News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

amarksp

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

LME inventories of nickel continue to fall, dropping another 606 tons to total 11,286 tons. Deduct another 606 from chart below.

EXPLORATION AND PRODUCTION - GOING FULL CIRCLE

from virtual metals Oct.

The cyclical nature of gold exploration is as regular and dependable as the seasons. We have all seen it many times before. First, the gold price comes out of the doldrums. That is swiftly followed by junior exploration companies deciding that the time is right - thanks to a higher gold price - to go into business. There then is a time lag while they raise (usually very limited) exploration dollars. Once that’s done, they send the geologists into the field. The geologists do their job and return to head office with apparently exciting finds. The junior companies then try to drum up support from those willing to finance full drilling programmes and prefeasibility reports. The banks and brokers either get excited, and then they beat the same drum; or they don’t in which case the junior company moves onto the next street with their story. Of the finds, only a handful (if that) ever get to be designed, funded and commissioned, and quite often this is done in partnership with a more senior established mining company. Inevitably, the process of bringing a mine into being requires project-related price protection, and then the addition to global hedging begins.

Once it has a proven track record, the junior exploration company graduates to full mining company status, and frequently this attracts the attention of the senior companies. Swallowing up a successful junior is often cheaper and more efficient than going through the laborious and expensive process of green field exploration. And so the process of industry consolidation begins. In our experience, by this stage the gold price has gone through a cycle of its own, almost completely unrelated to what the miners might be up to, and - for what could be a multitude of reasons - is by now well off its peak and trading in lower ranges. Once off its highs, the speculative froth and excitement in the market tends to wane, and potential interest in investing in gold companies goes off the boil. The combination of rather dull prices and bored investors fills the industry with increasing lassitude, and even the entrepreneurs who might be interested in gold begin to rethink their strategies. In a nutshell, that’s the exploration cycle, from small beginnings to full boom and eventual shambolic retreat, full of recriminations and mutual disharmony.

Time passes. More than that, it drags, wearily on. The mature mining companies dominate the mining boards on the global stock exchanges. Investors chase off after the latest fad - tulips, IT, dotcoms, you name it. Brokers bemoan the fact that no one is interested in resource stocks. Exploration offices gather dust.

And then, for whatever reason, the gold price pops up again and the whole process begins to repeat itself.

We saw this in the 1980s in direct response to the 1979/80 price rally to over $800/oz. The exploration frenzy that followed was a direct consequence of that rally and the results were probably in proportion to the size of the price rise. The time lag from price rise to project financing (mainly through gold loans) and commissioning was between 5 and 8 years depending where the activity was in the world.

In Australia the time lag was very short. Shallow low grade deposits were quickly delineated and once the project got the go-ahead, there was no expensive or time-consuming shaft sinking. The juniors simply brought the heavy equipment in and removed the overburden. Knowing that the mines were not going to be around for very long, the companies aggressively sold the production forward and secured the contango. If our memories are correct, the record for the fastest mine start up - from go-ahead to first pour - was nine weeks.

In North America, it took only slightly longer but resulted in a huge increase in gold output, especially from the Nevada area. Again the mining companies loaded themselves with derivative products in such vast volumes that, cumulatively, had a dramatic affect on the gold price. Many argue that the very process of derivative usage caused the climate to change and precipitated the prolonged bear market in gold which followed.

Fast-forward to 2004. We are today seeing exactly the same pattern emerging. The gold price turned in mid-2000. The junior companies emerged swiftly. Some returned to the old geological reports shelved in the 1990s, but others went out and raised exploration capital. That is now beginning to manifest itself and the quest for feasibility and start-up capital is now on in earnest.

But will the pattern continue along the same lines as previously? The tune played by the juniors is no doubt the same -listen to the presentations made at the Denver Gold Show and you will recognise the melody. The difference this time is that the bullion banking sector today is far different from what it used to be. Since the last boom times in gold mining exploration and derivative growth there has been a sharp contraction of the number of bullion banks; those that are left are still licking their wounds. This time we sense that the traditional banks perceive the gold business today as a shadow of its former self (which actually at the moment it is) and over the past five years or so have been responding by internally diverting resources and funding to other industries. We now could have a situation where the juniors find they have to knock on the doors of financiers other than the traditional bankers. And there of course lies the opportunity for newcomers into bullion banking.

And where might this new wave of gold production come from? Certainly we might see some new commissions from north and south America. Africa is showing very promising signs. But the regions to watch are China and Russia. Granted, both have obstacles other than geology and mining finance to contend with. This implies either longer development times or higher entry costs or indeed a combination of both; but this is no reason to dismiss these areas of great potential. The political risk involved in going into Russia and China, where currently many junior (and some senior) gold mining companies are placing great faith for the future, is largely a matter of guesswork right now. The investment environments of these two countries is a subject we will return to in a future monthly commentary.

virtual metals Dec report

http://www.virtualmetals.co.uk/Pages/other/GMonDec04.pdf

Nov Report

http://www.virtualmetals.co.uk/Pages/other/GMonNov04.pdf

Nicaragua Politics

The Sad Decline of Sandinista Leader Daniel Ortega

Friday, 18 February 2005, 9:42 am

Column: Council on Hemispheric Affairs

The Sad Decline of Daniel Ortega: Rewriting the Nicaraguan Constitution Once Again, with the Help of Corruption Incorporated, Arnoldo Alemán

• Daniel Ortega, veteran leader of the leftwing opposition National Sandinista Liberation Front (FSLN), and Arnoldo Alemán, former president and leader of the rightwing Liberation Constitutionalist Party (PLC), once again have joined forces, this time in an effort to eliminate Nicaragua’s constitutional separation of powers.

• The joint campaign of Ortega and Alemán to remove President Enrique Bolaños from office, or severely impede the executive branch’s power, appears to have no constitutional basis.

• One might suspect that Alemán has a personal vendetta to settle against the incumbent president, after the former was convicted of money laundering and subsequently sentenced to twenty years in prison by the Bolaños administration.

• Ortega and Alemán have a history of “behind closed doors” negotiations, conspiring to rewrite the Nicaraguan constitution for their own self-interests. However, some observers support these attempts to change the constitution, hoping that these reforms will create more balance among the government’s branches.

• In an attempt to avert a national crisis, Bolaños recently succeeded in petitioning the Sandinista and PLC-controlled National Assembly to temporarily delay its effort to remove him from office, on the basis that the proceedings may be unconstitutional..

• The resulting delay has cleared the way for the formal launching of a national dialogue set to take place among representatives of the country’s major political parties, facilitated by representatives of the Catholic Church and the United Nations.

Opposition leaders Daniel Ortega, head of the National Sandinista Liberation Front (FSLN) and Arnoldo Alemán, ex-president and leader of the rightwing Liberal Constitutionalist Party (PLC), in an attempt to strip President Enrique Bolaños of much of his power, are proposing constitutional changes that, if successful, would considerably alter the framework of Nicaragua’s democracy. On January 10, the National Assembly passed a bill first introduced last November that would change the constitution and remove President Bolaños’ power to directly appoint cabinet ministers, vice-ministers, diplomats and directors of state agencies, thus severely undermining the chief executive’s authority. Bolaños, however, in an appeal for international assistance, has temporarily managed to avert a major crisis by implementing an Accord for National Dialogue to be overseen by Cardinal Obando y Bravo and Jorge Chediek, delegates of the Catholic Church and the UN, respectively. By initiating this endeavor that requires the legislative and executive branches to reach a consensus before any constitutional change can take effect, Bolaños has been able to sidestep the measure recently passed by the National Assembly that would limit his powers. The Dialogue is a clear indication of the lengths Bolaños will have to go in order to preserve what he sees as the nation’s democratic foundations.

An Attack on Democracy?

The recent constitutional reforms proposed by the National Assembly are aimed at crippling executive powers, the one remaining branch of government not controlled by the two caudillos (strongmen) – Ortega and Alemán. The National Assembly, however, possesses no constitutional authority to declare itself an independent body, superior to the other branches of government. Thus, the proposed constitutional change currently being rushed through the National Assembly appears to violate Article 129 of the Nicaraguan Constitution, which states: the legislative, executive, judicial, and electoral powers are independent of each other and they will cooperate harmoniously, subordinated only to the supreme interests of the nation and that which is established in the present Constitution. Since no one specific branch possesses the constitutional power to subordinate, much less eliminate, the autonomy of another, the very notion of the National Assembly usurping the chief executive’s power would arguably alter the nation’s fundamental democratic principles and eliminate the checks and balances that most would argue are needed to maintain harmonious cooperation.

It should also be noted that the proposed PLC-Sandinista constitutional reforms would nullify the vote of the Nicaraguan people, for Bolaños is, after all, a popularly- elected president. However, some independent observers feel that the 1987 constitution drafted by the Sandinistas granted too much power to the executive branch and therefore support the National Assembly’s current reforms. The strength of the executive branch is an issue being hotly contested, especially by those who view Bolaños as “a friend of the bankers” and a man aligned with Washington’s rightwing ideologues. Furthermore, these observers who continually express their discontent would argue that the new constitutional changes are not, in fact, negative. It has become a part of Nicaragua’s political culture for a president to appoint cabinet members and other officials based on “personal favors, business affinity, ideological loyalties, patronage, nepotism and the like, rather than professional capacity,” as was reported in Nicaragua's Envío News Magazine (“Year-end Firework in the Legal Country and the Real One,” January 2005). However, whether or not one supports the proposed reforms, the fact still remains that they are unconstitutional. The removal of Bolaños from office, or even the subordination of the executive branch’s power, violates Nicaragua’s democracy.

Taking it Personally

There is little doubt that PLC leader Arnoldo Alemán has a vendetta to settle against his former vice president, Enrique Bolaños. Following his defeat of Sandinista leader Daniel Ortega in the 2001 elections, Bolaños pledged to rid Nicaraguan politics of corruption – a campaign vow that led to his virtual ouster from the PLC by Alemán and his cronies. In a nationwide anti-corruption campaign that won him much international praise, the president cracked down on his former running mate after a money-laundering scandal involving Alemán surfaced. An investigation by Comptroller General Agustín Jarquín revealed that Alemán had diverted government funds for personal use by purchasing property from impoverished farmers whose parcels had been devastated by Hurricane Mitch in 1999. Alemán’s candid admission that he used public resources on a construction project at one of his private estates, in addition to acknowledging that his personal assets significantly increased during his time as president, promptly led to his arrest.

Alemán’s subsequent conviction on the grounds of corruption has not been well received within the National Assembly, where he has many friends. In October 2004, the Comptroller General’s Office called upon the Assembly to remove Bolaños from office for his failure to disclose the origin of $7 million purportedly used in his 2001 presidential campaign. In reaction, both the FSLN and the PLC requested that unless Bolaños tender his resignation, they would move to impeach him. However, the questionable tactics being used to remove Bolaños, or severely limit the executive branch’s governing power, seems to be a method designed to protect the FSLN and the PLC. Given the dubious history of Nicaragua’s politicians who administered previous reforms, it must be asked: does the current legislative “package” actually further the possibility for a greater democracy, as Ortega and Alemán would argue, or is it merely providing a narrow corridor through which the two caudillos can seize control of Nicaragua’s political processes?

Corruption: A Cornerstone of Alemán’s Presidency

During his presidency, Alemán created an Anti-Corruption Commission in an attempt to disguise the methods that he and his confederates used for diverting public funds. Ironically, this commission was to be headed by then Vice President Bolaños. The anti-corruption attitude adopted by Alemán and his party cohorts, however, only helped to increase, instead of curtail, the growing distrust among average Nicaraguans. While president, Alemán’s governing style – namely the concentration of power in his own hands – frustrated and angered many sectors of Nicaraguan society, Daniel Ortega and members of the FSLN included. Over time, as it became increasingly difficult to unilaterally consolidate power, Alemán had no choice but to look to Ortega and his Sandinista followers for support. Alemán and Ortega began to engage in a series of “behind closed doors” negotiations, from which was spawned their infamous Pacto Liberal-Sandinista, or as it is more commonly referred to, El Pacto.

After several meetings concerning a series of proposed constitutional reforms, a final version of El Pacto was drafted in August 1999 and received the necessary legislative support to become law in January 2000. Alemán and Ortega, by means of the PLC-Sandinista dominated National Assembly, managed to functionally rewrite the Nicaraguan Constitution in pursuit of their own sectarian interests. El Pacto was not solely a strategically planned political alliance that created alternating turns of governance for the two parties at both the provincial and municipal levels, but also contained language devised to ensure immunity for Alemán after his presidency was concluded. Furthermore, these reforms made it extremely challenging for any smaller third party to elect candidates to office, thus greatly undermining a capacity for political competition and participation – both demonstrably crucial for a functioning democracy. The potential threat of greater caudillo control, which seeks to maintain only the appearance of a democracy instead of its substance, presents an extremely difficult challenge for President Bolaños if his power is in fact reduced.

Bolaños Fights Back

In a nationwide television address delivered on December 9, 2004, Bolaños announced that he would strongly oppose the constitutional changes put forth by the National Assembly. Furthermore, the president intends to prove that the methods being used to remove him represent an attempted “coup d’etat,” as stated in a January 7 press release issued by the Nicaraguan Embassy in Washington.

The constitutional referendum proposed by Bolaños, as outlined in the Accord for National Dialogue, is based on a three-pronged political attack that attempts to thwart the National Assembly’s goals by permitting the electorate to vote on key issues. The first tactic seeks to reform the method by which delegates are selected to the National Assembly. The president suggests that Nicaraguans be permitted to vote for their own representatives, instead of having to choose from a list of pre-selected candidates. He is also seeking to ban the re-election of former presidents, such as Ortega and Alemán, in order to counter the institutionalized corruption inherent in Nicaragua’s political system. Giving citizens an opportunity to reject the joint campaign of the PLC and Sandinista “regime” would provide an opportunity to restore the separation of powers that Ortega and Alemán have, in effect, attempted to eliminate. Finally, Bolaños has proposed that any future constitutional changes (like those currently being debated within the National Assembly) only be made via a national referendum.

National Dialogue: A Lasting Solution or another Futile Effort?

It appears that the constitutional referenda outlined by Bolaños in the accord, although strongly opposed by most of the National Assembly, have attracted support from Nicaraguans and members of the international community. This support has helped to pave the way for the formal launching of a national dialogue. A January 18 press release distributed by the Nicaraguan Embassy states that “The eight point Accord [lays] out an expansive agenda for discussion of key political issues…‘professionalization’ of the Supreme Court, the Supreme Electoral Council and the National Comptroller General…commitments to discuss internally democratizing the political parties, and examining the way that delegates are elected to the National Assembly.”

Additionally, the Nicaraguan ambassador to the U.S., Salvador Stadthagen, unsurprisingly observed that “[The accord] is a real testament to the leadership of President Bolaños and the spirit of reconciliation in Nicaragua. We have to congratulate and thank Nicaraguan civil society and the international community, particularly the United Nations, for their constructive role in getting us to this point.”

Nonetheless, the active participation of each of the political parties involved in the Accord will be crucial for resolving Nicaragua’s national crisis; for the time being, however, it seems that the measures to remove the president have temporarily abated. Neighboring El Salvador, Guatemala and Honduras, in addition to Catholic Church and UN delegations, will be paying close attention to what emerges from these sometimes acrimonious debates to ensure that the legal norms of the System of Central American Integration (SICA), an institutional framework designed to facilitate the eventual economic and political integration of Central America, are not violated.

“ Now that the dialogue is starting,” states Stadthagen, “it is absolutely critical for the world to continue watching…this is an ambitious agenda and we will need the world community’s support.” As for Bolaños, who is continuing his struggle with the National Assembly to uphold his democratic vision for Nicaragua, he will ultimately be tested by the political challenges he presently confronts.

This analysis was prepared by Adam Kleiman, COHA Research Associate.

nickel inventories falling sharply here lately... now at 11,892 tons (chart below is as of a few days ago).

"LME stocks fell yet again yesterday, this time falling below 12M tons. With another 564 tons being taken out of warehouse, a total of 11,892 are left. Nearly 30% drop in LME stocks in the last 2 weeks. Last year, LME nickel stocks gradually fell from a high of 24,030 tons to 7,800 tons in July, when they began to recover. Last year on this date, LME had 14,652 tons in nickel inventory."

Loonie ?? Par schmarr...

The Loonie will get at par soon enough against the US$, likely within the next 3 years...

Well I picked up some CLG today at US$1.40 average, after selling all but 100 shares in my trading account...

CLG has a new corporate presentation dated Feb 2005.

http://www.cumberlandresources.com/pres/corp_pres/slide1.htm

Figure if POG goes above $450, then CLG leverage to POG should have it outperform most all HUI components...? CLG still has $37M cash so no risk of dilution anytime soon. 1Q05 should bring release of new feasibility study.

Only near term potential problem would be permitting.

FWIW, one of CC's Top 10 Long Term Holds...

"You all remember Cumberland Resources. It has been a favorite for a long time. It still is. Despite this year problems with higher than expected capital costs at Meadowbank, Kinross took a 10% stake in the company. It is not hard to figure that CLG will eventually become a bargin again with its 4 millions ounces of gold and $50 millions in the bank. It is only a matter of time for the economics to improve at Meadowbank. If you want a safe gold resource in Canada, Cumberland is for you." Dec 2004

see that Clive Maund has started ocverage on RNC Gold... research report dated 1/18/05, trying to get a copy of what this report says..., if someone has read this report, please advise what Maund says about RNC. Thanks!

http://www.clivemaund.com/gold.php

MFN finally making a nice move upward above resistance...?

hopefully that feasibility study is published soon and within my capex and total cash cost estimates...

Endeavour NAV = C$4.69 , selling at 27% discount

http://www.endeavourminingcapital.com/nav.php

I can understand up to a 20% discount, given the performance/incentive fees paid to Endeavour Financial. However EDV ability to participate in PP should offset this 20% fee somewhat, say to 15% maximum discount that I would expect. 27% discount is far too much it seems to me, especially for a stock paying a 2% dividend.

SA golds ‘compelling buy’ - Hathaway

David McKay

Posted: Fri, 11 Feb 2005

[miningmx.com] -- JOHN Hathaway, a fund manager for The Tocqueville Gold Fund, has said South African gold shares are a compelling buy because the rand was unlikely to strengthen further. “I think South African shares are a compelling buy right now because there’s so much unanimity that the rand is going to stay strong,” he told miningmx. “I think there’s pretty good argument to say the rand could weaken quite a bit,” he said.

The South African rand has strengthened from a low of R13 to the dollar in 2001 to its current level of just below R6/dollar.

“The real issue is the rand price of gold, and that could go up no matter what the exchange rate is,” Hathaway said. “I think we’ve seen as much damage to the rand gold price as we’re likely to see based on the exchange rate to the dollar. And I’m extremely bullish on the gold price. I think this is going to be a very positive year for the dollar gold price,” he said.

“I’m the most emphatically positive on South Africa right now that I can remember being in three or four years,” he said.

Hathaway said Placer Dome had been given “a new look” by the opening of the South Deep mine, an operation with resources of about 55 million ounces, and potential to accelerate production. “If I’m right about this being a great buying opportunity in South African shares, particularly in the gold sector at this moment, that has to accrue to Placer to some extent,” Hathaway said.

Commenting on Harmony Gold’s proposed merger with Gold Fields, Hathaway said he was “aghast”.

“I believe Harmony shares were ... almost twice the price before this all started. Granted, the rand has been strong and the gold price has faded a little bit, but I have to believe that a good deal of the pressure on Harmony is related to the possibility that they could issue a lot of stock.

“To me, what looks like a very diluted transaction, so I’m aghast,” he said.

“I like Harmony; I like owning Harmony, and I like Gold Fields. But I don’t see an economic case so far for putting them together,” Hathaway said.

Last year, Hathaway wrote an open letter to Bernard Swanepoel, Harmony Gold CEO, in which he said shareholder value was undermined using either return on capital or shares per ounces produced. Harmony responded claiming the dilutive effects of the deal would be outweighed by R1bn worth of cost savings.

“I’m hoping that this just runs out of steam and that we can go back to normality, whatever that is. I guess my concern would be that at some point along the way he may feel compelled to raise his offer which I think would be very destructive,” Hathaway said.

Hathaway has been running the Tocqueville Gold Fund since 1998 when it was established as a response to the excessive enthusiasm in telecomms and internet stocks. “I made the suggestion, half jokingly, that we set up a gold fund. And so I was given the job,” Hathaway said.

chaos

I've written before about the old Chase FX room motto during Louvre Accord interventions, fade the Bank of Italy. This was not a motto which sprang up the first time the Central Banks intervened but rather was informed by experience. In the aftermath of the quite successful Plaza Accord interventions, standing up to the Central Banks was not initially considered to be a wise move. Over time, however, as the intervention was seen to be ineffectual, market players unlearned their fear of it and came to embrace it as a means to execute trades on their side of the price.

I've been waiting for something similar to happen in the Gold market and I believe I see signs of the ongoing "learning process." One of the reasons I have been so sanguine about Gold's ups and downs over the past few years is that I expect to see its price double, triple and quadruple. What's 20%, I've thought, when I'm expecting 400% or more? In order for that to happen, the market will have to come to grips with and overcome their fear of intervention (or the Central Banks will need to embrace the Gold rally). That process will, of necessity, be a nerve wracking one for Gold investors like myself, as it will involve the market shorting in front of or concurrent with expected intervention only to have the market rise after the initial fall.

I won't claim that this process is near complete but for the all the fears of IMF gold sales and the mass exodus from the Gold shares (more on that later) the price of Gold is almost back at the previously noted $422 level. What is even more interesting to me is that speculative market positioning has changed considerably while the price has barely budged. The overhang of spec longs has largely been worked through.

A few months back, one could argue that the $ short trade was extremely crowded but this doesn't appear to be an accurate characterization at this point. Indeed, the past few months offer an excellent window into market mechanics. The market, in a sense, is the meeting place between the real sector and financial/intermediation or perhaps more appropriately for our purposes, speculative sector. As intermediaries, the spec crowd produces and consumes nothing, they are middle men. While there are times when the speculative sector can drive the real sector, (in the process creating correlations which are seen by some as causal but are eventually proved to be spurious) ultimately the arrow of causation runs the other way.

In other words, if enough Chinese, Indians, Turks, Arabs, etc. etc. all want to buy physical Gold with their ever increasing flow of US$, a substantial long position in Gold in the spec crowd can be worked off with less market effect than would otherwise be the case. It is this demand, combined with inflation fear stoked western private sector investment demand which will make or break the Gold trade. It still strikes me funny to recall the old Nike saying about the Chinese shoe market (2 billion feet) in its application to Gold. I lived for many years in Asia and have a reasonable sense of Chinese culture. For good or ill, Gold is deeply linked with the Chinese sense of wealth, despite the years of Communist "re-education." This linkage of Gold with their sense of wealth and China's continued mercantile policies should keep physical demand brisk from the Middle Kingdom.

Given the volatility in the gold shares, let's revisit the old idea of Gold equities as options. In previous expositions on the topic I've argued that one needs to keep the arrow of causation firmly in mind, i.e. the price of Gold, relative to production costs, is the independent variable, the price of the equities is the dependent variable. This might recall the above discussion of the spec community versus the real sector. Over the past few days, the gold equities have exhibited what seems to me to be classic option trading characteristics. Fears of a return to the old sub $400 range had the equities sinking like a stone in much the same way that low delta soybean call prices will sink like a stone when fears of a drought dissipate. This can be very disconcerting when long soybean calls but such perceptions can change very quickly. Moreover, given the exponential relation of the underlying to the option, or in our case the price of Gold to the equity, in the event that the equities get ahead of the underlying in either direction, price volatility can be extreme.

From my, admittedly biased, perspective, this has been a great week for Gold. It has weathered the fears of IMF sales, and worked off the spec crowd long position without significant losses. Greenspan's wishful musings of an imminently-correcting current account deficit have about as much market credibility as those of the soon to be dropping fiscal deficit. While I wouldn't be surprised to see further intervention and jawboning I think it will become less and less effective. On the policy side, the G7 meeting has come and gone with no resolution to right the imbalances so the driving force will only continue to grow. Maybe a decade from now some aspiring market commentator might recall the good old days when the motto of the Gold market was FADE GORDON BROWN.

Have a good one

Martin M comments...

8:30p ET Tuesday, February 8, 2005

Dear Friend of GATA and Gold:

The Reuters story appended here about IMF gold sales may be most interesting for the observations of the Canadian gold market analyst Martin Murenbeeld, who speculates that any gold sold will be sold to central banks, particularly those with large surpluses of U.S. dollars. Thus the gold would remain in official hands and never reach the spot market but would continue to do its most important work -- remaining theoretically available for dumping by governments and thus

always scaring private investors away from the precious metal.

So would it be better to oppose IMF and central bank gold sales or to support complete dishoarding by central banks and the IMF so they would forfeit a crucial tool of currency market manipulation?

Of course that is exactly why they are not likely ever to part with all their gold.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

* * *

IMF Seen Favouring Gold Sales Over Revaluation

By Lesley Wroughton

Reuters

Tuesday, February 8, 2005

http://www.reuters.co.za/locales/c_newsArticle.jsp;:4208586d:3b951d1b

70c8856e?type=businessNews&localeKey=en_ZA&storyID=7563449

WASHINGTON -- The International Monetary Fund is likely to favour sales over revaluation as it considers ways to use its huge gold cache to help the world's poorest nations without disrupting bullion markets, analysts said.

Finance chiefs of the rich Group of Seven nations asked IMF Managing Director Rodrigo Rato at a weekend meeting in London to report back by April on proposals for using IMF gold reserves to write off debts of the fund's poorest borrowers.

Any such move will require agreement among the IMF's biggest

shareholders, including large gold producers Canada, Australia, and South Africa, and the United States, which looks likely to oppose the proposals.

The global lender's gold stocks are the world's third largest at

103.4 million ounces, worth some $42.3 billion at today's market

prices.

But under a 1971 agreement, some IMF gold is valued at just over $50 an ounce, about a tenth of current prices.

While most analysts think the Washington-based lender's best course would be to sell some of its gold stocks rather than revalue them, it could face powerful opposition.

When trade opened on Monday following the weekend G7 meeting, the possibility of IMF gold sales sent the yellow metal down to October 2004 lows as the market tried to guess the outcome.

Spot gold ended European trade at $413.90/414.70 a troy ounce, after hitting its lowest since mid-October at $413.

Gold analysts bet the gold sale plan would be blocked by the United States, which has enough IMF voting power for a veto and has its own plan for debt relief involving more grant aid.

U.S. Treasury Under Secretary John Taylor said at the G7 meeting the United States was "not convinced" it was necessary to use IMF gold stocks to ease poverty.

The United States holds the world's largest bullion stockpile and gold sales would need the consent of Congress, which together with gold producers opposed gold sales in 1999.

IMF shareholders, however, agreed in December 1999 to an off-market gold transaction of up to 14 million ounces to help finance a global debt relief initiative for poor nations.

British finance minister Gordon Brown has said revaluing the gold could free up billions of dollars to ease debt burdens on the world's poor.

While revaluing the gold stocks would increase the carrying price of the gold on the IMF's books, analysts said, it would not provide cash to fund the debt write-off. It would also come with costs for certain borrowers and shareholders.

Selling part of the gold pot would be more straightforward and would raise money to fund the cancellation of some $11 billion in debt, they said.

Martin Murenbeeld, a Canadian-based gold analyst, said the IMF had the option to bypass the market by selling to buyers such as central banks, which would not affect trading.

He said countries like Japan and China, with their large U.S.

currency reserves, could swallow the IMF's gold stocks "without so much as a hiccup."

"It is not clear the IMF will choose to sell gold," he said. "We'd put the probability of it at less than 25 percent. If it did sell, I think it would do so under the auspices of the ... second central bank agreement on gold."

Under that deal, European central banks agreed to cap their total gold sales at 2,500 tonnes in the 2004-2009 period, compared with 2,000 tonnes in the previous five years.

Murenbeeld said Germany offered an avenue for an official party to sell 112 tonnes of gold this year by announcing in December it would sell only 8 tonnes of its 120-tonne allotment.

Nancy Birdsall, head of the Washington-based Center for Global

Development and author of "Delivering on Debt Relief," said

revaluing the gold would be less politically sensitive but would

lower the IMF's cash balance and stifle its ability to lend to needy countries in the future.

"When it is gone, particularly if it is revalued so that there is a loss on the balance sheet, the heads of central banks of the G7 and other non-borrowing countries will sleep somewhat less well at night," Birdsall said.

"On the other hand, there may be a lot of the world's poorest people who get a bit more education and health services, so that is the trade-off that ought to be made," she added.

gold stock bellweathers looking better...

http://www.investorshub.com/boards/read_msg.asp?message_id=4104671

my busy tax season, not much time for reading or posting, cranking out corporate and partnership tax returns...

FWIW, added to RNC at US$1.03

interesting..., thanks!

The Federal Open Market Committee decided today to raise its target for the federal funds rate by 25 basis points to 2-1/2 percent.

The Committee believes that, even after this action, the stance of monetary policy remains accommodative and, coupled with robust underlying growth in productivity, is providing ongoing support to economic activity. Output appears to be growing at a moderate pace despite the rise in energy prices, and labor market conditions continue to improve gradually. Inflation and longer-term inflation expectations remain well contained.

The Committee perceives the upside and downside risks to the attainment of both sustainable growth and price stability for the next few quarters to be roughly equal. With underlying inflation expected to be relatively low, the Committee believes that policy accommodation can be removed at a pace that is likely to be measured. Nonetheless, the Committee will respond to changes in economic prospects as needed to fulfill its obligation to maintain price stability.

Voting for the FOMC monetary policy action were: Alan Greenspan, Chairman; Timothy F. Geithner, Vice Chairman; Ben S. Bernanke; Susan S. Bies; Roger W. Ferguson, Jr.; Edward M. Gramlich; Jack Guynn; Donald L. Kohn; Michael H. Moskow; Mark W. Olson; Anthony M. Santomero; and Gary H. Stern.

In a related action, the Board of Governors unanimously approved a 25-basis-point increase in the discount rate to 3-1/2 percent. In taking this action, the Board approved the requests submitted by the Boards of Directors of the Federal Reserve Banks of Boston, New York, Philadelphia, Cleveland, Richmond, Atlanta, Chicago, St. Louis, Minneapolis, Kansas City, Dallas, and San Francisco.

thanks

EDV - ho, hum... time to pocket another dividend...

will be interesting to see EDV's NAV as of Jan 31, they own a bunch of NTO stock and warrants..., so much for that NTO takeover rumor though, just another PP

GEORGE TOWN, Feb 01, 2005 (Canada NewsWire via COMTEX) --

Endeavour Mining Capital Corp. ("Endeavour" or "Corporation") is pleased to announce that its Board of Directors has declared a cash dividend of CDN$0.035 per share, payable on February 28, 2005 to shareholders of record at the close of business on February 11, 2005. The Corporation's Board maintains a policy of paying a semi-annual dividend.

another Randy Martin interview

http://www.robtv.com/shows/past_archive.tv?day=thur

8:50 AM ET

AM Business with Kim Parlee

Power Breakfast

Randy Martin, president and CEO, RNC Gold

Duration: 5 m 41 s

LCC going into full torque overdrive mode... up 18%

Martin M

VANCOUVER--(Mineweb.com) The chief economist for Dundee Securities suggests that a new central bank agreement, heavy reliance on the U.S. dollar by Asian central bank portfolios and dehedging should all continue to be positive for gold.

In a presentation Wednesday to the Mineral Exploration Roundup in Vancouver, Economist Martin Murenbeeld predicted that the medium-term outlook for gold is positive because of macroeconomic and supply/demand factors, such as further decline of the dollar, and higher debt levels that will pressure monetary policy to remain relaxed in the medium to long term.

Dundee's base scenario suggests an average gold price of $461 per ounce this year. The company's more bullish scenario puts a 35% probability on a $506 average.

"The U.S. trade account is deeply in the red with the number of key countries," according to Murenbeeld. The U.S. trade deficit with Japan is around $70 billion, in excess of $100 billion with the Euro area, $65 billion with Canada, and $150 billion with China. "Indeed, the current account deficit throws off about $2 billion a day on foreign exchange markets, which have to be absorbed," he explained.

Murenbeeld, who called himself a "dollar bear," said, that using 1985-87 as a guide, he believes the dollar "has at least another 15% to fall." When interest rate hikes in 1987 'led directly to the stock market crash in October of that year," the dollar did not bottom until it "became clear that the U.S. current account deficit was finally turned around," according to Murenbeeld. "Gold, meanwhile, continued to rise right through the interest rate hikes, topping out only when the dollar bottomed."

Dundee Securities feels that the current upturn in the dollar will prove to be a "correction," and that the dollar will remain in a downward channel. "If so, we would expect gold to remain in an upward channel," according to Murenbeeld. He predicted that the next major move in the dollar "should come at the expense of the Asian currencies in general, and the Chinese Yuan specifically."

Murenbeeld theorized that since the U.S. economy has excess capacity, "the Federal Reserve will not want to tighten monetary policy too much." Since it is believed that the world economy suffers from too much capital and labor capacity and too little demand, he explained, "economy policy is well advised to remain somewhat loose. ...Loose policies that are designed to reflate demand are good for gold."

Meanwhile, the U.S. had a deficit of $413 billion as of September 2004 while total U.S. debt has risen to nearly 200% of GDP. "The last time the debt level was this high was during the Great Depression when GDP contracted sharply," he declared. Budget deficits also lead to concerns about overall debt. "The household sector is also carrying record debt," Murenbeeld said. "In the event interest rates rise significantly, the service burden will take a record bite out of disposable income."

"Even the U.S. net financial liabilities are set to double over the next 25 years, and it could be worse in the event the U.S. government cannot control its budget deficit in the coming years," Murenbeeld said. He suggested that the government must choose among several options including putting more financial responsibility on the household sector, cutting services, and printing more money.

Murenbeeld believes that the new Central Bank Gold Agreement (CBGA) involving 15 nations offers advantages such as market transparency, the continued absence of uncertainty and fear of central bank gold sales, higher gold prices for official sales, and benefits for producing countries in Africa and elsewhere. "The agreement did increase the amount of gold to be sold each year," he noted, adding "in light of gold returning by the way of dehedging, I believe the market can handle the increase."

Murenbeeld suggested that Asian central bank reserves represent a potential source of future gold demand. "A small shift in these countries' preference to gold (lessening their dependence on U.S. dollar reserves) could represent a dramatic new demand for gold," he said. For instance, if China were to adopt the 15% rule for gold as a percent of reserves as the European Central Bank as decided, China could buy 7875 tonnes of gold, he added.

In the meantime, a decline in mine production output has resulted from the weakness in gold prices in recent years. "This is a positive for the medium-term gold price outlook," he declared. As gold producers are dehedging, "there is a positive impact on the gold price, but the 400 or so tonnes annually dehedged adds only about $20-$25 to the gold price," according to Murenbeeld. Therefore, dehedging has not been the main driver of gold prices in recent years, he suggested.

Another positive factor for gold in the medium term is the competition that has developed among gold bullion investment products including the World Gold-sponsored gold ETF on the NYSE, Murenbeeld stated. Meanwhile, "the tremendous wave of gold liberalization that is sweeping South Asia is bound to have a positive impact on gold demand," he declared.

Did you ask how they were exercised...? That is, did SouthGold shareholders exercise them outright for cash in whole or part, or did GBN find an institutional investor for these shares...?

Please advise.

Magic-Carpet News-Ride

check out this newsmap..., by country.

http://www.marumushi.com/apps/newsmap/newsmap.cfm?layout=0&selected=au,ca,in,uk,us&categorie...

Well a larger operation at Burnstone would be good news:

"GREAT BASIN SIGNIFICANTLY EXPANDS BURNSTONE RESOURCES

Almost 120,000 metres of drilling over 2 years at Burnstone has outlined 7.3 million ounces of gold within measured and indicated resources of 45.1 million tonnes grading 4.99 g/t - an increase of 36% from resources used for the Area 1 pre-feasibility study. Inferred resources doubled. A feasibility study for a larger operation is planned in 2005."

A problem with Burnstone is you have 7.3M ounces but original pre-feasibility study had only 236K ounces of production/yr. Hence, a 30 year mine life. Economics would be greatly improved if GBN could figure a way to produce 700K ounces/year and thus a 10 year mine life... Capex would be increased but payback would be much quicker.

Further, 500K-700K ounces/year production would make Burnstone a much more attractive takeover target for a major.

Remains to be seen whether a larger operation is in fact feasible, but at least GBN is thinking in the right direction. For Burnstone thin reef mining, it may take some creative engineering to figure out a better way to mine this deposit, seems the original design was very labor intensive because of the difficulty in mining this thin reef.

Just a few days left before those SouthGold US$.75 warrants are exercised, Jan 31 expiry. Will be interesting to see whether GLG/GBN has large volume these next few days, or not. More interesting will be whether Director Rob Still/SouthGold SA Trust increases its 12%+ position or not with this warrant exercise.

larger operation mentioned here:

http://www.hdgold.com/i/pdf/hdi-jan2005.pdf

What they should be producing now!! Note their annual production forecast for 2005 is 100K or 25K per quarter. Thought 24K was achievable for 4Q04...

La Libertad had problems continuing from 3Q so Oct production was weak there, was back on track at the end of the quarter. Bonanza hit some lower grade ore in the 4Q but should be getting normal/better grades in 1Q05 and beyond.

Iraq

After the Election

By George Friedman

It is now a week from the Iraqi elections. Apart from knowing the precise levels of violence the insurgency will be able to reach before the election, most of the rest of it is clear. The election will be held. In much of the Sunni region, the turnout will be extremely low -- low enough that the election might be suspended there. The Shia will win. The United States could choose to suspend the elections -- and there should be no mistake about who is making the decisions on this -- but the point for that has passed. If the elections were going to be postponed, one would think that Washington would have made that decision weeks ago.

The next decision that will have to be made is whether to certify the election. There is not much choice there either. Washington knows the vote in the Sunni region will be disrupted. To hold the election and then fail to certify it because of the guerrilla war makes no sense. The guerrilla war has been there for a long time now. If you are going to hold the election anyway, not certifying it would be an exercise in futility.

If the vote is certified, a government will be formed. The Shia will dominate that government. They would have dominated any government for simple demographic reasons. With the Sunni vote suppressed, they will dominate the government overwhelmingly. The United States has proposed in the past some artificial formula to guarantee Sunni representation in the government, a substitute for an election, but the Shia have rejected it. Moreover, if the United States allowed the Sunnis to take a full seat at the table in spite of their inability to suppress the insurrection, there would be zero incentive in the future for Sunni elders to take a chance. Undoubtedly, some sort of contrived Sunni presence will be inserted, but this will be a Shiite government.

Thus, at some point in February, a Shiite prime minister, governing through a predominantly Shiite Cabinet, will become the government of Iraq. The Shia have been waiting for this moment for decades. Although divided, the formation of a government that reflects -- or over-reflects -- Shiite power will be a moment of enormous triumph. The evolution of this government is unclear. It could evolve into an Iranian-style theocracy, although the Iraqi religious leaders seem to take a different view of this than the Iranians. It might be ruled by Islamic principles without the overtly theocratic elements. It could even be, for a time, formally pluralist or secular. Whatever it will be, it will be Shia, and it will be under the heavy control of the religious leaders.

The first problem the new government will face will be the Sunni uprising. Sunni guerrillas recently killed two of Grand Ayatollah Ali al-Sistani's aides. They have been conducting a fairly one-sided assault against the Shia for months. The reasoning behind the attacks appears to have been to intimidate the Shiite leadership prior to its taking power. What they have done instead is infuriate the Shia. The Shia have suffered from suppression by the Sunni-dominated regime of Saddam Hussein -- Sunni by birth if not by religious principle. They have been the dispossessed. It is now their time.

The Shia understand they cannot simply remain in a defensive mode. They have been passive in the run-up to the election, but after the election their credibility as the government of Iraq will depend on how they deal with the guerrillas. They must either suppress the guerrillas or negotiate a deal with them. Since a deal is hard to imagine at this time, they will have to act to suppress them. If they don't, the government will either be destroyed by the insurgents or Iraq will split into two or three countries, an evolution unacceptable to the Shia or to Iran.

Therefore, the Shia will fight. The Shiite leadership has made it clear it wants the United States to remain in Iraq for the time being. This does not mean it wants a long-term American presence. It means it wants U.S. forces to carry the main battle against the Sunnis on its behalf. In the same way that al-Sistani wanted the Americans to deal with Shiite leader Muqtada al-Sadr during the An Najaf affair, he wants the Americans to carry the main burden now.

The United States is prepared to carry a burden, but it is not prepared to single-handedly deal with the Sunnis any longer. The Shia have substantial armed militias. It is these forces -- not the failed Iraqi army the United States has tried to invent -- that will be the mainstay of the regime. The Shia don't want this force ground up because it is the guarantor of their security. The United States is not going to protect the regime without these forces engaged.

At this point, something interesting happens. The Shia have a greater vested interest in the viability of this government than even the Americans. The Americans can leave. The Shia aren't going anywhere. For the first time, the United States has a potential ally with capabilities and motivation. Most important, it is an ally that is not blind on the ground. Its intelligence capability is not perfect among the Sunnis, but it is better than what the Americans have.

It is an opportunity for the Americans. It is hard to get excited any longer about opportunities. We have seen so many open up and either prove chimerical or be fumbled by the United States that we temper our enthusiasm in all things. Nevertheless, the Shia will be the government for the first time; they have been waiting for this; they owe the Sunnis a beating and they might, with the United States, have the means to deliver it.

In all of this, the role of Iran is the most complex. The Iranians supported the Shiite community throughout the post-Desert Storm period. During the first phase of the American occupation, the two Shiite communities were close. Since the events of April 2004, the long-term wariness between the two communities has returned. Iran might not be as enthusiastic as it once was to see a Shiite government in Iraq. Alternatively, Iran could use its ongoing influence to manipulate and control that government.

It is no accident, in our view, that Washington is beating the war drums against Iran in the weeks before the Iraqi election. It is not only about nuclear weapons or not even about them. It is warning the Iranians not to intrude into Iraqi affairs. The Iranians might listen, but it's unlikely. Iraq is a fundamental national interest of Iran, and the Iranians will be playing.

Thus, the election brings a new government with new interests and new crises. If the government is seated, and we can't see why it wouldn't be, the next thing to watch is what steps it takes with its militias against the insurgents. Certainly, the guerrillas will be hitting them hard, so passivity is not an option. The Iranians will be manipulating the government and the Americans will be squeezing it. But it is at this point that something might finally, if temporarily, break in favor of the United States. Certainly that is the bet Washington is making.

chaos snippet

All of which brings us the the meat of today's essay. China, Japan and much of the rest of the Asian nations have long been unwilling to give up on their mercantile polices. With Europe now unwilling to take the hit on their external account, I think it quite possible the $ could easily stay stable or even rise in the FX markets, but fall vs. goods and services, which include Gold and Silver. It looks as if the old "beggar thy neighbor" policy is no loner a viable option. This doesn't mean that the force of truth, if you will, is no longer operating, rather that it will simply work on a different, but related vector- a vector that is much more likely, in my opinion, to resolve the imbalances.

When Stephen Roach of Morgan Stanley writes about the need to adjust relative prices through exchange rates he is hoping that such changes will change the relative savings and consumption ratios (a cheaper $ is hoped to raise US savings and reduce consumption while coincidentally raising foreign consumption relative to savings). However, the US manufacturing base is so hollowed out that it would take a very cheap $ over a very long period of time to induce the change, even if the foreign CBs were amenable to such a plan, which, as noted, they appear not to be. Rather than that long and difficult path, it seems to me that a global inflation, with the US leading the pack, would be a quicker solution. In that event, Gold, other precious metals and commodities, not foreign currencies, would be the best way to denominate savings.

In a sense, what seems to me to be happening is a very circuitous method of debt monetization. The US isn't simply buying its own debt with newly printed currency, foreign Central Banks are doing their dirty work for them-buying US government debt with export receipts. Unless people believe the US plans to recover those receipts through trade, or by keeping the world safe for capitalism, they are just funny money. However, with the Neo-Con faction currently in charge pushing for more war, prospects of a resolution of trade imbalances look slim. The Jan 30 proposed Iraqi elections loom large as a potential pivot point. If the US can't leave Iraq because violence persists after the elections, while oil prices continue to climb, the game of $ hot potato may begin in earnest. This game may not be so easily played as in the recent past, though. Dollar alternates, if you will, are not equal.

thanks!

Nicaragua Politics

U.N.-brokered accord avoids 'coup' in Nicaragua

By Tom Carter

THE WASHINGTON TIMES

Published January 22, 2005

A uneasy calm has settled over Nicaragua after an agreement brokered by the United Nations and a Catholic cardinal rescued President Enrique Bolanos from a "constitutional coup" that would have stripped him of most of his powers.

"We are in a holding period," said Manuel Orozco, Nicaragua specialist at the Inter-American Dialogue, a Washington-based policy group.

Nicaragua's democracy came under assault when former President Daniel Ortega and his cadre of supporters in the Marxist Sandinista party joined forces with insurgents in former President Arnoldo Aleman's Liberal Party.

The effort was intended to end an anti-corruption campaign championed by Mr. Bolanos by gutting the office of the president.

The "two caudillos," or bosses, as Aleman and Mr. Ortega are known in Nicaragua, are cynically using each other at the expense of the Nicaraguan people for their own personal and political gain, said a senior U.S. State Department official on the condition of anonymity.

Aleman, convicted of stealing millions of dollars while president, is for the moment allied with his former enemy, Mr. Ortega, who has managed to place Sandinsita judges on the Supreme Court.

The court released Aleman from a 20-year prison term, imposed after he was convicted of stealing $100 million, to a comfortable house arrest at his luxury ranch outside Managua.

Mr. Ortega and Aleman then joined to sponsor legislation that would have stripped the presidency of most of its power.

On Jan. 12, a constitutional crisis was averted when Cardinal Obando y Bravo, U.N. representative Jorge Chediek, Mr. Bolanos and Mr. Ortega announced the "Accord for National Dialogue," which keeps new measures restricting the president from going into effect.

Nevertheless, the Sandinistas, with the backing of Aleman, have gained "virtual control" over the legislative and judicial branches of the Nicaraguan government, according to Salvador Stadthagen, Nicaragua's ambassador in Washington.

"The Sandinistas are in the best position they have been in since 1989 or 1990, to win the presidency [in 2006] ... both sides are being played by Daniel [Ortega]," the U.S. official said.

"The democratic forces have to realize that they have more in common than what divides them," the official said. "The Sandinistas' ability to use the judicial process" to punish enemies and reward their friends is paralyzing the country.

Nicaraguan citizens continue to support Mr. Bolanos.

In a recent poll by M&R, published in the El Salvadoran newspaper La Prensa Grafica, 77 percent of those surveyed disagreed with Mr. Ortega's statement that the time had come to "put an end to the current administration."

The Sandinistas, led by Mr. Ortega, have never won the Nicaraguan presidency in three elections since being forced to the ballot box by the U.S.-backed Contras in 1990.

But the Sandinista party retains a substantial following, consistently winning about 40 percent of the vote in each national election.

It lost the presidency first to Violeta Chamorro in 1990, Aleman in 1996 and then to Mr. Bolanos in 2001, who won with 56 percent of the vote.

The difference in 2006 is that 40 percent of the vote may be enough to give Mr. Ortega the presidency this time if Aleman supporters continue to work with the Sandinistas, analysts said.

Thanks, did not see that press release.

Nonetheless, the most important factors for RNC are:

1) Produce over 100,000 oz/year in Nicaragua at under $270 total cash cost

2) Acquire San Andres/Honduras for under 8M shares plus assumption of under $7M debt and get this into production in 1Q 2005 at 75,000 oz/yr at under $260 total cash cost.

I was disappointed with the 4Q04 production results, really thought RNC would be at around 24K ounces for the quarter rather than at 20.6K ounces. FWIW, my understanding is RNC mine managers have committed to achieving 70K ounces at La Libertad and 30K ounces at Bonanza for 2005, and this is what their bonuses are based on... I believe 100K ounces is still sandbagging, La Libertad should be capable of producing 80K ounces and Bonanza 36K ounces if everything goes right. Everything does not go right, so I am using 106K for my model.

I am using 74K ounces for La Libertad and 32K for Bonanza in my models=106K ounces total for Nicaragua. Assuming San Andres closes by 1Q05, total production should be 162K ounces for 2005.

tend to agree that CKG is overvalued, but Randy runs CKG just like Francisco, i.e. like a bank...!!@!, and substantially different than all other gold explorers that are dependant on PP for funding. With CKG, interest income funds all exploration and other expenses, if it utilizes same business model as Francisco, and it likely will. If POG goes ballistic and drill results satisfactory, then and only then will CKG raise more money (i.e. at higher CKG stock price, e.g. over $10) to generate more interest income to fund more exploration/development, again like Francisco.

Thus, there are only 2 ways CKG will decline substantially in value:

1) CKG does not hit on its initial exploration drill results.

2) CKG share price rises substantially in price and Randy decides to issue a new PP.

Given CKG business model, i.e. run like a bank and CKG actually has positive EPS via interest income, it truly is unique in the gold exploration industry and does not participate in the Canadian 2 Step PP Game.

I am not buying more CKG at this price, but if I owned none I well might. Also, given CKG is one of my larger positions, I may well sell 25% or so if/when its first drill results come out positive. CKG may well be overvalued right now, but it will become even more overvalued if they have decent first drill results...

Nicaragua Articles again

Crisis averted

Nicaragua's ambassador is relieved that his government stopped a power grab engineered by the leader of the country's former Marxist rulers.

"A full-scale constitutional crisis was averted in no small measure due to the fact that the world was watching," Ambassador Salvador Stadthagen said yesterday.

Mr. Stadthagen urged foreign leaders to continue monitoring an agreement reached between President Enrique Bolanos and Daniel Ortega, the leader of the Sandinista Party, which tried to strip the president of much of his power.

"Now that the dialogue is starting, it is absolutely critical for the world to continue watching," the ambassador said. "This is an ambitious agenda, and we will need the world community's support."

The agreement was reached last week after Jorge Chediek, an envoy from the United Nations, intervened. The deal was overseen by Cardinal Miguel Obando y Bravo, who gained international respect in the 1980s by standing up to the Sandinistas' authoritarian regime.

The agreement basically stops the National Assembly, controlled by opponents of Mr. Bolanos, from unilaterally imposing constitutional changes, and it gives the president the option of accepting or rejecting any proposed limits to his authority.

"This accord is a real testament to the leadership of President Bolanos and the spirit of reconciliation in Nicaragua," the ambassador said. "We have to congratulate and thank Nicaraguan civil society and the international community, particularly the United Nations, for their constructive role in getting us to this point."

The dispute grew out of Mr. Bolanos' anti-corruption campaign that ensnared former President Arnoldo Aleman. Aleman was sentenced to 15 years in prison and later released by the Sandinista-controlled Supreme Court.

He is under a comfortable house arrest at his ranch outside the capital, Managua. Aleman enlisted the aid of his Liberal party supporters in the legislature to join the Sandinistas and form a majority of lawmakers in opposition to Mr. Bolanos.

_____________

Petroleum World

• Nicaragua's president, Enrique Bolanos, avoided a de facto coup last week only by striking a deal with former Sandinista ruler Daniel Ortega, who has threatened to use a corruptly assembled alliance to alter the constitution and transfer power from the presidency to the Sandinista-run legislature. Though polls show that an overwhelming majority of Nicaraguans oppose him, Ortega is closer to regaining power than at any time since Nicaragua rejected his Marxist dictatorship and returned to democracy in 1990.

____________

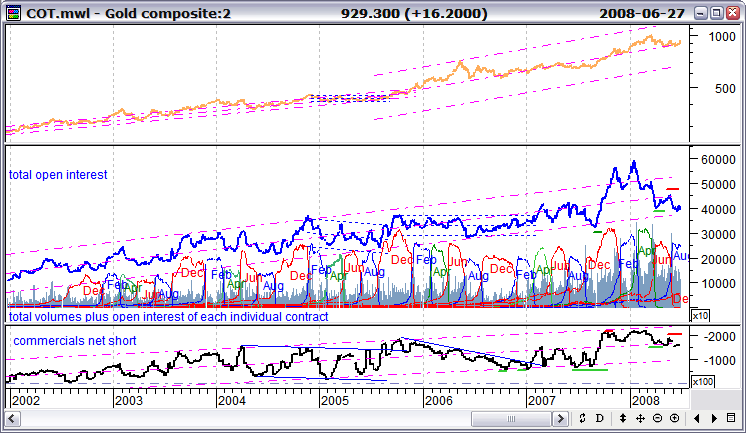

Louis COT Charts-auto updated to current week

"so, your post will be updated with the new charts once they are out of the server's buffer.<g>"

guess I am waiting on the server buffer...?

got a new home for your charts...

http://www.investorshub.com/boards/read_msg.asp?message_id=5191980

remember, timeliness next to godliness...

Nicaragua: Largest gold endowment

By: Dorothy Kosich

Posted: '21-JAN-05 05:00' GMT © Mineweb 1997-2004

RENO--(Mineweb.com) Nicaragua may well generate "the largest gold endowment in Central America says Meridian Gold President and CEO Brian Kennedy.

On Thursday at the Informed Investors Forum Kennedy praised Nicaragua's "upside potential', saying he believes "huge potential" exists at Radius Gold's El Pavon project, located in central Nicaragua. In a joint venture, Meridian has agreed to make at least US$3,500,000 in exploration expenditures over the first two years of the agreement with the objective of establishing a resource of at least 1,000,000 ounces that can subsequently be developed into a mineable reserve.

Kennedy said Nicaragua offers "large areas of prospective volcanic terrain," which have been under-explored by modern exploration methods.

Meridian is striving to be a one million ounce gold producer by 2008 with cash costs of below $150/oz and a project resource life of 10 years. Kennedy said Meridian will continue to adhere to its policy of organic growth, which has cost $28/oz to find gold in contrast to acquisitions, which currently run more than $100 per ounce of gold acquired.

Nicaragua Politics Article

National Dialogue Starts to Deal with Crisis in Nicaragua

Managua, Jan 19 (Prensa Latina) A national dialogue will begin Wednesday to try and solve the crisis among the Nicaraguan state powers and institutions, without having solved the fundamental differences between the government and majority parties.

The Presidential House protested again Tuesday because the Parliament published the Constitutional reforms, a regulation reserved for the Executive power by law.

A press release clarifies that consensus about the reforms was not reached either, as was agreed upon in a previous meeting among the sides.

Negotiators for the FSLN (Sandinista National Liberation Front) and PLC (Liberal Constitutional Party) announced they “are ready to talk to government authorities face to face.”

The single-chamber Congress chairman Rene Nuñez said confidence and communication among the sides are key for a positive national dialogue.

The FSLN member confirmed that his party´s agenda is aimed at finding a solution to the serious social problems, unemployment, and poverty that affect most people in the country.

He said what is important in the first meeting, which was scheduled for Wednesday afternoon, is to reach an agreement in an effort to favor Nicaraguans and their national sovereignty.

Although liberal Deputy Enrique Quiñones said Tuesday the PLC is willing to “make progress in the talks,” he asserted that their beginning would be a “political show.”

He also said his organization´s delegation expects everything will develop seriously and honestly, but warned that President Enrique Bolaños has refused to tackle the problems affecting the population and prefers to discuss constitutional reforms.

Sources revealed that the negotiation table will be established in Managua´s Catholic University.

Cardinal Miguel Obando appointed Monsignor Eddy Montenegro as observer and liaison among participants.

--From Prensa Latina

________________

Russia welcomes Nicaragua national dialogue agreement

20.01.2005, 13.14

MOSCOW, January 20 (Itar-Tass) - - Russia welcomes the signing of the agreement on a national dialogue with the participation of the main political forces of Nicaragua, spokesman for the Russian Foreign Ministry Alexander Yakovenko said on Thursday, answering the question by Russian mass media regarding the situation in Nicaragua.

According to the diplomat, the successive implementation of the document “will promote the formation of the favourable socio-political climate and strengthen stability.” Russia “has invariably supported the Nicaraguan government’s steps aimed at achieving such aims, and will continue to support this line,” Yakovenko said.

The agreement was signed on January 12 by President Enrique Bolanos of Nicaragua and General Secretary of the Sandinist Front of National Liberation Daniel Ortega who acted on behalf of the united opposition.

Buffett sees US$ going down

19/01/2005 21:33 - (SA)

WASHINGTON - The dollar cannot avoid further declines against other major currencies unless the US trade and current account deficits improve, legendary investor and businessman Warren Buffett said.

"I think, over time, unless we have a major change in trade policies, I don't see how the dollar avoids going down," the world's second-richest individual told CNBC television.

"I don't know when it happens. I don't have any idea whether it will be this month or this year or next year, but we are force-feeding dollars on to the rest of the world at the rate of close to a couple billion dollars a day, and that's going to weigh on the dollar."

Buffett noted the record US deficit of $164.7bn in the third quarter of 2004 in the current account, which measures trade and investment flows.

Buffett, nicknamed the Oracle of Omaha for his investment acumen, has a net worth of some $41bn, second only to Microsoft chief Bill Gates, according to Forbes magazine. But he said he saw few opportunities in the near term.

"I'm having a hard time finding things to buy, if that says anything about the market," he said.

"If I find something ... tomorrow to buy, I don't give a thought as to whether the market is going up," he added. "I barrel in."