News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

$KOSK .0099 DD

Security Details: https://www.otcmarkets.com/stock/KOSK/security …

Profile: https://www.otcmarkets.com/stock/KOSK/profile …

Overview: News..Charts and Financials: https://www.otcmarkets.com/stock/KOSK/overview …

Great DD Articles: http://wallstreettradereport.com/onestepvending/

http://wallstreettradereport.com/onestepvendinginvestorsdeck/ …

$CHIT retires debt; converts remaining debt to restricted

common shares. Things are about to get wild.

$BDCI Great Article Here http://mystock.pics/BDCI/

$RNVA ALERT http://www.rennovahealth.com/about/overview

***** $COYN Ceo Interview.*****

https://audioboom.com/boos/4588553-uptick-network-interview-with-ceo-ronald-woessner-with-copsync-inc?utm_campaign

I Love The Accumulation On $KLDX The Past 6 Months.

$BSSP The initial deployment for sales of the specific IPF for Cancer indication product and treatment programs to Mexico are now in process with four hospitals positioned and in process of licensing requirements which have been submitted. Canteck is positioned to oversee the development, manufacturing and commercialization processes for our lead product to be the Irreversible Pepsin Fraction (IPF) specific to the Cancer indication, with options for other indications.

"Our transition to the corporate platform for development and deployment of targeted therapeutic immunotherapeutic technology represents an important event in our transition and growth," said Dennis Alexander, CEO of the Company. "Further, the Company welcomes our current and future development with Canteck Pharma, Inc., and working together with our new Board of Directors and Management including Mr. and Mrs. Zhabilov, as the Company looks forward to bringing these novel technological advancements to the forefront initially to Mexico to assist treatment and solutions for specific Cancer treatment and to become available in a cost effective manner to assist the severity of medical needs going unmet."

"The licensing agreement with Reve Technologies, Inc. is very much an important milestone in our goal to develop and commercialize our immune-oncology based IPF treatment as a new therapy for difficult-to-treat tumor indications on a scalable international level initially in Mexico." Said Mr. Harry Zhabilov, Jr. BSc, McS and newly appointed Chief Sciencist of the Company. "We are delighted to have a committed partner and management team and with our missions aligned and look forward to working together to obtain approvals for our IPF Irreversible Pepsin Fraction specific to the Cancer indication, and to bring these much-needed therapeutic options as soon as possible for delivery and availability to Mexico.

Sounds like a lot of UPDATES will be coming fairly quickly

http://marketersmedia.com/reve-acquires-exclusive-license-for-cantecks-ipf-irreversable-pepsin-fraction-specific-to-cancer-indication-only-for-mexico/112197

Well, the truth is that this isn’t the case at all. The global economic meltdown is steaming along, even if it is moving just a little bit slower than many of us had originally anticipated. We are moving in the exact direction that myself and many others had warned about, and the rest of 2016 is looking quite ominous for the global economy.

So hopefully everyone (including the critics) is using whatever time we have left wisely. Because I definitely wish the very best for everyone during the exceedingly hard times that are coming.

Yes, the stock market has been on quite a run for the past several weeks, but that temporary rebound is not based on the economic fundamentals.

The truth is that the real economy is definitely starting to slow down substantially. If you want to break it down very simply, less stuff is being bought and sold and shipped around the country, and that tells us far more about what is coming in the months ahead than the temporary ups and downs of stock prices.

Another huge red flag is the fact that the inventory to sales ratio in the U.S. has hit the highest level that we have seen since the last financial crisis…

Those that were hoping for an “economic renaissance” in the United States got some more bad news this week. It turns out that the U.S. economy is in significantly worse shape than the experts were projecting.

Retail sales unexpectedly declined in March, total business sales have fallen again, and the inventory to sales ratio has hit the highest level since the last financial crisis. When you add these three classic recession signals to the 19 troubling numbers about the U.S. economy that I wrote about last week, it paints a very disturbing picture.

Virtually all of the signs that we would expect to pop up during the early chapters of a major economic crisis have now appeared, and yet most Americans still appear to be clueless about what is happening.

Even I was surprised when the government reported that retail sales had actually fallen in March. Consumer spending is a very large part of our economy, and so if consumer spending is slowing down already that certainly does not bode well for the rest of 2016.

Lone Star Value Nominates Five Candidates for Election to Board of Dakota Plains

Seeks to Upgrade Board, Overhaul Corporate Governance, and Maximize Stockholder Value

PR Newswire Lone Star Value Management, LLC

March 18, 2016 9:18 AM

$DAKP .10

OLD GREENWICH, Conn., March 18, 2016 /PRNewswire/ -- Lone Star Value Management, LLC (together with its affiliates, "Lone Star Value", "we" or "us"), the largest stockholder of Dakota Plains Holdings, Inc. ("Dakota Plains" or the "Company") (NYSE MKT: $DAKP, with ownership of approximately 11.0% of the Company's outstanding shares, announced today that it has formally nominated five candidates for election to the Company's board of directors (the "Board") at the Company's upcoming 2016 annual meeting of stockholders (the "2016 Annual Meeting").

Lone Star Value, a stockholder of Dakota Plains since early 2014, is committed to maximizing value for ALL Dakota Plains' stockholders by upgrading and replacing the existing Board, overhauling the Company's corporate governance and compensation policies, and running a proper strategic alternatives process.

We believe the Company's poor stock price performance is a direct result of the failures of the CEO and incumbent Board. We are confident our five nominees will dramatically improve the Board by adding a stockholder's perspective and the required expertise to improve performance. We believe the need for an immediate upgrade to the Board is undeniable given Dakota Plains' stock price decline of 96% during Craig McKenzie's tenure as CEO[1] and its decline of 91% since the Board was partially reconstituted last year.[2]

As we have noted in prior press releases, Dakota Plains' CEO, Craig McKenzie, and Chairman, Adam Kroloff, have a long history of destroying stockholder value beyond Dakota Plains:

Canadian Superior Energy, Inc. - stock price declined over 60% while McKenzie served as CEO[3]; and

Toreador Resources Corporation - stock price massively underperformed peer group while Mr. McKenzie served as CEO and declined more than 60% while Mr. Kroloff served as a director.[4]

Under pressure from Lone Star Value, Dakota Plains made several defensive and unilateral changes to the Board and Bylaws in February 2015. The Board also made multiple claims and promises to stockholders that it has failed to keep in what can only be seen as a ploy to gain support prior to last year's annual meeting:

Dakota Plains announced a strategic alternatives process in February 2015.

The Board has failed to show any progress in its strategic alternatives process and terminated its advisors a few months ago after incurring $1.1 million in costs in 2015.[5] We believe the Company's original announcement was just for show and question whether a legitimate process was ever truly pursued.

In December 2014, Dakota Plains issued very precise EBITDA guidance for 2015 of $23.4 million with CEO McKenzie saying at the time "While the volumes we are providing in our 2015 guidance represent significant growth over 2014, I believe they will prove to be conservative… we don't make guidance lightly. Those who follow the company would know, we didn't provide guidance at all last year. And so with $23.4 million of the EBITDA guidance we're certainly seeing that is something that we can deliver for stockholders and based on ongoing discussions we're hopeful that we'll be in a position to do even better."[6] CEO McKenzie re-affirmed this guidance a few months later stating "we are right in line with our 2015 plan…and we have no reason to believe that we're not going to be meeting our guidance, so therefore today, it is reiterated."[7]

In May of 2015, CEO McKenzie removed Dakota Plains' 2015 guidance citing a change in market conditions. Either he did not understand the Company's profit drivers in December 2014 or he issued misleading guidance and reiterated this guidance in an attempt to create stockholder support ahead of the 2015 Annual Meeting.

The Company's actual EBITDA for 2015 was $8.7 million[8], 63% below the CEO's December 2014 forecast.

The Board claimed to be acting in the best interest of its stockholders, but has unilaterally adopted numerous anti-stockholder provisions contrary to best corporate governance practices such as:

Amending the Bylaws to prohibit stockholders from acting by written consent and calling special meetings until the conclusion of the 2015 Annual Meeting;

Further amending the Bylaws prior to the conclusion of the 2015 Annual Meeting to perpetuate the suspension of such critical stockholder rights until the conclusion of the 2016 Annual Meeting; and

Adopting a poison pill earlier in January 2016.

We firmly believe that each of these stockholder-unfriendly changes should have been approved by stockholders prior to their adoption in accordance with best corporate governance practices rather than being unilaterally adopted by the incumbent Board.

To us, these violations of stockholder rights and broken promises can only be explained by a desire by the incumbent Board to stay in power another year and enrich themselves at stockholders' expense. Again, we would like to remind stockholders that the Company's stock price has declined 91% since the Board was partially reconstituted in February 2015.[9] It is evident to us that significant changes to the Board are necessary given the Company's continued underperformance under the leadership of the incumbent Board.

We believe another major factor contributing to the destruction of stockholder value at Dakota Plains is the extravagant compensation packages given to CEO McKenzie and the members of the Board. The compensation paid to CEO McKenzie during his first two years, for example, totaled approximately $5 million. This amount equates to a staggering 84% of the Company's EBITDA during this period.[10] In addition, Board members each receive compensation totaling $150,000 in cash and stock per year, which we believe is excessive given the Company's size and poor performance.

Given the significant value destruction that has persisted under the incumbent Board, Lone Star Value calls on the Board to hold the 2016 Annual Meeting without delay in order to allow stockholders to elect representatives who have their best interests in mind at this critical stage for the Company. We further call on the Board to terminate the poison pill immediately and to refrain from taking any of the following actions prior to the 2016 Annual Meeting without prior stockholder approval:

Delaying the 2016 Annual Meeting;

Maintaining the poison pill;

Making any acquisitions;

Issuing equity or equity-linked securities; or

Adopting any corporate governance changes that serve to further entrench the Board, including classifying the Board.

Lone Star Value would like to remind each of the incumbent directors that they have a fiduciary duty to act in stockholders' best interests and any breaches thereof may have serious personal consequences that may even result in personal liability under certain circumstances.

If elected, our independent nominees would commit to the following actions at Dakota Plains:

Implement a pay-for-performance structure for management to better align executive compensation with stockholder value creation;

Reduce Board compensation;

Review all expenses, especially corporate overhead, with a goal of significantly reducing all corporate costs;

Improve corporate governance; and

Analyze all strategic alternatives over the short, medium, and long term with a sole goal of maximizing value for stockholders.

Lone Star Value's Nominees:

Lone Star Value has nominated five highly-qualified director candidates for election to the Board at the 2016 Annual Meeting whose experience encompasses transportation, energy, investment banking, mergers & acquisitions, capital markets, and turnaround expertise. Our nominees are Jeff Eberwein, Michael Hidalgo, Kevin Rendino, Josh Schechter, and Galen Vetter. We believe our five nominees possess a well-balanced set of skills that will create an immediate impact and drive stockholder value at the Company.

Highlights of our highly-qualified director nominees include the following:

Jeff Eberwein:

Founder and CEO of Lone Star Value, Dakota Plains' largest stockholder.

As Chairman of the Board of Digirad Corporation (DRAD), he helped orchestrate a complete turnaround which restored the company to profitability and has overseen multiple accretive acquisitions; DRAD also bought back stock and started paying a dividend; DRAD's stock price is up 186%[11] during Mr. Eberwein's tenure on its board of directors.

Mr. Eberwein joined the board of NTS, Inc. (NTS) in December 2012 and in less than a year, led the Special Committee in a sale of the company to a private equity firm for $2.00/share, reflecting a 122% return[12].

As Chairman of the Board of AMERI Holdings, Inc. (AMRH), he has overseen value-enhancing acquisitions along with an approximate 333%[13] stock price return in ten months.

Mr. Eberwein has served on a total of 9 public boards.

He was previously a Portfolio Manager at Soros Fund Management and Viking Global Investors.

Michael Hidalgo:

Mr. Hidalgo currently serves as the Vice President of Orchard Global Asset Management focusing on direct lending.

Mr. Hidalgo previously founded and served as CFO of Buckhorn Energy Services, an oilfield environmental services company focused on the Bakken.

Prior to his departure, Buckhorn was valued in excess of $90 million and was preparing for listing in the public MLP market in fall of 2014.

Kevin Rendino:

Mr. Rendino is currently the President and CEO of RGJ Capital, LLC, a fund focused on investing in securities that are undervalued relative to the future true worth of their underlying assets.

Mr. Rendino served as a Portfolio Manager and Managing Director at BlackRock, Inc., where he was head of the Basic Value Equity Group ($13 billion in assets), as well as being a member of BlackRock's Leadership Committee.

Mr. Rendino served as a Managing Director and Portfolio Manager at Merrill Lynch Investment Managers, prior to merging with BlackRock in 2006.

Mr. Rendino has been a frequent contributor to CNBC, Bloomberg TV, Fox Business, and other financial newspapers and magazines, including the New York Times and the Wall Street Journal.

Josh Schechter:

Within a year of Mr. Schechter joining the board of The Pantry, Inc., the company formed a strategic committee and sold the company for a 138%[14] premium to the stock price on the day he joined the board.

Mr. Schechter currently serves as a director of Viad Corp.

Former director of WHX Corporation and Puroflow, Inc.

Previously served as Managing Director of Steel Partners Ltd.

Galen Vetter:

Mr. Vetter currently serves as a director of ATRM Holdings, Inc., Alerus Financial, Inc., Crossroads Systems, Inc., and Hill Capital Corporation, and is an advisory board member of Land O'Lakes Inc.

He has previously served as President of Rust Consulting, Inc., Global CFO of Franklin Templeton Investment Funds, and held numerous positions with RSM US LLP (formerly McGladrey).

Mr. Vetter is a licensed CPA (inactive) and is a member of the National Association of Corporate Directors, including being Board Leadership Fellow certified.

CERTAIN INFORMATION CONCERNING PARTICIPANTS

Lone Star Value Investors, LP, together with the other participants named herein, intends to file a preliminary proxy statement and accompanying proxy card with the Securities and Exchange Commission ("SEC") to be used to solicit votes for the election of their slate of five highly-qualified director nominees at the 2016 annual meeting of stockholders of Dakota Plains Holdings, Inc., a Nevada corporation (the "Company").

Lone Star Value Management STRONGLY ADVISES ALL STOCKHOLDERS OF THE COMPANY TO READ THE PROXY STATEMENT AND OTHER PROXY MATERIALS AS THEY BECOME AVAILABLE BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION. SUCH PROXY MATERIALS WILL BE AVAILABLE AT NO CHARGE ON THE SEC'S WEB SITE AT HTTP://WWW.SEC.GOV. IN ADDITION, THE PARTICIPANTS IN THIS PROXY SOLICITATION WILL PROVIDE COPIES OF THE PROXY STATEMENT WITHOUT CHARGE, WHEN AVAILABLE, UPON REQUEST. REQUESTS FOR COPIES SHOULD BE DIRECTED TO THE PARTICIPANTS' PROXY SOLICITOR.

The participants in the proxy solicitation are Lone Star Value Investors, LP ("Lone Star Value Investors"), Lone Star Value Investors GP, LLC ("Lone Star Value GP"), Lone Star Value Management, LLC ("Lone Star Value Management"), Jeffrey E. Eberwein, Michael Hidalgo, Kevin Rendino, Joshua E. Schechter, and Galen G. Vetter (collectively, the "Participants").

As of the date hereof, Lone Star Value Investors directly beneficially owns 5,654,454 shares of common stock, par value $0.001 per share (the "Common Stock"), of the Company. Lone Star Value GP, as the general partner of Lone Star Value Investors, may be deemed the beneficial owner of the 5,654,454 shares of Common Stock beneficially owned by Lone Star Value Investors. As of the date hereof, 400,000 shares of Common Stock were held in a certain account managed by Lone Star Value Management (the "Separately Managed Account"). Lone Star Value Management, as the investment manager of Lone Star Value Investors and the Separately Managed Account, may be deemed the beneficial owner of the 6,054,454 shares of Common Stock beneficially owned in the aggregate by Lone Star Value Investors and held in the Separately Managed Account. Mr. Eberwein, as the manager of Lone Star Value GP and sole member of Lone Star Value Management, may be deemed the beneficial owner of the 6,054,454 shares of Common Stock beneficially owned in the aggregate by Lone Star Value Investors and held in the Separately Managed Account. As of the date hereof, none of Messrs. Hidalgo, Rendino, Schechter, or Vetter beneficially own any shares of Common Stock.

About Lone Star Value Management:

Lone Star Value Management, LLC ("Lone Star Value") is an investment firm that invests in undervalued securities and engages with its portfolio companies in a constructive way to help maximize value for all stockholders. Lone Star Value was founded by Jeff Eberwein who was formerly a Portfolio Manager at Soros Fund Management and Viking Global Investors. Lone Star Value is based in Old Greenwich, CT.

Investor Contact:

John Glenn Grau

InvestorCom

(203) 972-9300 ext. 11

[1] Stock price decline during Mr. McKenzie's tenure as CEO at Dakota Plains calculated from 02/12/2013 to 02/29/2016.

[2] Stock price decline during new Board's tenure calculated from 02/12/2015 to 02/29/2016.

[3] Stock price decline during Mr. McKenzie's tenure as CEO at Canadian Superior Energy calculated from 10/01/2007 to 12/04/2008.

[4] Stock price decline during Mr. Kroloff's tenure on the Board of Toreador calculated from 06/05/2009 to 12/07/2012.

[5] Announced in Dakota Plains' Full Year and Q4 2015 press release on 3/11/2016.

[6] Quote from Dakota Plains' business update call on 12/12/2014.

[7] Quote from Dakota Plains' Q4 2014 Earnings call on 3/16/2015.

[8] Announced in Dakota Plains' Full Year and Q4 2015 press release on 3/11/2016.

[9] Stock price decline during new Board's tenure calculated from 02/12/2015 to 02/29/2016.

[10] Compensation data taken from Dakota Plains' proxy statement filed with the SEC in 2015; Adjusted EBITDA taken from Dakota Plains' 10-K filed with the SEC in 2015.

[11] Total shareholder returns (dividends reinvested) during Mr. Eberwein's tenure on the Digirad board calculated from 04/20/2012 to 02/29/2016.

[12] Total shareholder returns during Mr. Eberwein's tenure on the NTS, Inc. board calculated from 12/20/2012 to 06/09/2014.

[13] Total shareholder returns during Mr. Eberwein's tenure on the Ameri Holdings board calculated from 05/26/2015 to 02/29/2016.

[14] Total shareholder returns during Mr. Schechter's tenure on the Pantry Inc. board calculated from 03/13/2014 to 03/17/2015.

WEM & APP FARM ?@WorldFlix Mar 16

From last PR: APP FARM ... Joint Venture interests, representing Companies capable of placing Swantry on tens of thousands of smart phones.

$WRFX .001 - 52w low holding on a Friday.

Got a feeling EOD dump coming on $WRFX - moved bids down to .0008 and .0009.

Here's to hoping .001 holds on $WRFX

$WRFX - is it go time? .0012s up with support at .0011

$WRFX on bid at .001 and .0009. Looks like she wants another 52w low.

$SRCO oh yea! Look at those gains! Said it for weeks. Buy the dips. Onward to .01!

$MEDA doing well today. Looking much stronger than previous weeks.

FLST is ripe for a run.. Up 44% and super thin

130 mil float hearing. http://stockcharts.com/h-sc/ui?s=icnv

CRCO- Low float play, loading zone here, we break .001 and this could fly, keep on watch :)

Max Sound Provides An Update On Contempt Hearing

Date : 03/11/2016 @ 6:15PM

Source : InvestorsHub NewsWire

Stock : Max Sound Corporation (QB) (MAXD)

Quote : 0.0026 0.0 (0.00%) @ 3:56PM

Max Sound Provides An Update On Contempt Hearing

Max Sound Provides An Update On Contempt Hearing

SANTA MONICA, CA -- March 11, 2016 -- InvestorsHub NewsWire -- Max Sound Corporation $MAXD provides a litigation update to its Shareholders on the contempt case against VSL. On March 9th, VSL requested an ex-parte 30-day extension as they claimed that they changed their legal counsel yet again. VSL’s new lawyers made no appearance and their existing counsel did not provide proof of engagement. The Judge did not find any acceptable argument for a 30-day extension. However, while reviewing the courtroom schedule, the Judge decided that the half-day scheduled on March 24th was no longer sufficient to complete the hearing given the magnitude of contempt, and rescheduled the hearing for 9:00AM April 7th, the earliest full day available on the court’s calendar.

“We believe the date change is a non-event, and no matter how many lawyers VSL brings or claims to be bringing in the future, we’re confident in a positive outcome for Max Sound,” said John Blaisure CEO of Max Sound Corporation.

About Max Sound Corporation: As creators of acclaimed MAX-D HD Audio, Max Sound can provide a better solution for Audio, Video and Data transmissions. Max Sound Corporation is the company that brings forth technologies for the betterment of our digital world, including VSL's Optimized Data Transmission Technology. Max Sound®, MAXD® and MAX-D Audio Perfected® are registered trademarks. All other trademarks are the property of their respective owners. To learn more about the MAX-D Technology, please visit http://maxd.audio.

SAFE HARBOR STATEMENT UNDER THE PRIVATE SECURITIES LITIGATION REFORM ACT OF 1995: Statements in this press release which are not purely historical, including statements regarding Max Sound's intentions, beliefs, expectations, representations, projections, plans or strategies regarding the future are forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. The forward-looking statements involve risks and uncertainties including, but not limited to, the risks associated with the effect of changing economic conditions, trends in the products markets, variations in the company's cash flow or adequacy of capital resources, market acceptance risks, technical development risks, and other risk factors. The company cautions investors not to place undue reliance on the forward-looking statements contained in this press release. Max Sound disclaims any obligation and does not undertake to update or revise any forward-looking statements in this press release. Expanded and historical information is made available to the public by Max Sound Corporation and its Affiliates on its website http://maxd.audio or at http://www.sec.gov.

Contact:

Max Sound Corporation

info@maxsound.com

$ICNV .001

Our Story

Icon Vapor is your Total Vapor Solutions Company.

We offer a wide variety of Vape Products, including Mods, Pens, Accessories and Vape Juice in a variety of Flavors and Nicotine Strengths that are all Made in the USA. Icon Vapor Inc. is a Publicly Traded Company available through the OTCQB under the ticker symbol ICNV. The Icon Vapor Brand has entered the exciting and growing market place of Vaping. Icon Vapor products are distributed through Core-Mark and other distributors to the convenience store marketplace throughout the United States and Canada.

http://www.iconvapor.com/

$MEDA someone is accumulating from week hands today. Got a feeling things

are getting close with this one.

$WRFX looking for a move to .0024 to try and break the upper trend line.

$GNBT Daily Chart

see, CMF was red for a few weeks and once it ran then turned green and then it fell from 07 the CMF was green whole time until now wtf

at times the CMF plays tricks on you

can i get a chart for GNBT

I will be watching, $SPDC - thank you for the tip!

YODA watch SPDC...you'll thank me... Aloha

$MEDA someone is loading. I may just buy their loading wall

sitting at .0025 and see what they do next...

watch SPDC...you'll thank me... Aloha

$AHIX dump and dilution fest, but got a feeling we

see a bounce back soon. #lotto

$WRFX looking good bouncing off new 52w low.

$PGH President’s Message

To our shareholders,

2015 presented some difficult and challenging times for the oil and gas business. The precipitous decline in world crude oil prices and the negative investment sentiment around the business resulted in a very challenging environment both operationally and within the equity markets. However, despite these challenging headwinds, we remained steadfast in our efforts and our teams rose to the challenge to help steward the Company through these turbulent times. We have established a strong track record of operational performance and delivering on our commitments, and in 2015, we demonstrated this once again.

We responded to the drop in oil prices by taking prudent actions at the start of the year designed to safeguard the health and wellbeing of the Company. As the year developed and the outlook for lower commodity prices persisted, we once again acted and introduced additional measures to ensure the Company remained protected. In 2015 we delivered strong operating results, notwithstanding the continued deterioration in the commodity price environment that persisted throughout the year. We successfully executed the start-up of the first commercial phase of Lindbergh, and achieved production rates from Lindbergh in excess of the 12,500 barrels per day (bbl per day) nameplate capacity. Production from Lindbergh exceeded 16,000 bbl per day for the first time during five days in early December. We continued to generate strong results from our conventional operations, achieving annual average production of 71,409 barrel of oil equivalent per day, coming in at the high end of our production guidance, despite significant asset sales and an 80 percent reduction in capital spending year over year and shut-in uneconomic production.

Protection of our financial strength and flexibility was paramount throughout the year, where we curtailed our capital spending and instituted cost management initiatives across all segments of our business. We also made the difficult decision to reduce our staffing levels by 30 percent in the year, to realign our business to the current environment and right size the organization. These cost reduction initiatives resulted in the achievement of operating and G&A expenses that were below the low end of corporate guidance and most importantly, we were able to reduce our debt position by $280 million through the use of funds flow and proceeds from our ongoing disposition program.

Consistency in funds flow performance was a key theme that emanated in 2015 despite the significant decline in commodity benchmark prices. Our strong performance was supported by our robust commodity hedging program, which generated realized cash gains of $327 million during the year, resulting in 2015 funds flow of approximately $459 million. This represented a decline of only nine percent from 2014 funds flow levels, despite a 43 percent reduction in average benchmark prices year over year. We remain well hedged in 2016 with a significant portion of our crude oil and natural gas production protected at prices well in excess of the current market prices.

We continued to build the foundations for long-term growth by delivering strong reserves performance in 2015, successfully replacing 282 percent of 2015 production with proved plus probable (2P) reserve additions, prior to the impact of dispositions and 145 percent of production net of dispositions. We were able to do this at a competitive 2P finding and development cost of $7.12 per boe including future development costs. In total, 2015 2P reserves increased two percent to 569 million barrels of oil equivalent, this in spite of significant asset divestitures in the year. The significant reserve additions came from two of our key focus areas, the Lindbergh and Groundbirch resources. These two areas represent future growth potential and value creation in the company and for our shareholders.

Looking forward into in 2016, we remain disciplined and prudent in our approach to managing our business in this low commodity price environment. In 2016 we announced the suspension of our dividend and adopted a lean capital program for the year that contemplates no development activity but will allocate some minor capital to advance long-term projects, namely at Lindbergh and Bernadet. These projects represent excellent low cost, opportunities for longer-term production growth. Our 2016 capital budget was conservatively based on the assumption of an average WTI crude oil price of US $30.00 per bbl, an AECO natural gas price of Cdn $2.40 per Mcf, WTI/WCS heavy oil differential US$12.60 per bbl and a $0.70 US/Cdn exchange rate, which represents the environment that we believe, could persist throughout the year.

We remain committed to our debt reduction initiative in 2016 and with no scheduled debt maturities in 2016, we expect to be in a position to materially reduce our outstanding debt through a combination of strong funds flow from operations supported by a substantial hedging program, disposition proceeds, and our ongoing cost reduction initiatives. We retain ample financial flexibility with our $1.0 billion committed revolving credit facility, which was renewed and extended in

PENGROWTH 2015 President's Message

1

2015 resulting in a maturity date of March 31, 2019. These initiatives are expected to allow the Company to remain compliant with its debt obligations as we navigate our way through this low commodity cycle.

2015 was undoubtedly a very challenging year for the business and we acknowledge that the year was very difficult on our shareholders. We strongly believe the efforts we demonstrated in 2015 and the actions we have taken in 2016 are the appropriate ones to ensure that the Company remains financially sound and emerges from this downturn a stronger Company. We are committed to our strategy and have confidence in our ability to deliver on that strategy. We have great assets that provide us with a solid foundation and the opportunity to create long-term growth and value for our shareholders, a fact that we believe will be acknowledged by the capital markets.

On behalf of our Board of Directors, management and all of our employees, I would like to take this opportunity to thank all of our shareholders for their continued support. As well, I would like to thank our employees for their tireless dedication, commitment and support in what has been a difficult year.

Sincerely,

Derek W. Evans

President and Chief Executive Officer

February 24, 2016

$AZUR: Azure Midstream Partners delays Q4 earnings release and conf call; co said it could exceed the permitted ratio of debt to adj. EBITDA contained in its credit facility as early as the end of Q1 of 2016, evaluating strategic alternatives (2.37 -0.19)

Co announced that it plans to postpone the distribution of its 2015 fourth quarter results and related conference call and webcast, previously scheduled for Thursday, March 10, 2016

Azure is a party to a credit facility, which, as of March 8, 2016, had borrowing capacity of $238.0 mln with total borrowings of $231.7 mln

While Azure expects to be in compliance with all of its financial covenants under its credit facility as of Dec 31, 2015, Azure anticipates that, due to the continuation of adverse industry conditions, it could exceed the permitted ratio of debt to adjusted EBITDA contained in its credit facility as early as the end of Q1 of 2016

Upon any such default under the credit facility, indebtedness under the credit facility could, after the expiration of any grace period and at the election of a majority of the lenders under the credit facility, be accelerated and become immediately due and payable

As a result of this potential default and acceleration, the Partnership's auditors have informed us that its opinion to be issued in connection with the Partnership's consolidated financial statements to be included in the Partnership's annual report on Form 10-K is expected to include an explanatory paragraph to the effect that these conditions raise substantial doubt about the Partnership's ability to continue as a going concern

The Partnership is currently working with its lenders to waive or eliminate the requirement in the credit facility which states that the receipt of a going concern explanatory paragraph is considered an event of default

Likewise, the Partnership continues to pursue options to address the potential covenant violation that may occur as early as the end of the first quarter of 2016

As previously announced, the Partnership continues to pursue options to strengthen its balance sheet. These options include potential equity restructuring, capital raise and strategic alternatives that will provide visibility into stabilizing future distributions and providing excess liquidity to the Partnership

The Board of Directors and management are in the process of evaluating strategic alternatives to help provide the Partnership with financial stability, but no assurance can be given as to the outcome or timing of this process.

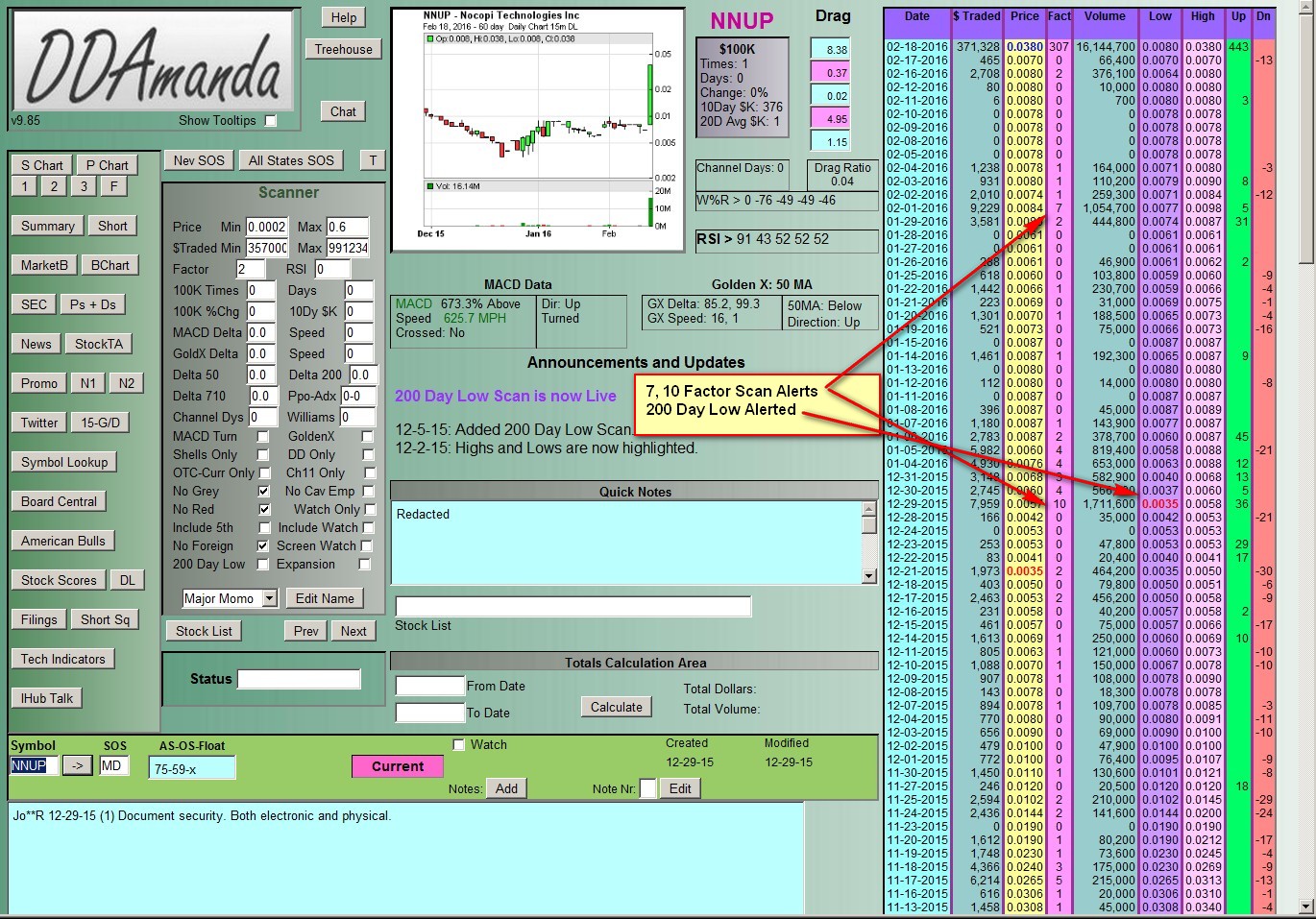

DDAmanda® Chart on: $NNUP: Click on the chart twice to see it better.

z

|

Followers

|

44

|

Posters

|

|

|

Posts (Today)

|

0

|

Posts (Total)

|

4145

|

|

Created

|

06/23/15

|

Type

|

Free

|

| Moderator PennyStockYoda | |||

| Assistants 1~Eye~Jack!! RoadRunner3 | |||

It's time to make some money!

Our Picks

| IFCR | .0011 | .0033 | ||

| PWDY | .0004 | .0009 | ||

| SIRGQ | .0003 | .0029 | ||

| CJTF | .0002 | .0012 | ||

| RMRK | .0003 | .0013 | ||

| CTLE | .001 | .002 | ||

| IGEX | .0004 | .004 | ||

| OCLG | .0014 | .0022 | ||

| IFCR | .0014 | .002 | ||

| SYNJ | .0003 | .0038 | ||

| EDXC | .021 | .04 | ||

| NESV | .06 | .27 | ||

| OCLG | .0012 | .0008 | ||

| NESV | .045 | .11 | ||

| EDXC | .021 | .025 | ||

| WOGI | .0115 | |||

|

Posts Today

|

0

|

|

Posts (Total)

|

4145

|

|

Posters

|

|

|

Moderator

|

|

|

Assistants

|

| Volume | |

| Day Range: | |

| Bid Price | |

| Ask Price | |

| Last Trade Time: |