News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

zsvq1p

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Gonna fill some gap when debt ceiling raised.

70% of our treasuries are purchased by our government. How would one confirm this?

Cobra target $35

Joanne Klein says you can wait to buy these next couple days... Money Wave in RED.

http://stockcharts.com/public/1107832/chartbook/274769300;

OPEC ready to cut supplies in 2013 to support oil prices

VIENNA: OPEC does not see increased US oil output as a threat to its interests but is skeptical about current forecasts on the boom of American shale gas production, a senior official of the 12-nation group said.

OPEC Secretary-General Abdullah Al-Badry also said figures supplied by Iran show it producing around 3.7 million barrels a day. That is the same amount as Tehran pumped before international embargos on its crude that took effect this year and had been estimated to have cost it hundreds of thousands of barrels a day in sales.

Al-Badry spoke to reporters a day after OPEC ministers agreed to keep their daily crude production target unchanged at 30 million barrels.

They also extended his term for a year after failing to agree on a successor for the post because of rivalries among member states.

OPEC, which accounts for about a third of the world’s oil production, is projecting a slight fall in demand for its crude next year, and world inventories are well stocked, in part because of resurgent production by the United State, which is tapping into oil extraction from shale.

The Paris-based International Energy Agency is predicting that America will be a net exporter of oil by the next decade and could overtake Saudi Arabia as the world’s top crude producer by 2020. Analysts have suggested a looming dent in OPEC influence as a result.

But Al-Badry said his organization “is not really concerned” about any increase in world supply due to US shale extraction.

He questioned industry estimates that US shale extraction could amount to an extra 3 million barrels of oil a day within 20 years as well as forecasts of US energy independence. At the same time, he said any extra supply was welcome.

“It’s fine with us, it’s another source of energy and the world really needs this oil, I don’t see it as a threat to OPEC” he said.

His comments on Iranian production indicated that figures from other organizations may be off or that Tehran’s statistics might be inaccurate.

Oil exports from Iran have dropped this year as a result of international sanctions imposed due to concerns that Tehran may be seeking nuclear arms — something Iran denies. The International Energy Agency, which offers energy expertise to industrialized country, said last month that Iranian oil output was at a daily 2.7 million barrels in October.

But Al-Badry said Iran has told OPEC that it is producing 1 million barrels a day more than that, which would equal output before the embargoes took hold.

Ahead of Wednesday’s OPEC oil ministers’ meeting, Iranian Oil Minister Rostam Ghasemi played down the effects the sanctions were having on his country, claiming the Iranian state had cut its financial dependence on oil income by 20 percent in the last three years.

“Next year we will do the same,” he said.

I think you own this one right now...

- debt ceiling about to rise; dollar to get weak...

- Fall off cliff will be wild.... filled with those that beleive it will increase revs in Fed is good, and those the think it will slow spending on goods and sevices as cause economic disaster. Mass confusion coming IMO. Safe investments to be desire.

Soon will be a chance to make a whole bunch of money on this one...

I think sell now! the goal is to take it back to private.

I think sell now! the goal is to take it back to private.

a 1-for-10,000 reverse stock split

If you have 10,000 shares ($2700), after the 1-for-10,000 reverse stock split, you will have 1 share ($2700). Not many folks buy shares at that price. Risk! someone offers $50 and someone takes it... or maybe even $1000? You just lost. I just don't think many people gonna buy at $2700 a share.

followed by a 1,000-for-1 forward stock split and a $2,000,000 share repurchase program

Notice the order?

The Board is also considering payment of a potential special cash dividend pending the results of the stock splits, the share repurchase program and the Company's cash flow.

Let's say nobody trades. Price stays at $2700.. then they followed by a 1,000-for-1 forward stock split.. You now have 1000 shares... $2.70 a share.. that is when they start to use the $2 million to finish everyone off. The the final is a divy to then try and get more shares back...

Who knows the other big shareholders? Jason Wadzinski has 36 million.. I think his brother has a bunch too. These large shareholders might be part of the private company coming? Hard to say.

A 14 file is coming... maybe more details.

Just my thoughts.

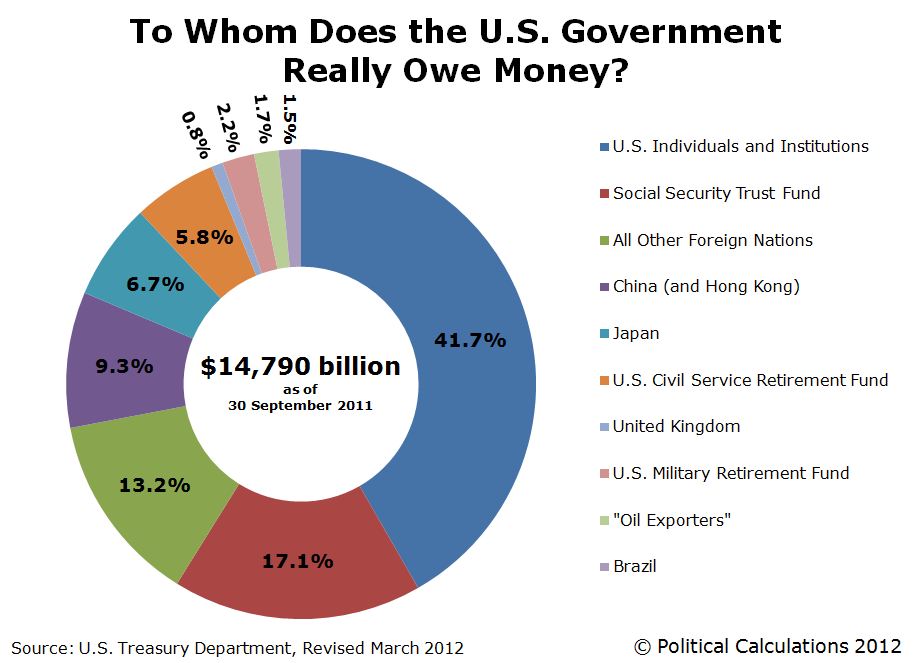

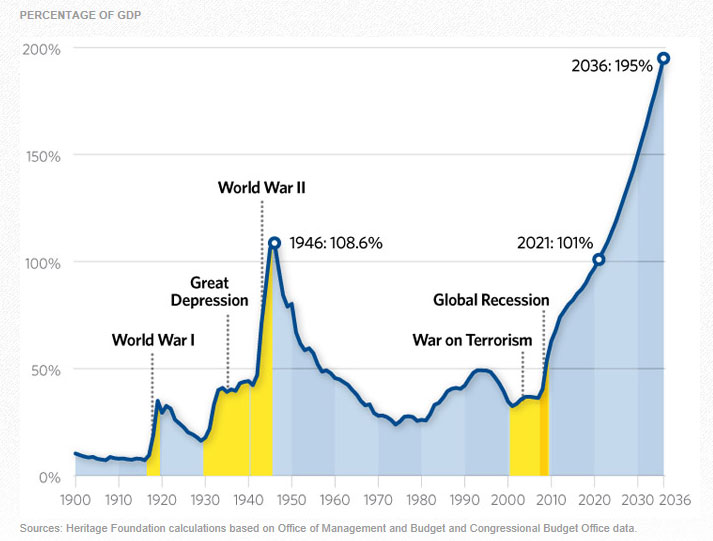

Gold vs US debt

Now that Obamacare seems to be going to happen.... US Debt should increase and gold too.

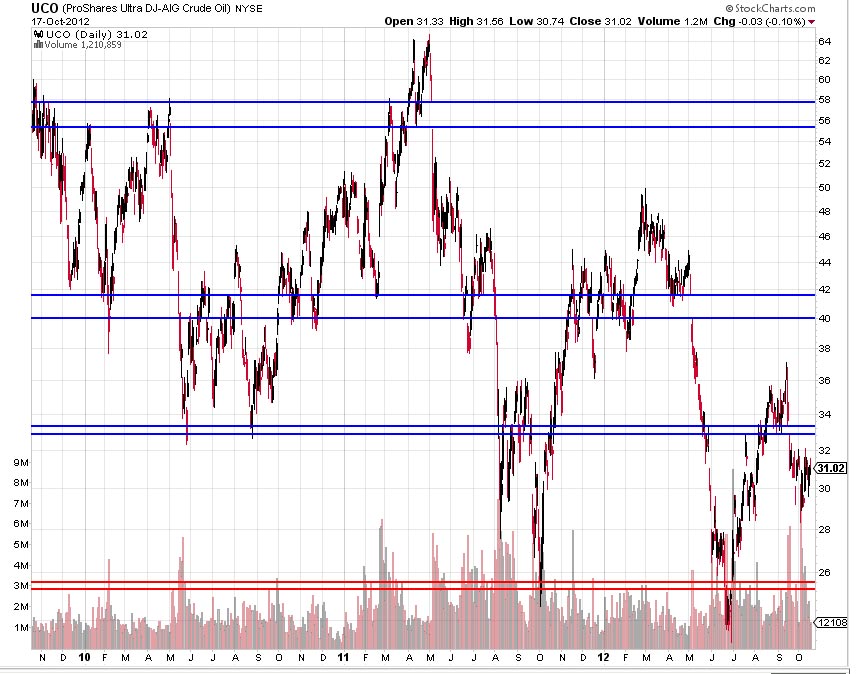

Up and down that fast.. Looks like we are about to hit some very low oil prices soon.. I think UCO is going below $24.77

Nice call... Gap up this morning... I think it gets filled at some point again. We'll see.

10,414,389 outstanding shares.... $33 million in cash and securites plus some assets... The technology is worth something.

$6 mil of debt..

It's worth at least $3? Right?

shooting for 25.50 or so...

watching 45.50 IMO

don't give up yet

Oil ends lower; pipeline, Mideast, dollar in focus

Contracts for petroleum products and natural gas also close lower

By Myra P. Saefong and Sara Sjolin, MarketWatch

SAN FRANCISCO (MarketWatch) — Oil futures settled lower Monday, below $89 a barrel, with investors eyeing the expected restart of a key North American pipeline as well as developments in the Middle East and moves in the U.S. dollar.

Other energy futures also finished lower, with natural gas leading the percentage declines.

“With the Keystone pipeline due to restart today, we were not surprised to see the selloff in crude continue,” said Tariq Zahir, a managing member at Tyche Capital Advisors LLC. “With those fears easing, traders are looking back to the fundamentals of the energy markets where at least we are very well supplied and way above our five-year averages of inventories.”

Crude for November delivery fell $1.32, or 1.5%, to settle at $88.73 a barrel on the New York Mercantile Exchange, after trading in a range between $90.80 and $88.20.

The November contract expired at the close. December crude /quotes/zigman/2084380 CLZ2 -1.81% , which became the front-month contract when the regular Nymex session ended Monday, settled at $88.65 a barrel, down 1.8%.

“With the slight tick upward in the U.S. dollar and the weakness in economies worldwide, the demand for energy is weak and supplies plentiful,” said Zahir. “We feel we could continue to see downward pressure in the upcoming days as the energy markets are starting to focus on the fundamentals.”

Supply concerns arose following the temporary closure of a key pipeline in North America last week. The Keystone pipeline, which sends about 500,000 barrels per day from Canada to the Midwest, was shut last Thursday but was reportedly due to restart Monday, a day later than expected.

A spokesman for TransCanada Corp. /quotes/zigman/27173 CA:TRP -0.07% /quotes/zigman/27155/quotes/nls/trp TRP -1.31% told MarketWatch in an email Monday that he would provide an update once the company has a better sense on the restart.

Tensions in the Middle East were also in focus. Brig. Gen. Wissam al-Hassan, Lebanon’s intelligence chief, was assassinated in a Friday car bombing in Beirut. Media reports said he was allied with the anti-Syria opposition, raising fears of a political crisis in Lebanon.

“The uncertain situation in the Middle East [...] remains a factor with the tendency to drive prices upward. Lebanon has now become a new seat of unrest, with violent disputes having taken place there yesterday,” analysts at Commerzbank wrote in a note.

“The biggest risk factor for the oil price is further deterioration of general market sentiment and accompanied growth in risk aversion,” they added.

Iran, meanwhile, is likely to wait until the U.S. presidential election in November before deciding what course to take on its nuclear program, Dennis Ross, former Middle East adviser to President Barack Obama, said Sunday on Platts Energy Week, an all-energy news and talk show.

Late in the trading session, a slight turn higher in the dollar added to pressure on dollar-denominated oil prices. The dollar index /quotes/zigman/1652083 DXY +0.50% , which measures the greenback against a basket of six rival currencies, was at 79.651, up from an earlier low of 79.470 and up from 79.629 late Friday.

Heating oil for December delivery /quotes/zigman/2101426 HOZ2 -1.01% shed nearly 6 cents, or 1.8%, to $3.08 a gallon, while November gasoline /quotes/zigman/2315457 RBX2 -1.96% fell 5 cents, or 1.8%, to $2.65 a gallon. Natural gas for November delivery /quotes/zigman/2199366 NGX12 +0.35% declined by 16.5 cents, or 4.6%, to $3.45 per million British thermal units. It ended last week up 0.2%.

Natural gas recently revisited the technical resistance level of $3.65, and it “looks like profits were taken up at those levels,” said Tyche Capital’s Zahir. “Of course, supplies are not a concern in the natural-gas market.”

Sara Sjolin is a MarketWatch reporter, based in London.

OK we are dipping.. I know this will bring Opportunity.

Discourse of the Common Wealth of this Realm of England, 1549...

"We must always take heed that we buy no more from strangers than we sell them, for so should we impoverish ourselves and enrich them."

Still solid as a rock

As far as I know, you pay no fees. It is an ETF an traded like a stock. They are build into the stock.

When? What will trigger this prediction? Others in the world are our slaves. China stops buying... we stop importing. Why is that good for China? It's not. Our market is too large for them... 300,000,000 strong. The US a food making machine. Plus, our energy cost are low. Coal and gas is plenty.

I cannot say if we have meltdown. Nobody can. Seems to me since 1990 people said a market crash was coming. Nothing. Even 2008 did not hurt as many as I would have thought. Most folks have come back strong.

What to do?? Own your house I say. Pay it off. ... maybe buy a shotgun too... a few 9 mm.. lol...

Derivative Meltdown and Dollar Collapse

The frightening prospects from a derivative meltdown, well known for years, seem to deepen with every measure to prop up a failing international financial system. The essay Greed is Good, but Derivatives are Better, characterizes the gamble game in this fashion:

"The elegance of derivatives is that the rules that defy nature are not involved in intangible swaps. The basic value in the payment from the risk is always dumped on the back of the taxpayer. Ponzi schemes are legal when government croupiers spin loaded balls on their fudged roulette tables."

Under conventional international trading settlement, the world reserve currency is the Dollar. The loss of confidence in the Federal Reserve System causes a corresponding decline in value in U. S Treasury obligations. Add into this risk equation, derivative instruments that are deadly threats that can well destroy national currencies. One such response to this unchecked danger can be found in a Bloomberg Businessweek perceptive article, A Shortage of Bonds to Back Derivatives Bets, makes a stark forecast.

"Starting next year, new rules will force banks, hedge funds, and other traders to back up more of their bets in the $648 trillion derivatives market by posting collateral. While the rules are designed to prevent another financial meltdown, a shortage of Treasury bonds and other top-rated debt to use as collateral may undermine the effort to make the system safer."

However, what happens when buyers of Treasury notes abandon the reoccurring cycle of rollover debt and stop buying new T-Bonds? Take the Chinese example as a template for things to come. China's yuan hits record high amid US pressure, "The Yuan touched an intraday high of nearly 6.2640 to $1.0, according to the China Foreign Exchange Trade System, marking the highest level since 1994 when the country launched its modern foreign exchange market."

While it is old news that the Dollar consistently drops in purchasing power, the circumvention of typical trade agreements, that by-pass transitions using the Dollar as the currency of exchange, is relatively recent. The next report forewarns of a major departure from the post Bretton Woods global trade environment.

China And Japan Move Away From Dollar, Will Conduct Bilateral Trade Using Own Currencies, is one method to avoid the direct consequences of a derivative meltdown.

"The China Foreign Exchange Trade System, the division of the People's Bank of China which manages currency trading, said that the country will set a daily trading rate based on a weighted average of prices given by market makers. The People's Bank said on Tuesday that an initial trading rate would be set at 7.9480 Yuan for every 100 Yen at market in Shanghai. Unlike yuan-dollar trading, which only allows for a daily fluctuation of 1 percent in Yuan trading value, Yuan trading with the Yen will be able to move within a 3 percent range."

Timing of a Dollar reputation is almost impossible to pinpoint with precise market foreknowledge. Yet the inevitability that The Dollar is Doomed, refers to the insight of "Hans F. Sennholz in his essay - Saving the Dollar from Destruction - we are presented with a bleak financial future. Even under optimum conditions, the alternatives are not pleasant. Now let’s ask the 64,000 dollar question. What will happen when interest rates start to rise?"

The economic havoc, with the rise in interest rates, will greatly disrupt existing worldwide trade agreements and practices. In the article How The U.S. Dollar Will Be Replaced, Brandon Smith addresses the pragmatic measures undertaken by major trade partners to protect their domestic economies from a Dollar freefall.

"To those people who consistently claim that the dollar will never be dropped, my response is, it already has been dropped! China, in tandem with other BRIC nations, has been covertly removing the greenback as the primary trade unit through bilateral deals since 2010. First with Russia, and now with the whole of the ASEAN trading bloc and numerous other markets, including Japan. China in particular has been preparing for this eventuality since 2005, when they introduced the first Yuan denominated bonds. The bonds were considered a strange novelty back then, especially because China had so much surplus savings that it seemed outlandish for them to take on treasury debt. Today, the move makes a whole lot more sense. China and the BRIC nations today openly call for a worldwide shift away from the dollar:"

After historic downgrade, U.S. must address its chronic debt problems.

"Dagong Global, a fledgling Chinese rating agency, degraded the U.S. treasury bonds late last year, yet its move was met then with a sense of arrogance and cynicism from some Western commentators. Now S&P has proved what its Chinese counterpart has done is nothing but telling the global investors the ugly truth."

The derivatives time bomb lingers over every financial market on the planet. Reforms cannot remove excess and greed, from risk management fiscal contracts. When the largest foreign trading partners look to insulate their transactions from an unstable Dollar currency, the panic has already begun.

It should be self-evident that additional U.S. Treasury bailouts with unlimited Federal Reserve claims against every asset of collateral that can be attached, is obscene in its nature. Hedging is equivalent to reassigning betting risk to unfunded insurance underwriters that would never be able to pay off the claim. Governments are broke by almost any financial standard. Central banksters accumulate titles to real property and assets by hook or crook.

Nation states held hostage to financial manipulation are slaves to the central banks. With the demise of the Dollar, the fake debt obligations of the United States must be repudiated. Foreign states are prepared to sever their links to the Dollar reserve currency, by trading directly in the domestic currencies of other countries. Interacting commerce in Dollars with American companies will continue, but the yoke of Federal Reserve Notes legal tender will be rejected when the derivative meltdown explodes.

James Hall – October 17, 2012

A Shortage of Bonds to Back Derivatives Bets

By Bradley Keoun on September 20, 2012 Tweet

Go Starting next year, new rules will force banks, hedge funds, and other traders to back up more of their bets in the $648 trillion derivatives market by posting collateral. While the rules are designed to prevent another financial meltdown, a shortage of Treasury bonds and other top-rated debt to use as collateral may undermine the effort to make the system safer.

Derivatives allow buyers to bet on the direction of currencies, interest rates, and markets, insure against defaults on bonds, or lock in a price on commodities. The new rules are rooted in the 2010 Dodd-Frank Act, passed in reaction to the near-collapse of the financial system in 2008, which was caused in part because derivatives contracts weren’t backed by enough collateral. American International Group (AIG) needed a $182.3 billion bailout from the U.S. government after it failed to make good on derivatives trades with some of the world’s largest banks. In response, Congress required that most privately negotiated derivatives transactions, known as over-the-counter trades, go through clearinghouses.

Clearinghouses, run by firms such as Chicago-based CME Group (CME) and London-based LCH.Clearnet Group, make traders provide collateral, including government bonds, that can be seized and easily converted into cash to cover defaults. Traders may need from $2 trillion to $4 trillion in extra collateral to meet the new requirements, according to Timothy Keaney, chief executive officer of BNY Mellon Asset Servicing.

The trouble is finding all that high-grade debt. The U.S. had $10.8 trillion in Treasuries outstanding at the end of August. Other countries, including Japan and European nations rated AAA or AA, had about $24 trillion of debt in the second quarter of 2011, according to an April report by the International Monetary Fund. Those government securities are already in heavy demand from central banks and investors.

The solution: At least seven banks plan to let customers swap lower-rated securities that don’t meet standards, in return for a loan of Treasuries or similar holdings that do qualify, a process dubbed “collateral transformation.” The maneuver allows investors who don’t have assets that meet a clearinghouse’s standards to pledge corporate bonds or mortgage-linked securities to a bank in exchange for a loan of Treasuries. The investor then posts the Treasuries—the transformed collateral—to the clearinghouse. The bank earns fees plus interest, and the investor is obliged at some point to return the Treasuries. In effect, the collateral is being rented.

That’s raising concerns among investors, bank executives, and academics that measures intended to avert risk are hiding it instead. “We just keep piling on lots of operational risk as we convert one form of collateral into another,” says Richard Prager, global head of trading at BlackRock (BLK), the world’s largest asset manager.

JPMorgan Chase (JPM) and Bank of America (BAC) are already marketing their new collateral-transformation desks, executives at the companies say. Other banks confirmed they’re planning to offer the service too, including Bank of New York Mellon (BK), Barclays (BCS), Deutsche Bank (DB), and State Street (STT). “Collateral transformation is a client service that does not hide risk,” says Jennifer Zuccarelli, a spokeswoman for JPMorgan Chase. “It is a form of short-term secured lending, which has always been an important part of capital markets, subject to tight capital and liquidity rules and fully transparent to regulators.” Goldman Sachs Group (GS) also plans to offer collateral transformation, a person with knowledge of the matter said. A spokeswoman for the bank declined to comment.

For the banks, an expanded securities-lending market could generate billions of dollars in fees, even as the industry faces shrinking profits due to regulations that increase price reporting and competition in derivatives trading, according to a report from consulting firm Oliver Wyman Group. At the same time, they could suffer losses if a trader defaults and his collateral is seized. In that case, the bank loses its Treasuries and is left holding lower-grade bonds that the trader posted in the collateral transformation. The banks’ new lending business “smells like trouble,” says Anat Admati, a finance and economics professor at Stanford Graduate School of Business who studies markets and trading and advises bank regulators on systemically important firms. “The point of the initiatives on derivatives was that derivatives can hide a lot of risk,” Admati says. “Now they’re going to just shuffle the risk around.”

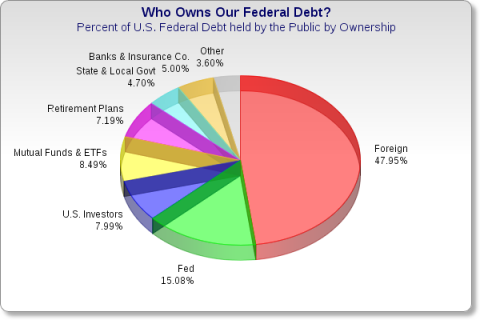

China must buy our bonds.

Would It Really Matter If China Stopped Buying U.S. Bonds?

August 17, 2011 | 67 commentsby: Michael Pettis | includes: FXI, PGJ Is the PBoC going to stop buying USG bonds? Once again we are hearing very worried noises from various sectors about the possibility of a reduction in Chinese purchases of USG bonds. Here is what an article the South China Morning Post said:

China will press ahead with diversification of its US$3.2 trillion in foreign exchange reserves, the State Administration of Foreign Exchange (SAFE) said on Thursday, adding it does not intentionally pursue large-scale foreign currency holdings. Officials have long pledged to broaden the mix of the country’s huge reserves – as much as 70 per cent of which are now in US dollar assets, according to analysts’ estimates – but the process has been gradual.

“We will continue to diversify the asset allocation of our reserve assets and continue to optimise the holdings based on market conditions,” the foreign exchange regulator said in a statement, responding to questions about its reserve management from the public. It did not mention the US debt debacle. Top Republicans and Democrats worked behind the scenes on Wednesday on a compromise to avert a crippling US default and potential credit rating downgrade.

Xia Bin, an adviser to the central bank, told reporters earlier this month that China should speed up reserve diversification away from dollars to hedge against risks of the US currency’s possible long-term decline.

It sounds like this time the PBoC might be pretty serious about diversifying their risk away from USG bonds, right? Let’s leave aside the fact that every six months we have heard the same thing for the past several years, and nothing has happened, shouldn’t we nonetheless be worried? Won’t reduced PBoC purchases be hugely disruptive to the US economy and to the US Treasury markets?

No, they won’t. There is so much nonsense still being said about this, even by economists who should know better, that I thought I would try to address what it would mean if the PBoC were actually serious and not simply making noises aimed at domestic political constituents.

First of all, remember that the PBoC does not purchase huge amounts of USG bonds because it has a lot of money lying around and doesn’t know what to do with it. Its purchase of USG bonds is simply a function of its trade policy.

You cannot run a current account surplus unless you are also a net exporter of capital, and since the rest of China is actually a net importer of capital, the PBoC must export huge amounts of capital in order to maintain China’s trade surplus. In order the keep the RMB from appreciating, the PBoC must be willing to purchase as many dollars as the market offers at the price it sets. It pays for those dollars in RMB.

It is able to do so by borrowing RMB in the domestic markets, or by forcing banks to put up minimum reserves on deposit. What does the PBoC do with the dollars it purchases? Because it is such a large buyer of dollars, it must put them in a market that is large enough to absorb the money and – and this is the crucial point – whose economy is willing and able to run a large enough trade deficit.

Remember that when Country A exports huge amounts of money to Country B, Country A must run a current account surplus and Country B must run the corresponding current account deficit. In practice, only the US fulfills those two requirements – large financial markets, and the ability and willingness to run large trade deficits – which is why the PBoC owns huge amounts of USG bonds.

If the PBoC decides that it no longer wants to hold USG bonds, it must do something pretty drastic. There are only four possible paths that the PBoC can follow if it decides to purchase fewer USG bonds.

The PBoC can buy fewer USG bonds and purchase more USD assets.

The PBoC can buy fewer USG bonds and purchase more non-US dollar assets, most likely foreign government bonds.

The PBoC can buy fewer USG bonds and purchase more hard commodities.

The PBoC can buy fewer USG bonds by intervening less in the currency, in which case it does not need to buy anything else.

We can go through each of these scenarios to see what would happen and what the impact might be on China, the US, and the world. To make the explanation easier, let’s simply assume that the PBoC sells $100 of USG bonds.

The PBoC can sell $100 of USG bonds and purchase $100 of other USD assets. In this case basically nothing would happen. The pool of US dollar savings available to buy USG bonds would remain unchanged (the seller of USD assets to China would now have $100 which he would have to invest, directly or indirectly, in USG bonds), China’s trade surplus would remain unchanged, and the US trade deficit would remain unchanged. The only difference might be that the yields on USG bonds will be higher by a tiny amount while credit spreads on risky assets would be lower by the same amount.

The PBoC can sell $100 of USG bonds and purchase $100 of non-US dollar assets, most likely foreign government bonds. Since in principle the only market big enough is Europe, let’s just assume that the only alternative is to buy $100 equivalent of euro bonds issued by European governments.

There are two ways the Europeans can respond to the Chinese switch from USG bonds to European bonds. On the one hand they can turn around and purchase $100 of USD assets. In this case there is no difference to the USG bond market, except that now Europeans instead of Chinese own the bonds. What’s more, the US trade deficit will remain unchanged and the Chinese trade surplus also unchanged.

But Europe might be unhappy with this strategy. Since there is no reason for Europeans to buy an additional $100 of US assets simply because China bought euro bonds, the purchase will probably occur through the ECB, in which case Europe will be forced to accept an unwanted $100 increase in its money supply (the ECB must create euros to buy the dollars).

On the other hand, and for this reason, the Europeans might decide not to purchase $100 of US assets. In that case there must be an additional impact. The amount of capital the US is importing must go down by $100 and the amount that Europe is importing must go up.

Will this reduction in US capital imports make it more difficult to fund the US deficit? Not at all. On the contrary – it might make it easier. Why? Because if US capital imports drop by $100, by definition the US current account deficit will also drop by $100, almost certainly because of a $100 contraction in the trade deficit.

A contraction in the US trade deficit is of course expansionary for the economy. Since the purpose of the US fiscal deficit is to create jobs, and a $100 contraction in the trade deficit will create jobs, the US fiscal deficit will contract by $100 for the same level of job creation – perhaps even more if you believe, as most of us do, that increased trade is a more efficient creator of productive jobs than increased government spending.

In other words although there is $100 less demand for USG bonds, there is also $100 less supply (or more) of USG bonds. It is of course possible that the USG ignores the employment impact of the contraction in the trade deficit, and goes ahead and spends the $100 anyway, but in that case unemployment would drop even more than expected.

This is the key point. If foreigners buy fewer USD assets, the US trade deficit must decline. This is almost certainly good for the US economy and for US employment. When analysts worry that China might buy fewer USG bonds, in other words, they are worrying that the US trade deficit might contract. This is something we should welcome, not deplore.

But the story doesn’t end there. What about Europe? Since China is still exporting the $100 by buying European government bonds instead of USG bonds, its trade surplus doesn’t change, but of course as the US trade deficit declines, the European trade surplus must decline, and even possibly go into deficit. This is because by selling dollars and buying euro, China is forcing the euro to appreciate against the dollar.

This deterioration in the trade account will force Europeans either into raising their fiscal deficits or letting domestic unemployment rise. Under these conditions it is hard to imagine they would tolerate much Chinese purchase of European assets without responding eventually with trade protection.

The PBoC can sell $100 of USG bonds and purchase $100 of hard commodities. This is no different than the above scenario except now that the exporters of those hard commodities must face the choice Europe faced above. Either they can neutralize the trade impact of Chinese purchases by buying US assets or they have to absorb the employment impact of deterioration in their trade account.

This, by the way, is a bad strategy for China but one that it seems nonetheless to be following. Commodity prices are very volatile, and unfortunately this volatility is badly correlated with Chinese needs. Since China is the largest or second largest purchaser of most commodities, stockpiling commodities is a good investment only if it continues growing rapidly, and a bad investment if its growth slows. This is the wrong kind of balance sheet position any county, especially a very poor country like China, should be engineer. It simply exacerbates underlying conditions and increases economic volatility – never a good thing, especially for a poor and undeveloped economy.

The PBoC can sell $100 of USG bonds by intervening less in the currency, in which case it does not need to buy anything else. In this case, which is the simplest of all to explain, China’s trade surplus declines by $100 and the US trade deficit declines by $100 as the RMB rises. The net impact on US financing costs is unchanged for the reasons discussed above. Chinese unemployment will rise because of the reduction in its trade surplus unless it increases the fiscal deficit.

It’s about trade, not capital

This may sound counterintuitive to all except those who understand the way the global balance of payments work, but countries that export capital are not doing anyone favors unless incomes in the recipient country are so low that savings are impossible or the capital export comes with technology, and countries that import capital might be doing so mainly at the expense of domestic jobs. For this reason it is absurd to worry that China might stop buying USG bonds.

On the contrary, the whole US-China trade dispute is indirectly about China’s insistence on purchasing USG bonds and the US insistence that they stop. Because make no mistake, if the Chinese trade surplus declines, and the US trade deficit declines too, by definition China is directly or indirectly buying fewer USG bonds, and this reduction in bond purchases will not cause US interest rate to rise at all. If it did, it would be like saying that the higher a country’s trade deficit, the lower its domestic interest rates. This statement is patently untrue.

Inevitably whenever I write about trade and capital exports someone will indignantly point out a devastating flaw in my argument. Since the US makes nothing that it imports from China, they will claim, a reduction in China’s capital exports to the US (or a reduction in China’s trade surplus) will have no impact on the US trade deficit. It will simply cause someone else’s exports to the US to rise with no corresponding change in the US trade balance.

No it won’t, unless this other country steps up its capital exports to the US and replaces China – which is pretty unlikely. Aside from the sheer idiocy of the claim that the US does not produce, or is incapable of producing, anything it imports from China, the claim is irrelevant even if it were true. Trade does not settle on a bilateral basis but must settle on a multilateral basis. If the US imports less capital its current account deficit must decline, whether because of bilateral changes in trade or not. I explain this in a blog entry early last year.

The basic point is that if reduced intervention in Chinese capital exports causes a reduction in Chinese exports to the US to be matched dollar for dollar with an increase in, say, Mexican exports to the US, the story doesn’t end there. Since Mexico’s trade balance is itself decided by the relationship between domestic investment and savings, a rise in Mexican exports will mean a rise in Mexican imports. It may very well be that lower Chinese exports to the US are matched by higher US imports from Mexico, but this will come with higher US exports to Mexico. And if it isn’t Mexico, it will be someone else.

Will China Stop Buying U.S. Debt?

20 September 2011 5 Comments

A few weeks ago, the Telegraph UK did a story about the sharp drop in foreign holdings of U.S. Treasuries. One of the big buyers of American debt is, of course, China. There are those that think China is forced to buy our debt otherwise its economy will collapse. Until the Treasury releases what is called “TIC” data (Treasury International Capital) in November, we really will not know what is going on. That is when the world will know for sure who is buying U.S. debt and who is NOT buying. Brandon Smith from Alt-Market.com thinks China is already heading for the exits when it comes to Treasuries. He makes a very good case for his point of view in the post below. Please read and enjoy. –Greg Hunter–

————————————————————-

Is China Ready to Pull the Plug?

By Brandon Smith Guest Writer for USAWatchdog.com

There are two mainstream market assumptions that, in my mind, prevail over all others. The continuing function of the Dow, the sustained flow of capital into and out of the banking sector, and the full force spending of the federal government are ALL entirely dependent on the lifespan of these dual illusions; one, that the U.S. Dollar is a legitimate safe haven investment and will remain so indefinitely, and two, that China, like many other developing nations, will continue to prop up the strength of the dollar indefinitely because it is “in their best interest”. In the dimly lit bowels of Wall Street such ideas are so entrenched and pervasive, to question their validity is almost sacrilegious. Only after the recent S&P downgrade of America’s AAA credit rating did the impossible become thinkable to some MSM analysts, though a considerable portion of the day-trading herd continue to roll onward, while the time bomb strapped to the ass end of their financial house is ticking away.

The debate over the health and longevity of the dollar comes down to one very simple and undeniable root pillar of economics; supply and demand. The supply of dollars throughout the financial systems of numerous countries is undoubtedly overwhelming. In fact, the private Federal Reserve has been quite careful in maintaining a veil of secrecy over the full extent of dollar saturation in foreign markets in order to hide the sheer volume of greenback devaluation and inflation they have created. If for some reason the reserves of dollars held overseas by investors and creditors were to come flooding back into the U.S., we would see a hyperinflationary spiral more destructive than any in recorded history. As the supply of dollars around the globe increases exponentially, so too must foreign demand, otherwise, the debt machine short-circuits, and newly impoverished Americans will be using Ben Franklins for sod in their adobe huts. As I will show, demand for dollars is not increasing to match supply, but is indeed stalled, ready to crumble.

China, being the second largest holder of U.S. debt next to the Fed, and the number one holder of dollars within their forex reserves, has always been the key to gauging the progression of the global economic collapse now in progress. If you want to know what’s going to happen tomorrow, watch what China does today.

Back in 2005, China began a low profile program to issue government debt denominated in the Yuan, called Yuan bonds, or “Panda Bonds”. This move was almost entirely ignored by establishment economists. They should have realized then that China was moving to strengthen the Yuan, expand its use in other markets, and recondition their economic structure away from export dependency and towards consumerism (as they have done with the establishment of the ASEAN trading bloc). Of course, in the MSM at that time, there was no derivatives bubble, no credit crisis, no debt implosion. America was on cloud nine. China, through inside knowledge, or perhaps a crystal ball, knew exactly what was about to happen, and insulated itself accordingly by generating distance between its system and the soon to derail retail based society of the U.S. This dynamic has not changed since the 2008 bubble burst, and Chinese activity is still the ultimate litmus test for economic volatility.

Today, there is widespread confusion in markets over the direction of America’s financial future. In the wake of the credit downgrade, most investors unaware of the bigger picture are desperately clinging to any and every piece of news no matter how trivial, every rumor from the Fed, and every announcement from the government no matter how empty. China’s economic news feeds have been tightly regulated and filtered, even more so than usual (which is cause for concern, in my opinion), while distractions in Europe abound. Let’s take a step by step journey through these issues, and see if we can’t produce some clarity…

U.S. versus EU: A Game Of Hot Potato…To The Death?

The theatrical seesaw between the U.S. and Europe is not only becoming obvious to the most narrow of economic analysts, it is also becoming kind of boring. The entire ordeal has been subversively exploited as a false example of systemic “contagion”, and with purpose; global banks need to convince average Americans and average Europeans that destabilization in one portion of the world will automatically lead to destabilization everywhere. This concept is true only so far as forced globalization and centralization have made it true. That said, the charade has been somewhat effective in conditioning the populace with ideas of collectivist survival. In other words, we are being trained to take fiscal responsibility for countries outside of our sovereign national boundaries as if we are morally tied to every penny they have or do not have (global socialism/feudalism – here we come!). This process is culminating in worldwide harmonization through fear as well as guilt.

What we are witnessing is NOT contagion. Instead, we are seeing multiple and mostly separate collapses activated simultaneously. Each nation suffering dire straights in Europe is doing so because of its own particular financial problems, not the problems of other countries nearby, and certainly not those of countries on the other side of the world. Contagion arguments are only applicable to those economies overly dependent on exports, yet, China has already shown (at least in the case of the U.S.) that such dangers can be controlled by minimizing exposure to the poisoned portions of the system and reverting to more internalized wealth creation.

Treasury Secretary Timothy Geithner and the heads of World Bank and IMF have perpetuated the lie of contagion between the U.S. and the EU primarily to service the progress of globalization, but also to hide the inflationary effects of dollar devaluation. While the greatest threats are stacked squarely against America’s economy and the dollar, somehow we have been led to focus on the comparatively less explosive drama in the EU. U.S. dollars, as well as Chinese funds, are flooding into Europe to support the region, while investment in the U.S. and its debt weakens and disappears. In the meantime, a weaker Euro makes the dollar look more attractive (at least on paper), but in reality, both currencies are on the path to bloody hari-kari.

How much longer can this game of hot potato go on? Again, China decides. Eventually, China is going to have to choose which currency to support; the dollar or the euro. Supporting both is simply not an option, especially when the chance of collapse in both currencies is so high. So far, the most logical path has been the euro. While the EU may suffer an astonishing breakdown, we must take into account that our own Treasury and central bank have seen fit to throw trillions of dollars into propping up Europe (with even more on the way):

http://www.reuters.com/article/2011/09/15/us-eurozone-idUSTRE78B24R20110915

With so much inflation and devaluation being thrust upon the dollar in the name of saving the EU, China’s move towards a stronger economic relationship with Europe at the expense of the U.S. is a no-brainer:

http://www.bloomberg.com/news/2011-09-14/china-willing-to-buy-bonds-from-sovereign-debt-crisis-nations-zhang-says.html

If I were to place a bet on who would come out of the crisis less damaged, my money would be on the EU, everyone else’s money certainly seems to be…

China Discreetly Moving To Dump U.S. Debt

China has been tip-toeing towards this for years, and has openly admitted on numerous occasions that they plan to institute a break from U.S. debt and the dollar in due course. Anyone who continues to argue that a Chinese decoupling from America’s economy is impossible at this point is truly beyond hope. Though increasingly more rare, news on China’s push to drop the U.S. still leaks out. Recently, a top advisor to China’s central bank let slip that a plan is in place to begin “liquidating” (yes, they said liquidate) their U.S. Treasury bonds as soon as possible, and reposition national investments into more physical assets:

http://blogs.telegraph.co.uk/finance/ambroseevans-pritchard/100011987/china-to-liquidate-us-treasuries-not-dollars/

But let’s step back for a moment and pretend China hasn’t told us exactly what it is going to do time and time again. Instead, let’s look at the fundamentals.

The primary concern in China right now is inflation. Because China does not yet have the ability to export its fiat to other markets the way the U.S. does, its own liquidity injections in the face of the credit crisis have led to severe price increases. In August alone, overall inflation was rated at 6.2% (always double government produced numbers to get true inflation). Food prices jumped 13.4%, while meat and poultry jumped 29.3%. Because these numbers are around 1% lower than in previous months, the Chinese government has prematurely proclaimed a “cooling period”:

http://www.telegraph.co.uk/finance/china-business/8751482/China-inflation-cools-as-food-price-rises-slow.html

With harsh inflation continuing unabated, eventually, the Asian nation will be forced to enact abrupt policies. This will likely take the form of a strong Yuan valuation, or a “floating” of the Yuan. A sizable increase in the value of the Chinese currency is the ONLY way that the government will be able to combat rising prices. By increasing the buying power of its citizens, the government allows them to keep pace with rising prices, and eases the tension within the populace which could otherwise lead to civil unrest. For China to ensure that a floating of the Yuan will lead to a much higher value, their forex and treasury holdings will have to fall. Period.

A dumping of the dollar will give the Chinese room to breath, and this space will be needed very soon. The debt ceiling deal made by Congress in the aftermath of the credit downgrade left the rest of the world unimpressed. While the MSM tries to make us forget that this event ever occurred, most foreign investors have not. Markets are anxiously awaiting an announcement from the Fed for further liquidity injections. If this announcement is not made after meetings next week, then it will certainly be made before the end of the year. Ironically, the same quantitative easing that investors are clamoring for today is liable to become the final signal for China to cut its losses and separate from U.S. securities completely. China has been positioned for many months now to take such measures…

Lights Out…

Delusions of Chinese dependency on the U.S consumer still abound, and those who suggest a catastrophic dump of U.S. debt and dollars in the near term are liable to hear the same ignorant talking points we have heard all along:

“The Chinese are better off with us than without us…”

“China needs export dollars from the U.S. to survive…”

“China isn’t equipped to produce goods without U.S. technological savvy…”

“America could simply revert back to industry and production and teach the Chinese a lesson…”

“The U.S. could default on its debts to China and simply walk away…”

“The whole situation is China’s fault because of their artificial devaluation of the Yuan over the decades…”

And on and on it goes. Though I have deconstructed these arguments more instances than I can count in the past, I feel it my duty to at least quickly address them one more time:

U.S. consumption of all goods, not just Chinese goods, has fallen off a cliff since 2008 and is unlikely to recover anytime soon. China has done quite well despite this fall in exports considering the circumstances. With the institution of ASEAN, they barely need us at all.

China is well equipped to produce technological goods without U.S. help, and if Japan is inducted into ASEAN (as I believe they soon will be), they will be even more capable.

America will NOT be able to revert back to an industrial based economy before a dollar collapse escalates to fruition. It took decades to dismantle U.S. industry and ship it overseas. Reeducating a 70% service based society to function in an industrial system, not to mention resurrecting the factory infrastructure necessary to support the nation, would likely take decades to accomplish.

If the U.S. deliberately defaults on debt to China, the global reputation of the dollar would implode, and its world reserve status would be irrevocably lost. We won’t be teaching anyone a “lesson” then.

Yes, China currently manipulates its currency down, but then again, so does the U.S. though quantitative easing. Both sides are dirty. Taking sides in this farce is pure stupidity…

Now that all that has been cleared up (again), the primary point becomes rather direct; the reason it is difficult to predict an exact time frame for an American collapse is because all the pieces are in place to trigger an event right now! There are, of course, stress points within the system that set a time limit, even on global banks and China, but a full spectrum catastrophe is not only a concern for some distant future. Every element needed for the so called “perfect storm” is ever present and ready to ignite at a moments notice. The destructive potential coming from China alone is undeniable. Everyday that the spark is subdued should be treated as a gift, an extra 24 hours of education and preparation. This is how close we are to the edge. It is not for us to be alarmed, but to be ready, and ever aware.

why would china stop buying our debt?

http://www.treasury.gov/resource-center/data-chart-center/tic/Documents/mfh.txt

When will china change? IF Mitt gets elected? He said it in the debate. "rules will change". The Obama connections may have kept China on a path keeping it's currency low? Oh what to do??? when must China's buying dollars end?

How does China Manipulate its Currency?

by Manshu on January 26, 2009

China’s currency manipulation remarks by Mr. Tim Geithner hit the front pages of all major newspapers last week. So let’s take a look at how China manipulates it currency.

To be fair to China, almost every country in the world manipulates its currency. In an ideal free market world – there would be no government intervention in the currency markets. However, there is hardly any Central Bank in the world that doesn’t intervene, when its currency starts to appreciate or depreciate beyond a certain price band.

Almost every Central Bank has a certain price band for its currency in its mind, and as soon as the currency goes beyond that band, governments start intervening in one way or the other.

This government intervention can be direct or indirect.

Buying Dollars to Keep the Dollar Price High

China has been interested in keeping the Yuan (Chinese Currency) undervalued relative to the US Dollar, and the easiest way (if you can afford it) to keep the Dollar price high, and the Yuan low is to buy dollars from the open market.

A country like China, which runs a huge Trade Surplus can afford to buy dollars in the open market to keep the demand for dollars high, and push the dollar price upwards relative to the Yuan. This keeps the Yuan undervalued.

Indirect Measures

There can be indirect interventions like putting a cap on the amount of foreign assets that locals can invest abroad. For example – India allows its residents to invest only up to $50,000 in foreign assets every year.

Other indirect measures can relate to taxation laws. For example – by allowing tax free repatriation of the Great Britain Pound – the British government can help boost inflow of Pounds in the country, and influence the exchange rate.

Why Does China Wish to Undervalue the Yuan?

China’s engine of growth is exports. The lower the value of the Yuan, the better it is for China’s exporters. Basically, if 1 Dollar buys 7 Yuans, and a exporter sells a Chinese Shirt for 10 dollars – he pockets 70 yuans. But if one Dollar was worth only 5 Yuans, the exporter would only be able to pocket 50 yuans.

By How Much is the Yuan Undervalued?

It is really impossible to tell by how much the Yuan has been undervalued, but estimates suggest that this range is between 15% – 40%.

A direct consequence of keeping the local currency undervalued is inflation, and since China faced rather high inflation rates in 2008 – it did plan to let its currency appreciate in 2008 (but that was before sub-prime).

How is the US Impacted?

It can be argued that the US is flooded with cheap imports from China not because China is really cost – competitive, but because China has artificially kept its currency undervalued. If the Yuan was allowed to appreciate – Chinese imports may no longer be cheap enough to compete with American produced goods.

On the other hand, it could really be that the Chinese are cost competitive, and it is really cheaper to produce goods in China than it is to produce them in US.

The truth probably lies somewhere in the middle.

US Stimulus Spending

The US runs huge trade deficits, and has plans for massive stimulus spending. The deficits mean that this stimulus spending can be done by either issuing more debt to foreign countries or printing more dollars.

If Mr. Geithner’s comments continue; they may aggravate China to such an extent that it stops showing up at the Treasury Bond auctions.

If that happens, then the US will have to resort to printing currency and quantitative easing on a scale that unleashes massive inflation.

It will be interesting to see how the situation unfolds, and how Mr. Geithner deals with China’s “Manipulation” – if and when he actually takes office.

looks like Dollar is about to be a bear...

Huge if you bought in June 2012 to today... 60% gain

If the dollar is directly related to oil...

maybe you can get large profit by buying oil? Gaps always fill.

Now might be the time to protect against Dollar drop?

China, Russia, and the End of the Petrodollar

by John Rubino on October 9, 2012 ·

Say you’re an up-and-coming superpower wannabe with dreams of dominating your neighbors and intimidating everyone else. Your ambition is understandable; rising nations always join the “great game”, both for their own enrichment and in defense against other big players.

But if you’re Russia or China, there’s something in your way: The old superpower, the US, has the world’s reserve currency, which allows it to run an untouchable military empire basically for free, simply by creating otherwise-worthless pieces of paper and/or their electronic equivalent. Russia and China can’t do that, and would see their currencies and by extension their economies collapse if they tried.

So before they can boot the US military out of Asia and Eastern Europe, they have to strip the dollar of its dominant role in world trade, especially of Middle Eastern oil. And that’s exactly what they’re trying to do. See this excerpt from an excellent longer piece by Economic Collapse Blog’s Michael Snyder:

China And Russia Are Ruthlessly Cutting The Legs Out From Under The U.S. Dollar

China and Russia are not the “buddies” of the United States. The truth is that they are both ruthless competitors of the United States and leaders from both nations have been calling for a new global currency for years.

They don’t like that the United States has a built-in advantage of having the reserve currency of the world, and over the past several years both countries have been busy making international agreements that seek to chip away at that advantage.

Just the other day, China and Germany agreed to start conducting an increasing amount of trade with each other in their own currencies.

You would think that a major currency agreement between the 2nd and 4th largest economies on the face of the planet would make headlines all over the United States.

Instead, the silence in the U.S. media was deafening.

However, the truth is that both Russia and China have been making deals like this all over the globe in recent years. I detailed 11 more major agreements like the one that China and Germany just made in this article: “11 International Agreements That Are Nails In The Coffin Of The Petrodollar”.

A few of the things that will likely happen when the petrodollar dies….

-Oil will cost a lot more.

-Everything will cost a lot more.

-There will be a lot less foreign demand for U.S. government debt.

-Interest rates on U.S. government debt will rise.

-Interest rates on just about everything in the U.S. economy will rise.

So enjoy going to “the dollar store” while you can.

It will turn into the “five and ten dollar store” soon enough.

Some thoughts

Snyder goes on to note that both China and Russia are accumulating gold, which will protect them from the coming currency crisis and give the ruble and yuan greater legitimacy in global trade. In Jim Rickards’ book Currency Wars, he tells the story of financial war games conducted by the US military, in which one of the scenarios was a Russian gold backed currency that challenged the dollar. We’re apparently not far from that plan becoming feasible.

The US spends a big chunk of its $700 billion a year defense budget on dominating the Middle East in order to force the trading of oil in dollars. Let that trade be diversified into several currencies and the demand for petrodollars goes way down. Central banks and global corporations will sell part of their dollar holdings, sending the dollar’s exchange rate into a tailspin. This in turn will make it harder for the US to finance its military empire/welfare state.

The net result: America becomes Spain, no longer able to simply whip out the monetary credit card to cover its overspending. We’ll have to live within our means, cutting maybe $3 trillion a year in government largesse (including the growth in unfunded entitlements liabilities).

Cuts on this scale can’t be accomplished smoothly, as Europe is discovering. So in this scenario the coming decade will be even messier than the last one, with “Occupy” movements shutting down cities and every election producing incumbent massacres. A combination of higher prices for necessities and lower wages will demote much of the middle class to “working poor.”

Meanwhile, China and Russia will reap the rewards of stronger currencies, and will divide (or share) control over their part of the world. It’s hard to know who to feel sorrier for, Americans who thought they could depend on government programs for a middle class lifestyle, or the neighbors of China and Russia who will see the relatively light hand of the American empire replaced with something far more atavistic.

What ya thinking?

I think you make a good point... Thing is China won't want a lower dollar. That means we pay them more for goods. Demand will drop. US makers will make more profit hiring more people. Gold might take off! This news could be already built into the market.

NEW YORK (Commodity Online)08 May 2012 at 18:05 IST: Iran is reportedly accepting Yuan as a settlement currency for its oil trade with China, posing a significant threat to the dominance of the US Dollar as the international trade currency, especially if other countries start to barter similar deal

As per the Financial Times, Iran uses the Yuan to purchase goods from China. Some of the trade is even in barter form. For eg; China's Zhuhai Zhenrong oil trading company provides services such as drilling to Iran in exchange of oil.

Increasing US sanctions have been straining Iran from its oil revenues as its major markets began to cut back oil imports from the country in a bid to comply with US requests. But the sanctions may boomerang back at the US with countries starting to use their respective currencies instead of the US Dollar for oil trades.

Earlier, India and Iran had agreed on a deal whereby India would pay about 40% of its oil imports in the for of Indian Rupee and Iran could use the currency to purchase goods and services from India.

And now with China joining India in a similar deal with Iran, it has to be seen if other countries over the world follow suit.

still a good one

Wow what a reversal for oil to drop from 100 to 91 so quick!

Seems like I did make a good move by selling.. Looking back in at lower gap... $29-$30ish.

Darn.. guessed the wrong way.. Next gab is low 40's.

Got it.. I'm out for now..

U.S. District Court Dismisses Class Action Lawsuit against ProShares

ProShares announced today that on September 10, 2012, the United States District Court for the Southern District of New York dismissed, in its entirety, the class action lawsuit filed against the Company in 2009. The court rejected the plaintiffs’ claim that certain risks associated with holding leveraged and inverse ETFs for periods longer than one day were omitted from the disclosures set forth in the registration statements.

“We have maintained since the beginning of this case that the allegations were wholly without merit, and we are pleased that the claims have been dismissed in their entirety,” said Amy Doberman, ProShares’ General Counsel. “ProShares has demonstrated a long-standing commitment to educating investors about our products and their risks and benefits, so it is gratifying that Judge Koeltl’s ruling rests on the strength and quality of our disclosures.”

In his order dismissing the case, Judge John G. Koeltl ruled that the registration statements accompanying ProShares leveraged and inverse ETFs stated “in plain English” their daily performance objectives and clearly disclosed the possibility that “the ETFs’ value could diverge significantly from the underlying index when the ETFs were held for longer than one day.”

Judge Koeltl’s ruling concluded that ProShares disclosures “addresse[d] the relevant risk directly” in a way that any “reasonably prudent investor would have understood.”

Seems normal trading to me.

almost hit 36