News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

dr_airtime

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Andy Homes Latest on Zinc.

Zinc up +$.05 since article and all this action and uptrend since June still intact per the second link.

https://www.reuters.com/article/us-zinc-tightness-ahome/zincs-bull-narrative-blurred-by-fog-of-lme-spreads-war-andy-home-idUSKBN1CO0PL

http://www.kitcometals.com/charts/zinc_historical_large.html#6months

ASND.TO

I haven't but am interested. It had a huge speculative run-up so next phase up would have to be driver by a successful turn around but I'm very interested now. Here is an article just released

http://motherlodetv.net/index.php/2017/10/26/ascendant-resources-turning-around-a-honduras-zinc-lead-silver-mine/

USA.TO - Sinaloa state....

...so the only thing to worry about for USA is that it is in Sinaloa state which is run by the Sinaloa cartel. They robbed Mcewen mining but there is no risk of them stealing a zinc-lead-silver concentrate likely getting shipped up to Teck's zinc smelter in Trail, BC (they like PM-heavy zinc & lead concentrates).

http://www.insightcrime.org/news-briefs/mining-company-admits-relationship-mexico-organized-crime

The Sinaloa Cartel is probably on defense now that the CJNG is recognized as the richest cartel in the world.

Project Huskies...

...I am working on a transaction in Washington state so in honour (note the Canadian/British spelling:) ) of Bob's team I am calling it 'Project Huskies'.

Kozuh - thanks as always for the junior energy microcaps ideas :)

MND.TO - SA case for doubke

https://seekingalpha.com/article/4112283-mandalay-resources-misfortune-grows-opportunity

USA.TO/USAS - I think $7 possible by December

Americas having a nice run-up again. If zinc keeps going up for next couple months (likely) and Americas announces a successful San Rafael start-up, when/if USA goes past $6.00, roughly $6.80 is the next "technical target" where there is a huge gap dating back to 2012. The share count was much, much smaller back in 2012, so this is technical only, but a logical place to keep in mind for next round of trading profits.

FYI - this is the only time this Canadian has been cheering "USA, USA!"

Updates on two new(ish) zinc explorers...

..Tinka TK.V has a CAD 120M MC and 18.8 MT of inferred 8% Zn-Eq resources that are about 70% zinc by metals content. This is before their huge 2017 South Ayawilca discovery. Tinka is a buy here. This post is about two other explorers though. Tinka is a comp.

Canada Zinc Metals CZX.V has 28MT of Indicated and inferred 9% Zn-Eq resources at that are about 85% zinc by metals content. This is their Cardiac Creek Deposit. CAD 53M MC or half that of Tinka. CZX.V has released some of the best holes yet on Cardiac Creek:

http://www.canadazincmetals.com/news/2017/index.php?&content_id=267

CZX.V is 30% owned by Chinese Tongling Nonferrous Metals who is one of of biggest smelters in the world. For comparison, Sewlyn mines north in the Yukon was bought out by a Korean smelter. Cardiac Creek is in BC.

In addition both Teck and Korea Zinc are earning in to CZX.V's other properties - CZX.V has three potential suitors. 28MT @ 9% Zn-Eq is a world class resource so I think CZK is a good speculation here anyways.

Anyone looked closer?

Presentation:

http://www.canadazincmetals.com/_resources/presentations/CZX-Corp-Pres-Sept-2017.pdf

Canadian Zinc CZN.TO - different company. Has former producing Prarie Creek Mine and just announced a feasibiltiy study with the results speaking for themselves. 8MT LOM at 9% zinc plus 9% lead or 18% Zn+Pb. This is nice and high grade.

http://www.canadianzinc.com/images/Docs/News_Releases/CZNNR20170928.pdf

NPV is miles above market cap but they would have to finance it. They ran feasiblity study at $1.10 zinc though.

Also - the upgrade of the winter road to all season has been approved by the local authority, but I believe they still need the provincial regulatory approval. This is in order to power this remote mine by LNG instead of Diesel.

http://www.canadianzinc.com/images/Docs/News_Releases/CZNNR20170912.pdf

Long Zinc Miners? Teck's slides **must read!**

If you're long zinc you **Must Read** Teck's latest zinc slides 31 to 41 below.

$2.00/lb is in the cards easy for 2018. LME stocks getting close to exhausted and per slide 40, most of these stocks are from 2008-2010 in New Orleans and customers have concerns about the build up of rust. This is not premium product. Effective stocks for consumption may actually be lower.

I'm going to to re-allocate more acapital to zinc stocks this week after reading this!

http://www.teck.com/investors/presentations-webcasts/teck-s-vancouver-and-red-dog-site-visit-

ROE.V - THE oil play on Mexico?

Per my last two posts. Here are my notes from subscriber summit. ROE.V is betting big on Mexico and were the largest successful bidder in the first Mexico onshore oil block auction. Mexico is undergoing a hige change of course liberaliIng their entire energy sector from electrical generation, transmisson, distribution to oil and natural gas production to midstream. ROE.V is a way tonplay the production side. These are my notes. I have never looked at company before somI have nonidea about capital structure and balance sheet. Reply to this tbread with comments. 10 minute CFO presentation:

ROE Renaissance Oil

- Mexico state oil production peaked at 3.5M boepd 10 years ago. 2M boepd now

- Pemex focused offshore and neglected onshore historically

- 160 on-shore farmouts to come in next few years

- 200 blocks designated for auction in next 5 years

- 2015 ROE.V locked up 3 of best properties including almost half of OOIP in auction, most of production too. Leaped into being largest independent producer in country at 1600 boepd after auction. This is small.

- LucOil partnership hopefully sitting in middle of next big shake play.

- Starting to recomplete and do workovers this month. Low hanging fruit

- Will start to lay first pads in Nov and Dec for 'transformational' wells into their shale play.

- Ian Telfer is biggest backer. Founded goldcorp as a mexican focused miner

- Amatitlan could be shale sweet spot. ROE is operator but partnered with LucOil

- Upper Jurrasic shale 3X thicker than US. They think big potential of courae.

- Need to drill first horizontal in Mexico.

- 1550 boepd from Chiapis. Think they can double or triple production in next few years here. Pretty easy. No modern optimization or workovers

PNO.V Pentanova notes from CFO presentaion today...

...at Keith Schaefer O&G subscriber summit:

Pentanova

- have offices in Bogota, argentina manager lives in BA. All senor mgmt lives in Bogota

- 2P $200M value of first drilling target in Colombia

- Argentina needs heavy oil to optimize refineries

- Sarafino-Giustra play. Petrominerales 2.0

- Will move rig to Colombia in November

- Disxovery well 18Mmcfs by texaco but suspended in 1980 on their Colombia property

- Target is production by july 2018 at 26MMCFD

- Looking for 30-40% reserve increase at Colombia in next 6 months

- Right next to Canacol's land in Colombia

- Ecopetrol suspended another well at 10MMCFD in 1980s on Colombia package

- Llamcanello argentina heavy oil. 1400bopd current production. Pipeline goes to stranded refinery that needs heavy oil. 100 wells drilled, 33 on production. No other low hanging fruit heavy oil properties like this globally. That is because Argentina is a basket case though

CNE.TO - time to buy old favourite...

...attended the Keith Schaefer O&G subscriber summit today. Canacol CFO presented for 10 mins. New pipeline capacity slates to be commissioned on Dec 1, 2017. This shohld be a catalyst for a 30-50% share price run IMO. After that there is another 90MMCFD slated to come on through a third pipeline expansion in 2019. When this is complete Canacol will generate USD 300M/year in EBITDA. EV is 840M if I remember from presentation. Debt will be reduced. 2-3 year double potential from here IMO. Not a micrcap anymore but I don't aee anyone else posting!!

- 90MMcFD pipeline capacity currently, wells can do 200MMCFD

- Chevron historical coastal gas discoveries dropping from 477 mmcfd in 2015 to 250mmcfd in 2020

- 2TCF of unrisked exploration resources - Gaffney Cline

- $4/Bbl netback

- Gas has only a 10% decline rate. Only need to drill 2 wells/year @ US 7.5M/well to offset decline

MND.TO - $CAD 150 MC here is Denver Summary:

From Denver Gold Show webcast. Mandalay now one of cheapest +100k/year Au-equivalent producers based on producing Bjorkdal and Costerfield mines.

I think Mandalay will stay down here in low-30's until it is announced that Cerro Bayo is reopened and then it will jump 20% higher in a day IMO when mine opening announced. Per the CEO's comments though we have throug October and a lot of November until we hear about mine reopening. It was not a mine collapse but a "lake inundation". Mining definitely would have contributed but it was not the portal that collapsed.

Cerro Bayo Lake Shore Collapse

- did not lose any reserves from lake edge collapse. Vein that collapsed within weeks of being mined out.

- 3rd party engineering company conducing root case assessment

- on track to complete risk assessment for mine restart by end of October

- Need to show risk assessed plan to regulator to reopen. this will be submitted in early November.

- 8 permits between 4 veins for LOM plan. Permits for mining and waste dumps.

- Drilled 25 geotech holes around existing mines

- announcement for reopening likely to be guided in November. Sounds like December at the earliest.

Bjorkdal

- Bjorkdal turn around complete, but they have not even initiated the optical sorting yet, so there is more processing upside.

- Expect to announce +150k oz of P&P reserve increase, net of depletion later this year. 3+ year mine life extension.

- Bjorkdal will produce 55-60k Au-ounces per year at $700 cash costs (not AISC) going forward

USA.TO/USAS - nice update on San Rafael

Things going to plan. Remember that zinc and lead are in bull markets and USA.TO gets a substantial portion of their revenues from BOTH San Rafael and Galena (Idaho) from Zinc and Lead

http://www.americassilvercorp.com/i/pdf/nr/nr20171003.pdf

If you haven't followed lead the chart is not dead weight! Check out this page.

http://www.kitcometals.com/charts/lead_historical_large.html

Reminder: I sold 50% of my USA at ~5.75 and bought all that back at ~5.10 so I have more $$ than ever in this position.

GSC.TO/GSS Hold Thesis

See 15:00 in the now-available Denver Presentation. Hoisting and Processing capacity is double the feasibility mining rates so this foreshadows Golden Star's ability to increase production should they discover more reserves.

The only thing prior to the 15:00 mark that is important is that Prestea has produced 9M ounces over 100 years and there are "very few ore bodies that have produced that over such a short strike length". Feasiblity mining rates are 6500 TPD and they can hoise 1500 TPD.

The production growth GSC.TO (25% to 2019) looks attainable.

http://www.denvergoldforum.org/dgf17/company-webcast/GSS:US/

Two new buys - 60%/25% production growth through 2019...

...with that 60% growth coming from new mines that are almost operational.

Nothing to bet the farm on here. But both of these gold producers have CAD 400M market caps and are guiding for 60% production growth for 2019 (relative to 2017 production). The small producer space is dwindling and I think these should be good holds through gold's typically strong fall.

AR.TO Argonaut Gold

- 60% production growth coming from producing El Castillo/San Agustin complex. All the growth is coming from the new San Agustin pit close to producing El castillo mine. They have already announced the first gold pour. San Agustin does not have a feasibility I believe so commerical production cannot be announced with 43-101 regulation.

http://www.argonautgold.com/news_events/news/news_release/index.php?&content_id=353

- Argonaut has 2M M&I heap leachable pit-constrained resources (not reserves) between El Castilo, San Agustin and La Colorada mines. See page 25 of presentation which reflects the updated M&I ounces they announced in latest press release from Sept 21st.

http://www.argonautgold.com/_resources/presentations/corporate-presentation-Sept-2017.pdf

GSC.TO/GSS Golden Star

- Will technically have 60% growth from 2016 to 2019, about 25% growth from 2017 to 2019.

- Management has turned around operations and refocused on high grade underground. Is closing the Prestea surface open pits and refocusing on Prestea Underground which has a P&P resource of 1.1MT @ 14 g/t for 500k Au. 5.5 year mine life.

- Recent drilling success shows Prestea's mine life will be longer than 5.5 years.

- Prestea has a 100 year mining history so there will be a longer life. See page 14:

http://s1.q4cdn.com/789791377/files/doc_presentations/2017/08/Jefferies-presentation-Aug-2017-FINAL.PDF

- slides 10 & 11 from Denver shows the Prestea mine plan. I would guess the mined-out areas around the 200m shaft represent the "100 years of prior production".

http://s1.q4cdn.com/789791377/files/doc_presentations/2017/09/Denver-presentation-Sept-2017-FINAL.pdf

- Golden star has recently announced they have started mining the first stop at Prestea underground.

- The open pits will continue to produce through the end of 2017, after which point all of GSC's production will come from Wassa and Prestea Underground.

REG.V - nice hole....

Both holes at 70 degrees with mineralization starting at 170/200m.

Lone Clone - do you know where we can find the drill data for 2012 holes SDH-034 and SDH-037 which were drilled in 2012? These appear to have hit the "heart" of both the volcanic and Skarn mineralization so I'm curious what depth the mineralization starts at. Lower depth always better of course = less pre-strip and better open pit economics.

The 2012 43-101 on the website doesn't have the 2012 holes (only holes before 2012). Maybe you know from a newsletter reference? Information public I just couldn't find it after 10 minutes.

43-101 only goes up to SDH-10 so missing SDH-11+

http://www.regulusresources.com/wp-content/uploads/AntaKori-Technical-Report-Scott-Wilson-Consulting.-July-2-2012.pdf

Thanks!

PNO.V - update

Hello??? Is anyone still on this board? Guess it just Kozuh's entertaining Seattle heckling.

Anyways - here is an update from Laurentian research on SA for Penta Nova.

You may recall he follows Canacol closely too.

the big prize for Penta Nova is the Argentinean Heavy Oil.

https://seekingalpha.com/article/4108789-pentanova-colombia-flawless-execution-long-thesis-confirmed

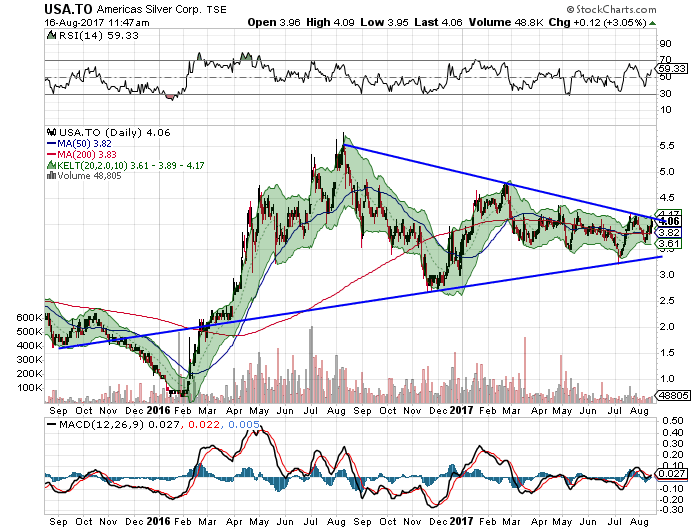

USA.TO - case for a double in 2018

Edge - It'a silver producer...

...so i'll trade in and out of a core position since the sector is so volatile but starts aligned for a nice 2 year hold I think. Whenever the zinc market tops that will put a ceiling on the stock for a while. They will do 7.5M oz in 2018 so they are actually inching towards silver mid-tier status. I guess they officially get this with 2 mines.

EDV.TO has a CAD 375M MC with CAD 60M in cash for 315M EV and will do 8.75M Ag-Eq Oz in 2017 for CAD 36/oz

GPR.TO has a CAD 260M MC with CAD 60M in cash for 200M EV and will do 4.1M Ag-Eq Oz in 2017 for CAD 49/oz

Endeavour is one of the cheapest on an EV/Ag-Eq Oz production basis. This is supported by slide 11 from their presentation below (looks about USD 25-30 ballpark which aligns with my calc in CAD)

http://www.edrsilver.com/_resources/presentations/EDR_presentation_Sept_2017.pdf

**Slide 11 is really important to look at in context of my analysis below**

Endeavour is the cheapest @ CAD 36/Ag-Eq oz.

USA.TO will do 7.5M Ag-Eq oz in 2018 so that equates to an EV of CAD 270M @ CAD 36/Ag-Eq oz.

USA's cash will drop into December as they commission San Rafel. They have a Glencore CAD 20M (USD 15M) prepayment facility which is basically debt so this backs into an implied market cap of CAD 250M at the lowest end of the silver mid-tier producer valuations (**See the slide !!**) With America's low AISC they should trade at a premium to Endeavour. At GPM.TO's CAD 50/Ag-Eq oz that is a CAD 375M EV and CAD 355M MC.

USA.TO's current MC is CAD 195M @ 5.05 (TSX).

The target upside to trade in line with Endeavour is +25%

The target upside to trade in line with Great Panther is +80%

Endeavour and Great Panther are both high-AISC producers. Americas will the one of the the lowest AISC producers in 2018, if not the lowest (this was CEO's claim at Denver). As a result I expect +100% or another double from CAD 5.00 SP on TSX to CAD 10.00 in 2018.

We should get a double easy if silver actually moves higher. I expect Zinc too move up of course. Zinc may top in 2018. It topped in 2006 and then collapsed as fast as it went up. This is important to follow if you invest in USA.TO or EXN.TO. Their near-term fortunes are tied to zinc somewhat.

Sprott is also a big holder here. I think if do get a continuation of the gold bull (silver follows) they could do something here and try to put together Americas with another miner (Excellon, Great Panther, etc.). I'm not sure who their other big positions are. Sprott installed the management team of Americas and merged the former U.S. Silver with Scorpio Mining (Mexican assets) to form the now Americas Silver.

USA.TO - highlights of Denver Presentation

Link won't work unless you go back to PMS conference website but anyways....

http://www.gowebcasting.com/events/precious-metals-summit-conferences-llc/2017/09/19/americas-silver-corporation/play/stream/23114

- claim to be lowest AISC silver producer in world in 2018 (zinc and lead credits here)

- in their P&P + M&A + Inferred resource base they have a billion pounds of led and 700M lbs of zinc in addition to silver (about 80M oz of silver in three categories)

- cash balance will bottom at $6M in November 2017 before increasing once cosala is online

- 60% institutional shareholder base - very high for micro silver. Mix of Canadian and American institutional.

- The $15M glencore pre-payment facility was only at LIBOR + 4.5% back in 2016 - speaks to quality of Cosala (130% unlevered project IRR)

- 27 historic mines @ Cosala - mostly open pits that didn't go underground. They announced great step-out results about a month ago. 4M tons of 200g/t in zone 120. Aiming for 5M tons in M&I category and go straight to pre-feas to bring the next mine on line instead of mining at the end of the life of San Rafael. Minimal capital required here because

- 1.6-2M dollars to expand San Rafael mill which they think they will do in 2018 based on zone 120 exploration success.

- own 100% of properties, no royalties, no streams, no partners.

- On new acquisition the veins they have (5M tons) move onto Penoles ground so they are trying to do a deal here.

- 7.5M oz production in 2017. Potential from a triple here still.

I did ending up selling 50% of my holdings at 5.75 and have bought most of it back now at 5.10. Still have a bit more to buy.

Re: KNT.V Edge83

The CEO left for a lithium explorer. He is still on as a director but this is a bit of a red flag. There are 600 years of Lithium Reserves - more than any other metal so i find it funny the CEO would have left unless K92 was not going to be a smashing success. I sold mine. Curious on your thoughts here.

http://www.k92mining.com/2017/08/k92-appoints-mr-john-lewins-as-chief-executive-officer/

https://www.lsclithium.com/investor-centre/news-releases/press-release-details/2017/LSC-Lithium-Appoints-Ian-Stalker-as-CEO-and-Provides-Exploration-Progress-Update/default.aspx

ORV.TO - copper way down in FY18, not that great...

...once I crunched the numbers below. Applying current spot prices against 2017 and 2018F mid-range production I'm only seeing revenue go up by USD 11M in 2018. Gold production up, copper production down big time. Mostly a nicely presented PR by Orvana.

However, El Valle revenue goes up by $15M. It remains to be seen if this will translate into a significant AISC decrease at El Valle which is where all Orvana's high historical costs have emerged from. Can they focus their mining on higher grade ore? Small position here but the potential is still there for a triple IMO as the market cap is only $36M. If they turn things around $100M is very reasonable.

Spot prices applied against guidance in ORV's latest news release

Here is what I replicated from the news release:

Here is the news release:

http://s2.q4cdn.com/372236871/files/ORV-NR-FY2018-Guidance_FINAL-13092017.pdf

GSC.TO/GSS (NYSE) - here is the turn around story

This is my newest buy. Super small position as digesting the opportunity but this is another turn around story a few years in the making. Going to officially commission the re-development of Africa's highest grade underground mine in Q3, which previously produced 9M oz of gold over the last century. Not an unproven mine.

USD 280M MC but catch is USD 185M of net debt split between cash, the Royal Gold Loan (technically deferred revenue on the BS), a senior royal gold debt facility (19M) and other debt which is mainly convertible debentures. Overhang here is that Royal Gold and the convertible debentures really own the company with the scraps left over for common equity. The next 12 months are "show me" time and if they keep delivering on the turn-around plan the market will get comfortable with GSC's ability to carry the debt. Gold loan no problem.

Link back to my last post for the presentation and look at slides 8. 2018 and 2019 will be around 300,000 oz of production per year around $900 AISC.

Recommend you take 10 minutes and read through this GREAT article that overviews the mines and the turnaround:

http://www.northernminer.com/news/sam-coetzer-breathes-new-life-golden-star/1003786969/

I'm winning...haven't visited board in 2 months!

Just goes to show you how much luck plays into these contests!

USA.TO is up another 20% this week so should be good close.

Need to look into the trading rules - thanks again for hosting Skillz!

PRU.TO things start to get interesting...

...in December 2017. Yaoure FS releases this month, they go into Jan-June 2018 high production period from Edikan, and commission next mne sissingue in March 2018.

All the information on this here. Page 4 has the production increase in H2 of Fiscal 2018. Not all of that increase is from Sissingue.

Perseus could move before that December-start to catalysts.

I don't own any currently.

http://www.perseusmining.com/aurora/assets/user_content/PRU(7).pdf

GSC.TO - another turn around - anyone watching?

After looking for gold miner buy candidates the last week I've spotted the turn around at Golden Star.

Anyone else followed or have an opinion. Got some buy orders in which will force me to look closer if executed?

http://s1.q4cdn.com/789791377/files/doc_presentations/2017/08/Jefferies-presentation-Aug-2017-FINAL.PDF

Summary of presentation above:

5 Straight quarters of production growth and hit $785 AISC in Q2 (slide 6).

Production guided to grow in 2018 and 2019 (slide 8).

Production roughly 50%/50% between Wassa and Prestea Open Pit Oxide Ore.

Wassa is 50% open pit, 50% underground. Wassa underground grade to increase in future years.

Prestea is currently being mined from open pit oxide ore. The mine will transition to underground with COD guided for Q4-17. There is a high grade reserve of 1.1MT @ 14 g/t here for 500k oz.

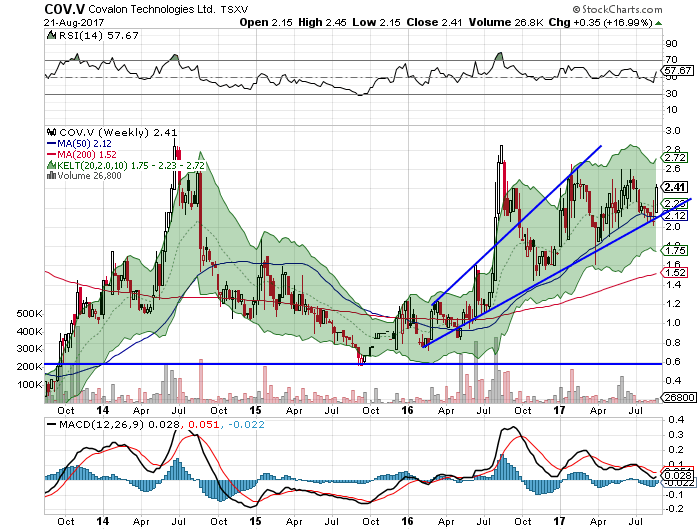

COV.V - my read on today's PR...

....phrased to be super bullish suggesting this is $14M in incremental sales but after digesting it I think there is $7M in incremental sales here as the $14M in sales is guided for Fiscal 2018:

http://ir.covalon.com/phoenix.zhtml?c=183092&p=irol-newsArticle&ID=2298293

Back in 2016 they guided for $7.6M in sales to Saudi Arabia in Fiscal 2017:

http://ir.covalon.com/phoenix.zhtml?c=183092&p=irol-newsArticle_Print&ID=2194399

Good news nonetheless but I think you can't simply add this $14M in sales to Covalon's current run-rate revenue base. The Price/Sales ratio you get then is ridiculous. Things looking great nonetheless. What will rocket Covalon higher is contracts into new markets (e.g. Mexico).

All $ are CAD eh.

USA.TO/USAS - look at EXN.TO too

Didn't expect it to move this fast at all. I'm looking at chart and thinking "I should take some profits" but volume is low and don't want to make mistake I did on Trevali.

I loaded a big position in Trevali at $.60 back in 2016 and then sold most at $.90 because it moved there ridiculously fast. It kept going to $1.20 though non-stop and then consolidated between $1.25 and $1.10 for almost a year, and is still going higher. I should of held to see what the multi-month top was (i.e. $1.25). The only way to tell where the top is to ride it up and then sell on the way down. This is Jesse Livermore-ism.

I think zinc has much more upside and Silver has barely budged so USA.TO could be higher in a month's time. This doesn't mean its not going to go back to $5.00 though first (TSX $5.00, it's trading at $5.40 today).

I also don't think that USA.TO is really on the mainstream's radar as a zinc play.

Take a look at Excellon and chart almost looks identical to USA.TO (gone vertical out of big triangle) so you can keep an eye on both of them. Excellon is super high grade silver + zinc + lead. From EXN.TO's webpage their La Platosa resource is:

M+I RESOURCE OF 428,000 TONNES @ 760 G/T SILVER, 8.28% LEAD AND 9.88% ZINC

Zinc is in a bull market, market is expecting silver to move higher over next couple months and Lead has also been moving higher for last 1.75 years. I'm glad I looked at this because it is the same forces pulling up both USA.TO and EXN.TO.

http://www.kitcometals.com/charts/lead_historical_large.html

Good week though!

USA.TO/USAS - no target price...

...I'll have to figure that one out.

The latest drill hole screams "10 year mine life on San Rafael, not 6 years" so combined with the great turn around of the extremely mature Galena mine by this management team (start mining wider-vein Pb-Zn rich silver veins with lower diluation <$10 AISC), rather than narrow, hard-to-follow high grade silver veins), the direction for USA.TO is up.

We have zinc going higher, and gold/silver having a major breakout today. Silver is also going to help USA.TO

I'll check for any analyst estimates this week.

LC - REG, I'm in....

...read through the two most important PRs in depth and get what you're saying about the blue sky being the discovery of the porphyry centre. Bought some this morning and have more orders in as we speak.

Is it your understanding that the current 43-101 based on only 18,000m of drilling by Southern Legacy is all based on the younger (i.e. a more-recent hydrothermal event) high sulphidation mineralization? I haven't read the 43-101.

Explicitly AK-17-001 intercepted the younger mineralization which was discussed in the mid-August PR.

If CMC is mining the younger mineralization then it looks like the blue sky that REG management sees here is discovery of the porphyry centre and that is what you are alluding to below:

" low sulphidation with mineral aresenic.....order of magnitude larger".

Perhaps since the high-sulphidation younger mineralization has been economic no one has bothered exploring for the older porphyry intrusive centre?

This is from the PR where REG announced their 2017 drill program a few months ago:

Copper-gold sulfide mineralization at AntaKori occurs within skarn and breccias within Cretaceous sedimentary rocks and also as younger epithermal high-sulphidation mineralization in overlying Miocene volcanic rocks that host the adjacent Tantahuatay heap-leach gold mine to the south. The younger high-sulphidation mineralization locally

overprints the earlier skarn mineralization, particularly along the southern extent of the AntaKori system. The skarn and breccia hosted mineralization is likely related to a porphyry copper-gold intrusive center, that is yet to be intersected by drilling, although there are fragments of well-mineralized porphyry locally within some of the

breccias.

Lone - can you give a...

..high level summary of buyout price? $10 would be $CAD 900M MC which seems extremely high considering Nevsun bought Reservoir for $CAD 365M and this was the highest grade copper discovery in years.

It looks like SLP-Regulus is earning in on Colquirummi from CMC (Buenaventura), but this is separate perhaps from AntaKori which is 100% Reguls owns, had the recent drilling results and a NI 43-101 inferred resource of 294M tonnes @ 0.48% copper and 0.36 g/t Au.

I realize Beunaventura may have minimal to-no-capex (circuit optimization if metallurgy different) as Colquirummi and AntaKori are right next to their current mine.

This above is all based on 15 minutes of reading but would appreciate your thoughts. Results like these are usually "buy now and assess in a couple weeks" situations.

This appears to be most important PR setting out the MOU

http://www.marketwired.com/press-release/regulus-resources-announces-agreements-collaborative-exploration-antakori-copper-gold-tsx-venture-reg-2126461.htm

Thanks!

USAS no?

Looks like it already trades no? About the same volume as TSX (37k/day average vs. 34k/day on TSX).

NYSE MKT is simly the old AMEX if I'm not mistaken?

https://www.google.ca/finance?q=TSE%3AUSA&ei=pzufWfj4HtjCeueCpcAI

http://www.americassilvercorp.com/s/NewsReleases.asp?ReportID=775911

USA.TO +7% here we go. Hope everyone on board!

Last Wednesday, USA jumped through the resistance line I kept highlighting and then has been backtesting for the 5 trading days to follow. This news release today with nice step out results on San Rafael (60m @ +300 g/t Au & 0.80% Cu) are suggesting mine life will be longer than initial 6 years in the prefeasibility.

http://www.americassilvercorp.com/i/pdf/nr/nr20170824.pdf

Here's the breakout, backtest and 7% candle from today.

Last 6 months, lead, zinc & copper are all up significantly. We're only waiting on Gold, so Silver will follow out of the summer doldrums.

CDH.TO - more thoughts...

...Old Harry is a wildcard. If Sable Island is really in decline then the forces have to support the lifting of the fracking ban. It looks like Corridor has actually delineated a lot of the Frederick Brook Shale and have some wells in before the fracking ban was perhaps put in place.

1100m gross thickness is pretty insane and I've seen a couple older presentations highlighting how wells are getting super low decline. What if this was a world class shale gas reservoir like the Motney?

Here is a 2015 presentation I dug up from Google. Middle pages outline the wells they have drilled across the Frederick Brook. It looks like the liquids shale layer is so long (1100m) they only need to drill vertical wells but perhaps still frack them vertically to complete them.

https://corridor.ca/wp-content/uploads/2014/05/2015-12-Corporate-Presentation.pdf

Another older presentation I found from 2014:

https://www.scribd.com/document/223288092/Corridor-Resources-Jan-2014-Investor-Presentation

And here is the forces against Old HArry:

http://www.jwnenergy.com/article/2016/8/corridor-resources-faces-uphill-battle-drill-old-harry-offshore-newfoundland/

CDH.TO - potential upside.

See slide 6. This is you long thesis. 100% upside and that still gives zero value to Old Harry offshore prospect or call option if New Brunswick lifts fracking ban.

https://www.corridor.ca/wp-content/uploads/2017/08/Corporate-Presentation-August-2017.pdf

See slides 21-23 for shale horizontal potential if fracking ban is lifted.

COV.V - still same story....

...fundamentals still looking good but majority of value being driven off of single contract in Saudia Arabia. If they can keep growing US sales and add a new key contract in one of other markets they are targeting then direction is very much up for next 12 months. Market will be looking for this.

Jump today was off support line dating back to Early 2016. Good sign. This is a four year chart.

OT: This board's gone quiet.

Hopefully these two Canadian Companies I've featured will 'stoke the coals'

eh!

CDH.TO - a true energy microcap with negative enterprise value!

Value Digger @ SA still one of my two favorite authors over there. Check out this piece on Corridor Resources which has a negative enterprise value at (CAD) $0.64. I bought last week @ $0.62. It closed there today. Ignore the chart as the new floor for CDH is $.60 as the article will explain.

https://seekingalpha.com/article/4094126-value-investors-overlooked-investment-idea-good-true

Thesis here is hold for year for recovery to a more rational valuation. The blue sky potential here is them getting a JV partner that carries them for a deliniation well in next couple years for offshore oil Old Harry prospect and they discover another Hibernia (masssive NFLD offshore field finally going into production now). You get this optionality for free. I have no idea if it has Hibernia potential. It is free anyways. You get the company and their 21 year PDP reserve life for zero.

Because they are a little specialized producer they have a 21 year PDP - I have never seen a reserve life this long! Goes to show you the true valuation for this little company is not a zero enterprise value!

PNO.V - Pacific Rubiales 2.0?

In case you missed it Penta Nova is now being promoted and the same rock-start management team is trying to repeat the Pacific Rubialies story in Argentina, funded off Colombia Gas.

Must read to keep on your radar. If you know Canacol you'll understand the Colombia gas (deficit) story too:

https://oilandgas-investments.com/2017/latest-reports/the-best-growth-story-ever-in-junior-oil/

USA.TO - cancel that. Zinc breaking out.

After that post I just went and bought 3000 more share in various accounts as zinc just leaped upwards to $1.41/lb today past previous high from March 2017. Trevali is +7% right now.

It could be the zinc bull that pulls USA through that upper triangle resistance line. I'm not waiting as market just digesting the zinc move now.

My largest PM position but technicals and fundamentals (zinc breaking out, hoping silver will in September) lined up nicely here. Want to be riding any breakout here.

http://www.kitcometals.com/charts/zinc_historical.html

USA.TO getting close...

...didn't go a couple weeks ago. San Rafael zinc production is the fundamental driver for 2018 but silver price (which follows gold) will likely be what pulls USA up through the resistance and we're getting near the end of the summer doldrums. I'm thinking there is less than a two week window here.