News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Dragon Lady

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

LOL quote, "Catch u guys in the morning going to do some more digging $BHRT"

Digging? Ole BHRT is a SHOVEL READY PROJECT- it's getting buried, literally.

Today's low, .0046 which is an all, all, all, all time low for this 99.99% loser. Quite the accomplishment IMO.

$5.00 at IPO = 5000 cents

500 cents - .005 cents = 499.995 / 500 = .9999 X 100 = 99.99% TOTAL LOSS to common shares since it went public. Wow.

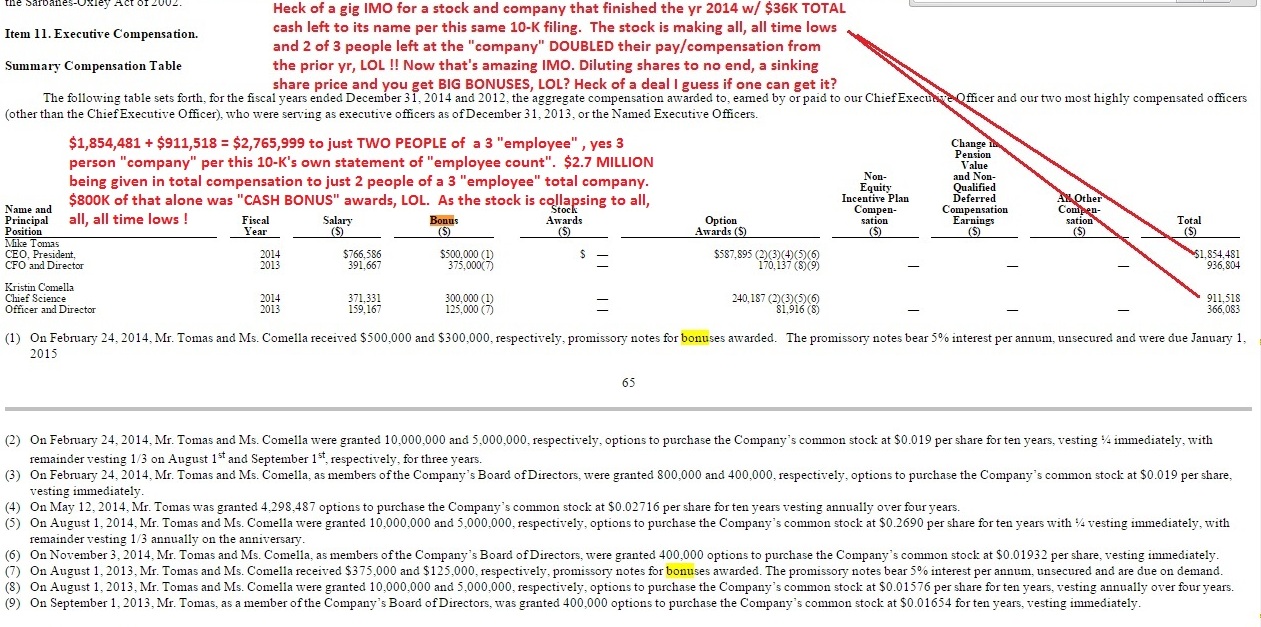

And that got the CEO a $500K CASH bonus on page 65 of the most recent filed 10-K and about $1.8 MILLION in total annual compensation, a doubling of his pay from approx 1 yr ago, LOL

SINK YOUR COMMON SHARES to sub one cent, .0046 day's low and get a big ole bonus. Too funny IMO. Fantastic. Penny-ville to the tee.

LOL quote, "Awesome Bioheart presentation that was posted yesterday from last year "

Oh yeah, a "presentation" ??? Too funny. Did the company manage in the ole "presentation", did they manage to explain ending 2014 with a grand total of $36K cash left in their bank account (see most recent filed SEC 10-K, cash on hand), despite like 300 MILLION shares of dilution?

Any "presentation" talking about how they did 65 MILLION shares of dilution in just Jan, Feb and early March of 2015 and are still diluting, unabated at a furious pace?

Any "presentation" about how they added 3 more toxic, convertible debt deals in just Jan, Feb and early March of 2015 per page F-34 of their just filed 10-K (KBM Worlwide, Vis Vires group, and Fourth Man) - all for pittances more of survival cash?

Anything in the ole "video presentation" about the recent $2.3 MILLION lawsuit they're facing and how they'd pay back that debt if the plaintiff prevails- when their common share price just hit a day's low of .0045? LOL?

http://lawsuitpressrelease.com/investors-sue-bioheart-inc-millions-unpaid-debt

Anything in the ole "presentation" about how they hacked more than $500K out of their R&D budget, bringing it to near zero, while jacking up the pay to just TWO people of a now THREE person total company- including $800K in "CASH BONUSES" to just those two, LOL? That one deserves a slide of its own IMO. All, all, all time lows to the common shares- but TWO people in a company that now has 3 people left in it, those TWO are now pulling down a combined $2 million plus in annual compensation between the two of them- in a cash broke "company"??? LOL !

PAGE 65 most recent filed 10-K (COMPENSATION TABLE for "the two")

AMAZING, IMO.

How bout the "going concern warnings" plastered all throughout their just filed, most recent 10-K, any of that make it in to a "presentation" and cool video anywhere?

10-K, PAGE 56:

"At December 31, 2014, we had cash and cash equivalents totaling $36,674; our working capital deficit as of such date was $10,957,443. Our independent registered public accounting firm has issued its report dated March 16th, 2015 in connection with the audit of our financial statements as of December 31, 2014 that included an explanatory paragraph describing the existence of conditions that raise substantial doubt about our ability to continue as a going concern.

"

Never saw any "presentations" about all those little tid bits. Wonder why?

LOL BS quote, "$BHRT HUGE BOUNCE TODAY OFF 52 WEEK LOW"

BHRT didn't bounce off anything? And it's not a 52 week low? It's an all, all, all time low.

The stock is in mass collapse. There's no "bounce" whatsoever? They're diluting shares like water and the stock is in mass free fall.

What supposed "bounce"??

LOL quote, "Important details from the recently published 10-K: "

OR, try these FACTS from the recent 10-K:

PAGE 26:

"We will need to secure additional financing in 2015 in order to continue to finance our operations. If we are unable to secure additional financing on acceptable terms, or at all, we may be forced to curtail or cease our operations.

As of December 31, 2014, we had cash and cash equivalents of approximately $36,674 and an accumulated capital deficit of approximately $120,434,494. As such, our existing cash resources are insufficient to finance even our immediate operations. Accordingly, we will need to secure additional sources of capital to develop our business and product candidates as planned. We are seeking substantial additional financing through public and/or private financing, which may include equity and/or debt financings, research grants and through other arrangements,"

PAGE F-4 (Their INCREASED LOSS FROM OPERATIONS in 2014 vs 2013)

Net loss from operations 2014: (3,529,452)

Net loss from operations 2013: (2,831,750)

Or PAGE 56:

"At December 31, 2014, we had cash and cash equivalents totaling $36,674; our working capital deficit as of such date was $10,957,443. Our independent registered public accounting firm has issued its report dated March 16th, 2015 in connection with the audit of our financial statements as of December 31, 2014 that included an explanatory paragraph describing the existence of conditions that raise substantial doubt about our ability to continue as a going concern."

Or PAGE F-34:

"Subsequent financing

On January 7, 2015, the Company entered into a Securities Purchase Agreement with KBM Worldwide, Inc. (“KBM”), for the sale of an 8% convertible note in the principal amount of $38,000 (the “Note”).

The Note bears interest at the rate of 8% per annum. All interest and principal must be repaid on October 9, 2015. The Note is convertible into common stock, at KBM’s option, at a 45% discount to the average of the three lowest closing bid prices of the common stock during the 10 trading day period prior to conversion. In the event the Company prepays the Note in full, the Company is required to pay off all principal, interest and any other amounts owing multiplied by (i) 140% if prepaid during the period commencing on the closing date through 179 days thereafter. After the expiration of 180 days following the date of the Note, the Company has no right of prepayment.

On January 28, 2015, the Company entered into a Securities Purchase Agreement with Fourth Man, LLC., for the sale of an 9.5% convertible note in the principal amount of $25,000 (the “Note”).

The Note bears interest at the rate of 9.5% per annum. All interest and principal must be repaid on January 27, 2016. The Note is convertible into common stock, at Asher’s option, at a 47% discount to the lowest daily closing trading price of the common stock during the 10 trading day period prior to conversion. In the event the Company prepays the Note in full, the Company is required to pay off all principal at 150%, interest and any other amounts.

On February 19, 2015, the Company entered into a Securities Purchase Agreement with Vis Vires Group, Inc. (“VIS”), for the sale of an 8% convertible note in the principal amount of $38,000 (the “Note”).

The Note bears interest at the rate of 8% per annum. All interest and principal must be repaid on November 23, 2015. The Note is convertible into common stock, at VIS’s option, at a 45% discount to the average of the three lowest closing bid prices of the common stock during the 10 trading day period prior to conversion. In the event the Company prepays the Note in full, the Company is required to pay off all principal, interest and any other amounts owing multiplied by (i) 140% if prepaid during the period commencing on the closing date through 179 days thereafter. After the expiration of 180 days following the date of the Note, the Company has no right of prepayment."

Or page F-34 again (over 65 MILLION pure dilution shares already issued out in just Jan, Feb and early March of 2015. 65 MILLION in less than 3 months- you know, cause the "revenues" are so great, LOL !)

"

Subsequent stock issuances

In January 2015, the Company issued 4,783,568 shares of its common stock in settlement for services, provided 14,299,567 shares of its common stock in settlement of $49,500 of outstanding convertible notes payable, and $2,981 accrued interest and 2,096,450 shares of its common stock for net proceeds of $16,118 from equity drawdown under the Magna Purchase Agreement.

In February 2015, the Company sold an aggregate of 1,443,656 shares of its common stock for net proceeds of $16,270. In connection with the stock sale, the Company issued an aggregate of 1,443,656 warrants to purchase the Company’s common stock for five years at $0.01127 per share. In addition, the Company issued 20,219,367 shares of its common stock in settlement of $132,500 of outstanding convertible notes payable and $2,520 accrued interest and 16,556,976 shares of its common stock for net proceeds of $135,645 from equity drawdown under the Magna Purchase Agreement.

In March 2015, the Company issued 6,185,432 shares of its common stock in settlement of $25,000 of outstanding convertible notes payable and $1,226 accrued interest. In addition, the Company issued 635,357 shares of its common stock as true up shares relating to the February 2015 equity drawdown under the Magna Purchase Agreement.

"

DUE DILIGENCE IMO, not one-liner bullet points selected from some crafted Power Point presentation- missing like 90% of the "real story" IMO. The 10-K must be READ IN FULL, cover to cover to get the "true picture" IMO. Their financial situation is dire IMO if one reads the entire 10-K, not even debatable. There own auditors think so too.

PAGE F-2:

" the Company has suffered recurring losses from operations and used significant amounts of cash in its operations. In addition, at December 31, 2014 the Company’s current liabilities exceed its current assets by $10,957,443. These conditions raise substantial doubt about the Company’s ability to continue as a going concern. The financial statements do not include any adjustments that might result from the outcome of this uncertainty.

/s/Fiondella, Milone & LaSaracina LLP

Glastonbury, Connecticut

March 16, 2015"

So someone who paid .02, TWO CENTS only what, a few months ago - is now down 75% on their shares. HOLY COW !

That means they only would need a 4X increase (300%) gainer from here to get back to break-even.

The common shares since BHRT went public in 2008 have now lost:

$5.00 (500 cents) 500 - .005 = 499.995 / 500 = .9999 X 100 = 99.99% of their value.

THAT is staggering. What's left to lose to their common share value other than full-up BK I guess? Fascinating to me.

Since the present CEO took over in mid 2010, the common shares have lost how much? They were about .50 cents each on the low side when he took over full control of running this company.

.50 - .005 = .495 / .50 = 0.99 X 100 = 99%

Yep, the common shares have now lost pretty much 99% of their value under the command and watch and Sr Mgt role of the present CEO. And for that "performance" - he got this, from the latest filed 10-K, PAGE 65:

A $500K "cash" bonus and about $1.8 MILLION a yr in 2014/2015 in "total compensation" and that's up from $936K in 2013/2014, LOL.

Amazing. Simply amazing IMHO.

LOL quote, "What is going on here? has anyone contacted the Company?"

They're probably too busy to answer the phone, all THREE of them- maybe they're on the other line CALLING MAGNA FOR MORE CASH or inking the next toxic, convertible note deal with some penny finance hedge firm probably IMO, LOL.

(Asher, Magna, Daniel James, Fourth Man, KBM Worldwide, Vis Vires Group, INSERT NAME OF NEW TOXIC LENDER HERE) LOL !!

17 MILLION shares and a DAY'S LOW of .0045, WOW !!

This is in total collapse IMO. Past free fall. How they gonna keep raising dilution money to stay solvent at these prices?

This is heading to BK perhaps now? Or a desperation R/S?

If a firm is converting in here- and they get the "avg of the past 3 days closing price blah, blah" or the "avg of the past 10 days closing price blah, blah" then they're gonna get shares, 10's of MILLIONS of shares in the .0025 or lower range probably?

This thing is a shovel ready project- getting buried, stick a fork in it IMO.

They're probably on the phone with MAGNA right now calling for another "draw" on the credit line, LOL.

What an epic implosion- but can't say I didn't sorta see it coming- when the last page, F-34, of the just filed 10-K showed qty-3 more toxic, floorless convertible debt deals, including a new hedge firm called "Vis Vires" and then in the same 10-K section showed over 65 MILLION dilution shares being passed out in just Jan, Feb and early March of 2015. That and the $36K total cash left for 2014 were sorta, kinda pretty strong hints to me that they were still in deep financial troubles and dire straights.

Just cause it bounces a tad here- I wouldn't step under this falling piano IMO. Remember, these convertible debt dudes do it in stair-steps, "tranches" they call it. They plaster it like the last few days, let it breathe a tad and hunt down some buyers, then plaster it again, always making LOWER LOWS and LOWER HIGHS in a collapsing spiral, the DEATH SPIRAL.

CDEL is back in first position again and has it "bracketed" - so no way IMO this is out of the dilution crusher. Maybe they'll let it breathe a bit, maybe not.

0.0054 / 0.0058 (700000 x 325000)

http://www.otcmarkets.com/stock/BHRT/quote

My .0045 cents worth

Magna must be "hot" on this now- read and watch now they "do what they do" - it's fascinating IMO:

http://www.bloomberg.com/news/articles/2015-03-12/josh-sason-made-millions-from-penny-stock-financing

LOL, quote, "Massive OCAT run ahead according to this post.

No lack or limitation here yahoo OCAT post: "

Oh, OK. A "Yahoo post"?? LOL. Right.

That "Yahoo post", pure BS IMO.

How bout OCAT hasn't even started the ole "big FDA phase II" yet and botched their secondary offering for $62 and thus never banked any large cash- but instead is tapping the ole Lincoln "credit card" still to this day, now into Q2 2015?

"yahoo post" said, LOL !!

Still has NOT EVEN HIT Nov 2014 price area- it's not even in a technical uptrend or reversal yet. It traded at $7.25 a share in just Nov of 2014 and has gone nowhere from that time period. Flat at best, from almost 6 months ago now.

Just look at a long term chart- not a lot to get excited about here yet IMO. It's got a long ways to go still to even put in a reversal and even sustain itself above levels it traded at as an old OTC stinker.

This is not some "major move here" yet IMO. It's done this many times since just 2014 and always gave it all back- when Lincoln got back on their sell-n-dump the shares plan.

3 MILLION shares and it just FELL OFF THE CLIFF TO .005 ???

This is looking pretty grave in here IMO. Free fall? It's like re-entry from space and burning up the capsule IMO. Wow.

As much as the price dropping- it's the freaking VOLUME. It's picking up and gaining volume TO THE MASSIVE DOWNSIDE and showing no signs of abating and no buyers stepping in to suck up all this sell-side massive volume.

This here, IMO, would be like jumping in front of a freight train or under a falling piano. Who can predict a bottom now when it's trading like this? Wow again.

0.005 / 0.0055 (456200 x 251000)

DOWN BLEEDING RED -23%. DOWN TWENTY THREE PERCENT in a single free fall?? What the heck?

http://www.otcmarkets.com/stock/BHRT/quote

Question to me is- what hedge firm (convertible toxic debt lender) is converting in here at these prices or is this MAGNA? It's gotta be one or the other IMO.

Converting in here now- you'd have firms getting their shares now for almost about .0025 CENTS each. Wow. It's being run through the dilution crushing machine looks like to me.

My .005 cents worth

Quote, "Makes sense. We all know this should have a higher market cap. What's the point of driving this down to these levels?"

Who knows it "should" have a higher market cap, based on what?

It's a share dilution machine essentially- and that's what's driving the price down IMO. Endless use of toxic debt financing comes with a price- the SEC warns about it as do numerous other well documented market research and financial press sources.

BHRT diluted out over 300 MILLION shares in approx the past 1 yr prior to the recently filed 10-K and then in that 10-K, last section it shows they took on qty-3, THREE more floorless, "toxic" convertible debt deals and issued out over 65 MILLION more dilution shares in just Jan, Feb and early March of 2015. How's that not going to eventually bury the common share price? It seems impossible that it wouldn't?

They, BHRT, also finished 2014 with a grand total of $36K lousy pittance of cash to their name, in the bank. They're teetering on insolvency. They have a grand total of 3, THREE people at the company per that just filed 10-K but they still dilute at a furious pace, on-going, essentially endlessly. There's a huge number of convertible debt deals all coming due one after another for months, all through this summer and clear to at least Oct 2015 and they're also tapping the dilution Magna line at the same time.

It's obvious to me what's crushing this share price.

And meanwhile- they hand out enormous pay package increases to just 2 of an big giant 3 person "company"? As the stock hits ALL TIME LOWS and the market cap has collapsed to below $4 million lousy bucks- the CEO alone is now pulling down more than $1.5 million in total annual compensation per the recently filed 10-K. That's at a 3 person company who just finished their past yr with $36K cash in the bank, LOL. It makes zero sense IMO.

They're in desperation straights. The lower this share price goes- the harder it gets for them to raise even pittances of dilution cash using more toxic finance deals- which is what they live off of. It's not that complicated IMO.

The company now also has a huge $2.3 million lawsuit hanging over their head- which if they need to pay, would bust their bank (they have no cash in the bank essentially) but would require massive dilution to settle the $1.5 million in principal the suit claims is owed (and shows right on the BHRT 10-K balance sheet as "subordinated debt, related party) plus the interest. $2.3 million worth of dilution at these prices? It would sink this thing to oblivion IMO.

http://lawsuitpressrelease.com/investors-sue-bioheart-inc-millions-unpaid-debt

Check that out. Make all, all time lows on your share price for the common share holders- and get some big ole cash bonuses ! I wonder what this year's, 2015 massive pay increases will be for these two- if the past few yrs have been any indication? They've TRIPLED their total compensation, those two, in a period of a few years as the stock has sunk to all time lows. I don't know anyone getting 100% raises/pay increases a year in this economy, LOL !! Amazing to me.

And meanwhile, just dilute away using the worst the worst "toxic" debt, convertible debt deals to no end, qty-3 new ones in just early 2015 alone. And now the infamous MAGNA too !

http://www.bloomberg.com/news/articles/2015-03-12/josh-sason-made-millions-from-penny-stock-financing

Bid .0052 HOLY COW !! And CDEL is parked back on the Ask with a good sized block, not the usual 10K share "cap" block

Looks like it might be another real rough day on this one perhaps.

0.0052 / 0.0065 (472600 x 410000)

http://www.otcmarkets.com/stock/BHRT/quote

At least it's at this point in the AM it's showing about even Bid to Ask. It's typically been heavy to the Ask/sell side for several weeks lately.

BMAK is sitting a few levels out on the Level II and it looks like it might be CDEL and this new on BKRT in doing the "work" on it today- I guess we'll see.

Bid just moved now to .0055 as I'm about to hit enter. But a Bid in the .005's is the lowest it's ever been in the entire history of this stock as far as I know.

0.0057 / 0.0065 (10000 x 310000)

Now it just went heavily stacked o the Ask/sell side again- as about to hit enter.

That's 30 to 1 to the Ask/sell now showing. Gonna be rough in here again more than likely. Wow.

It looks like perhaps more free-fall today could very well be in the cards.

Retail selling- well I'd speculate yes by now. That some holders are just looking at this thing going through the crusher and are just throwing in the towel and selling for whatever they can get.

So yes, I'd say as this thing "spirals in" on itself- at some point you get capitulation of retail holders who just toss in the towel, take their lumps and losses and move on.

Just look at how many might of been holding from even 2 cents say- who would now be getting plastered for a more than 60% loss. They may just cut their losses, put in the sell and bail.

I'd say yes- the selling at these levels now probably begins to just feed on itself, brutally.

Today 6 million shares solid red, after 10 million shares on Friday- it's pretty stunning IMO the level and speed of the collapse and just no buying pressure stepping in at all that I can see, just none. It's in nose dive, pull back on the stick till it bends and still can't exit the dive territory.

I think mass dilution, convertible debt down pressure just trumps all at this point IMO. 10's and 10's if not 100 MILLION or more shares just piling on to the Ask now.

Imagine any convertible debt firms holding/converting in here now- and there's a whole slew of them all coming due one after another after another per the latest 10-K. They're getting like 45% to 47% share discounts in nearly all deals (see any 10-K or 10-Q filing and look for names like Asher, Daniel James, Fourth Man, KBM Worldwide, Vis Vires, etc)- so what would they get their shares for at these prices?

.006 X .47% discount = .003 essentially. Yep.

So lets say that firm/debt holder converts even a lousy $35K of debt.

$35K / .003 = 11.65 MILLION shares it will cost BHRT just for a lousy $35K of debt (and it will be worse than that as interest will be added on).

$75K convertible debt getting converted, just more than double that $35K number- figure 23 MILLION shares or so at least.

It just feeds on itself the lower the share price goes, those firms then dump some more shares to the sell side, it drops again, they convert more again, sell some more- wash, rinse, repeat to infinity essentially with the convertible debt holder making nothing but money all the way down.

It's called a "death spiral" or "ratchet" for a reason.

http://www.sec.gov/answers/convertibles.htm

Quote from the SEC:

"By contrast, in less conventional convertible security financings, the conversion ratio may be based on fluctuating market prices to determine the number of shares of common stock to be issued on conversion. A market price based conversion formula protects the holders of the convertibles against price declines, while subjecting both the company and the holders of its common stock to certain risks. Because a market price based conversion formula can lead to dramatic stock price reductions and corresponding negative effects on both the company and its shareholders, convertible security financings with market price based conversion ratios have colloquially been called "floorless", "toxic," "death spiral," and "ratchet" convertibles."

.0062, I believe that's a NEW ALL, ALL, ALL TIME LOW.

There it went- those dilution shares IMO just drove those dilution MM's to keep dumping, not only to a 52 week low, but a new all, all time low.

Market cap has been CRUSHED to just barely $4 million now, despite massive share dilution that should be propping it up somewhat. The thing is just getting plastered for months, and now some brutal weeks.

Wow. It's just in total free fall, bottomless IMO. Convertible debt deals seemingly never ending per even most recent 10-K filing, 65 MILLION shares of dilution in just Jan, Feb and early March 2015 per page F-34 just filed 10-K, and the then conversion of the toxic debt to ever bigger piles of shares the lower the price goes.

0.0063 / 0.0068 (10000 x 456100)

45 to 1 to the Ask/Sell side still. Just endless shares it appears piling on the Ask, unabated. And it's hitting over 4 million shares traded so volume to this huge downside break is high. Friday was 10 million plus shares of mass dumping.

Again, IMO, I think one or several convertible, "toxic" debt (hedge) loan houses are converting or BHRT is making a "draw" from Magna again.

http://www.otcmarkets.com/stock/BHRT/quote

My .0063 cents worth

http://www.sec.gov/answers/convertibles.htm

http://www.bloomberg.com/news/articles/2015-03-12/josh-sason-made-millions-from-penny-stock-financing

LOL, "$OCAT Covered Short Position has increased "??

The open short interest on OCAT as a percentage of float is pretty much NIL and has been nil. It's noise level.

What difference does any short interest make? It's nothing at this point?

Open short interest is like 1% of float, "maybe".

It's a non issue.

Only thing going on right now is Lincoln is in "breather" mode between unloading credit-card shares IMO. Nothing more, nothing less. Same pattern going back to at least Nov of 2014.

Total BS quote, "OCAT Post by Bogeyfree:

What Happens if Fujifilm buys Ocata?

"

There's not one shred of proof that Fujifilm is interested in "buying" OCAT or even knows or cares who OCAT is? None IMO.

Total nonsense IMO. Myth.

Interesting, a new MM (market maker) BKRT has it "bracketed" this AM on both the Bid and Ask?

http://www.otcmarkets.com/stock/BHRT/quote

0.0072 / 0.0076 (10000 x 150000)

That's loaded 15:1 to the Ask/sell side.

BMAK appears to be backed way, way off both the Bid and Ask and CDEL is now a few levels out, down both the Bid/Ask too? Interesting. So now it's this BKRT moved in?

Will be interesting IMO to see what this does today?

It just posted 38K shares ($296 bucks worth) on open ABOVE the Ask, like plus 11% up or something LOL? That sure didn't last long though? Wonder what that was?

A Google search shows some threads that this MM "BKRT" is thought to be another "dilution MM" and usually a heavy seller for institutional/pro level trading desks.

Here's a couple of links to I-HUB posters/threads about MM BKRT:

http://investorshub.advfn.com/boards/read_msg.aspx?message_id=104723309

http://investorshub.advfn.com/boards/read_msg.aspx?message_id=77747388

BKRT pretty sure is Buckman, Buckman & Reid- they list "hedge fund" and "institutional" order flow and order routing and similar "services" right on their web page.

http://www.buckmanbuckman.com/institutional_clients.htm

Will be fascinating to see what happens now with this MM "BKRT" parked on this now? I don't remember seeing that MM around much, if at all on BHRT prior (could be wrong, but certainly don't remember seeing them down on the Ask and Bid directly?).

LOL quot, "Bogeyfree followup post:

Control 3 of the 4 ways ways hESC's and IPSC's come about via key patents coupled with many surrounding patent processes of these stem cells and one can gain a major foothold in what could be a trillion dollar industry in 10-15 years. "

Oh, holy cow- so now it's a fantasy $TRILLION "dollar industry" in just 10 or 15 yrs? Lickety split- just like that?

Does this ole "Bogeyfree" even know how many $TRILLION dollar industries even exist on planet earth as of right now, today? Or how many countries or nations even do a $TRILLION in GDP, the entire economic output of an entire nation's population producing all its total goods and services created by their entire population?

There's presently about 15 countries on planet earth who have GDP's over a $Trillion dollars. That's out of 196 total. The entire GDP for one yr of the USA is about $16 TRILLION, that's all goods and services produced in all industries, by all workers, in a given yr- manufacturing, services, all of it. China is 2nd place closing in on the USA. Japan 3rd at about $4.8 trillion and Germany 4th at about $3.7 trillion, etc

Yeah, lil ole $6 and change, 35 person OCAT is a $TRILLION dollar "industry", LOL. There's not a $TRILLION company in existence yet, anywhere. Apple "might" make a $Trillion market cap, maybe Google, Exxon-Mobile was close at one time. None exist yet.

The myth of the $trillion dollar "industry" and ole OCAT? OK, sure.

LOL quote, "If my infant was arguably the smartest scientist of our time, that analogy would be fair."

Well, was that infant in charge of a cash poor, nearly broke public traded company that literally diluted their common shares out to 3 BILLION plus while driving their common share price to a literal 5 CENTS each (at which point not a single insider involved with the company bought so much as ONE NICKEL'S WORTH of their own stock using their own money), and now a pre R/S split price of 6.6 CENTS each?

Cause that's what this "infant" OCAT has done so far.

From the latest filed OCAT 10-K filing, March 2015, PAGE 16:

"Our independent auditor’s report for the fiscal year ended December 31, 2014 includes an explanatory paragraph regarding substantial doubt about our ability to continue as a going concern.

Due to the uncertainty of our ability to meet our current operating and capital expenses, in their report on our audited annual financial statements as of and for the year ended December 31, 2014, our independent auditors included an explanatory paragraph regarding concerns about our ability to continue as a going concern. Recurring losses from operations raise substantial doubt about our ability to continue as a going concern. If we are unable to continue as a going concern, we might have to liquidate our assets and the values we receive for our assets in liquidation or dissolution could be significantly lower than the values reflected in our financial statements. In addition, the inclusion of an explanatory paragraph regarding substantial doubt about our ability to continue as a going concern and our lack of cash resources may materially adversely affect our share price and our ability to raise new capital or to enter into critical contractual relations with third parties."

Or PAGE F-7:

"The accompanying consolidated financial statements have been prepared in conformity with GAAP which contemplate continuation of the Company as a going concern. However, as of December 31, 2014, the Company has an accumulated deficit of $349.1 million, recurring losses from operations, and negative working capital which raise substantial doubt about the ability of the Company to continue as a going concern. The ability to continue as a going concern is dependent upon many factors, including the Company’s ability to raise additional capital in a timely manner. On a long-term basis, we have no expectation of generating any meaningful revenues from our product candidates for a substantial period of time and must rely on raising funds in capital transactions to finance our research and development programs. Our future cash requirements will depend on many factors, including the pace and scope of our research and development programs, the costs involved in filing, prosecuting and enforcing patents, and other costs associated with commercializing our potential products. Accordingly, management’s plans to continue as a going concern contemplate raising additional capital including the execution of an agreement for a $30 million equity line in late June 2014, of which approximately $18.6 million remains available as of December 31, 2014. There can be no assurances that management can raise the necessary additional capital on favorable terms or at all. The accompanying financial statements do not include any adjustments that might be necessary if the Company is unable to continue as a going concern."

LOL quote, "When i read this post i think and feel like a multi millionaire. "

When I read that junk, total BS I think I'm reading a fairy tale and pure 100% made-up nonsense.

We're already well in to Q2. A little over 2 months left. Let's check that mythology $35 per share price "projection" on June 30, 2015 and see how it works out, LOL.

OCAT is parked right now at $6 and change, BELOW where it was even end of 2014 and despite the big ole Nasdaq "uplist" and the big "article" and all the rest. Further, OCAT just went to Lincoln for more low grade "credit card", keep the lights on financing money- as they've raised no major cash to date yet, despite filing a $100 million shelf offering and trying (unsuccessfully) to pitch and sell a portion of that as a $62 million secondary.

And it's April 11, 2015 in Q2 and NO, the "big phase 2" slated to supposedly start by end of 2014 is NOT happening as of yet.

Tall tales and fantasy projections = not worth much IMO. Wrong about 99% of the time- especially given the micro "blog" site where they all originate from.

LOL, quote, " "Ocata's "multibillion-dollar" cellular therapy."

What OCAT so called "therapy", let alone a mythology "multibillion" supposed therapy?

They might end up with a $billion in sunk, lost capital at the rate they're going- but what exact "therapy" or even a single, salable imaginary product does OCAT actually have? Which one exactly?

OCAT has never generated so much as a DIME from any "therapy" they do not have? When did this occur?

From the OCAT most recent filed 10-K, March 16 2015, PAGE 13:

"We have never generated any revenue from product sales and may never be profitable.

We have limited clinical testing, regulatory, manufacturing, marketing, distribution and sales experience capabilities, which may limit our ability to generate revenues. Due to the early stage of our therapeutic products, including regenerative medical therapies and stem cell therapy-based programs, we have not yet invested significantly in regulatory, marketing, distribution or product sales resources. We cannot assure you that we will be able to invest or develop any of these resources successfully or as expediently as necessary, either alone or with strategic partners, to generate revenue."

Same PAGE 13:

"We have a history of operating losses and we may not achieve future revenues or operating profits.

We have generated modest revenue to date from our operations. Historically, we have had net operating losses each year since our inception. As of December 31, 2014, we have an accumulated deficit of $349,134,225 and a stockholders’ deficit of $2,735,545. We incurred net losses of $34,748,945, $31,022,248, and $34,584,115 for the years ended December 31, 2014, 2013, and 2012, respectively. We have limited current potential sources of income from licensing fees and we do not generate significant revenue from any other source. We have no therapeutic products currently available for sale and do not expect to have any therapeutic products commercially available for sale for a period of years, if at all. Additionally, even if we are able to commercialize our technologies or any products or services related to our technologies if approved, it is not certain that they will result in revenue or profitability."

Which imaginary $Billion blah, blah OCAT "therapies" (cellular based or whatever) are those again? Which ones exactly?

Quote wrong, "I'm seeing after hour it jumped up to 0.009 (28%) might be that 3.5 mil shares"

No. OTC stocks do not trade after hours. It never traded anywhere near .009 today and did not close at that price or post any after hours trades- simply not true.

The closing, final printed price is .007 down 10.26%.

0.0068 / 0.0077 (20000 x 150000)

http://www.otcmarkets.com/stock/BHRT/quote

The 3.5 million shares printed prior to market close, prior to 4 PM Eastern. Nothing after hours on an OTC stock.

The last trade printed right on the I-HUB ticker posted at 3:56:13 PM Eastern, that included the 3.5 million shares near end of day that brought it to the 10 million plus shares for the day.

How low? I have no idea, not a clue.

I really think major dilution is the pure driver here right now- but who, and how much, and what firms, no one can ever figure that out that I know of. They route orders through all kinds of methods, use various MM's, etc I don't think there's a single known way to figure out who's doing the selling/share dumping at these kind of volumes. I don't believe for a second that most of it is Joe Q. Public. I think this is convertible debt folks or Magna related as I've stated many times. A simple Google search of I-HUB other boards will reveal numerous seasoned members here discussing other stocks that used Asher, Magna and other convertible debt firms- and have similar tales of what eventually happened to the common share price.

I-HUB has an entire board dedicated to just Asher that someone put together. And now it's believed that KBM Worldwide, who BHRT just did a couple of toxic, convertible debt deals with (see 10-K page F-34 and past 10-Q) - the word on many boards is that firm is operated by the brother of the guy who originally created Asher. The word is that KBM is a "sister" firm to Asher w/ one brother running one and another running the other.

http://www.hollywoodreporter.com/news/afm-daniel-grodnik-teams-kramer-747466

Curt and Seth Cramer are supposedly the ones behind Asher and now KBM Worldwide, who BHRT has done several finance deals with now.

Then, if one looks at all the convertible debt deals BHRT has coming due on through the Summer and clear to October- it's mind blowing IMO if those firms all convert and sell/dump in this price range. They all get like 45% to 47% discount on the low end, which would mean shares at what, like .0035 now or something? Wow. (Daniel James, KBM, Asher, Fourth Man, Vis Vire, etc)- I was reading the 10-K and started trying to figure out all the due dates- which IMO means those firms will convert their shares by that date at the latest and be selling/dumping on the way down more than likely. Remember, the whole convertible debt thing is, the lower the price goes, those firms just get that much more shares when they convert and can make money no matter how low the share price goes.

And then Magna is in the picture. If BHRT is tapping Magna again, well who knows. All I've been able to find and read on Magna is they're brutal as all these hedge lending firms are. Not sharks, not pretty nasty, these types of convertible debt and penny finance places from what I've been able to research and read- they probably eat sharks for a delicacy. They're past brutal. They're wrecking ball, heartless, cold money minded machines IMO. That's what one reads and that's what that Bloomberg piece concluded about Magna IMO.

http://www.bloomberg.com/news/articles/2015-03-12/josh-sason-made-millions-from-penny-stock-financing

So a bottom, I have no clue, none. It's stepping under a falling piano in here at this point IMO. Catch the falling knife thing- pretty dangerous to pick a bottom IMO unless it's put in some kind of confirmed reversal of the trend and the MM's seem to back off, sell volume abates etc.

From a technical/chart point of view - it's past free fall and downtrend so I don't think charting is even any good in here or tech analysis. It's broken down under all technical indicators.

So I don't know. It's one micro smidge off the all, all, all time low. If it breaks that .0063 next week- then it's putting in historic lows. The market cap is I think something like only $4.5 million now w/ today's closing price. Just amazing, how much the market cap has been punished given that the big share dilution should be propping that market cap number up much higher (total shares X price per share = $market cap).

Don't have a clue personally. I think that poster asked yesterday if it was going to go "trip" and you asked what that meant? I thought about it and I'm pretty sure he's asking "triple zeroes" I'm almost sure. Like it means will it get 3 zeroes after the decimal as in .000X per share ("trip" being slang for 3 zeroes after decimal I guess). It's obviously not there yet, but who knows at the pace it's going?

10 MILLION shares, what the heck?

Whoah, someone just plastered on 3.5 MILLION shares into the Friday close, minutes or seconds before the close? I looked a minute or two ago and it was like 6.5 MILLION shares.

Checked the screen and it has blasted past 10 freaking MILLION shares traded today, BLEEDING RED minus 10% down and more?

Wowza? Train wreck in slow motion today? I thought it looked weak the past few days and this AM, but what the heck? Who's unloading all this mass dilution? Is this one firm converting discounted debt or several or just Magna or what?

http://www.otcmarkets.com/stock/BHRT/quote

Shows .00675 as the final closing price. That's a micro hair off the all, all time low.

6.5 MILLION shares, down 10% plus, holy cow !

Just within a smidge of the all, all, all time low of .0066 or .0063 (whichever it was?) made in Dec of 2013 I believe it was.

0.0068 / 0.0077 (20000 x 150000)

Still stacked to the sell/Ask side, just brutal. .0068 on the Bid is all. Wow.

http://www.otcmarkets.com/stock/BHRT/quote

It's all dilution selling at this point IMO. Toxic, convertible, floorless debt resulting in 10's and 10's of millions of free trading shares just getting plastered on to the sell/Ask side non stop.

No way IMO that 6.5 MILLION shares on a Friday is Joe Q. Public just buying and selling as usual or whatever. No way to me.

This is either the convertible debt hedge boys or especially Magna IMO. I've got a feeling BHRT is making a Magna "draw" (can't prove it, don't know for sure) and this is Magna setting the price as low as possible- to make the most they can on any credit-line draw down. That's Magna's well known reputation in penny-ville according to easily found research using Google - at least what I found and read. They're a notorious share price crusher from my research.

Here's the Bloomberg Finance journalism piece they did on Magna and the SEC link about toxic, convertible, floorless debt and what it can do to share prices- especially of nano-cap tiny penny stocks like this one.

http://www.sec.gov/answers/convertibles.htm

http://www.bloomberg.com/news/articles/2015-03-12/josh-sason-made-millions-from-penny-stock-financing

Falling Bid and falling Ask- it's in free fall IMO. Bottomless at this point.

0.0074 / 0.0078 (40000 x 10000)

http://www.otcmarkets.com/stock/BHRT/quote

Dilution is the total driver now, me thinks. And there's nowhere near enough buyers to overcome the mass dilution and all the convertible debt that's driving this down here now via pure, mass common share dilution, IMO.

Someone posted the other day is it "going trips"? I think that means "triple zeros", like 3 zeroes after the decimal point.

I don't know if that's quite here yet, but making new, all, all, all time lows- I don't doubt it for a second now. .0063 was the previous all, all time low. And it's seems to be about to hug that zone pretty darn quick here soon.

If you got convertible debt holders who are now converting and getting 10's of MILLIONS of share for say .0035 or .004 at the most- those hedge houses can sell/dump those shares as low as .006 or .005 and still be making like 30% to 50% on their money, easy.

I don't see any break in the mass dilution shares IMO- it's ongoing, non stop. Read the latest 10-K, PAGE F-34, they already diluted out over 65 MILLION shares in just Jan, Feb and just early March of this yr, 2015. And no, the "revenues" made no difference- they ended 2014 nearly broke, $36K total cash left in their bank account against massive debts, debts due soon.

And then they already took on qty-3 more toxic, floorless, convertible debt deals in just the early months of 2015: KBM Worldwide, Fourth Man and some new company/hedge named Vis Vires group or something (PAGE F-34 of most recent filed 10-K)

Lots more dilution to come IMO, like super tankers full. They diluted over 300 MILLION shares in about the prior 1 yr period and based on the first 3 months of 2015 in that 10-K filing, they look on track to easily do that much again this yr, if not more. The lower the price goes- the more dilution they will need to raise each pittance of cash using toxic debt deals or the Magna dilutive credit line.

My .0075 cents worth

LOL quote, "If you got balls !, eyeballs that is, Ocata can fix'em !!!

They can put a fresh layer on your balls, your eyeballs ! "

Well actually, NO, NO they can't legally- at least not in the USA or Euro or other major nations, unless during a clinical trial, a controlled trial. Cause OCAT HAS NO APPROVED PRODUCTS, it has NO PRODUCTS, "treatments" or "cures" or anything else FOR SALE or commercial use in humans as of today, and won't have any for many, many, many years, if ever (their own words, OCAT).

OCAT isn't "fixing" any eyes yet- that's a myth. What products or "treatments" do they have for sale today that can "fix an eye"?? Where? Where can these "treatments" be had and paid for?

From the most recent OCAT SEC filed 10-K, PAGE 1:

" We have no therapeutic products currently available for sale and do not expect to have any therapeutic products commercially available for sale for a period of years, if at all. These factors indicate that our ability to continue research and development activities is dependent upon the ability of management to obtain additional financing as required."

I stick with the FACTS in the 10-K. Their own words, right there- THEY HAVE NO EYE "treatments" or any other "therapeutic products" commercially available for sale and will not for a period of YEARS, IF EVER.

Clear as it gets IMO. What mythology treatments are these "eye cures" again?

Same 10-K filing, PAGE 13 (they sure seem to want to point these FACTS out):

"We have a history of operating losses and we may not achieve future revenues or operating profits.

We have generated modest revenue to date from our operations. Historically, we have had net operating losses each year since our inception. As of December 31, 2014, we have an accumulated deficit of $349,134,225 and a stockholders’ deficit of $2,735,545. We incurred net losses of $34,748,945, $31,022,248, and $34,584,115 for the years ended December 31, 2014, 2013, and 2012, respectively. We have limited current potential sources of income from licensing fees and we do not generate significant revenue from any other source. We have no therapeutic products currently available for sale and do not expect to have any therapeutic products commercially available for sale for a period of years, if at all. Additionally, even if we are able to commercialize our technologies or any products or services related to our technologies if approved, it is not certain that they will result in revenue or profitability."

Or, LANZA speaking outside a SEC 10-K setting, to a journalist in a local MA newspaper:

http://www.telegram.com/article/20141014/NEWS/310149525&Template=printart

Quote from article, never refuted by OCAT:

"We treated the last UK patients last month, and they also have not seen any safety issues related to the transplanted tissues themselves, either," Dr. Lanza said.

Advanced Cell now hopes to launch a 100-patient, phase 2 study in Stargardt's patients by the end of the year, according to Dr. Lanza.

A second, smaller phase 2 study in patients with age-related macular degeneration would follow, he said. Any treatment might not be ready for FDA approval until 2020, Dr. Lanza said. "

Well, that big ole 100-patient ole phase 2 study didn't start by the "end of the year" (2014) and now it's mid April 2015 and it STILL HAS NOT STARTED.

What OCAT mythological "eye treatment" to "fix your eye" is this again? Where can one go and get it done today?

Being driven into the .007's 2 million plus shares on the Ask/sell side

BMAK is parked with a 10K share block now at .0081, so that's the top today IMO. Massive sell side on the Ask this AM. It's being driven into the .007 range now IMO.

I think, some big convertible debt holder is converting or else BHRT has made another "draw" request to Magna and this is Magna driving her down during the period known as the "draw request" (it's some complicated formula that's all detailed in the Magna share registration SEC filing and SEC prospectus Magna made BHRT file for the $3 million credit-line product)

There is a bunch of convertible, aka toxic debt all coming due one after another in the next several months- so this may also be Asher, Daniel James, KBM etc "converting" piles of debt to 10's of millions of common shares IMO.

I think it's one or the other - and it's just gonna stack 10's of millions of cheap shares onto the Ask, on-going for months, probably forever IMO.

If those convertible debt holders convert in this price range- they all get like 45% to 47% discounts on their share conversions (see any recent 10-K or 10-Q filing and any Asher, Daniel James, Fourth Man, Vis Vire, KBM etc toxic debt deal and the share discount)-

So if they convert in this price range of the .007 to .008 area say, then they're gonna be getting 10's of MILLIONS of shares for about .004 or even cheaper probably.

STAGGERING on-going dilution happening IMO. Just 10's and 10's of millions of shares being converted and also probably a Magna credit-line draw. This is being driven by pure dilution now IMO.

My .0075 AM Bid cents worth

0.0075 / 0.008 (340000 x 2286400)

2.2 MILLION on the Ask/sell side, 7 to 1 sell versus the Bid.

http://www.otcmarkets.com/stock/BHRT/quote

Next 10-Q, well it's about 3 months (one qtr) between filings typically. Q1 technically just ended, end of March.

The past filing dates for most recent SEC filings are :

3/16/2015 10-K

11/7/2014 10-Q

8/1/2014 10-Q

5/9/2014 10-Q

So based on that history, I'd say about May 9th or so 2015 would be the 10-Q for Q1 probably, give or take a week. You notice the 10-Q's come a little quicker, a little closer together usually as they're unaudited and only cover the single qtr. The 10-K is the biggie, is outside audited and covers the whole year - so it usually takes a little longer.

I'd say May 9th is is about right for next 10-Q. Pretty much one month from today then IMO.

LOL quote, "Twitter is 33 billion market cap. A useful but glorified text messaging service. Bioheart $5 million never made sense to me IMO"

Well, maybe cause ole Twitter has like 250 MILLION plus monthly users and revenues that now well surpass $1 BILLION annually (growing rapidly) and over 3500 employees versus say THREE employees at ole BHRT? Maybe?

Ole Twitter has a global reach to every corner of planet earth. They have free cash flows (meaning they live on internal generated cash and not desperation toxic debt financing and similar like BHRT) - free cash flows of over $100 million and cash-on-hand after debt of about $2 BILLION cash sitting on their books. Unlike BHRT that just finished their "big sales yr" with a grand total of $36K total cash left to their name- against $10 million plus in debts.

Maybe that's why Twitter commands the market cap it has, versus ole 3 person, 700 MILLION and climbing O/S share ole BHRT (Twitter with a $billion plus in annual sales and 3600 employees has about 600 million shares O/S)? Maybe?

Just a few possibilities maybe to consider, IMO.

My .008 dilution shares worth (and sinking)

LOL quote, "The PPS will go to $25 a share in 5 years in my opinion."

OK?? It's at 7/10th of a PENNY yesterday and sinking like a boar anchor and they're diluting like a dilution machine = reality. But it's gonna just like magic go to some fantasy $25 a share in 5 years, LOL? Ok? Right on I guess?

Lets just make up imaginary share prices I guess? Based on what? The company is teetering on BK and insolvency per their own just filed SEC 10-K, which has I don't even remember how many "going concern" WARNINGS in it. They're gonna be lucky to survive for 5 yrs IMO and that apparently of their own auditors who reviewed and signed their just filed 10-K.

The lower the share price sinks- the more they need to dilute for ever smaller amounts of survival cash. That's just reality- versus making up prices like $25 a share out of thin air.

This company has lost over 99% of it's common share value since it went public in 2008 at $5 a share. It rapidly sank in price from $5 a share and was delisted from the Nasdaq barely 1 yr later. It's never gone up or traded up since then. It had about 20 million shares O/S at most in 2008/2009, today it has over 700 MILLION shares O/S and climbing rapidly (over 65 MILLION shares of dilution in just Jan, Feb and early March of 2015 were issued, see page F-34, just filed 10-K, most recent 10-K SEC filing).

$25 a share, LOL? How bout it ever reaches .25 CENTS a share again, and then $1 a share ever again, before some total fantasy number of $25 a share? What would possibly ever make this 3 person "company" worth $25 a share and the market cap that would come with that- a staggering market cap to say the least?

Total fantasy nonsense IMO, $25 a share. I'd highly doubt this will ever even see .50 CENTS a share ever again- the price it traded at (with about 30 million or less O/S shares when the present CEO took over control of running the company) in 2010.

My .0077 diluted cents worth (and sinking)

LOL, quote, "No lack or limitation here yahoo OCAT post:

OCATA Therapeutics PPS projections based on TOTAL ADDRESSABLE MARKET(TAM) for Pivotal SMD and Phase 2 AMD and upcoming milestones 2015/2016 "

Oh yeah. The ole lets just MAKE UP A BUNCH OF FANTASY SCENARIOS and imaginary share prices and play like it's really going to happen, LOL?

Gosh, ONLY $35 a share by what fantasy, 100% made up "scenario" date was that?

OCAT couldn't even pull off a successful $62 million secondary offering and hasn't even started the ole "BIG PHASE II" as they don't have the large funding to do it- but some "yahoo poster" can write a 100% fantasy based "story" telling everything that's going to happen in the next, coming 1 yr period and then attack a bunch of 100% made up "projections" and guesses and pure fantasy numbers to it, LOL?

OK. Sure. Right on. Let me guess what little, nothing, "stem cell" blog place that one originated from? It may have been on Yahoo, but I'd bet I know what micro "stem cell" blog place it originated from. The usual one- the one with more wrong "predictions" and more just plain old wrong info than any other one I've ever read or seen. Like batting zero for 100 in the ole "predictions" and fantasy made up scenarios and price share "predictions" department.

Sure, $35 a share by date XYZ and then $100's per share by blah, blah, blah and all the other imaginary stuff happening in between- meanwhile, the reality is they, OCAT, just had to go back and tap Lincoln for a few more months of survival burn-rate and pay the big executives money and keep the lights on and doors open dilution money. NOT "big trials" getting funded and moving ahead rapidly money- but keep the gig going and pay the big boys money IMO. Lincoln is not going to get this company anywhere near fully funded for a major, large, complex FDA phase II trial rocking on down the road- no way IMO. They need to spend and spend rapidly to even enroll- using expensive outside contract firms (OCAT only has about 35 employees and 5 or 6 are high paid execs who ain't gonna be doing any heavy lifting in a clinical trial)- so who at that little company is going to be running and actually conducting a large Phase II?

"Yahoo said in a post", sure. Right on. I'd say the price is treading water at $6 and change- right where it's been clear back to Nov 2014 and even before that and they have no major source of high quality funding in place as of today, right now. And I don't see a single thing in the Yahoo "fantasy projection" scenario even remotely coming true or even beginning to happen. None of it IMO.

LOL, quote, "The market can pour 400 million dollars into Go Daddy,

a failed web site company,

but,

it has no love for a curative therapy for blindness? "

What, they imaginary "cured" blindness again? When? Where did this fantasy "cure" take place? Where does one go to get this proven "cure" for human blindness? What major hospitals and what major insurance carriers are offering this imaginary "blindness cure" thingy again? I can't find it listed anywhere? The FDA approved this "cure" and I missed it? When was this?

GoDaddy is a failure, LOL? They just did an actual, real IPO and attracted top-shelf "big money" to the tune of half a $BILLION dollars, rather than a TWO MOONS KACHINA reverse merger straight to the OTC pinks and it's GoDaddy that's the "failure", LOL? Really?

GoDaddy is now valued at $4 BILLION by the free market place and attracted top Wall Street money and firms to sell their actual IPO and they're the "failure", LOL? Which company recently had a failed secondary trying to pitch and sell a lousy $62 mil worth of shelf filed dilution shares? GoDaddy used savvy marketing and well run business practices to become the largest web registrar in the world surpassing the old dog, Network Solutions and now has built an entire platform to host millions of web sites and small businesses all over the globe with near perfect precision and up-time, security solutions, site building tools, etc. No SEC violations and fines and no big legal settlements being paid by shareholders, no mass dilution to sink $350 million plus in lost, paid in, up in smoke capital down a 20 yr hole that lead to a single "article" in some journal that no one seems to care about as the OCAT share price treads water and goes nowhere.

See, the so called "failed" GoDaddy has millions of paying customers who want what the actual products they offer and sell. OCAT has no products and no customers and essentially pays insiders large coin (including bonuses LOL) while their common shares literally diluted out to over 3 BILLION plus shares and sunk to a literal 5 CENTS each, LOL.

GoDaddy went from about $100 MILLION in sales in approx 2005 to over $1 BILLION in sales by 2013, and that's a imaginary "failure" here in OCAT fantasy-ville, LOL? What's OCAT ever done to even come close to that growth story? 20 years of OCAT and what? What do they have? An "article" and a micro "trial" that may lead to nowhere by all statistical odds? GoDaddy at least has free cash flow, self generated and is not relying on some payday loan joint like Lincoln for month to month dilution survival, LOL.

Yeah, which company is the "failure" here and why? LOL.

Quote, "Agreed I feel commons are getting screwed here on the open market.. Why new investors going to buy when they know the loans will be converted into 45% discounts and sold on the open market from what I understand. Imo"

Equity, exactly correct IMO too.

I don't have time right now- but will try and do it later, but there is a bunch of these convertible debt deals all coming due one after another in the coming months, all the way to at least Oct 2015. It's gonna be staggering dilution IMO which in turn hits the Ask/sell-side of the market every single time.

Read page F-34 of the just filed 10-K, I've posted it a few times now. 65 MILLION plus shares of pure dilution were already issued out in just Jan, Feb and early March of 2015. Less than 3 months and 65 MILLION freaking shares got passed out- and doing the math on um shows that some of um went out as low as less than .004 cents each, staggering IMO. Mind blowing.

And I don't see any end to it- they inked that Magna deal and said they intend to tap and use ALL of that $3 million credit line if possible. The lower the share price goes that of course gets harder and harder to do- as there are percentage limits and caps on how much they can draw-down each time and it gets massively more dilutive the lower the share price goes.

And the real kicker- is Magna was not enough apparently. They then, in the first 3 months or less of 2015 inked qty-3 more convertible debt (aka toxic, floorless formula deals) with KBM Worldwide, Fourth Man and now a new hedge fund finance house called Vis Vires which I've never seen them use in the past.

The dilution will continue to be staggering IMO. 10's and 10's of millions of shares, easily surpassing 100 MILLION more shares within only months- given that 65 MILLION already had gone out by only early March of 2015.

It's dilution that's punishing the common shares IMO. I think it's immutable and beyond any doubt IMO as to that being the #1 cause and driver of the severe selling pressure and price decline. Remember, from their SEC filings- they diluted out over 300 MILLION shares in approx just the last 1 yr period alone. THAT is staggering IMO and has to have negative consequences to the common shares and common share holders- I just don't see how it can't?

Quote, ".008 broke support is Mike seeing this PPS? What happen to the plans of the CC we had? We were going to launched sales people etc I thought?"

How could he not, he personally signs every dilution finance deal they do- and they just did a bunch more in early 2015 and also diluted out over 65 MILLION shares just in beginning 2015 (Jan, Feb and till mid March, 2015. How would he not know their own massive dilution plans?)

Must be the share buyback LOL ?? You know, using part of the $36K total cash they had left on hand per their just recently filed SEC 10-K, the $36K total cash they had against over $2 MILLION in just accounts payable and then over $800K in "cash bonuses" (PAGE 65, just filed 10-K) awarded to just 2 people of a now 3 total "employee count" company, per their just filed 10-K's own statements. $500K of that $800K bonuses awarded is to him. His annual compensation package per PAGE 65 of the just filed 10-K is now over $1.8 MILLION worth, up from $936K in 2013. If that ain't a sweet gig in this economy- then I don't know what is? You know anyone doubling their total comp and pay package in 1 yr, when their company's shares are hitting all, all time lows and their market cap is breaking below $5 million today, even when massive share dilution is factored in?

How would the CEO not know what's going on?

PAGE F-34, most recent, just filed SEC 10-K:

http://www.sec.gov/Archives/edgar/data/1388319/000114544315000378/bioheart_10k.htm#x1_d284237a019

His personal signature is on the bottom of that 10-K filing. From that signed 10-K:

"Subsequent stock issuances

In January 2015, the Company issued 4,783,568 shares of its common stock in settlement for services, provided 14,299,567 shares of its common stock in settlement of $49,500 of outstanding convertible notes payable, and $2,981 accrued interest and 2,096,450 shares of its common stock for net proceeds of $16,118 from equity drawdown under the Magna Purchase Agreement.

In February 2015, the Company sold an aggregate of 1,443,656 shares of its common stock for net proceeds of $16,270. In connection with the stock sale, the Company issued an aggregate of 1,443,656 warrants to purchase the Company’s common stock for five years at $0.01127 per share. In addition, the Company issued 20,219,367 shares of its common stock in settlement of $132,500 of outstanding convertible notes payable and $2,520 accrued interest and 16,556,976 shares of its common stock for net proceeds of $135,645 from equity drawdown under the Magna Purchase Agreement.

In March 2015, the Company issued 6,185,432 shares of its common stock in settlement of $25,000 of outstanding convertible notes payable and $1,226 accrued interest. In addition, the Company issued 635,357 shares of its common stock as true up shares relating to the February 2015 equity drawdown under the Magna Purchase Agreement.

Options granted

On February 2, 2015, the Company granted an aggregate of 7,000,000 options to purchase the Company’s common stock to Board of Directors members at an exercise price of $0.01116 for ten years, vesting immediately.

Subsequent financing

On January 7, 2015, the Company entered into a Securities Purchase Agreement with KBM Worldwide, Inc. (“KBM”), for the sale of an 8% convertible note in the principal amount of $38,000 (the “Note”).

The Note bears interest at the rate of 8% per annum. All interest and principal must be repaid on October 9, 2015. The Note is convertible into common stock, at KBM’s option, at a 45% discount to the average of the three lowest closing bid prices of the common stock during the 10 trading day period prior to conversion. In the event the Company prepays the Note in full, the Company is required to pay off all principal, interest and any other amounts owing multiplied by (i) 140% if prepaid during the period commencing on the closing date through 179 days thereafter. After the expiration of 180 days following the date of the Note, the Company has no right of prepayment.

On January 28, 2015, the Company entered into a Securities Purchase Agreement with Fourth Man, LLC., for the sale of an 9.5% convertible note in the principal amount of $25,000 (the “Note”).

The Note bears interest at the rate of 9.5% per annum. All interest and principal must be repaid on January 27, 2016. The Note is convertible into common stock, at Asher’s option, at a 47% discount to the lowest daily closing trading price of the common stock during the 10 trading day period prior to conversion. In the event the Company prepays the Note in full, the Company is required to pay off all principal at 150%, interest and any other amounts.

On February 19, 2015, the Company entered into a Securities Purchase Agreement with Vis Vires Group, Inc. (“VIS”), for the sale of an 8% convertible note in the principal amount of $38,000 (the “Note”).

The Note bears interest at the rate of 8% per annum. All interest and principal must be repaid on November 23, 2015. The Note is convertible into common stock, at VIS’s option, at a 45% discount to the average of the three lowest closing bid prices of the common stock during the 10 trading day period prior to conversion. In the event the Company prepays the Note in full, the Company is required to pay off all principal, interest and any other amounts owing multiplied by (i) 140% if prepaid during the period commencing on the closing date through 179 days thereafter. After the expiration of 180 days following the date of the Note, the Company has no right of prepayment.

F-35

"

He personally signed off on all that: 65 MILLION plus shares of recent dilution and Qty-3 "toxic" (the SEC's definition and term, not mine) convertible, floorless debt financing deals- w/ KBM Worldwide, Fourth Man and a new firm they signed on with called Vis Vires.

Of course the CEO knows the drill and what's happening IMO. It's 100's of millions of shares of pure dilution and near endless, continuous, on-going use of toxic debt finance lending firms- this is the common outcome of that taking place. As old as the OTC and penny-ville.

Wow, 10K shares left at .008 ??

They had a big ole pile on there just a while ago, all gone now? Next stop is .007's if they burn up that $80 bucks worth at .008

Did someone actually suck up the 300K or 400K plus they had showing at .008 or did the MM's just pull um off the Bid?

That was weird?

0.0075 / 0.0081 (10000 x 10000)

Oh, there it went, the MM CDEL just took the Bid down into the .007's, holy cow. Guess the .008 shares really are gone then. Wow.

http://www.otcmarkets.com/stock/BHRT/quote

CDEL on the Bid w/ 10K and good ole BMAK on the Ask w/ 10K?? If that ain't two peas in a pod, eh?

Wonder where the bottom is now on this?

Some firm converting debt or a Magna "draw" on the credit line maybe?

Sure looks like some firm is "working it" again hard to drive the price down further. Remember, the toxic, convertible debt formulas and how they work. It's always based on some formula worded like, " the lowest of the prior 3 or prior 10 trading days closing price", something to that effect in the wording always (see any recent 10-K or 10-Q filing and look at Asher, Daniel James, KBM Worldwide, Fourth Man, Vis Vire, etc.- any of those toxic note, convertible debt deals).

So if the firm like Magna wants more shares, it's to their advantage to have the price lower after BHRT makes a "draw request" on that Magna credit line and same for like an Asher if they're deciding to convert their loans to shares, which they always do of course as BHRT has no cash to pay them back (and there is a truck load of these convertible debt, "toxic note" deals all coming due soon (see latest 10-K SEC filing or any recent 10-Q from 2014), so I'd not be surprised if several toxic debt firms are converting about now before the "note" final due date: Daniel James, Asher, Fourth Man, etc are all holding convertible debt all due in the coming months).

If this breaks the .008 level in here, it's look out below again IMO. This thing may take one of these mega price drop, rapid down spikes here again IMO, if this is indeed some "big boys" working this related to convertible debt and/or the Magna dilution credit line IMO.

500K shares almost, seconds after the open and it was to the down side again and both the Bid and Ask are pinned down hard right near .008 levels again this AM.

Looking like tough sledding in here still IMO. Dilution, dilution, dilution is driving the ship at this point IMO.

http://www.otcmarkets.com/stock/BHRT/quote

0.008 / 0.0082 (589600 x 111111)

About $4,700 on that Bid right now left at .008 and the next stop as of now is .0072, wow.

Wait and see what happens here I guess. Tough opening again so far.

What LOL, quote, "Fidelity fund ONEQ is holding OCAT/OCATA."???

Huh?

"Institutional" aka "fund" ownership of ole OCAT is like 0.04% of O/S shares. Like NON EXISTENT for all intents and purposes:

From thee Nasdaq market place itself:

http://www.nasdaq.com/symbol/ocat/institutional-holdings

Institutional Ownership 00.04%

GOOSE EGG on any funds owning this one. Not a happening.

I looked on the "daily holdings log" of that Fidelity "ONEQ" and didn't find ole OCAT. Might of missed it? That fund holds 100's of stocks and most at like $10K worth or less. If they do hold any OCAT, it's noise level money- it's an index type ETF style fund. They probably buy/sell micro holdings of stuff all day long- I saw many of their "holdings" were $5K worth or less.

Non event/issue IMO. Not an "institutional" buyer/holder that I'm aware of?

When they get to 10% or 15% or 20% institutional ownership (IF EVER) - it might be worth noting then IMO.

Quote wrong, "old old news once again... OCAT is not ACTC and nobody here is at a 98.725% loss...lol. "

1) OCAT and ACTC are one in the same- their own SEC filings, recent articles about the company, etc use the company names interchangeably. Much of what would constitute their supposed "intellectual property" (if it's worth anything) would be in the name of ACTC and not "OCAT".

2) Doesn't matter who here is at a 98.7% loss or not- it's still the actual and 100% real loss to the common shares since the company going public (straight to the OTC by the way). ANY institutional or "big money" investor is certainly going to consider the company's historical poor share performance, poor business mgt and poor performance, ROI of which OCAT/ACTC has none, historical dilution, failure to perform or produce for 20 yrs, etc. It's as real as it gets. Wonder why the secondary failed and no one wanted to pay anything but bottom basement for ACTC/OCAT OTC shares? Their historic track record was and is horrible- 3 BILLION plus shares of dilution driving their stock price to a literal 5 CENTS. That's why no major investment firm is going to step in and buy a single, large block of their stock w/o demanding a very steep discount (risk premium) IMO.

It'd be foolish to think that a historic performance of their shares losing nearly all their value won't have a very strong influence on any potential "big money" firm they're trying to pitch their shares to. Most firms don't buy losers, almost never. They want a track record of price APPRECIATION, PERFORMANCE and GROWTH. NONE of which OCAT/ACTC has yet to produce or show they can produce. Add in SEC violations with fines and prosecution, large legal settlements being paid for with share dilution and you got a highly tainted recent past (not "old news" or old history, but RECENT performance failures) IMO.

It takes more than a quick name change, a new "logo" and a few bucks to change one's web site to clean up a past as tainted as this one is carrying IMO. They got a lot of baggage to shed IMO. Gonna take a lot to prove they're a different deal now. So far- not impressed. Botched the secondary and have yet to raise any large source of financing. The change to the Nasdaq has done nothing for the share price- it's trading below where it was on the OTC and hasn't attracted dime one of institutional money, or major fund investment, none.

REALITY versus the big myths and tall tales IMO.

Here's REALITY from their just filed 10-K (March 16, 2015), NOT "old news":

PAGE 16:

"Our independent auditor’s report for the fiscal year ended December 31, 2014 includes an explanatory paragraph regarding substantial doubt about our ability to continue as a going concern.

Due to the uncertainty of our ability to meet our current operating and capital expenses, in their report on our audited annual financial statements as of and for the year ended December 31, 2014, our independent auditors included an explanatory paragraph regarding concerns about our ability to continue as a going concern. Recurring losses from operations raise substantial doubt about our ability to continue as a going concern. If we are unable to continue as a going concern, we might have to liquidate our assets and the values we receive for our assets in liquidation or dissolution could be significantly lower than the values reflected in our financial statements. In addition, the inclusion of an explanatory paragraph regarding substantial doubt about our ability to continue as a going concern and our lack of cash resources may materially adversely affect our share price and our ability to raise new capital or to enter into critical contractual relations with third parties.

"

PAGE 43:

"We cannot assure you that public or private financing or grants will be available on acceptable terms, if at all. Several factors will affect our ability to raise additional funding, including, but not limited to, the volatility of our common stock and the broader public equity market. If we are unable to raise additional funds, we will be forced to either scale back our business efforts or curtail our business activities entirely. As of December 31, 2014, the Company has an accumulated deficit of $349.1 million, recurring losses from operations, and negative working capital which raise substantial doubt about the ability of the Company to continue as a going concern. Furthermore, an emphasis of matter paragraph related to an uncertainty as to the Company’s ability to continue as a going concern has been included in the auditor’s opinion."

PAGE 46:

"We have also audited, in accordance with the standards of the Public Company Accounting Oversight Board (United States), the consolidated balance sheet of Ocata Therapeutics, Inc. and Subsidiary as of December 31, 2014, and the related consolidated statements of operations, stockholders' deficit, and cash flows for the year then ended and our report dated March 16, 2015 expressed an unqualified opinion thereon and included an emphasis of a matter paragraph relating to an uncertainty as to the Company’s ability to continue as a going concern.

/s/ BDO USA, LLP

Boston, Massachusetts

March 16, 2015"

PAGE F-1:

"The accompanying consolidated financial statements have been prepared assuming that the Company will continue as a going concern. As described in Note 2 to the consolidated financial statements, the Company has suffered recurring losses from operations and has a net capital deficiency that raise substantial doubt about its ability to continue as a going concern. Management’s plans in regard to these matters are also described in Note 2. The consolidated financial statements do not include any adjustments that might result from the outcome of this uncertainty.

We have also audited, in accordance with the standards of the Public Company Accounting Oversight Board (United States), Ocata Therapeutics, Inc. and Subsidiary’s internal control over financial reporting as of December 31, 2014, based on criteria established in Internal Control — Integrated Framework (2013) issued by the Committee of Sponsoring Organizations of the Treadway Commission (COSO) and our report dated March 16, 2015 expressed an unqualified opinion thereon.

/s/ BDO USA, LLP

Boston, Massachusetts

March 16, 2015"

PAGE F-7: