions with maximum potential and maximum returns in mind. C'est la vie PPHM HELLO CDMO

FU#323070:

Don't get me wrong. I am not saying IP does not have value! I bought TCLN because I believed it did have value. I could hear the enthusiasm in Dr Thorpe's voice when he presented it. That was powerful! I just think the IP has been squandered all these years and nobody knows how much more money must be spent to realize it's real worth and with failed PIII no one is willing to take a chance on it. Hence, It's not worth much at this point in time. I think best path forward is CDMO to recoup invested money.

By: Aikifredicist 1-18-18 8:16pmET #322961

https://investorshub.advfn.com/boards/read_msg.aspx?message_id=137795041

I got up at the meeting and asked about Exosomes, but Lias just fudged on the answer. He doesn’t know what he has.

By: North40000 1-22-18 11:33amET #323194 (Initial Main Report)

https://investorshub.advfn.com/boards/read_msg.aspx?message_id=137869635

...Hawkfan posted that my comments to the CDMO BOD at the ASM last Thursday morning seemed to him impassioned. I was not aware of that quality in my remarks. I did try to portray facts, as I knew them, to the BOD, with suggestions as to what that BOD should do to bring increased value to CDMO, PPHM and SH assets/share value or $$$price.

Frankly, those facts & remarks seemed to me to fall on deaf ears - the stolid, expressionless faces of BOD members while I spoke made me feel I was talking to an army or array of Chinese stone soldiers. I was pleased to see one BOD member take notes during my presentation (I hope it was not a grocery list for his wife when he returned home). It was like delivering remarks to a judicial bench of judges who were not sufficiently informed of the record [history] before them to know what questions to ask.

I began explaining that we had invested in past years some $550k in PPHM therapy technology, and once had ~ 500k shares of PPHM with a break-even point of $1.10/share. Now, with a reverse split behind us together with a change in focus and name of PPHM to CDMO, we hold ~73k shares CDMO with a break-even point of ~ $7.70/share. I expressed my own opinion that the individual new BOD members had the qualifications necessary to bring CDMO share price/value well beyond the above $7.70 eventually. I was a bit dismayed to see from the slides that revenues might increase to $200mm by 2022 from >$100mm in 2018. The identity of further customers signed by Avid/CDMO since Jan.2017 was not further explained.

For now, I will not belabor my previous comments as to what Dr. Jedd Wolchok and other MSKCC personnel have told me in face-to-face conversations at SITC 2016, Wistar (Dec. 7, 2016), AACR 2017 or JHU (Johns Hopkins) in Baltimore(Dec. 7, 2017). Nor will I expand my comments re: conversations had with Dr. Nikoletta Kallinteris (PPHM) or Dr. Thomas O’Kleen (Precision for Medicine) at SITC in Nov.2017. My remarks are already recorded here, and my comments last week to the CDMO BOD contain basically the same information, including the fact that Precision for Medicine has acquired $200mm in addl. funds and has >1000 employees world-wide...

EARLIER #323153:

When I asked PL at ASM what SK is doing these days, PL told me he is occupying his time acting as a kind of entrepreneur… marketing PPHM platform.

FU#323169:

No mention by any of 6 new BOD members of what you post (Biopharm: GORE Protein Capture Device) at least that I heard. Indeed, but for Dr. Lias, I heard none of the other 5 new BOD members speak at all about anything - all 6 that were there at the front table [one could not attend the ASM at all due to snow in N.Car.] had secreted themselves out of our sight until shortly before 10am, when they all filed in from a heretofore closed door, sat down in chairs with name placards in front of them, were introduced by either the new BOD chairman [who welcomed us and called the meeting to order] or Dr. Lias [I forget which]. The new BOD chair & Dr. Lias had evidently decided who should thereafter speak and run the meeting, and it was all Dr. Lias after that who stepped to the microphone to speak.

After the meeting was adjourned post Q&A session, we were in a large group of SHs and employees who lined up in front of that same door mentioned above for an Avid/Myford facility tour. I do not know where the BOD members went, or whether any remaining SHs had an opportunity to speak to them.

In a curious way, I personally felt I was back in the courtroom at 717 Madison Place in WashDC, where I had argued many appellate cases before a 5-judge tribunal, sitting at a more elegant bench with placards identifying them by name in front of them. A major difference - at least those judges asked questions.

= = = = = = = = = = = = = = =RECALL:

1-8-17: EBD's Biotech Showcase 2018 (parallel w/JPM Conf.), SanFran https://ebdgroup.knect365.com/biotech-showcase

...1-2-18 PR: https://tinyurl.com/ydcc9agv

...3:30pmPT: CEO Roger Lias, Corporate Presentation

...1-8-18 Lias BioShowcase’18 Presentation PDF (24 slides): https://tinyurl.com/ya6tgxxa

FULL HISTORY of PPHM-Ronin PR’s, Letters, 13-D’s, Form4’s, Proxy’s, etc: https://tinyurl.com/ycb3fpfm

12-26-17: Roger Lias replaces Steven King as Pres./CEO; in process of changing name to Avid Bio. and new Nasdaq Ticker ("early 2018") https://tinyurl.com/yb34e2t8

12-11-17: Qtly. Conf. Call (Lias/Lytle) Transcript https://tinyurl.com/ybycb2s6

...Dr. Lias, "the company is undergoing a broad-scale transformation, the goals of which are to shift complete focus to the Avid Bioservices CDMO business and the complete divestiture of all of Peregrine's legacy R&D assets, which include bavituximab."

Thx much, North40k. Please do me a favor before I re-post the Attendee reports compilation with your latest one included…

For me, and others I’m sure, would you translate these abbreviations that you used (or give me hints so I can look them up and expand them for clarity)…

THANK YOU!

JHU = xxx

UPDATE – I think I’ve got these 3:

Dr. NK = xxx => I know now: PPHM’s Dr. Nikoletta Kallinteris

Dr. TK (s/b TG ?) = Tobias Guennel (Precision for Medicine)

PFM = Precision for Medicine, Frederick, MD

THIS SECTION:

N40K: “For now, I will not belabor my previous comments as to what Dr. Jedd Wolchok and other MSKCC personnel have told me in face-to-face conversations at SITC 2016, Wistar (Dec. 7, 2016), AACR 2017 or JHU in Baltimore(Dec. 7, 2017). Nor will I expand my comments re: conversations had with Dr NK(PPHM/CDMO) or Dr. TK(PFM) at SITC in Nov.2017. My remarks are already recorded here, and my comments last week to the CDMO BOD contain basically the same information, including the fact that PFM has acquired $200mm in additional funds and has >1000 employees world-wide.”

https://investorshub.advfn.com/boards/read_msg.aspx?message_id=137869635

Keep 'em coming, Attendees - much thanks! DELETE

1-18-18/2017 ASM: Roger Lias’ Slideshow & Attendee Reports

...Attendee Reports are after the Slides. I will update & re-post as more come in over the next few days.

1-18-2018: Avid Bioservices’ 2017 Annual Shareholder’s Mtg http://ir.avidbio.com/events.cfm

…10amPT at Avid’s Myford Facility, 14191 Myford Rd, Tustin, CA 72780 MAP: https://tinyurl.com/y9kpqesd

Webcast https://edge.media-server.com/m6/p/ij9i8ypx

PROXY/14A: https://tinyurl.com/y7qprpg9 VotingRecDate=11-27-17

CEO Roger Lias’ ASM Presentation Slides (1-18-18):

ATTENDEE REPORTS (2017 ASM 1-18-18):

By: Hawkfan1 (Michael) 1-18-18 9:41pmET #322974

https://investorshub.advfn.com/boards/read_msg.aspx?message_id=137796412

Here are some of my notes taken at the ASM. They are very brief paraphrases, since I never took shorthand in school.

As usual, Brandon Cox was the first to take the microphone with a long list of questions, that at least this shareholder very much appreciated.

Q. You are burning $3-4mm/qtr, with no cash and no back log. How do you plan to raise capital?

A. Your estimate of our burn rate is in the right ball park. We do have $33mm in backlog, but that is quite conservative. Most companies recognize all of an order when it is placed, but traditionally, PPHM has only recognized backlog as work orders for that order are placed. But clearly, we need more capital. We must eliminate the 'going concern' clause. While it may not be ideal for a small biotech, it is probably something they can live with. But for a manufacturing company, it is a death knell. Customers need to know that you are going to be around for the long term.

Q. How dilutive will it be?

A. We don't know yet. We don't know how much we will need yet.

Q. Is anyone from the old management team working to help sell the R&D technology?

A. Yes, Shelly. And others are working as consultants.

Q. Most CDMO's are private companies. Are there any plans to take the company private?

A. Not currently. (He did mention, kind of jokingly, that it would be nice).

Q. Who are the major institutional investors?

A. Still Ronan, Tappan, and Eastern Capital.

Q. Will they be involved in the capital raise?

A. Hopefully.

Q. What is the cost of being a public company?

A. About $2-3mm/year.

Q. As a strictly mfg. company, do we really need 7 board members?

A. Right now, the experience that they all bring is extremely helpfull. Down the road, maybe not.

Q. How much cash do we currently have?

A. $27.7mm. (Not quite sure I got this right, but I think that $10mm was in customer deposits). [NOTE: the $27.7mm is a/o 10-31-17, the last 10-Q (Deposits were $13.1mm): https://tinyurl.com/ybycb2s6 ]

Q. Will Avid expand beyond the earthquake prone Tustin area?

A. It could be done relatively easily. Down the road, it will be evaluated.

Then Brandon relinquished the mike and North40k gave a long and impassioned commentary about various trials and people (such as Dr. Wolchok) that the company should contact about Bavituximab. He mentioned Wolchok's comment that his next trial "depends on the company".

Dr. Lias stated that Dr. Wolchok has not contacted the company. He mentioned that an associate of Dr. Wolchok had said that it will be 18 mos. before the next trial proceeds. (This was met with incredulity from several shareholders in attendance).

Dr. Lias stated that they have numerous discussions regarding CAR-T, but there was no interest. In some other discussions, they found our technology interesting, but then said "prove it in a trial".

N40k then asked if the recent Halozyme trial failure would affect Avid. It will not.

Brandon Cox then resumed his questioning. He asked a question regarding the IP patent clock, which I previously reported. For continuity, Dr. Lias's answer was that as patents start to expire, and a BP realizes that it will take about $70mm and 3-4 years to bring a product to market, a 5-year patent life is not that exciting to them.

Q. How much Bavi do we have in storage?

A. Enough for a couple of small trials, nothing big.

Q. Client #1 is Halozyme. We don't know the name of client #2, but are they gone for good?

A. No, but I don't expect them to be hugely successful. They will be years down the road.

Q. Question regarding the interest in the Exosome test kit.

A. Not much commercial interest.

Q. Are you trying to sell the IP in bits and pieces or as a package deal?

A. While a package deal would be ideal, not gonna happen.

Then Greg got up and asked about the process of sell the IP. Dr. Lias commented that there was not much interest. The previous board has talked to everyone - it is not a secret - just not much interest.

Then N40k asked the board to contact Precision for Medicine, which concluded the Q&A.

Again, this is very roughly paraphrased from my notes. Other members that were in attendance, please correct anything that I may have inadvertently gotten wrong.

As I decided to take the tour, I was not able to talk to the board members one on one after the meeting.

BY: HAWKFAN1 (MICHAEL)

... 1-18-18 7:54pmET #322954 (INITIAL POST)

https://investorshub.advfn.com/boards/read_msg.aspx?message_id=137794640

Dr. Lias comment about the lack of interest in the IP by BP was in response to a question by Brandon Cox about the declining IP clock. His example was that if BP knows that it will take about $70M and 3-4 years of trials to get a drug to market, then a 5-year patent life is just not that exciting to them. This doesn't address the question of getting a patent extension, however. If this is true, then Dr. Lias needs to be made aware of it.

FU #323010:

Just a few more general impressions from the meeting today. Like the rest of you, I was very disappointed in the approach to marketing the IP. On the one hand, Dr. Lias said that there were on-going discussions that he could not talk about, but he continually down played any expectation that we would receive much value for it. It was almost like they have already given up and have a 'Hey, we tried, but nobody is interested' attitude. They certainly didn't spell out any detailed marketing plan.

On the CDMO front, they generally impressed me as qualified, and will probably do a fine job, but I almost choked when Lias said that Tracy Kinjersky "hit the ground running". Hopefully, she will not emulate Mary Boyd.

The tour of the Myford facility was as impressive as ever. The 2 new 2000L reactors are installed, tested and ready to go, but have not yet been used in production. Someone asked how many employees we have now and we were told about 200, of which 30 something (I don't remember the exact number) are in production. I asked, if only 30 something are in production, what do the others do? I was told quality control, testing, etc., which I would consider as part of production. This brought the number up to about 75. Unfortunately, we were interrupted, and I wasn't able to pursue this breakdown any further.

It seems reasonable to me that we can get to $200mm in sales, but it will be at least 2-3 years down the road. They already have space in the Myford building to build out a duplicate of the existing facility, except that I believe it will use all 2000L reactors. But this space is still raw warehouse space, and will take a minimum of a year to build. And they won't start building it until they have reached significant profits from the exiting facility. So it all hinges on how fast they can attract new clients.

FU#323064:

re: How many in meeting? I didn't actually count, but I was going to guess that there were probably about 20 shareholders, and we were matched, if not outnumbered, by company employees. My impression was that it was a bit smaller attendance by shareholders than in years past.

By: Holotawoopas 1/18/18 4:49pmET #322902

https://investorshub.advfn.com/boards/read_msg.aspx?message_id=137790910

For those who have pinned their hopes on the value of the IP it is time to mourn your loss and move on as there was nothing concrete about any potential monetizing extrapolated at the ASM. N40 gave a valiant effort to plead the case of value of the IP but IMO it fell on deaf ears! The CEO said no BP interest has been received!

FU#322909:

The CEO stated that the biggest down fall to monetizing the IP has nothing to do with leverage but has everything to do with patent expiration!!!

By: Eb0783 1/18/18 1:45pmET #322864

https://investorshub.advfn.com/boards/read_msg.aspx?message_id=137783413

ASM votes: #1 all re-elected, #2 for 36.4mm, #3 for 15.2 v. against 3.6, #4 1 year

FU#322879:

Per Lias, there is no formal process, group, or investment bank in place to sell the IP.

FU#322934:

Lias said he wasn't a patent expert when made those comments about short patent life being an issue. It was obvious he wasn't aware that patents could be extended due to years lost in development. Some of us took that short patent life excuse with a grain of salt.

FU#323063:

re: How many in meeting? I counted about 40 at the start of the meeting. I would guess 50%-60% were shareholders. That is about normal from my experience. I remember counting 40 & 50 in previous ASMs.

FU#323066:

The thing is, if they are really not having a process, group, or IB in place to evaluate/sell our IP, they don't have to spend anything to do it. At the very least, give the task to some IB or 3rd party expert on contingency: you can keep 50% of whatever you can sell it for. (You lawyers often take cases on the same basis and accept 30, 40, 50% quite often). I said that to Lias after the meeting, with Ziebell & Lytle standing there - no comment from them. I find their stance on this incredulous, if true!

By: Djohn 1-19-18 2:18pmET #323067

https://investorshub.advfn.com/boards/read_msg.aspx?message_id=137818937

MY THOUGHTS AFTER THE ASM: I missed the fancy danish, the cream cheese and bagels also missed the fancy hotel backdrop making me think we were on the verge of something astronomical. What did not miss was my thoughts of how many shares had to be sold to pay for me to bite on my bagel, sip on my fine coffee while looking at a beautiful swimming pool at a posh hotel.

It’s amazing what can be done with a couple of cases of bottled water, one pot of coffee and a room with chairs. That alone convinced me our new leadership is serious about how they spend the shareholders money!

For me the ASM went as I expected. It just confirmed to me that we are no longer chasing a dream. We no longer have a questionable cast of characters spending our money diluting our shares. It’s pretty easy, we are a manufacturing company now with basic straight forward business model. We have people in place who are qualified to grow this business and IMO recoup the total amount I invested in PPHM maybe even more.

I have given up the dream! I will awake daily and put on a BaviDermCQ patch. I will develop a 12-step program to wean myself from astronomical thoughts. One of those steps will be to not visit this board as often. Another step will be to fully investigate the members of the BOD in any company I ever invest in again. One other will be to take full responsibility for my investment decisions and accept how they turn out.

I bugged out right after the ASM ended and didn’t stick around for the tour of Avid. I had a flight to catch. Only one flight I could get to make it home that day. Maybe some of you there could gather more insight in talking with BOD or management during the tour. I went on the Avid tour last year and was impressed with the facilities.

FWIW This is what I gathered and is my opinion about the current situation. I saw a group of highly qualified individuals both on the new BOD and new leadership for Avid. These individuals are try to make lemonade out of lemons. Face it folks, after years and years of being told we had a bag of diamonds but we ended up with a bag of lemons! I am not saying that PS/Bavi/IP is worthless. Nobody really knows! Yet! but because the leadership of legacy PPHM did not do the correct things to prove it’s worth, we are left with an IP in shambles. After spending several hundreds of millions they left us with no value for the IP and the only way to prove value of the IP is to spend many more millions. ( A Bag of Lemons) Basically, after Sunrise failure the PPHM leadership decided to spend millions more to search around in the bag of lemons to see if they could just one diamond. We can all speculate on why legacy PPHM leadership continued down their path.

Fact to me is last year PPHM had two things. An R&D division with the IP and faced with spending millions more to prove some worth with low chance of success, even lower based on past successes. A CDMO business that with the right leadership and direction could become a nice profitable business in a few years. The chance of success with CDMO is very high IMO and I think valued much higher than R&D portion.

I think Ronin saw the CDMO business as a good development opportunity and took it. Real business people made real business decisions with maximum potential and maximum returns in mind. C'est la vie PPHM HELLO CDMO

FU#323070:

Don't get me wrong. I am not saying IP does not have value! I bought TCLN because I believed it did have value. I could hear the enthusiasm in Dr Thorpe's voice when he presented it. That was powerful! I just think the IP has been squandered all these years and nobody knows how much more money must be spent to realize it's real worth and with failed PIII no one is willing to take a chance on it. Hence, It's not worth much at this point in time. I think best path forward is CDMO to recoup invested money.

By: Aikifredicist 1-18-18 8:16pmET #322961

https://investorshub.advfn.com/boards/read_msg.aspx?message_id=137795041

I got up at the meeting and asked about Exosomes, but Lias just fudged on the answer. He doesn’t know what he has.

= = = = = = = = = = = = = = =RECALL:

1-8-17: EBD's Biotech Showcase 2018 (parallel w/JPM Conf.), SanFran https://ebdgroup.knect365.com/biotech-showcase

...1-2-18 PR: https://tinyurl.com/ydcc9agv

...3:30pmPT: CEO Roger Lias, Corporate Presentation

...1-8-18 Lias BioShowcase’18 Presentation PDF (24 slides): https://tinyurl.com/ya6tgxxa

FULL HISTORY of PPHM-Ronin PR’s, Letters, 13-D’s, Form4’s, Proxy’s, etc: https://tinyurl.com/ycb3fpfm

12-26-17: Roger Lias replaces Steven King as Pres./CEO; in process of changing name to Avid Bio. and new Nasdaq Ticker ("early 2018") https://tinyurl.com/yb34e2t8

12-11-17: Qtly. Conf. Call (Lias/Lytle) Transcript https://tinyurl.com/ybycb2s6

...Dr. Lias, "the company is undergoing a broad-scale transformation, the goals of which are to shift complete focus to the Avid Bioservices CDMO business and the complete divestiture of all of Peregrine's legacy R&D assets, which include bavituximab."

I do hope we'll get more Attendee Reports/Followups.

I'll keep adding them to the compilation, and re-posting as makes sense.

LATEST ASM Post:

https://investorshub.advfn.com/boards/read_msg.aspx?message_id=137805841

1-18-18/2017 ASM: Roger Lias’ Slideshow & Attendee Reports

...Attendee Reports are after the Slides. I will update & re-post as more come in over the next few days.

1-18-2018: Avid Bioservices’ 2017 Annual Shareholder’s Mtg http://ir.avidbio.com/events.cfm

…10amPT at Avid’s Myford Facility, 14191 Myford Road, Tustin, CA 72780

Webcast https://edge.media-server.com/m6/p/ij9i8ypx

...PROXY/14A: https://tinyurl.com/y7qprpg9 VotingRecDate=11-27-17

CEO Roger Lias’ ASM Presentation Slides (1-18-18):

ATTENDEE REPORTS (2017 ASM 1-18-18):

By: Hawkfan1 (Michael) 1-18-18 9:41pmET #322974

https://investorshub.advfn.com/boards/read_msg.aspx?message_id=137796412

Here are some of my notes taken at the ASM. They are very brief paraphrases, since I never took shorthand in school.

As usual, Brandon Cox was the first to take the microphone with a long list of questions, that at least this shareholder very much appreciated.

Q. You are burning $3-4mm/qtr, with no cash and no back log. How do you plan to raise capital?

A. Your estimate of our burn rate is in the right ball park. We do have $33mm in backlog, but that is quite conservative. Most companies recognize all of an order when it is placed, but traditionally, PPHM has only recognized backlog as work orders for that order are placed. But clearly, we need more capital. We must eliminate the 'going concern' clause. While it may not be ideal for a small biotech, it is probably something they can live with. But for a manufacturing company, it is a death knell. Customers need to know that you are going to be around for the long term.

Q. How dilutive will it be?

A. We don't know yet. We don't know how much we will need yet.

Q. Is anyone from the old management team working to help sell the R&D technology?

A. Yes, Shelly. And others are working as consultants.

Q. Most CDMO's are private companies. Are there any plans to take the company private?

A. Not currently. (He did mention, kind of jokingly, that it would be nice).

Q. Who are the major institutional investors?

A. Still Ronan, Tappan, and Eastern Capital.

Q. Will they be involved in the capital raise?

A. Hopefully.

Q. What is the cost of being a public company?

A. About $2-3mm/year.

Q. As a strictly mfg. company, do we really need 7 board members?

A. Right now, the experience that they all bring is extremely helpfull. Down the road, maybe not.

Q. How much cash do we currently have?

A. $27.7mm. (Not quite sure I got this right, but I think that $10mm was in customer deposits). [NOTE: the $27.7mm is a/o 10-31-17, the last 10-Q (Deposits were $13.1mm): https://tinyurl.com/ybycb2s6 ]

Q. Will Avid expand beyond the earthquake prone Tustin area?

A. It could be done relatively easily. Down the road, it will be evaluated.

Then Brandon relinquished the mike and North40k gave a long and impassioned commentary about various trials and people (such as Dr. Wolchok) that the company should contact about Bavituximab. He mentioned Wolchok's comment that his next trial "depends on the company".

Dr. Lias stated that Dr. Wolchok has not contacted the company. He mentioned that an associate of Dr. Wolchok had said that it will be 18 mos. before the next trial proceeds. (This was met with incredulity from several shareholders in attendance).

Dr. Lias stated that they have numerous discussions regarding CAR-T, but there was no interest. In some other discussions, they found our technology interesting, but then said "prove it in a trial".

N40k then asked if the recent Halozyme trial failure would affect Avid. It will not.

Brandon Cox then resumed his questioning. He asked a question regarding the IP patent clock, which I previously reported. For continuity, Dr. Lias's answer was that as patents start to expire, and a BP realizes that it will take about $70mm and 3-4 years to bring a product to market, a 5-year patent life is not that exciting to them.

Q. How much Bavi do we have in storage?

A. Enough for a couple of small trials, nothing big.

Q. Client #1 is Halozyme. We don't know the name of client #2, but are they gone for good?

A. No, but I don't expect them to be hugely successful. They will be years down the road.

Q. Question regarding the interest in the Exosome test kit.

A. Not much commercial interest.

Q. Are you trying to sell the IP in bits and pieces or as a package deal?

A. While a package deal would be ideal, not gonna happen.

Then Greg got up and asked about the process of sell the IP. Dr. Lias commented that there was not much interest. The previous board has talked to everyone - it is not a secret - just not much interest.

Then N40k asked the board to contact Precision for Medicine, which concluded the Q&A.

Again, this is very roughly paraphrased from my notes. Other members that were in attendance, please correct anything that I may have inadvertently gotten wrong.

As I decided to take the tour, I was not able to talk to the board members one on one after the meeting.

BY: HAWKFAN1 (MICHAEL)

... 1-18-18 7:54pmET #322954 (INITIAL POST)

https://investorshub.advfn.com/boards/read_msg.aspx?message_id=137794640

Dr. Lias comment about the lack of interest in the IP by BP was in response to a question by Brandon Cox about the declining IP clock. His example was that if BP knows that it will take about $70M and 3-4 years of trials to get a drug to market, then a 5-year patent life is just not that exciting to them. This doesn't address the question of getting a patent extension, however. If this is true, then Dr. Lias needs to be made aware of it.

FU #323010:

Just a few more general impressions from the meeting today. Like the rest of you, I was very disappointed in the approach to marketing the IP. On the one hand, Dr. Lias said that there were on-going discussions that he could not talk about, but he continually down played any expectation that we would receive much value for it. It was almost like they have already given up and have a 'Hey, we tried, but nobody is interested' attitude. They certainly didn't spell out any detailed marketing plan.

On the CDMO front, they generally impressed me as qualified, and will probably do a fine job, but I almost choked when Lias said that Tracy Kinjersky "hit the ground running". Hopefully, she will not emulate Mary Boyd.

The tour of the Myford facility was as impressive as ever. The 2 new 2000L reactors are installed, tested and ready to go, but have not yet been used in production. Someone asked how many employees we have now and we were told about 200, of which 30 something (I don't remember the exact number) are in production. I asked, if only 30 something are in production, what do the others do? I was told quality control, testing, etc., which I would consider as part of production. This brought the number up to about 75. Unfortunately, we were interrupted, and I wasn't able to pursue this breakdown any further.

It seems reasonable to me that we can get to $200mm in sales, but it will be at least 2-3 years down the road. They already have space in the Myford building to build out a duplicate of the existing facility, except that I believe it will use all 2000L reactors. But this space is still raw warehouse space, and will take a minimum of a year to build. And they won't start building it until they have reached significant profits from the exiting facility. So it all hinges on how fast they can attract new clients.

By: Holotawoopas 1/18/18 4:49pmET #322902

https://investorshub.advfn.com/boards/read_msg.aspx?message_id=137790910

For those who have pinned their hopes on the value of the IP it is time to mourn your loss and move on as there was nothing concrete about any potential monetizing extrapolated at the ASM. N40 gave a valiant effort to plead the case of value of the IP but IMO it fell on deaf ears! The CEO said no BP interest has been received!

FU#322909:

The CEO stated that the biggest down fall to monetizing the IP has nothing to do with leverage but has everything to do with patent expiration!!!

By: Eb0783 1/18/18 1:45pmET #322864

https://investorshub.advfn.com/boards/read_msg.aspx?message_id=137783413

ASM votes: #1 all re-elected, #2 for 36.4mm, #3 for 15.2 v. against 3.6, #4 1 year

FU#322879:

Per Lias, there is no formal process, group, or investment bank in place to sell the IP.

FU#322934:

Lias said he wasn't a patent expert when made those comments about short patent life being an issue. It was obvious he wasn't aware that patents could be extended due to years lost in development. Some of us took that short patent life excuse with a grain of salt.

By: Aikifredicist 1-18-18 8:16pmET #322961

https://investorshub.advfn.com/boards/read_msg.aspx?message_id=137795041

I got up at the meeting and asked about Exosomes, but Lias just fudged on the answer. He doesn’t know what he has.

= = = = = = = = = = = = = = =RECALL:

1-8-17: EBD's Biotech Showcase 2018 (parallel w/JPM Conf.), SanFran https://ebdgroup.knect365.com/biotech-showcase

...1-2-18 PR: https://tinyurl.com/ydcc9agv

...3:30pmPT: CEO Roger Lias, Corporate Presentation

...1-8-18 Lias BioShowcase’18 Presentation PDF (24 slides): https://tinyurl.com/ya6tgxxa

FULL HISTORY of PPHM-Ronin PR’s, Letters, 13-D’s, Form4’s, Proxy’s, etc: https://tinyurl.com/ycb3fpfm

12-26-17: Roger Lias replaces Steven King as Pres./CEO; in process of changing name to Avid Bio. and new Nasdaq Ticker ("early 2018") https://tinyurl.com/yb34e2t8

12-11-17: Qtly. Conf. Call (Lias/Lytle) Transcript https://tinyurl.com/ybycb2s6

...Dr. Lias, "the company is undergoing a broad-scale transformation, the goals of which are to shift complete focus to the Avid Bioservices CDMO business and the complete divestiture of all of Peregrine's legacy R&D assets, which include bavituximab."

1-18-18/2017 ASM: R.Lias’ Presentation (Slideshow)

PS: Attendee Reports will be added as they come in.

1-18-2018: Avid Bioservices’ 2017 Annual Shareholder’s Mtg http://ir.avidbio.com/events.cfm