News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

ls7550

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Not a recommendation, just a observation, free download https://www.gyroscopicinvesting.com/forum/download/file.php?id=3343 of Seth Klarman's Margin of Safety book that literally sells for thousands of dollars online due to being quite rare (as only a few hundred copies were ever printed). Book pages 217 onward align well with AIM, average-in rather than lump-in, selling is normally hard to do - unless you have AIM nudging you :)

Clive

Hi Toofuzzy

I built the calculator to spit out the hold zone ( top part ) so I wouldn't need to do the calculations every month, only when I had an order. I wrote the hi and low trade prices on an index card for all my securities and just needed to check if it was out of the zone and I would have a trade or if close, place a Good Till Cancel order.

AIM is a form of over-rebalancing style, which will benefit when there's a tendency towards mean-reversion. Such tendency has been known since the 1930's, mean reversion--under the name "reversals"--was reported in a peer-reviewed academic journal in 1937: Cowles 3rd, Alfred E. and Herbert E. Jones (1937). "Some A Posteriori Probabilities in Stock Market Action". Econometrica 5 (3): 280–294).

https://bogleheads.org/forum/viewtopic.php?p=7517697#p7517697

Generally there's a tendency towards months to a couple of years of momentum, inclination towards mean reversion after 2 - 5 years. AIM is likely a good a choice as any in order to play that. For better prospect of 'reversion', index funds are better than individual stocks. Sector or main stock index funds are much less inclined to fail.

Clive

PS same namesake (Alfred Jones) as sourced my userid (LS7550). But that was Alfred Winslow Jones whereas the above paper is Alfred E Jones. Alfred Winslow Jones is attributed as being the first hedge fund manager, both long and short (LS) in around 75/50 respective proportions.

Hi Jake

Investing is easy. Pick some assets you wouldn't mind holding long term, and buy the dips. One of the greater risks is what sits between the computer screen and back of chair. Many opt to buy when high (greed), sell when low (fear). Oddly might do the complete opposite with stocks to what they do when grocery shopping

AIM is a mechanical method to aid in being a better investor

You can even pre-calculate next AIM trades and place good-till-cancelled orders to yet further implement better behavior.

AIM will typically start flagging buy trades after around a 25% drawdown/pullback. Combined two lots of 10% SAFE + 5% minimum trade size amount.

Start with 33% in stock, average the remainder 66% into stocks over the next decade or so, each at a 25% discount price, and after 30 years you would have averaged around 90/10 stock/cash, where most of the stock (two thirds of shares) were purchased at a 25% discount. Whilst you also reduced the risk of having started by lumping in at a bad time.

Funds/ETF's are less inclined to go broke than individual stocks so are more preferable. Don't worry about cash/reserves as if that's all deployed sooner rather than later so more the better. Yes stock prices may continue down further, however you're better positioned than most others in having averaged in at a lower price.

Clive

Hi Jake

Cash percentage if you pool cash (and manage its level based on the VWave)

Hello all - If you're pooling cash across several AIM machines, do you try to maintain a cash percentage based on the VWave, as you would for cash allocated to an individual stock?

I'm thinking that if I pool cash, I might want to keep its percentage a bit lower in relation to the total value, based on the guess that the stocks or funds might not all rise or fall in unison and so wouldn't all need to draw on cash at the same time for AIM-directed buys.

Does that make sense ... or would it be better to treat each stock or fund as having its own separate amount of cash?

The following HTML is pretty much my AIM for heirs calculator. A simple once/year AIM of the Dow/Gold ratio (Dow index divided by price of gold per ounce) - that then advises what stock/gold percentage weightings to rebalance your actual portfolio to at the start of each year. i.e. AIM and (maybe) rebalance once/year and you're done for the year.

Historically that worked OK at scaling up/down stock exposure in a timely manner, yielded a better overall outcome compared to fixed/constant weightings.

Copy the text from the first html tag to the bottom, paste that into a text file and save with a .html filename suffix and then clicking on that file should open it up in a browser. There's a inline image towards the end that shows the historic year start %gold weightings back to 1932. Note how in 1980 when gold was high it indicated no gold, in 1999 when stocks were high it indicated low stock weighting.

Sometimes there's a residual flaw, where straight after one trade AIM would have you trade immediately again, so best to click the calculate button several times until it indicates 'no action'

Good practice to keep a written note of the Portfolio Control, Number of shares and AIM Cash values, so if/when your PC blows up you have a offline record of the values.

Clive

<html><head>

<title>Calculator for AIM</title>

<meta name="KEYWORDS" content="investment, Lichello, AIM">

<meta name="DESCRIPTION"

content="Calculators for Robert Lichello's AIM.">

<script language="javascript">

function figure() {

/* calculate market order */

pc= document.f1.PC.value*1;

ns= document.f1.NS.value*1;

p= document.f1.P.value*1; /* dow/gold value */

bs= 0.1;

mp= 0.05;

ss= 0.1;

CASH=document.f1.CASH.value*1;

if ( p > 0 ) {

sv = p * ns;

/* alert("stock value is "+sv); */

shareflag = "yes";

}

else

{

shareflag = "no";

}

if (sv >= pc ) {

Y= (sv - pc)-(sv*ss);

if (Y >= (sv * mp)) {

if (shareflag == "yes") {

shares= Math.round(Y*100/p)/100;

sharetext = "Number of shares reduced by " + Math.round(shares) +

"\nIncreased AIM cash value by " + p*Math.round(shares) +

"\nLeft Portfolio Control as-is";

document.f1.NS.value = document.f1.NS.value - Math.round(shares);

document.f1.CASH.value = Number(document.f1.CASH.value) + Number(p*Math.round(shares));

shares = shares - Math.round(shares);

CASH = document.f1.CASH.value;

}

else

{

sharetext = "";

}

Y=Math.round(Y);

alert(sharetext);

}

else

{

alert("no changes required");

document.f2.NS.value = document.f1.NS.value;

document.f2.DG.value = document.f1.P.value;

document.f2.AC.value = document.f1.CASH.value;

tv=document.f2.NS.value * document.f2.DG.value;

tv= Number(tv) + Number(document.f2.AC.value);

document.f2.TV.value = tv;

document.f2.GPC.value = Math.round( 1000 * CASH / tv ) / 10;

document.f2.SPC.value = Math.round( 1000 * ( 1 - (CASH / tv))) / 10;

return;

}

}

else

{

if (pc > sv) {

X = ( pc - sv ) - ( sv * bs );

if (X >= (sv * mp)) {

if (shareflag == "yes") {

shares= Math.round(X*100/p)/100;

if ( CASH > (p * Math.round(shares)) ) {

sharetext = "Number of shares added " + Math.round(shares) +

"\nReduced AIM cash value by " + p*Math.round(shares) +

"\nIncreased Portfolio Control by " + p*Math.round(shares)/2;

pc=Number(pc) + Number(p*Math.round(shares))/2;

document.f1.PC.value = pc;

document.f1.NS.value = Number(document.f1.NS.value) + Number(Math.round(shares));

document.f1.CASH.value = document.f1.CASH.value - p*Math.round(shares);

CASH = document.f1.CASH.value;

shares = Number(shares) + Number(Math.round(shares));

}

else

{

sharetext = "Insufficient AIM cash to fully cover " +

"the purchase of indicated shares,\nso added " +

Math.round(CASH / p) +

" shares,\nreduced AIM cash to zero\n" +

"and increased Portfolio Control by " + (CASH/2) ;

document.f1.NS.value = Number(document.f1.NS.value) + Number(Math.round(CASH / p));

document.f1.PC.value = Number(document.f1.PC.value) + Number(CASH/2);

document.f1.CASH.value = 0;

CASH = 0;

shares = document.f1.NS.value;

}

}

else

{

sharetext = "";

}

X=Math.round(X);

alert(sharetext);

}

else

{

alert("no changes required");

}

}

}

document.f2.NS.value = document.f1.NS.value;

document.f2.DG.value = document.f1.P.value;

document.f2.AC.value = document.f1.CASH.value;

tv=document.f2.NS.value * document.f2.DG.value;

tv= Number(tv) + Number(document.f2.AC.value);

document.f2.TV.value = tv;

document.f2.GPC.value = Math.round( 1000 * CASH / tv ) / 10;

document.f2.SPC.value = Math.round( 1000 * ( 1 - (CASH / tv))) / 10;

}

function figure1() {

// calculate hold range

pc= document.f1.PC.value*1;

ns= document.f1.NS.value*1;

ss= 0.1;

bs= 0.1;

mp= 0.05;

i = pc/(1-(mp+ss));

i = Math.round(i);

j = pc/(1+(mp+bs));

j = Math.round(j);

k = i*mp;

k = Math.round(k);

l = j*mp;

l = Math.round(l);

m = i/ns;

m = Math.round(m*100)/100;

n = j/ns;

n = Math.round(n*100)/100;

o = (i*mp)/(i/ns);

o = Math.round(o*100)/100;

q = (j*mp)/(j/ns);

q = Math.round(q*100)/100;

alert("Next AIM directed trades occur above/below\n\nUpper Dow/Gold ratio of "+m+

"\nLower Dow/Gold ratio of "+n );

}

</script>

</head>

<body>

<h2 align="center">

<font color="#FF0000">

AIM ADVICE CALCULATOR

</font>

</h2>

<center>2022 year end PC 11437.7825 #S 641 AIM CASH 10567.853</center>

<p></p>

<form name="f1">

<table cellspacing="0" cellpadding="0" width="50%" align="center" border="2">

<tbody>

<tr valign="center" align="left">

<th>Name</th>

<th>Value</th>

</tr><tr valign="center" align="left">

<td>Portfolio Control </td>

<td><input name="PC" value=11437.7825> </td>

</tr><tr valign="center" align="left">

<td>Number of Shares </td>

<td><input name="NS" value=641></td>

</tr><tr valign="center" align="left">

<td>AIM Cash </td>

<td><input name="CASH" value=10567.853></td>

</tr>

</tbody></table>

<div align="center">

<input onclick="figure1()" type="button" value="Reveal Dow/Gold ratio HOLD ZONE levels for these values">

</div>

<p></p>

<center>

<h4 align="center">Enter the current Dow stock index divided by current Gold price (in US Dollars)</h4>

<table cellspacing="0" cellpadding="0" width="50%" align="center" border="2">

<tbody>

<tr valign="center" align="left">

<th>Name</th>

<th>Dow/Gold ratio Value</th>

</tr><tr valign="center" align="left">

<td>Dow/Gold ratio

</td>

<td><input name="P"> </td>

</tr>

<!--

<tr valign="center" align="left">

<td>Stock Value </td>

<td><input name="SV"></td>

</tr>

-->

</tbody></table>

<P></P>

</form>

<p><p></p><center>

<hr>

<p></p>

<h3>With Robert Lichello's AIM you :</h3>

</p><p>

Start with an investment portfolio worth $SV = Stock Value ... <br>

and some cash. (The cash is in case AIM says "buy more".)<br>

You maintain a PC = Portfolio Control (which increases with each Buy).<br>

Initially, PC = SV, your initial investment portfolio.<p></p>

Each month you check your SV.<br>

If, subsequently, your SV is $X larger than PC, say X = SV - PC, then you Sell: Y = X - 0.1*SV<br>

(provided Y exceeds a minimum Dollar Amount of 5% of SV).<br>

If your SV is $X smaller than PC, say X = PC - SV, then you Buy: Y = X - 0.1*SV<br>

(provided Y exceeds a minimum Dollar amount of 5% of SV).<br>

Each time you Buy $Y worth of stock, you increase your Portfolio Control by 0.5*Y.<br>

(PC is always left unchanged after you Sell shares)</p></p>

We've adapted the former AIM calculator as we AIM the Dow/Gold ratio once yearly<br>

to identify a appropriate amount of stock/gold weightings to start each year with.<br>

We only need to keep a record of the PC, number of shares and the AIM cash value,<br>

that we can then load into this calculator - that indicates if we need to adjust those figures.<p></p>

The total AIM portfolio value is the number of shares x dow/gold ratio summed with<br>

AIM cash value. Dividing the AIM cash value by that total portfolio value<br>

identifies the actual percentage gold weighting we should rebalance our portfolio<br>

to, where the remainder portfolio value is invested in a US stock accumulation fund/ETF

<P></P>

<form name="f2">

<table cellspacing="0" cellpadding="0" width="50%" align="center" border="1">

<tbody><tr>

<th># Shares</th>

<th> x Dow/Gold</th>

<th> + AIM Cash</th>

<th> = Total Value</th>

</tr>

<tr><td>

<input name="NS" readonly></td><td align="center"><input name="DG" readonly></td><td align="center"><input name="AC" readonly></td><td align="center"><input name="TV" readonly></td>

</tr>

<tr><td align="center">Stock weighting % =</td><td><input name="SPC" readonly></td><td align="center">Gold weighting % =</td><td><input name="GPC" readonly></td></tr>

</tbody></table>

</form>

<div align="center">

<input onclick="figure()" type="button" value="CALCULATE">

</div>

<P></P>

Note that AIM can encounter what is called a residual flaw, where immediately after<br>

calculating another additional (trades) might be indicated against those new settings<br>

We suggest clicking the calculate additional times until the calculator indicates<br>

"no changes required (or indicates no AIM cash remaining)"

<p></p>

After aligning your actual real portfolio stock/gold weightings to the indicated weights<BR>

<font color=red>DON'T FORGET TO SCROLL BACK UP TO THE TOP OF THE PAGE AND RECORD THE<br>

PORTFOLIO CONTROL, NUMBER OF SHARES AND AIM CASH values</font><br>

write them down and store that safely for next years review.

<p></p>

In 1980 the Dow/Gold ratio was near 1, it took just a single ounce of gold to buy<br>

a Dow stock index share (or a single Dow stock index share bought a ounce of gold).<br>

In 1999 the Dow/Gold ratio was around 40, it took 40 ounces of gold to buy a single<br>

Dow stock index share (or a single Dow stock index share bought 40 ounces of gold).<br>

The Dow/Gold ratio might be considered as being a relative value indicator, in 1980<br>

stocks were relatively inexpensive/gold was relatively expensive; In 1999 stocks were<br>

relatively expensive, gold was relatively inexpensive. We let AIM use the Dow/Gold<br>

ratio as a indicator of a reasonable year start weighting/allocation to stocks and<br>

gold and where historically that yielded a better 30 year SWR outcome and higher<br>

average reward than if we just rebalanced yearly back to a fixed target weighting<br>

of stocks and gold.

<hr>

<img src="data:image/gif;base64,

iVBORw0KGgoAAAANSUhEUgAAAoIAAAFvCAMAAADpHFrmAAAAMFBMVEUBAAE/j9HDci+zsa7+2Fvq

7NVbQjD+zTP+4Xv+wQf+/v5OYoQrFBIKFk2R0Of+548h6/lYAAAgAElEQVR42u1dCYKDIAx0WxCs

Wv7/2xVF5UgsKiq2Sbu9kCsOkwCaLV4kJJdKQSogIQiSEARJSAiCJARBEhKCIAlBkISEIEhCECQh

IQhu7ktrfXkUf8EBw2/OYRsFKv3WqonJ1wsH1bdHp6khqIqpf03B+9fiPSXZtXUJnTR1HVt003eT

P8suZ1vW7x+F4LMsWqMzVrwJgsC5mXDW9ArSeAmSZghq+YsEt1a8nLO9N0Jwu/qPguDyCXRTtRrU

UDtv6tfBEAzFhWCK4Zwagk3xGLExsmDZv+vmNi4E+UBqkRjsy5UdoJ9cZ3uWyxAUQKlije75knpF

Sggu1uSnPorx5fVo+SYIimQQ5BlCkBV/amzWyIJy6HHXcQ+C74kdY+xJWfSZ6t2+4L1ZsHdHzHD8

21bDd7Ng2elmZL2RBfngxHUQKkIWHD79DU5O07mG77lnj6Idy9RdrzWMi8AzmjKN+tC8Wr9dPdu/

9YdpTT4GQPO6K6J9Gg2PXx6DtW/9A4LSpyE3kIt9MK+71hnHzarQarlbE3S81Y5Bw21f1Rs0w07j

olQDadrqQZjPtKuvfG6brdOxXdB5OB6C/ekYeX5kwWHMah+mAFnQKOBhuXjl6EbyaRrSlxr0x840

qbMX51Dnt1FdnYY0IqQpolecnMqb1escAJRemo40xlOYD24s+MwVDgLVBB3vQ3AyxI/Qdphjy75x

caoJNe30wMlXGgiWY4tEAMFybqzTmPMgOKjF6GtiwZ7AdFIDsyDTGbr5cs1fvCyK0VR0oNVvbFBG

b4fLCd3DLMbJNNQ7//RnT9Ot34y6imGg846Du4Y8ewBxPW5fnJdWN5wDoNJNA/vpknPwq9Ruqxoa

PVU4nftaH2jXhBwfTkee3REqPLVO4yJVE2ja7UGYz7TLTvd0imvqDAgOGDPjcxhZWgUaPnqEISwo

i35Q1+bU/JnT2RXT1CPzDda88SDoZHoZMv0bgeM7P+a3UV1vxzEyVdaB0+MdEJZuBlPfa+dgx9hx

z+MtC9Spd4/3Uzv7ptWi9dFZvfb9grsZqZpA024PwnxjuyarHDbZLsfV1PEQZEN1ajRDb3N+ut/7

pCUWHM2Z6DPrIzuvp8duMRdtsXrfRTdTr4fSg9Yr+G3yW0zaKFYjbPYBD/DM/HQ2nIN7r6oXAEls

mNo7PAcfD7r8j+bdg16/g92MVE2gabcHYb6xXcJZY3V0Kuz6T/YF5+bbhrh3MvpBv+QLjl+ZGXhv

bb77t/Y1L0N4EHQzFa2FbLvr7m8uBBtb5Y0FQT75E84BHFBsz0j9L87BvLHUEaxfPHtX720lwceD

Cx+8q40PiEC6GamaQNNNCEEn39gcBrGglQRr6mgI8sJZbZ5ZULum9QtlwSYctV0v5ODwGGYtzJyk

SM+C71dwoMuCwAGuYvW3pg0O7mzhc3JPICTpRVGLS5DjIQiW7bgo07T7WNDXtNOD27HgVJuyBk+v

TzV4CcXCuuDouzTGGW8fA30OjqWcnMB6rox7mdb5gtOeTe2AJoCgdwDk4XSFmQY6B5uzoIoCXcXl

M9egxwMZxbwuaEHwMSnp7xWrmkDTTg+cfK8mYMEXzoJOptMgOJux/pPFgs5sBd4dcWdw3ekwa7DO

DMfaHSn3zognO9dzD+/npmowjcM81XQnOACY5+lm8uDgR39sN0GEIFjWXT/4wwxW48aDxzfB6gsf

1jN9Q7xlRhxo2ukBOCO2WXBsW8iCl8yIpb149Tdyns18i3vEzjqW/vbXD6ih0GmsP6dsNd+5Lugt

0PVp0irv4a0L2qttnnmRk6Ltg5VpKGiIG7/QFjv+4awLDjtz0xLYw7X8q9cFA0273QXXBS0WfPhL

017SyeuCVs94UVhL0xgLelfK2Kv5WhGDp24o8s/yn5piPm7P7sjLmoeOZfB+z+I9fpwntuMB8Jr/

zFTm4OfYuLaGfcF+J8QUOtYEHz+1w1t4CBZl5sa9V6jG1bTXAy/f22fBsW0hC3qNOfEyhWPkEX1V

0jXCmzaj1jQHaWtTuU0cBPm8NTmufGonYfT92eU4zeoMAwgs8xgiTFOXvp4wh3KjMxXzepRl9nv/

tH0PO+G8udcVwqefeN9Vu9BYDM7NO4dyozMV00zMOJvF03xs/sY98ZZgtiTCTI0yYGPtfjX1O4ty

ozMV8yxhXuPvXZth41q7q2+CGclxMmwLTksmxu/Xl/yNLEhmmORwCD76K5TKor/cdF5x0r7gH5lh

khMgqPrpSFM2DgSHGbHqr8aYN22eJCSpxF+UeWvra0NwWJmp56mxLU8avSTpWNDMYBxfcJxZt51T

2N+0QRAkORqCj8K7RPlllgSbP2B1miBIkhKCejYyXDJlrQsOJPgaIEgsSHIoBK0LVszuyLDUyswV

I+QLkhwMQX1NxXzpSdGMi/1mSfAB3EBOECRJ7guuE4IgCUGQhCBIQkIQJCEIkpAQBEkIgiQkBEES

giAJCUGQhCBIQkIQJCEIkpAQBEkIgiQkBEESgiAJyRoIWkH1YiNrEQRJEkJwjPQ+x8b8HFmLIEiS

EIKsaXWM4/7/FMRG1iIIkiSEoLl/fVVkLYIgSVJD3L6nf9sUGVmLIEiScjqiyvFfL0ZH1iIIkqSE

4KMBIEiRtUhOi6zFimk6QpG1SK5gQdv6UmQtkqshSJG1SK5YlGmH0FoUWYvkqkWZYHeEImuRnDoj

HvaIB1RRZC2SCyC4QQiCJARBEoLgF4vzD704tz5ywgxB8AwEVmr+IistgonKiGCSgEgQPFY6tE0g

UxUgjJBDEDxSNOrERIigEHIIggeT4IhBBIG2oSYhCB5Bgp1I/RlB4ESSJATBA8RiOoFBsKIJCUHw

MJEzzBiKwIEjSQiCR5LgByHsEAQPEhYJwTtPSBRBMGPhkQi889KgrAQnCOYBtx0keOMJCcur9b8M

QR4aUx6PwLtaYi4ya/4vQ1D4XKBEtULETcddbkPohyHowYjLaqXcyxLzXlR+3uxw70gxBTP6ncha

wqUCXq2WO01IOEjwQvERnyoLCNav74+sxSrGnWkH34zAOy0NLnRPKikutcszwQl9r9K3R9Ziw9i3

Jr5iOwLvMyFROXP6DMH+3uEvj6w1AY+5OOJiEwTvYoll1q7tBEFl7uH85shaDFH9Ng68DQRF3r2Z

INjb3O+OrIWs+YmNHHiTZRmZ+wx/hCAf5sPfHFlrK9AWIJh/p9kaUr8ustbLtsD2t9c3RdZKj8D8

p8Tr1tqra1nQBDL62shavKp+D4LiFjN8Ay1pAhl9a2QtWf0gBPk9fFsDrdJY3i+NrCWqX4SgvMdC

Z2FPRl5fFllLVUJKxXl1lPAvG3jiOgjO049viqx1HPTuAcGbdOibr5QRvw1BtaFDjCB4gynIbSAo

b9Kj74Xg8WY48+sUxE269L0QrH4cgluHoCQIJhL26xBUWzvFCII7Nc/3nYCvgeD2MXjyHZ7fBkHt

g7MOhqcgMOuoHreZZn0ZBHl1qmQMwV2aEATBrOcg97hmdZ8nQhDMeg5yDwiK2zi5XwVBdTICc75s

+j4exldBsCIIJnKKBUHwAtvzXRDcuztJELyFGc75gsG9w1ERBLNfj8kcgjeaaH0PBAVBMKFFEATB

W5jhfCG4f3WKnwxB/miadrgy+q6RtS4hwWwvGNyvDXUuBM2/Zbf+K/vrbpG1ZEUQTOoXs3MhWBbt

+8Wff/eNrMUrgmDaASlOhaCc7p+7bWQtRhBMvUbPz4Tgo/ibIXjLyFpXkWCmFwyqW3Wt6AH3fjRF

+3zdNrKWIAgmtwnsXAiW43TkY2StLCGoKoJgeptwLgQ1Az6bIiKyVpYRzC5D4Pnx0FIHdFuQM4O7

GV+wt743jKzFxXUQzPKy6Zv1TUNL2BC8W2QtxaoLJcdrVtXN+lYMiNPLgkVxv8haUlQVQfCgBaoz

l6bNPx6xdkfuEVlLVVdLhhBMt0DFT4RgvzHcPqePN4msxS5HYI7XrMq7Obo3vlJGVATB4yYj53Xu

thDkVUUQPNg5IQjm7QZmesEgIwj+FgKzg2BS48AJgvkjMDsISoLgD/mBWUIw6RxNEQRzngvnecFg

2sFJELwBAnODYNr7FyRB8Aw1fxcE045ORhDMfCqSHwQTO8mCIJj5VCS/a1YVQfDnEJgZBFN7yQTB

/BGYFwSTa4cgmLkfmB0E1S093VtBMD8E5nXlviAI/h4C87pm9Z4cfyMI5ojArCCo7gtBXkyxjDKO

rJUlArOCIPsOCGYbWStPBGZ1zepNB9gAwQlj2UbWyhSBOUFQfQcEc4msxdU9EJgTBNlNezdAsG2K

IchqJpG19BqrkIpnuyKd0QWDfFRTdWsITg5gHpG1Js7rYJg5Aq+GoNJrgYwfpaTTIFh3/t+zySay

lqtMplRFEIQVNdleyY+5q/rcdUGlaTBZZC12y0BZGySXiGLshr0Llqb1HCQ6spb8ZErFbit8D7nw

gsETokmoU1mQF+0rPrIW+7xbqRJYYYLgtZo6C4KPmo++YHRkLRGxSrppVUkQBDPS1GkQDHdHPkbW

qmKMqeBfT4LXXa11isMiT4Igr7vJb2lAFhlZa3n0s809UATBnMwFOwmCm/YjVcxupfh6O3wZBM8Z

q1lDUEZZ09WWuCII5jRWRc4QXBof+k5fsckSK4JgVopKDUFlq4vvhGD1eYSK9cvrrM+FPfO7SOEq

CA7/ZeBgDW04f5+5e9YXY3shyKNmtTyhHRb5Pa+6eUTCgEvdudQQlJbZYNVOCIqF4a+sbsi15uVO

JHjaJXUwCVZHa0gkXvbkluvCqmo3C8ooT1msHiV3IkFRiUsgqGDMHUDySSHItMIGDIrZgGyGoBAL

8BzOznpfSeB6JBa0h6oAUCeO8HVVchLsebBv8G5DXOFD1DYTAVlyrpSUHB/cJnvwKjJ8XHTZNKum

+o/UUOIJv6W0KgELLrgJrLIUFCDVMLxQ2OCem2i/5sqC4hIIzix1rIZEytmWsqk7AQsiIBpstKUg

4SGVTW1QIK7F3EL7VeRJguIaFuTWED9UQ0n9DKuFw2neb4glavGFzYIMVh4wwHjlsKClVmuIi2xe

zcfLZiNHa8hmqh3DRYrB65JuE0WC6QjWOuYASTg0wYUNMQYtdomZBWdSdAdQANCLPl/GgtKe7/nq

TtbLFN3j0swIOPfKTcKC1SLfzk/ur6jOz9BddWbTQVEZrUlPn67YH3ZH5pF6EjsZ0BksXtlsNwvC

VwPyQCfSnSvbT/YKKFLkDDybkMdPF1yz6ijo4KG2cxEmMGHWczcLImtG0iew2VviQninz5nSKN8W

5A6/AQDnQ5C7OjxWYTu6x4TnMHgN3b8oI+TS4o+1CKTCaxAEYIoZ4PlluRLoNu98CKrgdB7Y3x3d

831M34tOwIICs9BehYxzsy4UPpi9bOQNaojEL//s/3gBBBmwBBM6CIk+qx0jRUDLRfOLx4K8Mbcs

PZsxuNtjKbgbBkGF2gghfANd2dac+608Sqe7P3vtPB+Cwp+vHYfDPTt0et4uRDh8p48eBB8Ggl5w

t+GWzj+E7DgyQp2qPzzEPGTu8nC/nn7BID+1t9u7h3ms08M1xKx4mjuIi3dUcDeseeBZWnywgTxF

ddPH6RBUpw43eVgzXRbsiE71EDS3shdWcDcFBnfrS5FovUu0B5xDVd0WgedfNi1tVR7eP7bLDi8+

HAh2RDdCMDK4mxDg/kionlBNQVtcDrSfxILoVXdnqUfs8liX2ukYYtmTXf3ygrvxheBuwlnx85dk

nBf/3UeZECH8YDwi+a89BrRUR15F6I/ngzG4fT4caMzDgcWC/XxjYMHmU3C3MSjSUFYY68mvxv6w

ZJUR5MFHooy6+OtB5YAxxI4MSRUaikOfG1vJPmrX3qB7aIANEASDu0EBPYaSVOAKenQREN74J4IT

PTOi88ydBEFnSQl54GwEbeAhT77HDpu/yjrpc9EzC5ogq538wcHdwLBGoK86uimLKvJAWnkGGT4a

RsKHspdzJCqHwa74YcuF0jqNZ3jNfM9AcZrpu2gMgWBkcDdTKvdWrCZQLQwrARoSLI9LhQsgqrxS

qk0IjCnH/cTgyZo8fjbivh/1t226JR0jVjklhixoYOuvC75eVnC3RwEaYq99ygbZAgGGhrb6QJou

JKvAaAts+rOYY1s5fruQ9YKjaBAeqBXqROx9V1vt8MezyUAIusHdZMFfSHC30a570J/VMZt+zw0I

fxmPBjJUIAuGIPcY03I5rRxBlm3luG2CIMir42iQAxbFU2Wid/OmNtthwPAJ2Bd0IDjsEfPZDL/g

4G5jIzlgnYVHHLalAH6vPEJyMwQgdLhLeBzvA6iy3j2rvrkcvyDsBPCjZiPu6HENXeX2MMH3dUOJ

W3ZYOCbR1viQsPdKGaCB3CU/4fCb80PwO5YhKNErGyImBz0iINlqfzmVM7GHHCFxGA0y33jYHak8

Je/9rkWuGyBMGXhYwAvO5aA+uRuCg3iad0k8nF8iAy5wDQHr4I6lyp9L++RQiWDluwJ/XV+OcH7m

0IxBiINo0BuglefLVJ7zse/76h26PpfiKvC4AqerErshCMzZP3Ka2HCEf3y1WEwFEGYVX3N0OXYi

YiKOifXB3cmTCBm+cqdVW7/PnVztAn5Wf2Wbid0syMIlGWR+UQGc7zphwII2oHBkmadySw8da2DK

sbUc50xxaDZyFA1yxK/YMp4XmWE+cWtRUfnujTP9s6xIKggKx1Fe9uNWOoLBT1VMxipWydvLcUc6

h2YMg0VKPxlhi4gJVhO2fheLLB9Fgp+1vhuCwboRWzyB1QorXH2GTwWay8qfYkDeJjD3wKilWjhO

oECT3jBPxH9Kgm7CpxGy/rsn8VzOQLOGtjIZC0p37FdiHSVVuw+sEtmg1eVUyCliY5JMPw+pDuk6

yKoj0KMhqKroM1clYUFvlKgFlACzfsy3h8x2tYYrqw9uQOwpQ8sJTrvCdJN0WYZ/dlIq/BSs/b7Y

vyUSrD5bviqZIXabqMTPikLBwg6F4FnC4j3BdbIfgpXVxB9GIHTFGrBommJX5CLhazzBFeY+HQt2

TfxlBAYQlIdAUObTwVRjJCEE1U8jMJh0sEMgyK7rIDuogQkh+OMicdUctDGXoyXmgiCYCwT5piW1

rBWujmFpguBBdkodAkGeUQ9TASIlBBlB8GgIXutu80PatxOCzMcdIwiGU1f1JRCUh8yWbAg+S32p

9Hu+atq9WBqMrDWgbngO+GP2TzHPmNOb6LkWVWuKYYFmWHoISq/6Azq9xxLztXWyWTtFf4tIL837

FR9Zi0EEyFae58+PVCpc+YgvRz8hp61PYekgyBzgsSM6jSqDfbbEKhwZnzVssaCqny9z21x8ZC1n

sE1K2X+Wj1BjIshiJXkQtCyDSjghZpaZEeeN3qE++XmEMA+EnzUc+IJcm93oyFpspj1mlZqamJIp

MQFmGUaEEB+wSB8qdkLMHDvDjuj0ojI+2eFpXDhQjGbBoZQefSsia02j0qo5VxJkSUgQbjhzrZS0

+SrZdQpczEzMIkmQpXRi+Mfdw5mUIqrvO6JsCDLt/3kxZT5E1rJnIAI/QTuxlcySpLDccDn+jayO

15Z6QsyizQ1L68bIz0t0DvQ/kSDzWVDoOYgX3G05shZzOxk9ON1B+vkvkT8dX+GC9uBymBt7yqIr

P2mHyPV6tn3SfX99aZ9b506XHIqCVcxCQ1yviazFHNjb9jhqvYDZx39637cew0R0RR8qhhvuzHu5

45AnY0Hm6zm616ne+bIddtVmawdTLbQ0rWMLRkfWcljQGaIRT3YW/NgOncPn1Yef5dNM9xdZRyRc

k/Hqjez1LhXYhcpPkxGG4Q4p1/MFLQjGRtZiwufATbg5GIEiJQJZiMf+6UDQHY484ZrMioGOYXHH

O1u+rS+EfNhW/92C4OP51jskeiUmOrIWvAC5zU1jQdNZuoXVDxWg31eUGbLglMhTTYgBZol3g1d2

HfjePZc3a6FKP9VvQ3DYHWmt3ZGPkbUCVWzFHtuP47Mf/lfpTl3tA3myCXFKDW8qZHHNMpY8nI92

rOlHWUzhtGIjazF6jA8bgtJNSwXBDHrJF7evtxSpdl6sRdCbHsw7H9Yj0Q6dzKCbPHnjElysRQ/z

cFdPgIGeYE3m8odKDgWC4DEQPIQFRc4Q3FykIggeDsFULMhz6GV+EOw1TE/mTRYN9MYXmRCC48tF

73JpwUg/t/IqTUd2T0bsySIfTsUEmTQQVG6pl7yja9P2+Fjzl8YXZKbAX3511yum8zFyZMI1maHS

i97xrnBhq2IFslMYYuFZnZ/8rFVvQ3BO7D+kW5OxqryGBfmH8THb4pj3FIbYMIE14n/u86h55ZyP

UTHpWHCyX17V8/Pw70sQtH1BFvs+q23ndEQ4bjk0fr79d+asVyjm0WCa2QgTgLrDpizMmPanL7Gg

BdQVLLjXF2TuaBfODz/y+5jmsaB9IE80Ibbrhkjq8HR0YVDNLqNwylh8TzAjdsblXL43Wfzu3ydW

Uq5Vsg/kSWYjzK5aAEPCrvKYdIZBUNoZYlmwP1btZ0G/3qDp3/77KMqjBEt4oglxwFLBkDg4HV3j

9EEQwYKJfEHhcu/vsqCz+ifZATt00mdBhrLYUekMX5v2QPB5JjLpLxkLit/2BbVI0Dh4BLlrTcaH

A1v25ZKn978uIMEt6SMLDp8SbdCROCcn0EkKCEJqRlQvjktH1jg5WsYHACZkwZ8X4UAwPQvyXDrK

8c2RTWJBkD/LomjNhdGRkbWIAhEW9ESmmRBnDMHtIxe4d+T1WhFZi8TSJriClwqCMpduqsQDxIag

jqzVsd+ayFqEO4gf+AEsmI0dPhKCBlRDWKPYyFokURBk32OHT4NgZGQtgt1ZEMzGDsOMnhKCZbsm

shbBDuIHlR6C+dhhGIIyHQQH/ouPrEViK9NoBYDg7phaGXUzcfvcK2W6GYgdz+hzZC2CXSQL7t0k

znLtKU37HBbkZfO2sRcRWYvkFAjynLrJj4Mgb9r3aI4jI2sR7M6BoPoNCKqmnaZ0sZG1JOEOgKBM

DkGZYzcTsbQFwXLYHennHNGRtUhmt3qaK8rIxbR72mGZFoIy3KAbpr2RkbWk1jw9mXSWK4BktdcO

yzw6KTEW3F4kXSmTjAO7J8qCch8Emcymk/DCYCIW3Oaj0EOOZ2ZcruAsTFd77XAmvZSWv2HT9I5C

d0OQZDwzbIagTOsLykxYcGxH0hn7XhYkApwIQr8a51kCpLXXDufEgjw7FqSpyIhCbtlN14ffA0El

mTMduOpvmhJxEAcbZzdJWJCe4ws3kPFT97GglG5R17GgefKlJq7Rmr1YkMQQ21r6rc/jS8iC43Fs

FwKtSq7480YaML3fCj+rtB2G2Gncb36e3mYWDFL5DjPsV3MN+82fVaKVEQfQNB3Zd4akrU0FWU2+

B4GZPQII8j2jg9YFU+JQ4ajZCEGeZW+hzZHNKNwLQWK/cEAr6Cj+RQiUcDOvYUGiP+fUKGBcbjPE

PGMEhp3Zw4KSWHAP5GB6gNJWbhJrW64U304t50JQXciCQ8X0HN8gpQwvfCUEl+s7dZi5PdFPDjU3

WllewbtZkOBnnyHjnbjo7F/UauuyiPjTBBhn4ZRYTf2MGq5uwcSCifhv+DQ4cBB5qKRD+3QWdLus

0rFgEl+QADh/Mr659dP4p9ZOhBerPPOPheMhgGA0CfoFe4ZY/0Pi8Y71yMhacmJWm2B/53VU6PjC

Bxb0NM3kyk1i7tUEVMkCD+2Yd6eX46tCYBCrr1k7niGe4mrFR9Yaa57e2I/B0AGgHCFoD/dRVrPg

XC4DqjzPFZQ2XsxnBAax+nIQa0OwrcfbNqMja4EsyBztfftn+2MPQQV683LlhNjUAao1nO0c9e4D

foQhyoJx+mK2ofB8QQPB6MhaCLB/57PzKzMQBOaubDUE/cIRUEzfjnlnFglareAQaUfpy68mhGDj

RlP4FFkrpGu/YvnFn5lHGCgLjknrJsSgWgGv6rB3FPbefIRH6ytwbxnGgtGRtU72TLIX5UNwVvpK

CGYrDIHgLp2FLBgdWYtA56lTx9WCx+WqOFrZi9NclRSCAQsuR9Yi0IXqRJL4ujWZzIVjrmsqFoyO

rEWgOwKC6h4dPQiC7brIWgS6aAiqr4KgPJoF4yNrkfwmCzrdUSlKKl5zaK12RWQtAl1ADnw/C8qf

gqCCIRgdWYvkRyGokrWX77tSRhHoIiGo1DdNiF1ncB+Wd1+sRSCclTlCUEEpqyCocu+osiwxV5vb

q/az4NAaegyP/sRwSCfuOYthwcz7abP6jvbqF7XbENPTfvKXMggMnjxeqeoOnfVYcNNTJTDEN1HX

Sc+BBQOVmEc0BO+hUheCG7CXigXp4RliAyAgfY2DfYPOcsd33WqGJ+uw1xDTYzovrn6tAR/rDPKb

dFYl4qEULEjImx+GBV2tjC/fCsG9KtvpCxLqbKR15wUflbEQnDGbdV8nVldqdVZnbO5kwVHzJEYT

mEr0jzxSp312mX1fLQiuaK30P+72BUd90WNmQaPfYPDzaJ3egARnx2IdBDyNJWBBokFvTE++IJC6

hgVv0FvbG9usMUksmJQFO2aQs4KD1FgIqnt0lw+yGQEOknewIIkjXAYuj5UYOSG+Eesn0Nh+CJIZ

ts8LXzw9URD8Nd+FWPBMUohck/kpfXGC4KlmmlQaDlcEgpGRtQhUBMGDfMHYyFoEqpVCEIyEYHRk

LcIUQTCRTgqfBCMjaxGmUlti/qsqCSAYGVmLMEUQPAaC0ZG1CFOpLTH/VZXgEIQja00Q5CQr5RME

f1UjCxAEI2s9SUhSybIv+CmyFglJIoFnxJ8ja5GQHAPB6MhaJCTHQDA6shYJyUEQjI2sRUJyFARJ

SAiCJARBEhKCIAlBkISEIEhCECQhIQiSEATXy3gFhCucP/HrleonlsJ5mvoXq8frT1U9dR+vfwsE

n2OTS2fThPe19zt8/oXW/NEMG3/ILksRNuPZNO8Z0XEAAAYpSURBVLXerQ4LQ6pfqP9T9UD9ePXU

/cTdXw9Brstr32HTH8PdJkVdN97tJjpLWdd12RTuNdi1EZ3JbV9XTlP8lUXdqeEdVT1eP1o9Xj9a

PXU/Xfc3Q/BRtM9n2VfjNqIp+pe3bknrZTEd7MZV7Q6/pn8W+tXJoi/WefQD6uEWhlaP149Wj9eP

Vk/dT9f9zRAcQP7QI8FtRP+tf+GBdsZxobx2t0+uH0XRvQQK5VBhaPV4/Wj1eP1o9dT9dN3fDEFT

TNnyF9DVYTRB2oHcjvHKxLBpc4+grkLV4/Wj1eP1o9VT99N1fwcLmua33PcGWnPlv/SoeB4HPkl3

fq++Mixsms6iekdEuVnQ6vH6F6rH6kerp+6n7P5GCJamRN603pju3M36WbbPwCHt3Ir+EkT+AKZL

urzwHGifo2w7BfkOBFo9Xv9S9Uj9aPXU/aTd3zodMeWoJuR1I39BHixlGInhOehnXu8+X/uOqx6v

f7F6sH60eup+4u5vWpSZ5u+qLP3uPOqyhBY6+bMs27KGF4Z044Ec2kPustU8unq0/sXqwfqx6qn7

qbufyQbdhlX4b6r/t7t/KgSf9dqEhZT1in4+16bgWZKeaRwCcApfKIkjvz/XpujlmlwhqOryPTiZ

78iExTn5YgKS0jF7W9axKbw3Dv0u0V9kCp6lwTqHJmiD1sLbXWhC56EhKfw5rCWHteEp+AYZlvJx

T0/PTBpszaT0GzZa57pMAkHV+5XdnKlrJMcS3CzoRhC+Q4WmNE0/L9OL+t4MH03B947QFDyLPi9P

Dg4WJAHf7sL3wfANur6DJYRNLEXPLWqzQcbjUvAsGwilH0jgnuL2GXHNH62eqz/cvqIJ1kZQ46+a

IglLWfo1g7dW098rKgXfO0JT8CxFockGYDw0Ad/uwvfBFjboar0w/Nap/nBCUqYSghUWNAXPsgGC

w55e8065NP3WezDQqimSoDeC9D5Ql+j5F2gCnqJ7MTCTDMCBpOB7R2jKcpZnqU0Uf8UlONtdbVTC

UpZRvw9oBRhKaSZjFa4zIykLWWbxdkewBHNOSmBPcSsEl/eOwF0dXjbwRhCagKcMQHsh4ABT8L0j

NOXTdlPvd7XPqIQtGvuwQVcUyHCCUvANMjRlKUvTmkdg0OCEeU/vnXSDrgBPG6ZQfCMKT8BSZqC9

UAi+YveO0BQ8y1R0Z1uKqISl3TZ8H2whi2FGaDhBKfgGGZqCZylnI18UUQkLe4pbIdjX1S9WcN+z

QRKMUwEPAjQBSZmnCCoAB5Iy7h3VT+BSNjgFz2I1iD+iEsbtrhZyueCEpSy13umqw+6jKfgGGZqy

lOUPRhqasLCnuBWCbNKJN+tAEyZWgx1YNAFMGXZ66hc06cFS8L0jNAVN2LCwNGx3sXC7C034kKWn

xxK6mBRMwTfI0BQ0wYK3uzuCJiztKW5dF5yWax91ZMJ8Vl+rEuC9o/4B1YKn4HtHeAqSgG0z4QlL

211YwtIOWdnU8FoynmI2yHh8Cp5l/Yr80p7i2bsjybYHSL5Iiq1g4isTLs/yRrO812e5W/e3bNCd

kmUjBNGNIDTh17M8PmydHZsF323j6zfoUmbZCsFhI6gFNoKwhLRZGjRLg9eib+KCa4FTFrMUWJai

WNg6u1Rj8B1saEpcFh6VsJCyFYLDRlADbQQhCXlkad8c3dTiK7P0/xoIygIlZNF9A9L6FZVyTpYd

S9PjEugDWzUF944oy5VZzMJJ7K19p2TZDEF7I6iNSqAsGWSB1i43bdCly7KPBRW2EaTQvSPKcmUW

s3mwe4MuZZadvqB+kdB1REACZbk4S9INunRZts+Im3HbqATCnUAJlOXSLEk36JJm2bwuyMuyBTdu

0ATKcmmWhTvY0JRzsuzZHSEhSSUEQZI7Q7Ap1yZQlguy4HewoSnnZEkAwWQ3ZVKWA7Pgd7ChKedk

IQj+Shb8DjY05ZwsmyG45R4qynJlFvQONjTlnCybIbjpHirKcmWW/g24gw1NOSfLZghuuIeKslyZ

Bb+DDU05J8tmCG64h4qyXJkFv4MNTTkny2YIbriHirJcmQW/gw1NOScLLU3/iuB3sKEp52QhCJLk

IQRBEoIgCUGQhIQgSPK78g/xWPT4ckOXvwAAAP5hbFBoeNrtwYEJAAAMAqCzO7/OGAM1gUsFAAAA

AAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAA

AAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAA

AAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAA

AAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAIDnBln+

pjDwLglaAAAAAElFTkSuQmCC

alt="Base64 encoded image" width="480" height="276"/>

<hr>

</center><p></p>

</body>

</html>

Hi Rickson

I prefer a variation to the method proposed in the book when adding a lump sum into a existing AIM. Adding the lump sum in proportion to the current stock value/cash weightings as well as updating Portfolio Control by the value of the newly added shares, and of course increasing the number of shares held in reflection of the added shares.

$10,000 AIM value, $6000 stock value, $4000 cash. Add $2000 and 60/40 split that between additional/new shares and cash, so $1200 into stock, $800 into cash, increase AIM's record for number of shares held to account for the newly added shares and increase Portfolio Control by $1200.

Clive

Hi Tom. 20 minutes into this video (that I found by a linked video presented at the end of that last link I posted) ...

Hi Tom. 0 to 60 in 1.4 seconds?

Hi Toofuzzy

Thanks for the pointer. Not sure that's available from over here, as is the case for many/most US funds nowadays, and where when you might/can they typically are taxed more punitively. All part of general global de-dolarization/de-globalization.

Clive

Hi Tom

I see that GBTC, basically a stock/fund whose value is mostly comprised of bitcoins such that the share price changes somewhat reasonably reflects Bitcoin price changes, for 2016 to recent had a 28% CAGR. In contrast AIM of GBTC, monthly reviews with classic AIM settings, yielded a 32% XIRR.

As you know XIRR is like CAGR but where it accommodates irregular cash flows - as is the case for AIM, basically reflects the annualized gain achieved relative to the actual amount of $$$ invested (that varies over time due to AIM trades). If you had another AIM that bought as one sold, and vice versa then the weighted XIRR's might reasonably reflect your actual gains.

For gold since 1968, weekly reviews classic settings the XIRR was 20%, whilst gold just bought and held yielded a 8% CAGR. Add in yet other assets/stocks such that your cash tends to remain continually fully deployed and XIRR measures will tend to reflect your actual overall portfolio CAGR.

I don't know the actual correlations of Bitcoin to other assets, but there is a prospect that in some cases AIM of bitcoin might be buying when another AIM is selling and vice-versa.

IIRC Steve (Grabber) used to pretty much run his AIM's that way, as one sold look to deploy the cash sale proceeds into another AIM that was signalling a buy. In effect running many AIM's on paper, not real money, alongside real AIM's where real money was actually invested. AIM tends to do a pretty decent job of achieving reasonable XIRR rates of returns.

Somewhat Buffett style, where he considers his main role to be a asset allocator i.e. find appropriate places into which cash thrown off by other parts of the business/portfolio can be deployed. Like AIM'ers, he too also tends to not deploy all of cash reserves, primarily because his business model (insurance) might have sudden unexpected call upon large amounts of cash. For others with less need to have instant/large cash reserves there may be little need to hold much/any cash. The hardest part is finding appropriate investments with inverse correlations. If everything is down and AIM is flagging 'buy, buy, buy' and nothing is selling, then you can't actually take advantage of those opportunities. Also as part of that as a asset allocator you also have to consider the limits of how much capital you might deploy into any one asset such as Bitcoin. For Bitcoin IMO it would be unwise to invest any more than a relatively small amount, perhaps no more than 5% of your total portfolio value at most.

PV

I'm not really a smart phone user, more a laptop'er, nor do I use MS, but its nice to see a AIM app for those that do.

Clive

Hi Toofuzzy

I understand what you are doing but I don't understand the math.

You could just AIM a Dow fund and hold the cash in GLD or IAU ( or even better WPM ) but I don't understand how dividing the dow by gold price gives you the trade signal.

Are you using that ratio as "PRICE" ?

Where does your # of shares come from ?

What securities are you actually buying ?

Hi Tom. Monthly vs Yearly reviews

For a 1985 start year, setting AIM initial %CASH to the same as the longer running (older history) yearly AIM, to level the field, and rolling forward from there and the monthly reviewed version of AIM of Dow/Gold ratio progressively pulled ahead, for a while before seeing a spike down and then subsequently catching up and over-taking the yearly AIM again.

Overall the log linear regression (exponential trend line slopes) were near equal. The average of the yearly changes was higher for the monthly reviews, but so also as the standard deviations in yearly changes. Comparable rewards with higher volatility = lower risk-adjusted reward for monthly reviews compared to yearly reviews.

Monthly reviews was much quicker to throw away its 'cash' (gold) reserves into declining stock prices than was yearly reviewed.

Clive

AIM vs constant weighted 30 year outcomes

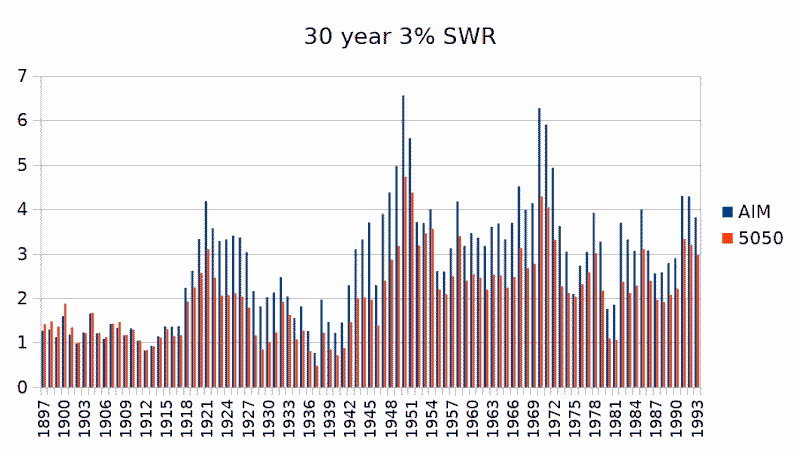

The dynamics of AIM of Dow/Gold as a indicator of weightings and trade times, reflected into 30 year 3% SWR outcomes (final portfolio value after 30 years as a multiple of the inflation adjusted start date portfolio value) for both US and UK data/portfolios indicates that AIM sometimes just bettered constant weighted 50/50 stock/gold (yearly rebalanced) by a little, sometimes by a lot

but AIM was always as good as or better than constant weighted.

That used the same AIM of dow/gold indicated %cash (gold weighting) for both US Dollar and UK Pound data, holding US stock and gold, and the outcomes from both suggest that the times when AIM was significantly better somewhat aligned in both markets. 1920's and 1960/1970's decades. Which were times when the Dow/Gold ratio transitioned from relatively high to low levels. Being 30 year measures the data only runs up to the early 1990's start years (that run up to present 2020's years). The late 1990's was also a time of very high Dow/Gold so is perhaps indicative that as forward time dots/measures are added to the right of those charts we may very well see cases of AIM having significantly outperformed constant weighted. Perhaps with a peak centered around the 2009 stock lows and perhaps extending out to recent start years of more modest relative out-performance. A wild guess, but where perhaps AIM started in more recent times might end 30 years with around 1.5 times more than constant weighted.

Very much doubt I'll be around to see that confirmed or not as I'm borderline graduating into the 'old' category (alongside OldAIMGuy, old-John) myself.

But as Einstein said, its all about relativity ...

so ...

Young-Clive :)

[PS however they do say you're as old as you feel, and recently I've been feeling pretty old (stairs and knees)].

For yearly reviews the simplicity is nice

We just need to record the PC, #S (number of shares) and the AIM 'CASH' values, and then each year just look up the current Dow and Gold prices, divide the Dow figure by the gold price as our AIM 'Share Price' (SP) value and use the AIM calculator https://investorshub.advfn.com/boards/read_msg.aspx?message_id=88637795

For the last couple of years no action was indicated, so job done for the year.

In other years a buy or sell trade will be indicated, in which case we do the AIM math, identify the new %CASH that AIM is indicating, and rebalance our stock/gold portfolio to where the percentage of gold is around the same as the AIM indicated %CASH value. That will result in PC maybe being changed (if a Buy) or otherwise left as-is, a new #S and a new %CASH AIM values being recorded/updated in readiness for the next review a year later.

Or alternatively just do it on paper. Peter Ponzo (sadly no longer with us) outlined the basics here https://www.gummystuff.org/AIM.htm

In return that will scale up/down stock/gold weightings in reflection of the Dow/Gold ratio, where generally that was better than just a fixed constant weighting of stock/gold being rebalanced to each year. For instance had us all out of gold/all in stock in the 1980's when gold was relatively expensive, a single ounce of gold buying a Dow stock index share, more into gold/less into stock in 1999 when the Dow/Gold ratio was up at 40 levels (a single Dow index share bought 40 ounces of gold). As per that image I posted earlier

Might still broadly average 50/50 stock/gold, but where at times held 0% gold, other times held near 80% gold. And where historically at least those dynamics were better than just a fixed/constant weighted choice such as constant 50/50 weightings, and yielded higher rewards, and tended to do so with less risk such as lower (not as bad) drawdowns (which tended to also improve the likes of how much SWR (income) could have been drawn).

And all that you need is a little piece of paper with your

PC 9954

#S 569

CASH 15583

or whatever figures tucked into your wallet.

At times you may hear breaking news stories of stock prices collapsing or gold prices soaring or whatever, at which times you may like to monitor activities more closely and potentially calculate AIM trade signals if you think things (events) may be at a near peak/trough turning point. Buy from the scared, sell to the greedy as Tom says, but where its judgemental as to when they are the most scared/greedy.

Clive

Hi old_john

I'm wondering if there would be any advantage or disadvantage (other than perhaps the time required) in doing the AIM rebalancing on a monthly, quarterly or semi-annual basis?

Hi Tom

When the solution is simple, God is answering -- Albert Einstein

I'm no Einstein, far from it, but I do like simplicity.

Clive

AIM Dow/Gold ratio

Starting from 1925, apply AIM once yearly to the Dow/Gold ratio, AIM settings of 10% SAFE, 5% of cash value minimum trade size. From that we identify years where a trade occurred and what level of %cash that adjusted to.

Use that as a paper AIM, where %cash indicates how much gold weighting to hold, and when to rebalance to that revised gold weighting i.e. in years when AIM actually made a trade.

Applied to the Total Stock Market (TSM = similar to S&P500) and gold, where gold was T-Bills pre 1934 (as gold was money back then, and you could deposit that money in return for interest), and the outcome was pretty good, averaged 44% gold, but at times held as little as 0% gold, at other times around 80% gold. Broadly yielded total returns that compared to TSM

and did a reasonable job of scaling up/down gold weighting in reflection of changes in the Dow/Gold ratio

and was relatively safer in the sense of enduring lower drawdowns

In terms of 30 year 4% SWR outcomes, at times when 100% TSM struggled, AIM did better and vice-versa

A reasonable choice therefore might have been to run two portfolios, one for TSM, the other for dow/gold ratio AIM, initially 50/50 weighted into both, and then just left to run separately. In which case the final combined outcome was decent, 4% SWR never ending with less than the inflation adjusted start date portfolio value still available at the end of 30 years. The following chart shows the multiple of inflation adjusted start date value that remained at the end of 30 years, so a value of 1.0 = 100%, 2.0 = twice a much (in inflation adjusted terms) ...etc. In the best case you ended with 8 times more in inflation adjusted terms than what you started with 30 years earlier after 30 years of 4% SWR withdrawals. Great cases are great, but for most its the worst case outcomes that are the main concern and diversifying to dilute down the worst case risk worked out well when that diversification involved initial 50/50 weightings into TSM and AIM

Some retirees use a 4% SWR guide as the amount that they might draw, and where typically that is measured over 30 year periods and where the worst case left nothing remaining at the end. The above however is indicative that you could have applied a 4% SWR with in effect 2% being provided by AIM of Dow/Gold, and the other 2% from TSM, and always having ended with your portfolio value still intact.

SWR of 4% is to initially draw 4% of the portfolio value as income in the first year, and then adjusted that $$$ amount by inflation as the amount drawn as income in subsequent years, so a regular inflation adjusted income.

Clive

AIM Dow/Gold Ratio

For once yearly realignment (rebalancing) at each calendar year end, a AIM of the Dow/Gold ratio, with 0% SAFE (infrequent reviews so we don't need any 'slowing' of cash-burn/stock-purchase rate) and for data since 1968 (relative to a AIM original start date of 1896) ...

... and AIM has done a pretty decent job of aligning indicated %cash (gold) weightings to the Dow/Gold ratio

Robert Lichello mentioned Harry Browne in his book. Basically Harry was what some describe as a gold-bug back in the 1960's/1970's and was heavily into gold (and made considerable gains) during the those years. Harry subsequently devised the Permanent Portfolio as a means to diversify that heavy gold concentration after the large 1970's gains in gold. It was sensible to have been gold-heavy during those years, less so after the large gains, such that he subsequently diluted down that high gold concentration into other assets (stocks, bonds, cash ...etc.) as a means to better preserve that accumulated wealth.

Similarly in the late 1990's stocks were 'expensive', it made sense to water down your exposure to stocks. The Dow/Gold ratio (Dow index value / price of gold) has historically provided a reasonable indicator of stock and gold highs and lows, and AIM did a good job of mapping the Dow/Gold ratio to a actual indicated appropriate %gold level. Late 1920's prior to the Wall Street Crash for instance AIM of Dow/Gold was indicating similar levels of %gold as in 1999 (high gold weighting, lowish stock weighting).

Rebalancing a stock and gold blend portfolio once/year in reflection of the AIM of Dow/Gold indicated %gold weighting resulted in a better outcome than either 50/50 yearly rebalanced stock/gold, or 100% stock. Overall it directed to around 25% average gold but at times held 0% gold, at other times around 70% gold. For those in a withdrawal phase (retired) a 3.33% 30 year SWR was supported for all 30 year periods since 1896, you both had your money returned via 30 yearly inflation adjusted instalments, and also ended with the same or more as the inflation adjusted start date portfolio value still available at the end of 30 years. Or in the worst case supported a 4.5% SWR, leaving nothing left after 30 years in that worst case outcome, but on average left 2.5 times more in inflation adjusted terms at the end of the average 30 year case outcome.

More recently, start of 2023 and AIM was indicating 16% gold weighting at year start, down from 22% at the start of 2022. In effect is sayings its neither a particularly great time for stocks (don't bother holding any gold), nor a bad time for stocks (hold a relatively high chunk of gold), is simply suggesting mediocre stock times, in reflection of the Dow/Gold ratio level being somewhat average.

Clive

Hi Toofuzzy

What is SWR ?

ALSO physical gold has a very high trading cost. I would own a miner over a depository like IAU . In my case I like streaming companies specifically WPM which has done much better than the underlying gold / silver.

Hi Steve

Do they use Nitrous Oxide (laughing gas) in the UK?

Hi Adam

About cash. My SWVXX Schwab money market fund is now yielding 4.67% which is a marked difference from before. Before, cash was deadwood bringing performance down, but now it makes much more sense to follow the vWave and hold the recommendation in cash. I think AIM works much better in times of moderate interest rates like today, than when the interest rate is zero.

Hi Tom

Hi Clive, I forgot to mention that in my version of the Talmud portfolio it's actually 30/30/30/10 with the last 10% being a cash reserve. We've been letting the dividends collect in the Cash column and have been able to rebalance using the reserve in most instances. That helps defeat the "All Ships Rising At Different Rates" problem that Rebalance can have.

Rebalance is less stressful when there's cash available. There may be no need to sell something just because there's a need to buy in another sleeve. It appears that this is going to work out well over the long haul.

AIM S&P500 real price since 1871

Started 2023 with 75% cash being indicated !!! I suspect that high level is somewhat a reflection of US taxation policy changes in the mid 1980's to incite more of earnings being retained rather than paid in dividends - somewhat accelerating price appreciation ??? Or maybe a wise AIM decision :) When it seems quite popular at present for some to be loading heavily into TIPS/iBonds ladders that are yielding positive real yields following large declines in bond prices in 2022

Clive

a Gold/Stock/REIT Rebalance blend that has been working well since April of 2021

Lumping in/out

Elsewhere on another board, yet another periodically highlighted how ...

example periods of time when the SP500 required more than a decade to “permanently” exceed a previous high water mark

20 yrs. May 1901-Aug 1921

20 yrs. Aug 1929–May 1949

15 yrs. Nov 1968-Mar 1983

13 yrs. Mar 2000- Jan 2013

Exactly. Almost nobody lump sums in on the peak or trough

I watch the Accumulation/Distribution of IAU over time. It gives good correlation with price change most of the time.

Was gold a good hedge 2008 to 2009 and Spring of 2020 ?

InvestorsHub web site was previously just about tolerable, but in more recent form (not sure as from when as I don't visit that often nowadays) its almost beyond usable for the ageing eyes/laptop visitor that employ larger fonts.

A top of page video detaches to place itself across the bottom/middle screen region when you scroll down on nearly every page/click. Header section takes up most of the top half of screen. And where things simply don't scale well when a non micro-text default is being used.

I guess maybe OK on a desktop/larger screen, but I mostly use a laptop of just modest screen size.

Apologies if I don't respond to posts, not intending to be rude/ignoring, rather its just a case of (dis)comfort of usage.

Clive

Want to Beat the Stock Market? Avoid the Cost of ‘Being Human’

https://www.wsj.com/articles/active-vs-passive-index-fund-beat-the-stock-market-58e8bd83?st=0v7d1rmgtuwozx0&reflink=desktopwebshare_permalink

The typical fund returned an average of 7.7% annually over the three decades, after fees. Fund investors, however, earned only 6.9% annually because of their chronic compulsion to chase hot performance and flee when it goes cold.

Such buy-high-and-sell-low behavior tends to flood fund managers with cash at times when stocks have already risen in price—and to force the funds to sell stocks after a decline. The managers can perform only as well as their worst investors allow them to.

That cost of “being human,” as Prof. Bessembinder puts it, is almost as high as the drag from annual fees

Applying the same to US data, VISVX / gold ratio, and levelling the AIM %cash (gold) to the same as the UK version at the start date ...

... worked well

The mid section third (cash) chart would have dropped closer to 0% has a 5% MTS been used instead of the 10% MTS I set (fewer/larger 'trade' frequency).

Clive.

... on second thoughts !!! ...

The stock/gold ratio at the start date was pretty low and as such it would have been more sensible to start with a relatively high stock weighting/low gold weighting. Adjusting for that (to a 25% initial gold weighting) and AIM excelled constant weighted, averaged near 40% average gold over the total period, and to more recent lagged 100% all-stock total returns by just 0.7% annualized. It did lag all-stock in the 1990's big stock up-run, but has subsequently closed down that gap.

UK FT250 is much like US small cap value and I've noticed that partners well with gold, tending to both have similar levels of volatility and a degree of multi-year low/inverse correlation. US data for SCV/gold is also noted as giving 100% Total Stock Market a good run for its money, with less risk (portfolio volatility) PV US example for the similar years. And considerably better if you adjust that PV example start date back to 1972 (the oldest data that PV has available).

Monte Carlo sim was also significantly better

MC for 60/40 SCV/gold 4% 30 year SWR and ditto for 100% Total Stock Market MC suggests differences of >99% success rate compared to 86% success rate respectively.

Indicative of how the likes of the vWave as a indicator of initial loading/weightings can make a relatively large overall difference in outcome.

Clive

AIM of stock/gold ratio

Similar to the Dow/Gold ratio I loaded UK FT250/gold ratio (midcap stock index price to gold ratio) and AIM'd that with default settings (initial 50% 'cash, 10% SAFE, but did opt for a higher 10% minimum trade size).

For monthly reviews ...

Using AIM indicated %CASH I set that as each months percentage gold weighting, the rest being in stock (total accumulation index that includes dividend being reinvested), and that broadly averaged 50% AIM cash having been indicated. I then compared that to the monthly constant 50/50 stock/cash total returns.

Generally a high Dow/Gold ratio (stock/gold ratio) is suggestive of high stock prices/low gold prices, and equally a low ratio suggests low stock prices/high gold prices. Adjusting stock and gold weightings in reflection of that as directed by AIM resulted in inconclusive overall benefit/or-not. For the earlier years that had relatively high AIM %cash (and hence gold weighting), but then in around 2009 the stock/gold ratio dived and had low/no gold being suggested (all stock), a great time to have rotated into that (Financial Crisis lows).

So broadly lagged, but then jumped to lead. Overall is winning, to the more recent date, but could be argued either way as having been good/not-so-good.

At one point the AIM directed / constant weighted was lagging by a 0.8 factor (so in total having a -20% lower $$$ portfolio value). As of recent that has spiked to it leading by around a 1.4 factor (so in total having a 40% higher $$$ recent portfolio value compared to constant weighted.

Pushed to approximate recent relative values and I'd agree with AIM, with FT250 stock index values being relatively low, gold values being relatively high, so AIM in that sense has made a reasonable call, given no more than just historic prices data.

Just thought I'd share the observation.

Happy Easter to all

Clive.

3x stock, short term treasury, gold (silver pre 1976), yearly rebalanced thirds each

Minimum 30 year SWR = 4.6%

Hi Tom

He thinks he has it tough!!! I have a Triple Mandate!

1) Price Appreciation over Time

2) Dividend Capture over Time

3) Profitable Volatility Capture over Time

That's where the 3X leveraged funds don't cut it. No #2, Questionable #1 while working #3 as hard as possible. Plus high annual expense ratios.

This is a PV example (US data) comparing 20/80 SPXL (3x leveraged S&P500) and IEF (7 - 10 year treasury ETF) to that of 60/40 SPY/IEF

On the basis that ETF's could fail, potentially along with their custodian with them - perhaps due to some complex fraud, you might hold Treasury bonds directly instead of IEF, which has the benefit of being fully protected, no matter how much $$$ is invested.

Similar overall reward, but with 80% in the safest asset (Treasury bonds), instead of just 40%.

In that link I left it set at yearly rebalanced. In practice the higher the leverage the more often you should rebalance. 2x and once/year is generally sufficient, 3x and 6 monthly is a reasonable choice. 10x and you're looking at monthly rebalancing (basically what Zvi Bodie does, where he holds monthly Traded Options that reflect 10x leverage, so for instance for a conventional 60/40 stock/bond allocation he'd instead hold 6% in 10x leveraged stock exposure, leaving 94% in safe (treasury) bonds).

Clive

RE: Leveraged ETF's

I exclusively use leveraged ETF's - but from a counter-party risk reduction angle rather than scaling up exposure. For example a third as much in a 3x as would be held in a 1x. Nowadays (retired) wealth preservation is more important to me and since the 2008/9 financial crisis there's been greater tendency towards bail-in's ... where investors/savers are increasingly more likely to fund the bail out of banks/custodians in the event of failures, rather than taxpayers. Shares are commonly pooled, not actually yours, just a record of your name/share of that pool. Bank deposits aren't yours, again just your name recorded. Single bank/broker (custodian) risks are low, but do periodically present. US protections are better than for the likes of me (non-US) such that I keep counter-party risk down to below 20%, as such a loss whilst unpleasant is no different to what a portfolio may lose in some years naturally.

Leverage ETF's do tend to (proportionately) attenuate downside, amplify up-side, due to their daily rebalancing (reduce-low/add-high). The 'trick' is to play/work the trends/turning-points. IIRC Ocroft some years back presented a method whereby he'd delay actual trades until a existing trend had passed, for instance if AIM signalled sell, then he'd wait for subsequent sequential AIM sells to end before actually making a trade. Looking to place larger amounts traded at just past the peak (or just past the trough for sequential buys). I don't know how effective or not that was, nowadays I don't really trade other than via directed withdrawals.

Clive

AIM had the better left tail (was safer)

(supplementary image for completeness)

When the worst case is better, so that equates to a higher overall SWR (as standard SWR figures reflect the worst case outcomes)

Favorite Chapter,

"The Reliefer Who Made a Fortune in the Stock Market" is my favorite chapter. It is a bit sad, but it has a lot of wisdom in it.

I like the answer to this question:

"Mr. S.", I said, remembering my assignment, "what is the mistake most investors make in the stock market?"

"The answer is ignorance. Buy only stocks in things which are necessary, and buy only the leaders: AT&T, General Motors, United Steel, and so forth. They will always win in the end .......

1929, in particular a September start month was conceptually a worse start year for AIM, particularly if you were using a 4% SWR. Basically burned through cash quickly to leave you all-in with further and pretty deep declines yet to come. AIM pretty much remained at all-in thereafter for the full 30 year term. However even though all of cash had been deployed within a year or so, that meant you had around 40% more shares than a investor who had lumped 100% into shares from the start, as many might have been tempted to do around that time given how even shoe-shine boys were talking-stocks and many were borrowing as much as they could to buy stocks ... in the lead up to the Wall Street Crash.

That AIM, that was near-as all-stock (but with 40% more shares) went on to do OK, basically supplemented dividends by selling some shares to pay the SWR and carried a retiree through 30 years OK, even at a 4% SWR rate. Only had around 16% of the inflation adjusted start date amount available at the end of 30 years, but still succeeded in a 30 year 4% SWR objective.

The 3.33% SWR was considerable more successful, got back into AIM trading/some-cash in later years and went on to end 30 years with having more than the inflation adjusted start date amount still available.

Of course AIM hadn't been invented back then, at the start of 1929 Robert Lichello was only 2 and a quarter years old (kids like to count part years as for a 1 year old a year is a lifetime :)

Clive