News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Bullwinkle

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Interesting List of Taxes that exist today

TAXES:

Accounts Receivable Tax

Building Permit Tax

Capital Gains Tax

CDL license Tax

Cigarette Tax

Corporate Income Tax

Court Fines (indirect taxes)

Dog License Tax

Federal Income Tax

Federal Unemployment Tax (FUTA)

Fishing License Tax

Food License Tax

Fuel permit tax

Gasoline Tax (42 cents per gallon)

Hunting License Tax

Inheritance Tax Interest expense (tax on the money)

Inventory tax IRS Interest Charges (tax on top of tax)

IRS Penalties (tax on top of tax)

Liquor Tax

Local Income Tax

Luxury Taxes

Marriage License Tax

Medicare Tax

Property Tax

Real Estate Tax

Septic Permit Tax

Service Charge Taxes

Social Security Tax

Road Usage Taxes (Truckers)

Sales Taxes

Recreational Vehicle Tax

Road Toll Booth Taxes

School Tax

State Income Tax

State Unemployment Tax (SUTA)

Telephone federal excise tax

Telephone federal universal service fee tax

Telephone federal, state and local surcharge taxes

Telephone minimum usage surcharge tax

Telephone recurring and non-recurring charges tax

Telephone state and local tax

Telephone usage charge tax

Toll Bridge Taxes

Toll Tunnel Taxes

Traffic Fines (indirect taxation)

Trailer Registration Tax

Utility Taxes

Vehicle License Registration Tax

Vehicle Sales Tax

Watercraft Registration Tax

Well Permit Tax

Workers Compensation Tax

COMMENTS:

"Not one of these taxes existed 100 years ago and our nation was the most prosperous in the world, had absolutely no national debt, had the largest middle class in the world and only one parent had to work to support the family."

What happened?

http://www.thepowerhour.com/news2/tax_list.htm

CAGW - Citrizens Against Government Waste

http://councilfor.cagw.org/site/PageServer?pagename=reports_porkbarrelreport

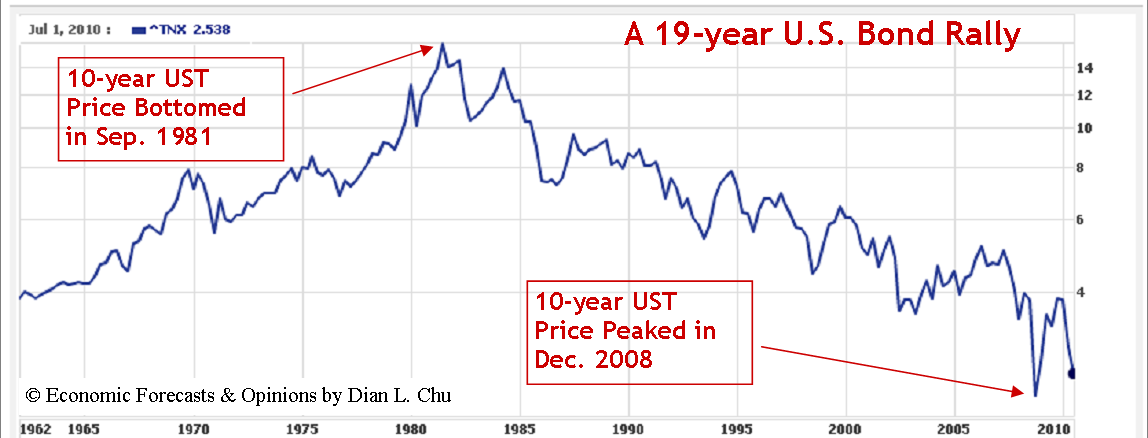

Faber and Schiff: The American Bond Bubble

by Dian L. Chu,, Economic Forecasts & Opinions

Posted on 08/25/10 at 10:32pm

As I've been saying for some time that the bond market is screaming for an imminent burst, now Dr. Marc Faber and Mr. Peter Schiff also spoke with CNBC on Aug. 23 warning of a bond bubble trouble.

Faber - Stay Away from a 19-year Rally

Faber advises investors "stay away from Treasurys as they’ve been rallying since 1981--equivalent to a 19-year bull run,"--when the 10-year bottomed out on Sep. 21, 1981. Faber says Dec. 18, 2008 was the peak of the bond bubble with yield of 2.08% and 2.53% on 10-year and 30-year respectively. (See 10-year chart)

“I think that there isn’t much upside potential in Treasurys unless it’s for the short term. Even the short term is uncertain. But if I look 10 years ahead, where do I want to have my money, then certainly not in US Treasuries.”

Faber's biggest concern is that because of a weak economy, the U.S. budget deficit will likely remain high, and continue to go up under the Obama administration, which could make interest payments on government debt unbearable.

He also warned against the misguided confidence arising from still strong foreign demand for U.S. Treasurys:

“In 1999 and 2000, foreigners (bought) the NASDAQ and what happened afterwards was a major collapse. I would not look at foreign buying as a very intelligent leading indicator.”

Faber says a better place for investor's money now is farm land, agricultural commodities and gold should also be a part of investor's portfolio.

Schiff - The Mother of All Bubbles

Schiff basically declares the bond market the mother of all bubbles, and noted that when the bubble bursts, the loss will dwarf the combined losses of the bubbles of stock market and the real estate. Eventually, the government will either inflate or default. Either way will ultimately make bond investors go bust.

For risk-averse investors, Schiff believes gold and foreign bonds such as Switzerland where government debt level is not as high, would be better options than U.S. treasuries.

My Thoughts

Dismal economic data has spooked investors flocking to Treasuries driving down yields. Traditionally, bonds are considered to be safer and less volatile than equities and commodity. However, the financial markets have evolved in such a way that the same players are active in all sectors, employing the same trading technique. This, in part, has made bonds behave almost like stocks with similar volatility. (See comparison chart)

So, investors should start looking at bond the same way as equities, and commodities, and now is the time to move out of bond and into either equities (dividend-paying blue chips as noted in my previous post), or commodity such as gold.

And for the highly risk-averse, parking in cash for the short term would still be better off than staying in "the mother of all bubbles."

(Recommended Reading: Self Fulfilling Prophecy: The Bond Trade, Yield, Dow 30 vs. 10-year U.S. Treasury, and Bonds & Equities: Expect a Major Shift)

http://www.benzinga.com/10/08/443492/faber-and-schiff-the-american-bond-bubble

Hiring, Manufacturing Probably Cooled on Signs U.S. Recovery Is Stumbling

By Shobhana Chandra - Aug 28, 2010 9:00 PM PT

Hiring and manufacturing probably cooled in August, showing companies are scaling back as the U.S. recovery shows signs of stumbling, economists said before reports this week.

Private payrolls that exclude government agencies rose by 47,000 this month after a 71,000 July gain, while the unemployment rate rose to 9.6 percent, according to the median estimate of 33 economists surveyed by Bloomberg News. Factories expanded at the weakest pace in almost a year, an Institute for Supply Management report is forecast to show.

Federal Reserve Chairman Ben S. Bernanke said last week the central bank will do “all that it can” to sustain an expansion that’s still restrained by weaker-than-anticipated consumer spending and “painfully slow” job growth. Other reports this week may show household purchases are stagnating and service industries, the biggest part of the economy, decelerated.

“We have a lot to worry about for the second half, as this recovery is losing steam,” said Scott Brown, chief economist at Raymond James & Associates Inc. in St. Petersburg, Florida. “The job market will remain pretty lackluster. There is no magic fix in terms of policy.”

The jobs report, due from the Labor Department on Sept. 3, will also show overall payrolls fell 100,000 this month, reflecting the dismissal of temporary workers hired by the government to conduct the census, according to the survey median. The unemployment rate probably rose from 9.5 percent.

Manufacturing Cools

The Tempe, Arizona-based ISM’s factory gauge dropped in August to 52.8, the median estimate in the Bloomberg survey. The report is due on Sept. 1 and figures greater than 50 signal expansion.

The projected figure would be the weakest since September 2009, indicating manufacturing, which spearheaded the recovery as customers rebuilt inventories and shipped more goods overseas, may be starting to pull back.

The supply management’s group may report on Sept. 3 that its services index, which covers almost 90 percent of the economy, declined to a six-month low of 53.2 in August from 54.3, according to the survey.

A report from the Commerce Department last week showed orders for non-defense capital goods excluding aircraft, a proxy for future business investment, slumped 8 percent in July.

Intel Corp., the world’s biggest chipmaker, last week cut its third-quarter revenue forecast. Sales are getting hurt by “weaker than expected demand for consumer PCs in mature markets,” Santa Clara, California-based Intel said in a statement, referring to personal computers.

‘Painfully Slow’

“The painfully slow recovery in the labor market has restrained growth in labor income, raised uncertainty about job security and prospects, and damped confidence,” Bernanke said at the Kansas City Fed’s annual monetary symposium in Jackson Hole, Wyoming, on Aug. 27.

The Fed “is prepared to provide additional monetary accommodation through unconventional measures if it proves necessary, especially if the outlook were to deteriorate significantly,” Bernanke said.

Stocks rallied and Treasuries retreated after Bernanke pledged to safeguard the economy. The Standard & Poor’s 500 Index gained 1.7 percent to 1,064.59 at the 4 p.m. close in New York on Aug. 27. The yield on the 10-year Treasury surged to 2.65 percent from 2.48 percent late on the previous day.

Fed Meeting Minutes

The Fed on Aug. 31 will release the minutes of its last meeting, during which policy makers retained their commitment to keep the benchmark interest rate close to zero for an “extended period” and decided to maintain their holdings of securities to stop money from draining out of the financial system.

Cooling growth and a sluggish labor market may also feed voter discontent heading into the November elections that will determine which party controls Congress.

Polls show the public is increasingly skeptical of President Barack Obama’s performance. Public approval for the president’s handling of the economy was at 41 percent in an Aug. 11-16 Associated Press-GfK survey, an all-time low and down from 50 percent last July.

Households are trying to pay off debt and limit purchases after the U.S. lost more than 8 million jobs since the recession began in December 2007. Consumer spending rose in July as auto sales rebounded from the lowest level in four months, a report tomorrow is projected to show.

Consumer Spending

Purchases climbed 0.3 percent after no change the prior month, according to the survey median. The increase in spending probably also reflected the biggest gain in prices in a year, indicating the advance will be almost wiped away when the figures are adjusted for inflation.

The lack of employment is restraining sentiment, raising the risk that household spending, which accounts for about 70 percent of the economy, will falter. The Conference Board’s index of consumer confidence, due on Aug. 31, was little-changed at 50.9 this month after 50.4 in July, according to the median forecast in a Bloomberg survey.

Housing is also retreating. Gains in home prices probably cooled in June, a, Aug. 31 report from S&P/Case-Shiller is projected to show. Two days later, data from the National Association of Realtors may show pending home sales, or the number of contracts to purchase previously owned houses, fell in July for the third consecutive month.

Bloomberg Survey

==============================================================

Release Period Prior Median

Indicator Date Value Forecast

==============================================================

Pers Inc MOM% 8/30 July 0.0% 0.3%

Pers Spend MOM% 8/30 July 0.0% 0.3%

Case Shiller Monthly YO 8/31 June 4.6% 3.6%

Chicago PM Index 8/31 Aug. 62.3 57.0

Consumer Conf Index 8/31 Aug. 50.4 50.9

ADP Payroll ,000’s 9/1 Aug. 42 17

ISM Manu Index 9/1 Aug. 55.5 52.8

Construct Spending MOM% 9/1 July 0.1% -0.5%

Initial Claims ,000’s 9/2 28-Aug 473 475

Factory Orders MOM% 9/2 July -1.2% 0.4%

Pending Homes MOM% 9/2 July -2.6% -1.0%

Nonfarm Payrolls ,000’s 9/3 Aug. -131 -100

Private Payrolls ,000’s 9/3 Aug. 71 47

Manu Payrolls ,000’s 9/3 Aug. 36 10

Unemploy Rate % 9/3 Aug. 9.5% 9.6%

ISM NonManu Index 9/3 Aug. 54.3 53.2

==============================================================

Downbeat mood at Jackson Hole

By Robin Harding in Jackson Hole

Published: August 29 2010 19:51 | Last updated: August 29 2010 19:51

If the mood at Jackson Hole in 2008 was one of crisis, and 2009 sounded relief, the mood in 2010 was one of angst. The central bankers gathered at the Wyoming resort in the US were worried about the growth outlook but doubtful they can do much to improve it.

“Last year, it was pretty clear that third-quarter growth was going to be positive . . . and that was making people feel upbeat,” said James Bullard, president of the St Louis Fed. “Here, you’ve got the opposite, where all the recent news on the economy has been upsetting.

A year into the US economic recovery, the unemployment rate is still 9.5 per cent, the growth rate in the second quarter was a feeble 1.6 per cent and recent data look little better.

The tone was set on the first morning by Carmen Reinhart of the University of Maryland. She said that in the decade after a severe financial crisis, the median unemployment rate was 5 percentage points higher than normal in advanced countries. Following 10 of the 15 crises she studied, unemployment never fell back to its pre-crisis level.

The main cause is the level of debt. “The debt overhang bears the ultimate responsibility for slowing down the economic recovery,” said Jean-Claude Trichet, president of the European Central Bank, in his speech to the conference. “Left with the need to reduce their debts and accumulate more assets, households have increased their saving rates, leading to protracted sluggishness in the growth of private consumption.”

The Fed is confident it can stop medium-term inflation from falling below its target level by using unconventional tools such as asset purchases. “We can do our part, in particular we can defend our inflation target on the low side,” said Mr Bullard.

Given the debt overhang, however, Fed officials fear that on-target inflation may not be enough to lower unemployment and create strong growth.

Ben Bernanke, chairman of the Federal Reserve, said it would “strongly resist” any downward slide in inflation and “do all that it can” to ensure the recovery continued. But he added: “Central bankers alone cannot solve the world’s economic problems.”

Central bankers fear being asked for more than they can deliver and worry about a backlash when it does not arrive. For example, they have no control over tax or education policy, both of which have a huge influence on growth.

“These are extraordinary times for monetary policy and my sense is that we should be cautious about promising too much,” said Raghuram Rajan, a professor at Chicago Booth business school and former chief economist at the International Monetary Fund.

“I guess the thing I’m most worried about with some of the current discussion is that monetary policy is going to end up being asked to do more than it’s capable of,” said Charlie Bean, deputy governor of the Bank of England, arguing that monetary policy should not be used to burst asset price bubbles.

In the wake of the sovereign debt crisis, a new area of focus at Jackson Hole was fiscal policy. Mr Bernanke noted that “managing fiscal deficits and debt is a daunting challenge for many countries”.

Mr Trichet said that “fiscal consolidation will have to be ambitious”.

Eric Leeper, a professor at Indiana University, warned of a “coming era of fiscal stress” caused by the healthcare and pension costs of an ageing population that will make monetary policy harder to manage. He called for a new “fiscal science” compared to today’s “alchemy” to take some politics out of tax and spending and make it work more like monetary policy.

http://www.ft.com/cms/s/0/d83698a8-b39d-11df-81aa-00144feabdc0.html

China's Gold Demand: Saving, Not Spending

By: Adrian Ash | Wed, Aug 25, 2010

What jewelry-selling Western consumers have discovered about China's gold buying...

WHATEVER the reasons for China's massive household savings rate (Western economists blame the lack of social security, so you can guess their cure), the World Gold Council's Gold Demand Trends today showed private consumers putting ever-more money into physical gold.

Compared to household savings, in fact, revised forecasts here at BullionVault this morning put likely gold purchases in 2010 at the equivalent of almost 1.7% - over twice the level of five years ago.

This confounds Western analysts who foresaw substitution - from gold jewelry to consumer gadgets - as China's household wealth grew. Because gold demand, even for the kitschest gold kitten, remains an expression of saving, not spending.

That might jar with Western tastes and ideas. But it's clear in the numbers.

According to Peking professor Michael Pettis - and despite disposable income growth of perhaps 15% annually since 2000 - consumption growth in the world's No.2 (and fastest-growing) economy "is anemic" by comparison. A BIS study last month suggested it's because household earnings are falling as a proportion of national income. But either way, and in contrast with consumption spending, private Chinese gold demand has risen 26% annually by volume in the last decade, drawing a still-greater share of retained wealth as domestic gold prices rose near three-fold.

So where Western analysts divide "jewelry" from "investment" demand, Chinese gold buying - as in India, the world's No.1 market (for now) - cannot be so easily split. Gold's form doesn't define its purpose so tightly in China, as North American and European gold sellers have rediscovered since the financial crisis began.

Swapping gold-for-cash by ditching unwanted jewelry, the Western world's new "scrap gold" sources are simply finding in gold a value they'd forgotten was there. Stored wealth in whatever shape is still wealth. The trick, of course - and as China's fast-growing "investment products" demand now shows - lies in reducing your transaction costs both on purchase and sale.

P.S: As for the People's Bank buying gold, Beijing's reserve managers are very much the junior player in China's gold market. In the 30 months between Jan. 2008 and June 2010 alone, according to WGC data, private households bought more gold (1057 tonnes) than the central bank reports in its entire hoard (1054 tonnes).

http://www.safehaven.com/article/17961/chinas-gold-demand-saving-not-spending

The Dark Side of Deficits

By: John Mauldin | Sat, Aug 28, 2010

http://www.safehaven.com/article/17990/the-dark-side-of-deficits

An Update on the Hindenburg Omen of August 2010

By: Robert McHugh

Sun, Aug 29, 2010

You are not going to believe this, but on Friday, August 27th, we got both a fifth official Hindenburg Omen observation and a 90 percent up day. Completely bizarre combination, which is the point. It is this sort of confrontational confusion inside markets which is the basis and background for all of the stock market crashes over the past 25 years. This does not mean we are definitely going to get a stock market crash, but it does mean the odds of getting one are far greater than the normal less than one-tenth of one percent on any given day. Because this set-up is rare, only 27 such set-ups over the past 25 years, it throws the market into a unique and infrequent population of only 27 occurrences, and within that unique 27 occurrence set-ups, we have seen a market rattling stock market crash 8 times, or 30 percent of the time this unique set-up occurred. The time span for this set-up is 120 days, 120 days of high risk. The market lacks uniformity, lacks certainty, lacks its normal stability. There were no instances over the past 25 years when a stock market crash occurred without an official Hindenburg Omen being on the clock. We now have a five observation Hindenburg Omen cluster.

First, let's give the details on the latest and fifth Hindenburg Omen, which ironically arrives on a day when the Industrials rose 165 points, not the sort of day one would expect to see a Hindenburg Omen observation. There were 141 New NYSE 52 Week Highs (and by the way, coming on a day when U.S. Bonds tanked), with 74 New NYSE lows. The lower of the two came in at 2.36 percent of total NYSE issues traded Friday, which was 3,140. New Highs were not more than twice New Lows, the McClellan Oscillator was negative (-48.34), and the 10 Week Moving Average was Rising.

As for the 90 percent panic buying up day Friday, there is an amazing phenomenon going on since the April 26th, 2010 top. We have now had twelve 90 percent panic buying up days and thirteen 90 percent panic selling down days since that top. That is, 25 out of the past 87 trading days have been panic trading days, with an approximate equal number of up versus down. This is astonishing.

What does this mean? Pretty much the same thing as the confirmed and official Hindenburg Omen observation means, that the market lacks uniformity, that the market is in an unstable condition, and it is at these times that markets are especially vulnerable to a stock market crash. Again, this does not guarantee a crash, as the odds are only about 30 percent, but compared to the normal less than one-tenth of one percent probability for a crash on any given day, that is an astronomical increase in the odds for a crash. A 90 percent up day occurs when both up points and up volume are above 90 percent of total volume, with the converse being true for 90 percent down days. These are usually rare, but the incidences since April 26th, 2010 have been anything but rare. We get one on average every fourth trading day.

That said, if you are a high stakes gambler, there is a 70 percent chance we will not see a full-blown crash over the next three and a half months (120 days from the first observation, August 12th, 2010). But there are higher odds that a large and significant decline could come over this period, even if it falls short of a crash. The odds of a decline of 10 percent or more are 40.8 percent; the odds of a decline 8 percent or greater are 55.6 percent; and the odds of a decline greater than 5 percent are 77.8 percent -- pretty high. Since August 12th, 2010, the date of the first observation, the Industrials have fallen 3.7 percent, and since the second and cluster-confirming observation on August 20th, the Industrials have fallen 2.7 percent. But there is a long way to go before the threat period ends.

On page 16 and 17 in this Weekend's Expanded Market Report we show that the large Head & Shoulders top patterns from November 2009 have now completed in the S&P 500 and NDX, prices having fallen to the necklines. This increases the odds that a stock market crash is slowly developing and will have an acceleration point over the next several months. Why? Because to reach the downside price targets would require a decline greater than 15 percent, actually greater than 20 percent from the top of the right shoulders.

http://www.safehaven.com/article/17994/an-update-on-the-hindenburg-omen-of-august-2010

India's Gold ETF Assets May Soar 17 Times on Refuge Demand, Executive Says

By Madelene Pearson

Aug 29, 2010 5:54 PM PT

Gold held by exchange-traded funds in India, the world’s biggest buyer of bullion, may surge as much as 17 times in the next three years as investors seek a refuge from financial turmoil and inflation.

Assets may reach “100 tons to 200 metric tons” from 12 tons now, said Rajan Mehta, executive director of Benchmark Asset Management Co., which runs the nation’s first and biggest gold exchange-traded fund. “The growth will definitely be faster than what we have seen in the past.”

Investors globally bought 291.3 tons of gold in ETFs in the second quarter, the second-highest amount on record, as prices climbed to an all-time high of $1,265.30 an ounce during the sovereign-debt crisis in Europe, the producer-funded World Gold Council said on Aug. 25. London-based researcher GFMS Ltd. and Goldman Sachs Group Inc. expect gold to advance to $1,300 this year as the metal heads for a 10th straight annual gain.

India’s seven bullion-backed funds had 19.7 billion rupees ($420 million) in assets on July 30, more than double the amount a year earlier, according to the Association of Mutual Funds in India. Increased inflows may help support prices.

Investment demand for the yellow metal in India more than tripled to 92.5 tons in the six months ended June 30 from 25.4 tons, the World Gold Council said.

Exchange-traded funds have become popular worldwide since their creation in 1993 as they widened investors’ access to different type of assets. Holdings in the SPDR Gold Trust, the biggest exchange-traded fund backed by bullion, expanded to a record 1,320.44 tons in June, and were at 1,298.56 tons as of Aug. 27, according to the company’s website.

‘Room to Grow’

“Today the industry has only 12 tons, which is very small compared with volumes all over India,” Mehta said in an interview in Goa. “There is a lot of room to grow.”

Benchmark’s Gold Bees had 9.85 billion rupees in assets on July 30 and has returned 19.6 percent annually since its introduction in March 2007, according to its website.

India’s seven gold funds have gained an average 19 percent in the past 12 months, compared with a 25 percent jump in local prices, Bloomberg data show. Futures reached an all-time high of 19,198 rupees ($410) per 10 grams on June 8.

“Gold has delivered good returns, so normally many advisers feel safer in advising gold as part of asset allocation,” said Mehta. “Gold as an investment theme is gaining ground.”

To contact the reporter on this story: Madelene Pearson in Mumbai on mpearson1@bloomberg.net

http://www.bloomberg.com/news/2010-08-30/india-s-gold-etf-assets-may-soar-17-times-on-refuge-demand-executive-says.html

Bob Chapman, The International Forecaster

Posted Monday, 30 August 2010

US MARKETS

The Congressional Budget Office thinks the country faces serious budget problems, as well as serious economic problems, because it estimates that the deficit for 2011 will be $1.066 trillion. In addition it sees fiscal 2010, which ends on September 30th, at $1.34 trillion, or 9% of GDP. Last year was 9.9%.

The lesson in Ponzi finance has not been lost on foreign investors who continue to buy less dollar denominated investments. That in spite of what the Federal Reserve is buying through its fronts overseas, which includes foreign central banks. The purchase of Treasuries and Agencies are so vital that you hear few references to deflation or inflation in the major media. All there is is the canard that there is no inflation. You would think these boobs in government would rig inflation at 1-1/2% to make it believable, but that obviously is beyond their mental capabilities, when real inflation is over 7%. The only conclusion we can come to is that government wants to obscure the fact that investing for a 10-year T-note at 2.50% is a 4.50% loser with inflation at 7%. These low rates of return, a zero interest rate policy and the creation of $2.5 trillion still has not been able to bring lasting recovery to the economy. That is because the present solutions have never worked and there is no intention of making them work. The idea is to destroy the US and world economy to force its inhabitants to accept world government.

What is obvious for whatever reason, is that quantitative easing, or throwing money at the problem, doesn’t work. We have just witnessed the greatest monetary expansion ever and no one seems to notice it didn’t work. In fact the Fed is creating another bubble in relation to interest rates and the bond market. This could be much worse than 2005 and 2006. In spite of this probable outcome, banking, Wall Street and corporate America are clamoring for more stimuli as consumption again fades. Again there is no historical basis to believe that today’s corporate fascist Keynesianism will work, in fact history tells us just the opposite. The extreme fiscal and monetary measures that have been chosen simply do not work. If QE or fiscal spending does not create inflation, then deflationary depression will become predominate and the entire financial system will collapse taking the world economy with it.

This cycle of inflation to deflation has been going on since the 1960s and each time finance and the economy were resurrected a new cycle began with greater damage. Today we have finally reached the end of the line.

Those who look at today’s bond bubble forget the bond rally of the early 1990s and the subsequent bust in 1994 when the 30-year bond hit 8-3/16%. Incidentally that was one of our first forecasts, which helped the IF get off the ground. Later in the 90s we called the Asian contagion, Russian failure of their currency engineered by criminals from Harvard and the failure of LTCM, which was bailed out by Wall Street. Their greatest mistake was being short gold. When all was said and done it cost $7 billion. Wall Street lies so much who knows how much was recovered.

Keynes must be proud of himself having created the basis economically and financially for the imposition of corporatist fascist government. Some wonder why leadership doesn’t seem to care. They do care, they deliberately created this monster. Those not in on the planning and execution possibly go along for the ride. If they do, they do not their jobs but in most instances if they do not they never work at their professions again. Some even meet an untimely end. What the pundits don’t understand is that it was planned this way. Stabilization and recovery are not part of the plan. Only extension of the economy until the right spot is reached to pull the plug on the entire system. The key to that is the bond market, which is ten times larger than the stock market. That is where the smart money resides and that is where eventually the biggest losses will be taken. Yes, fiscal debt and monetization are going to take the system down and anyone with any foresight can see that.

Our mortgage market led by the GSEs, Fannie Mae, Freddie Mac, Ginnie Mae and FHA, for the past three years have been insuring and writing loans, most of which are subprime. That is now triggering a 50% failure rate, again. This has been done to keep real estate from totally collapsing. Today we have zero interest rates and 4.42%, 30-year fixed rate mortgages. This is another national socialist program that we predicted seven years ago when we wrote that Fannie and Freddie were broke. You know what has happened since. You can now see, as those in Italy and Germany in the 1930s saw, there are no longer any limits to government intrusion. The result has been the deflation in prices and to offset that the deliberate creation of inflation. Within all of this the Fed is still bailing out those connected within the elitist system and those who own the Fed and are designated too big to fail. That is what the enormous fiscal and monetary stimulus is all about. It’s about lowering the economy in stages until it’s ready for total destruction. There are no policies for relief or recovery. This depression will last for many years as government tightens its grip on the people and extinguishes their freedom. The stitches are being pulled from the fabric one by one.

The economy is being allowed to move sideways via monetization. As we move forward in time more and more confidence will be lost as inflation increases, wages and unemployment remain stagnant, free trade and globalization continue to flourish and the structural underpinnings of our economic and financial system collapse. As each day passes the situation worsens, although its planned demise is imperceptible to most. The global economy is in a financial bubble and there is no escape. The bubble is being ignored and that is sure to bring great heartache to all the world’s inhabitants. If you have wealth the only way you can protect it is via gold and silver assets. There is no other choice.

All this is covered in words that are new and different. We call them euphemisms. Lying is socially and politically acceptable. Price stability is merely price fixing and TARP the Troubled Asset Relief Program, is simply the bailout of the financial structure by the taxpayer. Socialism for the rich in the cloak of fascism. Then, of course, we have quantitative easing, is the creation of money and credit out of thin air. That is followed by lower interest rates, which gives banks the incentive to lend under the fractional banking system. It’s all manipulation, but under the Federal Reserve Act it is all legal. This is what so-called monetary policy is all about. Unfortunately that game will soon be over. We are about to follow that shinning example Japan into monetary oblivion. After 20 years of depression the land of the rising sun is about to descend deeper into depression and the world is about to follow. Their venture into chaos has been delayed by the ability to easily access export markets and a huge domestic pool of savings, which was tapped to keep their system going. Those advantages are ending and the rest of the world will follow, but not in 20 years. That is because the world’s debt has been borrowed from foreign sources that must be repaid albeit in cheap dollars or currency. A massive erosion of fiat value. The profligated spending of governments is being paid for by bondholders and by the fall in the purchasing power of the currency, as expressed via inflation.

At this juncture the Fed has no options excepting a deflationary depression. They have zero interest rates and continue to monetize as a fiscal policies create $1.5 trillion annual deficits. If they don’t continue stimulus and zero rates the economy and financial structure will collapse. It really is as simple as that. The Fed’s, Mr. Bernanke, is an expert on depressions. He knows there is no way out. We also find it of interest that the current phase of the crisis was deliberately caused by the Greek crisis, which had been common knowledge for years.

As we plow forward we see the trade deficit for June at a record deficit of $7.9 billion, which is in part a reflection of the phony dollar rally of earlier in the year, when the dollar ran from 74 on the USDX to 89, which made US goods and services 12% to 16% more expensive than euro zone exports.

At the same time real unemployment is 21-1/2% with about ten million working an average of 34.2 hours per week. The sting is strong as borrowers reduce credit card debt by 8% and the use of credit cards has fallen by 23.2%.

In just four months the yield on the 10-year t-note fell from 3.99% to 2.42%. Needless to say, the bonds are trading near a high. This is by design and a reflection of QE. As this unfolded daily, the PPT buys SPUs, which keeps the stock market from tanking. This is how the Fed rigs the stock market that is by injecting reserves into the system. They are assisted by propriety trading desks and hedge funds, which the PPT uses. It is not surprising that Goldman thinks the Fed will buy at least another $1 trillion in securities – bonds. We envision $2.5 trillion over the course of the coming year. The Fed is also in the process of reselling more than $1.8 trillion in CDOs and MBS back to the banks. The Fed refuses to tell us what they paid the banks for the toxic waste, because it is a state secret. We believe it was $0.80 on the dollar and we bet the buyback by the banks will be $0.20 on the dollar. The taxpayer makes up the difference, which is about $1.1 trillion. The remaining $700 billion plus will be used by the Fed to buy Treasuries and Agencies. It will have cleaned up its balance sheet, and the banks’ books to some extent at the same time. The injection of funds will be assisted by bank lending and Treasury and Agency purchases of $1 trillion plus. At this writing these tactics have resulted in mortgage rates of 4.42% on 30-year fixed-rate mortgages, which will probably fall lower. These mortgages will add to the load of guarantees, already at 97%, of Fannie Mae, Freddie Mac, Ginnie Mae and the FHA. This is how you tie the ends together. These circumstances will continue on indefinitely, because the minute the Fed ceases to monetize the system will collapse.

As of yet low mortgage rates are not producing new residential real estate buying. Most of the buying is by speculators. New and used home sales have fallen off a cliff and will continue to do so without special incentives.

At the same time the administration has no intention of cutting deficit spending as revenues continue to fall. There will be annual $1 trillion budget deficits as far as the eye can see. Any leader who steps in tries to stop this band of criminals will quickly be liquidated. Do not forget they control the dark side of the CIA. All the administration is concerned about is lengthening the maturity of Treasury debt, so that they can continue their fiscal profligacy. Of course, the Fed will assist them in this endeavor.

http://news.goldseek.com/InternationalForecaster/1283148720.php

Rydex Asset Analysis

by Carl Swenlin

08/27/2010

The basic Rydex Ratio is the result of dividing Rydex bear funds by Rydex bull funds, and we can use it to gage market sentiment. I think it is useful because it is based on the deployment of real money, not just opinions.

I haven't mentioned the Rydex Ratios much in the last several years because Rydex mutual funds began losing assets after an historical high at the end of 2004, and I began to wonder if the Ratio concept would survive a continuously diminishing asset base. On the chart below we can see how Rydex total assets began a down trend in 2005 that lasted until the end of 2008. Most of that decline took place while the stock market was in a rising trend.

The reason for this decline in assets, I believe, was due to a huge increase in ETFs, which drained assets away from traditional mutual funds. Rydex was particularly vulnerable because these funds were set up to attract active traders, and ETFs were (and are) superior products in that they trade like stocks and ETF positions can be opened and closed at any time during the trading day.

I recently noticed that assets have been flowing back into the Rydex group since the 2009 low, so I took a look at what was going on with Rydex cash flows. (Note that cumulative cash flow differs from total assets in that it shows total dollars flowing in/out of a fund, not simply the current value of fund assets.) The chart below shows that money has indeed been moving into bear funds durning the rally that began in 2009; whereas, flow into bull funds has been tentative -- making new highs, then dropping back to the 2007/2008 base. Incredibly, there was virtually no outflow from bull funds during the 2007/2008 bear market. Note that the bull fund outflow from the April top took the Bull+Sector index to a low not seen since the 2000/2002 bear market.

Looking at the raw readings we can detect the tentative nature of the bulls that has plagued this bull market, and it is obvious that the bears have been progressively more aggressive. Next we need to do the Ratio calculation.

The Ratio helps us identify points at which bullish or bearish sentiment have reached extremes that could result in price reversals. When we look at the Rydex Cash Flow Ratio below, we can see a trading range that has persisted since 2003. There are only two instances where the top of the range has been reached, and each resulted in a correction the most recent being the most severe. The bottom of the range was encountered numerous times, and each time there was a rally. Most notable is that the recent rally has so far been one of the smallest.

I have also marked the bottom of a smaller trading range that formed during the recent bull market. The Ratio blew through the bottom of that range during the current correction, and the most recent Ratio top suggests that it could prove to be a new benchmark for overbought.

Bottom Line: Upon closer inspection, I believe that the proliferation of ETFs has not adversely affected the usefulness of the Rydex Ratios. The most difficult problem to solve when using them is to provide a context within which to identify levels where sentiment is too extreme in one direction or the other. The range of the last seven years looks like something we could rely upon in the future; however, we also need to be alert for the formation of more narrow ranges that may be useful during shorter time frames. For now I think there is the potential for a Ratio range between the July low and the August top. I will be looking for price tops at the top of that range, and for rallies at the bottom.

* * * * * * * * * * * * * * * * * * * * *

Technical analysis is a windsock, not a crystal ball.

* * * * * * * * * * * * * * * * * * * * *

http://blogs.decisionpoint.com/chart_spotlight/2010/08/rydex-asset-analysis.html

MMA Comments for the Week Beginning August 30, 2010

Written by Raymond Merriman

Review and Preview

In the first week following the geocosmic center mass of the Cardinal Climax, and the first week of the new Mercury retrograde cycle (August 20-September 12), equity markets around the world continued their sell-off, and then appeared to reverse at the very end of the week. Yet what may be more interesting is how many economic leaders are changing their tune about the future of the economy since going through that midsection of the Cardinal Climax, July 21-August 21. Prior to - and even during the early part of that time band - the near-unanimous consensus was that the USA would not have a double dip recession. Now the majority are stating that the odds of a double dip recession have just increased, with some actually calling for an outright double dip recession in the next year. Welcome to Mercury retrograde, on the heels of the Cardinal Climax. You are likely to hear many adjusted and “double message” forecasts about the probability of a “double dip recession” as U.S. Treasuries continue to exhibit a “double bubble trouble” pattern.

In Europe, all equity indices we follow declined to new monthly lows on Wednesday, August 25. Those lows did not take out the lows of early July, and were followed by decent rallies into Friday. In Asia and the Pacific Rim, it was a little different. Most indices bottomed on August 25, but in the case of the Japanese Nikkei, it was a new yearly low, below 9000. The Nikkei fell to 8807 on August 25, its lowest price since May 1, 2009. In India, the market didn’t fall to a low at all. In fact the NIFTY index made a new yearly high on August 23.

In the Americas, The Argentine Merval index made a low on August 25 too. Brazil’s Bovespa bottomed out the next day. And in the USA, both the Dow Jones Industrial Average and the NASDAQ Composite bottomed early Friday, and then commenced a healthy rally into the close, following Ben Bernanke’s speech from the Jackson Hole, Wyoming banking summit. Each of these indices held above their lows of early July.

Gold and especially Silver found new life as well after initial softness early last week. From a low of 1773 on Tuesday, September Silver shot up to 1934 during the day on Friday. It closed around 1904. Gold made a new monthly high at 1246 on Thursday in the December contract. Less than a month ago it was trading below 1160. Crude Oil’s performance was similar to the equities and precious metals. That is, it ended a decline to 70.76 on Wednesday, August 25, its lowest price since early June, and then rallied to close the week above 75.00 on Friday.

But the big story continues to be in U.S. Treasuries. They reached a new post-panic high on Wednesday, August 25, but then fell sharply into the close of the week. The Japanese Yen was another fascinating story. It skyrocketed against the dollar, which fell below 84.00 on Tuesday, August 24, its lowest level to the Yen since early 1995, The dollar then rallied sharply into the close of the week too.

Short-Term Geocosmics

So what was so important about early last week, when equities and Silver bottomed, while Treasuries and the Japanese Yen topped out? Well, it was within three trading days of three important “Level 1” (strongest) geocosmic signatures that unfolded August 20 and 21. These included the Sun-Neptune opposition, Venus-Mars conjunction, and the 32-37 year waning square of Saturn and Pluto. On top of that, Mercury also turned retrograde on August 20. Combinations like this, so close in time to one another, usually produce a reversal within three trading days. This was no exception. How long this reversal will last, however, is another matter, because under Mercury retrograde, reversals oftentimes do not last long. More often than not, big price thrusts in any direction usually lose momentum quickly, i.e. within 4 trading days. We also note that these reversals occurred close to the Virgo-Pisces full moon of Tuesday, August 24. Lunations in mutable signs seem to have the most correspondence to reversals in many financial markets, as opposed to lunations in other types of signs.

The next series of important geocosmic signatures starts up on September 4. An abundance of signatures will then unfold lasting through Venus retrograde on October 8. Prepare yourself for another roller coaster ride during that 5-week period, for in addition to ending with the powerful Venus retrograde, we will also encounter the second of three Jupiter-Uranus conjunction passages on September 18. These are two of the highest historical correspondences of all geocosmic signatures to primary or greater cycles in equities, as reported in the studies of “The Ultimate Book on Stock Market Timing, Volume 3: Geocosmic Correlations to Trading Cycles.”

Longer-Term Thoughts

For some time now I have been writing about a “bubble” in financial assets. More recently (since June) I have referenced that such a bubble seems to building in U.S. Treasuries. But the concept of “bubbles” means different things to different analysts. In the strictest numerical sense, a “bubble” is a phenomenon where a financial asset increases sharply in price without any notable and normal declines. In almost all cases, the advance of that asset is at least 100% of a price from which the move up started. More often than not, the increase is 4-10 times higher.

Bubbles have correlations to Financial Astrology. They pertain to Jupiter and/or Uranus, either in the skies at a given point in time, or to the chart of particular entity associated with a financial market. The NASDAQ Composite’s tech bubble started from a base of 750 when Uranus entered Aquarius in 1995 to its high of over 5000 in March 2000, as Uranus advanced to the last third of Aquarius, squared by Saturn and Jupiter in Taurus. Aquarius is associated with technology, and the NSADAQ is a tech-heavy index. Or you could look at the bubble in Crude Oil as Uranus moved into Pisces in early 2003 from a base of about $25/barrel to a high of $147.27 in July 2008, when Uranus was in the last third of Pisces. Pisces is the sign associated with Crude Oil. In each case, the ensuing decline took prices down 70-80% within 6-24 months.

But there is another way to look at bubbles rather in terms of multiples of 4-10 times. Bubbles can coincide with periods of excessive greed or fear, driving investors to flock to a particular investment and thus drive its value sharply higher. This is the case with Treasuries right now, in my opinion, and the basis for my concerns that Treasuries are forming a “Double Bubble Trouble.” There is no way that Treasury Bonds or Notes will appreciate 4-10 times their price at the base from which the move up began, due to the way Treasuries are valued. From a base of 95-105 in 1999 and 2007, Ten Year Treasury Notes rallied to an all-time high of 130/25 on December 19, 2008, as the Federal Reserve Board experienced its 12-year Jupiter return. That was also in the peak of the Financial Panic. It fell back to 115 as recently as April 2010, but is now approaching the 130 area again (the high last week was close to 127).

The reason I suspect this is a bubble is because of the psychology behind this sharp run up in the last 4 months. It is due to excessive fear, again, as investors have piled much more money into the “safety” of Treasuries than they have the stock market. I see this as a dangerous trend – even a “bubble” - due to the psychological factors. But I also see it as “bubble” from the Financial Astrology point of view. Jupiter and Uranus have been in conjunction in the very early degrees of Aries. And this forms a T-square to the Sun-Pluto opposition in the Federal Reserve Board chart (created December 23, 1913). The Fed and the financial products it affects through its decisions (such as Treasuries) are thus akin to a “bubble.”

Many astrologers were baffled that the astrological midsection of the Cardinal Climax did not produce any spectacular events, such as another financial crisis or political overthrow, or start of a new world war. Yet this simply demonstrates a lesson in how astrology works. It is not “causal” in terms of human activity, although it may be causal in terms of natural phenomenon, such as the severe heat and dryness that led to the fires and drought in Russia, and the floods that displaced hundreds of thousands in China and Pakistan.

Astrology correlated to human activity is more “synchronistic” than causal. In the thoughts of the great Swiss psychologist and astrologer Carl Jung, “Every moment of time has its own unique quality, and whatever is born in that moment takes on that quality.” So as I approach the study of astrology, it is not from the viewpoint of predicting an event related to the meaning of each planet and sign. I am more interested in “what is born in that moment” in which an unusual cosmic pattern unfolds. To me, that is the key to understanding what the outcome will be.

As I see it, there were at least three important economic and mundane policies and decisions that were “birthed” in the July 21-August 21 Cardinal Climax midsection. And those decisions commence the cycles that will soon grow into something transformative regarding our economic future. In fact, they have already begun. As I stated in the Forecast 2010 Book, the year 2010 may be the most important year of our collective life as seen from the study of astrology. We have choices going into the summer of 2010. But by then, the choices will have been made and it will be very difficult to turn back the consequences that those choices will generate.

What were those choices and how do they relate to astrology? The first was the Financial Regulatory Reform Act of July 21, which took place as Saturn entered Libra, and with Jupiter and Uranus opposite in Aries. Each of these transits squared the USA Venus and Jupiter. Venus and Jupiter are the “money” planets, and this can be a classical bankruptcy aspect related to spending more than one can afford. And then on August 10, the Federal Reserve Board decided to abandon its pre-announced plan of an “exit strategy” by drawing down its balance sheet. Instead it decided to reflate its portfolio by resuming purchases of long-term Treasuries. It did this as Jupiter was stationary, in exact square to Pluto (an aspect of holding too much debt), forming a T-square to the Fed’s Sun-Pluto opposition. When Jupiter is involved in these kinds of aspects, there can be a tendency to misjudge via over-estimation and exaggeration. That’s the astrological perspective, as I see it. Decisions were made and there will be consequences that will grow out of these new initiatives, and they will have an impact upon life as we know it, for better or worse, per the dynamics of the most potent line up of geocosmic signatures in our lifetime. As above, so below.

The third decision that was made during this period occurred last Saturday, August 21. That was when Russia loaded the rods for a nuclear reactor in Iran. It was on the day of Saturn square Pluto, but also still at the beginning of the 78-year period when the progressed Mars in the USA chart has turned retrograde. Mars rules one’s military outlook. If anyone says that the heart of the Cardinal Climax was a non-event, I beg to differ. I believe it was every bit as important as financial astrologers throughout the world expected. And the markets are reflecting this.

http://www.mmacycles.com/weekly-preview/mma-comments-for-the-week/mma-comments-for-the-week-beginning-august-30,-2010/

•• International Indices Aug 29th ••

]

•• Economic Data for the Week Ahead ••

This Coming Weeks Economic #'s

http://biz.yahoo.com/c/ec/201035.html

Last Weeks Economic Results

http://biz.yahoo.com/c/ec/201034.html

•• Earnings Calendar for the Week Ahead ••

B = Before-Market Hours

D = During-Market Hours

A = After-Market Hours

EARNINGS CALENDAR - REPORTS TO BE ANNOUNCED WEEK OF AUG 29 – SEP 04

Company Symbol Date Time Eps PrevYr

Agria Corp GRO 08/30 B 0.05 0.02

Gazprom O A O OGZPF 08/30 B n/a n/a

Gazprom O A O OGZPF 08/30 B n/a n/a

Ku6 Media Co Ltd KUTV 08/30 B n/a -0.22

Medisana Ag MHH.F 08/30 B n/a n/a

Partner Communications PTNR 08/30 B 0.54 0.48

Agfeed Industries Inc FEED 08/30 D 0.04 0.03

American Italian Pasta AIPC 08/30 D 0.84 0.74

Cascade Bancorp CACB 08/30 D -0.03 -1.00

China Mass Media Corp CMM 08/30 D 0.04 0.00

Delta Nat Gas Inc DGAS 08/30 D n/a -0.16

Deutsche Wohnen Ag DWN.F 08/30 D n/a n/a

Energy Xxi (bermuda) Lt EXXID 08/30 D 0.07 -0.60

Franklin Electr Publish FEP 08/30 D n/a -0.13

Fuqi International Inc FUQI 08/30 D 0.45 0.45

Harrington West Finl Gr HWFG 08/30 D n/a -2.16

Ibasis Inc IBAS 08/30 D n/a -0.01

Innsuites Hospitality T IHT 08/30 D n/a n/a

Jackson Hewitt Tax Svcs JTX 08/30 D -0.75 -0.67

Jesup & Lamont Inc JLI 08/30 D n/a 0.01

Jos A Bank Clothiers In JOSB 08/30 D 0.54 0.48

Life Sciences Resh Inc LSR 08/30 D 0.19 -0.43

Linktone Ltd LTON 08/30 D n/a 0.02

Marshall Edwards Inc MSHLD 08/30 D n/a -0.07

Mesabi Tr MSB 08/30 D n/a 1.26

Nco Group Inc NCOG 08/30 D n/a n/a

Neurobiological Tech In NTIID 08/30 D 0.00 0.53

Nevsun Res Ltd NSU 08/30 D -0.01 -0.01

Origin Agritech Limited SEED 08/30 D 0.61 0.47

Pike Elec Corp PIKE 08/30 D 0.00 0.07

Qiao Xing Mobile Comm C QXM 08/30 D -0.18 0.01

Viryanet Ltd VRYAF 08/30 D n/a n/a

Vocaltec Communications VOCLD 08/30 D n/a -0.17

Volt Information Scienc VOL 08/30 D n/a -1.07

Waste Services Inc Del WSIID 08/30 D 0.15 0.07

Winn Dixie Stores Inc WINN 08/30 D 0.16 0.17

Donaldson Inc DCI 08/30 A 0.64 0.30

Prospect Capital Corpor PSEC 08/30 A 0.28 0.32

Sws Group Inc SWS 08/30 A 0.10 0.25

Baldwin Technology Inc BLD 08/31 B 0.07 0.02

Co Don Ag Teltow German CNW.F 08/31 B n/a n/a

Cpi Corp CPY 08/31 B -0.28 -0.53

Dsw Inc DSW 08/31 B 0.11 0.25

Elbit Imaging Ltd EMITF 08/31 B n/a n/a

Energy Conversion Devic ENER 08/31 B -0.60 -0.37

Funtalk China Holdings FTLK 08/31 B 0.15 n/a

Isle Of Capri Casinos I ISLE 08/31 B 0.11 0.02

Marfin Popular Bank Pub CPB.N 08/31 B n/a n/a

Oil Co Lukoil LUKOY 08/31 B n/a 3.81

Verwaltungs Und Privat VPB.S 08/31 B n/a n/a

Aig Intl Real Estate Kg ARE.F 08/31 D n/a n/a

Applied Signal Technolo APSG 08/31 D 0.22 0.25

Aristotle Corp ARTL 08/31 D 0.04 -0.67

Bank Nova Scotia Halifa BNS 08/31 D 0.87 0.78

Biomerica Inc BMRA 08/31 D n/a 0.01

Champion Inds Inc W Va CHMP 08/31 D 0.02 0.00

China Gerui Adv Mat Gr CHOP 08/31 D 0.24 n/a

Collectors Universe Inc CLCT 08/31 D 0.00 0.15

Crystal Riv Cap Inc CYRV 08/31 D n/a -0.26

Dialysis Corp Amer DCAI 08/31 D 0.09 0.07

Dollar Gen Corp New DG 08/31 D n/a n/a

Duane Reade Inc DRD 08/31 D n/a n/a

Envestnet Inc ENV 08/31 D n/a n/a

Heart Tronics Inc SGN 08/31 D n/a n/a

Image Metrics Inc IMGXE 08/31 D n/a n/a

Imaging Diagnostic Sys IMDS 08/31 D n/a n/a

Ivivi Technologies Inc IVVIE 08/31 D n/a -0.15

K Sea Transn Partners L KSP 08/31 D -0.33 0.16

L & L Energy Inc LLEN 08/31 D n/a 0.13

Metalink Ltd MTLKD 08/31 D n/a n/a

Oceanfreight Inc OCNFD 08/31 D 0.01 -0.10

Oramed Pharm Inc ORMP 08/31 D n/a n/a

Orchard Enterprises Inc ORCD 08/31 D n/a -0.18

Pharmacyclics Inc PCYC 08/31 D -0.08 -0.20

Pinnacle Bank Gilroy Ca PBNK 08/31 D n/a n/a

Polski Koncern Naftowy PSKNY 08/31 D n/a n/a

Protalex Inc PRTX 08/31 D n/a n/a

Riskmetrics Group Inc RISK 08/31 D 0.12 0.11

Spuetz Ag Duesseldorf SPZ.F 08/31 D n/a n/a

Switch & Data Facilitie SDXC 08/31 D 0.06 0.05

Tefron Ltd TFRFF 08/31 D n/a -2.20

Terrestar Corp TSTR 08/31 D n/a -0.44

Txco Res Inc TXCOQ 08/31 D n/a -0.51

Viasystems Group Inc VIAS 08/31 D -0.04 -0.48

Vina Concha Y Toro S A VCO 08/31 D n/a 0.66

Abm Inds Inc ABM 08/31 A 0.41 0.36

Accuray Inc ARAY 08/31 A 0.05 0.02

Concurrent Computer Cor CCUR 08/31 A 0.03 0.03

Culp Inc CFI 08/31 A 0.24 0.14

Silicon Graphics Intl C RACK 08/31 A -0.27 n/a

Sociedad Quimica Minera SQM 08/31 A 0.31 0.32

Unify Corp UNFY 08/31 A n/a -0.27

Borders Group Inc BGP 09/01 B -0.16 -0.18

Brown Forman Corp BFB 09/01 B 0.84 0.81

China Cord Blood Corp CNDZF 09/01 B 0.04 n/a

Express Inc EXPR 09/01 B n/a n/a

G-Iii Apparel Group Ltd GIII 09/01 B -0.02 -0.17

Genesco Inc GCO 09/01 B -0.02 -0.02

Intralinks Hldgs Inc IL 09/01 B n/a n/a

Joy Global Inc JOYG 09/01 B 1.02 1.21

Ltx-Credence Corp LTXC 09/01 B 0.10 -0.07

Trintech Group Plc TTPA 09/01 B n/a 0.04

American Software Inc AMSAE 09/01 D 0.06 0.07

Calavo Growers Inc CVGW 09/01 D 0.41 0.17

Charming Shoppes Inc CHRS 09/01 D 0.03 -0.03

Conolog Corp CNLG 09/01 D n/a n/a

Global Crossing Ltd GLBC 09/01 D -0.74 -1.23

Heinz H J Co HNZ 09/01 D 0.73 0.67

Lantronix Inc LTRXD 09/01 D n/a -0.01

Magal Security Sys Ltd MAGS 09/01 D n/a n/a

Mktg Inc CMKG 09/01 D n/a n/a

Quinenco S A LQ 09/01 D n/a n/a

Casella Waste Sys Inc CWST 09/01 A -0.17 -0.09

China Green Agriculture CGAG 09/01 A 0.24 0.24

Collective Brands Inc PSS 09/01 A 0.33 0.54

Fuelcell Energy Inc FCEL 09/01 A -0.15 -0.21

Greif Inc GEF 09/01 A 1.21 0.88

Hovnanian Enterprises I HOV 09/01 A -0.52 -2.16

Martek Biosciences Corp MATK 09/01 A 0.36 0.27

Oxford Inds Inc OXM 09/01 A 0.07 0.37

Saic Inc SAI 09/01 A 0.33 0.31

Claires Stores Inc CLE 09/02 B n/a n/a

Clientele Life Assuranc CLI.J 09/02 B n/a n/a

Methode Electrs Inc MEI 09/02 B 0.15 0.00

Orascom Constr Inds S A OCIC 09/02 B n/a n/a

Sycamore Networks Inc SCMRD 09/02 B -0.09 -0.20

Toronto Dominion Bk Ont TD 09/02 B 1.41 n/a

Uti Worldwide Inc UTIW 09/02 B 0.17 0.12

Banknorth Group Inc New BNK 09/02 D n/a n/a

Blyth Inc BTH 09/02 D 0.07 -0.01

Cascade Corp CASC 09/02 D 0.50 -1.14

Del Monte Foods Co DLM 09/02 D 0.27 0.30

Inventiv Health Inc VTIV 09/02 D 0.35 0.34

Layne Christensen Co LAYN 09/02 D 0.28 0.23

Movado Group Inc MOV 09/02 D -0.01 0.06

Targeted Genetics Corp TGEND 09/02 D n/a -0.09

Wimm Bill Dann Foods Oj WBD 09/02 D 0.00 0.30

Arcsight Inc ARST 09/02 A 0.13 0.09

Block H & R Inc HRB 09/02 A -0.41 -0.39

Cooper Cos Inc COO 09/02 A 0.71 0.54

Esterline Technologies ESL 09/02 A 1.19 1.09

Finisar Corp FNSRD 09/02 A 0.23 0.03

Krispy Kreme Doughnuts KKD 09/02 A 0.00 0.00

Quiksilver Inc ZQK 09/02 A 0.03 0.03

Seachange Intl Inc SEAC 09/02 A 0.13 -0.01

Take-Two Interactive So TTWO 09/02 A -0.09 -0.66

Ulta Salon Cosmetcs & F ULTA 09/02 A 0.05 0.06

Xinhua Sports & Entmt L XSEL 09/03 B 0.03 0.01

Campbell Soup Co CPB 09/03 D 0.30 0.30

Corpbanca BCA 09/03 D n/a 0.88

•• Monetary Base as of Aug 29th ••

Monetary Base Exponential Average (10 periods) blue, Momentum (Mo) 26 periods

and MACD (exponential 6 and 13 periods), 26 periods ROC (rate of change) blue.

The data is biweekly (1 period)

The Monetary base (definition):

The currency and central bank deposits that together provide the base for the money supply under fractional reserve banking. Also defined as the central bank assets the acquisition of which creates this monetary base by injecting domestic money into the economy. The latter definition usually includes international reserves and domestic credit. By either definition, the monetary base changes as a result of open market operations and exchange market intervention. The data is bi-weekly.

•• YoY & LT Inflation Rate thru Aug 29th ••

•• SGS Alternate Data Series ••

by John Williams

Updated on Aug 6th thru Aug 27th

Money Supply Aug 14th

Inflation - as of Aug 13th

Unemployment - as of Aug 6th

GDP- as of Aug 27th

USD - as of Aug 10th

•• Yield Spreads thru Aug 29th ••

Yield Spread (Recent) between 5 year Treasury Notes yield (blue), and

13 week T-Bill yield (red). 10 year Notes yield (black),30 year Bonds

yield (magenta). Spread between 5 year Notes and T-Bills (maroon).

Yield Spread between 5 year Treasury Notes yield (blue),and 13 week

T-Bill yield (red). 10 year Notes yield (black),30 year Bonds yield

(magenta). Spread between 5 year Notes and T-Bills (maroon).

•• Daily Sentiment Readings thru Aug 29th ••

Rydex Funds Nova/Ursa Sentiment Ratio

NASDAQ Daily Sentiment Index (NDSI)

Option Buyers Sentiment Gauge (OBSG)

•• AAII Sentiment & Market Vane thru Aug 29th ••

![]()

(as of 8/25/2010)

Bullish: 20.74%

Neutral: 29.79%

Bearish: 49.47%

•• Deviation Charts thru Aug 29th ••

•• Short Sales Data Aug 29th ••

Short Interest Ratio

Data Unavailable

Recent Put/Call Options Ratio OEX

Put/Call Options Ratio OEX

OEX Hines Ratio

•• Sentiment & Contrary Opinion Charts are no longer available, it has turned into a pay site.

NOTE: Indicators are not updating, will take a look into the problem

•• CoT Charts thru Aug 29th ••

•• Wall St. Courier Stats thru Aug 29th ••

•• Major Indicators & Indices thru Aug 29th ••

•• Baltic Dry index (BDI) thru Aug 29th ••

BDI - Short Term

BDI - Long Term

BDI vs SPX

BDI vs GOLD

BDI vs OIL

BDI vs CRB

•• Daily/Weekly VIX-VXN thru Aug 29th ••

•• PitBull Crash Index thru Aug 29th ••

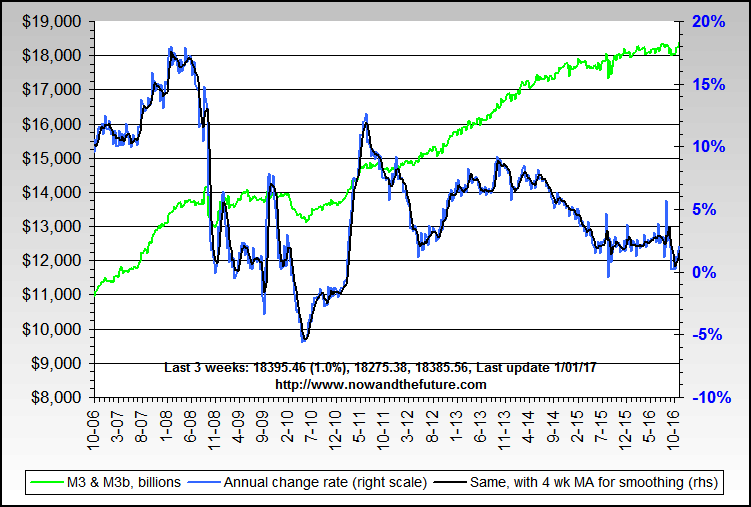

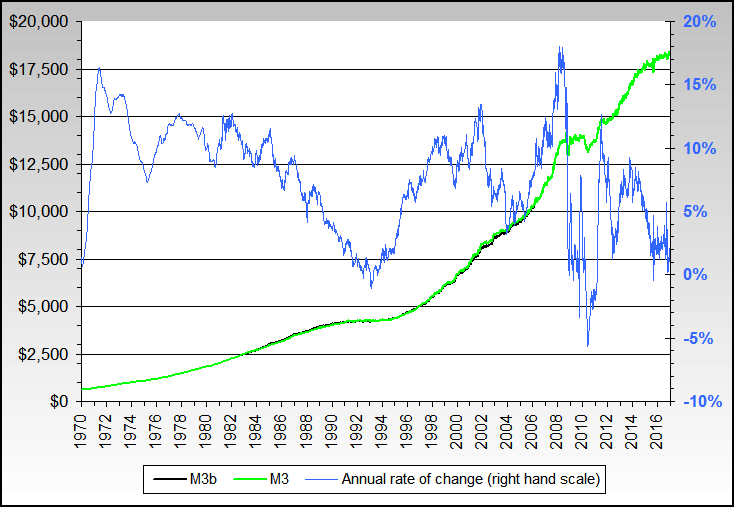

•• M3(b) ST/LT Money Supply thru Aug 29th ••

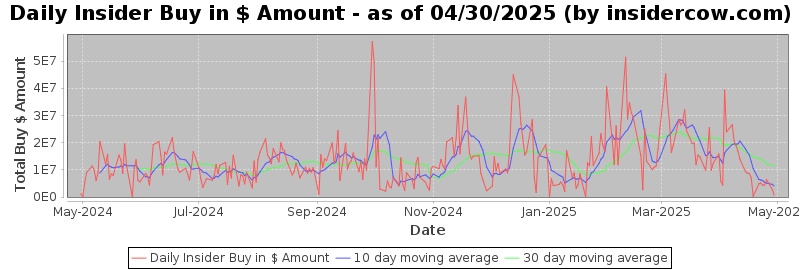

•• Insider Trade Activity thru Aug 29th ••

Top Buys/Sells Over Last 30 Days

http://news.moneycentral.msn.com/process/insider/top10insider.aspx?

•• Fed Market Operations thru Aug 29th ••

FRB POMO Data

http://www.ny.frb.org/markets/pomo/display/index.cfm?showmore=1

FRB SOMA Data

http://www.ny.frb.org/markets/soma/sysopen_accholdings.html

•• Program Trade •• Unavailable - For some reason program trade data is showing Feb'09 data as the last date entered

http://www.nyse.com/press/12_2010.html

•• Program Trade 27.4% NYSE Volume (Aug 2-6) ••

http://www.nyse.com/press/1281607146627.html

Top 20 Most Active Firm

http://www.nyse.com/pdfs/PT080210.pdf

Top 3 Most Active Firms

MORGAN STANLEY & CO. INCORPORATED

GOLDMAN, SACHS & CO.

SG AMERICAS SECURITIES, LLC

NEW ORG

Aug 02-06 25.5% or ~51.0%

Jul 28-02 28.4% or ~56.8%

Jul 19-23 27.4% or ~54.8%

Jul 12-16 28.7% or ~57.4%

-------------------------------------

4-Wks Rolling Avg 27.5% or ~55.0%

•• Fund Flows for Week of Aug 29th ••

08/25/2010 Equity Fund Outflows -$4.6 Bil; Taxable Bond Fund Inflows $3.9 Bil

xETFs - Equity Fund Outflows -$1.4 Bil; Taxable Bond Fund Inflows $2.9 Bil

08/18/2010 - Equity Fund Outflows -$9.1 Bil; Taxable Bond Fund Inflows $4.5 Bil

(xETFs - Equity Fund Outflows -$961 Mil; Taxable Bond Fund Inflows $3.5 Bil)

08/11/2010 - Equity Fund Outflows -$503 Mil; Taxable Bond Fund Inflows $2.8 Bil

(xETFs - Equity Fund Outflows -$153 Mil; Taxable Bond Fund Inflows $2.7 Bil)

08/04/2010 - Equity Fund Inflows $2 Bil; Taxable Bond Fund Inflows $2 Bil

(xETFs - Equity Fund Outflows -$688 Mil; Taxable Bond Fund Inflows $2.1 Bil

MONTHLY

08/20/2010 - July Equity Fund Outflows -$5.2 Bil; Taxable Bond Fund Inflows $28.8 Bil

(xETFs - Equity Fund Outflows -$7.4 Bil; Taxable Bond Fund Inflows $24.1 Bil)

http://www.amgdata.com/#create:home:Home:/php/signup_trial.php

•• Treasury Yield Curve thru Aug 29th ••

U.S. Treasuries

3-Month .14%

6-Month .18%

12-Month .25%

2-Year .55%

3-Year .81%

5-Year 1.49%

7-Year 2.09%

10-Year 2.64%

30-Year 3.60%

Inflation Indexed Treasury

5-Year .12%

10-Year 1.01%

20-Year 1.50%

30-Year 1.64%

National Municipal Bond Yield

2-Year 0.31%

5-Year 1.11%

7-Year 1.66%

10-Year 2.40%

15-Year 2.51%

20-Year 3.91%

30-Year 4.16%

•• National Mortgage Rates thru Aug 29th ••

30 Yr Fixed 4.50%

15 Yr Fixed 3.83%

30 Yr Fixed Jumbo 5.34%

15 Yr Fixed Jumbo 4.85%

3/1 ARM 4.37%

5/1 ARM 3.40%

7/1 ARM 3.63%

10/1 ARM 4.07%

3/1 ARM (I/O) 5.04%

5/1 ARM (I/O) 3.50%

7/1 ARM (I/O) 3.85%

•• Business Closings (~175) Aug 16th thru Aug 29th ••

August 29 , 2010

Perry's Smorgy, Restaurant in Waikiki

Proposed Cuts in Texas, Puts Nursing Homes in Danger of Closing

2

--------------------------------------------------------------------------------

August 28 , 2010

Hampton Towne Centre in Hampton Township Michigan

Dollar Video in DeKalb Illinois

Buckeye Subs and Pizzeria in Bucyrus

Walgreens in Kenosha WI

2 Newark Public Library NJ

5

--------------------------------------------------------------------------------

August 27 , 2010

Maine Department of Education Considering Closing 3 Schools

St. Cecilia Elementary School in Detroit

Northern Airborne Technologies

Acclaim's client-based games Shutting down?

Native Tobacco 101 in Cloverdale

Vista Auto Sales in VA

A free clinic in Kalamazoo Michigan

The Best Chocolate In Town Closing Shop in Chase Tower

Blue Mug Coffee & Tea in Downtown Escondido

7 Oakland California Daycare Centers to Possibly Close

The Value Fresh supermarket at 2401 Cleveland Highway Dalton Georgia

MaggieMoo's Ice Cream in Plymouth

Bruno's Home Furnishings store in Okalahoma City

Keepsake Plants in Parrish Fl - 66 Jobs Lost

Bass Hooligans in Wichita Kansas

French Les Halles Brasserie in Coral Gables.FL

Rosetta Stone Cafe and Wine Bar in Youngstown

Space Happy in CA

Fry's Food Stores Inc in Arizona

Food Land in Gretna

Owning Antiques by Design in Littleton MA

2 Head Start preschools in Hood River

The Teen and Family Counseling Center in Campbell

Bud's Used Office Furniture in Downtown Calgary ( International )

24

--------------------------------------------------------------------------------

August 26 , 2010

Update: Brasserie JO Closing Sunday

Rock Forge Neighborhood House

Maharaja's Jeweler Store in Panama City Beach FL

Update: Royal Bank of Scotland Plans on Closing 14 Insurance Offices - 2,000 job Cuts

Glass Garden Greenhouse in Mount Vernon Ohio

Bruster's Real Ice Cream in Gaston NC

The School of Journalism and Mass Communication in Jeopardy of Closing

Silgan Plastics in Port Clinton Ohio

Athletic Village stores in Edmond and Norman Oklahoma

Pizza Hut at 2250 Chester Blvd. in Richmond Indiana

4 Pamrapo Savings Bank branches on Broadway in NJ

Granny's Chicken Ranch in Wyandotte County

Bally's Blue Ash Location Ohio

Perdue Grocery in Charleston

CVS Mail Order Pharmacy in Birmingham - 400 Jobs Lost

Hillside Pharmacy in Manhattan

Duro Bag to Close Hudson Plant - 63 Jobs Lost

American Eagle Outfitters to close 50 - 100 Stores

Milwaukee's Historic Turner Restaurant

Superfresh in Dulaney Plaza in Towson MD

New Leaf Center in San Francisco CA

The Boulware Mission Center in Owensboro

Gilda's Club in Shorewood Wisconsin

Aviat Networks Inc to Close NC Plant

24

--------------------------------------------------------------------------------

August 25 , 2010

The North Mankato branch of the MRCI Thrift Shop

Blockbuster Video Store in Wilmington / New Hanover County NC

Happy Joe's Pizza at 551 South Duff Ave in Ames Iowa

British Nightclubs Closing due to economy

Wild Orchid Restaurant ( International )

5

--------------------------------------------------------------------------------

August 24 , 2010

Tuscany's Coffee House and Bistro Abilene Texas

Irine Fokine Dance Studio in Ridgewood NJ

Widows Creek Fossil Plant near Stevenson, Ala

Dix Campus in Raleigh NC to Close Most Services by End of Year

A Consolidated Container Co. LLC Closing Lakeland Florida Bottle Plant

Sacred Heart School in Michigan

Chips and Deli in Riverdale MD

Niagara Markets ( International )

Blue Marble Closing Its Atlantic Avenue FlagShip Store

Update: Burke's Pharmacy in Scranton PA closing Today

Nearly New Shoppe in Oklahoma

Julie’s Music in Ann Arbor

Update: PW Markets Closing 2 San Jose CA Stores Today

Qualcomm - Software Development Office in the University of Illinois Research Park

Santa Barbara Harley-Davidson

Colony Ford in Warwick , Closing Ford Dealership Side of Business

16

--------------------------------------------------------------------------------

August 23 , 2010

Russel Metals Inc Closing Niagara Area Plant and Cutting 40 Jobs

Jigger's Diner in East Greenwich RI

Bryan & Scott Jewelers Limited in Downtown Colorado Spring

Samuels Furniture and Interiors Closing Cordova Store

Rec Room Plus closing its Omaha store

Jorgensen Supermarket in Greenville Michigan

The Big Kmart at Brooklawn Shopping Center in NJ

Hostess Brands, Inc to Close Decatur Illinois Plant

Update: The Pathmark supermarket in the Broomall Section in PA - 100+ Jobs Lost

Troy and Bloomfield Hills Libraries in Detroit May Close Temporary

Betty Lou’s Health Foods in downtown Duluth Minnesota

Clay Theater in SF CA

A substance abuse prevention center Charleston W. VA

Country Club Closing Nationwide

Fire Station 36 in Burlingame CA, Idle for Rest of the Year

15

--------------------------------------------------------------------------------

August 22 , 2010

Albert Auto Repair in Cedar Rapids Iowa

Carleton Grange Pub

2

--------------------------------------------------------------------------------

August 21 , 2010

Bayer CropScience Plant in Camden County

Bally's in Rockford

Update: Abercrombie & Fitch to close 110 Stores by 2011

Winston’s Pub & Grille & Winston’s Coffee House

Fort Madison Kum & Go

The Golf Galaxy store at Ray Road in Chandler AZ

Frank L. Moose Jeweler in Roanoke VA

CIB Marine Bancshares Branch in Decatur, Ill

Zen 32 Restaurant in AZ

Tula, a high-end boutique at 3738 N. Southport

My Gym, a children's fitness center in Roanoke VA

Joint Forces Command in Norfolk Closing Still Possible

12

--------------------------------------------------------------------------------

August 20 , 2010

Fort Worth Library Texas, Plans to Close 3 Branches

The Varsity Jr. in Atlanta Georgia

Update: Ballard's Ella Mon in Seattle

The Swanson Group Glendale Sawmill

The Ashley Furniture Home store on Huffine Lane in Bozeman

10 Leading Companies Closing Stores

Quattro Wireless ad network

The China Shop in Torrington CT?

Eatmor food market in Pittsgrove NJ

Altmans Winnebago to Close Colton, California Location

Ultimate Escapes Closes its Fort Collin CO Office

Video Expo in Abilene TX

Cotter Corp - Cañon City milling facility

Update: Meridian School in Utah

TerraSalis Garden Center in W. Virginia to Phase out their Retail Operations

Z Galleries in Long Beach CA

Lewiston YWCA in Maine - 32 Jobs Lost

Update: Tree House Books in Holland Michigan

Richard Jones Pit Bar-B-Que in Austin Texas

Bistro Restaurant in downtown Dothan Alabama

20

--------------------------------------------------------------------------------

August 19 , 2010

Strickland Dail Dining in Snow Hill and Farmville

Cocoa Michelle in Downtown Westport

Ham's Restaurant on High Point Road in Greensboro NC

Jim’s Coffeehouse in Elyria Ohio

LLyod's Banking Group Closing Irish Banking Division

CitiMortgage office in Frederick - 930 Jobs Affected

Del-Fair Lanes bowling alley in Delhi Township OH

Krome Studios - Closing / Layoffs??

Crossroads Appliance in Seattle

Wonderland Greyhound Park in Revere

Armstrong Flooring Closing England Plant

Overhead Door Corp in Athen GA closing moving to Florida - 111 Jobs Lost in Athens

12

--------------------------------------------------------------------------------

August 18 , 2010

Fat Beats Closing LA and NYC Store

Eldora’s Books, Etc in Cadiz KY

Toy Box Catering in Danville KY

Stanley Druckenmiller Closing his Hedgefund Company

Main Street Furniture and Appliances Maine

Genuardi's Chesterbrook store in Tredyffrin

The Samba Room restaurant in Downtown Fort Lauderdale

Blockbuster in Pennsville

Jonesy’s Restaurant - a landmark at Napa County Airport

HoneyBaked Ham in Rib Mountain WI

ImClone Systems in Branchburg NJ? - 140 People Affected

American Harley-Davidson dealership on Jackson Road in Ann Arbor

12

--------------------------------------------------------------------------------

August 17 , 2010

Carolina Harley-Davidson

Dobie Theatre, located next to UT in Austin

Propex’s Bainbridge plant

Loon Lake Lodge in Indiana

North Fort Myers popular Pincher's Crab Shack in FL

Bank of America Cinema

Abercrombie & Fitch - 60 Stores

Ferrin's Fruit Winery in Carmel Indiana

BTB Burrito Packard Location in Ann Arbor

Saks Incorporated Closing 5 Stores, including Plano Texas and Cali. Store

Marty's HobbyCraft in Downtown Austin

Plainville True Value Hardware CT

12

--------------------------------------------------------------------------------

August 16 , 2010

Ben and Jerry's on Veterans Parkway in Columbus GA

Menze Construction in Michigan

Schnuck Markets Store in Cordova Tenn.

Professional beach volleyball's AVP Tour

Abilene Adult Day Care in Abilene Texas

Update: Superfresh Stores - 25

Lane County Extension in Oregon

Food for Thought Restaurant Closing but will Keep on Catering

Delphi plans to close a UK plant - 180 Jobs Will be Lost

The University of Scranton Press

Polished Apple, a school supply store in Jacksonville NC

Carrollton Lumber and Wrecking Company closing part of the business

The Lorraine Theatre in Hoopeston IL in Danger of Closing

Update: Talley's on Main Street in CO

14

•• Bankruptcy (~19) Aug 16th thru Aug 29th ••

August 29 , 2010

0

--------------------------------------------------------------------------------

August 28 , 2010

Digital Telecommunications - Chapter 11 Last Week

1

--------------------------------------------------------------------------------

August 27 , 2010

NCoat - Chapter 11

1

--------------------------------------------------------------------------------

August 26 , 2010

Trico Marine Services Inc

Sanluis Co-Inter

2

--------------------------------------------------------------------------------

August 25 , 2010

Oriental Trading Company, Inc

1

--------------------------------------------------------------------------------

August 24 , 2010

0

--------------------------------------------------------------------------------

August 23 , 2010

Boca Raton Bridge Hotel Faces Bankruptcy

Branscum Produce LLC

2

--------------------------------------------------------------------------------

August 22 , 2010

0

--------------------------------------------------------------------------------

August 21 , 2010

Midwest Banc Holdings Inc

Professional Veterinary Products

2

--------------------------------------------------------------------------------

August 20 , 2010

L&H Trucking Company Inc

Lighter and Fuel Maker RCLC Inc

Sierra Nevada Community Access Television

Amcore Financial Inc

4

--------------------------------------------------------------------------------

August 19 , 2010

Boston Generating LLC - Chapter 11

EBG Holdings LLC

2

--------------------------------------------------------------------------------

August 18 , 2010

Mid-Cape Racquet & Health Club

Fletcher Granite Company - Chapter 11

2

--------------------------------------------------------------------------------

August 17 , 2010

Apex Digital - Chapter 11

Audio Visual Integration Inc. of Fort Wayne

2

--------------------------------------------------------------------------------

August 16 , 2010

0

•• Layoffs (~135) Aug 16th thru Aug 29th ••

August 29 , 2010

Swiss drugmaker Roche Holding - Could Cut Thousands of Jobs

Oregon Budget Crisis - Could Mean Layoffs Coming

City of Naples FL - 2

Moll Industries - 91

Viking Range Corp - 18

Update: Long Beach CA - 130 Layoffs for Oct. Planned

6

--------------------------------------------------------------------------------

August 28 , 2010

Fair Lawn NJ - 4