News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Economics Professor: Negative Interest Rates Aimed at Driving Small Banks Out of Business and Eliminating Cash

GeorgeWashington.com

Feb. 9, 2016

More than one-fifth of the world’s total GDP is in countries which have imposed negative interest rates, including Japan, the EU, Denmark, Switzerland and Sweden.

Negative interest rates are spreading worldwide.

And yet negative interest rates – supposed to help economies recover – haven’t prevented Japan and Europe’s economies from absolutely going down the drain.

Nor have they even stimulated spending. As ValueWalk points out:

Japan has had ultra-low rates for years and its economy has been terrible. Trillions of debt in Europe now trades at negative interest rates and its economy isn’t exactly booming. Denmark, Sweden and Switzerland all have negative interest rates, but consumer spending isn’t going up there. In fact, savings rates have been going up in lockstep with the decrease in interest rates, exactly the opposite of what the geniuses at the various central banks expected.

Why is this happening? Simply, savers are scared. Lower interest rates have wrecked their retirement plans. Say you were doing some financial planning 10 years ago and plugged in 3% from your savings account. Now its 0%. You still have to plan for your retirement. Plug in 0%. What happens to your planning now? 0% compounded for X years is 0%. The math is simple. So in order to have your target savings at retirement, you need to save more, not spend more. But for some reason, the economists that run central banks around the world can’t see this. They are all stuck in their offices talking to one another and self-reinforcing this myth that they can drive spending up by reducing the rate of return on investments. Want to see consumer spending go up? Don’t wreck their savings plans so that they are too scared to spend. But that’s too simple. Instead, central banks use a chain of causation that doesn’t exist to try to create change 3 or 4 steps down the line. It hasn’t worked, and it won’t work. It isn’t in an individual’s self-interest to go out and spend their money on more “stuff” in order to spur economic growth.

So what’s really going on? Why are central banks worldwide pushing negative interest rates?

Economics professor Richard Werner – the creator of quantitative easing – notes:

The experience of Switzerland [shows that] negative rates raise banks’ costs of doing business. The banks respond by passing on this cost to their customers. Due to the already zero deposit rates, this means banks will raise their lending rates. As they did in Switzerland. In other words, reducing interest rates into negative territory will raise borrowing costs!

If this is the result, why do central banks not simply raise interest rates? This would achieve the same result, one might think. However, there is a crucial difference: raised rates will allow banks to widen their interest margin and make their business more profitable. With negative rates, banks’ margins will stay low and the financial situation of the banks will stay precarious and indeed become ever more precarious.

As readers know, we have been arguing that the ECB has been waging war on the ‘good’ banks in the eurozone, the several thousand small community banks, mainly in Germany, which are operated not for profit, but for co-operative members or the public good (such as the Sparkassen public savings banks or the Volksbank people’s banks). The ECB and the EU have significantly increased regulatory reporting burdens, thus personnel costs, so that many community banks are forced to merge, while having to close down many branches. This has been coupled with the ECB’s policy of flattening the yield curve (lowering short rates and also pushing down long rates via so-called ‘quantitative easing’). As a result banks that mainly engage in traditional banking, i.e. lending to firms for investment, have come under major pressure, while this type of ‘QE’ has produced profits for those large financial institutions engaged mainly in financial speculation and its funding.

The policy of negative interest rates is thus consistent with the agenda to drive small banks out of business and consolidate banking sectors in industrialised countries, increasing concentration and control in the banking sector.

It also serves to provide a (false) further justification for abolishing cash. And this fits into the Bank of England’s surprising recent discovery that the money supply is created by banks through their action of granting loans: by supporting monetary reformers, the Bank of England may further increase its own power and accelerate the drive to concentrate the banking system if bank credit creation was abolished and there was only one true bank left – the Bank of England. This would not only get us back to the old monopoly situation imposed in 1694 when the Bank of England was founded as a for-profit enterprise by private profiteers. It would also further the project to increase control over and monitoring of the population: with both cash and bank credit alternatives abolished, all transactions, money creation and allocation would be implemented by the Bank of England.

If this sounds like a “conspiracy theory”, the Financial Times argued in 2014 that central banks would be the real winners from a cashless society:

Central bankers, after all, have had an explicit interest in introducing e-money from the moment the global financial crisis began…

***

The introduction of a cashless society empowers central banks greatly. A cashless society, after all, not only makes things like negative interest rates possible, it transfers absolute control of the money supply to the central bank, mostly by turning it into a universal banker that competes directly with private banks for public deposits. All digital deposits become base money.

http://www.zerohedge.com/blogs/george-washington

Real Estate in Real Terms

Armstrong Economics

Feb 20, 2016

INQUIRY:

Dear Marty,

When talking about negative interest rates and a shift of cash from banks to the stock market from 2017, would that not mean that cash may also shift to property and other assets? Yet I thought that we have seen the high in the property market already?

ANSWER:

Real estate has peaked in REAL TERMS. The sub-prime market that made the high in 2007 was not exceeded. The secondary rally into 2015 was the high-end, so we now have the IRS targeting NYC and Miami in their hunt for money.

The high-end will now decline. The average home will make the transition, but will not be making new highs. In real terms, the high is in. Real estate varies tremendously based upon location. This is due to capital inflows that drive certain markets like Vancouver and Toronto in Canada or New York and Miami in the States. Washington, D.C., held up in 2007-2009 because politicians did not want to lose their jobs. Taxes will also prevent real estate from reaching new highs in “real terms.”

In nominal terms, some areas will make the transition to new currencies; the movable assets will appreciate the most. Those are the assets that you do not have make annual payments on to hold them annually.

We also have a collapse in long-term interest rates to the point that banks do not want to write 30-year mortgages anymore. As that long-term view collapses, so does the leverage. That will cause housing to decline in “real terms.”

https://www.armstrongeconomics.com/markets-by-sector/real_estate/real-estate-in-real-terms/

The US Economy's Problem Summed Up In 1 Simple Chart

02/09/2016

Too much mal-invested, Fed-fueled, hope-driven "if we build it, they will buy it" inventory... and not enough actual demand. This has never, ever, ended well in the past - so why is this time different?

At 1.32x, the December inventories/sales ratio is drasticallyhigher than at year-end 2014 and is back at levels that have always coincided with recessions...

And just in case you needed more convincing that all is not well - the current spread between sales and inventories is now at a record absolute high...

As Sales tumble and inventories continue to rise...

And all because The Fed (ZIRP) and Government (Subsidies) are breathing life into Zombies when they should be dead and gone.

http://www.zerohedge.com/news/2016-02-09/us-economys-problem-summed-1-simple-chart

US Investment Grade Credit Risk Spikes To 5-Year Highs

02/09/2016

When it rains it pours...

The market has taken over The Fed's role - forget above 25bps here or there, the cost of funding for even the highest quality US Corporates is exploding...

Simply put, the credit cycle has turned and is accelerating rapidly - crushing any hopes for debt-funded shareholder-friendliness.

http://www.zerohedge.com/news/2016-02-09/us-investment-grade-credit-risk-spikes-5-year-highs

Deutsche Bank Stock Crashes To Record Low

zerohedge.com

02/09/2016

enough said,....

A Key Technical Indicator Just Rang The Bell On The Cyclical Bull Market

by ZeroHedge

February 5, 2016

While the primary topic of Albert Edwards’ most recent note is the question how long China can sustain its FX intervention before tapping out and letting the hedge funds win with their short Yuan bets once total reserves drop below the critical redline of $2.7 trillion (the answer incidentally is between 5 months and 10 months assuming monthly reserve burn rates of $130BN to $60BN), we will skip that part as we have discussed it extensively in the past, and instead will fast forward to some chart porn by the SocGenarian.

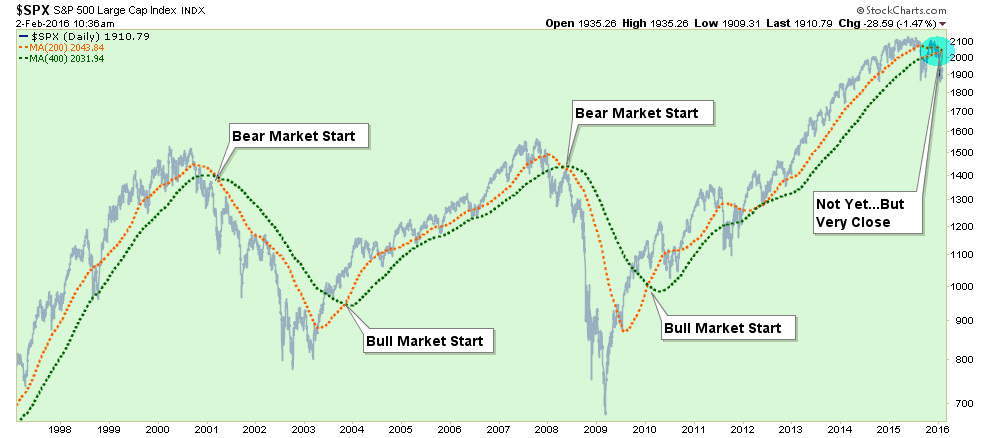

Here is Albert Edwards showing that the S&P had breached key moving averages normally seen at the start of a bear market.

Back in the mid-1990s I spent three memorable years working at Bank America Investment Management, among some of the industry’s finest. Having previously spent three years as an economist at the Bank of England, I was new to markets and I let my economic enthusiasm often get the better of me when making recommendations to fund managers.

I remember the head of fixed income explaining to me it was far better not to try and pick market tops or bottoms but to wait and observe the market turn, making the trade late rather than prematurely trying to pick the bottom or top.

So the chart below is notable, showing that key 200d and 320d moving averages for the S&P have just been breached to the downside. If one is looking for key technical indicators to ring the bell on the cyclical bull market- maybe it has just rung loud and clear.

A renminbi devaluation will only sever an already badly frayed safety rope.

http://www.zerohedge.com/news/2016-02-05/key-technical-indicator-just-rang-bell-cyclical-bull-market

Something This Way Wicked Comes—–A Deep Dive Into The Market Charts

by Lance Roberts

February 6, 2016

Last week, I discussed the boost the market received as the BOJ made an unexpected move into negative interest rate territory combined with end of the month buying by portfolio managers. To wit:

“However, the announcement by the Bank of Japan (BOJ) to implement negative interest rates in a desperate last attempt to boost economic growth in Japan was only the catalyst that ignited the bulls. The “fuel” for the buying came from the end of the month portfolio buying by fund managers.”

But more importantly, was the push higher by stocks that I have been discussing with you over the last couple of weeks. To wit:

“Over the last few weeks, I have suggested the markets would likely provide a reflexive rally to allow investors to reduce equity risk in portfolios. This was due to the oversold condition that previously existed which would provide the “fuel” for a reflexive rally to sell into.

I traced out the potential for such a reflexive rally two weeks ago as shown in the chart below.”

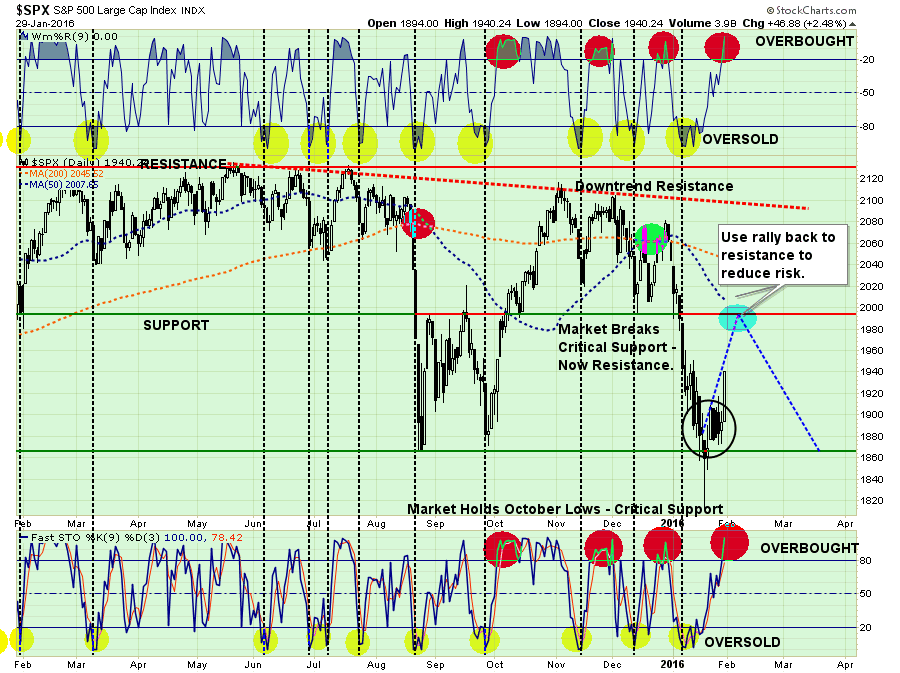

Previous Chart

As I stated then, the most important parts of the chart above are the overbought / oversold indicators at the top and bottom. The oversold condition that once existed has been completely exhausted due to the gyrations in the markets over the last couple of weeks. This leaves little ability for a significant rally from this point which makes a push above overhead resistance unlikely.

“Just as an oversold condition provides the necessary “fuel” for an advance, the opposite is also true.”

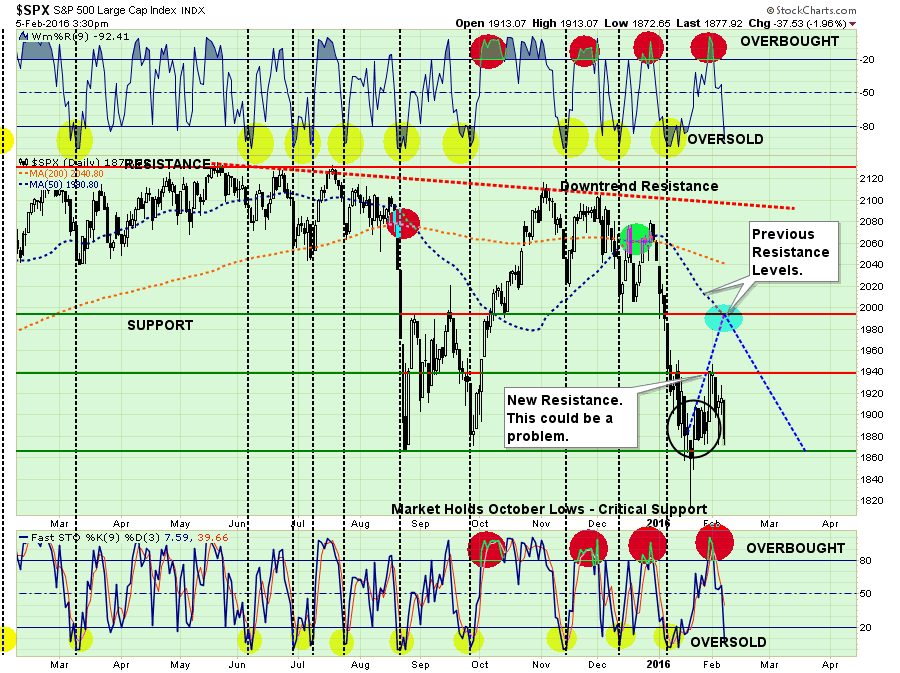

Here is the problem. I have updated the chart above through Friday’s close.

The rally failed at the previous reflex rally attempt during the late December/January plunge. This failure now cements that high point as resistance. Furthermore, the market continues to fail almost immediately when overbought conditions are met (red circles), which suggests that internals remain extraordinarily weak.

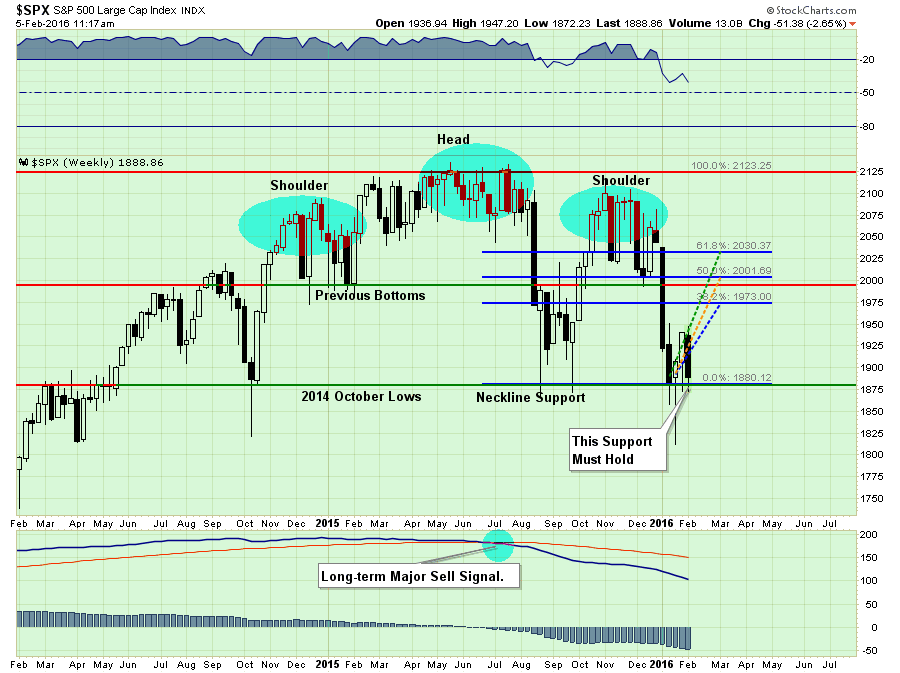

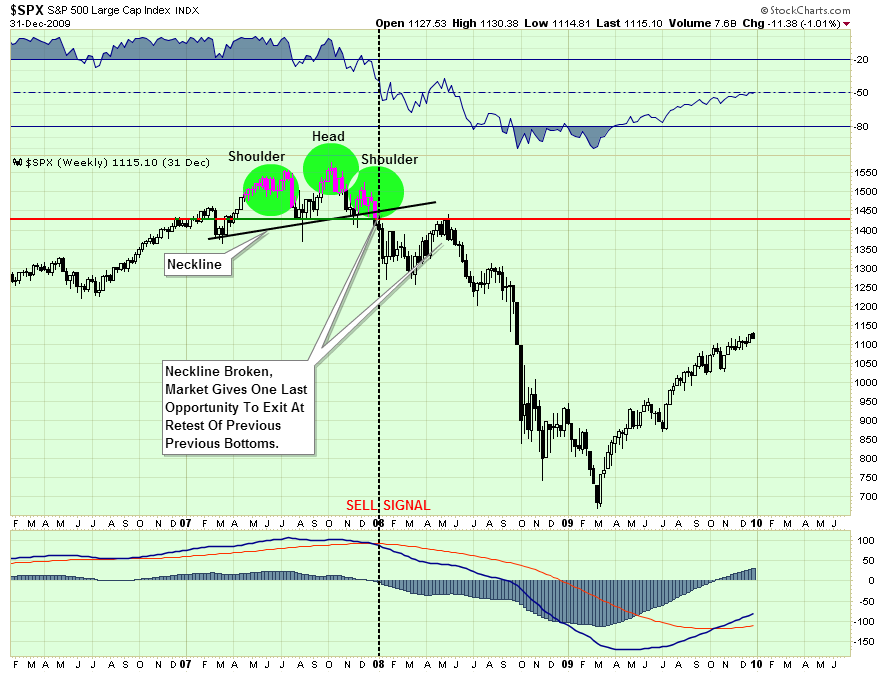

HEAD & SHOULDERS – NOT JUST DANDRUFF

The good news, if you want to call it that, is that the market is currently holding above the recent lows as short-term oversold conditions once again approach. It is critically important that the market holds above that support, which is also the neckline of the current “head and shoulders” formation, as a break would lead to a more substantive decline.

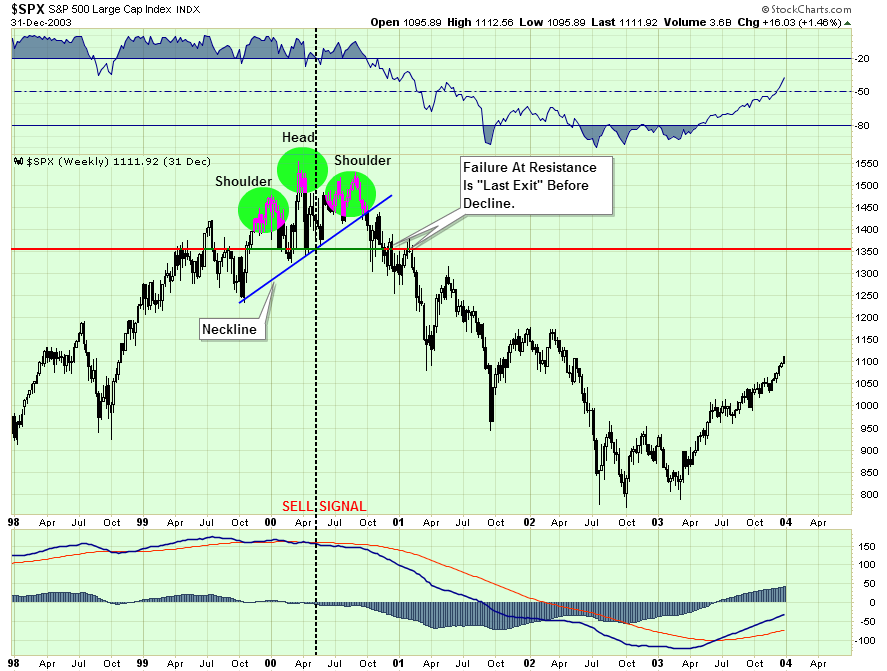

However, this isn’t the first time that we have seen a “head and shoulders” topping pattern form COMBINED with a long-term major sell signal as shown above. I emphasize this point because many short-term technicians point out “head and shoulders” formations that consistently do not lead to more important declines. However, when this topping process combines with enough deterioration in the markets to issue long-term “sell signals,” it is something worth paying attention to.

The first chart shows the same development in 2000.

And again in 2007.

These are the only two points since the turn of the century where a topping process was combined with a long-term sell signal.

It is important to note that in both previous cases the markets did provide one last chance to exit before a more substantiative decline ensued. This is because by the time the market has declined enough to break the neckline, sellers have been temporarily exhausted. This allows the market to rise enough to test previous resistance where “sellers” once again emerge.

It is very likely that if, or when, the market breaks current neckline support, individuals will be given one last chance to exit the markets for safer ground. A failure to do so has previously been the start of the “trail of tears.”

PREDICTING OR PAYING ATTENTION?

Last night I gave a presentation to a group of doctors discussing the economy, the markets and what is most likely to come over the next few months.

One of the questions I was asked during the Q&A section was:

“How can you be so sure that you are right? No one can time the market?”

It is an interesting question, and one that I have been asked before. If you scroll down to the bottom of this report you will see a chart of the S&P 500 with the history of portfolio adjustments over time. You could call this timing, however, I prefer to call this risk management.

For me, “timing the market” is trying to be “all in” or “all out.” If you try and do that playing poker you are eventually going to go broke.

However, a good poker player understands the “risk of losing” given the particular hand that he is dealt. He will bet much heavier given a “full house” versus a “pair of deuces.” However, even given a great hand, a good poker player reads the other players at the table and adjusts his bets accordingly.

The same is true when it comes to managing your portfolio. While you may have a “great hand of stocks,” you must read the rest of the players in the market. If they are all buying or selling, what do they know that you possibly don’t.

So, that brings me to the question above. I am NOT sure that I am right.

However, since last May I have held exposure in portfolios to 50% of normal equity allocations because the price trends of the market have been deteriorating. Furthermore, they continue to do so which is leading me to reduce allocations even more (see next section.)

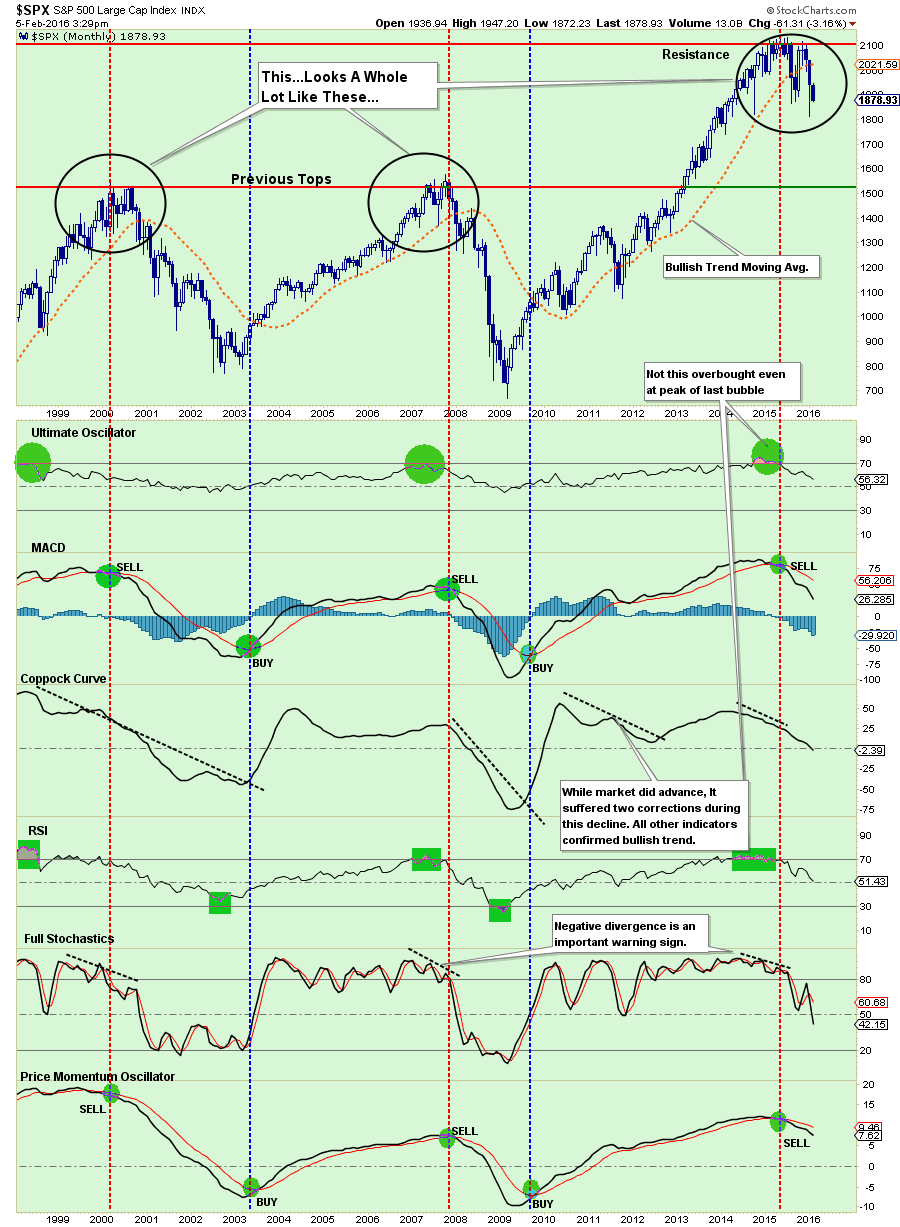

Am I predicting a major market decline? NO. However, I am suggesting that given the current weight of evidence that one may very likely already be in process. The chart below is a MONTHLY chart of market indicators that measure a variety of market internals. Currently, every single measure is registering a “SELL” signal which has only occurred during the previous two bull market cycles.

Now, you can certainly make the case for why “this time is different.” However, if you are a good poker player, should you really be betting heavily given the current hand?

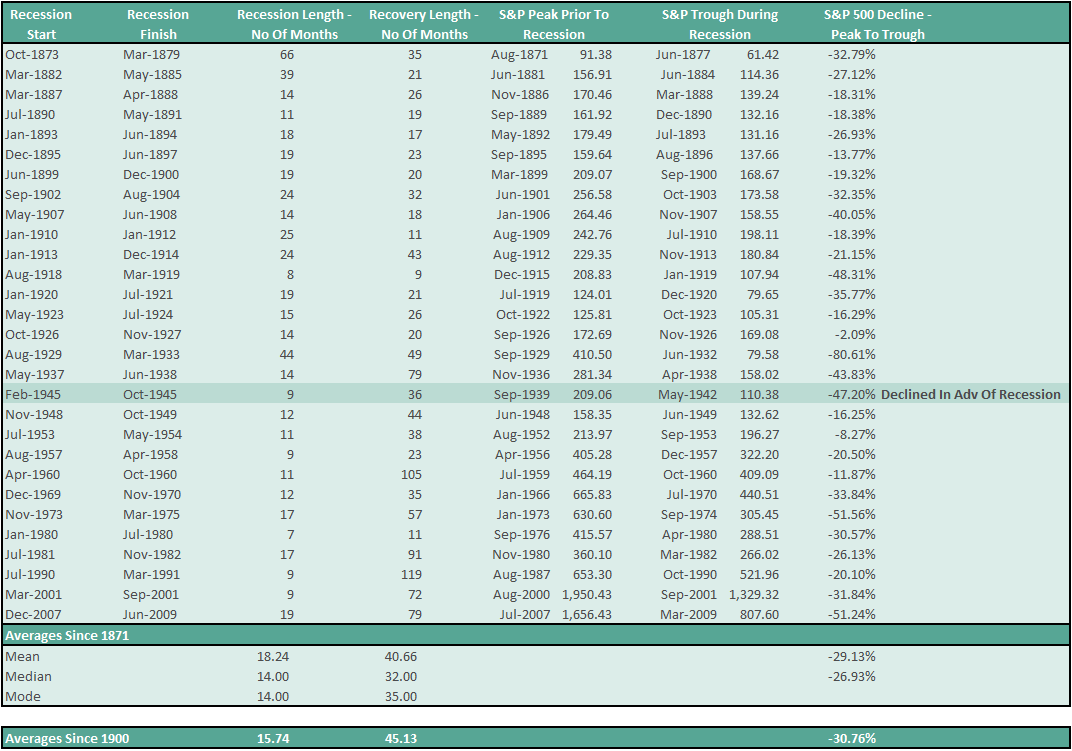

Even if correction only reverts back to the previous peaks of the past two bull markets, such would entail an additional decline of 18% from current levels, or 27% from the previous peak. Such a correction would just about meet the average draw down of a bear market cycle throughout history as shown in the table below.

ary. I’ve gone through many of them, having started my career in investment management just two months before the 1987 crash.

While different circumstances led to each one, the fundamental aspect of a correction (or even a bear market) is that the market simply reprices securities to better match the underpinnings of an investment as they currently are.

Sometimes, this may happen because of a recession, which we do not think is the most likely scenario, but in many other cases, it’s simply because stocks got a little ahead of themselves. Right now, stocks in the S&P 500 are more expensive relative to their earnings than they historically have tended to be, according to Ned Davis Research. That means that investors bid up share prices more than (or perhaps one might even venture to say “earlier than”) they should have. In that sense, a correction is just that: “correcting” a stock’s value to what the earnings and net worth of the company in question should dictate.”

This really goes to the root of why I am so fed up with the financial advisory industry as a whole. Let me translate the above for you.

“We don’t really manage your money. What we do is encourage you to buy some stuff and then sit on it so we can charge you a fee.

When prices decline, because we don’t really pay attention to the markets, we have to send out an excuse letter to keep you from transferring your money to another advisor who actually pays attention to what is going on.

Even though we knew stocks were overvalued, and such overvaluation leads to corrective cycles in the market, we really didn’t think about selling stocks to reduce the risk of loss. We are too busy trying to get other people to invest money with us. The more the better.

We hope you understand, but our revenue line is more important than yours. Oh, and please deposit more money in your account because dollar cost averaging works better for us than you.”

I realize that is a bit harsh, but I want to make a point. I know some really great advisors that work extremely hard for the clients, manage risk and try to ensure their clients reach their goals. If you ever read a site like Seeking Alpha, you will see a lot of them. Then there are these guys which give the rest of the industry a bad name.

Let me be clear with you. YES, it is time to worry, and it may be time to worry a lot.

If I am wrong, and the markets turn around, we can ALWAYS buy stuff and sit on it again. But now is not that time.

Apparently, if you don’t take some action with respect to the risk in your portfolio, no one else is going to either.

THE MONDAY MORNING CALL

As stated above, the market bounce failed much sooner than anticipated. This changes the tone of the market to substantially more bearish.

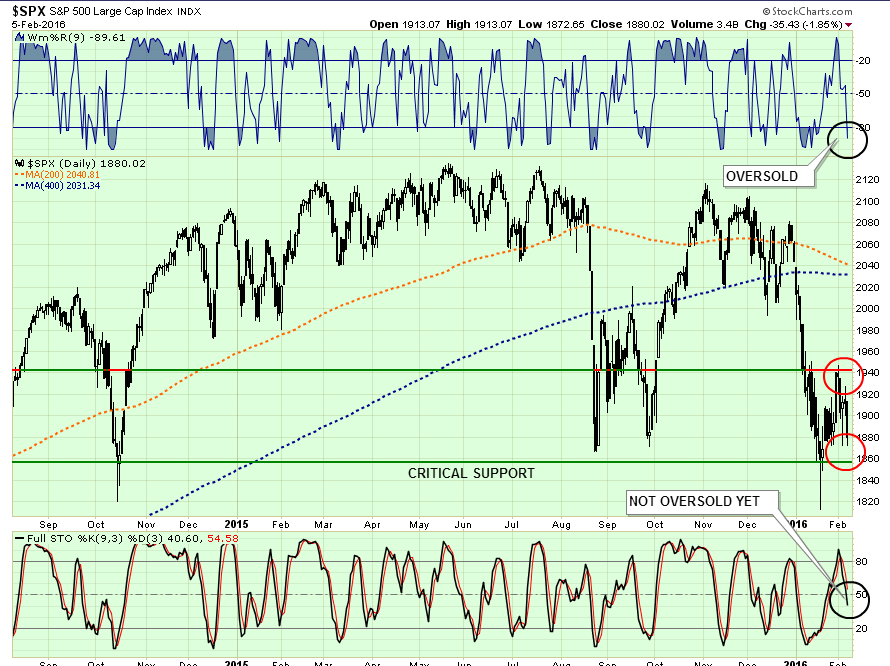

As shown in the chart below, on a very short-term basis the market is oversold and once again suggests the markets could get some buying early next week. However, they are also on the verge of breaking critical support.

I continue to suggest taking actions to reduce risk in portfolios by taking the following actions on ANY RALLIES:

Trim back winning positions to original portfolio weights: Investment Rule: Let Winners Run

Sell positions that simply are not working (if the position was not working in a rising market, it likely won’t in a declining market.) Investment Rule: Cut Losers Short

Hold the cash raised from these activities until the next buying opportunity occurs. Investment Rule: Buy Low

One other point. The two moving averages in the chart above are the 200-day and 400-day. As you will notice they are about to cross. Because these two moving averages are so long in nature, THEY WILL CROSS. It is now inevitable UNLESS the market immediately reverses to a runaway stampede higher.

This “real death cross” was brought to my attention earlier this week by a loyal reader:

“Most identify the death cross as when the 50-day moving average breaks below the 200-day moving average on the S&P 500. However, the real death cross takes place when the 200-day moving average crosses below the 400. In 13 of the last 18 major correction episodes going back 1920- 72% this crossover marked the onset of a major Bear market.

In the five exceptions, which were 1953, 1990, 1984, 1987, and 1996, the same crossover actually ended the correction at that time. Importantly, these five episodes were during strongly trending SECULAR bull market cycles. Given we are not currently in one of those periods, it is likely a cross-over now would be more related to each of the market failures since the turn of the century.”

As I stated above, I am not “predicting” anything. What I am doing is suggesting that current trends, based on historical precedents, suggests that “something wicked this way comes.”

http://davidstockmanscontracorner.com/something-this-way-wicked-comes-a-deep-dive-into-the-market-charts/

The Cozy Relationship Between The Treasury And The Fed

Submitted by David Howden via The Mises Institute,

02/04/2016

Last year was a tough one for investors. Gold was down 10 percent. The Dow Industrials fell 2.5 percent, and most bond indexes finished down by at least that much.

One institution that performed remarkably well in 2015 was the Federal Reserve. It just finished its most profitable year on record. The $100 billion in net income earned last year was a slight improvement over the previous year. That total was also roughly three times higher than the Fed’s income from 2007, the last year before it initiated its Quantitative Easing programs in the wake of the financial crisis.

Since the Fed does not exist to generate profits, some may be confused as to how it could have such a great year at doing so.

Here’s how it works. Every time the Fed expands the money supply it buys an asset. Typically the asset is a financial security, like a US Treasury bond, and the counterparties are typically large banks. Figure 1 gives a simplified look at the Fed’s balance sheet at the end of 2015 and how it evolved over the year:

Compared to previous years, 2015 was relatively uneventful at the Fed. Having completed the tapering of its Quantitative Easing programs in October 2014, the Fed’s asset holdings held constant over the year. This was in stark contrast to the previous six years, during which the Fed purchased $3.5 trillion of assets. The Fed earns interest on its assets but most of its liabilities are non-interest bearing, like the $1.4 trillion worth of Federal Reserve notes crumpled in people’s pockets or buried under our mattresses. The Fed does pay interest on Reserve Bank balances, but at the current rate of 0.5 percent, this figure was a drop in the bucket relative to its total income. (Almost all of the Fed’s assets earn interest, while it incurs an interest expense on less than half of its liabilities.

What Does the Fed Do With All That Income?

The question that arises is what the Fed does with its profits.

Each year, the Fed remits to the US Treasury its net income, and thus provides the federal government with an important source of funding. Figure 2 shows how this figure has evolved since 2001.

A decade ago, back when the Fed was a smaller size, Fed remittances were fairly steady, in the neighborhood of $20 billion a year. This all changed after 2008 as the Fed’s Quantitative Easing programs increased the amount of interest-earning assets that would generate funds to transfer back to the Treasury. This year’s figure of $97.7 billion is more than four times the amount transferred just ten years ago, an annual growth rate of more than 16 percent. (At least something is growing quickly in this economy.)

Big Bucks for the US Treasury

For the US Treasury, Fed remittances are something of a free lunch. When someone buys a Treasury bond, the government must pay them interest. This applies to the Fed as well, but then at year-end the Fed remits the interest back to the Treasury.

The federal government paid out $223 billion in interest payments last year. The Fed remitted almost $100 billion back, leaving the net interest expense at around $125 billion. It’s not just historically low interest rates that are making it easier for the Treasury to borrow in a way that, if it were done by anyone else, would classify them as subprime. The Fed is also chipping in and helping out where it can.

Also shown in figure 2 is the percentage of the federal interest expense that is remitted back by the Fed. For 2015, this figure neared 45 percent. That figure is a good way to think about the free lunch that the Fed gives to the Treasury.

In more “normal” times (i.e., prior to 2008) around 10 to 15 percent of the Treasury’s interest payments were paid back to it by the Fed. This figure has grown to almost four times that amount over the past seven years and it doesn’t look likr this trend will abate anytime soon.

Implications for Fed “Independence”

As much as economists talk about the independence that the Fed holds from Congress, these remittances represent a strong link. In fact, since they enable federal spending they create a form of quasi-fiscal policy for the Fed to use, in addition to its more common monetary policy options.

Consider that since Treasury debt is almost never repaid in net terms (old issues are retired but replaced with new debt issuances), the true cost of financing the US government’s borrowing is not the gross amount of debt outstanding but the annual interest expense it faces. Viewed this way, nearly half of the Treasury’s borrowing was financed by the Fed last year. Absent these Fed remittances, Congress would need to look at either an alternative funding source (though I am not sure how many takers there are for the Fed’s $2.5 trillion Treasury holdings) or make some serious cuts.

How serious? NASA’s operating budget was roughly $18 billion last year, so a lack of Fed remittances would cause the Treasury to cut around five NASA-sized programs. Alternatively, the governments Supplemental

Nutrition Assistance Program (previously known as “food stamps”) cost $70 billion in 2014. Without the Fed’s remittances, Congress would have to stop paying out all food stamp recipients plus it would be forced to defund almost two NASAs.

More important in many Americans’ hearts is their monthly social security check. In 2014, $830 billion of social security checks were mailed out. Without Fed remittances, retirees might see their monthly check cut by about 12 percent.

For those concerned with the burgeoning size of the federal government, putting a stop to Fed remittances would put a serious dent in public finances and force some serious thought as to what programs need to be cut.

http://www.zerohedge.com/news/2016-02-04/cozy-relationship-between-treasury-and-fed

When Mother Market Force Takes Over Central Banking! Watch Rates Rise Even Though the Fed Doesn't

by Reggie Middleton

02/04/2016

CNN reports the US running out of space to store oil.

At the same time, OPEC actually ramps up oil production...

oil pricesOPEC oil supply

Many "smart guys" allege that the drop in oil is bad for the ecomomy. I call BS. Oil prices are an input costs. Input costs are what strip revenues down to profits and potentially losses. The lower the input cost, the higher profit. What has occured was a decades long credit bubble that fueld a profligate binging on debt.

It is hard to get off of that drug called free money, particuarly as your dope pusher (those that push rates outside of market force bounds) continues to give you more of that smack. The problem is, eventually, it will catch up to you. The Central Banks have signaled higher rates, and have raised rates 25 bp (roughly 2% of retracement - whoo hoo!).

The market (well, the fed funds rates futures, not the market per se) is quite skeptical on the Fed raising rates any time soon. So am I, as you have seen above.

Alas, as rates scrape against the zero barrier for sometime now, and break through towards negative, the party is over and the punchbowl is being removed by the grownups, aka the natural market forces. The Financial Times reports:

The sharp drop in commodity prices and a rising expectation of defaults by highly indebted companies have shaken investors and closed the door on new debt sales. Investors say the dearth of liquidity has made it even more difficult to own paper rated triple C. Late last year several bond funds closed that held high amounts of low-rated and unrated debt.

“You are seeing a lack of appetite in the new issue market for these types of issuers,” said Matthew Mish, credit strategist with UBS. “[Funds] have outflows and the Federal Reserve is no longer printing money.

Portfolio managers are also experiencing a wave of redemptions from investors. US junk bond mutual and exchange traded funds have counted more than $20bn of withdrawals since mid-November, according to Lipper.

You know what that means. Those oil producers with higher than OPEC costs and high yield debt financing are GUARANTEED to meltdown as oil drops below their breakeven costs (I'd wager somewhere around $50 - $60/bbl if I was a betting man), and stays there. Recent financial reporting seems to corroborate this hunch...

“We expect a shakeout this year in the US oil and gas market, as highly leveraged companies will be forced to declare bankruptcy,” said Bronka Rzepkowski, an economist with Oxford Economics.

A Q&A: Using Veritaseum to take positions in energy companies through multiple markets. Please be aware that Veritaseum is currently in beta, and the current Java client will be deprecated in lieu of a ubiquitous HTML5 client by the end of the quarter. The info below is for illustrative purposes only.

How do I enter the trade via Veritaseum? Am I using the web client? My own client that consumes Veritaseum APIs? Place the trade over the phone / fax with Veritaseum’s sales team?

If you are an advanced player you can simply go to our site and conduct the trade yourself using the system and/or your own network to find a counterparty.

As an institution, you can purchase Veritas (ex. $50,000 blocks) to redeem them for advisory services such as setting up trades and finding bespoke counterparties.

Large institutions with their own IT infrastructure can integrate Veritaseum into their system via API. This can also entail a Veritas purchase to assist in the integration, customizations and feature requests.

Where does the counterparty for the trade come from?

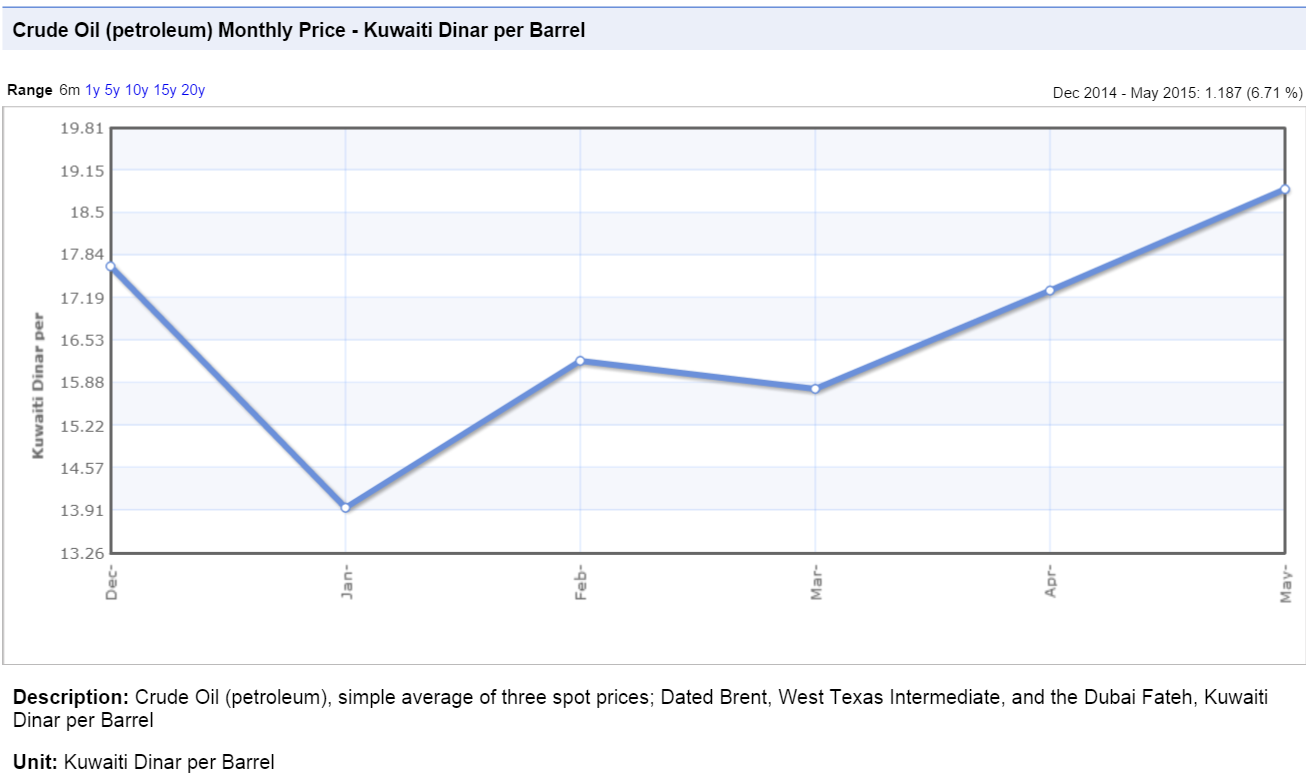

Japan is the largest consumer of Kuwaiti oil, followed by India, Singapore, and South Korea. Since Asia is such a large consumer of OPEC oil in general (and Kuwaiti oil in particular), they can be very aggressive in their purchasing terms, resulting in material concessions from the oil (and risk) producers - the most painful of which are price discounts. We can offer the oil consumers in these markets the ability to directly hedge their purchase risks - both in terms of currency and oil price fluctuation (or oil price volatility, as illustrated above) accentuating the benefits of discounts while simultaneously making discounts potentially less painful by hedging risks for the oil (risk) producers. Their (the Asian companies) purchase of said risks is the counterpart of the sale of the risk from KOC. The oil refineries of Japan, India, Singapore, and South Korea are the most likely potential counterparties but you can also include the money center banks within these countries, not not to mention the major hedge and trading funds and corporations who consume the finished product en masse. Remember, the USD component of the swap can easily be replaced with the Japanese yen, Chinese Remnibi/yuan, Indian rupee or the Korean won.

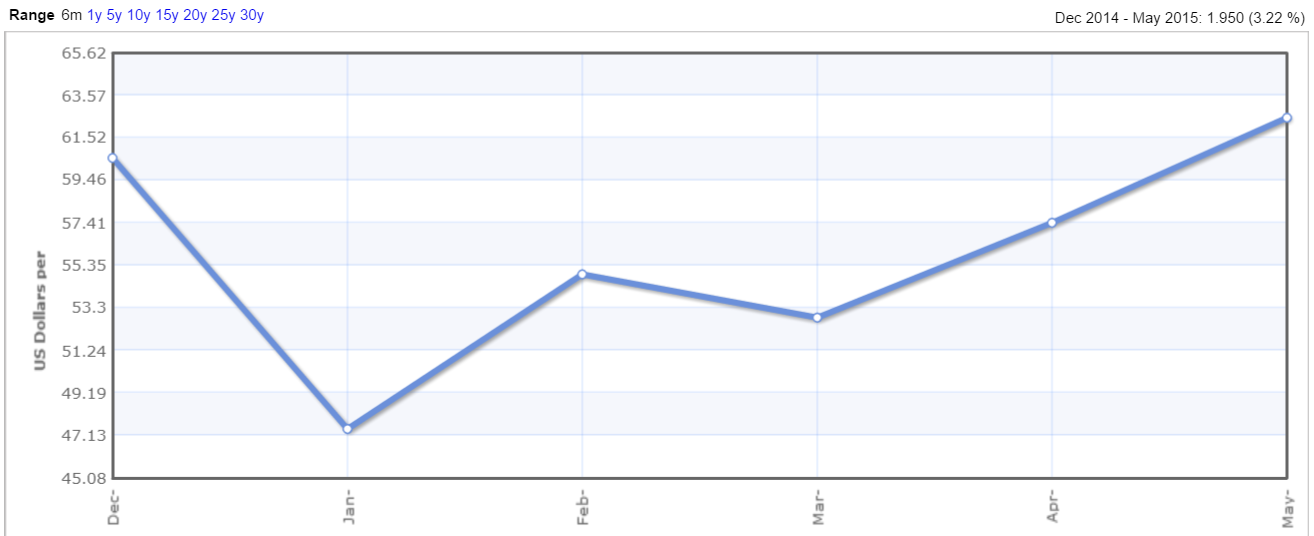

This same chart expressed in USD shows where the hedge benefits, particularly in December…

Entities that aren’t exposed to the Kuwaiti Dinar can still benefit by buying the oil risk and selling their local currency with Veritaseum via a separate swap. The Kuwaiti dinar can also be substituted for Saudia Arabian native currency, or Iraqi dinars, etc.

Who are the specific counterparties (consumers) of OPEC (producer, of which Kuwait is a major member) oil risk?

A joint venture between PetroChina Co. (Chinese), Aramco (Saudi Arabian) and Yunnan Yuntianhua Co. (Chinese) is currently building a 260,000 barrel-a-day refinery in the southwest of the Asian nation.

Aramco already manages a 280,000 barrel-a-day refinery and petrochemical complex in China’s Fujian province along with China Petroleum & Chemical Corp., known as Sinopec, and Exxon Mobil Corp.

China is the largest oil consumer after the U.S.

IF you are interested in finding about more about this new way of accessing exposure and laying off risk, read the Pathogenic Finance research report, then contact me at reggie AT veritaseum.com.

Here are the highlights from the report in this most excellent interview with Max Keiser of RT's Kesier Report.

http://www.zerohedge.com/news/2016-02-04/when-mother-market-force-takes-over-central-banking-watch-rates-rise-even-though-fed

Another Nail In The US Empire Coffin: Collapse Of Shale Gas Production Has Begun

SRSroccoReport.com

Feb. 2, 2016

The U.S. Empire is in serious trouble as the collapse of its domestic shale gas production has begun. This is just another nail in a series of nails that have been driven into the U.S. Empire coffin.

Unfortunately, most investors don’t pay attention to what is taking place in the U.S. Energy Industry. Without energy, the U.S. economy would grind to a halt. All the trillions of Dollars in financial assets mean nothing without oil, natural gas or coal. Energy drives the economy and finance steers it. As I stated several times before, the financial industry is driving us over the cliff.

The Great U.S. Shale Gas Boom Is Likely Over For Good

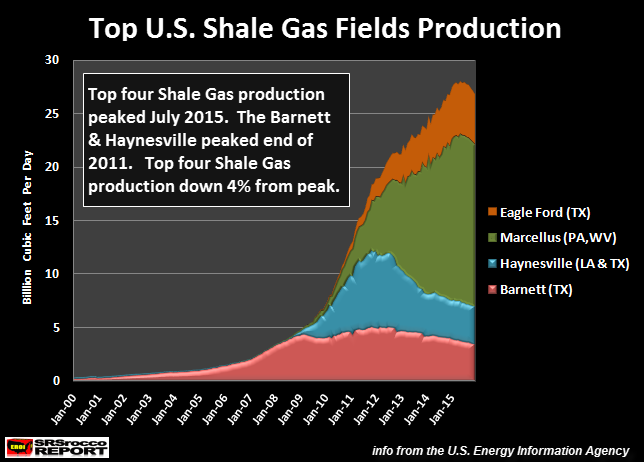

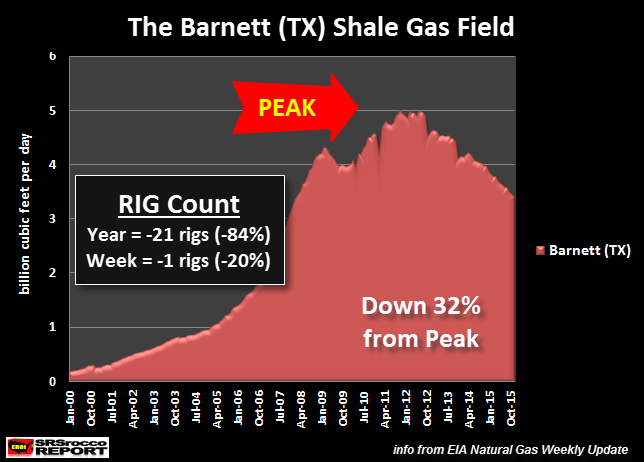

Very few Americans noticed that the top four shale gas fields combined production peaked back in July 2015. Total shale gas production from the Barnett, Eagle Ford, Haynesville and Marcellus peaked at 27.9 billion cubic feet per day (Bcf/d) in July and fell to 26.7 Bcf/d by December 2015:

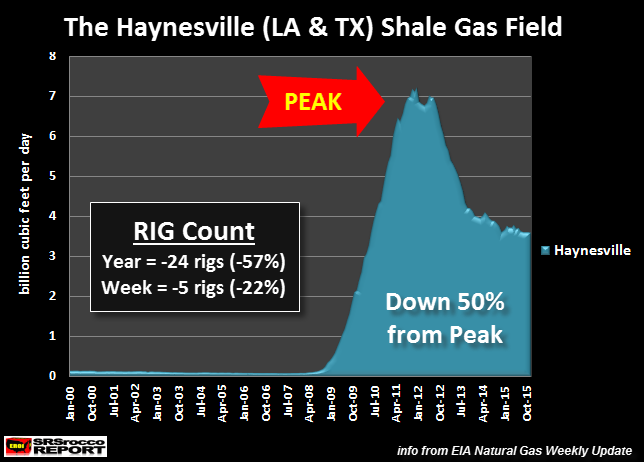

As we can see from the chart, the Barnett and Haynesville peaked four years ago at the end of 2011. Here are the production profiles for each shale gas field:

According to the U.S. Energy Information Agency (EIA), the Barnett shale gas production peaked on November 2011 and is down 32% from its high. The Barnett produced a record 5 Bcf/d of shale gas in 2011 and is currently producing only 3.4 Bcf/d. Furthermore, the drilling rig count in the Barnett is down a stunning 84% in over the past year.

The Haynesville was the second to peak on Jan 2012 at 7.2 Bcf/d per day and is currently producing 3.6 Bcf/d. This was a huge 50% decline from its peak. Not only is the drilling rig count in the Haynesville down 57% in a year, it fell another five rigs this past week. There are only 18 drilling rigs currently working in the Haynesville.

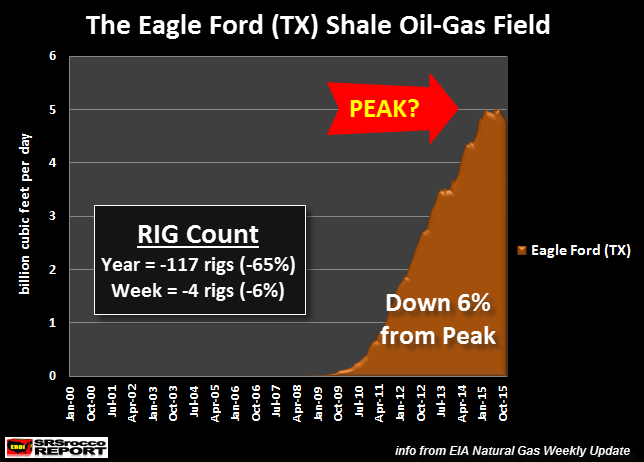

The EIA reports that shale gas production from the Eagle ford peaked in July 2015 at 5 Bcf/d and is now down 6% at 4.7 Bcf/d. As we can see, total drilling rigs at the Eagle Ford declined the most at 117 since last year. The reason the falling drilling rig count is so high is due to the fact that the Eagle Ford is the largest shale oil-producing field in the United States.

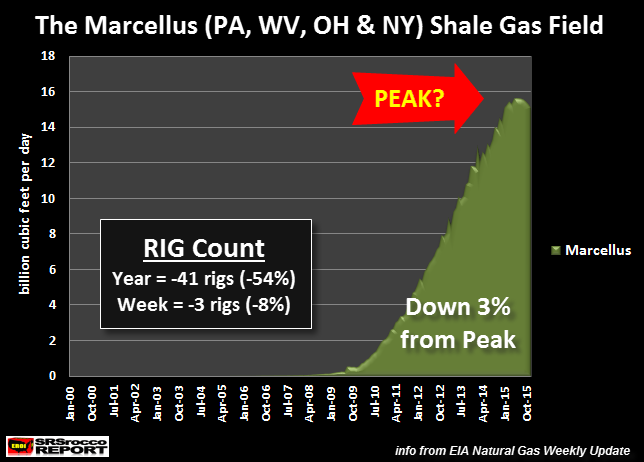

Lastly, the Mighty Marcellus also peaked in July 2015 at a staggering 15.5 Bcf/d and is now down 3% producing 15.0 Bcf/d currently. The Marcellus is producing more gas (15 Bcf/d) than the other top three shale gas fields combined (12.1 Bcf/d).

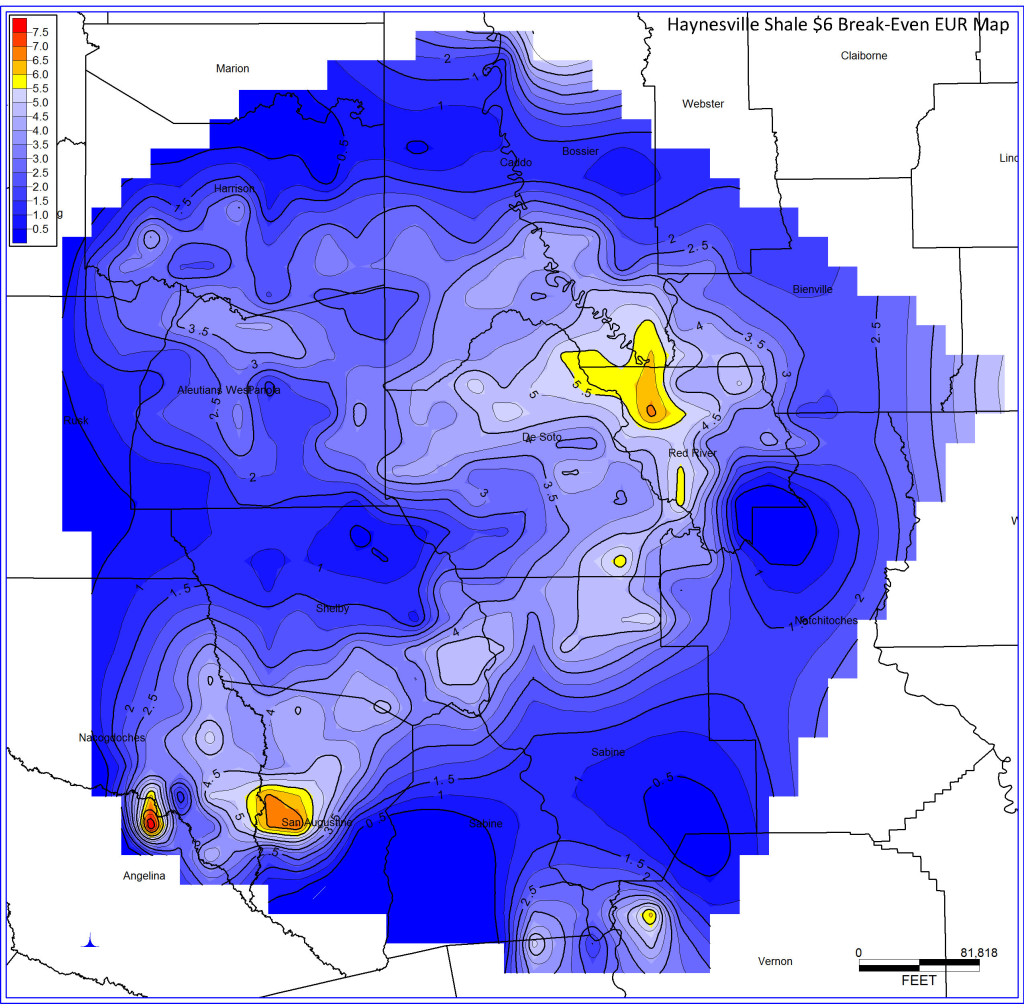

I have posted the Haynesville shale gas production chart below to discuss why U.S. Shale Gas production will likely collapse going forward:

What is interesting about the Haynesville shale gas field, located in Louisiana and Texas, is the steep decline of production from its peak. On the other hand, the Barnett (chart above in red) had a much different profile as its production peak was more rounded and slow. Not so with the Haynesville. The decline of shale gas production at the Haynesville was more rapid and sudden. I believe the Eagle Ford and Marcellus shale gas production declines will resemble what took place in the Haynesville.

All you have to do is look at how the Eagle Ford and Marcellus ramped up production. Their production profiles are more similar to the Haynesville than the Barnett. Thus, the declines will likely behave in the same fashion. Furthermore drilling and extracting shale gas from the Haynesville was a “Commercial Failure” as stated by energy analyst Art Berman in his Forbes article on Nov 22 2015:

The Haynesville Shale play needs $6.50 gas prices to break even. With natural gas prices just above $2/Mcf (thousand cubic feet), we question the shale gas business model that has 31 rigs drilling wells in that play that cost $8-10 million apiece to sell gas at a loss into a over-supplied market.

The Haynesville Shale play needs $6.50 gas prices to break even. With natural gas prices just above $2/Mcf (thousand cubic feet), we question the shale gas business model that has 31 rigs drilling wells in that play that cost $8-10 million apiece to sell gas at a loss into a over-supplied market.

At $6 gas prices, only 17% of Haynesville wells break even (Table 3) and approximately 115,000 acres are commercial (Figure 2) out the approximately 3.8 million acres that comprise the drilled area of the play.

The Haynesville Shale play is a commercial failure. Encana exited the play in late August. Chesapeake and Exco, the two leading producers in the play, both announced significant write-downs in the 3rd quarter of 2015.

Basically, the overwhelming majority of the shale gas extracted at the Haynesville was done so at a complete loss. So, why do they continue drilling and producing gas in the Haynesville?

The reason Art Berman states is this:

What we see in the Haynesville Shale play are companies that blindly seek production volumes rather than value, and that care nothing for the interests of their shareholders. The business model is broken. It is time for investors to finally start asking serious questions.

Chesapeake is one of the larger shale gas producers in the Haynesville as well as in the United States. According to its recent financial reports, Chesapeake received $1.05 billion in operating cash in the first three-quarters of 2015, but spent $3.2 on capital expenditures to continue drilling. Thus, its free cash flow was a negative $2.1 billion in the first nine months of 2015. And this doesn’t include what it paid out in dividends.

The same phenomenon is taking place in other companies drilling for shale gas in the other fields in the U.S. This insanity has Berman perplexed as he states this in another article from his site:

This has puzzled me because the shale gas plays are not commercial at less than about $6/mmBtu except in small parts of the Marcellus core areas where $4 prices break even. Natural gas prices have averaged less than $3/mmBtu for the first quarter of 2015 and are currently at their lowest levels in more than 2 years.

The reason these companies continue to produce shale gas at a loss is to keep generating revenue and cash flow to service their debt. If they cut back significantly on drilling activity, their production would plummet. This would cause cash flow to drop like a rock, including their stock price, and they would go bankrupt as they couldn’t continue servicing their debt.

Basically, the U.S. Shale Gas Industry is nothing more than a Ponzi Scheme.

The Collapse Of U.S. Shale Gas Production Even At Higher Prices

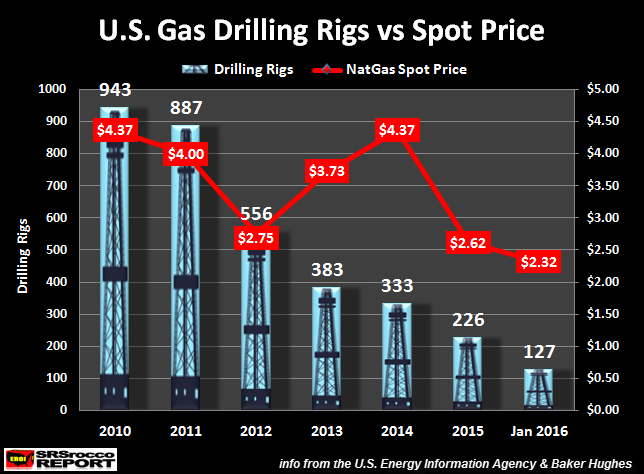

I believe the collapse of U.S. shale gas production will occur even at higher prices Why? Because the price of natural gas increased from $2.75 mmBtu in 2012 to $4.37 mmBtu in 2014, but the drilling rig count continued to fall:

As the price of natural gas increased from 2012 to 2014, gas drilling rigs fell 40% from 556 to 333. Furthermore, drilling rigs continued to decline and now are at a record low of 127. Just as Art Berman stated, the average break-even for most shale gas plays are $6 mmBtu, while only a small percentage of the Marcellus is profitable at $4 mmBtu.

Looking at the chart again, we can see that the price of natural gas never got close to $6 mmtu.. the highest was $4.37 mmBtu. Thus, the U.S. Shale Gas Industry has been a commercial failure.

Now that the major shale gas producers are saddled with debt and many of the sweet spots in these shale gas fields have already been drilled, I believe U.S. shale gas production will collapse going forward. If we look at the Haynesville Shale Gas Field production profile, a 50% decline in 4 years represents a collapse in my book.

The Two Nails In The U.S. Empire Coffin

As I stated in several articles and interviews, ENERGY DRIVES THE ECONOMY, not finance. So, energy is the key to economic activity. Which means, energy output and the control of energy are the keys to economic prosperity.

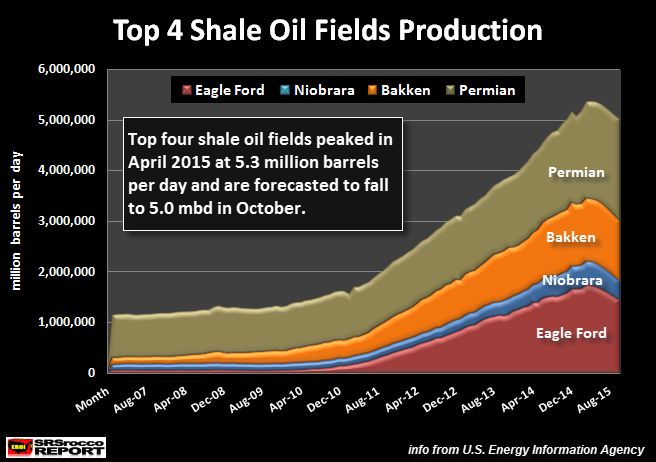

While the collapse of U.S. shale gas production is one nail in the U.S. Empire Coffin, the other is Shale Oil. U.S. shale oil production peaked before shale gas production:

This chart is a few months out of date, but according to the EIA’s Productivity Reports, domestic oil production from the top four shale oil fields peaked in April of 2015… three months before the major shale gas fields (July 2015).

Unfortunately for the United States, it was never going to become energy independent. The notion of U.S. energy independence was built on hype, hope and cow excrement. Instead, we are now going to witness the collapse of U.S. shale oil and gas production.

The collapse of U.S. shale oil and gas production are two nails in the U.S. Empire coffin. Why? Because U.S. will have to rely on growing oil and gas imports in the future as the strength and faith of the Dollar weakens. I see a time when oil exporting countries will no longer take Dollars or U.S. Treasuries for oil. Which means… we are going to have to actually trade something of real value other than paper promises.

I believe U.S. oil production will decline 30-40% from its peak (9.6 million barrels per day July 2015) by 2020 and 60-75% by 2025. The U.S. Empire is a suburban sprawl economy that needs a lot of oil to keep trains, trucks and cars moving. A collapse in oil production will also mean a collapse of economic activity.

Thus, a collapse of economic activity means skyrocketing debt defaults, massive bankruptcies and plunging tax revenue. This will be a disaster for the U.S. Empire.

http://www.zerohedge.com/news/2016-01-30/another-nail-us-empire-coffin-collapse-shale-gas-production-has-begun

Negative Interest Rates Already In Fed’s Official Scenario

Feb. 2, 2016

Over the past year, and certainly in the aftermath of the BOJ's both perplexing and stunning announcement (as it revealed the central banks' level of sheer desperation), we have warned (most recently "Negative Rates In The U.S. Are Next: Here's Why In One Chart") that next in line for negative rates is the Fed itself, whether Janet Yellen wants it or not. Today, courtesy of Wolf Richter, we find that this is precisely what is already in the small print of the Fed's future stress test scenarios, and specifically the "severely adverse scenario" where we read that:

The severely adverse scenario is characterized by a severe global recession, accompanied by a period of heightened corporate financial stress and negative yields for short-term U.S. Treasury securities.

As a result of the severe decline in real activity and subdued inflation, short-term Treasury rates fall to negative ½ percent by mid-2016 and remain at that level through the end of the scenario.

And so the strawman has been laid. The only missing is the admission of the several global recession, although with global GDP plunging over 5% in USD terms, we wonder just what else those who make the official determination are waiting for.

Finally, we disagree with the Fed that QE4 is not on the table: it most certainly will be once stock markets plunge by 50% as the "severely adverse scenario" envisions, and once NIRP fails to boost economic activity, as it has failed previously everywhere else it has been tried, the Fed will promtply proceed with what has worked before, if only to make the true situation that much worse.

Until then, we sit back and wait.

Here is Wolf Richter with Negative Interest Rates Already in Fed’s Official Scenario

The Germans, with Teutonic precision, call them “Punishment Interest.” Negative interest rates are spreading from the ECB’s negative deposit rate across the bond market and to some savings accounts in the Eurozone. The idea is to enrich existing bond holders and flog savers until their mood improves. Stock prices are allowed to get crushed by reality.

Negative interest rates destroy one of the most essential mechanisms in an economy: the pricing of risk. Investors end up taking huge risks with no reward. Many of them will get cleaned out down the road.

In Switzerland, punishment interest already causes “perverse unpredictable effects,” as mortgage rates have started to soar. It’s wreaking havoc in Denmark and Sweden. Bank of Canada Governor Stephen Poloz let the idea float that he’d unleash punishment interest to destroy the Canadian dollar. The Bank of Japan announced Friday morning – timed for maximum market effect – that it too would inflict negative interest rates on its subjects.

In the US, Ben Bernanke has been out there preaching to the choir about them. Over-indebted corporate America, except for the banks, would love this absurdity; it would allow them to actually make money off their mountain of debt.

“Potentially anything – including negative interest rates – would be on the table,” Fed Chair Janet Yellen told a House of Representatives committee in early November.

Fed Vice Chair Stanley Fischer has been publicly obsessing about them for a while. Monday, during the Q&A after his speech at the Council on Foreign Relations, he said that negative interest rates are “working more than I can say I expected in 2012.”

It seems to be just talk. But negative interest rates are already baked into the official scenario for 2016. It’s in the Board of Governors’ new report on the three scenarios to be used in 2016 for the annual stress test that large banks are required to undergo under the Dodd-Frank Act and the Capital Plan Rule.

The scenarios – baseline, adverse, and severely adverse – start in the first quarter 2016 and also include economic factors in the Eurozone, the UK, Japan, and the weighted aggregate of China, India, South Korea, Hong Kong, and Taiwan.

In the “severely adverse scenario,” things get interesting.

But don’t worry, the Fed emphasizes that “this is a hypothetical scenario” for the purpose of a bank stress test and “does not represent a forecast of the Federal Reserve”:

The severely adverse scenario is characterized by a severe global recession, accompanied by a period of heightened corporate financial stress and negative yields for short-term U.S. Treasury securities.

GDP begins to tank in Q1 2016 and by Q1 2017 is 6.25% below pre-recession peak. The unemployment rate hits 10% by mid-2017. Headline CPI rises from an annual rate of 0.25% in Q1 2016 to 1.25% by the end of the recession. Asset prices “drop sharply,” with stocks down “approximately 50%” through the end of this year, accompanied by a surge in volatility, “which approaches the levels attained in 2008.” Through Q2 2018, home prices plunge 25%, commercial real estate prices 30%.

“Corporate financial conditions are stressed severely, reflecting mounting credit losses, heightened investor risk aversion, and strained market liquidity conditions.” Bond spreads blow out, with the yield spread between investment-grade corporates and Treasuries jumping to 5.75% by the end of 2016.

So things are going to get ugly. And here is what the Fed is going to do next:

As a result of the severe decline in real activity and subdued inflation, short-term Treasury rates fall to negative ½ percent by mid-2016 and remain at that level through the end of the scenario.

Short-term Treasury rates can only fall to a negative 0.5% if the fed funds rate is at that level.

And the whole yield curve comes down, with the 10-year Treasury yield collapsing to 0.25% by the end of this quarter, but then “rising gradually” all the way to a whopping 0.75% by the end of the recession and to 1.75% by Q1 2019 (it’s 1.93% now).

The international component “features severe recessions” in the Eurozone, the UK, and Japan, and a mild recession in developing Asia, along with a “pronounced decline in consumer prices.”

Due to “flight-to-safety capital flows,” the dollar appreciates against the euro, the pound, and the currencies of developing Asia, but will “depreciate modestly” against the yen, “also in line with flight-to-safety capital flows.”

One of the differences between the severely adverse scenarios for 2015 and 2016? The scenario this year “features a path of negative short-term U.S. Treasury rates.”

Who are the winners? Existing holders of long-term Treasuries who will benefit from “larger gains on the existing portfolio of these securities.”

However, the Fed makes no promises about stocks, having seen the debacle playing out in Europe where stocks have plunged despite negative interest rates. And banks will get hit as “negative short-term rates may be expected to reduce banks’ net interest margins and ultimately, to lower PPNR [pre-provision net revenue].

And there you have it. The Fed already has a “path” to negative interest rates.

But note: not a single word about QE.

If the stock market crashes 50% this year, as the “severely adverse” scenario spells out, all the Fed will do is slash the fed funds rate to a negative 0.5%. And if stocks crash only 25% this year, instead of 50%?

That’s the case in the Fed’s middle scenario, the merely “adverse” scenario. Short-term rates will “remain near zero” it says – maybe slightly below where they’re right now. So no negative interest rates. And no QE either. Stocks can go to heck, the Fed is saying. It’s worried about credits, particularly high-grade credits. Junk bonds and stocks are on their own.

And this concept of switching to negative interest rates and away from QE is even in line with the Bank of Japan’s desperate head fake. Read… QE in Japan Nears End: Daiwa Capital Markets

Over the past year, and certainly in the aftermath of the BOJ's both perplexing and stunning announcement (as it revealed the central banks' level of sheer desperation), we have warned (most recently "Negative Rates In The U.S. Are Next: Here's Why In One Chart") that next in line for negative rates is the Fed itself, whether Janet Yellen wants it or not. Today, courtesy of Wolf Richter, we find that this is precisely what is already in the small print of the Fed's future stress test scenarios, and specifically the "severely adverse scenario" where we read that:

The severely adverse scenario is characterized by a severe global recession, accompanied by a period of heightened corporate financial stress and negative yields for short-term U.S. Treasury securities.

As a result of the severe decline in real activity and subdued inflation, short-term Treasury rates fall to negative ½ percent by mid-2016 and remain at that level through the end of the scenario.

And so the strawman has been laid. The only missing is the admission of the several global recession, although with global GDP plunging over 5% in USD terms, we wonder just what else those who make the official determination are waiting for.

Finally, we disagree with the Fed that QE4 is not on the table: it most certainly will be once stock markets plunge by 50% as the "severely adverse scenario" envisions, and once NIRP fails to boost economic activity, as it has failed previously everywhere else it has been tried, the Fed will promtply proceed with what has worked before, if only to make the true situation that much worse.

Until then, we sit back and wait.

Here is Wolf Richter with Negative Interest Rates Already in Fed’s Official Scenario

The Germans, with Teutonic precision, call them “Punishment Interest.” Negative interest rates are spreading from the ECB’s negative deposit rate across the bond market and to some savings accounts in the Eurozone. The idea is to enrich existing bond holders and flog savers until their mood improves. Stock prices are allowed to get crushed by reality.

Negative interest rates destroy one of the most essential mechanisms in an economy: the pricing of risk. Investors end up taking huge risks with no reward. Many of them will get cleaned out down the road.

In Switzerland, punishment interest already causes “perverse unpredictable effects,” as mortgage rates have started to soar. It’s wreaking havoc in Denmark and Sweden. Bank of Canada Governor Stephen Poloz let the idea float that he’d unleash punishment interest to destroy the Canadian dollar. The Bank of Japan announced Friday morning – timed for maximum market effect – that it too would inflict negative interest rates on its subjects.

In the US, Ben Bernanke has been out there preaching to the choir about them. Over-indebted corporate America, except for the banks, would love this absurdity; it would allow them to actually make money off their mountain of debt.

“Potentially anything – including negative interest rates – would be on the table,” Fed Chair Janet Yellen told a House of Representatives committee in early November.

Fed Vice Chair Stanley Fischer has been publicly obsessing about them for a while. Monday, during the Q&A after his speech at the Council on Foreign Relations, he said that negative interest rates are “working more than I can say I expected in 2012.”

It seems to be just talk. But negative interest rates are already baked into the official scenario for 2016. It’s in the Board of Governors’ new report on the three scenarios to be used in 2016 for the annual stress test that large banks are required to undergo under the Dodd-Frank Act and the Capital Plan Rule.

The scenarios – baseline, adverse, and severely adverse – start in the first quarter 2016 and also include economic factors in the Eurozone, the UK, Japan, and the weighted aggregate of China, India, South Korea, Hong Kong, and Taiwan.

In the “severely adverse scenario,” things get interesting.

But don’t worry, the Fed emphasizes that “this is a hypothetical scenario” for the purpose of a bank stress test and “does not represent a forecast of the Federal Reserve”:

The severely adverse scenario is characterized by a severe global recession, accompanied by a period of heightened corporate financial stress and negative yields for short-term U.S. Treasury securities.

GDP begins to tank in Q1 2016 and by Q1 2017 is 6.25% below pre-recession peak. The unemployment rate hits 10% by mid-2017. Headline CPI rises from an annual rate of 0.25% in Q1 2016 to 1.25% by the end of the recession. Asset prices “drop sharply,” with stocks down “approximately 50%” through the end of this year, accompanied by a surge in volatility, “which approaches the levels attained in 2008.” Through Q2 2018, home prices plunge 25%, commercial real estate prices 30%.

“Corporate financial conditions are stressed severely, reflecting mounting credit losses, heightened investor risk aversion, and strained market liquidity conditions.” Bond spreads blow out, with the yield spread between investment-grade corporates and Treasuries jumping to 5.75% by the end of 2016.

So things are going to get ugly. And here is what the Fed is going to do next:

As a result of the severe decline in real activity and subdued inflation, short-term Treasury rates fall to negative ½ percent by mid-2016 and remain at that level through the end of the scenario.

Short-term Treasury rates can only fall to a negative 0.5% if the fed funds rate is at that level.

And the whole yield curve comes down, with the 10-year Treasury yield collapsing to 0.25% by the end of this quarter, but then “rising gradually” all the way to a whopping 0.75% by the end of the recession and to 1.75% by Q1 2019 (it’s 1.93% now).

The international component “features severe recessions” in the Eurozone, the UK, and Japan, and a mild recession in developing Asia, along with a “pronounced decline in consumer prices.”

Due to “flight-to-safety capital flows,” the dollar appreciates against the euro, the pound, and the currencies of developing Asia, but will “depreciate modestly” against the yen, “also in line with flight-to-safety capital flows.”

One of the differences between the severely adverse scenarios for 2015 and 2016? The scenario this year “features a path of negative short-term U.S. Treasury rates.”

Who are the winners? Existing holders of long-term Treasuries who will benefit from “larger gains on the existing portfolio of these securities.”

However, the Fed makes no promises about stocks, having seen the debacle playing out in Europe where stocks have plunged despite negative interest rates. And banks will get hit as “negative short-term rates may be expected to reduce banks’ net interest margins and ultimately, to lower PPNR [pre-provision net revenue].

And there you have it. The Fed already has a “path” to negative interest rates.

But note: not a single word about QE.

If the stock market crashes 50% this year, as the “severely adverse” scenario spells out, all the Fed will do is slash the fed funds rate to a negative 0.5%. And if stocks crash only 25% this year, instead of 50%?

That’s the case in the Fed’s middle scenario, the merely “adverse” scenario. Short-term rates will “remain near zero” it says – maybe slightly below where they’re right now. So no negative interest rates. And no QE either. Stocks can go to heck, the Fed is saying. It’s worried about credits, particularly high-grade credits. Junk bonds and stocks are on their own.

And this concept of switching to negative interest rates and away from QE is even in line with the Bank of Japan’s desperate head fake. Read… QE in Japan Nears End: Daiwa Capital Markets

The Numbers Are In: Hedge Funds Furiously Dumped The Rally; Selling Was "Biggest In Nearly Two Years"

zerohedge.com

02/02/2016

As we wrote yesterday when reviewing the latest note from JPM's Mislav Matejka, according to the JPM strategist not only had the window to buy stocks into the torrid S&P500 rebound closed, but traders should "start fading it within days" as JPM stuck "to the overriding view that one should use any strength as an opportunity to reduce equity allocation."

Today, when reading the latest report by BofA's equity and quant strategy team looking at what the "smart money" - institutions, hedge funds and private clients - are doing, we find that JPM's advice was heeded, and the rally was indeed sold with reckless abandon.

From BofA:

Last week, during which the S&P 500 rallied another 1.8%, BofAML clients were net sellers of US stocks for the first time in five weeks, in the amount of $1.2bn. Net sales were led by hedge fund clients, who had previously been net buyers for the prior five weeks, while private clients and institutional clients were also net sellers. (Institutional clients have alternated between buying and selling in recent weeks, while private clients have been sellers for the last three weeks.)

Perhaps just as notable is that according to BofA, buybacks by corporate clients decelerated last week to their lowest level year-to-date, but on a four-week average basis buybacks are well above last January’s levels.

In other words, just as we suggested yesterday, much of the February buybacks expected by Goldman's David Kostin to come to the rescue of the market, have been pulled forward into January, leaving far less dry powder available for the month of February.

What was the smart money selling?

Net sales last week were chiefly in large caps, while small caps also saw outflows; clients continued to buy mid-cap. Previously, all three size segments had seen net buying every week of 2016.

Among the details, one sector stands out: recent hedge fund darling, the healthcare sector, is seeing a furious exit by existing holders with sales "the biggest in seven months and the third-largest in our data history" as what worked until now no longer works. Tech was also slammed and sakes were "the largest in fifteen months and the fourth-largest in our data history."

Net sales last week were led by Tech and Health Care stocks, despite overall 4Q earnings for these sectors coming in better than expected. Health Care—which has been one of the most crowded sectors within the S&P 500—was the worst-performing sector last week, and we’ve noted that revision and surprise trends have been rolling over for this sector. This is the only sector with a multi-week net selling trend, and outflows from Health Care stocks last week were the biggest in seven months and the third-largest in our data history (since ’08), led by hedge funds. Sales of Tech were the largest in fifteen months and the fourth-largest in our data history, led by institutional clients. Energy stocks saw the biggest net buying by our clients last week amid the rally in oil prices; with inflows from all three client groups. This sector has now seen four consecutive weeks of buying by our clients, suggesting increasing conviction that oil has bottomed. Financials stocks also saw net buying for the fifth consecutive week amid the sell-off in this sector, while clients also continued to buy Telecom stocks for the fifth week.

But nobody sold more than the very pinnacle of smart money: hedge fund investors, where "net sales last week by hedge funds were the biggest in nearly two years and the fourth-largest in our data history. This follows near-record levels of net buying by this group in early January."

One final observation:

"overall for the month of January, clients were net buyers of single stocks, while ETFs saw more muted net buying. This would be the first year in our data history (since ’08) that clients bought single stocks."

A return to normalcy perhaps?

Finally, while weekly flows tend to be notoriously volatile, the long-term trend across all three investor classes are clear.

http://www.zerohedge.com/news/2016-02-02/numbers-are-hedge-funds-furiously-dumped-rally-selling-was-biggest-nearly-two-years

A Chinese Banker Explains Why There Is No Way Out

zerohedge.com

01/30/2016

Over the past year, we have frequently warned that the biggest financial risk (if not social, which in the form of soaring worker unrest is a far greater threat to Chinese civilization) threatening China, is its runaway non-performing loans, which at anywhere between 10 and 20% of total bank assets, mean that China is one chaotic default away from collapsing into the post "Minsky Moment" singlarity where it can no longer rollover its bad debt, leading to a debt supernova and full financial collapse.

And as China's total leverage keeps rising, and according to at least one estimate is now a gargantuan 350% of GDP (incidentally the same as the US), the threat of a rollover "glitch" gets exponentially greater.

To be sure, in recent months the topic of China's bad debt has gained increasingly more prominence among the mainstream, and notably none other than Kyle Bass has made the bursting of China's credit cycle the basis for his short Yuan trade as noted here previously:

What I think the narrative will swing to by the end of this year if not sooner, is the real issue in China is not simply that profits have peaked. The real issue is the size of their banking system. Do you remember the reason the European countries ended up falling like dominoes during the European crisis was their banking systems became many multiples of their GDP and therefore many, many multiples of their central government revenue. In China, in dollar terms their banking system is almost $35 trillion against a GDP of $10 and their banking system has grown 400% in 8 years with non-performing loans being nonexistent. So what we are going to see next is a credit cycle, and in a credit cycle you see some losses, but if China's banking system loses 10%, you are going to see them lose $3.5 trillion.

And judging by the surge in recent and increasingly louder calls for a Chinese devaluation, some advocating a major one-off currency debasement, Bass' perspective is certainly prevalent among the trading community. Bank of America goes so far as to speculate that the "upcoming G20 meeting in Shanghai offers an opportunity for policy makers to seize the “expectations” initiative via a one-off China devaluation." It does, however, also add that the "risk is markets need to panic first" before instead of piecemeal devaluation, China follows through with a Plaza Accord-type currency intervention.

Friday's adoption of NIRP by Japan, which send the US Dollar soaring, has only made any upcoming future Chinese devaluation even more likely.

But whether China devalued or not, one thing is certain: it is next to impossible for China - under the current socio economic and financial regime - to stop the relentless growth in NPLs, which even by conservative estimates at in the trillion(s), accounting for at least 10% of China's GDP.

Sure enough, a cursory skimming of news from China reveals that even Chinese bankers now "admit the NPL situation is dire, but will keep on lending" anyway.

As the Chiecon blog notes, NPL "ratios might be closer to 10%... supported by revelations in this article, where Chinese bankers complain of missing performance targets, spiraling bad loans, and end of year pay cuts."

“Right now, we’ve nowhere to issue new loans” said Mr. Zhang, a general manager in charge of new loans at one of the listed commercial bank branches. Zhang believes NPL ratios have yet to peak, with SME loans the worst hit area. Ironically this has forced Zhang to direct lending back to the LGFVs, property developers and conglomerates, industries which the Chinese government had previously instructed banks to restrict lending to, based on oversupply and credit risk fears.

But the main reason why China is now trapped, and on one hand is desperate to stabilize its economy and stop growing its levereage at nosebleed levels, while on the other hand it is under pressure to issue more loans while at the same time it is unwilling to write off bad loans, can be found in the following very simple explanation offered by Mr. Zhou, a junior banker at a Chinese commercial bank.

"If I don’t issue more loans, then my salary isn’t enough to repay the mortgage, and car loan. It’s not difficult to issue more loans, but lets say in a years time when the loan is due, if the borrower defaults, then I wont just see a pay cut, I’ll be fired, and still be responsible for loan recovery."

And that, in under 60 words, explains why China finds itself in a no way out situation, and why despite all its recurring posturing, all its promises for reform, all its bluster for deleveraging, China's ruling elite will never be able to achieve an internal devaluation, and why despite its recurring threats to crush, gut and destroy all the evil Yuan shorts, ultimately it will have no choice but to pursue an external devaluation of its economy by way of devaluing its currency presumably some time before its foreign reserves run out (which at a $185 billion a month burn rate may not last for even one year).

However, before it does, it will make sure that it also crushes every Yuan short, doing precisely what the Fed has done with equity shorts in the US over the past 7 years.

http://www.zerohedge.com/news/2016-01-30/chinese-banker-explains-why-there-no-way-out

"Pandora's Box Is Open": Why Japan May Have Started A 'Silent Bank Run'

zerohedge.com

01/30/2016

As extensively discussed yesterday in the aftermath of the BOJ's stunning decision to cut rates to negative for the first time in history (a decision which it appears was taken due to Davos peer pressure, a desire to prop up stock markets and to punish Yen longs, and an inability to further boost QE), there will be consequences - some good, mostly bad.

As Goldman's Naohiko Baba previously explained, NIRP in Japan will not actually boost the economy: "we do have concerns about the policy transmission channel. Policy Board Member Koji Ishida, who voted against the new measures, said that “a further decline in JGB yields would not have significantly positive effects on economy activity.” We concur with this sentiment, particularly for capex. The key determinants of capex in Japan are the expected growth rate and uncertainty about the future as seen by corporate management according to our analysis, while the impact of real long-term rates has weakened markedly in recent years."

What the BOJ's NIRP will do, is result in a one-time spike in risk assets, something global stock and bond markets have already experienced, and a brief decline in the Yen, one which traders can't wait to fade as Citi FX's Brent Donnelly explained yesterday.

NIRP will also have at most two other "positive" consequences, which according to Deutsche Bank include 1) reinforcing financial institutions’ decisions to grant new loans and invest in securities (if only in theory bnecause as explained further below in practice this may very well backfire); and 2) widening interest rate differentials to weaken JPY exchange rates, which in turn support companies’ JPY-based sales and profit, for whom a half of consolidated sales are from overseas.

That covers the positive. The NIRP negatives are far more troubling. The first one we already noted yesterday, when Goldman speculated that launching NIRP could mean that further QE is all tapped out:

... we believe the BOJ thinks that JGB purchases will have reached their technical limit in quantitative terms eventually, and it is highly likely it was a last-ditch measure to somehow maintain the current pace of purchases for some time. If not, we would have expected the BOJ not to introduce a negative interest rate this time either and to have opted instead to further increase JGB purchases.

Today, Deutsche Bank's Japan analyst Mikihiro Matsuoka jumps on the bandwagon and adds that "we are worried about a possible opening of a Pandora’s Box by explicitly removing the lower bound of nominal interest rates."

Here, according to Deutsche, are the most severe consequences of Japan opening the NIRP Pandora's box :

1.as the monetary base target of expanding by JPY80trn a year continues, the tax on financial institutions expands rapidly also, even if an upper bound on excess reserves that are subject to the negative rate is set. The net interest margin of Japanese commercial banks is lower than in other countries.

2.it is unlikely to deliver a combination of the reduction in excess reserves and a rise in lending on private financial institutions’ balance sheets: financial institutions cannot avoid this tax. If they intend to shift reserves to loans and holding securities in order to avoid the tax from the negative interest rate, excess reserves (a part of the monetary base) should fall, which the BoJ would not accept. As long as the target for monetary base expansion is maintained, the mostly likely outcome would be increases in both excess reserves and bank loans (or the holding of securities). On the other hand, in order for the monetary base to continue to expand, there have to exist sellers of government securities to the BoJ. A downward shift of the yield curve could cause financial institutions to refrain from selling government securities with higher associated capital gains to the BoJ.

3.the negative interest rate is, in effect, a tax on financial assets, and not the BoJ’s intention. This could lead to an opposite outcome to that of the initial intention, whereby the country encourages companies and households to engage in capital outflow.

It is that last bullet point which is most important because it leads us to the most disturbing topic of all for Japan - the risk that NIRP backfires and leads to another "China", where the local citizens rush to park their assets offshore, resulting in a slow at first then rapidly accelerating capital outflow.

This is how DB explains it:

if the negative interest rate continues for longer or goes deeper, commercial banks may have to set negative interest rates on deposits, which would expand not only the tax on commercial banks, but also on depositors (households and companies). This could lead to a ‘silent bank run’ via a shift of deposits to cash (banknotes), which in turn damages the sound banking system by enlarging the leakage of funds from the credit creation mechanism in the banking system.

That, and the capital outflow noted above. The good news is that Japan has a lot of physical banknotes to allow the NIRP bank run to continue for quite a while before collapsing the financial system.

In short, to grasp the worst possible consequence of Japan's panicked response to a rising Yen and plunging Nikkei look no further than China's unprecedented capital control attempts to stem the monetary outflow. Could it be that in its eagerness to devalue the Yen, the BOJ - like the PBOC - will be fighting tooth and nail in a few months to prop it up?

And if that wasn't cheerful enough, here is DB's conclusion which confirms that just a month after the Fed made a policy mistake, it is Japan's turn to follow in Yellen's shoes:

We wonder whether removing the last breakwater of the lower bound at a zero interest rate could end up being an expensive choice in the long run. The factor which pushed the BoJ down this path is probably its view that causality runs from economic activity to wages and then to prices, which we do not agree with. Our view is that causality runs from economic activity to prices and then to wages, and we do not share the argument that inflation does not rise because wages have not risen.

We believe the additional room that the BoJ has to lower rates on bank reserves is smaller than in other countries that have already introduced a negative interest rate, because of the lower net interest margin of commercial banks in Japan. However, if the BoJ pursues this path, we could reach the point of the trade-off of possibly damaging the soundness of the banking system.

By then, however, a Davos peer-pressured Kuroda will be long gone, and the doomed attempt to keep the system together will be someone else's problem. For now, all that matters is that stocks bounced... if only for a ahort time.

http://www.zerohedge.com/news/2016-01-30/pandoras-box-open-db-warns-japan-may-have-started-silent-bank-run

Pay attention to long-term debt cycle

Ray Dalio

Jan. 25, 2016

I have a controversial view that is based on my alternative economic template, and I feel a responsibility to share at this precarious time.

In brief, the Federal Reserve’s template, and that of most economists and market participants, reflects the business cycle.

Based on it, tightening should occur when a) the rate of growth in demand is greater than the rate of growth in capacity and b) the usage of capacity (as measured by indicators such as the GDP gap and the unemployment rate) is becoming high.

As a result, tightening now makes sense.

However, as I see it, there are two important cycles to pay attention to — the business cycle, or short-term debt cycle, and the debt supercycle, or long-term debt cycle.

We are seven years into the expansion phase of the business/short-term debt cycle — which typically lasts about eight to 10 years — and near the end of the expansion phase of a long-term debt cycle, which typically lasts about 50 to 75 years.

It is because of the long-term debt cycle dynamics that we are seeing global weakness and deflationary pressures that warrant global easing rather than tightening.

Since the dollar is the world’s most important currency, the Fed is the most important central bank for the world as well as the central bank for Americans, and as the risks are asymmetric on the downside, it is best for the world and for the US for the Fed not to tighten.

Since the long-term debt cycle issue is the biggest issue that separates my view from others, I’d like to briefly focus on its mechanics.

What I am contending is that there are limits to spending growth financed by a combination of debt and money. When these limits are reached, it marks the end of the upward phase of the long-term debt cycle. In 1935, this scenario was dubbed “pushing on a string”.

This scenario reflects the reduced ability of the world’s reserve currency central banks to be effective at easing when both interest can’t be lowered and risk premia are too low to have quantitative easing be effective.