News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Cassandra

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Investigations by the Securities and Exchange Commission

Securities and Exchange Commission (SEC) investigations are conducted confidentially to protect evidence and reputations. Important documents could be destroyed if an investigation is publicly announced, so confidential treatment may help to preserve key evidence in a case. A confidential process also protects the reputations of companies and individuals where the SEC finds no wrongdoing by the firm or the individuals that were the subject of the investigation. As a result, the SEC generally will not confirm or deny the existence of an investigation unless and until it becomes a matter of public record.

An investigation becomes public when the SEC files an action in court or through an administrative proceeding. The SEC website contains information about public enforcement actions. For additional information on how SEC investigations work, please see the following bulletin by the SEC’s Office of Public Affairs.

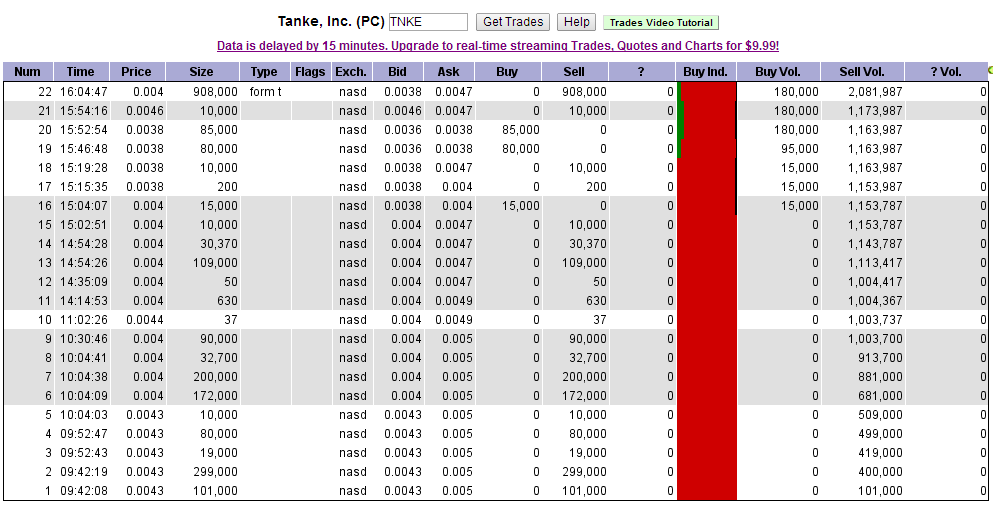

TNKE Form T: 908,000 shares @ $.0040. These are shares that were traded during trading hours but the MM withheld reporting until after trading closed to avoid detection of bulk selling. It is a continuous pattern with TNKE stock.

The closing share price was painted up from $.0038, a new all-time low, to $.0046 with a purchase of 10,000 shares ($46). The bid and ask at the closing appear to have been manipulated up.

The VWAP was $.0041 both for volume during trading hours and total volume when the T-trade is factored in (rounded from $.00407).

Form T trades that are at, near or below the LOD and are large compared with daily volume are often indicative of dilution to a company's float by a financier or insider.

I began reviewing the daily trading data for TNKE on 8/28/14. Seven of the nine trading days since then have had very large, low-priced Form T trades reported. I suspect this trend had been occurring for months.

SRGE filed a Form 15 to deregister its stock in April 2011. Like many OTC stocks that have been suspended by the SEC, there is no registration to revoke. Unless FINRA eventually deletes the symbol, SRGE will be a perpetual grey market stock.

http://www.otcmarkets.com/stock/SRGE/filings

The vast majority of formerly suspended OTC non-reporting stocks simply remain grey market issues in perpetuity. For example, look at CKYS where the CEO is in prison for criminal fraud and the IR firm, Big Apple Consulting, was found guilty of fraud in civil court, yet the ticker remains on the GM.

Eddie Vakser's other stocks include ARTS, PBHG, PRPM, SWRF, TDEY and TSRR. ARTS was suspended by the SEC and the registration revoked.

He is one of the CEOs who came emerged with the notorious IR firm of Big Apple Consulting which diluted dozens of stocks into the ground. Several BAC CEOs have run multiple dilution scams with Vakser being one of the worst.

SUTI was not only a client of the original BAC but signed up for its replacement firm of Boost Marketing after BAC was sued for fraud, for which they were eventually found guilty on all counts. BAC clients who used Boost knew they were going to be subject to more massive dilution as occurred with BAC.

SUTI shareholders should expect toxic dilution under Vakser's reign that exceeds even past dilution.

Info on BAC and Vakser's other stocks:

http://investorshub.advfn.com/Big-Apple-Consulting-Clients-20582/

SUTI share structure a/o 6/30/14:

A/S: 5,500,000,000

O/S: 4,864,693,123 (common only)

Float: 4,551,587,372

Total O/S including preferred shares: 5,177,673,874

Source: http://www.otcmarkets.com/financialReportViewer?symbol=SUTI&id=125489

A/S increased to 5.5 billion on 4/30/14:

http://nvsos.gov/sosentitysearch/corpActions.aspx?lx8nvq=3qx4hm2n442ri3%252fWAZJXGA%253d%253d&CorpName=SUTIMCO+INTERNATIONAL%2c+INC.

... why is the registration not revoked yet?

BioAdaptives (BDPT) was not a formerly suspended stock so is not a valid comparison with KMAG's situation. Prior to the MM submitting a Form 211 to FINRA, BDPT was already a fully-reporting company that had a Form S-1 registration statement declared effective by the SEC. The Form 211 was for initial quotations under Rule 15c2-11.

KMAG is a Caveat Emptor stock that was suspended by the SEC for making false and misleading statements in its press releases. A market maker would be foolish to sponsor such a company.

There is no reason to believe that Jeff Reid is somehow more truthful in Tweets and Facebook posts, many of which don't even make a specific claim.

None of Reid's claims on Twitter and Facebook have proven true and some have been proven to be blatantly false (such as claiming that the audited financial statements were delayed because they needed to undergo a peer review, etc.):

http://investorshub.advfn.com/boards/read_msg.aspx?message_id=105163731

IMO KMAG's financial statements have not been audited, there is no completed Form 10 (it's a FACT that one has not been filed with the SEC) and, even if Reid hints that a Form 211 has been filed, one will never be approved by FINRA.

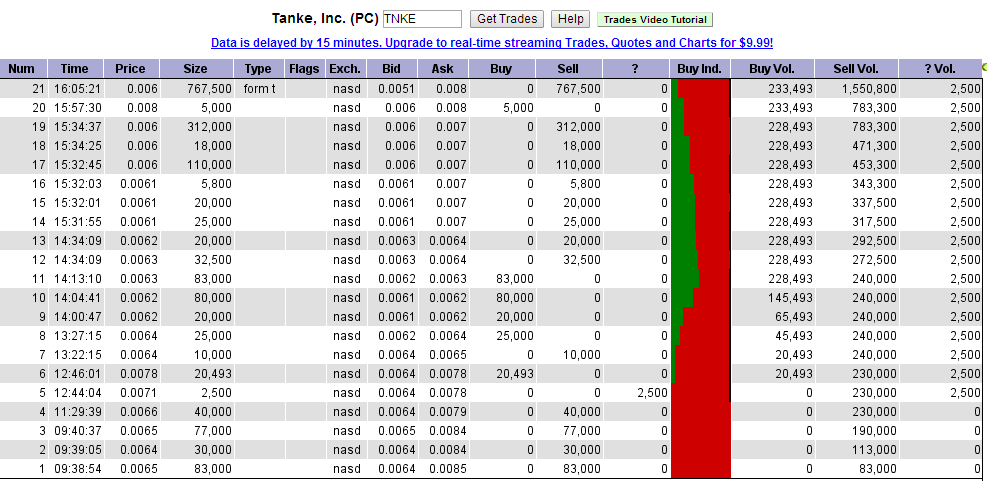

TNKE Form T: 325,900 shares @ $.0051 (the all-time low). These are shares that were traded during trading hours but the MM withheld reporting until after trading closed to avoid detection of bulk selling. It is a continuous pattern with TNKE stock.

For the first time in several days, the closing share price was not painted up. All transactions today were at the bid. The VWAP on volume during the trading day was $.0054, but dropped to $.0052 when the T-trade is factored in.

Form T trades that are at, near or below the LOD and are large compared with daily volume are often indicative of dilution to a company's float by a financier or insider.

I began reviewing the daily trading data for TNKE on 8/28/14. All six trading days since then have had very large, low-priced Form T trades reported. I suspect this trend had been occurring for months.

TNKE Form T: 417,000 shares @ $.0051 (the all-time low). These are shares that were traded during the day but the MM withheld reporting until after trading closed to avoid detection of bulk selling. It is a continuous pattern with TNKE stock.

The closing share price was again painted to $.007 (6,500 shares @ $.007 = $45.50).

This daily pattern of large, low-priced Form T transactions combined with daily EOC paint jobs is very likely illegal manipulation.

Additionally, Form T trades that are at, near or below the LOD and are large compared with daily volume are often indicative of dilution to a company's float by a financier or insider.

I only began reviewing the daily trading data for TNKE on 8/28/14. All five trading days since then have had very large Form T trades reported. I suspect this trend had been occurring for months.

TNKE Form T: 546,000 shares @ $.0057. These are shares that were traded during the day but the MM withheld reporting until after trading closed to avoid detection of bulk selling. It is a continuous pattern with TNKE stock.

The closing share price was painted to $.007 with a $70 trade (10,000 @ $.007).

This daily pattern of large, low-priced Form T transactions combined with daily EOC paint jobs is very likely illegal manipulation.

Additionally, Form T trades that are at, near or below the LOD and are large compared with daily volume are often indicative of dilution to a company's float by a financier or insider.

I only began reviewing the daily trading data for TNKE on 8/28/14. All four trading days since then have had very large Form T trades reported. I suspect this trend had been occurring for months.

TNKE Form T: 645,000 shares @ $.0061. These are shares that were traded during the day but the MM withheld reporting until after trading closed. These bulk transactions are shown as "buys" because they are reported after hours when the bid is usually far lower than even the LOD during trading hours. In actuality, they are almost always bulk sales made through dilution friendly market makers.

Form T trades that are at, near or below the LOD and are large compared with daily volume are often indicative of dilution to a company's float by a financier or insider.

I only began reviewing the daily trading data for TNKE on 8/28/14. All three trading days since then have had very large Form T trades reported. I suspect this trend had been occurring for months.

XNRG: More on the seriously erroneous financial statements submitted for periods ending 11/30/13 and 2/28/14 (the later stated in the earlier post).

The income statement for the 3 and 6-month periods ending 11/30/13 are even more messed up than the one filed for the period ending 2/28/14.

XUN booked a credit (negative of a negative) of $51,686 general and administrative expenses instead of debiting actual expenses. Remember that executive salaries alone are $35,000/mo.

A credit of $363,170 is booked as general and administrative expenses for the 3 months ending 11/30/13, which causes the company to erroneously book a profit of $231,743 for the quarter.

http://www.otcmarkets.com/edgar/GetFilingHtml?FilingID=9718736

Neither the income statements for periods ending 11/10/13 or 2/28/14 flow from the Q1 for QE 8/31/13:

http://www.otcmarkets.com/edgar/GetFilingHtml?FilingID=9550117

XNRG: MAJOR understatement of operating expenses in the quarterly report for QE 2/28/14!

XUN reported only $81,803 in operating expenses for the entire 9-month period ended 2/28/14 ($9,089/mo). Salary expenses alone would have totaled $315,000 ($35k/mo). The operating expenses shown for the 9 months ended 2/28/14 are LESS than the 3-month period ended 2/28/14 of $133,489. The booked expenses are also a reduction of nearly $1.1 MM from the same period in 2013. The operating expenses for 6-month period ending 11/30/13 are also drastically understated and actually show a net credit of $51,686 (see next post for details).

Operating expenses for the nine months ended February 28, 2014 and February 28, 2013 totalled $81,803 and $1,166,156.

The "market value" (i.e. market capitalization) is merely the number of shares outstanding X the share price. It has nothing to do with revenue.

As of 7/31/14, XNRG claims there were 6,851,568,163 share outstanding, which equates to a market cap of $685,157 at a share price of $.0001. The market cap a/o 3/31/14 increased only because the O/S increased. The share price actually dropped in that time.

Massive dilution has driven the share price to no bid X $.0001 ask causing severe illiquidity. Because more dilution is scheduled and planned, it is unlikely that there will be any sustainable increase in share price. A reverse split is likely needed to restore liquidity, however it would result in an equivalent share price of less than $.0001 for existing shares.

That's correct. When an OTC company is suspended by the SEC, it loses its Rule 15c2-11 qualification, can no longer be quoted by market makers and becomes a grey market stock. The only way to reestablish qualification is to have a market maker essentially sponsor the company by submitting a Form 211 to FINRA, which would have to approve it.

TNKE Form T: 767,500 shares @ $.0060, which is the all-time low. These are shares that were traded during the day but the MM withheld reporting until after trading closed. These large, low-priced Form T trades are often indicative of new shares being dumped into the float.

There was also an EOD paint job of 5000 shares @ $.0080 ($40.00) to show a close of $.008 instead of $.006.

The VWAP (volume-weighted average price) was $.0062.

TNKE stock continues to be manipulated to make it appear stronger than it is and to hide huge low-priced block trades. I only began to look at the trading data yesterday. I suspect these Form T trades and EOD paint jobs have been going on for quite some time.

TNKE Form T: 314,000 shares @ $.0067. These are shares that were traded during the day but the MM withheld reporting until after trading closed. Form T trades that are at or below the LOD and are large compared with daily volume are often indicative of dilution.

There was also an EOD paint job of 3000 shares @ $.0085 ($25.50) to show a close of $.0085 instead of $.0068.

TNKE is indeed being manipulated, but the manipulation is to make it look stronger than it is and to hide the bulk sale of dilution that would bring the share price down.

The annual report for PVEC's FYE 06/30/14 is due Monday, September 29, 2014. If Peter Villiotis files his usual notice for a late report, the deadline is extended for 10 more days.

For future reference regarding companies that submit financial reports to the OTC News and Disclosure Service of OTC Markets:

Annual reports are due 90 calendar days from the end of the FY, which can be extended for 10 calendar days if a notice of late filing is issued.

Quarterly reports are due 45 calendar days from the end of the Q, which can be extended for 5 calendar days if a notice of late filing is issued.

The FY end for each OTC company is shown on its Company Profile page at otcmarkets.com.

For additional information, although some refer to financial reports submitted to OTCM as a 10-K or 10-Q, these refer to SEC forms filed only with the Commission via EDGAR.

Reverse mergers with public non-SEC filers have no requirements whatsoever for either the public or private entity. No corporate or financial disclosures are required -- not even unaudited financial statements.

Private companies choose to do reverse mergers with entities that already have Rule 15c2-11 qualification so they don't have to worry about corporate disclosure or financial statements. No new Form 211 is needed.

This is why it would be stupid for anyone to try to do a RM with PIPI, which lost its Rule 15c2-11 qualification when it was suspended by the SEC.

Other than obtain access to a group of existing shareholders who might naively buy or trade the stock if they thought a real business was going to be inserted (especially if promises were made that a MM would be filing a Form 211), a private company would have no advantage doing an RM with a GM stock. It would still not be eligible for market maker quotations.

I would not be surprised to see Ken or a surrogate insert some private entity into the PIPI shell and try to stimulate volume with promises of moving back to OTC Pink (fka Pink Sheets) in the future.

Because PIPI is a shell with no assets, the filing of a Form 211 by a B/D (MM) would never happen. Ken Ash or one of his surrogates could try to do a reverse merger with a private corporation and try to convince a MM to sponsor the new company, but unless the new company had an operating history and audited financial statements, even that would be extremely unlikely to happen. A RM also typically involves substantial dilution and often a R/S.

Even though PIPI will likely remain a grey market stock in perpetuity, Ken Ash may believe he can stimulate trading of the stock in volumes sufficient to provide some liquidity (for himself?). Ash was trying to do that same thing with IDCN when it was suspended by the SEC.

Ken Ash was made the court-appointed Custodian of IDCN on 3/5/12. Although this was certainly "material" information, Ash made no public announcement until he issue a PR on 3/23/12.

Prior to the public announcement on 3/23/12, the trading volume of IDCN dramatically increased starting in the time leading up to and especially following the 3/5/12 default judgment in WY. It is my belief that Ken Ash, his SCG followers and other shareholders involved in or selectively informed of the WY action were trading on what they assumed would be received as very good news when finally made public three weeks after the fact.

http://investorshub.advfn.com/boards/read_msg.aspx?message_id=73629528

Ken Ash was very irresponsible as the Custodian of Indocan Resources and seems to have acted primarily in his own self interest as well as that of his followers.

Ash did not timely announce the action, even when a company named Oxygen Orchard thought it had acquired the IDCN shell. He also failed to do the only thing the court tasked, to hold a shareholder's meeting to elect a new BOD.

If Ash is behind the recent PIPI trading activity, which appears to be blatant manipulation, nothing good will come of it IMO.

CNWD SEC Suspension:

http://www.sec.gov/litigation/suspensions/2014/34-72924.pdf

Order:

http://www.sec.gov/litigation/suspensions/2014/34-72924-o.pdf

Admin Proceeding to revoke registration of stock:

http://www.sec.gov/litigation/admin/2014/34-72925.pdf

GHII SEC Suspension:

http://www.sec.gov/litigation/suspensions/2014/34-72928.pdf

Order:

http://www.sec.gov/litigation/suspensions/2014/34-72928-o.pdf

Admin Proceeding to revoke registration of stock:

http://www.sec.gov/litigation/admin/2014/34-72929.pdf

CLTH SEC Suspension:

http://www.sec.gov/litigation/suspensions/2014/34-72930.pdf

Order:

http://www.sec.gov/litigation/suspensions/2014/34-72930-o.pdf

Admin Proceeding to revoke registration of stock:

http://www.sec.gov/litigation/admin/2014/34-72931.pdf

WTFS SEC Suspension:

http://www.sec.gov/litigation/suspensions/2014/34-72926.pdf

Order:

http://www.sec.gov/litigation/suspensions/2014/34-72926-o.pdf

Admin Proceeding to revoke registration of WTFS stock:

http://www.sec.gov/litigation/admin/2014/34-72927.pdf

Have you been able to reach Mr. Johnston? If so, did he provide an explanation regarding the Form 10 registration statement that some KMAG shareholders claim was submitted directly to the SEC for private review rather than uploaded electronically via EDGAR as the SEC requires?

Thank you for contacting the U.S. Securities and Exchange Commission (SEC). We appreciate the opportunity to assist you.

You indicated that you have concerns about KMA Global Solutions International, Inc. and asked that we contact you. Please let me know how we can best assist you.

I look forward to hearing from you.

Sincerely,

Steven G. Johnston

Special Counsel

Office of Investor Education and Advocacy

U.S. Securities and Exchange Commission

(202) 551-6349

www.sec.gov

www.investor.gov

www.twitter.com/SEC_Investor_Ed

Correct. Complaints about the SEC's past or alleged current actions in regard to KMA Global Solutions should be submitted to the OIG. Any KMAG shareholders who truly believe that the SEC is withholding from the public a Form 10 registration statement allegedly submitted directly to the Commission instead of filed via EDGAR should file a complaint to the OIC via the contact information below.

SEC Office of Inspector General Contact Information

Mailing Address:

U.S. Securities and Exchange Commission

Office of Inspector General

100 F Street, NE

Washington, DC 20549-2977

Telephone: (202) 551-6061

FAX: (202) 772-9265

Email: oig@sec.gov

Hotline

Tollfree phone number (877) 442-0854

Online Complaint Form: www.reportlineweb.com/sec_oig

The Office of Inspector General (OIG) is an independent office within the U.S. Securities and Exchange Commission (SEC or Commission) that conducts, supervises, and coordinates audits and investigations of the programs and operations of the SEC. The mission of the OIG is to prevent and detect fraud, waste, and abuse and to promote integrity, economy, efficiency, and effectiveness in the Commission's programs and operations.

If a ceo had a company suspended I would doubt the sec would just give them another company to take public without proving their innocents first.

Im trying to tell you the sec wouldnt allow it. If Reid did anything wrong there would be no trii trading publicly.

The best SEC division to send those letters is the Office of Investor Education and Advocacy. Contact information and options for sending such letters can be found at: http://investor.gov/contact-us#.U_lpaPldUlK

Letters can be mailed or faxed to:

U.S. Securities and Exchange Commission

Office of Investor Education and Advocacy

100 F Street, NE

Washington, DC 20549-0213

Telephone: (800) 732-0330

Fax: (202) 772-9295

Letters can be sent via the special online form found at this link:

Questions and Feedback

Please use this form to send us your questions and comments. If you have a complaint about your broker or a securities transaction, you will get better results by using our online Complaint Center.

Although we use secure socket layer encryption, do not hesitate to print this form and send it by mail or fax if you have any concerns about security. Please read our Privacy Act Notice to learn more about how we may use the information you send to us.

Enforcement Tips and Complaints

If you would like to provide us information about fraud or wrongdoing involving potential violations of the securities laws, which may include the conduct listed below, use the Tips, Complaints and Referrals Portal. See also further information about submitting a tip or complaint.

* Ponzi scheme, Pyramid Scheme, or a High-Yield Investment Program

* Theft or misappropriation of funds or securities

* Manipulation of a security's price or volume

* Insider trading

* Fraudulent or unregistered securities offering

* False or misleading statements about a company (including false or misleading SEC reports or financial statements)

* Abusive naked short selling

* Bribery of, or improper payments to, foreign officials

* Fraudulent conduct associated with municipal securities transactions or public pension plans

* Other fraudulent conduct

Ceo who are scam artists dont go public with another company. It easy to understand.

Does this mean that it is Ken Ash and his Stock Charter Group trading among themselves when there is no new public information to raise the share price and create the appearance of interest in this grey market, caveat emptor, non DTC-eligible (non DWAW-eligible) stock?

Jerry clearly stated "not from the video" that no r/s is happening in the near future. He also stated when the next update will happen.

We may not have access to the full amount under the equity line of credit.

For the five consecutive trading days prior to September 9, 2013, the lowest closing trade price of our common stock was $0.0008. There is no assurance that the market price of our common stock will increase substantially in the near future. The entire commitment under the equity line of credit is $15,000,000. The aggregate number of shares of common stock necessary to raise the entire $15,000,000 at $0.0008 per share is 18.5 Billion. The number of common shares that remains issuable is lower than the number of common shares we need to issue in order to have access to the full amount under the equity line of credit. Therefore, we may not have access to the remaining commitment under the equity line of credit unless the market price of our common stock to increase substantially. The Company may have to restructure the common stock through a common stock reverse split to meet its minimum price of $0.50 per share of common stock.

The application Jerry submitted to the FL EDC apparently claimed that Xun was a manufacturer a flywheel technology. Jerry was questioned by a member of the public making a presentation who did not believe that to be the case and he responded "no." However Jerry later did some dancing around to explain why the letter to the Commissioners stated Xun was such a manufacturer.

Below are the minutes of part of the exchange between Jerry and Commissioner Trudie Infantini at the hearing. It is not a direct transcript and is extremely poorly punctuated. I broke it into paragraphs for easier reading.

Commissioner Infantini inquired how the number of jobs and amount of money the company was going to create; stated right now she has not seen any revenue; she understands they filed a new S1 saying they were going to be issuing $79 million more shares for $52,000; and inquired if that is correct.

Mr. Mikolajczyk responded it is not for $52,000, that is an SEC requirement, that is what the value of that stock is as of the date the S1 was filed, or within five days of it.

Commissioner Infantini inquired how they came up with how much they were going to be investing; state if they are not going to be manufacturing flywheels, $22 million is a nice investment; and inquired if they do not need a manufacturing facility, what is it that the $22 million is going to be building.

Mr. Mikolajczyk advised to clarify her statement about not manufacturing, on the EDC letter to the Board it stated they were manufacturing; they are not manufacturing right now; they propose or plan to manufacture the flywheel technology; his background is in oil, gas, mining, construction, and manufacturing; he sat down with their board; and they worked out a plan of what the staffing requirements would be not only for the corporate office, but for their manufacturing facilities. He went on to say it pulls it together with his experience, over 40 years in the industry; he has worked with engineers and all that; and he was able to price it out and put the application together.

Having one or more producing wells does not mean a company ceases to be in the oil exploration business. Such companies continue to explore for additional sources of oil and are considered extremely speculative. These businesses may also be called "exploration & production" companies:

http://www.investopedia.com/terms/e/exploration-production-company.asp

Xun's business plan makes it completely ineligible for an SBA loan regardless of whether it produces any oil. It's strains credulity to think that Jerry didn't know that there was no chance of an SBA loan when he was asserting the possibility of one and that an unnamed consultant said it looked like Xun would qualify

I don't know why he would even risk and lead shareholders on a possibility of the loan.

Dont forget about the SBA loan.

Ineligible Businesses

A business must be engaged in an activity SBA determines as acceptable for financial assistance from a federal provider. The following list of businesses types are not eligible for assistance because of the activities they conduct:

(Last on list):

* Speculative businesses (such as oil exploration)

Thank you for clarifying Peter's post by pointing out that the drilling rig that was demobilized as of 7/5/14 referred to the drilling rig he announced on 5/23/24 had been mobilized to the site. I misinterpreted his forum post and agree that it does appear that he does indeed imply that production would be continuing. Sorry for the misinterpretation.

That said, after doing some research I am skeptical about Jerry's claim that a drilling rig was actually mobilized to the Rice lease on or about 5/23/14. Among other things, I reviewed the difference between a drilling rig and a service rig, the latter of which was stated as about "to be spotted" in the 5/23/24 PR. They look very similar with a service rig typically being smaller. The costs of employing each are also very different as are the crews and hours of operation.

My research also included reviewing the YouTube videos created by Jon Malis who is the owner of Northeastern Consolidated Energy Partners, Inc. and a co-owner of Utica Resources Inc. Malis is apparently working on behalf of Vencedor Energy Partners for the Rice lease - specifically Rice #15.

I will post my concerns about the accuracy and/or timeliness of the following two statements in a separate post as it will be quite lengthy.

5/23/14:

In addition to the completion of Rice #15, the drilling rig for the second Rice oil well has been mobilized on the site.

The drilling rig was demobilized from the Rice lease and is not scheduled for drilling the remaining four oil wells on the lease at this moment. Management decided to wait until all of the funding is in before re-scheduling the drill rig.

If you scroll down to "Item 4: Ownership" on the SC 13G, it shows the amount beneficially owned by Asher as 6,455,398 shares and the percent of class as 9.99%. Perhaps it is an error.

I'm not sure where I copied the O/S of 33,013,274 as it is not on the Asher SC 13G (where no O/S is given at all). I had multiple SC 13Gs open and may have copied if from a different one so the O/S number I posted may not be accurate for that date.

You are correct that 6,455,398 would be 19% if 33,013,274 was the accurate O/S for 4/23/14. I didn't take the time to do the math, put just did a cut and paste job.

The O/S would have had to be about 64,618,598 for the amount reported as beneficially owned to be 9.99%.

Is there a list of the initial O/S after each R/S so that that the O/S can be approximated for a specific time frame?

The SC 13G: http://www.sec.gov/Archives/edgar/data/1322587/000135448814002014/nlh_sc13g.htm

The main points I was trying to make in my post were that Asher and the other toxic financiers dump their shares very quickly and that their financing agreements are set up to assure they make money even in the event of a R/S.

Asher's SC 13G filed on 4/23/14 shows 6,455,398 shares beneficially owned, which represented 9.99% of the total shares outstanding of 33,013,274 on that date. That's as much as they could own without being deemed an affiliate (a control entity), which would impose restrictions they don't want.

http://www.sec.gov/Archives/edgar/data/1322587/000135448814002014/nlh_sc13g.htm

Asher Enterprises and all of the other toxic financiers who buy stock at approximately a 50% discount allegedly relying on Reg D, Rule 504 as an exemption from registration, typically begin dumping immediately to dispose of their shares as quickly as possible.

It's possible that Asher had already dumped most of them before the 1 for 50 R/S on 5/15/14.

It's also possible that Asher's Share Purchase Agreement had a clause regarding issuance of additional shares in the event of a reverse split.

Shrewd financiers like Asher, Magna Group, Hanover Holdings, Fairhills Capital, Ironridge Global, etc. cover all the possible contingencies in their agreements to be sure they make money. As NEWL investors have learned, they also use the courts to aggressively enforce compliance by the issuer with the terms of those agreements.

I tried to find the a 6-K announcing the financing agreement with Asher, which would have had the agreement attached, but was unable to locate it. Does anyone have the date it was issued or a link to it? The company should have disclosed the terms of all such material agreements.

FWIW, a SC 13G/A amending the original SC 13G does not need to be filed until 45 days following the end of the calendar year. Although Asher filed it on 8/20/14, it's unknown when they really completed their dumping.

http://law.uc.edu/sites/default/files/CCL/34ActRls/rule13d-2.html

Deals with these notorious toxic financiers have time-proven very predictable consequences, so they can't really be blamed for doing what they always do.

It was the management of of Newlead that chose to do these deals knowing that they would be massively dilutive. They also chose to repetitively do reverse splits to try to raise the price, which just continued to fall. Management is ultimately to blame for the destruction in shareholder value.

These deals are like Aesop's Fable of the scorpion and the frog, except adapting it to toxic financiers has the scorpion surviving after getting a free ride across the stream from the frog it kills.

http://www.aesopfables.com/cgi/aesop1.cgi?4&TheScorpionandtheFrog

If this wasn't the TRUTH the SEC would have already done something about Mr. Reid ...

The Commission temporarily suspended trading in the securities of the above-listed issuers

because of questions regarding the adequacy and accuracy of information about the companies,

including their assets, business operations, current financial condition and/or issuances of shares

in company stock.

KMA Global Solutions International Inc. is a Nevada corporation based in

Ontario, Canada. Questions have arisen concerning the adequacy and accuracy of

press releases concerning the company’s operations.

If any broker, dealer or other person has any information which may relate to this matter, they

should immediately contact any of the following individuals:

In connection with: Alto Group Holdings, Inc., Fox Petroleum, Inc., KMA Global Solutions

International, Inc., and Mobile Star Corp:

Andrew M. Calamari, (212) 336-0042 or calamaria@sec.gov

Associate Regional Director, New York Regional Office

Sharon Binger, (212) 336-0462 or bingers@sec.gov

Assistant Regional Director, New York Regional Office

XNRG will have to do a substantial reverse split in order to sell any shares to AGS Capital Group under the Reserve Equity Financing agreement (REF).

If the minimum share price needs to be $.50 or more, a minimum 1 for 5000 split would be needed. However, because dilution would bring that down below $.50 immediately, a much larger split may be needed. Even if there were no minimum share price, a R/S would still be needed as the stock has been diluted to no-bid X $.0001 ask.

It has been posted here that reporting companies need to give 30 days notice before a R/S. That does not seem to be the case. The following SEC link regarding reverse splits make no mention of prior notice but says only the following regarding reporting companies enacting a R/S:

If a company is required to file reports with the SEC, it may notify its shareholders of a reverse stock split on Forms 8-K, 10-Q and 10-K.

We may not have access to the full amount under the equity line of credit.

For the five consecutive trading days prior to September 9, 2013, the lowest closing trade price of our common stock was $0.0008. There is no assurance that the market price of our common stock will increase substantially in the near future. The entire commitment under the equity line of credit is $15,000,000. The aggregate number of shares of common stock necessary to raise the entire $15,000,000 at $0.0008 per share is 18.5 Billion. The number of common shares that remains issuable is lower than the number of common shares we need to issue in order to have access to the full amount under the equity line of credit. Therefore, we may not have access to the remaining commitment under the equity line of credit unless the market price of our common stock to increase substantially. The Company may have to restructure the common stock through a common stock reverse split to meet its minimum price of $0.50 per share of common stock.

... if a company changes names/ ticker do your shares follow