News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Bernanke's Former Advisor: "People Would Be Stunned To Know The Extent To Which The Fed Is Privately Owned"

April 12, 2016

With every passing day, the Fed is slowly but surely losing the game.

Only it is not just former (and in some cases current) Fed presidents admitting central banks are increasingly powerless to boost the global economy, even if they still have sway over capital markets. What is far more insidious to the Fed's waning credibility is when former economists affiliated with the Fed start repeating mantras that until recently were only a prominent feature in the so-called fringe media.

This is precisely what happened today when former central bank staffer and Dartmouth College economics professor Andrew Levin, special adviser to then Fed Chairman Ben Bernanke between 2010 to 2012, joined with an activist group to argue for overhauls at the central bank that they say would distance it from Wall Street and make its activities more transparent and accountable to the public.

Levin is pressing for the overhaul with Fed Up coalition activists. Many of the proposed changes target the 12 regional Federal Reserve Banks, which are quasi-private and technically owned by commercial banks in their respective districts.

All of that is not surprising. What he said to justify his new found cause, however, is.

"A lot of people would be stunned to know” the extent to which the Federal Reserve is privately owned, Mr. Levin said. The Fed “should be a fully public institution just like every other central bank” in the developed world, he said in a conference call announcing the plan. He described his proposals as "sensible, pragmatic and nonpartisan."

Why is that stunning? Because it has long been a bone of contention if only among the fringe media, that at its core the Fed is merely a private institution, beholden only to its de facto owners: not the people of the U.S. but to a small cabal of banks. Worse, the actual org chart of who owns what is not disclosed, even as the vast majority of the U.S. population remains deluded that the Fed is a publicly owned institution.

As the WSJ goes on to note, the former central bank staffer said he sees his ideas as designed to maintain the virtues the central bank already brings to the table. They aren’t targeted at changing how policy is conducted today. “What’s important here is that reform to the Federal Reserve can last for 100 years, not just the near term,” he said.

And this is coming from a former Fed employee and Ben Bernanke's personal advisor! That in itself is a most striking development, because now that the insiders are finally speaking up, it will be a race among both current and prior Fed workers to reveal as much dirty laundry as possible ahead of what is increasingly being perceived by many as the Fed's demise.

To be sure, Levin's personal campaign for Fed transformation will not be easy, and as the WSJ writes, what is being sought by Mr. Levin and the activists is significant and would require congressional action. Ady Barkan, who leads the Fed Up campaign, said the Fed’s current structure “is an embarrassment to America” and Fed leaders haven’t been “willing or able” to make changes.

Specifically, Levin wants the 12 regional Fed banks to be brought fully into the government. He also wants the process of selecting new bank presidents—they are key regulators and contributors in setting interest-rate policy—opened up more fully to public input, as well as term limits for Fed officials.

This would represent a revolution to the internal staffing of the Fed, which will no longer be at the mercy of its now-defunct shareholders, America's commercial banks; it would also mean that Goldman Sachs would lose all its leverage as the world's biggest central bank incubator, a revolving door relationship which has allowed the Manhattan firm to dominate the world of finance for the decades.

Levin’s proposal was made in conjunction with the Center for Popular Democracy’s Fed Up coalition, a group that has been pressuring the central bank for more accountability for some time. The left-leaning group has been critical of the structure of the regional banks, and has been pressing the Fed to hold off on raising rates in a bid to make sure the recovery is enjoyed not just by the wealthy, in their view.

The proposal was revealed on a conference call that also included a representative from Bernie Sanders’s presidential campaign, although all campaigns were invited to participate.

The WSJ adds that according to Levin, who knows the Fed's operating structure intimately, says the members of the regional Fed bank boards of directors, the majority of whom are selected by the private banks with the approval of the Washington-based governors, should be chosen differently. The professor says director slots now reserved for financial professionals regulated by the Fed should be eliminated, and that directors who oversee and advise the regional banks should be selected in a public process involving the Washington governors and local elected officials. These directors also should better represent the diversity of the U.S.

Levin also wants formal public input into the selection of new bank presidents, with candidates’ names known publicly and a process that allows for public comment in a way that doesn’t now exist. The professor also wants all Fed officials to serve for single seven-year terms, which would give them the needed distance from the political process while eliminating situations where some policy makers stay at the bank for decades. Alan Greenspan, for example, was Fed chairman from 1987 to 2006.

As the WSJ conveniently adds, the selection of regional bank presidents has become a hot-button issue. Currently, the leaders of the New York, Philadelphia, Dallas and Minneapolis Fed banks are helmed by men who formerly worked for or had close connections to investment bank Goldman Sachs.

Levin called for watchdog agency the Government Accountability Office to annually review and report on Fed operations, including the regional Fed banks. He also wants the regional Fed banks to be covered under the Freedom of Information Act. A regular annual review hopefully would insulate the effort from perceptions of political interference, Mr. Levin said.

* * *

While ending the Fed may still seem like a pipe dream, at least until the market's next major crash at which point the population may finally turn on the culprit behind America's serial boom-bust culture, the U.S. central bank, Levin's proposal would get to the heart of the most insidious conflict of interest in the US: the fact that the Federal Reserve works not for the people of America, but for its owners - the banks.

Which is also why, sadly, this proposal will be dead on arrival, as its passage would represent the biggest loss for Wall Street in the past 103 years, far more significant than anything Dodd-Frank could hope to accomplish.

http://www.zerohedge.com/news/2016-04-11/bernankes-former-advisor-people-would-be-stunned-know-extent-which-fed-privately-own

The ‘Data Dependent’ Fed Blows Its Cover… Annihilates Its Credibility

by Wall Street Journal

March 18, 2016

Normal is a lot harder than it looks.

The Federal Reserve on Wednesday not only refrained from raising interest rates, but it telegraphed that it would almost certainly raise rates at an even slower pace than it previously expected. This is a break from its outlook of just three months ago, when it raised its benchmark rate at the December meeting and laid out the path for the awkwardly phrased “policy normalization.”

The Fed has been talking about normalizing rates for several years now, so it’s rather jarring that just a few months after it starts doing just that, it handcuffs its own policy. Even more odd is that the data back up its original goals. All of this gives a short-term boost to the risk-on set, but it is unsettling to anybody who’s time-frame is not measured in nanoseconds.

In December, the Fed concluded that the economy was largely headed in the right direction, that the twin mandate of maximizing employment and stable prices were being met. The bank also clearly stated that it understood that policy works with a time lag, and that in order to get prices and jobs good and maximized, it needed to act then, knowing those higher rates would take some months to work their way through the system.

All that disappeared yesterday, as the Fed quickly reversed field. “It was as if a light bulb went off,” UBS’ Art Cashin wrote. The four rate hikes the Fed had been planning on for this year suddenly became two.

The practical result of all this can been seen in the U.S. dollar this morning. The dollar is down 1% against the euro and 1.2% against the yen. The WSJ Dollar Index is down 1%. “No matter where you turn, U.S. dollar charts are ‘puking,’ ” said DailyFX currency analyst Christopher Vecchio. “Most everyone was on one side of the trade, and now everyone is rushing for the exits at the same time.”

The dollar selloff started, in fact, with the first question asked of Ms. Yellen at Wednesday’s press conference. CNBC’s Steve Liesman asked if the Fed now had a credibility problem, after reversing itself so quickly. Ms. Yellen of course answered no, but the market seems to feel different. “At that point,” Dennis Gartman wrote in his daily newsletter, “the dollar was doomed. It remains ‘doomed’ thus far this morning and it may worsen we fear.”

Why does the Fed have a credibility problem?

Because it has been arguing for months, years, that it is being guided by data – by U.S. data – but yesterday’s decision simply does not comport with the data. Unemployment is at 4.9%. Inflation is rising – the year-over-year “core” CPI reported on Wednesday morning came in at 2.3%. We understand that isn’t the Fed’s “preferred” gauge, but it is also not an entirely ignored gauge either. More importantly, in the three months since the Fed’s December meeting, both of these measures have further strengthened.

If you’re in the camp that thinks the odds of a recession are material if not overwhelming, then the Fed stepped back from a potentially obvious policy mistake: raising rates too soon. This is something that the Fed rather infamously did all the way back in 1937, and critics have never let them forget it. Indeed, we’ve been seeing references to 1937 for years. Here’s Bruce Bartlett writing in the New York Times on the topic in 2011. Here’s Christina Romer writing in the Economist on the topic – in 2009.

There is, however, nothing in the data that signal an imminent recession. There just isn’t. You can make all the arguments you want that point to the fallibility of the data – we do all the time – but if you’re telling the world over and over that you are “data dependent” and then you stop depending upon the data, you can see how that might confuse a few folks. What exactly is the Fed looking at now, if not the data? “The Fed’s goal is now a perfect world,” Lindsey Group’s Peter Boockvar wrote. “As we of course will never get there, the rest of us are left flying blind as to what to expect from monetary policy.”

If the data are right and the Fed is dragging its feet, that could still result in a policy mistake. Indeed, Ms. Yellen was asked if the Fed is intentionally letting inflation overshoot the target. The Fed’s credibility problem will either be amplified if the economy doesn’t behave, or vaporized if it does. The ultimate arbiter will be reality.

http://davidstockmanscontracorner.com/the-data-dependent-fed-blows-its-cover-annihilates-its-credibility/

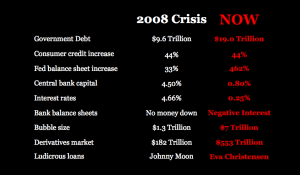

9 Signs That 2016 Looks Ominously Like 2008 (Just Before The Crisis)

by Simon Black via SovereignMan.com

March 17, 2016

If you haven’t seen the 2015 Best Picture nominee, The Big Short, I strongly recommend it.

The Big Short is based on Michael Lewis’ book which examines how such an extraordinary financial crisis gripped the world in 2008, and the handful of people who saw it coming.

The movie opens asking a very simple question about the global financial meltdown:

Wall Street missed it; the Federal Reserve missed it; the government missed it; every major financial institution missed it; the homebuilders missed it.

So how is it that a handful of people were able to see it coming? How could they see what nobody else saw?

Easy. They looked.

For anyone who actually looked, it was obvious that the banking and housing boom in the early 2000s was built on a house of cards. The data was all there.

Given the financial establishment’s astonishingly short-term memory and capacity to make even bigger mistakes than ever before, we now find ourselves in a very similar position today.

Once again, the financial system is in desperate condition. And the data is all there for anyone who cares to look.

Let’s look at a few of the numbers together.

Back in 2008, much of the calamity was caused by an implosion of “subprime loans” in the housing market.

These were frequently no-money down loans at teaser interest rates made to people with poor credit and limited income.

Banks made these toxic loans with your money.

The best example of this was probably Johnny Moon, a homeless man with no income or employment history who was able to borrow more than $600,000 to speculate in real estate.

The total value of these subprime loans was a whopping $1.3 trillion.

Not much has changed.

In 2016, instead of loaning money to subprime home buyers, the financial system is now loaning money to bankrupt governments.

They’ve even managed to go beyond “no-money down”, and are actually paying governments to borrow money at negative interest rates.

Japan is as great example.

Even though Japan’s national debt exceeds 200% of GDP, and it takes over 25% of tax revenue just to pay interest on the debt, the Japanese government is able to borrow money for ten years at negative interest.

This means that investors are GUARANTEED to lose money. It’s worse than no money down. And it’s total madness.

The bigger issue is that the size of this bubble is an astounding $7 trillion, far bigger than the subprime bubble in 2008. And it grows larger by the day.

To expect that this will turn out any differently is foolish.

Back in 2008, US government debt was “only” $9.5 trillion. The Federal Reserve’s balance sheet was $850 billion. Interest rates were over 4%.

So at least they had some capacity to slash interest rates and fight the crisis using traditional policy tools.

Today, US government debt exceeds $19 trillion, well in excess of 100% of GDP.

They have to borrow money just to pay interest, and they have entire pension funds that are on the brink of bankruptcy.

The Federal Reserve’s balance sheet has exploded to $4.5 trillion, and interest rates are barely above zero.

The government has no means to bail anyone out, including itself. And the Fed has no capacity to print more money and expand its balance sheet without causing a major currency crisis.

Simply put, the bubble is just as insane as in 2008, but much bigger. And the financial establishment has no ammunition to fight it.

If you want a more detailed comparison of the 9 most ominous similarities between 2008 and 2016 click here to watch today’s video podcast.

https://www.sovereignman.com/sm-presentation/?utm_source=sm_prospects&utm_medium=website&utm_campaign=egw_webinar&utm_content=email_notes_160317

Why The Fed Is Paralyzed - Its Economic Model Is Junk

Jeffrey Snider via Alhambra Investment Partners

March 17, 2016

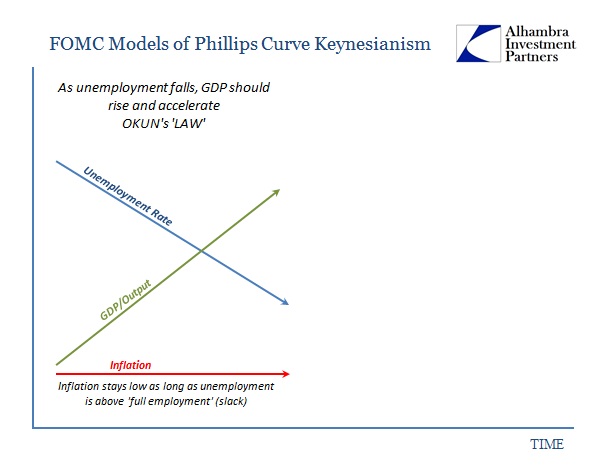

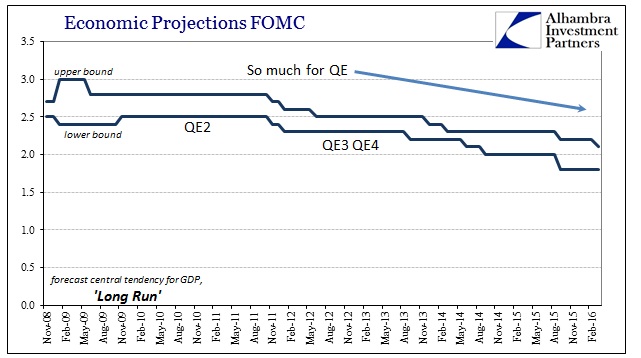

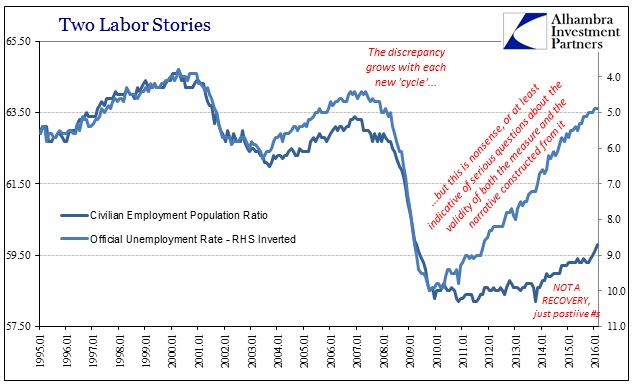

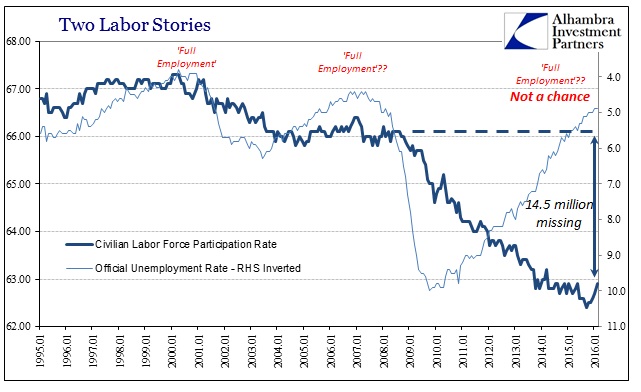

If there is any doubt as to the confusion inside the FOMC, one needs only to examine its models. The latest updated projections make a full mockery of both monetary policy and the theory that guides it. Ferbus and the rest don’t buy the labor market story, either, which is why the Fed can only be hesitant at best about “normalization.” Coming from the (neo or not) Keynesian persuasion, what is showing up should never happen.

The theoretical notion of recovery is very straightforward in orthodox economics. In recession, the economy starts with high unemployment and therefore low inflation. Using the Phillips Curve as a short-term guide, orthodox models assume that as levels of unemployment begin to normalize, output (GDP) will rise. That will occur first without any uptick in inflation as the “slack” produced by the recession keeps price pressures to a minimum.

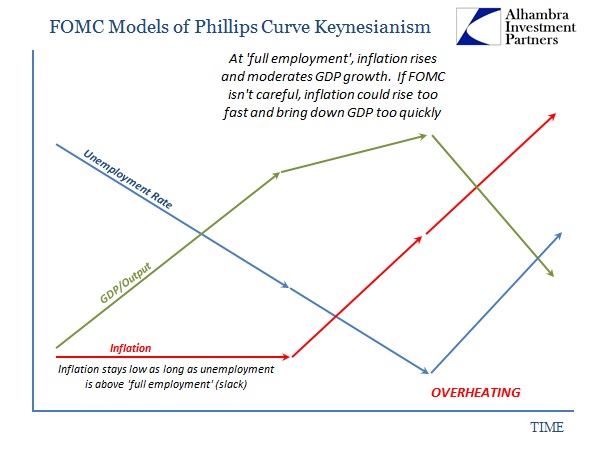

In Stage 1 everything is easy, so long as you can gain forward momentum in unemployment or output (which is what the QE’s were supposed to accomplish with regard to theoretical notions of hysteresis). Stage 2 gets slightly more complicated as the economy nears or reaches “full employment.” At that point, inflation should start to rise which will moderate output growth. If it progresses too far, that means the economy has reached “overheating” whereby inflation gets out of control and actively suppresses output, even reversing employment gains.

By the simple act of communicating a rate hike in December (though not actually carrying it out in meaningful fashion), the FOMC proclaimed closeness to overheating. But there is a huge problem with not just observed conditions but also projected economic conditions for the immediate future. If the economy and recovery has progressed sufficiently through Stage 2 to demand policy action before overheating, we should see a concurrent rise in inflation as well as output. The FOMC estimates show no such thing; worse, they estimate the opposite for especially inflation, as modeled GDP projections continue to muddle. That was true for not just CY 2015 as it was completed in full disappointment, but now encompassing CY 2016 as well.

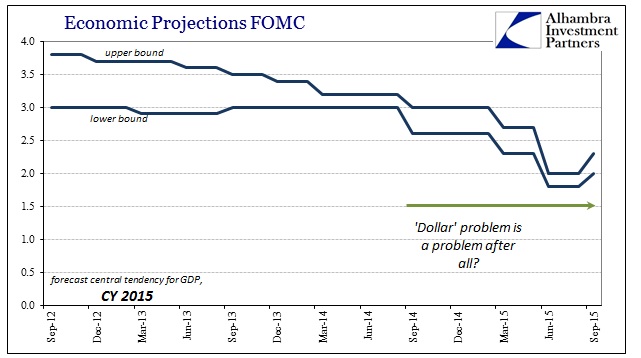

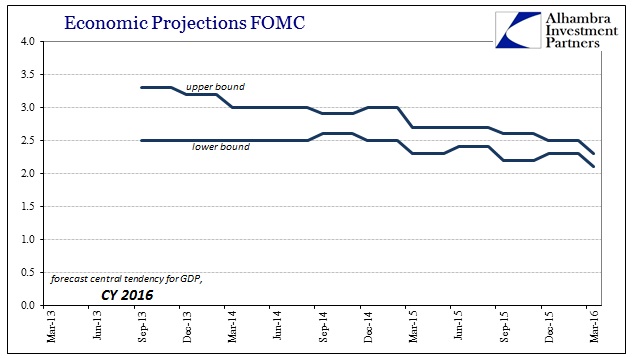

Both years start out in the earliest projections as they should according to theory, or close enough to be plausible; GDP should accelerate to at least something significantly better than the deficient output expansion of the recent past. Instead, as time rolls forward, that acceleration never materializes as GDP has stagnated around 2% year after year. The March 2016 projections show yet again another year absent acceleration in output (losing track of how many years in a row that would make).

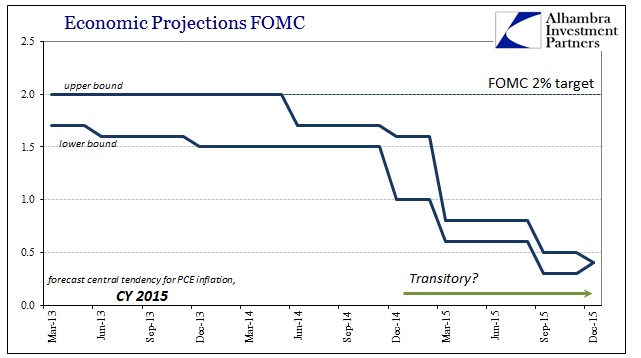

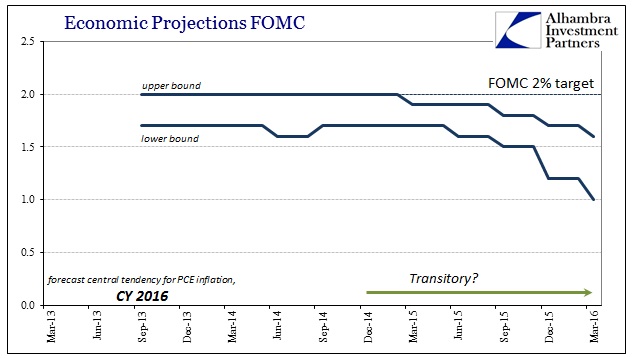

In terms of inflation, the trends are even worse. When oil prices first crashed in late 2014/early 2015 that was demanded to be “transitory” uniformly across both models and orthodox interpretations (redundant, I know). A year later, not only did inflation never materialize for the rest of 2015, it is now modeled to be increasingly absent in 2016, as well.

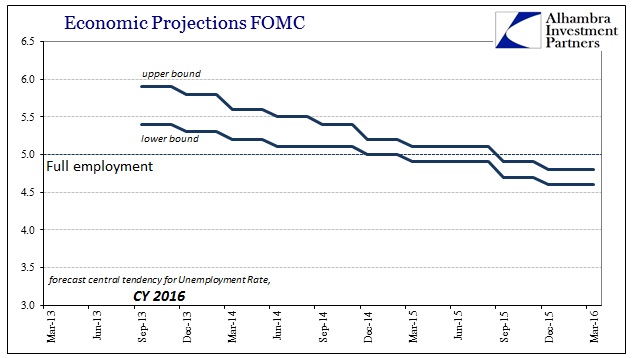

That’s a huge problem because the unemployment rate only gets better and better at each forecast. Back in late 2013 as the sounds of taper grew louder, the FOMC’s staff models projected the unemployment rate in 2016 would only be 5.4% to 5.9% (central tendency). That was forecast as a relatively slow improvement because output growth had been so lacking to that point, and even though it was expected to accelerate it was never thought to attain true recovery mechanics (something more like 4-5% rather than 3-3.5%). Instead, as noted above, GDP growth never accelerated at all – but the unemployment rate fell far faster than orthodox theory predicted anyway. In fact, so fast it asserts a major problem somewhere because Okun’s Law suggests GDP should have been, given the unemployment rate improvement, not just higher than 2.1% to 2.3% but higher than even the 3.3% once thought the upper bound back in 2013.

In other words, in late 2013 the models suggested relatively modest GDP of 2.5% to 3.3% in 2016 which would bring unemployment down also modestly to 5.4% and perhaps as high as 5.9%. That progress was supposed to be closing in on full employment enough to propel inflation very close to the 2% target for the PCE deflator. Instead, as of the March 2016 projections, the unemployment rate is expected to be enormously lower at just 4.6% to 4.8%, but GDP still stuck (and being downgraded each quarter) at 2.1% to 2.3% while inflation at the lower bound of the central tendency is 1%? One of these factors really doesn’t add up even in this orthodox context.

It isn’t difficult to determine which one, as persistently low calculated “inflation” is fully consistent with insufficient economic growth (or worse) for the nth year in a row. It is the huge and unexpected improvement in the unemployment rate blowing right on past “full employment” almost two years faster than predicted that is completely out of line; this “best jobs market in decades” that doesn’t project beyond really questionable BLS statistics.

As if to emphasize this statistical struggle against orthodox theory, the models are “forced” by the inequity between reported unemployment and the continuing disagreement via output and inflation to reduce to the long run growth rate estimate in order to make 2.2% growth seem like it could possibly belong in Stage 2 as if it were acceleration.

That means the unemployment rate is so far out of whack that the FOMC, a committee dedicated to believing in it above all else, really cannot base monetary policy on the most basic Keynesian, Phillips Curve assumptions. In fact, by count of even orthodox theory, the unemployment rate cannot be real. It doesn’t take much survey outside of these three variables to confirm the suspicion. As much as policymakers want it to be meaningful and representative, the fact that their own models not only fail to confirm it but openly refute it (with emphasis) is why Janet Yellen is slow on the rate hikes even though she talks about the jobs market at every opportunity (as if the unemployment rate as merely a number were, rational expectations, itself a stimulant that QE never was or could be).

It was the best jobs market in decades that once again finds nobody actually in it; not even the economists.

http://www.zerohedge.com/news/2016-03-17/why-fed-paralyzed-its-economic-model-junk

World’s Second Largest Reinsurer Buys Gold, Hoards Cash To Counter Negative Interest Rates

March 17, 2016

The world’s second-largest reinsurer, German Munich Re which is roughly twice the size of Berkshire Hathaway Re, is boosting its gold reserves and buying gold in the face of the punishing negative interest rates from the European Central Bank, it announced today.

As caught by Mark O'Byrne at GoldCore and reported by Thomson Reuters this afternoon, the world’s largest reinsurer is far from alone in seeking alternative investment strategies to counter the near-zero or negative interest rates that reduce the income insurers require to pay out on policies.

Munich Re has held gold in its coffers for some time and recently added a cash sum in the two-digit million euros, Chief Executive Nikolaus von Bomhard told a news conference.

“We are just trying it out, but you can see how serious the situation is,” von Bomhard said.

The ECB last week cut its main interest rate to zero and dropped the rate on its deposit facility to -0.4 percent from -0.3 percent, increasing the amount banks are charged to deposit funds with the central bank.

Munich Re is one of the largest reinsurance companies in the world - It oversees €231 billion in investments. A small 3% allocation to gold would equate to buying gold worth €8.19 billion. At the current spot price of €1,130 per ounce that would equate to 7.2 million ounces or 225.4 tonnes of gold bullion

The news is interesting and we believe that other institutions will follow in their footsteps and diversify into gold in order to protect themselves from negative yields. We have not heard of any other non central bank institutions diversifying into gold but it stands to reason that a small percentage will follow in Munich Res footsteps.

* * *

It isn''t just gold: the German company confirms that when rates turn negative enough, physical cash will be increasingly more valuable.

As Bloomberg reports, the German company will store at least 10 million euros ($11 million) in two currencies so it won’t have to pay for the right to access the money at short notice, von Bomhard said at a press conference in Munich on Wednesday. “We will also observe what others are doing to avoid paying negative interest rates,” he said.

Institutional investors including insurers, savings banks and pension funds are debating whether it may be worth bearing the insurance and logistics costs of holding physical cash as overnight deposit rates fall deeper below zero and negative yields dent investment returns. The ECB last week cut the rate on its deposit facility, which banks use to park excess funds, to minus 0.4 percent.

“This may well become a mass phenomenon once interest rates are low enough -- the only question will be where that exact point is,” said Christoph Kaserer, a professor of finance at the Technische Universitaet in Munich. “For large institutions, that may be the case sooner rather than later. The ECB will react with countermeasures, such as limiting cash.”

As Bloomberg adds, Munich Re’s strategy, if followed by others, could undermine the ECB’s policy of imposing a sub-zero deposit rate to push down market credit costs and spur lending. Cash hoarding threatens to disrupt the transmission of that policy to the real economy.

Munich Re, which oversees a total of 231 billion euros in investments, wants to test how practical it would be to store banknotes, having already kept some of its gold in vaults, von Bomhard said. This comes at a time when consumers are increasingly using credit cards and electronic banking to pay for transactions. Deutsche Bank AG Chief Executive Officer John Cryan has predicted the disappearance of physical cash within a decade.

“This shows the difficulties that the ECB is facing in its efforts to stimulate the real economy,” said Andreas Oehler, a professor of finance at Bamberg University in Bavaria. “Charging negative rates on overnight liquidity doesn’t stimulate longer-term lending. All it does is make companies’ and institutions’ payment transactions more expensive.”

Incidentally, once the Fed's infatuation with playing central planning doctor fizzles as the economy relapses into an accelerating downward spiral, negative rates are coming to the US next, as such the real-time experiments of how to evade a repressive monetary regime such as those conducted by the Munich Re CEO will be particularly useful to those who want to protect their assets once NIRP crosses the Atlantic.

http://www.zerohedge.com/news/2016-03-16/world’s-second-largest-reinsurer-buys-gold-hoards-cash-counter-negative-interest-rat

Oil Prices Heading For A Fall, Possibly Hard

by Forbes • March 11, 2016

By Art Berman at Forbes

Oil prices should fall, possibly hard, in coming weeks. That is because fundamentals do not support the present price.

Prices should fall to around $30 once the empty nature of an OPEC-plus-Russia production freeze is understood. A return to the grim reality of over-supply and the weakness of the world economy could push prices well into the $20s.

A Production Freeze Will Not Reduce The Supply Surplus

An OPEC-plus-Russia production cut would be a great step toward re-establishing oil-market balance. I believe that will happen later in 2016 but is not on the table today.

In late February, Saudi oil minister Ali Al-Naimi stated categorically, “There is no sense in wasting our time in seeking production cuts. That will not happen.”

Instead, Russia and Saudi Arabia have apparently agreed to a production freeze. This is meaningless theater but it helped lift oil prices 37% from just more than $26 in mid-February to almost $36 per barrel last week. That is a lot of added revenue for Saudi Arabia and Russia but it will do nothing to balance the over-supplied world oil market.

The problem is that neither Saudi Arabia nor Russia has greatly increased production since the oil-price collapse began in 2014 (Figure 1). A freeze by those countries, therefore, will only ensure that the supply surplus will not get worse because of them. It is, moreover, doubtful that Saudi Arabia or Russia have the spare capacity to increase production much beyond present levels making the proposal of a freeze cynical rather than helpful.

Saudi Arabia and Russia are two of the world’s largest oil-producing countries. Yet in January 2016, Saudi liquids output was only ~110,000 bpd more than in January 2014 and Russia was actually producing~50,000 bpd less than in January 2014. The present world production surplus is more than 2 mmbpd.

By contrast, the U.S. plus Canada are producing ~1.9 mmbpd more than in January 2014 and Iraq’s crude oil production has increased~1.7 mmbpd. Also, Iran has potential to increase its production by as much as ~1 mmbpd during 2016. Yet, none of these countries have agreed to the production freeze. Iran, in fact, called the idea “ridiculous.”

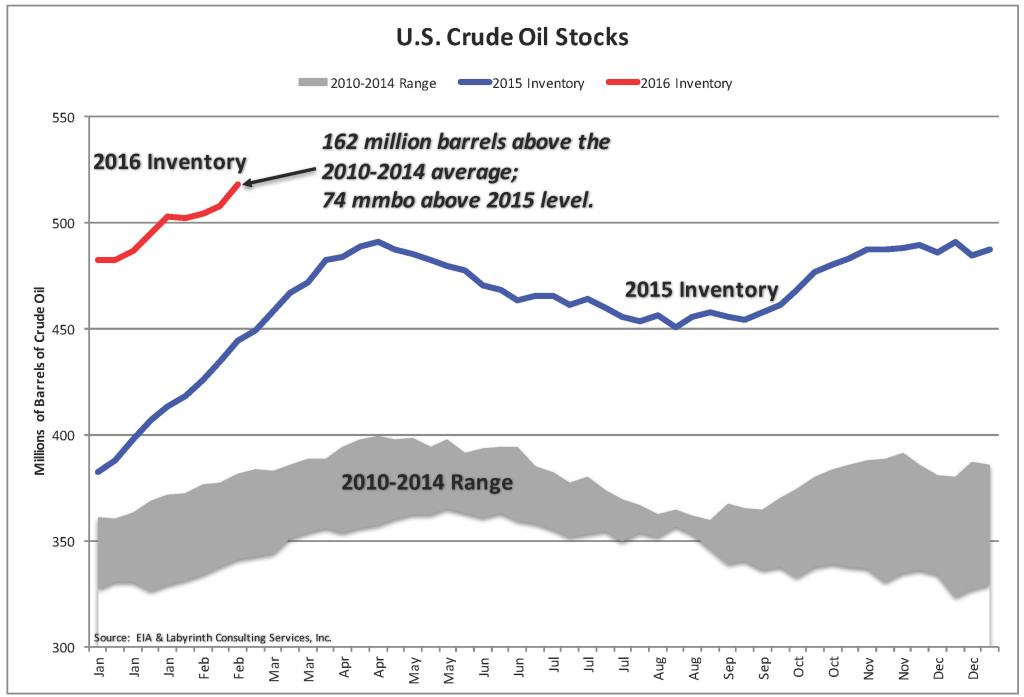

Growing Storage Means Lower Oil Prices

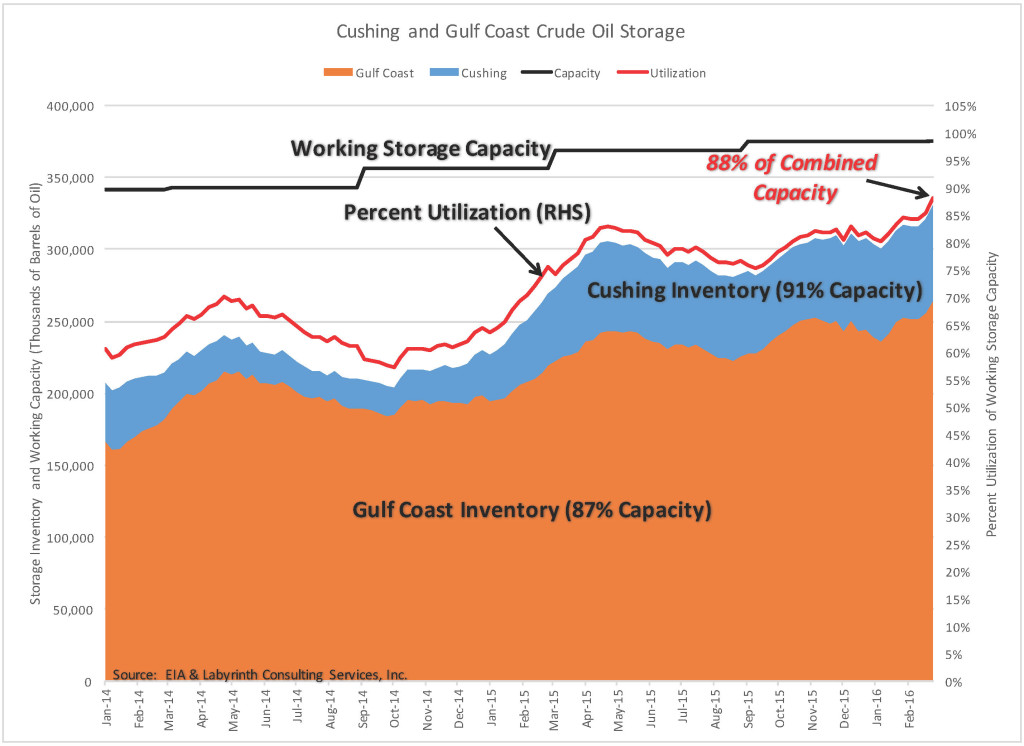

U.S. crude oil stocks increased by a remarkable 10.4 mmb in the week ending February 26, the largest addition since early April 2015. That brought inventories to an astonishing 162 mmb more than the 2010-2014 average and 74 mmb above the bloated levels of 2015 (Figure 2).

The correlation between U.S. crude oil stocks and world oil prices is strong. Tank farms at Cushing, Oklahoma (PADD 2) and storage facilities in the Gulf Coast region (PADD 3) account for almost 70% of total U.S. storage and are critical in WTI price formation. When storage exceeds about 80% of capacity, oil prices generally fall hard. Current Cushing storage is at 91% of capacity, the Gulf Coast is at 87% and combined, they are at a whopping 88% of capacity (Figure 3).

Prices have fallen hard in step with growing storage throughout 2015 and early 2016. Since talk of a production freeze first surfaced, however, intoxicated investors have ignored storage builds and traders are testing new thresholds before they fall again.

The truth is that prices will not increase sustainably until storage volumes fall, and that cannot happen until U.S. production declines by about 1 mmbpd.

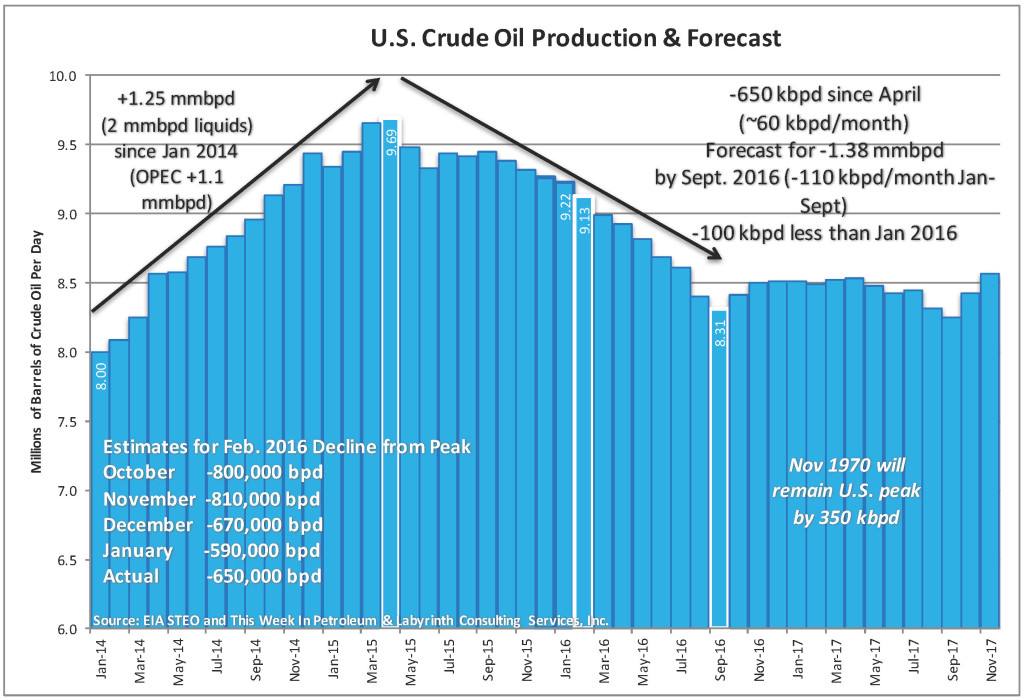

Despite extreme reductions in rig count and catastrophic financial losses by E&P companies, production decline has been painfully slow. Thelatest data from EIA indicates that February 2016 production will fall approximately 100,000 bpd compared to January (Figure 4).

That is an improvement over the average 60,000 bpd monthly decline since the April 2015 peak. It is not enough, however, to make a difference in storage and storage controls price.

EIA and IEA will publish updates this week on the world oil market balance and I doubt that the news will be very good. IEA indicated last month that the world over-supply had increased almost 750,000 bpd in the 4th quarter of 2015 compared with the previous quarter. EIA data corroborated those findings and showed that the surplus in January 2016 had increased 650,000 bpd from December 2015.

Oil Prices and The Value of the Dollar

Why, then, have oil prices increased? Partly, it is because of hope for an OPEC production freeze and that sentiment is expressed in the OVX crude oil-price volatility index (Figure 5).

The OVX reflects how investors feel about where oil prices are going. It is sometimes called the “fear index.” That suggests that investors are feeling pretty good and less fearful about the oil markets than in the last quarter of 2015 when oil prices fell 47%. Since mid-February, prices have increased 37%.

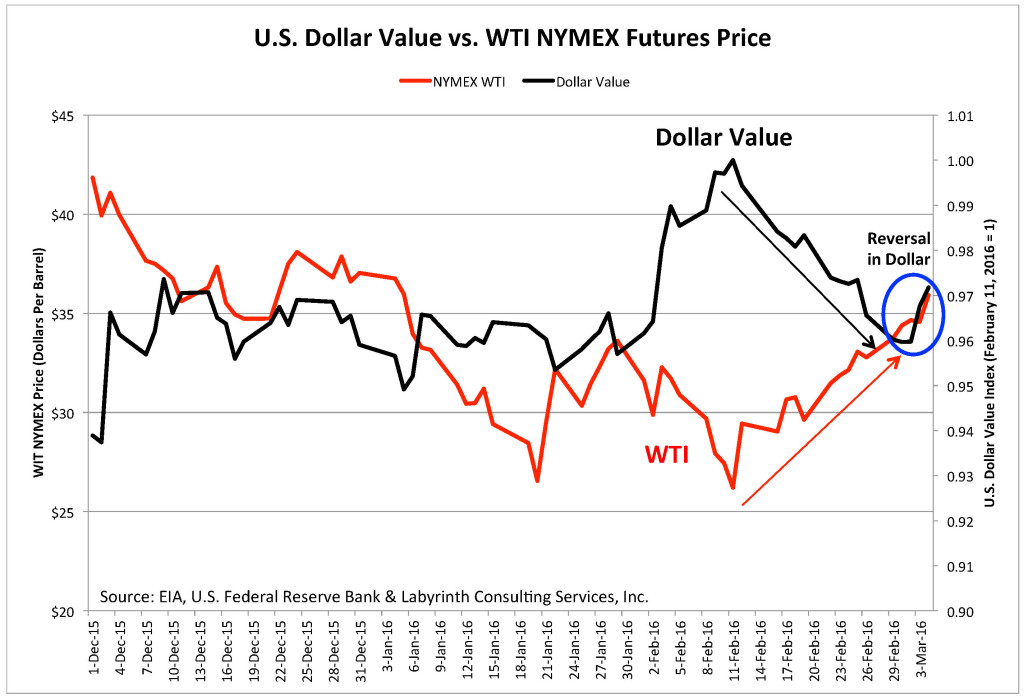

But there is more to it than just hope and that may be found in the strength of the U.S. dollar. The negative correlation between the value of the dollar and world oil prices is well-established. The oil-price increase in February was accompanied by a decrease in the trade-weighted value of the dollar (Figure 6).

Now, that trend has reversed. The U.S. jobs report last week was positive so continued strength of the dollar is reasonable for awhile. Assuming the usual correlation, that means that oil prices should fall.

Oil Prices Should Fall Hard

It is a sign of how bad things have gotten in oil markets that we feel optimistic about $35 oil prices. It should also be a warning that the over-supply that got us here has not gone away.

Oil storage volumes continue to grow and that is the surest indication that production has not declined enough yet to make a difference. It is impossible to imagine oil prices rising much beyond present levels until storage starts to fall. In fact, it is difficult to understand $35 per barrel prices based on any measure of oil-market fundamentals.

The OPEC-plus-Russia production freeze is a cynical joke designed to increase their short-term revenues without doing anything about production levels. An output cut would make a difference but a freeze on current Saudi and Russian production levels means nothing. It apparently made some investors feel better but it didn’t do anything for me. Iran got this one right by calling it ridiculous.

No terrible economic news has surfaced in recent weeks but that does not change the profound weakness of a global economy that is burdened with debt and weak demand. The announcement last week by the People’s Bank of China that it sees room for more quantitative easing may have comforted stock markets but it only added to my anxiety about reduced oil consumption and future downward shocks in oil prices.

I hope that oil prices increase but cannot find any substantive reason why they should do anything but fall. As market balance reality re-emerges in investor consciousness and the false euphoria of a production freeze recedes, prices should correct to around $30. A little bad economic or political news could send prices much lower.

Now, that trend has reversed. The U.S. jobs report last week was positive so continued strength of the dollar is reasonable for awhile. Assuming the usual correlation, that means that oil prices should fall.

http://www.forbes.com/sites/arthurberman/2016/03/07/oil-prices-should-fall-possibly-hard/#7a8fc1196f45

"Gloom" Returns To China's Economy: Industrial Production, Retail Sales Miss Lowest Estimates

03/12/2016

After an unprecedented surge in Chinese attempts to stimulate the economy in late 2015, mostly on the fiscal side, coupled with recent monetary easing by the PBOC which cut the banks' reserve ratio recently and unleashed a tsunami of new loan creation in January, many expected that this unprecedented credit impulse would translate into at least a modest rebound for the economy, prompting a stable pick up in spending for the economy which many are touting is now consumer-spending driven as opposed to export and production.

However, that did not happen: according to data released overnight by the National Bureau of Statistics, Chinese factories and retailers not only missed expectations, but slowed down materially from the December prints, as anemic demand and excess capacity continued to bear down on the world’s second-largest economy.

Specifically, Jan-Feb factory output grew just 5.4% in January and February from a year earlier, data released by the National Bureau of Statistics (NBS) showed, slowing from a 5.9% rise in December to the weakest since November 2008; the print matched the lowest Wall Street estimate.

Meanwhile, retail sales rose 10.2% over the two-month period from a year ago, below the lowest Wall Street estimate of 10.5%, and far below the December’s 11.1% increase, pushing the trend growth in this series to lows not seen since early 2015.

"Overall, the picture is still quite gloomy," said Commerzbank AG economist Zhou Hao. “Normally, because of Chinese New Year, there’s a big drop and a big jump. This year there’s only a big drop.”

The retail data was particularly disappointing because as the WSJ writes "while industries have been battered by the economic slowdown, retail sales have been relatively buoyant, so the downtick surprised some economists, especially since it occurred around the Lunar New Year holiday when consumption is usually strong."

And to think record, if fake, box office numbers were supposed to carry China's economy in the aftermath of the absolutely disastrous trade data released earlier in the month.

To be sure, the commentary immediately explained that the weak data will mean even more stimulus, even though it was just last week when the Congress laid out all the measures that China will adopt to assure "GDP growth" of 6.5%-7.0%.

Here's Reuters: "China's activity data remained weak in the first two months of 2016, with factory output growth hitting the weakest since the global financial crisis, keeping pressure on policymakers to do more to avert a sharper showdown in the world's second-largest economy."

Unlike the recent collapse in Chinese exports and imports, the overnight data could not be "explained away" due to calendar effects as it combines the January and February timeframe: China's government combines some economic data for January and February to minimize distortions tied to the Lunar New Year holiday, which falls during those two months. It was in early February this year.

It wasn't all bad news: one area that did pick up was investment in factories, buildings and other fixed assets, which increased a faster-than-expected at 10.2?% year-over-year in January and February, compared with a 10% increase for all of 2015. However, economists said that boost came largely from government spending on infrastructure and from investment in parts of the overbuilt property market.

In other words, China is adding even more excess capacity to an economy already drowning in excess capacity.

Ultimately, the problem for China remains: weak demand at home and abroad is weighing on industries and many factories continue to churn out unneeded goods. "A recovery is still eluding China’s industrial sector,” Mizuho Securities Asia Ltd. said in a recent report, before the release of the data Saturday.

Worse, for all the talk about a massive stimulus, China's economy continues to deteriorate: as quoted by the WSJ, Chen Zhenxing, sales manager with Zhejiang Lanxi Shanye Machinery Co., which produces hand carts and other logistics equipment in the eastern city of Jinhua, said his company faces ongoing problems raising capital and boosting prices: "competition is cutthroat,” he said. “Too many companies make products that are pretty much the same, so the focus turns to lowering prices."

Ultimately many will have to go out of business, leading to millions in layoffs, and forcing the Beijing politburo to face its greatest nightmare.

The problem with China's economy is that the local population, having tired of the stock market bubble, has now shifted its attention back to reflating the housing bubble, where as we reported recently there has been an unprecedented 50% surge in some Tier 1 cities such as Shenzen. As such the economy is focused not on creating new goods and services, but merely facilitating financialization and extracting rents.

This is why China's leaders have now put all their eggs in the housing market basket: Zhang Yiping, an economist with China Merchants Securities, said property investment and domestic consumption could be China’s major growth drivers this year given sluggish global demand and Beijing’s plans to cut industrial overcapacity.

Commerzbank’s Mr. Zhou and other economists expressed concern that investment is flowing into a few real-estate markets that show signs of overheating, rather than into new ventures. “Monetary policy is relaxed, but it’s reluctant to go to the real economy, only to property assets,” he said.

The slower pace of retail sales in January and February may reflect the turbulent financial markets and weak corporate profits last year, which dampened wage hikes and bonuses, economists said.

Even accounting for data volatility around the Lunar New Year holiday, China’s economy is off to a slow start this year following economic growth in 2015 of 6.9%, the slowest pace in 25 years. A host of stimulus measures late last year and into 2016—most recently a 0.5 percentage point cut in bank reserves late last month, have yet to reverse the slide in momentum.

The biggest problem, one which we have warned about since 2010, is that China remains mired under an unprecedented debt load, one which makes any forecast for 6.5% growth on the back of credit which is growing at double this pace, laughable.

Weekend Reading: The Bull/Bear Struggle Continues

March 11, 2016

by Lance Roberts

via RealInvestmentAdvice.com,

The standoff between the “bulls” and “bears” continued this week as prices struggled to rise. The “bulls” continue to “hope” that the recent turmoil that started at the beginning of this year has come to an end. The “bears” continue to point out silly things like an ongoing earnings recession, weakening economic data, and deteriorating technicals to make their case.

Silly “bears”.

Interestingly, on Thursday, the ECB launched its biggest “bazooka” yet pushing further into negative interest rates, increasing their already failed QE program and crossing every finger and toe for “good luck.” Via the ECB:

“At today’s meeting the Governing Council of the ECB took the following monetary policy decisions:

(1) The interest rate on the main refinancing operations of the Eurosystem will be decreased by 5 basis points to 0.00%, starting from the operation to be settled on 16 March 2016.

(2) The interest rate on the marginal lending facility will be decreased by 5 basis points to 0.25%, with effect from 16 March 2016.

(3) The interest rate on the deposit facility will be decreased by 10 basis points to -0.40%, with effect from 16 March 2016.

(4) The monthly purchases under the asset purchase programme will be expanded to €80 billion starting in April.

(5) Investment grade euro-denominated bonds issued by non-bank corporations established in the euro area will be included in the list of assets that are eligible for regular purchases.”

Question:

“What happens during the next global economic recession when these unsecured corporate bonds go bankrupt?”

If you remember, Lehman bonds were IG unsecured corporate bonds the DAY BEFORE they went into bankruptcy. That event sparked the global financial crisis. But this time will be different, right?

I’m only asking the question.

Anyway, I digress. This week’s reading list takes a look at various views on the market, the latest jobs report, oil prices and other interesting reads.

1) Do Any Of The Recent Rallies Pass The Sniff Test by Charles Hugh Smith via OfTwoMinds

“As Chris Martenson and many others have noted, “price discovery” is a joke now, as markets are either propped up by central bank “we got your back” guarantees or outright asset purchases, or driven up and down by speculative hot money flows.

This is not capitalism, or a functioning market: this is the end-game of legalized looting and financialization. What’s the value of real estate? If interest rates are pushed negative, then that gooses housing demand, as the cost of interest on a mortgage declines to near-zero in real terms.”

2) The Markets Are Stretched, So I’m “All-In” Short by Doug Kass via Real Clear Markets

“My recent column Not So Super Tuesday highlights why I believe markets are tipping over to short-term bearish, while my Top 10 Reasons to Sell Stocks Now piece incorporates most of my intermediate-term concerns.

That’s why I moved to “all-in short” on Friday during the market’s post-jobs-report ramp-up. I believe stocks’ recent rally from their mid-February low has stretched valuations and drastically altered the risk-vs.-reward ratio.

I‘d also note that Friday’s seemingly good February U.S. jobs report wasn’t quite as “clean” as the strong headline number of 242,000 non-farm job gains suggests. For instance, average wages dropped by 0.1%, while average hours worked fell by 0.2 — a decline usually seen in recessions. (Previous similar drops occurred in February 2010 and December 2013.)”

But Also Read: The Market Is Doing The Most Bullish Thing It Can Do by Kevin Marder via MarketWatch

And Read: Stocks Won’t Earn Nearly As Much Over Next 7-Years by Mark Hulbert via MarketWatch

Further Reading: The Perfect Storm Isn’t Over Yet by Mohamed El-Erian via Project Syndicate

3) The Wall Street Profits Illusion by Sam Ro via Yahoo Finance

“Wall Street gurus like Societe Generale’s Andrew Lapthorne, have been tracking the discrepancy between GAAP and non-GAAP reported profits for years.

But last fall, more experts like Deutsche Bank’s David Bianco grew increasingly concerned with what was becoming a growing divide between GAAP and non-GAAP profits.

‘Blended [non-GAAP] 4Q earnings per share is $29.49 with GAAP EPS of $19.92,’ Bianco said of S&P 500 profits on Monday. He further noted that this 67% ratio of GAAP to non-GAAP EPS is ‘well below the normal ~90% ex. recessions.'”

4) February Jobs Report A Little Misleading by John Crudele via New York Post

“Labor trumpeted that 242,000 new jobs were created in February, although wages declined 0.1 percent, the average workweek dropped by 0.2 hours and aggregate hours worked fell 0.4 percent. And part-time work soared in February while full-time job growth was mediocre.

Even the 242,000 job growth looked hokey. Retailing, for instance, saw an unbelievable (as in “not to be believed”) jump of 55,000 jobs despite the fact that February isn’t exactly the month when stores hire people to handle a swarm of shoppers.

As I said last Thursday and in a special Saturday column, the February job report was helped by rogue statistics — untrustworthy seasonal adjustments (especially in retailing) and giddy assumptions made by Labor that will probably have to be corrected later.“

Also Read: Wages – Shadow Hanging Over Jobs Market by Jeff Cox via CNBC

And Read: Does Jobs Report Point To Recession by Jared Pincin via Real Clear Policy

5) Oil Prices Should Fall, Possibly Hard by Art Berman via Forbes

“Oil prices should fall, possibly hard, in coming weeks. That is because fundamentals do not support the present price.

Prices should fall to around $30 once the empty nature of an OPEC-plus-Russia production freeze is understood. A return to the grim reality of over-supply and the weakness of the world economy could push prices well into the $20s.“

http://realinvestmentadvice.com/weekend-reading-the-bullbear-struggle-continues/

Why Crude Prices Are Heading For Another Deep Plunge

March 10, 2016

In this bipolar market, where only momentum, liquidity, technicals and short squeezes matter, as well as the occasional kneejerk reaction to a flashing red headline (usually some lie out of Venezuela or Nigeria about an imminent OPEC meeting which has not even been scheduled), one thing that no longer seems to have an impact on prices is actual news and fundamentals. So to help those who are blindly following the price of oil as an indicator of what is happening, here is a brief recap of the main news and research reports that should be impacting where oil trades today, but almost certainly won’t.

Among today’s key highlights compiled by Bloomberg we learn that JBC Energy doesn’t expect China to maintain record crude imports seen in Feb. as refinery maintenance, elevated storage impact. FGE says proposed producer accord to freeze output a “joke”, while Deutsche Bank says “fading oil demand may hamper price recovery.”

Here are the top stories via Bloomberg:

JBC Energy

China probably can’t maintain Feb.’s record crude imports amid refinery maintenance, storage capacity limitations

Feb. imports likely were boosted by “continued weakness in outright prices,” higher crude runs at teapot refineries

Facts Global Energy chairman Fereidun Fesharaki

Deal to cap crude output at record “a joke”; production freeze is “nonsense”

Libya can boost output to 1.2m b/d, taking prices down to $20/bbl

CNPC Chairman Wang Yilin

Current $30-40/bbl oil price not sustainable; $50-60 a “reasonable” range

Co. drafting development plans for long-term low oil price environment

Bloomberg story

Oil producers slow to add hedges as they wait for higher prices

As prices continue to rise, “we should see producer hedging accelerate,” says BNP Paribas head of commodity markets strategy Harry Tchilinguirian

Eurasia Group global energy, natural resources director Bruno Stanziale

Oil at $50 will bring U.S. producers back to mkt

Oil prices to see “gradual” rise to around $40/bbl by yr-end, avg. $50/bbl in 2017; price “volatility will dry up”

Institute for Energy Research

U.S. shale oil boom makes renewable fuels standard obsolete, helped to reduce dependence on imports

JBC Energy

European gasoline cracks to see further upside in coming wks on higher U.S. consumer demand

Increased gasoline imports by Nigeria may be supporting Mediterranean market

Deutsche Bank report

Fading Chinese oil demand may hamper price recovery

Chinese fuel consumption “may begin to flatten more quickly than some long-term projections indicate.” This could reduce global oil demand growth to 800k b/d by 2024, compared w/ 1.1m b/d from 2000-2016

ESAI report

Libyan production will not recover as “the ongoing civil war and the rise of ISIS in Libya will carry on for years”: Boston-based consultant

* * *

And now back to your liquidity/squeeze driven melt up/down.

http://www.zerohedge.com/news/2016-03-09/output-freeze-joke-china-demand-fall-and-other-news-should-be-moving-oil

Amend, Extend, Pretend—-How Bankers Will Intensify The Global Deflation

by SHTFPlan.com • March 8, 2016

In 2011, as gold prices rocketed to $1900 and oil was trading above $120 a barrel, there were few analysts who saw anything but further gains. But Marin Katusa ofKatusa Research had a different opinion. At a major commodity conference Katusa, to boos and jeers from the audience, held strong to his analysis that an imminent deflationary collapse in commodity prices was on the horizon. And collapse they did.

According to Katusa, who is closely involved in the Canadian resource sector, most people simply assumed the good times would go on forever… because it was different this time. But like any uninhibited party fueled by unlimited cash, the hangover was sure to follow.

There’s no doubt you had massive high paying jobs. In Canada, the province that benefited the most is Alberta… In the last twelve months they’ve had 70,000 layoffs of jobs paying over a hundred grand a year.

…when I’d go to these oil towns you’d sit down at the casinos with them and these guys were all about the hookers and blow… they were all about their toys… big fancy trucks… snow mobiles… and they’re in the field for two weeks and they make $20,000 and blow it all at the casinos.

You knew it couldn’t last.

As Katusa notes in his latest interview with Future Money Trends, though the crash has been brutal for the sector, it’s not over yet and it’s going lower for longer.

They [OPEC] can survive at $20 oil…

For two years everyone’s been saying, “OPEC’s going to cut back.”

They reality here is, why would OPEC cut production? That would only prop up the Russians and the shale sector.

And while most will argue that low oil prices will wipe out most of America’s shale industry, Katusa has a contrarian view, suggesting that shale sector debt, while significant, is not necessarily going to cause these companies to go under in the immediate future.

Why?

Because what banker in their right mind wants to get dirty and actually operate an oil field?

So the debt will be amended, extended and then they’ll pretend.

… Because you can’t just shut down an oil field. You have to reclaim those wells, which means you have to shut them down and environmentally reclaim them… and it costs more to do that today than what the actual value is.

The bankers know that.

… With innovation, in the Western world, costs will decrease and the bankers have no choice but to amend, extend and pretend the debt.

So they’re going to go lower for longer.

In short, going forward we should expect widespread manipulation from the producers and the banks themselves to keep the bankruptcies at bay.

But recession still looms, and Katusa says that there are two things we can count on in the near future and why people need to rethink their investments:

The economy is changing… In a zero-interest rate policy world people have to rethink their investments… You’re looking at higher volatility, lower returns, but much higher risk.

With all this going on in the world there are only two things that can happen.

We continue with negative interest rates, which I see the trend globally… 35% of Eurozone countries already have negative interest policies…

And there’s going to be quantitative easing for the people… QE4-P… and that’s the reality here.

Negative interest rates are a tax on wealth… a tax on savers.

And if you haven’t already guessed, amid all the volatility and debasement of currencies, one asset class, according to Katusa, will survive and counter the coming helicopter drop of freshly printed dollars:

There’s a great way to make money on this if you get ahead of QE4P… the quantitative easing for the people… and gold is one of the ways to do that.

In his must-see interview, Katusa expands on this forecast by noting that, on top of all the bailouts, trade tariffs, and quantitative easing to follow, China, in an effort to maintain the perception of stability in their economy and financial markets, will soon begin flooding the global economy with commodities like aluminum, steel, iron ore and coal, which will continue to have a deflationary impact on broader commodity markets.

But the one sector they can’t flood – precious metals – is the very sector investors should be looking at as a way to not only preserve wealth going forward, but to grow it exponentially as crisis continues to hammer the global marketplace. That’s why Katusa has disclosed he is writing million dollar checks to one specific gold acquisition company, in similar fashion to other noteworthy insiders who are moving heavily into gold including Doug Casey, Eric Sprott, George Soros, Stanley Druckenmiller and Carl Icahn.

http://davidstockmanscontracorner.com/amend-extend-pretend-how-bankers-will-intensify-the-global-deflation/

Deflation Is Coming To The Auto Industry As Used Car Prices Drop, Off-Lease Deluge Looms

03/08/2016

Last week, we learned that vehicle leasing as a percentage of monthly light-vehicle sales hit a record in February at 32.3%.

In other words, a third of the over 1 million cars and light trucks “sold” during the month were leases, according to J.D. Power.

This is indicative of what is now a long-term trend. Have a look at the following chart from WSJ, which shows that since 2009, the share of monthly auto leases as a percentage of vehicle sales well more than tripled:

Of course the thing about leased vehicles is that they come back, and as WSJ wrote last week, “about 3.1 million vehicles will return to dealer lots off leases this year, up 20% from 2015 [and] the number will climb to 3.6 million in 2017 and 4 million in 2018.”

So what does that mean for dealers? Deflation.

And what does that mean for the automakers? Hefty losses.

Nothing about this is hard to understand. You get a supply glut causing pricing assumptions for your existing inventory to prove wildly optimistic and you end up with giant writedowns.

This has happened before. "The auto industry expanded the use of leasing in the mid-1990s, helping to fuel retail sales of new vehicles," WSJ recounts. "Eventually, a glut of off-lease cars sent resale values down and auto lenders who had bet residuals would remain high ended up racking up billions of dollars in losses, having to sell the cars for much less than they anticipated."

Right. Nothing difficult to grasp about that. But the especially silly thing about the dynamic with auto leases is that it was the dealers and the automaker-affiliated financing companies that made the leases in the first place. In other words, it's not like this was some supply shock that couldn't have been forecast ahead of time. In fact, they knew exactly when the off-lease deluge would start, so it's not entirely clear why they would have set optimistic residual assumptions.

Anyway, the cracks are already starting to show.

The Manheim Used Vehicle Value Index posted its largest Y/Y decline in over two years last month, falling -1.4% and -1.5% M/M. We're now 3.5% below the peak.

"All else equal, it puts pressure on lease residuals - though we note most fincos had assumed declining used vehicle prices in their lease writing," Goldman said, earlier today. "Second, while improving inventory acquisition cost for the dealers, it may put downward pressure on the value of existing dealer inventories, which can be negative for used margins."

Well yes, declining used vehicle prices "may" be a "negative for used margins" - in fact that's almost a tautology.

And of course falling used car prices means pressure on new car prices as well, which would be a shock to America's booming auto market.

Obviously, the scariest part about all of the above is that consumers still have the pedal to the metal (pun fully intended) when it comes to leases, which means there's no end in sight to the off-leases and thus no way to determine, at this juncture, how big the residual writedown wave and deflationary auto industry calamity will ultimately end up being.

So, you know... "buckle up."

* * *

Bonus chart: largest used car price decline for any February since 2008

http://www.zerohedge.com/news/2016-03-08/deflation-coming-auto-industry-used-car-prices-drop-lease-deluge-looms

The Oil Short Squeeze Explained: Why Banks Are Aggressively Propping Up Energy Stocks

March 8, 2016

Last week, during the peak of the commodity short squeeze, we pointed out how this default cycle is shaping up to be vastly different from previous one: recovery rates for both secured and unsecured debts are at record low levels.

More importantly, we noted how this notable variance is impacting lender behavior, explaining that banks - aware that the next leg lower in commodities is imminent - are not only forcing the squeeze in the most trashed stocks (by pulling borrow) but are doing everything in their power to "assist" energy companies to sell equity, and "persuade management" to use the proceeds to take out as much of the banks' balance sheet exposure as possible, so that when the default tsunami finally arrives, banks will be far, far, away from the carnage.

All of this was predicated on prior lender conversations with the Dallas Fed and the OCC, discussions which the Dallas Fed vocally denied and accused us of lying, yet which the WSJ confirmed, showing that it was the Dallas Fed who was lying.

This was our punchline:

[Record low] recovery rate explain what we discussed earlier, namely the desire of banks to force an equity short squeeze in energy stocks, so these distressed names are able to issue equity with which to repay secured loans to banks who are scrambling to get out of the capital structure of distressed E&P names. Or as MatlinPatterson's Michael Lipsky put it: "we always assume that secured lenders would roll into the bankruptcy become the DIP lenders, emerge from bankruptcy as the new secured debt of the company. But they don't want to be there, so you are buying the debt behind them and you could find yourself in a situation where you could lose 100% of your money."

And so, one by one the pieces of the puzzle fall into place: banks, well aware that they are facing paltry recoveries in bankruptcy on their secured exposure (and unsecured creditors looking at 10 cents on the dollar), have engineered an oil short squeeze via oil ETFs...

... to push oil prices higher, to unleash the current record equity follow-on offering spree...

... to take advantage of panicked investors some of whom are desperate to cover their shorts, and others who are just as desperate to buy the new equity issued. Those proceeds, however, will not go to organic growth or even to shore liquidity but straight to the bank to refi loan facilities and let banks, currently on the hook, leave silently by the back door. Meanwhile, the new investors have no security claims and zero liens, are at the very bottom of the capital structure, and face near certain wipe outs.

In short, once the current short squeeze is over, expect everyone to start paying far more attention to recovery rates and the true value of "fundamentals."

Going back to what Lipsky said, "the banks do not want to be there." So where do they want to be? As far away as possible from the shale carnage when it does hit.

Today, courtesy of The New York Shock Exchange, we present just the case study demonstrating how this takes place in the real world. Here the story of troubled energy company "Lower oil prices for longer" Weatherford, its secured lender JPM, the incestuous relationship between the two, and how the latter can't wait to get as far from the former as possible, in...

"Why Would JP Morgan Raise Equity For An Insolvent Company"

I am on record saying that Weatherford International is so highly-leveraged that it needs equity to stay afloat. With debt/EBITDA at 8x and $1 billion in principal payments coming due over the next year, the oilfield services giant is in dire straits. Weatherford has been in talks with JP Morgan Chase to re-negotiate its revolving credit facility -- the only thing keeping the company afloat. However, in a move that shocked the financial markets, JP Morgan led an equity offering that raised $565 million for Weatherford. Based on liquidation value Weatherford is insolvent. The question remains, why would JP Morgan risk its reputation by selling shares in an insolvent company?

According to the prospectus, at Q4 2015 Weatherford had cash of $467 million debt of $7.5 billion. It debt was broken down as follows: revolving credit facility ($967 million), [ii] other short-term loans ($214 million), [iii] current portion of long-term debt of $401 million and [iv] long-term debt of $5.9 billion. JP Morgan is head of a banking syndicate that has the revolving credit facility.

Even in an optimistic scenario I estimate Weatherford's liquidation value is about $6.7 billion less than its stated book value. The lion's share of the mark-downs are related to inventory ($1.1B), PP&E ($1.9B), intangibles and non-current assets ($3.5B). The write-offs would reduce Weatherford's stated book value of $4.4 billion to - $2.2 billion. After the equity offering the liquidation value would rise to -$1.6 billion.

JP Morgan and Morgan Stanley also happen to be lead underwriters on the equity offering. The proceeds from the offering are expected to be used to repay the revolving credit facility.

In effect, JP Morgan is raising equity in a company with questionable prospects and using the funds to repay debt the company owes JP Morgan. The arrangement allows JP Morgan to get its money out prior to lenders subordinated to it get their $401 million payment. That's smart in a way. What's the point of having a priority position if you can't use that leverage to get cashed out first before the ship sinks? The rub is that it might represent a conflict of interest and [ii] would JP Morgan think it would be a good idea to hawk shares in an insolvent company if said insolvent company didn't owe JP Morgan money?

The answer? JP Morgan doesn't care how it looks; JP Morgan wants out and is happy to do it while algos and momentum chasing daytraders are bidding up the stock because this time oil has finally bottomed... we promise.

So here's the good news: as a result of this coordinated lender collusion to prop up the energy sector long enough for the affected companies to sell equity and repay secured debt, the squeeze may last a while; as for the bad news: the only reason the squeeze is taking place is because banks are looking to get as far from the shale patch and the companies on it, as possible.

We leave it up to readers to decide which "news" is more relevant to their investing strategy.

Is This Whole Rally Just One Big TRAP?

by Phoenix Capital Research

03/07/2016

I don’t trust this rally.

Few analysts realize that the sharpest, most aggressive rallies occur during bear markets. The reason for this is that during bear markets, investors tend to go short (borrow shares to bet on a collapse).

So when the market rallies even a little bit, it often will go absolutely vertical as these individuals panic and cover their shorts (which increases the buying).

Consider the Tech Bubble. When it burst, we had THREE monster rallies of 17%, 33% and 16% in just SIX months time!

Anyone who bought into these moves for the long-term ended up get crushed as the market soon rolled over and worked its way down. The below chart gives some perspective on just how much further stocks would fall relative to these traps.

Smart investors, however, used those rallies to prep for the next round of the drop. They didn’t get suckered into believing that it was the beginning of the next bull market.

http://www.zerohedge.com/news/2016-03-07/whole-rally-just-one-big-trap

China Is About To Unleash A Monster Housing Bubble, In Six Easy Steps

March 7, 2016

One week ago we showed the disturbing degree to which the latest (and greatest) housing bubble among China's Tier 1 has gripped the broader public, when we reported that local speculators are waiting in line for days to flip homes.

Visually, it looks as follows - the bubble is entirely in the Tier 1 cities; for now everyone has given up on the other regions which are suffering greatly as a result of the bursting of the commodity bubble and have seen an exodus of recently unemployed workers:

The demand for housing in Shanghai and Shenzen has gotten so "bubbly" that even the government-run news agency Xinhua on Wednesday warned of increasing leverage risks and called for further tightening measures to rein in the market. Which is ironic, because just days later the People's Congress announced it would support the Chinese housing market, sending conflicting messages of whether it does or does not want another housing bubble.

And while we know that retail speculators are simply feeder-fish piggybacking on the latest housing craze, it is the people with far more capital - and leverage - who are ultimately pulling the strings, as an article in the local media explains in detail.

In an article written on Caijing, we get to the bottom of the rapid rise in housing prices in Shenzhen and other Tier I cities. As it notes, the property boom is ominous, and ultimately hints of even more capital outflow and currency devaluation to come.

The gist of the article (in Chinese) is that the business owners, foreign factory bosses and other powerful people are the cause of the meteoric housing price rise. Here is the link. Some of the other highlights:

The typical housing transaction in this latest housing bubble looks as follows:

1. The business owner creates a fake employment contract with his maid or driver, showing an impressive income to justify a high monthly mortgage.

2. The owner sells his property to his maid/driver at the highest price possible (as much as the bank will appraise for). Maid/driver doesn't care about what the price is and accepts the asking

3. The owner gives his maid the money for the down payment of 30% (lowered recently as PBOC policy), while receiving the the full or above full value of the property

4. Maid/driver moves into the upscale property of the owner, which is why mainstream media is characterizing the boom as 'upgrade buys'. And continue to live there until the actual owners decide to stop outlaying for the mortgage payment.

5. The owner cashes out of the property basically with PBOC's help (ease of credit, lowered down payment etc), promptly moves the money out of China through import/export channels, contributing to capital outflows.

6. At some point in the future, the owners will stop making mortgage payment, since they've already cashed out of the property with a huge windfall. Bank goes to foreclose; maid/driver will go back to living where they lived before.

In Shenzhen, housing debt as percentage of total debt is 22.4%, 1.7X Shanghai and 2.25X Beijing.

But what's more worrisome is that since this trick can be applied basically anywhere in China, it will be and the elite in Shanghai and Beijing will catch on as will tier 2-4 cities, whose governments are even more desperate to rescue the housing market.

With the elite and smart money milking the existing banking system in this way and moving money out, China's 3.2 Trillion (and declining for 4 consecutive months) official reserves doesn't look all that impressive.

The Last Time The Market Was So Overbought, This Happened

March 3, 2016

The last 3 weeks have been a near unprecedented rip higher in stocks... as markets anticipated G-20 cooperative actions (and then BoJ and ECB follow-through) creating a vicious short-squeeze bounce...

This has sent The McClellan Oscillator to its most overbought since January 2009...

What happened then?

The Group of 20 leaders from major developed and emerging economies had pledged on their meeting on Saturday short-term measures such as fiscal stimulus in order to try to keep the global economy from falling into a deep slump and promised to look at ways to tighten regulations to prevent future crisis.

That did not end well!

"The Bounce Has Run Its Course" Bob 'The Bear' Janjuah Warns S&P Heading To 1700s

March 5, 2016

Nomura's Bob Janjuah warend in January that "the bubble implosion can't be fixed this time," and, as he explains in his latest note, he is pleased with all six of his key forecasts for 2016...

In particular on Commodities, with his expectation that crude would trade below $30 (the price per barrel fell from $37 in early January to a low so far of $26 in February).

And on Rates, the 30yr UST yield fell from 2.95% in early January to a low so far of 2.49% in February, below his 2.5% target for 2016, and the 10yr UST yield fell from 2.2% in early January to a low so far of 1.66% in February, in line with his expectation over 2016 of a move in yields down from 2% towards 1.5%.

The reasons for his latest note are:

1. To reiterate my bearish views on risk assets for H1 2016 – I continue to see much lower equity prices, lower core bond yields, wider credit spreads, and weakness in EM and commodities over the next four months (at least). In January I said that the S&P500 would fall from 2000/2050 to the 1500s as my target over 2016. I reaffirm this view. I note with interest that at the global equity market ”lows” so far in 2016, seen earlier in February, virtually all major global stock markets were in official bear market territory. For example, the Eurostoxx 50 fell over 30% from its 2015 high to its (so far) 2016 low. The MSCI World fell 20% from its 2015 high to its (so far) 2016 low. The key exception to this move into official bear market territory has been the major US indices, but I expect this to correct itself over the next four months or so.

2. To highlight that, in my view, stocks’ countertrend bounce off the February lows has now run its course and I believe we are – in early March – likely to see the onset of the next leg weaker in risk, vs stronger in core duration. I expect this next leg of weakness to last three to five weeks and to result in new lows so far in this cycle in stocks (S&P500 into the 1700s) and new lows in core government bond yields (target 1.5% in 10yr USTs). It is important to remember that in bear markets the strength is to the downside, the violence is to the upside, with countertrend rallies in bear markets often being the most painful. Markets simply do not go down (or up) in straight lines. But if I am right that this bounce is over, we should continue to see a series of lower lows and lower highs in stocks around the globe.

To protect against being wrong, particularly with respect to timing, it is prudent to put in place a stop loss, triggered if/when we see a consecutive weekly close in the cash S&P500 index above 2040.

3. To admit that even I am a little surprised by the desperation already evident among central bankers. As per my January note, I expected the BOJ to ease in Q1, but going straight to negative rates has seriously harmed the BOJ’s credibility and the credibility of Abenomics. ECB QQE has clearly failed to create the inflation Mario Draghi promised us, but I have no doubt the ECB will ease again this month. And even the Fed is now “drip-feeding” negative rates into the market through its usual channels. The Fed has made a major policy error already, and I remain convinced that the Fed will be easing by the end of the year. But I would not be surprised if Fed hubris “forces” it to tighten once more before end-June. Focusing so much on an extremely lagging and “technically created” number like the unemployment rate is at the root of this policy error. The Fed is simply not focusing enough on important issues like weak earnings, poor quality jobs, imported deflation, weakness in investment spending, weakness in corporate revenue and profit (not EPS) growth, and deeply scarred consumer behaviour. I could go on, but suffice it to say that I think the Fed has backed itself into a corner, and will only be able to free itself to get ahead of the curve (rather than as it is now, way behind the curve) once the data and markets truly hit some form of capitulation bottom. As I have written in the past, I don’t see a “Fed put” until the S&P500 trades down into the 1500s.

4. To stress that central bank credibility is draining fast and, assuming that the BOJ and ECB go again this month, I now see a risk of a breakdown in markets and outcomes that are the opposite of what central bankers are trying – and have been failing for over seven years now – to achieve, i.e. nominal GDP at 5%, EVEN IF THIS 5% CONSISTS OF 0% REAL AND ALL 5% FROM INFLATION. We are entering an extremely worrying time and we have got here even faster that I had feared – a place where monetary policy and central banks become the problem and not the cure. As discussed above, the Fed is in a hole of its own making by using self-serving metrics to fix a debt and asset bubble crisis with a policy that relies on more debt and even bigger asset bubbles. But in the short term – this next month – I am concerned that markets will react badly and contrary to policymaker expectations when both the BOJ and the ECB attempt to ease further this month. I suspect the ECB and the BOJ are – as far as markets are concerned – “damned if they do, and damned if they don’t” with any residual credibility likely to decay away this month. But both institutions should realise this is down to their own mistakes, whereby (like the Fed) they have sought to fix the ills of excessive debt, asset bubbles and a lack of competitiveness thorough policies which merely result in a zero-sum outcomes (FX wars) and/or which rely on the “greater fool” theory requiring “someone” to take on more debt to continually speculate on an un-burstable asset price bubble. Sadly, of course, mankind has so far failed to create un-burstable bubbles, especially where the underlying foundations are so flimsy. This competitiveness issue is global and critical. Since the global financial crisis (GFC) very little production capacity reduction has been allowed to occur in the DMs (courtesy of QE and ZIRP, which together facilitate the avoidance of default cycles, which are central to reducing capacity). At the same time, globally, particularly in places like China and in industries like Energy and Shipping, we have seen significant production capacity added since the GFC. Again, in part due to QE and ZIRP policies in DMs. Of course, this would be less of a problem if global aggregate demand growth had increased strongly over the last seven years, but this has clearly not happened. In particular, the debt-driven consumption frenzy of the years leading up to the GFC in the DMs has barely come back, while at the same time demand growth in the EM sphere has been much slower than hoped for (and needed), and latterly severe economic downturns in places like Russia, China, the Middle East and Brazil have hampered this handover even more. So the response to all of this has been the zero-sum game referred to above, FX wars, which merely operate to allow temporary and transitory relative shifts in competitiveness but with severe (unintended?) consequences.