News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Bullwinkle

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

The 27 were born with a silver spoon .. the 397 are the cautious non spending consumers taking cover until the dust settles, could take decades to clear up and with a nation built around service sector jobs and consumer spending, I just do not see how that could be good for anybody... This is why the wealthy are not spending either, be it on goods and services or US investment.

If you can trade around this trash of a market, more power to you. You are one of the few...

Otherwise, buy PMs and commodities, the only real bull market for the last 10 years.

Cycle work has become less and less reliable. I like and follow cycles, but when you have a hand fed trading society as opposed to a free market, cycles are just not as reliable as they once were...

I miss 5 days and come back to a pleasant surprise

WooooHooooo!!! Time to sell an Oz or 2....

Another day or 2 of gains?, retest 1240-1260 support then up and over 1300 .. mmm hmmm, yesir

Very good 8^)

Sell some if he needs some cash or would just like to cash in on some winnings, but silver set to outperform gold (on a pct value) otherwise metals still have a long way to run.

For melt values, go here (very cool website):

Scroll down page for melt values

http://www.coinflation.com/

Sorry for being MIA the last 5 days people, had an episode with some of my meds. All straightened out now, looking forward to getting caught up and posting again... 8^)

Gold Fever Strikes Mom and Pop Prospectors in US West

By: Thomson Reuters

Wednesday, 15 Sep 2010 | 10:37 AM ET

When John Brewer's construction business soured along with the economy, he sought to replace lost income by prospecting for gold from the river valleys of central Idaho to the wilds of Alaska.

Armed with the tools of the trade -- a metal detector, gold pan and sluice box, a series of screens that sort gold from alluvial material like sand and gravel -- the Montana man represents the new face of a pursuit that once paved the way for settlement of the Western frontier.

The poor economy and a record price of gold have renewed interest in prospecting in Western states where public lands are rich with deposits and small-scale operators are all but free from government regulation.

What Brewer has in common with 19th century prospectors is a drive for gold equaled in intensity only by the instinct to keep quiet about its location and volume.

"Asking a miner where they found it and what they found is like asking an angler about his secret fishing hole," said Brewer. "We're not going to tell anybody. As soon as you tell anybody, there will be a crowd—and that would be counterproductive."

Gold prices [XAU=X 1273.8 8.15 (+0.64%) ] hit a record $1,275.20 per ounce Tuesday.

Some gold mining sites economically feasible for the first time in years, prompting mid- and large-scale operators to apply to mine on national forests and on acreage overseen by the U.S. Bureau of Land Management in the Rocky Mountains.

"When gold goes over $1,000 an ounce, everybody becomes a miner," said Russ Bjorklund, minerals manager with Salmon-Challis National Forest in Idaho.

He is among federal land managers reporting a marked resurgence in gold mining, from amateurs armed with pans to corporations working hardrock mines.

Susan Elliott, geologist with Humboldt-Toiyabe National Forest in Nevada, said the rush is on in a state that is the fourth largest producer of gold in the world.

Elliott linked a 75 percent increase in mining activity on the 6.3 million-acre forest to the rise in gold prices in recent years.

"We've got all types: individuals out there with pick and shovel and companies with heavy equipment," she said.

Jon Cummings, who promotes gold-mining adventures at his Idaho resort, says finding what prospectors call "color" in the pan ignites a passion.

"You start finding a little gold in the pan—that's when gold fever kicks in. It's like a drug and you're ready to work all night," he said.

International gold-mining giant Barrick Gold in February gained approval from the federal Bureau of Land Management to expand its Bald Mountain mine in northeastern Nevada.

Bald Mountain represents one of the company's 25 operating mines, eight of which are in the western United States.

Large-scale operators like Barrick must clear a number of hurdles in advance of gold mining, often a years-long process.

But Ray TeSoro, minerals specialist for the U.S. Forest Service region that includes Montana, also described an influx of "mom and pop operations."

Those small-time prospectors, like Brewer, mostly engage in low-impact, stream-side mining like gold panning and sluicing, techniques which rely on gravity to separate heavy gold from sediment.

In the mountains of central Idaho, gold fever is behind trespassing incidents.

Beverly Cockrell, a rancher near Salmon, Idaho, has confronted strangers with "sticky fingers" on her creek-side land, including one who reportedly raided a sluice box.

"We're having to run people off," Cockrell said.

And some economists take a dim view of the gold rush.

"You've got this pretty metal—what does it do?" said James Hamilton, economics professor at University of California, San Diego. "It doesn't create dividends, it doesn't create more productivity; it's a hedge against certain kinds of risks."

But it will take more than discouraging words to dampen the enthusiasm of gold hunters like Brewer, who declined to say what profit he turns from prospecting.

"It doesn't replace a full-time job with benefits, but you work hard enough at it, you might get lucky," he said.

Copyright 2010 Thomson Reuters. Click for restrictions.

http://www.cnbc.com/id/39189036

Obstacle to Deficit Cutting: A Nation on Entitlements

By SARA MURRAY

SEPTEMBER 14, 2010

Efforts to tame America's ballooning budget deficit could soon confront a daunting reality: Nearly half of all Americans live in a household in which someone receives government benefits, more than at any time in history.

At the same time, the fraction of American households not paying federal income taxes has also grown—to an estimated 45% in 2010, from 39% five years ago, according to the Tax Policy Center, a nonpartisan research organization.

A little more than half don't earn enough to be taxed; the rest take so many credits and deductions they don't owe anything. Most still get hit with Medicare and Social Security payroll taxes, but 13% of all U.S. households pay neither federal income nor payroll taxes.

"We have a very large share of the American population that is getting checks from the government," says Keith Hennessey, an economic adviser to President George W. Bush and now a fellow at the conservative Hoover Institution, "and an increasingly smaller portion of the population that's paying for it."

The dimensions of the budget hole were underscored Monday, when the Treasury reported that the government ran a $1.26 trillion deficit for the first 11 months of the fiscal year, on pace to be the second-biggest on record.

Yet even as Americans express concern over the deficit in opinion polls, many oppose benefit cuts, particularly with the economy on an uneven footing. A Wall Street Journal/NBC News poll conducted late last month found 61% of voters were "enthusiastic" or "comfortable" with congressional candidates who support cutting federal spending in general. But 56% expressed the same enthusiasm for candidates who voted to extend unemployment benefits.

As recently as the early 1980s, about 30% of Americans lived in households in which an individual was receiving Social Security, subsidized housing, jobless benefits or other government-provided benefits. By the third quarter of 2008, 44% were, according to the most recent Census Bureau data.

That number has undoubtedly gone up, as the recession has hammered incomes. Some 41.3 million people were on food stamps as of June 2010, for instance, up 45% from June 2008. With unemployment high and federal jobless benefits now available for up to 99 weeks, 9.7 million unemployed workers were receiving checks in late August 2010, more than twice as many as the 4.2 million in August 2008.

Still more Americans—19 million by 2019, according to the Congressional Budget Office—will get federal aid to buy health insurance when legislation passed this year is implemented.

The expanding federal safety net has helped shelter many families from the worst of the downturn. Charlene A. Mueller-Holden doesn't fit the stereotype of a person on benefits. Laid off from J.P. Morgan Chase & Co. in January 2008, Ms. Mueller-Holden, 38, drew unemployment for 99 weeks.

The Newark, Del., resident knocked $40 a month off her mortgage payments through the federal Making Home Affordable Program, designed to keep people in their homes by helping them modify or refinance their mortgages. But when her unemployment benefits ran out, Ms. Mueller-Holden and her husband, a government employee, couldn't afford the $1,008 monthly payments.

She turned to the Delaware State Housing Authority which, under a federally subsidized program aimed at helping families with children stay in their homes, gave her $1,000 a month for five months toward mortgage payments. She and her two sons ate lunch for free at the local school this summer, and she has applied for free lunch for one of her sons who will be a first grader this year.

Ms. Mueller-Holden's family earned too little to pay federal taxes last year, and received an extension on their state taxes. "Quite frankly, I don't care about the deficit," says Ms. Mueller-Holden. "It's going to take years upon years upon years to pay this all back," she says, so it's better to focus on job growth now and deal with the deficit later.

Government data don't show how many of the households receiving government benefits also escape federal taxes. But there is certainly some overlap between the two groups, since many benefits are aimed at those earning too little to pay income taxes and at people who don't have jobs, and who thus don't pay payroll taxes.

Cutting spending on these "entitlements" is widely seen as an inevitable ingredient in any credible deficit-reduction program. Yet despite occasional bouts of belt-tightening in Washington and bursts of discussion about restraining big government, the trend toward more Americans receiving government benefits of one sort or another has continued for more than 70 years—and shows no sign of abating.

An aging population is adding to the ranks of Americans receiving government benefits, and will continue to do so as more of the large baby-boom generation, those born between 1946 and 1964, become eligible. Today, an estimated 47.4 million people are enrolled in Medicare, up 38% from 1990. By 2030, the number is projected to be 80.4 million.

The difficulty of restraining benefits when so much of the population depends on them is now on view across Europe, where efforts to rein in deficits are forcing governments to cut popular entitlements. European countries have traditionally provided far more generous welfare benefits than the U.S. has, including monthly allowances for children regardless of income, free college tuition and universal health care. Public retirement programs are also bigger, since the combination of aging populations and low birth rates means fewer workers are paying into the system.

In recent months, political leaders in Europe have struggled to convince voters that change is necessary. German Chancellor Angela Merkel has exempted pensions from her government's planned budget cuts, reflecting the growing power of the retiree vote. French President Nicolas Sarkozy is facing mass protests, including a national strike week, as he tries to raise France's minimum retirement age from 60 to 62. Greece's government had to face down demonstrations this year when it slashed pension benefits, as it was forced to do to get bailout money from other European countries and the International Monetary Fund.

Still, Europe does offer examples that change is possible. Germany slashed benefits for the long-term unemployed in 2004, a step that analysts credit with prompting more Germans to get jobs as well as improving the country's budget balance. Cuts to entitlements are politically possible, says Daniel Gros, director of the Center for European Policy Studies, a nonpartisan think tank in Brussels, "but societies need some time to get used to the idea."

The U.S. government first offered large-scale assistance during Franklin Delano Roosevelt's New Deal. The Social Security Act, passed in 1935, created the popular retirement program as well as unemployment compensation, the early stages of what became known as "welfare" and assistance to the blind and elderly. In the 1940s, the G.I. Bill offered unemployment benefits, education assistance and loans to veterans. That same decade, Washington began offering free or reduced-price lunches to children from low-income families and, a decade later, monthly benefits to the disabled.

Lyndon Johnson's Great Society programs brought food stamps plus Medicare and Medicaid. In the 1970s, Supplemental Security Income was created on top of routine Social Security benefits for the poorest of the elderly and disabled, and so-called Section 8 vouchers began subsidizing rental housing. The earned-income tax credit was launched in 1975 to offer extra cash to low-wage workers, and grew in the 1990s to become one of the government's principle antipoverty programs.

Benefits for children were expanded in 1997 with the State Children's Health Insurance Program during the Clinton administration—and were expanded again in 2009. Shortly after President Barack Obama took office, Congress passed the American Recovery and Reinvestment Act, the stimulus bill, which among other things extended unemployment compensation and offered incentives for states to cover more workers.

All this is expensive. Payments to individuals—a budget category that includes all federal benefit programs plus retirement benefits for federal workers—will cost $2.4 trillion this year, up 79%, adjusted for inflation, from a decade earlier when the economy was stronger. That represents 64.3% of all federal outlays, the highest percentage in the 70 years the government has been measuring it. The figure was 46.7% in 1990 and 26.2% in 1960.

When the economy recovers, some—but not all—current recipients of federal aid are likely to lose their benefits, which some say is reason enough to keep them going for now.

"If there became an expectation that government was going to provide over half of the population's well-being to a significant degree without requiring anything of the recipients, there would be reason for concern," says Robert Reischauer, a former Congressional Budget Office director and now president of the Urban Institute, a liberal-leaning think tank in Washington, D.C. "I don't think that's where we are or where we're headed."

The public appears divided on what to do. A new Allstate/National Journal poll found that 35% of voters want the government to make sure future retirees receive all the benefits they've been promised even if it means raising taxes. Another 34% said the government should make retirement programs "financially sustainable" by making some cuts to those benefits and raising some taxes, and 22% said they'd be willing to see benefits cut to restrain the programs' rising costs.

The call for restraining benefits resonates with voters like Robert Letherman. "You name it, someone is lining up to get bailed out, or a handout, courtesy of the hard-working American taxpayer," says Mr. Letherman, 39, a real-estate developer in Elkhart, Ind.

Mr. Letherman says he has struggled through the recession like many others, but doesn't qualify for government assistance. His income has declined 40% since 2007. Some $4 million in development projects percolating in the spring of 2007 have since been shelved.

He supports helping people in need, says Mr. Letherman, but believes many people game the system. Extended unemployment benefits, for example, give some Americans an excuse not to go back to work, he says. If it were up to him, government would be half the size it is now.

He favors eliminating pensions for all government workers, excluding military and intelligence personnel, and would impose a nationwide sales tax to pay off the country's debt. "If we continue down the path of deficit spending, the great recession of 2008 will be nothing compared to what we will face in five, 10, 20 years," he says.

Cutting federal benefits while the economy is still weak would be a mistake, some analysts say, because it could hinder recovery by giving consumers less money to spend.

Paul Hester has relied on government benefits since he lost his job in June 2009. The 54-year-old microbiologist has a master's degree and was earning a salary of $50,000 at the Indiana State Department of Health. He says he regularly looks for jobs, but has landed only two interviews in the past year.

Influenced by the credit wariness of parents who lived through the Great Depression, the Indianapolis resident has always been thrifty. He once watched his dad walk into a dealership, "plop down $10,000 in cash and buy a car." Mr. Hester has one credit card, and before he was unemployed, he tried to pay it off every month.

He lives on $375 a week in unemployment checks and his health-insurance premiums are subsidized by the federal government under a provision in the fiscal stimulus enacted by Congress in February 2009. His daughter, a college sophomore, pays for part of her schooling with Pell Grants, a federal program for low-income students that is set to expand because of new legislation that increased the number and size of grants.

"I don't like taking government money," says Mr. Hester, but "what else is there?"

—Marcus Walker contributed to this article.

http://online.wsj.com/article/SB10001424052748703791804575439732358241708.html?mod

MBA: Mortgages Applications Drop For Second Week

by RTT Staff Writer

9/15/2010 7:53 AM ET

(RTTNews) - U.S. mortgage applications dropped to their lowest since early August last week, as extraordinarily low interest rates failed to spark demand for home purchases, industry data revealed Wednesday.

Refinancing activity also tailed off, as most qualified homeowners wishing to lower their monthly mortgage costs have already done so.

The Mortgage Bankers Association's (MBA) Market Composite Index for the week ending September 10, 2010 decreased 8.9 percent on a seasonally adjusted basis from one week earlier, when mortgage apps slipped 1.5 percent.

The results include an adjustment to account for the Labor Day holiday. On an unadjusted basis, the Index decreased 27.4 percent compared with the previous week.

The Refinance Index decreased 10.8 percent from the previous week. The seasonally adjusted Purchase Index decreased 0.4 percent from one week earlier.

The average contract interest for 30-year fixed-rate mortgages decreased to 4.47 percent from 4.50 percent. 15-year rates decreased to 3.96 percent from 4.00 percent.

http://www.rttnews.com/Content/USEconomicNews.aspx?Id=1419398&SM=1

Crude Stocks Fall In Line With Expectations

By Naureen S. Malik

09-15-10 11:15 EST

US OIL INVENTORIES:Crude Stocks Fall In Line With Expectations

NEW YORK -(Dow Jones)- U.S. crude inventories fell in line with analysts' expectations last week, according to data released Wednesday by the U.S. Department of Energy.

Crude oil stockpiles fell by 2.5 million barrels to 357.4 million barrels for the week ended Sept. 10, right in line with analysts' estimates. Late Tuesday, the American Petroleum Institute, an industry group, reported a 3.3-million- barrel increase.

On the New York Mercantile Exchange, crude oil futures maintained early losses, with October contracts recently down 1.7% at $75.51 a barrel. October futures for gasoline were recently down 1.2% at $1.9464 a gallon and heating oil was 0.4% lower at $2.1207 a gallon.

Inventories of crude oil and petroleum products remain at unusually high levels for this time of the year.

Gasoline stockpiles decreased by 694,000 barrels to 224.5 million barrels, the department's Energy Information Administration said in its weekly report. That compares to the forecast calling for a decrease of 1.1 million barrels in a Dow Jones Newswires survey of 12 analysts.

Distillate stocks, which include heating oil and diesel fuel, fell 340,000 barrels to 174.5 million barrels. Analysts projected an increase of 200,000 barrels.

Refining capacity utilization declined by 0.6 percentage point to 87.6%. Analysts had expected a 0.7-percentage point decline.

API pegged the refinery utilization rate at 85.6% of capacity last week, also a 0.6 percentage point drop. The industry group's data showed a 1-million decline in gasoline inventories and that distillate stocks fell by 1.5 million barrels.

U.S. Oil Inventories:

For week ended Sept. 10:

Crude Distillates Gasoline Refinery Use

EIA data: -2.5 -0.3 -0.7 -0.6

Forecast: -2.5 +0.2 -1.1 -0.7

Swaziland -

http://www.saplaces.co.za/swaziland.html

Everbank

https://www.everbank.com/

Oanda

http://www.oanda.com/

>>> At least that 4 trillion is given back to the taxpayer >>>

Sounds good, NOT...

Republicans now claim top 2% tax cut necessary for economic rebound

http://www.examiner.com/special-interests-in-chicago/republicans-now-claim-top-2-tax-cut-necessary-for-economic-rebound

Rich Americans Save Tax Cuts Instead of Spending, Moody's Says

http://www.bloomberg.com/news/2010-09-13/rich-americans-save-money-from-tax-cuts-instead-of-spending-moody-s-says.html

Related Story: Republicans pledge to fight to preserve Bush-era tax cuts

http://www.washingtonpost.com/wp-dyn/content/article/2010/09/13/AR2010091303980.html

This is from the Your Economy board and posted by kismetkid .. Unbelievable... #msg-54416182

http://tinyurl.com/2587ffa

Wow! That's amazing .. very sad.

BP could not possibly ever make up for the amount of destruction they've created. Even worse is they could have prevented this if they had followed protocol and replaced the faulty equipment.

I am sure a lot of fisherman are out of work and a lot of sea life that may not ever be replaced.

OT: (sort of) Patriotism as a Threat to Capitalism

Sep 13, 2010 - 10:29 AM

By: Kel_Kelly

From The Case for Legalizing Capitalism - Having learned that the government acts in ways detrimental to its citizens economically, and by causing wars, we should ask exactly why we support our politicians, why we support most of our military operations, and why we support our very national identity. In short, we should ask ourselves why we are patriotic.

What is patriotism? What exactly are we supporting when we are patriotic? If the answer is "our country," does that mean a geographical region that our government has artificially and arbitrarily identified as its own? If so, does our patriotism change when the boundaries change? Should we not have been patriotic toward the southwestern states before we stole them from Mexico? Should the residents there have been patriotic toward the United States once they were forced to be citizens? Should the citizens of the various countries of the Soviet republic have been patriotic to the USSR after they were forced at gunpoint to be countrymen? Should the citizens of Czechoslovakia — who were forced together by Woodrow Wilson — have been patriotic toward the Czech republic or to Slovakia after the nation split up? Geographical borders are only imaginary, temporary, lines.

Is patriotism instead the act of being loyal to the land itself, specifically the land upon which one grew up? If so, should someone who grows up in Nevada but moves to Connecticut for their career be patriotic toward Nevada or Connecticut? One might reply that the answer is both, because one lived in and identified with both regions.

If that's the case, what if one grew up in the United States, but had a career overseas in South Korea teaching school or working for a multinational corporation? Is it bad if such a person is also patriotic toward South Korea? What if I have lived in France and learned to love the people and the land and actually prefer France to the United States? To whom should I be patriotic, to France or to the United States? Am I unpatriotic to favor France?

If so, were our forefathers unpatriotic to want independence from their native Britain and make America their new home? We Americans don't seem to think so now. But if the Latinos of Miami wanted to make Miami their own new Cuba by seceding, or if the southwestern states wanted to secede from the nation as a separate country or once again become part of Mexico, we would call them traitors.

Or is patriotism based on a connection to the people of a nation, to our fellow citizens? If so, should I be loyal to Americans because they are my compatriots? Why should I? It is my very patriotic neighbors who democratically vote to take my property and give it to someone else against my will. It is my neighbors who vote for regulation and government intervention that makes my life worse. It is my fellow citizens who vote for politicians that create wars and send millions of their own citizens to die.

Naturally, our government leaders call stealing from our neighbors patriotic. In 2008, Joe Biden said, "it's time [for the rich] to be patriotic … time to jump in … time to be part of the deal … time to get America out of the rut." Many people in fact do believe that the rich need to pitch in and help us innocent workers who are in this rut — a rut created by Biden and other government officials by their policies of printing money, spending more than they can steal from citizens, and in many other ways destroying our wealth and bringing on economic crises. It is a rut that was created because we voted yet again for the same bad policies of the last 100 years.

Biden implicitly says the wealthy are using too much of their money to provide us with goods and jobs. They should instead turn their assets into cash and give it to us to consume. Thus, according to Biden, it's unpatriotic to provide the things that improve our lives. Conversely, it's patriotic to squander all our wealth.

If this is patriotism, we should all be anti-American. Most Americans support these terrible ideas and support terrible politicians like Biden who cause this harm. The same applies to politicians and citizens in every country. Why should one be loyal to such people?

The people of Argentina — and other Latin American countries — face massive economic crises caused by their thieving politicians every decade, crises that involve hyperinflation that wipes out their life's savings, creates banking crises, mass unemployment, massive national debt, and general suffering. They have endured human-rights abuses, political persecution, subservient judiciaries, lack of accountability, widespread corruption, virulent demagoguery, social upheaval, and the absence of individual economic rights for centuries. Yet Argentineans are incredibly patriotic and proud of their nation.

Citizens of Mexico and Cuba risk life and limb to escape to the United States in order to find work and survival, because their fellow citizens and government offer them few opportunities at home for prosperity. Yet both of these peoples proudly display their native flags while in exile.

Citizens of Germany and Austria have been led into war over and over with millions of fathers and brothers killed, yet they are historically always patriotic and ready for the next war (though since World War II they have been largely antiwar). Why should any of these people be patriotic? Exactly what are they supporting by being devoted to their country?

"National borders mean nothing."

Patriotism is an abstract notion with no real substance. It means nothing; it's just a façade, a fake, imaginary glue that keeps a people naively devoted to causes, countries, governments, and neighbors who usually bring them harm (the phrase "come together" is similarly ambiguous and empty). National borders mean nothing. They would not exist without government force, and they are usually laid out for reasons of politics and power, not in accordance with the religions, identities, culture, or preferences of individuals.

Time and again, decade after decade, borders change. The people on each side of a new border are supposed to be loyal to people within their new border, and to the new government forced upon them. They often resist and want their previous identities back. It is for this reason, and for reasons of freedom and self-rule, that regions such as Chechnya, Georgia, Palestine, Quebec, Northern Tibet, Taiwan, Sri Lanka, and Kosovo, among many others, often fight for independence. More often than not, those who fight for freedom (and for socialism, incidentally) are called freedom fighters, but they are labeled terrorists by those who oppose their separation.

In today's America, patriotism, effectively, is the act of aggressing upon other nations; it is the act of stealing from our fellow man in the name of furthering our prosperity, while in fact destroying our prosperity. It is under the name of patriotism and supposed freedom that it is justifiable for the United States to attack citizens of any country, including its own.

Patriotism is usually the cause of many of our problems, not the solution to them. And as time passes, we become more obsessed with it. Now, a government official, or even football players and referees, cannot appear in public without an American flag on their lapel or jersey. Soon, it will be required that each of our cars have the red-white-and-blue ribbon plastered on it (for the few left that don't already) — and such things have certainly happened in this country previously. We must all show that we are, as Biden said, "part of the deal." It is reminiscent of Nazism, where all citizens swore allegiance to their ruler and proudly saluted and waved the Nazi flag in the name of nationalism; they lived and died for the glorious fatherland. We are only several steps behind them.

The right-wing radio hosts further this cause by obsessing about why we need to protect ourselves from aggressors and terrorists and fight for our freedom. In truth, there would be little to no protection needed if we would just leave the rest of the world alone. And not only do Republicans not offer us freedom through the economic and social policies they propose, but they cause us to lose freedom at rapid rates during the wars they sucker us into.

The patriotism charade is now at the point that these talk show hosts tell each caller (that they agree with) that they "are great Americans," and each caller, in return, tells the host that he, too, "is a great American." One wonders how they don't feel just a bit silly with such melodramatic antics.

And when all of "our boys," our "heroes," are at war, willingly taking money to go and kill other people around the world, many of us blindly "support our troops." It does not matter whether our troops are actually helping or harming us, or saving people or destroying them: because they are American troops, we should support them … just as the German people blindly supported their Nazi troops simply because they were German.

Patriotism leads people in each country to think that their country is superior to others, and that their country must survive and prosper at all costs — even if it means death to people in other countries. Patriotism breeds an "us-versus-them" attitude. Without the notion of patriotism and national borders, people would live wherever and however they prefer, practice the religions they want, marry whomever they desire, and produce, exchange, and prosper in whatever way they see fit. (There does need to be, and there would be, a governing body, just not a single one with monopoly powers of enforcement and control.) We would not see ourselves so much as members of particular groups (nationalities), but as various people of the world. And yet we are forced by law to "celebrate" diversity in our government-controlled world.

"No one should be loyal and patriotic to someone who allows them to be mostly free."

In absence of government borders, people would more easily mix and mingle in the world and not look at each other as "those other people" but instead naturally look at them as their neighbors. Those who wanted to be racist or simply to keep to their own kind would be able to do that, too, on as much property as they could peacefully acquire through exchange.

People could quickly rush to judge me as unthankful. They could say that I should be grateful that my country has permitted me the level of freedom that it has, which is in fact far in excess of most countries, even if it diminishes by the month. Indeed, I am grateful to be lucky enough to live in a place that offers relative freedom. But this is not a reason to be loyal. If it were, we could also argue that a wife who gets beaten up periodically by her husband who threatens to bring much greater harm to her if she tries to leave him, but is otherwise treated well and quasi lovingly by him, should also be loyal to him. She should in this case be thankful that he allows her a relatively normal life, even if he threatens to use force against her and periodically does.

This thinking is wrong. No one should be loyal and patriotic to someone who allows them to be mostly free but still treats them unfairly. Freedom from harm and coercion should be a natural right, not something granted by those good enough not to kill us or keep us as slaves. This is why, for example, it is still illegal and unacceptable to forcefully hold women against their will or to strike a fellow man as an initiating aggressive act. Aggression is aggression, even in a free society.

The Ills of Democracy and Political Parties

Political parties in every country have their shticks, and each one usually entails some form of socialism. In the United States, the Republicans' agenda consists of imposing their hypocritical and extreme religious beliefs on our country and causing wars, killing, and setting up dictators in other countries. The Democrats' agenda involves deliberately trying to destroy our means of increasing our standards of living, and trying to equalize everyone by dragging us all down to the lowest economic common denominator. These issues are the things each party merely focuses on; but, in fact, both parties promote most of the same policies. Both of these groups, along with every other form of government, engage in the use of force to make people live and act differently from what they would otherwise choose, and to make them hand over much of their personal property once it's been fairly earned.

Regardless of the fact that Republicans (and Democrats to a lesser degree) claim to be about free markets and capitalism, they are not. Republicans are socialist and totalitarian just like the Democrats. Individuals fervently support their respective Republican and Democratic parties, and see the other party, which they detest, as supporting reprehensible views. In the bigger picture, Republicans and Democrats are virtually side by side on the political spectrum that runs from communism (full socialism) on one side, to free-market capitalism (complete freedom) on the other. Both parties, for example, recently had their respective plans for government bailouts, and for nationalizing our healthcare system.

Our society is always proud to support "democracy" as though it automatically equates to freedom. But freedom is not necessarily related to democracy and may or may not coincide with it. A dictator, such as Pinochet in Chile, can create largely free markets, and a democracy can create near or complete totalitarianism, as was the case with the democratic election of Adolf Hitler and more recently with that of Hugo Chavez. Democracy can really be reduced simply to a method of voting, one that allows the expropriation of the property of others — "the tyranny of the majority."

Though it is socialists of one stripe or another, be they fascists, dictators, communists, or Democrats who have begun every war in the last century, killing hundreds of millions, who have strictly and often violently controlled and directed individuals in their respective countries, and who have caused starvation, unemployment, and suffering of millions for decades, it is socialism that most people in the world cling to as something that will help them. Mild socialists (your average Democrat or environmentalist), curiously, think that extreme socialists (communists) are bad, even though communism is just an advanced state of the policies socialists adamantly support.

After World War II, our economists and government officials were impressed with the socialist system that destroyed Germany's economy, and they wanted to replicate it for the economy of the new West Germany. Thankfully, West German leaders, aware of this, and aware of the destruction that Nazi economic policies had caused, through twists and turns, set up a system of relatively free markets that brought dramatic economic growth for the next 30 years (overcoming the negative effects of the Marshall Plan[1]).

People support the evil of socialism because, ironically, they fear that individual companies — which have rarely, if ever, had anyone killed, and which, absent government regulation, have never taken anything forcefully from anyone, and could not only not bring harm, but provide improvements for our lives — can somehow hurt them. All because they don't understand what capitalism is and how it works.

The Patriotism of Politicians

While politicians claim to be patriotic and to do what's best for America, they do the opposite. How could they know what would truly help or hurt American citizens? Have they spent years studying economic cause and effect? Have they learned production techniques that could result in greater output? Have they read numerous books on organizational behavior, so that they can "plan" the economy? Of course not!

They have spent their days kissing babies, polling to find out what voters want, learning to be actors, and making emotional, passionate speeches that appeal to the masses who will be suckered into such antics. In short, politicians are equivalent to game-show hosts. If they were really patriotic, they would spend their time figuring out how truly to help people, instead of simply figuring out how to win votes.

We naively believe politicians are there to "lead us." We believe that the president, in "running the country," has the toughest job on earth. This is partly because people who do not understand economics believe that a country cannot "run" on its own. But it can.

It is the individual people and businesses that progress our lives. The president does not get up in the morning and turn on the factory lights or start the machines. He does not determine how much should be produced that day. He does not decide who should work where. Individuals, capital, and market prices run the country.

"The president does not get up in the morning and turn on the factory lights or start the machines."

President Obama is not "leading" us through this crisis — he's simply manipulating the economy further than it was already manipulated. Had he not done so, the market (i.e., individuals) could have already fixed itself.

We have seen that the government's planning does not help an economy. We have seen that regulation does not protect citizens from companies, and that military actions do not protect citizens from foreign aggressors (except in special circumstances). Of course, some of the actions the president engages in involve setting or adjusting laws pertaining to protecting our legal rights and our legal property. But most of his actions involve just the opposite — taking our property or preventing our free-will choices.

For example, there are laws that prevent gangs from barging into our homes and kicking us out of them; but, at the same time, there are many more laws linked to how our homes will be taken from us by the government if we fail to pay one of the myriad taxes forced upon us — taxes that legally allow our property, our paychecks, to be given to others, including these very gangs, via wealth redistribution.

The same type of "work on behalf of the people" is done by all members of Congress and the Senate, and to a lesser degree by state and local government. The country would get along quite fine in any given year if Congress and the president ignored all of the "work" it would otherwise do, except for focusing on the 1 percent or so of the decisions that involve truly protecting citizens and providing basic services that we want and need. Most of the other 99 percent of their work involves imposing implied or actual government force for the purpose of benefiting one group at the expense of another. The government is simply an institution — an instrument — that is used to bring about these iniquitous actions.

Politicians' "work" involves doing what is needed to please their constituents. Their constituents, in turn, usually want government subsidies, regulation, wealth transfers, or some other government force imposed, so that they can benefit from the suppression of others when they otherwise could not.

Almost everything we see government doing today consists of this: bankers, car companies, airlines, and steel companies are subsidized at the expense of taxpayers so that they don't have to go out of business; workers are protected from having to receive market wages; poor workers are protected with a minimum wage; companies are regulated so that they don't harm consumers; government forces the negation of contracts such that borrowers can benefit at the expense of lenders; inflation is generated so that more money can be taken from taxpayers and given to others; environmental legislation is imposed in order to let environmentalists "protect our environment" at the expense of the rest of us; one industry is prevented from producing a particular product so that another industry's profits will not be affected. The list literally goes on and on for tens of thousands of pages (in the national register).

Though all of these actions are detrimental to society, politicians don't care. What they care about is getting votes. They care about getting re-elected. They will therefore do what appears to help voters, even though their actions usually harm voters. The long-term health of the country is not in their interest; the short-term success of their career is. They do not know exactly what would help or what would harm, but they need not be concerned with such immaterial matters.

This is why it is so vitally important for voters themselves to understand what helps and harms them. If voters would demand of politicians the things that would truly benefit them, politicians would give it to them, for they will pass or not pass whatever laws will get them votes.

If people demanded that government quit printing money, quit regulating businesses, quit taxing, and stopped stealing from the rich, the government would cease these operations. Then, all members of society would see a dramatic increase in their standards of living, with jobs available to everyone and prices falling by the day.

But there is a catch: those of us who earn less than the average — those who are net beneficiaries of wealth redistribution — would have to clearly understand how they would benefit from refusing to vote for free money. They would have to understand that, instead of having money handed to them, they would instead earn money in the form of a salary. But this change in structure would result in significantly increased wealth for this group. This issue is likely the biggest challenge free markets face, for it is very difficult to convince someone that if they refuse free money they will be better off.

Kel Kelly has spent over 13 years as a Wall Street trader, a corporate finance analyst, and a research director for a Fortune 500 management consulting firm. Results of his financial analyses have been presented on CNBC Europe, and the online editions of CNN, Forbes, BusinessWeek, and the Wall Street Journal. Kel holds a degree in economics from the University of Tennessee, an MBA from the University of Hartford, and an MS in economics from Florida State University. He lives in Atlanta. Send him mail.

http://www.marketoracle.co.uk/Article22657.html

The Samson Indicator

By Robert Morley

September 14, 2010

Hindenburg Omens, inverted yield curves, cardboard boxes and a better economic indicator.

Everybody has their idea on where the economy is headed. And there are many economic indicators that claim to predict America’s economic future. Some work better than others. The Samson Indicator beats them all.

Consider America’s economic pillars—the columns supporting America’s economy.

Pillar 1: Housing Market

In August, America’s unsold housing inventory increased for the eighth straight month. At the current rate of sales, it would take 12.5 months to sell the houses already on the market. In the past, housing inventory averaged between six and seven months’ supply. During the boom years, there was sometimes less than a four-month supply.

The volume of house sales is simply crashing. In July, sales were down 27 percent from the previous month, the National Association of Realtors reported. Compared to last year, sales are down 25 percent—no small feat considering last year’s dismal numbers.

Why is the housing industry so important to the economy? During the euphoric years, the housing market and related industries, including investment bankers, mortgage brokers, realtors and appraisers, created up to 40 percent of all jobs. Now those jobs are gone, and some say for good.

Manias and Ponzi schemes—like America’s housing bubble—burn many people when they burst. And when they do, they drastically alter national psychology. Smaller is now better. Property taxes do matter. Lower rent is preferred. No upkeep is vogue. Increased mobility is valued. In short: Renting is in and buying is out.

The “get rich from housing” mantra is replaced by the “I will never buy a house again” creed.

Keeping their job is now the priority for most people. But jobs are not so easy to find anymore.

Pillar 2: Industry

After World War ii, America became an industrial superpower. “American made” was shipped around the world. Americans exported products, and in return, imported gold as payment.

The world needed what America produced, and America became rich. Employers couldn’t find enough workers, and thus the prosperity trickled down.

But wealth led to complacency and consumerism.

American culture no longer values production. America has allowed its manufacturers to go out of business or relocate overseas to low-wage, low-union locales. Recently General Electric announced that due to new government regulations requiring energy conservation, it would close its last incandescent light bulb factory in the U.S. Two hundred employees will lose their jobs when this last plant closes. Instead, the government has decided that consumers should purchase fluorescent light bulbs.

Unfortunately, florescent light bulbs are only produced overseas—so Americans will be forced to send money overseas to import them (so much for the promise of all those green jobs).

Yes, America manufactures a lot less of the things people want or need these days.

Take a look at Boeing—perhaps one of America’s most strategic companies. Where does Boeing produce its new Dreamliner aircraft?

The wings are produced by Mitsubishi in Japan. The horizontal stabilizers are made by Aeronautica Italy. The wingtips are contracted out to Korea and the wing flaps to Australia. The fuselage is fabricated in Japan, Italy and the United States, while the under-fuselage is made in Canada. The passenger doors are made in France, while the cargo and crew escape doors are stamped “made in Sweden.” The floor beams are manufactured in India. The wiring and landing gear are also made in France, while the engines are produced both in Britain and America.

Is Boeing really even an American company?

There was a time when the whole aircraft—from drawing board to factory floor—was made in America, providing jobs to tens of thousands of Americans, and hundreds of thousands more within the supply chain.

Those days are gone. In July, America lost 47,000 more manufacturing jobs, according to the Bureau of Labor Statistics

Even many of the minerals used to build the planes are imported. Although carbon fiber is produced in the United States, all the aluminum and about 70 percent of the titanium has to be imported because America’s mining industry has been allowed to atrophy. There is a whole host of other strategic minerals that America no longer mines too.

Ever wonder why China gets 10 percent growth and America gets 10 percent unemployment, as Historian Niall Fergusson commonly notes?

Because we are a nation of consumers, while China is a nation of producers!

Actually, the economic divide is far worse than what Fergusson says. In August, China reported that its industrial production grew 13.9 percent, and that retail sales grew 18.4 percent—while back in America, the real unemployment rate is closer to 20 percent, according to John Williams at Shadowstats.

Pillar 3: Middle Class

But not all people are suffering.

The top 5 percent of income earners account for 37 percent of all consumer spending in America. Ten years ago, the top 5 percent accounted for 25 percent of spending. The top 1 percent of households own about 35 percent of the nation’s wealth. The top 20 percent own approximately 85 percent, according to sociology professor G. William Domhoff at the University of California–Santa Cruz. And the percentages have increased since 2007.

The gap between the rich and poor is growing. The middle class is getting crushed.

Forty million Americans, or one in eight people, are now on food stamps. An astounding 10 million workers are receiving unemployment benefits. So it is no surprise that recent studies show that a shocking 15 percent of Americans now live beneath the poverty line.

A large middle class is something that has set America apart from much of the rest of the world.

The middle class is said to be much of the power behind America’s dynamism and innovative spirit. These are people who build and create and are responsible for starting thousands of small businesses each year. They are the brains within the mega corporations. Think of all the products and inventions over the years that were the product of middle-class Americans. Think Bill Gates and Henry Ford. These men are products of middle-class America.

If you are reading this, you are probably a product of middle-class America. But look around you: The middle class is being destroyed. Your friends and colleagues, if they are like most Americans, are saturated with debt. Students are graduating universities with useless degrees and tens and hundreds of thousands of dollars of debt. Americans act like they are wealthy, living beyond their means, but it is really all a sham—an expensive, unsustainable, debt-powered sham, but a sham nonetheless. And it is coming to a crashing end.

Cracked and Buckling

America’s economic pillars are snapping like small twigs. No matter where you look—our massive debt, state debt, local debt, personal debt, our dependence on foreign lending, our addiction to oil, the Federal Reserve printing money to fund the Treasury, our sick currency, the economic quagmires in Iraq and Afghanistan—the stress lines are showing.

It doesn’t take a genius to see which way the economy is headed.

The Samson Indicator is this: When the pillars break, the roof collapses. As it is, what is left of America’s support columns is barely holding up. It is almost as if some invisible force is just barely keeping the building together.

America could quickly be thrust back into the Great Depression or worse. It wouldn’t take much more of a push for it all to come crashing down: a failed bond auction or two, a surprise banking failure, a new war. It could be any number of things, because America’s whole economic house is shaky.

Yet, as depressing as that may sound, America’s looming economic collapse will not last forever. The system is headed for collapse, but once the current unsustainable system is wiped out, and once people are fed up enough with the current system, then a new honest and affluent system will be built.

http://www.thetrumpet.com/index.php?q=7471.6052.0.0

Gold: Heads You Win, Tails You Win

Bsspoke Investment Group

Thursday, September 9, 2010 at 05:40PM

If someone came up to you and said that they were going to flip a coin and if heads came up you win and tails came up they lose, you would probably walk away and tell the person to get lost and go try to con someone else. In terms of gold, though, we are increasingly beginning to hear people argue that gold will rise no matter what happens!

Today we read one article that quoted an analyst as saying "Either a swift economic recovery or further dismal economic performance should bring new buyers into the market." We realize that there are certainly some valid arguments for buying gold, but a comment like this is not one of them. Now, we wouldn't necessarily go as far as to say that gold is in a bubble. After all, unlike a lot of recent asset bubbles where prices skyrocketed even as supply expanded, the supply of gold is relatively constrained. That being said, arguments presented as a win win regardless of the outcome are usually found closer to the peak of a move than the beginning.

http://www.bespokeinvest.com/thinkbig/2010/9/9/gold-heads-you-win-tails-you-win.html

Restaurant Stocks Shoot Higher

Bespoke Investment Group

Wednesday, September 8, 2010 at 01:20PM

Below is a list of the 30 biggest restaurant stocks in the Russell 3,000 run through our trading range screen. The rally in McDonald's (MCD) has received a lot of attention recently because it is the biggest of the bunch, but the entire group has been doing very well. As shown below, only 2 of the 30 names listed are currently trading below their 50-day moving averages (Sonic and Red Robin), while 23 are trading in overbought territory. Well-known names like Buffalo Wild Wings (BWLD), Chipotle (CMG), Brinker (EAT), PF Changs (PFCB), Panera (PNRA), and Yum! Brands (YUM) are all trading more than 2 standard deviations above their 50-days. While the S&P 500 is still down for the year, the average stock in this group is up 24.25% in 2010. Chipotle (CMG) is up the most at 88.97%, followed by Domino's Pizza (DPZ) and DineEquity (DIN). Sonic (SONC) is down the most at -22%.

http://www.bespokeinvest.com/thinkbig/2010/9/8/restaurant-stocks-shoot-higher.html

Year-End Consensus S&P 500 Price Target Drops to 1,205

Bespoke Investment Group

Wednesday, September 8, 2010 at 11:31AM

A number of Wall Street strategists have recently lowered their year-end S&P 500 price targets in Bloomberg's weekly survey. This has caused the average target to drop to 1,205, which is 20 points below where it started the year. Five of the twelve strategists have now lowered their targets after raising them earlier in the year. At 1,205, the consensus is still looking for a gain of 9.47% from current S&P levels to the end of 2010. Have a look below at all the changes that have been made to the target throughout the year. It's bad enough to try to predict where the market will be a year from now, and now they have to go changing them all the time?

http://www.bespokeinvest.com/thinkbig/2010/9/8/year-end-consensus-sp-500-price-target-drops-to-1205.html

Stocks with the Highest Short Interest

Bespoke Investment Group

Tuesday, September 7, 2010 at 05:31PM

Below is a list of the stocks in the Russell 1,000 with the highest short interest as a percentage of float (SIPF). For each stock we also provide its year-to-date change as well as its change since the start of the month. Generally when the market is rising, the most heavily shorted stocks outperform, and we've seen that so far this month as well.

In the Russell 1,000, AutoNation (AN) has the highest short interest as a percentage of float at 40.74%. With a gain of 25%, AN has hit the shorts pretty hard year to date. Alliance Data Systems (ADS) and MGM Resorts (MGM) rank second and third in terms of short interest and are the only other names with SIPF above 30%. SunPower (SPWRA) and Sears Holdings (SHLD) round out the top five with SIPF of 27.65% and 26.05% respectively.

Netflix (NFLX), MBIA (MBI), and Las Vegas Sands (LVS) are all on the list as well, and the shorts have gotten killed in these names this year. All are up more than 100% year to date. Shorts have had a field day this year with SunPower (down 52%), Comstock (down 48%), and ITT Education (down 43.7%). Some other notable names on the list include Green Mountain Coffee (GMCR), US Steel (X), First Solar (FSLR), Jefferies (JEF), AIG, Newell Rubermaid (NWL), and Garmin (GRMN).

http://www.bespokeinvest.com/thinkbig/2010/9/7/stocks-with-the-highest-short-interest.html

Key ETFs Farthest Above 50-Day Moving Averages

Bespoke Investment Group

Friday, September 3, 2010 at 10:23AM

Below we highlight the key ETFs that we follow that are currently trading the farthest above their 50-day moving averages. As shown, the Internet stock ETF (HHH) is currently on top of the list at 10.31% above its 50-day. Malaysia (EWM) ranks second at 9.29%, followed by Base Metals (DBB), Australia (EWA), and then REITs (IYR). A lot of times we'll see ETFs from one asset class clustered at the top of the most overbought list, but it is currently pretty diverse.

Below is a chart of the Internet ETF (HHH) that is currently trading 10% above its 50-day. As shown, the ETF has made a huge move over the last four days. We also provide a table of the stocks that make up HHH. As shown, Amazon.com (AMZN) and eBay (EBAY) collectively make up about 60% of the ETF. Both have been soaring lately and are now trading more than two standard deviations above their 50-days. They're the reason HHH has done what it has done this week.

http://www.bespokeinvest.com/thinkbig/2010/9/3/key-etfs-farthest-above-50-day-moving-averages.html

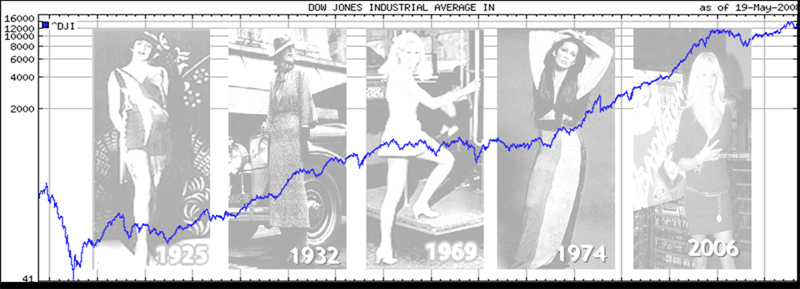

The Hemline Index

By Barry Ritholtz

September 13th, 2010, 11:30AM

With NY Fashion Week over, perhaps its time to take a look the hemline index, which we last looked at in June.

Here is the math behind the psychology, via Baardwijk & Franses of the Econometric Institute:

“Urban legend has it that the hemline is correlated with the economy. In times of decline, the hemline moves towards the floor (decreases), and when the economy is booming, skirts get shorter and the hemline increases. We collected monthly data on the hemline, for 1921-2009, and evaluate these against the NBER chronology of the economic cycle.

The main finding is that the urban legend holds true but with a time lag of about three years. Hence, the current economic crisis predicts ankle length shirts around 2011 and 2012.”

Intriguing...

![]()

Sources:

The hemline and the economy: is there any match?

THE ECONOMICS OF HEMLINES AND CLEAVAGES

A Hemline Index, Updated

http://www.ritholtz.com/blog/2010/09/the-hemline-index/

7 Things To Do To Improve

The Kirk Report

Wednesday, September 8, 2010 at 10:18 AM

In celebration of my 7th anniversary, I would like to share with you 7 simple things I think you can do to improve your performance in the markets for the remainder of the year:

1. Stop believing the market is logical – The market is primarily moved by both perception and emotion far more than reality or logic. Trade what you see, not what you think you should or want to see. There’s a reason why most people stink at trading as they fail to understand that markets are often illogical and influenced by emotion rather than reality. Whenever possible, try to adopt and hold an “opportunistic” mindset rather than a dominant bullish or bearish posture.

2. Concentrate your holdings – If you have more than 5 to 10 positions in your portfolio, you are hindering your performance without even realizing it. With the availability of ETFs now, you can diversify as much as you need. Likewise, even if the best of environments, you probably should only be able to find a handful of really good opportunities that offer the most upside with the least amount of risk. Frankly, if you are able to find more than that, then you really don’t understand what it means to find a true low risk/high reward opportunity!

3. Stop chasing performance – The very best opportunities before you now are in stocks and sectors that no one is talking about or even knows to look at. Likewise, stop looking to chase the hot hand of others. The media and far too many investors are always focused on what is working well now and who is making the most money while the best opportunities are frequently elsewhere. Go where the market is quiet and which no one is interested in and you’ll find more opportunity. In addition, being patient when you don’t find anything that really fits your eye is more than half of the battle.

4. Turn off the noise – Information may be the world’s most precious commodity, but 99% of the information at your disposal is not. In today’s age of real-time information, opinions, analysis, etc. it is my strong belief that information overload and noise is hindering performance far more than it is helping. The first step is to stop watching all TV and to place severe restrictions on all media. In addition, to perform better this year you must stop wasting time on seeking out advice and opinions that only serve to confirm what you really want to hear in order to justify your positions. If anything, what time you spend in social media should be devoted to looking for ideas that challenge your positions and/or offer unique insight you can really learn something from.

5. Understand your limitations and strengths – Not everyone can be a short-term trader nor do they have to be. The mistake that many make is copying another’s strategy that doesn’t fit them nor one they truly understand. This is why they also readily abandon those strategies when the pressure is on which really hurts performance. So, figure out how much time you can devote, what skills you already have, and formulate a strategy that works best for you based on that. Keep in mind also that the best strategies are often so simple that you should be able to explain how they work to those who aren’t intimately involved in the markets.

6. Accept you will make many mistakes – Those who learn how to minimize the damage when they are wrong and who readily own up to the mistakes they make will do far better over the long haul. Making mistakes is a part of this game, but knowing how to handle them is everything. Likewise, if you attach your ego to your portfolio’s performance you are destined for failure. The market absolutely loves to kill those with big giant egos and who look for the markets as a place to prove how smart they are. Markets chew and spit out these folks routinely for good reason and they will continue to do so at every available opportunity.

7. Become a specialist, not a jack of all trades – You don’t have to know everything about everything to do well. In fact, those who focus on a specific setup, chart pattern, program pattern, industry group, or even just trade only one ETF frequently perform far better than those who know a lot about a lot of things but have no real discernible edge. I run into people all of the time who know a great many things, but are not an expert of any one thing and that is to their clear disadvantage. So, find something that interests you more than anything else and concentrate all of your time and focus on that one thing. That path will lead you to developing an clear edge that will provide huge profits to you down the line.

If you follow these 7 tips, I’m confident you will see a meaningful improvement in your bottom line results this fall!

http://www.kirkreport.com/category/freereports/

On a Yield Basis...

Ticker Sense

September 09, 2010

Many of the DJIA members have pretty attractive dividend yields versus bonds.

http://tickersense.typepad.com/ticker_sense/2010/09/on-a-yield-basis.html

Blogger Sentiment Poll

Ticker Sense

September 13, 2010

The poll is at the highest bullish levels of the year for the first full week of trading in September.

Blogger Sentiment Poll Participants:

24/7 Wall St (+) Carl Futia (+) Dash of Insight (+) Elliot Wave Lives On (+) Fallond Stock Picks (-) In the Money Learning Curve (-) MaoXian Millionaire Now (N) Peridot Capitalist (N) StockAdvisors.com Smart Money Tracker (+) Traders-Talk (-) Wishing Wealth (+)

http://tickersense.typepad.com/ticker_sense/2010/09/september-13th-blogger-sentiment-poll.html

Geithner Urges Action on Economy

SEPTEMBER 12, 2010

By DEBORAH SOLOMON

WASHINGTON—Treasury Secretary Timothy Geithner said Washington is at risk of undercutting an already sluggish economic recovery if it fails to provide quick, additional support to business and individuals.

Mr. Geithner said the biggest challenge facing the economy right now was Washington paralysis. He urged Congress to take up the White House's recent proposals to give tax incentives to business and fund new infrastructure projects.

"If the government does nothing going forward, then the impact of policy in Washington will shift from supporting economic growth to hurting economic growth," Mr. Geithner said during an interview with The Wall Street Journal in his U.S. Treasury office, citing the example of countries who "shift too quickly to premature restraint" after a crisis, including the U.S. in the 1930s.

Mr. Geithner's comments are part of a White House campaign to convince a nervous public that the administration understands what ails the economy, and to push lawmakers to act on its prescriptions, including extending tax cuts for the middle-class. Coming ahead of the November midterms, his comments also echo the Democrats' emerging election pitch: that they are better stewards of the economy than Republicans.

Congress returns this week for its final session ahead of the November midterm elections to confront a series of contentious issues, including the expiration of the Bush tax cuts and a $30 billion package to aid small business.

On Sunday, a top Republican lawmaker signaled there might be room to compromise on extending the Bush tax cuts for high-income earners but, in a sign of how fraught the issue is, his words drew immediate skepticism from Obama administration officials. "I want to do something for all Americans who pay taxes," House Minority Leader John Boehner of Ohio said on CBS' "Face the Nation." "If the only option I have is to vote for some of those tax reductions, I'll vote for it. But I've been making the point now for months that we need to extend all the current rates for all Americans if we want to get our economy going again, and we want to get jobs in America."

Austan Goolsbee, the newly appointed chairman of the White House Council of Economic Advisers, said of Mr. Boehner's comments: "I noticed the qualifier, 'if my only choice is'."

Mr. Goolsbee, speaking on ABC's "This Week" added: "If he's truly saying that we can, as the president called for, get a broad consensus to extend the middle-class tax cuts, we should do it."

Some Democrats have joined Republicans in urging an extension of all the tax cuts, including those for high-income earners, while others want all the cuts to expire. President Barack Obama has said he wants to extend all but the top two brackets. Lawmakers may put off the issue until after the elections.

“[The] typical error most countries make coming out of a financial crisis is they shift too quickly to premature restraint. You saw that in the United States in the 30s, you saw that in Japan in the 90s. It is very important for us to avoid that mistake. If the government does nothing going forward, then the impact of policy in Washington will shift from supporting economic growth to hurting economic growth.”

--Timothy Geithner on risks to the U.S. economy

Mr. Geithner, in the interview, rejected the view of many economists that allowing taxes to rise is unwise at this point in the recovery. The White House estimates the one-year cost of extension at $35 billion and the 10-year cost at $700 billion.

"We don't have unlimited resources," Mr. Geithner said. "We just don't think it would be responsible for this country, given the size of our future deficits, and given the substantial burden the middle class has been bearing over the past decade in particular, to go out and borrow $700 billion from our children so we can sustain those Bush tax cuts that only go to the wealthiest 2% of Americans."

He said the U.S. can no longer rely on consumer spending, which has long powered the economy, to be the growth engine that leads the recovery this time around and said Washington needed to plant the seeds for business investment and exports.

"We can't go back to a situation where we're depending on a near short-term boost in consumption to carry us forward," he said.

Last week, Mr. Obama rolled out a package of proposals aimed at spurring business investment and job creation, including making a research tax credit permanent, allowing companies to temporarily expense 100% of capital investments and funding $50 billion in new infrastructure projects. The administration says the proposals would be paid for by ending other corporate tax breaks and closing loopholes.

Business groups and some economists embraced portions of the package, particularly the tax incentives, but there is little consensus among lawmakers and no clear indication that any of the ideas will find traction in Congress. Some Democrats, including Michael Bennet of Colorado, have already come out against more infrastructure spending.

Douglas Holtz-Eakin, a Republican economist and president of the American Action Forum think tank, said the tax incentives were a good idea but questioned ending other corporate tax breaks to pay for them.

"Expensing probably would be a bonus and would send something like the right signal to the business community. But they're not willing to just do it," he said. "The business community won't support" ending other tax breaks to pay for new ones, he said.

http://online.wsj.com/article/SB10001424052748703897204575488053602454926.html?mod=WSJ_hpp_LEFTWhatsNewsCollection

At Goldman, Partners Are Made, and Unmade

By SUSANNE CRAIG

Published: September 12, 2010

On Wall Street, becoming a partner at Goldman Sachs is considered the equivalent of winning the lottery.

This fall, in a secretive process, some 100 executives will be chosen to receive this golden ticket, bestowing rich pay packages and an inside track to the top jobs at the company.

What few outside Goldman know is that this ticket can also be taken away.

As many as 60 Goldman executives could be stripped of their partnerships this year to make way for new blood, people with firsthand knowledge of the process say. Inside the firm, the process is known as “de-partnering.” Goldman does not disclose who is no longer a partner, and many move on to jobs elsewhere; some stay, telling few of their fate.

“I have friends who have been de-partnered who are still there, and most people inside think they are still partners,” said one former Goldman executive, who spoke only on the condition of anonymity. “It is something you just don’t talk about.”

Goldman has roughly 35,000 employees, but only 375 or so partners. The former Treasury Secretaries Henry M. Paulson Jr. and Robert E. Rubin, and former Gov. Jon S. Corzine of New Jersey, now chief executive of financial firm MF Global, were all partners.

It can take years to make partner, and being pushed from the inner circle can be wrenching.

“Being partner at Goldman is the pinnacle of Wall Street; if you make it, you are considered set for life,” said Michael Driscoll, a visiting professor at Adelphi University and a senior managing director at Bear Stearns before that firm collapsed in 2008. “To have it taken away would just be devastating to an individual. There is just no other word for it.”

The financial blow can be substantial as well. Executives stripped of partnership would retain their base salary, roughly $200,000, but their bonuses could be diminished, potentially costing them millions of dollars in a good year.

While gaining the coveted status of partner, and then losing it, is certainly not unheard-of at private financial and law firms on Wall Street, Goldman’s partnership process stands out for its size and intricacy.

Goldman weeds out partners because it is worried that if the partnership becomes too big, it will lose its cachet and become less of a motivational tool for talented up-and-comers, people involved in the process say. If too many people stay, it creates a logjam.

The average tenure of a partner is about eight years, in part because of natural attrition and retirements. Goldman insiders also note they have what they call an “up-and-out” culture, leading to the active management of the pool.

The process of vetting new candidates for partner and deciding which existing partners must go began in earnest in recent weeks, according to people with knowledge of the process, which takes place every two years. They spoke on the condition of anonymity. The 2010 partners will most likely be announced in November.

Candidates are judged on many qualities, primarily their financial contribution to the firm. But lawyers and risk managers — who are not big revenue producers — can also make it to the inner circle.

The executives responsible for running the partner process this year are the vice chairmen, J. Michael Evans, Michael S. Sherwood and John S. Weinberg; the head of human resources, Edith W. Cooper; and the bank’s president, Gary D. Cohn.

Goldman typically removes 30 or so partners every two years, said those people who described the process. The number is expected to be significantly higher this year because fewer senior executives have left the firm as a sluggish economy and uncertain markets limit their opportunities elsewhere.

Removing partners like this is unique to Goldman among publicly traded firms. When companies go public, they shed the private partnership system, and ownership of the company is transferred to shareholders. Goldman’s ownership was also transferred to shareholders, but it created a hybrid partner model as an incentive for employees.

Those whom Goldman does not want to keep are likely to be quietly told in the coming weeks. Each situation is handled differently, the people with knowledge of the process say. Some partners are given time to find other jobs outside the firm. Others are told they will not be made partner and are asked to consider what they want to do next within the company.

While Goldman is on track to remove many more executives than usual, the process is in its early stages and no final decisions have been made, these people caution.

A Goldman spokesman declined to comment on how it selects and removes partners.

The process is at the heart of Goldman’s culture, a way for the firm to reward and retain top talent. Goldman was one of the last of the big Wall Street partnerships to go public, selling shares in 1999.

When it was private, the partners were the owners, sharing in the profits, and in some cases having to put in money to shore up losses. To retain that team spirit as a public company, Goldman continued to name partners. In 1999, there were 221.

Yet there are differences from past practices. When Goldman was a private partnership, it was rare that a partner would be asked to leave.

“Once you made partner, you typically retired as a partner,” said another former Goldman executive who used to be involved in the process. “If we asked someone to leave, it was because we had really screwed up and the person wasn’t pulling their weight.”

It has been a rough year for Goldman. In July, it paid $550 million to settle civil fraud accusations that it had duped clients by selling mortgage securities while failing to make critical disclosures. The firm did not admit or deny guilt.

Still, even in the worst of years, the chance to ascend into the private partnership at Goldman is a huge honor. Candidates can be up for partnership two or even three times before finally being chosen.

Partners get investment opportunities not offered to other employees, and are typically the highest paid at the firm. Goldman will even book tables for them at fashionable New York restaurants.

A big payday is not guaranteed, however. When the firm does not do well, partners tend to bear the brunt of it.

Top Goldman executives did not receive bonuses in 2008, the peak of the financial crisis. But in 2007, a banner year for Goldman, the firm set aside $20.19 billion for compensation and benefits, and its chief executive, Lloyd C. Blankfein, took home $68.5 million in stock and cash.