News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Waste management sector -- >>> No Disappointments In 'Waste Land'

Nov 12 2013

includes: RSG, WCN, WM

http://seekingalpha.com/article/1830602-no-disappointments-in-waste-land?source=yahoo

The US non-hazardous solid-waste services industry generates annual revenue in excess of $50 billion, a staggering number just to keep our streets clean. Waste Management (WM), Republic Services (RSG), and Waste Connections (WCN) dominate this market, generating greater than 60% of industry revenues and controlling an equal percentage of valuable disposal capacity. The top line for the group can be expected to expand at a nominal-GDP rate, with pricing growth in the industry adding an additional tailwind thanks to recent consolidation (Republic Services/Allied Waste), a rational focus on return on invested capital, and cost pressures facing independent mom-and-pop trash companies and municipalities.

Operators generate strong and predictable cash flow. Within the collection line of a waste hauler's business, residential services provided to municipalities and individual households are on a service-based model (not-volume based) and can largely be viewed as insulated from economic pressures. Such a constant revenue stream helps to mitigate cyclical pressures in a trash taker's commercial collection and industrial roll-off lines, which also fall into the overall waste-collection category. Cell-by-cell landfill build-out provides additional flexibility with respect to capital outlays, as haulers can scale back expenditures during troubled economic times.

Year-to-date, Waste Management's third-quarter performance shows free cash flow (cash from operations less capital expenditures) of $1.03 billion, roughly 9.8% of sales, while Republic Services' year-to-date mark of $448.5 million represents 7.1% of sales. Waste Management more effectively converts sales to free cash flow, as capital expenditures (as a percentage of sales) are roughly 3 percentage points lower than those of Republic (7.9% versus 11%). We think Republic's capital requirements will steadily decline in coming years to a high-single-digit mark as percentage of sales once the hefty equipment expenditures of today are completed.

Transfer and disposal is the most lucrative revenue stream in the waste business. Landfill ownership can largely be viewed as the primary competitive advantage for a solid-waste operator. Though anyone that can finance a truck can bid on collection routes (service is undifferentiated), new entrants are at a significant disadvantage for disposal. For starters, building a landfill is expensive, time-consuming (permits can take 3-7 years to obtain, sometimes longer), and NIMBY (not-in-my-backyard) opposition has only increased with suburban sprawl. Subtitle D of the Resource Conservation and Recovery Act (1991) significantly increased the cost and complexity of landfill ownership (composite liners, leachate collection systems, zoning, etc.). As a result, many landfills in the US have been closed, and disposal airspace should only become more valuable over time.

Since collected waste must go somewhere (direct haul is only practical for 40-50 miles), the company that controls the disposal assets in a given "wasteshed" (locality) often dictates pricing. Owning the only dump in town also limits hefty tipping fees paid to other participants. Waste Management and Republic Services internalize -- dispose of into their own company-owned landfills -- more than 60% of collected waste, bolstering operating margins relative to privately-held, independent operators. Importantly, landfilling still represents the most prominent form of disposal, declining only 3 percentage points (as a percentage of generation) during the last decade. Materials recovery (including recycling) should continue its march upward, but the pace of this trend is far from tragic for the waste-hauling sector.

Waste Management's and Republic Services' third-quarter pricing trends certainly didn't disappoint. The former put up core pricing expansion of 3.9%, while the latter posted an average yield increase of 1.3% for the period. Though these numbers may not seem aggressive, they are quite meaningful across the large revenue bases of the two garbage giants. The commentary of Waste Management's CEO David Steiner regarding ongoing pricing expansion was particularly encouraging:

"In the third quarter, collection and disposal yield was 2.3%, the fifth quarter of sequential improvement, and nearly triple the yield we saw in the third quarter of 2012."

Valuentum's Take

We're huge fundamental fans of the garbage hauling industry and hold Republic Services in the portfolio of our Best Ideas Newsletter. There's really nothing too frightening about the dividend health of Waste Management and Republic given their robust free cash flow, but we're not rushing to add them to the portfolio of our Dividend Growth Newsletter on the basis of their mediocre Valuentum Dividend Cushion scores (and hefty debt loads). Still, the structural characteristics of the garbage industry are among the strongest in our coverage universe given the value of landfill ownership. We're keeping a close eye on the group.

<<<

Stericycle -- >>> Stericycle - Replicating A Successful Strategy Abroad

Sep 23 2013

http://seekingalpha.com/article/1707662-stericycle-replicating-a-successful-strategy-abroad?source=yahoo

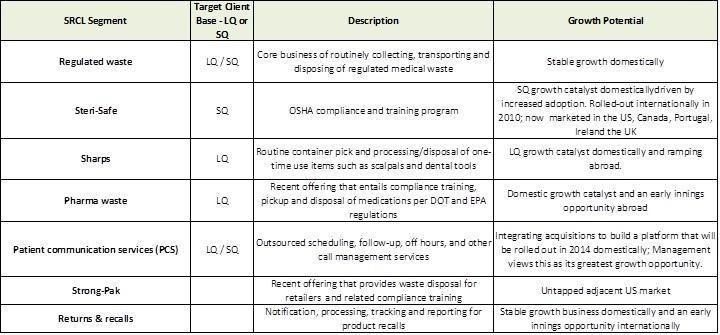

Stericycle Inc. (SRCL) is the domestic market leader (32% share) providing medical waste management services to large quantity (LQ) and small quantity (SQ) medical waste generators. Shares have grown by 30x since 2000 through organic investments and acquisitions. The underlying business strategy capitalizes on regulation that mandates proper collection, transportation and disposal of medical waste. SRCL grew by targeting SQ clients with basic waste services and gaining incremental revenue upselling ancillary offerings to a client base of 550k accounts. The company is introducing new ancillary services domestically and rolling up the industry abroad with the same strategy that drove robust US growth in the last decade. Accordingly, continued execution on a familiar strategy will result in sustainable, and profitable, business growth. I estimate shares are worth $151, thus offering 30% upside through FY14.

More Than Just Medical Waste Management

SRCL is essentially a one-stop shop for various medical waste needs with its core business being medical waste collection and disposal. The SRCL business model is to supplement organic growth with acquisitions for regional concentration, thus allowing for better route economies. SRCL then upsells ancillary services to existing customers once an expansive platform is in place. This approach has resulted in 10yr revenue CAGR of 17%, where upselling drives incremental margins. As an example, a base SQ customer with waste services has a mid-50's gross margin, compared to high 60's with a premium service like Steri-Safe. The company breaks out revenues by two segments - recalls & returns and regulated medical waste (RMW), of which the latter houses the ancillary business lines (please see below table for a segment overview). US operations (13% FY12 revenue growth) are currently driven by secondary services such as Steri-Safe for SQ, in addition to Sharps and Pharma Waste for LQ. Patient communication services will be rolled out to SRCL's client base in FY14 and it stands to be one of the company's greatest growth opportunities. International operations (17% FY12 revenue growth) are currently driven by Steri-Safe and will be boosted by increased adoption of ancillaries as the company increases its client base and route density. Both will act as a platform from which additional services can be delivered to existing clients internationally.

(click to enlarge)

Low-Cost Medical Waste Manager

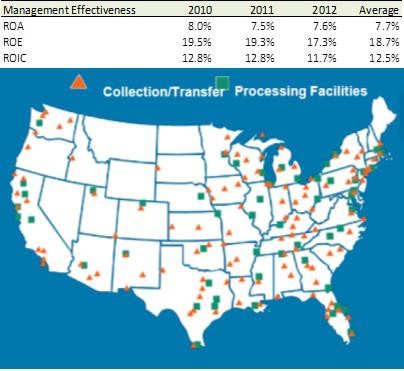

SRCL has a leg up on the competition as it is the low-cost provider. Strategic moves by management to consolidate the industry have put SRCL in an enviable position where route density increases profitability. Management has led 323 acquisitions since 1993 with the end goal being to increase regional concentration and rationalize operations with a focus on increasing efficiency. The company now has a network of 358 collection and processing facilities that allows SRCL to undercut competitors on pricing and maintain profitability through better route economies (see chart below for facility footprint). Transportation costs eat up approximately 50% of COGS. SRCL is more efficient with its fleet spending less time driving between client locations while consuming less fuel. Without a large domestic footprint (much like its competitors - Waste Management has 23), transportation costs can reduce gross margins and erode any low-pricing advantage. Management's contributions to this strategy with prudent capital allocation can't be underestimated. Capital allocation is perhaps the most important factor for companies complementing organic growth with acquisitions. Management has executed consistently, compounding book value per share at 17% over the last 10 years, in line with revenues. Management experience gives SRCL a distinct advantage as it attempts to consolidate secondary markets to achieve low-cost provider status internationally.

Industry Growth Drivers

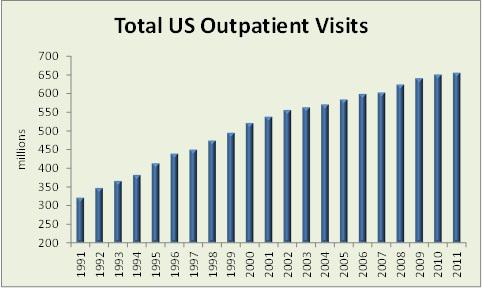

Industry growth benefits from both cost pressures resulting from regulation and secular trends in patient visits. Medical waste is regulated by agencies such as the Dept. of Labor (OSHA), DOT, EPA and DEA. Hazardous medical waste must be collected, transported and processed through regulated methods that require documentation and reporting every step along the way. Costs of regulatory compliance have relegated waste management to outsourcing providers who have expertise processing waste economically. The industry is now mostly outsourcing waste management due to regulation, as opposed to in-house processing as done in the late 80s when SRCL began consolidating providers. Continued US/international medical waste regulation will further drive outsourcing to specialized providers through heightened costs of regulation. The Affordable Care Act, should it ultimately come to fruition, stands to insure millions of individuals who previously lacked coverage. Accordingly, patient volumes could increase substantially for outpatient facilities (i.e. SQ business) who offer lower cost services than hospitals. Patient visits continue to move to outpatient facilities, rather than hospitals, both domestically and in Europe. Total US outpatient visits have increased 104% since 1991 while hospital admissions have remained relatively flat (See chart below). Along with this trend comes increased need for SQ clients to manage medical waste. Most SQ clients lack training and resources necessary for proper compliance and SRCL has focused on such clients for these reasons. Industry growth will also continue to be a function of selling ancillary medical services to an underpenetrated service base. Only 20-30% of SRCL's client base has adopted multiple offerings and industry providers are targeting greater adoption through sales efforts.

(click to enlarge)

Additional Color On Margins

Gross margins have more than doubled since FY96 from 21% to 45% in FY12. Two factors underlie this impressive feat. One is the transition from lower margin LQ business to a more fragmented SQ client base where pricing power is higher and where the potential revenue opportunity is greater. Typical SQ clients could generate 9x more revenue per account with premium services such as Patient Communication Services (PCS) and Steri-Safe, while LQ clients have an additional revenue opportunity of 4x. For these reasons, economics favor SQ generators where margins can be impacted to a greater extent. Second, is what I discussed above with route density. Critical mass is achieved with scale. I estimate SRCL reached an inflection point in the late 90's/early 2000's. Margins ramped 18 percentage points in a matter of four years from FY96-FY00. Incremental facility tuck-ins bolstered transportation route efficiency and profitability. The company was aggressively expanding its network as customer growth increased 490% over the same period. The below charts illustrate that critical mass (i.e. significant margin expansion) was achieved when SRCL surpassed 100-200 transportation and processing facilities. Note, the charts also evidence diminishing profitability when industry capacity becomes saturated, as could be the case in for US operations in years to come. Current operations in Europe are eerily similar to SRCL's US business in the early 2000s. Its route footprint is approaching critical mass (154 facilities FY12), gross margins run in the low 30's and revenues are predominantly LQ based. Management is replicating a familiar strategy by investing abroad in route concentration, while focusing on an untapped market of higher-margin SQ clients. It is likely international margins will trend along a similar path as US operations once critical mass is reached abroad. Fortunately, management has experience executing such a strategy, which provides compelling support that SRCL can capitalize on prospects in Europe.

(click to enlarge)

Replicating US Strategy In Europe

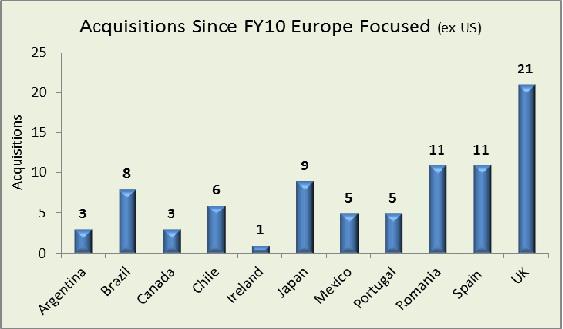

Since 2000, share prices have grown at a 32% CAGR on the back of margin and revenue expansion driven by an SQ focused strategy, acquisitions and upselling ancillary services in the US. Management is replicating the same strategy in Europe through industry consolidation where it can attain critical mass and low-pricing status. Europe is mostly low-margin, bulk LQ business currently and the company is acquiring competitors to increase route density while targeting high-margin SQ business (sound familiar?). SRCL must have an expansive platform in place so that it gains route economies allowing it to underprice competitors and roll-out ancillary services to win SQ clients. SRCL is gaining SQ penetration with its Steri-Safe offering. Steri-Safe is now offered in the UK, Ireland, Portugal and is soon to be rolled out in Spain where acquisition activity has been aggressive. The UK market evidences how successful this strategy has been as SQ business in the UK as a proportion of total UK revenues has grown approximately four percentage points annually to 32%. As other countries come online, it is likely SQ accounts will be similarly penetrated with consolidated gross margins expanding 200-300bps as international revenues comprise a larger portion of total revenues. Note, this process takes years to accomplish, will likely require additional debt issuances (current net debt to capital 45%) and may have a slower growth rate than the US as SRCL doesn't have an early-mover advantage in Europe. Keep in mind, Europe is not all about SQ potential. Sharps and recalls & returns operations should bolster growth for LQ accounts. Sharps business is poised to drive revenues as it has currently done in the US. SRCL recently brought a UK plant online in FY12 for its Sharps waste management and services are now offered in Ireland, Portugal and recently introduced in Spain.

(click to enlarge)

International Growth With a US Kicker

Revenue sustainability comes into question whenever double-digit growth is the norm. For SRCL, top-line growth will continue from not only international, but also from US contributions. SRCL has grown domestic revenues by a 13% CAGR since 2008 (21% internationally) through introducing niche services built off its existing distribution platform. Sharps and Steri-Safe are prime examples as each was introduced as a secondary service to gain incremental revenue and margins with existing clients. Looking long-term, the focus will shift to PCS in the US. PCS will continue to be driven by cost pressures from increased regulation, notably Medicare reimbursements for Hospitals. Current legislation details how hospitals will receive Medicare reimbursements based upon patient satisfaction surveys. Surveys address levels of physician care to quality of hospital offerings, and perhaps most importantly for SRCL, effectiveness of communication with patients. PCS allows hospitals to outsource patient communications and call management to those with such expertise. Enhanced patient relations should result from consistent contact and scheduling, 24-hour call center management and post-discharge calls, thus resulting in better survey results and higher reimbursements. Moreover, PCS alleviates cost pressures for hospitals that are investing to improve operations internally with the goal of improved treatment quality and survey results. SRCL acquired PCS providers NotifyMD and Beryl Healthcare in FY11 and FY12, respectively, and both are leaders in patient communications outsourcing. SRCL is integrating operations and technology platforms throughout FY13, and upselling this service is on track to begin domestically in FY14. If 25% of SRCL's client base signs up for PCS services, the company would stand to gain $866m-$1210m annually, thus potentially boosting revenues by 63%. Moreover, PCS gross margins currently run in the mid-40s. It's in the early stages of the growth cycle. As operations are integrated the SRCL way with a focus on efficiency gains and profitability, consolidated margins should benefit.

Geographic Based Valuation

The SRCL story will take years to play out and I am comfortable holding shares for an extended period as I believe expansion of both the top and bottom line is sustainable. Shares have consistently traded at premium valuations (1.9x the industry P/S average) and multiples will react as Europe and ancillary US growth seasons. I tend to look at valuation as a set of binary outcomes and the situation simply materializes as either favorable or not. I am comforted that the more probable outcome of the in between means I make a considerable return. In a best case scenario, shares are worth $212, and conversely, $90 in a worst case scenario. The "in between" results in a $151 price target, thus offering 30% upside through FY14 and a risk-to-reward of 3.5x. I am valuing SRCL shares by breaking down domestic and international operations and applying a proper P/S multiple to each. Since business abroad is utilizing the same SQ penetration and ancillary upsell strategy executed successfully in the US, I am assuming international will track along a similar trajectory. Valuing consolidated SRCL operations traditionally on a P/E, P/B, and EV/EBITDA basis yields similar price target results.

(click to enlarge)

Risks

I believe there are three primary risks to my thesis on SRCL. 1) PCS business is a new adjacent market for SRCL but unrelated directly to medical waste management. The company may be unsuccessful in its attempts to profitably integrate operations and then upsell PCS to its customer base. 2) Multiples could compress from premium levels if growth abroad (or with PCS) fails to materialize. SRCL is targeting SQ business in Europe for margin expansion and top-line growth, and not executing on this strategy would likely see multiples fall. 3) In the intermediate-term, margin directionality is relatively neutral for SRCL. There are signs of saturation domestically as the company has acquired lower margin business in recent years. Further down the income statement, net margins have minor tailwinds in coming years. Probable future debt issuances will offset some benefits of gross margin expansion and SG&A leverage.

Wrapping It Up

SRCL is the kind of company where you look at a historical 10y chart and kick yourself for not having the foresight to have initiated a position previously. The question then becomes is now too late and is the model sustainable for years to come? I believe the answer is undoubtedly yes since the company is undertaking a proven strategy abroad, complemented by a middle innings opportunity domestically. While I believe shares are worth $151 through FY14, holding onto SRCL could result in far greater returns for those with such patience.

<<<

>>> Continental Prison Systems Announces Name and Symbol Change

http://finance.yahoo.com/news/continental-prison-systems-announces-name-133000446.html

IRVINE, Calif., Aug. 16, 2013 (GLOBE NEWSWIRE) -- Continental Prison Systems, Inc. (CPSZ) (the "Company") - a payment processing technology company that specializes in the $500 billion government payment space, is pleased to announce that it has received FINRA approval for the previously announced 1-100 reverse stock split, name change, and symbol change. The Company's new name will be General Payment Systems, Inc. when the market opens on September 3, 2013. For twenty business days beginning on September 3, 2013, the Company's ticker symbol will be CPSZD. After that twenty day period, the D, which signifies that the reverse stock split occurred, will be removed and the Company's new ticker symbol will be GPSI.

"Our new corporate name allows the company to more effectively convey our core purpose and intent, to become a leader in the vast municipal payment space," stated Ron Hodge, CEO, Continental Payment Systems. "While we are most appreciative of the solid footing that our successes in the corrections space have afforded us, we know for the benefit of this company and its shareholders that a brighter future lies in the penetration of the enormous municipal payment market where our proven technology has the potential to handle payments for taxes, tickets, utilities, and much, much more."

"We have already accomplished a number of important milestones in municipal payments. Now it is time to take our operations to the next level," Hodge added.

Shareholders of record at the end of trading on September 2, 2013, will be affected by the 1-100 reverse stock split. When the market opens on September 3, 2013, every one hundred (100) shares of issued and outstanding common stock will be converted into one (1) share of common stock. All fractional shares created by the reverse stock split will be rounded to the nearest whole share. If the fraction created is one half or less, it will be rounded down to the nearest whole share. If the fraction is more than one half, it will be rounded up to the nearest whole share. Each shareholder will get at least one share. The reverse stock split will also reduce the Company's authorized common stock from 2,000,000,000 to 100,000,000.

The Company's transfer agent, Action Stock Transfer, will adjust its records to reflect each shareholder's post-split position. Share adjustments to certificates can be made upon surrender to the transfer agent. Please contact Action Stock Transfer for further information and costs. Action Stock Transfer can be reached at (801) 274-1088 or info@actionstocktransfer.com.

About Continental Prison Systems

Continental Prison Systems Inc (dba EZ Card and Kiosk) is a technology company that provides government agencies with proprietary hardware (Kiosks) and cloud based software systems that automate the process of collecting payments from the general public (Cash, Debit and Credit). These systems deliver payment acceptance, real-time accounting and payment risk-mitigation services. The company distributes these technologies through direct sales, channel partners, and various licensed entities.

<<<

>>> Continental Prison Systems Processes Record Transactions in Q1 of 2013

Jun 17, 2013

http://finance.yahoo.com/news/continental-prison-systems-processes-record-103000728.html

IRVINE, Calif., June 17, 2013 (GLOBE NEWSWIRE) -- Continental Prison Systems, Inc. (CPSZ) - a payment processing technology company that specializes in the $500 billion government payment space, is pleased to announce that the company's transactional volume for the first quarter of 2013 is its largest to date, continuing a pattern of escalating transactional volume over the past few years.

Transactional volume, in number of transactions is as follows:

2010: 238,339 transactions

2011: 399,261 transactions

2012: 526,366 transactions

Q1 2013: 172,262 transactions

"The rise in transactions is directly attributable to an ongoing expansion of locations using our technology in the corrections and municipal payment industry," stated Ron Hodge, CEO, Continental Prison Systems. "We are continuing to aggressively pursue the large market opportunity presented to this company and to deliver long term value to our shareholders."

About Continental Prison Systems

Continental Prison Systems Inc (dba EZ Card and Kiosk) is a technology company that provides government agencies with proprietary hardware (Kiosks) and cloud based software systems that automate the process of collecting payments from the general public (Cash, Debit and Credit). These systems deliver payment acceptance, real-time accounting and payment risk-mitigation services. The company distributes these technologies through direct sales, channel partners, and various licensed entities.

<<<

>>> Continental Prison Systems Adds Kiosks in Broward County, Florida

Press Release: Continental Prison Systems, Inc.

Jun 13, 2013

http://finance.yahoo.com/news/continental-prison-systems-adds-kiosks-100000260.html

IRVINE, Calif., June 13, 2013 (GLOBE NEWSWIRE) -- Continental Prison Systems, Inc. (CPSZ) - a payment processing technology company that specializes in the $500 billion government payment space, is pleased to announce that it has been asked to expand its presence and services provided in correctional facilities located in Broward County, Florida. The expansion represents an increase in revenue potential equal to or greater than a number of Continental's current accounts.

In total, Continental will deploy four additional kiosks to accept cash at the time the inmate is booked at the facility, bringing the total to nine kiosks. By using Continental's proprietary technology, the intake/booking process will be expedited and can potentially save the jail hundreds of man hours reconciling cash on a monthly basis. The kiosks are set to launch June 19, 20, and 21 of 2013.

"The announcement of our increased presence in Broward County is a welcome addition to our revenue line and to increasing our presence in this very large county and in Florida in general," stated Ron Hodge, CEO, Continental Prison Systems. "It affirms our appeal to these institutions who are embracing our technology as a means to improve efficiency and reduce costs in their facilities."

"Additionally, Continental is finding that it has established three lines for continued expansion," Hodge added. "First, our in-house sales team led by senior management continues to drive opportunity and new agreements. But we are also experiencing organic growth from facilities like Broward County which want more technology provided by Continental. Lastly, and perhaps most significantly, our valued channel partner Archonix has been highly productive in delivering contracts in new regional markets where Continental had limited or no business presence."

"The confluence of these new business lines has created an expansion of the use of Continental's technology that is unprecedented in our history," Hodge added. "We look forward to communicating further successes as contracts are signed and we are allowed to report the events."

About Continental Prison Systems

Continental Prison Systems Inc (dba EZ Card and Kiosk) is a technology company that provides government agencies with proprietary hardware (Kiosks) and cloud based software systems that automate the process of collecting payments from the general public (Cash, Debit and Credit). These systems deliver payment acceptance, real-time accounting and payment risk-mitigation services. The company distributes these technologies through direct sales, channel partners, and various licensed entities.

<<<

>>> Continental Prison Systems, Inc. Announces Annual Shareholders' Meeting

Continental Prison Systems, Inc.

Jun 12, 2013

http://finance.yahoo.com/news/continental-prison-systems-inc-announces-133000012.html

IRVINE, Calif., June 12, 2013 (GLOBE NEWSWIRE) -- Continental Prison Systems, Inc. (CPSZ) (the "Company") is pleased to announce its annual shareholders meeting has been scheduled for 11:00 a.m. on July 16, 2013 (the "Meeting"). The Meeting will be held at the Irvine Marriott, which is located at 18000 Von Karman Avenue, Irvine, CA 92612. A formal notice of the Meeting will be sent to all shareholders of record as of the end of trading June 14, 2013.

During the last 18 months, the Company completed private offerings totaling approximately 470,000,000 shares leaving the Company with 865,746,365 shares of common stock issued and outstanding.

At the Meeting, the Company will discuss the status of its independent financial audit and its plans to transition to fully reporting status under the Securities Exchange Act of 1934 as well as the following matters:

(i) Consideration of a reverse stock split through which the issued and outstanding shares would be reversed one for one hundred, while the authorized shares would be reversed one for ten;

(ii) Consideration of changing the name of the Company to General Payment Systems, Inc. reflecting the Company's increasing expansion into court, probation and government service payment products and services;

(iii) Such other matters as may lawfully be brought before the Meeting.

Ron Hodge, President of the Company provided the following comments: "We have a number of exciting developments in our products, services and market share which we will begin releasing to the stock market between now and the shareholders meeting. The previous 12 months have been a productive period for the Company as it secured resources sufficient to support a fully reporting public company. We are prepared to address any questions or concerns of our shareholders at our shareholders meeting and would like to thank our shareholders for their patience and support. We remain cautiously optimistic that our company's performance will now reward our shareholders and other supporters and that obtaining fully reporting status will allow our company's successes to be appreciated by a much broader constituency of retail and institutional investors."

About Continental Prison Systems, Inc.

Continental Prison Systems, Inc. (dba EZ Card and Kiosk) is a technology company that provides government agencies with proprietary hardware (kiosks) and cloud based software systems that automate the process of collecting payments from the general public (cash, debit, and credit). These systems deliver payment acceptance, real-time accounting and payment risk-mitigation services. The Company distributes these technologies through direct sales channels, channel partners, and various licensed entities.

<<<

Continental Prison Systems -- >>> Continental Prison Systems Signs 512 Bed Butler County Prison in Pennsylvania

Channel Partner Archonix Continues to Deliver for CPSZ

Press Release: Continental Prison Systems

May 2, 2013

http://finance.yahoo.com/news/continental-prison-systems-signs-512-103000533.html

IRVINE, Calif., May 2, 2013 (GLOBE NEWSWIRE) -- Continental Prison Systems, Inc. (CPSZ) - a payment processing technology company that specializes in the $500 billion government payment space, is pleased to announce that it has signed an agreement to provide payment processing to the 512 bed Butler County Prison in Butler County, Pennsylvania. The agreement calls for multiple kiosk installations in the correctional facility. Among the services to be provided are Money Load, Bail, and Debit Release Card solutions.

"The addition of Butler County Prison is a significant addition to our ever expanding portfolio of institutions using our technology," stated Ronald Hodge, CEO, Continental Prison Systems. "Led by Archonix's powerful relationships in the region we are continuing to effectively penetrate and to drive revenue for the benefit of our shareholders."

"We view each of these events as both a clear value-add and a catalyst," added Hodge. "For us, the deal validates our trust and faith in Archonix and their reach, but these deals singularly become advertisements for our technology to a market that frequently looks to its peer group for guidance. And we are clearly and successfully filling an important need in the modern jail and prison system."

About Continental Prison Systems

Continental Prison Systems Inc (dba EZCard and Kiosk) is a technology company that provides government agencies with proprietary hardware (Kiosks) and cloud based software systems that automate the process of collecting payments from the general public (Cash, Debit and Credit). These systems deliver payment acceptance, real-time accounting and payment risk-mitigation services. The company distributes these technologies through direct sales, channel partners, and various licensed entities.

<<<

Rollins -- >>> Rollins Expands to Guam

5-9-13

By Zacks Equity Research

http://finance.yahoo.com/news/rollins-expands-guam-194501105.html

Rollins Inc. (ROL), an established consumer and commercial services company, recently announced that it has set up a franchise in Guam through its wholly owned subsidiary Orkin, LLC.

Orkin is an Atlanta based company, and is of one of the leaders in pest control services and protection against termite damage, insects and rodents. Apart from providing services in the U.S., Orkin’s network is spread across a number of international locations as well, such as Canada, Asia, Europe and Mexico. Orkin uses a three-step method to provide its services and has also taken due care to control pests and protect against damages. It has collaborated with the Centers for Disease Control and Prevention (:CDC) and eight major universities to conduct research and spread awareness about the health hazards caused by pests.

Orkin had established its first two international franchises in Africa. The recent set-up in Guam is ideal, given the island’s typical tropical climate. Guam, a territory of the U.S. in the western Pacific Ocean, has unique pest problems persisting throughout the year. Consumers can thus avail of Orkin’s services to control the menace from pests.

The franchise is owned by Dewan Worldwide, Inc., and will provide services to both homeowners as well as businesses. Orkin will provide initial training to the franchise owners from its headquarters in Atlanta.

Rollins Inc. is based in North America and operates through its wholly owned subsidiaries, such as, Orkin Canada, HomeTeam Pest Defense, Western Pest Services and The Industrial Fumigant Company, to provide pest control services.

<<<

Waste Management -- >>> There's a Jewel to Be Found in Waste

By Piyush Arora

May 1, 2013

http://beta.fool.com/piyusharora/2013/05/01/theres-a-jewel-to-be-found-in-waste/32020/?source=eogyholnk0000001

Investing in income-growth stocks as a way to ride out market uncertainty has always been a good strategy. But investing in just any income-growth stock could be disastrous. For this kind of investing, a company needs to have a solid balance sheet, as well as ample and consistent cash flows to sustain its payouts. One such company that meets the criteria is Waste Management (NYSE: WM), and here are a few reasons why it makes a great income-growth play.

Investors’ delight

Waste Management is known to return (quite a lot of) value to its shareholders. At current prices, shares of Waste Management yield an impressive 3.8%, while Republic Services (NYSE: RSG) and Waste Connections (NYSE: WCN) yield 2.9% and 1.1,% respectively. Waste Management pays out 80% of its earnings, while the Waste Connections and Republic Services payouts are just 28.6% and 58.2% of earnings, respectively.

Naturally, Waste Management's dividend sustainability comes into question with such a high payout ratio. But since the company isn’t planning any expansions or acquisitions, its cash flow can comfortably be directed toward dividends.

Its annual dividend burden aggregates to $680.1 million, which gets entirely covered by its trailing-12-month (ttm) free cash flow of $785 million. Moreover, Waste Management has around $307 million in cash and cash equivalents, which altogether points toward sustainable future payouts.

The company also has a $500 million share-repurchase program underway. At the current price, this represents the pending repurchase of 13 million shares, which should artificially boost its dividend yield to 3.9%. But the company isn’t stopping here.

Management said that it would be focusing on improving the company's yield along with reducing operating costs and increasing its overall operational efficiency over the next couple of years. Although management didn’t quantify the dividend boosts, it’s safe to assume that Waste Management would sustain its payouts for the coming years.

Growth prospects

On Jan. 31, Waste Management announced the acquisition of Greenstar, which is one of the largest private recycling businesses in the U.S. Last year, Greenstar recycled around 1.5 million tonnes of waste, and served around 12,000 domestic customers. This acquisition is expected to boost Waste Management’s recycling capacity by around 11% and bolster its material-refining facilities by 10%. Waste Management's management aims to process around 20-million tonnes of waste by 2020, and the acquisition bodes well with its long-term prospects.

But that’s not all. Waste Management is making strides in improving its financial health. For FY13, it expects to grow its free cash flows to between $1.1 billion and $1.2 billion (around a 52% increase y-o-y) with capital expenditures between $1.3 billion and $1.4 billion. If management is able to deliver what it promises, three things can happen here.

1.) Its dividend yield gets a boost to around 5.5%; 2.) Its board can approve another share buyback; 3.) It can repay a fraction of its total net-debt of approximately $9.2 billion

Of course, the logical move would be to lower its debt/equity of about 1.6x, which would eventually increase its net earnings (due to lower interest expenses).

For the recent quarter, Waste Management reported quarterly EPS of $0.57, which missed estimates of $0.60. However, its revenue rose to $3.4 billion, up from $3.3 billion in last year’s quarter.

Peer talk

Republic Services also disappointed the Street. Its quarterly profits stood at $127 million, down from $191 million in last year’s quarter. Its revenue also remained flat, and analysts expect its annual sales to grow by just 2% to 2.5% in FY13. Additionally, analysts estimate its annual EPS to grow by a meager 3.6% over the next five years, which is discouraging for investors.

Although the company is rapidly expanding its waste recycling capacity, its debt/equity is worsening quickly. At the end of the quarter, Republic Services had total long-term debt of $7 billion with operating cash flow (ttm) of $1.5 billion and cash of $67 million, due to which its cash flow-to-debt equates to 4.5x.

Compared to Waste Management's cash flow-to-debt of 4.2x along with cash and cash equivalents of $307 million, Waste Management is in a better position.

However, Waste Connections posted impressive results. Its quarterly net income stood at $448.8 million, which rose by a whopping 18.2% and beat the Street’s estimates of $445.7 million. The staggering growth was primarily driven by the acquisition of R360 Environmental Solutions in October, which reported annual revenue of $300 million last year.

Meanwhile, EPS of $0.37 missed the estimated $0.38 but rose by $0.02 per share as compared to last year’s quarterly results. Its stellar financial performance was due to masterful execution and a result of its relatively smaller size, which allowed Waste Connections to grow at a rapid rate. But the company isn’t involved in the waste-to-energy conversion business, which is a huge drawback.

As far as its long-term strategy is concerned, Waste Connections continues to expand in regions which aren't saturated with waste-recycling solutions (suburban areas), and offer less competition. This might be beneficial over the long run, but its management affirmed that its short-term growth lies in inorganic expansions in its existing markets.

This clearly puts Waste Management ahead of its peers.

A short conclusion

I don’t like to be a broken record, but if you didn’t already guess, I’d gladly put my money on Waste Management. The company has a high yield, which seems sustainable, and its pending share repurchases will further bolster its EPS. Furthermore, its acquisition of Greenstar and cash flow improvements suggest that Waste Management is well poised for an upside.

<<<

Waste Mgt Sector -- >>> 8 Modern Day Alchemists Turning Trash Into Gold

December 31, 2012

by: David Kronenfeld

http://seekingalpha.com/article/1088401-8-modern-day-alchemists-turning-trash-into-gold?source=yahoo

I love the waste industry. In my former life as an investment banker, I worked with a waste management client and spent several months getting my hands dirty (no pun intended) learning the ins and outs of the industry. There are very few industries where a company is guaranteed demand for its services and can often generate revenue from the very product that it is paid to haul away (i.e. sale of recycling materials, gas collected from decommissioned landfills or electricity from waste-to-energy plants). It is also an industry where a vertically integrated company can dominate a geographic area simply by owning a few key pieces of the waste puzzle.

The chief components of the industry are the disposal trucks and related infrastructure, landfills, recycling facilities and waste-to-energy plants. Disposal trucks and their related infrastructure are easy to acquire, however, collecting trash is only the first step in the process. Unless a company has a favorable landfill contract, then it will lose money on the disposal end of the transaction. The environmental and regulatory permitting as well as geographic parameters (size, location away from NIMBY types, etc.) required to operate a landfill function as a two-edged sword. While it may be difficult to open a landfill, those same obstacles help keep competitors out of the market. For example, one of the fifteen largest municipal areas in the United States is served by only one landfill. By purchasing this landfill, one large waste company was able to guarantee that it would control the entire market as the landfill's current contracts with smaller waste collectors expire.

The past few years have been very favorable for the waste management industry as municipalities across the country have chosen to privatize their waste collection functions in order to save money in an era of tighter budgets. This has created numerous opportunities for small companies to win contracts for the waste disposal in various cities and towns. As described above, though, the big players are utilizing their financial strength to purchase the landfill bottlenecks in order to control the larger, more lucrative markets. These markets are lucrative simply because more trash can be collected (and thus more fees) with fewer resources expended as the population is concentrated. As cities continue to grow, these markets will only continue to become larger and more lucrative. Thus the larger players in the market stand to increase their top line revenues through consolidation and demographic shifts.

Below are eight of the top 50 waste companies in the U.S. as compiled by Waste 360, an excellent industry resource.

Waste Management (WM) - Waste Management is the largest waste management company in the U.S. and has leveraged its resources to branch out into various related industries (i.e. port-a-john servicing, medical waste collection, etc.). The company has also invested in over 1,000 waste collection trucks that run on compressed natural gas. Not only do these trucks offer the benefit of cleaner emissions, they also offer significant fuel savings over the life of the trucks. Waste Management is a mature company with a history of increasing its dividends and offers investors stability, a 4.2% dividend and the prospect of some limited growth as the amount of waste it handles increases.

Republic Services (RSG) - Republic is the second-largest waste management company in the U.S. and has not diversified into related industries like Waste Management. Instead, Republic has chosen to focus on commercial and household waste collection and disposal in the U.S. and Puerto Rico. Currently the company is trading at a lower P/E ratio than Waste Management, however, Waste Management's diversity and strong history of increasing its dividend probably makes it the better investment.

Clean Harbors (CLH) - Clean Harbors specializes in hazardous waste collection and disposal as well as environmental and oil and gas services. The company has traded as low as $47 and as high as $70 over the last 12 months and is currently at $52.90. Clean Harbors recently acquired competitor Safety-Kleen for $1.25 billion financed through a combination of cash on hand, proceeds from a common stock offering and the issuance of senior notes. The acquisition should be immediately accretive and dramatically expands the company's environmental services arm. Between the company's exposure to the booming oil and gas industry as well as the continued demand for environmental services, Clean Harbors is poised for significant growth.

Veolia Environmental (VE) - Veolia is a French waste management company with significant operations in the United States. Over the past two years the company has run into financial troubles and fallen from $30 to $12. Veolia currently offers a 6.4% dividend and appears to be on a better financial footing, but, despite its position as the fourth-largest waste management company in the U.S., I would avoid the stock. Any financial hiccups or a reduction in the dividend could cause the stock to fall further and, while there is significant upside, the risk associated with the upside is quite high.

Stericycle (SRCL) - Stericycle provides medical waste disposal services to clients both in the U.S. and abroad. The company has grown into one of the largest waste management companies in the U.S. through both bolt-on acquisitions and organic growth. Stericycle's aggressive growth strategy has resulted in two 2 for 1 stock splits over the last 10 years. The company has chosen to re-invest its earnings in expansion and does not currently pay out dividends. Over the last year the company has returned 15% and offers investors a financially strong company in an industry that still offers growth prospects. The only significant downside to the stock is potential fall-out from the Patient Protection and Affordable Care Act that could result in reduced margins for the company.

Waste Connections (WCN) - Waste Connections focuses primarily on waste collection and disposal in secondary markets, although the company also offers rail waste shipping services. The stock is trading near its 52-week high, has a P/E ratio higher than either Republic or Waste Management, and only offers a 1.2% dividend payout. The company acquired R360 Environmental Solutions in late October 2012, which will allow it to expand its offerings in the oil and gas environmental waste disposal sector. Despite the company's prospects for growth, I would avoid Waste Connections and invest in one of the other waste management providers listed here.

US Ecology (ECOL) - Along with Stericycle, this is one of my favorite companies in the waste sector. Based in Boise, Idaho, US Ecology provides disposal services for hazardous waste, in particular radioactive waste. With locations in Canada and throughout the western U.S., the company is well-positioned to continue its growth - it hit record earnings in Q3 of 2012. In addition to its strong growth prospects (over the past year the company has climbed from ~$18 to $22.81), the company provides investors with a 3.2% dividend yield. Although the stock is thinly traded, it is well-worth further research by investors looking to add a waste management company to their portfolio.

CSX - CSX presents investors with a play on the long-haul transportation of a wide range of waste materials. The company is the largest rail transporter of waste in the U.S. and, despite it being primarily a rail transportation company, it ranks 27th among U.S. waste companies. As cities expand and current landfills reach capacity, long-haul transportation of waste to cheaper and less regulated locations is becoming an attractive solution. CSX will benefit from this transition and offers investors exposure to a diverse array of industries.

<<<

Cinemark -- >>> The 10 best stocks in the world

Nov 21, 2012

Kiplinger

http://money.msn.com/investment-advice/the-10-best-stocks-in-the-world-1

Stock symbol: CNK

The U.S. theater market may be relatively moribund, but growth prospects are good in emerging markets, where more people are entering the middle class and heading to the movies for entertainment.

Cinemark is one of the primary beneficiaries. The Plano, Texas, company operates 461 multiplexes in the United States, Mexico, Brazil and 11 other Latin American countries. Growth over the past five years has been blistering. In the first half of 2012, revenues jumped 11%, to $1.2 billion, and profits jumped 43%, to $93.7 million.

Cinemark probably can't keep up that pace, but the growth is far from over. The company says it plans to open 11 more theaters in 2012 and has signed agreements to open 16 in 2013 and beyond. Analysts predict that earnings will grow at a 12% annual rate over the next several years. Meanwhile, the stock, at about $24, sells for 15 times estimated 2012 earnings of $1.57 per share.

But what most impresses Osterweis' Berler is that Cinemark is delivering solid results despite a strong dollar (which results in money earned overseas getting translated into fewer bucks). That speaks to the strength of its Latin American business. If the currency head winds abate, Cinemark could clean up, Berler says.

<<<

Waste Management Sector -- >>> 4 Waste Removal Stocks With High Valuations to Avoid Now, 2 to Watch

By Bill Edson

November 6, 2012

Tickers: CVA, RSG, SRCL, WCN, WM

http://beta.fool.com/billedson11/2012/11/06/cashing-trash-are-these-6-junk-stocks-buys/15860/?ticker=SRCL&source=eogyholnk0000001

As dirty as their businesses are, many waste management companies are not trading like garbage. Even the temporary service interruption of Hurricane Sandy did not drop valuations significantly. In fact, in its aftermath many of these stocks are trading at very dear multiples. So do investors today love trash? Investors should exercise care to make sure they are not overpaying for waste industry stocks.

Dumpster Diving

At roughly $32 per share Waste Connections (NYSE: WCN) fails to provide investors a discount for buying a waste management stock. In addition to typical waste services, including waste collection, disposal, and recycling, the company is a leading provider of non-hazardous oilfield waste treatment, recovery and disposal services in several of the most active natural resource producing areas in the United States, including the Permian, Bakken, and Eagle Ford Basins.

Investors can buy more revenues per dollar from the S&P 500, since this stock has a much higher 2.55 price-to-sales ratio, while the index has a ratio of 1.29. Waste Connections shares currently trade at a high 24.01 price-to-earnings ratio, a higher value than the 14.1 price-to-earnings ratio average of the S&P 500 index. Shares trade at a 2.20 price-to-book ratio, which is near the 2.05 average of the S&P 500. The firm is not over-leveraged based on its reasonable 0.54 debt-to-equity ratio.

Covanta (NYSE: CVA) is a waste-to-energy mid cap stock trading at glamor valuations. At a price of roughly $18, Covanta shares are trading at a rich 27.39 price-to-earnings ratio, more than twice the 14.1 average of the S&P 500. Unfortunately, enthusiasm for generating energy trash burning doesn’t make up for the high price-to-earnings multiple.

Covanta’s dividend payments offer little solace. Sure, this stock pays a hefty 3.30% dividend, which is about twice the 10-year treasury yield. However, the firm's 0.85 payout ratio is shaky since this leaves very little room for adverse events and scarce funds for reinvestment to grow the firm.

Shares of Stericycle (NASDAQ: SRCL) are are trading at roughly $95 per share. Investors can buy more than three times the revenues per dollar invested from the S&P 500, since index has a price-to-sales ratio of 1.29 while this stock has a much higher 4.43 ratio. Stericycle shares are trading at a high 31.37 price-to-earnings ratio, a price multiple more than four times the 14.1 P/E ratio of the S&P 500. Even the 5.57 price-to-book multiple of this stock dwarfs the 2.05 S&P 500 price-to-book ratio. This stock is trading like a Silicon Valley growth technology stock, rather than a stock that disposes of healthcare waste.

Shares of Waste Management (NYSE: WM) are also not fairly priced at $32 per share. This stock has been flat over the past year. Waste Management shares are trading at a fair 17.33 price-to-earnings ratio, in line with the S&P 500 average. Shares trade at a 2.43 price-to-book ratio, which is near the 2.05 S&P 500 average. The only price multiple that is in favor of Waste Management is the price-to-sales multiple: the stock's 1.12 P/S multiple is below the 1.29 average of the S&P 500.

Republic Services (NYSE: RSG) has received media attention based on share purchases by Bill Gates. Fortunately, the press coverage has not inflated the price of the stock to insane valuations. At a $26 price level, the firm's 1.27 price-to-sales ratio is in line with today's prevailing market multiples. Republic Services shares are trading at a fair 15.46 price-to-earnings ratio, in line with the S&P 500. The price-to-book multiple of this stock is 1.34, cheaper than the 2.05 S&P 500 average. Republic Services shares are also attractive for income based on a dividend yield of 3.30%, and have a sustainable 0.49 payout ratio.

Investors might want to steer clear of this stock until it grows into its dividend policy. Its high 4.30% dividend yield requires a 0.70 dividend payout ratio. This leaves very little earnings as a cushion for failure and scarce funds for reinvestment.

Fortunately, some waste management firms trade at reasonable valuations. One such stock Darling International, which is trading at a $16 price level. The firm's 1.14 price-to-sales ratio, 14.00 price-to-earnings ratio, and 1.96 price-to-book ratio are midrange in today's market. The firm is also opportunistically growing its food waste recycling empire by acquiring assets.

Investors can also look beyond publicly-traded stocks for reasonably priced investment opportunities in waste management. Small ventures like JunkIt are reinventing the trash business. Rather than focus on repeat utility-like service, JunkIt focuses on special order and one-time disposal jobs around Toronto. The firm offers different levels of service, from dumpster pick up to in-home removal. Growth in this industry can come from other innovative combinations of cleaning services and waste disposal.

Conclusion

Value investors dumpster dive for out-of-favor stocks to find cheaply-valued companies. Often the companies they find are considered disgusting or irrelevant for most investors. Value investments are the cigar butts or garbage in the world of financial assets; but at today’s prices, these garbage companies are not value investments.

Investors seeking value investments should keep an eye on Darling International and Republic Services. They are trading at reasonable valuations and could hit compelling valuations after small price declines.

<<<

US Ecology, Energy Solutions -- >>> There's Controversy Here, but Profits, Too

By Selena Maranjian

October 29, 2012

http://www.fool.com/investing/general/2012/10/29/theres-controversy-here-but-profits-too.aspx

Exchange-traded funds offer a convenient way to invest in sectors or niches that interest you. If you'd like to add some companies focused on nuclear energy to your portfolio, the Market Vectors Uranium+Nuclear Energy ETF (NYSEMKT: NLR ) could save you a lot of trouble. Instead of trying to figure out which companies will perform best, you can use this ETF to invest in lots of them simultaneously.

The basics

ETFs often sport lower expense ratios than their mutual fund cousins. The Market Vectors ETF's expense ratio -- its annual fee -- is 0.60%. The fund is fairly small, too, so if you're thinking of buying, beware of possibly large spreads between its bid and ask prices. Consider using a limit order if you want to buy in.

This ETF's performance is ... well, not so great. It has underperformed the world market over the past three and five years. Still, it's the future that counts much more than the past. And as with most investments, of course, we can't expect outstanding performances in every quarter or year. Investors with conviction need to wait for their holdings to deliver.

Why nuclear?

If you don't like the idea of fossil fuels, or think that their demand and/or supply will run out too soon, you might want to consider nuclear-focused companies. Nuclear power has many detractors, but it also makes sense to a lot of people, and permits are being issued for more plants.

Some nuclear-power-related companies had strong performances over the past year. US Ecology (Nasdaq: ECOL ) surged 35%, for example, focusing on waste treatment, disposal, and recycling, including radioactive materials. In its second-quarter earnings presentation, management noted some work with oil and gas drilling waste, noting that it could become a new market for the company.

Other companies didn't do as well last year but could see their fortunes change in the coming years. Down 24% over the year is EnergySolutions (NYSE: ES ) , another company involved in nuclear clean-ups, even doing some work at Japan's Fukushima disaster site. It does sport positive free cash flow, but it has also been posting net losses in recent years, and carries a lot of debt. Management at the company is rather new, and in a recent conference call, the CEO noted that EnergySolutions needs to be more focused and to lower its costs, among other things.

Down 12% is Exelon (NYSE: EXC ) , America's largest nuclear-power company -- which is also involved in more traditional energy-generation businesses It's not a very volatile stock, but it's trading near a 52-week low, suffering in part because of the relatively high cost of nuclear energy in an environment of very low gas prices. The current situation won't last forever, though, and for patient investors, the stock recently yielded 5.9%. It carries a lighter debt load than many peers as well, and it's expanding into solar and wind power.

Canada-based uranium specialist Cameco (NYSE: CCJ ) shrank by about 8%, but it expects demand to pick up as gas and coal prices eventually rise, and because of new nuclear plants being built. Southern (NYSE: SO ) has permission to build two, and SCANA (NYSE: SCG ) also plans to build two. China is also expected to demand more uranium over time.

<<<

Stericycle -- >>> Stericycle Earnings: Double-Digit Revenue Growth Continues

By Derek Hoffman

October 24, 2012

http://wallstcheatsheet.com/stocks/stericycle-earnings-double-digit-revenue-growth-continues.html/

S&P 500 (NYSE:SPY) component Stericycle Inc. (NASDAQ:SRCL) reported its results for the third quarter. Stericycle manages regulated waste and provides related services. It operates in the United States, Canada, Argentina, Chile, Mexico, Ireland, Portugal, Romania and the United Kingdom.

Earnings season is back and more important than ever. Get our newest CHEAT SHEET stock picks now

Stericycle Inc. Earnings Cheat Sheet

Results: Net income for Stericycle Inc. rose to $65.5 million (75 cents per share) vs. $59.2 million (68 cents per share) in the same quarter a year earlier. This marks a rise of 10.5% from the year-earlier quarter.

Revenue: Rose 14.1% to $480.5 million from the year-earlier quarter.

Actual vs. Wall St. Expectations: Stericycle Inc. reported adjusted net income of 84 cents per share. By that measure, the company beat the mean estimate of 83 cents per share. It beat the average revenue estimate of $467.7 million.

Key Stats:

The company has seen double-digit year-over-year percentage revenue growth for the past five quarters. Over that span, the company has averaged growth of 14.7%, with the biggest boost coming in the third quarter of the last fiscal year when revenue rose 16% from the year earlier quarter.

The company has now seen its net income increase for three consecutive quarters. In the second quarter, net income rose 21.7% and in the first quarter, the figure rose 16.5%.

The company has now surpassed analyst estimates for four quarters in a row. It beat the mark by one cent in the second quarter, by 2 cents in the first quarter, and by 2 cents in the fourth quarter of the last fiscal year.

Looking Forward: The average estimate for the fourth quarter is steady at 86 cents a share. For the fiscal year, the average estimate has been unchanged at $3.27 a share.

<<<

Waste Management Sector -- >>> Has Republic Services Become the Perfect Stock?

By Dan Caplinger

October 25, 2012

http://www.fool.com/investing/general/2012/10/25/has-republic-services-become-the-perfect-stock.aspx

Every investor would love to stumble upon the perfect stock. But will you ever really find a stock that provides everything you could possibly want?

One thing's for sure: You'll never discover truly great investments unless you actively look for them. Let's discuss the ideal qualities of a perfect stock, then decide if Republic Services (NYSE: RSG ) fits the bill.

The quest for perfection

Stocks that look great based on one factor may prove horrible elsewhere, making due diligence a crucial part of your investing research. The best stocks excel in many different areas, including these important factors:

•Growth. Expanding businesses show healthy revenue growth. While past growth is no guarantee that revenue will keep rising, it's certainly a better sign than a stagnant top line.

•Margins. Higher sales mean nothing if a company can't produce profits from them. Strong margins ensure that company can turn revenue into profit.

•Balance sheet. At debt-laden companies, banks and bondholders compete with shareholders for management's attention. Companies with strong balance sheets don't have to worry about the distraction of debt.

•Money-making opportunities. Return on equity helps measure how well a company is finding opportunities to turn its resources into profitable business endeavors.

•Valuation. You can't afford to pay too much for even the best companies. By using normalized figures, you can see how a stock's simple earnings multiple fits into a longer-term context.

•Dividends. For tangible proof of profits, a check to shareholders every three months can't be beat. Companies with solid dividends and strong commitments to increasing payouts treat shareholders well.

With those factors in mind, let's take a closer look at Republic Services.

Since we looked at Republic Services last year, the company hasn't been able to gain back the point it lost from 2010 to 2011. Revenue has remained pretty much stagnant this year, and the stock has actually lost a little ground, falling about 5% in the past year.

Republic often gets lost in the shuffle of the waste industry, which Waste Management (NYSE: WM ) dominates. But the company really gained in importance after its 2008 merger with Allied Waste, which combined the No. 2 and No. 3 players in the industry under one roof. Although revenue hasn't moved much since the merger, cost savings from the merger have helped Republic's margins, which are more than a percent and a half higher than Waste Management's. It also no longer needs to worry about direct competition from Veolia Environment (NYSE: VE ) , which abandoned the U.S. trash collection business in a recent move to reorganize and refocus on its core markets.

Still, Republic can't just stand still in the face of ambitious competitors. For instance, Stericycle (Nasdaq: SRCL ) has focused on the medical-waste-disposal industry, a niche that should provide solid growth for years to come thanks to favorable demographic trends. With margins much higher than traditional waste collection, Stericycle's medical-waste emphasis poses an obstacle to keep Republic from expanding into the lucrative area.

Republic is taking steps to innovate and keep up with improving technology. Its partnership with Clean Energy Fuels (Nasdaq: CLNE ) involves using natural-gas-powered vehicles for waste hauling and other transportation needs. As long as natural gas stays cheap, this move should be a winner for Republic.

For Republic to improve, it needs to focus on finding new sources of revenue and on continuing to work its debt levels down. Slowly but surely, though, Republic has plenty of potential to become a perfect stock down the line.

Keep searching

No stock is a sure thing, but some stocks are a lot closer to perfect than others. By looking for the perfect stock, you'll go a long way toward improving your investing prowess and learning how to separate out the best investments from the rest.

Republic Services' partnership with Clean Energy Fuels is a smart move toward using alternative energy for lower costs and a cleaner environment. With plenty of potential to add its trucks to corporate fleets across the nation, Clean Energy Fuels looks like a promising investment. But is Clean Energy Fuels a buy right now? Read our new premium report on the stock and get the answers you need. Just click here to get started.

<<<

Clean Harbors -- >>> Clean Harbors Signs Definitive Agreement to Acquire Safety-Kleen – A Leading Provider of Environmental and Recycling Services

$1.25 Billion Transaction Will Broaden Clean Harbors Waste Treatment Capabilities and Drive Significant Waste Volumes into Its Disposal Network; Company to Hold Conference Call Today at 9:00 a.m. ET

Press Release: Clean Harbors, Inc.

Mon, Oct 29, 2012

http://finance.yahoo.com/news/clean-harbors-signs-definitive-agreement-110000182.html

NORWELL, Mass.--(BUSINESS WIRE)--

Clean Harbors, Inc. (“Clean Harbors”) (CLH), the leading provider of environmental, energy and industrial services throughout North America,today announced it has signed a definitive agreement to acquire Safety-Kleen, Inc. (“Safety-Kleen”), the largest re-refiner and recycler of used oil in North America and a leading provider of parts cleaning and environmental services. Under the terms of the agreement, Clean Harbors will purchase Safety-Kleen in an all-cash transaction valued at $1.25 billion. The acquisition is subject to approval by U.S. and Canadian regulators, as well as other customary closing conditions. The transaction is expected to be completed by year-end.

Based on the current operating and anticipated future performance of Safety-Kleen, Clean Harbors expects the acquisition will be immediately accretive, excluding one-time fees and acquisition-related expenses. The Company has received a financing commitment from Goldman Sachs Bank USA, but is currently considering several financing options for the transaction that may include a combination of existing cash, debt and equity.

The transaction will enable Clean Harbors to:

• Penetrate the small quantity waste generator market

• Broaden its waste treatment capabilities to include re-refining waste oil and expanded solvent recycling capabilities

• Drive substantial increase in waste volumes into its existing waste disposal treatment network

• Capitalize on the growing demand for recycled products including re-refined oil

• Enhance its commitment to sustainability

• Leverage the combined sales forces to maximize cross-selling opportunities

• Add an immediately accretive business to accelerate growth

• Leverage operating efficiencies through the combined company

• Add to its strong cash flow generation

“This acquisition is a landmark achievement for Clean Harbors that we believe will build significant long-term value for our shareholders,” said Alan S. McKim, Chairman and Chief Executive Officer. “Safety-Kleen is a recognized leader in the environmental services field with a corporate heritage that dates back nearly 50 years with a strong service culture. We have the benefit of a long and positive relationship with Safety-Kleen as a result of our acquisition of its Chemical Services Division a decade ago. Safety-Kleen has been a large customer of our environmental services business. The addition of its entire organization aligns perfectly with our acquisition strategy of expanding our Environmental Services business in North America. Safety-Kleen is the largest collector of waste from the small quantity generator market and the leader in re-refining used oil in North America.”

“Adding Safety-Kleen’s re-refining and recycling capabilities to our current offerings will enhance the sustainability options available to our existing customers and significantly broaden the range of services we can offer customers of both companies,” McKim said. “Safety-Kleen services over 200,000 customer locations, and we envision substantial cross-selling opportunities with its extensive customer base. These Safety-Kleen customers will now have direct access to our industry-leading network of disposal facilities.”

Bob Craycraft, Safety-Kleen’s President and CEO, said, “We believe this transaction represents an opportunity to combine two truly dynamic organizations. Clean Harbors’ history of innovation and commitment to sustainability mirrors our philosophy of delivering our customers the latest in re-refining, recycling and hazardous waste management, as we continually upgrade the environmental services we offer. Safety-Kleen’s talented group of employees are joining an exceptional, well-managed company with a track record of success. At the same time, Safety-Kleen’s customers will benefit from access to Clean Harbors’ expansive suite of environmental, energy and industrial services.”

With more than 200 locations throughout North America, Safety-Kleen services commercial and industrial customers in the U.S., Canada and Puerto Rico. Safety-Kleen currently employs approximately 4,200 employees and operates a sizeable service fleet of more than 2,300 vehicles and 1,000 rail cars. Safety-Kleen’s portfolio of assets include the largest oil re-refinery in the world at its East Chicago, Indiana location and the largest re-refinery in Canada at its Breslau, Ontario location. Currently, the company collects approximately 200 million gallons of used oil annually, the majority of which it returns to the marketplace as reusable motor oil. In 2011, Safety-Kleen managed hazardous and non-hazardous waste volumes equivalent to approximately 680,000 55-gallon drums. Safety-Kleen generated revenues of $1.3 billion and adjusted EBITDA of $161 million in 2011.

McKim said, “Safety-Kleen’s professional approach toward compliance, health and safety excellence, and commitment to customer service is closely aligned with Clean Harbors’ devotion to those very same principles. Safety-Kleen is led by a first-class management team and we are excited to work together with Bob and his team to complete this merger. We are confident that working together we can capture substantial synergies between our two organizations and the significant upside potential of the combined company.”

“Looking ahead, our focus will be on gaining the necessary approvals, planning our integration and completing the acquisition by year-end. We appreciate the strength and intrinsic value of the Safety-Kleen brand. Therefore, we intend to maintain its brand going forward and operate its network of branch locations as a subsidiary. We look forward to welcoming Safety-Kleen’s employees into the Clean Harbors family. This transformative merger of two great companies will further reinforce our position as the premier provider of environmental, energy and industrial services in North America,” McKim concluded.

Davis, Malm & D'Agostine served as legal counsel to Clean Harbors. Credit Suisse served as lead financial advisor to Safety-Kleen. Morgan Stanley and Houlihan Lokey provided additional financial advisory support. Skadden, Arps, Slate, Meagher & Flom served as legal counsel to Safety-Kleen.

Third-Quarter Results

Clean Harbors will be announcing its third-quarter results on its regularly scheduled date, which as previously announced will be Wednesday, November 7. There will be no update on its quarterly financial results provided in conjunction with today’s announcement.

Conference Call Information

Management will hold a conference call today to discuss the Safety-Kleen transaction at 9:00 a.m. ET. Those who wish to listen to the webcast of the call and view the accompanying slides should visit the Investor Relations section of the Company’s website at www.cleanharbors.com. The live call also can be accessed by dialing 201.689.8881 or 877.709.8155 prior to the start of the call. If you are unable to listen to the live call, the webcast will be archived on the Company’s website.

About Safety-Kleen

Safety-Kleen is a leading North American used oil recycling and re-refining, parts cleaning and environmental solutions company, with approximately 4,200 employees serving more than 200,000 customer locations in the United States, Canada and Puerto Rico. Safety-Kleen provides a broad set of environmentally-responsible products and services that keep North American businesses in balance with the environment. Safety-Kleen is owned by a group of investors including Highland Capital Management, L.P. of Dallas, Texas, its largest investor. For more information about the company, please visit www.safety-kleen.com.

About Clean Harbors

Clean Harbors is the leading provider of environmental, energy and industrial services throughout North America. The Company serves more than 60,000 customers, including a majority of the Fortune 500 companies, thousands of smaller private entities and numerous federal, state, provincial and local governmental agencies.

Headquartered in Norwell, Massachusetts, Clean Harbors has more than 200 locations, including over 50 waste management facilities, throughout North America in 38 U.S. states, seven Canadian provinces, Mexico and Puerto Rico. For more information, visit www.cleanharbors.com.

<<<

Rollins -- >>> Rollins Inc.’s Orkin unit has opened its first South American franchise in Santiago, Chile.

Jacques Couret

Atlanta Business Chronicle

August 7, 2012

http://www.bizjournals.com/atlanta/news/2012/08/07/orkin-now-open-in-chile.html?ana=yfcpc

Rollins Inc.’s Orkin unit has opened its first South American franchise in Santiago, Chile.

The new franchise also marks Atlanta-based Orkin’s 22nd international franchise.

Orkin Santiago Chile will offer commercial, residential and termite pest control services.

“We are proud to bring Orkin services to South America, and especially to Santiago, Chile, the country’s capital and largest city,” said Tom Luczynski, Orkin vice president of U.S. and international development and franchising. “There is a wide variety of climates throughout Chile, from one of the world’s driest deserts to subtropical climates. Each creates unique pest problems throughout the year, so customers will benefit from Orkin’s experience.”

Atlanta-based Rollins (NYSE: ROL) owns and operates Orkin, HomeTeam Pest Defense, Western Pest Services, PCO Services, The Industrial Fumigant Co., Waltham Services, Crane Pest Control and TruTech. It has franchises in the United States, Canada, Central America, the Caribbean, the Middle East, Asia, the Mediterranean, Europe and Africa.

Rollins recently reported its second-quarter profit was up about 7 percent to $33 million.

<<<

GESI - Green Energy Solution Industries, Inc

Chart shows continued accumulation and positive CMF. W%R did not drop below -80, showing signs of uptrend.

http://stockcharts.com/h-sc/ui

News is pending any day. Take a look at GESI.

GESI Announces Major Development for $45 Million Funding of its Alternative Energy Project on StockTradersTalk.com Radio Show

http://ih.advfn.com/p.php?pid=nmona&article=53457782

A system for swing trading the market (see below), using the 5 day and 13 day exponential moving averages.

It's extremely simple - you buy when the 5 day EMA (blue line) crosses above the 13 day EMA (red line), and vice versa for selling/shorting. As long as the blue line is on top you stay long, and when the red line is on top you stay out or stay short.

It appears to work well, though if the market gets choppy you may have to get in and out a couple times before the trend is established. This looks a lot easier than trying to trade individual stocks and chart patterns -

10 day -

5 weeks -

3 months -

3 months -

Informatica -- >>> Informatica Slumps After Quarterly Sales Miss Estimates

By Kathleen Chaykowski - Jul 6, 2012 5:00 PM ET

http://www.bloomberg.com/news/2012-07-06/informatica-slumps-after-quarterly-sales-miss-estimates.html?cmpid=yhoo

Informatica Corp. (INFA) slumped the most in 11 years after the provider of data-integration software said weak demand in Europe caused an unexpected drop in quarterly sales and profit, sending down other software stocks.

The shares fell 28 percent to $31.39 at the close in New York, for the biggest daily decline since July 2001. The Redwood City, California-based company had risen 17 percent this year through yesterday.