News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

The role of genius is not to complicate the simple, but to simplify the complicated.

Dancing in the dark

![]()

![]()

The role of genius is not to complicate the simple, but to simplify the complicated.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

The role of genius is not to complicate the simple, but to simplify the complicated.

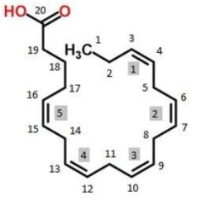

About icosabutate

Icosabutate is a patent protected, new chemical entity, and a structurally enhanced fatty acid developed as a synthetic modification of the omega-3 fatty acid eicosapentaenoic acid (EPA). Compared to currently available prescription omega-3 fatty acid formulations which are usually given as 4 grams a day to achieve clinical efficacy, icosabutate is designed to provide superior triglyceride-lowering at a much lower dose (600 mg) with a convenient once daily oral dosing with or without meals.

https://industries.basf.com/en/Omega-3/News-Events/News-Release/2015/Phase-2a-Clinical-Study-of-Icosabutate-in-Patients-with-Severe-Hypertriglyceridemia.html

Product Description

Icosabutate is a synthetic ?-3 polyunsaturated fatty acid derived from eicosapentaenoic alcohol and 2-bromo butyric acid. It was designed to resist ß-oxidation and complex lipid incorporation and increase efficacy in fatty acid-responsive intracellular signaling systems.1,2 In a clinical trial, oral administration of icosabutate (600 mg) significantly reduced triglyceride, very low-density lipoprotein cholesterol, and Apo c-III levels in patients with very high triglyceride levels.1,2

Product Description References

1. Bays, H.E., Hallèn, J., Vige, R., et al. Icosabutate for the treatment of very high triglycerides: A placebo-controlled, randomized, double-blind, 12-week clinical trial. J.Clin.Lipidol. 10(1), 181-191 (2016).

2. Kastelein, J.J.P., Hallén, J., Vige, R., et al. Icosabutate, a structurally engineered fatty acid, improves the cardiovascular risk profile in statin-treated patients with residual hypertriglyceridemia. Cardiology 135(1), 3-12 (2016).

i guess i was unclear.

..............Product revenue, net.........$ increase over prior year

2020.....$700,000,000.00.................$272,000,000.00 ... (800 sales people)

2019.....$428,000,000.00.................$199,629,000.00 ... (400 sales people)

2018.....$228,371,000.00.................$48,546,000.00

2017.....$179,825,000.00.................$50,859,000.00

2016.....$128,966,000.00.................$47,979,000.00

2015.....$80,987,000.00..................$26,785,000.00

2014.....$54,202,000.00...................

Amarin's guidance for increase of revenue of only 65% year over year for 2020(less of an increase YoY than in 2019) seems much too low

perhaps different amazon fulfillment centers are in play ;)~

... how clear it was pre-MARINE that many thought that results from an exclusively Japanese population couldn't be extrapolated to any other population?

https://iiroc.mediaroom.com/2019-12-23-IIROC-Trading-Halt-ACST

just a guess, nasdaq miscoded IIROC's halt?

3) someone accidentally entered a large sell order at 1.87 instead of 2.87

that trade is getting more crowded by the minute.

unless the results have leaked and surpass MARINE study results:

"As reported in November 2010, the primary endpoint of the MARINE study was achieved with statistically significant reductions in triglycerides compared to placebo of 33% (P<0.0001) for the 4 gram and 20% (P=0.0051) for the 2 gram per day doses, respectively.AMR101 did not result in a statistically significant increase in median LDL-C compared to placebo at either dose."

i am not suggesting another cash raise.

i am suggesting those who acquired the 22.5M shares @ $18 last july are using the immense volume the past two days to exit profitably.

or, not yet ...

ample opportunity

Jul 18, 2019

https://investor.amarincorp.com/news-releases/news-release-details/amarin-prices-public-offering-american-depositary-shares-3

to exit profitably today

make that $1.5B volume before day end. just wow!

nice push shorts. getting uncomfortable yet?

gonna test 22.82 again or ?

$1B in trade volume before day end.

(think back 2 years ... just wow!)

~500k pre market. who is meeting this buy demand @ only 10% increase? odd

question: with TG >150, did we effectively get anchor label also?

Effect of AMR101 (Ethyl Icosapentate) on Triglyceride (Tg) Levels in Patients on Statins With High Tg Levels (≥ 200 and < 500 mg/dL) (ANCHOR)

40.00 doesn't mean anything, i know

http://ih.advfn.com/stock-market/NASDAQ/amarin-AMRN/level2

yes T3 now. soon

bid 27.50

On Friday afternoon, the FDA stamped its landmark approval on the industrial strength fish oil for reducing cardio risks for a large and well defined population of patients. The approval doesn’t give Amarin everything it wants in expanding its use, losing out on the primary prevention group, but it goes a long way to doing what the company needed to make a major splash.

No language on statins?

ACST is moving while we wait.

maybe, but it's moving and it's higher than the ask

bid 27.00 now

level 2 ask is 26.29.

12.5 years ... waiting for this moment. gulp!

i like the model ( but what does that matter?)

how's come there's no indication of dividends or share buyback?

(or to be blunt, what the #$)%(*& is happening to the $32.5B?)

can amarin do better than 0.1644 GIA?

if GIA, how will amarin spend capital (cash or equity) in contrast to buyer of amarin?

how many shares could amarin buy back with the cash resulting from $1, $2, $5B in revenues?

vague recollection: from april 2007 when i invested ... there were less than 100M shares outstanding, can they get back to 200M outstanding?

NVS optimistically projected $59B in total sales over 20 yrs and overpaid for MDCO at $9.7B

not so much stuckholder selling this time through $24-25

@JL,

just look at the stock react!

First, all of the primary prior art references relied upon by the generics were previously before the Examiner or discussed by the Examiner during prosecution of the patents. That, in itself, is not determinative that the district court will side with Amarin. There is precedent of courts invalidating patents based upon prior art previously considered during prosecution. Nevertheless, it does not help the generics, and adds an extra weight to their load.

Second, the burden of proving obviousness is on the generics, and it is a relatively high one. The generics must show that the patents are invalid based upon a “clear-and-convincing-evidence” standard. In short, if the case really comes down to a close call, and the court correctly applies the standard, that suggests that the court should in theory rule against invalidating the patents.

i was under the misconception this case was about just how soon generics could sell icosapent ethyl, not about whether or not amarin's patents are actually valid? settling this case is secondary in importance only to the reduce-it label!

gia vs. buyout

perspectives:

sell the product vs. sell the company

low share cost basis (pre reduce-it) vs. high share cost basis (post reduce-it)

ability/willingness to absorb temporary decline in share price while awaiting greater gains vs. inability/unwillingness to absorb temporary decline in share price if no buyout

already made a small fortune vs. looking for a quick gain on buyout premium

gratified, awaiting greater gratification vs. seeking gratification

(now carry on with your efforts to persuade one other)

oh well, i guess i am not entirely ignored on this board. 8)