News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

dr_airtime

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

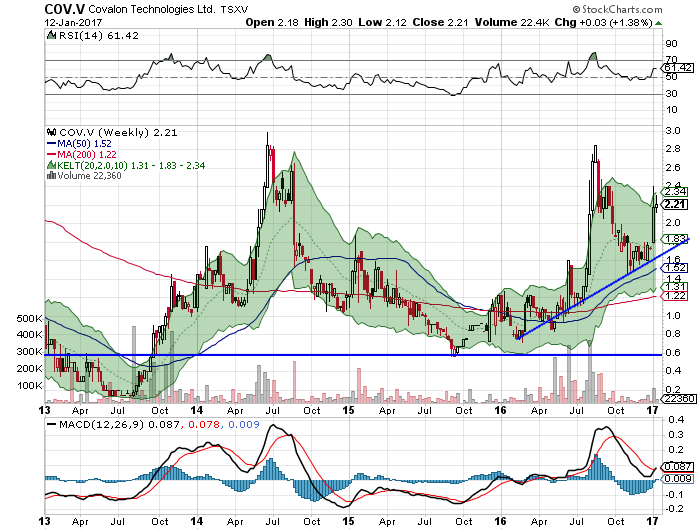

COV.V - Case for double in 2017...

...is very well laid out. Not a zip code changer in 1 year, but thought I would post here anyways.

Covalon came out with this PR about a week ago which suggests that Q1 of 2017 should generate positive EBITDA, and earnings (net income) which should put COV.V on Canadian smallcap fund managers radar:

http://ir.covalon.com/phoenix.zhtml?c=183092&p=irol-newsArticle&ID=2233328

I found this post below which confirmed what I saw in my DD (65-70% gross margins). This investor has been following Covalon longer than me. I started tracking once a few people picked Covalon for either the last or second last SKILLZ Pick 3 contest.

He is expecting $CAD 6.5M in total opex in F2017. Total opex for F2016 is tracking towards $CAD 6.1M (4.6/75%)

Covalon could technically come down to the $1.90 level but the analysis above is quick to do any I am sure many other investors are thinking the same so I put in my order at 2.15 today which was filled. Pretty thinly traded too.

Note to get to the $CAD 0.30 in earnings the investor divided $6.5M by (14.422M shares o/s @ June 30 + 5.793M warrants = $20.2M FD shares) = $0.32 in earnings. The 14.422 includes shares issued up to June 30 for conversion of convertible debt. Covalon is now det free with $CAD 3.1M of working capital at June 30.

CGT.TO

Gold $1200? I would take some trading profits!

EDV.TO Endeavour 2.0 = LMC-H.V Leagold

Former Endeavour CEO who led the charge building out Endeavour apears to have left and started Leagold.

First transaction is buying Goldcorp's Los Filos mine with 2 years of open pit reserves left.

Put it your watchlist and we'll see if they build another Endeavour.

http://finance.yahoo.com/news/canadas-goldcorp-sell-mexican-mine-150252922.html

http://www.leagold.com/

TV.TO + 0.16/14% - anyone see any news?

No explanation other than someone couldn't wait to see if Trevali would head to $1.00 level or consolidate for a bit? Anyone see anything on the news front?

May be time to buy back in.

Re: Auryn AUG.TO...

...future looks bright for Auryn with 100% of a previously unexplored greenstone belt in Nunavut, trouble is, in hindsight of course, the time to buy was during early stages of 2016 rally as Auryn went +400% to peak in 2016 and is still +340% from January 1, 2016.

I would consider adding on a pullback to 50 DMA though as there should be many mines on Auryn's properties, the question is though, how far into the future - 10 years?

DPM.TO + 0.48/17%...

...the Christmas gift that continues to give! I'm plus 60% on most of my family's accounts and was (and now strongly is) largest holding in all of them.

Beigledog - becuase...

...they are good at operating mines in the Canadian North. Hits -40 (celsius) in Nunavut in the winter.

DPM.TO - staying long, + SBB.TO update

Up again today so will hold as long as Gold looks like it will may a start-of-year rally.

Dundee will be a 270 au-oz per year producer in 2019 when Krumovgrad hits run-rate production in 2019. They will start building this year with first ore in H2-2018.

They also own 10% of SBB.TO Sabina which, has been put back 1-2 years through some environmental permitting issues, but I bet will be bought out by Agnico Eagle for +$USD 500M or $50M to DPM.TO when all the permits are in place.

http://www.sabinagoldsilver.com/news/sabina-gold-and-silver-provides-update-on-permitting-for-the-back-river-gold-project-nunavut-canada

Apparently - Dunnedin also asked the Federal Minster to intervene with the NIRB and hasn't recieved feedback. They are first inline so there will be no news on SBB.TO until Dunnedin has received news.

http://www.dunnedinventures.com/2016/04/11/dunnedin-provides-community-consultation-permitting-update/

DPM.TO +0.35/15%

+15% on a combination of market catching up to 84m @ 14 g/t & 2.87% Cu after Holidays and potential technical breakout of recent downtrend.

Best performing larger MC gold/silver equity today out of the 96 listed intermediates/seniors here by Kitco and you heard it here first with a few posts from me along the way....

http://www.kitco.com/stocks/companyname_asc.html

ASR.TO not sure...

...must of been a GDX to GDXJ transfer of shares or vice versa? Year end rebalance?

Good way to end new year.

Portfolio crazy green today including my NUGT position +23% and Victoria Gold VIT.V + 15%. Nice.

Been holding Victoria so not in the money but it is a hold for me until a buy-out which I am crossing fingers for. Nothing a sure bet of course. If it was one of the best candidates it would have been bought already in 2016.

My Miners Tax Loss Selling Portfolio

FYI - loaded up on gold/silver miners from Dec 20th-23rd. Thesis here is hoping for at least a strong bounce into January and then reassess for longer term at that point. Everything is now in the money and I tried to buy the miners I was familiar with that had the most oversold charts going into Dec 23rd (last day of tax loss selling in Canada).

Here's what I bought in the smaller category FWIW. I also bought First Majestic, Mag Silver, Pretium and Gold Fields (GFI) with GFI being a favorite tax loss sellin buy of CL001

Alacer - building sulphide expansion fully funded and will be operating for 15 years +

Dundee - announced transormational 84m @ 14 g/t + great by-product grades next to existing underground infrastructure at bottom of market.

Sandstorm - easy pick for a bounce. Story here is all POG.

Teranga - the $.60s/.70s have always been good to me since the merger with Oromin (.60 to 1.20 in a few months). Cost here is 0.72 and it is already looking like TGZ is going higher.

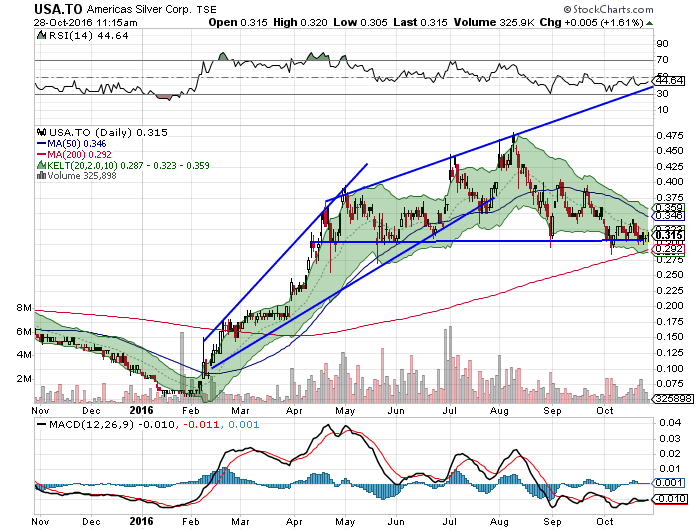

Americas Silver - turn around complete. Market will figure it out eventually. If Zinc goes to $1.50/lb in 2017 and Market looks and sees Americas producing 50M lbs of zinc for 6 years (43-101 pre feas) then USA.TO will fly in H2-2017 IMO. Not super oversold but 2017 should be the year for Americas. Below is the stockcharts corrected chart for the 12:1 share consolidation.

NXE.TO - thanks.

Cameco dropping below 2009 lows after a 8 month continuous downtrend was a big part of that thesis.

Haven't looked at Uranium in a bit but when Cameco breaks down trend the bear is over.

DPM.TO - PP at $2.45, buy at $2.00!

http://finance.yahoo.com/news/dundee-precious-metals-announces-c-003400601.html

Tomorrow is last day of tax loss selling. With Dundee's transformational drill hit from a few days ago and a fully financed balance sheet for Krumovgrad things looking good for the next years. You've been able to buy around C$2.00 for the last couple days. Worth a shot here and imagine DPM will be back at $2.45 within a month of the sector rebounding, then we'll assess for the current state of the Gold Bull - it does appear dead in the $USD but is still on in the $CAD

DPM is sitting on the support where it broke out from the 2009 financial crisis lows. Could go lower. I doubt so with the 84M @ 14 g/t just announced.

DPM.TO - 84M @ 14 g/t

One of the hits of the year. Released at 12:12 PST for some reason. Hoping that market totally missed this today and just put $20k into DPM for a trade. Hits like this next to existing u/g infrastructure sent Richmont (RIC.TO) and Wesdome (WDO.TO) soaring in the last two years.

http://www.dundeeprecious.com/English/Corporate-News/press-release-details/2016/Dundee-Precious-Metals-Announces-New-High-Grade-Copper-Gold-Zone-Discovered-at-Chelopech-Mine/default.aspx

Had this earmarked for other miners. We'll see if I'm right tomorrow morning!

Now to get back up to speed on DPM....buy first and now I have to ask questions.

USA.TO...

...maybe market just figuring USA has bottomed and should outperform becuase it has barely budget in 2016 compared to other silver producers that are still up in the stratosphere from a chart perspective. I didn't sell any on trip down to low 0.22's but looks like before year end is the time to add.

Zinc - must read...

...interview with Doug Ramshaw of VTT.V on current state of zinc market and potential for metal to rally in next couple years. Link back for background on VTT.V as well. I met with Doug when he outlined the Corex Gold story for me (CGE.V - godfather of heap leach start up)

For those that followed me Trevali has doubled and locked in my profits. Hoping to buy back a bit lower.

https://ceo.ca/@newton/deep-dive-on-the-zinc-markets-with-doug-ramshaw-vtt

GRG.V/GARW - Silver Standard Buyout

Golden Arrow's Chinchilla Project could be fully bought out by Silver Standard as their Piraquitas mine runs out of ore. Chinchilla is 30km from Piraquitas and Silver Standard and Golden Arrow have struck a deal for a 75%/25% JV. I think the more likely sceanario is Silver Standard buys out the 25% for a fair value (read=full value) since 50% of Golden Arrow is held by tight hands.

There are tons of articles out on this but I'm looking for a valuation calculation anyone else out there may have seen who follows Golden Arrow.

i think buy-out could range from USD 50-100m. Could be a cash cow as there is likely little up-front capex, but higher cash costs with trucking 30km. Lower end of USD 50M is around $CAD 67M vs. current market cap of $CAD 75M. Get the rest of Golden Arrow for free who is one of biggest land holders in Argentina.

The best find I have is this conference call link from third article below

http://blog.geckoresearch.com/wp-content/uploads/2016/11/SSO_2016-11-9_QF_Conf_Call.mp3

https://www.theaureport.com/cs/user/download/co_file/4794/2016-05-18_TNM.pdf

http://seekingalpha.com/article/4026661-golden-arrow-resources-silver-standards-upcoming-silver-joint-venture-great-value

https://www.theaureport.com/pub/na/a-decision-on-golden-arrows-chinchillas-project-could-be-near-plus-the-election-and-precious-metals

TV.TO - taking profits.

Sub 0.60 to 1.35 right now in about 5 months. Not bad. Zinc gone from 0.90 to 1.23 right now.

I just put in orders to try to sell most of my TV.TO at 1.35 based on chart below. Zinc bull has a long way to run yet but i'm trying to get better at taking profits. This has also been my biggest position for about a month.

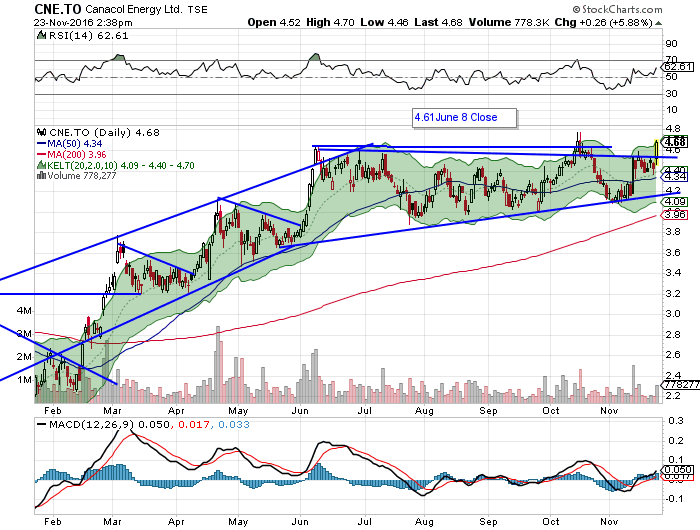

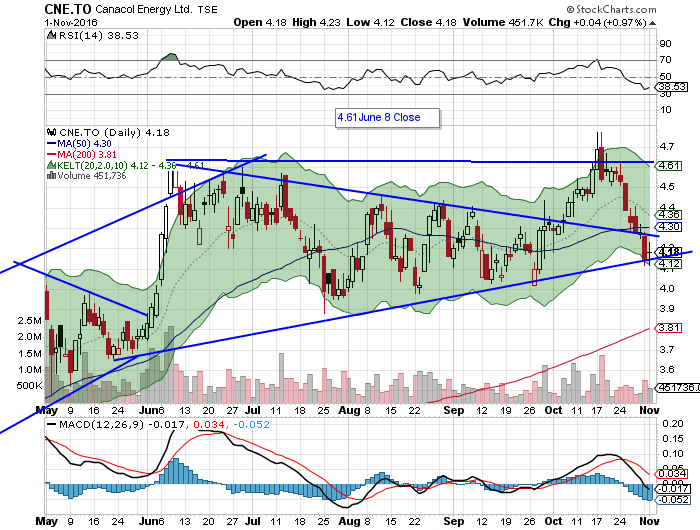

CNE.TO - must read PR and new 104 wk high...

...or set to close at new high currently trading at 4.69. See the PR below and my post over on IV below too. You are getting drilling results from 2016 for free, future expansion for free and oil property upside for free.

http://www.canacolenergy.com/i/pdf/nr/11.23.2016.pdf

http://www.investorvillage.com/groups.asp?mb=17397&mn=40648&pt=msg&mid=16599142

GPM.V...

...risk reward perhaps better than when I bought. Market Cap now down to $CAD 4.5 million. If they hit a solid intercept when they do the RC drilling on the northwest anomaly it could be a single day 10 bagger from here. Could also find nothing though.

GPM.V - zinc exploration. First drill results. Nothing....

...so far but never explored here before due to multi decade land access issues. They tested the outcropping gossan which makes sense (lowest hanging fruit) but market will now be waiting for RC results from next target to northwest I extracted below. From what i understand lead is an indicator you may be near the system but looking for world class zinc-lead hits (+50m, +5% zinc-equivalent) intersecting the heart of a mineralized system.

The RC drilling will infill the wide spaced diamond drill pattern and then move northwest to test a combined magnetic and gravity anomaly.

The North – South trending magnetic and gravity anomaly is located 5km north of WD#7 and 1.5km west and down-dip of the outcropping gossanous Balbirini Fm. This anomalous feature is interpreted to be a basin margin fault and the potential major conduit for mineralising fluids

Press release:

http://www.gpmmetals.ca/node/72

Locations and results detail here on website:

http://www.gpmmetals.ca/australia

Uranium bottomed? NXE.V & CCO.TO breakout

...Cameco broken downtrend. NXE bounced off $1.40 support. Pain not over for Uranium but maybe prices bottomed?

Copper broken upwards to so perhaps market is saying industrial commodites bear market bottom is in.

Here is great article overviewing the fundamentals for Uranium sector:

https://ceo.ca/@danielm/uranium-collapse-signals-2020-supply-shock-goviex-ceo

TV.TO - oops..

..I was tearing through the Q3 FS before the press release came out (I use stockwatch.com) and was looking at 9 month YTD CFOps for My EBTIDA guess. Too high. Sorry. They disclosed $CAD 15M for the quarter in the PR, though they don't provide a calculation anywhere in the MD&A. I think $CAD 15M per quarter could average $CAD 20M/quarter in 2017 with higher zinc prices and Caribou ramped up. This would be $CAD 80M annualized so $CAD 495M EV/80m = 6X EV/EBITDA.

Trevali pretty fairly valued for two mines but in a zinc bull I'm planning on market bidding up Trevali into a few tradable highs that can be sold for profits. I'll let you when I think that is :) It is simply the best zinc leverage alternative for North American investors.

TV.TO Trevali + .06 to 1.17 on Q3 results and...

...zinc going from 1.11 to 1.17 today. Newly commissioned Canadian Caribou mine operating at 2/3 of 3000 TPD capacity in first quarter of commmercial production in Q3. Average zinc sales price was $1.03. Did $CAD 32M in CFOps before WC changes as proxy for EBITDA in the quarter.

When Caribou is fully ramped and if zinc holds say $1.20 for 2017, with the combination of revenues going up and cash costs down at Caribou this $32M in EBITDA could become $45M per quarter or $CAD 180M annualized. MC is $CAD 384M and net debt (including leases) is $CAD 110M for ~$CAD 495M EV or only 2.75X EV/EBITDA.

(note - Trevali reports in Canadian, but cash costs and some other production metrics in $USD)

With zinc on a tear and Trevali the only pure-play-producing zinc miner available on North American exchanges, and a junior, the sky is the limit for how much the market wants to bid Trevali up.

In hindsight I've noticed that Hindustan Zinc on the Bombay exchange may have been the best public-markets pure play (they now operate the largest zinc mine in world in Rajhastan with Australia's Century mine closed). It has doubled, Trevali has tripled in 2016.

USA.TO/USAPF - also zinc...

...50 million pounds. If you've been following my posts on zinc your conclusion should be "the bull is on". Zinc +.06 today to $1.17/lb. My most overweight position Trevali right now is also at 1.17 share price! See the 5 year chart here:

http://www.kitcometals.com/charts/zinc_historical.html

Zinc took it's third tap at the $1.10/lb ceiling and blasted through. If zinc is at $1.30 next year when San Rafael comes online then AISC is going to be even more negative.

The San Rafael Feasibility study assumed $.85/lb zinc. If Zinc is $1.30 next year that is +$0.45/lb x 50 million lbs = $22.5M in annual revenue higher than expected. The average revenue in the feasibility for years 1-5 is $45M so the zinc pricing upside has the potential to increase revenues by 50%/year from the pre-feas. Dependent on zinc price of course.

Also - page 154 below shows annual zinc production of about 40M pounds so not sure where USA is getting 50M from. Maybe a pump as they know the zinc bull is on.

Page 153 - pricing

Page 154 - revenue calculation

http://www.americassilvercorp.com/i/pdf/reports/SanRafaelReport.pdf

FYI - pretty

Copper...

...maybe better observation is "the low appears to be in so there could be a tradeable net move higher over the next couple years". Copper not going back to 4.50 anytime soon of course.

Vicious 5 year downtrend broken that is all. This has also pulled copper miners down so I think once the recent skyrocket upwards in copper corrects it is worth allocating some capital to copper producers that are a going concern.

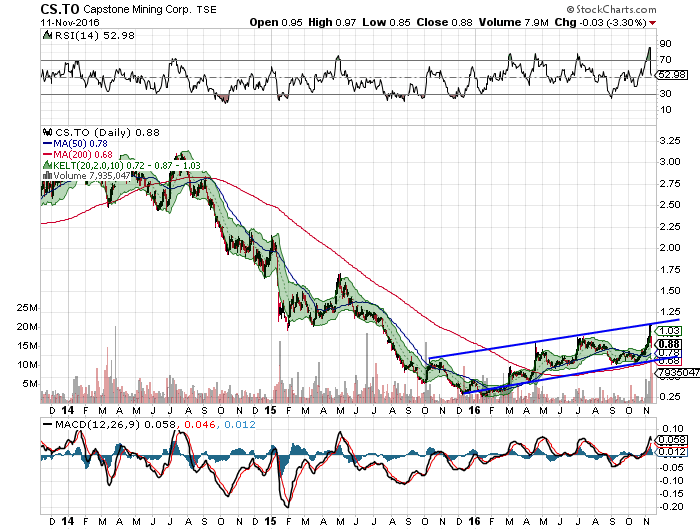

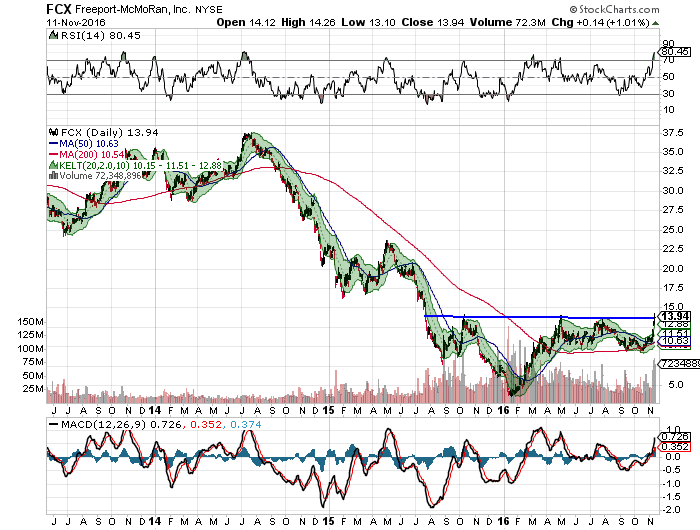

Copper Bear Market Over. Here are some ideas.

2 Hrs of idea generation into this post with basically "high level scan DD" **Please reply with any thoughts/opinions on miners to buy** chart saying bear market now over in Dr. Copper.

Copper went up for 14 straight days before going down friday. As always the media is wrong and this was not because of Trump, but was a purely technical event as Copper broke its 2011 downtrend. If you look at daily chart Copper is super over bought so will retrace probably for the next couple weeks but the message appears to be the bear market is over. Here is a copper chart and some ideas for junior copper producers (Capstone - $C 281M MC; Copper Mountain $C 107M MC; Nevada Copper - $C 73M MC). Just for fun I threw in $US 19B MC Freeport which is the no brainer hold if copper does go higher over next year.

Copper Mountain - CUM.TO. Single asset 17 year mine-life 0.34% P&P LOM grade open pit in BC. $C 107M MC with $C 322M in low-interest debt. Have barely been surviving last year but just hit record throughput at 42k TP in Q3-2016. This is most leveraged play.

Capstone Mining. $C 281M or $USD 208M MC with $US 224M of Net Debt for $US 432M EV. Just did $US 50M in EBITDA in Q3-15 or $US 200M annualized for 2.16X EV/EBITDA. Have three mines - Pinto (Arizona), Cozamin (Mexico), and Minto (Yukon) so much less risker than CUM.TO above.

http://s2.q4cdn.com/231101920/files/doc_news/2016/oct/2016-Q3-Financial-Results-NR.pdf

Nevada Copper - best undeveloped asset of scale in North America. Fully permitted, private land, water, power, natural gas all close-by, Nevada, Solar Power deal in works with Berkshire Hathaway, likely to be sold in competitive auction in next couple years IMO. 0.41% open pit LOM grade. Chart has huge upside but also risk as they can't dilute equity en-route to construction with capex >$1B so need a buyout.

http://www.nevadacopper.com/i/pdf/NCU_CP.pdf

And finally...Freeport.

Zinc holding past $1.10...

...1.125 again. I wish I took a screen shot of how zinc leaped past $1.10 on third try. Went from $1.09 to $1.12 in about a minute. This means the bull could be on.

Trevali TV.TO is currently my largest position as a result. Trader overweight as looking for quick jump from $1.00 to $1.20.

VTT.V is currently selling off since 321gold.com put it on the map a few weeks ago. Potentially lowest Capex-to-production near-term zinc play. I'm going to talk to one of the corp dev guys there as he is the same guy working for my Corex Gold (CGE.V - Godfather of heap leach) holding.

http://www.321gold.com/editorials/moriarty/moriarty092616.html

My thoughts on Uranium, Nexgen & Cameco...

..I've never spent time to follow the sector closely before. Many here have. I have traded NXE.TO NexGen to a near-100% in 2016 as the one of the best uranium discoveries ever in the Athabasca Basin. Most Athabasca basin Uranium underground deposits are contained in the boundary between the sandstone and hardrock, making mining challenging and often requiring expensive freezing. NexGen's arrow is hosted in basement rock. Arrow will be a mine, the question is who will buy them out. When Nexgen bottoms before the end of the year the only question is how high will it go? Where it bottoms no one knows!

Here is presentation. Very simple.

http://www.nexgenenergy.ca/_resources/presentations/corporate-presentation.pdf

On Nuclear - tons of French reactors are offline (20 o 58 at last report) so this likely explains a large part of the recent 50% selloff in spot uranium.

Also - a group of friends here in Vancouver mining-land have learned an important life lesson again relating to the lowest cost diversified miner in the world Teck Resources (TCK/TCK.TO). That lesson is "buy Teck at the bottom of the commodities bear market. You will know when this has occured when Teck breaks out higher above a trend line after a massive decline". Look at a chart. December 2008 post-financial crisis and December 2015 commodity market lows (in hindsight of course!) were amazing buy-opps for Teck.

What does this have to do with Uranium? Well the same rule, but for Uranium bear market lows should apply to Cameco (CCO.TO/CCJ) who is the lowest-cost uranium producer! I think if Cameco goes down to $10 (TSX) or lower during the last two tax selling months of 2016 it should easily return to $15 in 2017 even in a bear market for uranium.

Put NXE.TO on Watchlist - anyone following Uranium?

My word. Uranium is in the pits. Dropped from $40 to about $20 in two months. Cameco has shuttered Rabbit Lake and US In-Situ operations and still spot pricing goes down (most production long term contracted).

http://thestarphoenix.com/business/mining/layoffs-continue-at-cameco-corporate-office-months-after-rabbit-lake-shutdown

This should be a good opportunity so pick up NXE.TO when it bottoms. Where that will be no one know but no need to rush. Could bottom around $1.30 to $1.40 on support per below or decline to around $1.10 where there is a gap to fill from the upside surprise on their maiden resource estimate from March 2016. I would think spot Uranium would have to drop to $10 for the latter to happen.

http://www.nexgenenergy.ca/news/index.php?&content_id=178

Feeling like a genius selling my NXE back in the mid $2.00s earlier this year.

NXE going back on watchlist. Should be a major bottom in the next two months. Likely not to happen on Dec 23rd last day for TSX tax loss selling IMO. Could be this month. Best Uranium (future) mine discovery in decades. There has to be a suitor out there watching closely and waiting for bottom and a low 20 day trailing moving average.....

CNE.TO/CNNEF

I bought a bunch at 4.30 when it looked like it was breaking out. It closed about the previous 104 week high for a day and then walked right back down. Kind of caught up with short term oil sell off. I still wonder when the market will start treating Canacol like a lower risk, fixed price, contacted natural gas producer.

Not selling as think we may have bottomed on a support line and we'll see if she goes up back higher.

Zinc just leaped past 1.10...

...in last 30 mins. At 1.11 now breaking previous high from a few years ago. If this holds the zinc bull is officially on. Pretty limited list of juniors to buy

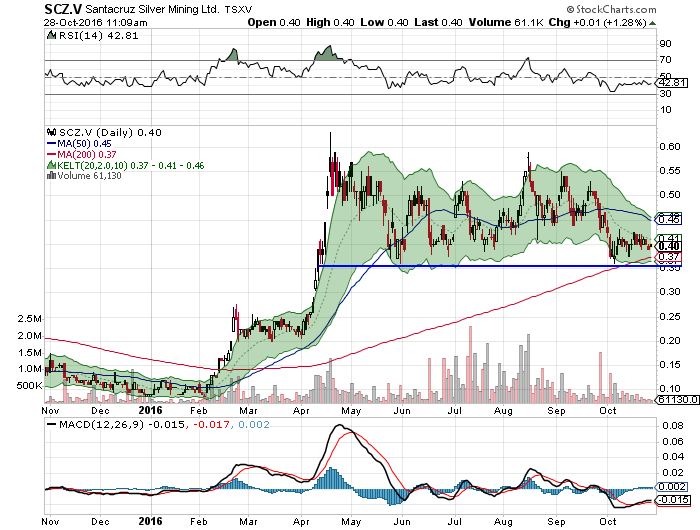

USA.TO - also look at SCZ.V Santa Cruz

Will take a look this weekend but both USA.TO and SCZ.V are small silver miners that are consolidating like a coiled spring ready to move higher. In next phase of Silver/Gold market I would think these two outperform the now-larger cap intermediate and senior silver producers simply becuase the latter have been bid so high (even with recent correction).

Will look into Santa Cruz again this weekend. Seems operationally higher risk than USA.TO who have proven their turn around. Here is a starting point:

https://www.theaureport.com/pub/na/santacruz-silver-mining-the-market-still-doesnt-get-it

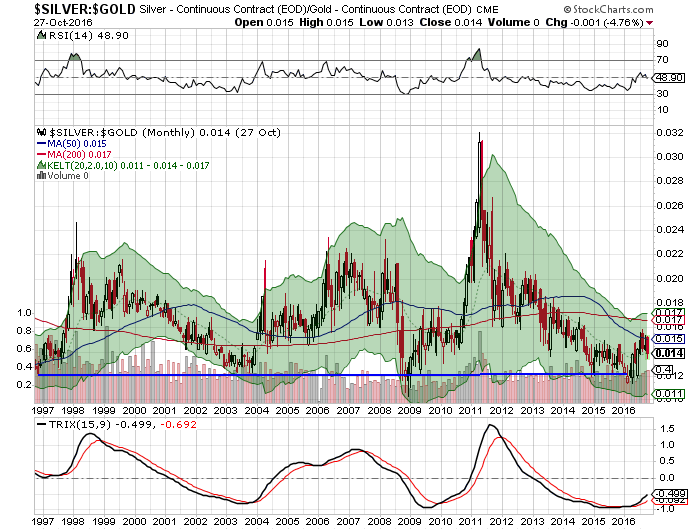

A couple charts comparing SCZ and USA (identical!) and a reminder where we are at with the 20 year silver to gold ratio. Have a good weekend!

USA.TO - Scorpio more of a merger...

...Sprott but USA ex-Barrick Manager in charged of USA when they merged US Silver with RX Gold. RX Gold shut down later and likely never to open again as veins aren't really continuous, though they are high grade. Impossible to mine. Sprott was largest SH of both I believe.

Sprott also largest shareholder of Scorpio I believe so behind merger of Spcorpio and US Silver to rename 'Americas Silver'. '

...just a bit of context. See my next post after this!

USA.TO - yup agree with all of that.

I'm following what zinc does very close and the combination of simply continuing to execute with low cash costs/AISC and the zinc price going upward will eventually lead to a quick double in USA.TO just like EXN.TO earlier this year IMO.

Frustrating to hold when all other silver miners were into the stratosphere earlier but USA's time will come!

Zinc is on fire last two days +.05 to 1.07

Was a 1.01 on Friday, now 1.07. Reminder, if zinc breaks $1.10 in next couple weeks the bull market is on, otherwise if could set up a head and shoulders bottom by going back to $.90. Rest of this week and next week looks exciting!

XOP.V - Africa Oil of late 2016?

+.02 to $.15 this morning on 6X average volume.

Remember when Africa Oil went from $1 to $10 in 2012? There is that potential here if XOP hits.

News from my swing-for-the fence play this morning that partner Exxon will start drilling deep water Liberia Well in a month. My cost is $.12 here and would be ecstatic to sell at $.24 and ride free shares into drill results but we'll see.

http://www.proactiveinvestors.com/companies/news/167647/copl-shares-advance-as-investors-look-forward-to-liberia-well

COPL has a 17% carried interest by Exxon in an offshore Liberian Block that is one of the few where a Junior is involved in Offshore West Africa.

Original idea here comes from Warren Irwin who outlines the long thesis well and "pumps" the opportunity big time saying:

I've been in the business 30 years, and I have never seen a higher-octane, more awesome risk/reward situation than this one, which involves the former CEO of Oilexco Inc., Arthur Millholland.

If XOP is successful just remember to sell before Arthur runs the company into the group again!

https://www.theaureport.com/pub/na/hedge-fund-chief-warren-irwins-blockbuster-uranium-call-and-his-best-metal-and-oil-plays

FYI - there is an important lesson to learn here as I was well aware of this story earlier in 2016. That lesson is "buy the TSX Venture oil producer that is drilling the most high impact, highly anticipated exploration well of the year early, before the crown, sell for a double and ride the free shares into the results"

This applied to XOP and also worked for Taipan TPN.V in 2012 who had a high impact well in Kenya. Taipan wasn't successful but I actually walked away with a double+ here based on that theory as never bought back.

Zinc - this week important. Here's why....

Some basic charting on the LME closing price using the charts from Kitco page below

Zinc either keeps going up and breaks 52 week high of 1.091 and then 1.10 from Feb-14 and May 15 within 2-3 weeks or breaks down in 1-2 weeks and goes back to $.90 thereby potentially forming a perfect head and shoulder bottom in anticipation of run to close over $2.00 fueled by speculators. This would be healthy of course.

Wood Mackenzie target during 2017-2019 zinc supply crunch is $3800/tonne of $1.72/pound. If this actually materializes thought, the market is small and the LME speculators should jump aboard and take us to a $2+ overshoot if all goes as planned.

http://www.kitcometals.com/charts/zinc_historical_large.html

CNE.TO - officially off to new 52 week highs.

Has busted past July closing high of 4.61 as of this morning. Operational, fundamental and technicals all supporting upwards trend. Hope everyone bought, I am like the only one posting here these days!

See slide 17 of current corporate presentation that shows a 60% EV upside based on a pre-tax NPV10% valuation of $US 1165M and slide 16 which shows how Canacol's leverage is decreasing dramatically over the next few years.

Once again though, a pre-tax valuation for CNE.TO doesn't make sense as Marginal tax rate in Colombia is 39%-43% (if I recall it is 39% now and increasing to 43% but about a year since I looked at this). See my older valuation post below pic for a reminder

Ultimate pre-tax NPV10% valuation will be higher than $USD 1165 anyways as Canacol drills out its resources so market may ignore this for now.

Takeaway is I'm not sure where Canacol is going for 2016 but there should be a tradable high in next couple months if past price action continues!

http://investorshub.advfn.com/boards/read_msg.aspx?message_id=115409558