News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Fruno

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Thanks, that's the information I was looking for. So as dark pool volume increases, fewer shares are available on the public exchange.

I understand that part (sort of). But how do shares become available to these private exchanges in the first place? Are institutions buying shares of LWLG on the NASDAQ, then trading them on a dark exchange (removing those shares from the number available to individual investors)? Or does LWLG allocate shares to the dark pools?

How do shares get into these dark pools in the first place? Do entities buy them on the open market first, then subsequently trade them in a dark pool, or is there some other mechanism?

Thanks.

Did someone just buy 4.9% of the company?

TDAmeritrade has 1 report for LWLG. It rates it as a strong sell.

In this and the previous presentations, Lebby said "we are in the prototyping and piloting stage". These are the first times he's included "piloting" that I know of. This is an advance from previous presentations.

Here is the basis for the r33 of 400 pm/V (or higher). These are both very powerful statements.

From the 2021 3rd quarter report:

In May 2020, we announced that our latest electro-optic polymer material has exceeded target performance metrics at 1310 nanometers (nm), a wavelength commonly used in high-volume datacenter fiber optics. This material demonstrates an attractive combination at 1310 nm of high electro-optic coefficient, low optical loss and good thermal stability at 850 Celsius. The material is expected to enable modulators with 80 GHz bandwidth and low drive power, and has an electro-optic coefficient of 200 pm/V, an industry measure of how responsive a material is to an applied electrical signal. This metric, otherwise known as r33, is very important in lowering power consumption when the material is used in modulator devices. This technology is applicable to shorter reach datacenter operators, for whom decreasing power consumption is imperative to the bottom line of a facility. We considered this a truly historic moment—not only in our Company’s history, but in our industry–as we have demonstrated a polymer material that provides the basis for a worldclass solution at the 1310 nm wavelength, something which other companies have spent decades attempting to achieve

On August 4, 2021, we announced that we developed improved thermal design properties for electro-optic polymers used in our Polymer Plus™ and Polymer Slot™ modulators, enabling the speed, flexibility and stability needed for high-volume silicon foundry processes. We successfully created a 2x improvement in r33, while allowing higher stability during poling and post-poling. This provides better thermal performance and enables greater design flexibility in high-volume silicon foundry PDK (process development kit) processes.

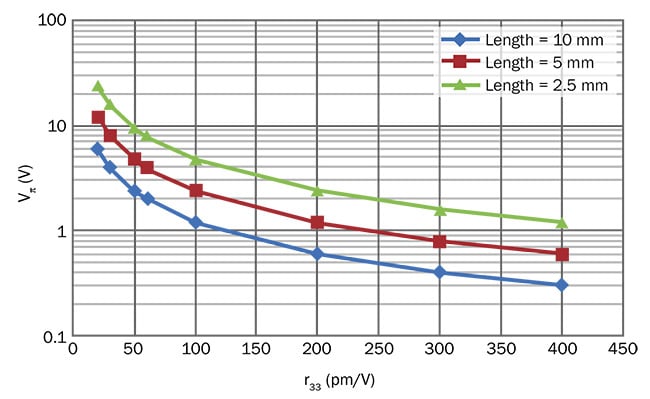

Here is Figure 4 from the article. (Finally was able to post an image!)

It shows that increasing the r33 lowers the voltage.

Check out this article (written by LWLG):

Electro-Optic Polymers Improve Speed and Power Efficiency

The article states that " The only way to reduce the voltage while maintaining speed for this device is to increase the material’s r33 coefficient."

LWLG has stated they achieved r33's of over 200 pm/V. Doubling that puts them over 400 pm/V. Based on Figure 4 in the article, the voltage should be 0.5V or lower, which they have also achieved. Both these goals are necessary for the devices to be 'direct drive'.

Double big block at close. Someone mentioned this last week. 2 blocks of 11,073 shares each. I've seen this a couple of times before. No idea what is going on.

I don't know caly personally, but he is still posting on the Silicon Investor boards as of June. Still listed as "emcee" of the LWLG board there.

forztnt2:

I was referring to both patent 11067748 "Guide Transition Device and Method" and the not-yet announced patent you mention.

My point was that, looking at the last few patents, they build on each other, working toward an integrated component that includes not only the modulator, but the light source (laser), the guides for the light, hermetic packaging (for better environmental protection), and other pieces that result in a low-cost, easy to manufacture solution to replace current modulator technology.

To quote from the not-yet-announced patent (application no. 16/710,066):

"It is another object of the present invention to provide a new and improved laser and polymer modulator integrated on a common platform with more efficient coupling between source laser and optical modulator, efficient 3-layer polymer modulators, higher performance (multi GHz), and very low voltage to allow direct drive without the use of a driver circuit."

and:

"...a monolithic photonic integrated circuit is provided including a platform, a monolithic laser formed in/on the platform, and a polymer modulator monolithically built onto the platform and optically coupled to the monolithic laser."

In other words, LWLG will not be selling modulators. They will be selling a new photonic component that incorporates lasers and modulators and all the tech needed to couple it to a semi-conductor substrate (silicon, etc.), plus provide excellent environmental protection, etc. And, since LWLG has patented both the "stuff" and the means to manufacture it, no one can else can substitute their part(s) into it without going through LWLG.

The patent documents discuss issues with current tech and how each new patent provides solutions. They are worth reading, or at least skimming (even with the technically dense language) to get a feel for the improvements being made. Plus, there are lots of diagrams.

In my non-expert opinion, I think these are some cost-saving factors:

Making Perkinamine is not expensive (or it's used in tiny amounts)

Replacing silicon or other substrates with plastic

Eliminating a (higher-powered) laser and it's driver chip

Integration means there are fewer manufacturing steps

Lower energy usage and production of waste heat, so energy savings

The company hasn't addressed cost in detail. Hopefully, someone more technically astute will provide a better explanation.

The companies patents, over time, have more commonly included wording like "... and method", meaning they are not only patenting new devices/components, but the means to manufacture them. The last few seem to build on on the previous one.

Someone found another patent that has been approved but not announced yet. It adds an integrated light source.

So it appears LWLG has developed a single, integrated component, and the means to manufacture it, that incorporates a modulator, a light source, and all the means to guide the light and resulting optical signal to and from an underlying substrate (silicon, etc.). It will be smaller, faster, use less power, and hopefully be cheaper than anything available now.

All this dovetails neatly with the statement in recent 10-Qs that the company is "... currently focused on testing and demonstrating the simplicity of manufacturability and reliability of our devices, including in conjunction with the silicon photonics manufacturing ecosystem."

It's been convenient over the years to think of the company as developing a chromophore, then a polymer, and then a modulator. But that's only part of the magic. They are creating a whole new way of switching light and the means to build it. That's what the industry is waiting for.

I don't have an answer for that. I'm just musing on the possible path to mass commercialization.

You asked a relevant question. I recall the company saying there are 3 barriers to tipping the market to their technology - speed (200 Gbps and higher), power consumption (less then 1 Volt) and cost (don't remember the criterion). (I can't find the statement now, working from memory. Maybe someone can post it.)

LWLG has demonstrated the speed in devices that can be packaged to meet the industry goal, and have shown power consumption in the 0.5V range. I haven't seen any specifics on cost.

The last several quarterly reports state that the company is "...currently focused on testing and demonstrating the simplicity of manufacturability and reliability of our devices, including in conjunction with the silicon photonics manufacturing ecosystem." Manufacturing cost is a component of the total cost of a device.

Maybe agreeing on a PDK with a foundry is the last piece to provide potential buyers with the price per device?

In my posts yesterday, I was suggesting that maybe a foundry needed to see real demand for a product before committing to manufacture them. Ergo, the PDK would be the last step before mass commercialization. Maybe I have it backwards - the PDK is needed to develop the pricing, which is what customers need before committing to buy.

I am. Been staying tuned for 15 years.

I'm no expert in the chip foundry business, I just don't think a foundry will use capacity speculatively (making LWLG chips with no guarantee of sales).

Really, all I'm suggesting is that some "minor" revenue streams will be established before the "major" revenue stream from mass device sales. Those "minor" streams will involve polymer sales and design agreements, as stated by the company in the quarterly report.

See Polariton's home page at https://www.polariton.ch. There's a graphic comparing their modulator with lithium niobate and silicon photonics. The last line is "Maturity". Under Polariton, it says "First product 2021". Also, they issued a PR (https://www.polariton.ch/wp-content/uploads/2021/07/Press-release-NLM-Polariton.pdf) announcing availability of a product using EO material from NLM.

"It" is Polariton's plasmonic modulator.

I had questions when the joint PR with Polariton was issued as to what the future relationship of the 2 companies would be. Polariton's modulator requires an electro-optic material - LWLG has the industry-leading EO material. However, Polariton is using a material from NLM. I just speculating that Polariton might find a way to use LWLG's polymer in the future, providing a revenue stream for LWLG.

I didn't expect my speculation to be controversial. I believe that LWLG's devices will one day dominate the market. I'm just saying that there will likely be a few more steps to take before they get there. The company says they expect revenues from polymer sales and product development agreements. I'm just suggesting what that might entail.

I read that. I'm not suggesting that LWLG will acquire Polariton or even partner with them in any way. Polariton has developed a plasmonic modulator and has shown that it works with LWLG polymer inside. Polariton also says on their website that it will be available this year. So maybe they manufacture and sell some using LWLG polymer. Thus, a small revenue stream for LWLG.

Don't think I'm twisting anything. We (me included) are expecting large revenue streams from device sales at some point. The company is also expecting revenue from ".. sales of non-linear optical polymers.." and "..product development agreements". Those would be smaller revenue streams than device sales, IMO. I think it's realistic that those smaller revenue streams will start to flow before large-scale device sales.

There seem to be many on the board who expect the next PR to announce a deal (likely w/ GFS) to manufacture mass quantities of chips containing LWLG modulators that will lead to billions in revenues. I think this is unrealistic. There has to be a market first before a foundry will dedicate capacity to LWLG, even after a PDK is developed. It's more realistic that there will be an agreement with a company, or several companies, to provide design services for (greatly improved) devices that will create that demand. A design contract will be much smaller than that eventual billions that will be generated once LWLG technology becomes "ubiquitous".

Revenue from sales of polymers will also be small in comparison to device sales.

Thanks for passing on this info. A couple of things I found in the report:

In the "Nature of Business Discussion" on page 7, first paragraph -

"Currently the Company is in various stages of photonic device and materials development and evaluation with potential customers and strategic partners."

Lebby says in the latest presentations that we are in the prototyping phase. Not sure why he doesn't use the above language.

The next sentence -

"The Company expects to obtain a revenue stream from datacom and telecom devices, sales of non-linear optical polymers, and product development agreements prior to moving into full-scale production."

So some small revenue streams may be generated before reaching "mass commercialization". Maybe selling polymers to Polariton for their modulator? It would be nice to be paid some design fees, too.

From Note 2 on page 8, they say monthly expenses are estimated at $865,000 for the next 12 months, but that "... cash

requirements are expected to increase at a rate consistent with the Company’s path to revenue as we expand our activities and operations..." so that estimate is likely the minimum monthly outlay.

They received $3,449,650 in October from the LPC deal.

"We currently have no debt to service." An oldie but a goodie.

First off, great find.

If you want more info, follow the link, click on 'Images', then click on 'Full pages' in the panel on the left. This brings up the entire document. The best description of what the patents achieves is in the 'Background of the Invention' section on page 22.

[0003] Laser modulators have been in use for 20 years.

Initially discrete lasers were positioned next to discrete

modulators so that higher performance signaling ( and speeds

above 10 Gbps) could be attained. While this technique has

been commercialized it is not optimized. That is it does not

reach the low cost targets, or space/size requirements, and

takes lots of time to align the components, place them,

package them, and test them. Also, while some integration

of lasers and modulators has occurred, optical alignment of

the components can be a costly and tedious task.

[0004] It would be highly advantageous, therefore, to

remedy the foregoing and other deficiencies inherent in the

prior art.

[0005] Accordingly, it is an object of the present invention

to provide a new and improved polymer modulator integrated

on a common PIC platform.

[0006] It is another object of the present invention to

provide a new and improved polymer modulator integrated

on a common PIC platform with novel new design and

process.

[0007] It is another object of the present invention to

provide a new and improved laser and polymer modulator

integrated on a common platform with more efficient coupling

between source laser and optical modulator, efficient

3-layer polymer modulators, higher performance (multi

GHz), and very low voltage to allow direct drive without the

use of a driver circuit.

I do. That's why I noted it as sarcasm.

It's a post-deadline paper so it doesn't count. /s

Don't see any reference to drive voltage.

It's a post-deadline paper so it doesn't count. /s

Rockley is also up over 17% right now. Coincidence?

Thanks. Good to know. Polariton touts datacom along with Lidar and other applications on it's website.

So did LWLG pay Polariton to use their polymer in the modulator Polariton is marketing just to get confirmation of the properties? This data is not from an LWLG Mach-Zender modulator. Polariton is already marketing modulator with NLM's HLD EO material, based on their July 26 PR. Would Polariton help a potential competitor? Are these 2 different products for different markets, or are they dumping NLM?

There is no partnership, as yet. Also, the share price projections that are being thrown around are based on LWLG producing it's own modulators. Those projections change considerably if LWLG is only providing the polymer for someone else's modulators.

Confirmation of the polymer/chromophore properties as far exceeding any other material by leaders in the industry is the most important milestone I've witnesses in 15 years of following this company. However, I will be disappointed if foundry deals, PDKs and freedom of manufacturing were diversions. My impression of what we've been hearing this year is that LWLG would not have to partner to provide modulators. I'm confused as to how this will work out.

So on July 26, 2021, Polariton and NLM announce a partnership (their word) and "devices ready for commercialization", then today issues a joint PR with LWLG about using our polymer. NLM has a 'high-performance' electro-optic material.

So is Polariton dumping NLM? Do all 3 fit together?

The ramifications for LWLG (beyond the highly welcome validation of the polymer) are unclear to me.

Based on the wording of the PR it seems that LWLG is only providing the electro-optic material for Polariton's modulator. The confirmation that the polymer/chromophore works is great, but how does this fit into the business model based on freedom of manufacturing and incorporating LWLG's devices?

I may be wording my question badly, but having a foundry manufacture chips using all-LWLG tech is different than providing the polymer to a different modulator company.

Sorry, had trouble with the image

From the Polariton home page - "First products 2021". Hmmm...

https://www.polariton.ch

IMHO, no. Would be nice to happen, though.

Feel free to dispute my status as 'knowledgeable' as to the company's plans. My main qualification is that I have owned stock for 15 years.

Since May, there has been a flow of good technical news, including 2 important patents, a breakthrough in thermal properties. The ASM video outlined the strategy of partnering with foundries and talk of co-authored PRs. The PPS went over $4, which opened the door to the NASDAQ. Plus plenty of optimistic talk from Lebby as previously discussed. All good.

I don't expect the a co-authored PR to have revenue numbers included. It will likely announce a joint venture of some type to finalize a PDK, which, along with preparations for manufacturing, will take some time. I'm not expecting significant revenue this year. Despite Lebby's enthusiasm, my feeling is that this is still down the road a bit. But it is coming.

I don't think Lebby, despite being very smart, is manipulating everything in some ninja-like manner. He's getting things lined up, but there are other parties that have to cooperate. Part of the reason I feel this way is the lack of response to the move to the NASDAQ. No big price jump, no surge in volume, no indication of significant institutional buying. The company is still unknown (or unproven) to the broader investment community.

I'm not worried about the financial end. The company made it this far in good shape, and will be in better shape once the tech is confirmed as ground-breaking as we all think it is. The shelf will be used wisely.

I remain optimistic. Hopefully, more will be revealed this week, but if not, I'll continue to wait and watch. The momentum is building.

No problem. I hope to see LWLG appear on the list soon!

That link shows the market value of each company held in the fund (no. of shares X PPS). That's not the market cap.

I looked through some of the legal documents for the funds to see if there was anything about buying OTC stocks, but couldn't find any information. I'm not aware of any OTC stocks being held in any ARK funds, but haven't done an exhaustive search.

...ubiquitous...

...unrivaled...

This patent describes the fabrication of "mirrored" surfaces to bounce light produced on the chip up to the overlying polymer layer (containing the modulators), then reflecting the modulated light back down to the chip (or wherever it needs to go).

The last few patents have taken 12-18 months to be reviewed and granted. When Lebby gave the presentation at the ASM, he knew these were close to approval, and he knew the improved performance results announced since that time were also close to release. All of this progress has been made with input from potential customers, via the NDAs. That is why I am optimistic.

There are companies interacting with LWLG in a positive manner, even if Intel is not.