News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

FINRA 4320 Short Sale Delivery Requirements

fourkids_9pets Share Friday, March 04, 2011 2:57:40 PM

Re: camper9 post# 1713 Post # of 7494

FINRA 4320. Short Sale Delivery Requirements

(a) If a participant of a registered clearing agency has a fail to deliver position at a registered clearing agency in a non-reporting threshold security for 13 consecutive settlement days, the participant shall immediately thereafter close out the fail to deliver position by purchasing securities of like kind and quantity.

(1) Provided, however, if a participant of a registered clearing agency has a fail to deliver position at a registered clearing agency for thirty-five consecutive settlement days in a non-reporting threshold security that was sold pursuant to SEC Rule 144, the participant shall immediately thereafter close out the fail to deliver position in the security by purchasing securities of like kind and quantity. The requirements in paragraph (b) shall apply to all such fails to deliver that are not closed out in conformance with this paragraph (a)(1).

(b) If a participant of a registered clearing agency has a fail to deliver position at a registered clearing agency in a non-reporting threshold security for 13 consecutive settlement days (or 35 consecutive settlement days if entitled to rely on paragraph (a)(1)), the participant and any broker or dealer for which it clears transactions, including any market maker that would otherwise be entitled to rely on the exception provided in paragraph (b)(2)(iii) of Rule 203 of SEC Regulation SHO, may not accept a short sale order in the non-reporting threshold security from another person, or effect a short sale in the non-reporting threshold security for its own account, without borrowing the security or entering into a bona-fide arrangement to borrow the security, until the participant closes out the fail to deliver position by purchasing securities of like kind and quantity and that purchase has cleared and settled at a registered clearing agency.

(c) If a participant of a registered clearing agency reasonably allocates a portion of a fail to deliver position to another registered broker or dealer for which it clears trades or for which it is responsible for settlement, based on such broker or dealer's short position, then the provisions of this Rule relating to such fail to deliver position shall apply to the portion of the fail to deliver position allocated to such registered broker or dealer, and not to the participant.

(d) A participant of a registered clearing agency shall not be deemed to have fulfilled the requirements of this Rule where the participant enters into an arrangement with another person to purchase securities as required by this Rule, and the participant knows or has reason to know that the other person will not deliver securities in settlement of the purchase.

(e) For the purposes of this Rule, the following terms shall have the meanings below:

(1) the term “market maker” has the same meaning as in Section 3(a)(38) of the Exchange Act.

(2) the term “non-reporting threshold security” means any equity security of an issuer that is not registered pursuant to Section 12 of the Exchange Act and for which the issuer is not required to file reports pursuant to Section 15(d) of the Exchange Act:

(A) for which there is an aggregate fail to deliver position for five consecutive settlement days at a registered clearing agency of 10,000 shares or more and for which on each settlement day during the five consecutive settlement day period, the reported last sale during normal market hours for the security on that settlement day that would value the aggregate fail to deliver position at $50,000 or more, provided that if there is no reported last sale on a particular settlement day, then the price used to value the position on such settlement day would be the previously reported last sale; and

(B) is included on a list published by FINRA.

A security shall cease to be a non-reporting threshold security if the aggregate fail to deliver position at a registered clearing agency does not meet or exceed either of the threshold tests specified in paragraph (e)(2)(A) of this Rule for five consecutive settlement days.

(3) the term “participant” means a participant as defined in Section 3(a)(24) of the Exchange Act, that is a FINRA member. The term “registered clearing agency” means a clearing agency, as defined in Section 3(a)(23)(A) of the Exchange Act, that is registered with the SEC pursuant to Section 17A of the Exchange Act.

(This is 3(a)(23)(A): The term "clearing agency" means any person who acts as an intermediary in making payments or deliveries or both in connection with transactions in securities or who provides facilities for comparison of data respecting the terms of settlement of securities transactions, to reduce the number of settlements of securities transactions, or for the allocation of securities settlement responsibilities. Such term also means any person, such as a securities depository, who (i) acts as a custodian of securities in connection with a system for the central handling of securities whereby all securities of a particular class or series of any issuer deposited within the system are treated as fungible and may be transferred, loaned, or pledged by bookkeeping entry without physical delivery of securities certificates, or (ii) otherwise permits or facilitates the settlement of securities transactions or the hypothecation or lending of securities without physical delivery of securities certificates.

(5) the term “settlement day” means any business day on which deliveries of securities and payments of money may be made through the facilities of a registered clearing agency.

==========================================

WHY IS FINRA 4320 SO EXCITING TO THE SECURITIES LAWYERS AND THE CORPORATIONS THAT HAVE SURVVIVED THESE NSS ATTACKS?

1) It finally addresses abusive naked short selling in non-reporting issuers. Up until now the regulators and SROs have found that the investors in development stage corporations somehow did not deserve the provision of investor protection.

2) Even though it is entitled “short sale delivery requirements” it covers the failures to deliver (FTDs) involved with intentionally mislabeled “long sales”. One way to bypass the newer short selling rules is to illegal mislabel your short sale as a “long sale” and just voluntarily fail to deliver the shares.

3) It affects FTDs held in “ex-clearing” because all (approximately 1,000) clearing firms that are “participants” of the NSCC/DTCC are indeed “registered clearing agencies” in and of themselves. (see 3(a)(23)(A) in the smaller print above.)

4) It addresses the FTDs of even market makers held at registered clearing agencies. The bona fide MM exemption from needing to pre-borrow or “locate” shares before making admittedly naked short sales is the main loophole being abused. THIS IS A VERY BIG DEAL.

5) It expressly forbids a crooked clearing firm from “crossing” failed to be delivered shares to a co-conspiring clearing firm in order to reset the 13-day clock. These illegal “wash sales” are pandemic.

6) There is no “grandfathering” in of old delivery failures held in illegal “ex-clearing arrangements” as these are still FTDs as nothing ever got delivered. The mere marking to market of the monetary value of failed delivery obligations has nothing whatsoever to do with making the “good form delivery” of the securities sold needed to accomplish the “settlement” of a trade.

7) In the abusive naked short selling world there are very, very bad guys and other semi-bad guys. The semi-bad guys will probably voluntarily cover their not so huge naked short positions BEFORE the really bad guys will have time to. They may even go net long after covering knowing that their bigger brother bad guys might be in deep doo-doo.

8) All of the crooks are not going to run willy-nilly tomorrow morning and cover BUT THOSE CORPORATIONS WITH IMMENSE NAKED SHORT POSITIONS THAT ARE ABLE TO PULL OFF SOME SORT OF LARGE CORPORATE ACCOMPLISHMENT WILL BE GREATLY BENEFITTED AND THEIR NAKED SHORT POSITIONS MIGHT RISE TO THE TOP OF THE “SHORT POSITIONS TO IMMEDIATELY COVER” LIST.

=============================================================

From HookMeister:

Doc, I've posted this question previously and haven't heard any response from anyone so I thought I'd ask you if you don't mind.

With respect to the NSS issue and the new regulations starting Monday, will MMs who already hold short positions prior to the new regulations be required to now comply with the new regs concerning their already existing short positions or will it only apply to new short positions going forward??

Hi HookMeister,

It’s actually the combination of all of the various new rules kicking in right now that will FINALLY make a difference as they all block some of the various loopholes in existence. The weak link has always been that the old rules only applied to delivery failures held at “registered clearing agencies” like the NSCC. The crooked clearing firms simply “paired off” outside of the NSCC, entered into illegal “ex-clearing arrangements” and forgave each other’s delivery obligations. Instead they chose to merely mark to market the monetary value of their failed delivery obligations and hide them in a “side pocket”. As a result, U.S. investors have no clue as to the damaged nature of the corporation they are investing in.

What the various “securities cops” were just reminded of is that these crooked clearing firms are indeed “registered clearing agencies” in and of themselves as per the ’34 Exchange Act. Up until now, nobody has been tallying the delivery failures hiding in these illegal “ex-clearing arrangements”. The new FINRA 4320 as of tomorrow mandates the buying in of 13 day old delivery failures of non-reporting issuers (like Medinah) IF MEDINAH’S NAME APPEARS ON THE FINRA THRESHOLD LIST. Medinah’s name is to appear on this list if both their delivery failures exceed 10,000 shares and are worth over $50,000 in the aggregate. Although Medinah’s approximately 1.3 billion shares of failed delivery failures are currently (@12-cents) worth approximately $156 million MEDINAH IS STILL NOT ON THE LIST. This is a testimony to the pandemic nature of these illegal “ex-clearing arrangements”

Why is this? FINRA leaves the tallying of the delivery failures up to the NSCC. The NSCC only tallies the delivery failures officially held at the NSCC which the crooks now avoid like the plague as the hiding spot for their delivery failures. The NSCC management, which operates as an “SRO” or “self-regulatory organization”, insanely holds that the delivery failures held by their “participants/bosses” outside of the NSCC in “ex-clearing arrangements” are of a “contractual” nature which is none of their business.

Wait a minute, the SEC has said that the SROs like FINRA and the NSCC are to provide “the first line of defense against market abuses”. Congress in Section 17A of the’34 Exchange Act mandated that its parent the DTCC “promptly settle” all securities transactions. This means that the sellers of securities must promptly deliver that which they sold on or near T+3. Illegal “ex-clearing arrangements” intentionally circumvent the “prompt settlement” of securities transactions. By definition, an SRO like the NSCC is mandated to “draft and enforce rules and regulations and to monitor the “BUSINESS CONDUCT” of its co-owning “participants.”

How can the management of an SRO like the NSCC with that SRO mandate as well as that congressional mandate as well as acting as the party acting in the capacity of providing “the first line of defense against market abuses” claim that it has no authority to address the efforts of their bosses to intentionally circumvent the “prompt settlement” of securities transactions? How can you claim to be “powerless” to follow a congressional mandate?

Forced buy-ins of 13-day old delivery failures are critical as they represent the only source of meaningful DETERRENCE to these crimes and they are the only treatment available when the sellers of securities absolutely refuse to deliver that which they sell. With FINRA 4320 in effect, non-reporting issuers are FINALLY afforded protection via mandated buy-ins but only if that 10,000 shares and $50,000 worth of delivery failures metric is reached. If the NSCC management continues to refuse to tally the delivery failures held in these “regulated clearing agencies” known as “clearing firms” in these “ex-clearing arrangements” in order to keep their bosses from being bought-in then the issue of a “securities cop” with all of these various mandates acting to directly aid and abet as well as cover up these frauds comes front and center.

The gist of it is that the mere marking to market of the monetary value of a failed delivery obligation has nothing to do whatsoever with the congressionally mandated “prompt settlement” of a securities transaction. In fact, although from a distance it serves to lend an air of legitimacy it actually is the ideal COVER UP FRAUD used to mask the fact that “prompt settlement” is not occurring.

Most securities lawyers I work with predict that FINRA 4320 will force the NSCC management to pull a “Pontius Pilate” and wash its hands of this aiding and abetting role and providing this cover up fraud and buy-in these previously unaddressed delivery failures which they theoretically had no idea existed. No doubt they will say WE ARE SHOCKED, SHOCKED and shame on you abusive bosses of ours. We had no idea these crimes were being committed on our watch.

The concept of a “securities cop” like the NSCC intentionally MANIPULATING downwards the metric needing to be reached so that investor protection is provided in order to look after the financial interests of its misbehaving bosses is unconscionable and the investing public will not tolerate these thefts any longer.

source

original post from camper9

POST

=============================================================

1) WHY DO ABUSIVE NAKED SHORT SELLERS NEVER, NEVER, NEVER VOLUNTARILY COVER THEIR NAKED SHORT POSITIONS?

ANSWER:

A) They can easily gain access to the funds of uneducated investors without ever delivering anything to them. All they’re asked by the NSCC to do is to collateralize the monetary value of the failed delivery obligation on a marked to market basis. As the readily sellable share price depressing “security entitlements” resulting from all of these intentional delivery failures pile up the share price and therefore the collat. requirements drop allowing the investor’s money to flow to the party refusing to deliver that which they sold.

B) Until 4320 came along there was no deterrence, no forced buy-ins, no perp walks and no meaningful fines levied.

C) There’s a huge bonus available for bankrupting a company i.e. no taxable capital gains.

D) Often they run up so high of a naked short position that they can’t even stop their daily NSS-ing lest the share price go up and the collateralization requirements of the immense uncovered position become unbearable.

E) This is their turf and they know the loopholes better than uninformed investors (excepting of course the average Medinah investor that will soon be omniscient in these matters or die trying.)

F) These crooks have high paid lobbyists that keep convincing the politicians that the injecting of liquidity by even abusive MMs is critical to allow our markets to function smoothly.

G) The delivery failures were invisible to the investing public and the “securities cops” until 4320 came along as well as the new DTCC “obligation warehouses”.

2) What is the direct result of this phenomenon?

A) Companies that have been under attack for as many as 14 years are going to have accumulated enormous open naked short positions if the crooks have failed to bankrupt them before the world learned that they were MISDIAGNOSED as “scammy pump and dumps”.

3) What is the biggest benefit of 4320 once a company under attack gets onto the “nonreporting threshold list”?

A) Mandated buy-ins on day 13 by a party (clearing firm) that doesn’t particularly care what he pays for the stock because he gets to hand the bill to the guilty party.

4) What is the main truly meaningful deterrent to committing these crimes?

A) The fear of being bought-in at an inopportune time by a party that doesn’t care what he pays.

5) What is the ONLY cure available when the seller of securities absolutely refuses to EVER deliver the securities that it sold after contracting to deliver them by T+3?

A) Mandated buy-in.

(from www.theminingplay.com, posted by Brecciaboy)

==============================================================

A DIFFERENT WAY OF LEARNING THE HEINOUS NATURE OF “EX-CLEARING” CRIMES

Your brokerage firm uses a clearing firm to “clear” the trades you make. Corrupt clearing firms have a metaphorical backroom known (metaphorically) as a “sponsor table” room. When you buy Medinah shares let’s pretend you pay with a bucket full of silver dollars. If the clearing firm of the MM that sold you shares refuses to deliver that which you purchased your bucket of coins goes into your clearing firm’s “sponsor table” firm. Your coins are dumped onto the table that the clearing firm of the MM “sponsored”.

These “sponsor tables” are unique in that that have netting around them. The floor of the “sponsor table” room is unique in that it tips as share prices drop. Since nothing was delivered your coins exist in a state of limbo UNTIL delivery occurs if it ever occurs. As the share price predictably tanks and the floor tips from naked short sales which open up more and more “sponsor tables” the clearing firm of the crooked MM as well as the crooked MM itself get to collect all of your coins that slipped into the netting EVEN THOUGH THAT WHICH THE MM SOLD NEVER EVEN EXISTED. Your coins “collateralize” the debt of the crooked MM.

The interest that your coins earn is split by your clearing firm and the crooked MM IF AND ONLY IF YOUR CLEARING FIRM REFUSES TO YELL AT THE MM AND ASK HIM TO DELIVER THAT WHICH HE SOLD TO HIS CLIENT i.e. you. In other words if he is willing to throw your financial interests under the bus he gets to share in the interest earnings. “Sponsoring” tables is easy, all you have to do is to refuse to deliver the securities that you sell.

Every night the crooked MM that sold you nonexistent shares gets to go into the “sponsor table” room and collect whatever coins fell into the netting from all of the tables he sponsored which might be in the thousands or tens of thousands after 14 years. If the crooked MM “recruits” other MMs and various hedge funds to sponsor tables the coins will flow into the netting very rapidly FROM ALL “SPONSORED” TABLES as the share price plummets. If they succeed in bankrupting the company they targeted to destroy all of your coins will be gone and in the possession of the crooked MM despite the fact that he still hasn’t delivered anything and what he sold to you doesn’t even exist.

After you bought the shares you got a monthly brokerage statement that “implied” that your clearing firm was “holding long” your shares. You probably assumed they were in some type of vault at the DTC depository. Two corrupt clearing firms can easily “pair up” outside of the NSCC (ex-clearing) and offer each other and each other’s clients the use of their “sponsor table” rooms. This amounts to allowing a bunch of crooks to sell a given clearing firm’s clients fake shares and never deliver them if and only if the other clearing firm extends the same courtesy. The NSCC management mandated to regulate the “business conduct” of its “participating clearing firms” that co-own the NSCC holds that what their bosses do outside of the NSCC proper is none of their business.

(from www.theminingplay.com, posted by Brecciaboy)

=================================================================

My most popular question du jour has to do with historically when do the naked short sellers typically cover. The answer is usually never or about as often as a tiny junior explorer makes a discovery like that at Lipangue which is next to never.

First of all, you have to qualify which type of short sellers you’re referring to-the jet skiers or the aircraft carriers.

The jet skiers are the smaller market makers, broker/dealers, hedge funds, prime brokers, etc. that might be short only perhaps 30 million shares. They have a lesser ability to collateralize their naked short position as the PPS advances. They’ll typically cover first but they’re actually in the catbird seat because they can cover and then go net long if they know that an aircraft carrier that’s short maybe 400 million shares is in deep doo-doo. When there’s blood in the water on Wall Street all bets are off.

Aircraft carriers can’t turn on a dime and cover and go net long like the jet skiers can. At this point in the battle the jet skiers are ticked off at the aircraft carriers because they were probably “recruited” by the aircraft carriers to help finish off this “scammy” PinkSheet piece of gradu that turned out to be a little feistier than anticipated.

One thing about abusive naked short sellers is that they have discipline. They’ll cover when they know their goose is cooked. When you’re naked short thousands of development stage U.S. corporations the aircraft carriers only have “X” amount of net capital reserves to spread around to collateralize these “open positions”. If you “accidentally” ran up an immense naked short position but failed to kill your target you’re typically left with 3 options to still win the war. You can do whatever is needed to get your target delisted, bankrupt them or get their registration revoked. If Medinah lands a generous JV arrangement then all 3 of those options are gone.

Since abusive naked short sellers never really know how many other crooks are naked short the target then it sometimes becomes a race to beat the others to cover. Oftentimes the jet skiers have no choice in covering because the clearing firm they operate through starts sweating bullets because it is eventually on the hook for the failed delivery obligation. If the jet skiers do not supply much order flow to the clearing firm then they’re apt to be thrown under the bus. Clearing agreements always spell out that the clearing firm can buy-in those “open positions” whenever they so choose. Since the monetary value of all open naked short positions needs to be collateralized on a daily marked to market basis it’s usually financial constraints that lead to the covering.

When the goose is indeed cooked, a powerful option is lost to the crooks. When under duress the crooks can always transfer a naked short position “across the street” like a hot potato until the heat is off. Then it’s transferred back by another illegal “wash sale”. When the goose is cooked and everybody knows it there won’t be any willing co-conspirators to accept that transfer. The new FINRA Rule 4320 kicking in soon looks really nice. For the first time the CLEARING FIRM of the bad guys is handcuffed from misbehaving.

(from www.theminingplay.com, posted by Brecciaboy)

=================================================================

IS NSS TECHNICALLY “UNLAWFUL” OR “ILLEGAL”?

In regards to issues of “unlawfulness” or “illegalities” in the securities markets one has to go to the all encompassing anti-fraud rule within the ‘34 Exchange Act namely Rule 10b-5.

Rule 10b-5 -- Employment of Manipulative and Deceptive Devices

It shall be unlawful for any person, directly or indirectly, by the use of any means or instrumentality of interstate commerce, or of the mails or of any facility of any national securities exchange,

a. To employ any device, scheme, or artifice to defraud,

b. To make any untrue statement of a material fact or to omit to state a material fact necessary in order to make the statements made, in the light of the circumstances under which they were made, not misleading, or

c. To engage in any act, practice, or course of business which operates or would operate as a fraud or deceit upon any person,

in connection with the purchase or sale of any security.

=============================================================

The first concept to keep straight is that a technically “unlawful” act has nothing to do with whether or not that act is regularly prosecuted by the authorities. The DOJ or FBI usually need a referral from the SEC before they come on the scene. When it comes to abusive naked short selling crimes the SEC, FINRA, and the DTC and NSCC subdivisions of the DTCC are squarely in “cover up” mode. The last folks the regulators and the SROs want sniffing around is the DOJ, FBI or the FFETF [Financial Fraud Enforcement Task Force] with the power to put people in jail.

IS WHAT IS DESCRIBED BELOW AN “UNLAWFUL” SCHEME TO DEFRAUD DONE IN CONNECTION WITH THE SALE OF A SECURITY?

1) A corrupt MM illegally accesses the universally abused bona fide MM exemption from needing to effect a pre-borrow or “locate” before making admittedly naked short sales. He has no intent to ever deliver that which he is selling. Note that a truly bona fide MM that legally accesses that exemption would cover that naked short position on the very next downtick in share prices when the injection of buy-side liquidity is needed.

2) He sells nonexistent shares to a buyer but refuses to either deliver them or buy them back when the share price drops.

3) The buyer’s account is credited with a readily sellable share price depressing “security entitlement” as per UCC Article 8. Because of this the buyer is blindfolded to the deceit/fraud.

4) As these “refusals to deliver” and the “security entitlements” they spawn accumulate invisibly in the share structure of the corporation targeted for destruction the share price predictably tanks because the “supply” of that which must be treated as being readily sellable (shares and/or “security entitlements”) is knowingly and intentionally being manipulated upwards (scienter).

5) Since the NSCC only mandates that its “participants” collateralize the monetary value of failed delivery obligations on a daily marked to market basis as the share price drops (gets MANIPULATED downwards-a crime) so too do the collateralization requirements.

6) This results in the funds of the investor flowing to the MM that illegally accessed the bona fide MM exemption but refused to cover his naked short position on the very next downtick after the naked short sale was made as a truly bona fide MM would have. This flow of investor funds occurs despite the fact that what was sold never existed and never got delivered. With this being the NSCC policy, imagine the checks and balances that would be in place in a clearance and settlement system with integrity should abusive participants access this gold-plated invitation to defraud investors. The alarm bells would start sounding on about T+6 or so and forced buy-ins would rapidly occur.

Quite clearly this is an “unlawful scheme to defraud investors done in connection with the purchase and sale of a security”.

WHAT IS THE “SCHEME” TO DEFRAUD?

The “scheme” is to be able to sell nonexistent securities via illegally accessing the bona fide MM exemption and avoid the costs or potential unavailability associated with making legitimate pre-borrows in order to gain access to the funds of the investor without ever having to deliver the nonexistent shares you sold.

WAS THE BUYER OF THE SHARES DECEIVED OR DEFRAUDED?

The buyer was under the impression that he was buying and getting delivery of SEC-registered units of equity ownership (“shares”) in a corporation of which there are a finite amount “outstanding” as indicated on that company’s financials. He was deceived. He thought he was acquiring a voting power equal to the amount of shares he purchased divided by the number of shares advertised as being “outstanding” in the company’s 10-K. He didn’t get this. He thought he would earn preferential tax treatment for all of his shares on any “qualified dividend” the company issued. He will not get this as per IRS policies limiting the tax preferential treatment only to the number of shares legally “outstanding”.

He thought that the amount of shares readily sellable at any given time were just the number of shares “outstanding” plus any shares borrowed for the sake of legitimate short sales and subsequently sold. He was wrong. He thought that in the case of insolvency he had a valid claim to the percentage of assets calculated by dividing the number of shares “outstanding” by the number he purchased (dissolution rights). He was wrong. He thought that there were no parties on Wall Street heavily financially incentivized to bankrupt this company. He was mistaken. He thought that the DTCC was going to follow its congressional mandate to make sure that his trade would “promptly settle” i.e. buy-in the delivery failure on perhaps T+6 when it became obvious that the seller had no intent to deliver that which he sold. Again, he was deceived/defrauded.

AS PER SECTION “C” OF 10B-5 DOES THIS “COURSE OF BUSINESS…OPERATE AS A FRAUD OR DECEIT UPON ANY PERSON IN CONNECTION WITH THE PURCHASE OF A SECURITY”?

Of course it does.

WALL STREET’S REBUTTAL: STEALING THE FUNDS OF INVESTORS IN DEVELOPMENT STAGE U.S. CORPORATION ACTUALLY HAS ALTRUISTIC UNDERPINNINGS.

FACT: The most readily available supply of shares to borrow and then legally short sell come from margin accounts and institutional shareholders trying to earn a little margin interest to increase their “alpha”.

FACT: The nonmarginable “penny stocks” typically attacked do not have many if any shares in either location and are thus difficult or extremely expensive to legally short sell.

FACT: The best way to circumvent this reality is to work with crooked MMs willing to illegally access their bona fide MM exemption. Access is typically attainable by directing cash generating order flow in the direction of a willing MM.

THE MINDSET OF SOME ABUSIVE NAKED SHORT SELLERS: The destruction of certain U.S. corporations and the stealing of the funds of investors in companies that we abusive naked short sellers deem (in our infinite wisdom) to be “scams” is actually a good way to “hasten the demise” of these “scammy pump and dumps” so that future investors don’t get swindled by these scamsters. In other words, stealing from investors is a good way to address assumed stealing from investors and perpetrating a heinous form of securities fraud is the proper way to address suspected frauds.

The question arises; why not just file a complaint with the SEC in order to perform your “shareholder advocate” role.

Possible answer: That doesn’t pay as well.

ISSUES REGARDING SECTION b OF 10b-5 AND THOS MANDATED TO KEEP TALLIES OF DELIVERY FAILURES

Section b deals with facts of a “material” nature. It deems it unlawful to EITHER “make any untrue statement of a material fact or to omit to state a material fact necessary in order to make the statements made, in the light of the circumstances under which they were made, not misleading in connection with the purchase or sale of any security”.

In connection with the “full disclosure” of all “material” facts to prospective investors what fact could possibly be more “material” to the prognosis for the success of a potential investment then the presence of an enormous amount of share price depressing “security entitlements” poisoning the share structure and prognosis for success of a corporation?

Note that Section b makes it unlawful to omit to state a material fact. Who is or should be in possession of the combined number of delivery failures residing in either the DTCC or in “ex-clearing arrangements”? The answer is BOTH the NSCC as the party keeping the tally as well as FINRA mandated to receive the reports of the NSCC and construct and maintain the “threshold lists”.

The question arises as to how these 2 SROs mandated to act as “the first line of defense against market abuses” (as per the SEC) and also acting with the mandate to create and enforce laws associated with the “business conduct” of its “participants” in the case of the NSCC and “members” in the case of FINRA can refuse to keep this most “material” of all information secret from prospective investors.

The answer is simple, due to the levels of historical abuses our SROs and regulators are stuck in “cover up” mode and by definition you cannot be acting in robust investor protection mode and cover up mode simultaneously. What is at stake here is millions of U.S. citizens learning that many of the investments they have made throughout history in development stage corporations never had a chance to succeed. Instead the fates of these corporations, the jobs they could have provided and the investments made therein were thrown under the bus in exchange for some type of corrupt vigilante type service.

It is extremely obvious that in order to move from cover up mode where investors have no clue how damaged the corporation is that they are buying shares of back into robust investor protection mode an embarrassingly obvious event must occur. The sellers of nonexistent shares caught gaming the system must be FORCED to go into their wallet, retrieve the stolen money and buy back and deliver the shares they promised to deliver on T+3 but refused to.

The obviousness of this only solution and the refusal to demand it up until now has forever tarnished the integrity of our markets. Once the share price depressing “security entitlements” are forcibly removed from these corporate share structures then an unmanipulated “supply” variable can finally interact with an unmanipulated “demand” variable to “discover” an unmanipulated share price through the price discovery process. What could possibly be a more obvious remedy to finally reroute our SROs and regulators away from cover up mode and back into investor protection mode.

SUMMARY

Relatively defenseless nonmarginable “penny stocks” are the easiest for short sellers to bankrupt. The problem is that they are the most difficult to LEGALLY short sell since very few shares are held in margin accounts or by institutions willing to loan them out. Short sellers not afraid to act outside of the securities laws can easily find corrupt MMs to ILLEGALLY “rent out” space under their “bona fide MM” umbrella of immunity from having to pre-borrow or make a “locate” before making naked short sales. Avoiding either expensive or unavailable “pre-borrows” is often the inducement to break the law. The corrupt MMs are rewarded for their breaking of the law by cash generating order flow from the criminals refusing to play by the rules.

The added expense and difficulty to legally short sell development stage securities in a sense should add protection to these corporations that are relatively defenseless during their particular stage of development in these “corporate incubators” known as the PinkSheets and the OTCBB. It is also true that these circumstances could foster and promote “pump and dumps”. The concept that abusive naked short sellers justify stealing the funds of today’s investors in order to hasten the demise of corporations in order to protect future investors in that (allegedly) “scammy” corporation from being defrauded by corrupt management teams represents a pathological mindset beyond comprehension. At the very least, these criminals should carry some form of billion dollar “malpractice” insurance when their diagnosis that “X” U.S. corporation is a “scam” proves to be unfounded.

(from www.theminingplay.com, posted by Brecciaboy) Emphasis above is mine.

============================================================

thanks to camper9 .. brecciaboy and the miningplay.com for

the above posts .. wanted to combine all of the posts into

one for ease of access and reading on the NSS board

thanks to greg for the request :)

==

4kids

all jmo

BMFL<OD

next week(s) is here

I will get back to you on that!

BMFL<OD

next week(s) is here

CELLAR BOXING SERIES is a MUST READ

for all new investors!!!

dehydratedman Share Monday, August 02, 2010 12:24:34 PM

Re: None Post # of 7494

CELLAR BOXING SERIES is a MUST READ for all new investors!!!

PART 1 http://investorshub.advfn.com/boards/read_msg.aspx?message_id=52672689

PART 2 http://investorshub.advfn.com/boards/read_msg.aspx?message_id=52664836

PART 3 http://investorshub.advfn.com/boards/read_msg.aspx?message_id=52664935

Thanks for this education...it was a great find!!!

GeneO

BMFL<OD

next week(s) is here

Thank You srm4u

Good to see some of the old timers!

Thank you for all that you have done for the shareholders in the past!

BMFL<OD

next week(s) is here

Thank you for your kind words!

BMFL<OD

next week(s) is here

Doesn't bother me Bull Finch, I can always go find another dormant board to use for storage or what ever.

As for boards being hijacked by nefarious forces I know what you mean. I've seen it before with some of the Q stocks. I appreciate and sympathize with the situation. It sucks.

I say if you can use the WAGI board as a neutral landing zone for something else that's getting manipulated, by all means go for it !

Hate to say it but as for some of the "family tree" ala Hunt Gold et al, you mentioned, they seem to be a sorry bunch of losers.

No personal complaints on Hunt Gold since I doubled my money (and then some) on them in the rah rah run up a couple years ago but I saw it was a scam and bailed.

With so many primo opportunities out there in junior miners right now I don't know why anyone would keep putting the spurs to the dead horses you mentioned, but hey, to each their own.

Good luck with your (ad)ventures and I cede my "quiet place" (good one!) to you. Hope you guys make a pile of cash.

cork

I'm sorry your quiet place is no longer!

WAGI is ours and WE are taking it back before the HYENAS do.

You are more then welcome to stay and join us. I see you are a Gold man and so are we, we have at least that in common.

BMFL<OD

next week(s) is here

I repeat there are no WAGI shares!

Thank You for reminding us of that. WAGI is no longer, shares from WAGI became GWGO. Shares from GWGO became FFGO. FFGO shares become HGLC and soon the remainder of the FFGO share will become NMGL A & B perferred shares.

As for some sort of a scheme, again we are staying one step ahead of HYENAS. We also took control of the GWGO board today and took control of the HGLC board on 10/25/11. That is all nothing more.

When I refer to WE above I am talking about shareholders, and some of us have been here since the WAGI days that's why we are here at the Grandfather.

"There are no WAGI shares to benefit from any remuneration or dividends even if they are due.

I'd like a straight answer as to what is going on with this board.

Posting a bunch of Press Releases from 8 or 9 years ago about a dead dead company smacks of some sort of a scheme.

I intend to report it if I don't get a satisfactory answer, so quit screwing around trying to be cute and come clean with it.

Say what is going on or else."~the cork

BMFL<OD

next week(s) is here

Thanks for the invitation, Bull Finch! SevenTenEleven, I think we are on the radar (if we weren't already) and maybe this FFGO filing suspension was a necessary first step or an "easy" "low hanging fruit" to pluck compared to unraveling years of missing, imcomplete Fails To Deliver going back to 08-09? 07,06,05,04???

There are no WAGI shares to benefit from any remuneration or dividends even if they are due.

I'd like a straight answer as to what is going on with this board.

Posting a bunch of Press Releases from 8 or 9 years ago about a dead dead company smacks of some sort of a scheme.

I intend to report it if I don't get a satisfactory answer, so quit screwing around trying to be cute and come clean with it.

Say what is going on or else.

In Fight Against Securities Fraud,

S.E.C. Sends Wrong Signal

basserdan Share Thursday, October 27, 2011 3:26:00 PM

Re: None Post # of 7494

In Fight Against Securities Fraud, S.E.C. Sends Wrong Signal

By Jesse Eisenger,

PROPUBLICA

October 26, 2011, 12:50 pm

Back when the Financial Crisis Inquiry Commission was doing its work, I would check in periodically with someone who worked there to find out how it was going.

“Good news!” my source would joke. “We got the guy who caused it.”

That is the way I felt last week when the Securities and Exchange Commission announced that it had agreed to a measly $285 million settlement with Citigroup over the bank having misled its own customers in selling an investment it created out of mortgage securities as the housing market was beginning its collapse.

In addition, the S.E.C. accused one person — a low-level banker. Hooray, we finally got the guy who caused the financial crisis! The Occupy Wall Street protestors can now go home.

After years of lengthy investigations into collateralized debt obligations, the mortgage securities at the heart of the financial crisis, the S.E.C. has brought civil actions against only two small-time bankers. But compared with the Justice Department, the S.E.C. is the second coming of Eliot Ness. No major investment banker has been brought up on criminal charges stemming from the financial crisis.

To understand why that is so pathetic and — worse — corrupting, we need to briefly review what went on in C.D.O.’s in the years before the crisis. By 2006, legions of Wall Street bankers had turned C.D.O.’s into vehicles for their own personal enrichment, at the expense of their customers.

These bankers brought in savvy (and cynical) investors to buy pieces of the deals that they could not sell. These investors bet against the deals. Worse, they skewed the deals by exercising influence over what securities went into the C.D.O.’s, and they pushed for the worst possible stuff to be included.

The investment banks did not disclose any of this to the investors on the other side of the deals, or if they did, they slipped a vague, legalistic disclosure sentence into the middle of hundreds of pages of dense documentation. In the case brought last week, Citigroup was selling the deal, called Class V Funding III, while its own traders were filling it up with garbage and betting against it.

By the S.E.C.’s own investigations of and settlements with Goldman Sachs, JPMorgan Chase and Citigroup, and by reporting like my ProPublica work with Jake Bernstein and early stories by The Wall Street Journal, we know that these breaches were anything but isolated. This was the Wall Street business model. (Goldman, JPMorgan and Citigroup were all able to settle without admitting or denying anything, which, of course, is part of the problem.)

Neither the Citigroup settlement nor any of the others come close to matching the profits and bonuses that these banks generated in making these deals. And low-level bankers did not, and could not, act alone. They were not rogues, hiding things from their bosses.

Last week’s S.E.C. complaint makes clear that the low-level Citigroup banker that it sued, Brian H. Stoker, had multiple conversations with his superiors about the details of Class V. At one point, Mr. Stoker’s boss pressed him to make sure that their group got “credit” for the profits on the short that was made by another group at the bank.

Pause, and think about that. The boss was looking for credit, but as far as the S.E.C. was concerned, he got no blame.

The S.E.C. did not respond to a request for comment, so we are left to wonder what explains its failure to reckon adequately with the pervasive problems. Contrary to expectations, the embattled and oft-assailed agency has done almost everything right with structured finance investigations, taking aim at abuses related to C.D.O.’s and other complex deals.

The S.E.C. has also devoted adequate resources to the issue. It put together a special task force on structured finance, sending the proper signal of the agency’s priorities both internally and externally. The task force is staffed by bright people, an invigorating mix of young go-getters and experienced hands. Those people have understood for years what was wrong with the C.D.O. business on Wall Street.

O.K., so what is it? Risk aversion.

Based on the major cases the S.E.C. has brought, a pattern has emerged. It is making one settlement per firm and concentrating on only the safest, most airtight cases. The agency’s yardstick seems to be, who wrote the stupidest e-mail? Mr. Stoker of Citigroup wrote an incriminating e-mail that recommended keeping one crucial participant in the dark. Goldman’s Fabrice Tourre, the other functionary the agency has sued, wrote dumb things to his girlfriend.

But the S.E.C is not the G-mail G-man. It is the securities police. Imprudent e-mailing is not the only way to commit securities fraud.

Maybe the agency hopes that private litigation will take up the slack. It cannot investigate and wring a prosecution or settlement out of every corrupt deal. Instead, it has long aimed to plant a flag and let private litigants take care of the rest.

But private litigation has failed. One problem is that the defrauded institutions often committed their own sins. In a monstrous daisy chain, C.D.O.’s bought pieces of other C.D.O.’s. These investments were run by management companies. They might have been the victim in one C.D.O., but complicit in the predations of another.

Other victims, like large financial institutions and money managers, do not want to sue because it could reveal their own compromised behavior. Or they would be revealing to customers that they had simply been taken by other, smarter bankers. You cannot very well convince people that you are a good steward of their money if you are simultaneously complaining that the Wall Street sharpies fleeced you.

And private litigation has changed in the last decade and a half. The Private Securities Litigation Reform Act of 1995, which was meant to make class-action lawsuits harder to bring, has had a spillover effect beyond those cases, according to plaintiffs’ lawyers. Courts have raised the bar for securities fraud cases, even where the act does not apply. The rules color how judges look at financial disputes.

So the S.E.C. has the wrong approach.

This is a matter of will and leadership. Its chairwoman, Mary L. Schapiro, while deserving credit for pushing investigations of structured investments, is sending the signal that she does not want to lose. Her agency is meekly willing to get token settlements when the situation calls for Old Testament justice.

Someday, the S.E.C. will have to go up against a top executive who has resources to fight, and who was too sophisticated to put anything rash in writing. This seems to be our fate: our bankers took reckless risks, but our regulators take none.

http://dealbook.nytimes.com/2011/10/26/in-fight-against-securities-fraud-s-e-c-sends-wrong-signal/?ref=business

BMFL<OD

next week(s) is here

Help us get to 1,000,000

fourkids_9pets Share Thursday, October 27, 2011 9:25:29 AM

Re: fourkids_9pets post# 7396 Post # of 7494

794,616 have joined. Help us get to 1,000,000

http://www.avaaz.org/en/the_world_vs_wall_st/?fp

slowly but surely ..

===

original link courtesy of alanc

==

4kids

all jmo

About West Africa Gold Inc.:

West Africa Gold (www.westafricagold.com) is an aggressive gold

exploration company that has acquired certain rights to mine for minerals,

primarily gold, in various regions of the Republic of Mali, which is located

in West Africa. Their outstanding exploration and operational management team

has in excess of 60 years of professional geological experience, and has

extensive familiarity on a local level in respect of mining in Africa. The

team is highly educated, including PhDs, and all have recognizably solid

reputations throughout the mining industry. The company also recently

announced and executed a 10-for-1 forward stock split to improve trading

liquidity and to attract smaller investors.

West Africa Gold currently has five projects underway. They are Toubikoto

(Gold), Manianguinti (Gold), In Darset (Gold, Base Metals), Anefis (Gold, Base

Metals), and Touban (Nickel, Copper, pge's). The five projects are diversely

located throughout Mali, and aggregately cover an impressive 1000 square

kilometers. Since 2001, Mali has been the 3rd largest gold-producing country

in Africa, trailing only South Africa and Ghana. Most importantly, to West

Africa Gold, is the political stability and harmony enjoyed by both the Malian

people and foreign Mining companies operating in Mali. Gold accounts for

approximately 90% of Mali's total mineral exports, and in excess of 20% of all

exports. Malian gold production is expected to almost double to 37% when

several new projects go into full production. Mali has been extensively

evaluated and it has been concluded that the country has an incredible

350 tons of recoverable gold, and is widely recognized as having enormous

potential for abundant gold extraction. West Africa Gold is well positioned

to reap great benefits from its Malian properties. The Independent Geological

Evaluation of West Africa Gold's properties are that they may contain an

Inferred Geological Resource of up to 3,000,000 ounces of gold. Extremely

high Values of Zinc and Copper have also been recorded. Mali is also known

for its low extraction costs, so certain expenses will be controlled.

Considering the amount of gold in Mali, as well as the sheer size and

professionally evaluated potential of its properties, West Africa Gold has a

very bright future ahead of it. Its Advisory Committee will consist of

renowned mining and geological experts. This highly experienced and dedicated

team will have the local expertise so as to be familiar with Mining operations

in Mali. West Africa Gold is debt free and is in the final stages of

preparation to raise an additional US$5 million in additional funding. The

company plans to use this money to continue to explore and create additional

value to its current properties, and to identify and secure additional Gold

Mining Properties. West Africa Gold has many positive factors that weigh

heavily in its favor, and with Gold holding its own at around the US$380/oz

level, it continues to be a company with enormous potential.

Statements contained in this press release, which are not historical

facts, are forward-looking statements as that term is defined in the Private

Securities Litigation Reform Act of 1995. These forward-looking statements

are based largely on the Company's expectations and are subject to a number of

risks and uncertainties beyond the Company's control, including but not

limited to economic, competitive and other factors affecting the Company's

operations, management team effectiveness, expansion strategies, available

financing, market prices and recovery costs, government regulations involving

the Company, facts and events not known at the time of this release, and other

factors discussed in the Company's filings with the Securities and Exchange

Commission.

These statements are not guarantees of future performance and readers are

cautioned not to place undue reliance on these forward-looking statements,

which speak only as of the date of this release. The Company undertakes no

obligation to update publicly any forward-looking statements.

BMFL<OD

next week(s) is here

"Naked" Short Selling

In a "naked" short sale, the seller does not borrow or arrange to borrow the securities in time to make delivery to the buyer within the standard three-day settlement period. As a result, the seller fails to deliver securities to the buyer when delivery is due (known as a "failure to deliver" or "fail").

Failures to deliver may result from either a short or a long sale. There may be legitimate reasons for a failure to deliver. For example, human or mechanical errors or processing delays can result from transferring securities in physical certificate rather than book-entry form, thus causing a failure to deliver on a long sale within the normal three-day settlement period. A fail may also result from naked short selling. For example, market makers who sell short thinly traded, illiquid stock in response to customer demand may encounter difficulty in obtaining securities when the time for delivery arrives.

Naked short selling is not necessarily a violation of the federal securities laws or the Commission's rules. Indeed, in certain circumstances, naked short selling contributes to market liquidity. For example, broker-dealers that make a market in a security generally stand ready to buy and sell the security on a regular and continuous basis at a publicly quoted price, even when there are no other buyers or sellers. Thus, market makers must sell a security to a buyer even when there are temporary shortages of that security available in the market. This may occur, for example, if there is a sudden surge in buying interest in that security, or if few investors are selling the security at that time. Because it may take a market maker considerable time to purchase or arrange to borrow the security, a market maker engaged in bona fide market making, particularly in a fast-moving market, may need to sell the security short without having arranged to borrow shares. This is especially true for market makers in thinly traded, illiquid stocks such as securities quoted on the OTC Bulletin Board, 5 as there may be few shares available to purchase or borrow at a given time.

What is a Threshold Security? Threshold securities are equity securities that have an aggregate fail to deliver position for:

- Five consecutive settlement days at a registered clearing agency (e.g., National Securities Clearing Corporation (NSCC));

- Totaling 10,000 shares or more; and

- Equal to at least 0.5% of the issuer's total shares outstanding.

Threshold securities only include issuers registered or required to file reports with the Commission ("reporting companies"). Therefore, securities of issuers that are not registered or required to file reports with the Commission, which includes the majority of issuers on the Pink Sheets,18 cannot be threshold securities. This is because the SROs need to look to the total outstanding shares of the issuer in order to calculate whether or not the securities meet the definition of a "threshold security." For non-reporting companies, reliable information on total outstanding shares is difficult to determine.

Regulation SHO

Compliance with Regulation SHO began on January 3, 2005. Regulation SHO was adopted to update short sale regulation in light of numerous market developments since short sale regulation was first adopted in 1938. Some of the goals of Regulation SHO include:

Establishing uniform "locate" and "close-out" requirements in order to address problems associated with failures to deliver, including potentially abusive "naked" short selling.

Locate Requirement: Regulation SHO requires a broker-dealer to have reasonable grounds to believe that the security can be borrowed so that it can be delivered on the date delivery is due before effecting a short sale order in any equity security.6 This "locate" must be made and documented prior to effecting the short sale.

"Close-out" Requirement: Regulation SHO imposes additional delivery requirements on broker-dealers for securities in which there are a relatively substantial number of extended delivery failures at a registered clearing agency7 ("threshold securities"). For instance, with limited exception, Regulation SHO requires brokers and dealers that are participants of a registered clearing agency8 to take action to "close-out" failure-to-deliver positions ("open fails") in threshold securities that have persisted for 13 consecutive settlement days.9 Closing out requires the broker or dealer to purchase securities of like kind and quantity. Until the position is closed out, the broker or dealer and any broker or dealer for which it clears transactions (for example, an introducing broker)10 may not effect further short sales in that threshold security without borrowing or entering into a bona fide agreement to borrow the security (known as the "pre-borrowing" requirement).

Temporarily suspending Commission and SRO11 short sale price tests12 in a group of securities to evaluate the overall effectiveness and necessity of such restrictions. The Commission will study the impact of relaxing the price tests for a period of one year.13

Creating uniform order marking requirements for sales of all equity securities. This means that orders you place with your broker-dealer must be marked "long," "short," or "short exempt."

BMFL<OD

next week(s) is here

The Kool-Aid drinking hyenas

are laughing now, lets see how much they'll be laughing on the RECORD DATE!

BMFL<OD

next week(s) is here

Bull, add to that the numbers I ran prior to these. Imagine how many were mismarked by UBS and others.

http://investorshub.advfn.com/uimage/uploads/2010/9/12/xnocyFFGO_-_Short_Volume_Since_02012010_Page_1.jpg

http://investorshub.advfn.com/uimage/uploads/2010/9/12/gvchwFFGO_-_Short_Volume_Since_02012010_Page_2.jpg

http://investorshub.advfn.com/uimage/uploads/2010/9/12/xyywxFFGO_-_Short_Volume_Since_02012010_Page_3.jpg

http://investorshub.advfn.com/uimage/uploads/2010/9/12/nhaqmFFGO_-_Short_Volume_Since_02012010_Page_4.jpg

Of course the system is designed to steal. They are called brokers because they leave you broker. lolzzz

WAGI historical dividends please!

This is the SHORTMANS Problem!

20111026|FFGO|2150000|0|2150000|O

FINRA short sale numbers for Novemeber 2010 for FFGO!!!

20101101|FFGO|2849999|3849999|0 74%

20101102|FFGO|1750000|1750000|O 100%

20101103|FFGO|7000000|7107200|O 98%

20101104|FFGO|2000000|2000000|O 100%

20101105|FFGO|7999999|10999999|O 73%

20101108|FFGO|15050000|26500000|O 57%

20101110|FFGO|1000000|2898917|O 34%

20101111|FFGO|2419999|2419999|O 100%

20101112|FFGO|3100000|3200000|O 97%

20101116|FFGO|1000000|1340000|O 75%

20101117|FFGO|6000001|10778584|O 56%

20101118|FFGO|2000000|4014600|O 50%

20101122|FFGO|19845000|19845000|O 100%

20101123|FFGO|500000|1000000|O 50%

20101130|FFGO|20385000|21035000|O 97%

Nov. totals: 79,354,998.00 107,739,299.00 74% sold short

Here are the FINRA short sale numbers for December 2010:

20101202|FFGO|999999|999999|O 100%

20101203|FFGO|615000|4585000|O 13%

20101206|FFGO|1100000|1220000|O 90%

20101207|FFGO|700000|3700000|O 19%

20101208|FFGO|750000|1017259|O 74%

20101209|FFGO|2500000|4500000|O 56%

20101210|FFGO|57089999|74194973|O 77%

20101213|FFGO|6000000|10005000|O 59.7%

20101214|FFGO|28900077|31695902|O 91%

20101215|FFGO|5500000|5704441|O 96%

20101216|FFGO|33250000|54755000|O 61%

20101217|FFGO|8890998|9340998|O 95%

20101220|FFGO|5615800|6660800|O 84%

20101221|FFGO|9600000|11200000|O 86%

20101222|FFGO|24577777|31723803|O 77%

20101227|FFGO|154399995|176901620|O 87%

20101228|FFGO|4999999|4999999|O 100%

20101229|FFGO|9382269|9426819|O 100%

20101230|FFGO|7000000|7010000|O 100%

20101231|FFGO|4081168|8192303|0 50%

Dec. totals: 361,453,081.00 457,833,916.00 79%

2010 short sale totals: 440,808,079. out of a total volume of 565,573,215 or 78% shares sold short. Note well the SEC only started publishing FINRA's daily short sale numbers in Nov. of 2010.

CRISIS FOR SHORTY!!!!! FFGO FINRA SHORT NUMBERS!!!!

January 2011

20110103|FFGO|20000000|22953402|O 87%

20110104|FFGO|9100000|9400000|O 96.8%

20110105|FFGO|8250000|13250000|O 62.3%

20110106|FFGO|11000000|11220000|O 98%

20110107|FFGO|9999999|9999999|O 100%

20110110|FFGO|400000|900000|O 44%

20110111|FFGO|1500000|2000000|O 75%

20110112|FFGO|1400000|1400000|O 100%

20110113|FFGO|1300000|1800000|O 72%

20110114|FFGO|23859999|38587151|O 61%

20110118|FFGO|3000400|3400400|O 88%

20110120|FFGO|7499999|8099999|O 92.5%

20110124|FFGO|1800000|1800000|O 100%

20110125|FFGO|800000|800000|O 100%

20110126|FFGO|10000000|10000625|O 99.9%

20110131|FFGO|317800|317800|O 100%

February 2011

20110202|FFGO|20700000|36210000|O 57%

20110203|FFGO|13400000|38601000|O 34.7%

20110209|FFGO|200000|365000|O 54.7%

20110210|FFGO|2900000|3700000|O 78.3%

20110211|FFGO|500000|4970000|O 10%

20110214|FFGO|2000000|2006250|O 99.6%

20110216|FFGO|17700000|27770000|O 63%

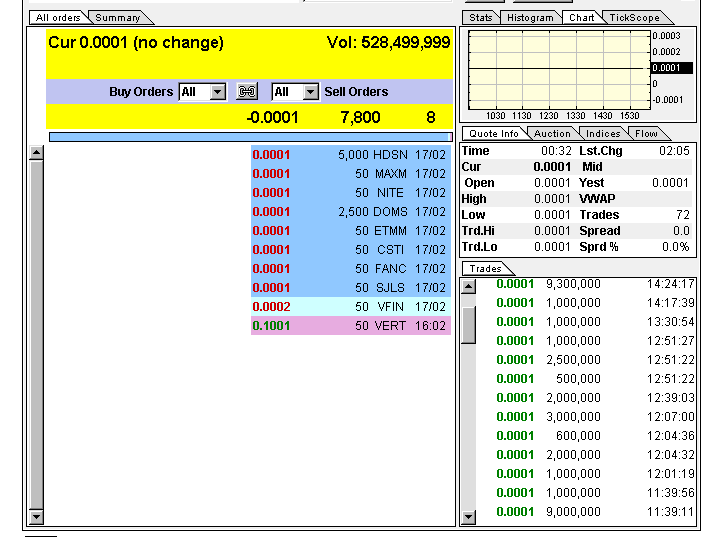

20110217|FFGO|525499999|528499999|O 99.4% COLD WINTER DAY

20110218|FFGO|7600000|8725000|O 87.1%

20110222|FFGO|10000000|10526708|O 94.9%

20110223|FFGO|2000000|2700000|O 74%

20110225|FFGO|1000000|1455000|O 68.7%

March 2011

20110301|FFGO|1000000|0|1350000|O 74%

20110303|FFGO|1795000|0|3492848|O 51%

20110304|FFGO|100000|0|100000|O 100%

20110307|FFGO|1800000|0|1800000|O 100%

20110311|FFGO|500000|0|500000|O 100%

20110314|FFGO|2000000|0|2000000|O 100%

20110315|FFGO|3500000|0|4500000|O 77.7%

20110316|FFGO|11500000|0|11500650|O 99.99%

20110317|FFGO|3114000|0|3617357|O 86%

20110318|FFGO|13020000|0|13020000|O 100%

20110324|FFGO|150000|0|701113|O 21%

20110325|FFGO|110000|0|110000|O 100%

20110329|FFGO|1497300|0|1497300|O 100%

20110331|FFGO|1999999|0|3430269|O 58%

April 2011

20110404|FFGO|5891100|0|6651100|O 88.5%

20110405|FFGO|126400|0|126400|O 100%

20110406|FFGO|150000|0|150000|O 100%

20110411|FFGO|456000|0|456000|O 100%

20110413|FFGO|876543|0|876543|O 100%

20110414|FFGO|4100000|0|4741400|O 86.4%

20110415|FFGO|1500000|0|2500000|O 65%

20110420|FFGO|100000|0|100000|O 100%

20110421|FFGO|1560000|0|1560000|O 100%

20110425|FDTC|4000|0|25000|O 16%

20110426|FFGO|1000000|0|1000162|O 99.9%

20110427|FFGO|1000000|0|1000000|O 100%

20110428|FFGO|8072700|0|8322700|O 96.9%

20110429|FFGO|30210000|0|30210000|O 100%

May 2011

20110502|FFGO|4476700|0|4476700|O 100%

20110503|FFGO|7338600|0|10788600|O 68%

20110504|FFGO|2000000|0|2000000|O 100%

20110505|FFGO|1620000|0|2140000|O 75.7%

20110506|FFGO|1500000|0|1505583|O 99.6%

20110509|FFGO|1000000|0|1000000|O 100%

20110511|FFGO|3000000|0|3040000|O 88.2%

20110512|FFGO|7200000|0|8200000|O 87.8%

20110516|FFGO|8200000|0|8300000|O 98.7%

20110517|FFGO|4099900|0|4199900|O 97.6%

20110518|FFGO|585000|0|585000|O 100%

20110520|FFGO|1000777|0|1000777|O 100%

20110523|FFGO|2000000|0|2000000|O 100%

20110524|FFGO|500000|0|800000|O 62%

20110525|FFGO|18585000|0|18585000|O 100%

20110527|FFGO|1000000|0|1000000|O 100%

20110531|FFGO|7628700|0|8031462|O 94.9%

June 2011

20110603|FFGO|400000|0|400000|O 100%

20110606|FFGO|2710000|0|2710000|O 100%

20110607|FFGO|24000000|0|24000000|O 100%

20110608|FFGO|173800|0|173800|O 100%

20110609|FFGO|2500000|0|2500000|O 100%

20110610|FFGO|83100|0|83100|O 100%

20110614|FFGO|1500000|0|1500000|O 100%

20110615|FFGO|1000000|0|1000000|O 100%

20110616|FFGO|2000000|0|2000000|O 100%

20110617|FFGO|1105223|0|1355223|O 81.5%

20110621|FFGO|423000|0|423000|O 100%

20110623|FFGO|1000000|0|1000000|O 100%

20110624|FFGO|3401333|0|3401333|O 100%

20110629|FFGO|8619200|0|8619200|O 100%

20110630|FFGO|200400|0|200400|O 100%

July 2011

20110701|FFGO|5497995|0|5497995|O 100%

20110706|FFGO|400400|0|700400|O 57%

20110711|FFGO|500000|0|1400000|O 35%

20110714|FFGO|1102699|0|1102699|O 100%

20110715|FFGO|300100|0|400100|O 75%

20110718|FFGO|10850000|0|10850000|O 100%

20110719|FFGO|74000000|0|74000000|O 100%

20110720|FFGO|54100000|0|54100000|O 100%

20110722|FFGO|30000000|0|30000000|O 100%

20110725|FFGO|10346500|0|10346500|O 100%

20110727|FFGO|2400100|0|3400100|O 70.5%

August 2011

20110801|FFGO|8900000|0|8900000|O 100%

20110803|FFGO|5550000|0|5550000|O 100%

20110804|FFGO|7000100|0|10325100|O 67%

20110805|FFGO|5573333|0|5723333|O 100%

20110808|FFGO|405800|0|405800|O 100%

20110809|FFGO|3400000|0|3500000|O 97.1%

20110811|FFGO|3279000|0|3279000|O 100%

20110812|FFGO|100100|0|100100|O 100%

20110815|FFGO|14500000|0|14500000|O 100%

20110816|FFGO|1000000|0|1000000|O 100%

20110817|FFGO|10490000|0|10490000|O 100%

20110818|FFGO|4000000|0|4000000|O 100%

20110822|FFGO|467000|0|467000|O 100%

20110823|FFGO|55633600|0|55633600|O 100%

20110824|FFGO|500000|0|500000|O 100%

20110825|FFGO|750000|0|750000|O 100%

20110829|FFGO|1500000|0|1500000|O 100%

20110831|FFGO|45327062|0|61885560|O 73.2%

Here are the month of September and year to date FINRA short sale numbers for FFGO:

September 2011

20110901|FFGO| 777000|0| 832000|O 93.3%

20110902|FFGO|4000000|0|4000000|O 100%

20110908|FFGO|1920000|0|1920000|O 100%

20110909|FFGO|2500000|0|2500000|O 100%

20110913|FFGO|5000000|0|5299100|O 94.3%

20110914|FFGO|3000000|0|3000000|O 100%

20110923|FFGO|2000000|0|2320000|O 86.2%

20110928|FFGO|1000600|0|1125600|O 88.8%

Month totals: 20,197,600/20,996,700 96.1%

October 2011

20111003|FFGO|500000|0|500000|O 100%

20111004|FFGO|2000000|0|2000000|O 100%

20111005|FFGO|310000|0|590000|O 52.5%

20111006|FFGO|600000|0|1600000|O 37.5%

20111010|FFGO|100000|0|100000|O 100%

20111012|FFGO|2010000|0|2390000|O 84.1%

20111013|FFGO|2999999|0|2999999|O 100%

20111014|FFGO|4000000|0|4000000|O 100%

20111018|FFGO|8000000|0|11000000|O 72.7%

20111019|FFGO|1000000|0|1000000|O 100%

20111026|FFGO|2150000|0|2150000|O 100%

Month totals: 23,659,999/28329,999 83.5%

FFGO YEAR TO DATE

JAN 110,228,197/ 135,899,376

FEB 603,499,999/ 665,528,957

MAR 42,086,299/ 47,619,537

APR 55,046,743/ 57,719,305

MAY 71,734,677/ 77,653,022

JUN 49,116,056/ 49,366,056

JLY 189,497,794/ 191,797,794

AUG 168,375,995/ 188,509,493

SEP 20,197,000/ 20,996,700

OCT 23,659,999/28,329,999

Year to date totals

1,333,442.759/ 1,453,420,239 91.7% SHORT VOLUME for shares sold in 2011

regsho.finra.org/FORFshvol20110324.txt

Total short volume since FINRA began publishing records in Nov. 2010:

1,774,250,838 short shares sold out of total volume of 2,018,993,454 or 87.9% of all shares sold were sold short!

BMFL<OD

next week(s) is here

The system has been designed to steal

from us, we will see if the 5 TRILLION A/S TRAP will work!

BMFL<OD

next week(s) is here

They may have turned over their short selling clients for the reduced fine. One will never know.

WAGI historical shareholders deserve to be paid what is due them.

"token" fine

To spill the beans!

BMFL<OD

next week(s) is here

The fine of $12MM was most likely a "token" fine. The big burden of financial liability will come in the form of settlement with the companies UBS and others have destroyed with abusive naked short selling, IMO.

WAGI is possibly one of the big recipients of such abusive "oversights".

Tic Toc

Appears to me that FINRA's digging back in 2008 and 2009 may have uncovered massive and abusive naked short selling going all the way back to WAGI days.

UBS Fined $12 Million For Yet Another Trading Incident

UBS Securities was fined $12 million for failing to “properly supervise short sales of securities.”

The Financial Industry Regulatory Authority (FINRA) announced yesterday that UBS violated Regulation SHO and failed to supervise short sales and as result millions of short sale orders were mismarked or placed to the market “without reasonable grounds to believe the securities could be borrowed and delivered.”

In other words UBS was placing short sale orders without first making sure that the securities would be available. UBS was also mismarking millions of sale orders in its trading systems. For example, many of the orders were short sales that were actually mismarked “long”, FINRA says.

The FINRA fine is a drop in the bucket compared to the massive $2.3 billion loss UBS took when one of its traders allegedly made unauthorized trades. That incident triggered UBS CEO Oswald Grübel to resign from his post.

Despite the trading loss, UBS said on Monday that it earned $1.2 billion in the third quarter thank in part to an accounting gain.

FINRA, a self regulatory organization, said in a statement:

FINRA found that UBS’ Reg SHO supervisory system regarding locates and the marking of sale orders was significantly flawed and resulted in a systemic supervisory failure that contributed to serious Reg SHO failures across its equities trading business. First, FINRA found that UBS placed millions of short sale orders to the market without locates, including in securities that were known to be hard to borrow. These locate violations extended to numerous trading systems, desks, accounts and strategies, and impacted UBS’ technology, operations, and supervisory systems and procedures. Second, FINRA found that UBS mismarked millions of sale orders in its trading systems. Many of these mismarked orders were short sales that were mismarked as “long,” resulting in additional significant violations of Reg SHO’s locate requirement. Third, FINRA found that UBS had significant deficiencies related to its aggregation units that may have contributed to additional significant order-marking and locate violations.

Brad Bennett, FINRA executive chief of enforcement said, “Firms must ensure their trading and supervisory systems are designed to prevent the release of short sale orders without valid locates, and properly mark sale orders, in order to prevent potentially abusive naked short selling. The duration, scope and volume of UBS’ locate and order-marking violations created a potential for harm to the integrity of the market.”

http://www.forbes.com/sites/halahtouryalai/2011/10/26/ubs-fined-12-million-for-yet-another-trading-incident/

BMFL<OD

next week(s) is here

Historically goes back to WAGI!

That's why I'm here.

BMFL<OD

next week(s) is here

WAGI - Advocation for investors will pay off for shareholders, both historically and currently. Both the company and the shareholders have suffered from abusive market manipulation by naked short sellers.

Hey Bull I don't wanna be an assistant thanks for asking though

Yes puppy used to like the phrase

There's always next week(s) !

BMFL<OD

next week(s) is here

Bull Finch, Thanks for the invite and the research on history, your efforts much appreciated.

I'm a little hazy on your sign off statements.

"BMFL<OD

next week(s) is here"

The BMFL<OD ??????????????????????????

"next(s) is week is here", I believe that could be due to the suspensition.

I am thinking it would be due to the fact FFGO could not issue a "Cash" Dividend if we were trading, as it would be a material change that would be looked upon by SEC as mannipulation.

They "may" take this oppitunity to announce the dividend, (who knows)therefor your statement week(s) are here?????????????

If I remember correctly it was puppydot that added the (s) to the week, to adgitate shareholders lol.

Thanks again

it's a welcome escape....

To escape from the Hyenas!

a doglike carnivore of the family Hyaenidae, of Africa, southwestern Asia, and south central Asia, having a coarse coat, a sloping back, and large teeth and feeding chiefly on carrion, often in packs that has migrated to ihub.

the cork Share Saturday, October 29, 2011 12:43:45 PM

Re: Bull Finch post# 57 Post # of 79

So why the sudden interest in a dead board?

Just curious.

BMFL<OD

next week(s) is here

NEW YORK, NY--(MARKET WIRE)--Oct 18, 2004

-- West Africa Gold, Inc. (OTC BB:WAGI.OB - News) takes pleasure in announcing that the Chairman of its Advisory Committee, Dr. Wayne P Colliston, is continuing with the re-assessment of West Africa Gold Inc.'s Mining assets, and has completed his report on the 1,300 acre Bouse gold (silver -- copper) property situated in the La Paz area of western Arizona, USA, near the California border and on the Mockingbird Project situated in Mohave County, Arizona; as well as the "In Darset" Gold Mining Property in Mali, West Africa.

ADVERTISEMENT

The Bouse Project :-

Dr. Colliston reports that the mineralising event at Bouse was a mid-Tertiary epithermal event, causing complex mineralization of gold, fluorite, barite, and associated metals into previous copper-specularite mineralization. The prime cause was regional crustal extension along the Plomosa Fault, just north of the Plomosa Mountains, which has now been identified as a detachment fault. The "detachment fault" style of deposit is best seen at Copperstone, the biggest gold discovery in Arizona in the past 50 years, where 500,000 oz of gold was profitably mined by Cyprus Gold in the open pit there. The Mesquite mine is another of this type.

Mineralization at Bouse is located primarily below the fault trace, in the lower plate, in pre-Cambrian rocks older than 1 billion years. Mineralization is found both in steeply dipping quartz veins and in laterally extensive breccia zones. The nature of these structures and associated mineralization over almost all of the 1,300 acres suggest further potential for major detachment fault gold deposits, and other deposits associated with this style of mineralization.

The Bouse area is an historic gold producer, with the Little Butte open pit and underground mines as known producers. Importantly, the historical grade recovered here averaged over 0.4 oz/ton. Around 2/3 of this production was from the Little Butte Mine, where the Arizona Department of Mines and Mineral Resources has recorded that the results of a 16-hold drilling programme showed about 5 million tons of inferred ore grading between 0.05 and 0.30 oz/ton.

Others areas of interest within the Company's 1,300 acres are the Brindle Claims, the high grade Arrastre Mine, the Blue Slate Mine and the Flat Fault Mine.

At the current gold price of approximately US $400/oz, this provides a value estimate for the deposit in the range of up to $600 million. This estimated gold resource is for the little Butte area only, and does not include any potential from the remainder of the property.

The Mockingbird Project :-

Dr. Colliston reports that the Mockingbird mineralization is tectonically and structurally controlled an important feature which may not have received sufficient attention from previous owners of the property. Mockingbird is an historic gold producer, with some 15,000 ounces from high-grade ore at an average grade of 0.8 oz/ton being produced. Most of this production was from the Mockingbird Mine itself, the centrepiece of the Company's present land position. Other mines which produced gold at this location included the Great West, the Hall (Dandy) and the Pocahontas Mines, all of which are included in the Company's property.

West Africa Gold, Inc.'s Mockingbird Project contains a new and important type of gold deposit, a "detachment fault" deposit (first recognized as a separate form of gold deposit in the 1980s), and the best example of which is Copperstone. This was the biggest gold discovery in Arizona in the past 50 years. Cyprus Gold profitably mined the 500,000 oz open pit Copperstone resource during the 1980s. Based on underground drilling by the American Bonanza company, it is likely that the underground high-grade resource at Mockingbird is even larger.

The Company's mining title consists of 2,500 acres of mineral rights comprising a number of federal claims with 3 lode deposits and 16 placer deposits, as well as the Mockingbird Claims. Significantly, these include the 4 existing mines -- Mockingbird, Great West, Hall (Dandy) and Pocahontas, all of which contributed significantly to the past gold production in this important gold producing mining district.

Mineralization is found both in quartz veins and in breccia zones hosted by steep faults, with the mines located along north-west to east-west striking, north-dipping to flat quartz veins containing specular hematite, oxidized copper and free gold. The nature of these structures and associated mineralization suggest even further potential for a major detachment fault-associated gold/copper deposit, similar to the proven and mined Copperstone and Mesquite deposits.

The Mockingbird Project area therefore has the potential for the development of a large gold reserve. Anaconda estimated a deposit at Mockingbird of at least 10 million tons grading 0.05 to 0.1 oz/ton gold, with additional resources of silver and copper, putting the potential deposit size in the range of 500,000 to 1,000,000 ounces of gold, approximately the same size as Copperstone. The Anaconda estimate is corroborated by US Geological Survey Open File Report 92-002 and the Arizona Department of Mines and Mineral Resources.

At the current gold price of approximately US $400/oz, this provides a value estimate for the deposit in the range of US $200 to $400 million. The estimated gold resource does not include any potential from the 16 gold placers identified on the property.