News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

CSKH - waiting for the sun to shine

up-down

![]()

![]()

CSKH - waiting for the sun to shine

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

CSKH - waiting for the sun to shine

The news is good enough for me

I'm going to whack NITE's .0256 offer for 100k!

I'm calling his bluff, I'll bet he throws me on the bid for support.

If he does its a sure sign they're ready for the pps to move north

NITE offering .0256, what a joke

bidders getting fills, amazing.

Sellers should NOT fill bidders, LET THEM CHASE

If this PR won't move the pps nothing will

"...As we close the month of May with more than $7 million in closed sales for 2011..."

There is no way they would outright lie about this. This $7M will be in subiquent 10Q's

CSKH's stock should preform nicely in 2011

.025 appears to be solid support, .03 should fall this week!

It stands to reason more news will follow to confirm all these "we're going to" do $7M dollars worth of solar installations.

Yet here we are stuck at .025 cents. Decent volume, yet all trades are matched. Until those willing to sell below .03 dries up we're stuck here I'm afraid.

Is this EVER going to turn up?

I have no problem with the residential work. It may take more jobs to get substantial revenues but they appear to be doing it. Verifiability will come in the upcoming quarterly reports. Prior to that they could just tell us. Imagine if they state "X" revenues booked in a PR and its not in the Q - The stock would be toast. They would never knowing lie like that.

If they are telling the truth with $7M in jobs signed and the work is to be carried out as permitting etc allows, we're going to be alright here.

I would hate to bail and look for greener pastures only to see this rocket once I pulled out. I think they are trying really hard to gain diversified business so there can be no future repeats of the Q4 debacle. (The G&S commercial jobs we're just to good to be true)

fingers crossed

Huge upside if they deliver.

We longs have really been put the wringer here with forward looking statements not coming to fruition. Ezra better not be blowing smoke this time!

I'm looking forward to a PR announcing completed work. Sooner or later they have to produce something concrete, Then the pps will adjust appropriately.

I left this morning seeing AUTO on the best offer at .025 (another investor throwing in the towel)

whats with the 6am PR's?

Peeps are still asleep at 6am. Penny stocks need 9 to 9:30am PR's when traders are looking for news.

Only 5 prints on stellar (but unverifiable) news in the 1st hour of trading - sheesh.

good post, primed and ready. All they need to do is EXECUTE.

I hope its has some solid meat to it.

The recent PR's have been good but the their effects on the pps have been nil.

05/17/2011 6:00AM Clear Skies Backlog Grows

05/11/2011 6:00AM Clear Skies Sign 162 KW Contract

05/04/2011 6:00AM Clear Skies Solar Receives Patent

good post mkendra. The ibox has been undergoing changes and I hope everyone finds it to their liking.

Most potential investors want to know the share structure, revenues if any, and to see to some charts before DD'ing the recent news and SEC filings. All of these are front and center. Further down is more basic info about the company, its officers, and the rate at which they issue stock to fund the company since they are not yet profitable.

Most current shareholders just keep ibox's closed, especially if they are just over stuffed as many are with entire PR's reprinted and way too many photos.

Its not overloaded but it does cover the basics with many links for further reading.

Ihub still shows no news for CBAID

http://ih.advfn.com/p.php?pid=squote&symbol=CBAID

but once the D comes off the news section in the ibox will be fixed.

that looks brutal on a non-logarithmic scale

Hopefully we can get this moving north next week. The sun is sure strong this time of year!

What Does Chill Mean?

Special restrictions that can be placed on a given security by the Depository Trust Company (DTC). Chill restrictions are intended to limit the potential for problems within the financial marketplace, and can be placed on a security for various reasons.

Investopedia explains Chill

Owned by many financial companies including the New York Stock Exchange (NYSE), the DTC acts as a clearinghouse for stock exchange securities, settling trades in corporate and municipal securities. If the DTC has cause to be concerned about a specific security currently processed through its system, it may place a "chill" status on the security. This will restrict brokerages' ability to transfer the shares or units of the security through DTC until the security's issues are cleared up or it ceases trading on the market.

--------------

That was some good DD Pick _M_Low. It looks like this Chill has cost shareholders close to millon dollars already! (Because thats who will be paying this bill)

The Company has been forced to negotiate settlement agreements with its existing

investment bankers to settle alleged breachs of contract as a result of this DTC chill and

the unavailability of DTC electronic transfer for chilled Company shares. Such settlement

agreements have already cost the Company approximately $820,000 in damages.

Nasty candle today

Not much bid support and large orders on the offer are making it hard to gain ground, even in the light of the recent news stating they have boat loads of work. We need something concrete from management. $6M in new work for 2011 is wonderful. The question is will it actually materialize. If it does, faith will be restored.

hitting .03 today (white candle) would prove the direction

.03 today!

Well its registered in Delaware along with the parent company and carbon 612

https://delecorp.delaware.gov/tin/GINameSearch.jsp

4472639 CLEAR SKIES SOLAR, INC. Incorporation Date / Formation Date: 12/12/2007

4593269 CARBON 612 CORPORATION Incorporation Date / Formation Date: 09/10/2008

4937977 CLEAR SKIES FINANCIAL CORP. Incorporation Date / Formation Date: 02/08/2011

A tall white candle

I can envision three in a row!

one of the problems is management's penchant for releasing PR's 3 1/2 hrs before the open.

I'm certain PR's released at 9:25am would have a far greater impact

yeah, some 900k in volume yesterday and nadda movement.

good luck on your future plays.

that 5k brush stroke was mine, lol.

guess they didn't need it on these new jobs

"...These projects are cash deals to CSS being financed by the clients themselves. Realizing the financial benefits of investing in solar, the clients decided to fund these projects internally and gain the benefits that come along with owning solar energy systems in New Jersey..."

"...CSKH) today announced the formation of a new wholly owned subsidiary, called Clear Skies Financial Inc., to fund the Power Purchase Agreement or PPA of smaller high volume projects the Company has pending in its pipeline of business..." 2/17/2011

"...Our investors have delivered LOIs that represent the funding of the CSS Power Purchase Agreement (PPA). These 5 agreements total 457.50 kws of commercial projects brought in under our new-expansion program. These projects represent approximately $2 million which is in addition to what we have announced in the last several weeks," said Ezra Green, CEO of Clear Skies Solar..." 2/23/2011

-----------------

if you are new to the industry it might be hard wrap your head around how Solar Power deals are structured. One of the common ways commercial, and increasingly residential customers, buy solar power or other renewable power is through something called a Power Purchase Agreement (referred commonly as a PPA). That is to say, they buy the power generated by the solar panels, but they don’t necessarily own the solar panels on their roofs.

http://blog.cleantechies.com/2008/06/06/explaining-ppa-financing/

--------------

A Power Purchase Agreement (PPA) is a legal contract between an electricity generator (provider) and a power purchaser (buyer). Contractual terms may last anywhere between 15 and 20 years, and during this time the power purchaser buys energy, and sometimes also capacity and/or ancillary services, from the electricity generator. Such agreements play a key role in the financing of independently owned (i.e. not owned by a utility) electricity generating assets. The seller under the PPA is typically an independent power producer, or "IPP." Energy sales by regulated utilities are typically highly regulated by local or state government, so that no PPA is required or appropriate. Commercial PPA providers can enable businesses, schools, governments, and utilities to benefit from predictable, renewable energy.

http://en.wikipedia.org/wiki/Power_Purchase_Agreement

what party-pooper dumped 79k at the .0251 bid.

ok lets close this at .0285

decent news and we're only up .0001 - unreal

maybe they bought it to kill it

"...Total’s sales last year came in a tad over $211 billion, while SunPower’s cracked $2.22 billion. Simply put, the solar company is roughly 1/100th the size of its soon-to-be majority owner...."

5 MM's in front of .03 (depressing)

no .03 prints today I'm afraid. We need a mud horse to get us through this quagmire.

UCLA Study: Solar on L.A. Rooftops Could Power Whole City

Posted on March 18th

A new study released by UCLA’s Luskin Center for Innovation shows that Los Angeles County homes are prime real estate for solar installations. In fact, they could potentially offer enough energy to power the whole city—even on days where temperatures (and energy usage) is high.

The Los Angeles Solar Atlas highlights the findings, breaking down the solar potential for this city and several others. It shows that the available roof space (mostly on single-family homes) could be used to generate 19,000 megawatts of power.

To put this in perspective, on extremely hot days the city tends to use about 6,177 megawatts of power. On a normal day it rests somewhere around 5,500 megawatts.

While the findings seem promising, they don’t take a few variables into account, such as areas shaded by trees, or homes that wouldn’t support solar installations. In truth, there is still much research to be done in the field.

Los Angeles, a nightmare city in terms of negative environmental impact, is attempting to wean itself off of nonrenewable energy sources by 2020, making it a prime candidate for more solar installations.

However, it should be noted that solar isn’t the singular solution for such a large issue. In fact, a city can’t rely just on solar for its energy needs because it’s not always reliable. To combat cloudy days, other energy sources must be used, like wind power.

But the findings are still positive. If Los Angeles begins to use even a quarter of its available roof space for solar installations, the result could be huge—even better than desert-destroying projects like the 9,500-acre Blythe Solar Millennium project.

After all, if the structures are already there, why not use them to up LA’s renewable energy potential?

Solar Rebates are Highest in Los Angeles County

Posted on May 16th

You may have heard that LADWP put its solar rebate program on hold. But for those of you in Southern California Edison (SCE) territory, your chances at scoring amazing solar rebates are much, much higher.

In fact, SCE still offers the best solar rebates in Los Angeles (and all of California, for that matter). Through the California Solar Initiative, qualifying homeowners receive $1.10 per watt of solar energy installed.

So, if solar costs an average of $6 per watt, that’s a little over 18% saved on your installation. Add to that the 30% return from the Residential Renewable Energy Tax Credit, and you’ve eliminated nearly 50% of your total costs.

For example, if your system costs $25,000, you would pay only $12,500 after rebates.

State rebate savings = ~20%

Federal tax credit savings = 30%

Total incentives = ~50%

This is phenomenal, considering that many U.S. rebate programs have been reduced, halted or cut altogether due to overwhelming demand. PG&E in Northern California and California Center for Sustainable Energy (CCSE) currently offer only $0.65 per watt, or about 11% savings.

Solar Rebates are Going Fast

It’s important to note, however, that these rebates won’t last forever. SCE incentives have reached 42% capacity, so when those remaining rebates are assigned, incentive levels drop down to the next level, or $0.65 per watt.

You can check the Statewide Trigger Tracker for updates on how much rebate money is left. The sooner you find an installer, the less your system will cost. Estimates are easy to come by, and can be had for free by clicking here.

Not sure if your home qualifies for rebates from SCE? County territories include much of Los Angeles, Orange County, Santa Barbara, San Bernardino, Riverside, Ventura, Kern, Tulare and Inyo.

We recommend getting your roof examined for solar potential. A licensed installer can assess whether your roof gets enough direct sunlight for solar collection, among other factors.

http://solar.calfinder.com/blog/solar-funding/solar-rebates-highest-los-angeles-county/

the "Dell of solar cells"

Lowe's Teams Up with Sungevity to Accelerate Solar Sales

By Danny Bradbury, BusinessGreen

Published May 17, 2011

Residential solar firm Sungevity has signed home improvement company Lowe's as a distributor, significantly expanding its reach into the fast expanding market for domestic solar panels.

The company, which currently uses web-based tools to provide fast quotes for solar installation, said the new partnership will allow it to deliver in-store consultation and sales for Lowe's customers.

Lowes will provide customers with in-store access to iQuote, the Sungevity system that uses satellite images and aerial photography to estimate the cost of a residential solar installation.

Displays branded with Sungevity's material will begin appearing in the chain's stores this summer, before rolling out across eight states.

Sungevity launched three years ago in California, setting itself up as the "Dell of solar cells." It provided an automated sales process that used a geometric algorithm to calculate the angle of the roof and the available surface area for installation. This enables it to give a next-day quote to potential customers, who access its sales tools online.

The company is attempting to penetrate the mass-market for solar installations, and the firm said the Lowe's deal will help educate the market and make its products more available to a wider base of people.

Sungevity offers solar leasing products, in what it calls its "solar as a service" program. It monitors and maintains its systems, fixing them if it detects that they are operating suboptimally.

The company raised $15 million in series C funding last December, bringing its total to more than $25 million.

Read more: http://www.greenbiz.com/news/2011/05/17/lowes-teams-sungevity-accelerate-solar-sales#ixzz1Md7Piu9D

----

The best way to save money with solar panels is still to pay for them yourself (which Sungevity also offers). But the high cost of a solar system has scared many people away from this option. Leasing a system, on the other hand, accords the buyer all the green bragging rights of buying one — with no money down.

Such leasing programs have proven a powerful incentive to green-wannabes. According to CEO Danny Kennedy, Sungevity installed as many systems in March and April as in all of last year — and 90 percent of those sales were leases. (proving 2011 so far has been good for solar business)

If the guaranteed savings and maintenance sounds too good to be true, it’s not. But some people may find that the savings involved are not worth the hassle.

Sungevity is unique among solar installers in that it has tried to put as much of the process of buying solar panels online as possible, thereby reducing transaction costs. “Probably 10 percent of the end price is pencil pushing, filling out forms,” said Kennedy. “We’ve done as much as we can, legally, to digitize that.”

After determining the type of system appropriate, Sungevity use a network of local contractors to actually install it.

http://www.triplepundit.com/2010/05/sungevity-spying-on-celebrities-with-solar-technology/

a 10K is a year end (audited) report. Q2 ends June 30th and its 10Q is due 45 days later on August 15th, three months from now.

Hopefully we'll get some photos of some of these jobs on the company website as proof. Otherwise any proof is 90days away. They are expecting panel delivers this week so they should have completed some of the these jobs in time for them to show up in the 2nd qtr 10Q. I'll wager 1/2 of them won't show up until Q3, due Nov 15th

"...The focus on smaller projects has brought our 2011 sales to approximately $6 million to date and we expect this growth to continue in the future..." 5/11/2011

"...CSS in the first four months of 2011 has signed and financed projects in excess of last year's revenue and expects to steadily increase that growth through 2011..." 5/17/2011

"...we will be announcing the further expansion in the coming weeks into additional US markets..." 5/17/2011

Looks like a .03 break is in the cards to today. Most weak hands have already folded.

...feeling good Lewis, lol.

"...With sales of $5.5 million in 2010, CSS in the first four months of 2011 has signed and financed projects in excess of last year's revenue and expects to steadily increase that growth through 2011..."

profitable?

Our revenues during the three month periods ended March 31, 2011 and 2010 were zero and $1,685,932, respectively. We recognized net losses of $1,200,709 and $3,170,316 (or a basic and diluted loss of $.01 and $.04 per common share) for the three months ended March 31, 2011 and 2010, respectively. The net loss for the three months ended March 31, 2011 and 2010, respectively, includes a total of $427,960 and $2,367,403 of non-cash charges, primarily stock based compensation.

they owe $437M.

thats what happens when you try and manufacture solar panels in the US, the Chinese who work for peanuts will clobber you.

AWSR Announces First Quarter 2011 Results

Today : Monday 16 May 2011

America West Resources, Inc. (OTCBB: AWSR), a domestic compliant coal producer with mining operations in Central Utah, today announced its financial and operational results for the three month reporting period ended March 31, 2011.

Financial Highlights for the Three Months Ended March 31, 2011 Compared to the Three Months Ended March 31, 2010:

* Revenues climbed 217% to $3.49 million, up from $1.10 million.

o Quarterly coal production, from development, reached a record level in the first quarter of 2011, nearly doubling to 94,648 tons when compared to 47,903 tons produced for the three months ended March 31, 2010.

o In January 2011, the Company took delivery of a new continuous miner and deployed it in a second section of the Horizon Mine in late February, which helped contribute to the increase in coal production and revenues.

* Loss from operations decreased 56% to $1.43 million from $3.22 million.

* Net loss increased to $6.53 million, or $0.19 loss per basic and diluted share, compared to a net loss of $4.97 million, or $0.23 loss per basic and diluted share. The rise in net loss was largely attributable to an approximate $2.5 million one-time non-cash charge to interest expense and an approximate $500,000 one-time, non-cash loss on extinguishment of debt for the three months ended March 31, 2011. These non-recurring charges were associated with the restructure of loans with shareholders, and the conversion of approximately $5 million of shareholder debt to equity.

The Company's balance sheet reflects total assets of $28.15 million as of March 31, 2011, up from $23.48 million at December 31, 2010, while total liabilities declined to $27.04 million from $32.58 million, respectively. As a result, the Company succeeded in reversing what was total stockholders' deficit of $9.11 million as of yearend 2010 to total stockholders' equity of $1.11 million as of the end of March 2011.

During March and April 2011, the Company raised $4.5 million through a private placement of its common stock through New York-based investment banking firm John Thomas Financial, and negotiated the conversion of approximately $5 million in debt to equity.

Commenting on the results, Dan Baker, Chief Executive Officer of America West Resources, noted, "The investments we have made over the past two and half years in mine development initiatives, mining equipment and an expanding workforce, are now beginning to pay off. With the deployment of the second continuous miner at Horizon late in the first quarter of this year, we achieved a record quarter in production for our Company. In addition, we hope to begin pulling pillars in certain developed areas of the mine this month, representing another major milestone for America West. When that occurs, daily coal production should notably increase to fuel record revenue growth over the next several quarters," concluded Baker.

For more detailed information relating to the Company's first quarter 2011 results, please refer to the financial statements included with this press release and the 10-Q that was filed with the U.S. Securities and Exchange Commission on Friday, March 13, 2011.

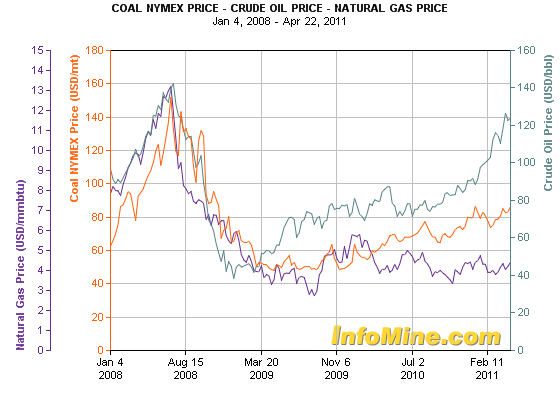

Coal versus Oil vs Nat Gas

Standard & Poor's outlook on coal prices

Wednesday May 11, 2011 (02:00 PM EDT)

SECTORS: KING COAL TO LOSE ITS CROWN

Negative Potential Implications: ARCH COAL INC. (ACI30.90 **), CONSOL ENERGY INC. (CNX49.13 **).

We recently downgraded our fundamental outlook on the Coal&Consumable Fuels sub-industry to negative from neutral. This is due to our belief that pricing for both industry metallurgical and thermal coal is too high. Our opinion is largely based on our belief that factors that have caused the run up will subside over the near-term. Also, we think industry coal prices are likely to decline moderating supply/demand dynamics.

Since September 2010, commodity coal prices have increased significantly. For instance, prices for coal in storage at the port of Qinhuangdao in China have increased by nearly 24%. We also note that prices for coal originating from Newcastle, Australia, a major international coal port, have increased by more than 36%. In addition, benchmark coal prices out of South Africa, another major supplier of internationally traded coal, have risen 42%. Coal prices in the U.S. have also reacted. For example, prices for coal originating from the Eastern U.S. have risen by 20% over the same period.

We believe global price increases have occurred for a number of reasons, which also includes improving demand. However, we think a great deal of the price increase since late 2010 is from other factors. For instance, coal market disruptions, following the Australian floods, have limited the supply of coal in seaborne coal markets, leading to higher metallurgical and thermal coal pricing globally. In addition, we also think that coal prices have moved upward in the wake of the Fukushima crisis in Japan, as markets have anticipated a push away from nuclear and toward power from coal. In turn, markets have reacted to the potential for increased coal demand. Another factor in rising coal pricing, in our opinion, has been the increase in inflation expectations, as exemplified by the spread between interest rates on Treasury bonds and Treasury Inflation Protected securities (TIPS). Our analysis shows that higher inflation expectations imbedded in this spread are a gauge for coal pricing.

For several reasons, we think these catalysts will prove to be temporary and are likely to lead to a pull back in pricing. For one thing, coal production that was curtailed by the floods in Australia has already shown signs of coming back online. In addition, we believe initial negative sentiment surrounding nuclear incident in Japan has toned down as we believe that the world realizes that nuclear power is needed in the future mix of energy production. Lastly, we think that price increases resulting from necessitated safety reviews of nuclear power plants is temporary.

Another dynamic aspect of coal pricing, that is rarely discussed, is weather. To our thinking, weather is a major determinant that drives changes in both supply and demand of coal. Hence, it effects industry pricing. To that end, we note that the air temperatures experienced during the summer of 2010 were far above normal. According to the National Oceanic and Atmospheric Association (NOAA), degree cooling days, a measurement reflecting the demand for energy used to cool properties, was 23% greater than the 30-year average in the summer of 2010. This drove demand and pricing. However, NOAA forecasts that degree cooling days will decline by nearly 20% during the summer of 2011. Should this forecast prove true, we think this will restrain weather-driven demand for coal this summer and reduce prices.

While factors such as the build-out of coal-based power plants in China and India, or the theory that global coal production will eventually peak suggest a positive long term outlook, we think prices will weaken in the near term for the reasons mentioned above, which suggests that the Coal and Consumable sub-industry will underperform the broader market. Coal companies that we have sell recommendations on include Arch Coal (ACI 31 **) and Consol Energy (CNX 49, Sell).

MATHEW CHRISTY, CFA, S&P Equity Analyst

http://www.outlook.standardandpoors.com/NASApp/NetAdvantage/i/SPO/displayIndustryFocusEditorialStory.do?subtype=INDI&pc=NET&tracking=NET&context=IndustryFocus&prefix=i

Q1 revenue: $3.5 million

We had revenue for the three months ended March 31, 2011 of approximately $3.5 million, a 217% increase from revenues of $1.1 million for the same three month period in 2010. The increase in revenues was attributable to an approximate 98% increase in coal production in 2011 compared to 2010 due to 1) the Company deploying a second continuous miner in February 2011, and 2) the Company intermittently idling the mine in the first quarter of 2010 due to lower demand for coal at that time. All coal sales revenue during the first quarter of 2011 was related to coal produced from our Horizon coal mine operations by our wholly-owned subsidiary, Hidden Splendor Resources, Inc.

Our production costs during the three months ended March 31, 2011 were approximately $2.4 million, an increase of 91% over the production costs of approximately $1.3 million reported for the three months ended March 31, 2010. The 91% increase in production costs was due to approximately 98% higher production volume in the first quarter of 2011 compared to the same period in 2010.

We had a gross profit of approximately $0.6 million for the three months ended March 31, 2011, representing a favorable variance of 147% from the approximate $1.3 million gross loss recognized during the three months ended March 31, 2010. The variance is primarily attributed to higher coal production in the first quarter of 2011 compared to 2010 for the reasons stated above.

Operating expenses for the three months ended March 31, 2011 totaled approximately $2.1 million, an increase of approximately $0.17 million, or 9%, from operating expenses of approximately $1.9 million in the prior year’s comparable three month period. The increase is primarily attributed to an approximate $0.6 million increase in MSHA compliance legal expenses in the first quarter of 2011 compared to 2010, partially offset by an approximate $0.4 million decrease in royalty expense associated with the cancellation of royalties previously accrued, which are no longer due to third parties. The Company’s legal expenses in the first quarter of 2011 are fees related to MSHA compliance and are expected to be significantly lower going forward.

Loss from operations decreased approximately $1.8 million or 56%, due to the aforementioned increase in revenues offset by the increase in operating expenses.

Total net other expenses totaled approximately $5.1 million for the first three months of 2011, compared to net other income of $1.7 million for the first three months of 2010. The negative variance between periods of approximately $3.4 million was primarily due to an approximate $3.4 million increase in interest expense. Interest expense increased due to an approximate $2.5 million one-time charge associated with the amortization of debt discount in relation to the restructure of loans with shareholders.

We incurred an approximate $6.5 million net loss for the three months ended March 31, 2011, compared to an approximate $5.0 million net loss for the three months ended March 31, 2010. The negative variance between the periods of $1.6 million, or 31%, is primarily attributed to the $3.4 million variance in net other expenses, partially offset by the approximate $1.8 million positive variance in loss from operations as described in detail above.

Of the $6.5 million net loss for the three months ended March 31, 2011, approximately $4.5 million is associated with expenses that are one-time charges and/or non-cash items, composed of the following:

$2.5 million – one-time non-cash charge to interest expense associated with the restructure of shareholder loans

$0.6 million –legal expenses related to MSHA compliance which are not expected to be recurring

$0.6 million - non-cash charge on extinguishment of debt associated with extension of loans and issuance of stock for liabilities

$0.4 million – non-cash charge for the amortization of deferred financing costs associated with warrants issued in relation to a previous financing

$0.4 - non-cash charge associated with previous issuance of stock options to management and employees, as well as warrants previously issued to third parties for services

http://sec.gov/Archives/edgar/data/867687/000107878211001361/amwest10q033111.htm

During the three months ended March 31, 2011, America West issued 5,034,822 common shares for the conversion of $5,000,000 of principal and $34,822 of accrued interest.

During April 2011, America West sold an aggregate of 1,190,000 common shares for cash proceeds of $1,035,300 net of issuance costs of $154,700.

In April 2011, America West entered into a debt settlement agreement with a third party lender pursuant to which America West issued the former 550,000 common shares as settlement of a total of $521,875 principal and accrued interest.

the loan agreement...

Through multiple amendments between February 11, 2011 and March 31, 2011, all debt and interest owed to a third party was modified and consolidated into one convertible loan with a principal amount of $10,765,839. This loan includes $9,125,088 of principal and $1,640,751 of accrued interest converted to principal. The modified note bears interest at the rate of 8% per annum and matures on June 1, 2014. The modified note requires monthly principal and interest payments of $221,259 beginning on July 1, 2011 with a final payment upon maturity of the unpaid principal and interest. The note is secured by essentially all of the assets of America West, subject to the Hidden Splendor (wholly-owned subsidiary) bankruptcy security requirements. As part of the loan agreement, the Company must comply with certain covenants which, among other matters, include restrictions in the amounts of capital stock and stock options that can be issued for each of the years 2011, 2012 and 2013. America West is also not allowed to incur or assume any debt or contingent liabilities not provided for in the loan agreement.

America West evaluated the modification under FASB ASC 470-50 and determined that the modification was substantial due to a substantive conversion option being added and the revised terms constituted a debt extinguishment. At any time prior to the full payment of the note, the creditor has the option to convert all or any portion of the unpaid balance of the note into shares of common stock. The first 50% of the debt is convertible at $1.00 per share, the next 25% is convertible at $1.25 per share and the last 25% is convertible at $1.50 per share. If the entire principal balance was converted, 9,330,394 shares of America West’s common stock would be issued.

http://sec.gov/Archives/edgar/data/867687/000107878211001361/amwest10q033111.htm