News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Dragon Lady

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

8 mil shares sure looks to be sitting on Bid at .008, MM "ATDF", wow !

Quick Google shows MM "ATDF" to be "Automated Trading Desk Financial Solutions" - seems to be some automated private order routing network or something it seems? So who knows who can place or route orders onto that system? Interesting stuff.

http://www.atdesk.com/pdf/AUTO_OrderHandling.pdf

Remember though- they've (the MM's) have been doing some Bid and Ask "flashing" quite a bit lately- they flashed like 2 million plus last week on the Ask several times that never seemed to fill and then just vanished.

Will be interesting to see if they drop that Bid to the .008 level and if anyone takes a crack at any of that 8 million share block.

BMAK is still parked down now at .0091 on Ask with the usual 10K share block- like setting the "cap" it seems. Maybe they're trying to drive it towards that .008 area to get at those shares?

That's a pretty big chunk hanging out there (8 million X .008 = about $64K worth)- I think the biggest we've seen flashed on this in months, a long time for sure. Lets see if it stays there today, gets filled at all or just vanishes.

Interesting.

http://www.otcmarkets.com/stock/BHRT/quote

Quote, "I was hoping to get more shares at these levels. Thanks for the update."

No sweat. Not really a "update", just facts and observations as I see um happening- just stock watching on the boards.

The Ask just dropped again, BMAK just slid down to .0091. So it might be a great opportunity perhaps to just wait a tad and you can really get some more at better pricing "at these levels" it looks like.

Here's the Level II shot- you can see BMAK lowered the Ask, so might be some real lower pricing perhaps, especially if the Bid drops next too- next level would be .0081 if they chew through those Bid blocks showing at present.

Great time for you maybe.

http://www.otcmarkets.com/stock/BHRT/quote

0.0089 / 0.0091 (560000 x 163000)

Good luck.

Oh, there it went, right as I was typing.

Was going to state that BMAK just slid onto the ask w/ a 10K share block at .0099 and also took up a position on the Bid at the same time at .0088. It's been a while since BMAK "bracketed" it on both the Bid/Ask- very interesting IMO.

I thought maybe the MM's were gonna let it run/breathe maybe today, maybe for a week or so- but looks like Magna or Asher or whoever is "BMAK" isn't done yet I guess?

Guess the "predictions" of a big run and "charts" saying "big run" from some other sites- don't look to be happening today IMO. Also, this stock had already made it's "big run" and blown it's top off at .08 by this date last year- it spent a month or so increasing and building a base before that happened, much higher basing than these low, SUB ONE CENT levels. If it doesn't happen by the end of this week, aka tomorrow, then all these attempts to match this year's prediction that "certainty it will run big" because it did at this particular date last year seem "off" IMO. No comparison IMO this yr to last yr it looks like to me. I just don't see it? The 2014 Feb/March run was over and on the decline by this date last year, March 10th, it was back into decline essentially. And it started from a much higher base than this is at now and had huge buying vol- somewhere hitting like 20 million shares on the biggest day and 8 million or more on several of the other days. Don't see any indication that is happening now or is about to happen? None as "predicted" many times by others?

Not looking good here IMO, still major weakness and strong, unbroken down-trend and selling on higher volume days- look at how high the sell-off vol is now versus yesterday's tiny uptick.

BMAK per several forums right here on I-HUB and also from Google research I did, is an MM believed to be closely associated with Asher and especially Magna- that's what I found be researching them. They are all over this Level II for the past several months.

http://www.otcmarkets.com/stock/BHRT/quote

My 2 cents. I still think it's under tremendous dilution selling pressure from all I can see. No sign yet of any up-trend reversal or similar, and really no buyers coming in or large buying pressure that I've seen? Not seeing it yet?

Looks RED in pre-market and down on initial opening trades. Bid going lower now to $6.40, no Bid support appears here yet.

It's still in weakness looks like. I guess the "predictions" on that other "wonderful site" (claimed reversal and big buying today) are gonna be wrong again today. Guess maybe the charts being used for the leader's "predicting powers" are all out of adjustment as usual over there or something? "massive flow of money" coming in??

Opening to the weak side is not a good sign IMO. There's no buying interest at all in here it seems.

50 DMA is at $6.40 and it looks like it's gonna test it right now

200 DMA is way up at $6.94

So it can't even start a technical trend reversal and get into an actual uptrend until well above $6.94 long enough to get the 50 DMA back above the 200 DMA where it's supposed to be- if not trading in a down-trend. The 50 DMA crossing under the 200 DMA for technical traders is often called a "death cross"- it's not good for a stock that now may be coming up on automated trading algo's of the Nasdaq big boys. They use "death cross" patterns for everything from watching the DOW or S&P major indices as key indicators to individual technical trades- especially shorts from what I've read.

Thus, the stock is in a sustained down trend and the 50 DMA is actually inverted, under the 200 DMA which to the pro traders now of Nasdaq-ville and their auto trading algo's is a short target alert IMO. They short most often on technical weakness- it's largely automated now.

Being a recent OTC convert with technical weakness showing = possible short target for Nasdaq pro trading desks and worst of all the hedgey fund big boys. It doesn't take much right now, dollar wise, to drive a weak stock like this, that much lower.

It's gonna take some major, big time news and buying pressure on volume IMO to get this to even try and turn around and get back into even the beginnings of an actual uptrend and build some support. Right now- it's the slow bleed down looks like to me.

Quote: "The real story behind this company. Thank you for posting."??

So the company's own duly filed and legally binding SEC filings (10-K, 10-Q, 8-K's etc) are not the "real story" of the company's condition, financial facts etc?

But some single, couple of lines on some Power Point "slide" given in some "presentation" is the "real story" behind the company? NOT the 100's of pages of SEC filings sent to, and filed on the SEC EDGAR U.S. Govt database versus ONE SLIDE that has maybe 6 or 7 bullet points on it total- and a few number figures is the "true story" of the company versus all those SEC filed "balance sheets" and "condensed statements of operations" and "cash flow statements" and "going concern warnings" from not only Sr. Mgt in their own words but the words of their duly hired licensed and fiduciary bound auditors, and details of near continuous use of toxic debt financing and near endless dilution of the common stock shares given to the last share issued in detail, etc??

Wow, fascinating to know that a single power point slide with a few brief bullet points on it gives the entire "true story" of a public traded company versus 100's and 100's of pages of legally binding SEC filed annual and quarterly reports and all the rest? This is fascinating and all new to me? I wonder why companies even bother then to file pesky, time consuming "stuff" like 10-Q reports and the upcoming very expensive (as it's audited- ever see what they pay the audit firm, it's in the filing- and it's a lot of money) - all that effort to file a annual 10-K report, when all they need to give the "true story" behind the company is a SINGLE POWER POINT SLIDE? Wow. Amazing and fascinating stuff IMO.

Great "selective info" in the ole Power Point "cliff's notes" version "slide" the company put out IMO. Too bad it leaves out so much other key info about the true, dire financial condition of the company and how "revenues" did't really change much of any of that desperate financial condition IMO.

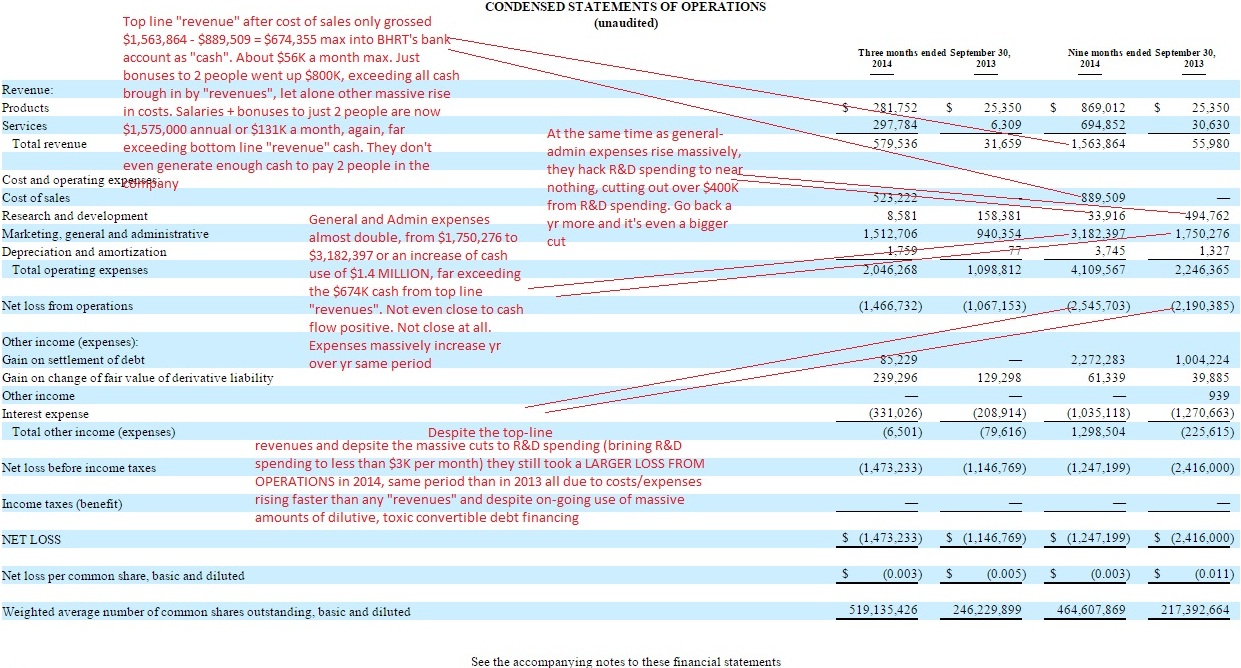

1) Despite what the slide says about top line "revenue" it fails to show that their expenses massively increased and that's despite hacking out their R&D spending to near zero (less than $3K per month). It also fails to show that despite top line "revenues" and continual use of toxic, convertible debt financing- they finished that same qtr that the slide speaks of, with a pittance of $46K total cash in their bank account, against over $2 MILLION in just immediate accounts payable and total immediate debts of $10 million plus.

2) The nifty little slide failed to show the continued "going concern" warnings in the same 10-Q it's speaking of. A condition which speaks specifically of "liquidity problems" - aka a company's possible problems paying their bills in a timely manner as they come due, due to lack of adequate cash, usually a precursor to potential bankruptcy.

3) The nifty little slide fails to show that of course cash use was reduced- when they hacked out/cut over $400K to their R&D budget- for what deems itself to be some sort of "medical research and development" company- and that they've cut far more than that from R&D in the past 1.5 yrs- of course decreasing cash use.

4) The nifty little slide fails to show that despite top line "revenues" that the company is actually taking a larger loss to operations this yr, period over period that last yr as costs/expenses on the "general/admin" line have far out grown any result of top line revenues after cost of sales is subtracted out.

5) The nifty little slide fails to show that the company is still heavily relying on "toxic" aka convertible debt financing, aka "floorless" toxic debt deals- in increments as low as $25K they are so desperate for cash.

From the last filed 10-Q (the one the slide is referring too):

PAGE 12:

"NOTE 2 — GOING CONCERN MATTERS

The accompanying unaudited condensed financial statements have been prepared on a going concern basis, which contemplates the realization of assets and the satisfaction of liabilities in the normal course of business. As shown in the accompanying unaudited condensed financial statements, during nine months ended September 30, 2014, the Company incurred an operating loss of $1,247,199 and used $747,184 in cash for operating activities. As of September 30, 2014, the Company had a working capital deficit (current liabilities in excess of current assets) of approximately $10.0 million. These factors among others may indicate that the Company will be unable to continue as a going concern for a reasonable period of time.

The Company’s existence is dependent upon management’s ability to develop profitable operations and to obtain additional funding sources. There can be no assurance that the Company’s financing efforts will result in profitable operations or the resolution of the Company’s liquidity problems. The accompanying statements do not include any adjustments that might result should the Company be unable to continue as a going concern."

PAGE 26: (toxic debts as recent as Oct 2014, for pittances as low as $25K cash, highly dilutive finance deals with horrible terms)

"Subsequent financing

KBM Worldwide

On October 6, 2014, the Company entered into a Securities Purchase Agreement with KBM Worldwide, Inc., for the sale of an 8% convertible note in the principal amount of $38,000 (the “Note”).

The Note bears interest at the rate of 8% per annum. All interest and principal must be repaid on July 8, 2015,. The Note is convertible into common stock, at holder’s option, at a 45% discount to the lowest daily trading price of the common stock during the 10 trading day period prior to conversion. In the event the Company prepays the Note in full, the Company is required to pay off all principal and accrued interest at 150%, and any other amounts.

Daniel James Management

On October 3, 2014, the Company entered into a Securities Purchase Agreement with Daniel James Management, Inc., for the sale of a 9.5% convertible note in the principal amount of $25,000 (the “Note”).

The Note bears interest at the rate of 9.5% per annum. All interest and principal must be repaid on October 2, 2015. The Note is convertible into common stock, at holder’s option, at a 47% discount to the lowest daily trading price of the common stock during the 10 trading day period prior to conversion. In the event the Company prepays the Note in full, the Company is required to pay off all principal and accrued interest at 150%, and any other amounts."

See the condensed statement of operations- HUGE CUTS to R&D, HUGE RISE in "general/admin" expenses" and LARGER LOSS FROM OPERATIONS this yr than in 2013, same time period:

And see the balance sheet to see the $46K total cash remaining, against immediate debts that are magnitudes larger than that pittance of cash.

IMO, the "slide" tells a tiny portion of a much bigger picture- a picture I don't see fundamentally changed simply because of top line "revenues" - given primarily what's happening on the expense/spending side. All the revenues in the world will make no difference to a company if their expenses always end up being just $1 more every time. This company is not even remotely close to being cash self sufficient and the two toxic debt deals (for micro amounts of cash) as late as Oct 2014 IMO prove that- and then those 2 deals were followed with a Magna "note" also to get more survival cash and then a Magna "credit line"- ALL dilutive to the common stock.

Quote: "They pay their CEO $500k a year, which is way too much IMO. I'd like to see them put some of that back in to R&D or in to other investments. "

Actually it's far, far more than that for just the CEO and the CSO (Chief science officer)- just those 2 "employees" of a company in their last SEC filing stated as having "4 full time and 1 part time employee"- just those 2 combined consume (are paid) $1,575,000 dollars from mid 2014 until their next round of pay increases/cash bonuses which they've gotten every yr since at least 2012. The CEO's annual compensation package of just base salary plus "cash" bonus now exceeds $1 million annually and that's for a near cash broke company that finished it's last qtr with $46K total cash on-hand in their 10-Q filing and that does not include additional "kickers" the CEO gets like stock options (large block grants) and other perks.

Those 2 alone have more than doubled their base pay since 2012 and also received annual cash bonuses (large ones) all as the company R&D spending/expense line has been cut to near zero (about $3K a month total spent on R&D per last 10-Q filing, PAGE 5).

Last filed 10-Q, PAGE 23:

"Employment agreements

On July 28, 2014, the Company’s Board of Directors approved the 2014/2015 salary for Mike Tomas, Chief Executive Officer, at $525,000 per year, beginning July 1, 2014 with an incentive bonus ranging from $150,000 to $500,000. In addition, the Board of Directors will grant Mr. Tomas options to be determined on or before June 30, 2015. The Company’s Board of Directors approved a bonus of $500,000 and options to acquire 10,000,000 shares of the Company’s common stock for ten years with four year vesting and a cashless exercise provision at an exercise price equal to the five day average closing price of the Company’s common stock as of August 1, 2014. The cash bonus may be paid in the form of a six month promissory note.

On July 28, 2014, the Company’s Board of Directors approved the 2014/2015 salary for Kristin Comella, Chief Scientific Officer, at $250,000 per year, beginning July 1, 2014 with an incentive bonus ranging from $100,000 to $300,000. In addition, the Board of Directors will grant Ms. Comella options to be determined on or before June 30, 2015. The Company’s Board of Directors approved a bonus of $300,000 and options to acquire 5,000,000 shares of the Company’s common stock for ten years with four year vesting and a cashless exercise provision at an exercise price equal to the five day average closing price of the Company’s common stock as of August 1, 2014. The cash bonus may be paid in the form of a six month promissory note.

"

That right there, from July of 2014 to July of this yr, 2015, means just those 2 "employees" are receiving $525K base + $500K cash bonus + $250K base + $300K cash bonus = $1,575,000 in annual compensation (not counting stock awards n other forms of compensation)

To see how massive the rise in the rate of pay to just those 2 individuals has been since 2012- see the " executive compensation table" from the company's last filed 10-K (annual report):

To see what has happened to the massive cuts to R&D spending have occurred while the corresponding huge increases in "general and admin" expenses have occurred - see the "Condensed statement of operations" PAGE 5 of the last filed 10-Q qtrly report:

And what was the company's cash and asset position as those very large pay increases w/ "cash" bonuses were being awarded? Well, pretty desperate IMO when looking at their own, latest filed 10-Q balance sheet PAGE 4, latest filed 10-Q:

To see what the common stock has done as these 2 "employees" have received massive pay increases, essentially wiping out the common share holders to the tune of a 99% plus loss to the common shares- see any multi yr stock chart such as the one below. The common stock shares have lost approx 98% of their value since the present CEO took over in mid 2010. From approx then .50 cents a share to now approx 1 CENT a share.

50 -1 = 49/50 = .98 X 100 = 98% LOSS to common.

That kind of stellar common stock "performance" as shown in that chart gets one large annual compensation increases going on 3 yrs running and large "cash" bonuses too boot and over a $million in annual compensation to just one of the 2 people. Not bad, not bad at all IMO.

Quote, "That's a great article.".

That's an old article and makes no sense IMO. Explaining why a company that's been around for what, 15 yrs is like a "garage operation" and still only worth one CENT a share or whatever? A long ramble about a bunch of successful companies with zero relationship to this one- and why because they were successful, one is now supposed to "imagine" what one cent invested in them would be worth today? What? But they were never penny stock companies that lost over 99.8% of their common share value after having over $100 million in sunk capital lost on them? So what's the "comparison"- there's no logic to that IMO? It just makes no sense at all to me?

What sense does that make asking what the "value" of ONE CENT is? The value of ONE CENT is well, always ONE CENT and always will be ONE CENT. What other explanation is there? Trying to explain away why the common shares of this particular company have lost 98.8% of their value (actually a tad more at today's prices probably) and why they now trade sub ONE CENT via some convoluted arguments and why a common shareholder is supposedly supposed to feel good about that, makes me confused if anything?

Makes zero sense IMO. Just another "blog" that hasn't made a difference to the share price since it was released well over several weeks ago or a month or so now? They don't even date their material on that tiny blog site- any info published should always have a date stamp.

BHRT is trading today on much lower volumes and just on the spread really. The Bid hasn't moved up at all. Saw this same pattern several times in the past few weeks when BMAK moves off the Ask for a day or two. No real buying going on here- just no serious buying interest at all, even at sub ONE CENT. Volume is not even a 3rd of what it was on the past few weeks of large selling days- where it was doing 3 million plus shares a day. Spread today between Bid/Ask right now is almost 10% on very slow moving volume and long periods of "flat-lining" where little trading is occurring (aka ill-liquid essentially).

Nothing new here IMO.

No, Quote, "Yeah it's on record"

Nothing there "on the record" in which the CEO says specifically that there will be "no news announced until the 10-Q is released".

Simply does not exist. I did not hear it or read it- it's not there.

http://www.sec.gov/answers/form8k.htm

This is one place (among many)in which the SEC discusses a public companies obligation to release "material event" items (aka important "news") to public shareholders- there are dates given, as in maximum number of days allowed in which the filing must be made to disclose the info to the public.

Quoting from the SEC page:

" Form 8-K is the “current report” companies must file with the SEC to announce major events that shareholders should know about."

http://en.wikipedia.org/wiki/Regulation_Fair_Disclosure

Discusses "fair disclosure" law- again, the concept that key "news" when known, must be made available to all the public at the same time, as in no "selective releases", holding back key "news" that might affect the course of the business, etc

Quote:

"Regulation FD fundamentally changed how companies communicate with investors by bringing more transparency and more frequent and timely communications, perhaps more than any other regulation in the history of the SEC."

Another govt. website talking about the importance and requirements for public traded companies to disclose "key events" or "major events" aka " big news" that would be "material" to the business in a timely and equal manner to all the public:

http://investor.gov/introduction-markets/how-markets-work/public-companies

It's all over via simple research. Material events must be made known- they can't be hidden if they can affect the course of the business, it's financial condition, have a major impact on the stock either positive or negative, etc. It's a hallmark of public company disclosure laws. Nothing new or unusual. "material events" get disclosed when known. Simple as that IMO.

Please look it up yourself. Not my job to look things up for others.

Material information is disclosed when known- public companies can't "sit on news" or "material events" until convenient.

Cite otherwise please, using SEC law.

QUOTE, "Mike Thomas states that there wouldn't be any news until after the release of the 10K. The 10K is now upon us, any day now."

Is that Mike Tomas, CEO "states there wouldn't be any news until after the release of the 10K" in writing somewhere - where it can be viewed?

A public traded company can't "sand bag" and hold back material event news items or anything of financial or otherwise importance to the company. If they "know it" - then it must be made public. That's what being a "public traded" firm is all about.

So I don't understand how a CEO can say "we're not releasing any news" until event XYZ (the 10-K being released for example) unless the CEO for 100% is saying that there is nothing, no "news" to be released and they know it with 100% certainty?

Public companies can't "sit on" material events and release them when convenient- that would not be per SEC laws per my understanding. If they "know it" then it's to be made public to all of the public at the same time, as soon as it's known and can affect the stock share price or business either positive or negative. That's my understanding.

Which tells me- they have "no news" to release or they'd of already done it IMO.

Bid dropping and vol is low- they had to drop the Ask also as there's over a million shares parked for sale but hardly any buying interest.

Given the sharp drop-off in vol (and this did this a few times over the past month or two)- I'd say some "big boy" house a) just got done either converting some convertible debt shares or b) Magna or similar got notice of a "draw down" request for the credit line perhaps- and spent a few weeks driving the price down on mega volumes (it's been averaging 3 to 4 million shares a day for weeks)- in order to set the conversion price for the shares lower based on the "floorless" aka "market based" conversion formula of the lowest of avg of X number of trading days prior to conversion blah, blah, blah.

BMAK moved way off the Ask, now it appears it's back to "regular trading" at least for part of yesterday maybe and for sure today it looks like- but there's very little volume and just no apparent real buying interest IMO from watching the level II and the volumes.

Over 1 million on the Ask and it's still there- only moving little bits in like 10K chunks or less (buy's of a few $100 at a time, total vol on the day so far maybe $3K or so)

I don't see any rush of buyers barreling in here at even 1 CENT and now sub one CENT again as it looks like the MM just dropped the Ask as they couldn't get much action for several hours on 1 million plus shares at 1 CENT.

Will wait to see if any buyers appear from somewhere or if this lasts for more than a few days before BMAK or whoever possibly moves back down on that Ask side. (again, saw this a few times over the past month or so).

See where they close it today and if anyone steps up to buy enough to chew through over 1 million shares for sale today.

http://www.otcmarkets.com/stock/BHRT/quote

0.0091 / 0.01 (551000 x 1393641)

(1.3 MILLION on the Ask, no big takers as of yet it appears, 2.5 hours into trading day. Over 2:1 ratio to the sell side, Ask)

BMAK has backed way, way off the Level II Ask.

Looks like the MM's want to let it breathe a little or are done converting "maybe" for a bit- they did this a few times over the past few months since the Magna deal and all. Exact same pattern. Notice, the day BMAK is moved way off the Ask, there isn't even an opening trade, it's gonna go "flat-line" slow motion now IMO with long periods of no trades, etc. Yesterday had over 2 hours w/o a single trade printing and much lower daily volume.

There's a million plus shares for sale on the Ask right now for starters w/ only 10K on the Bid side (all tilted to the sell side). But no single buyer or opening trade. This has been the pattern for well over a month now that I've observed- I'd expect a big drop in vol now and maybe the MM's will open the spreads real wide and "try" and get it to move up a bit. We'll see. That's been the pattern- they pounded it down for weeks on mega high volumes and now not even an opening trade and the Ask is moved up and BMAK moves off the Ask. Yep.

See what happens here now.

0.0095 / 0.01 (10000 x 1026800)

Only 10K on the Bid and nothing moving and the Bid not really moving up and after that 10K on the Bid (a lousy $95 bucks worth) it's back to .009 and below.

See how long it takes to even get an opening trade and how wide they open the spread today and how much the daily vol drops off- if this is the pattern the MM's have used periodically over the past 2 months or so when they want to "run it" a tad after apparently unloading convertible shares or setting the price of conversion by driving the price as low as possible IMO.

Farview- agree.

The short and sweet summary way to put it: is they have to come up with some pretty big bucks here pretty soon, somehow, someway.

That's the key to the entire puzzle going forward at this point IMO.

How they get those "big bucks" to keep the train rolling on down the track is the more than $million dollar question. Lots of theories, lots of speculation - but no for sure yet.

Only solid pieces of data in place at the moment that I'm aware of:

1) They filed a $100 million shelf registration with the SEC. Meaning they can "tap" into as much as $100 million in cash via selling that amount of their common shares of their stock as a secondary (non IPO) type offering(s). As far as I'm aware that shelf registration remains open and good to go if they want to use it. Will need to go back and read it again - not sure if it has an expiration of some sort or not?

2) In Dec of 2014, OCAT hired qty-3 underwriters and were proposing to sell approx. $60 million worth of their stock using that shelf registration as the underlying mechanism. Hiring qty-3 pretty high quality underwriters and having them do a lot of up front work and draft a prospectus and apparently start a mini "road show" and run a "book" and all is not cheap- I'd be totally guessing but spending say $250K to $500K for those services in just up-front fees would not surprise me in the slightest. So to pull the plug on that deal after plunking down some pretty serious coin doesn't come cheap- and thus probably isn't a willy-nilly decision for Sr. Mgt to make.

3) We then found out in early 2015 that the underwritten secondary offering of approx $60 million worth of stock (slated to fund the phase II trial, get it really rocking and rolling among paying other expenses) - we found out that offering was "pulled" and the only wording was "due to market conditions". As far as we know- the qty-3 underwriters stopped all activities they were hired for and that all as of today is essentially done, stopped, over- whatever one wants to call it. At least for now apparently.

That to me is about it so far. I don't think today's "presentation" by the CEO shed anymore light on anything not already known- especially in the critical area of cash, funding and how to fund the key phase II and really move it ahead which is a very expensive undertaking. From all appearances- the only certainty from a financial standpoint right now is they, OCAT are for all intents and purposes "living off of" Lincoln, which in and of itself is a dilutive finance vehicle and not a high quality one at that and is "fund amount limited" to less than approx $20 million or so (probably less even now, as they'd of had to have been tapping it to keep the doors open IMO and pay common monthly bills since the last balance was known).

So that's about it IMO. Cash and funding is the key to it all at this point I think and those questions are open and unanswered it appears. I think until all that is made crystal clear- the common shares probably will remain in a position of weakness and rudderless- in the slow down trend they've been in now for a long, long, long time.

Funding, big cash would be the single biggest catalyst I can see moving this stock one way or the other. Dilutive big bucks might cause down pressure on the stock for a while- but may even bump it up as uncertainty would be removed. A real golden type financial infusion of some sort- enough to fund the phase II and it probably could get this moving in a reversal uptrend and out of the bottom dragging it's stuck in now.

My 2 cents.

BHRT is flat-lining today too. Interesting in that we really haven't seen that in a while (several weeks I believe since this long a period of no-trade?)

Last trade was 10:22 Eastern. It did a big million shares or so almost out of the gate- but has now sat parked w/o a single trade since 10:22 Eastern? It's now 12:45 Eastern, 2 hours later and not a single trade?

And that's with a lousy 10K share block ($96 bucks worth on the Ask) which tells me no takers even for $96 bucks worth on that Ask price?

It's been blowing off 3 to 4 million shares a day for a few weeks now, and now it just sits, parked for 2 hours w/o one single trade printing in 2 hours?

This is a strange OTC beast IMO. Strange indeed.

http://www.otcmarkets.com/stock/BHRT/quote

0.009 / 0.0095 (355000 x 10000)

BMAK still sitting in 1st position on the Level II Ask w/ a 10K share block at .0095 for 2 hours now, but not a single trade has printed since 10:22 Eastern? 355K shares are on the Bid but again, no takers there either at .009?

Go figure on that one?

Update:

Uh, just hit click on the post- and now see a single spike on the daily chart just appeared, literally as I hit click to post- so it took 2 hours and looks like a trade will print now. Looks like it's on the Ask side, or at least above the Bid by the spike up. Will see what happens here now.

Auger, Yeah, I've read that one too, "The GARY ZONE", LOL !

It's selling below or no better than where ole Gary Rabin left the common share price(Gary being the SEC violator previous, former CEO) - which is certainly pretty amazing IMO given all the "big news" and "new" super management team and stacking the "C" level with high paid new hires and what not?

Just saw a typo in that post I made, "bid day" should be "BIG day". Another one come and gone- and well, it's just nothing more it looks like than another ole "presentation" (which is what I figured). If anything the info seems to indicate delays perhaps, not major progress or the much spoken about "JV" or all this other "stuff" being bantered around (gotta listen and re-read the slides again, but I thought I sensed or heard some delays to the previous Q-1 targets, promised time line in there?). Several bubbles due for Q-1 aren't even completed and I believe the wording, something like "we hope in a month or two" something like that was said- which means those may be Q-1 "misses" per the big plan. End of Q-1 is end of this month- the ole clock is ticking and waits for no one.

Oh well, I'm with you per your previous posts; looking like "on the side lines" until I see what the dilution-solution is (another good saying IMO). I think if they have to go the dilution route, which IMO is a strong, strong possibility- then there's gonna be down side pressure, maybe a lot of it. Why buy now if I can buy it cheaper later?

BMAK just slid back into 1st position on the Ask w/ a 10K share block at .0095.

http://www.otcmarkets.com/stock/BHRT/quote

That tells me, IMO, that it's not going much above that today. BMAK tends to set the day's "cap" price from what I've seen now for about a month of watching the Level II on this one.

Looks like dilution shares and the MM's associated with those 10's of millions of dilution shares are driving this ship and the share price, at least for now, IMO.

Always said, dilution and lots of it, especially when in combo with massive use of "convertible debt" (aka floorless, toxic debt deals) has to have consequences sooner or later (negative to the common share price IMO)- I just don't see how it can't and here's what the SEC themselves says about it too:

http://www.sec.gov/answers/convertibles.htm

From THEE SEC:

"By contrast, in less conventional convertible security financings, the conversion ratio may be based on fluctuating market prices to determine the number of shares of common stock to be issued on conversion. A market price based conversion formula protects the holders of the convertibles against price declines, while subjecting both the company and the holders of its common stock to certain risks. Because a market price based conversion formula can lead to dramatic stock price reductions and corresponding negative effects on both the company and its shareholders, convertible security financings with market price based conversion ratios have colloquially been called "floorless", "toxic," "death spiral," and "ratchet" convertibles.

Both investors and companies should understand that market price based convertible security deals can affect the company and possibly lower the value of its securities. Here's how these deals tend to work and the risks they pose......"

LOL, quote: "Ocata has a placebo eye that is called the "untreated eye".

Well, all except that's NOT even close to what a "placebo" is or is used for or does, etc

“Don’t waste your time quoting TV shows. TV rots the brain.” Bob Smith (From “The history of TV”, Season 1)

$6.60, oh my my. Not looking good here for ole Nasdaq listed OCAT. Nasdaq shark short desks must be smelling blood in the water IMO. If those pro-short desks trading algo's start to pile on- it's look out below. The Nasdaq is where the big boys play- and they got near bottomless bank and coin to work with on their side. Those pro Nasdaq shorts IMO pray daily for weak stocks- like a recent OTC transfer with little cash and only a dilutive credit line like Lincoln that they're using to survive on.

Wow, SOLID RED and dropping, $6.74 on another "bid day".

Today's "Presentation" looks like a huge hit out of the park as always?

Just like all the other "big happenings" of recent (the "article", the "uplist", a lot of "PR", name change, the logo "thingy" and all the rest) - and it's trading below where it was over 3 yrs ago on the OTC.

Just no real buying interest on this one at this stage of the game it seems IMO, Nasdaq or no Nasdaq?

Oh well, it's wait and see time. Stepping in front of this here is likely to result in getting run over by a bus. I'll wait for a lower entry point which seems like a certainty to me- they're gonna have to massively dilute to fund any phase II trial unless they get a magic pile of money from somewhere else. Today obviously wasn't "magic pile of money announcement day" at the ole "big presentation" so that means more wait and see to me.

With no trial funding in place and large dilution their most likely solution that I can see- this is probably a prime target for the NASDAQ pro-short desks now. If they start to step on this thing, they can take the price down real quick. Need a lot of buying pressure now to counter all the stops and disappointed buyers that will get taken out in here if it drops much more IMO.

They got a whole new group stuck with a pile of shares at .08 or above or else a healthy loss- their Nasdaq debut crowd. I'm sure that group is real happy? Don't think others aren't watching that group who got stuck with shares above .08 that lost their value in a matter of days - and now just went to the side lines to wait it out and find the real bottom.

Looking real weak in here. Technical weakness as it just broke the 200 DMA of $6.93 and it's already in major technical weakness as the 50 DMA and 200 DMA are "inverted" - which is always not good and a sign of a down trend being solid in place.

Remember, now that it's on the big-boy's playground of the Nasdaq, their pro trader short desks and hedge funds and all- they short stocks using computerized algo's that look for this kind of technical weakness and then just pile on it- usually via automatic HFT trades and similar. Don't even always need a human sitting at a trade desk- their algo's just hunt and sniff and look for weak, down-trend stocks and then short um at-will. That's the big-boy land of Nasdaq.

My 2 cents.

Quote, "Bounce time IMO"??

Not seeing it- the stock has no real buying interest or buying happening yet?

All I see is that MM BMAK has moved a few levels back-off the Level II which they did several times in the last month or so- like a "breathing day" and right now they're moved out to .01. However, they did this several times in the past month where they moved their 10K share block off that Ask for a day or so, but sometimes it didn't even last a day and they moved right back down, always right on the Ask or usually one level off, always with a 10K share block.

Right now NITE (well known MM) is sitting parked on the Ask w/ a 10K share block at .0096 which would be a lousy $96 bucks worth and no one, no buyers are rushing in to get those shares. If there was any real buying demand, those 10K shares should be gone faster than a blink- but they're just sitting there parked, w/ no one interested in paying .0096 for um, $96 whole dollars worth. Hardly some reversal or new trend IMO.

This needs to double in price to the .02 area just to get back to the 200 DMA area and even come close to "starting" to try and reverse what's now a 10 month plus down trend line.

This is just trading this AM on the spread being opened up a tad by the MM's- the Bid is really not being moved much at all, only slightly off the .0082 to .0086 area of the past week.

There's a 1 million share block parked on the Ask for sale at .01, one level off on the Level II. Until that goes nothing much is happening IMO. There's only 150K shares (about $1,300 buck worth) left on the Bid side to chew up and it's back in the .008's again.

Still seems to me that dilution shares and a lot of um- and BMAK and a few other MM's with the dilution shares are still running and controlling the Level II from what I see.

0.009 / 0.0096 (150000 x 10000)

http://www.otcmarkets.com/stock/BHRT/quote

My .0095 cents worth (still a SUB ONE CENT stock in March now)

RED first day of March on higher than avg volume.

BMAK sitting all day on Ask with a what? You got it, a 10K share block of shares. BMAK seems to now essentially "set" each day's "cap" when watching on the Level II.

Also, saw for certain at one point a 2 million plus share order sitting for sale on the Ask, but then it seems to disappear but not be reflected in the daily volume numbers- are they, the MM's flashing large sell orders now too or something? (saw same thing at least one other time last week and then also an actual day where some very big blocks showed and at least partially filled- usually very, very close to end of day)

As a previous poster just pointed out earlier- it seems IMO that dilution trumps all at least for now. Charts, PR, "news"- nothing has seemed to overcome the extremely large share overhang and dilution that has occurred and is presently apparently "in play" - as in 10's of millions of low priced shares if numerous past convertible debt deals are being converted along the way here.

And, IMO, the biggest "wild card" now is Magna sitting out there (my web research shows some pretty credible sounding sites that say the MM "BMAK" is closely associated with Asher and/or Manga and I know I saw BMAK show up almost to the day that the ink dried on that first Magna convertible "note" deal, followed by the Magna credit line now being in place).

10-K will be interesting IMO as one will know for certain if a "draw" has been made on the Magna credit line- it will either state it in direct wording IMO or will be seen in shares issued to Magna or in the cash balances via some simple math being worked out- if a large block of cash arrived recently out of nowhere, I'd probably assume a Magna "draw" was made then.

Interesting stuff IMO. Lower highs and lower lows on very, very high volumes and not even a remote shot yet at breaking a now 10 month plus down trend that's fully intact and inching lower each week for all intents and purposes based on the long term trend line.

Very weak still in here at this point, on this one IMO. Very weak. A long road back to the 200 DMA and some enormous buying pressure would be needed to reverse the selling volume that's now been going on for over a month now.

My .0089 cents worth.

I think that link is sorta talking about Nasdaq and similar "listed" bio-tech stocks "leading the market". Which is fine and great and all.

But I sorta doubt IMO they're really including sub ONE CENT OTC penny stocks in their "leading the market" part of their analysis of the bio-tech sector and portion of "the market". Especially given how this stock, BHRT, is pretty much in a steady down trend and decline and is thus not actually "leading" anything for months and month now IMO.

Just really sorta doubt it.

My .009 cents worth

LOL, Quote, "Since safety has been proven, President Obama may want a legacy issue; especially since President GW Bush significantly slowed research in this area. Executive action is very possible IMO."

Wow. A sitting POTUS now "grants drug approvals too"?? What?

Has there ever been an "executive action" granting an FDA over-ride and drug approval? Ever?

Also, safety has NOT "been proven". Not possible via an 18 person, very tiny, phase I trial. NO way, no how IMO. One needs to look to the FDA drug approval process and see what part of the purpose of a Phase II is, which includes increased data using much larger population samples to continue the process to prove long term and more complex population subset drug "safety".

The Street.com, says SELL on Ocat. The Street.com aka "Cramers" site, aka Cramer of CNBC.

Well, there's probably IMO the first it looks like, much talked about, "coverage" and "visibility" that would come via being on the Nasdaq now.

http://www.thestreet.com/quote/OCAT.html

It says "SELL recommendation" on OCAT:

Quote-

"The Street's Analysis is Quantitative-driven / Fundamental Analysis. Here's the report:

RECOMMENDATION

We rate OCATA THERAPEUTICS INC (OCAT) a SELL. This is based on the dominance of unfavorable investment measures, which should drive this stock to significantly underperform the majority of stocks that we rate. The company's weaknesses can be seen in multiple areas, such as its weak operating cash flow and feeble growth in its earnings per share.

HIGHLIGHTS

Net operating cash flow has decreased to -$5.99 million or 21.55% when compared to the same quarter last year. In addition, when comparing the cash generation rate to the industry average, the firm's growth is

significantly lower. OCATA THERAPEUTICS INC's earnings have gone downhill when comparing its most recently reported quarter with the same quarter a year earlier. This company has reported somewhat volatile earnings recently.

We feel it is likely to report a decline in earnings in the coming year. During the past fiscal year, OCATA THERAPEUTICS INC turned its bottom line around by earning $0.00 versus -$1.00 in the prior year. This year,

the market expects a decline in earnings from $0.00 to -$0.30.

The company, on the basis of net income growth from the same quarter one year ago, has significantly underperformed compared to the Biotechnology industry average, but is greater than that of the S&P 500. The net income increased by 35.3% when compared to the same quarter one year prior, rising from -$5.75 million to -$3.72 million.

This stock has managed to decline in share value by 2.52% over the past twelve months. Regardless of the rise in share value over the previous year, we feel that the risks involved in investing in this stock do not

compensate for any future upside potential. The revenue fell significantly faster than the industry average of 36.4%. Since the same quarter one year prior, revenues slightly dropped by 2.5%. Weakness in the company's revenue seems to have hurt the bottom line, decreasing earnings per share."

Looks like OCAT is getting some "coverage" now like all Nasdaq stock typically do. "Coverage" can be good or bad I guess IMO -it cuts both ways.

Totally agree Aug. And 3 years to finish a tiny, tiny phase I. 18 patients or whatever it was.

If that's the track record to date- then year 2020 IMO is the fastball track. Phase II is not unusual to take 1 to 2 yrs or so minimum. A large, good sized well run FDA level Phase III? Not unusual in the slightest to be 2 to 3 yrs from start to "first data" let alone the compiling then of the data, the writing of the FDA submission (which isn't some 2 sided form to be filled out) but looks like a small text book when submitted- 100's and 100's of pages long typically, an enormous undertaking.

To have this complex a process involving the human eye just blown off as some "slam dunk done deal" now just cause they crossed the first baby step of a tiny Phase I is IMO folly.

This company has a long, hard and expensive road still ahead to get near even attempting an FDA submission, let alone the holy grail of an FDA "approval". The biggest and the best of "big pharma" who have legions of expert staff, entire departments dedicated to just "FDA regulatory affairs" and near bottomless money/cash hoards- they fail to get most of their initial drug "candidates" ever approved. That's just the reality of it.

Here's an article or two on what it costs and takes now days to get ONE DRUG/complex medical process FDA approved- these are from "think tank" and industry group research firm numbers- it's daunting:

http://www.manhattan-institute.org/html/fda_05.htm

Note in the beginning, key line: 90% of COSTS OF A DRUG APPROVAL are incurred in the large, lengthy, difficult PHASE 3 process.

http://www.forbes.com/sites/matthewherper/2012/02/10/the-truly-staggering-cost-of-inventing-new-drugs/

http://www.forbes.com/sites/matthewherper/2013/08/11/how-the-staggering-cost-of-inventing-new-drugs-is-shaping-the-future-of-medicine/

It ain't a "slam dunk" IMO, not by a long, long shot. Not given the industry wide, well researched "norms" and staggering costs, etc

My 2 cents

Quote, "A placebo arm is needed for comparison to study (test) criteria in question."??

That's actually not what a placebo arm is or for, or does, etc; not even close.

The "placebo effect" is used for many issues and to reveal many issues surrounding the testing and attempts to proving the EFFICACY (statistical relevance) of a drug/treatment process in medicine. It's used to screen for numerous issues that are very difficult to otherwise prove, screen or account for when trying to show efficacy and most important also, understand side-effects in human population sub sets. Since it's impossible (because of costs, time, logistics, etc) to test every new drug or medical or surgical procedure on literally millions of patients - one must use statistical methods of "sampling" and try and get good cross representations of all possible human sub set groups in good trial design (for example younger patients response versus older patients, patients with concomitant diseases or health issues versus those deemed 100% "healthy", aka are some patients taking other medications that may interact with the proposed new drug- placebo helps test and show any statistical relevant interactions if they exists, testing for side effect issues one of the most critical things a placebo arm reveals- as in did 30% of patients get eye pain post treatment regardless of whether it was the "cell" injection or a neutral "saline eye wash solution" or similar- that is what placebo does and is used for among many, many other things.)

Placebo testing is not limited by any means to orally ingested medications or "pills" - where is that written? Now days they even test some surgical and other medical procedures against "sham" or placebo arm treatments- as placebo has been shown to have not only "psychological" effects but neurological, physiological, pain and brain receptor effects, immune up or down regulation effects- pretty much anything and everything involving the human body. It's one of the greatest mysteries of all of medicine.

The single biggest area one can see OCAT needing "placebo testing" IMO would be for side effect statistical measuring and ability to show the FDA or similar with hard numbers the amount, or lack of amount. from a statistical human population standpoint- of what side-effects are known, expected and thus proven safe or not across all populations sub-sets (old, young, middle age, taking other drugs, having other medical conditions/health problems, etc) - the stuff the FDA always wants to know and will demand is in a drug "cut sheet" as quantified numbers so a practicing physician can know what to expect.

In other words, the physician will be able to read in the drug labeling and "cut sheet" that 18% of treated patients are likely to have "immediate eye swelling for the first week of post treatment" and 3% showed possible severe blah, blah and if blah, blah is seen- consider it a potential serious side effect and monitor the patient for X number of weeks. THAT is what a drug "cut sheet" looks like. Not the little one pager you get at the pharmacy like Wallgreens or whatever. If you've ever been handed a sample pack of a new drug by your physician- it will almost always have in it the true "cut sheet" - which is a huge, multi fold out piece of paper than when opened up typically takes two hands to hold, is double sided and printed in micro print- enough to fill pages and pages of a small book. It shows the atomic structure of the drug, describes the chemistry of it, the "theoretical mechanism of action" and massive amounts of info on trial results, statistics, expected side effects, etc. It's the equivalent of what will one day be published in the "Physicians Drug Reference" or a similar tome and the pharmacological text books and similar.

That is a "tiny" bit of info as to what "placebo" is about and used for- it's massively complex and way, way beyond the simplified, totally incorrect one-liner given in the other post. And it's not limited to oral medications or "pills" or whatever the claim was. Not by a long shot.

Quote, "Do you have a link from the FDA about needing a "full placebo arm"?"

Well, I for one am not aware of a single drug ever approved in "modern" times (probably the last 20 yrs ) that didn't involve being tested against placebo in some form or another (it's possible I'm sure that a few may exist)? It's in the hand-out, detailed cut-sheet on every drug on the market I've ever seen- how that drug performed against a placebo to show statistical, proven efficacy. In fact, numerous articles have been written and published recently about the "problem" big pharma faces of not "beating the placebo" as being one of their most troubling problems- industry wide. Their best "Drug candidates" often can't beat the common sugar pill or a "sham" treatment.

Here are numerous links about the FDA and "placebo"- numerous links and also links about the enormous complexities and lengthy time periods faced during a new drug approval process.

Here, here is just a recent one from the enormously well funded Michael J. Fox Foundation and how one of their most promising "drug candidates" was recently sunk and flushed in Phase II for "lack of ability to outperform the ole placebo". (added in a few more links writing about the "placebo problem" that plagues the pharma/bio-tech biz, the problem being they often can't beat or prove efficacy against the placebo arm and these are some of the biggest, well funded and most experienced drug companies on planet earth)

https://nwpf.org/stay-informed/news/2009/08/placebos-one/

http://www.wired.co.uk/magazine/archive/2009/10/features/the-placebo-problem-big-pharmas-desperate-to-solve

Here is the FDA on the "new drug approval process" (daunting and long and expensive)

http://www.fda.gov/Drugs/ResourcesForYou/Consumers/ucm289601.htm

http://www.fda.gov/drugs/resourcesforyou/consumers/ucm143534.htm

Discussion of trial design - "placebo" beibg one of the key methods IRB's consider:

http://www.fda.gov/RegulatoryInformation/Guidances/ucm126501.htm

From the FDA's own "History of the FDA and drug regulation" page:

http://www.fda.gov/AboutFDA/WhatWeDo/History/Overviews/ucm304485.htm

Quote from the FDA itself:

"Although several kinds of randomized controlled trial methodologies can be useful to researchers and regulators, ultimately, it was the randomized, double-blinded, placebo controlled experiment which became the standard by which most other experimental methods were judged, and it has often subsequently been referred to as the "gold" standard for clinical trial methodology. "

Again, I'm just not familiar with many, if any modern FDA approvals being made these days (could be wrong?) through the phase II and then much, much larger and difficult phase III in which a "placebo arm" is not required or strongly preferred to be used by the FDA review boards.

My 2 cents. No way IMO that OCAT skips a phase III on "the eye"- about as close a main line into the human brain (via the optic nerve) as one can get. If one wants to get a drug quickly into the human brain- just put it in the eye and it's there faster than one can blink. The eye is a very critical, "close to the brain/blood barrier" part of the body as far as I'm aware? I'd highly doubt the FDA is going to take anything lightly that deals with a drug process and the human "eye".

2 MILLION plus on the Ask, sell side, Wow !!

And BMAK is slid down one level off the Ask with a 10K share block at .0095 (as always it seems now for the past month or so at least now)

Looks like BMAK then is "setting the cap" most likely for the day at around that .0095 mark and the Bid/Ask is now heavily tilted to selling.

0.0088 / 0.0095 (138000 x 2019020)

About a 15:1 at least ratio to the Ask, sell side. That's a lot of shares to chew through on that Ask, they look to be unloading more selling for "someone"- who, who knows?

http://www.otcmarkets.com/stock/BHRT/quote

Only about $2,500 bucks worth on the Bid presently- that if it gets chewed up would drop that Bid quickly back to that .008 range.

Seems for at least now- they wanna get around .0095 for those 2 million plus shares they're unloading for some "big boy" is seems IMO.

Still a lot of weakness and selling, down-side pressure here from that Level II stack, looks to me.

Well the name "Bioheart" doesn't appear in a single place in that link to some "Global Stem Cell Group" China thingy whatever (not that I could find via reading it?)- so not sure what difference it makes then to Bioheart? As far as I know- it's not even clear what "partnership" Bioheart even has with "Global Stem Cell Group"??

Bioheart has had a lot of "partnerships" claimed over the years IMO and most of um I never heard or read about again later on? Not sure why that is, but that's what I've found many, many times.

Here is a recent example, the South Africa "partnership" as described in grand sounding (IMO) PR- but didn't sound so grand in the ole SEC filing once it came out, IMO.

The original "South Africa Partnership" PR's:

http://www.marketwired.com/press-release/bioheart-announces-joint-venture-in-south-africa-otcbb-bhrt-1923668.htm

http://finance.yahoo.com/news/bioheart-announces-grand-opening-facility-120000841.html

Sounded pretty great, it was a "partnership" sorta-kinda I guess?

Well, here's what the latest filed 10-Q had to say about it- just a "tad" bit of a different story IMO form those PR:

Latest filed 10-Q, PAGE 23:

"Joint Venture

We announced a joint venture in South Africa and the facilities called “South African Stem Cell Institute” were successfully opened in September, 2014 with the intention to retain a 49% ownership of the new entity. As of September 31, 2014, however, there was no formal legal entity established and no formal operating agreement for this joint venture. In additional the Company has not yet incurred any material expenses associated with this venture. Management has concluded that as of September 31, 2014 this announcement is not material to the Company’s financial statements."

"partnerships"?? Been a lot of um "announced" over the years IMO. What they amount to? Never seems clear to me. That's my 2 cents. The words Bioheart don't even appear once in the link/press release provided. Don't see how it makes any difference then to Bioheart or why wouldn't they specifically be mentioned?

My .009 cetns worth.

Quote, "I knew I seen this chart pattern before:"

I'm just not too sure that ole Magna and Asher and Daniel James and Fourth Man and KBM Worldwide (all convertible, aka "toxic" debt lenders to BHRT in just the fairly recent time frame and all I believe with "conversions" coming due within the next 3 to 6 months or so max) - I'm just not too sure IMO that those kind of folks pay too much attention to "charts" and all?

I think those firms sell and convert their debt (notes) they hold to maximize their own profits pretty much every single time they do a convertible "not" deal to any penny stock or similar company. Which means dilution and lots and lots and lots more of it coming to the common shares of this company IMO.

So, not too sure about a "chart pattern" carrying much weight at this point right now?

My 2 cents (well, .009 cents or whatever it is now)

From the last 10-Q, PAGE 26 (just some recent convertible debt dilution coming due soon)

"Subsequent financing

KBM Worldwide

On October 6, 2014, the Company entered into a Securities Purchase Agreement with KBM Worldwide, Inc., for the sale of an 8% convertible note in the principal amount of $38,000 (the “Note”).

The Note bears interest at the rate of 8% per annum. All interest and principal must be repaid on July 8, 2015,. The Note is convertible into common stock, at holder’s option, at a 45% discount to the lowest daily trading price of the common stock during the 10 trading day period prior to conversion. In the event the Company prepays the Note in full, the Company is required to pay off all principal and accrued interest at 150%, and any other amounts.

Daniel James Management

On October 3, 2014, the Company entered into a Securities Purchase Agreement with Daniel James Management, Inc., for the sale of a 9.5% convertible note in the principal amount of $25,000 (the “Note”).

The Note bears interest at the rate of 9.5% per annum. All interest and principal must be repaid on October 2, 2015. The Note is convertible into common stock, at holder’s option, at a 47% discount to the lowest daily trading price of the common stock during the 10 trading day period prior to conversion. In the event the Company prepays the Note in full, the Company is required to pay off all principal and accrued interest at 150%, and any other amounts.

Magna Equities, LLC

On October 7, 2014, the Company entered into a securities purchase agreement (the “Purchase Agreement”) with Magna Equities II, LLC, a New York limited liability company (“Magna”). The Purchase Agreement provides that, upon the terms and subject to the conditions set forth therein, Magna shall purchase from the Company, a senior convertible note with an initial principal amount of $307,500 (the “Convertible Note”) for a purchase price of $205,000 (an approximately 33.33% original issue discount). Pursuant to the Purchase Agreement, the Company issued the Convertible Note to Magna. The Convertible Note matures on August 7, 2015 and, in addition to the approximately 33.33% original issue discount, accrues interest at the rate of 12% per annum.

The Convertible Note is convertible at any time, in whole or in part, at Magna’s option into shares of the Company’s common stock, par value $0.01 per share (the “Common Stock”), at a fixed conversion price of $0.01035 per share. $40,000 of the outstanding principal amount of the Convertible Note (together with any accrued and unpaid interest with respect to such portion of the principal amount) shall be automatically extinguished (without any cash payment by the Company) under certain conditions described in the Purchase Agreement.

LOL Quote, "-FDA decision (I don't foresee this needing a phase III)"

Well, not sure the ole FDA is gonna see it that way? A few steps left out of that "list" IMO? Like about 2 yrs minimum on the phase II, getting past an actual phase II with an approval- most drugs that fail, they fail in the phase II portion- as it's much larger and much more stringent than a tiny, 18 person phase I. Also, it's not even clear yet if this OCAT phase II will be blinded and have a full placebo arm? If not then that has to occur at some point also or the FDA won't even consider the drug or look at it IMO.

Then there's a very large phase III, at least one at a minimum and sometimes even more than one needed if the FDA isn't convinced of the data presented in the first phase II/III trial cycle- which is a minimum of probably 5 yrs away which is exactly the time frame Lanza himself said.

Long, hard and very expensive road ahead. The "list" was missing about 500 or more steps IMO. It's a lot tougher for a drug approval that 1,2, 3 stamp it and sell it and an imaginary "lets just skip phase III" cause well, it sounds like a good idea. Again, not a chance in heck IMO the FDA would ever see it that way.

Year 2020 per Lanza's own words (and a dump truck full of cash along the way he didn't even mention- cash they presently do not have):

http://www.telegram.com/article/20141014/NEWS/310149525&Template=printart

Quoting that local, MA newspaper journalist speaking direct to Lanze:

"New medical treatments generally must undergo three phases of human study to demonstrate safety, proper dosing and efficacy before the Food and Drug Administration will approve them for sale. In addition to its phase 1 study in the United States, Advanced Cell has been conducting a phase 1 study of its RPE cells in patients in the United Kingdom.

"We treated the last UK patients last month, and they also have not seen any safety issues related to the transplanted tissues themselves, either," Dr. Lanza said.

Advanced Cell now hopes to launch a 100-patient, phase 2 study in Stargardt's patients by the end of the year, according to Dr. Lanza.

A second, smaller phase 2 study in patients with age-related macular degeneration would follow, he said. Any treatment might not be ready for FDA approval until 2020, Dr. Lanza said. "

Well, that was dated Oct of 2014 so they didn't even make the "hopes to" and by the "end of the year" part for starters.

Lanza also clearly stated, "ANY treatment" and then the word "MIGHT not be ready" - very carefully phrased IMO. So 2020 isn't even a sure thing- which of course makes common sense. A 100 ways to get tripped up by the FDA or other issues along the way in a phase II. It's always that way with new drug R&D. Nothing's a slam dunk, sure-think here by a long, long, long shot here IMO. No way. Not even finished a phase II yet. They're barely out of the starting gate into a long, difficult gauntlet known as the FDA process.

3 year DOWN TREND still intact.

The "big article" was published, the "new management" the "name change" and then a "new logo and re-branding" (to distance themselves from a pretty tainted SEC violation past and all the rest IMO), then the "plan" and now the "uplist" to Nasdaq and all the rest of the biggest events in company history (I guess?) and the stock is below where it was 3 yrs ago and is still in a sustained down trend??

Pretty amazing IMO. All that "stuff" and it's in a technical down trend still and priced below where it was 3 yrs ago where it was as an OTC traded penny stock and is in technical weakness with the 50 DMA inverted (below) the 200 DMA meaning a solid, long term technical down trend is still solidly intact the way I read it.

What exactly does it take to get this off the dime and not just in an few blips of momentary price spike or here and there (that literally last days typically at best)- but get some actual, sustained buying up-pressure and get it into a true uptrend which it hasn't seen for years and years?

3 yr chart: (at the very, very best the stock is flat for 3 yrs but in reality is even below where it was 3 yrs ago and below much of the avg price of the past 3 years- it's been dead money IMO for a long, long time unless day-traded w/ near perfect precision perhaps)

Integrating the area above or below the closing price line does not give one insight into how much volume transpired for the given area under the curve. This is not a simple integration problem of solving the area under a curve. Not how it works.

One would need to know the corresponding vol under that curve for it to indicate the net buying or selling taking place. Knowing the daily tick by tick volumes would be difficult to get w/o some very specific trading software. It's likely available but I don't have a program like that. One has to just use the daily chart in general and look for the very large vol "prints" which show up as large vol spikes on the daily chart.

To integrate the area under the area above and below the daily neutral line really won't tell on much of anything significant unless multiplied by the corresponding total volumes for those given areas.

One would integrate say area from "a" to "b" above the line and then multiply by volume "X" positive above the line and then say integrate the area under the volume under the daily neutral line from "c" to "d" and then multiply it by "-y" and get a negative number for under the line total area X vol. One could then subtract using X - Y and see if it's a positive or negative number. That might give some indication of net volume flow above or below the neutral line.

Simply integrating area above or below the daily neutral line is not going to reveal much IMO. W/o vol a key indicator is missing. One has to especially also bring into play things like MM's, what vol was short, the size of vol orders, etc. Net money flow is more or less what one is looking for- was it positive or negative and a simple area integration won't reveal that.

Actually the largest sell of the day was in the AM- the one that sunk the very brief AM "pop" hard to the red side.

It did the majority of the day's volume below the red-line. Just look at the daily chart. It wasn't some end of day "paint the tape"- it was sustained selling a good part of the day w/o enough buying pressure to push it green or hold it. Both days so far on the Nas it sold off into the moments of strength.

That means either profit taking, plain-jane selling or it's being shorted already IMO.

Closed solid red on higher than avg volume (about a 50% increase in the daily avg volume).

Any gain it made- it sold off into strength each time on volume.

It's showing weakness so far IMO despite the big move to the NASDAQ.

W/o some clarity on how they're going to finance and sustain themselves, let alone fund a serious phase 2 trial which is the key to their entire plan they presented- I think they're open to the pro shorts of the Nasdaq.

Until they clarify if it's all more dilution going forward- or some other funding source, then they'll be in a position of weakness to me. If they have to do a large dilution share sale cash raise then the price will most likely come under at least temporary down pressure- which may be putting buyer's on the sidelines until clarified IMO.

They are living off of Lincoln right now (in itself dilutive) and they don't have anywhere near the cash at this point to fund a high quality, much larger FDA level phase II trial. Lincoln pretty much pays their present burn rate- but doesn't in any way fund a serious trial that I can see. The numbers don't add up.

So some key pieces of the puzzle are still missing that they need to clarify. The share offer got pulled either because of weak demand and low pricing power IMO or they have some other plan they're trying to put in place (the shelf filing is still open and good as far as I can tell).

If they have something- it'd already be announced. Public companies can't sand bag or hold back major material events- if they know and it's a done deal then it gets made public ASAP and is filed with the SEC on an 8-K or similar of needed.

Which tells me at this point- they don't have it yet, whatever it is they may be trying for. Else, it'll be back to a dilution offering, a large one IMO. Maybe they decided to try and sell the shares once on the Nasdaq hoping for a little more pricing power? They spent a bundle on up-front fees and those underwriters and legal and all to pitch that prospectus- so to just "can" it, they must have a pretty good reason? Question is- what's the plan and where's the cash gonna come from?

My 2 cents

Re: 10K

Well, the dates of the last 3 yr's filings are below- so I'd expect somewhere approx. around the same time frames. Sometimes a company is a little early with a filing, sometimes a little later. Remember, the 10-K is fully audited unlike a 10-Q so it's more complicated and expensive to do. Tomas as CEO does a lot of the 10-Q's probably to a large degree himself with some accounting firm or contract accountant assistance or whatever.

But on a 10-K filing, it's like rolling up all the 10-Q's of the full yr, getting it all put together, then it goes to the independent auditor's place (forget BHRT's auditor firm name, it's in their SEC filing- but basically a big, licensed, fiduciary duty type CPA firm that does these public traded company audits) and then they do an audit of the 10-K as Sr Mgt has prepared it (that's my understanding).

I'd guess the auditor's may make some comments or whatever and it goes back to Sr. Mgt who either agree or disagree or whatever. They then get the final document all agreed upon (probably the company SEC or stock legal counsel maybe even takes a review at it too- who knows?) - and then last step is Mr Tomas as CEO signs off on it and then the auditor's also put their name and signature to it and say something to the effect (you'll see it in the 10-K's), "We the audit firm of ABC have reviewed this filing and believe to the best of our knowledge that it's a true and accurate representation of the financial condition of company XYZ blah, blah and we also disclose blah, blah if we agree or don't agree with something". Something to that effect.

Also, the audit firm is the one then (I think) who will either insist or not to the "going concern" warning to be present or not in the filing- cause if you read all the past "going concern" warnings they will refer or state something like, "As of date XYX our independent audit firm noted the following concerns of our ability to continue as a going concern as noted in exhibit or notes section ABC, see below" or something like that. So the auditor is the one typically involved in making that "going concern" warning determination or any other financial issue "warnings" or whatever (I'd guess it's based on ratios and stuff in the "generally accepted accounting standards" these firms abide by) and then Sr Mgt I suppose agrees to include it or the audit firm probably won't sign off. Whether there will still be a "going concern" warning in this next 10-K we'll see I guess? It was still in the most recent, last filed 10-Q last qtr.

Here's the dates for prior 10-K filings:

10-K yr ended 2013:

3/25/2014

10-K yr ended 2012:

3/29/2013

10-K yr ended 2011:

4/12/2012

http://www.bioheartinc.com/Investors/SECFilings

So I'd say it looks to be about the end of March pretty much solid for about 3 yrs now. So I don't see why that would change this year? About 25 days, maybe one month away then is my guesstimate for formal 10-K release and upload to the SEC EDGAR database.

2 MILLION plus for sale on the Ask, wow !!

The selling is just not abating? Who is selling this much stock and/or for who I wonder?

Amazing IMO. The sell side pressure has been like 10 to 1 or more to buy side on many of the days of the past several weeks.

0.009 / 0.0094 (100000 x 2035000)

BMAK is sitting one level off that Ask, 10K share block at .0094 parked like always recently. They did open the spread a bit today- like they want a little "upside" on this big blog these MM's are trying to unload it looks like. These OTC MM's are just brutal IMO. Amazing.

http://www.otcmarkets.com/stock/BHRT/quote

Oh gosh, solid RED selling?

OCAT listing on the Nasdaq apparently hasn't solved all their problems I guess?

They'll still more than likely need to do a very large share dilution too, as they don't have anywhere near the funds to conduct the promised large, phase II trial. As of now they're simply living off of and keeping the lights on and door open using Lincoln for survival- but that's not serious FDA trial kind of money IMO. Also, Lincoln in and of itself is dilutive, on-going.

If this is the relatively dilution-free version on the Nasdaq, I wonder what happens if they do a large dilution deal? They're gonna need a boat load of money- and it's gonna have to come from somewhere?

Looking pretty weak in here for the big "debut" on the Nasdaq? Not sure what's creating the selling- but the buyers seem to be in short supply so far?

BMAK parked on the Ask with a 10K share block at .0094

Looks like BMAK is setting the "cap" for the day again?

Looks like BHRT ends this week as a SUB ONE CENT stock IMO. Just no real buying pressure or interest in here even at these prices it seems to me?

Nothing has been able to really bring it off bottom or the continual dropping Bid/Ask and lower lows and lower highs. Another tough week with no buying interest really at all from the decline on high volumes.

http://www.otcmarkets.com/stock/BHRT/quote

AM Bid/Ask is tilted heavy to the sell-side looks like again.

0.0085 / 0.009 (64783 x 465000)

Looking real, real weak in here at this point IMO.

Uh, all except that MSFT was PROFITABLE FROM ESSENTIALLY DAY ONE and then went on to one of the greatest company rapid growth rates, rapid rise in pure profitability in all of world biz history. MSFT became a cash printing, rapid growth machine producing a train load of millionaires (including an original early employee like a secretary) and some of the world's wealthiest billionaires the day they went public- still in the record books of world biz history.

ACTC never even had an actual "IPO" because of lack of funds or growth or a product to sell- they used the "back door" poor man's method of trading public- via reverse merging into the TWO MOONS KACHINA DOLL COMPANY of Utah straight on to the OTC market place.

OCAT is nothing of the sorts of an "early Microsoft" - not even a distant remote comparison to the history of MSFT as a business?

http://www.nature.com/news/stem-cell-research-never-say-die-1.9759