News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

investor15

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Valdor Makes Submission to SEC for Listing on US OTCQB

VANCOUVER, British Columbia, March 26, 2014 (GLOBE NEWSWIRE) — Valdor Technology International Inc. (“Valdor”) (VTI) (VTIFF) is pleased to report that application to the Securities Exchange Commission (SEC) to have Valdor listed on the OTCQB Securities Market in the US is completed and is being filed today.

OTC Markets Inc., located in New York, N.Y., operates the world’s largest electronic interdealer quotation system for broker-dealers to trade over 9,000 securities not listed on any other U.S. stock exchange. It is organized into three tiers based on the level of disclosure: OTCQX, OTCQB and Pink Sheets. When this listing is completed, North American & International investors will be able to find news, current financial disclosure and real-time Level 2 quotes for Valdor on www.otcmarkets.com.

Mr. Brian Findlay, CFO/Director, states: “We want investors throughout the world to have ready access to Valdor stock ownership so we can facilitate stock distribution internationally. Listing on the US OTC Bulletin Board market will greatly help us achieve this objective.”

About Valdor Technology International Inc. (www.valdortech.com): Valdor is a technology company with two divisions: 1) Valdor Fiber Optics, a fiber optic components company specializing in the design, manufacture and sale of fiber optic splitters, connectors, laser pigtails and other optical and optoelectronic components, including some that use the Valdor proprietary and patented Impact MountTM technology. The company specializes in harsh environment products and in particular splitters and connectors and; 2) Niagara Streaming Media, a streaming video business that owns four patents and markets the Niagara and GoStream product lines. Streaming video is the future of television.

The Valdor business plan incorporates growth by acquisition. For further information on Valdor’s product lines please visit www.valdor.com.

Twitter: http://twitter.com/ValdorTechInt

Facebook: http://www.facebook.com/valdortech

ON BEHALF OF THE BOARD OF DIRECTORS OF VALDOR TECHNOLOGY INTERNATIONAL INC.

The TSX Venture Exchange has not reviewed and does not accept responsibility for the adequacy or accuracy of this news release.

Contact:

California Operations

3116 Diablo Avenue

Hayward, CA 94545

Telephone: (510) 293-1212

Fax: (510) 293-9997

Email: info@valdor.com

Canadian Office

450 – 789 W. Pender Street

Vancouver, BC V6C 1H2

Telephone: (604) 687-3775

Fax: (604) 689-7654

Email: bfindlay@valdor.com

Investor Contact:

Stuart T. Smith

SmallCapVoice.Com, Inc.

P. 512-267-2430

F. 512-267-2530

Skype: SmallCapVoice.com

Twitter: @smallcapvoice

www.facebook.com/SmallCapVoice

http://smallcapvoice.com/blog/valdor-makes-submission-to-sec-for-listing-on-us-otcqb/

Big Oil’s Drive for War With Russia

Mar 16, 2014 - 02:46 PM GMT

By: Mike_Whitney

“We are witnessing a huge geopolitical game in which the aim is the destruction of Russia as a geopolitical opponent of the US or of the global financial oligarchy…..The realization of this project is in line with the concept of global domination that is being carried out by the US.”- Vladimir Yakunin, former Russian senior diplomat

“History shows that wherever the U.S. meddles; chaos and misery are soon to follow.”- Kalithea, comments line, Moon of Alabama

Following a 13 year rampage that has reduced large swathes of Central Asia and the Middle East to anarchy and ruin, the US military juggernaut has finally met its match on a small peninsula in southeastern Ukraine that serves as the primary operating base for Russia’s Black Sea Fleet. Crimea is the door through which Washington must pass if it intends to extend its forward-operating bases throughout Eurasia, seize control of vital pipeline corridors and resources, and establish itself as the dominant military/economic power-player in the new century. Unfortunately, for Washington, Moscow has no intention of withdrawing from the Crimea or relinquishing control of its critical military outpost in Sevastopol. That means that the Crimea–which has been invaded by the Cimmerians, Bulgars, Greeks, Scythians, Goths, Huns, Khazars, Ottomans, Turks, Mongols, and Germans–could see another conflagration in the months ahead, perhaps, triggering a Third World War, the collapse of the existing global security structure, and a new world order, albeit quite different from the one imagined by the fantasists at the Council on Foreign Relations and the other far-right think tanks that guide US foreign policy and who are responsible for the present crisis.

How Washington conducts itself in this new conflict will tell us whether the authors of the War on Terror–that public relations hoax that concealed the goals of eviscerated civil liberties and one world government–were really serious about actualizing their NWO vision or if it was merely the collective pipedream of corporate CEOs and bored bankers with too much time on their hands. In the Crimea, the empire faces a real adversary, not a disparate group of Kalashinov-waving jihadis in flip-flops. This is the Russian Army; they know how to defend themselves and they are prepared to do so. That puts the ball in Obama’s court. It’s up to him and his crackpot “Grand Chessboard” advisors to decide how far they want to push this. Do they want to intensify the rhetoric and ratchet up the sanctions until blows are exchanged, or pick up their chips and walk away before things get out of hand? Do they want to risk it all on one daredevil roll of the dice or move on to Plan B? That’s the question. Whatever US policymakers decide, one thing is certain, Moscow is not going to budge. Their back is already against the wall. Besides, they know that a lunatic with a knife is on the loose, and they’re ready to do whatever is required to protect their people. If Washington decides to cross that line and provoke a fight, then there’s going to trouble. It’s as simple as that.

Perma-hawk, John McCain thinks that Obama should take off the gloves and show Putin who’s boss. In an interview with TIME magazine McCain said “This is a chess match reminiscent of the Cold War and we need to realize that and act accordingly…We need to take certain measures that would convince Putin that there is a very high cost to actions that he is taking now.”

“High cost” says McCain, but high cost for who?

What McCain fails to realize is that this is not Afghanistan and Obama is not in a spitting match with puppet Karzai. Leveling sanctions against Moscow will have significant consequences, the likes of which could cause real harm to US interests. Did we mention that “ExxonMobil’s biggest non-US oil project is a collaboration with Russia’s Rosneft in the Arctic, where it has billions of dollars of investments at stake.” What if Putin decides that it’s no longer in Moscow’s interest to honor contracts that were made with US corporations? What do you think the reaction of shareholders will be to that news? And that’s just one example. There are many more.

Any confrontation with Russia will result in asymmetrical attacks on the dollar, the bond market, and oil supplies. Maybe the US could defeat Russian forces in the Crimea. Maybe they could sink the fleet and rout the troops, but there’ll be a heavy price to pay and no one will be happy with the outcome. Here’s a clip from an article at Testosterone Pit that sums it up nicely:

“Sergei Glazyev, the most hardline of Putin’s advisors, sketched the retaliation strategy: Drop the dollar, sell US Treasuries, encourage Russian companies to default on their dollar-denominated debts, and create an alternative currency system with the BRICS and hydrocarbon producers like Venezuela and Iran…

Putin’s ally and trusted friend, Rosneft president Igor Sechin…suggested that it was “advisable to create an international stock-exchange for the participating countries, where transactions could be registered with the use of regional currencies.” (From Now On, No Compromises Are Possible For Russia, Testosterone Pit)

As the US continues to abuse its power, these changes become more and more necessary. Foreign governments must form new alliances in order to abandon the present system–the “dollar system”–and establish greater parity between nation-states, the very nation-states that Washington is destroying one-by-one to establish its ghoulish vision of global corporate utopia. The only way to derail that project is by exposing the glaring weakness in the system itself, which is the use of an international currency that is backed by $15 trillion in government debt, $4 trillion in Federal Reserve debt, and trillions more in unpaid and unpayable federal obligations. Whatever steps Moscow takes to abort the current system and replace the world’s reserve currency with money that represents a fair store of value, should be applauded. Washington’s reckless and homicidal behavior around the world make it particularly unsuitable as the de facto steward of the global financial system or to enjoy seigniorage, which allows the US to play banker to the rest of the world. The dollar is the foundation upon which rests the three pillars of imperial strength; political, economic and military. Remove that foundation and the entire edifice comes crashing to earth. Having abused that power, by killing and maiming millions of people across the planet; the world needs to transition to another, more benign way of consummating its business transactions, preferably a currency that is not backed by the blood and misery of innocent victims. Paul Volcker summed up the feelings of many dollar-critics in 2010 when he had this to say:

“The growing sense around much of the world is that we have lost both relative economic strength and more important, we have lost a coherent successful governing model to be emulated by the rest of the world. Instead, we’re faced with broken financial markets, underperformance of our economy and a fractious political climate.”

America is irreparably broken and Washington is a moral swamp. The world needs regime change; new leaders, new direction and a different system.

In our last article, we tried to draw attention to the role of big oil in the present crisis. Author Nafeez Ahmed expands on that theme in a “must read” article in Monday’s Guardian. Check out this brief excerpt from Ahmed’s piece titled “Ukraine crisis is about Great Power oil, gas pipeline rivalry”:

“Ukraine is increasingly perceived to be critically situated in the emerging battle to dominate energy transport corridors linking the oil and natural gas reserves of the Caspian basin to European markets… Considerable competition has already emerged over the construction of pipelines. Whether Ukraine will provide alternative routes helping to diversify access, as the West would prefer, or ‘find itself forced to play the role of a Russian subsidiary,’ remains to be seen.” (Guardian)

The western oil giants have been playing “catch up” for more than a decade with Putin checkmating them at every turn. As it happens, the wily KGB alum has turned out to be a better businessman than any of his competitors, essentially whooping them at their own game, using the free market to extend his network of pipelines across Central Asia and into Europe. That’s what the current crisis is all about. Big Oil came up “losers” in the resource war so now they want Uncle Sam to apply some muscle to put them back in the game. It’s called “sour grapes”, which refers to the whining that people do when they got beat fair and square. Here’s more from Ahmed:

“To be sure, the violent rioting was triggered by frustration with (Ukrainian President) Yanukovych’s rejection of the EU deal, (in favor of Putin’s sudden offer of a 30% cheaper gas bill and a $15 billion aid package) along with rocketing energy, food and other consumer bills, linked to Ukraine’s domestic gas woes ….. Police brutality to suppress what began as peaceful demonstrations was the last straw…” (Ukraine crisis is about Great Power oil, gas pipeline rivalry, Guardian)

In other words, Yanukovych rejected an offer from Chevron that the EU and Washington were pushing, and went with the sweeter deal from Russia. According to Ahmed, that pissed off the bigwigs who decided to incite the rioting. (“Putin’s sudden offer of a 30% cheaper gas bill and a $15 billion aid package provoked the protests…”)

Like we said before; it’s just a case of sour grapes.

So, tell me, dear reader: Is this the first time you’ve heard a respected analyst say that oil was behind the rioting, the coup, and the confrontation with Moscow?

I’ll bet it is. Whatever tentacles Wall Street may have wrapped around the White House, Capital Hill, and the US judiciary; Big Oil still rules the roost. The Apostles of the Fossil are the oldest and most powerful club in Washington, and “What they say, goes”. As Ahmed so articulately points out:

“Resource scarcity, competition to dominate Eurasian energy corridors, are behind Russian militarism and US interference…Ukraine is caught hapless in the midst of this accelerating struggle to dominate Eurasia’s energy corridors in the last decades of the age of fossil fuels.” (“Ukraine crisis is about Great Power oil, gas pipeline rivalry”, Guardian)

Did I hear someone say “Resource War”?

As we noted in an earlier article, NWO mastermind Zbigniew Brzezinski characterized the conflict with Russia in terms of cutting off “Western access to the Caspian Sea and Central Asia”. For some unknown reason, America’s behemoth oil corporations think the resources that lie beneath Russian soil belong to them. The question is whether their agents will push Obama to put American troops at risk to assert that claim. If they do, there’s going to be a war.

By Mike Whitney

Email: fergiewhitney@msn.com

Mike Whitney lives in Washington state. He is a contributor to Hopeless: Barack Obama and the Politics of Illusion (AK Press). Hopeless is also available in a Kindle edition. Whitney’s story on declining wages for working class Americans appears in the June issue of CounterPunch magazine. He can be reached at fergiewhitney@msn.com.

http://www.marketoracle.co.uk/Article44840.html

EDITORIAL: The criminal ‘link’ of forwarding websites

Justice Department wants to make sharing information a crime

By THE WASHINGTON TIMES

Tuesday, March 11, 2014

The genius of the Internet is that it seamlessly links from one item to another. The online “community” is without end; there’s always something else to click on.

A federal prosecutor in Texas wants to change that by making it a crime to link to things the government doesn’t want anybody to see.

For more than a year, a young journalist, Barrett Brown, has been held in custody, threatened with spending the rest of his life in prison because he shared a link.

Though the federal government retreated on some of the charges last week, the government’s threat to freedom of speech remains.

Mr. Brown writes for a number of left-leaning outlets, including the London Daily Guardian, Vanity Fair and the Huffington Post. His work drew the attention of the hacking group known as “Anonymous,” and his association with them made him a target of the Justice Department.

In December 2012, he was charged with 12 counts of “aggravated identity theft” and “device fraud” because he pointed out where Anonymous made available 200 gigabytes worth of emails and other data stolen from Stratfor Global Intelligence, a security contractor.

A member of Anonymous, Jeremy Hammond, was sentenced to 10 years in prison for the actual crime of stealing the data.

U.S. Attorney Sarah R. Saldana persuaded a grand jury to indict Mr. Brown for these acts: “Brown transferred a hyperlink from an Internet Relay Chat (IRC) channel to an IRC channel under his control.” That sounds bad, but it isn’t.

It describes the familiar process of cutting and pasting a website link that millions use every day to share a funny YouTube video with a friend. Mr. Brown distributed the link to the Stratfor documents so he could “crowdsource” it, persuading many to work together to find important facts in the large cache of documents.

The government does not argue that Mr. Brown participated in the actual theft, only that once the documents were in the open he merely pointed to them. The government argues that the act of creating a link violates credit card theft laws because one of the thousands of files contained personal credit card information.

The Electronic Frontier Foundation has been warning of the implications of the government’s pursuit of Mr. Brown. “The right of journalists — or anyone, for that matter — to link to already public information, including sensitive information,” the foundation observes, “is in serious jeopardy if Brown is convicted.”

Three years ago, federal agents arrested Yonjo Quiroa, the owner of the site ChannelSurfing.net, for creating a website that linked to videos of live sporting events. While held without bail, he took a deal to plead to copyright misdemeanor and was deported.

The Obama administration seems to be looking for a test case to punish those who view, read and distribute information it wants to hide. If they can’t get Edward Snowden, maybe they can get someone else for reading and passing on interesting information embarrassing to the government.

Whether on email, Facebook, Instagram or Twitter, links are the lifeblood of the Internet. Shut them down, and life at the White House becomes much more convenient.

This was to be “the most transparent administration in history” — Barack Obama himself said so. The First Amendment seems always under government assault.

Read more: http://www.washingtontimes.com/news/2014/mar/11/editorial-the-criminal-link/#ixzz2w2QS7NXZ

Follow us: @washtimes on Twitter

Is Russia Pulling Money Out of U.S. for Safekeeping?

Bloomberg Businessweek

By Peter Coy March 14, 2014

There’s circumstantial evidence that Russia may have yanked tens of billions of dollars in assets out of a custodial account at the U.S. Federal Reserve, possibly to keep it from being frozen by U.S. authorities in case of heightened conflict in Ukraine.

The Federal Reserve holds U.S. Treasury securities in custody on behalf of foreign central banks and other official institutions. This chart from Bloomberg shows the sharpest percentage drop in the Fed’s custodial holdings in records going back to 2002. It’s a decline of $105 billion, or 3.5 percent, from March 5 to March 12. (The Fed’s own report is here.)

The Fed doesn’t say who its custodial customers are. I spoke today to Marc Chandler, global head of currency strategy at Brown Brothers Harriman, who suspects Russia accounts for a big share of the draw-down. “It’s just to avoid being frozen,” Chandler says, not a protest against the U.S. He adds, ”You don’t let your politics dictate these decisions.”

In a note to clients, Chandler wrote, “The logic now is that Russia is bracing for the next round of sanctions.” He pointed out that this has happened before. In 1957, Russia shifted dollars from the U.S. to London, he said, fearing the U.S. would punish Russia financially for its invasion of Hungary. According to some accounts, that event gave birth to what’s known today as the Eurodollar market—dollar-denominated assets stashed outside of U.S. borders.

Bloomberg’s Susanne Walker reports today that Chandler isn’t the only one who sees Russia behind the big decline in Fed custodial holdings. She quotes Wrightson ICAP: “Escalating talk of sanctions over the Ukraine conflict would give [Russia] every reason to move those holdings to an off-shore custodian.”

Chandler suspects that Russia didn’t sell the Treasuries, but only moved them somewhere out of U.S. authorities’ reach. According to data compiled by Bloomberg, as of December, Russia held $139 billion in Treasuries, making it the ninth-largest country holder, accounting for about 1 percent of the total.

Coy is Bloomberg Businessweek's economics editor. His Twitter handle is @petercoy.

http://www.businessweek.com/articles/2014-03-14/is-russia-pulling-money-out-of-u-dot-s-dot-for-safekeeping#r=rss

Is Russia Pulling Money Out of U.S. for Safekeeping?

Bloomberg Businessweek

By Peter Coy March 14, 2014

There’s circumstantial evidence that Russia may have yanked tens of billions of dollars in assets out of a custodial account at the U.S. Federal Reserve, possibly to keep it from being frozen by U.S. authorities in case of heightened conflict in Ukraine.

The Federal Reserve holds U.S. Treasury securities in custody on behalf of foreign central banks and other official institutions. This chart from Bloomberg shows the sharpest percentage drop in the Fed’s custodial holdings in records going back to 2002. It’s a decline of $105 billion, or 3.5 percent, from March 5 to March 12. (The Fed’s own report is here.)

The Fed doesn’t say who its custodial customers are. I spoke today to Marc Chandler, global head of currency strategy at Brown Brothers Harriman, who suspects Russia accounts for a big share of the draw-down. “It’s just to avoid being frozen,” Chandler says, not a protest against the U.S. He adds, ”You don’t let your politics dictate these decisions.”

In a note to clients, Chandler wrote, “The logic now is that Russia is bracing for the next round of sanctions.” He pointed out that this has happened before. In 1957, Russia shifted dollars from the U.S. to London, he said, fearing the U.S. would punish Russia financially for its invasion of Hungary. According to some accounts, that event gave birth to what’s known today as the Eurodollar market—dollar-denominated assets stashed outside of U.S. borders.

Bloomberg’s Susanne Walker reports today that Chandler isn’t the only one who sees Russia behind the big decline in Fed custodial holdings. She quotes Wrightson ICAP: “Escalating talk of sanctions over the Ukraine conflict would give [Russia] every reason to move those holdings to an off-shore custodian.”

Chandler suspects that Russia didn’t sell the Treasuries, but only moved them somewhere out of U.S. authorities’ reach. According to data compiled by Bloomberg, as of December, Russia held $139 billion in Treasuries, making it the ninth-largest country holder, accounting for about 1 percent of the total.

Coy is Bloomberg Businessweek's economics editor. His Twitter handle is @petercoy.

http://www.businessweek.com/articles/2014-03-14/is-russia-pulling-money-out-of-u-dot-s-dot-for-safekeeping#r=rss

The Big Lie + What Happened To Ukraine’s Gold?

TND Guest Contributor: Dave Kranzler |

Mar. 15, 2014

The Big Lie is that Central Banks don’t care about gold. Nothing could be further from the truth. Ben Bernanke more than once claimed that he didn’t understand gold. When Ron Paul asked Bernanke in front of Congress why Central Banks own gold if it’s irrelevant, Bernanke flippantly suggested that it was out of tradition. In both cases Bernanke was lying and he knew it.

In comparison, Greenspan seemed to have some respect for the laws of economics and – at least that I can recall – never would outright state that gold was not an economic factor. Greenspan lied as much as Bernanke did about everything else but he never committed himself to lie about gold. Most of you have probably read Greenspan’s 1966 essay, “Gold and Economic Freedom” (linked). I have read it several times because it explains as well as anything out there why gold works as a currency and why Government-issued fiat currency does not.

What I find amazing about The Big Lie about Central Banks and gold is that if gold really is considered to be irrelevant, the how come Central Banks – especially the Fed – are so secretive about their gold storage and trading activities? What’s even more amazing is that no one other than Ron Paul and GATA asks them about this. Think about it. GATA spent a lot of money on legal fees attempting to get the Fed to publicly disclose its records related to the Fed’s gold activities. The Fed spent even more money denying GATA’s quest. And how come the Fed won’t submit to a public, independent audit of its gold vaults?

This brings me to the issue of the Ukraine’s gold. According to public records, the Government of Ukraine owns 33 tonnes of gold that was being safekept in Ukraine. Last week a Ukrainian newspaper reported that acting PM Arseny Yatsenyuk ordered the transfer of that gold to the United States. The actual report is here: LINK. Jesse’s Cafe Americain provided a translated version here: LINK.

On the assumption that the report is true, and so far I have not seen any commentary or articles suggesting it is not true, the biggest question is, how come the U.S. has absolutely no problem loading up and transporting 33 tonnes of gold from Ukraine to the U.S. but seems to have difficulty loading up and transporting any of Germany’s gold from New York to Berlin? And how come the U.S. and Ukraine seem to care about that gold at all, if indeed gold is irrelevant? It would seem that it would be a lot less expensive and logistically complicated just to have the U.S. military post a few armed guards around the gold if they’re worried about theft. On the other hand, I’m sure Putin would be happy to buy the gold from Ukraine.

What makes the story even more interesting is that GATA’s Chris Powell has spent considerable time trying to get an answer to the question of whether or not the U.S. has taken custody of Ukraine’s gold. When he queried the NY Fed, they responded with: “A spokesman for the New York Fed said simply: “Any inquiry regarding gold accounts should be directed to the account holder. You may want to contact the National Bank of Ukraine to discuss this report” (LINK). After trying for two days to get an answer from the U.S. State Department, they finally responded by referring him to the NY Fed (LINK).

The final piece in verifying that the report is true is deflection from Ukraine. Mr. Powell has queried the National Bank of Ukraine, the Ukrainian Embassy in DC and the Ukrainian mission to the UN in NYC. Crickets. As Chris states the case: “The difficulty in getting a straight answer here is pretty good evidence that the Ukrainian gold indeed has been sent to the United States.”

Unfortunately, it is likely that the citizens of Ukraine will end up paying the same price for allowing the U.S. to “safekeep” their sovereign gold. That price is the comforting knowledge that their gold has been delivered safely to vaults in China under U.S./UK bullion bank contractual delivery obligations, where it will be locked away for centuries.

All this skullduggery over a barbarous relic that has been deemed irrelevant by the U.S. Federal Reserve.

# # # #

Aspen1-daveAbout Dave Kranzler

I spent many years working in various analytic jobs and trading on Wall Street. For nine of those years, I traded junk bonds for Bankers Trust. I have an MBA from the University of Chicago, with a concentration in accounting and finance. My goal is to help people understand and analyze what is really going on in our financial system and economy. You can follow my work and contact me via my website Investment Research Dynamics. Occasionally, I publish on Seeking Alpha too.

As a co-founder and principal of Golden Returns Capital, LLC Mr. Kranzler co-manages the Precious Metals Opportunity Fund, a metals and mining stock investment fund.

http://thenewsdoctors.com/the-big-lie-what-happened-to-ukraines-gold/

The Big Lie + What Happened To Ukraine’s Gold?

TND Guest Contributor: Dave Kranzler |

Mar. 15, 2014

The Big Lie is that Central Banks don’t care about gold. Nothing could be further from the truth. Ben Bernanke more than once claimed that he didn’t understand gold. When Ron Paul asked Bernanke in front of Congress why Central Banks own gold if it’s irrelevant, Bernanke flippantly suggested that it was out of tradition. In both cases Bernanke was lying and he knew it.

In comparison, Greenspan seemed to have some respect for the laws of economics and – at least that I can recall – never would outright state that gold was not an economic factor. Greenspan lied as much as Bernanke did about everything else but he never committed himself to lie about gold. Most of you have probably read Greenspan’s 1966 essay, “Gold and Economic Freedom” (linked). I have read it several times because it explains as well as anything out there why gold works as a currency and why Government-issued fiat currency does not.

What I find amazing about The Big Lie about Central Banks and gold is that if gold really is considered to be irrelevant, the how come Central Banks – especially the Fed – are so secretive about their gold storage and trading activities? What’s even more amazing is that no one other than Ron Paul and GATA asks them about this. Think about it. GATA spent a lot of money on legal fees attempting to get the Fed to publicly disclose its records related to the Fed’s gold activities. The Fed spent even more money denying GATA’s quest. And how come the Fed won’t submit to a public, independent audit of its gold vaults?

This brings me to the issue of the Ukraine’s gold. According to public records, the Government of Ukraine owns 33 tonnes of gold that was being safekept in Ukraine. Last week a Ukrainian newspaper reported that acting PM Arseny Yatsenyuk ordered the transfer of that gold to the United States. The actual report is here: LINK. Jesse’s Cafe Americain provided a translated version here: LINK.

On the assumption that the report is true, and so far I have not seen any commentary or articles suggesting it is not true, the biggest question is, how come the U.S. has absolutely no problem loading up and transporting 33 tonnes of gold from Ukraine to the U.S. but seems to have difficulty loading up and transporting any of Germany’s gold from New York to Berlin? And how come the U.S. and Ukraine seem to care about that gold at all, if indeed gold is irrelevant? It would seem that it would be a lot less expensive and logistically complicated just to have the U.S. military post a few armed guards around the gold if they’re worried about theft. On the other hand, I’m sure Putin would be happy to buy the gold from Ukraine.

What makes the story even more interesting is that GATA’s Chris Powell has spent considerable time trying to get an answer to the question of whether or not the U.S. has taken custody of Ukraine’s gold. When he queried the NY Fed, they responded with: “A spokesman for the New York Fed said simply: “Any inquiry regarding gold accounts should be directed to the account holder. You may want to contact the National Bank of Ukraine to discuss this report” (LINK). After trying for two days to get an answer from the U.S. State Department, they finally responded by referring him to the NY Fed (LINK).

The final piece in verifying that the report is true is deflection from Ukraine. Mr. Powell has queried the National Bank of Ukraine, the Ukrainian Embassy in DC and the Ukrainian mission to the UN in NYC. Crickets. As Chris states the case: “The difficulty in getting a straight answer here is pretty good evidence that the Ukrainian gold indeed has been sent to the United States.”

Unfortunately, it is likely that the citizens of Ukraine will end up paying the same price for allowing the U.S. to “safekeep” their sovereign gold. That price is the comforting knowledge that their gold has been delivered safely to vaults in China under U.S./UK bullion bank contractual delivery obligations, where it will be locked away for centuries.

All this skullduggery over a barbarous relic that has been deemed irrelevant by the U.S. Federal Reserve.

# # # #

Aspen1-daveAbout Dave Kranzler

I spent many years working in various analytic jobs and trading on Wall Street. For nine of those years, I traded junk bonds for Bankers Trust. I have an MBA from the University of Chicago, with a concentration in accounting and finance. My goal is to help people understand and analyze what is really going on in our financial system and economy. You can follow my work and contact me via my website Investment Research Dynamics. Occasionally, I publish on Seeking Alpha too.

As a co-founder and principal of Golden Returns Capital, LLC Mr. Kranzler co-manages the Precious Metals Opportunity Fund, a metals and mining stock investment fund.

http://thenewsdoctors.com/the-big-lie-what-happened-to-ukraines-gold/

Fantastic article basserdan!

The Russians Have Already Quietly Pulled Their Money From The West

by Tyler Durden on 03/14/2014

Earlier today we reported that according to weekly Fed data, a record amount - some $105 billion - in Treasurys had been sold or simply reallocated (which for political reasons is the same thing) from the Fed's custody accounts, bringing the total amount of US paper held at the Fed to a level not seen since December 2012. While China was one of the culprits suggested to have withdrawn the near USD-equivalent paper, a far likelier candidate was Russia, which as is well-known, has had a modest falling out with the West in general, and its financial system in particular. Turns out what Russian official institutions may have done with their Treasurys (and we won't know for sure until June), it was merely the beginning. In fact, as the FT reports, in silent and not so silent preparations for what will be near-certain financial sanctions (which would include account freezes and asset confiscations following this Sunday's Crimean referendum) the snealy Russians, read oligarchs, have already pulled billions from banks in the west thereby essentially making the biggest western gambit - that of going after the wealth of Russia's 0.0001% - moot.

From the FT:

Russian companies are pulling billions out of western banks, fearful that any US sanctions over the Crimean crisis could lead to an asset freeze, according to bankers in Moscow.

Sberbank and VTB, Russia’s giant partly state-owned banks, as well as industrial companies, such as energy group Lukoil, are among those repatriating cash from western lenders with operations in the US. VTB has also cancelled a planned US investor summit next month, according to bankers.

The flight comes as last-ditch diplomatic talks between Russia’s foreign minister and the US secretary of state to resolve the tensions in Ukraine ended without an agreement.

Markets were nervous before Sunday’s Crimea referendum on secession from Ukraine. Traders and businesspeople fear this could spark western sanctions against Russia as early as Monday.

It probably will. What it will also do is force Russia to engage China far more actively in bilateral trade and ultimately to transact using either Rubles or Renminbi, and bypass the dollar. Perhaps even using gold, something which the price of the yellow metal sniffed out this week, pushing itself to 6 month highs. It will also make financial ties between the two commodity-rich nations even closer, while further alienating that "imperialist devil," the US.

Of course, the west thinking like the west, and assuming that all that matters to Russia is the closing level of the Micex, believes that a sufficient plunge in Russian stocks would have been enough to deter Putin. After all, the only thing everyone in the US cares about is if the S&P 500 closed at yet another all time high, right?

What the west didn't realize, as we predicted a month ago, for Putin it is orders of magnitude more important to have the price of commodities, primarily crude and gas, high than seeing the illusion of paper wealth, aka stocks, hitting all time highs. Especially since in Russia an even smaller portion of the population cares about the daily fluctuations of the stock market. As for the oligarchs, if there is someone who will be delighted to see their power, wealth and influence impacted adversely, if only for a short period of time, it is Vladimir Vladimirovich himself, whom the west misjudged massively once more. Not to mention that the general population will be even more delighted, and boost Putin's rating even higher, if these crony billionaires are made to suffer by the west, if only a little.

(Here we would be remiss not to comment on his easy it supposedly is for Obama to freeze the assets of a few corrupt Russian billionaires, and yet the very proud Americans who nearly brought the entire financial system to the brink in 2008, are now richer than ever.)

In the meantime, some of Russia's oligarchs are effectively welcoming the challenge. Bloomberg reports:

Alisher Usmanov, the country’s richest person, controls his most valuable asset, Metalloinvest Holding Co., Russia’s largest iron ore producer, through three subsidiaries, one of which is located in Cyprus, an EU member nation. The 60-year-old also owns a Victorian mansion in London that he bought in 2008 for $70 million, according to a May 18, 2008, Sunday Times newspaper report. He’s lost $1.5 billion since the crisis began, according to the Bloomberg ranking.

“We are concerned with the possible sanctions against Russia but don’t see any dramatic repercussions for our business,” Ivan Streshinsky, CEO at USM Advisors LLC, which manages Usmanov’s assets, including stakes in Megafon OAO and Mail.Ru Group Ltd., said in an interview at Bloomberg’s offices in Moscow today.

“Mail.Ru and Megafon revenue is coming from Russia and people won’t stop making calls and using the Internet,” he said. “Metalloinvest may face closure in European and American markets, but it can re-direct sales to China and other markets.”

Great job, Obama: you just pushed Russia and China even closer by necessity! Furthermore, it should come as no surprise that while Russians were pulling their money from the west, western firms were getting out of Dodgeski.

One senior Moscow banker said 90 per cent of investors were already behaving as if sanctions were in place, adding that this was “prudent exposure management”.

These moves represent the flipside of the more obvious withdrawal of western money from Russian markets that has been evident over the past fortnight.

Traders and bankers said US banks had been particularly heavy sellers of Russian bonds. According to data from the Bank for International Settlements, US banks and asset managers between them have about $75bn of exposure to Russia.

Joseph Dayan, head of markets at BCS, one of Russia’s largest brokers said: “It’s been quite an ugly picture in Russian bonds the last few days and some of it has to do with international banks reducing exposure.”

Although foreign banks have not yet begun cutting credit to Russian companies en masse, bankers said half a dozen live deals to fund some of Russia’s biggest companies were in limbo as lenders waited to see how punitive western sanctions would be.

So the bottom line is that Russia, thinking a few steps ahead, already has withdrawn the bulk of its assets from the West, and why not. Recall that a year ago it was revealed that the same Russians who were supposed to be punished in Cyprus had mostly withdrawn their funds in advance of the bail in: they tend to know what is coming. It was the ordinary Cypriot citizens, who had done nothing wrong, who were most impaired.

And so while the Russian response is already known, we wonder just how true is the inverse: just how prepared is the west, and especially Europe, to exist in a world in which a third of Germany's gas is suddenly cut off? We can't wait to find out early next week.

http://www.zerohedge.com/news/2014-03-14/russians-have-already-quietly-pulled-their-money-west

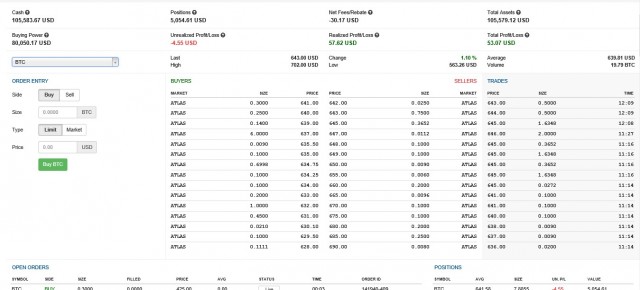

Move over, small-time Bitcoin exchange startups—Wall Street has arrived

Gentlemen, start your trading bots. Things are about to get crazy.

by Cyrus Farivar - Mar 12 2014, 1:45pm EDT

FINANCE

antanacoins

On Wednesday morning, Perseus Telecom and Atlas jointly launched their new high-speed trading platform for Bitcoin and likely other cryptocurrencies in the future. Perseus is a firm that specializes in high-speed financial data networks, while Atlas is a relative newcomer to the Wall Street scene since starting in 2013.

"The platform's debut puts Bitcoin trading much closer to the modern world of automated and secure trading. Atlas deals will have a matching speed of 30 millionths of a second. Modern trading firms colocate their systems as physically close to the “matching engines” as possible as a way to gain a few milliseconds of edge over others.

“Perseus offers high precision trading access in colocation centers worldwide, and adding Atlas as a new and highly liquid platform is an immediate response to customers demanding Bitcoin trading,” Perseus CEO Jock Percy said in a statement. “The Perseus Digital Currency Initiative is providing governance strictly supporting KYC (Know Your Customer) and AML (Anti-Money Laundering) principles.”

The two firms have founded what they call the “Digital Currency Initiative,” aimed at creating a set of industry-wide guidelines. The end goal is to reach “high precision trading standards executed each day by leading market makers, hedge funds, and investment banks.”

The new Atlas platform has already been running as a “soft launch” for some time now, Atlas CEO Shawn Sloves told Ars.

Sloves also noted that this new platform was not accelerated by MtGox's demise.

"[Perseus and Atlas'] backgrounds both on the trading infrastructure and the telecom side has been servicing ultra low latency clients, it takes years of capital and experience to achieve this type of setup," he said. "It cannot be replicated overnight or in a short period of time. This is an incredible achievement by both our companies. Regardless [of whether] MtGox failed or not, we went ahead and built this out. Our client focus is not necessarily users who had accounts at MtGox."

Enlarge / Here's the front-end of the new Atlas trading platform.

Atlas ATS

“I expect that this will help make more transparent liquid markets”

Bitcoin industry watchers say that this marks a notable turning point in the digital currency’s evolution.

“I expect more robust Bitcoin exchanges to emerge and replace the existing set of incumbents,” Gil Luria, a Bitcoin analyst at Wedbush Securities, told Ars by e-mail. “The new exchanges will be either venture capital-backed or units of existing financial institutions. That means they will have the resources to build robust platforms that are scalable, secure, and compliant. I expect that this will help make more transparent liquid markets for Bitcoin and its derivatives, which will translate to less price volatility and better utility for Bitcoin businesses.”

In an investor’s note released last month, Luria wrote that he is largely bullish on Bitcoin. Wedbush noted that it “will be accepting Bitcoin on a limited basis for previously published reports on the topic of cryptocurrency.”

Luria wrote:

More important, we see signs that entrepreneurs and developers are swarming to the Bitcoin platform (page 2). We see this as the best indication of the potential for Bitcoin as these developers are allocating their most valuable resource—development hours. We found nearly 3,000 Github repositories, double from six months ago, which was double from the previous six months. We believe nearly $86 million of venture funds have been invested in Bitcoin companies, mostly over the last 12 months, which does not include the >$200 million and counting we believe have been invested in mining equipment.

James Angel, a visiting finance professor at the Wharton School at the University of Pennsylvania, told Ars by e-mail that Atlas’ new platform debut is “not surprising.”

“With the interest of respectable [venture capital firms] and financial firms in Bitcoin, it makes sense for existing vendors of exchange services in other assets (like Atlas) to offer Bitcoin,” he said. “If you have a good trading platform that can trade currencies, it is pretty easy to add Bitcoin. Thus, it is a low-cost venture for an outfit like Atlas to do. By locating in the industry-standard data centers such as Equinix where the other financial players are located, they make it easier for mainstream financial industry participants to connect."

“Atlas claims to perform transactions in 30 microseconds, which is roughly the same speed as the best equity exchanges in the US," Angel said. "This kind of speed will allow electronic market makers to provide liquidity, lowering bid-ask spreads. Also, it will permit firms that scrape news feeds electronically to respond very quickly.”

The biggest takeaway from the Atlas news? The new platform may finally be a sign that Bitcoin’s freewheeling, anonymous, crypto-libertarian days are coming to an end.

“Wouldn’t you place your bitcoins at a place where the transactions are more likely to be honored?” Ivo Welch a finance professor at the University of California, Los Angeles, wrote to Ars. “There is an irony here. Bitcoins exist to avoid institutions, and now we will have institutions.”

http://arstechnica.com/business/2014/03/move-over-small-time-bitcoin-exchange-startups-wall-street-has-arrived/

Lord & Taylor’s Pounce Trial Could Be First Step in Bitcoin Plans

Pete Rizzo (@pete_rizzo_) Published on March 12, 2014 at 18:16 GMT

coindesk.com

A few months have passed since Overstock became, arguably, the most high-profile retailer to accept bitcoin. While only a handful of major brands have followed Overstock’s lead, that doesn’t mean its decision isn’t having an impact.

As evidence, Ryan Craver, senior vice president of corporate strategy at Hudson Bay Co., told CoinDesk that Overstock’s continued bitcoin sales were a key reason he decided to test the waters with bitcoin, albeit through a business partner.

On 10th March, it was revealed that Hudson Bay Co., which operates major brands like Lord & Taylor and Hudson’s Bay, would begin accepting bitcoin through omnichannel mobile shopping app Pounce.

Together, Lord & Taylor and Hudson’s Bay have more than 100 locations in the US and Canada.

Founded in 2012, the innovative mobile app allows customers to make purchases simply by scanning their smartphone over images in magazines and catalogs.

Pounce has inked a deal with Coinbase to accept bitcoin on behalf of its extensive list of clients, which include Macy’s, Ace Hardware and Toys “R” Us, among others.

It may surprise many readers to learn, however, that Pounce was encouraged to accept bitcoin by Craver, who was prompted by continued requests from Lord & Taylor and Hudson’s Bay customers.

A bitcoin news follower since mid-2013, Craver suggested that this could be just the beginning of his company’s work in the sector.

“We thought Pounce would be the best potential partner, that way we could figure out how large an audience we could truly have with bitcoin, and from there, make a determination about whether we roll this out on our mobile apps, our core site or even in stores.”

Craver notes that while he’s optimistic, ideas are still in their early stages. After all, Hudson Bay Co. won’t be accepting bitcoin payments directly, but both companies have high expectations for the deliverables this trial will return.

Project goals

Craver told CoinDesk that, his personal interest aside, he is still evaluating the business impact bitcoin could have on his brands. This means that so far he’s been following Overstock’s progress, and that he has had discussions with Coinbase.

However, Craver’s interest can also be seen as part of a larger experiment with omnichannel commerce.

Announced on 24th January, Hudson Bay Co. has seen what it considers a high level of success from its initial Pounce trial. Craver estimates Pounce users register seven engagements every time they use Pounce to browse its catalogs.

In turn, for Avital Yachin, CEO of Pounce, bitcoin arms his product with another incentive to appeal to early-tech adopters.

How buying works

Speaking to CoinDesk, Yachin was equally excited about brining bitcoin to Pounce, and provided a step-by-step overview of how the buying process will work with his app.

First, he said, users download the Pounce application. From there, they can browse products on the app itself or scan a Pounce-enabled printed catalog to shop or save products for later.

One of the biggest selling points for Pounce, however, is its one-click buying.

“You need to enter shipping and payment information, but this needs to be done only once. Once you have your payment information, you can then connect your Coinbase wallet [...] and you can continue purchasing through the app without typing your payment or shipping information again.”

Success so far

Yachin declined to provide hard figures for how well Lord & Taylor and other merchants are attracting bitcoin buyers, but indicated that a high percentage of new users are downloading Pounce and then connecting their Coinbase wallets to the app.

Said Yachin: “So far, we’re pretty happy with the results.”

Craver affirmed that this could be just the beginning of his company’s work with bitcoin as well.

“I think down the line, if we feel the attraction, we’ll need to evaluate it as a potential payment method.”

http://www.coindesk.com/lord-taylors-pounce-trial-could-be-first-step-in-bitcoin-payments-rollout/

Guess they've thought of everything take a look at this article dated Nov. 2013

No, You Can't Donate Bitcoin To Politicians Yet

Kashmir Hill Forbes Staff

Forbes

Welcome to The Not-So Private Parts where technology & privacy collide

Bitcoin goes before the Senate again Tuesday after having been given a tentative thumbs up by government agencies during a Senate Homeland Security hearing on Monday. The Banking Committee hearing Tuesday is a littler dryer — less about drugs and murder for hire for Bitcoin, and more about financial and banking issues around virtual currencies. During his opening remarks, hearing chair Senator Mark Warner said that he’s been “following Bitcoin for months” but is only now “wrapping his head around it.” He then remarked offhandedly that the Federal Election Committee recently approved Bitcoin for political donations. But he’s incorrect.

The Conservative Action Fund asked the FEC to decide whether PACs could accept Bitcoin donations. A draft opinion posted online suggested that the FEC would approve the request at its meeting last Thursday. It said that Bitcoins should be treated as as in-kind gifts like stocks and would need to be cashed out before they’re deposited with a campaign or used for goods and services. Media organizations started reporting that “soon you’ll be able to buy politicians with digital cash,” but the FEC actually wound up punting on the issue.

“The Commission discussed the drafts but held over the matter until next Thursday’s open meeting,” says FEC spokesperson Julia Queen. The issue comes up again this Thursday. One thing the committee is considering is a technical proposal by another PAC, Make Your Laws, that donation recipient must document the Blockchain transaction id for the donation as well as the Bitcoin addresses of the sending and receiving PAC.

“Without appropriate Bitcoin-specific transaction records, PAC transactions of Bitcoin would be completely unauditable,” writes Sai, of Make Your Laws PAC.

Whether donors can send cryptocoins to their party and politician of choice — and how that gets tracked — will get another look from the FEC this Thursday.

http://www.forbes.com/sites/kashmirhill/2013/11/19/no-you-cant-donate-bitcoin-to-politicians-yet/

Why Ukraine and Russia matter to commodity markets

Commentary: Conflict may have impact on natgas, palladium, potash

Mar. 7, 2014

By Myra P. Saefong, MarketWatch

The Ukraine-Russia conflict may influence much more than natural gas. Above: a section of the trans-Siberian Pipeline, Russia's main natural-gas export pipeline, in Ukraine.

SAN FRANCISCO (MarketWatch) — Oil, gold and wheat prices are in the limelight after Russia’s invasion of Ukraine’s Crimea region, but the conflict may have significant consequences for other commodities too — including natural gas, palladium and potash.

“Concerns over economic sanctions against Russia will put short-term pressure on [commodities] supplies,” said Jeffrey Sica, president and chief investment offer of Sica Wealth Management. “There is certain to be a significant element of the stockpiling of commodities in anticipation of escalation in the conflict.”

Once the situation in Ukraine heated up with Russia’s invasion of Ukraine’s Crimea region on Feb. 27, concern was evident in oil, gold and wheat markets.

On Monday, oil prices CLJ4 +0.99% surged to a five-month high and wheat WK4 +1.12% rallied by almost 5% to the highest level of the year on the potential for global supply disruptions, while gold prices GCJ4 -0.93% jumped to their highest in four months as investors fled to safety.

But the situation between Ukraine and Russia has a much wider reach in the commodities world.

Remember that Russia is the world’s largest producer of palladium and, together with Canada and Belarus is estimated to account for a little over two-thirds of global capacity for potash, a chemical compound used primarily in fertilizer. Ukraine, meanwhile, is the world’s fifth-largest exporter of wheat and third-biggest exporter of corn.

“Ukraine is known as the breadbasket of Eastern Europe and is one of the largest exporters of grain in the world, of which wheat exports would be the largest agricultural commodity impacted by an escalating conflict between Kiev and Moscow,” said Edmund Moy, strategist with gold-backed IRA provider Morgan Gold, who spent time in Ukraine and lectured at Kiev University.

Russia also supplies around a third of Europe’s natural gas, with more than half of that flowing through Ukraine.

“The real issue is natural gas,” said Matt Lasov, global head of advisory and analytics at Frontier Strategy Group. “Any sanctions led by Europe or the United States or further conflict with Ukraine’s government could cause Russia to squeeze Ukrainian gas flow in response, putting prices sharply higher.”

Ukraine itself is home to large shale natural-gas deposits that the U.S. Energy Information Administration says may allow it to diversify its supply need away from Russia, though commercial exploitation is years away.

Sanctions

Already, the U.S. has put limited sanctions in place, though they’re not a big concern yet.

U.S. President Barack Obama signed an executive order that authorizes sanctions on individuals who threaten the sovereignty of Ukraine, the White House announced on Thursday. The State Department has also put in place visa restrictions on a number of officials tied to what the U.S. calls the invasion of Crimea by Russia.

“These sanctions don’t make a difference,” said Martina Bozadzhieva, head of research for Europe, Middle East and Africa for Frontier Strategy Group. “They are the softest possible sanctions the U.S. could have imposed and effectively only hurt a small group of Russian individuals.”

That could soon change.

“If the situation were to escalate or if Russia hunkers down for the long haul and various sanctions by the U.S. and [United Nations] were imposed, then various key commodities can be expected to be impacted,” said Kevin Kerr, editor of CommodityConfidential.com.

“Clearly, any sanctions could upset the pricing matrix for oil and natural gas, as well as wheat and corn exports, especially if there is a real disruption,” he said, adding that potash, and key agricultural stocks like Deere & Co. DE +0.53% , could be impacted significantly as well.

“There would really be no winners if sanctions were forced to be imposed,” said Kerr.

Palladium and potash

Potash is among the commodities that have failed to come into the spotlight, despite the fact that Russia’s among the few countries that produce it.

Potassium chloride, also known as potash, at a processing plant at the OAO Uralkali mine in Berezniki, Russia.

A potential shortage of potash supplies is of “great concern since the lack of fertilizer is limiting the increase in crop output needed to accommodate the demand,” said Sica Wealth Management’s Sica.

Of course there are some non-Russian potash suppliers that could benefit if trade sanctions were to hurt Russian potash exports.

Those may be Potash Corp. of Saskatchewan POT -1.90% , Mosaic Co. MOS -0.88% and Intrepid Potash Inc. IPI -0.31% , according to Robbert van Batenburg, director of market strategy for Newedge. Shares of Potash Corp. have climbed nearly 5% this week.

Russia is also the largest producer of palladium PAM4 +0.05% , according to Johnson Matthey .

“My guess is that prices would move sharply higher if exports were affected by sanctions,” said Tim Murray, general manager of precious metals marketing at Johnson Matthey.

The metal has a variety of uses for medicine and electronics among others. Much of it is used to make catalytic converters that help reduce harmful vehicle emissions.

For now, however, the more important issue in the near term for the metal is South Africa, as the Association of Mineworkers and Construction Union-led walkout at the three largest platinum producers is in its sixth week, Murray said. Palladium prices on Comex climbed to their highest level in nearly a year on Thursday, fueled by concerns over the strikes as well as the conflict between Russia and Ukraine.

Natural gas

When it comes to energy commodities, shale may end up being Ukraine’s secret weapon.

Russia’s Gazprom has warned Ukraine to pay its bill or risk having its natural-gas supply cut off, according to an AFP report Friday. Ukraine owes Gazprom $1.89 billion, the energy giant said.

“Russia has a track record [of] using gas as a political tool, squeezing Ukraine in 2006 and 2009 with ripple effects in Europe,” said Frontier Strategy Group’s Lasov.

But the energy market needs to take into account Ukraine’s shale natural-gas reserves, which the country is working to develop for domestic consumption and exports to Western Europe by 2020, according to the EIA.

Ukraine has the fourth-largest shale natural-gas reserves in Europe — estimated at about 1.2 trillion cubic meters, EIA data show.

“The biggest threat to Moscow, in our view, may well be 21st-century shale technology,” said strategists at Bank of America Merrill Lynch, in a note this week.

“With NATO military protection, European capital and American technology, Ukraine could potentially become a competitive gas supplier to EU markets,” they said. “After all, the pipeline infrastructure is already in place.” Read: Russian natural-gas supplies aren’t a worry yet for Europe.

http://www.marketwatch.com/story/why-ukraine-and-russia-matter-to-commodity-markets-2014-03-07?pagenumber=1

Big banks jumping on bitcoin bandwagon

March 7, 2014, 1:21 PM

Marketwatch.com

Many major Wall Street banks are trying to understand bitcoin, the virtual currency that has gained interest in the last few years, and how it could change the global payment system, say industry experts.

Bloomberg A twenty-five bitcoin

“What we have learned is that many of the banks have individuals and teams now focused on getting to know bitcoin and how it impact the business,” said Barry Silbert, founder and CEO of SecondMarket, which is working on creating a U.S.-based bitcoin exchange and an investor in Bitcoin companies.

Silbert was speaking at a panel discussion at the MarketWatch Investing Insights event “Bitcoin: Boom and Bust” late Tuesday in New York.

Banks are trying to understand what a digital-currency world looks like from an infrastructure perspective, noted Silbert.

Bitcoin is a decentralized virtual currency that has been trumpeted as a faster and cheaper alternative to existing payments systems and has attracted the interest of high-profile venture capitalists. Some even say it has the potential to be a widely used currency. But it isn’t regulated and a prominent bitcoin exchange shut down last month after hackers stole all its customers’ bitcoins, leaving users with little recourse and raising concerns about security.

On Friday, Japan’s government said bitcoin isn’t a currency or a financial product and will be treated like other goods and services. Prices of bitcoin, meanwhile, have swung from $13 in early 2013 to above $1,000 in November and back down to around $625 on Friday.

So far, Bank of America Corp. BAC -0.46% , J.P. Morgan Chase & Co. JPM +0.48% , Citigroup Inc. C -0.45% , Goldman Sachs Group Inc. GS +0.30% and Wells Fargo & Co. WFC +0.60% have published reports on bitcoin for clients. Morgan Stanley has not.

J.P. Morgan analyst John Normand writes: “For corporates, bitcoin’s appeal is two-fold: no or low transaction costs from a peer-to-peer payments system, and potential brand recognition from trialing an innovative technology.”

Bank of America analysts say bitcoin may emerge as a serious competitor to traditional money-transfer providers. “As a medium of exchange, Bitcoin has clear potential for growth, in our view,” they add.

Wells Fargo hosted a panel on virtual currency in January that looked at bitcoin’s viability, compliance and future. Goldman Sachs included a panel on digital currency as part of a global macro conference on Thursday.

@barrysilbert discusses the world of digital currency at the @goldmansachs global macro conf #bitcoin

3:24 PM - 6 Mar 2014

“If payments or transactions can be done cheaper, there is an incentive for entrepreneurs and financial firms to get involved,” said Steven Englander, Citigroup’s global head of G10 FX strategy.

Financial firms have showed interest in key areas such as whether bitcoin is an investment opportunity, a commodity to be traded or a currency to be converted for clients.

A number of commodities and currency traders are digging into bitcoin and using their own money to to trade bitcoin, noted Silbert. And banks are also interested in the virtual currency, as exchanges are being to formed, to provide potential services to clients such as converting bitcoin into other currencies.

“Bitcoin’s primary attraction, in my view, is that it is a way to transfer funds instantaneously and cheaply with a pretty secure system,” said Englander.

Several high-profile business leaders have showed interest in bitcoin in recent months, including former Treasury Secretary Larry Summers, Nobel laureate economist Robert Shiller, Microsoft founder Bill Gates, former vice president Al Gore and venture capitalist Marc Andreessen, note industry enthusiasts, which is encouraging for the industry.

These are the early stages for banks getting involved in bitcoin, and the industry as a whole is hesitant in getting involved before regulators weigh in, says Silbert, the Secondmarket founder.

“Banks are waiting for clearer guidance at the federal level on how businesses are having interactions with bitcoin and there is still some questions on the state level,” he added.

– Sital S. Patel

Follow The Tell on Twitter @thetellblog

Follow Sital @Sital

http://blogs.marketwatch.com/thetell/2014/03/07/major-banks-are-looking-at-bitcoin/

China Sides With Russia On Sanctions; Ambassador Warns "Western Nations Would Be Hurting Themselves"

by Tyler Durden on 03/07/2014 12:22 -0500

Zerohedge.com

Amid a Russian spokesperson "hoping" tensions do not escalate into a new cold war with the US, China has come out (perhaps unsurprisingly) on Russia's side strongly condemning any sanctions:

"China has consistently opposed the easy use of sanctions in international relations, or using sanctions as a threat.”

The comments from China's Foreign Ministry reflect the country's close ties with Russia and confirm what Russia's ambassador to Canada noted, we "can always turn to China if the West follows through on threats of tougher sanctions," adding that "Western countries would largely be hurting themselves if they impose tougher sanctions."

China Sides With Russia On Sanctions; Ambassador Warns "Western Nations Would Be Hurting Themselves"

by Tyler Durden on 03/07/2014 12:22 -0500

Zerohedge.com

Amid a Russian spokesperson "hoping" tensions do not escalate into a new cold war with the US, China has come out (perhaps unsurprisingly) on Russia's side strongly condemning any sanctions:

"China has consistently opposed the easy use of sanctions in international relations, or using sanctions as a threat.”

The comments from China's Foreign Ministry reflect the country's close ties with Russia and confirm what Russia's ambassador to Canada noted, we "can always turn to China if the West follows through on threats of tougher sanctions," adding that "Western countries would largely be hurting themselves if they impose tougher sanctions."

Russian Dollar Dump Could Crash Financial System-John Williams

By Greg Hunter On March 5, 2014

By Greg Hunter’s USAWatchdog.com

Economist John Williams says if Russia sells its U.S. dollar holdings, it could trigger hyperinflation. Could it collapse the financial system? Williams contends, “Yes, it certainly has a potential to do that. Looking outside the United States, there is something over $16 trillion in cash, or near cash. That’s about the same size as our GDP. . . Nobody has wanted to hold the dollar for some time. The dollar, fundamentally, is weak. It couldn’t be weaker. All the major factors are against it. It’s just a matter of what would trigger the massive selling. Nobody wants to hold it. The Russians start selling, and you have China indicating a general alliance here in terms of what’s transpiring. If the rest of the world believes this is what’s going to happen, people who have been wanting to get out of the dollar for some time very easily could front-run the Russians. The scare is on. People will try to get out of it as rapidly as they can.

What would happen if there was massive dollar dumping globally? Williams says, “It would be disastrous for our markets. All those excess dollars coming in, with bonds being sold, interest rates would spike. The stock market would sell off and we’d see inflation. To prevent that and try and keep things stable, the Fed would tend to buy up those Treasuries. It would intervene wherever it could to stabilize the circumstance. It’s going to be very difficult, and it’s going to be very inflationary. Williams goes on to say, “You have to keep in mind, back in 2008, we had one of the greatest financial crises the United States had ever faced. The system was on the brink of collapse at that point in time. What the Fed and the federal government did was spend every penny they could, anything they could create or anything they could guarantee. They did everything they could possibly do to keep the system from crashing. They guaranteed all bank accounts. So, they saved the system, but now what they did has not borne fruit. We have not seen an economic recovery. We have not seen a return of health to the banking system. So, the system is very vulnerable; and if the Russians carry through with their threat, you have, indeed, the risk of it collapsing the system.”

Is this the end of the world as we know it in the U.S.? Williams says, “It does have the effect of creating a hyperinflation, which I think it would. It’s the type of circumstance that will not allow life to continue as we know it because the U.S. is not able to handle hyperinflation. We’re not structured for it. Zimbabwe had one of the worst hyperinflations that anyone has ever seen. They were still able to function for a while because they get paid in a rapidly depreciating currency. It was so rapid it became like toilet paper overnight, but they would go to a black market and exchange it for dollars. We (the U.S.) don’t have a black market to escape from our dollars. Gold is probably the closest thing to that. Gold will tend to rally here as the dollar sells off, baring very heavy intervention by the central banks which you may see. The fundamentals will eventually dominate, and you will see a very weak dollar and very strong gold coming out of this.”

Don’t look for the U.S. dollar as the safe haven because Williams says, “Historically the dollar has been the safe haven in a political or financial crisis, but that hasn’t been the case for four or five years now. Instead, what you have seen is a flight to other traditional safe havens such as gold and the Swiss Franc. The dollar has lost its magic. Nobody wants to hold it. So, if the Russians follow through and convince the rest of the world that they are going to do it and it looks like China may join them, a lot of countries will want to dump dollars and get out ahead of the crowd.”

On the overall economy, Williams says, “It is rolling over, and the numbers are starting to show we are starting into a new recession. You should have an actual quarterly contraction in the first quarter GDP. One of the best indicators of that are retail sales, and they gave a clear recession signal in January. That’s the strongest recession signal since September of 2007, which is three months before the ‘Great Recession’ took place, and I’ll contend it never ended.”

Join Greg Hunter as he goes One-on-One with John Williams of Shadowstats.com.

(There is much more in the video interview with John Williams.)

The Relentless, Systematic Tear-Down Of The Dollar Hegemony

by Wolf Richter - Testosterone Pit

Published : March 06th, 2014

China’s rapidly aging 1.3 billion folks are all trying to make it in the modern world, and they’ll see to it that their country will have major economic and political heft in the future. So in practically no time, China has become the second largest economy in the world. OK, its credit bubble of strenuously obfuscated magnitude will require a miracle, or else the noise of hot air hissing out of it will be deafening.

One of the long-term goals of consecutive Chinese governments has been to make China number one in just about everything. Including its currency. Displacing the dollar as the world’s reserve currency would be nice, and that’s certainly on the list, but first the yuan must become the most used payment currency. How long would that take, barring the accidental annihilation of the dollar as the Fed yanks on yet another experimental lever with unknown consequences?

Not that other currencies haven’t already tried to trounce the dollar, most notably – don't laugh – the euro. At the time of its invention, the thinking went that it would be the common currency of the entire European Union, a concept anchored in the treaties that each member state signed. There are 28 of them, now that Croatia has joined the ever expanding group. The next candidates have been cooling their heels for years, namely Iceland, Macedonia, Montenegro, Serbia, and Turkey. OK, Turkey, whose membership has been hung up in discord since 2004, has hit some big speed bumps recently. But hey. A slick regime change, and off we go.

But to the greatest chagrin of the Eurocrats, and quite inexplicably, only 18 of the 28 member states have adopted the sacrosanct currency, and a third of them quickly became casualties of the euro debt crisis and had to be bailed out to keep the Eurozone together.

During the early years of the euro, when euro-exuberance was still drowning out clear thinking in the business community, there was a whiff of certainty that the euro would become the world reserve currency and the number-one payment currency. Oil would soon be priced in euros. The petrodollar hegemony would be dismantled. It would make the eurozone burst with economic advantages and breathtaking growth. The dream turned into a nightmare in 2008. Meanwhile, the ECB’s promise to do “whatever it takes” in an “unlimited” manner has become the duct tape and bailing wire that keeps the Eurozone together. It's going to be a while before the euro trounces the dollar as payment currency.

So we stop grinning from ear to ear about the demise of the euro and take a closer look at the numbers provided by SWIFT, the NSA-infiltrated, member-owned cooperative that connects over 10,000 banks, securities institutions, corporate customers, and intelligence agencies in 212 countries and territories. If you’ve ever made an international wire transfer, you’ve dealt indirectly with SWIFT, which forwarded copies of your information to the NSA.

And SWIFT tells us that the euro’s share of world payments in January was 33.5%, just below the dollar, undisputed number one, with a share of 38.7%. Alas, undisputed only occasionally. In other months, the euro was number one, for example in January 2013, when 40.1% of world payments were in euros. The dollar was ignominiously in the second place with a share of 33.5%; or in January 2012, when the euro had a share of 44.0%, and the dollar a lowly 29.7%!

The loathed euro has beaten the green ink off the dollar in certain months! And given the Eurozone’s version of Manifest Destiny, the euro, despite all its problems, will continue to grow as payment currency – and by the time the Chinese yuan gets closer, it will have to aim for the euro, not the dollar.

And the yuan is getting closer. The Chinese government is systematically but gingerly boosting its convertibility and global use. In January, yuan payments increased by 30.6% – to “the highest payment value recorded,” said Michael Moon, a Director at SWIFT – versus 4.8% growth for all payments currencies. It edged out the Swiss franc for 7th place, behind the US dollar, euro, sterling, yen, Canadian dollar, and Australian dollar. In December, the yuan had been in 8th place, up from 12th place in October. Over the last three years, the yuan has passed 22 currencies.

But it isn’t there yet, as far as “global” is concerned: 73% of the yuan payment activity took place in Hong Kong. Most of the remainder was carved up between the UK, Singapore, Taiwan, the US, France, Australia, Luxembourg, and Germany. What share of the payments did it grab in January, compared to the euro’s 33.5% and the dollar’s 38.7%? It hit the phenomenal record of ... 1.4%.

So, a little ways to go.

But the yuan was already the second largest currency in traditional trade finance – Letters of Credit and Collections – that Chinese importers and exporters relied on, SWIFT reported in December. It had more than quadrupled its share between January 2012 and October 2013. This currency is hot! And it’s furiously breathing down the neck of the dollar. Its share of trade finance? 8.7%. Versus the dollar’s 81.1%.

“A top currency for trade finance globally and even more so in Asia,” is how Franck de Praetere, SWIFT’s Head of Payments and Trade Markets for Asia Pacific, described the yuan. OK, still a little ways to go.

But the writing is somewhere on the Chinese wall. The euro and now the yuan have been taking share away from the dollar. The euro’s campaign, which has already come very far, will be slow and halting, mostly triggered by countries acceding to the Eurozone. The yuan is the new kid on the block. It moves in leaps and bounds. The dollar’s iron grip on the number-one spot for payments has already loosened. And sometime in the future, its grip on the number-two spot will also loosen. Eventually, the same will happen – is bound to happen – to the dollar as the world’s sole reserve currency. And then the economic equations that the US has leaned on for decades to fund its gargantuan public debt and trade deficit will turn to mush.

The US has abused its phenomenal privileges – including the control of the only world currency – to put global financial stability at risk, “like a truck full of dynamite heading right toward us,” said the chairman of the International Advisory Board of the Universal Credit Rating Group. But a “new financial order” is forming. And there's a timeframe. Read....Next Step In Dismantling The Dollar And US Credit Hegemony

http://www.24hgold.com/english/news-gold-silver-the-relentless-systematic-tear-down-of-the-dollar-hegemony.aspx?article=5248320706H11690&redirect=false&contributor=Wolf+Richter

Russia prepares bill on foreign asset freeze in reply to sanctions – senator

Published time: March 05, 2014 08:56

Edited time: March 05, 2014 12:43

The entrance to the Russian Federation Council, on Bolshaya Dmitrovka Street.(RIA Novosti / Vladimir Fedorenko)

A top Russian lawmaker has revealed he is working on a bill that would freeze the assets of European and American companies operating in Russia in reply to Western economic sanctions.

The chairman of the upper house committee for constitutional law, Andrey Klishas, is sure that Russia must have an enough leverage to deal with the threat of sanctions coming from foreign countries.A team of lawyers are currently preparing a separate federal bill that would allow the Russian president and government to confiscate foreign owned property in Russia, including assets belonging to private companies, the senator told the RIA Novosti news agency.

The bill is in response to the major political crisis in Ukraine and the threat of sanctions against Russia coming from the USA and other countries.

“All sanctions must be mutual,” Klishas stated.

The senator added that he had no doubts that such a measure was in line with European standards. “We can recall the example of Cyprus where the confiscation was, in essence, one of the conditions for getting aid from European Union.