News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

would like to thank the Academy

CohibaMan

![]()

would like to thank the Academy

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

would like to thank the Academy

Gold Climbs as Higher Physical Demand Counters Decline From ETPs

By Glenys Sim - Apr 29, 2013

Gold advanced, trimming the worst monthly loss since December 2011, as demand for physical metal countered outflows from bullion-backed exchange-traded products. Silver climbed.

Bullion for immediate delivery rose as much as 0.7 percent to $1,472.78 an ounce, and traded at $1,468.65 at 11:55 a.m. in Singapore. Gold is heading for an 8.1 percent drop in April after the metal plunged into a bear market this month.

Gold climbed 4.2 percent last week, the best showing since January 2012, as coin and jewelry demand expanded from the U.S. to China and India. The volume for the benchmark contract on the Shanghai Gold Exchange surged to a record last week, while premiums to secure supplies in India jumped to five times the level before the slump. Coin sales by the U.S. Mint are set for the highest since December 2009, while inventories monitored by the Comex tumbled last week to the lowest level since July 2008.

“Buoyed by strong continuing Asian demand, gold moved higher,” Howard Wen, an analyst at HSBC Securities (USA) Inc., wrote in a note. “The reduction in Comex inventories may be due in part to dislocations in demand in the physical market, as metal is moving from the west to the east to satisfy demand for physical buying in India and China.”

Sales and volumes at Chow Sang Sang Holdings International Ltd.’s 44 shops in Hong Kong more than doubled in the period from April 13 to 27 from a year ago, according to Dennis Lau, director of sales operations at the jewelry maker and retailer.

Record Drop

While prices have advanced 11 percent from a two-year low of $1,321.95 on April 16, they are still 5.9 percent below the April 11 close of $1,561.45 that preceded the rout. Assets held in ETPs shrank 166.27 metric tons so far April, heading for the biggest monthly drop on record in tonnage terms, according to data compiled by Bloomberg.

Gold for June delivery rose as much as 1.3 percent to $1,472.20 an ounce on the Comex and traded at $1,467.80. Hedge funds and other large speculators held 69,726 so-called short contracts on April 23, within 0.6 percent of the all-time high reached six weeks earlier, U.S. Commodity Futures Trading Commission data show. A short position is a bet on lower prices.

Silver gained 0.9 percent to $24.215 an ounce, 15 percent lower this month, the worst loss since December 2011. Platinum rose 0.7 percent to $1,487.15 an ounce, set for a third monthly decline. Palladium rose 0.2 percent to $682.40 an ounce, down 12 percent this month in the worst performance since September 2011.

To contact the reporter for this story: Glenys Sim at gsim4@bloomberg.net

To contact the editor responsible for this story: James Poole at jpoole4@bloomberg.net

Obviously Mrs. EZ is the SMART one in the marriage.

But then you probably already knew that since day 1, lol.

Good morning EZ. Really loving the San Francisco Bay coffees out here. FOr $33 delivered, you get a box of 80 great k-cups. I have Breakfast Blend, Fog Chaser, and the French Roast. Pretty much 3 different levels of STRONG and BOLD coffee that taste great and a great price.

Good morning Stuff and Lottos! Will be posting from time to time today, lots of the usual Monday meetings and such to go through. Futures all very slight red while you sleep, but Gold and Silver VERY green. Should be a quiet night until econ data comes out.

You got your big hat for the Derby? Can't believe I will be here and missing it, that to me is the TRUE kick off to Spring.

I am off, back again tomorrow while everyone is sleeping. Going to be a busy market week, let's all make some money out there!!

I am going with NORMANDY INVASION for the Derby.

I agree with you Stuff, why I bought an electric push mower. I make my wife use it, tell her it saves the environment from carbon gas.

LOL, good morning EZ, was just talking about ya. How are you doing on this fine day?

I will be checking out your pony board one day, and see all the great winners you guys are picking. I can't wait to hit Yonkers when I get home.

For that price, I can probably get a few Mexicans to LIVE with me, mow the lawn, wash the dishes, clean the house, AND do the windows!

I bet EZ is out buying one right now.

Yeah, I was looking at it, but man, I just don't know which way it will go. My GUESS is that no matter what, it will pop, only because the short interest is so big. Look at GME, a POS that had crappy earnings and real crappy future guidance, but it is constantly making new highs because the short interest is insane at 75%!! The kind of move I am thinking CALL makes. HLF will probably do the same, so if it were me, $40 calls would be the play.

LOL, we were all having fun yesterday watching the news. Have you noticed that all of a sudden, the idea that MAYBE Syria has chemical weapons is quite alright by EVERYONE!!?? If it were Bush, the whole Lamestream Media would be frothing at the mouth, fighting to be first to call him a liar and a war criminal. Now, we were watching the Rachel Maddow show (No, we do NOT actually watch it because we want to, but AFN News Channel plays different shows) She was just chatting away on how dangerous these weapons are, when and how they are used, etc... Friggin' Incredible.

ANyway, I really find it hard to believe we would actually go there, but who the heck knows. If they can find me in Vegas.....

I still got some DVAX Calls I bought a few months ago, $2.50 JULY calls I got for .20 I am hoping for some sort of good FDA news, or a possible buyout as they have a very good Hepatitis drug.

Thanks DA, I am also hoping for a quick train up so I can get the heck out and start drinking beer and eating steak in Vegas. Oh yeah, my wife will be there as well, I guess I will need to take her out or something, lol.

Ah yes, I see that. Mmmm, I would sell DA for a few of those wings and a couple of COLD BEERS. It does look toppy, not really a place one thinks about for 'budget' food, more of a sports bar. PE looks a bit high, I willlook at $92.50 or $90 Puts tomorrow and maybe play a couple.

HOLY COW!! A very nice jackpot! I hope we win that one!

Just got off the phone with my mother, and she chewed my ear off about Syria, and will I be going, and please come home, etc.... I took care of her for Mother's Day.

We actually had a nasty HAIL storm out here over the week, screwed everything up and delayed our progress. Marble sized hail, and a few golf balls!

Good morning dD. Was looking at your post on earnings, the only one that looks interesting for a play on Monday AFTER the bell is SU. Looks beaten down, starting to come back, and a lot of names in this category are coming back to life lately, thinking maybe some $30 calls, depending on what it does tomorrow.

Thanks Stuff. FINALLY DONE!! We had to move a lot of big equipment from 2 different locations all the way to Kuwait, was a logistics nightmare. Now I am DONE, and will be pretty much staying here on KAF until it is time to go home next month.

ey DA! Just got back from cleaning my room, was going to bounce over to your room and throw up some picks and ask for some charts! I can NOT get any good charts up since I do not have any charting accounts right now, and FreeStockCharts is brutal here as the internet is just like frozen honey.

Back later Lottos. Man, I can not WAIT to get back home to my FAST internet, the speeds out here are PATHETIC. Need to get my charting accounbts back up, and get back in the stock picking groove. Will be palying some picks on Monday, see how it goes, but the slow internet REALLY makes it difficult.

SLV - Man, did I play this worng last month! I went with calls, and it dropped like a hot potato. Will watch it to fill the lower gap at $22 range, and then will look into trying calls again for the upper gap fill. Too much idiocy with printing money in the world for gold and silver to be down, and the paper market will need to catch up to the metals market. Short interest at 14% could make this fly.

Shrot Squeeze idea: CALL Earnings next week. They BEAT big time when they came out last month with late 4th quarter earnings, the Short Interest is HUGE (50%!!). Note pop recently, that started after they released the earnings date. If they beat real good again and show another quarter of growth, could be a nasty squeeze. Maybe $20 calls on CALL. Need to get past the $18 resistance.

C for Puts - Can't work FreeStockCharts on the work computer, but if anyone can do a WEEKLY chart for C over the past 3 years, note the drop from end of April into May each of the 3 years. Double toppy? I am looking at $46 Puts to ride right up to the last week, target of about $42, but would LOVE to see the $40 gap filled, but that may be pushing it. Edxspecting more of the March type move after the high.

WLT - Earnings this week. Last one that needs to pop, like CLF, X, and AKS. May be a good option play for May. Unknown the prices, but I would look at $17.50s if the price is right. Look at the charts below for CLF, X, and AKS, and see the nice pop they recently had. WLT late to the party! Decent amount short, so a mini squeeze can occur if their financials are not atrocious.

Global Economic Calendar (5-1-2013, Wed., A Big Day for News) ~ http://stks.co/tAAZ

Eurozone 2013 GDP Growth To Fall To -0.8%; EUR To Drift Towards 1.20 In H2 - Nomura http://stks.co/cRwc

And if the EZ economy tanks, ours is right behind, as the last GDP report showed.

But....MARKETS WILL BE UP UP UP

<zh>Earnings - Hope Is Fading

Submitted by Tyler Durden on 04/27/2013 19:05 -0400

We have long commented on the hockey-stick-like expectations of a second-half 2013 resurgence in EPS and revenue growth. This miracle waiting to happen is, sadly, increasingly unlikely. As Goldman notes, the S&P 500 bottom-up consensus EPS estimate for the remainder of 2013 has fallen 1% since the start of earnings season. Revisions have been most negative in the Materials (-4.1%) and Information Technology (-3.7%) sectors. Managements are guiding well below consensus estimates. Of the companies have provided 2Q guidance, 76% guided with a midpoint below the mean consensus estimate (versus an average of 69% over the past 28 quarters). The median firm guided 4% below consensus (versus 3% historically). However, since the start of earnings season, bottom-up consensus full-year 2013 estimates are down only 40bp; suggesting analysts and serial extrapolators alike have considerable more reality to catch up to yet - but for now, hope is fading a little with EPS, Sales, and Margins expectations for the rest of the year all being marked down.

It seems the hockey stick is starting to droop...

most notably in Materials, Tech and Industrials...

AAPL Phone Future? SAMSUNG leads the way currently:

Smartphones Outpace Feature Phones, Samsung Leads

More smartphones than feature phones shipped in the first quarter, an industry first, says IDC.

By Eric Zeman, InformationWeek

April 26, 2013

URL: http://www.informationweek.com/hardware/handheld/smartphones-outpace-feature-phones-samsu/240153720

With worldwide shipments of 216.2 million units during the first quarter, smartphones grabbed 51.6% of the total mobile phone market. According to IDC's data, this is the first time that hardware makers have shipped more smartphones than feature phones on a global basis. It's a significant milestone.

Phone makers shipped 418.6 million devices during the quarter, which was up 4% compared to the year-ago quarter (402.4 million), but down compared to the previous quarter (483.2 million). The first quarter typically sees a downturn in sales following the holiday quarter, so these numbers follow the seasonal trends.

The overall mobile market may have grown only 4%, but smartphone shipments improved 41.6% year-over-year, jumping from 152.7 million in 2012 to 216.2 million in 2013. Smartphone shipments dipped just 5.1% from the fourth quarter of 2012, which saw shipments of 227.8 million.

The worldwide transition from feature phones to smartphones has been a long time coming. Mature markets such as North America and Europe have shipped more smartphones than feature phones for a while now. It is emerging markets such as India and others in the Asia-Pacific Rim that are driving the push to smartphones.

"Phone users want computers in their pockets," said Kevin Restivo, senior research analyst with IDC. "The days where phones are used primarily to make phone calls and send text messages are quickly fading away. As a result, the balance of smartphone power has shifted to phone makers that are most dependent on smartphones."

That would be Samsung and Apple.

Samsung shipped more smartphones -- 70.7 million devices -- than any other vendor during the first quarter. It increased shipments by 60.7% percent compared to the year-ago period, and grabbed 32.7% of the smartphone market. Samsung was also the world's largest supplier of all mobile phones, with shipments climbing 22.9% from 93.6 million last year to 115 million during the first quarter. Samsung commands 27.5% of the entire mobile phone market.

When it comes to smartphones, Apple ranks a distant second to Samsung. The company shipped 37.4 million iPhones during the first quarter, giving it 17.3% of the smartphone market. Apple improved shipments only 6.6% year-over-year, and actually lost market share. Apple held 23% of the smartphone market during the first quarter of 2012.

LG, Huawei and ZTE round out the top five smartphone makers during the first quarter, with shipments of 10.3 million, 9.9 million and 9.1 million, respectively. All three companies saw significant year-over-year growth. In fact, LG was the biggest mover in the entire smartphone market, increasing shipments 110.2%. Huawei's growth wasn't far behind, improving 94.1% year-over-year. ZTE saw about half as much growth, improving shipments 49.2% from the year-ago period.

Looking at the entire cellphone market, Nokia ranked second after Samsung. According to IDC, Nokia shipped 61.9 million devices during the first quarter, representing a precipitous 25.1% drop in shipments from the year-ago period. Nokia managed to hold onto 14.8% of the mobile phone market during the first quarter.

Apple followed in third place with its shipments of 37.4 million iPhones. Apple laid claim to 8.9% of the overall phone market.

LG and ZTE round out the top five mobile phone makers, with shipments of 15.4 and 13.5 million, respectively. Those shipments gave LG and ZTE ownership of 3.7% and 3.2% of the cellphone market, respectively. Conspicuously absent from the top five phone makers are companies such as Motorola, Sony and BlackBerry.

The broader battle between Samsung and Apple is only going to intensify. Samsung may well extend its lead over the next six months. The Galaxy S4, its flagship device for the year, reaches the U.S. and other markets this month. Apple is not expected to offer a new iPhone until the fall, giving Samsung four or five months to build its user base.

The iPhone 5S, or iPhone 6, or whatever it's called, had better be an impressive device if Apple wants to hold onto its already-slipping market share.

Copyright © 2012 United Business Media LLC, All rights reserved.

Helicopter Ben leaving soon, here is his possible successor:

JANET YELLEN, Possible Fed Successor Has Admirers and Foes

By BINYAMIN APPELBAUM

WASHINGTON — In July 1996, the Federal Reserve broke the metronomic routine of its closed-door policy-making meetings to hold an unusual debate. The Fed’s powerful chairman, Alan Greenspan, saw a chance for the first time in decades to drive annual inflation all the way down to zero, achieving the price stability he had long regarded as the central bank’s primary mission.

But Janet L. Yellen, then a relatively new and little-known Fed governor, talked Mr. Greenspan to a standstill that day, arguing that a little inflation was a good thing. She marshaled academic research that showed it would reduce the depth and frequency of recessions, articulating a view that has prevailed at the Fed. And as the Fed’s vice chairwoman since 2010, Ms. Yellen has played a leading role in cementing the central bank’s commitment to keep prices rising about 2 percent each year.

Ms. Yellen is now widely viewed as a logical candidate to succeed the current Fed chairman, Ben S. Bernanke, when his term ends in January 2014. She has worked closely with him in shaping and building support for the Fed’s campaign to stimulate the economy and bring down unemployment.

But some of Ms. Yellen’s critics remain wary. They worry that she would not be sufficiently concerned about the possibility that inflation will accelerate as the economic recovery gains strength. If nominated, she could face opposition from Senate Republicans who have repeatedly expressed concern that the Fed’s campaign would destabilize financial markets and make controlling the pace of inflation more difficult.

“I think people read Janet Yellen’s speeches as saying that she puts a higher weight on joblessness compared to inflation” than the typical member of the Fed’s policy-making committee, said Vincent Reinhart, formerly the head of the Fed’s monetary policy staff and now the chief United States economist at Morgan Stanley. “And that includes Ben Bernanke.”

He added, however, that her nomination would be unlikely to shake financial markets because she already exercises considerable influence, so any shift in policy would most likely be modest.

Moreover, Ms. Yellen’s personal qualities, highlighted by the 1996 episode, have helped her win supporters even among her ideological opponents.

“She makes an argument on the merits and she sticks with it,” said Alan Blinder, an economics professor at Princeton nominated to the Fed alongside Ms. Yellen in 1994. “And she’s good at articulating an argument in a way that doesn’t leave people on the other side hopping mad at her.”

Despite their disagreement at the time, Mr. Greenspan said that he continued to hold Ms. Yellen in high regard. “I did listen to her more carefully because she articulates her position in a way that you can follow it analytically,” he said in an interview. “Intuitions are useless. Janet’s conversation and her presentations were factually based, and that always got my attention.”

If confirmed, Ms. Yellen would become the first woman to lead a major central bank. She is 66, seven years older than Mr. Bernanke. She would be 71 by the end of a four-year term as chairwoman. But she remains in good health, and friends say that, like other prominent women of her generation, she regards herself as being in the prime of a late-blooming career. Nor would she be the oldest person to lead the Fed. Mr. Greenspan began his fifth and final term in 2004 at 78.

Ms. Yellen, slight, white-haired and described by one colleague as a “small lady with a large I.Q.,” does not loom like Paul Volcker nor cut like Mr. Greenspan. Her personal style more closely resembles Mr. Bernanke’s soft-spoken manner. The force of her arguments can catch people by surprise.

Kevin Hassett, a staff economist at the Fed when Ms. Yellen arrived in 1994, recalled that she started to eat lunch regularly in the staff cafeteria to subvert the hierarchical system that limited communication between Fed governors and the vast army of research economists. Other governors had tried to change the rules but Ms. Yellen, he said, found a way around them.

“It showed a kind of grace and wisdom that is very unusual in Washington,” said Mr. Hassett, now a fellow at the right-leaning American Enterprise Institute.

Mr. Hassett is among those who worry that Ms. Yellen does not place a sufficient emphasis on controlling inflation. “But I hold her in the highest possible regard,” he said. If the Obama administration is “going to pick a Fed chair that thinks the way they do, then Janet Yellen would be the best possible choice.”

There has been no official word from the White House or Mr. Bernanke that the Fed will have a new chairman next year. The decision is up to Mr. Obama, and aides say he has not yet focused on who he wants in the job.

But Mr. Bernanke may have signaled his departure last week when the Fed announced that he planned to skip an annual summer conference in Jackson Hole, Wyo. The Fed’s chairman has attended the event in each of the previous 25 years.

People who have spoken with Mr. Bernanke say he is tired after leading the Fed through eight years that were mostly consumed by crisis. Mr. Bernanke has also sought to make monetary policy more transparent and predictable, dispelling the image of the Fed chairman as a kind of artist. “I don’t think that I’m the only person in the world who can manage the exit” from the Fed’s current policies, he said last month. The only way to prove that point would be to let someone else do it.

President Obama, for his part, has the opportunity to nominate the first Democrat to lead the Federal Reserve since President Carter chose Mr. Volcker in 1979 — and the person he selects will serve a term that extends two years beyond his own.

Ms. Yellen has avoided questions about her future, but she, too, appeared to address the subject indirectly this month. Asked about the dearth of female economic policy makers, she responded that it was “something we’re going to see increase over time, and it’s time for that to happen.”

She declined a request to be interviewed for this article.

There are other potential candidates for the job, including Roger W. Ferguson Jr. and Professor Blinder, both former Fed officials, and economic advisers to Mr. Obama including Timothy F. Geithner and Lawrence H. Summers. But Ms. Yellen appears to be the front-runner in a race that has not actually started quite yet.

None of the other obvious candidates possess the same combination of academic credentials and policy-making experience. No Fed chairman has been as deeply steeped in both the theory and practice of central banking.

“In the realm of plausible candidates, she is by far the best,” said Christina Romer, a former chairwoman of Mr. Obama’s Council of Economic Advisers who is an economics professor at the University of California, Berkeley. She has known Ms. Yellen for years and counts her as a friend.

Asked who else she would recommend that the president consider for the job, Ms. Romer responded, “I would stop after No. 1.”

Ms. Yellen, born in Brooklyn in 1946, has said that she became interested in economics as a way of thinking logically about how to help people. She studied at Yale under the Nobel laureate James Tobin, a leading proponent of the view that governments could mitigate recessions. Professor Tobin, now dead, told Business Week magazine in 1997 that Ms. Yellen had “a genius for expressing complicated arguments simply and clearly.”

She built an academic career at Berkeley together with her husband, the economist George A. Akerlof, whom she met in a Fed cafeteria. Much of their work together highlighted flaws in the economic theory that markets operate efficiently, a theory that basically treats government policy as inherently costly. Their work showed that government, including central banks, could indeed adopt economic policies that improved people’s lives.

Colleagues and people familiar with their work said that Professor Akerlof, who shared the Nobel in economics in 2001 with Joseph E. Stiglitz and A. Michael Spence, was the more creative thinker, while Professor Yellen was more rigorous.

“George can sometimes go off in a direction that is untethered from the real world, and Janet was better at bringing it back,” said Professor Romer, who joined the Berkeley economics faculty with her husband and collaborator, David Romer, about a decade after Ms. Yellen and Mr. Akerlof.

In 1994, the Clinton administration nominated Ms. Yellen to the Fed on the recommendation of Laura D’Andrea Tyson, a colleague at Berkeley then serving as the head of the Council of Economic Advisers.

Ms. Yellen and Professor Blinder were chosen to check the Fed’s tendency to curtail growth for fear of inflation. But in an unlikely twist, Mr. Greenspan became the strongest advocate for letting the economy grow more quickly, and Ms. Yellen helped provide intellectual justification for keeping interest rates low.

“She was much more aware of the current state of academic literature on fairly technical issues,” Mr. Greenspan recalled. “I found her very useful in that regard.”

At the time of the 1996 debate, inflation had fallen to a relatively stable pace of about 3 percent a year, eliminating much of the unpredictability that had plagued the economy. Mr. Greenspan saw clear benefits in pushing all the way to zero. But some economists worried that lower inflation might result in permanently higher unemployment, by making it difficult to adjust wages. And it would bring the economy dangerously close to deflation, the destabilizing condition in which falling prices freeze economic activity as people anticipate lower prices.

“I believe that heading toward 2 percent inflation would be a good idea, and that we should do so in a slow fashion, looking at what happens along the way,” Ms. Yellen said at the 1996 meeting. The debate continued for years; the Fed finally adopted a 2 percent inflation target last year.

But Laurence H. Meyer, a former Fed governor, recalled the 1996 meeting as a turning point. “She was the one who really brought the story that inflation could be too low,” said Mr. Meyer, a senior adviser at MacroEconomic Advisers. “And she was very effective. Once she said it, it seemed so obvious and sensible.”

Ms. Yellen began a second stint at the Fed in 2004 when she was named president of the Federal Reserve Bank of San Francisco. She has played a leading role in the Fed’s movement to provide “forward guidance” about the path of policy over the next several years, persuading investors that it is safe to accept lower interest rates.

But it is easy to overstate her differences with those more focused on inflation. “I think I am as committed to price stability and the attainment of price stability as any member of the F.O.M.C.,” a reference to the Federal Open Market Committee, Ms. Yellen said at a 2010 luncheon in Los Angeles. “When the time has come, am I going to support raising interest rates? You bet.”

Why this market MAY NOT DROP ANY TIME SOON....

Central Banks Load Up on Equities

By Sarah Jones - Apr 25, 2013

Central banks, guardians of the world’s $11 trillion in foreign-exchange reserves, are buying stocks in record amounts as falling bond yields push even risk- averse investors toward equities.

In a survey of 60 central bankers this month by Central Banking Publications and Royal Bank of Scotland Group Plc, 23 percent said they own shares or plan to buy them. The Bank of Japan, holder of the second-biggest reserves, said April 4 it will more than double investments in equity exchange-traded funds to 3.5 trillion yen ($35.2 billion) by 2014. The Bank of Israel bought stocks for the first time last year while the Swiss National Bank and the Czech National Bank have boosted their holdings to at least 10 percent of reserves.

“In the last year or so, I have spoken with 103 central banks on diversification,” Gary Smith, London-based global head of official institutions at BNP Paribas Investment Partners, which oversees about $649 billion, said in a phone interview. “If reserves are growing, so are diversification pressures. Equities are not for every bank tomorrow, but more are continuing down this path.”

Managers of banks’ assets are looking for alternatives to holding government bonds after efforts to stimulate growth from the Federal Reserve, the Bank of Japan and the Bank of England helped send yields near to record lows. Central banks’ foreign- exchange holdings have increased by about $8.5 trillion globally in the past decade, exceeding levels needed for day-to-day currency administration.

Currency Moves

Central banks typically hold assets such as government debt that can be sold easily if funds are needed to counter a move in their currency. The reliance on fixed-income securities at a time when bond yields are below inflation in many countries risks allowing to the value of reserves to decline.

While consumer prices are rising at a 1.5 percent annual rate in the U.S. and 1.7 percent in the euro area, the average yield to maturity of securities in Bank of America Merrill Lynch’s Global Broad Market Sovereign Plus Index fell to an all- time low of 1.34 percent on April 23, according to data compiled by Bloomberg.

The SNB allocated 82 percent of its 438 billion Swiss francs ($463 billion) in reserves to government bonds in the fourth quarter, according to data on its website. Of those securities, 78 percent had the top, AAA credit grade and 17 percent were rated AA.

More Risk

The survey of 60 central bankers, overseeing a combined $6.7 trillion, found that low bond returns had prompted almost half to take on more risk. Fourteen said they had already invested in equities or would do so within five years. Those conducting the annual poll had never before asked that question.

“I definitely see other central banks doing or considering equities,” said Jan Schmidt, the executive director of risk management at the Czech National Bank in Prague, which has built up stocks to 10 percent of its $44.4 billion in reserves since 2008. Even so, the risks of owning shares are the same as ever, he said in e-mailed comments.

Currency reserves among the world’s central banks climbed by $734 billion in 2012 to a record $10.9 trillion, according to data from the Washington-based International Monetary Fund. That’s about 20 percent of the $55 trillion market value of global stocks, data compiled by Bloomberg show.

Central banks’ purchases of shares show how the “hunger for yield” is changing the behavior of even the most conservative investors, according to Matthew Beesley, head of equities at Henderson Global Investors Holding Ltd. in London, which oversees about $100 billion.

‘Logical Move’

“Equities are the last asset class standing,” Beesley said in a phone interview on April 18. “When you have dividend yields in excess of bond yields, it’s a very logical move.”

Companies in the Standard & Poor’s 500 Index pay 2.2 percent of their combined share price as dividends, compared with the 1.69 percent yield on 10-year Treasuries, according to data compiled by Bloomberg.

The S&P 500 (SPX) closed at an all-time high of 1,593.37 on April 11 and is up 11 percent this year though April 23. Investors have earned 0.7 percent owning U.S. government debt repayable in one year or more, according to Bank of America Corp. bond indexes.

Stocks are also cheap compared with government bonds using a valuation method favored by former Fed Chairman Alan Greenspan that compares earnings with interest payments. Companies in the S&P 500 (SPX) generate profit equal to 6.4 percent of their share prices, about 4.7 percentage points more than yields on 10-year Treasuries, Bloomberg data show.

Beyond Pale

Even so, 70 percent of the central bankers in the survey indicated that equities are “beyond the pale.”

The growth in reserves has slowed as a strengthening dollar puts less pressure on policy makers to intervene by selling their currencies, data compiled by Bloomberg show. Central-bank assets grew by 1 percent last quarter, the smallest gain since the same period of 2012, as Taiwan’s reserves fell by more than $1 billion to $402 billion and Singapore’s dropped by a similar amount to $258 billion.

Some central banks, including the Fed in Washington and the Bank of England in London, have no mandate to buy stocks directly. The Fed has $42.6 billion in reserves and the Bank of England controls $65.1 billion, data compiled by Bloomberg show.

Other banks are deterred by price swings in equities that can be larger than for other securities. The MSCI All-Country World Index (MXWD) fell 3.3 percent in five days after rising to a 4 1/2-year high on April 11 and tumbled 11 percent in the five weeks through June 12 last year. The gauge of global stocks rose 0.6 percent at 8:33 a.m. in New York today.

SNB, Israel

Among central banks that are buying shares, the SNB has allocated about 12 percent of assets to passive funds tracking equity indexes. The Bank of Israel has spent about 3 percent of its $77 billion reserves on U.S. stocks.

In Asia, the BOJ announced plans to put more of its $1.2 trillion of reserves into exchange-traded funds this month as it doubled its stimulus program to help reflate the economy. The Bank of Korea began buying Chinese shares last year, increasing its equity investments to about $18.6 billion, or 5.7 percent of the total, up from 5.4 percent in 2011. China’s foreign-exchange regulator said in January it has sought “innovative use” of its $3.4 trillion in assets, the world’s biggest reserves, without specifying a strategy for investing in shares.

‘Pursue Yield’

“Central banks are looking at assets that I wouldn’t have necessarily expected in times gone by,” said Paul Price, London-based head of international distribution and client relations at Morgan Stanley Investment Management, which oversees about $338 billion. Low yields and “movement in the ratings around certain sovereigns is forcing central banks to rethink how they pursue yield and how equities are viewed in that context,” he said.

The yield on the benchmark 10-year U.S. Treasury reached a record low of 1.38 percent in July. The same month, German government rates of similar maturity declined to 1.13 percent. France’s 10-year yield retreated to 1.7 percent on April 23, the lowest level since Bloomberg began tracking the data in 1990.

“Government bonds remain a fundamental pillar of central- bank asset allocation, but there is scope to go into other asset classes to help provide a higher return,” said Massimiliano Castelli, head of strategy at UBS Asset Management’s global sovereign markets unit in London. “We are in a lot of discussions with several or so institutions who are considering such a step.”

To contact the reporter on this story: Sarah Jones in London at sjones35@bloomberg.net

<ZH>The Week That Was: April 22nd-26th 2013

Submitted by Tyler Durden on 04/26/2013 17:02 -0400

Succinctly summarizing the positive and negative news, data, and market events of the week...

Positives

1.Spanish spreads ignore reality, continue to compress

2.March new home sales beat expectations (average prices plunge)

3.Apple to 'return' billions to shareholders (and continue to avoid paying taxes)

4.UK avoided a triple dip recession (for now)

5.Gold begins to retrace its ugly plunge

6.BTFD! Central banks admit they're purchasing stocks – quite bullish for those trading on momentum & pretending it's fundamentals

7.Initial Jobless Claims beats expectations

8.Oil surges most in five months

9.EuroStoxx 600 surging (your textbook 'all news is good news' market hypothesis)

10.SBUX hits Q2 estimates, (lowers Q3 guidance)

11.UMich Consumer Sentiment beats expectations (but dropped and languishes at the same level as a year ago)

Negatives

1.Chinese & German PMI's disappoint

2.US Mint halts sales of gold bullion, as surging demand depletes inventory (negative for those who pretend paper gold is the same as physical)

3.The tweet heard 'round the world -- See one tweet make market liquidity completely disappear

4.US business cycle index plunges most in 22 months, equities ignore

5.There's a slideshow for that: CNBC viewership surges plunges to eight year lows

6.Unpossible: Countries ramp up fx reserve diversification (away from the USD)

7.March durable goods numbers are hideous, equities love it

8.Europe’s bank lending plummets

9.Bundesbank rejects OMT (potentially ruining Draghi’s ESM party)

10.The ‘fringe’ would like to know: What's happening with JP Morgan's gold?

11.Syrian chemical weapons – ‘incursion’ imminent?

12.Spain worst unemployment ever, slashes growth forecast and will miss deficit target

13.US GDP misses expectations

Additional

•YTD Hedge Fund performance update

•A visual history of asset bubbles

•Corzine finally named in lawsuit regarding firm's collapse

•220 years of treasury yields

•Surprise: Congress is trying to exempt themselves from Obamacare

•Do not panic: CBOE goes offline for a while

LOL, and I got into Baghdad in 2006, and I remember the landing and DAMN was it a joy ride. I wonder if he was my pilot! Great post EZ, thanks! With all the travelling I have done lately, I was on 3 different C-130s, a C-17, and a few C-5s.

Alright, it is a nice Sunday morning here in Kandahar, the 28th of April, some sort of Taliban Holiday where they are going to start all their damn shenanigans out here. Got in last night, did a TON of reading and getting caught up, will be posting lots of news and views while you sleep. Travels pretty much done now, missions all accomplished, next travel will be a few quick hops when my replacements get here and I get ready to GO HOME!!

Futures VERY GREEN this morning, the QE rally continues. Big earnings coming out this week, let's see if it can hang on.

Off to the airfield. Flgiht MAY be cancelled, it is actually raining out here right now, so you may be stuck with me later if I get delayed.

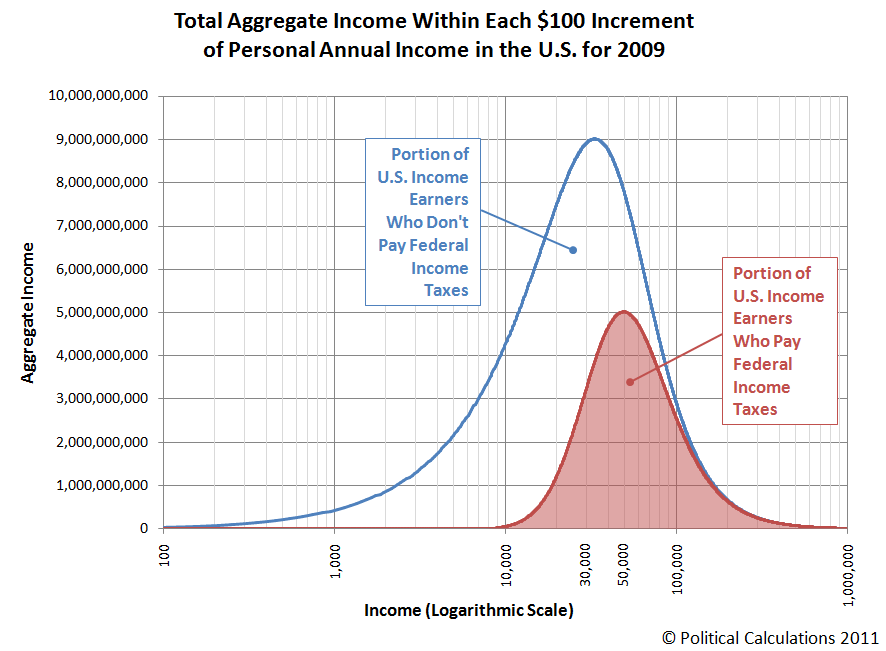

<MISH>Graph Shows Who Is And Who Isn't Paying Their Fair Share of Taxes

In response to 55% of Americans Say Their Income Taxes are Fair; 46.6% Paid No Income Tax in 2011 one seriously misguided soul responded "your hate for low income people disturbing".

The above response was humorous because the math shows a large number of people are unhappy even though thy pay no income taxes at all. Nowhere did I state or imply any hatred of anyone.

On a far more credible note, I received an email from Ironman at the Political Calculations blog who posted this chart on "Who Really Isn't Paying Their Fair Share of Income Taxes?"

I asked Ironman to explain the chart. Here is his reply.

We used U.S. Census data to model the total aggregate income earned by individual Americans for each $100 increment of income in 2009 to create the "blue" income distribution bell curve using regression analysis, which we originally did as part of another project, where we modeled the total money income distribution of Americans.

We then took the Tax Policy Center's data for the percentage of tax units without income tax liability for given levels of income and modeled that as well - and in doing that, we also get the percentage of tax units that do have income tax liability over the same income range.

We then multiplied the percentage of tax units with income tax liability by the total amount of aggregate income earned within a given amount of income to determine the portion of that aggregate U.S. income that is subject to income taxes. That result is represented as the "red"-shaded bell curve on the chart.

The unshaded region under the "blue" total aggregate income curve is then the portion of income earned by Americans that is not subject to income taxes.

What If?

In a followup email, I asked Ironman what the result would have been, if a 100% tax on all income above $1 million been in place. To that question he replied ...

"By our calculation, the U.S. government would have taken in $800 billion more in tax revenue if it had taxed people making more than $1 million at 100 percent, according to IRS data from 2008, the year Ryan used as his base point."

Thus, even taxing people making over $1 million at a rate of 100% would not have balanced the budget. Of course, if you tax anything at 100%, you are not going to get anywhere near the amount theoretically expected.

Some might point out interest income, but others would point out disability and food stamps. Specifically, I would like to point out Unwilling to Work; 25% in Hale County AL Collect Disability, 14 Million Nationwide; A Simple Solution.

Simply put, if you pay people enough to do nothing at all, you are going to encourage a lot of fraud by people willing to do nothing.

Regardless of what you think about top income earners, the system is setup to encourage fraud and avoidance at both ends of the scale.

Who suffers? Those in the middle.

Perhaps it's time for a consumption tax, excluding food, medicine, and essential clothes. Perhaps some combination of flat income tax in conjunction with a consumption tax excluding food, medicine, and essential clothes.

My only fear in suggesting such a thing is government nearly always screws things up by implementing things in a matter that will make matters worse.

Mike "Mish" Shedlock

http://globaleconomicanalysis.blogspot.com

Read more at http://globaleconomicanalysis.blogspot.com/2013/04/graph-shows-who-is-and-who-isnt-paying.html#iZmE4adRJjt4Lzj1.99

Dealers Say No End to QE in ’13; Hatzius Sees 2016 Rate Rise

By Daniel Kruger and Liz Capo McCormick - Apr 22, 2013

Wall Street’s biggest bond dealers see little chance the Federal Reserve will slow the pace of debt purchases designed to boost economic growth before year-end, even as policy makers face calls to curb the buying.

Of the 21 primary dealers that trade with the central bank, 14 said in a Bloomberg News survey that the Fed won’t start to reduce its $85 billion monthly bond buying until the last three months of 2013. Twelve forecast they will end in mid-2014 or later. Fifteen say it will take until at least June 2015 for policy makers to raise the record low benchmark interest rate target of zero to 0.25 percent. Goldman Sachs Group Inc. chief economist Jan Hatzius sees no increase before January 2016.

Fed Chairman Ben S. Bernanke, an academic expert on the seeds of the Great Depression, has pumped more than $2.5 trillion into the economy to fulfill the twin mandates of full employment and price stability. Critics, including officials within the central bank, say the purchases don’t create jobs and risk creating asset price bubbles. The bond market has backed the measures as inflation concerns diminish and investors push Treasury yields to about the lowest this year.

“It’s going to take a long time for the slack in the labor market to be unwound,” Hatzius, who was named one of the 50 most influential people in global finance by Bloomberg Markets Magazine in 2011, said in an April 18 telephone interview from New York. “We have inflation below the target for the next two years. We think they’re still going to be missing on the mandate, and if you’re missing on the mandate you’re going to want to do more.”

Survey Estimates

The earliest prediction for when the Fed will begin reducing bond purchases is the third quarter of this year by Deutsche Bank AG, while Mizuho Securities USA Inc. sees no tapering for two years. Deutsche Bank and Societe Generale SA estimate the buying will end this December. Bank of Nova Scotia (BNS), Bank of Montreal, BNP Paribas and Mizuho predict it will last into 2015.

Hatzius said the Fed won’t be able to raise its target overnight interest rate, which has been zero to 0.25 percent since December 2008, until January 2016. Of the 19 dealers with calls for when the Fed will increase rates, 17 predict it will happen in 2015.

‘Too Early’

“It’s still too early” to end the bond buying, Rajiv Setia, head of U.S. interest-rate research at Barclays Plc in New York, a primary dealer, said in an April 19 telephone interview. “This is the only tool they have. They’re doing all they can. At the end of the day, the benefits outweigh any risks of a bubble for now.” Barclays forecasts the Fed will slow its pace of purchases in the first three months of 2014 and end them by June next year.

Backers of Fed stimulus point to a sluggish economy. Unemployment was 7.6 percent in March as payrolls grew by 88,000, the least in nine months, according to Labor Department data released April 5. Retail sales fell in March by 0.4 percent, the biggest drop since June, the Commerce Department said April 12. Confidence as measured by the Thomson Reuters/University of Michigan preliminary index of consumer sentiment declined to 72.3 in April from 78.6 a month earlier.

The bond market has become more pessimistic on the economy in the last six weeks. On March 11 the 10-year Treasury yield closed at 2.06 percent, its high for the year, up from 1.76 percent at the end of 2012. It has since fallen as low as 1.68 percent on April 15, the biggest drop since the period from April 27 to June 1, 2012 when it slid 0.48 percentage point to a then record-low 1.45 percent as Europe’s debt crisis worsened.

Bond Trading

The benchmark U.S. 10-year yield rose two basis points, or 0.02 percentage point, to 1.72 percent at 9:48 a.m. London time, according to Bloomberg Bond Trader prices. The 2 percent note due February 2023 fell 6/32, or $1.88 per $1,000 face amount, to 102 15/32. The yield declined two basis points last week.

“We had one poor employment report and a bunch of lousy data thereafter,” said Joseph LaVorgna, chief U.S. economist at Deutsche Bank in New York in an April 18 telephone interview. “Six weeks of this data has gotten the market back on ‘uh-oh, here we go again camp,’ because, to one degree or another, we saw similar slowdowns in 2010, 2011, and 2012. The market has probably gotten way too worried.”

‘Not Convinced’

Fed asset purchases risk creating asset bubbles, according to Zach Pandl of Columbia Management Investment Advisers LLC.

“We’re not convinced that the easy policy won’t create serious risks to the financial system over the longer term,” Pandl, a senior interest-rate strategist in Minneapolis for the firm which oversees $340 billion, said in an April 19 telephone interview. “The U.S. economy would be in much worse shape if the Fed had not aggressively eased. But many things have been standing in the way, limiting the impact of the monetary easing going forward.”

Philadelphia Fed President Charles Plosser said in an April 11 speech in Hong Kong the Fed should begin reducing the pace of bond buying, citing the drop in unemployment to 7.6 percent in March from 8.1 percent in August since the start of a third round of asset purchases in September. “We have seen sufficient improvement to begin tapering our asset purchase program with the objective of bringing it to an end before year-end.”

Dealer Holdings

The dealers are holding on to Treasuries. The securities account for 38.5 percent of their debt holdings, excluding state and local government bonds, close to the record 39.8 percent reached in December, Fed data as of April 10 show. The dealers owned $137.9 billion, the most since $145.7 billion on Dec. 19 and the second-highest total going back to 1997.

Investors using borrowed funds to boost returns, so-called leveraged accounts, held a net $56.1 billion in contracts wagering on gains in 10-year Treasury futures in the week ending April 16, data from the Commodity Futures Trading Commission show. That’s approaching the record of $60.3 billion set in the week of April 2, which topped a mark set in August 2007 before credit markets froze and the economy went into recession, sparking a rally in government bonds. As recently as July, there were net bets against the Treasuries.

In a bullish sign for bonds, fixed-income money managers overseeing a combined $130 billion have increased their asset- weighted duration, a reflection of how long the debt they own will be outstanding, to 98.6 percent of target indexes as of April 16 from 97.2 percent on March 19, which was the least since September 2008, according to a survey by Stone & McCarthy Research Associates in Plainsboro, New Jersey.

Slower Growth

“The economy is very interest-rate sensitive, so if the Fed cuts its support too early the market would overreact and we would see a spike in yields and a rotation back to slower growth,” Larry Dyer, a U.S. interest-rate strategist with primary dealer HSBC Holdings Plc in New York, said in a telephone interview on April 16. “Slower growth would just mean more Fed, and they know that.”

HSBC expects smaller purchases beginning late this year.

The Federal Open Market Committee’s central tendency forecasts, released after the March 19-20 meeting, are for a jobless rate of 7.3 percent to 7.5 percent in the final quarter of 2013, falling to 6.7 percent to 7 percent a year later. The majority of Fed officials don’t anticipate raising the benchmark interest rate until 2015, according to their estimates.

Low Inflation

Bernanke, who published a collection of essays on the Great Depression in 2004, said after the Fed’s March 19-20 meeting that further gains in the labor market were needed before he would consider reducing monetary easing. Policy makers have said they won’t raise interest rates until joblessness is below 6.5 percent while inflation averages 2.5 percent or less.

Price increases are below that target. The Treasury sold $18 billion of five-year Treasury Inflation Protected Securities on April 18, with investors bidding $2.18 per dollar of debt sold, the lowest demand since October 2008.

The spread between five-year yields on TIPS and Treasuries not indexed for inflation, which shows the market’s expectations for inflation during the life of the debt, fell as low as 1.94 percentage points, the lowest since August, from 2.42 percentage points on March 14.

Inflation was 1.3 percent in January and February, matching the slowest pace since 2009, according to the Fed’s preferred measure, the personal consumption expenditures index deflator, the Bureau of Economic Analysis said March 27. The consumer price index declined 0.2 percent in March, the first drop since November, the Labor Department said April 16.

More Buying

Three regional Fed presidents said last week the prospects of too little inflation might lead the central bank to increase bond buying.

St. Louis Fed President James Bullard said April 17 that policy makers “should defend the inflation target from the low side,” a sentiment echoed by Minneapolis Fed President Narayana Kocherlakota the following day.

Richmond Fed President Jeffrey Lacker, a critic of current policy, said April 18 that “if inflation looked like it was going to sag further on a persistent basis, I would certainly consider stimulus for the purpose of bringing inflation up to target.” Lacker’s concern about disinflation comes even as he has advocated curtailing easing.

“Everyone got so caught up with the Fed exit from QE that they forgot the Fed can actually ramp it up,” George Goncalves, head of interest-rate strategy in New York at primary dealer Nomura Holdings Inc., said in a telephone interview on April 17. “If conditions change and they get worse, they can do more. It’s a two-way street.”

Nomura is forecasting the Fed will begin to slow purchases in September and end them by March 2014.

To contact the reporters on this story: Daniel Kruger in New York at dkruger1@bloomberg.net; Liz Capo McCormick in New York at emccormick7@bloomberg.net

GOLD AND SILVER MAKING A NICE MOVE THIS MORNING!

Both up close to 2%. BUY THE DIP!

European Stocks Rebound From Last Week’s Drop

By Tom Stoukas - Apr 22, 2013

European stocks rose, rebounding from the biggest weekly drop in five months, as Italy elected a president and the Group of 20 refrained from opposing the Bank of Japan’s stimulus policies. Asian shares and U.S. index futures also advanced.

ABB Ltd. (ABBN) increased 1.1 percent after saying it will acquire Power-One Inc. for about $1 billion. Delhaize Group SA gained 7.8 percent as its pretax profit forecast beat analysts’ estimates. Royal Philips Electronics NV (PHIA) slid for a seventh day after revenue and profit missed analysts’ estimates.

The Stoxx Europe 600 Index (SXXP) climbed 0.7 percent to 287.07 at 8:07 a.m. in London. The benchmark gauge retreated 2.5 percent last week as economic data from the U.S. to China and Germany missed forecasts. The measure has still risen 2.7 percent so far this year.

“U.S. markets closed higher on Friday, buoyed by a host of decent results from companies and optimistic expectations that this week’s bellwethers will do the same,” Jonathan Sudaria, a trader at Capital Spreads in London, wrote in e-mailed comments. “Japan’s optimism seems to be founded on the fact that they didn’t receive any explicit singling out at the G-20 for their exceptionally loose monetary policy.”

Standard & Poor’s 500 Index futures rose 0.6 percent today, signaling the benchmark measure will advance for a second day. The MSCI Asia Pacific Index climbed 0.6 percent, led by Japanese exporters as the yen slid to a four-year low against the dollar.

Italy Elections

Italian bonds rose today, pushing the yield on the two-year notes down seven basis points to 1.267 percent, the lowest since Bloomberg began compiling the data in 1993.

Giorgio Napolitano was elected to a second term as Italy’s president after accepting a last-minute appeal from party leaders to run again. The 87-year-old incumbent won the backing of parties led by former premier Silvio Berlusconi, caretaker Prime Minister Mario Monti and outgoing Democratic Party leader Pier Luigi Bersani. His re-election came after two months after inconclusive parliamentary elections.

BOJ Governor Haruhiko Kuroda emerged from the G-20 meeting saying he was emboldened to press ahead with the campaign to defeat deflation. The central bank meets this week after pledging April 4 to double the monetary base in two years.

U.S. Earnings

In the U.S., eight S&P 500-listed (SPX) stocks, including Halliburton Co., Caterpillar Inc. and Hasbro Inc. release their results today.

Existing home sales in the U.S. rose for a third month in March, increasing 0.4 percent to a 5 million annualized rate, according to a Bloomberg survey of economists. The last time sales exceeded that pace was November 2009, when first-time homebuyers rushed to take advantage of a temporary tax credit.

ABB gained 1.1 percent to 20.14 Swiss francs. The Swiss maker of power-transmission equipment agreed to acquire Power- One for about $1 billion to expand in solar inverters. Shareholders of the Camarillo, California-based company will get $6.35 a share under the terms of the offer, ABB said.

Delhaize added 7.8 percent to 45.99 euros. First-quarter preliminary results showed earnings before interest and taxes at about 214 million euros, up 13 percent from the same time last year. The the owner of the Food Lion supermarkets in the U.S. sees 2013 underlying pretax profit at about 775 million euros, beating analysts’ estimates of 741.5 million euros.

Copper producer Kazakhmys Plc (KAZ) rose 2.6 percent to 395.6 pence. The stock was raised to neutral from underperform at Credit Suisse Group AG and Exane BNP Paribas.

Philips slid 2.9 percent to 21.03 euros after it reported first-quarter profit that missed analysts’ forecasts. Earnings before interest, taxes, amortization and one-time items were 421 million euros, the world’s largest lighting manufacturer said, missing estimates of 441 million euros. Sales dropped 0.9 percent to 5.26 billion euros, trailing the 5.48 billion-euro analyst projection.

To contact the reporter on this story: Tom Stoukas in Athens at astoukas@bloomberg.net

To contact the editor responsible for this story: Andrew Rummer at arummer@bloomberg.net

Good morning Lottos!

About 2 more damn months here for me, and it has been crazier than hell. Going through a transitional phase where they are packing stuff up and decreasing the footprint, and I am in the middle of it all being the logistics guy. I was looking forward to a nice quiet few months, but the higher ups had other ideas. Will be on sporadically like I have been, looking forward to August when I am back at work and ready to rock after a few weeks in Vegas. Hope everyone is doing well and making money in the markets. Prayers to all those out in Boston, I am glad they caught the bastards. We are getting ready for the SPring Offensive out here, fingers crossed it stays relatively calm while I move around the theater.

Now, I will post some news and views and get ready to head out again. God Bless you all, forgive me for being so poor with posting, but I will make up for it with mega stock oicks of 10X or more. (LOL, I wish!)

Good morning Ske! Getting ready to jump into another stupid meeting, watching the PMs fall faster and harder in just the past few minutes! Talk about a bloodbath.

Congrats again to Louisville! My Syracuse boys just couldn't get past the Michigan boys. Next year!!

Damn, as of this minute, GOLD is under $1400!

Gonna be one of those days. I guess EZ is selling ALL his gold holdings.

Wow, Silver now down almost 12% this morning! Futures getting redder as well. We will need some REAL BAD US economic data today to get us back to green, lol.