News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Dragon Lady

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Quote Carlcarlos, "Asher, KBM, and Magma according to the CEO of $MMMW tried calling over 83 times since the beginning of the year to tried to sell their toxic poison."

(Just a note- it's MAGNA with an "N", not Magma. Just a name typo)

That is fascinating info to say the least. What's really interesting about it- is it jives 100% with what the Bloomberg financial journalist found and wrote about in a recent 2015 piece and that Bloomberg produced a video "short" piece about regarding "toxic" finance houses. That journalist stated the EXACT same thing as Carlcarlos appears to have validated here via the MMMW CEO provided info on this particular stock. EIGHTY THREE PHONE CALLS (or more, aka "cold sales calling" from toxic debt deal makers). THAT is stunning- but it 100% is in-line with what the Bloomberg piece wrote about and their investigative journalism team found.

http://www.bloomberg.com/news/articles/2015-03-12/josh-sason-made-millions-from-penny-stock-financing

Notice in the Bloomberg piece- it matches exactly what this MMMW CEO has stated. The "toxic" debt houses cold call- and they DO NOT EVEN CARE what business the company is in, they DO NOT EVEN CARE to look at the company financial statements, they don't even ask what product the company sells or care, etc. ALL THE TOXIC LENDER CARES ABOUT IS IF THE STOCK TRADES ENOUGH SHARES A MONTH- aka reasonable "liquidity" so that they, the toxic lender, can DUMP THEIR DISCOUNTED SHARES once in hand- no matter how low the share price goes. In fact- the lower the price is driven down in the eventual "death spiral", it is usually even better for the toxic lender and these "floorless" aka "convertible debt" deals.

Notice also in the Bloomberg piece- the "boiler room" (effectively what these hedge fund toxic lenders are IMO) they even have "salesman" who are really nothing more than 20 something yr olds- who take on pseudo names and pseudo personas to act and sound like "big money" guys, when all they are is cold callers, dialing CEO's of cash desperate companies who they've screened using software programs and all they care about is that the shares trade with reasonable liquidity and volume and they'll do a toxic debt deal with the company no questions asked essentially.

Fascinating. The Bloomberg piece even quotes a CEO who's stock had gotten crushed via use of toxic, convertible debt deals- and that CEO said no matter how low the share price went his phone was still ringing off the hook via these same hedge firms continually calling and offering to lend him even more money in their discounted "shares-for-cash" deals.

Amazing. EIGHT THREE plus phone calls trying to hook this CEO onto the "toxic debt" drug and easy cash money train. The "easy cash" route- but the one that is notorious for crushing the common shares eventually to dust, nearly every time and every place these deals gets done.

http://www.sec.gov/answers/convertibles.htm

The SEC's own warning about "floorless" aka "toxic" convertible debt. Their own words call it "toxic" and "death spiral" etc

LOL quote, "Why is the DeltaCell TM upgrading OCAT? "

"Upgrade"?? Where? It's a re-print of an existing article and contains no "upgrade"??

OCAT essentially has no analyst coverage for the most part- let alone any "upgrades" etc? Where?

A "trade mark", wow. How does that add value to a company or a stock? Anyone can file for a trademark on a name like "DeltaCell"- it's about a 10 minute form/piece of paper to fill out and mail in. What's it going to do to help the company pass large phase II and phase III clinical trials successfully? Has this "trade mark" gotten them any large funding? They can file "trade marks" for names till the cows come home- what difference does it make if they can't even fund their own key clinical trials and advance them as promised?

"trade marks", LOL. Wow.

Lanza says "CAUTION" in highly respected journal "NATURE". Peer review commentary in same article says sample size TOO SMALL to yet be meaningful- doesn't sound like any "slam-dunk" ole "done deal" yet to me??????

http://www.nature.com/news/stem-cells-pass-safety-test-in-vision-loss-trial-1.17451

The VERBATIM article, again, from the highly respected science journal, "NATURE"-

"A company that has spent more than 20 years trying to develop treatments based on embryonic stem cells is taking encouragement from small, preliminary tests of the cells in people with progressive vision loss. If the technique continues to impress in larger trials designed to assess its effectiveness, it could become the first therapy derived from embryonic stem cells to reach the market.

A study of four patients, published in Stem Cell Reports on 30 April1, shows that injection of retinal cells derived from stem cells is safe for people with macular degeneration. The report follows similar results from a trial in 18 patients that was published last October2.

Both studies were meant to assess safety only, and neither included a control group. In the latest study, conducted by researchers in Korea and the United States, three participants were able to read 9–19 more letters further on an eye chart a year after treatment — but two of the three also gained some ground in their untreated eyes."

MORE...

"“This bodes well,” says Robert Lanza, chief scientific officer at Ocata Therapeutics in Marlborough, Massachusetts, and an author of the study. “But I think we need to interpret this improvement cautiously until more controlled studies are done.”

The sample size is too small to warrant much excitement, cautions ophthalmologist Tien Yin Wong of the Singapore National Eye Centre. “At this stage it’s hard to say if the visual improvement will be sustained,” he says. “But it’s very promising.”

"

Ah, the ole UNTREATED EYE gained ground too "problem"?? THAT is where the big ole phase II's, the much more complicated, much broader patient cross-section, the ole control arm, the trials with a placebo arm can trip something like these micro tiny phase I's up every single time. The untreated eye showed improvement TOO?? Well SHAZAM, whata ya know? And a peer commentator- the SAMPLE SIZE IS TOO SMALL to "warrant much excitement"- SHAZAM again. Phase I micro trials are famous for this "problem"- it's common sense. What can one really know about a cross section of human beings when 18 or so people are involved and the company itself ran and controlled the entire "trial"- it's always the problem in the phase I stage. It's why most of the "promising" trials- if and when they fail, they fail big in the phase II portion. It's magnitudes harder than the tiny phase I's to pass the criteria.

https://www.michaeljfox.org/foundation/publication-detail.html?id=76&category=3

A CLASSIC phase II failure- of what was a "very promising" phase I "stem cell" so called "treatment" for Parkinsons. It bombed totally in phase II, when phase I just looked like such a "sure thing"- and everyone was disappointed. Classic example. FIVE YEARS they had in phase I and it was all super "promising" and "no safety issues" etc (SOUND FAMILIAR ?) Then a 71 person phase II, and it bombed. Out. Cancelled. Done. Over. And they had a big hitter, "Bayer Schering Pharma AG" partnered with um, it was no sluff, bush-league small timers doing this Phase II.

The "placebo problem" explained in great detail- why so many new candidates can't beat the ole placebo arm. It's one of the most perplexing problems in all of medicine and science:

https://nwpf.org/stay-informed/news/2015/02/for-patients-with-parkinsons-disease,-expensive-placebo-works-better/

Quote from article:

"The upshot is fewer new medicines available to ailing patients and more financial woes for the beleaguered pharmaceutical industry. Last November, a new type of gene therapy for Parkinson's disease, championed by the Michael J. Fox Foundation, was abruptly withdrawn from Phase II trials after unexpectedly tanking against placebo. A stem-cell startup called Osiris Therapeutics got a drubbing on Wall Street in March, when it suspended trials of its pill for Crohn's disease, an intestinal ailment, citing an "unusually high" response to placebo. Two days later, Eli Lilly broke off testing of a much-touted new drug for schizophrenia when volunteers showed double the expected level of placebo response."

All indications to me are that this OCAT stuff is YEARS and YEARS away from even a remote chance at an FDA or similar approval IMO- and $100 of millions worth of trial costs. I believe Lanza made that point clear when he was quoted near end of 2014 in a local MA newspaper- and said the phase II was supposed to start "hopefully by end of 2014" (it's now MID 2015 and no phase II is started yet) and he said year 2020 for a "chance at an FDA approval" or similar (paraphrasing).

http://www.telegram.com/article/20141014/NEWS/310149525&Template=printart

""We treated the last UK patients last month, and they also have not seen any safety issues related to the transplanted tissues themselves, either," Dr. Lanza said.

Advanced Cell now hopes to launch a 100-patient, phase 2 study in Stargardt's patients by the end of the year, according to Dr. Lanza.

A second, smaller phase 2 study in patients with age-related macular degeneration would follow, he said. Any treatment might not be ready for FDA approval until 2020, Dr. Lanza said."

That was dated Oct 14, 2014 and the END OF YEAR phase II DID NOT HAPPEN.

In his latest "talk", Lanza now said they "We're hoping in the coming months to certainly initiate our Phase II clinical trial." Oh, so now it's "hoping" and "in the coming MONTHS"??? How many MONTHS plural? 2, 4, 6, 8 months? End of 2015? Who knows what that vague a statement even means IMO? It's MAY 2015 now, but it was supposedly going to "start end of year" in 2014? Now it's we "hope in the coming months"??

Just keeps dragging out- just like the old ACTC, OTC penny days IMO. What's changed? Missed targets and a lot of "maybes" and "hopes" and vagaries is all I see? Oh, and tons of more money needed- which they do not appear to have at this point- including a botched/failed secondary that couldn't raise $62 million in a raging bio-tech bull market probably never before seen in the history of U.S. or world markets.

From their latest filed 10-K, PAGE 16:

"Other than our arrangement with Lincoln Park, we have no sources of debt or equity capital committed for funding. Recent attempts to raise capital in the public equity markets have proven unsuccessful, and we can provide no assurance that we will be successful in any future funding effort. "

If this is the supposed cat's meow, "slam-dunk" and medical miracle thingy and all- then why do they never attract any large funding? Never any high quality, non dilutive, high quality big time funding? Why is that?

Quote, "Sure but less and less amounts in toxic loans have been taken out."

What? What proof of there is that?

They, BHRT just did qty-3 new toxic, convertible, floorless debt deals in just early 2015 and have a whole slew of them coming due from 2014 and past and also inked a Magna 24 "credit line" which via it's various provisions, share discount, etc IMO makes it fall into the "toxic" and highly dilutive category.

What proof is there that BHRT is using less and less toxic debt? It appears to me that it's all they live and survive off of for all intents and purposes?

Most recent filed SEC 10-K, PAGE F-34:

"Subsequent financing

On January 7, 2015, the Company entered into a Securities Purchase Agreement with KBM Worldwide, Inc. (“KBM”), for the sale of an 8% convertible note in the principal amount of $38,000 (the “Note”).

The Note bears interest at the rate of 8% per annum. All interest and principal must be repaid on October 9, 2015. The Note is convertible into common stock, at KBM’s option, at a 45% discount to the average of the three lowest closing bid prices of the common stock during the 10 trading day period prior to conversion. In the event the Company prepays the Note in full, the Company is required to pay off all principal, interest and any other amounts owing multiplied by (i) 140% if prepaid during the period commencing on the closing date through 179 days thereafter. After the expiration of 180 days following the date of the Note, the Company has no right of prepayment.

On January 28, 2015, the Company entered into a Securities Purchase Agreement with Fourth Man, LLC., for the sale of an 9.5% convertible note in the principal amount of $25,000 (the “Note”).

The Note bears interest at the rate of 9.5% per annum. All interest and principal must be repaid on January 27, 2016. The Note is convertible into common stock, at Asher’s option, at a 47% discount to the lowest daily closing trading price of the common stock during the 10 trading day period prior to conversion. In the event the Company prepays the Note in full, the Company is required to pay off all principal at 150%, interest and any other amounts.

On February 19, 2015, the Company entered into a Securities Purchase Agreement with Vis Vires Group, Inc. (“VIS”), for the sale of an 8% convertible note in the principal amount of $38,000 (the “Note”).

The Note bears interest at the rate of 8% per annum. All interest and principal must be repaid on November 23, 2015. The Note is convertible into common stock, at VIS’s option, at a 45% discount to the average of the three lowest closing bid prices of the common stock during the 10 trading day period prior to conversion. In the event the Company prepays the Note in full, the Company is required to pay off all principal, interest and any other amounts owing multiplied by (i) 140% if prepaid during the period commencing on the closing date through 179 days thereafter. After the expiration of 180 days following the date of the Note, the Company has no right of prepayment."

So that's THREE new one's in 2 monts in 2015 right there plus the Magna credit line being tapped as those deals were being inked (see same page of the same 10-K)

And then there all these deals coming due in the same 10-K filing:

PAGE F-17:

"2014 Notes

During the year ended December 31, 2014, the Company entered into a Securities Purchase Agreements with Asher Enterprises, Inc. (“Asher”) or affiliates, for the sale of 8% convertible notes in aggregate principal amount of $334,000 (the “Asher Notes”)."

"The remaining principle balance as of December 31, 2014 was $151,000." (DUE NO LATER THAN AUG 2015)

"During the year ended December 31, 2014, the Company entered into Securities Purchase Agreements with Fourth Man, LLC. (“Fourth Man”), for the sale of an 8% to 9.5% convertible notes in the aggregate principal amount of $100,000 (the “Note”)."

"The remaining principle balance as of December 31, 2014 was $75,000."

(DUE NO LATER THAN AUG 2015)

"2014 Notes

During the year ended December 31, 2014, the Company entered into Securities Purchase Agreements with Daniel James Management (“Daniel”) for the sale of 8% to 9.5% convertible notes in aggregate principal amount of $135,000 (the “Daniel Notes”)."

"The remaining principle balance as of December 31, 2014 was $75,000."

(DUE NO LATER THAN Nov 30 2015)

"Magna Capital Group

2014 Notes

During the year ended December 31, 2014, the Company entered into a Securities Purchase Agreement with Magna Capital Group (“Magna”) for the sale of a convertible note in aggregate principal amount of $307,500 (the “Magna Note”) and an original interest discount (“OID”) of $102,500. $40,000 of the outstanding principal amount of the Convertible Note (together with any accrued and unpaid interest with respect to such portion of the principal amount) will be automatically extinguished upon the filing of the registration statement, following the closing of the Securities Purchase Agreement. In addition, $62,500 of the outstanding principal amount of the Convertible Note (together with any accrued and unpaid interest with respect to such portion of the principal amount) will be automatically extinguished if (i) the registration statement is declared effective by the SEC on or prior to the earlier of (A) the 120th calendar day after October 7, 2014 and (B) the fifth business day after the date we are notified by the Securities and Exchange Commission, or the Commission, that the registration statement will not be reviewed or will not be subject to further review, and this prospectus is available for use by Magna for the resale by Magna of all of the shares of our common stock issued or issuable upon conversion of the Convertible Note and (ii) no event of default under the Convertible Note or an event that with the passage of time or giving of notice would constitute an event of default under the Convertible Note has occurred on or prior to such date. On November 21, 2014, the Company filed its registration statement and on December 22, 2014, was declared effective. As such, the principle amount of the note was reduced by an aggregate of $102,500.

The Convertible Note matures on August 7, 2015 and, in addition to the approximately 33.33% original issue discount, accrues interest at the rate of 12% per year. The Convertible Note is convertible at any time, in whole or in part, at Magna’s option into shares of Company common stock at a fixed conversion price of $0.01035 per share, subject to adjustment pursuant to the “full ratchet” and standard anti-dilution provisions contained in the Convertible Note"

What indication is there that "less and less" of these toxic convertible are being used? The 10-Q is due out any time here- it will show if they inked any more deals in addition to the qty-3 already done at the start of 2015 alone.

IMO, I don't see any indication of "less and less" toxic debt being used? Again, IMO, the Magna line alone is about as "toxic" as it gets from all available info I could find on Magna and their reputation of how they "do what they do"

They, BHRT, got toxic notes thus "coming due" (aka will highly likely be converted- I don't think BHRT EVER pays these back, they always get converted to free trading, common share dilution at their STEEP discounts as far as I'm aware from all past SEC filings)- they have them coming due fromm essentially about right now to several in Aug 2015, Nov 2015 and all the way to Jan of 2016. And again, until the 10-Q gets released, there may be even more for all one knows- given they already did qty-3 in Jan/Feb of 2015 alone. They have a near never ending stream of "convertible notes" stacked in a cue all coming due one after another after another. It says so right there in those most recent 10-K statements. Pretty clear to me- the way I read it?

Again, IMO, the Magna line alone is about as "toxic" as it gets from all available info I could find on Magna and their reputation of how they "do what they do" That "credit line" is in place for 24 months, is for $3 million in dilution and BHRT stated they PLAN TO TAP and USE IT ALL in their filing statements (see SEC docs Magna share registration statements).

http://www.bloomberg.com/news/articles/2015-03-12/josh-sason-made-millions-from-penny-stock-financing

65 MILLION shares of common stock dilution already issued out in just less then the first 3 MONTHS of 2015 and a good chunk of it was to MAGNA and related to "tapping" the MAGNA dilution credit line. Due the math on what those shares got issued at- they're DISCOUNTED CHEAP due to the "true up" pricing and all the other intricacies written into that Magna deal. Again, what proof of "less and less" anything is there? Where? I don't see it?

PAGE F-34 most recent filed 10-K:

"NOTE 15 — SUBSEQUENT EVENTS

Subsequent stock issuances

In January 2015, the Company issued 4,783,568 shares of its common stock in settlement for services, provided 14,299,567 shares of its common stock in settlement of $49,500 of outstanding convertible notes payable, and $2,981 accrued interest and 2,096,450 shares of its common stock for net proceeds of $16,118 from equity drawdown under the Magna Purchase Agreement.

In February 2015, the Company sold an aggregate of 1,443,656 shares of its common stock for net proceeds of $16,270. In connection with the stock sale, the Company issued an aggregate of 1,443,656 warrants to purchase the Company’s common stock for five years at $0.01127 per share. In addition, the Company issued 20,219,367 shares of its common stock in settlement of $132,500 of outstanding convertible notes payable and $2,520 accrued interest and 16,556,976 shares of its common stock for net proceeds of $135,645 from equity drawdown under the Magna Purchase Agreement.

In March 2015, the Company issued 6,185,432 shares of its common stock in settlement of $25,000 of outstanding convertible notes payable and $1,226 accrued interest. In addition, the Company issued 635,357 shares of its common stock as true up shares relating to the February 2015 equity drawdown under the Magna Purchase Agreement."

I don't see any "less and less" of anything related to BHRT's use of toxic debt and dilution? None? All looks like more of the same IMO. AND, despite all that- they ended 2014 with a grand total of a pittance of $36K CASH left to their name. Total. $36K cash.

LOL quote, "This is one of those safe at any price stocks for a long time"

Oh yeah, right on. Cause it's ONLY lost 98% plus of the common share value to date. Heck, solid as a rock, LOL !! And some SEC violations and accounting problems and massive insider self enriching along the way just for the gravy on top.

Oh yeah, what the heck could possibly go wrong now- now that they've completed ONE tiny, tiny little trial in 15 years and $350 MILLION in sunk capital gone down the black hole, while diluting out to a literal 3 BILLION plus shares and to a share price of a literal 5 CENTS a share.

Oh yeah, it's "in the bag" for sure. Absolutely. I mean just a piddly ole phase II and then a phase III or maybe two if the FDA requires it and $100's of MILLIONS more in cash needed that they presently DO NOT HAVE, but heck yeah- just a "done deal" now. Right on. What could possible go wrong- since most clinical trials if they fail, fail in the phase II portion, oh yeah !!

LOL BS quote, "Premarket OCAT $7.80: Shares bought by Vanguard and Fidelity may be helping uptrend. Shorts finding it hard to find covering shares."

Vanguard and Fidelity don't buy some pittance of shares in the pre-market? What myth is this now? When an order gets electronically routed, as they ALL do nowadays, does it have a stamp or something on it that says "Fidelity" or "Vanguard", LOL???

The open short interest on this stock, as a percentage of float is noise level. It's nothing and has nothing to do with the share price weakness. LACK OF BUYERS and lack of a long term financing plan is probably what drives 90% of this right now IMO. They failed and botched their secondary. They live off a Lincoln credit card line which is pittance money compared to what it will take to fund and run a large phase II, let alone pay their overhead bloat and keep the lights on (what, like 6 or 7 "C" level managers for a 35 person total headcount company? It's got a serious case of TOP BLOAT IMHO, like a major serious case).

Lack of cash and the fact the phase II is sitting, going nowhere and it's now mid 2015 (remember the ole we hope to have it started by end of 2014?). That's all that's going on IMO- and why this still trades BELOW where it was as an OTC penny stinker, below where it was even 3 yrs ago.

From their just recently filed 10-K:

PAGE 16:

"Other than our arrangement with Lincoln Park, we have no sources of debt or equity capital committed for funding. Recent attempts to raise capital in the public equity markets have proven unsuccessful, and we can provide no assurance that we will be successful in any future funding effort."

PAGE F-7:

"The accompanying consolidated financial statements have been prepared in conformity with GAAP which contemplate continuation of the Company as a going concern. However, as of December 31, 2014, the Company has an accumulated deficit of $349.1 million, recurring losses from operations, and negative working capital which raise substantial doubt about the ability of the Company to continue as a going concern. The ability to continue as a going concern is dependent upon many factors, including the Company’s ability to raise additional capital in a timely manner. On a long-term basis, we have no expectation of generating any meaningful revenues from our product candidates for a substantial period of time and must rely on raising funds in capital transactions to finance our research and development programs. Our future cash requirements will depend on many factors, including the pace and scope of our research and development programs, the costs involved in filing, prosecuting and enforcing patents, and other costs associated with commercializing our potential products. Accordingly, management’s plans to continue as a going concern contemplate raising additional capital including the execution of an agreement for a $30 million equity line in late June 2014, of which approximately $18.6 million remains available as of December 31, 2014. There can be no assurances that management can raise the necessary additional capital on favorable terms or at all. The accompanying financial statements do not include any adjustments that might be necessary if the Company is unable to continue as a going concern"

RED, DOWN 25% on open ?? Holy cow !

The MM's just plastered it to .0051 again. Yesterday was .0049 for the AM low. Looks like 1/2 CENT is the range these MM's are aiming for here now, or what they'll pay for any sell order. Wow.

0.0065 / 0.0068 (23000 x 91000)

Then the MM brings the Bid back up to .0065 after hitting .0051 first thing- but it's only 23K shares on the Bid and all .005's below that. That means like $150 bucks left on the Bid and then it's .005's , or look out below.

Wow, this thing is just in free-fall it appears. Where are the buyers and buying pressure now that's it's in the 1/2 CENT range? Not a single rush of big buying for weeks and weeks, just the slow bleed down?

The lower this base price range goes- then the harder and harder and mega more dilutive it gets each time BHRT goes back to tap Magna or some other toxic, convertible debt lender which they from their SEC filings (even the most recent 10-K for example) appear to do on a regular, continual, on-going basis.

Looking pretty weak and pretty rough in here- might be another brutal Friday like some of the past ones IMO.

Well, that $150 bucks worth on the Bid is gone in the .006's now. It's all .005's now it looks like. What a drubbing this one is getting- these OTC MM's or just lack of buyers is really hitting it hard?

0.0056 / 0.0068 (320000 x 91000)

The 1/2 CENT range may be the new "normal" for a while it's looking like, more and more likely IMO.

Good post by another I-HUB member on toxic debt- a specific example of one company and how it's death spiral played out. Very well written and researched IMO.

http://investorshub.advfn.com/boards/read_msg.aspx?message_id=107118774

Look at the names- all the "usual suspects" were involved and even some other firms who's names I'd never seen. Might be good at some point to begin to compile and keep a running list on this board of all known "toxic" lenders that I-HUBers find in the SEC filings of the stocks they follow. Would be interesting to see how many names can be compiled.

Most have of course heard of:

Asher

Hanover holdings (I believe the "old" Asher name or associated firm)

Magna of course of new fame (see the Bloomberg article and video journalism piece on them)

http://www.bloomberg.com/news/articles/2015-03-12/josh-sason-made-millions-from-penny-stock-financing

Then I've heard of

KBM Worldwide

Daniel James

Fourth Man

Vis Vires Group

And now that post above by the other I-HUB member noted these names:

IBC Funds

Iron Ridge

Redwood Management

Tarpon Bay Partners

There's gotta be a whole lot more out there- try and list their names here when you see them. They will then come up in Google and other search results if people search "I-HUB toxic lenders" or similar terms and should bring them to this board- where they can get educated on "toxic", floorless convertible debt and the names to watch out for.

Might break even with it's old OTC share price, "maybe" except it sells off in to any strength, LOL.

They're living on the 100% dilution Lincoln dilution credit card "line" style financing- and no, it's not anywhere near enough to fund a large, phase II, FDA quality trial.

Lanza in his recent talk was very vague as to when the phase II would even start (as opposed to the 2014 interview where he said "he hoped end of 2014") now he just gave it the ole "we'd hope maybe sometime soon" (paraphrasing).

The "big news" again today barely bumps it and it sells off right into strength like clock work.

The most recent 10-K, PAGE 13:

"Our ability to become profitable depends upon our ability to generate revenue. We do not anticipate generating revenues from product sales for the foreseeable future, if ever. Our ability to generate future revenues from product sales depends heavily on our success in:"

and PAGE 16:

"Other than our arrangement with Lincoln Park, we have no sources of debt or equity capital committed for funding. Recent attempts to raise capital in the public equity markets have proven unsuccessful, and we can provide no assurance that we will be successful in any future funding effort. "

PAGE 43:

"

We cannot assure you that public or private financing or grants will be available on acceptable terms, if at all. Several factors will affect our ability to raise additional funding, including, but not limited to, the volatility of our common stock and the broader public equity market. If we are unable to raise additional funds, we will be forced to either scale back our business efforts or curtail our business activities entirely. As of December 31, 2014, the Company has an accumulated deficit of $349.1 million, recurring losses from operations, and negative working capital which raise substantial doubt about the ability of the Company to continue as a going concern. Furthermore, an emphasis of matter paragraph related to an uncertainty as to the Company’s ability to continue as a going concern has been included in the auditor’s opinion."

This little news "blip" today- what's it really change in the big picture at this point? They are YEARS away from commercialization in their own words. YEARS. And they need mountains of cash still to even attempt to get there- cash they presently do not have. The big "article" didn't move the needle, the "uplist" didn't move the needle (it's trading below where it did over 3 YEARS ago and is flat at best to its recent OTC levels), all the PR in the world so far has budge it in any meaningful way. I don't see this latest blurb making any big change here- just not seeing it. It sold off already into strength- not a good sign IMO.

Is this a 1/2 CENT stock now?

Seems like the new basing area is around .005 now IMO.

There's about $248 bucks worth left on the Bid at .0062 presently, and it's all .005's below that again, very similar to yesterday.

http://www.otcmarkets.com/stock/BHRT/quote

0.0062 / 0.0069 (40000 x 136000)

Look at today and yesterday- if one wants to sell so much as a few $hundred bucks worth- then the MM's take the Bid down to the .005 area, or as in this AM, even sub .005 to fill a sell order of a lousy few $100 bucks.

If one bought in the AM, say $500 worth, then changed their mind and wanted out, they'd have to take a 12% or 15% loss on the spread it looks like to get their sell order to fill- that's what today and yesterday's chart is showing.

It's building a base now in the .005 area, to .007 range tops now. Like this is not a one day down fluke- this looks like the new normal for the stock price now perhaps.

That blog thingy, maybe it will need to be re-written to the "VALUE OF 1/2 CENT" perhaps, no? If one can't get a $1000 sell order filled for more than about .005 or at most .006, then that appears to be the new base pricing IMO.

The stock has only traded a grand total of about $1,500 bucks so far today almost 3 hours into the trading day- and the MM's took it down twice hard- once to .0049 and then again to about .0051 on a single $600 or so sell order.

Where's all the volume and buyers rushing in here to get shares at sub ONE CENT, almost 1/2 a CENT? They're just not showing up that I can see? And that's after the big "conference call" and a lot of PR and what not? What gives I wonder?

"BID @ .0051??" Not only that - it posted a trade at .0049 ???

The day's trading range already on the I-HUB chart display and the OTC site itself has the range as .0049 to .0069 ?

0.0052 / 0.0066 (132000 x 172000)

http://www.otcmarkets.com/stock/BHRT/quote

Current Bid is only .0052 so the spread is cranked wide open again with these MM's. The only one showing Bid at .0049 is good ole BMAK. Like they took a spike down this AM all the way to .0049 ? Remember yesterday, the MM's took out all the .006's for a while and had it bidding in the .005s for quite a long period during the trading day- they only "painted the tape" on a very small trade or two right at the close to bring it back up end of day to .007, otherwise it spent most of the day down in the low .006s

These MM's are stepping all over this thing this week- and now the ultra wide spread mode too? The volumes have been below the daily avg- which from watching this for months is usually when the MM's "game it" and crank in the ultra wide spreads (it can swing +/- 15% or more in a blink, like one small trade of $100 or whatever) and then it flat-lines too. Yesterday is went several hours in the afternoon w/o really a single trade or at best, a few very tiny trades- it just sat, not moving almost all the last 2 hours of the day until moments before the close.

Where's the bottom? When an MM can just take it down to .0049 this AM, and the .005's on the Bid yesterday, I don't think I'm seeing any bottom yet, not by a long shot. Who knows if someone steps in and wants to sell a decent size chunk here- what would these MM's do with the price then? They might run this through a down-spike crusher like they did recently on the 20 million volume day that made the now all, all, all time low of .0045

What would the next all, all time low be? The .003's are next perhaps? Who knows IMO the way this is trading right now?

LOL quote, " I thought investors purchasing and selling quantities of "666" was normal. Lol. Ridiculous. I hope Mike is looking at tios forensically with help from counsel."

And what EXACT law is there against an order for 666 shares being bought or sold? Is this an imaginary FINRA or SEC law or what? What exactly is "mike" supposedly going to look at or whatever?

I don't think there's a single law (I Googled it) that says that buying a specific number of shares of a stock (666, or 999, or 1 share or 1001 shares or whatever) is imaginary "illegal" in any way, shape or form?

What EXACT supposed laws are being broken supposedly when a trade posted for 666 shares? So no other company in the entire history of the market (Apple, Google, GE, whatever) has ever had 666 shares traded and "printed" on the tape before? Really?

Funny IMO how everything related to this stock is supposedly "manipulation" or some vast criminal conspiracy or whatever? NEVER the fact that the company dilutes common share for all intents and purposes un-ending to the tune of 10's and 10's of MILLIONS of shares like it's nothing. Over 300 MILLION shares in a period of about 1 yr and 65 MILLION shares in less than the first 3 months of just 2015 according to PAGE F-34 of the most recent filed 10-K. (2 BILLION shares now authorized by the BHRT BOD)

NEVER anything to do with the company or how it's managed or its continual use of toxic, convertible debt financing and other dilutive financing constantly, or never its dire financial condition (see NUMEROUS GOING CONCERN WARNING in the most recent filed 10-K and their end of 2014 cash balance of a whopping $36K cash against about $11 MILLION in current debts)- never any of that reality? Always some supposed mystery "manipulation" scheme or whatever.

Fascinating IMO.

Maybe it's just more sellers than buyers and a lack of buyers? Maybe? Just maybe perhaps? Never the company's fault and the reality of their business and very poor financial condition (again, see their latest 10-K and their own auditor's opinion and WARNINGS as to their financial condition)- always some nefarious, conspiratorial outside "force".

Enterprise value is a pretty useless metric when attempting to "value" a company for the most part. And it certainly bears no relationship as to what the free market is valuing a company's shares at- not that I've ever seen or read or known about?

All one is really doing it taking market cap and in BHRT'S situation adding their current debts (I can find the 10-K page where that Fidelity computer "bot" scraped the $5.x million current debts from. While BHRT's total debts actually exceed $11 million presently) but it's just debt added to the present market cap as set by the current share price X the O/S share count- as anyone buying the company would have to acquire/pay off the debt also.

No one who does buy-outs that I've ever read about really looks at enterprise value in valuing a company. They'd IMO be much more interested in key things like CASH on-hand (which BHRT has essentially little to none at any given time, see latest 10-K, they finished yr 2014 with $36K total cash on-hand), things like positive cash flow(s)- which is cash thrown off from operations to fund and run and grow the business of which BHRT has none, things like debt of which BHRT has a lot when compared to their extremely poor cash position and poor liquidity situation- see their GOING CONCERN warnings in any recent 10-K or 10-Q filing, things like debt ratios, current ratios, etc.

Enterprise value - not of much value really. That Fidelity page or whatever it is- it's just a computer generated "bot" page using info scraped from the 10-K/10-Q filings and is just market cap plus debt typically or some variation similar to that.

No one looking to buy this company would give a rat's behind about the "enterprise value" IMO. The company has way to many other much more serious financial problems revealed by looking at their entire set of financials- not revealed via a simple glance at enterprise value.

Look at most stock market buy-outs or mergers, etc They're almost always done as multiple of cash flows, earnings, free cash, cash-on-hand taken into consideration, etc. A multiple of revenues, etc Not "enterprise value", let alone again- that "enterprise value" in any way, shape or form somehow indicates or dictates what the common shares should or would trade for.

My .0066 CENTS worth (or whatever it is today at this moment)

Bid just dropped to .0053 ??? HOLY COW.

http://www.otcmarkets.com/stock/BHRT/quote

0.0053 / 0.0065 (38000 x 107000)

The bottom is dropping out again it looks like and that's with volume picking up. Wow? No support or buying pressure at all it seems? The Bid is in free fall again- and it's only Wednesday. Friday's have been brutal lately- but this is getting punished again here mid week already it looks like?

A 1/2 CENT stock. It wasn't that long ago that the all, all, all time low was .0063 and that was one down spike day that was made in a late Dec trade (if I remember correctly, would need to check a chart) and it bounced off of that pretty quick if I remember right. But doesn't look to be the case here anymore? There appears to be no real bottom to this anymore at this point IMO? I guess it's just pure dilution driving it now perhaps? Not sure?

Wonder what gives- after the "conference call" and all? Where's the buying pressure even when the price keeps dropping?

10-Q will be out soon, maybe there will be more info in there?

Stacked to the Ask/Sell side again this AM, all in the .006's

0.0062 / 0.0069 (47000 x 177000)

http://www.otcmarkets.com/stock/BHRT/quote

Only about $1,500 bucks worth left presently showing on the Bid in the .006's and nothing really below that except ole BMAK showing a block of 10K at .0049

The way this is trading so far this week- this might be a 1/2 CENT stock again pretty soon IMO. Just no real buying pressure or large demand present at all here it seems- no matter how low the price is going.

Guess the next "big event" after the ole "conference call" will be the 10-Q coming out (about 1 week away I'd guess). Will tell how much cash is left on-hand, how much more common share dilution has occurred since the 10-K release in March, if they've tapped Magna again and for how much or if they've done any additional toxic, floorless, convertible debt financing deals since the "subsequent events, PAGE F-34 of the 10-K), how much is the total O/S share count now, etc

Should be an interesting read to see what the up to date financial picture looks like now. The lower this share price has been going- the use of convertible debt financing and Magna just gets that much more dilutive- so the 10-Q should be interesting IMO, given these recent, sustained low share prices and the very recent all, all, all time low of .0045 being made.

WOW, just hitting post and the Bid really dropped out? Only 300K left showing at .006 and then it's .005 below that, holy cow?

0.006 / 0.0065 (300000 x 107000)

http://www.otcmarkets.com/stock/BHRT/quote

May hit that 1/2 CENT level sooner than thought? That's only about $1,800 bucks left on the Bid showing now and then it's .005 below that, nothing in between and the Ask is dropping hard now too. Looking pretty weak here and it's only Wed.

LOL quote, "Within_a_few_days_they_could...see and count fingers

This is a SLAM-DUNK. "

SLAM-DUNK??? Uh, NO. The_number of people_in a tiny phase I (one totally controlled by the company itself and not blinded and w no placebo arm) is not even large enough to be statistically_significant yet.

MOST clinical_trials fail in the much larger, much more stringent_in terms of design requirements, much more difficult phase II.

The phase II that HAS_NOT EVEN STARTED YET_and for which OCAT presently DOES NOT HAVE ANYWHERE NEAR THE FUNDING YET to take to completion. The one that was supposed to start end_of_2014, and now it's almost mid 2015 and NO TRIAL has even begun.

Lanza being quoted from yesterdays big "talk" thing:

"We're hoping in the coming months to certainly initiate our Phase II clinical trial"

What? "Hoping"??? But this is a supposed_imaginary SLAM DUNK? "hoping"? Why wait if it's all_a_done deal supposedly?

Lanza again being quoted (local MA newspaper)

http://www.telegram.com/article/20141014/NEWS/310149525&Template=printart

"We treated the last UK patients last month, and they also have not seen any safety issues related to the transplanted tissues themselves, either," Dr. Lanza said.

Advanced Cell now hopes to launch a 100-patient, phase 2 study in Stargardt's patients by the end of the year, according to Dr. Lanza.

A second, smaller phase 2 study in patients with age-related macular degeneration would follow, he said. Any treatment might not be ready for FDA approval until 2020, Dr. Lanza said. "

From the latest filed (very recent) 10-K filing, PAGE 16:

"Other than our arrangement with Lincoln Park, we have no sources of debt or equity capital committed for funding. Recent attempts to raise capital in the public equity markets have proven unsuccessful, and we can provide no assurance that we will be successful in any future funding effort. "

That doesn't sound_like any so called_SLAM-Dunk to me by_any stretch of the_imagination??? Sounds like 5 YEARS minimum_and a whole bunch_of uncertainty at best. Peppered with "we_hopes" and "maybes" at every_step of the uncertain_way. Slam-dunk, NO IMO??

666 shares first trade, LOL?? Really? Now THAT is weird isn't it?

Are these OTC MM's dudes messing with people or what?

Someone would really post a trade for 666 shares at like .00665 and down, RED exactly 5% - which is an of amount like $4.42 bucks worth?

Gets more bizzaro by the day and moment?

LOL quote, "The Share Price Will Explode Rendering Lincoln Irrelevant "

What? Lincoln is ALL THEY GOT RIGHT NOW? How can Lincoln be rendered "irrelevant"?? ONE MONTH or two w/o being able to draw on Lincoln- and this little operation is for all intents and purposes BK, insolvent and LIGHTS OUT, close the door last one out and lock it.

From the latest filed (very recent) 10-K filing, PAGE 16:

"Other than our arrangement with Lincoln Park, we have no sources of debt or equity capital committed for funding. Recent attempts to raise capital in the public equity markets have proven unsuccessful, and we can provide no assurance that we will be successful in any future funding effort. "

Lincoln is literally their life line and only means of survival right now. HOW is Lincoln supposedly going to become "irrelevant", LOL? How? How would that work exactly?

Ask dropped to .0068 and BMAK is sitting hard on the Ask w/ a 10K share block at .007

Looks to me like it won't be going above that then today, IMO. Whenever BMAK parks that 10K share block, it's like a solid rock sitting on that Ask, and has been that way for months (pretty much all of 2015 so far that I've seen and observed)

The MM's look to be driving both the Bid and Ask lower again today- the usual dilution MM suspects (CDEL and BMAK both present)

http://www.otcmarkets.com/stock/BHRT/quote

0.0065 / 0.0068 (23700 x 50500)

Bid down now at .0065

Looks like these MM's want it in the .006's or below for now IMO. Dilution in play still here looks like to me. Volume is pretty low this AM, but BMAK parking hard on that Ask still makes it tough for any move out of this range from observing anytime in the recent past 4 plus months when BMAK shows up on that Ask w/ their 10K share block.

LOL quote, "OCAT Shorts leaning the wrong way? "

Open short interest on this stock- as a percentage of float or any other standard metric is still pretty much noise level at barely 1%. It's pretty much non existent. A micro change in the open short interest is supposed to mean what exactly?

When the open short interest gets to 5% or 10% or more of float- it's being heavily shorted. Right now, nothing much at all is happening- it's a non event IMO.

The main driver at this point- is Lincoln has probably taken a break selling dilution shares for a bit to let the price take a "breather" and recover a bit- that's been their pattern on this for a long, long, long time. When they get back on the sell-side with their flow of dilution shares it will put down pressure back on the Ask IMO, it's the typical OCAT pattern.

OCAT lives off of Lincoln dilution at this point and will for a long time to come- per their own wording in their own SEC filings. They got no other source of survival cash at this point. Simple as that.

BHRT market cap PER GOOGLE FINANCE is $4.34 MILLION. BARELY holding $4 million.

http://www.google.com/finance?q=bhrt&ei=6zU-VbmNLeeKjAKjoYCAAw

If the common share trading price dips "slightly" from where it closed Friday at .0067 then the market cap will go BELOW $4 million. Pretty clear IMO. (as in the very recent all, all, all time low price of .0046 made by the common stock shares of BHRT as traded on the OTC, the market cap would have been WELL BELOW $4 million. It actually would have gone slightly below $3 million at that point in time, a few weeks ago)

Some seem to think Google Finance publishes a "false" number for a stock/company's market cap, LOL?????

Barely a $4 million market cap against over $11 MILLION in current debt/obligations and ended 2014 with just $36K total cash on-hand (That's in the 10-K filed with the SEC. I suppose that is "false" too, LOL ???)

Market cap barely at $4 million now. WOW !

That's against debts of over $11 MILLION and from the last 10-K filing, immediate accounts payable of over $2 MILLION and only $36K cash left on hand.

The lower the price goes- the harder it's going to get to raise even pittances of cash using the toxic, convertible debt financing deals and/or Magna's dilutive credit line (the Magna line is based on a discount to market price, so it gets more and more dilutive the lower the share price goes- see the SEC filed registration statement about it)

From the most recent 10-K, PAGE 35:

"The extent to which we rely on Magna Equities II, LLC as a source of funding will depend on a number of factors, including the amount of working capital needed, the prevailing market price of our common stock and the extent to which we are able to secure working capital from other sources. If obtaining sufficient funding from Magna Equities II, LLC were to prove unavailable or prohibitively dilutive, we would need to secure another source of funding. Even if we sell all $3,000,000 of common stock under the Purchase Agreement with Magna Equities II,

LLC, we will still need additional capital to fully implement our current business, operating plans and development plans."

PAGE 36:

"The sale or issuance of our common stock to Magna Equities II, LLC at a discount may cause substantial dilution and the resale of the shares of common stock by Magna Equities II, LLC into the public market, or the perception that such sales may occur, could cause the price of our common stock to fall."

Even if they tap ALL of the Magna line (not likely IMO that they will be able to access all $3 million with these dropping share prices, could be wrong, who knows?)- they still state they'd NEED MORE MONEY via financing to implement their "plans" and "current business". That would mean to me- more deals with the convertible, toxic debt hedge type house like they already used in Jan and Feb of 2015 (names they've used already like Asher, KBM Worldwide, Daniel James, Fourth Man, the new one Vis Vires group, etc)

Pretty amazing IMO.

See what next week holds- that was a pretty brutal Friday given the "big conference call" and all that. The .006's again already, holy cow.

10-Q is the next big deal I guess. See how much new dilution, how low their cash is, what their debt is and immediate debts they owe like accounts payable and stuff, etc Should be interesting IMO.

LOL quote , "If anyone takes the 98% scenerio serious, you have to ask why?"

The common shares have not lost 98% of their value? MATH LIES? Really?

ACTC/Ocata went public in 2005 (TEN years ago) via the poor man's way- using a revese merger w/ the TWO MOONS KACHINA DOLL COMPANY OF UTAH and straight to the OTC.

From there- it's lost, more than 98% of the common share value. REALITY and a FACT.

When they merged on to the OTC as a public company- the shares traded for $5 a share in 2005.

$5 a share = 500 cents. Today's price is about 7.48 cents (adjusted for the R/S done recently; one must ALWAYS adjust for forward or reverse splits when looking at any stock's long term share price rise or decline)

Thus 500 cents - today's 7.48 CENTS = 492.52 / 500 = 0.985 X 100 = 98.5% loss to common.

Yep, the common shares since going public have LOST 98.5 percent of their value as of TODAY (Friday's closing price). Simple as that. The share pre R/S had diluted out to well over 3 BILLION shares and hit an actual 5 CENTS a share, again when the R/S is removed- which one must always do when looking at ANY company's historical stock performance.

The company has $350 MILLION in sunk capital and never so much as ONE CENT of ROI (return on investment). It's been a solid loser since day one- never once producing a return or positive cash flow and never a profit LOL, not even remotely close to that.

They've been financially distressed since going public 10 yrs ago and are financially distressed to this day- per their own Sr. Mgt and own auditor's "GOING CONCERN WARNINGS" plastered numerous, numerous places throughout their most recent filed 10-K.

Here's an article in the highly respected journal, "NATURE" that describes how they've been in financial distress and problems since essentially DAY ONE.

http://www.nature.com/news/stem-cell-research-never-say-die-1.9759

Some tid-bits from their most recent filed 10-K, aka RECENT evaluation of the current condition of the company:

http://www.sec.gov/Archives/edgar/data/1140098/000101968715000981/ocata_10k-123114.htm

PAGE 16:

"We will require substantial additional resources to fund our operations and to develop our product candidates. If we cannot find additional capital resources, we will have difficulty in operating as a going concern and growing our business."

"Other than our arrangement with Lincoln Park, we have no sources of debt or equity capital committed for funding. Recent attempts to raise capital in the public equity markets have proven unsuccessful, and we can provide no assurance that we will be successful in any future funding effort. "

PAGE 43:

"As of December 31, 2014, the Company has an accumulated deficit of $349.1 million, recurring losses from operations, and negative working capital which raise substantial doubt about the ability of the Company to continue as a going concern."

PAGE 46:

"We have also audited, in accordance with the standards of the Public Company Accounting Oversight Board (United States), the consolidated balance sheet of Ocata Therapeutics, Inc. and Subsidiary as of December 31, 2014, and the related consolidated statements of operations, stockholders' deficit, and cash flows for the year then ended and our report dated March 16, 2015 expressed an unqualified opinion thereon and included an emphasis of a matter paragraph relating to an uncertainty as to the Company’s ability to continue as a going concern.

/s/ BDO USA, LLP

Boston, Massachusetts

March 16, 2015"

PAGE 13:

"Our ability to become profitable depends upon our ability to generate revenue. We do not anticipate generating revenues from product sales for the foreseeable future, if ever. "

Another article about the history and historical performance of ACTC/OCAT (nothing like a name change to try and run from the tainted past, eh?)

http://www.nanalyze.com/2014/04/some-problems-with-advanced-cell-technology/

QUOTE from article:

" Investors who would have purchased this stock when it began trading in 2005 would have already lost -98% of their investment."

Of course- all along as the common shares have creamed their average retail investor- the insiders have profited handsomely for years, literally becoming very wealthy in most cases. Very impressive IMO. Several have an amazing, seemingly uncanny "knack" for being able to sell/dump the free shares they receive into nearly every short term "pop" and spike in the price of the stock. Amazing sage like abilities to time the near perfect top of spike with sage like accuracy- all while the common holders languish with large losses and dead money as a raging bull market passed their dollars by.

Yes, that 98% loss to the common shares is all just a tall tale of fiction I suppose- all except for the factual MATH and reality part of it.

LOL quote, "a company who's common shares have LOST a literal 98% PLUS of their value, is old old old news...... nobody cares....look at the charts"

Pull up a FIVE YEAR CHART, not "old new"?? The stock was $20 plus in 2011, NOT "old news". It's a 66% plus LOSER since 2011. It's been FLAT at best for over 3 yrs and lost 66% of its value since 2011 as the rest of the market passed through probably the greatest bull market run in WORLD HISTORY- with Biotechs being one of the top performing sectors of all, all except this little penny stinker. One would need a 200% plus gain just to break even to even 2011 level.

It's traded FLAT and down for 3 plus yrs now- going nowhere as the market has ripped to all, all, all time highs. Yeah, LOOK AT THE CHARTS.

Further, the 98% TOTAL LOSS to their common shares and the $350 MILLION in sunk capital is 100% relevant to today - as it's the legacy baggage hanging around their necks as a penny, OTC transfer stock. Wonder why they couldn't sell a lousy $62 million secondary VERY RECENTLY? Cause no "sophisticated" investors wanted to pony up for their shares- in the middle of a raging bull market, that's why. Now why would that be?

Um, just "maybe" perhaps, "possibly", "kinda" maybe because they have a highly tainted history of large losses, failure to produce and deliver on promises, of enormous sunk capital losses, of never returning so much as ONE CENT to their shareholders, of endless "GOING CONCERN" warnings (aka liquidity warnings, aka BK warnings), recent (not old news) SEC violations, accounting problems- and too much to list. Just "maybe" IMO?

NOT "old news" but 100% relevant to today- it likely sacked their attempt to float a secondary despite spending a bundle on qty-3 underwriters. Not "old news". They live off of, and survive off of, low grade Lincoln dilution, credit card style, "financing". Limping along, paying the insiders, NOT starting their major phase II trial(s) as promised (another miss again), etc

There's no "old news" here. The stock is not even at break even levels with where it traded many, many, many times on the OTC in the past THREE YEARS, as the bull market party raged on and left it sitting in the parking spot. Dead money.

LOL, "old news" and "look at a chart"?? Yeah, the picture ain't pretty on a chart- a 3 yr or 5 yr chart with the DOW, NASDAQ and RUSSELL 2000 or any other major metric plotted on the same chart- the dead money versus the raging bull ride.

From their most recent filed 10-K, not "old news" :

PAGE 16:

"

We will require substantial additional resources to fund our operations and to develop our product candidates. If we cannot find additional capital resources, we will have difficulty in operating as a going concern and growing our business."

"Other than our arrangement with Lincoln Park, we have no sources of debt or equity capital committed for funding. Recent attempts to raise capital in the public equity markets have proven unsuccessful, and we can provide no assurance that we will be successful in any future funding effort. "

PAGE 37:

"We have no therapeutic products currently available for sale and do not expect to have any therapeutic products commercially available for sale for a period of years, if at all. These factors indicate that our ability to continue research and development activities is dependent upon the ability of management to obtain additional financing as required."

PAGE 43:

" As of December 31, 2014, the Company has an accumulated deficit of $349.1 million, recurring losses from operations, and negative working capital which raise substantial doubt about the ability of the Company to continue as a going concern. Furthermore, an emphasis of matter paragraph related to an uncertainty as to the Company’s ability to continue as a going concern has been included in the auditor’s opinion."

And on, and on and on- pages and pages of it. NOT "old news". The BULL MARKET rages on and little ole OCAT can't even attract or raise any high quality large financing? Why? Why would that be? The markets are awash in CASH and companies are raising capital by the super tankers full for the past several years- but not this one? Why? Why would that be?

Quote total BS LOL, " Dr. Lanza is well known in CT and will be well received. Strong Pfizer connection with key offices in CT and Mass."

What? One can know ahead of time how someone will "be received" somewhere and also that a single individual is "well known" in an entire STATE like CT? What percent of people in CT have ever even heard of Lanza? How's that "work" exactly or is possible to know?

Also, WHAT does "Dr. Lanza" have to do with Pfizer and supposed "strong connections" in CT and Mass.???

Pfizer is a GLOBAL COMPANY with over 78 THOUSAND employees and is headquartered in New York, NY. What proof of is there of some supposed Lanza strong Pfizer "connection" at all, let alone in CT or Mass?

Since when does OCAT have some imaginary Pfizer "connection" or whatever? (is this like the non existent GE "connection" ??)

LOL quote, "And this is where we find ourself now.

EVERYTHING before the February Up List is

irrelevant. "

What?? Not according to ALL of stock market history and ALL easily available stock market research, especially regarding literal PENNY STOCKS.

By ALL historic norms- a company who's common shares have LOST a literal 98% PLUS of their value, while literally being diluted out to 3 BILLION plus shares and down to a literal 5 CENTS a share- by all commonly available stock market research, that company has LITTLE chance to survive or ever recover as a common stock, almost none. The odds are stacked highly against it (See the SEC site or any numerous stock market research sites that track the history and performance of company's who's shares become literal "penny", as in 5 CENTS a share, stock).

And NO, a R/S (reverse split) smoke n mirrors trick does not erase that PAST and highly relevant historic, failed performance of the stock and company IMO. Not even close. (nor does a name change and "new" website and a logo change).

Everything from the instant they went public via the poor man's reverse merger- STRAIGHT to the OTC markets using the TWO MOON'S KACHINA DOLL COMPANY to get there- all of it, is highly relevant to who this company still is today.

Just read any of their SEC filings like the recent 10-K. Their legacy issues are all there, including the enormous money pit of over $350 MILLION in sunk, lost capital. Never once returning so much as ONE CENT of ROI to investors. Highly relevant.

How relevant- well here's a few "statements" about it from their most recent SEC filed 10-K:

http://www.sec.gov/Archives/edgar/data/1140098/000101968715000981/ocata_10k-123114.htm

PAGE 46 (there own CPA firm, licensed and fiduciary bound auditors speaking)

"We have also audited, in accordance with the standards of the Public Company Accounting Oversight Board (United States), the consolidated balance sheet of Ocata Therapeutics, Inc. and Subsidiary as of December 31, 2014, and the related consolidated statements of operations, stockholders' deficit, and cash flows for the year then ended and our report dated March 16, 2015 expressed an unqualified opinion thereon and included an emphasis of a matter paragraph relating to an uncertainty as to the Company’s ability to continue as a going concern.

/s/ BDO USA, LLP

Boston, Massachusetts

March 16, 2015

"

And PAGE 43:

"We cannot assure you that public or private financing or grants will be available on acceptable terms, if at all. Several factors will affect our ability to raise additional funding, including, but not limited to, the volatility of our common stock and the broader public equity market. If we are unable to raise additional funds, we will be forced to either scale back our business efforts or curtail our business activities entirely. As of December 31, 2014, the Company has an accumulated deficit of $349.1 million, recurring losses from operations, and negative working capital which raise substantial doubt about the ability of the Company to continue as a going concern. Furthermore, an emphasis of matter paragraph related to an uncertainty as to the Company’s ability to continue as a going concern has been included in the auditor’s opinion."

It's all relevant IMO. Else, they wouldn't go out of their way to publish it in their own, Sr mgt duly signed, SEC filed 10-K statement.

Lanza quoted in a local MA newspaper:

http://www.telegram.com/article/20141014/NEWS/310149525&Template=printart

""We treated the last UK patients last month, and they also have not seen any safety issues related to the transplanted tissues themselves, either," Dr. Lanza said.

Advanced Cell now hopes to launch a 100-patient, phase 2 study in Stargardt's patients by the end of the year, according to Dr. Lanza.

A second, smaller phase 2 study in patients with age-related macular degeneration would follow, he said. Any treatment might not be ready for FDA approval until 2020, Dr. Lanza said. "

Well, the END OF THE YEAR has come and gone and that trial has NOT started. It's almost mid 2015 now.

Bid just dropped back into the .006's, holy cow !!

It's getting stepped on hard today. "STEM" another "stem cell" play is getting plastered today apparently because of a highly dilutive financing deal of some sort (I haven't read the details yet, but they're cash poor too and the glance at the financing terms look horrible). So don't know if there's any ripple effect spilling over to BHRT from that maybe today too? Who knows? "STEM" sell off is getting quite a bit of chatter on other "stem cell" related stock boards for sure today.

0.0067 / 0.007 (44700 x 229900)

http://www.otcmarkets.com/stock/BHRT/quote

Stacked HEAVY at about 5 to 1 to the Ask/sell-side still. No let up in sight here that I can see so far.

Looking like a tough Friday so far, probably all day more than likely IMO.

Quote what? "Relatively there hasn't been that much dilution recently."???

They diluted out 65 MILLION plus shares in just Jan, Feb and early March of 2015? (see most recent 10-K, March 2015, PAGE F-34) That's "relatively little"??? 65 MILLION shares more dilution on top of a prior year's approx 300 MILLION shares of dilution- essentially a more than doubling of their O/S shares and an increase to 2 BILLION in authorized shares? That's like 10% of total O/S shares being doled out in not even the first 3 months of 2015? It's massive dilution- and it's on-going, non stop for all intents and purposes.

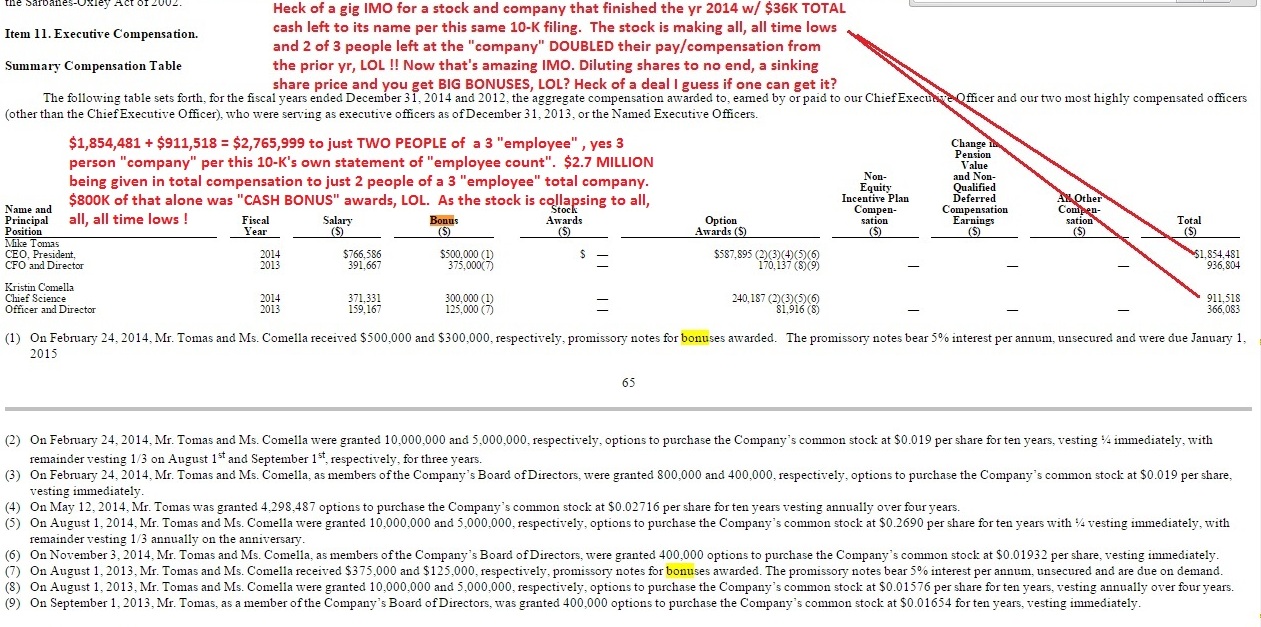

Also quote, " Mike Tomás warned against those that are tying to and I quote "derail Bioheart's success"."

Warned? What does that even mean? Who is this "derail Bioheart's success" and blah, blah? The Sr. Mgt and Tomas himself inks and signs every dilutive financing deal this company does. He triples his own salary (to over $1.5 MILLION annually) and that of one other in the company in a 2 yr or so period (2 people of a THREE person total "employee" company per the most recent 10-K), while they finished 2014 with $36K TOTAL CASH to their name as a company? He approved and issues every dilution share that ever gets sent to anyone - including 10's of millions shares for vague line item entries like "services rendered" being paid using common shares, aka dilution shares (see any of the past several yrs of SEC 10-Q or 10-K filings "shares issued" or "subsequent issues" etc).

So who or what is this "warning" thing? What does that even mean? I've never heard a public traded company CEO speak like that before? "Warning" to who or what? Again, what does that even mean??

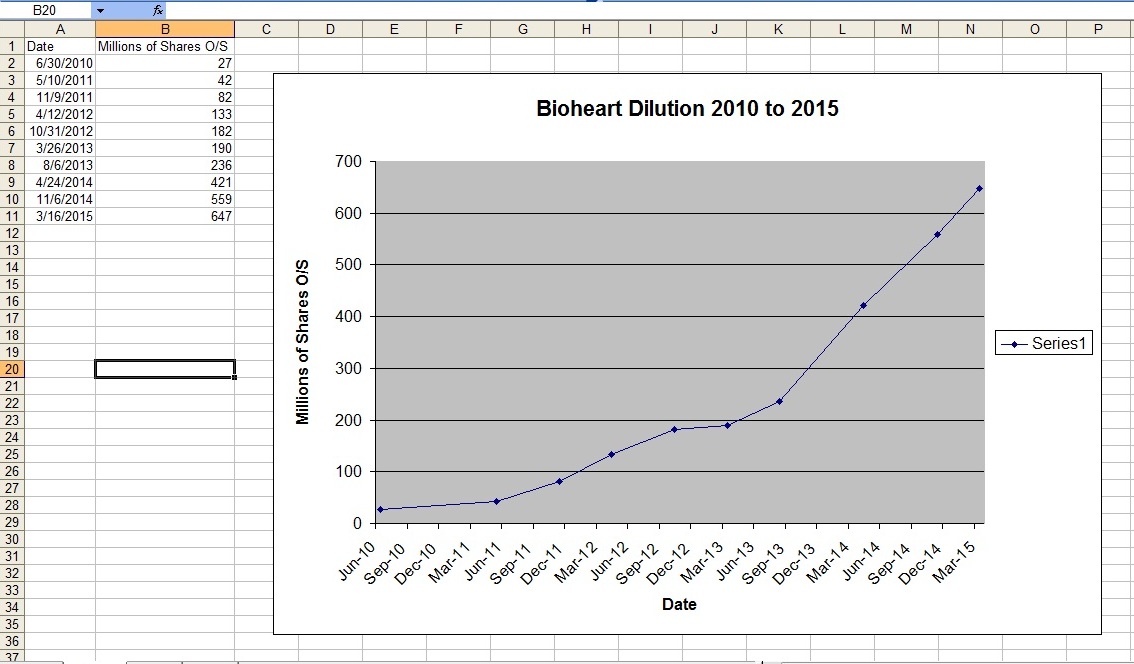

HE runs the company and is 100% in charge of it. ON HIS WATCH the common shares have lost about 99% of their value (approx. .50 CENTS a share when he took over mid 2010 to .0071 CENTS today and a new recent all, all, all time low of .0045 CENTS), the market cap has collapsed tremendously and dilution has gone from about 30 MILLION shares tops O/S in mid 2010 when he took over (at a price of about .50 CENTS each) to approx. 700 MILLION shares outstanding today.

"Warning" to who? To the Sr mgt of Bioheart? Anything that's happened to this company rests squarely on their shoulders (The CEO and the BOD and their own little creation called Northstar, LLC also made up of insiders). Who they "warning" and for what exactly? What kind of code-speak is that and what does it even mean or what is it even supposed to mean?

Amazing IMO. Again, NEVER heard a public company CEO speak like that. HE runs the ship and is responsible for it. HE and the BOD make every decision and spend every dime and allocate every dollar and ink every "toxic" dilutive financing deal and all the rest.

Makes zero sense to me IMO. None.

What does DILUTION look like "on the watch" of this CEO? Here's a graph of dilution taken from BHRT's own SEC filing share counts (usually PAGE 1 of any 10-Q or 10-K filing) and it's from mid 2010 to today which is when Tomas took over as CEO to today- says a lot IMO. LOOK at how the graph is going near vertical now- dilution is accelerating, massively IMO and the graph (aka MATH) proves it.

LOL, it's not even a 52 week or 2 YEAR high right now???

What's the big "excitement" that this is some "unprecedented" supposed "big buying" never seen before, blah blah? Look at the 2 YEAR chart- it traded higher than this MANY times as an OTC penny stinker. This isn't even a 52 week high, let alone even a sustained near-term high yet. It's gone to these levels many, many, many times in more than the past 2 years only to give it all back and then some.

They haven't even diluted yet- they have nowhere near the cash yet IMO to fund a major phase II, large, FDA quality trial and they have not even started the trial(s) yet- the one's that were stated to "hopefully" be well underway by END OF 2014. It's about to hit MID 2015 in a month or two here- and they got a goose egg sitting in the "new trials" box. The $62 million secondary failed and was pulled. They filed for $100 MILLION dollars and stated they had plans to use it all- meaning IMO that's the kind of coin they figured they'd need for running serious phase II trial(s).

That's a TWO YEAR chart- the old OTC days most of it- and it traded at these levels numerous times, what's the biggy here so far??

Here's another one with THREE YEARS of trading history:

It hasn't even reached sustained levels where it traded on the OTC, YEARS ago. Not sure what all the "excitement" is here yet? Lincoln has likely taken a breather from selling dilution shares- look at the historical charts, a normal pattern to let it come up for a "breather" between selling into strength as OCAT makes continual "draw-downs" on the dilutive credit line facility.

Nothing new here yet IMO. Same old.

$1,100 bucks worth left at .007 on the Bid as of right now. .006's might be a possibility again today the way this thing is trading early on?

0.007 / 0.0079 (165000 x 315000)

http://www.otcmarkets.com/stock/BHRT/quote

Ask/sell-side is stacked 2 to 1 to the Bid and both CDEL and BMAK are all over it today. The Bid is now thin at only .007 showing and nothing much left after that to be back in the .006's

Looking pretty darn weak here IMO. Friday's have been notoriously rough to the down-side on this one lately it seems.

Oh, little block at .0071 just popped in there - about another $400 bucks worth on the Bid. But still real thin IMO. If the MM's step on this hard (the volume is pretty high already) they may be looking to drive it to the .006's the way they're stacking up the Level II so far.

Not sure the "conference call" made much of a dent so far? PR doesn't seem to really move the needle much anymore either? Dilution maybe? Possibly? Convertible debt having an effect maybe? Possibly?

Just thinking out loud.

LOL quote, "The Value of One Cent! "?? Uh, LESS THAN ONE CENT, no?

Maybe it's time to revise that a "tad" maybe? .0045 cents (recent price in April of 2015) is the new all, all, all time low and the common shares are now at about .008 or less as of today and have been on a sustained basis for several months.

I'd say that qualifies as the "value" of HALF A CENT in the case of .0045 and LESS THAN ONE CENT for most of 2015, IMO. No?

Not so sure about that "story" of the "value" of ONE CENT? The whole thing, the way it was written, never made any sense to me personally when I first read it and it makes even less sense to me today.

My .0074 cents worth

LOL quote, "What is the expected revenues for 2015?"

Question to me is, What are the expected LOSSES and DILUTION for 2015??

What difference does "revenue" make when there is no positive cash flow, let alone even a remote shot at actual profitability IMO?

Just the salaries and bonuses of TWO people of a 3 person company (most recent filed 10-K, March 2015, PAGE F-11, "The Company has three full-time employees and no part-time employees. ")- the salaries and "cash" bonuses awarded for just TWO people of a 3 person company, those 2 alone now are a combined $766,586 base + $500K (bonus) + $371,331 base + $300K = $1,937,917. $1.9 MILLION in just base salary + "cash" bonus awards to TWO people of a 3 person company. Let alone overhead and what's left of the pittance of an R&D budget they have left after hacking out most of it in 2014, etc The "revenues" are gross. Once the cost of sales is subtracted out, it's not even enough to pay the salaries and bonuses for just those two- let alone fund and run a company, fund R&D, fund any "big phase 3" trials, fund day to day overhead, fund their debt, fund accounts payable which per the same 10-K exceeded $2 MILLION end of 2014 against just $36K cash left on-hand for the end of yr, etc

"revenues"?? It's not "revenues" that matter is it?? It's CASH FLOW and PROFIT and ability to throw off cash to fund their own operations IMO that matter most- and I don't see a single indicator showing them to be remotely close to that happening? WHERE in the 10-K does it show that? They ended 2014 with $36K TOTAL cash on-hand and a big ole "GOING CONCERN WARNING" from their own auditors. The "revenues" didn't change anything that I could see??

Latest filed 10-K, PAGE 55:

"Research and Development

Research and development expenses were $66,420 in 2014, a decrease of $560,563 from research and development expenses of $626,983 in 2013. The decrease was primarily attributable to a decrease in the amount of available funds.

The timing and amount of our planned research and development expenditures is dependent on our ability to obtain additional financing."

Latest filed 10-K, covering to end of 2014 w/ updates to early March 2015, PAGE 56:

"At December 31, 2014, we had cash and cash equivalents totaling $36,674; our working capital deficit as of such date was $10,957,443. Our independent registered public accounting firm has issued its report dated March 16th, 2015 in connection with the audit of our financial statements as of December 31, 2014 that included an explanatory paragraph describing the existence of conditions that raise substantial doubt about our ability to continue as a going concern."

Same recent 10-K, PAGE F-12:

"NOTE 2 — GOING CONCERN MATTERS

The accompanying consolidated financial statements have been prepared on a going concern basis, which contemplates the realization of assets and the satisfaction of liabilities in the normal course of business. As shown in the accompanying consolidated financial statements during year ended December 31, 2014, the Company incurred net losses of $2,253,511 and used $1,108,647 in cash for operating activities. These factors among others may indicate that the Company will be unable to continue as a going concern for a reasonable period of time.

The Company’s existence is dependent upon management’s ability to develop profitable operations and to obtain additional funding sources. There can be no assurance that the Company’s financing efforts will result in profitable operations or the resolution of the Company’s liquidity problems. The accompanying statements do not include any adjustments that might result should the Company be unable to continue as a going concern."

I'm not sure it's really "revenues" that are the biggest deal here right now IMO? Cash flows and "liquidity" would seem more pertinent IMO.

My .0073 CENTS worth

This must be the "big conference call effect, no???? LOL. All less than 10 or so minutes of it, according to statements I read here of those who listened to it (a grand total of about 7 1/2 minutes by one account posted here)

Bid buried at only .0071 on open? Ask is at .008 w/ BMAK sitting hard on it with the usual 10K share block? After the "big call" and all? Wow.

0.0071 / 0.008 (18000 x 54600)

http://www.otcmarkets.com/stock/BHRT/quote

I thought it was predicted to be 100% certain "going big" based on this incredible "conference call" thingy alone this time? Like all the 7 yrs of "going big" predictions since it traded public in 2008 and went straight down from $5.25 a share to now about .008 a share, a loss to the common shares of about 99.99% of their value. An impressive run to say the least IMO.

What happened I wonder? The 10 minutes or 7 1/2 minutes of the "big call" weren't didn't light the fire to launch this baby just yet (AGAIN)?? I guess not sure what I am missing here?

Is it possible the dilution, the 65 MILLION shares just in Jan, Feb and early March of 2015 could be having an effect or something like that, just maybe?

From the latest filed 10-K, PAGE F-34:

Subsequent stock issuances

In January 2015, the Company issued 4,783,568 shares of its common stock in settlement for services, provided 14,299,567 shares of its common stock in settlement of $49,500 of outstanding convertible notes payable, and $2,981 accrued interest and 2,096,450 shares of its common stock for net proceeds of $16,118 from equity drawdown under the Magna Purchase Agreement.