News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

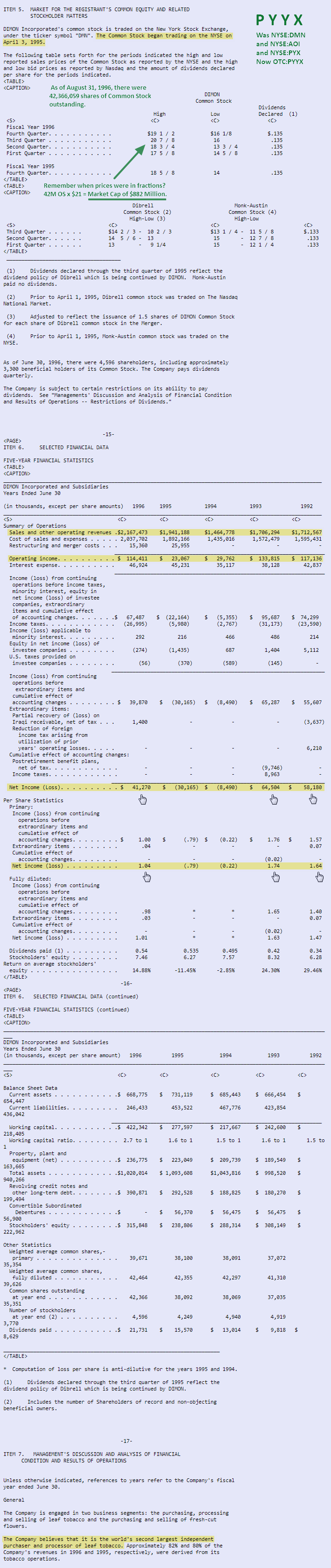

Market cap = $30.5 million now. Lost $1.15 Billion in value. Some big shoes to fill there...let's get going... :)

Market cap was $1.18 Billion in 1998.

They did a reverse split 1:10 in June 2015 so the $26.50 high, below in the table, is now $265 on a chart if one could find one...symbol was DMN (DIMON)...I'd love to see a chart with the complete history...price shows $265 in 1998 on an adjusted price reflecting the 1:10 split...adjusted OS equivalence would be 4.45M.

Market cap was $882 million...

...27 years ago.

We can do this...

Net Income over $50 million a couple years there (1993 $64.5M and 1992 $58M).

We do $50 million Net Income (PROFIT) next year, 2024, beginning April 2023...

$50M Net Income / OS 25M = $2 EPS x PE Ratio 15 = $30 price per share for a market cap of $750 million. Still undervalued. 25 bagger from here, tho, $1.20.

I think we have Net Income PROFIT this Q4 ending March 31st. Maybe even enough to make us profitable for the year.

Link > 10-K 1996

Someone was selling under $32M market cap just yesterday... ;)

Except I doubt highly you'll find a willing seller at that price.

•••••••••• HOLY SMOKES ••••••••••

FLOAT 8.5M | OS 25M | MARKET CAP $32M | TURNING AROUND NOW

Link to PR >> Pyxus-International-Inc.-Reports-Fiscal-Year-2023-Third-Quarter-Results

@elonmusk please review my proposal and wire the loan $32,000,000 to my account. 25% + principal will be repaid as soon as I buy Pyxus Intl Inc (PYYX) for it's market value ($32M) and I sell all the assets ($1.63 Billion) and pay off all the creditors/debt ($1.474 Billion)...

Stockholders' Equity of $156 million. Musk gets $40 million leaving me $116 million to cover the transaction fees and hassles, lol... :)

OS 25,000,000 | Price $1.28 | Market Cap $32,000,000 | SH Equity per share $6.24

Yeah, I was just using the P:S calculation from below... it's not my number. I wouldn't use price to sales for this company. The numbers get just too crazy for me to think anyone else will use them. I like to take the most conservative numbers and work from there. That's why I think the EV:EBITDA numbers are most appropriate, generally speaking... it's a measure of valuation that captures all the debt and all the equity and compares it against what is basically a cash operating income number...

That's all more or less correct, now let's take MO as a comparison... they have an EV:EBITDA of 12.2x.

So, just for the sake of illustration, if we say PYYX is worth not 9x but 12x... then we have to close a 3x EBITDA gap in the valuation.

The debt is more or less a fixed part of the capital structure, so all the incremental closing of the gap accrues to the equity portion...

so, to keep it simple, let's say the TTM EBITDA is $100 mm... and we need to get from 9 to 12, so we have to add $300 mm of valuation to the equity portion (again, because debt is debt and it's fixed).

So to get there, $32 million has to become $332 million... and there you have it.

With profit of $300 million ($75M per Q) EPS would be $12 ($300M / OS 25M). Multiplied by an industry average PE Ratio of 15 = $180 per share.

$180 x 25M OS = $4.5B market cap.

That would align with price-to-sales ratio of 2.25. Sales of $2B x 2.25 = $4.5B market cap.

Divide the above by 10 and you get $30M profit and $18 per share.

2-3 years $100+ pps very possible. JMO

Need to lower that interest expense which is running at approximately $120 million a year! Get the price up to $40 per share and sell another 25M shares...NO DEBT. NO INTEREST.

pyyx would have to be over $100.00 per share to achieve PSR of 2.3

price-to-sales ratio is now 2.37.

https://csimarket.com/Industry/industry_valuation_ttm.php?ps&ind=508

PYYX sales of $2B x price-to-sale ratio of 2.37 = $4.74B market cap using this valuation metric.

2.37 ratio is the current average price-to-sales ratio for the Tobacco Industry (use link above).

psr

25,000,000 X share price $1.20= $30,000,000

rev est 2 billion and i minus out the 700 million in debt=$1.3 billion

divide

results .023 In my calculation ( not sure why or how you get 2.3?

regardless we both know how cheap pyyx is

snakess, it was from my post...price-to-sales was 2.35 when I calculated that.

PYYX Sales $2B FYE 2023 March 31st x 2.35 (price-to-sales ratio) = $4.7B...

https://investorshub.advfn.com/boards/read_msg.aspx?message_id=171365432

SSEA, thanks for your input. I'm not familiar with this valuation metric:

EV:EBITDA (EV/EBITDA)

So I did a little research :)

EV is Enterprise Value.

EV = Market Cap + Debt - Cash

EV = $32M + $1.086B - $218M

EV = $0.9B or $900M

EV/EBITDA

Since EV/EBITDA is a valuation metric, lower enterprise multiple can be indicative of the company being undervalued. Usually, EV/EBITDA values below 10 are seen as desirable (undervalued).

Based on our expectations for continued improvement year-over-year, we have revised our expected fiscal 2023 sales to be between $1.85 billion and $2.00 billion and our adjusted EBITDA* expectations to be between $140 million and $155 million.

ss~ not sure your calculations are correct $1.20 X est. $2 billion and then sub out $700 million debt and divide by 25 million shs= $68.00

not sure where the $4 billion comes from

regardless when you see all these hyped over priced companies that do not compare to pyyx it is hard to believe or even understand.

I do like this. I would say, however, that it's almost always best to use enterprise value as a starting point because it smooths out the differences in capital structure (debt vs. equity) between the company you are valuing and the comparable you are valuing against.

So, for instance...

In your price to sales calculation (not at all my preferred, FWIW), you'd want to remove something like $700 mm of LT Debt from the $4.7 billion and then it's $4 billion over 25 mm shares, which is $160 not $188.

I tend to use EV:EBITDA most commonly... that way you get the total marketplace value against something very close to cash operating income... and you've eliminated all the noise that come form variations in capital structure among the comparables.

50k buyer back on bid @ $1.20 w/ 46k...

I did notice a huge 49k bid all day on Friday ! I first thought it was a set up for a cross by an institution, but that proved wrong. if i had extra funds i would surely add and wait for the pot of gold pending.

Great post SSEA...

Had to re-post it, added the red text:

I think if MO (Altria Group NYSE) wanted to own these assets in some kind of vertical strategy that they probably had that opportunity when the Company was in the bankruptcy process. I think the reason they don't want it is because to run this business at scale, you have to serve a diversified customer base and MO doesn't want to be in the position of having to serve it's competition as customers in any part of the business and vice-versa.

I think the very simple situation is that this company is necessary. The big guys don't want to deal with farmers in asia any more than they want to speak to a house subcommittee on the dangers of e-cigarettes....lol, good one SSEA

That means that PYYX is pretty solid with respect to customer relationships/support/receivables/etc. It's yet another reason the breakdown ratio of the enterprise valuation makes no sense of any kind whatsoever.

I did read your write up snakess. Well done. There were a few other 50k buys of PYYX shares, 2 in one day here https://investorshub.advfn.com/boards/read_msg.aspx?message_id=171311356 and then another the next day...think this is the 5th 50k purchase for someone(s)...all of the bids have started at 50k, closing in on a quarter million dollars @ $1.20...nice...smart...a 50 bagger turns that $250,000 investment into $12,500,000 in a couple/few years...JMO

current PSR is .02 a value of 1 cheap value of 3 fairly valued

as mentioned maybe one of these days the redditt herd will trip over it bid up to $20

helter i wrote this stock up in newsletter Feb 20th

https://saadvisory.com/update/archive/Feb-20-2023.htm

Thanks snakess, SSEA, think you'll like this one...

••• PYYX Valuations •••

First, let's do Price-to-Sales.

PYYX Sales FYE March 31st = $2B

Price-to-Sales Ratio for the Tobacco Industry Q4 (TTM) is 2.35* *changes daily

PYYX Sales $2B x Price-to-Sales 2.35 = $4.7B

$4.7B market valuation (market cap) / 25M OS = $188 per share!

Current Price is $1.28. $188 is a 147 bagger from here!

PYYX will be my first 100+ bagger :)

https://csimarket.com/Industry/industry_valuation_ttm.php?ps&ind=508

Second, let's use Stockholders' Equity for PYYX valuation.

Stockholders' Equity = Total Assets ($1.631B) - Total Liabilities ($1.475B)

Stockholders' Equity was $156 million end of Q3.

$156M / 25,000,000 OS = $6.24 per share!

Current Price = $1.28. $6.24 is a 5 bagger from here!

Thirdly, we will use P/E Ratio for PYYX's valuation.

As of end Q3 PYYX is losing money ($18.53M for 3 Qs, $2.33M Q3, $1.54M Q2, $14.66 Q1).

They can swing that to plus $25 million Net Income (gain) by having a PROFITABLE Q4 (Net Income) of $43 million.

Coincidently, ;) this scenario means PYYX would have Net Income for Fiscal Year 2023 (FYE March 31, 2023) of $25,000,000.

$25,000,000 Net Income / 25M OS = $1 EPS (earnings per share).

PE Ratio for the Tobacco Industry Q4 (TTM) is 15.3* *changes daily

PYYX EPS $1 x PE Ratio 15.31 = $15.31 per share!

Current Price is $1.28. $15.31 is a 12 bagger from here!

https://csimarket.com/Industry/industry_valuation_ttm.php?pe&ind=508

SSEA your reasoning sounds reasonable and i would agree with you. When i was on the call they mentioned the stock does not trade, we see that is really not an issue. 75% of the 25 million shares outstanding are owned by institutions . If the management does not have interest in the public company then they should go private. Technically they have the cash to take the company private at a sizable premium above the current level of trading.

Don't think that is going to happen either. I BELIEVE if they can show a net income /share this stock will appreciate.

Anything is possible, but regardless this may very well be the cheapest stock in the world. ( except for Russia Oil giants, which have been destroyed)

I did notice a huge 49k bid all day on Friday ! I first thought it was a set up for a cross by an institution, but that proved wrong. if i had extra funds i would surely add and wait for the pot of gold pending.

I think if MO wanted to own these assets in some kind of vertical strategy that they probably had that opportunity when the Company was in the bankruptcy process. I think the reason they don't want it is because to run this business at scale, you have to serve a diversified customer base and MO doesn't want to be in the position of having to serve it's competition as customers in any part of the business and vice-versa.

I think the very simple situation is that this company is necessary. The big guys don't want to deal with farmers in asia any more than they want to speak to a house subcommittee on the dangers of e-cigarettes....

That means that PYYX is pretty solid with respect to customer relationships/support/receivables/etc. It's yet another reason the breakdown ratio of the enterprise valuation makes no sense of any kind whatsoever.

For what it's worth, I'd be looking at:

The EBT number of $10.3 million and adding back the $4.4 million of non-cash depreciation expense... that's pre-tax cash earnings of $14.7 million.

and, even better....

The $176 million of operating cash flow they generated in the third quarter.

The idea that you think they only got close is because they did a shit job of explaining themselves in the 3Q disclosures.

$176 million of operating cash flow. In the quarter. $176 million.

Helter,

It honestly shouldn't matter. There is no earthly way that this enterprise valuation makes any sense at all. I've been in the institutional markets for 20 years and I've never seen anything like it. If it was going into liquidation, that's what would've happened. It on the OTHER side of chapter... yet, for some reason, no one wants to shake the thing loose and do actual price discovery.

I'm not sure if it's because it's a tobacco play, because it's just totally forgotten about, because they are stuck on the Pinks, because the debt holders destroyed the liquidity (and should've taken it private probably) to a degree that makes it fully uninteresting... or some other reason that won't hold for very long... but there's just no earthly way.

The simple, inescapable fact is that this company is a meaningful and important part of the global supply chain for some very powerful customers who do not want to do what they do. It's been that way for about a century and it doesn't appear that anyone wanted to change it enough to do more than a simple reorganization.

Owning the equity with this ratio in the capital structure is about the most powerful option-like trade I've ever seen. I know it sounds crazy, but the thought that this stock could go up thousands of percent is actually pretty rational.

helter: i like your work! i am assume you saw the recommendation via saaadvisory.com feb 20th. Interesting today a 49k bid ( i first thought it was a cross being planned, i guess i was wrong. many trades of large blocks have been cross within institutional holders. Somehow need to get wallstreetbets herd to view. ( only problem with them is that most are clueless about fundamentally cheap stocks). This stock even with the small loss, but not including the comprehensive income of around .09 vs other accounting procedures yielded a (.09) loss.

should be $5. minimum right now

••• P Y Y X •••

OS 25M | Market Cap $32M | Sales $2B | Cash $216M | Stockholders' Equity $156M | Equity Per Share $6.24

So close, so damn close. To turning a PROFIT in Q4 (period ending March 31st). That will blow the roof off for PYYX and unleash this hidden gem to the investment world!

Lost $2.33 million in Q3, lost $1.537 million in Q2, lost $14.66 million in Q1...come on Q4!

Need Q4 profit of over $19 million (net loss total is $18.533 million first 3 Qs, 9 months) to record a PROFIT for the entire fiscal year (ending March 31st).

This is VERY doable, folks. Here's a proforma income statement that I put together showing what it will take...more or less, still a work in progress, I'll update/explain it soon, some numbers, calcs, are squirrelly, lol, so don't base any investment decisions on this:

From PYYX Q3 10-Q

Link >> PYYX Q3 10-Q

Market cap $30,000,000 Sales $2,000,000,000 $PYYX

There isn't one, snakess. Pyxus (PYYX) will turn into The Darling of iHub and will be listed on the top of the Top 10 Forums, probably for 2-3 years... :) ...on our trip to $100 (market cap ~$2.5B)...

My "marketing girls" are prepared for the ride... ;)

show me a cheaper stock than pyyx

It is just a matter of time before either bought out, Wallstreetbets gets a whiff or brokerage firm hops on board for a money raise ( even though they don't need it ) something will change and this stock will fly. Even though upon refi their debt , which might have cost them more they raised prices by 25%. I just read Cuba's tobacco business has serious issues. With the closure of Chine over- they will be a driver in tobacco ussage.

It would be the perfect vertical acquisition for MO

Cheap Cheap Cheap

Sales $656 million. Cash $216 million. Burn rate last Q $2.33 million. $PYYX

5 bagger to Stockholders' Equity value! :)

Stockholders' Equity = Total Assets ($1.63B) minus Total Liabilities ($1.475B).

Stockholders' Equity $155,746,000 / 25,000,000 OS = $6.23 price per share!

PYYX could sell all their assets, pay off all their liabilities, and have $6.23 per share left for the stockholders.

Market Cap @ price per share $1.20 = Market Cap of $30,000,000.

Stockholders' Equity of $156 million. Cash $216 million. Property, Plant & Equipment $137 million...

Accumulate (down here) with abandon. :)

Another 50k on best bid @ 1.20 $PYYX

Thump thump...2 50k trades @ 1.25 $PYYX

hard to believe that investor types( not sure they really are investors because most are clueless concerning Benjamin Graham investing)If you or had the slightest knowledge about fundamentals you would not avoid pyyx . prs. ebidta, price to bk, cf and est. PE for fiscal 24.

this newsletter wrote a very compelling recommendation ( non paid)

How many ev companies have 2 billion in sales and trading at $1.39 ZERO

It is always about the herd mentality.

https://saadvisory.com/update/archive/Feb-20-2023.htm

Almost one TRILLION dollars and PYYX has ONLY 2 billion of it, 1/500th of this huge market. .2%. Point 2 percent.

$PYYX

The global tobacco market size was valued at USD 849.9 billion in 2021 and is expected to expand at a compound annual growth rate (CAGR) of 2.4% from 2022 to 2030. The demand has been sustained by the growing number of smokers in the developing regions of Asia and Africa. The extensive marketing campaigns run by the major companies have also been a significant factor sustaining the industry. The industry is witnessing a trend of new product launches which intrigues consumers to consume tobacco and thereby drive market growth.

The COVID-19 pandemic has had a significant effect on the consumption of tobacco. Smoking is perceived to be extremely deadly, as COVID-19 is a respiratory disease, and smoking only aggravates the situation. However, trends across the globe revealed that lockdown-induced stress only led to increased consumption. The addition of new smokers remained relatively low during this period. However, the industry is expected to benefit from the consumers who resorted to excessive smoking during the pandemic, as it is expected to have cultivated a new habit among them.

The addition of a new range of tobacco products shows a moderate increase in both the number of individuals who smoke and the percentage of people who try the new products. The use of intriguing advertising strategies has produced considerable results and has proven to be a means of remaining competitive and sustaining market dominance. For instance, specific products are promoted and advertised more intensely to specific demographic or racial groups.

According to the Centre for Disease Control and Prevention (CDC) estimates, companies such as Marlboro, Newport, and Camel, whose marketing campaigns specifically targeted the youth, were the highest marketing spenders. This led to them being the most preferred brand by the youths. Most people have seen tobacco as a significant part of their life over the previous decade. This factor is expected to drive the overall product demand in the forthcoming years.

The companies are spending huge on marketing campaigns to offset the negative impacts faced by the tobacco industry due to increased health consciousness among consumers. According to the CDC data, in 2019, USD 8.9 billion was spent by large companies on marketing smokeless tobacco and cigarettes in the U.S. This amount breaks down to USD 22.5 million per day or almost USD 1 million per hour. The companies have spent extensively on discounts, thereby increasing their market penetration and sustaining growth.

Tobacco consumption has been on the decline in developed and wealthy countries across the globe, due to the higher level of awareness among the population regarding the ill effects of its consumption. To maintain demand in such countries, the companies are introducing new products that are significantly less harmful than conventional products. The market has witnessed the introduction of new nicotine products and this category has been dubbed as new, alternative, or novel tobacco. These items are now referred to as Next-generation Products (NGP) by the tobacco control community.

Major companies have diversified their strategies to develop NGPs. Phillip Morris International, for instance, has carried out several investments in heated tobacco products. The company is strongly focused on delivering smoke-free heated tobacco products, as it envisions this category to be a game-changer in the industry. The IQOS technology is an integral part of Philip Morris's efforts to disrupt itself and become a smoke-free company by 2025. The product already accounted for 23.8% of the company's revenue in 2020. IQOS is a line of heated products developed as part of its "heat-not-burn" promotion. According to IQOS's 2020 Annual Report, the company has 17.6 million users, with 12.7 million of them switching to IQOS and quitting smoking.

Product Insights

Cigarettes captured the majority share of the market in 2021, accounting for nearly 86% of the overall revenue. Cigarette consumption has remained stable due to the introduction of flavored, and menthol cigarettes. It can also be attributed to the availability of small cigarettes that facilitate smaller amounts of tobacco consumption for smokers who wish to cut down on their smoking habit. Cigarettes have an inelastic demand, which is a major factor that has driven market growth despite the heavy taxation that has been levied across the globe.

The rising popularity of partying and pub culture among millennials and working-class communities has especially fueled the demand for flavored and unflavored cigarettes around the world in recent years. Furthermore, emerging economies such as India and Thailand are seeing a significant increase in cigarette demand as a result of rising youth populations in these countries. According to the Global Adult Tobacco Survey carried out in 2017, India had the second largest number of smokers in the world with 267 million tobacco users.

The tobacco market is expected to benefit greatly from the launch of next-generation products, which is expected to become the fastest-growing segment. Major companies are investing heavily in the development of NGPs as they see this category as severely overpowering other products in the market. For instance, Japan Tobacco Inc. launched its Ploom X next-generation heated device in August 2021. Ploom X is the JT Group’s next-generation device for heated tobacco sticks. It is also equipped with Bluetooth functionalities that connect with the user's smartphone, enabling them to check the battery status, lock & unlock the device, and such other functions.

Distribution Channel Insights

The offline channel led the market and accounted for the largest market share of more than 89% in 2021. It is projected to continue leading the market during the forecast period. The segment includes all retail outlets such as hypermarkets, supermarkets, convenience stores, and departmental stores. Consumers prefer these stores as they offer considerable discounts. Location proximity of these stores facilitates immediate demand fulfillment for tobacco consumption, which is also expected to drive the growth of the segment.

It'll come. Foolish sellers down here, don't they know that PYYX is going to turn a PROFIT this quarter (Q4 FYE 2023, March 31st 2023)??? Profit this Q, that's my premonition and prediction. I'll post the proforma when I get some spare time... :)

These are BARGAIN prices. Any thing under $10 is, really. Over $16 by Christmas 2023! :)

$PYYX 1.32 x 1.35

recommendation on pyyx

https://saadvisory.com/update/archive/Feb-20-2023.htm

Tiny tiny FLOAT >> 8,500,000 << $PYYX

Related Party Transaction

OS 25,000,000 | FLOAT 8,500,000 (25M OS - 16.5M)

Based on a Schedule 13D filed with the SEC on September 3, 2020 by Glendon Capital Management, L.P., Glendon Opportunities Fund, L.P. and Glendon Opportunities Fund II, L.P., Glendon Capital Management, L.P. reported beneficial ownership of 7,938,792 shares of the Company’s common stock, representing approximately 31.8% of the outstanding shares of the Company’s common stock. Based on Form 4 filed with the SEC on July 15, 2021, as well as Schedule 13D filed with the SEC on September 3, 2020, by Monarch Alternative Capital LP, MDRA GP LP and Monarch GP LLC, Monarch Alternative Capital LP reported beneficial ownership of 6,140,270 shares of the Company’s common stock, representing approximately 24.6% of the outstanding shares of the Company’s common stock. Based on a Schedule 13G/A filed with the SEC on February 10, 2022 by Owl Creek Asset Management, L.P. and Jeffrey A. Altman, Owl Creek Asset Management, L.P. is the investment manager of certain funds and reported beneficial ownership of 2,405,287 shares of the Company’s common stock on December 31, 2021, representing approximately 9.6% of the outstanding shares of the Company’s common stock. Pursuant to a Shareholders Agreement dated as of August 24, 2020 (the "Shareholders Agreement") among Pyxus and certain of its shareholders, including Glendon Capital Management L.P., on behalf of its managed funds and accounts, and Monarch Alternative Capital LP, as investment manager of Monarch Special Opportunities Master Fund Ltd, Monarch Debt Recovery Master Fund Ltd and Monarch Capital Master Partners IV LP, Holly Kim and Patrick Fallon were designated to serve as directors of Pyxus and each continues to serve as a director of Pyxus. Ms. Kim is a Partner at Glendon Capital Management L.P. and Mr. Fallon is a Managing Principal at Monarch Alternative Capital LP.

$PYYX

Vol 126,430, Dollar Vol $192,452, Vwap $1.522, Last $1.52

Get that share price up around $10-$20 and PYYX could sell 10 million shares for $200 million and pay off 1/2 their long term debt (or bank loans) lower the interest expense which is a killer...and on our way to $100 pps :) ...just a thought...

Have a great weekend back at ya, hb90! Great day here...volume and dollar volume coming in!

Another good day here... most volume accumulated at 1.50+. Once those shares get soaked up she flies. Good amount of shares came from the ask. Have a great weekend

Looks like around 1 million, hb90, no one knows about this TURNAROUND GEM!

Volume has always been NONEXISTENT for PYYX.

Low low OS 25,000,000, low FLOAT, and UNDISCOVERED (the turnaround by the new CEO).

Once solidly profitable (soon, I believe) PYYX could command a price-to-sales evaluation of 2x sales = $4 billion / 25 million OS = $160 price per share...!

Remember, QUARTERLY chart, the bars are 3 months each. VIRGIN.

Lots of shares purchased below .50 over the last year. Churn through those sellers and we rock n roll. 3 day weekend for more folks to find this and get more lovin next week

|

Followers

|

38

|

Posters

|

|

|

Posts (Today)

|

0

|

Posts (Total)

|

1505

|

|

Created

|

09/20/18

|

Type

|

Free

|

| Moderators | |||

"The world’s second-largest independent tobacco leaf dealer has been busy buying stakes in companies and forming joint ventures in emerging markets. The strategy is to sprinkle its expertise in agronomy over these businesses while expanding into such areas as liquids for vaping and Canadian cannabis."

Pyxus International, Inc., an agricultural company, engages in the provision of various agricultural products, ingredients, and services to businesses and customers. With 145 years’ experience delivering value-added products and services to businesses and customers, we are a trusted provider of responsibly-sourced, independently-verified, sustainable and traceable products and ingredients.

Pyxus International offers high-quality, distinct brands and products on the cutting edge of innovation and entrepreneurship in the E-Liquids, industrial hemp, legal cannabis and leaf tobacco industries.

Pyxus PowerPoint Presentation

The company was formerly known as Alliance One International, Inc. and changed its name to Pyxus International, Inc. in September 2018.

Pyxus International, Inc. was founded in 1873 and is based in Morrisville, North Carolina.

Pyxus International - pyxusintl.com

Global agricultural company w/ 145 years' experience as a trusted provider of responsibly sourced, independently verified, sustainable and traceable products & ingredients. Its CBD, E-Liquids, and cannabis companies are:

Bantam - bantamvape.com

Premium line of E-Liquids offering natural-tasting, artisanal, and real flavors, built from scratch using only food-grade materials that are fully FDA-compliant.

Criticality - criticalitync.com

North Carolina-based agricultural hemp company w/ a science-based approach to the extraction, refinement & formulation of high-quality, transparent industrial hemp derived products.

FIGR - figr.com

Locally grown, hand-crafted, high-quality cannabis that is fully traceable from source to market. Only available in Canada.

Humble - humblejuiceco.com

Humble Juice E-liquids was born from the single idea that hardworking, honest people can make high-quality juice at an affordable price. We are The Humble Juice Company. We are Made in The USA and we are proud of it

Korent - korenthemp.com

Expertly-crafted & responsibly-produced consumer cannabidiol (CBD) products, offering a natural path to improved well-being.

NICRIV - nicotineriver.com

Mixing flavor concentrates is an excellent way to make unique and layered flavors, but sometimes you just want something new straight out of the bottle. That’s why we’ve searched the industry for the best flavor concentrates and mixed them in-house for you. Nicotine River flavor concentrates are original, complex and verifiably tasty.

Purilum - purilum.com

E-Liquids & CBD flavoring and production with decades of scientific experience with complete traceability and batch labeling & an FDA-compliant predicate flavor library.

SENTRI - pyxusintl.com/sentri

SENTRI provides verifiable, accurate and comprehensive information on our products and methods, from source to customer, ensuring confidence-inspiring product integrity, while empowering industry-leading business insights. Covering 300,000 farmers across 5 continents, this platform combines technology, people, and processes to protect the integrity of our products.

Brands: Bantam, Criticality, FIGR, Humble, Korent, NICRIV, Purilum and SENTRI.

![]()

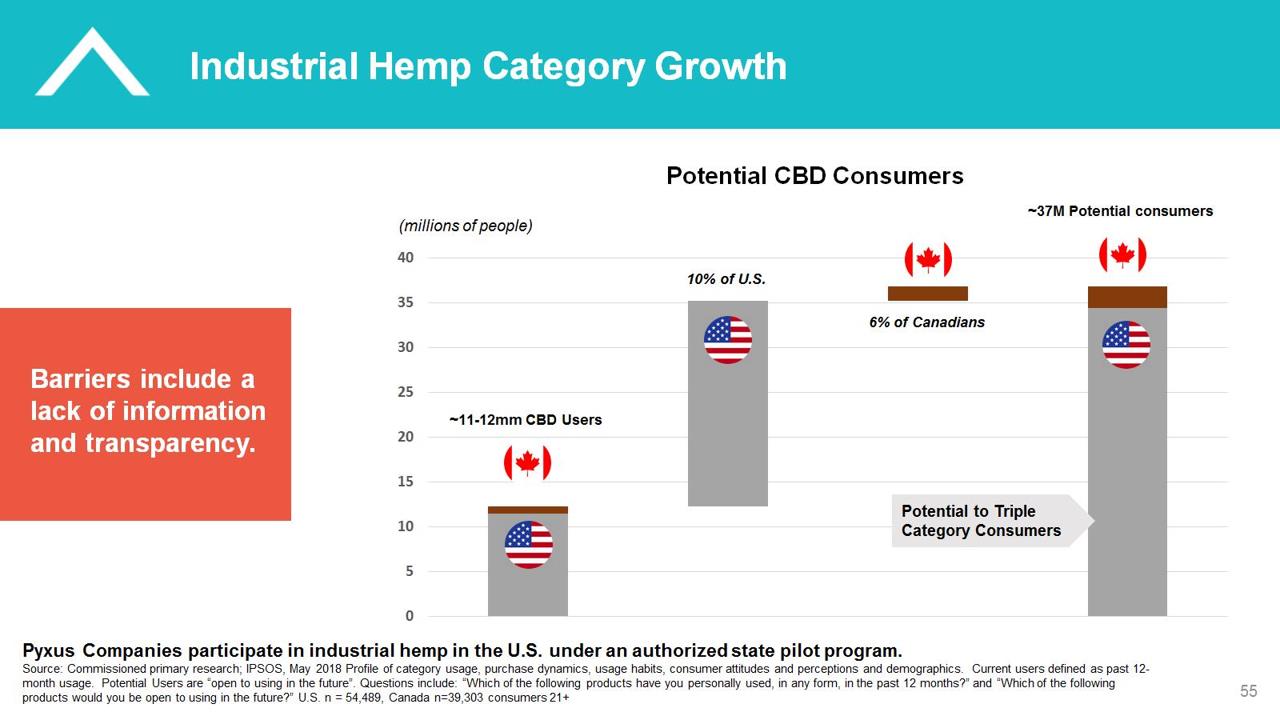

Industrial Hemp – Pyxus’ industrial hemp joint venture, Criticality LLC, (Criticality) continues to advance in the production of cannabidiol hemp oil (CBD) and related consumer products. The Company is receiving hemp and will be processing at its new facility in Wilson, NC, in December. In addition to producing bulk CBD products for industrial, B2B customers, Criticality will also manufacture and distribute a line of consumer products under the proprietary Korent brand. The effects of Hurricane Florence resulted in facility construction delays but had little impact on the current hemp crop. In spite of weather issues, Criticality maintains a strong focus on quality of product and optimal CBD concentration levels.

E-liquids – The continuous growth of our West Coast e-liquids businesses required an expansion of space from its 16,000 sq. ft. facility to a new 45,000 sq. ft. facility. The location enhances synergies and increases efficiencies for our Nicotine River, Humble Juice Company and our Zip Fulfillment operations.

Legal Cannabis – On October 17, 2018, the effective date for legalization of adult recreational cannabis use in Canada, Pyxus’ indirect Canadian subsidiary FIGR recorded the first-ever legal recreational cannabis sale on Prince Edward Island (P.E.I.). Additionally, FIGR was the only company to have oil available in P.E.I. and one of two companies to have oil in Nova Scotia on opening day. FIGR East (licensed under the name Canada’s Island Garden) received its Oil Production and Sales License on August 31, 2018, and is currently one of only 29 firms to have received an Oil Production and Sales License from Health Canada. FIGR products are now available for legal recreational purchase by adult consumers at all PEIMC retailers across P.E.I. and, with strong initial sell through at retail. For the first two weeks of sales, FIGR has attained 13% of the legal adult-use recreational cannabis market in P.E.I., and is growing market share rapidly in Nova Scotia. Also, following the announcement that the indirect Canadian subsidiary FIGR Norfolk (Goldleaf Pharm Inc.) received its cultivation license from Health Canada on September 28, 2018, the operation has begun cultivation at its Simcoe, Ontario, facility.

In this five-part series you see how your cannabis gets made.

Source: lift.co – Seed To Sale – This series is presented by FIGR.

In this five-part series you see how your cannabis gets made.

8001 Aerial Center Parkway

Post Office Box 2009

Morrisville, NC 27560-8413

United States

919-379-4300

http://www.pyxusintl.com

Sector: Consumer Defensive

Industry: Tobacco

Full Time Employees: 3,450

PYXUS INTERNATIONAL, INC. CIK#: 0000939930 (see all company filings)

SIC: 5150 - WHOLESALE-FARM PRODUCT RAW MATERIALS

State location: NC | State of Inc.: VA | Fisical Year End: 0331

formely: ALLIANCE ONE INTERNATIONAL, INC. (filings through 2018-10-02)

formerly: DIMON INC. (filings through 2005-05-11)

(Assistant Director Office: 5)

Get insider transactions for this issuer.

Institutional and Fund Ownership - Buyers

Source: https://fintel.io/s/us/pyx

.

| Volume | |

| Day Range: | |

| Bid Price | |

| Ask Price | |

| Last Trade Time: |