News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

amarksp

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Rand key to gold output stability:

great article... SA gold supply is a key variable to POG.

_____________________

Posted by: 4godnwv

In reply to: None Date:1/19/2005 11:14:26 PM

Post #of 2610

Rand key to gold output stability:

By Eric Onstad

January 19, 2005

Production decline 33% over decade

Johannesburg: Gold output in South Africa is expected to fall slightly this year, but a bigger slide is threatened if the rand extends its bull run, a government expert said yesterday.

SA gold production could nearly stabilise this year with a buoyant dollar gold price and a stable rand, Alex Conradie, chief mineral economist with the Department of Minerals and Energy, told Reuters.

The country has seen production tumble by over a third in the past decade as high-grade mines run out of ore and firms have to dig deeper to find new deposits.

This year output is forecast to slip only three tonnes to 363 tonnes, a decline of 0.8% after an estimated fall of six tonnes, or 1.6%, in 2004. Final figures for last year are not yet available. "But I think that there is definitely a danger that it could fall further (in 2005) with a stronger rand," Conradie added.

The main factor in knocking output over the past few years has been the rampaging rand, one of the world's best performing currencies, which has strengthened 127% against the dollar since late 2001.

A strong rand, which rallied by 18% versus the greenback in 2004, slashes local income from dollar sales of gold, making some mines unprofitable and vulnerable to closure.

Downscaling

Last year the largest domestic gold producer, Harmony Gold, announced downscaling at six unprofitable shafts that had been producing a total of 220 000 ounces (6.84 tonnes) of output per year.

But this year Conradie expects the rand to stabilise at an average of R6.00 against the dollar, not far from its midday level yesterday of R6.08.

He also projects the dollar gold price will average $447 per ounce in 2005, up from current levels just above $420 and near a peak achieved late last year.

"That is because of contin-uing instability, geopolitical reasons, especially the situ-ation in Iraq, and also the US economy with the dollar weakening," he said.

That would result in a domestic gold price of around R86 000 per kg, compared with just over R82 000 currently and a range of around R100 000-R75 000 last year. Gold production, however, could fall further if the rand extended its three-year march higher, but Conradie said no estimates were available under those scenarios.

Conradie sees the long-term downward trend continuing, with production down by 4.4% to 350 tonnes by 2008, when he projects the local gold price slipping to R80 000.

It would take a gold price of over R100 000 to significantly stem the decline, he added.

South Africa's share of global gold production has shrunk to under 15% from 27% in 1993, but the country still dominates the world in terms of reserves - underground deposits yet to be tapped - with 40%.

The bulk of those deposits, however, would only be economical if local gold prices doubled to R150 000 and above.

- Reuters

http://www.dailynews.co.za/index.php?fSectionId=500&fArticleId=2378697

very good article, SA supply is a key variable and with low Rand POG production is likely to decline further.

Just to follow up on GBN insider ownership, Rob Still & S Gold held over 12% of fully diluted shares as of the 4/30/04 proxy:

__________

"Robert G. STILL

Director

Sandton, Gauteng, South Africa

Since August 2003 Nil (4)"

Footnote (4)

(4) Mr. Still has an indirect interest in a trust which is associated with Ballottine. Ballottine holds 12,330,500 shares of the Company as at April 30, 2004.

http://www.sedar.com/csfsprod/data46/filings/00650051/00000001/m%3A%5CBETTYC%5CSEDAR%5CGBG%5CYE%5CSE.... page 5

_________

In addition, S Gold/Still also have the 5.5M warrants that expire on 1/31/05. It will be very interesting to see whether Still/S Gold sold some of these shares in 2004 and what insider position they maintain per the 2005 proxy.

If they sold no shares and exercise all their warrants, then they will own 17.8% of fully diluted GBN shares.

SI Posts referred to in deleted post 264

Message In Reply To:

Amarksp,

Speaking of consolidating posts - that was a good exchange you had with Russ Winter on SI regarding GBN and ANO. Going to have to consolidate those for myself.

_________________________________________

To: Taikun who wrote (33387) 12/14/2004 8:03:48 AM

From: russwinter Read Replies (1) of 34010

Good synopsis, and would add that one factor required to get more longer term institutional holdings is size (a threshold), and liquidity. Even the best advanced stage companies are just too small, and too far under the radar screen. That means buying interest will only come from the "gold bug community", as in the people on this board, and that can be very fickle.

If they aren't going to be munched by majors or mid tiers, then there may be something to be said for merging among juniors, except when you see it happening as in the ANO and GBN models, it doesn't seem to work either. In theory it makes the capital raising task a bit easier, and starts to hit the size and liquidity requirements to attract institutions. The success of AGI came because they were able to get NGT-AGI merged before NGT could overly dilute the situation. Then McCluskey did a superb job of financing at good levels and placing with institutions, so an excellent model of how to do it. When you look at the real companies in the sector that are attempting to get into production and become mid tiers, you see them distracted and often overwhelmed by development issues. Witness how slowly the MFN, GBU, MRB, MNG, AGT stories are evolving, broken records, and like watching paint dry. I find juniors going it alone and developing mines to be a flawed approach. Maybe someone will prove me wrong, but I'm skeptical.

I've been going off on the liquidity threshold and munch issues for several years now, but nothing seems to happen. I generally consider management (including majors) throughout the whole mining sector to be rather poor. Therefore my attitude has really changed toward juniors, I'm no longer a permanent or long term holder. To me they are nothing more than trades, to be bought when the retail buyers get fickle. Then during the periods when I get more aggressive, I can hope that maybe something I own gets munched for a decent premium. Or maybe something I don't own gets munched and sets off a good sector rally. If not, as the retail crowd comes back in, I just distribute. Scaling in and out has been a pretty good approach since the fall 03 blowoff peak.

_________________________

To: loantech who wrote (33618) 12/27/2004 11:57:05 AM

From: russwinter Read Replies (3) of 34010

I mentioned the ones I own or use actively. You must understand that I'm very price and sentiment sensitive (fearless when blood runs in the street) and these are very volatile stocks, they can move 10% in one day. It's really like buying a call option, but without the time decay (usually), so you have to be lucky and a good timer (why I use the Amex names) . For several years 00-03 I was obsessed with these stocks, went to shows, meet or called managements personally, subscribed to the hand full of people who followed it (like Claude for one), started this thread. I'm no longer that way, just don't devote as much time to it, am more strategic. Even though I consider myself extremely bright, here I had to be reminded of how royalities are priced into cash costs,

http://www.siliconinvestor.com/readmsg.aspx?msgid=20890189

so there you have it. I just don't know if am really a great (OK, I suppose) source for individual small cap stock picks. Some of these companies are hard to figure, plenty of land mines. I do know what I like and don't like is about all, and I see a sentiment opening now to pick up some of the better juniors.

So caveat emptor:

AGT: Speculative, seems like could be junk? Suppose I could be convinced otherwise.

AZK: don't know the story that well.

CBJ: not a fan of mgt, seems overvalued.

DEZ: Very interesting, some good pros and some cons, one I might use at the right moment.

EGO: kind of story I like to play, seems a tad overvalued because of it's inclusion into the HUI?

GBN (and ANO): I'm using on a price basis; bot at 1.21, not playing for huge upside though. Think ANO could be a big home run. Have to hold my nose because of Hunter-Dickinson though.

NTO: I bought this cheap, two bucks, and am going to play aggressively.

NXG: I was picking up a modest position in this up last week at 1.57. Won't be overly aggressive about upside targets.

NG: I used aggressively when it was being given away last year. I'm now out on a price basis.

QEE: Seems too high cost, potential problem for small caps, like AGT?

RIC: Don't know the story well enough to comment.

AUY: Interesting play, all their mines are low capex, may be a real story in the making with luck. Might be priced fairly right here though?

KGC: Major, and too pricey. I have a company I'd like them to munch.<g>

JAG: don't know story, don't tend to use Cdn llisted only names anymore.

_____________________

To: seventh_son who wrote (33918) 1/14/2005 8:48:31 PM

From: jackjc Read Replies (1) of 34010

Agree Russ, have been avoiding H/D stocks for that reason

for last couple yrs, GBN was one of my fundies for yrs

but now hold only the .33 pieces from early days.

Don't go to the meetings anymore. Have better things to do.

_______________________

To: russwinter who wrote (33917) 1/14/2005 11:36:52 PM

From: amarksp00 Read Replies (1) of 34010

Well, let me chime in on H-D (GBN & ANO)...

GBN and ANO offer the best exposure to SA than anything else, period. Both are undervalued and score well using my MCPRO metrics, so I own them both. Both should be owned by any gold investor that desires exposure to SA in their portfolios.

If and when SA stocks come back into fashion via an increasing POG of SA Rand 95,000/per kg, then GBN will outperform all HUI stocks substantially.

In regard to ANO, it will acquire producing SA gold/plantinum properties at bargain prices in the near future and I believe its upcoming listing of the SA stock exchange will show that SA investors believe it is way undervalued.

__________________

To: jackjc who wrote (33921) 1/15/2005 7:15:57 AM

From: russwinter Read Replies (2) of 34010

Jack, I haven't been avoiding HD of late. I have good positions now in ANO and GBN bought on avg slightly above these 1.10-1.15 levels, and am prepared to buy more on stinky bids below that. I agree with the cons expressed here that HD mgt tends to be self serving, and the stock seems poorly placed and held, but they've also make shrewd deals on their properties, and now the market values everything nominally, discounting I'm not sure exactly what.

Setting aside SA in the case of GBN, they have HL taking them into low cost production at Ivanhoe, it's permitted, and GBN will get 100,000 oz, generating (including a royality) about $35m cf a year at current POG. Plus it's quite expandable. When I calculate shares based on what's in or near the money, and the 5.5 m wts, I get a mkt cap of $108m @ 1.12 US. They have cash of $23m, so EV is $85m. That's way too low for $35m cf in Nevada starting in 07, and Burnside to boot.

Are you in Vancouver now, probably not huh, winter? I will likely be coming up for the gold show there next week, perhaps we can hook up, been awhile, and might be a chance to get to the bottom of some of this. You asked me about QRL, seems a little too high cost, although not an expensive stock at all. I've always leaned toward sub-200 production prospects, just my philosophy, and right now the market isn't valuing even those for much. BTW, the recent cvt bond financing AGI just did is exactly the way to do it now.

____________________

To: jackjc who wrote (33931) 1/15/2005 10:48:59 AM

From: russwinter of 34010

I was in early on at under a buck, and let it go (a little early, closer to two bucks than three) back in the fall of 03 run up on a valuation basis. And here we are a year plus later, they've made some gradual progress and are closer to their objective, and it's basically at early 03 valuations (when POG was $350), bizarre. Look at where everybody bought (see high volume on chart) though, explains alot. Is that GBN's fault?

GBN&t=2y'>http://finance.yahoo.com/q/bc?s=GBN&t=2y

__________________

To: amarksp00 who wrote (33923) 1/15/2005 11:02:19 AM

From: russwinter of 34010

Here's some stock performance that is really encouraging even if I missed my entry point, $1.60 when trading on the Amex. It shows that money will respond when good news breaks on these delay stories.

http://yahoo.reuters.com/financeQuoteCompanyNewsArticle.jhtml?duid=mtfh13578_2005-01-14_17-52-17_n14....

http://finance.yahoo.com/q/bc?s=NSU.TO&t=1y

Unfortunately, the pattern has been to overreact to the poor news, and again overact to the upside on better news, as I'm not sure much has changed with NSU except the stock price. There's probably a lesson to be appled from this to stocks like MRB, GBN, CLG, MNG who have been ravished by similiar monkey wretches.

_____________________

To: seventh_son who wrote (33934) 1/15/2005 11:35:07 AM

From: russwinter Read Replies (1) of 34010

Yes, but I don't think they will do PPs on GBN and ANO now will they, they have the cash. At any rate I plan on having a litle chit chat with them (the highest up person I can botton hole) at this show in Vancouver next week, and as Jackj has seen in the past, I don't fuck around or mince words in these conversations. I will report back here afterwords.

___________________

To: russwinter who wrote (33926) 1/15/2005 11:31:28 AM

From: seventh_son Read Replies (2) of 34010

>The question on them though is why are their stocks always so depressed, tending to have weak shareholders who unload in droves at what seems like the wrong time, and buy (in the case of ANO) at the wrong price and time?

I think that I might have an answer to that. I've seen that they pay newsletter writers in stocks and warrants just at the time that action starts to occur on their properties. The newsletter writers are very biased, excited about their own profits, and concerned to keep the stock prices up when they get high, maybe ahead of themselves. I saw outrageously zealous recommendations on both ARQ and NDM from one writer, practically promising that the stocks would double in short order, when the stocks had already made huge gains and were topping. Well, I imagine that by that time people who got in on cheap warrants and private placements earlier started to cash them in, the stocks started to fall, and eventually people who only bought in only because they thought that they would make easy money became totally disillusioned; maybe they were in over their heads but only bought because they thought they were a "sure thing". Of course the resulting withdrawal is all a prelude to the stock becoming undervalued and the people who have unloaded their placement stock to reload again on another private placement at low prices. People can make good money on H-D stocks, but I think that it's harder for those buying the stocks outright and sort of paying a tax to those who are getting in on cheap placements and diluting the stocks.

___________

To: seventh_son who wrote (33934) 1/15/2005 12:02:47 PM

From: russwinter Read Replies (3) of 34010

Added thought on GBN. Per the annual

http://www.sedar.com/csfsprod/data46/filings/00650304/00000001/m%3A%5CCAROLW%5CGBG%5CAIFMay2004.pdf

"beneficial security holdings of directors and officers was 1,011,258 shares (1.2% of outstanding)and 3,785,000 options". So they really aren't much of a stakeholder here, or don't especially have the shares to mount a defense. However if someone wanted to raid them or take a run at them (certainly more than feasible at today's valuations, and they way it's been neglected) would it have to be friendly because they need the HD intellectual capital and project knowledge? I wonder, although perhaps HL could do it, because they have the knowledge (and some shares already), at least in terms of Hollister.

Same thought on CLG, only about a million shares held by management, clearly something KGC is taking slow advantage of. Does KGC have the project knowledge, or can they attain it, by being such a large shareholder now?

______________

To: seventh_son who wrote (33934) 1/15/2005 11:35:07 AM

From: russwinter Read Replies (1) of 34010

Yes, but I don't think they will do PPs on GBN and ANO now will they, they have the cash. At any rate I plan on having a litle chit chat with them (the highest up person I can botton hole) at this show in Vancouver next week, and as Jackj has seen in the past, I don't fuck around or mince words in these conversations. I will report back here afterwords.

___________

To: russwinter who wrote (33937) 1/16/2005 2:03:52 AM

From: amarksp00 of 34010

good discussion on GBN & ANO. too busy with year end payroll and tax return preparation to contribute much...

few thoughts, GBN is owned more than 1.2% by insiders, do not believe SouthGold investors (specifically Director Rob Still) is adequately disclosed. believe Rob Still owns over 3% of GBN personally but it may somehow be in a trust or otherwise not reported properly.

the key with GBN is to watch for those 5.5M warrants being exercised by Jan 31. will be interesting to see whether Still & SouthGold exercise with their own cash (SouthGold shareholders are wealthy enough to do so, IMO) and do not sell into the market.

read the i-hub board... at Burnstone, appears water will not be available for Burnstone production until 2007, can start construction however with available water. Burnstone water is a great question to ask at the meeting.

in regard to ANO, note that insiders have exercised their options with their own cash and have NOT sold into the market. ANO is the most prevalently insider owned of HD companies, that should tell you something, it is HD management's favorite HD company followed by GBN and next is Taseko in that order.

_______________

To: russwinter who wrote (33937) 1/16/2005 11:32:58 AM

From: amarksp00 of 34010

Also, in regard to GBN, a great question would be when GBN plans to start more drilling on the Ivanhoe property. Specifically, what is GBN doing on that N-NW vein.

"A re-interpretation of exploration information for the eastern half of the property resulted in the recognition of a second major structural trend on the Ivanhoe property. The north-northwest trend of the newly identified major fault structures is the same as the principal ore-bearing structure at Ken Snyder and other mines in northeastern Nevada. This new structural trend provides outstanding potential to find significant, additional high-grade gold vein systems."

Consolidate Posts 255-262

board clutter...

Great Basin Signficantly Increases Burnstone Gold Resources

Tuesday January 18, 10:00 am ET

________________

M&I up to 7.2M ounces

==============================================================

Hi Mark,

If you have the time, may I ask how you arrived at that total?

Posted by: ewallman

In reply to: amarksp who wrote msg# 254 Date:1/18/2005 11:05:38 AM

Post #of 262

Well, well, that is good news. I like that it is now all considered one deposit.

Posted by: amarksp

In reply to: basserdan who wrote msg# 255 Date:1/18/2005 11:09:11 AM

Post #of 262

Use 350 cutoff (actualy I believe 325 cutoff would be more accurate, but not listed in table)

From the table (near the bottom):

350 45,763,000 4.93 7,246,000

Then I rounded to 7.2M ounces

_____________________

Be advised, GBN will only own 80% after required BEE deal, so the real number to use for MCPRO is 80% = 5.8M ounces.

Posted by: basserdan

In reply to: amarksp who wrote msg# 257 Date:1/18/2005 11:12:20 AM

Post #of 262

Thank you Mark.

You are the man.

Iyo, will their current water resources be sufficient?

Posted by: amarksp

In reply to: basserdan who wrote msg# 258 Date:1/18/2005 11:21:22 AM

Post #of 262

Still trying to get water issue answered. Per their tech report filing, adequate water to construct the mine but not adequate water to go into production until 2007 or so.

New water pipeline to be built by SA Government still in design phase. As soon as this pipeline approved for construction, likely in late 2005, would think GBN could start Burnstone capex. See prior posts in this regard.

Posted by: ewallman

In reply to: amarksp who wrote msg# 259 Date:1/18/2005 12:46:44 PM

Post #of 262

I am fairly confident with also throwing in the 'inferred' number at this point. Given the size of the resource and drilling success there is no reason to believe it is not there. And the grade is actually much higher on the inferred portion.

M&I&I @350 = 11.9M ozs

One hell of a deposit...

Posted by: amarksp

In reply to: ewallman who wrote msg# 260 Date:1/18/2005 1:10:34 PM

Post #of 262

Well, I am a bit more confident than you..., still using 12M

Believe GBN has 12M ounces after the 20% BEE deal and HL joint venture as follows:

13.8M M&I+Inferred ounces at Burnstone = 11M ounces post BEE

1.5M ounces at Ivanhoe = 1M ounces after HL (includes HL royalty payment to GBN)

11M Burnstone + 1M Ivanhoe = 12M total ounces of which 5.8M ounces are M&I

Using the above, my MCPRO calcs show currently GBN trading at:

$18.36 Market Cap per M&I ounce

$8.87 Market Cap per Total Resource ounce

GBN remains very undervalued relative to its peers... GBN would be a much better take over speculation if they could somehow get more annual production out of Burnstone, e.g. over 500,000 ounces of production per year... Appears the Burnstone thin reef mine does not lend itself well to mechanization, remains largely labor intensive and cannot be ramped up to larger annual production easily...

Posted by: huesos

In reply to: None Date:1/18/2005 1:39:50 PM

Post #of 262

Too much for me, I'm trying to get in now at 1.20 limit. I've got 5 years to wait and I like my chances.

Nicaragua Article

http://www.foxnews.com/story/0,2933,144636,00.html

Nicaragua's Crisis

Tuesday, January 18, 2005

By Stephen Johnson

When Nicaraguan citizens defeated communist comandantes at the ballot box in February 1990, it was the dawn of democracy in a country that had rarely known it and the triumph of elected civilian rule in a region long plagued by dictators.

Yet now, just as Nicaragua is set to receive a Millennium Challenge Account (search) grant rewarding anti-corruption efforts, greedy politicians are poised to roll back the country’s democratic gains, depose an elected president and install a kleptocracy -- a state based on stealing from the governed -- with a convicted felon and former dictator in charge.

The thievery began in the spring of 1990. Before turning over power to democratically elected President Violeta Chamorro (search), the outgoing Sandinistas (search) enacted laws protecting property seizures estimated at $300 million to $2 billion -- including luxury homes, office buildings and ranches. Comandante Daniel Ortega (search) reportedly padded his personal accounts with money from the Central Bank of Nicaragua.

President Chamorro declined to repeal the so-called piñata laws (search) or seek remuneration from the Sandinistas, supposedly to keep peace. Thus, her successor, Arnoldo Alemán (search), may have considered her actions a free pass to imitate the Sandinistas. During his term from 1997 to 2001, he allegedly used his office to transfer more than $100 million into Panamanian accounts.

Before leaving office, Alemán reconciled with his former adversary Daniel Ortega, then leader of the Sandinista bloc in the National Assembly. The two collaborated to amend the constitution to pack the Supreme Court, Supreme Electoral Council and Controller General’s Office with cronies, as well as award themselves parliamentary seats and immunity from prosecution of any crimes. Despite public outrage, supporters in the National Assembly passed these changes.

Elected on an anti-corruption platform, President Enrique Bolaños (search) obeyed popular calls to investigate Alemán, even though Alemán was a member of the same Liberal Party. As his attorney general gathered evidence, some 500,000 citizens signed a petition to lift Alemán’s parliamentary immunity so he could stand trial. He was convicted in December 2003 for embezzling and defrauding the government.

Since then, Alemán’s Liberal Party friends have been bargaining away the government to Sandinista Assembly members to secure the ex-president’s freedom from Sandinista judges. Last year the dominant Liberal and Sandinista blocs voted to obstruct all of President Bolaños’ reforms. Now they are attempting to amend the constitution to take away his powers to appoint cabinet officials -- a change considered unconstitutional by the Central American Court of Justice.

On Jan. 7, Alemán and Ortega released a joint public letter representing themselves as National Assembly leaders, even though Alemán has no legal status as a convict and Ortega is an un-elected delegate. They argued for the passage of their proposed amendments “to resolve grave social problems of employment, health, and education and guarantee peace.” Two days later, Daniel Ortega appeared on television with the head of the Catholic Church in Nicaragua and vowed to “put an end” to the Bolaños administration.

Cardinal Miguel Obando y Bravo -- once a defender of the poor who denounced the Sandinista dictatorship in the 1980s -- now figures in Nicaragua’s problems, having tacitly supported the Alemán-Ortega pact.

None of this sits well with the Nicaraguan public. A poll published on Jan. 11 showed 77 percent of respondents opposed both constitutional amendments and the president’s impeachment. But public sentiment doesn’t matter to parliamentarians who don’t represent districts and owe their loyalty solely to party bosses.

These deputies weren’t worried by stern warnings from the European Community, the Central American Court of Justice, the Organization of American States (search) (OAS) and Central America’s other presidents -- all of which Alemán and Ortega have ridiculed as meddling in Nicaraguan affairs.

In a roller-coaster twist, Ortega appeared with Bolaños on Jan. 12 to sign an agreement on behalf of the Sandinista bloc to let the president finish his term. To his credit, Cardinal Obando acted as guarantor. Whether Liberals will honor it and how long it sticks is anyone’s guess.

For its part, the Bush administration has suspended the visas and frozen the assets of Alemán and a business associate. But that is not enough. It should revoke the visas of any deputies who help defeat anti-corruption efforts, support other nations if they invoke the Inter-American Democratic Charter in the OAS, and withdraw grants and credit if laws are manipulated to overthrow an elected president.

Too much blood, sweat and tears were invested in helping fragile Central American democracies flower in the 1980s. America should not sit idly by as self-serving autocrats destroy a people’s aspirations for self-rule and prosperity.

Stephen Johnson is senior policy analyst for Latin America at The Heritage Foundation.

2004 New Tax Law Highlights

http://amarks.homestead.com/TaxLawCh.html

Great Basin Signficantly Increases Burnstone Gold Resources

Tuesday January 18, 10:00 am ET

________________

M&I up to 7.2M ounces

VANCOUVER, British Columbia--(BUSINESS WIRE)--Jan. 18, 2005--Ronald W. Thiessen, President and CEO of Great Basin Gold Ltd. (TSX:GBG - News; AMEX:GBN - News) is pleased to announce the results of a new overall mineral resource estimate for the Burnstone Project, located in the northeastern part of the Witwatersrand Basin, 80 kilometres southeast of Johannesburg, South Africa, where the Company has drilled 120,000 metres of core in 187 holes over the past twenty-four months. The current estimates, based on drilling to November 2004, show increases in the size and classifications of the gold resources at Burnstone.

The Burnstone goldfield is defined by an 18 kilometre long, northwesterly trending mineralized corridor developed within the Kimberley Reef, one of four main gold-bearing units in the Witwatersrand Basin. At Burnstone, the central portion of the gold corridor has been uplifted by two northwesterly trending sub-parallel faults and as a result, a significant portion of the deposit areas along the trend occur at relatively shallow depths of 250-750 metres. Drilling by Great Basin has also revealed that several of the gold-bearing areas are continuous, for example an area at the southern edge of the gold trend, previously known as Area 4 has been found to be contiguous with the Area 1 gold deposit. The Company's technical experts now suggest that the gold occurrences at Burnstone are all part of one deposit, with several areas of gold concentration. As a result, the current mineral resources for the entire Burnstone Project are now tallied together. The estimated mineral resources, diluted over a 1 metre width, are tabulated below:

-----------------------------------------------------------

-----------------------------------------------------------

Mineral Resources - Burnstone Goldfield

-----------------------------------------------------------

Cut-Off Grade Contained

Category (cmg/t) Tonnes (g/t) Gold (Ounces)

-----------------------------------------------------------

Measured 300 53,866,000 4.53 7,840,000

-----------------------------------------------------------

350 38,278,000 5.08 6,248,000

-----------------------------------------------------------

400 30,414,000 5.53 5,404,000

-----------------------------------------------------------

-----------------------------------------------------------

Indicated 300 10,325,000 3.82 1,268,000

-----------------------------------------------------------

350 6,896,0000 4.50 998,000

-----------------------------------------------------------

400 6,157,0000 4.58 907,000

-----------------------------------------------------------

-----------------------------------------------------------

Total M+I 300 64,192,000 4.41 9,109,000

-----------------------------------------------------------

350 45,763,000 4.93 7,246,000

-----------------------------------------------------------

400 36,571,000 5.35 6,311,000

-----------------------------------------------------------

-----------------------------------------------------------

Inferred 300 16,353,000 9.33 4,905,000

-----------------------------------------------------------

350 13,965,000 10.37 4,655,000

-----------------------------------------------------------

400 13,192,000 10.76 4,562,000

-----------------------------------------------------------

-----------------------------------------------------------

A Pre-feasibility Study was completed in 2004 for the Area 1 deposit, which comprises approximately 64% of the measured and indicated resources totalled above at the 350 cmg/t cut-off. The study indicated a strong internal rate of return for a 1.5 million tonnes per year underground operation, producing an average of 236,000 ounces of gold annually. With the significant increase in the estimated resources from the current study, it is anticipated that a larger operation could be developed. The Company intends to proceed with engineering studies focused toward completion of a feasibility study for the entire project.

South African consulting firms Global Geo Services (Pty) Ltd. ("GGS") and GeoLogix Mineral Resource Consultants (Pty) Ltd. ("GeoLogix") completed the current estimates. Ordinary Kriging and Inverse Distance to the power of three methods were used to estimate the resources in five distinct geo-zones, based on a database of 191 holes and a total of 544 deflections off the master holes (providing 735 valid intersections) drilled by Great Basin and previous operators. The resource classifications were defined by the range of a variogram (a graph which describes the variance of the samples in a deposit as a function of distance) determined from the drill hole data. The measured resources are defined as up to 50% of the variogram range, the indicated resources are up to the range of the variogram and inferred resources are beyond the variogram range, all within geo-zone boundaries.

Rigorous QA/QC procedures, designed and supervised by qualified persons, are integrated into Great Basin's exploration programs. The primary analytical facility for the Burnstone Project is SGS Lakefield Research Africa (Pty) Limited in Johannesburg, South Africa. Check assays are done by Acme Laboratories in Vancouver, BC.

Eugene Siepker, M.Sc., Pr.Sci.Nat., of GGS, and Deon van der Heever, B.Sc., Pr.Sci.Nat., of GeoLogix, independent qualified persons as defined by National Instrument 43-101, are responsible for the resource estimates. A technical report providing further details on the parameters and methodology used for the resource estimates, as well as sampling and quality control procedures, will be filed on www.sedar.com in 30 days.

Great Basin is a mining exploration and development company with advanced stage gold assets on the Carlin Trend in Nevada and the Witwatersrand Goldfield in South Africa. For additional details on Great Basin and its gold projects, please visit the Company's website at www.greatbasingold.com or contact Investor Services at (604) 684-6365 or within North America at 1-800-667-2114.

ON BEHALF OF THE BOARD OF DIRECTORS

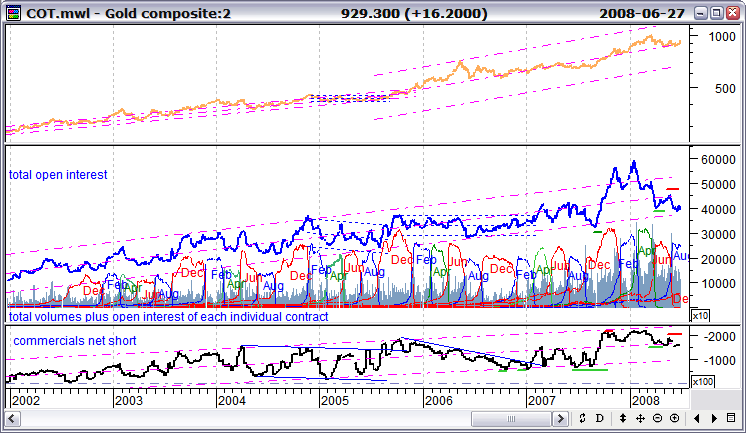

thanks Louis, would you please post both of these Gold charts each week on this board...

As Large Specs get longer & longer (increasing their contracts), price of gold goes up

As Large Specs start liquidating their contracts/positions, POG goes down

______________

Or one can use the Commercials instead of Large Specs and exact opposite of above

Nice Gold COT commercial liquidation... compare to $Gold

............>

what do you know about Guinea and Guinor...?

http://www.guinor.com/company_documents/presentations/031104/StoraksjekveldNov04.pdf

do you have knowledge of Guinor company management and operations?

Thanks!

Nicaragua article

washingtonpost.com

Narrowly Saving Nicaragua's Democracy

By Marcela Sanchez

Special to washingtonpost.com

Thursday, January 13, 2005; 10:30 PM

WASHINGTON -- Wednesday's surprise agreement between Nicaraguan President Enrique Bolaños and his archrival, Sandinista leader Daniel Ortega, seemed to have saved democracy in that nation. By Thursday though, new questions were raised about whether Ortega would keep to his end of the bargain.

The United Nations-brokered agreement is supposed to ensure that Nicaragua's elected president could keep his authority. Ortega and former President Arnoldo Aleman have been trying to engineer a constitutional overhaul that would gut the powers of the presidency. Ortega and Aleman should not get away with their legislative coup.

Unlike other recent threats to democratic order in the region, Nicaragua presents a very clear-cut case of a president under siege. Yet as the crisis dragged on for months, few regional leaders mustered the courage to throw their support behind Bolanos and unequivocally condemn his adversaries.

Bolanos swept into office three years ago promising to eradicate corruption in the hemisphere's poorest nationafter Haiti. Not surprisingly, those accustomed to manipulating Nicaragua through cronyism and corruption felt directly threatened by his reforms and hit back hard.

Up until early Wednesday, Ortega, Aleman and their henchmen in the National Assembly seemed intent on taking Bolanos down -- and democracy with him. The agreement does not eliminate the proposed constitutional changes. But it makes the implementation conditional on consensus from executive. Most notably, the agreement gives Bolanos a place at the table as an equal to his adversaries, rather than allowing Ortega and Aleman to hold "a gun to his head'' as they had been doing, said Nicaraguan Foreign Minister Norman Jose Caldera in an interview from Managua. He said pressure by the international community has been a crucial factor.

But in truth, this has not been one of the regional leaders' finest hours. As the crisis worsened last week, the best response the Organization of American States could cobble together was a tepid posting on its Web site late Friday stressing the separation of powers as an "essential element'' of democracy. On Tuesday, the OAS Permanent Council pledged to continue watching developments "very closely.''

Why is watching very closely, from the comforts of the OAS headquarters in Washington, the best this hemispheric body committed to defend democracy can do?

It is not as if leaders haven't been put in a similar situation before. It was, in fact, an OAS vote on June 23, 1979, calling for the "immediate and definitive replacement'' of Anastasio Somoza's "inhumane'' regime, which made Somoza's departure from Nicaragua three weeks later certain.

More often than not, circumstances are not as black and white in Nicagagua. Political, economic and strategic interests all combine to make the OAS demure. This is certainly the case in Venezuela, and perhaps more recently Ecuador, where those playing fast and loose with sacred divisions of power are the presidents themselves. Yet Presidents Hugo Chavez of Venezuela and Lucio Gutierrez in Ecuador retain some semblance of moral and democratic legitimacy as the popularly elected leaders of their countries and, in Chavez's case, his appeal to his countries' traditionally neglected citizens.

But perhaps the inability to be decisive has more to do with OAS internal battles than anything happening in Nicaragua.

Well-placed OAS diplomats told me that most member countries hoped Bolanos wouldn't go as far as invoking the Inter-American Democratic Charter, which puts respect for democratic order as a precondition to acceptance in the community of nations in the Americas. They said the charter was not meant for this kind of internal disagreement. (It is hard to imagine what else it is good for.)

Other OAS diplomats said they feared there was a backlash against Bolanos in order to spite the Bush administration, which holds the Nicaraguan president in high esteem.

This failure to appreciate a democratic crisis because of animosity toward the United States reinforces the notion in Latin America that international bodies such as the OAS are toothless tigers.

Ortega has used the fear of U.S. interference to try to scare Nicaraguans to his side. In the end, it was decisive involvement from the U.N. -- not the United States or the OAS -- that tried to put a hold to Ortega's ambitions. Whether it is successful is still an open question.

Marcela Sanchez's e-mail address is desdewash@washpost.com

EDV annual report now out...

http://www.sedar.com/csfsprod/data51/filings/00729294/00000001/p%3A%5CSEDAR%5CEMCC%5CGlos%5CAnnu.pdf

EDV has changed investment strategy to include energy investments in coal, oil & gas, & uranium and seems to be emphasizing base metals more than historically (when concentrated on precious metals).

"We nonetheless retain core merchant

banking positions in Bema Gold, Bolivar

Gold, Century Mining, Northern Orion,

Silver Wheaton and Wheaton River

Minerals, among others.

During the year, we broadened our

investment capital base by adding a number

of special situations in coal, platinum and oil

and gas to our predominately metals-based

core positions"

___________________

trying to do something about that discount to NAV as well..., this discount to NAV has been averaging over 25%

Our share price remains at a discount to

net asset value (NAV) per share. The Board

of Directors is addressing this situation and

considers the discount to be unjustifiable.

Endeavour Mining’s share price has yet to

reflect the company’s consistently high level

of profitability, increasing net asset value and

exceptional long-term growth prospects.

In the meantime, we have taken the

following steps to enhance shareholder

value:

Adoption of a dividend policy

Our semi-annual dividend is set at

CDN$0.035 per share (CDN$0.07

annually).

Posting of monthly NAV per share

Timely NAV per share information is now

available on our website. It supplements

our quarterly earnings results, allowing

investors to better assess the company’s

financial performance.

Graduation of common shares to TSX

Listing of our common shares and

warrants on the Toronto Stock Exchange

(TSX), the premier international mining

stock exchange, maximizing their visibility

and liquidity.

Evolving our growth strategy

Our continued financial achievements

confirm the effectiveness of our merchant

banking business strategy. They also give us

the confidence and the financial resources

to augment our strategy to take advantage

of growth opportunities in a broader range

of natural resource sectors.

agree: "if they don't hit on the first pass it could really collapse."

CKG has grown into one of my larger positions, got 2K shares from the Francisco acquisition and have added. May sell some right before the drilling results come out to recover all my capital, may not take but 20% of my shares...

Interesting blurb on the Nicaragua land holdings which appears relevant to RNC. In regard to MFL, believe Bailey may well do a spinoff similar to Francisco/CKG by selling Dolores and keeping MFL with its other properties.

nice website...

Just patiently waiting... am not much of a trader of stocks with good fundamentals, crosses or no crosses, up or down or sideways matters not...

Was impressed with that freemarket video clip. Martin looks good, very articulate, and handles himself well in front of the camera, valuable skills... He seems to walk the walk rather than talk the talk... We'll see, but my gut instinct is to trust the guy and I have spoken with him 3 times over the past 12 months (and with his financial staff dozens of times) while the stock was going down relentlessly...

Go to minute 6:40 of that video and listen through minute 9:00. Hope Martin is walking and not talking because if RNC has 1g/ton at new Bonanza discovery, then we are talking about 1M+ ounces of very economic gold ounces per my correspondence with Claude C., Claude wants to see .9 gram/ton on these future drill results. And, more importantly, RNC has the expertise to get it out of the ground itself rather than having to wait for third party feasibility consultants and mine engineers... If this new Bonanza open pit proves up, we will likely see 100K additional ounces being produced within 2-3 years (e.g. 1M ounces over 10 year mine life=100K ounces/yr)... That would give RNC annual production over 300K ounces, a true mid-tier.

Nicaragua Politics - articles

Would appear all Nicaragua political problems are resolved until at least Jan 2007 when new president is elected... Nice survey results indicating 77% of the Nicaraguan people are in favor of this outcome...

_______________

Nicaraguan leaders try to defuse crisis

Managua, Nicaragua - Sandinista opposition leader Daniel Ortega and ex-President Arnoldo Aleman agreed on Wednesday to support Nicaragua's right-wing President Enrique Bolanos to try and defuse a looming constitutional crisis.

The leftist Ortega signed a "governability agreement" with Bolanos pledging to recognise the validity of his government until the president's term ends in January 2007.

Aleman backed the accord, bringing on board the nation's main political parties.

"We have overcome the threats against the tranquillity of the nation," Bolanos said. "We have saved ourselves from falling into the abyss we were heading for."

In a tangled story of political infighting Bolanos had accused the Sandinistas and supporters of Aleman of plotting a constitutional coup against him.

In a tangled story of political infighting, state regulators have said Bolanos failed to disclose the origin of funds he raised during the 2001 election campaign, prompting corruption allegations by Bolanos' political rivals. He has refused to ratify constitutional changes passed by lawmakers.

The agreement signed by Bolanos, Ortega and leaders of Aleman's party calls for consensus on the reforms before they can take effect. It also calls for professionalizing the judicial and electoral systems and strengthening health, education and labor rights.

Aleman, Nicaragua's president from 1997-2002, is in home detention, serving a 20-year sentence for corruption.

Bolanos was a member of Aleman's Liberal Party and became his vice president, but he later led a drive to prosecute Aleman for corruption.

Ortega, who was president of Nicaragua's Marxist-inspired revolutionary government from 1979 to 1990, said he was committed to "reconciliation and peace".

He later met with Aleman at his home to finalize the agreement. Liberal Party leader Rene Herrera, a lawmaker who was at the meeting, called the agreement an "historic step for the country toward peace".

_________

January 13, 2005

Nicaraguans Back Bolaños In Political Crisis

(Angus Reid - CPOD Global Scan) – Many adults in Nicaragua reject a former president’s threat to "put and end to the current administration," according to a poll by M&R published in La Prensa Gráfica. 77 per cent of respondents disagree with the statement by Daniel Ortega of the Sandinista National Liberation Front (FSLN).

In 2001, Enrique Bolaños—candidate for the ruling Constitutionalist Liberal Party (PLC)—was elected with 56.3 per cent of the vote over Ortega. The president lost the support of the PLC in January 2002, when his government decided to take legal action against former president Arnoldo Alemán. Last year, Alemán—who governed the country from 1997 to 2002—was sentenced to 20 years in prison for fraud, money laundering and embezzlement.

In November, PLC and FSLN lawmakers at the National Assembly introduced a series of constitutional reforms that restrict presidential powers, by allowing the legislative branch to ratify, summon and dismiss government ministers. On Jan. 6, the Central American Court of Justice (CCJ) unanimously ruled that the Nicaraguan legislative branch must cease all procedures to go ahead with the proposed amendments. Bolaños originally asked the CCJ to review the situation last month.

Former presidents Ortega and Alemán issued a joint statement condemning the CCJ’s decision. 77 per cent of respondents disagree with their rationale.

Polling Data

Former president Daniel Ortega has threatened to "put and end to the Bolaños administration." Do you support or oppose this?

Support

16%

Oppose

77%

Unsure

7%

Former presidents Daniel Ortega and Arnoldo Alemán issued a joint statement condemning the decision of the Central American Court of Justice (CCJ). Do you support or oppose this statement?

Support

17%

Oppose

77%

Unsure

6%

Source: M&R / La Prensa Gráfica

Methodology: Interviews to 620 Nicaraguan adults, conducted on Jan. 9, 2005. Margin of error is 4 per cent.

________________

Posted on Thu, Jan. 13, 2005

NICARAGUA

Latin American & Caribbean Briefs

From Herald Wire Services

MANAGUA - President, Sandinistas

ease dispute over power

Nicaragua's leftist Sandinista Front agreed Wednesday to let President Enrique Bolaños finish his term, signing a surprise accord with the president that is designed to end months of conflict between the executive and legislative branches.

The agreement -- signed by Bolaños and Sandinista leader Bayardo Mendoza, and witnessed by Cardinal Miguel Obando y Bravo and U.N. representative Jorge Chediek -- appeared to end a monthslong battle between Bolaños and lawmakers who wanted to curtail the president's powers.

'With the signing of this agreement, we are strengthening the house of peace that is democracy,' Bolaños said in a message to the nation. ``No one beats anyone with this accord. The Nicaraguan people win.'

NEW YORK (ResourceInvestor.com) -- London based metal consultancy GFMS has brushed aside New Year pessimism about the gold price, setting a very bullish average price of $447 per ounce for the first half of 2005 [AU]. GFMS says downside price risk remains limited despite a dramatic decline in net investment demand for gold which slumped to 314 tonnes in 2004 from 900 tonnes a year earlier.

The forecast was contained in a new report issued by GFMS today, and is consistent with the views of key market watchers like Dr Martin Murenbeeld, and recent analysis provided by JP Morgan and ANZ Bank.

http://www.resourceinvestor.com/pebble.asp?relid=7799

THERE'S RNC GOLD IN THOSE HILLS!!

J.R. (Randy) Martin talks about things that make RNC Gold 24 carrot

Audio interview link via David Morgan's website

http://www.freemarketnews.com/portfolio/index.php

Hartman The Dollar and Treasuries

http://www.financialsense.com/Market/wrapup.htm

The record trade deficit took its biggest toll on the dollar with the U.S. Dollar Index falling to 82.20, and today was the biggest decline versus the euro in the last three weeks. The euro added 1.1% to 1.327, the yen gained nearly 1% to 0.981 and the big gainer in the currency pits today was the Canadian dollar with a 1.5% advance to 0.833. The Bloomberg article I mentioned earlier said, “Trade Gap Signals Growth,” but the columnist went on to say that the reported trade deficit “is raising concerns that a weaker U.S. currency may discourage international investors from buying longer-maturity treasuries.” I would have to agree with that comment. Early this morning treasuries opened lower and continued to move lower, but it didn’t last for very long. Right after the initial decline, treasuries were bought right back up to breakeven from yesterday’s close.

I very much believe there was active intervention to prop-up the treasury debt market because the U.S. Treasury was scheduled to auction $15 billion in 5-year notes today. I have NEVER seen treasuries take a significant decline on a day when the government is conducting debt auctions; it just doesn’t happen! Bonds should have sold off today, especially with all the new Fed-speak about higher interest rates and the horrible trade numbers we got this morning. One of the analysts interviewed by Bloomberg had this to say. “We’ve got a dollar that is weakening and the Fed saying they are going to keep hiking rates so there is no compelling reason to buy Treasuries,” said Jonathan Lee, a fixed-income analyst in London at Barclays. “You can understand why foreign central banks are looking to diversify their portfolios out of dollars.” By the end of the day Treasuries moved marginally higher. You can expect more of the same tomorrow since the Treasury will be auctioning another $10 billion in 10-year TIPS. At this juncture the U.S. Treasury cannot afford a big problem with the dollar or treasuries since they plan to borrow more than $100 billion via debt auctions between now and the end of February. It should get interesting.

With regard to the trade deficit, the fact remains that we are just going deeper into debt to continue buying all the things we need and want. The report showed import growth higher by 1.3% to $155.8 billion, but the big warning comes when we see that exports fell 2.3% from $97.8 billion in October to $95.6 billion in November. This was the first decline we have seen in exports since June 2004. The lower value of the dollar should be making U.S. exports more affordable to the rest of the world, but they’re not buying. Some analysts have suggested that foreigners are pulling away from U.S. products to voice their disapproval of the Bush administration’s foreign policies. Others are saying the huge imbalance with foreign trade indicates the U.S. is simply not up to the competition to produce quality products at a low price. It appears China and other developing countries such as India are taking more than just the “labor intensive” jobs. China is now preparing to make cars for sale in the U.S. The initial production scheduled for the U.S. is 250,000 cars…let’s watch and see how Ford and GM fight back or if they will have to concede sales to the competition.

Alamos Financing Comments

Appears what AGI has done is finance Mulatos mine 100% with this $45M convertible debt. Reviewing RBC analyst report I see $41.5M debt at year end 2005 on their 11/29/04 report and McFarlane had a $45M LT Debt requirement listed on their report dated 10/4/04.

So bottom line, this convertible debt appears to be the previously announced debt needed to finance Mulatos, and NOT new debt.

Now one could argue that straight debt would have been preferable to convertible debt, but that 5.5% interest rate would have likely been over 10% and would have likely required more hedging to obtain straight debt... So net/net this financing appears to be more of a positive fundamentally than a negative.

Now how the market interprets this financing is another matter...

Treasury Auction results, appear worse than expected...

"Jan. 12 (Bloomberg) -- U.S. Treasury notes failed to rise as a measure of demand at the government's $15 billion sale of five- year securities indicated weaker appetite for the debt.

Indirect bidders, the class of investors that includes foreign central banks, won 39.8 percent of the securities, down from 65.8 percent of the previous five-year note sale on Dec. 8. A drop in the dollar against the euro and yen also held back Treasuries.

``Dealers don't like it as they fear that foreign participation in the Treasury market could be slipping,' Rick Klingman, a five-year note trader who heads Treasury trading at ABN Amro Inc. in New York, said of the level of indirect biddders. While it's too early to draw that conclusion, ``the initial reaction is always to sell on a low indirect bidding number,' he said.

The most recently issued five-year note, a 3 1/2 percent note maturing in November 2009, was little changed at 99 3/32 to yield 3.70 percent as of 4:06 p.m. in New York, according to bond broker Cantor Fitzgerald LP. ABN Amro is among the 22 primary U.S. government securities dealers that are obligated to bid at the Treasury's auctions.

The new notes, which mature in January 2010, drew a yield of 3.731 percent, the highest at a five-year sale since June. There were $2.37 worth of bids for every $1 sold, compared with $2.60 at November's sale. The so-called bid-to-cover ratio averaged $2.60 at the past 10 sales.

Today's auction was the first of eight this month and next that government finance research firm Wrightson ICAP estimates will total $133 billion. The U.S. will sell $10 billion of 10- year inflation-linked securities tomorrow. "

AGI halted...

Our fearless board leader in remorse...

http://www.siliconinvestor.com/readmsg.aspx?msgid=20943350

here's the news...

Alamos Gold Inc.-New Issue

15:54 EST Wednesday, January 12, 2005

TORONTO, ONTARIO--(CCNMatthews - Jan. 12, 2005) - Alamos Gold Inc. ("Alamos Gold")(TSX:AGI) has announced today that it has entered into an agreement to sell to a syndicate of underwriters led by BMO Nesbitt Burns Inc. on an bought deal basis $45 million aggregate principal amount of 5.50% convertible senior debentures due February 15, 2010 (the "Debentures"). The Debentures will bear interest at a rate of 5.50% per annum, and will be convertible at the option of the holder into common shares of Alamos Gold at a conversion rate of 188.6792 common shares per $1,000 principal amount of Debentures, which is equal to a conversion price of approximately $ 5.30 per common share. The offering is expected to close on or about February 2, 2005.

The securities offered have not been registered under the U.S. Securities Act of 1933, as amended, and may not be offered or sold in the United States absent registration or an applicable exemption from the registration requirements. This press release shall not constitute an offer to sell or the solicitation of an offer to buy nor shall there be any sale of the securities in any State in which such offer, solicitation or sale would be unlawful.

Not for distribution to U.S. news wire services or dissemination in the United States.

FOR FURTHER INFORMATION PLEASE CONTACT:

NXG; $1.54; Merrill

EPS (Dec): 2003A $0.03; 2004E $0.17; 2005E $0.07

P/E (Dec): 2003A 51.3x; 2004E 9.1x; 2005E 22.0x

Event

Northgate Minerals reported Q4/04 and 2004 operating results. Northgate’s Kemess South operation reported its fifth consecutive year of increasing gold and copper production and its lowest cash costs to date.

Analysis – Record Results, As Expected For Q4/04, the company produced 94,673ozs of gold and 23.9mn lbs. of copper at full absorption cash costs of $116/oz (gold institute method $70/oz); this compares to 78,761ozs of gold and 22.2mn lbs. of copper at cash costs of $185/oz in the same period of 2003. We were looking for output of 86,600ozs of gold and 21.9mn lbs. of copper. For 2004, Northgate reported output of 303,475ozs of gold and 78.3mn lbs. of copper at full absorption cash costs of $137/oz (GI method $83/oz) vs. 294,117ozs of gold and 76.2mn lbs. of copper at full absorption cash costs of $219/oz in 2003. We had expected gold and copper production of 295,000ozs and 76.3mn lbs., respectively, at full absorption cash costs of $144/oz.

Production was basically in line with company guidance and our estimates for 2004. The improved cash costs realized in 2004 were essentially the result of improved efficiencies and higher copper prices (used as by-product credits). Going forward we anticipate that cash costs will increase as copper prices decline over the next few years (Merrill Lynch estimates).

Outlook: We are looking for gold and copper output of 301,000ozs and 78.8mn lbs., respectively, at full absorption cash costs of $163/oz in 2005.

Recommendation

Northgate is currently trading at a P/NAV of 1.6x, below the mid-tier average of 2.1x. Given Northgate’s hybrid production (gold and copper), relatively short mine life (excluding Kemess North) and single operation risk, we feel this is an appropriate level. Therefore, we are maintaining out Neutral rating on Northgate.

interesting article on ForEx

From: ild @ SI

From Fleck's web site:

Special feature for 1/11/05: Justin Mamis's brilliant discussion of currency trading (they don't behave like stocks) and the ongoing demise of the dollar as the worlds reserve currency.

http://www.fleckensteincapital.com/special_features/mamis/mamis01-11-2005.pdf

thanks much, has Market Vane ever been below 65% Bullish since you have been plotting this...?

ok, are we going to get a new chart anytime soon...!!@@!@!!

NXG continues to get no respect... Likely EPS of US$.08 for 4Q04 and selling for US$1.58

my annualized EPS estimate = $.32

based upon current metal prices

thus, NXG selling at 5x annual PE

this assumes their G&A and other 4Q expenses are in line with last quarter

compare the 4Q vs. 3Q production numbers

4Q news release

Northgate Reports Record Gold Production

Monday January 10, 9:29 pm ET

2004 Cash Cost of $137 Per Ounce

VANCOUVER, British Columbia--(BUSINESS WIRE)--Jan. 10, 2005--Northgate Minerals Corporation (TSX:NGX - News; AMEX:NXG - News) - (All figures in US dollars except where noted)

Northgate Minerals Corporation today reported record quarterly and annual operating results from the Kemess mine located in north central British Columbia.

2004 Highlights

Record annual gold production of 303,475 ounces

Record quarterly gold production of 94,673 ounces in the fourth quarter

Record annual copper production of 78.3 million pounds

Record quarterly copper production of 23.9 million pounds in the fourth quarter

Record low annual cash cost of $137 per ounce

Record low quarterly cash cost of $116 per ounce in the fourth quarter

Record quarterly mill throughput record for hypogene ore of 52,136 tonnes per day

3Q Financials

see page 3

http://www.northgateminerals.com/pdf/Q3_2004.pdf

(100 % of Production Basis) 3Q04 3Q03 9M 04 9M 03

Ore plus waste mined (tonnes) 13,854,977. 13,252,555. 42,339,253 39,392,302

Ore mined (tonnes) 4,717,920. 4,046,004 14,497,645 13,227,413

Stripping ratio (waste/ore) 1.94. 2.28 1.92 1.98

Ore milled (tonnes) 4,660,899 4,992,739. 13,793,191 14,048,513

Average mill operating rate (tpd) 50,662. 54,269. 50,340 51,460

Gold grade (gmt) 0.760 0.807. 0.686 0.689

Copper grade (%) 0.221. 0.207. 0.218 0.214

Gold recovery (%) 70. 65. 69 69

Copper recovery (%) 82. 76. 82 82

Gold production (ounces) 79,311. 84,132. 208,802 215,365

Copper production (000s pounds) 18,712. 17,346. 54,436 54,012

Cash cost ($/ounce)

Full absorption method 129. 201. 147 232

Gold Institute method 76. 151. 90 209

_____________

in short, 4Q vs. 3Q

gold production up to 94.6 from 79.2

copper production up to 23.9 from 18.7

cash cost down from $129 to $116

3Q EPS was US$.05, so I am guessing current quarter EPS of $.08

Martin M snippet

Even renowned long-term gold bull Dr Martin Murenbeeld has warned against excessive dollar bearishness, noting that the currency’s decline is forcing some hard choices: “Asian and European policies favouring domestic consumption are long overdue, and the decline in the dollar indicates that procrastination must now stop. The days of easy living off the U.S. consumer are coming to an end.”

http://www.resourceinvestor.com/pebble.asp?relid=7749

RNC Gold Confirms Bulk Tonnage Gold Target Open Along Strike and at Depth

Comparing the maps between the news releases, appears that the L45 trench is a "new find", not included with the prior news release. Plus, this L45 find appears to have the best grades and length/width to date...

new map showing new L45 trench with drill holes

http://www2.ccnmatthews.com/database/fax/2000/RNC%20Map%200110.pdf

old map 11/08/04

http://www2.cdn-news.com/database/fax/2000/rnc1108.pdf

_________________________

RNC Gold Confirms Bulk Tonnage Gold Target Open Along Strike and at Depth

1/10/05

TORONTO, ONTARIO, Jan 10, 2005 (CCNMatthews via COMTEX) --

Not for release in the United States

RNC Gold Inc. (TSX:RNC) today announced that additional assay results from 4,350 chip samples and four preliminary diamond drill holes on the recently identified bulk tonnage gold target at the Company's Bonanza property in northeastern Nicaragua have confirmed that this large target remains open along strike and at depth.

"This Phase 1 work helps to validate our theory that this widely disseminated mineralization extends well below surface," said J. Randy Martin, President & CEO, RNC Gold Inc. "We have made an expanded exploration program a priority and, in addition to further trenching, an initial RC drill program totaling 7,000-10,000 meters is scheduled to begin early in 2005."

The principal findings of the Phase 1 exploration are:

- Analyses received for the most recent 1,258 surface trench chip samples have extended the main area of gold in saprolite (weathered - oxidized bedrock) by another 150 meters to the northeast. Trench Line 45E, the most northeasterly trench and Trench Line 34E, across the middle of zone of interest, returned gold values as follows:

-------------------------------------------------------------------Trench_ID From To Length Gold (m) (m) (m) (g/t)--------------------------------------------------------------------------------------------------------------------------------------L 45 E 1) 4.7 487.8 483.1 0.92 Includes 89.9 486.2 396.3 1.01 2) 496.9 522.9 26.0 0.80 Includes 496.9 510.7 13.8 1.31 3) 577.7 740.8 163.1 0.65 includes 678.3 740.8 62.5 1.57L 34 E 1) 21.3 568.5 547.2 0.32 includes a) 64.8 80.8 16.0 0.78 b) 93.0 202.7 109.7 0.65 incl. 143.3 158.5 15.2 0.85 c) 227.1 242.3 15.2 0.70 2) 890.2 903.9 13.7 0.97-------------------------------------------------------------------

(See sketch Map attached)

- Less than 0.4% assayed above 10 g/t gold eliminating the need to cut high values.

- The four diamond drill holes encountered vertical thicknesses of mineralized saprolite varying between 20 and 40 meters and thickening toward the Neblina structure to the northwest.

- Gold values for the diamond drill holes are reported in the table below. The highest individual gold values are centered on individual quartz veins.

Table of Assays for the Diamond Drilling of the Foundling NE-Tesoro veins

---------------------------------------------------------------------Hole_ID From To Meters Gold (g/t) Geol. Unit------------------------------------------------------------------------------------------------------------------------------------------FNE-04-19 0.0 27.5 27.5 0.55 Saproliteincludes 9.0 13.0 4.0 1.50FNE-04-20 0.0 41.2 41.2 2.05 Saproliteincludes 0.0 13.0 13.0 5.55 or 4.0 6.0 2.0 26.60FNE-04-21 0.0 32.9 32.9 1.11 Saproliteincludes 27.0 33.0 6.0 4.41 or 30.0 33.0 3.0 7.95FNE-04-22 0.0 29.3 29.3 0.24 Saprolite 33.5 36.4 2.9 4.87 Andesite oxydisedincludes 35.0 36.4 1.4 9.15---------------------------------------------------------------------

- Trench Line 45E is cut at low angle to the NW trending Tesoro mineralized structure which is an important controlling factor for the emplacement of the gold mineralization, especially where it intersects the prevalent northeast trending mineralized veins.

- Most of the trenching completed to date has been conducted on lines spaced 120 to 150 meters apart across the northeast trending Neblina and Foundling mineralized structures defining more clearly a zone of surface gold mineralization 730 meters long and 500 meters wide on average.

- The zone remains open in both directions along strike and parallels the Neptune and Capitan mine-Venus mineralized structures located 250 and 650 meters to the southeast, respectively. The latter has previously been sampled on surface by trench L29E which returned 52 m of 0.72 g/t gold including 29 m of 0.86 g/t gold, 47.6 m of 0.78 g/t gold including 30.5 m of 1.0 g/t gold, and 148 m of 0.60 g/t gold including 78 m of 1.0 g/t gold (press release of Nov. 8 2004). See note on reporting procedures.

Sampling, analytical and reporting procedures

Continuous 1.5 meter chip samples were collected by digging a further 6 inches on the floors of the trenches and bagging 3 to 5 kilograms of the saprolite and, in some cases, colluvium (broken up bedrock fragments in soil), brown soil and/or fresh bedrock where saprolite was not available. The samples were shipped in barrels to the CAS Laboratory in Tegucigalpa, Honduras, for preparation where the samples were dried and pulverized to a minus 150 mesh to produce a 300 gram pulp sample. The samples were then shipped to Acme Laboratories in Vancouver, B.C., Canada, for analysis by ICP-MS (induced coupled plasma) using splits of 0.5 grams leached in hot (95C) Agua Regia. Gold analyses were prepared using a larger 15 gram split size for a more representative sample. Samples duplicates are analysed at regular intervals. The first batch of 2,500 samples was analyzed for the 30 element package for better characterization of the mineralized system. Samples are currently being analyzed for copper, lead, zinc, gold and silver. In this press release, composites of gold analyses are reported for various cutoff grades using a 0 maximum dilution width and minimum edge values corresponding to the selected cutoff grade. In the November 8, 2004 press release, composite analyses were reported without specifying a maximum dilution width and minimum edge values.

The qualified person on the project is Denis Francoeur, M.Sc, P.Geo., a practicing member (#0781) of the Association of Professional Geoscientists of Ontario.

About RNC Gold

RNC Gold Inc. is a gold mining company focused on projects in the Caribbean basin. From its current production base of 100,000 ounces of gold, RNC is positioned for growth through operational efficiencies, exploration potential on property around its present mines, through construction of new mines and the acquisition of new projects.

The Company's main assets include the La Libertad and Bonanza mines in Nicaragua, the Cerro Quema project in Panama and the Picachos exploration property in Mexico as well as the option to acquire 25% of the San Andres mine in Honduras.

NOTE: There is a Map available on CCNMatthews' website at: http://www2.ccnmatthews.com/database/fax/2000/RNC%20Map%200110.pdf

MUG could be related to recent PP...?, similar to DAE

__________________

To: amarksp00 who wrote (2969) 1/8/2005 1:58:55 PM

From: sunny1 Mark as Last Read / Read Replies (1) / Respond to of 2971

Very interesting - but I believe the last PP becomes free trading soon - next week ?

Don`t some large buyers often short the stock - to then deliver what they get in the PP - safe - locks in profit -then they just sit with the warrants .

To: sunny1 who wrote (2970) 1/8/2005 2:18:47 PM

From: amarksp00 Mark as Last Read / Respond to of 2971

Thanks, you are likely right, i.e. related to that 3M unit offering. But appears the hold period lasts until Mar 17, 2005.

"Dasher Exploration Ltd. (the "Company") (TSX VENTURE:DAE) announces that it has closed a private placement of 3,000,000 units priced at $0.80 each, announced September 21, 2004, for gross proceeds of $2,400,000. The units are subject to a hold period that will expire on March 17, 2005. "

Per TSE, DAE only has 9.3M shares outstanding..., so .5% of that is implies 47,000 shares minimum shorted in the USA.

Will be interesting to see if and how we can use this Reg SHO data on junior gold stock picks...

Dasher on it as well...

Wonder if this is .5% of total Dasher shares or .5% of shares available in the US...? Anyone know...?

Dasher on the Reg SHO list, i.e. more shares shorted than shares available...

DAEEF.....DASHER EXPLORATION LTD

http://www.nasdaqtrader.com/aspx/regsho.aspx

"where, for five consecutive settlement days:

1) There are aggregate fails to deliver at a registered clearing agency of 10,000 shares or more per security;

2) The level of fails is equal to at least one-half of one percent of the issuer’s total shares outstanding; and

3) The security is included on a list published by a self-regulatory organization (SRO)."

AV may be an interesting spec, I will participate via my ownership in EDV...

"Endeavour Mining Capital Corp. ("Endeavour" or "Corporation") announces that it had acquired 1,350,000 Common Shares of Adobe Ventures Inc. ("Adobe") (AV on TSXV) through public transactions at a price of $0.35 per common share.

Following this acquisition, Endeavour will hold a total of 4,963,500 common shares of Adobe, representing approximately 19.9% of the 24,901,378 Common Shares currently issued and outstanding. The Common Shares are being acquired by Endeavour for investment purposes only. Endeavour has no present intention of acquiring other securities of Adobe or disposing of any of the securities of Adobe it holds. Depending on its evaluation of Adobes' business, financial condition, the market for Adobe securities, general economic conditions and other factors, Endeavour may acquire additional securities of Adobe or sell some or all of the securities it holds (subject to compliance with any applicable hold periods under securities laws). "

___________________

Appears AV is a vertically integrated coal/utility company that will be operating on the island of Sardinia Italy and furnishing power to the island/Italian power grid.

http://www.newswire.ca/en/releases/orgDisplay.cgi?okey=98814

If one can buy AV at $.35 or lower as EDV just did (AV closed at $.45), may be an interesting speculation play...

Sardegna/Sardinia is the large island to the west of Italy...

wish there was a closer correlation between Hulbert vs. Market Vane

http://cbs.marketwatch.com/news/story.asp?guid={A3615992-0CA5-498C-9006-F0D948DBC254}&siteid=mkt....

ANNANDALE, Va. (CBS.MW) -- Gold bullion's plunge over the past month is likely to be a mere correction within the confines of a long-term bull market.

That at least is the conclusion of contrarian analysis, in light of how quickly most gold timing newsletters have jumped on the bearish bandwagon. More typical of a market top is stubborn bullishness, and what we've seen in recent weeks is anything but.

Consider the latest readings from the Hulbert Gold Newsletter Sentiment Index (HGNSI), which reflects the average exposure to the gold market among a subset of short-term gold timing newsletters tracked by the Hulbert Financial Digest. As of Thursday night's close, the HGNSI stood at negative 23.2%, which means that the average gold timer in this group is actually net short the market.

As recently as the end of November, when an ounce of gold bullion (38099902: news, chart, profile) was trading for nearly $30 more than where it's trading today, the HGNSI stood at plus 78.6 percent.

That means that, over the past month, the gold market exposure of the average gold timing newsletter has dropped by more than 100 percentage points. That's more than just an orderly retreat. That's a veritable rush to the exits.

On the contrarian theory that markets like to climb a wall of worry, this is good news.

In fact, the average gold timing newsletter that the HFD tracks is now more bearish than at any time since late 1997, more than seven years ago. Furthermore, the HGNSI's level at that time -- negative 31.3 percent -- was not that much lower than the current reading.

It's amazing that the HGNSI today is anywhere close to its low level of late 1997, if you stop to think about it. At that time, gold was more than 15 years into a severe bear market. Despair was an entirely understandable reaction to where the market stood.

Today, in contrast, bullion is higher than it at any time in years, but for a few trading sessions at the end of last year. And yet the average gold timer appears to be as dejected as he was near the depths of a punishing long-term bear market.

Another perspective on gold market sentiment comes by contrasting gold timers' recent behavior with stock market timers' reaction in March 2000, at what turned out to be the top of the stock market and the bursting of the Internet bubble. During the first 10 percent correction after that top, the average stock market timer actually increased his equity exposure.

Now that is stubborn bullishness. And we all know what happened next.

This is not at all the situation that currently prevails among gold timers.

_____________________

Frank, per our prior discussions on Market Vane participants, sure wish we could determine who exactly are those Market Vane folks that are surveyed, they must be polling GATA members...

BULLISH CONSENSUS ON Janaury 04:

24 Month Range Low Hi

Gold 68 from 73 on December 21 13 - 91

Guess you caught me..., am pumping MFN onto the big boyz now, in addition to all you peons residing here and SI...

Also note Sun Valley Gold, Peter Palmedo's investment company, owns 1%...

http://www.investorshub.com/boards/read_msg.asp?message_id=429796

http://www.investorshub.com/boards/read_msg.asp?message_id=4332551&txt2find=palmedo

Seriously, with institutions owning 50%, management 2%, and gold index and mutual funds likely a few more percent, would not think that MFN is that susceptible to mine or anyone else's pumping on message boards... When MFN needs financing, they likely just simply ask these institutions for the needed cash (without warrants) rather than those greedy, pump & dump Bay Street investment bank/firms...

MFN only has 36.5M shares outstanding, so the float outside institutions/management is under 18M shares. MFN already has 3M+ gold equivalent ounces and if capex comes in under $120M and $186 cash costs, then stock price should take care of itself with no pumping necessary...

Thanks for you and Frank attributing the MFN pump to me, maybe I can gather a following of sheep to join me in my RNC.to folly...

well, MFN could be getting pumped, I've been trying my best... BUT 15 institution own 49% of this stock and MFN has no warrants outstanding (MFN has raised cash via PP without warrants for the past several years). There are likely more than these 15 instituions, but MFN would not appear to be a stock prone to pumping...

1 Fidelity Management & Research Co. 4,591,790 861,930 28,836,441 0.00 12.60 09-30-04