News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Unkwn

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

An ability to slow development and increase margins is what I have been most waiting for.

It's your problem to provide that data. You are basing your claim of the lost process lead of Intel upon a faulty (semiwiki???) article that doesn't support your claim, omitting key components of the GF designs.

I'm not cherry picking. The major axes of the design are not quoted in that stupid semiwiki ragsheet article you posted. You are an idiot to read that stuff without healthy skepticism.

@Flum

You are just cherry picking what seems to support your statement, but you get the full picture in the article and I posted its conclusion. When it comes to actual circuits, like SRAMs, Globalfoundries 7nm is more dense than Intel 10nm. We can argue about a few nm pitch here and there, where one will win over the other, here and there. All this doesn't even remotely support your statement that Intel would have a lead. If anything, it is a wash and Intel will be late, so no lead.

And don't tell me about some 10nm chips that are out in the field by Intel. If that would indicate a mature process, they wouldn't delay volume production. It's all about volume production and that is going to be this year for the foundries on 7nm and next year for Intel 10nm. No lead for Intel here, nowhere and certainly no 3 years lead as often claimed by Intel.

Now you can stare at the chart and look for information about the future of this company, like those other monkeys.

If I was permitted more than one post per day then I would explain it to you. Basically Intel scales all components by volume, while "others" only scale one (maybe 2) dimensions. So Intel is doing the honest scaling, and they will end up ahead of the competition in doing so. But there are scads and scads of other components going onboard Intel chips, and I agree with BK that the obsession with size (in this case tiny) is the bugaboo of small minds, such as one finds littering up this mssg board. So, I am grateful to Phud and his henchmen for restricting me to one post per day because I don't drop in here very often, and that suits me just fine.

Comparing Intel's 10nm process to GF's 7nm process they are more similar than they are different. Since both companies are solving the same difficult physics problems this is in some ways not surprising.

The surprising part in my opinion is that GF at 14nm stumbled so badly they had to license it from Samsung. Now they have an internally developed 7nm process that matches up well with Intel's latest 10nm process.

It is also surprising to me to see how far Intel has fallen from the process lead they had. First with HKMG by several years, first with FinFet by several year, I suppose they are still first to do cobalt interconnect but in terms of process density the foundries have caught them and appear poised to take a substantial lead over the next several years.

With Intel offering foundry processes and GF, Samung and TSMC all offering leading edge processes the industry now has four viable leading edge process options.

We'll have to wait and see. I expect foundry 7nm to be denser in actual designs. In any case, Intel will be late with it and have no process lead anymore. That's new to their business. We'll see how they cope with it.

Here's an interesting comment/wrapup of the actual densities of Intel vs foundries.

A feature size, like SRAM cell size, is a much better indicator of actual achieved density than some pitch values, since it is a matter of many factors, how much you can integrate on a given area.

Note that Intel's SRAM size for high-density is 0.0312um2 and for high performance, it is 0.0441um2

GlobalFoundries, which AMD consistently uses for its Ryzen, Polaris and Vega chips, also has a higher density than Intel's. For high-density SRAM, it is 0.0269um2 and for high-performance SRAM it is 0.0353 um2.

What does this mean for AMD? Well, for the first time, Intel can no longer rely on process advancements for higher-efficiency, high-performance chips. Now, it is based on architecture and whose architecture is better. This means that with Zen 2 and Ice Lake, AMD would be the closest it has ever been in more than a decade to not only have a powerful architecture against Intel's Core series but also a process advantage. AMD had to contend with the process advantage for a decade, but now the tides appear to have been turned. Currently, with Zen+ coming out and the 12 nm (which is basically the same 14 nm20 nm process with further enhancements), AMD is still at a disadvantage. The IPC is worse than Kaby Lake's and Intel not only has a process advantage, but it also allows Intel to clock their chips higher than AMD's. (Though Ryzen does give more cores for the money) 2019 will be an interesting year for CPUs.

That's what happened to Moore's Law:

AMD announced in the earnings call that it is going to release a new server CPU on Global Foundries 7nm process by the end of this year. That's quite a big step from the current 14nm process and I wonder, how this CPU will compare to Intel's server CPUs by that time. To me, it seems like a smart move from Lisa Su to target the server market first with this 7nm CPU on the smallest process node, since Intel tends to switch to new processes late for its server portfolio. That made sense, as long as there was little competition, just to wait for the yields to mature, before switching those large, low volume and fast clocking server CPU dies to smaller nodes. That opens a window of opportunity for AMD, which they are obviously trying to benefit from.

you are clueless. If its a gaussian what do you count as the width? sigma? (1/2)sigma? 2 sigma? The bullshit is the obsession with the one metric that is most meaningless..."node size" wtf does that mean?

Good results from Intel. Main driver was the data center with 25% growth! So far, AMDs EPYC didn't seem to make a dent. It's a conservative business, though, major shifts are done carefully and slowly. AMD will have to prove that it is here to stay before larger groups will consider a major shift from Intel.

In general, the PC market finally seems healthy. Smartphones slowing down, tablets basically dead and people are still using their PCs (especially at work). More competition from AMD will lead to better and cheaper products, hopefully leading to increasing sales. Something that both, Intel and AMD, will benefit from. Intel will likely face lower margins and its lowered expenses into R&D are not particularly what they need now, to stay ahead of the crowd.

AMD did fine in its last call, by the way. Again a quarter in black, net debt isn't very high and revenue climbed significantly. AMD increased R&D spend by 26% vs the YoY quarter, which partly offsets the increase in gross result. I think it's a sensible move. Competitiveness is more important than short term results at this point. Still a long way to go and Intel likely isn't going to sit still in the meantime. Going to be very interesting. Intels next generation CPU vs Zen 2 may be a major indicator how this turns out.

Really, cmon, what's 10 nm? A 14nm Intel is about 7nm Samsung or Tsemi.

Samsung said to be early with its 7nm process:

The Samsung developers who participated in the development of the 7nm process have completed their mission and moved to 5nm development,.

First Zen+ Benchmarks released.

The 12nm CPU with slightly improved architecture and slightly higher clock speeds reaches close to Intel's single thread benchmarks and excels even further in multithreaded applications. In most games, it is now on par with Intel or even faster. Very few arguments left for the more expensive Intel CPUs.

Will be interesting how Zen 2 announced for next year, which is said to clock up to 5 GHz, will compare to Intel's offer by then. Intel's answer to this will be crucial. A 10% improvement won't be sufficient this time ...

The movement of a stock price in the past contains no information, whatsoever, about its movement in the future. A question of belief - for some.

Can someone address if Apple's future in-house SoCs can:

(a) have x86 backward compatibility to run current applications;

(b) run Windows applications using Parallels which a lot of Mac users are accustomed to; and

(c) any other potential technical issues

Intel and Micron decided to dissolve their 3D NAND partnership earlier this year. Tsinghua Unigroup is now Intel's best hope to improve its lowly position in NAND memory sales.

I wonder what kinds of profits this would be worth to Intel. I could see other companies switching to Intel if the price were right too.

TSMC pumping 24 billion, in words - twenty four billion, into the development of new processes. That is to fend off Samsung (Intel not so much). They plan for 5nm chips in 2020.

With all those crazy numbers, I wonder how high the risk of overspending is in all this. I can hardly imagine a scenario which makes sense economically with such high spending. Who is going to pay for those chips? Who is paying those huge mask costs? How is that killing the economies of scale in semiconductor, when shrinking by 40-50% costs you so much in depreciation of the fabs? Who is out there for only the performance benefits and willing to pay accordingly? Most chips are not highest performance class anyway. This is going to be very interesting.

FCF is what's left over after everything is spent investing in R&D, marketing, and capex.

You're ripping on Intel for having money left over (read: profits) and distributing it to shareholders while at the same time ripping on Intel for seeing reduced profits from 2012 levels (due to the very investments in new fabs, R&D, etc.)?

Record fourth-quarter revenue was $17.1 billion and record full-year revenue was $62.8 billion. Excluding McAfee, fourth-quarter revenue grew 8 percent year-over-year with data-centric revenue up 21 percent, and full-year revenue grew 9 percent year-over-year.

In 2017, Intel generated a record $22 billion cash from operations and returned nearly $9 billion to shareholders.

Semiconductor Capex industry comparison:

Intel is definitely not falling back ...

Some words about AMD's competitive road map that has been presented at CES. Seems like a very well focused portfolio. Especially the integrated graphics part should give AMD quite an edge due to the higher graphics performance at competitive CPU performance, power efficiency and lower cost. Looks like excellent execution on AMD's side.

Redesigned 12nm Zen parts with 12nm as power efficient as Intel 14nm+, according to AMD, will likely close the single thread performance gap further, with higher multithread performance than Intel offers. 7nm foundry then on par with 10nm Intel. We'll see who'll is first. Wouldn't bet on Intel. Losing market share and increasing capital expenditure for coming nodes is a poisonous combination for Intel. Could become a target for a nice short even.

In the meantime, Intel management is busy dumping its shares and let their HR guy lead the security team. Ridiculous, don't you think?

This is not an overall market drop. My Vanguard funds are all up and up well.

The era of owning particular stocks is done. Get with ETF's like SPY

or DLN or VYM. Or take a flyer.

Intel CEO insider selling to minimum before security issue published. I am not one of those who thinks that insider selling tells you much about a companies future, since there are a lot of rules that have to be followed by those owners. Still, I think reducing his share count to the absolute minimum he has to keep doesn't really show signs of much belief in the company he runs.

It is less about this security issue, of which the impact on the company is just unknown. In most cases, those things don't have much effect on sales in the mid to long term. Still, the CEOs action is a sign of overvaluation of the company. He knows best what impact AMD will have on Intel's numbers.

No opinion about the HBM or other integrated options/interfaces of Stratix 10. I know first hand, though, that Stratix 10 is only delivered as engineering samples so far. It's going to be available in quantities soon, I suppose, but that still makes it an almost 4 year delay! In addition, the highest density parts are shifted to 2019. There are even rumors that those will be shifted to 10nm altogether. Intel still seems to have major issues building them. In the meantime, Xilinx got the chance to overtake and they now have access to more advanced nodes than Altera/Intel. Looks like another failed acquisition from Intel.

What would bother me the most is the fact that Intel makes announcements that are that far off and then even doesn't justify in front of clients and investors. That is a style where a company quickly loses customer's and investor's faith. Intel talked a lot in recent years but delivered little. Not sure if or how that is going to change.

As long as they develop the cores at a brisk pace they are doing now, PC space is out of ARM's reach(just like mobile is out of Intel).

Intel compares Xeon with EPYC. Pretty comprehensive comment in this article:

Thoughts:

For the last five years Intel has largely owned the data center; currently, its processors power a whopping ~99.6% of the world's servers. Intel is currently restructuring and has bet a substantial portion of its future on data center-driven revenue, and while the company also faces threats from ARM-based competitors, such as Qualcomm's Centriq and Cavium's ThunderX2, AMD's processors have the advantage of the x86 instruction set architecture.

While the ARM-based competitors are attractive, it will take much more time for the software ecosystem to evolve, even with recent Linux support enhancements. That means EPYC-powered servers are the biggest near-term threat to Intel's dominance because they could serve as a simple and easy replacement.

It could take AMD several years to regain more than a single-digit market share even if EPYC is successful. That gives Intel plenty of time to adjust its product stack to counter the threat, but Intel's full-court marketing press highlights an urgency to counter AMD. That's because Intel's data center products are the figurehead of its high-margin ambitions, and none of its large customers, such as the Super Seven+1, pay anything remotely near MSRP.

EPYC CPUs are a threat to Intel's margins because they give Xeon customers another option. Consequently, Intel might have to get more price-competitive in key portions of its product stack, especially with high-volume customers. That means EPYC could affect Intel's bottom line, even if it doesn't gain significant market share.

Intel says it will share more test results with down-bin EPYC processors in the future, so the assault on EPYC will continue. It's certainly a strange time in the industry. AMD is supplying Intel with a custom GPU, but just months ago Intel insisted AMD was an inconsistent supplier. While the two companies may be participating in that venture, it's apparent the fight for the data center will be pitched.

AMD's EPYC is clearly setting off alarm bells, and it will be interesting to see if Intel takes the fight to the ARM-based competitors, like Qualcomm's Centriq, in the future.

EPYC based HP server with SPEC results released.

The 32 core EPYC seems pretty much on par with the 28 core Intel highend Xeon. It is a bit faster in floating point and a bit slower in integer, so basically a wash. Price is a lot different though, whereas the Xeon sells at 10k$, the EPYC sells at less than 5k$. It would be interesting to know the production costs since AMD will have presumably significantly better yields with its 4 die solution and the overall die area is pretty similar for the two cores.

Performance per watt will be crucial as is total cost of ownership, before datacenters will switch in larger numbers. Intel will go down in price before that happens, for sure. We'll see how much of their cash cows they are willing to sacrifice. Intel needs a lot of money for the (already very late) transition to 10nm.

In the Ryzen vs Skylake comparison, yes the core is bigger on the latter, but so is the performance. Skylake versus Ryzen core difference is much smaller if you compare it to the consumer Skylake which lacks AVX-512 and the extra L2 cache.

On the consumer side, Kaby and Coffee can clock 5GHz or more, while Ryzen struggles beyond 4GHz. That's in no insignificant way helped by the better performing transistors. Higher performing circuits also cost more in terms of die area.

Yes, but what did the do before that, 2000-2006

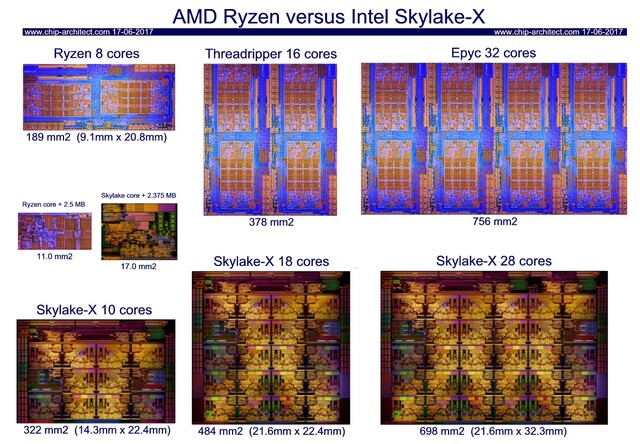

Adding to the discussion, here's a die size comparison between some Intel and AMD processors:

To recall: The 28 Intel core pretty much matches in terms of performance with the 32 core Epyc. The server processors are best to compare since they don't integrate graphics and such. The Intel CPU is single die, whereas the AMD CPU is multi-die (4 dies on interposer). Intel seems a bit more dense, but that is not by much (AMD's is 8% larger). But: Using 4 dies instead of 1 takes more area, since you need some additional area for pads and sawing etc. The advantage of AMD's 4 die solution, on the other hand, is cost. Mask costs spread across higher volume (multiple SKUs per die) and yield is better for smaller chips. Again, I don't see any process advantage for Intel as of today.

QCOM claims 18B transistors

Qualcomm published benchmarks of its server SoC Centriq 2400. The Spec benchmarks look good compared to Intel Xeon, at least considering price and power. Power seems to be about 40% less than Xeon with comparable performance (according to Qualcomm, that is). Performance per core is quite lower than the Xeons though, so it needs more cores for a similar result. It is manufactured on Samsung 10nm process which seems quite capable, also for high performance applications. The Centriq 2460, the highest end model, integrates 60 MByte cache, which seems quite a lot. Will be interesting to see how it compares in terms of die size to Intel 14nm and Globalfoundry 14nm with AMDs EPYC.

Price seems significantly lower (almost half for the high end one) but this is only when compared to single socket systems from Intel. Taking a dual socket Intel based system with cheaper processors, but ending up in the same performance ballpark, the resulting price, at least for the chips, is pretty similar.

The biggest question will be total cost of ownership, where platform cost and power consumption will be crucial, as well as software issues, since that is an ARM based design. My gut feeling is that it's not quite there yet, especially since Intel just got some real competition from AMD and will likely be forced to lower prices, making the Qualcomm solution even less attractive. It will also be interesting how a similar solution from AMD compares power-wise, when real platforms are available from all three architectures.

Very interesting, indeed. Not sure of Intel's "strategy" of outright buying each possible customer for its foundry business. Their track record with Altera seems not great so far.

It would lead to a powerful position of Intel in the mobile market. There would be a lot of redundancy with its existing comms unit. Intel wasted billions to become a force in mobile. They could have bought Qualcomm in the first place and save all that money. Seems a bit desperate to me, if true.

Here are some initial benchmarks of the new Intel+Radeon combo. Seems decent, though I don't have a comparison to what good discrete GPU solutions, but still not so clunky laptops, provide as benchmark results. Maybe someone can enlighten me.

Edit: And here are some results from Ryzen Mobile. Seems pretty much on par, meaning that AMD can basically deliver the same results with (really) integrated GPU as Intel does with its new combo package. It is a bit early though, so it isn't possibly to compare them in real life applications and also costs.

It could end up that AMD actually provides similar performance in the same form factor as Intel can at a few hundred dollars lower price point (Intel solution said to be for 1200-1400$ laptops, AMDs Ryzen Mobile for 800$ ASPs). Still, AMD would benefit from each of those combo packages Intel sells. Seems like a good deal for AMD.

oh clueless one......you need BOTH the integration scheme and the fabric that ties it all together.

But another SKU with Intel-CPU + Intel-GPU on one die (for the low-power-devices).

Yup, that's also how I understood it from the article I have linked to. I also got it wrong initially, since many headlines claim that it's integrated. The GPU is not integrated as IP but just a separate die on the interposer. As to AMD, no licensing involved, just selling the bare dies to Intel so they can make a tighter package. In the end it helps Intel with smaller form factors for performance laptops in the discrete graphics class and it helps AMD gain market share in that segment since NVIDIA can't provide the same package themselves. Looks like NVIDIA pissed Intel once too often.

This is also the reason why it isn't going agains Ryzen mobile. That's a different price segment (about half as much as those performance monsters). An integrated GPU is much cheaper but also quite slower. It should be less power hungry also, so this Intel+AMD solution is above 15-25W TDP I'd suspect.

Update: This article explains in more detail what the AMD+Intel deal seems to be about. It is not a licensing of AMDs graphics IP but the use of discrete AMD high performance mobile GPUs on the same chip carrier with an Intel CPU, including integration of the graphics memories in form of HBM. This replaces high end solutions in clunky notebooks with discrete graphics, since the package is thinner and more compact. This is good for both, Intel and AMD, since Intel can provide a high end solution for compact notebooks and AMD will likely sell more of its GPUs in high end laptops than NVIDIA. Win-win. Only loser being NVIDIA here.

New Intel Core Processor Combines High-Performance CPU with Custom Discrete Graphics from AMD