News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

GermanCol

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

More than 3 years and no sells, I'm an investor, not a flipper and my opinion of the company hasn't changed, so that's why I haven't sold. No problem if you believe me or not and if you think the value of my DD is "exposed". By the way, the DD is not in the chart but you can think it is. Have a good day.

Coachshot, buys are timed by VRUS, not by White Lion. also VRUS has the right and White Lion the obligation to execute:

Section 2.1 PURCHASE NOTICES. Upon the terms and conditions set forth herein (including, without limitation, the provisions of Article VII), the Company shall have the right, but not the obligation, to direct the Investor, by its delivery to the Investor of a Purchase Notice from time to time, to purchase Purchase Notice Shares provided that the amount of Purchase Notice Shares shall not exceed 250% of the Average Daily Trading Volume or the Beneficial Ownership Limitation set forth in Section 7.2(g)

Section 7.1 CONDITIONS PRECEDENT TO THE RIGHT OF THE COMPANY TO ISSUE AND SELL PURCHASE NOTICE SHARES.

Section 7.2 CONDITIONS PRECEDENT TO THE OBLIGATION OF INVESTOR TO PURCHASE PURCHASE NOTICE SHARES.

Everyone is free to expect whatever. As a long for more than 3 years that have done extensive due diligence, I expect the opposite, based on facts I exposed and proved in several posts. It would be reasonable to expect minimum or zero share-issuance at this level and all or the majority of issuance at much higher levels. Time will tell what happens.

Regarding the following affirmation, please provide us with evidence of that. And please, no private messages, all public.

LONGs are suddenly expecting these VRUS leopards to change their spots

ONCE AGAIN ..IT DOESN'T MATTER THE POINT HERE IS IT'S A MEGA DILUTION

AS vrus scam will SOON goes to triple zero, they will need to increase the OS.

Beneficial ownership is determined in accordance with the rules of the SEC. The selling stockholder’s percentage of ownership of our outstanding shares in the table below is based upon 2,290,449,898 shares of Common Stock outstanding as of June 5, 2019.

As of June 15, 2020 there were 2,593,435,051 shares of the issuer’s common stock, $0.000001 par value per share, issued.

Section 4.3 CAPITALIZATION. As of the date hereof, the authorized capital stock of the Company consists of 7,500,000,000 shares of Common Stock, par value of $0.000001 per share, of which approximately 2,594,000,000 shares of Common Stock are issued and outstanding.

I looked at the terms and analyzed them in detail as shown below:

https://investorshub.advfn.com/boards/read_msg.aspx?message_id=156918633

Please enlighten us and save us. Show us why this is a misinterpretation. Why some spend so much time trying to "save" us is beyond me.

Thanks a lot KeepItRealistic, excellent point. Agree 100%.

Actually, toxic or not toxic is very relevant. Since the discount on the shares is only 5%, there is no debt, so there is no interest, as consequence obviously there is no default interest (that normaly is double digit) and finally there is explicit prohibition to the investor or any related party to short, the ONLY way for the investor to have a real benefit is by the effect of higher share price times increase in share price. Otherwise is peanuts. The company has the RIGHT to use this financing or not and the investor has the OBLIGATION if the company wants to use it.

Toxic finance on the other hand has huge discounts (around 50% to 60%) and tipically double digit interest rates, so there is where lenders make the money. That's why they start to dump shares as soon as they can and also because they know that as they dump, the share price starts to collapse and they lose their benefit or part of it if they wait.

Please share with use the link or evidence thaty OS is going to increase. Now that the company has put to rest the RS false rumors looks like the new lie is that OS is going to increase.

I updated my analysis with the 4.9% of O/S limitation adjustment. Fortunatelly that doesn't change at all my opinion of this deal being excellent and much better than Andrew Garnock's.

Following is the link to the post with the analysis:

https://investorshub.advfn.com/boards/read_msg.aspx?message_id=156918633

You wrote:

Your notion that they would benefit by waiting until the price was much higher to buy shares is wrong. They should want to take this share price to the cleaners as many times as possible. I’d be shocked if they weren’t already trying to seal the deal on the initial purchase agreement so they can lock in .0018 and start selling ASAP.

I updated my analysis with the 4.9% of O/S limitation adjustment. Fortunatelly that doesn't change at all my opinion of this deal being excellent and much better than Andrew Garnock's.

Following is the link to the post with the analysis:

https://investorshub.advfn.com/boards/read_msg.aspx?message_id=156918633

Also, this is not toxic at all. It doesn't even involve debt or preferred shares, doesn't have interest and is not unlimited at all. Just google "toxic financing" and you will find the following from trustable sources like investopedia and others:

What is a Toxic Funding

A toxic financing is convertible debt or preferred stock that allows the financier, the holder of the debt or preferred shares, to essentially receive an unlimited number of free trading common shares when they convert their debt or preferred shares to common stock.

What Is Toxic Debt?

Toxic debt refers to loans and other types of debt that have a low chance of being repaid with interest. Toxic debt is toxic to the person or institution that lent the money and should be receiving the payments with interest. Toxic debt generally exhibits one of the following criteria:

Default rates for the particular type of debt are in the double digits

More debt is accumulated than what can comfortably be paid back by the debtor

The interest rates of the obligation are subject to discretionary changes

Any debt could potentially be considered toxic if it imposes harm onto the financial position of the holder.

Following is my updated analysis of the new agreement reached with White Lion. I think some people don’t understand the great deal it is for VRUS. I also want to share why I think this is a much better deal for the company and shareholders than Andrew Garnock’s. The following table summarizes the differences and all without exception are advantages of the new White Lion deal vs. Andrew Garnock’s.

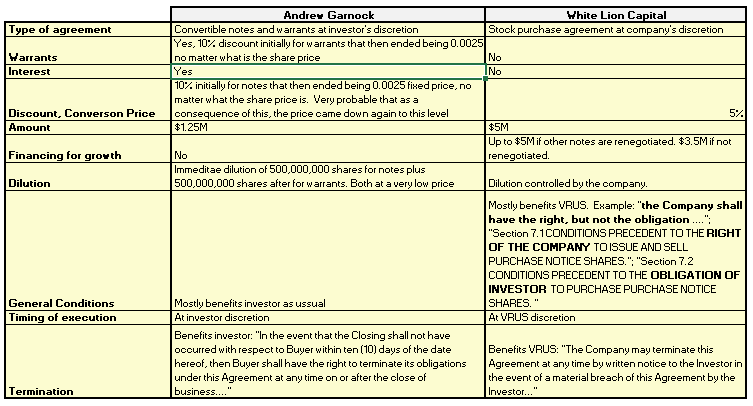

On the other hand, as shown below, last year the price started to increase and multiplied by around 20 times in 6 months when the new notes and warrants to replace the previous notes were announced:

I think the story is going to repeat and now with a much higher price increase than 20 times, because the company has a much bigger business (when previous agreement was done, the company only had the GCC business) and much higher Revenue (last Q Revenue $4.647 million during Covid and $6.173 million pre Covid and last Q Revenue reported when previous agreement announced was only $1.371 million). Additionally, now the funding is not only for paying notes but mainly for growth.

Because of not financing for growth through Garnock and Berdon agreements, the company ended having to take the notes that converted. I think Anshu learned from his mistake and now reached an agreement that left money for growth in case he doesn’t get commercial lending soon.

This new financing is a novel system that fully aligns investor and company . Contrary to toxic financing, both parties maximize benefits ONLY if price goes up as I’m going to explain. There is a limitation in the amount of financing of $5M and in the number of shares that the investor can have at any time of 4.9% of outstanding shares.

From company’s point of view, if share price goes up, less shares have to be issued to get the $5M in finance.

From the investor’s point of view, they have a limited number of shares that they can buy at each point in time, that is the smaller between:

- The number of such shares that, when aggregated with all other shares of Common Stock then owned by the Investor, would result in the Investor owning the Beneficial Ownership Limitation of 4.9% of the then outstanding shares

- 250% of the average daily trading volume in the 5 business days previous to the purchase notice.

So, the way to maximize the benefit for the investor is if they buy not at this share prices but much higher and with higher percentage increase in price.

Examples using just a 50% increase in price;

100,000,000 shares X 0.003 x 50% increase= $150,000

100,000,000 shares X 0.03 x 50% increase = $1,500,000

And if the percentage is more than 50%, benefit for investor will be much higher:

100,000,000 shares X 0.03 x 500% increase = $15,000,000

So, since the discount on the shares is only 5% of the share price, the ONLY way to maximize investor's benefit is by the exponential effect of the combination of two factors: share price times increase in share price. And that makes benefit explode.

Toxic finance discounts on the other hand are huge (around 50% to 60%), so there is where lenders make the money. That's why they start to dump shares as soon as they can and also because they know that as they dump, the share price starts to collapse and they lose their benefit or part of it if they wait.

For both, investor and company is not favorable to execute all the deal at this prices, but higher.

Additionally, as part of the agreement, there are limitations for the investor and for VRUS that represent benefits for shareholders. Examples of these are no dilution permitted for other deals and no short sales allowed, so guess what will happen with OS and share price. Also, as expressed all along the 8-K, White Lion has developed an extensive due diligence to VRUS and found it adequate to sign an agreement by which they have the obligation and the VRUS has the benefit if they want to use it of the $5M funds.

If Anshu can negotiate the extension of the existing notes supported on this agreement, it would be much better, because he will be able to use all of the $5M for growth and also he will be able to use it at much higher share prices.

You don’t have to believe me blindly. I'm a more than 3 years loyal shareholder, so I know what I own. Your own Due Diligence is your best weapon. It's all in the 8-K filing.

You're welcome kingpindg and thanks for bringing this comment of the 4.9% of O/S limitation. I think you are right and there was a misunderstanding from my part on that specific point. As you mentioned, the 4.9% of O/S limitation is not a one time thing.

Fortunatelly that doesn't change at all my opinion of this deal being excellent and much better than Andrew Garnock's.

I will adjust my analysis and post it again.

Thank you for the constructive comment and thanks all the others that posted kind messages regarding this analysis.

Reading comprehension issues? People should know what is the conversation about, before sending randomm comments. Any proof about teens soon prediction? I wiill patiently wait as I will patiently wait for share price correction. I don't know where the price will be soon, I just know I'm an investor and have total confidence here in VRUS and that is why spend time here. Not sure what are the motives for others.

I'm still waiting for the proof. Refute the facts in my analysis with facts.

Prove what you are saying and show us your analysis as I did.

Wow. Just, wow. Taking another crappy dilutive garbage loan and making it seem somewhat palatable. Bravo. *hand clap*

This world is in decline....

Thanks KeepItRealistic, agree 100%.

Welcome Porteño, great to see you back. Good luck!!!

I recommend everyone read thru the details of latest financing, not the A-Team's PR announcing it:

https://www.otcmarkets.com/filing/html?id=14257168&guid=H6VFUKubDWbxTyh

I think most of people don’t understand the greatness of this new White Lion financial deal. I want to share my analysis about it after reading in detail the corresponding 8-K. Also I want to share why I think this is a much better deal for the company and shareholders than Andrew Garnock’s. The following table summarizes the differences and all without exception are advantages of the new White Lio deal vs. Andrew Garnock’s.

On the other hand, as shown below, last year the price started to increase and multiplied by around 20 times in 6 months when the new notes and warrants to replace the previous notes were announced. Important to notice it was not announced that Garnock and Berdon were the notes and warrants holders, that was publicly known later:

I think the story is going to repeat and now with a much higher price increase than 20 times, because the company has a much bigger business (when previous agreement was done, the company only had the GCC business) and much higher Revenue (last Q Revenue $4.647 million during Covid and $6.173 million pre covid and last Q Revenue reported when previous agreement announced was only $1.371 million). Additionally, now the funding is not only for paying notes but mainly for growth.

Because of not financing for growth through Garnock and Berdon agreements, the company ended having to take the notes that converted. I think Anshu learned from his mistake and now reached an agreement that left money for growth in case he doesn’t get comercial lending soon.

This new financing is a novel system that fully aligns investor and company . Contrary to toxic financing, both parties maximize benefits ONLY if price goes up as I’m going to explain. There is a limitation in the amount of financing of $5M and in the number of shares that the investor can buy of 4.9% of outstanding shates, that corresponds to 133,625,991 as shown below:

New OS if White Lion buys all shares: 2,593,435,051 / (1 – 4.9%) =2,727,,061,042

Maximum number of shares for White Lion: 2,727,,061,042 * 4.9% = 133,625,991

From company’s point of view, the ONLY way to get the $5M in finance is if share price goes up, because at the prices we have now, it would only receive $400,878 of the $5M (133,625,991 shares X 0.003 = $400,878).

From the investor’s point of view, since they have a limited number of shares that they can buy, the ONLY way to maximize the benefit is if they buy not at this share prices but much higher and with higher percentage increase in price.

Examples using just a 50% increase in price;

133,625,991 shares X 0.003 x 50% increase= $200,439

133,625,991 shares X 0.03 x 50% increase = $2,004,390

And if the percentage is more than 50% benefit for investor will be much higher;

133,625,991 shares X 0.03 x 500% increase = $20,043,899

For both, investor and company is not favorable to execute all the deal at this pirces, but higher. All this is shown with the following calculation:

Average price:

5,000,000 / 133,625,991 = 0.03742

This is more than ten times the price we have now. So max conversion price is expected to be much higher than 0.03742.

.

No more dilution from others permitted according to terms of the agreement, so guess what will happen with OS.

If Anshu can negotiate new notes supported in this agreement would be much better because he will be able to use more of the $5M for growth and then he will be able to use it at much higher share prices with all the benefits yhat will bring.

The due diligence done by the investor and the limitations for any additional limitation also favors us as shareholders. No short sales

You don’t have to believe me blindly. My advantage, more than 3 years as a shareholder, so I know what I own. Your own Due Diligence is your best weapon.

Excellent deal in my opinion!! I wish I had more $ to add at this price. Have been a shareholder for more than 3 years. Congratulations!!

Hey Backstabbed, as usual, they come without facts!!! VRUS will prevail.

Cheers!!

Coachshot99 and for information of anybody interested, you don't have to be worried if Anshu does with VRUS what he did with XDSL. His warrants exercise price was adjusted post split like what happened with any shareholder shares and that is why his exercise price is so high now:

From 10Q filed on Feb 20, 2019 (pre-split):

Earned Warrants - Mr. Bhatnagar shall be entitled to receive warrants to acquire 4% of the outstanding fully diluted common stock of the Company (the

“Earned Warrants”) each time the Company’s revenue increases by $1,000,000. The exercise price of the Earned Warrants shall be equal to .0001/share

and the executive may not receive shares whereby Signing Shares and Earned Warrants exceed 80% of the fully diluted common stock of the Company

(“Warrant Cap”).

Earned Warrants - Mr. Bhatnagar shall be entitled to receive warrants to acquire 4% of the outstanding fully diluted common stock of the Company (the “Earned

Warrants”) each time the Company’s revenue increases by $1,000,000. The exercise price of the Earned Warrants shall be equal to $.50/share (adjusted for the

reverse split) and he may not receive shares whereby Signing Shares and Earned Warrants exceed 80% of the fully diluted common stock of the Company

(“Warrant Cap”).

Thanks shots60, the same goes to you. Please keep safe and strong holding your shares!! I think we will be handsomely rewarded.

Sorry Crozz to know you are leaving. You are one of the best posters here in my opinion. I'm loosing a lot of $ in this moment (in the paper because I'm not selling), but I have confidence in what is coming because of my more than 3 year ownership and DD, so I will keep my investment. I think it will be in the positive soon and will end up being very profitable. Actually after reading the last PR and 8-K, I think what was achieved was a great financial deal, much better than Andrew Garnock's deal last year. I will post my thoughts about it and why I think it's much better. I'm preparing it with facts. I really respect you, eventhough I don't agree with your last posts. Best of luck to you and keep safe!!

Thanks BBD for sharing!! Excellent email. I'm one of the longs that continues beleiving in VRUS. I really found last PR and 8-K very positive.

Excellent post Majk76, agree with you. I know what I own with more than 3 years as a VRUS shareholder.

Excellent post uksausage. Agree 100%. I'm also happy to stay in VRUS after more than 3 years. I'm an investor and not a day by day flipper. I feel bad for the ones selling scared by all the lies being spread on this board.

Excellent point DewmBoom

As a small fish, it is best to focus the DD on the business and not the stock movement.

Hahaha, not even you believe what you are saying. Anyone can look at the thread and see who is supporting his statements. Not answer as expected

No answers / evidence from you as I was expecting.

Right, 100% agreed. Our time is coming. Thanks to you my friend!! Have a great night too.

I'll do it after you answer my questions and give me the corresponding evidence.

No I don't have my answer / evidence / links, but really I'm not expecting them. I'm sure I will not get them. As with the previous posts, what you are saying now is not true.

Agreed, I'm still waiting the answer and will keep waiting. Thanks shots60 for your support!!

I never said you said they would not ever produce any masks.

And if you are trying to say that having that company in the links producing 2M masks per month means TAM will not produce for Philipines or outside Philipines what they are saying, now give me evidence about that please.

Besides the links to Ihub posts, you provided off topic links as I mentioned. And if you are trying to say that having that company in the links producing 2M masks per month means TAM will not produce for Philipines or outside Philipines what they are saying, now give me evidence about that please.

Still waiting. Links to Ihub Posts and off topic? Really? Lets close the topic we are talking about and then move to others if you want.

The same to you, shots60. Thanks for all the great things you bring here.

I'm waitng for the links or evidence for what was mentioned in your previous post. And now also for what you mention about VRUS being a pump and dump.

Here is a link for defamation crime in case you want to check it:

https://en.wikipedia.org/wiki/Defamation

Please share with us the links or evidence of what you are saying as I did with my links to 2017 agreement and the adjustment to reduce Anshu's participation in the company. I will be patiently waiting. By the way, public defaming is illegal.