News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Dragon Lady

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

LOL quote, "Big institutional buyers are buying. "

NO, no they're not.

The price is BELOW where it traded on the OTC (split adjusted) - large buying by anyone is a myth.

The share price does not reflect it in any way, shape or form. Misunderstanding a Form 13 is at the root of it all- the "list" does NOT mean those firms are necessarily buying and "holding" - they can be short, as much as "buying".

New all, all TIME LOWS: now back to FLAT LINING, slow trade mode-

This has been the pattern of these dilution MM's (mainly BMAK and CDEL) essentially since the beginning of 2015 from what I've observed.

Spread is now cranked wide open- the Bid is pinned low still, but the Ask is way up there and BMAK and CDEL are backed out a ways on Level II.

0.0048 / 0.0059 (435000 x 500000)

Ask already dropped this AM from .0065, looks like they got no takers "up there", so it's gonna slow drop during the day more than likely. IMO, that $650 "buy" might even be the dilution firm's own trading desk making that buy- to "paint it" to look like it's "up" supposedly. What's a lousy $650 being spent by them, when they're making $millions, these hedge lending firms? Or, they just managed to find some amateur AM buyer and "got um" on the mega AM spread, seconds after open? Who knows- they've been "gaming" the close for the past several days now IMO, the hedge lender dilution MM's (BMAK and CDEL)

The stock posted ONE trade for a whopping $650 bucks, only seconds after open- and now is sitting, parked, literally not posting or printing a single trade for going on 2 hours now.

This has been the pattern. It put in a new all, all, all time low of .004 on 10's and 10's of MILLIONS of shares traded in a 2 day period- and now it goes back to near nothing volume? How exactly does that "work" except in OTC-ville?

Each down "tranche" makes a new lower high and then lower lows "base level" - that's the pattern.

The next down leg "tranche" will thus likely put it into the .003 area IMO, since it now touched .004 twice now, recently, on extremely high volumes.

This is just the typical "breather" or "recovery" days IMO- it seems this is how Magna and Asher and the other dilution MM's "work it" (Asher, Daniel James, Fourth Man, KBM Worldwide a "sister" company to Asher, Vis Vires group etc- all hedge, convertible debt lenders to BHRT, recent convertible, floorless debt lenders to them) when these things are in the "death spiral" (that's what the SEC and other financial reporting sources call it)

http://www.bloomberg.com/news/articles/2015-03-12/josh-sason-made-millions-from-penny-stock-financing

http://www.sec.gov/answers/convertibles.htm

http://en.wikipedia.org/wiki/Death_spiral_financing

Looking pretty RED for a Wed morning?

Must be more of these supposed "big institutions" buying in imaginary droves, no?

HOW is the share price going absolutely nowhere when supposed (as in imaginary) net large buying is supposed to be taking place? How is that even possible?

If there is large "net buying" actuall taking place- the common share price must move up. That's how markets work. This stock is parked, near it's 52 week LOWS and is flat to BELOW where it was on the OTC, having gone nowhere in share price.

They have a failed secondary offering under their belt now, are extremely cash low, have a Phase II trial(s) going nowhere and no large funding anywhere in sight- the kind of money it takes to get a large phase II moving rapidly ahead, let alone even remotely funded to completion.

Why? Why is that? Where is all these "big institutional money" supposed people- when this thing is living off of nothing but Lincoln "credit card" low grade dilution money? And WHY did all these supposed "institutional buyers" say PASS to a $62 million secondary and the discounted shares the underwriters most certainly pitched to them then- in the still raging bull market, the same market that's cooled off considerably now?

OCAT has a $100 MILLION shelf filed and just sitting parked out there. Their shares are trading at or BELOW where they did (split adjusted) when they tried to pitch a $62 million, very expensive to underwrite, secondary offering that bombed out and failed. Why? Why is that the case? Now the myth is that the "institutions" are supposedly "buying big" on the open market though? What sense does that make?

From the OCAT most recent filed 10-K, the REALITY and FACTS according to the company Sr Mgt itself:

Most recent filed 10-K, PAGE 16:

"

Other than our arrangement with Lincoln Park, we have no sources of debt or equity capital committed for funding. Recent attempts to raise capital in the public equity markets have proven unsuccessful, and we can provide no assurance that we will be successful in any future funding effort. The timing and degree of any future capital requirements will depend on many factors, including:

"

Same 10-K, PAGE 16:

"We will require substantial additional resources to fund our operations and to develop our product candidates. If we cannot find additional capital resources, we will have difficulty in operating as a going concern and growing our business."

Same 10-K, PAGE 16:

"Our independent auditor’s report for the fiscal year ended December 31, 2014 includes an explanatory paragraph regarding substantial doubt about our ability to continue as a going concern.

Due to the uncertainty of our ability to meet our current operating and capital expenses, in their report on our audited annual financial statements as of and for the year ended December 31, 2014, our independent auditors included an explanatory paragraph regarding concerns about our ability to continue as a going concern. Recurring losses from operations raise substantial doubt about our ability to continue as a going concern. If we are unable to continue as a going concern, we might have to liquidate our assets and the values we receive for our assets in liquidation or dissolution could be significantly lower than the values reflected in our financial statements. In addition, the inclusion of an explanatory paragraph regarding substantial doubt about our ability to continue as a going concern and our lack of cash resources may materially adversely affect our share price and our ability to raise new capital or to enter into critical contractual relations with third parties."

Same 10-K, PAGE 46:

"We have also audited, in accordance with the standards of the Public Company Accounting Oversight Board (United States), the consolidated balance sheet of Ocata Therapeutics, Inc. and Subsidiary as of December 31, 2014, and the related consolidated statements of operations, stockholders' deficit, and cash flows for the year then ended and our report dated March 16, 2015 expressed an unqualified opinion thereon and included an emphasis of a matter paragraph relating to an uncertainty as to the Company’s ability to continue as a going concern.

/s/ BDO USA, LLP

Boston, Massachusetts

March 16, 2015"

"

LOL quote, "Yes Bartolo Colon got his fast ball back and was clocking 93 to 95 MPH when he joined the Yankees.

He attributes his new success to stem cells injections."

ONE person "claiming" to have been cured or "helped" or whatever is NOT SCIENCE by a million miles. A one time self "report" is known as an ANECDOTE and means nothing.

1) He could have been injected with say "saline" and reported "getting better" and no one would know the difference. Therese a better than 50% chance he could of been injected with water or saline and reported "getting better".

OR, he could have taken a couple of Advil, done some heat/ice and physical therapy and rested for an off-season and have highly likely been doing EVEN BETTER today- no one knows when an ANECDOTE is being "reported". OR, even taken STEROID INJECTIONS or cortisone or similar- all of which may have been done already, at the same time as the "stem cells" and NO ONE WOULD NO THAT EITHER. Further, for all one knows he may be getting paid a fee to "report" this supposed "cure" or whatever- that's highly likely in the shady world of stem cell near "miracle treatments" especially when athletes and similar "go public" about it and tout it (see recent AP, Associated Press article below about this very thing, they investigated it and have proven it as FACT). Highly likely.

2) It can be pure placebo effect- which is highly likely.

It means completely nothing.

Read this high quality AP (Associated Press) and U.S. News And World Report piece of journalism- that reveals how much "science" and "credibility" is involved in these so called "stem cell treatments" and "clinics" and all the rest of it- it's largely snake oil to most highly trained critic and peer review. ANECDOTES abound in this highly un-regulated new cottage cash-for-treatment (which is no "treatment" at all) new "industry"- with a bunch of fly by night operators and sham artists and "doctors" even causing death or permanent damage to patients- well researched and thorough article on the state of stem cell ANECDOTE INCORPORATED:

http://www.usnews.com/news/business/articles/2015/05/18/stem-cell-wild-west-takes-root-amid-lack-of-us-regulation

HIGHLY likely a massive FDA crackdown is coming, soon. VERBATIM from the article:

"Unproven stem cell procedures flourish across the US, outpacing regulation

By MATTHEW PERRONE, AP Health Writer

BEVERLY HILLS, Calif. (AP) — The liquid is dark red, a mixture of fat and blood, and Dr. Mark Berman pumps it out of the patient's backside. He treats it with a chemical, runs it through a processor — and injects it into the woman's aching knees and elbows.

The "soup," he says, is rich in shape-shifting stem cells — magic bullets that, according to some doctors, can be used to treat everything from Parkinson's disease to asthma to this patient's chronic osteoarthritis.

"I don't even know what's in the soup," says Berman. "Most of the time, if stem cells are in the soup, then the patient's got a good chance of getting better."

It's quackery, critics say. But it's also a mushrooming business — and almost wholly unregulated.

The number of stem-cell clinics across the United States has surged from a handful in 2010 to more than 170 today, according to figures compiled by The Associated Press. Many of the clinics are linked in large, for-profit chains. New businesses continue to open; doctors looking to get into the field need only take a weekend seminar offered by a training company.

Berman, a Beverly Hills plastic surgeon, is co-founder of the largest chain, the Cell Surgical Network. Like most doctors in the field, he has no formal background in stem cell research. His company offers stem cell procedures for more than 30 diseases and conditions, including Lou Gehrig's disease, multiple sclerosis, lupus and erectile dysfunction.

There are clinics that market "anti-aging" treatments; others specialize in "stem-cell facelifts" and other cosmetic procedures. The cost is high, ranging from $5,000 to $20,000.

Berman and others point to anecdotal accounts of seemingly miraculous recoveries. But while stem cells from bone marrow have become an established therapy for a handful of blood cancers — and while there are high hopes that the cells will someday lead to other major medical advances — critics say entrepreneurs are treating patients with little or no evidence that what they do is effective.

Or even safe. They point to one stem-cell doctor who has had two patients die under his care.

"It's sort of this 21st century cutting-edge technology," says Dr. Paul Knoepfler, a stem cell researcher at the University of California at Davis. "But the way it's being implemented at these clinics and how it's regulated is more like the 19th century. It's a Wild West."

___

DISCOVERING 'LIQUID GOLD'

Doctors in South Korea and Japan pioneered the fat-based stem cell technique, using it to supposedly enhance face lifts and breast augmentation. For years, U.S. patients would travel to hospitals in Asia, Latin America and Eastern Europe — places where regulation is more lax than in the United States — to have these procedures as part of the international "stem cell tourism" trade.

Plastic surgeons in the U.S. quickly realized the financial potential of the fat they were already taking out of patients' bellies and backsides through liposuction — something that had been disposed of previously. Berman calls it "liquid gold."

Some early adopters have expanded into chains, offering doctors across the country a chance to join the franchise after buying some equipment and attending a seminar. These doctors sometimes appear on local TV news broadcasts, drumming up new business from patients and stoking interest from other doctors.

One national chain markets itself online with accounts of celebrity athletes who have been treated with its stem cell procedures. Prospective patients are then directed to a call center, where sales representatives try to match them with stem cell doctors over the phone."

Yeah, he's pitching supposedly "better" (more like SALES PITCHING, not baseball LOL) cause of those ole magic "stem cells" and that's supposed to be "science" and actual "medicine", right LOL. The guy is likely being PAID TO PROMOTE- the article above from the AP says just that from their investigative journalism.

ANECDOTES = snake oil. Simple as that IMO. It ain't "science" by a million miles.

BMAK and CDEL both "gamed" it again, moments into the close, LOL !!

0.0048 / 0.0065 (214000 x 180593)

That's CDEL on both the Bid and the Ask (bracketing it) and BMAK is right behind CDEL on the Ask, only moments into the close. Wow, like clockwork everyday.

Amazing, simply amazing. Like another 25% plus swing supposedly "up" on nothing volume into the close, after it trades down on sell size orders of 300K share block and more. Too funny. Like a 30% spread/swing- always moments before the close. This thing is really being "worked" IMHO. OTC-ville classic stuff.

The day's low is .004 again, it spent all day RED and "flat-lined" almost all day long- barely trading for several hours (actually two hours not posting a single trade), then both BMAK and CDEL open up the spread on the Ask to past GRAND CANYON WIDE to .0065 while the Bid stayed locked at .0048.

How do these OTC dilution MM's get away with this? Wild stuff.

When these dilution MM's run their next "down tranche"- I'd bet this goes to the .003's, easy this time. It's like they're setting the table, these MM's, just getting it all set for the next leg down. This has been the pattern since pretty much the beginning of 2015, at least that I've observed.

LOL BS Quote, "FDA_Endpoints_ComingForPhase2 Pivotal! Because, RPE Therapy Works! "

What? They don't_need any cash cause_the_myth that they are somehow_going to skip, like magic_needing to conduct an FDA phase 3 trial(s)???

Pure fantasy and total_conjecture IMO.

OCAT can't_even raise the_funding to start their now_late and delayed_PHASE II (remember Lanza, we HOPE TO START END OF 2014, and it's now JUNE of 2015 essentially? They're going to be heading to a yr late from their original claims and statements)- but now one is_to_believe they're gonna somehow skip phase III trials and gain some imaginary_early_approval?

Total nonsense IMO and 100% contrary to everything they just put_out in their_latest SEC filed 10-Q. The company NOWHERE states that CASH or money isn't a problem. Their 10-Q is PLASTERED with GOING CONCERN WARNINGS- it's probably the wording used more than any other words in their SEC, duly filed 10-Q.

Open the 10-Q and do a word count on GOING CONCERN (aka SHORT ON CASH) warnings- they're plastered from beginning_to_end of that latest_10-Q filing.

Here's a few "samples" of THEE COMPANY'S OWN WORDS, versus some myth that "cash is no problem" and they're supposedly just gonna sail on in to some "early_approval" blah, blah, blah.

Just filed OCAT 10-Q, PAGE 13:

"Our ability to become profitable depends upon our ability to generate revenue. We do not anticipate generating revenues from product sales FOR THE FORESEEABLE FUTURE, IF EVER. "

(What? WHY WOULD THAT BE, if their mythological "therapy" already "works"?? Why?)

OR,

PAGE 7, SAME SEC filed 10-Q, most recent:

"The Company has NO THERAPEUTIC PRODUCTS CURRENTLY AVAILABLE FOR SALE AND DOES NOT EXPECT TO HAVE ANY THERAPEUTIC PRODUCTS COMMERCIALLY AVAILABLE FOR SALE FOR A PERIOD OF YEARS, IF AT ALL. These factors indicate that the Company’s ability to continue research and development activities is dependent upon the ability of management to obtain additional financing as required."

(WHAT?? HOW CAN THAT BE? That's OCAT'S most recent filed SEC 10-Q?? According to MYTH they have a "therapy", RIGHT NOW, that supposedly "just works" and one can GET, NO???? So why does their 10-Q say just the opposite of the myth? The 10-Q says, "The Company has NO THERAPEUTIC PRODUCTS CURRENTLY AVAILABLE FOR SALE AND DOES NOT EXPECT TO HAVE ANY THERAPEUTIC PRODUCTS COMMERCIALLY AVAILABLE FOR SALE FOR A PERIOD OF YEARS, IF AT ALL." Something's a miss it seems. OCAT says they HAVE NO THERAPIES currently proven "that work" or "are for sale", NONE??? Why would they print that in their SEC filed 10-Q??)

Or, how bout why they're just about OUT OF MONEY when they have these mythological "therapies" that already supposedly "JUST WORK" as supposed unchallenged FACT? What? Why did they put all this other "stuff" then in their most recent SEC filed 10-Q and why did their own Lanza make statement verbatim like the ones below, ones where HE SAYS CAUTION and MORE TESTING NEEDED? When something supposedly AS FACT (which is a myth) plain old supposedly "JUST WORKS" well SHAZAM, then one doesn't say or need all the junk and stuff like below, the FACT BELOW said by the company's own Sr. Mgt and printed and signed in their own duly filed SEC documents- why, why would they say all the FACTS below:

From the highly respected science journal NATURE:

www.nature.com/news/stem-cells-pass-safety-test-in-vision-loss-trial-1.17451

Lanza doesn't say "IT WORKS"??? He says CAUTION and MORE TESTING NEEDED to "prove" anything? He didn't dispute or retract or question the NATURE article? Why? He DOES NOT EVER SAY "it works" - he says MORE TESTING NEEDED, lots more testing and lots more MONEY.

The VERBATIM article, again, from the highly respected science journal, "NATURE"-

"A company that has spent more than 20 years trying to develop treatments based on embryonic stem cells is taking encouragement from small, preliminary tests of the cells in people with progressive vision loss. If the technique continues to impress in larger trials designed to assess its effectiveness, it could become the first therapy derived from embryonic stem cells to reach the market.

A study of four patients, published in Stem Cell Reports on 30 April1, shows that injection of retinal cells derived from stem cells is safe for people with macular degeneration. The report follows similar results from a trial in 18 patients that was published last October2.

Both studies were meant to assess safety only, and neither included a control group. In the latest study, conducted by researchers in Korea and the United States, three participants were able to read 9–19 more letters further on an eye chart a year after treatment — but two of the three also gained some ground in their untreated eyes."

MORE...

"“This bodes well,” says Robert Lanza, chief scientific officer at Ocata Therapeutics in Marlborough, Massachusetts, and an author of the study. “But I think we need to interpret this improvement cautiously until more controlled studies are done.”

The sample size is too small to warrant much excitement, cautions ophthalmologist Tien Yin Wong of the Singapore National Eye Centre. “At this stage it’s hard to say if the visual improvement will be sustained,” he says. “But it’s very promising.”

Lanza speaking to a local MA newspaper-

www.telegram.com/article/20141014/NEWS/310149525&Template=printart

"We treated the last UK patients last month, and they also have not seen any safety issues related to the transplanted tissues themselves, either," Dr. Lanza said.

Advanced Cell now hopes to launch a 100-patient, phase 2 study in Stargardt's patients by the end of the year, according to Dr. Lanza.

A second, smaller phase 2 study in patients with age-related macular degeneration would follow, he said. Any treatment might not be ready for FDA approval until 2020, Dr. Lanza said."

THOSE are the "FACTS" as Lanza has stated um "on the record"- not the other myths that this is a DONE DEAL and SLAM DUNK and already "proven" to work, blah, blah, blah.

That was dated Oct 14, 2014 and the END OF YEAR phase II DID NOT HAPPEN.

Where's the BIG MONEY? Why don't they ever attract any large capital investments- especially any "high quality" money (non dilutive) or at least not cash-for-dilution-shares deals with discounts and all the rest attached to them? Why? Why is that? Why? They live on low grade dilution money and have NO WHERE NEAR the funds to get a large Phase II even started- let alone funded to completion? Why? Why is that?

It took like FIVE YEARS to get a micro sized phase I done. They've yet to even start the large and magnitudes more difficult and magnitudes more expensive Phase II trials (with control arms and placebo blinding)- why? If the phase I took about FIVE YEARS, then how long will these phase II trials take- the one(s) that were supposedly going to be fully funded and rocking and rolling by END OF 2014 and it's now almost half way through 2015 and the trial(s) are in the parking space, going nowhere and the latest Lincoln cash is dwindling down at an alarming rate. Why? Why is that?

www.sec.gov/Archives/edgar/data/1140098/000101968715001797/ocata_10q-033115.htm

Just filed OCAT 10-Q, PAGE 13:

"Our ability to become profitable depends upon our ability to generate revenue. We do not anticipate generating revenues from product sales for the foreseeable future, if ever. "

PAGE 7:

"The Company has no therapeutic products currently available for sale and does not expect to have any therapeutic products commercially available for sale for a period of years, if at all. These factors indicate that the Company’s ability to continue research and development activities is dependent upon the ability of management to obtain additional financing as required."

PAGE 7:

"The accompanying consolidated financial statements have been prepared in conformity with GAAP which contemplate continuation of the Company as a going concern. However, as of March 31, 2015, the Company has an accumulated deficit of $356.2 million, recurring losses from operations, and negative working capital which raise substantial doubt about the ability of the Company to continue as a going concern. The ability to continue as a going concern is dependent upon many factors, including the Company’s ability to raise additional capital in a timely manner. The Company has no expectation of generating any meaningful revenues from our product candidates for a substantial period of time and must rely on raising funds in capital transactions to finance our research and development programs. Our future cash requirements will depend on many factors, including the pace and scope of our research and development programs, the costs involved in filing, prosecuting and enforcing patents, and other costs associated with commercializing our potential products. Accordingly, management’s plans to continue as a going concern contemplate raising additional capital including the prior execution of an agreement for a $30 million equity line in late June 2014, of which approximately $12.5 million remains available as of March 31, 2015. There can be no assurances that management can raise the necessary additional capital on favorable terms or at all. The accompanying financial statements do not include any adjustments that might be necessary if the Company is unable to continue as a going concern."

PAGE 24:

"We cannot assure you that public or private financing or grants will be available on acceptable terms, if at all. Several factors will affect our ability to raise additional funding, including, but not limited to, the volatility of our common stock and the broader public equity market, especially public equities issued by other pre-commercial biotechnology companies, and our ability to raise capital through non-dilutive transactions such as out-licenses. If we are unable to raise additional funds, we will be forced to either scale back our business efforts or curtail our business activities entirely. As of March 31, 2015, the Company has an accumulated deficit of $356.2 million, recurring losses from operations, and negative working capital which raise substantial doubt about the ability of the Company to continue as a going concern.

"

Most recent filed 10-K, PAGE 16:

"

Other than our arrangement with Lincoln Park, we have no sources of debt or equity capital committed for funding. Recent attempts to raise capital in the public equity markets have proven unsuccessful, and we can provide no assurance that we will be successful in any future funding effort. The timing and degree of any future capital requirements will depend on many factors, including:

"

Same 10-K, PAGE 16:

"We will require substantial additional resources to fund our operations and to develop our product candidates. If we cannot find additional capital resources, we will have difficulty in operating as a going concern and growing our business."

Same 10-K, PAGE 16:

"Our independent auditor’s report for the fiscal year ended December 31, 2014 includes an explanatory paragraph regarding substantial doubt about our ability to continue as a going concern.

Due to the uncertainty of our ability to meet our current operating and capital expenses, in their report on our audited annual financial statements as of and for the year ended December 31, 2014, our independent auditors included an explanatory paragraph regarding concerns about our ability to continue as a going concern. Recurring losses from operations raise substantial doubt about our ability to continue as a going concern. If we are unable to continue as a going concern, we might have to liquidate our assets and the values we receive for our assets in liquidation or dissolution could be significantly lower than the values reflected in our financial statements. In addition, the inclusion of an explanatory paragraph regarding substantial doubt about our ability to continue as a going concern and our lack of cash resources may materially adversely affect our share price and our ability to raise new capital or to enter into critical contractual relations with third parties."

Same 10-K, PAGE 46:

"We have also audited, in accordance with the standards of the Public Company Accounting Oversight Board (United States), the consolidated balance sheet of Ocata Therapeutics, Inc. and Subsidiary as of December 31, 2014, and the related consolidated statements of operations, stockholders' deficit, and cash flows for the year then ended and our report dated March 16, 2015 expressed an unqualified opinion thereon and included an emphasis of a matter paragraph relating to an uncertainty as to the Company’s ability to continue as a going concern.

/s/ BDO USA, LLP

Boston, Massachusetts

March 16, 2015"

"

Boy, for a company with a mythological "therapy" that's PROVEN AS FACT to "just WORK" supposedly, they sure do like to plaster the GOING CONCERN WARNINGS all throughout their own SEC filings (GOING CONCERN is business speak for becoming "ill-liquid" which then leads to greatly cutting costs/spending or filing for BK)

But the myth is, that it all supposedly "JUST WORKS"??? LOL ! That OCAT is on some supposed "fast track"?? MYTH and conjecture and nothing more. The company's own SEC filings and public statement are in 100% contrast to "it just works". OCAT is fast running out of cash because NOTHING "just works" so far- and that's the reality. They're down to MONTHS worth of cash left to fund their operation and just booked another massive quarterly loss in their most recent SEC filed 10-Q and the common shares are being continually diluted and sitting near a 52 week low- in a still raging bull market.

Just FACTS versus conjecture and myths such as some "therapy" just "WORKS", LOL. In their own words, OCAT, they are YEARS and YEARS away from any "therapy" that "works" and can be sold to "human customers", IF EVER. That's their OWN WORDS.

Kinda RED here today???

This is the mythological "big institutional buyers" doing their "buying", here then, no? LOL.

I'm confused I guess? How is it- the common share price literally goes nowhere, sits hugging a 52 week low, when all this imaginary net "big buying" by supposed "big institutions" who are supposedly now "buying and holding" is going on?

How is large, imaginary "net buying" possible- but the share price never moves off bottom? How? How exactly, in detail, is that even possible?

I don't get it?

LOL BS quote, "However Paul Wotton is in UK and Europe to promote early approval by the MHRA and EMA respectively as well as Institutional buying $OCAT shares for Long-Term investments."

What? Is there a PUBLIC PR and PUBLIC SOURCE for this info? Or is this pure conjecture and just make it up out of thin air stuff?

WHERE did OCAT ever state thee above quote- as the reasons why Wotton is supposedly "in Europe" and in "the UK" ???

The guy is from Europe- for all one knows he's maybe vacationing over there and just "hanging out" for all one knows?

Where is the proof he's there to "promote institutional buying" and blah, blah, blah? Again, is there a PUBLIC PR saying those exact words or anything even remotely similar? A source from OCAT itself?

Quote, "From Icell"

I've personally never found that blog thingy to be a credible source of info for much of anything, I'd never use it myself, personally.

How that blog can take an article written about a totally different company, "REGENERON" or whatever it was, and then do a vast "extrapolation" (conjecture and wishful thinking IMO) - to somehow supposedly make an argument it means something even remotely true about this company, OCAT, is beyond me?

I find that's typical of what's done there daily- a lot of bad information and just plain old wrong "predictions" and similar.

Thus, I personally would never use it as a source of info myself. Never.

Quote, "The battle is between the 30 Institutionals vs Covered Shorts and the outcome of this will determine the PPS."

I'd say the "battle" is between this company living off of low grade Lincoln dilution money- or EVER raising any serious cash, the kind of cash that can even remotely begin to fund, let alone be remotely close to enough to fund to completion, a large Phase II clinical trial.

OCAT is desperately cash low as of right now (a solvency GOING CONCERN RISK per their own just filed 10-Q) - w/ cash below a pittance amount of approx $12 MILLION left in their bank and they just finished a qtr where they burned through and lost about $7 MILLION in just day to day overhead- while not funding so much as DIME ONE of a large clinical trial.

The little "list" of the supposed "institutional" blah, blah- is being totally misunderstood and over played IMO. It's NOT a sign of some mass supposed "institutional" buying, blah, blah, blah. It's simply the mechanics of a filing system of the way the Nasdaq works- if a form 13 is filed, some computer "bot" scrapes it and tabulates it, and that's all that "list" means.

The common share price is sitting near its 52 week low as the markets have made new all time highs. There's been no large "net buying"- it's simply not true. This stock is treading water at best and TRADES TODAY, BELOW WHERE IT TRADED AS AN OTC PENNY STINKER. Thus, the myth of the "list" and the supposed "institutions" doesn't hold any water in my book.

It's CASH, CASH IS KING that's going to determine the outcome of this "Game" and if OCAT is even going to be a player, let alone, even be let in to the stadium to play at this point. IF all these mythological "institutional buyers" supposedly existed- then WHY couldn't OCAT pull off a lousy $62 million secondary offering (with THREE high priced underwriters pitching it) - at a time when the markets were even stronger than today and deals were getting done in even higher numbers than today? When bio-tech was the hottest thing going- and now has "cooled" considerably? WHY? WHY would that secondary have failed if all this imaginary "institutional" supposed "big money" was all sitting out there waiting for a piece of OCAT supposedly?

Makes no sense and is not happening IMO. The stock has been a net sell for a month now- it blew off a top at a lousy $7.50 a share and couldn't even hold that- just headed right back down near $6 (6 CENTS pre R/S) and is languishing there now, still to this day.

Bid looks plastered back at .0046/.0045 this AM w/ only about $1000 bucks worth before it would hit the .003's

0.0045 / 0.0055 (200000 x 185000)

Interesting, the spread is much wider (at least at this moment, just prior to market open) and both CDEL and BMAK slid several levels back off the Ask on the Level II (for now, they've done this many times in the past few months), yet the Bid remains buried at this point? If either one of those two MM's slide back down that Ask at some point in the day- then it tells me nothing really has changed and the dilution MM's are still running the show.

It's done this several times in the past many months- after making a new all, all, all time low- these two MM's (CDEL and BMAK) back off the Level II ask for a "breather", sometimes it lasted a day or two, and a few times it only lasted hours at the most.

Will be real interesting IMO to see what these MM's do with it here today- after the mega volumes and new, all, all time lows made yesterday (Monday) and also Friday (14+ million shares yesterday driving it to .004 and 19+ MILLION on Friday driving it to .0043)- but the MM's closing it via "painting of the tape" (both CDEL and BMAK moving way off the Ask, Level II, only moments before the close on both days of new all, all time lows being made) - to bring the share price back "up" (sort of, LOL) within minutes or even seconds of market close on both those days.

Well, just about to hit "click" to post this- and BMAK has already slid down the Ask to .0055 (that didn't take long). So it already looks like that is the day's "capping price" more than likely right there IMO. BMAK just parked a 10K share block at .0055, they were clear out at like .0098 only moments ago. So BMAK IS BACK as usual- looks like it's not going anywhere above the .0055 area, which seems right where they want it from the past several day's action- while they ran massive down legs during the past 2 day, reaching a new all time low of .004

Pretty wild stuff in here- is there even a bottom? At this point, I'd say no real bottom exists as long as Magna is involved and BMAK and CDEL show up daily on the Level II. That's my take on it.

BigAl posted that "this is what Magna, aka BMAK does" and I'd have to say I totally agree with his post, 100% IMO.

LOL quote, "That was me eod throwing away more $$$."

Well, if one wanted to pick a stock in which to "throw away more $$$" I don't think they can find one much better than this one- since it makes a NEW ALL, ALL, ALL TIME LOW practically every day, LOL !!

.004 today. That's a new all time record low- since it went public in 2008.

Looking like the .003's are likely to be reached any ole day here now, very soon if it continues on the down-trend it's been in for over a year now, the down-trend that's been rapidly accelerating recently. Not much left after that but probably the ole infamous OTC "triple zeroes" or the "trips" as they are commonly known, the ole .000X per share, yep.

That .004 reached today, that's a 99.99% loss to the common shares since BHRT began trading public at about $5.00 a share in 2008 (and was delisted from the Nasdaq only about 1 yr later, forever relegated to the OTC ever since). Yep. Can't lose much more than 99.99%. That leaves .01% to go to ZERO.

Pretty amazing track record IMHO. Stunning in fact. All through probably the greatest bull market in world history- and probably the greatest bio-tech bull market ever seen. Yep. Losing 99.99% of the common share value during those good times is a real accomplishment- and gets the insiders large cash "bonuses" too boot.

Can't do much more to "throw away more $$$$" than that IMO, nope.

LOL, these MM's are gonna "PAINT THE TAPE" at close AGAIN !!

No freaking way?? BMAK and CDEL just vanish off the Ask and like Friday- it posts a few $100 lousy bucks worth of trades seconds into the close to make it look like it closed "flat" or even "up", LOL??

The OTC wild, wild West with dilution MM's with brass ones as big as bowling balls.

AFTER it got buried again today on MEGA VOLUME making a new all, all, all time lows of .004 it now supposedly closed flat to "up" on probably a few $50 trades, LOL. Really? I mean really?

How is this not lighting up the FINRA and SEC alert radars? How?

This is as wild as I've ever seen- even for the OTC/Pinks.

Too funny IMO. What a crack up. Yeah, it just suddenly goes up like 25 FREAKING PERCENT seconds in to the close on less than $500 traded (proably less than even $100 traded)- after being buried all day on how many MILLIONS of shares traded- including a single SELL, a down-tick, SOLID RED SELL of 6 MILLION shares in a single block, printed right smack on the daily chart.

Wait, let me guess- this was JOE Q. PUBLIC "retail" buyer who stepped in at end of day and suddenly just picked up those shares that magically brought the price up after it was buried on MILLIONS of shares all day, DOWN SOLID 25% ALL DAY LONG, LOL. (oh, and MM BMAK suddenly vanished way off the Ask and CDEL just happens to suddenly raise the Ask, like 20% plus in a blink- minutes, or even seconds in to the close- oh yeah, right on baby. Fa sure !!)

Yeah right. Sure. Got it. Right on. What a racket, eh? OTC-ville, LOL.

Stem Cells, the "un-regulated" WILD WEST according to the AP (Associated Press) and U.S News and World Report- journalism piece.

FASCINATING article IMO. Really amazing journalism - and full of some real interesting key words about the presently highly un-regulated "WILD WEST" of the "stem cell" field- according to this journalism piece, even quoting the highly respected stem cell researcher at U.C. Davis and blogger, "Dr. Paul Knoepfler,"

http://www.usnews.com/news/business/articles/2015/05/18/stem-cell-wild-west-takes-root-amid-lack-of-us-regulation

Quoting the article:

"Unproven stem cell procedures flourish across the US, outpacing regulation

By MATTHEW PERRONE, AP Health Writer

BEVERLY HILLS, Calif. (AP) — The liquid is dark red, a mixture of fat and blood, and Dr. Mark Berman pumps it out of the patient's backside. He treats it with a chemical, runs it through a processor — and injects it into the woman's aching knees and elbows.

The "soup," he says, is rich in shape-shifting stem cells — magic bullets that, according to some doctors, can be used to treat everything from Parkinson's disease to asthma to this patient's chronic osteoarthritis.

"I don't even know what's in the soup," says Berman. "Most of the time, if stem cells are in the soup, then the patient's got a good chance of getting better."

It's quackery, critics say. But it's also a mushrooming business — and almost wholly unregulated.

The number of stem-cell clinics across the United States has surged from a handful in 2010 to more than 170 today, according to figures compiled by The Associated Press. Many of the clinics are linked in large, for-profit chains. New businesses continue to open; doctors looking to get into the field need only take a weekend seminar offered by a training company.

Berman, a Beverly Hills plastic surgeon, is co-founder of the largest chain, the Cell Surgical Network. Like most doctors in the field, he has no formal background in stem cell research. His company offers stem cell procedures for more than 30 diseases and conditions, including Lou Gehrig's disease, multiple sclerosis, lupus and erectile dysfunction.

There are clinics that market "anti-aging" treatments; others specialize in "stem-cell facelifts" and other cosmetic procedures. The cost is high, ranging from $5,000 to $20,000.

Berman and others point to anecdotal accounts of seemingly miraculous recoveries. But while stem cells from bone marrow have become an established therapy for a handful of blood cancers — and while there are high hopes that the cells will someday lead to other major medical advances — critics say entrepreneurs are treating patients with little or no evidence that what they do is effective.

Or even safe. They point to one stem-cell doctor who has had two patients die under his care.

"It's sort of this 21st century cutting-edge technology," says Dr. Paul Knoepfler, a stem cell researcher at the University of California at Davis. "But the way it's being implemented at these clinics and how it's regulated is more like the 19th century. It's a Wild West."

___

DISCOVERING 'LIQUID GOLD'

Doctors in South Korea and Japan pioneered the fat-based stem cell technique, using it to supposedly enhance face lifts and breast augmentation. For years, U.S. patients would travel to hospitals in Asia, Latin America and Eastern Europe — places where regulation is more lax than in the United States — to have these procedures as part of the international "stem cell tourism" trade.

Plastic surgeons in the U.S. quickly realized the financial potential of the fat they were already taking out of patients' bellies and backsides through liposuction — something that had been disposed of previously. Berman calls it "liquid gold."

Some early adopters have expanded into chains, offering doctors across the country a chance to join the franchise after buying some equipment and attending a seminar. These doctors sometimes appear on local TV news broadcasts, drumming up new business from patients and stoking interest from other doctors......."

Amazing. Seems like the FDA is going to start putting even more scrutiny to this "stem cell stuff" now, more than ever IMO. This article has got to be lighting up the FDA's regulatory radar big time IMO. Big time.

Remember, the FDA has already ruled and won in court- that STEM CELLS are to be regulated "as DRUGS":

http://www.nature.com/news/fda-s-claims-over-stem-cells-upheld-1.11082

http://www.the-scientist.com/?articles.view/articleNo/39108/title/Judges-Side-with-FDA-on-Stem-Cells/

http://www.fda.gov/AboutFDA/Transparency/Basics/ucm194655.htm

QUOTE from the FDA website (you know, the myth that claims it's "a FACT" that this OCAT stuff just "works" LOL)

"Stem cells, like other medical products that are intended to treat, cure or prevent disease, generally require FDA approval before they can be marketed. At this time, there are no licensed stem cell treatments."

http://www.fda.gov/ForConsumers/ConsumerUpdates/ucm286155.htm

Market cap now BARELY $3 MILLION dollars, holy cow.

What a massive collapse in market cap. In the last 10-Q, the accounts payable alone were about $2 MILLION, now more than 50% of their market cap and total obligations/debt was $11 MILLION or so, now over 3X their market cap. Is it possible for them to stay solvent with this ever dropping share price- while still needing near continual common share selling/dumping dilution money to survive? Seems pretty dicey in here- and the "GOING CONCERN WARNINGS" were already plastered all throughout that most recent filed 10-Q (see the 10-Q linked below and just look for GOING CONCERN, it's all throughout that SEC filing), and things have only gotten worse now, in just the past 1 month or so?

From the most recent 10-Q, PAGE 1:

http://www.sec.gov/Archives/edgar/data/1388319/000114544315000630/bioheart_10q.htm

"As of May 05, 2015, there were 734,759,150 outstanding shares of the Registrant’s common stock, par value $0.001 per share. "

The day's low so far is .004 cents

So that put the market cap this AM at:

734,759,150 X .004 = $2,939,036

Their market cap actually dipped SUB $3 MILLION this AM.

Wow, amazing.

What's "BROKEN"?? LOL quote, "10-Q Blah What? huh? duh? Broken record"

0.0042 / 0.0043 (110000 x 410000)

4 to 1 to the Ask/sell-side on new all, all, all time lows. What's "broken" exactly?

The only thing that appears "broken" IMO is this company of a few people and the ever dropping common share price, LOL??

Bid as low as .0041 this AM, soon it appears to be reaching the .003's and they ended the last qtr, the "big revenue" thingy quarter with a grand total of about $79K cash left and just the accounts payable debts were $2 MILLION plus and total current obligations are like $11 MILLION and they took a larger loss from operations despite the "revenues" thingy.

Yeah, those pesky SEC filed 10-K's and 10-Q's are a real bummer I guess, cause the whole "story" is contained therein. Including the massive share dilution numbers (87 MILLION shares approx in a period of only a few months) and the continual use of toxic, convertible, floorless debt deals and also the continual tapping of the dilution Magna "credit line" deal- ALL in detail in those gosh darn SEC 10-Q's and 10-K's. Yep.

BROKEN RECORD appears to likely be the situation of any common shareholder- as the common shares have lost 70% of their value in 2015 alone and 99.99% of their value since they went public. A literal $5 DOLLARS a share to now .004 (4/10ths of ONE CENT) a share.

Just since the present CEO took over in mid 2010, the common shares have lost about 99% or more of their value.

http://www.prnewswire.com/news-releases/bioheart-announces-mike-tomas-appointed-ceo-97013034.html

In June of 2010, the common shares traded for about .50, 50 CENTS and maybe as high as .70 or 70 CENTS. They trade today for about .004 CENTS.

50 - .004 = 49.996 / 50 = .9992 X 100 = 99.92% LOSS to the common shares "on the watch" and command of the present CEO.

For that incredible "performance" to the common shareholders- what does one get? How bout some LARGE CASH BONUSES and about a TRIPLE of their base pay in a period of only the past few years. NOT BAD, eh? Not bad at all IMO.

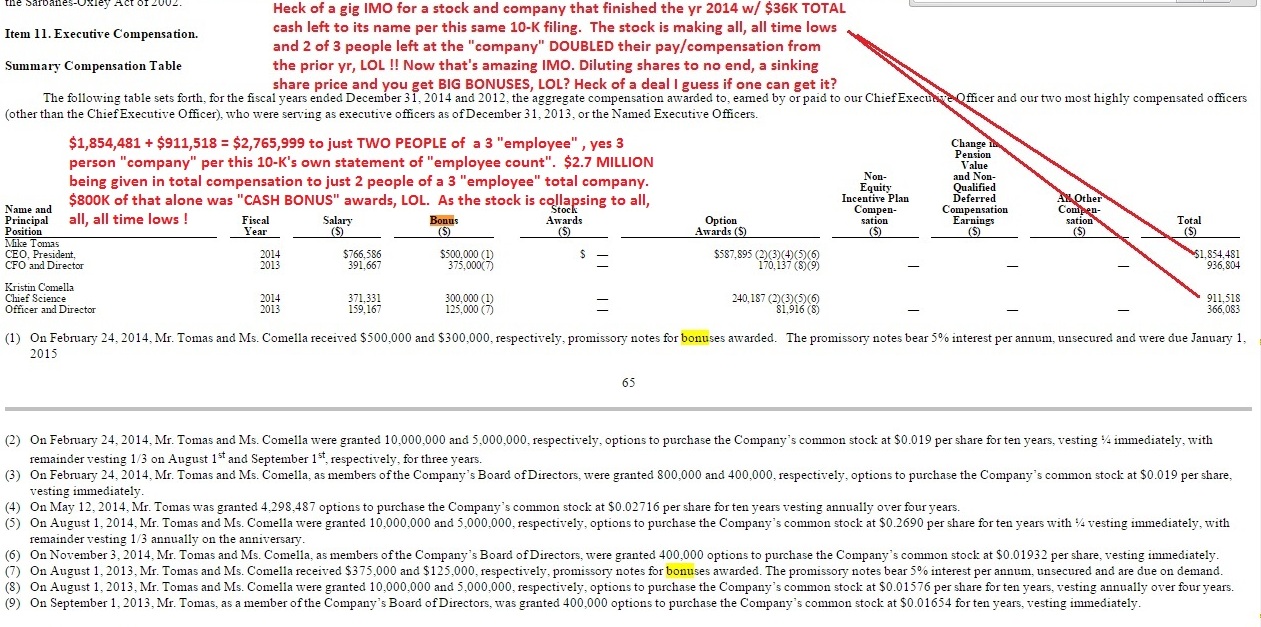

This table is from their last SEC filed 10-K (see the one before that to see how much the pay has increased from 2013 to now- a TRIPLE pretty much, plus cash bonus awards to only TWO people of the company)

Not bad, not bad at all IMO. The "broken record" appears to be BHRT's "record" of common share performance and NO ROI to its shareholders- that's the way it seems to me personally, IMO. The insiders seem to be doing pretty well though, according to that SEC filing, no?

HOLY COW, new ALL, ALL TIME LOW - wipe out. Wow.

0.0041 / 0.0043 (25000 x 410000)

BOTH the Bid and Ask are now at new all, all time lows- holy cow !! The volume just blew up in an instant to almost 5 MILLION shares as the dilution MM's sunk it like a lead boat anchor- wow.

It really looks like the .003's are coming soon. It really does IMO. This thing is in total Bid free-fall, and not a sign in sighe to stop or abate it IMO. It's stunning the sell-side pressure this thing has been under for essentially all of 2015 now.

And no "PR" or "SEC" 10-Q or "news" of some "new business "plan" or the "revenues" thingy or whatever has appeared to make a wit of difference. It seems to me- that 85 MILLION shares of raw dilution in only a few month period (see the most recent 10-Q and the most recent end of 2014 10-K SEC filing share counts- and look at the rate of dilution) is just too much to overcome perhaps? Maybe?

Also, the inking of qty-5, FIVE more toxic, floorless, convertible debt financing deals in just Jan/Feb and then April of 2015 already (see 10-K most recent page F-34 and most recent 10-Q "subsequent financing")- it seems inking just more toxic, highly dilutive financing, essentially continuously for all intents and purposes- with steep, steep share discounts (see SEC filings, 45% and 47% discounts are the norm, Daniel James, KBM Worldwide, Asher, Fourth Man, Vis Vires, etc)- and the now near continual use of tapping the MAGNA dilution credit line- well, it all seems like it might just be putting a lot of down, sell-side pressure on the common shares, a real "death spiral" as the SEC site calls it.

Maybe? I mean something has to explain this? This continual Bid collapse and making of new all, all time lows is pretty stunning IMO.

http://www.marketwired.com/press-release/bioheart-inc-completes-financing-with-magna-otcqb-bhrt-1960953.htm

http://www.bloomberg.com/news/articles/2015-03-12/josh-sason-made-millions-from-penny-stock-financing

http://www.sec.gov/answers/convertibles.htm

http://en.wikipedia.org/wiki/Death_spiral_financing

Bid only .0045, that "was" the new all, ALL TIME LOW until Friday.

Spread is cranked pretty wide open this AM, like the dilution MM's maybe are gonna try and hunt up some buyers perhaps on the spread? But it's still stacked heavy to the Ask/Sell-side again. Looking real weak still with the Bid at sub 1/2 CENTS, plastered just off the new all, all, all time low put in last Friday, now at .0043 (wasn't that long ago that this stock's all, all time low was .0063, WOW, how fast things can change on the ole OTC I guess?)

0.0045 / 0.0052 (158327 x 670000)

So that's 4 to 1, almost 5 to 1 again to the Ask/sell-side.

It put in massive down-side volume last Friday, reaching almost 20 million shares traded as it made its new all, all, all time low of .0043

Now the Bid today is only .0045, so it looks like sub 1/2 CENT might be starting to be the new "normal" and base area perhaps? No catalyst appears to be able to stop or abate the dilution selling or even remotely begin to reverse what is for all intents and purposes now a ONE YEAR solid down trend?

Pretty amazing IMO. Still real weak in here it looks like. Might be another brutal week on this one?

LOL BS quote, "RPE Therapy Works! This Is An Unchallenged FACT! "

What? It's actually not a "fact" but a pure myth, and is highly "challenged" via the company's own SEC filings and Sr Mgt's own public statements? What "fact" that a OCAT produced imaginary "therapy" exists that just "works"?? Where? Where can one go buy and use this mythological OCAT made "therapy" that supposedly "just works" today?

Just filed OCAT 10-Q, PAGE 13:

"Our ability to become profitable depends upon our ability to generate revenue. We do not anticipate generating revenues from product sales FOR THE FORESEEABLE FUTURE, IF EVER. "

(What? WHY WOULD THAT BE, if their mythological "therapy" already "works"?? Why?)

OR,

PAGE 7, SAME SEC filed 10-Q, most recent:

"The Company has NO THERAPEUTIC PRODUCTS CURRENTLY AVAILABLE FOR SALE AND DOES NOT EXPECT TO HAVE ANY THERAPEUTIC PRODUCTS COMMERCIALLY AVAILABLE FOR SALE FOR A PERIOD OF YEARS, IF AT ALL. These factors indicate that the Company’s ability to continue research and development activities is dependent upon the ability of management to obtain additional financing as required."

(WHAT?? HOW CAN THAT BE? That's OCAT'S most recent filed SEC 10-Q?? According to MYTH they have a "therapy", RIGHT NOW, that supposedly "just works" and one can GET NOT???? So why does their 10-Q say just the opposite of the myth? The 10-Q says, "The Company has NO THERAPEUTIC PRODUCTS CURRENTLY AVAILABLE FOR SALE AND DOES NOT EXPECT TO HAVE ANY THERAPEUTIC PRODUCTS COMMERCIALLY AVAILABLE FOR SALE FOR A PERIOD OF YEARS, IF AT ALL." Something's a miss it seems. OCAT says they HAVE NO THERAPIES currently proven "that work" or "are for sale", NONE??? Why would they print that in their SEC filed 10-Q??)

Or, how bout why they're just about OUT OF MONEY when they have these mythological "therapies" that already supposedly "JUST WORK" as supposed unchallenged FACT? What? Why did they put all this other "stuff" then in their most recent SEC filed 10-Q and why did their own Lanza make statement verbatim like the ones below, ones where HE SAYS CAUTION and MORE TESTING NEEDED? When something supposedly AS FACT (which is a myth) plain old supposedly "JUST WORKS" well SHAZAM, then one doesn't say or need all the junk and stuff like below, the FACT BELOW said by the company's own Sr. Mgt and printed and signed in their own duly filed SEC documents- why, why would they say all the FACTS below:

From the highly respected science journal NATURE:

www.nature.com/news/stem-cells-pass-safety-test-in-vision-loss-trial-1.17451

Lanza doesn't say "IT WORKS"??? He says CAUTION and MORE TESTING NEEDED to "prove" anything? He didn't dispute or retract or question the NATURE article? Why? He DOES NOT EVER SAY "it works" - he says MORE TESTING NEEDED, lots more testing and lots more MONEY.

The VERBATIM article, again, from the highly respected science journal, "NATURE"-

"A company that has spent more than 20 years trying to develop treatments based on embryonic stem cells is taking encouragement from small, preliminary tests of the cells in people with progressive vision loss. If the technique continues to impress in larger trials designed to assess its effectiveness, it could become the first therapy derived from embryonic stem cells to reach the market.

A study of four patients, published in Stem Cell Reports on 30 April1, shows that injection of retinal cells derived from stem cells is safe for people with macular degeneration. The report follows similar results from a trial in 18 patients that was published last October2.

Both studies were meant to assess safety only, and neither included a control group. In the latest study, conducted by researchers in Korea and the United States, three participants were able to read 9–19 more letters further on an eye chart a year after treatment — but two of the three also gained some ground in their untreated eyes."

MORE...

"“This bodes well,” says Robert Lanza, chief scientific officer at Ocata Therapeutics in Marlborough, Massachusetts, and an author of the study. “But I think we need to interpret this improvement cautiously until more controlled studies are done.”

The sample size is too small to warrant much excitement, cautions ophthalmologist Tien Yin Wong of the Singapore National Eye Centre. “At this stage it’s hard to say if the visual improvement will be sustained,” he says. “But it’s very promising.”

Lanza speaking to a local MA newspaper-

www.telegram.com/article/20141014/NEWS/310149525&Template=printart

"We treated the last UK patients last month, and they also have not seen any safety issues related to the transplanted tissues themselves, either," Dr. Lanza said.

Advanced Cell now hopes to launch a 100-patient, phase 2 study in Stargardt's patients by the end of the year, according to Dr. Lanza.

A second, smaller phase 2 study in patients with age-related macular degeneration would follow, he said. Any treatment might not be ready for FDA approval until 2020, Dr. Lanza said."

THOSE are the "FACTS" as Lanza has stated um "on the record"- not the other myths that this is a DONE DEAL and SLAM DUNK and already "proven" to work, blah, blah, blah.

That was dated Oct 14, 2014 and the END OF YEAR phase II DID NOT HAPPEN.

Where's the BIG MONEY? Why don't they ever attract any large capital investments- especially any "high quality" money (non dilutive) or at least not cash-for-dilution-shares deals with discounts and all the rest attached to them? Why? Why is that? Why? They live on low grade dilution money and have NO WHERE NEAR the funds to get a large Phase II even started- let alone funded to completion? Why? Why is that?

It took like FIVE YEARS to get a micro sized phase I done. They've yet to even start the large and magnitudes more difficult and magnitudes more expensive Phase II trials (with control arms and placebo blinding)- why? If the phase I took about FIVE YEARS, then how long will these phase II trials take- the one(s) that were supposedly going to be fully funded and rocking and rolling by END OF 2014 and it's now almost half way through 2015 and the trial(s) are in the parking space, going nowhere and the latest Lincoln cash is dwindling down at an alarming rate. Why? Why is that?

www.sec.gov/Archives/edgar/data/1140098/000101968715001797/ocata_10q-033115.htm

Just filed OCAT 10-Q, PAGE 13:

"Our ability to become profitable depends upon our ability to generate revenue. We do not anticipate generating revenues from product sales for the foreseeable future, if ever. "

PAGE 7:

"The Company has no therapeutic products currently available for sale and does not expect to have any therapeutic products commercially available for sale for a period of years, if at all. These factors indicate that the Company’s ability to continue research and development activities is dependent upon the ability of management to obtain additional financing as required."

PAGE 7:

"The accompanying consolidated financial statements have been prepared in conformity with GAAP which contemplate continuation of the Company as a going concern. However, as of March 31, 2015, the Company has an accumulated deficit of $356.2 million, recurring losses from operations, and negative working capital which raise substantial doubt about the ability of the Company to continue as a going concern. The ability to continue as a going concern is dependent upon many factors, including the Company’s ability to raise additional capital in a timely manner. The Company has no expectation of generating any meaningful revenues from our product candidates for a substantial period of time and must rely on raising funds in capital transactions to finance our research and development programs. Our future cash requirements will depend on many factors, including the pace and scope of our research and development programs, the costs involved in filing, prosecuting and enforcing patents, and other costs associated with commercializing our potential products. Accordingly, management’s plans to continue as a going concern contemplate raising additional capital including the prior execution of an agreement for a $30 million equity line in late June 2014, of which approximately $12.5 million remains available as of March 31, 2015. There can be no assurances that management can raise the necessary additional capital on favorable terms or at all. The accompanying financial statements do not include any adjustments that might be necessary if the Company is unable to continue as a going concern."

PAGE 24:

"We cannot assure you that public or private financing or grants will be available on acceptable terms, if at all. Several factors will affect our ability to raise additional funding, including, but not limited to, the volatility of our common stock and the broader public equity market, especially public equities issued by other pre-commercial biotechnology companies, and our ability to raise capital through non-dilutive transactions such as out-licenses. If we are unable to raise additional funds, we will be forced to either scale back our business efforts or curtail our business activities entirely. As of March 31, 2015, the Company has an accumulated deficit of $356.2 million, recurring losses from operations, and negative working capital which raise substantial doubt about the ability of the Company to continue as a going concern.

"

Most recent filed 10-K, PAGE 16:

"

Other than our arrangement with Lincoln Park, we have no sources of debt or equity capital committed for funding. Recent attempts to raise capital in the public equity markets have proven unsuccessful, and we can provide no assurance that we will be successful in any future funding effort. The timing and degree of any future capital requirements will depend on many factors, including:

"

Same 10-K, PAGE 16:

"We will require substantial additional resources to fund our operations and to develop our product candidates. If we cannot find additional capital resources, we will have difficulty in operating as a going concern and growing our business."

Same 10-K, PAGE 16:

"Our independent auditor’s report for the fiscal year ended December 31, 2014 includes an explanatory paragraph regarding substantial doubt about our ability to continue as a going concern.

Due to the uncertainty of our ability to meet our current operating and capital expenses, in their report on our audited annual financial statements as of and for the year ended December 31, 2014, our independent auditors included an explanatory paragraph regarding concerns about our ability to continue as a going concern. Recurring losses from operations raise substantial doubt about our ability to continue as a going concern. If we are unable to continue as a going concern, we might have to liquidate our assets and the values we receive for our assets in liquidation or dissolution could be significantly lower than the values reflected in our financial statements. In addition, the inclusion of an explanatory paragraph regarding substantial doubt about our ability to continue as a going concern and our lack of cash resources may materially adversely affect our share price and our ability to raise new capital or to enter into critical contractual relations with third parties."

Same 10-K, PAGE 46:

"We have also audited, in accordance with the standards of the Public Company Accounting Oversight Board (United States), the consolidated balance sheet of Ocata Therapeutics, Inc. and Subsidiary as of December 31, 2014, and the related consolidated statements of operations, stockholders' deficit, and cash flows for the year then ended and our report dated March 16, 2015 expressed an unqualified opinion thereon and included an emphasis of a matter paragraph relating to an uncertainty as to the Company’s ability to continue as a going concern.

/s/ BDO USA, LLP

Boston, Massachusetts

March 16, 2015"

"

Boy, for a company with a mythological "therapy" that's PROVEN AS FACT to "just WORK" supposedly, they sure do like to plaster the GOING CONCERN WARNINGS all throughout their own SEC filings (GOING CONCERN is business speak for becoming "ill-liquid" which then leads to greatly cutting costs/spending or filing for BK)

But the myth is, that it all supposedly "JUST WORKS"??? LOL ! That OCAT is on some supposed "fast track"?? MYTH and conjecture and nothing more. The company's own SEC filings and public statement are in 100% contrast to "it just works". OCAT is fast running out of cash because NOTHING "just works" so far- and that's the reality. They're down to MONTHS worth of cash left to fund their operation and just booked another massive quarterly loss in their most recent SEC filed 10-Q and the common shares are being continually diluted and sitting near a 52 week low- in a still raging bull market.

Just FACTS versus conjecture and myths such as some "therapy" just "WORKS", LOL. In their own words, OCAT, they are YEARS and YEARS away from any "therapy" that "works" and can be sold to "human customers", IF EVER. That's their OWN WORDS.

LOL quote, "Ocata Therapeutics to Present at the Jefferies 2015 Global Healthcare ConferenceAdditional Presentations at the London Regenerative Medicine Network and 10th Annual World Stem Cells & Regenerative Medicine Congress 2015 "

When all else fails (like RAISING CASH and being down to your last $12 MILLION while your "big trial" fails to start or progress forward, you know, by END OF 2014, and its now almost JUNE OF 2015)- GIVE "talks" and "presentations", LOL !!

Might as well burn some cash off that ole travel expense wine n dine junket budget line- cash NOT being spent on clinical trials.

Great, another "talk" and another "presentation", cause you know- the ones so far have made such a big difference as the common shares hug the bottom near the 52 week low, BELOW where they traded on the OTC and as the last of the biggest raging bull market in world history passes right on by.

Just filed OCAT 10-Q, PAGE 13:

"Our ability to become profitable depends upon our ability to generate revenue. We do not anticipate generating revenues from product sales for the foreseeable future, if ever. "

PAGE 7:

"The Company has no therapeutic products currently available for sale and does not expect to have any therapeutic products commercially available for sale for a period of years, if at all. These factors indicate that the Company’s ability to continue research and development activities is dependent upon the ability of management to obtain additional financing as required."

PAGE 7:

"The accompanying consolidated financial statements have been prepared in conformity with GAAP which contemplate continuation of the Company as a going concern. However, as of March 31, 2015, the Company has an accumulated deficit of $356.2 million, recurring losses from operations, and negative working capital which raise substantial doubt about the ability of the Company to continue as a going concern. The ability to continue as a going concern is dependent upon many factors, including the Company’s ability to raise additional capital in a timely manner. The Company has no expectation of generating any meaningful revenues from our product candidates for a substantial period of time and must rely on raising funds in capital transactions to finance our research and development programs. Our future cash requirements will depend on many factors, including the pace and scope of our research and development programs, the costs involved in filing, prosecuting and enforcing patents, and other costs associated with commercializing our potential products. Accordingly, management’s plans to continue as a going concern contemplate raising additional capital including the prior execution of an agreement for a $30 million equity line in late June 2014, of which approximately $12.5 million remains available as of March 31, 2015. There can be no assurances that management can raise the necessary additional capital on favorable terms or at all. The accompanying financial statements do not include any adjustments that might be necessary if the Company is unable to continue as a going concern."

PAGE 24:

"We cannot assure you that public or private financing or grants will be available on acceptable terms, if at all. Several factors will affect our ability to raise additional funding, including, but not limited to, the volatility of our common stock and the broader public equity market, especially public equities issued by other pre-commercial biotechnology companies, and our ability to raise capital through non-dilutive transactions such as out-licenses. If we are unable to raise additional funds, we will be forced to either scale back our business efforts or curtail our business activities entirely. As of March 31, 2015, the Company has an accumulated deficit of $356.2 million, recurring losses from operations, and negative working capital which raise substantial doubt about the ability of the Company to continue as a going concern.

"

Most recent filed 10-K, PAGE 16:

"

Other than our arrangement with Lincoln Park, we have no sources of debt or equity capital committed for funding. Recent attempts to raise capital in the public equity markets have proven unsuccessful, and we can provide no assurance that we will be successful in any future funding effort. The timing and degree of any future capital requirements will depend on many factors, including:

"

Same 10-K, PAGE 16:

"We will require substantial additional resources to fund our operations and to develop our product candidates. If we cannot find additional capital resources, we will have difficulty in operating as a going concern and growing our business."

Same 10-K, PAGE 16:

"Our independent auditor’s report for the fiscal year ended December 31, 2014 includes an explanatory paragraph regarding substantial doubt about our ability to continue as a going concern.

Due to the uncertainty of our ability to meet our current operating and capital expenses, in their report on our audited annual financial statements as of and for the year ended December 31, 2014, our independent auditors included an explanatory paragraph regarding concerns about our ability to continue as a going concern. Recurring losses from operations raise substantial doubt about our ability to continue as a going concern. If we are unable to continue as a going concern, we might have to liquidate our assets and the values we receive for our assets in liquidation or dissolution could be significantly lower than the values reflected in our financial statements. In addition, the inclusion of an explanatory paragraph regarding substantial doubt about our ability to continue as a going concern and our lack of cash resources may materially adversely affect our share price and our ability to raise new capital or to enter into critical contractual relations with third parties."

Same 10-K, PAGE 46:

"We have also audited, in accordance with the standards of the Public Company Accounting Oversight Board (United States), the consolidated balance sheet of Ocata Therapeutics, Inc. and Subsidiary as of December 31, 2014, and the related consolidated statements of operations, stockholders' deficit, and cash flows for the year then ended and our report dated March 16, 2015 expressed an unqualified opinion thereon and included an emphasis of a matter paragraph relating to an uncertainty as to the Company’s ability to continue as a going concern.

/s/ BDO USA, LLP

Boston, Massachusetts

March 16, 2015"

"

Sounds like a great time to just TALK MORE, LOL !! When one can't deliver the "goods" as promised- just wine and dine and travel and GIVE TALKS. Why not? Any CASH going to come from these "talking" events?

LOL quote, "Professional investors say that you are in error. $2mil of new investment in $OCAT says it all!!! "

Really? The SHARE PRICE ALONE SAYS YOU are in "error" as does the OPEN SHORT INTEREST which is greater than the table of supposed "institutional buys" being interpreted 100% incorrectly.

OPEN SHORT INTEREST is almost 1/2 MILLION shares, exceeding any supposed "institutional buying", LOL. How does that "work" exactly?

That little "list" by no means those firms are now "long" OCAT or going to "hold" it etc. NOT what it means. It simply means a SEC form 13 got filed for any of numerous reasons- and a computer program auto "scraped it" and read it and creates that NASDAQ table.

The common shares are sitting just shy of their 52 week LOW as the bull market has been raging to new highs.

There's no mythological "large buying" or large institutional "accumulation" of OCAT supposedly taking place? The share price alone completely disproves that- the shares are DOWN approx 20% in a very short period from the near term, VERY SHORT TERM "pop" to only $7.50 (7.5 cents pre R/S) and then sold right back off to $6, not being "bought" in volume as is claimed? What proof is there of that? The stock has been a NET SELL recently- losing 20% from a near term top?

The stock today traded BELOW its former OTC price when split adjusted- again, conclusive proof it's been SELLING OFF if anything. NOT being bought in large volumes or accumulated, simply not true.

OPEN SHORT interest is GREATER THAN so called "institutional ownership" - which actually isn't even "institutional ownership" per say.

The number of shares SHORT exceeds the so called "institutional ownership" - which is not even necessarily "ownership" or long term holders of the stock.

Open short interest: 434,695 (almost HALF A MILLION shares)

Supposed "institutional ownership" (including those who hold/held like 20 shares LOL): 352,331

It's being SHORTED more than any so called "institutions" are supposedly "buying it", let alone "holding it" supposedly.

The little "list" continually being quoted is just a "scraping" of ANY firm that files a form 13, as this stock is now on the Nasdaq and that's a Nasdaq requirement for firms who transact a certain annual or total share volume of ANY shares of stock, etc.

That firm may be a computerized hedge fund that buys n sells shares of companies all day long- and may enter and exit a position in OCAT in a matter of minutes or days or a week or whatever. (look at the "list"- it shows like 20 or 100 shares in some cases, LOL. One really imagines some "institutional buyer" sat and decided to pick up 20 freaking shares of lil ole OCAT, LOL !! Really? )

The list shows "Citigroup" with 54, yes FIFTY FOUR shares, LOL. If one really believes that some supposed "institutional ownership" division in Citigroup went and bought 54 shares to HOLD and GO LONG of a $6 buck stock- well, then too funny IMO. That's just some computer generated form 13 entry that got generated on some Citi tabular SEC filing or something more than likely- and I don't believe Citi is now "long" $324 bucks worth or whatever of lil ole OCAT, not a chance.

It can be done by computerized index buying - which is the case in probably most of that little ever changing "list". And it can be HEDGE FUNDS who are going to short the stock into the dirt for all one knows and they want inventory or auto-bought "X" number of shares per some algo or something- who knows.

It can also be "wealth mgt" firms buying for an unknown client who wants to remain unknown- like maybe some legal settlement deal or who knows what- as OCAT has a long list of people they're paying shares off too and similar.

The idea that ever name on that list is now "long" and going to "hold" OCAT is pure nonsense IMO. Read the Nasdaq disclosure at the bottom of that table- also, I can find many other sites with differing numbers than the little "list", again cause it's all done via "bots" that auto-scrape SEC form 13 filings and nothing more. No further investigation is done to know who or what transacted those shares and if they are "long" and are actual "investors" as is being claimed, etc.

It's a big ta-do about nothing. It's noise level- not even 1% of the O/S float. The open SHORT INTEREST has more shares as a percentage of float than the imagined "institutional" supposed "new holders" of OCAT- some of who again, would have bought like 20 shares (LOL x 1000) according to the little "table/list" being cited over and over.

Means nothing. The shares are sitting very close to the 52 week LOW, and have gone NOWHERE since being listed on the NASDAQ. The shares today trade BELOW where they did as OTC penny shares when R/S split adjusted. What's all this imaginary "big institutional" supposed "buying" and "holding" done for the share price?? NOTHING, LOL- a goose egg. DOWN. DOWN almost 20% in a short period from the $7.50 recent spike when Lincoln took a dilution breather for a few days.

The real massive dilution hasn't even gotten underway yet- the way they're gonna (if they even can) raise even cash to even remotely have close to enough to begin a large phase II, let alone fund one to completion- no one knows what that huge block of shares will be sold at, and how much the dilution is going to be?

They tried once in the secondary market and bombed- they couldn't sell $62 million worth, even with qty-3 expensive underwriters (who they paid a bundle, that money is gone), they couldn't pull it off in a raging bull market- and the market today has cooled if anything, not just bio-tech, but overall it's a much weaker market than when they pitched the secondary and failed.

Most recent filed 10-K, PAGE 16:

"

Other than our arrangement with Lincoln Park, we have no sources of debt or equity capital committed for funding. Recent attempts to raise capital in the public equity markets have proven unsuccessful, and we can provide no assurance that we will be successful in any future funding effort. The timing and degree of any future capital requirements will depend on many factors, including: "

Most recent filed SEC 10-Q:

PAGE 7: