News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

investor15

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Why the Volcker Rule Is Now 3x Longer Stock-Markets / Financial Markets 2013

Nov 20, 2013 -

By: Money_Morning

Shah Gilani writes: Let’s talk about the so-called Volcker Rule.

When the Dodd-Frank Act was signed into law in 2010 – the bank-busting, save the system, “we’ll never again have a financial meltdown that could destroy the world” legislation – it was more of an outline.

The ostensible idea, in the aftermath of the credit crisis, was to give regulators time to write sensible rules and not throw the baby out with the bathwater. Yeah right.

Of course, the real deal was about giving banks and financial services institutions time to fight every rule and regulation, from first drafts to final implementation.

Along the way, it was proposed that banks should spin off their risky businesses into separately capitalized companies, in the form of what an investment bank or a merchant bank used to be. That way they could play hard and fast. And if they failed, tough luck, you’d be on your own. Meantime, the sister bank would have FDIC insurance to cover its depositors and make loans and do traditional bank things. Boring and stuffy bank things.

The Obama administration didn’t go for that. President Obama, for all his bluster about bad banks needing a spanking, didn’t go for that.

Obama advisor Paul Volcker – himself one the most revered and celebrated Federal Reserve Chairmen in the institution’s 100-year history – wanted the separation of gun-slinging banks from insured depository institutions. He suggested banks stop proprietary (or “prop”) trading altogether. (That’s betting the house’s money to make outsized gains to enrich the homeboys who are pulling leveraged levers for fun and profit.)

That suggestion became known as the Volcker Rule.

There’s still no finished Volcker Rule. When I wrote about it 18 months ago, it was 300 pages long (see “Why the Volcker Rule Is a Cop-Out and a Joke“). There’s now a 1,000-page draft circulating with all kinds of marks and bruises all over it. But it’s not done, not nearly done. It’s one rule.

Part of the problem is that banks and bank lobbyists and Congressmen in the banks’ pockets are trying to stymie what they don’t like, meaning the rule itself.

But the bigger problem is this: No fewer than five regulatory agencies are collaborating on the rule.

The Fed and the SEC want to cut banks as wide a highway as they can, so banks aren’t “hindered” from doing what they do that facilitates smooth-running capital markets. The CFTC and the FDIC want to fill in the loopholes being written into the rule. The OCC, they’re clueless anyway, so they’re just reading drafts over lunchtime martinis.

It all comes down to banks wanting to conduct “important functions” – such as market-making and hedging – without stupid restrictions. After all, market-making is not proprietary trading, they say, and hedging, well, that’s hedging, they say.

I was a market-maker (that’s an official stamp) on the Floor of the CBOE. And I was the hedge trader for one of the world’s biggest banks. Let me tell you what market-making is and what hedging is… really.

Market-making[color=red][/color] is when you are supposed to make a two-sided market. It’s your job to simultaneously bid and offer for a stock, an option, a commodity, whatever.

I’ll use stocks as an example. If you (supposing you’re a broker or dealer or floor trader) ask me for a “quote,” I have to give you a price I would buy the stock at and a price I would sell you the stock at and how much stock I am willing to buy or sell.

You might want to ask a bunch of market-makers what their quotes are (or these days you see what their quotes are on your computer screen), and you try to buy at the lowest price being offered by some market-maker or sell at the highest price some other market-maker is quoting.

Market-making is all about taking risks. Market-making is itself proprietary trading. You want to buy stock, and I sell you stock. I did that to facilitate you. But in doing so, I took a position, I sold you stock, maybe I sold you stock I didn’t own, so I shorted the stock to you. I am now short the stock. I have a position. I have on a proprietary trade.

Let’s say you’re a big customer and you want to buy a ton of stock from me. I will go out and amass a huge position, because I’m going to facilitate you. I’m making a market for you. I’m taking a huge risk building up a position that you said you want to buy. What if you don’t buy that position I’ve built up? What if I made up the fact that I had a customer that I needed to facilitate? What if I just wanted to pretend I was making a market but really wanted to amass a huge position to make money for my trading desk, for my bank, for my bonus pool?

How on earth are regulators going to know if banks are taking proprietary positions and just calling them client-related positioning or market-making? They aren’t. It’s a giant loophole.

Hedging?[color=red][/color] Let me say this about that. Hedging is when you have an at-risk position and you don’t like the risk. So, instead of just dumping the risk position (which is better than hedging), which you may not be able to do or unwilling to do for any number of reasons, you put on a hedge. A hedge is another position that makes money if your other position loses money. A perfect hedge (which is very hard to accomplish) means you don’t lose any money. You don’t make money, but you don’t lose money. An imperfect hedge will result in you probably losing some money, and once in a blue moon, you can make a little money on a hedge.

If you’re a bank, though, you can make a ton of money on a hedge, or you can lose a ton of money on a hedge.

Why? Because you weren’t really hedging. You were saying you were hedging. But you were taking another position with a lot of risk to make money on that part of your hedge.

You weren’t hedging. You were lying about hedging. You were prop trading.

That just happened. The JPMorgan “Whale” trade in London, the one that lost them $6.5 billion, that was a “hedge” trade. Yeah, that’s what they called it. It was a hedge trade that went bad. That was a prop trade lipsticked-up and called a hedge trade.

Market-making and hedging are both loopholes. They will be used to prop trade. It’s that simple.

Treasury Secretary Jacob Lew is pushing hard to get the Volcker Rule done by year-end, this year. But the Fed now wants to give banks until July 2015, instead of 2014, to implement whatever it looks like.

If the rule ends up being 1,000 pages, you can guess why it’s that long. It’s that long so that there will be enough fine print loopholes in it to give banks what they want… the ability to prop trade and not call it proprietary trading.

The only thing I can tell you for sure about this pending Volcker Rule is this: When it comes out, I will read it and I will spell out for you where the loopholes are and how banks will use those loopholes.

That much I can promise you.

Shah

Source :http://www.wallstreetinsightsandindictments.com/2013/11/why-the-volcker-rule-is-now-3x-longer/

Money Morning/The Money Map Report

US Government Lets JPMorgan Off the Hook for Mortgage Fraud

By Andre Damon and Barry Grey

Global Research, November 20, 2013

On Tuesday, the US Justice Department announced a long-awaited official settlement with JPMorgan Chase & Co., the largest US bank, on an array of charges by state and federal agencies related to the bank’s sale of toxic mortgage-backed securities, which contributed to the 2008 financial crash.

US Attorney General Eric Holder touted the agreement, which includes $9 billion in fines and $4 billion in consumer relief, as a major victory for the public over the banks. “The size and scope of this resolution should send a clear signal that the Justice Department’s financial fraud investigations are far from over,” said Holder, adding, “No firm, no matter how profitable, is above the law, and the passage of time is no shield from accountability.”

In reality, the settlement falls far short of holding JPMorgan accountable for its fraudulent sale of mortgage-backed assets, which netted the bank tens of billions of dollars in profits while exacerbating the sub-prime mortgage crash that led to over ten million foreclosures in the US and a global economic downturn that thrust many millions more into unemployment and poverty.

Holder himself, in an interview broadcast Tuesday by NBC News, said that, in his opinion, JPMorgan’s actions played a direct role in the biggest financial crisis since the Great Depression. Yet in return for the settlement, the bank is released from a raft of lawsuits by the Justice Department, state attorneys general and three federal agencies.

The settlement’s statement of facts asserts that “employees of JPMorgan… received information that, in certain instances, loans that did not comply with underwriting guidelines were included in the RMBS [residential mortgage-backed securities] sold and marketed to investors; however, JPMorgan… did not disclose this to securitization investors.”

New York State Attorney General Eric Schneiderman, head of the Obama administration’s mortgage fraud task force, said the company “acknowledged it made serious, material misrepresentations to the public—including the investing public—about numerous RMBS transactions.”

While JPMorgan endorsed as factual the government’s claim that it knowingly sold defective mortgage-backed bonds to investors in violation of securities laws, the settlement does not include a direct admission of criminal wrongdoing by the bank. In months of closed-door negotiations between bank executives, including CEO Jamie Dimon, and top Justice Department officials, including Attorney General Holder, the bank resisted making such an acknowledgment of guilt, which would have opened it up to a wave of private lawsuits. In the end, the Obama administration complied with the bank’s wishes.

The Justice Department said it was continuing a criminal investigation of JPMorgan’s mortgage bond business, but there has as yet been no criminal indictment of Dimon or any other leading JPMorgan official.

This is in keeping with the administration’s policy of shielding the Wall Street elite from prosecution for its criminal actions both before, during and after the financial crash of September 2008. Not a single top banker has been criminally charged, let alone convicted and jailed, despite detailed exposures of illegal actions made public two years ago by a special investigatory commission into the financial crisis and, in a separate report, the Senate Permanent Subcommittee on Investigations.

The settlement, hailed by the Obama administration and the media as a “breakthrough” in government policing of the banks, is nothing of the kind. The headline figure of $13 billion is deliberately deceptive. Only $9 billion of the total is in cash, the rest taking the form of relief to troubled homeowners, partly through reductions in mortgage principals and partly through the lowering of interest payments. It is likely that JPMorgan was already planning to offer much of this $4 billion in relief for business reasons.

Moreover, according to Reuters, $11 billion of the total penalty is tax deductible. The news agency quoted Gregg Polsky, a law professor at the University of North Carolina, as saying the bank’s fine would effectively be reduced by $4 billion. The total cost to the bank for settling virtually all outstanding civil suits stemming from its fraudulent mortgage business prior to the crash will thus be about a third of its reported $21 billion profit for 2012.

The deal worked out mutually between the US government and JPMorgan is calibrated to include a fine large enough to give the appearance of a sharp rebuke, while insuring the bank’s continued viability and profitability. JPMorgan has, moreover, already set aside $28 billion to settle the large number of lawsuits and investigations into its activities.

The very fact that top Justice Department officials have spent months cajoling Dimon to agree to a such a deal highlights the immense power wielded by Wall Street over the government and the entire political establishment. The victims of predatory loans sold by JPMorgan or packaged into securities sold by the bank, who were then unable to meet their mortgage payments, were accorded no such consideration before they were thrown onto the street and had their homes seized.

Following the Justice Department announcement on Tuesday, Dimon said in a statement: “We are pleased to have concluded this extensive agreement with the president’s RMBS Working Group and to have resolved the civil claims of the Department of Justice and others.”

The blanket settlement releases JPMorgan from civil investigations by the Department of Justice and the state attorneys general of California, Delaware, Illinois, Massachusetts and New York, as well as civil litigation by the Federal Deposit Insurance Corporation (FDIC), the Federal Housing Finance Agency (FHFA) and the National Credit Union Administration (NCUA).

The company’s stock jumped by 0.74 percent following the announcement, even as other financial stocks closed lower for the day.

Multiple probes into the fraudulent sale of mortgage bonds constitute only one area of JPMorgan’s activities that are currently under investigation. In September, the bank agreed to pay close to $1 billion to settle charges that it lied to investors and government regulators and committed accounting fraud to conceal $6.2 billion in losses in derivatives bets last year. A 300-page report on the so-called “London Whale” scandal issued last March by the Senate Permanent Subcommittee on Investigations concluded that the bank sought “to hide hundreds of millions of dollars of losses,” and that top executives, including Dimon himself, knowingly misinformed the public and investors.

According to the New York Times, the bank is currently being investigated by “at least eight federal agencies, a state regulator and two European nations.”

The actions under examination include the bank’s participation in the Libor-rigging scandal, allegations that JPMorgan facilitated Bernard Madoff’s multi-billion-dollar Ponzi scheme, accusations by the Federal Energy Regulatory Commission that it manipulated energy prices, allegations that it bribed Chinese officials, and the bank’s participation in the so-called robo-signing scandal, in which the employees of major mortgage lenders claimed to have reviewed foreclosure documents with which they were totally unfamiliar.

http://www.globalresearch.ca/us-government-lets-jpmorgan-off-the-hook-for-mortgage-fraud/5358794

US Government Lets JPMorgan Off the Hook for Mortgage Fraud

By Andre Damon and Barry Grey

Global Research, November 20, 2013

On Tuesday, the US Justice Department announced a long-awaited official settlement with JPMorgan Chase & Co., the largest US bank, on an array of charges by state and federal agencies related to the bank’s sale of toxic mortgage-backed securities, which contributed to the 2008 financial crash.

US Attorney General Eric Holder touted the agreement, which includes $9 billion in fines and $4 billion in consumer relief, as a major victory for the public over the banks. “The size and scope of this resolution should send a clear signal that the Justice Department’s financial fraud investigations are far from over,” said Holder, adding, “No firm, no matter how profitable, is above the law, and the passage of time is no shield from accountability.”

In reality, the settlement falls far short of holding JPMorgan accountable for its fraudulent sale of mortgage-backed assets, which netted the bank tens of billions of dollars in profits while exacerbating the sub-prime mortgage crash that led to over ten million foreclosures in the US and a global economic downturn that thrust many millions more into unemployment and poverty.

Holder himself, in an interview broadcast Tuesday by NBC News, said that, in his opinion, JPMorgan’s actions played a direct role in the biggest financial crisis since the Great Depression. Yet in return for the settlement, the bank is released from a raft of lawsuits by the Justice Department, state attorneys general and three federal agencies.

The settlement’s statement of facts asserts that “employees of JPMorgan… received information that, in certain instances, loans that did not comply with underwriting guidelines were included in the RMBS [residential mortgage-backed securities] sold and marketed to investors; however, JPMorgan… did not disclose this to securitization investors.”

New York State Attorney General Eric Schneiderman, head of the Obama administration’s mortgage fraud task force, said the company “acknowledged it made serious, material misrepresentations to the public—including the investing public—about numerous RMBS transactions.”

While JPMorgan endorsed as factual the government’s claim that it knowingly sold defective mortgage-backed bonds to investors in violation of securities laws, the settlement does not include a direct admission of criminal wrongdoing by the bank. In months of closed-door negotiations between bank executives, including CEO Jamie Dimon, and top Justice Department officials, including Attorney General Holder, the bank resisted making such an acknowledgment of guilt, which would have opened it up to a wave of private lawsuits. In the end, the Obama administration complied with the bank’s wishes.

The Justice Department said it was continuing a criminal investigation of JPMorgan’s mortgage bond business, but there has as yet been no criminal indictment of Dimon or any other leading JPMorgan official.

This is in keeping with the administration’s policy of shielding the Wall Street elite from prosecution for its criminal actions both before, during and after the financial crash of September 2008. Not a single top banker has been criminally charged, let alone convicted and jailed, despite detailed exposures of illegal actions made public two years ago by a special investigatory commission into the financial crisis and, in a separate report, the Senate Permanent Subcommittee on Investigations.

The settlement, hailed by the Obama administration and the media as a “breakthrough” in government policing of the banks, is nothing of the kind. The headline figure of $13 billion is deliberately deceptive. Only $9 billion of the total is in cash, the rest taking the form of relief to troubled homeowners, partly through reductions in mortgage principals and partly through the lowering of interest payments. It is likely that JPMorgan was already planning to offer much of this $4 billion in relief for business reasons.

Moreover, according to Reuters, $11 billion of the total penalty is tax deductible. The news agency quoted Gregg Polsky, a law professor at the University of North Carolina, as saying the bank’s fine would effectively be reduced by $4 billion. The total cost to the bank for settling virtually all outstanding civil suits stemming from its fraudulent mortgage business prior to the crash will thus be about a third of its reported $21 billion profit for 2012.

The deal worked out mutually between the US government and JPMorgan is calibrated to include a fine large enough to give the appearance of a sharp rebuke, while insuring the bank’s continued viability and profitability. JPMorgan has, moreover, already set aside $28 billion to settle the large number of lawsuits and investigations into its activities.

The very fact that top Justice Department officials have spent months cajoling Dimon to agree to a such a deal highlights the immense power wielded by Wall Street over the government and the entire political establishment. The victims of predatory loans sold by JPMorgan or packaged into securities sold by the bank, who were then unable to meet their mortgage payments, were accorded no such consideration before they were thrown onto the street and had their homes seized.

Following the Justice Department announcement on Tuesday, Dimon said in a statement: “We are pleased to have concluded this extensive agreement with the president’s RMBS Working Group and to have resolved the civil claims of the Department of Justice and others.”

The blanket settlement releases JPMorgan from civil investigations by the Department of Justice and the state attorneys general of California, Delaware, Illinois, Massachusetts and New York, as well as civil litigation by the Federal Deposit Insurance Corporation (FDIC), the Federal Housing Finance Agency (FHFA) and the National Credit Union Administration (NCUA).

The company’s stock jumped by 0.74 percent following the announcement, even as other financial stocks closed lower for the day.

Multiple probes into the fraudulent sale of mortgage bonds constitute only one area of JPMorgan’s activities that are currently under investigation. In September, the bank agreed to pay close to $1 billion to settle charges that it lied to investors and government regulators and committed accounting fraud to conceal $6.2 billion in losses in derivatives bets last year. A 300-page report on the so-called “London Whale” scandal issued last March by the Senate Permanent Subcommittee on Investigations concluded that the bank sought “to hide hundreds of millions of dollars of losses,” and that top executives, including Dimon himself, knowingly misinformed the public and investors.

According to the New York Times, the bank is currently being investigated by “at least eight federal agencies, a state regulator and two European nations.”

The actions under examination include the bank’s participation in the Libor-rigging scandal, allegations that JPMorgan facilitated Bernard Madoff’s multi-billion-dollar Ponzi scheme, accusations by the Federal Energy Regulatory Commission that it manipulated energy prices, allegations that it bribed Chinese officials, and the bank’s participation in the so-called robo-signing scandal, in which the employees of major mortgage lenders claimed to have reviewed foreclosure documents with which they were totally unfamiliar.

http://www.globalresearch.ca/us-government-lets-jpmorgan-off-the-hook-for-mortgage-fraud/5358794

Pilot Hits Home Run

Bob Moriarty

Archives

Nov 20, 2013

There are some wonderful aspects to getting old and coming down with Alzheimer’s. For one, you get to hide your own Easter eggs . As a writer you can go back and read what you wrote a few months ago and think, “By golly, that writer got it just right,” when reading your own crap.

I wrote a piece about the Kinsley Mountain project of Pilot Gold two months ago. By golly, I got it just right. Other than misspelling the name of the Rock Whisperer, Moira Smith.

On the 18th of November, Pilot announced the drill results of some 32 core and RC holes at the Kinsley project. Assays are pending for an additional 26 holes. The company has drilled about 14,200 meters of a 20,000 meter program due to end this month.

When I visited Kinsley two months ago Moira told me that her theory was that Alta Gold was producing from the wrong package of rocks and if they could drill the same rock sequence that they had found at Long Canyon, she thought the project had district scale potential.

She also felt the NS trending structures were as important or more important than the prevailing NNW structures that Alta had been mining. Alta had been mining the Candland Shales and she thought the limestone and shales underneath the Candland sequence would show better mineralization.

In short, Moira and her team wanted to apply the Long Canyon model to Kinsley. The initial drill results from the 2013 program support her theory. Proof of Concept came in the form of a 36.6-meter intercept of 8.53 g/t gold. To give you an idea of how significant that is, the hole was located some 550 meters from Alta’s mining. It was the single best intercept of over 1300 drill holes drilled at Kinsley.

I’d say Pilot and Moira Smith and her team just hit a giant home run. I wonder if Newmont has another $2.3 billion they would like to spend on another multi-million ounce deposit in the Long Canyon Trend.

Pilot has about $23 million in the bank and is well cashed up for the coming future. Look for more drill results in the next month.

Pilot is an advertiser and I am biased. Do your own due diligence.

Pilot Gold Inc

PLG-T $.92 (Nov 19, 2013)

PLGDF OTCQX 89.9 million shares

Pilot Gold website

###

Bob Moriarty

President: 321gold

Archives

321gold Ltd

http://www.321gold.com/editorials/moriarty/moriarty112013.html

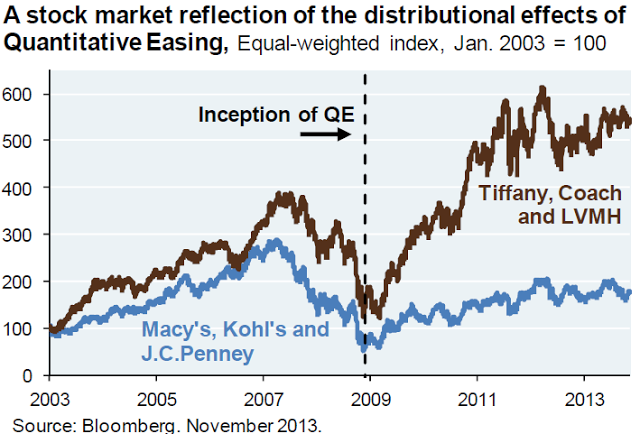

The Red Queen’s race and the real winners from Quantitative Easing: Celebrating the five year anniversary of redistributing wealth to the top.

Posted by mybudget360.com

Nov. 20, 2013

The Federal Reserve is celebrating its 5 year anniversary of Quantitative Easing. As the stock market reaches record highs, it is useful to examine the real winners from QE. Luxury good purchases have done extremely well during this period as income inequality in the nation has reached levels last seen during the Gilded Age. Yet for the average American worker, salaries are stagnant and wage growth is nearly non-existent. After factoring in for inflation, many are stuck in having to run faster and faster just to stay in the same place. The Red Queen’s race in Through the Looking Glass involves a race where you have to run faster just to stay in the same place. Or in other words, trying to maintain a middle class lifestyle in an era of massive Fed intervention. QE has made it harder for savers and most American families to keep up while the leveraged top has been able to maximize all the benefits of QE. After 5 years, it is rather clear who the winners are.

Examining luxury goods

Few people have the means to buy Tiffany or Coach products. So it is interesting to compare these luxury brand companies versus other places where average Americans shop after QE:

It is clear that QE has provided a dramatic benefit to products that really cater to a small sliver of the population. QE has been a direct punishment to savers and most Americans since many do not own one piece of stock. This is why the 144% rally in the S&P 500 has not provided the expected benefits from such a significant run. Very little has trickled down.

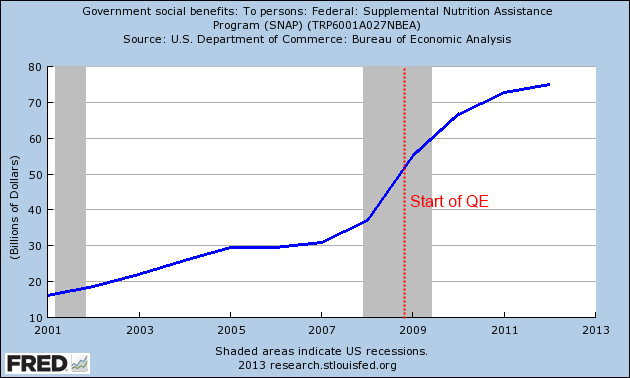

We also have a very large number of Americans on food stamps. It appears that we now have a structurally poor part of our country that seems to be permanently entrenched. Over 47 million Americans are now on food stamps and the costs are not reversing:

You’ll notice that QE did very little in reversing this trend. And why would it? QE is merely a focus on assisting banks and hoping that the financial industry has the best interest of the nation at heart. First, let us set aside that the financial crisis that led us to this cliff was brought on by none other than our financial system. No reforms ever came about and instead more money was funneled into the banking sector and even accounting laws were paused simply to assist banks. 5 years later banks are back to making mega profits while many Americans are shutout of this prosperity. It is a massive system of corporate social welfare.

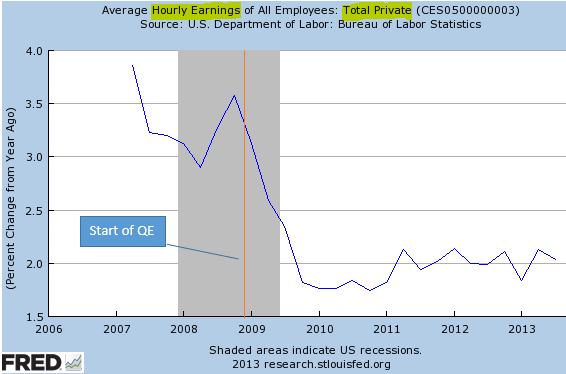

Where the wages stagnant

If we look at average hourly earnings we find that QE was not much help here either:

Source: SoberLook

This wasn’t a very positive development for your regular worker. We also find that many of the jobs added since the recession officially ended in the summer of 2009 have come in the form of lower paying jobs. It is the case that the largest employment sectors in the US pay very little:

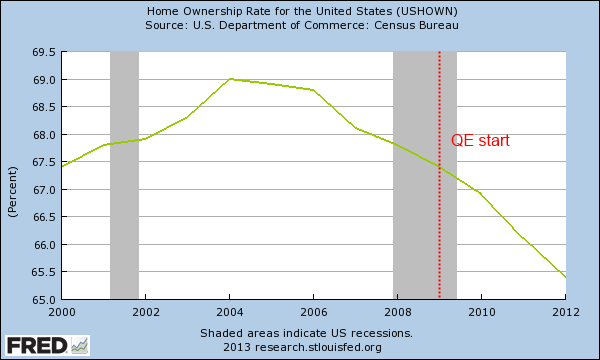

It is clear that QE has been a big win for the banking sector. It has allowed banks the time to inflate assets and get rid of loans in a timely manner (of their choosing circumventing generational accounting rules and standards). Ironically the real estate market has also boomed but over 5 million foreclosures have occurred over this period and many of these were sold to large banks and hedge funds for low prices financed with easy debt provided by the Fed. In other words, from one bank to another bank and away from regular households. You can see this in the drop in homeownership over this same time:

The Federal Reserve has been primarily focused on helping the financial industry. In this mission they have succeeded. However, as most know there is no economic free lunch and we are seeing this at the 5 year anniversary of QE.

RSSIf you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market!

http://www.mybudget360.com/fed-qe-anniversary-wealth-distribution-qe-quantitative-easing-history/

Banks Syphoning Off the Financial Blood of their Customers

Nov 18, 2013 - 10:13 AM GMT

By: James_Quinn

Reports like the recent one from SNL Financial – Branch Networks Continue to Shrink really get my goat. As I travel the increasingly vacant highways of Montgomery County, PA I’m keenly aware of my surroundings. If I were a foreigner visiting for the first time, I’d think Space Available was the hot new retailer in the country. I’ve detailed the slow disintegration of our suburban sprawl paradise in previous articles:

Thousands of Space Available signs dot the bleak landscape, as office buildings, strip malls, and industrial complexes wither and die. Gas stations are shuttered on a daily basis as the ongoing depression results in less miles being driven by unemployed and underemployed suburbanites. At least the Chinese “Space Available” sign manufacturers are doing well. The only buildings doing brisk business are the food banks and homeless shelters.

The sad part is that I live in a relatively prosperous county with a low level of SNAP recipients and primarily occupied by a white collar college educated populace. If the clear downward spiral in my upper middle class county is an indication of our country’s path, the less well-off counties across the land must be in deep trouble.

While hundreds of thousands of square feet of retail, restaurant, office and industrial space have been vacated in the last six years, the only entities expanding in my area have been banks, drug stores, municipal buildings and healthcare facilities. I have been flabbergasted by what I’ve viewed as a complete waste of resources to create facilities that weren’t needed and wouldn’t be utilized. I have seven drug stores within five miles of my house. I have ten bank branches within five miles of my house. While two perfectly fine older hospitals in Norristown were abandoned, a brand new $300 million super deluxe, glass encased Einstein Hospital palace was built three miles away by a barely above junk bond status non-profit institution. None of this makes sense in a contracting economy.

This is another classic case of mal-investment spurred by the Federal Reserve easy money policies, zero interest rates, and QEternity. Cheap money leads to bad investments. I’m all for competition between drug store chains and banks. CVS, Walgreens, and Rite Aid are the three big chains in the country. I have my pick of multiple stores close to my house. There are clearly too many stores competing for a dwindling number of customers, with a dwindling supply of disposable income. The only reason Rite Aid is still in the picture is the easy money policies of the Federal Reserve. They have been teetering on the verge of bankruptcy for the last five years, but continue to get cheap financing from the Wall Street cabal, who would rather pretend they will get paid, than write-off the bad debt. Who in their right mind would continue to lend money to a company with $6 billion in debt, NEGATIVE $2.3 billion of equity, and losses exceeding $2 billion since 2008? They are the poster child for badly run businesses that over expanded, took on too much debt and should be liquidated. There are over 4,600 zombie Rite Aid stores littering the countryside waiting to be put out of their misery.

Rite Aid will never repay the $6 billion of debt. They know it. Their auditors know it. Their Wall Street lenders know it. The Federal Reserve Bank regulators know it. Anyone with a functioning brain knows it. Tune in to CNBC for those who are paid to keep clueless investors from knowing it. Interest rates that actually reflected risk and weren’t manipulated to an artificially low level by the Federal Reserve would make financing for a dog like Rite Aid a non-starter. Creative destruction would be allowed to work its magic, with winners separated from losers. Instead Rite Aid continues as a zombie entity, barely surviving for now. This exact scenario applies to J.C. Penney, RadioShack, Sears and a myriad of other dead retailers walking. Rather than suffering the consequences of appalling management judgment, dreadful strategic decisions, and reckless financial gambles, they have been allowed to remain on life support compliments of Bernanke, his Wall Street chiefs, and the American taxpayer.

In a truly free, non-manipulated market the weak would be culled, new dynamic competitors would fill the void, and consumers would benefit. Extending debt payment schedules of zombie entities and pretending you will get paid has been the mantra of the insolvent zombie Wall Street banks since 2009. The Federal Reserve is responsible for zombifying the entire country. And it wasn’t a mistake. It was a choice made by those in power in order to maintain the status quo. The fateful day in March 2009 when the pencil pushing lightweight accountants at the FASB rescinded mark to market accounting rules gave birth to zombie nation. And not coincidently, marked the bottom for the stock market. Wall Street banks were free to fabricate their earnings, pretend they didn’t have hundreds of billions in bad loans on their books, and extend the terms of commercial real estate loans that were in default. With their taxpayer funded TARP ransom, ability to borrow at 0% from Uncle Ben, and the $3 trillion of QE cocaine snorted up their noses in the last four years, the mal-investment, fraud, and idiocy of the Wall Street drug addicts has reached a crescendo.

The mal-investment by zombie drug store chains has only been exceeded by the foolish, egocentric, insane bank branch expansion by the Too Big To Trust Wall Street CEOs. In the last ten years dozens of bank branches have been built in the vicinity of my house and across the state of Pennsylvania. These gleaming glass TARP palaces are on virtually every other street corner across Montgomery County. Stunning, glittery, colorful branches stuffed with bank employees pretending to loan money to non-existent customers. They have become nothing but a high priced marketing billboard with an ATM attached. By 2010, the number of bank branches in this country had reached almost 100,000. The vast majority are run by the usual insolvent suspects:

Wells Fargo – 6,500

J.P. Morgan – 6,000

Bank of America – 5,700

The top ten biggest banks, in addition to holding the vast majority of deposits, mortgages and credit card accounts, operate 33% of all the bank branches in the country. The very same banks that have paid out $66 billion in criminal settlement charges over the last three years and have incurred $103 billion of legal fees to defend themselves against the thousands of actions brought by victims for their criminal misdeeds, decided it was a wise decision to open new bank branches from 2007 through 2010. Only an Ivy League educated MBA could possibly think this was a good idea.

It was almost as if the CEO’s of the biggest Wall Street banks didn’t care about pissing away the $2.5 million to build the average 3,500 square foot bank branch, which would require $30 million of deposits to breakeven. This level of deposits isn’t easy to achieve when your customers are unemployed due to your bank destroying the American economy, broke due to their real household income declining by 10% over the past fourteen years, and your bank paying them .15% on their deposits. It also probably doesn’t help when you charge them $3 every time they withdraw their own money from your bank and you charge them $25 when their bank balance falls below $1,000 because they just got laid off from Merck on Christmas Eve. It is now estimated that one-third of all bank branches in the country lose money. Who can afford to run something that consistently losses money, other than our government? Wall Street bankers can when the taxpayer is footing the bill and Bernanke/Yellen subsidizes their mal-investment by lending to them at 0%, providing them $2.5 billion per day of QE play money, and paying them $5 billion per year in interest to park the excess reserves that aren’t getting leant to small businesses and consumers at their thousands of gleaming bank branches.

Hasn’t one of the thousands of highly educated MBA vice presidents occupying offices at the Too Big To Control Wall Street banks explained to Stumpf, Dimon and Monyihan that bricks and mortar are dead? A new invention called the internet has made in-person banking virtually obsolete. Why does anyone need to go into a bank branch in this electronic age? I’ve been in my credit union branch five times in the last ten years, twice for a refinance closing on my home and a couple times to get a certified check. With ATM machines, direct deposit and on-line bill paying, why would the country need 100,000 physical bank locations? I pay 90% of my bills on-line. If I need cash, I hit the ATM at Wawa, where there are no ATM fees (my credit union doesn’t charge me to get my own money). The only people who go into bank branches on a regular basis are old fogeys that don’t trust that new-fangled internet. The older generations are dying out and the millennial generation has no need for bank branches. Their iGadgets function as their bank connection. Plus, since they don’t have jobs or money, a bank account at the local bank branch of J.P. Morgan seems a bit trite.

The writing had been on the wall for a long time, but the reckless bank executives continued to build branches in an ego driven desire to outdo their equally irresponsible competitor bank executives. Now the race is on to see which banks can close the most branches. Bank consultant Jim Adkins succinctly sums up the pure idiocy of physical bank branches:

“There’s almost nobody in the branches. You could shoot water balloons all over the place and not hit anybody.”

It seems my humble state of Pennsylvania leads the pack in closing branches in the past year, with 149 abandoned and only 43 opened. Only two states in the entire country had more branch openings than closings.

After shuttering 2,267 branches in 2012, the industry is on track to closing another 2,500 in 2013. Shockingly, the leader of the Wall Street zombie apocalypse, Bank of America, led the pack in bank branch closings with 194 in the last year. Staying true to his hubristic arrogance, Jamie Dimon actually opened 62 more branches than he closed in the last year, despite his upstanding institution having to pay tens of billions in fines, settlements and pay-offs for their criminal transgressions.

There are now 93,000 bank branches remaining in this country, and one third of them don’t generate a profit. That percentage will grow as the older generations rapidly die out and are replaced by the techno-narcissists who never leave their family rooms. Online banking already accounts for 53% of banking transactions, compared with 14% for in-branch visits. Younger bank customers increasingly prefer online and mobile banking, as advancing technology enables them to make remote deposits, shop for loans and manage accounts more efficiently from their desktops or smartphones. This trend will only accelerate in the years to come.

Banking industry profits reached a record level of $141 billion in 2012 as more vacancy signs appeared on Main Street. Now that the Wall Street cabal have syphoned every ounce of blood from their customers/victims through ATM fees, overdraft fees, minimum balance fees, credit card fees, late payment fees, and paying no interest on deposits, they are forced to focus on the $300,000 average loss per bank branch. QE and ZIRP might not last forever. Yeah right. AlixPartners, a New York consulting firm, expects the number of bank branches to drop to 80,000 over the next decade. They are wrong. They have failed to take into account the lemming like behavior of Wall Street banks. As their accounting gimmicks to generate fake profits dissipate, the increasingly desperate insolvent zombie banks will rapidly vacate their prime corner locations in droves. With approximately 30,000 locations already generating losses, the Wall Street MBAs will be closing branches quicker than you can say “mortgage fraud”. There will be less than 70,000 branches within the next five years. That means another 20,000 to 30,000 Space Available signs going up on Main Street. That means another 200,000 to 300,000 neighbors without jobs. But don’t worry about Jamie Dimon and the rest of the Wall Street bankers. They’ll be just fine. In addition to being endlessly fed by the Fed, they’ll get creative and charge their customers a new bank branch access fee of $50 for the privilege of entering one of their few remaining outlets. By now we should know how cash flows to Main Street in this corporate fascist paradise.

Do your part to starve the beast. Move your bank accounts to a local credit union. Don’t support criminals.

Join me at www.TheBurningPlatform.com to discuss truth and the future of our country.

By James Quinn

quinnadvisors@comcast.net

James Quinn is a senior director of strategic planning for a major university. James has held financial positions with a retailer, homebuilder and university in his 22-year career. Those positions included treasurer, controller, and head of strategic planning. He is married with three boys and is writing these articles because he cares about their future. He earned a BS in accounting from Drexel University and an MBA from Villanova University. He is a certified public accountant and a certified cash manager.

http://www.marketoracle.co.uk/Article43162.html

Banks Syphoning Off the Financial Blood of their Customers

Nov 18, 2013 - 10:13 AM GMT

By: James_Quinn

Reports like the recent one from SNL Financial – Branch Networks Continue to Shrink really get my goat. As I travel the increasingly vacant highways of Montgomery County, PA I’m keenly aware of my surroundings. If I were a foreigner visiting for the first time, I’d think Space Available was the hot new retailer in the country. I’ve detailed the slow disintegration of our suburban sprawl paradise in previous articles:

Thousands of Space Available signs dot the bleak landscape, as office buildings, strip malls, and industrial complexes wither and die. Gas stations are shuttered on a daily basis as the ongoing depression results in less miles being driven by unemployed and underemployed suburbanites. At least the Chinese “Space Available” sign manufacturers are doing well. The only buildings doing brisk business are the food banks and homeless shelters.

The sad part is that I live in a relatively prosperous county with a low level of SNAP recipients and primarily occupied by a white collar college educated populace. If the clear downward spiral in my upper middle class county is an indication of our country’s path, the less well-off counties across the land must be in deep trouble.

While hundreds of thousands of square feet of retail, restaurant, office and industrial space have been vacated in the last six years, the only entities expanding in my area have been banks, drug stores, municipal buildings and healthcare facilities. I have been flabbergasted by what I’ve viewed as a complete waste of resources to create facilities that weren’t needed and wouldn’t be utilized. I have seven drug stores within five miles of my house. I have ten bank branches within five miles of my house. While two perfectly fine older hospitals in Norristown were abandoned, a brand new $300 million super deluxe, glass encased Einstein Hospital palace was built three miles away by a barely above junk bond status non-profit institution. None of this makes sense in a contracting economy.

This is another classic case of mal-investment spurred by the Federal Reserve easy money policies, zero interest rates, and QEternity. Cheap money leads to bad investments. I’m all for competition between drug store chains and banks. CVS, Walgreens, and Rite Aid are the three big chains in the country. I have my pick of multiple stores close to my house. There are clearly too many stores competing for a dwindling number of customers, with a dwindling supply of disposable income. The only reason Rite Aid is still in the picture is the easy money policies of the Federal Reserve. They have been teetering on the verge of bankruptcy for the last five years, but continue to get cheap financing from the Wall Street cabal, who would rather pretend they will get paid, than write-off the bad debt. Who in their right mind would continue to lend money to a company with $6 billion in debt, NEGATIVE $2.3 billion of equity, and losses exceeding $2 billion since 2008? They are the poster child for badly run businesses that over expanded, took on too much debt and should be liquidated. There are over 4,600 zombie Rite Aid stores littering the countryside waiting to be put out of their misery.

Rite Aid will never repay the $6 billion of debt. They know it. Their auditors know it. Their Wall Street lenders know it. The Federal Reserve Bank regulators know it. Anyone with a functioning brain knows it. Tune in to CNBC for those who are paid to keep clueless investors from knowing it. Interest rates that actually reflected risk and weren’t manipulated to an artificially low level by the Federal Reserve would make financing for a dog like Rite Aid a non-starter. Creative destruction would be allowed to work its magic, with winners separated from losers. Instead Rite Aid continues as a zombie entity, barely surviving for now. This exact scenario applies to J.C. Penney, RadioShack, Sears and a myriad of other dead retailers walking. Rather than suffering the consequences of appalling management judgment, dreadful strategic decisions, and reckless financial gambles, they have been allowed to remain on life support compliments of Bernanke, his Wall Street chiefs, and the American taxpayer.

In a truly free, non-manipulated market the weak would be culled, new dynamic competitors would fill the void, and consumers would benefit. Extending debt payment schedules of zombie entities and pretending you will get paid has been the mantra of the insolvent zombie Wall Street banks since 2009. The Federal Reserve is responsible for zombifying the entire country. And it wasn’t a mistake. It was a choice made by those in power in order to maintain the status quo. The fateful day in March 2009 when the pencil pushing lightweight accountants at the FASB rescinded mark to market accounting rules gave birth to zombie nation. And not coincidently, marked the bottom for the stock market. Wall Street banks were free to fabricate their earnings, pretend they didn’t have hundreds of billions in bad loans on their books, and extend the terms of commercial real estate loans that were in default. With their taxpayer funded TARP ransom, ability to borrow at 0% from Uncle Ben, and the $3 trillion of QE cocaine snorted up their noses in the last four years, the mal-investment, fraud, and idiocy of the Wall Street drug addicts has reached a crescendo.

The mal-investment by zombie drug store chains has only been exceeded by the foolish, egocentric, insane bank branch expansion by the Too Big To Trust Wall Street CEOs. In the last ten years dozens of bank branches have been built in the vicinity of my house and across the state of Pennsylvania. These gleaming glass TARP palaces are on virtually every other street corner across Montgomery County. Stunning, glittery, colorful branches stuffed with bank employees pretending to loan money to non-existent customers. They have become nothing but a high priced marketing billboard with an ATM attached. By 2010, the number of bank branches in this country had reached almost 100,000. The vast majority are run by the usual insolvent suspects:

Wells Fargo – 6,500

J.P. Morgan – 6,000

Bank of America – 5,700

The top ten biggest banks, in addition to holding the vast majority of deposits, mortgages and credit card accounts, operate 33% of all the bank branches in the country. The very same banks that have paid out $66 billion in criminal settlement charges over the last three years and have incurred $103 billion of legal fees to defend themselves against the thousands of actions brought by victims for their criminal misdeeds, decided it was a wise decision to open new bank branches from 2007 through 2010. Only an Ivy League educated MBA could possibly think this was a good idea.

It was almost as if the CEO’s of the biggest Wall Street banks didn’t care about pissing away the $2.5 million to build the average 3,500 square foot bank branch, which would require $30 million of deposits to breakeven. This level of deposits isn’t easy to achieve when your customers are unemployed due to your bank destroying the American economy, broke due to their real household income declining by 10% over the past fourteen years, and your bank paying them .15% on their deposits. It also probably doesn’t help when you charge them $3 every time they withdraw their own money from your bank and you charge them $25 when their bank balance falls below $1,000 because they just got laid off from Merck on Christmas Eve. It is now estimated that one-third of all bank branches in the country lose money. Who can afford to run something that consistently losses money, other than our government? Wall Street bankers can when the taxpayer is footing the bill and Bernanke/Yellen subsidizes their mal-investment by lending to them at 0%, providing them $2.5 billion per day of QE play money, and paying them $5 billion per year in interest to park the excess reserves that aren’t getting leant to small businesses and consumers at their thousands of gleaming bank branches.

Hasn’t one of the thousands of highly educated MBA vice presidents occupying offices at the Too Big To Control Wall Street banks explained to Stumpf, Dimon and Monyihan that bricks and mortar are dead? A new invention called the internet has made in-person banking virtually obsolete. Why does anyone need to go into a bank branch in this electronic age? I’ve been in my credit union branch five times in the last ten years, twice for a refinance closing on my home and a couple times to get a certified check. With ATM machines, direct deposit and on-line bill paying, why would the country need 100,000 physical bank locations? I pay 90% of my bills on-line. If I need cash, I hit the ATM at Wawa, where there are no ATM fees (my credit union doesn’t charge me to get my own money). The only people who go into bank branches on a regular basis are old fogeys that don’t trust that new-fangled internet. The older generations are dying out and the millennial generation has no need for bank branches. Their iGadgets function as their bank connection. Plus, since they don’t have jobs or money, a bank account at the local bank branch of J.P. Morgan seems a bit trite.

The writing had been on the wall for a long time, but the reckless bank executives continued to build branches in an ego driven desire to outdo their equally irresponsible competitor bank executives. Now the race is on to see which banks can close the most branches. Bank consultant Jim Adkins succinctly sums up the pure idiocy of physical bank branches:

“There’s almost nobody in the branches. You could shoot water balloons all over the place and not hit anybody.”

It seems my humble state of Pennsylvania leads the pack in closing branches in the past year, with 149 abandoned and only 43 opened. Only two states in the entire country had more branch openings than closings.

After shuttering 2,267 branches in 2012, the industry is on track to closing another 2,500 in 2013. Shockingly, the leader of the Wall Street zombie apocalypse, Bank of America, led the pack in bank branch closings with 194 in the last year. Staying true to his hubristic arrogance, Jamie Dimon actually opened 62 more branches than he closed in the last year, despite his upstanding institution having to pay tens of billions in fines, settlements and pay-offs for their criminal transgressions.

There are now 93,000 bank branches remaining in this country, and one third of them don’t generate a profit. That percentage will grow as the older generations rapidly die out and are replaced by the techno-narcissists who never leave their family rooms. Online banking already accounts for 53% of banking transactions, compared with 14% for in-branch visits. Younger bank customers increasingly prefer online and mobile banking, as advancing technology enables them to make remote deposits, shop for loans and manage accounts more efficiently from their desktops or smartphones. This trend will only accelerate in the years to come.

Banking industry profits reached a record level of $141 billion in 2012 as more vacancy signs appeared on Main Street. Now that the Wall Street cabal have syphoned every ounce of blood from their customers/victims through ATM fees, overdraft fees, minimum balance fees, credit card fees, late payment fees, and paying no interest on deposits, they are forced to focus on the $300,000 average loss per bank branch. QE and ZIRP might not last forever. Yeah right. AlixPartners, a New York consulting firm, expects the number of bank branches to drop to 80,000 over the next decade. They are wrong. They have failed to take into account the lemming like behavior of Wall Street banks. As their accounting gimmicks to generate fake profits dissipate, the increasingly desperate insolvent zombie banks will rapidly vacate their prime corner locations in droves. With approximately 30,000 locations already generating losses, the Wall Street MBAs will be closing branches quicker than you can say “mortgage fraud”. There will be less than 70,000 branches within the next five years. That means another 20,000 to 30,000 Space Available signs going up on Main Street. That means another 200,000 to 300,000 neighbors without jobs. But don’t worry about Jamie Dimon and the rest of the Wall Street bankers. They’ll be just fine. In addition to being endlessly fed by the Fed, they’ll get creative and charge their customers a new bank branch access fee of $50 for the privilege of entering one of their few remaining outlets. By now we should know how cash flows to Main Street in this corporate fascist paradise.

Do your part to starve the beast. Move your bank accounts to a local credit union. Don’t support criminals.

Join me at www.TheBurningPlatform.com to discuss truth and the future of our country.

By James Quinn

quinnadvisors@comcast.net

James Quinn is a senior director of strategic planning for a major university. James has held financial positions with a retailer, homebuilder and university in his 22-year career. Those positions included treasurer, controller, and head of strategic planning. He is married with three boys and is writing these articles because he cares about their future. He earned a BS in accounting from Drexel University and an MBA from Villanova University. He is a certified public accountant and a certified cash manager.

http://www.marketoracle.co.uk/Article43162.html

Jim Rogers on QE, Currency Wars, Gold and Inflation Commodities / Gold and Silver 2013

Nov 19, 2013 - 03:15 PM GMT

By: Submissions

BGG writes: In this revealing interview with Birch Gold Group, Jim Rogers, legendary investor and author, explains just how badly Quantitative Easing and ongoing currency wars are damaging the U.S. economy, and why it’s so important for any person to protect their savings with physical gold and silver.

MF Global Admits Liability; Will Pay $1.2Bn Restitution & $100MM Penalty

Submitted by Tyler Durden on 11/18/2013 12:06 -0500

(special thanks to the cork)

The CFTC has won a consent order against MF Global requiring it to pay $1.212 billion in restitution to customers and a further $100 million civil penalty:

*MF GLOBAL TO PAY $1.2 BLN RESTITUTION, $100M PENALTY

*CFTC:PENALTY TO BE PAID AFTER MF FULLY PAYS CUSTOMERS/CREDITORS

*CFTC:LITIGATION CONTINUES VS CORZINE,O'BRIEN,MF GLOBAL HOLDINGS

*CFTC: MF GLOBAL ADMITS TO ALLEGATIONS OF LIABILITY IN ORDER

The big question is - of course - where is the money coming from?

Full CFTC Statement:

The U.S. Commodity Futures Trading Commission (CFTC) obtained a federal court consent Order against Defendant MF Global Inc. (MF Global) requiring it to pay $1.212 billion in restitution to customers of MF Global to ensure customers recover their losses sustained when MF Global failed in 2011.

The consent Order, entered on November 8, 2013 by U.S. District Court Judge Victor Marrero of the U.S. District Court for the Southern District of New York, also imposes a $100 million civil monetary penalty on MF Global, to be paid after MF Global has fully paid customers and certain other creditors entitled to priority under bankruptcy law. The Trustee for MF Global obtained permission from the bankruptcy court to pay restitution in full to customers to remedy any shortfall with funds of the MF Global general estate.

The consent Order arises out of the CFTC’s complaint, filed on June 27, 2013, charging MF Global and the other Defendants with unlawful use of customer funds (see CFTC Press Release 6626-13, June 27, 2013). In the consent Order, MF Global admits to the allegations pertaining to its liability based on the acts and omissions of its employees as set forth in the consent Order and the Complaint. The CFTC’s litigation continues against the remaining defendants: MF Global Holdings Ltd., Jon S. Corzine, and Edith O’Brien.

Gretchen Lowe, Acting Director of the CFTC’s Division of Enforcement, stated, “Division staff have worked tirelessly to ensure that 100 percent restitution be awarded to satisfy customer losses. The CFTC will continue to ensure that those who violate U.S. commodity laws and regulations designed to protect customer funds will be vigorously prosecuted.”

The CFTC’s Complaint charged MF Global, a registered Futures Commission Merchant (FCM), with violating provisions of the Commodity Exchange Act and CFTC Regulations intended to protect FCM customer funds and requiring diligent supervision by registrants. Specifically, the Complaint charged that during the last week of October 2011, MF Global unlawfully used customer segregated funds to support its own proprietary operations and the operations of its affiliates. In addition to the misuse of customer funds, the Complaint alleged that MF Global

(i) unlawfully failed to notify the CFTC immediately when it knew or should have known of the deficiencies in its customer accounts,

(ii) made false statements in reports it filed with the CFTC that failed to show the deficits in the customer accounts,

(iii) used customer funds for impermissible investments in securities that were not considered readily marketable or highly liquid in violation of CFTC regulation, and

(iv) failed to diligently supervise the handling of commodity interest accounts carried by MF Global and the activities of its partners, officers, employees, and agents.

end

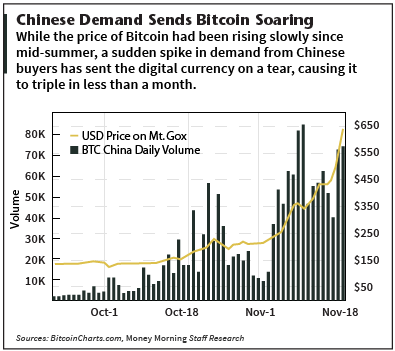

Why Bitcoin Prices Are Rising So Quickly – And Will Keep Going

By DAVID ZEILER, Associate Editor,

Money Morning November 18, 2013

[Update: The positive comments about Bitcoin from numerous federal officials at Monday's Senate hearing, in addition to a letter from Fed Chairman Ben Bernanke to the Homeland Security Committee saying that Bitcoins "may hold long-term promise," caused the digital currency to spike briefly to $900 Monday evening. As of Tuesday morning, however, Bitcoin prices on Mt. Gox had settled back to about $650.]

Anyone wondering why Bitcoin prices are rising need look no further than China.

Since the beginning of November, a massive spike in Chinese buying of the digital currency has almost single-handedly caused Bitcoin prices to triple.

When you look at the numbers, it's almost surreal.

At the start of November, one Bitcoin was worth about $213 on Japan-based Mt. Gox, the world's second-largest Bitcoin exchange. Today (Monday) one Bitcoin traded as high as $675.

Volume on BTC China, where Chinese yuan can be exchanged for Bitcoins, has risen 10-fold in just over a month. Volume jumped from 2,000 to 5,000 Bitcoins traded per day as recently as September to 40,000 to 60,000 Bitcoins traded per day in the past few weeks.

The spike has made BTC China the world's largest Bitcoin exchange by volume, surpassing Mt. Gox, which allows Bitcoin trades in U.S. dollars, euros, and more than a dozen other world currencies.

The sudden surge in Chinese interest in Bitcoin - mostly as buyers - is the primary reason why Bitcoin prices are rising so rapidly.

With the total number of Bitcoins in existence having just crossed the 12 million mark, that means the total value of the currency has soared from about $2.5 billion to about $8 billion in less than three weeks.

While some have dismissed Bitcoin as a fad, the virtual currency has slowly gained traction since its inception by an anonymous creator named Satoshi Nakamoto in 2008.

In the past couple of years, more and more businesses around the world, particularly in Europe, have begun to accept Bitcoin as a form of payment.

In fact, one of the events that triggered Chinese interest in Bitcoin was in late October when Baidu Inc. (Nasdaq ADR: BIDU), a search engine company even more dominant in China than Google Inc. (Nasdaq: GOOG) is in the United States, announced it would take Bitcoin.

But it was a much more dramatic development that sent Chinese in far larger numbers to the BTC China exchange...

Why Bitcoin Prices Are Rising in China

In a very rare move, the Chinese government seems to be actually encouraging its citizens to invest in Bitcoin.

This is one of the most glaring oddities about the popularity of Bitcoin in China, as the Chinese government is not known for allowing rogue economic activity that it cannot control. But the government has done nothing to curb the Bitcoin craze.

In fact, shortly after Baidu made its October announcement, the official state television network CCTV broadcast an extremely favorable 30-minute documentary on the digital currency. And it's probably not a coincidence that the People's Daily newspaper published a positive story on Bitcoin at about the same time.

It's possible that Beijing sees Bitcoin - an international online currency beyond the control of any central bank - as a way to indirectly poke a few holes in the dominance of the U.S. dollar.

"China realizes that the yuan has to clear a lot of hurdles before it can become a reserve currency. If people start using and holding more Bitcoins in place of the dollar, it would likely lead to a less U.S.-centric global economy and that's what China wants," Kyle Drake, founder of CoinPunk, an open-source hybrid web wallet, told CNBC.

Regardless of Beijing's motives, the double-barreled stamp of approval from the Chinese government sent the populace scurrying to buy as much Bitcoin as they could.

But that still leaves the question: Why? What do the Chinese love about Bitcoin?

The short answer is that it fills several needs.

"The main reason why Bitcoin has become big in China is because Chinese people are savers, and more people are seeing Bitcoin as a way to store and invest their money," Linke Yang, vice president of BTC China, told Agence France-Presse at a recent conference in Singapore.

One big problem that Bitcoin solves for the Chinese upper-middle class is that the Beijing government has made it difficult to move yuan outside of the country - Bitcoin can be transferred anywhere in the world with the click of a mouse.

Finally, much of the new wealth in China has almost no place else to go.

"Traditionally, high net-worth individuals and investors first go to the property market to invest and then the stock market, but since the property market is capped and controlled and stocks maybe aren't doing so well that's changing," Yang said.

While Bitcoin prices almost surely will not continue shooting up at the pace of the last few weeks, any correction will be mitigated by the keen interest of Chinese investors.

"The sky's the limit in some sense," Bobby Lee, a co-founder of BTC China, told TechCrunch. "The price eventually will settle down when there's a good balance between supply and demand, but clearly as more people are learning about Bitcoin, all that means is more people are becoming aware of it - and as they become aware they become comfortable buying some Bitcoin. A few hundred dollars or a few dollars. But everything adds to the push-up in price."

Editor's Note: Michael Robinson, Money Morning's Director of Technology Investing, is getting ready to release the most comprehensive Bitcoin guide ever created. This guide covers Bitcoin A to Z. Not only does it give you the full history of Bitcoin and the technologies driving it... it also serves as a step-by-step "how-to" manual for putting into action the best Bitcoin investing opportunities. If you would like to receive this guide for free as soon as it's available, just sign up below. You'll also get Michael Robinson's weekly updates from Strategic Tech Investor where you'll learn about the best technology investing ideas on the planet right now.

http://moneymorning.com/2013/11/18/why-bitcoin-prices-are-rising-so-quickly-and-will-keep-going/

The U.S. Gov't Owes You $1 Million

By Porter Stansberry

Tuesday, November 19, 2013

It's a funny thing about people and lies…

If a lie lasts long enough... and is repeated enough... it becomes a kind of truth. Not a real truth, of course... just a lie that has become accepted and respectable.

That's what's happening right now to the idea of inflation...

Long (and rightfully) seen as the bane of the working man, the inevitable consequence of paper money, and a hidden tax... inflation has suddenly become not only acceptable, but lauded. In fact, central bankers and economic leaders – people who should really know better – are now saying in public that what we really need is more inflation.

Three weeks ago, The New York Times published what I would describe as an ode to inflation. Said the Gray Lady:

There is growing concern inside and outside the Fed that inflation is not rising fast enough. Some economists say more inflation is just what the American economy needs to escape from a half-decade of sluggish growth and high unemployment...

Janet Yellen has long argued that a little inflation is particularly valuable when the economy is weak. Rising prices help companies increase profits; rising wages help borrowers repay debts. Inflation also encourages people and businesses to borrow money and spend it more quickly.

The school board in Anchorage, Alaska, for example, is counting on inflation to keep a lid on teachers' wages. Retailers including Costco and Wal-Mart are hoping for higher inflation to increase profits. The federal government expects inflation to ease the burden of its debts.

People who believe that inflation will lead to an increase in prosperity or our standard of living are simply fools. Cutting more slices out of a pizza doesn't create more pizza.

What inflation does accomplish is shift the dynamics of who wins and loses in our economy. Very simply: People whose income and wealth are manufactured through their asset base become vastly wealthier on a relative basis. People whose wealth is tied to their labor and wages become vastly poorer.

For example, retailers want inflation because it enables them to mark up their goods. And combined with negative real interest rates (like we have now), they can maintain inventories for free (or even to produce a carrying profit). The school board knows that inflation will eat away at the real costs of the wages it must pay. And the federal government – the world's largest debtor – needs both inflation and negative real interest rates to pay for the absurd promises it has made to voters.

In current dollars, based on the net present value of all of its current and future obligations, the federal government owes more than $1 million to every citizen of the United States.

Hopefully, you realize that these promises cannot be kept. What you might not realize is that absent negative real interest rates (driven by inflation), the federal government's current obligations couldn't be financed.

Inflation, unlike what our economic leaders seem to believe, isn't Santa Claus. It can't bring gifts to everyone. All it does is shift the benefits of our economy around. In the immortal words of President OBAMA!... inflation "spreads the wealth around a little."

Inflation penalizes wage earners for the benefit of asset owners. It benefits debtors at the expense of creditors. There's no net increase in the nation's wealth. One group is merely taxed for the benefit of the other. This is sold as a benefit to the country by our government. It has to sell it to us because without inflation it couldn't pay its bills.

Ironically, left-leaning middle-class citizens believe in the benefits of mild inflation most fervently. They are simply bad at math.

Since 1971, when we left the gold standard currency system, wages have stopped tracking gains to productivity. In the past, when innovations would cost some workers their jobs, there was a reciprocal benefit: The real value of wages increased at the same pace as productivity. Thus, they could be nearly assured higher wages in their next position.

The fact that wages were tied to productivity through a stable, gold-backed currency was what propelled the middle class to prosperity. And it led to the United States' political dominance.

But as you can see in this chart, based on one originally published by the Economic Policy Institute think tank... when we took the dollar off gold and allowed the central bank to continuously debase the currency, the dollar and the wages paid in the dollar no longer kept pace with inflation. Thus today, when trade or innovation leads to a gain in productivity (and the loss of a job), there is no reciprocal benefit to wages for the middle class. The replacement job is sure to come at a much lower real wage.

It's this gutting of wages that most appeals to corporate America. To the wealthy, inflation provides easy ways of increasing the size of their asset base: All they have to do is borrow money at a negative real rate of interest and buy up productive assets. That's why farm prices have soared, why private-equity funds now control trillions in assets, and why the wealthy now dominate the middle class politically.

There are two good reasons to believe our current love affair with inflation will end badly…

First, real wages have fallen so far and for so long that they are no longer attractive to many workers. The lack of labor participation has become an enormous burden with a record number of healthy Americans no longer working and instead living on taxpayer-funded assistance.

The other, even more powerful reason is that negative real interest rates have enabled our government to borrow truly unbelievable amounts of money. Not only will this eventually lead to a crisis in the U.S. Treasury market (with soaring interest rates), but this chronic borrowing has transformed America from the world's largest creditor nation (with massive income from global investment) into the world's largest debtor nation.

Foreign investors now own $5 trillion more of America's best assets than we own of foreign assets. Generations of Americans will be sending foreigners net investment income, month after month. If these capital flows continue, it won't be long before no one wants to hold a U.S. dollar.

What's the trigger? When will my dark fears about the future of our economy come to fruition? When will the inevitable next crisis strike? No one knows, of course. My "canary in the coal mine" is the dynamic between the price of gold (which represents sound money) and the price of U.S. long-dated Treasury bonds (which represents the global paper money system).

You can track long-dated Treasury bonds (which mature in 20 years or more) by tracking TLT on the stock market. It's an exchange-traded index fund that holds a basket of long-dated U.S. Treasury bonds. Over the last year, it's down by 15%. You can track gold using the SPDR Gold Shares Fund (GLD), which holds gold bullion. Over the last year, gold has corrected significantly (after a massive 12-year bull market) and is down about 25%.

When the market finally realizes that inflation isn't good for the economy... that wages are far too low... and that debts are far too high, you won't want to be holding U.S. long-dated Treasury bonds. I expect within the next few years, we'll see a real panic in Treasury bonds, with annual yields reaching more than 10%. Many investors will flee into gold, as the U.S. dollar will be seen as unstable.

You'll see a dramatic inversion between TLT (which will collapse) and GLD (which will soar). This prediction, by the way, isn't really a prediction at all. It's a trend. Over the last five years, gold has outperformed the long bond by more than 100%.

That tells you all you really need to know about inflation.

Regards,

Porter Stansberry

http://dailywealth.com/2590/the-u-s-gov-t-owes-you-1-million

The U.S. Gov't Owes You $1 Million

By Porter Stansberry

Tuesday, November 19, 2013

It's a funny thing about people and lies…

If a lie lasts long enough... and is repeated enough... it becomes a kind of truth. Not a real truth, of course... just a lie that has become accepted and respectable.

That's what's happening right now to the idea of inflation...

Long (and rightfully) seen as the bane of the working man, the inevitable consequence of paper money, and a hidden tax... inflation has suddenly become not only acceptable, but lauded. In fact, central bankers and economic leaders – people who should really know better – are now saying in public that what we really need is more inflation.

Three weeks ago, The New York Times published what I would describe as an ode to inflation. Said the Gray Lady:

There is growing concern inside and outside the Fed that inflation is not rising fast enough. Some economists say more inflation is just what the American economy needs to escape from a half-decade of sluggish growth and high unemployment...

Janet Yellen has long argued that a little inflation is particularly valuable when the economy is weak. Rising prices help companies increase profits; rising wages help borrowers repay debts. Inflation also encourages people and businesses to borrow money and spend it more quickly.

The school board in Anchorage, Alaska, for example, is counting on inflation to keep a lid on teachers' wages. Retailers including Costco and Wal-Mart are hoping for higher inflation to increase profits. The federal government expects inflation to ease the burden of its debts.

People who believe that inflation will lead to an increase in prosperity or our standard of living are simply fools. Cutting more slices out of a pizza doesn't create more pizza.

What inflation does accomplish is shift the dynamics of who wins and loses in our economy. Very simply: People whose income and wealth are manufactured through their asset base become vastly wealthier on a relative basis. People whose wealth is tied to their labor and wages become vastly poorer.

For example, retailers want inflation because it enables them to mark up their goods. And combined with negative real interest rates (like we have now), they can maintain inventories for free (or even to produce a carrying profit). The school board knows that inflation will eat away at the real costs of the wages it must pay. And the federal government – the world's largest debtor – needs both inflation and negative real interest rates to pay for the absurd promises it has made to voters.

In current dollars, based on the net present value of all of its current and future obligations, the federal government owes more than $1 million to every citizen of the United States.

Hopefully, you realize that these promises cannot be kept. What you might not realize is that absent negative real interest rates (driven by inflation), the federal government's current obligations couldn't be financed.

Inflation, unlike what our economic leaders seem to believe, isn't Santa Claus. It can't bring gifts to everyone. All it does is shift the benefits of our economy around. In the immortal words of President OBAMA!... inflation "spreads the wealth around a little."

Inflation penalizes wage earners for the benefit of asset owners. It benefits debtors at the expense of creditors. There's no net increase in the nation's wealth. One group is merely taxed for the benefit of the other. This is sold as a benefit to the country by our government. It has to sell it to us because without inflation it couldn't pay its bills.

Ironically, left-leaning middle-class citizens believe in the benefits of mild inflation most fervently. They are simply bad at math.