News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Madcowelixir

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Why do you think that "Arms Length Treatment" the BOD granted Ryan "BEFORE" he invested in the 3 notes is?

Ryan's convertible note investment is ARM'S LENGTH (unrelated) to his CEO Fiduciary Duty.

The Notes are just treated as Investor A.

Amerop knows this. So does Amerop's embarrassing law firm.

Now you know.

Amerop's letter of interest expires on Nov 3

Ryan's ARMS LENGTH convertible notes are due Nov 8

If Ryan converts on Nov 8, how does it harm MSLP any greater than if Buck were to purchase $18m of those options?

It doesn't.

Buck is playing games as his letter of intent expires 5 days before Ryan's convertible due date.

Buck's letter of intent no longer exists on Nov 4 and he knows this. The lawyer is playing games.

Buck's ridiculous Hail Mary expires 5 days before Ryan's due date because Buck knows he has ZERO standing and just "hopes" Ryan will grant a courtesy and possible "illegal" heads up on what Ryan will do on Nov 8th notes before other investors.

Buck is just crying over his idiotic decision to invest $4.5m in now worthless common shares with zero security.

Buck can easily be accused of fishing for illegal insider information with this desperate move.

s777

I'm not going to waste a bunch of time tutoring you on tangible or what is often called hard assets (that can be pledged for LOC funded by distressed asset financing firms) and what is often called blue sky or intangible assets such as Intellectual Property, Brand Name, Customer Lists, Distribution channels, etc....

Ryan's collateral covers everything.

Bad news screenshots straight from the SEC filings

What Fiduciary Duty?

Amerop letter of interest expires 5 days before Ryan is obligated to do anything.

Ryan is not obligated to do anything until Nov 8 on his notes.

If he converts on the 8th, the interest payment obligation ceases. Same as what Buck is proposing.

Quit crying Buck. You made a poor investment. Say goodbye to your $4.5m

Financially Illiterate investors here don't realize Amerop's $18m number is not for working capital or anything that helps the day-to-day ops of MusclePharm. Fiduciary Duty doesn't even come into play.

Amerop is holding $4.5m of unsecured worthless shares and is trying to salvage that investment by expressing interest in buying Ryan's secured shares (think preferred shares for you investors with a remedial knowledge).

Amerop simply is interested in "swapping places" with Ryan and Ryan is not obligated to even respond.

Think I can go to Facebook BOD and say I want all Zuckerberg's shares and am willing to pay what he paid. There is no Fiduciary Duty there.

Ryan's shares actually have value as they grant 1st lien on all MusclePharm assets in case of default.

Buck's shares have zero value and he want's Ryan's deal but he is not entitled.

I don't know if Buck felt he had some sort of tacit agreement with Ryan when he bought the Arnold settlement shares in a private transaction and now sees they are worthless with the distressed operating situation MusclePharm finds itself in.

Either Buck got screwed on a handshake deal with Ryan or Buck is the dumbest investor in the world.

It is 50/50 in my opinion.

I suggest anyone interested to go review how many times Amerop letter mentions bankruptcy and how likely it is soon.

Bankruptcy is the most popular word in the Amerop letters.

A few key metrics

MSLP is basically just 2 products.

Combat Protein Powder makes up 35%-55% of total world-wide sales just in the Costco retail channel

Combat Crunch Protein Bars "made" up 35% of world-wide total sales until the Bakery Barn fiasco. We will hear in Q3 earnings release how far this will fall

Total domestic sales (USA) are now down to $14m a Q and trending below $50m a year for 2018 forecast.

With the Bakery Barn fiasco and massive customer rejection we have seen on retail sites (Top 50 list free-fall and customer review revolt), MSLP is toast.

CEO Brad covered the MSLP operating losses by greatly growing revenue that allowed sufficient cash flow to keep the doors open.

CEO Ryan has spiked sales down and now operating losses are only funded with the subprime secured loans on hard assets from Debtor in Possession Finance Companies like CrossRoads and Prestige that specialize in bankruptcy funding for liquidation.

As of the emergency CrossRoads secured loan on Inventory, there are no more assets left upon which to hock.

Everything is either been sold or pledged as collateral.

Amerop is not offering working capital. Amerop is only expressing interest in Ryan's options (controlling interest) as it sees it's $4.5m unsecured investment is just toilet paper.

Amerop letter of interest expires on Nov 3

Ryan is not obligated to do anything on his notes until Nov 7

On Nov 4th, Amerop's letter doesn't exist.

Buck Wessel is an idiot and just realized it 30 days ago.

Amerop is NOT willing to invest an additional $18m in MSLP stock.

Amerop is simply claiming to "express an interest" in "possibly" investing $18m in gaining control of MusclePharm by "maybe" purchasing Ryan's unexercised options on the $18 in notes funded by Ryan.

The letter of interest from Amerop expires on Nov 3. Ryan is not obligated to do anything on his notes until Nov 7. This is a foolish dog and pony act by Amerop with no teeth.

Amerop has already foolishly invested $4.5m in worthless common MSLP shares.

How can Buck sell over 2m shares even if he chose to?

His $4.5m current investment is already worthless (essentially already bankrupt)

He's trapped and desperately flailing around casting wild accusations and when you separate the wheat from the chaff, merely is feeling out if he can invest more to gain secured interest.

Buck has no legal path to security. It is all dependent on what Ryan chooses to do on Nov 7 (19 days from today).

Will Ryan convert? He is legally entitled to do this

Will Ryan declare default on the notes? He is legally entitled to do this

Will Ryan declare MSLP bankrupt? He is legally entitled to do this

Stay tuned.

Less than 1000 shares have traded in the past 5 hours.

Amerop's lawyers charge more than the draw up the ridiculously inane letter.

There is zero volume or interest in this equity.

If a small dead cat bounce before bankruptcy excites you, I feel sorry for financial acumen.

SLC-JD

You're missing a lot

Rather than address your misguided points one-by-one, I will issue the blanket statement that I have addressed each and every one your topics ad nauseam and the archive clearly contains the answers you may be looking for.

Feel free to review Goldberg-Stein on the Seeking Alpha site too for additional help.

Good luck!

Stock is flying

202 shares have traded the past 3 hours

Is the market open?

Haha

MTC

You're welcome to read it and weep. In addition to this security interest collateral upon default specifically spelled out, Ryan has a change of control restriction clause in all three notes.

https://www.sec.gov/Archives/edgar/data/1415684/000141568416000018/mslpq316ex102.htm

MTC

You wrote

I think AMEROP sees value in MSLP anyways, so they would not have amassed 2+MIL shares if they don't. People don't throw millions of money at something to give up so easily.

The real desperation

The real desperation is that Buck Wessell realizes that MusclePharm is very likely to declare bankruptcy any day now and that grants Ryan the ability to foreclose on the assets and take the business under and move to Ryan's place in SoCal

This move has already been announced

Ryan's secured debt due date is Nov 7 (just 19 days from today) and gives him the path to bankruptcy and foreclosing on the assets

That is why Amerop letter specifically has a deadline of 4 days before Ryan's notes due date

Amerop is ready, willing and able to allocate the required resources to complete this transaction on or prior to November 3, 2017.

**Updated**How does 15% shareholder Amerop out vote 48% shareholder Drexler?

Drexler was granted the board seats in the valid convertible debt contract. Yes the notes are due on Nov 7, 2017.

The exclusive asset collateral on the convertible notes are iron clad.

How does Amerop legally gain title outside of bankruptcy disposition of assets in which Ryan clearly owns title?

Your slow motion coup lacks logic or legal precedent.

This is clearly dumb investor panic by Amerop in slow motion realizing he was duped.

Amerop is free to go ahead an sue but good luck common shareholders. The sand has passed through this hourglass.

The only reasonable option Buck Wessel may actually hold is forcing Ryan to convert/not convert on the deadline Nov 7, 2017 as that is Ryan's contractual option.

Buck can't sweeten the offer 1 penny better than Ryan on the due date and trump/steal Ryan's position.

Ryan has the exclusive legal option to convert at $1.83

If Ryan chooses not to convert, then fiduciary duty applies, but Buck is not offering working capital. He is only attempting to steal control from Ryan at this point in the letters.

This in no way benefits common shareholders.

This Wessel attempt is lame. Read the letter for yourself

All this is is an email from a disgruntled minority shareholder who sees his investment going bad.

Ryan is not obligated to mitigate Buck Wessell's stock purchase losses any more than he is to mitigate TexLong and Haig's poor MusclePharm investment losses.

Here is the email.

Interesting read in its desperation. Wessell comes off as very naive.

http://bit.ly/2zz2X1u

The grammar and punctuation would fail high school equivalency test.

The topic and conclusions are inane.

Crying over a -$2m stock investment loss in the letter and blaming the company debt is a red herring.

The issue is operating losses (COGS and SGA).

The debt is a byproduct of the real issue.

The 'new' investment proposal does nothing to solve the company's problem; only addresses the entitlement in disposition of assets.

Disingenuous attempt by a desperate Amerop to mitigate losses based on ignorance and financial illiteracy.

Buck is NOT offering to buy $18m of new unregistered stock to be used as working capital.

Buck is only offering to inject $18m to gain Ryan's controlling interest in MSLP.

Ryan has been rolling the interest payments over (accruing on balance sheet) so no cash expense for MSLP.

MSLP is still posting real EBITDA losses.

Wessel's lame excuse that interest expense is to blame for MSLP's demise is disingenuous.

He is merely desperately flailing illogical assertions with an inane idea he can acquire controlling interest in MusclePharm that Ryan has built for over 2 years because Buck now realizes he was the patsy in the Arnold private transaction legal settlement. Now Bucks $2.15 shares are worth $1.

As an investor, you can only blame yourself as you are responsible for own due diligence regarding management.

It was no secret Brad has a criminal record with academic fraud and bankruptcy in bio before he ever became CEO of MLSP

Same with Ryan.

I provided an immediate unimpressive bio of Ryan on this board regarding his lack of business acumen and failures at activist investing with Quiksilver and Bebe Sport.

I posted his failures in real estate investment and movie production.

Buck's desperation now that he realizes this poor investment is immature and naive.

A harmless and toothless letter with no legal basis nor precedence from an attorney offering to take control of a distressed asset he has no legal entitlement to doesn't scare anyone.

Wessell is attempting the same losing move that Ryan tried and failed with at now bankrupt Quiksilver (ZQK) and now bankrupt Bebe Sport (BEBE). At least Ryan realized he was just an activist investor and not a patsy. Wessel the idiot doesn't have a clue and is now whining like a baby.

Ryan bought several million $$ in open market purchase common shares and wrote activist letters to the respective BOD explaining how he could do it better than existing management but had no legal path to power.

This is exactly what Buck is trying to do in desperation and will lose.

Here are the links to Ryan's failed attempts before MusclePharm

Here is the failed Quiksilver call that is nearly word for word what Buck is trying

http://bit.ly/2zz8GVd

http://prn.to/2yseOAO

Here is the exact same call on BEBE from Ryan. Read it and weep Buck

http://prn.to/2zz8lSq

So one is to believe that CEO who currently owns 48% of the fully diluted shares (unconverted) now agrees to a deal that merely makes him a 6% shareholder just to get his $18m in cash he invested back when he defrauded Capstone?

So now CEO Ryan is just 6% shareholder on a $550K salary.

Okay.

NOT!

Ryan would be left holding just 1.5m shares he purchased in 2014 with an new MSLP Outstanding Share total of 25m of which 11m would be held by unrelated 3rd party Amerop.

Defies logic.

Especially as Ryan's conversion exercise price today is $1.83 and he would just give away the difference for free between his exercise price and the $1.96 Amerop is supposedly willing to pay.

Why would Ryan give away an instant 7% arbitrage return on $18m for nil?

Defies logic.

Ryan has a two year history of rolling over his convertible notes and adjusting the interest rate up 2% every time (from initial 8% in 2015 to 12% currently on the $18m) and adjusting the conversion exercise price from $2.30 in 2015 to $1.83 in 2016 and just had his law firm publish a letter with his intent to do it again and adjusting the conversion to below $1.00

Defies logic.

Believe what you wish.

Why doesn't Ryan do this? Ryan can convert at $1.83 and sell to Amerop for $1.96? There is no logic.

Ryan's terms

Both the principal and the interest under the 2016 Convertible Note are due on November 8, 2017, unless converted earlier. Mr. Drexler may convert the outstanding principal and accrued interest into 6,010,929 shares of the Company’s common stock for $1.83 per share at any time.

On October 17, 2017, Amerop made a proposal to the special committee (the “Special Committee”) of the board of directors (the “Board”) of the Issuer, contained in written materials (the “Amerop Proposal”), indicating its interest in purchasing approximately $18 million of newly issued shares of Issuer Common Stock at a price of $1.96 per share.

This was the fake news salvation a couple weeks ago

This is all "Hide the Baloney" like in a pre-divorce legal proceeding

Ryan is moving the legal title to the remaining assets pre-bankruptcy.

Additionally "expressing interest" from a clearly collusion party is not a legal contract. This is a press release type rumor filing like "Chinese PE firm looks to acquire Accor Properties" or "Nordstrom explores going private" only for unfounded and completely irrational rumors to be dismissed soon and stock crashes.

This is meant to create opportunity to "sell" into the pump. There was ZERO interest in this equity and when the Q3 earnings debacle is made public in about 3 week.......hold your hats.

@idee

Then why not Ryan exercise the options himself at the lower price already contracted in his convertible debt?

Your statement on acquisition makes no logical sense.

Amerop, even if the deal is consumated, would already "acquire" MSLP in bankruptcy proceeding as they would hold title to 100% of the MSLP secured assets. Common shareholders would get nothing.

Notice the "maybe I'm interested in paying 2x market price for equity" came from 3rd party.

Why?

What Is A Quiet Period?

Apart from the quiet period related to IPO offerings, companies observe a quiet period between the time immediately preceding/following the end of the quarter and ahead of its earnings release. The company limits its interaction with investors and analysts during this period just so that it refrains from divulging any information that could unduly influence its stock price.

During the quiet period, the company is privy to the quarterly numbers, although these have not yet been publicly communicated. The quiet period associated with earnings release does not have a standard length and therefore is fixed at the discretion of the company.

How Quiet Periods Play Into The Hands Of Stock Pumpers

Since the company refrains from making any comments on market sensitive information about itself, stock pumpers have an unhindered run during this time to sway the stock in the direction they want to.

A case in point is Twitter's move, defying the logic, ahead of its fourth quarter results. On February 3, a Tweet from the Twitter handle @CalConfidence said Walt Disney Co

DIS 0.16%

is working with a consortium to make a $27 per share all cash offer for Twitter.

Making sense of the spike in Twitter shares on February 7, Charles Gasparino of Fox Business Network tweeted the rally was not due to M&A rumors but due to the company introducing anti-troll rules, which clear the way for a potential takeover in the future.

In a blog post, Twitter announced on February 7 that it is making three new changes to make it a safer place. This included stopping the creation of new abusive accounts, introducing safe search results and collapsing potentially abusive or low quality content.

Stock pumpers, thus, have field days during the quiet period, when companies can do little to refute the unfounded rumors that can be very damaging for the stock. Buyers beware!

Why doesn't Ryan simply convert the contractually agreed debt at a lower price than this Amerop proposal?

Wouldn't that make all the sense in the world if 20m OS dilution is the goal? Debt to Equity swap is completed at a lower exercise price already contracted. Why float the Amerop deal that makes no sense any 3rd party independent investor to pay 2x current market price for equity?

Cleary Ryan's legal team has dissuaded him from his "proposal" to roll the debt over, jack up the rates and slash the exercise option price.

https://www.sec.gov/Archives/edgar/data/1415684/000165495417008273/mslp_8k.htm

Wouldn't that make all the sense in the world if 20m OS dilution is the goal? Debt to Equity swap is completed at an already valid contract with a lower exercise price.

That wouldn't play as well in bankruptcy court.

Now they are floating this deal to Buck where he is paying 2x market price for the debt. It makes sense to no one and will still play off tune in bankruptcy court.

This only moves the assets off-shore during any litigation and limits Ryan's personal liability and moves it Amerop shell.

huh?

The quote contains the word "you" and that is why i added the disclaimer that I didn't mean actually "you" but the accurate historical quote.

When you can't identify the "mark" or "sucker" at the poker table, it's probably "you" is the old poker adage.

I'm not personally attacking actual you but relating the historically accurate adage so you may better understand.

turok

When you can't identify the "mark" or "sucker" at the poker table, it's probably "you" is the old poker adage.

I'm not personally attacking you but relating the adage so you may better understand.

This "transaction" that doesn't even exist yet or may never will, does very little to the balance sheet in any meaningful way.

100% of the assets are still pledged as security in a no cash and sales declining environment that has been 7 alarm bell ringing since the Bakery Barn fiasco.

MSLP is still receiving essentially bankruptcy Debtor in Possession Financing from Prestige Financial @ 20% on Receivables

MSLP is still receiving essentially bankruptcy Debtor in Possession Financing from Crossroads Financial @ 18% on Inventory

What other assets are there on the balance sheet?

Cash?

NONE! MSLP has crashing sales and no impetus to carry inventory they can't afford to purchase from 3rd party contract manufacturers that demand COD upfront.

There are no assets left other than the 2 encumbered (Receivables and Inventory)

MSLP still owes $8m in delinquent Payables (accrued liabilities) in addition to the $9m in current Payables. That is $17m due TODAY of which they have some lint in their pockets.

Operating Losses are still being financed via the Ponzi Scheme and nothing has essentially changed other than the bankruptcy outcome clearing up by moving assets away from Ryan and over to Ryan's proxy (his buddy's FATHER) and eliminating the whole arms length "iffy" transaction.

Why wouldn't Ryan simply convert at the already lower conversion price than the Buck proposal?

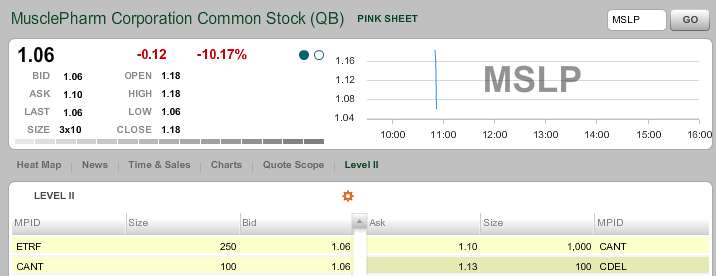

I see .96 cents just a few bids below the current Cantor Fitzgerald (CANT still on best bid and ask) fire sale game that is still being played.

Do we go under $1 PPS today?

Soon.......

Any retail mooches get suckered this morning?

I was speaking of "accrued interest". It is going to Ryan. He is clearly continuing to recoup his underwater investment (as I have repeatably stated as he for the first time began taking $600K in cash out for interest in Q2) and the assets on the balance sheet have been wiped out. The Receivables have been borrowed against @ 20%. The Inventory has been borrowed against @ 18%. BioZone and everything that was or wasn't bolted down has been sold and Ryan is moving out of the MusclePharm HQ complex.

And now we have "indicated interest" in the "conversion" and dilution with over 20m shares outstanding with a couple key insiders holding controlling interest (~70%) into the current "declining sales" environment that is sure continue with Bakery Barn fiasco.

This is a bankruptcy set up.

Ryan is attempting move assets "off-shore" as debt continues to grow at subprime rates to Crossroads Financial and Prestige Financial to fund operating losses.

No more interest?

Where do you see that?

The interest stays the same, it just goes to Buck via the shell game they are playing.

Ryan's $18m in secured debt is due in full in two weeks.

This is a legal maneuver to get Ryan's personal liability limited on several pending lawsuits that he has been named personally as defendant and the "arms length" that is iffy in court..

He is moving the assets "offshore" as they say as bankruptcy is impending.

Oh Grasshoppers

Get a clue.

All of the proceeds of the proposed transaction will be used solely to repurchase and retire immediately at the closing of such proposed transaction the Notes, together with accrued interest, and all rights related thereto.

turok, It says "indicating interest"

I "indicate interest" in buying a 60's era Ferrari Spider. Doesn't mean I bought one and I sure wouldn't offer to pay 2X the current value.

Remember the Doc Frost capital infusion several years ago. Frosty received 2:1 share ratio for every $1 investment. Essentially he invested .50 cents and was granted $1 in equity. The deal made sense.

This "indicating interest" filing by Ryan's good friends FATHER is supposedly offering to pay double the current market price. Why?

This "indicating interest" was already disclosed 2 Quarters ago (6 months) and was being valued at $1.60 a share. Why increase the option price as the stock has gone down -50% since the time of disclosure?

Here is your likely answer:

Ryan is transferring the title to 100% of the MSLP assets to Buck Wessel and curing his "arms length notes" that could get tied up in bankruptcy court with several lawsuits currently pending that he has been sued personally for.

The reason the option price is 2x todays value is that Ryan's option price is that number on the $18m in debt due November 5 and he has to meet the value which is ridiculous over priced.

This can only be part of a take-under and going private move that will leave shareholders holding an empty bag.

Here is a simple tutorial for you cheerleaders

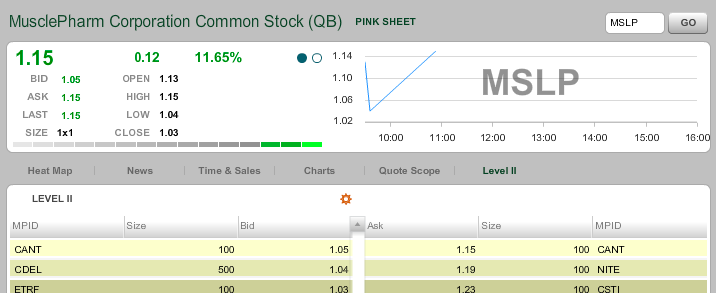

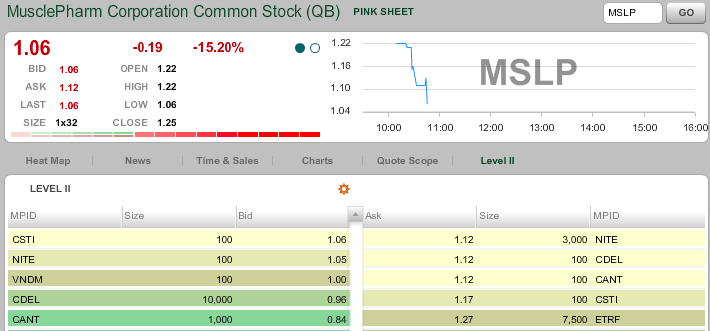

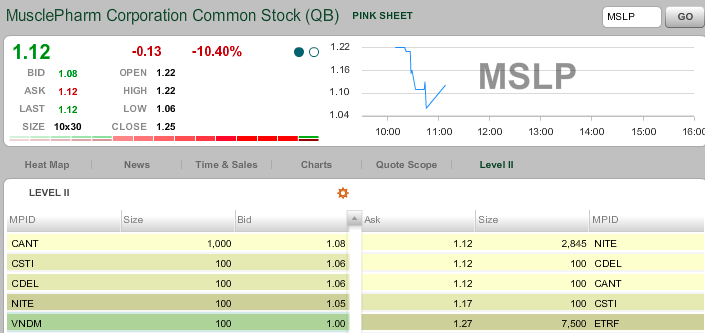

Notice MPID CANT (Cantor Fitzgerald) is the best "bid" and the best "ask" on no authentic retail demand for MSLP stock. CANT pays the exchanges for early sneak peek at all MSLP stock orders (read Flash Boys for details of this arrangement).

Now CANT can either fill an authentic "buy" or "sell" order OR can simply advertise its prices and pull its "bid" or "ask" if any authentic "buy" or "sell" order his placed and then the order falls to next best on LEVEL II.

If you notice, CANT is always the "best ask" even if it pulls its "bid" as CANT is truly a NET SELLER of MSLP stock. They have no intention of buying MSLP stock. They are sellers. In a low or no demand environment like we have in MSLP stock, CANT is able to walk the stock price up by initiating "fake" trades that they are buying and selling to itself. They do this draw attention (PPS going up on the fake volume) from dumb retail investors who may be enticed to "buy" MSLP.

Remember***Important****CANT is always the "best ask" as they are sellers only and the CANT bid is always fake.

Here are 5 recent screenshots when I posted what would happen in real time. Notice CANT is best "bid" and "ask" with ability to fake trade and walk the price up hoping to entice any retail buy orders that CANT will fill.

Here is October 5th. Look at CANT best bid and ask

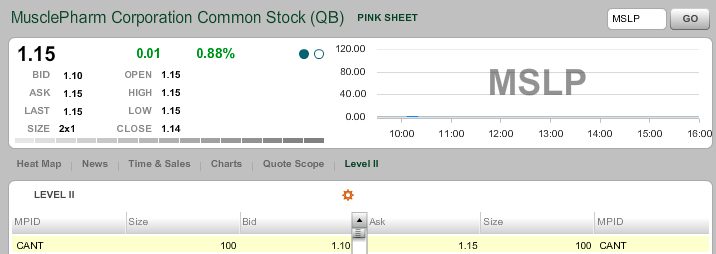

Here is October 6th. Look at CANT best bid and ask

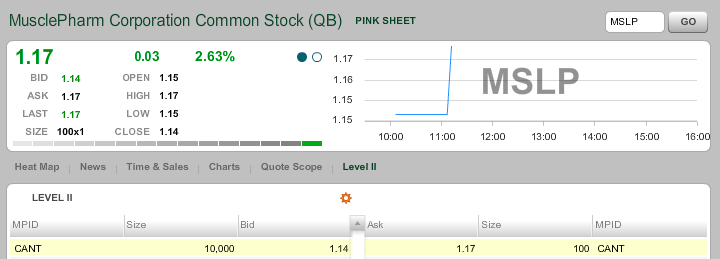

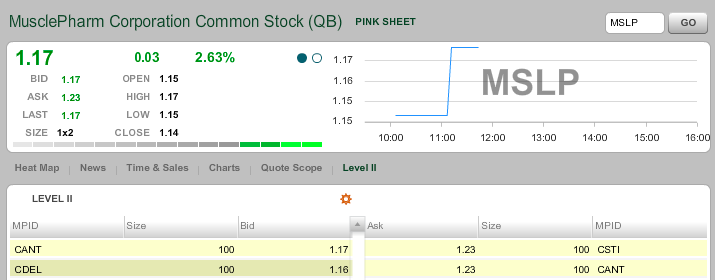

Here is October 10th when I wrote several posts on this thread that CANT would now walk up the price. Look at CANT best bid and ask and trading itself

Step 2 on October 10 best bid and ask trading itself

Step 3 on October 10 best bid and ask trading itself

Then yesterday you have all this fake volume 50K+ shares of fake trading between CANT and CANT. Of course this not real but meant to attract attention. It caught Turokman and S777 as they began posting positive messages about the "bullish" move. CANT trading itself.

Then as I said would happen if an authentic seller came in. CANT would pull its "bid" BUT WOULD KEEP THE "BEST ASK" AS THEY ARE A SELLER NOT A BUYER. Look at this in action this morning. A real seller came in and CANT pulled "bid" and PPS crashed 15% on just a couple thousand real shares traded BUT CANT STAYED ON THE "BEST ASK" (Notice they are on LINE 3 on LEVEL II but as the matching best "ask" they were the seller. They are the HFT with that pays the fees to exchanges to sneak peek the orders and has first priority to pull or fill any retail order before competitors. Again, read Flash Boys for details of this arrangement.

Now REPEAT Process as the authentic seller has finished and CANT can go back to "best bid" and "best ask" and walk up price with fake trading itself again. See this morning after the -15% decline. Pay attention as CANT is on line 3 again on LEVEL II but is technically the "best ask" and first in line to sell but can pull its fake $1.08 bid. Notice how the fake trade from $1.06 up to $1.12 was CANT selling to itself as the authentic seller finished.

The moral of this tutorial is CANT is desperate to sell (or naked short) MSLP stock and is not a buyer. CANT is trying to trap MSLP buyers. They have been doing this for a decent period. Good luck.

What did you say turk and S777?

Like I said....it was all fake and as soon as Cantor Fitzgerald (MPID CANT) pulled their bid (and their fake trading) the equity is crashing again.

MusclePharm getting crushed

Look at how far the "New and Improved" Combat Crunch Bars have fallen to competitors. Nice job on the whole Bakery Barn fiasco CEO Ryan

Sure it did. All on the sell side (bid) including a 25K block that was sold by the same brokerage (Cantor Fitzgerald) to itself as they try to walk it up on fake volume in an attempt to lure dumb retail mooches pre earnings release. Go back and review my previous screen shots of the move in real time as I posted exactly what they would do with no authentic volume/demand last week.

Including 5 separate 3 digit trades. ie $1.272 for 27 shares

That is HFT cover when they get a early exchange peek at the bid/ask and fire on their own shares on a third party order in order to walk it up.

Fake!

What does MusclePharm have left to sell? Can you say broke as a joke? Now MusclePharm is forced to take out $3m loan at 18% interest forced to pledge inventory as collateral. How do you make a profit when you are paying Ryan 15% interest on his debt, Crossroads 18% on Inventory and Prestige 20% on Receivables? Margins (Cost of Goods Sold) were terrible before all the debt interest payments but how do you see a way out under the crushing debt load where everything is pledged as collateral?

How broke is MusclePharm?

They can't afford to buy inventory from suppliers to stock in their most popular retail channels. 8 of 13 products are "unavailable" as MusclePharm doesn't have the cash to pay suppliers who demand MP pay up front in advance before any manufacturing or delivery.

Remember former MSLP CFO John Price who resigned with no notice not long ago?

He took a job with a new company and is still plying the fraud trade like he did at MSLP

He reported operating margin of +43% when it actually was -207%.

He obviously learned his craft at MusclePharm.

MusclePharm lost its lawsuit to Bakery Barn on October 6th.

That is why MSLP was forced to takeout an 18% LOC with Crossroads Financial. To pay off the losing another lawsuit.

The ultimate crazy world of MusclePharm

MusclePharm has no cash in the bank or operating capital of any relevance.

Proof? MusclePharm can't afford to stock inventory in popular retail channels

MusclePharm owes CEO Ryan $18m in a little over 3 weeks and yet the only company statement is that MusclePharm has agreed to pay 18% interest to Crossroads Financial to borrow more money against inventory to keep the checking account from being overdrawn.

The company that buys MusclePharm's Accounts Receivable at a -20% discount to face value already is owed more than the maximum borrowings of the new Inventory collateral Line of Credit so the credit card shuffle is in high gear. Borrowing $ from Crossroads to pay Prestige to pay CEO Ryan's cash bonus for cutting expenses. This is crazy!

The MusclePharm Ponzi Scheme is in the Madoff phase.

Oh, those pony-tailed Trust fund baby CEOs.

You know you're in big trouble....

when your no-name carnitine product is selling better on M&S than the former #1 overall best selling product on M&S.com. The good news is CCB is barely outselling an off brand shaker bottle.

CEO Ryan really stepped in it when he stiffed Bakery Barn and was forced to find another CCB manufacturer. The former customers are livid and are sharing the experience with every review.