News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Cash forecast:

Based on my figures, which include a slight overrun of Heron-1 due to the G2G permit issue and then the cancellation of Velociraptor MATD will have net cash left on Dec 31st 2019 of 7.5m US$

Perhaps someone can ask Mike that on 12th November.

Production start up requires a couple of hundred thousand dollars only, just some facilities and storage tanks - everything else is there already.

.

(Note that the 16m US$ cash at half year end includes lots of advance payments for the drilling of RD-1, H-1 and G-1.......... long lead time items, deposits etc... all paid in advance. They dont just drill a well and pay the full amount on completion. Large part of well costs is paid in advance. )

Looking at the potential news flow ahead :

Operational Update - completion of all testing operations at Heron-1 - (possible)

Block XX update - reserves and prospects - submission of documents to MRPAM for Exploitation License (probable)

Award of Exploitation License for Block XX (probable) (Dec 2019 or Jan 2020)

Once the Exploitation License is awarded then MATD have something with which to secure a Farm Out or Bank Loan so farm out/loan update Jan/Feb 2020

Post Exploitation License award - Ops Update Production start up progress (probable early 2020)

Production started Operations Update (early 2020)

Looks like a transcript of the TV interview.

https://www.inews.mn/a/10477

Basic points again.....

Gazelle still very much in play, thought to be drilled on the edge of the Strat Trap and so expecting much thicker pay in alternate location.

Heron-1 - no water produced at all, very much thinking that its bigger than 25 MMBO recoverable pre drill estimates. This man seems to think the lack of any water means much bigger........ Mike has not said that yet, he refers only to the very conservative 15% recovery factor used pre-drill. Maybe he is saving the water/size upgrades for the presentations to come........

12th November event in London for those who want to attend.

https://www.eventbrite.co.uk/e/oil-gas-investor-briefing-with-ceos-from-eco-atlantic-coro-energy-tickets-77838684601

MATD headlining, also ECO and CORO

.

Thanks again Pro. My Mongolian is non-existent but it is encouraging that the interview is on a TV broadcast to the nation, Bloomberg Mongolia. Implies that this is a big deal for Mongolia.

thanks pro .

A bright future for the company if we find other oil wells! than heron-1 and maybe gazelle?

we will have to be patient for a few more years before we get 1 £ (pounds) and more.

Interview with one of the MATD Exploration Geologists.

http://bloombergtv.mn/post/58338/

Sadly, all in Mongolian. However the key points are, as posted yesterday. No Water Cut at Heron-1 so Heron will be bigger than the current 25 MMBO recoverable. Gazelle still in play, looking for thick net pay elsewhere as current well hit the fringe as it was secondary target of Gazelle-1 - now they know the Strat Trap Play is a primary target.

Thanks Pro for posting your comments about the interview.

Very good interview with Mike which confirms all what was suspected.

https://audioboom.com/posts/7407804-valuethemarkets-podcast-027-with-mike-buck-ceo-of-petro-matad-matd

Heron-1 exploitation license application in process, we will see production in Q1 2020.

Incremental well count using FCF (eg no plans for any placing, generate the cash, get another well done on Heron - basic option pending band debt or farm out).

Confirms enough cash left for a cheap drill (2nd Heron well)

Heron size upgrades possible.

Gazelle - potential for thicker net pay meaning Gazelle may be a commercial size discovery.

South Tamtsag Basin (Erdenetsagaan area) potential for sone very material sized prospects now following Gazelle strat trap play prove.

No plans as yet for Phoenix or Raptor in 2020 however very interesting that they might consider using a truck mounted rig to drill bore holes into them in Block V, or at least VelociRaptor in Block V. The bore hole approach has been done before - very cheap way of proving oil or not. I like that, thinking outside the box.

Certainly looks very exciting and Mike has intimated quite clearly they have the cash to move forward in a steady way, getting Block XX into production and incrementally increasing production and therefore incrementally increasing Free Cash Flow to then reinvest.

Heron Pre-drill estimate

Heron 165 MMBO OIP with 15% RF giving 25MMBO recoverable.

So why is Mike so excited and delirious ?

Net Pay is bigger than expected as per old RNS - TICK

Porosity is way better than expected - TICK

Permeability is way better than expected - TICK

Structure 5 meters higher than pre-drill estimate, so its bigger - TICK

Flow rates (not stimulated and natural flow - wow factor) - TICK

165MMBO plus 20% for better net pay = +33MMBO

165MMBO plus 15% for better porosity = +24 MMBO

165MMBO plus 10% as bigger area = +16.5 MMBO

So now Heron might well be 165+33+24+16.5 = 238.5MMBO OIP

Now........lets say the RF is not 15% but given the very light oil and the high permeability its more like 30%......

Now means Heron is looking at being 71.5 MMBO recoverable. Which is currently 100% owned.

Now you might see why Mike is pretty damn pleased and beaming from ear to ear. BUT BUT BUT, dont forget that Gazelle has been cased and will be tested in future.

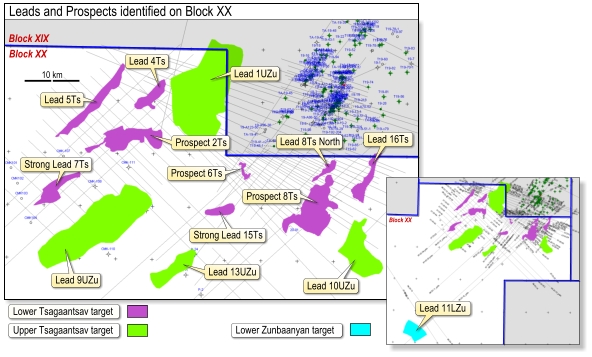

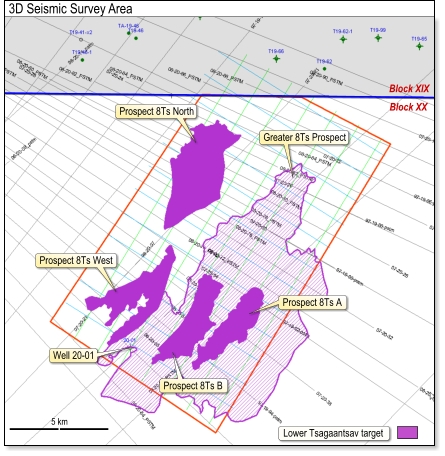

Gazelle may be the key to some very serious upside. We have NGL's in the wet gas, a lot of it and then also 3M of net oil pay and this was drilled at the fringe. So not only may Gazelle deliver something important, it will deliver some very serious upside from similar strat trap plays down at the Erdenetsagaan area........ones which are multiple times the size of Heron - a few over a hundred million MMBO recoverable targets and all there in Block XX at the southerly end of the Tamtsag basin.

Lots of upsides and upgrades to come out yet..........expect to see many interviews and loads of PR over the coming weeks as MATD have a very good story to tell now and will be a producer very soon and generating their own cash.

Thanks for posting the link. Indeed, very good news.

thanks and finally good good prospects for the company and shareholders

I'm not sure what the gray and orange percentages mean on a barrel. Can you explain?

Thanks for posting that graphic.

This was the scoping economics for Blocks IV, V and XX done some time ago (oil was 90US$ then).

As can be seen, the company expects flow rates of between 100bopd to 200bopd per production well on any of the blocks.

Link below, click on it to open the pic.

https://i.ibb.co/VxSf5bx/Annotation-2019-10-19-063458.jpg

.

scumbags...I look forward to the results

Thanks to Malcys blog October 17,2019

Petro Matad

The Gazelle-1 well result is at best highly inconclusive, the Lower Tsagaantsav is dry and the upper reservoir had ‘good wet gas shows recorded’ as well as 3m of net oil in good quality sandstones defined on the logs. From here any success will now be defined by further testing probably after the Heron works which are ongoing. Finally the company has postponed plans to drill in Block V this year, interestingly you may remember that I noticed way back in the spring that MATD had dropped Block V from this year’s plans so I’m not quite sure what that is about. Until I get to speak to Mike Buck there isnt much more I can add.

Read at:

https://www.malcysblog.com/2019/10/oil-price-trinity-premier-petro-matad-and-finally/

Thanks Pro for posting this link.

Thanks for posting that link

As its been brought it up I have run some figures to get an idea of the minor difference flow rates would have to valuations. Using 60US$ a barrel

Expectation is 200 bopd per well. You can discount down say 15% if the flow rate is a more conservative 100 bopd. You can mark up 30% if the flow rate is a more exceptional 400 bopd.

NPV10 based on Heron being 25 MMBO recoverable 145 million US$ = 118 million GBP circa 18p a share @200bopd per well @60US$ oil price

NPV10 based on Heron being 40 MMBO recoverable 260 million US$ = 213 million GBP circa 32p a share @200bopd per well @60US$ oil price

NPV10 based on Heron being 25 MMBO recoverable 124 million US$ = 102 million GBP circa 15.4p a share @100bopd per well @60US$ oil price

NPV10 based on Heron being 40 MMBO recoverable 222 million US$ = 213 million GBP circa 27.5p a share @100bopd per well @60US$ oil price

NPV10 based on Heron being 25 MMBO recoverable 189 million US$ = 118 million GBP circa 23.5p a share @400bopd per well @60US$ oil price

NPV10 based on Heron being 40 MMBO recoverable 338 million US$ = 213 million GBP circa 42p a share @400bopd per well @60US$ oil price

Running those figures with a 50% farm out to PetroChina who drill the development wells for that farm in cost......

25 MMBO @60US$ @50% post farm out @ 200 bopd per well = 9p a share

40 MMBO @60US$ @50% post farm out @ 200 bopd per well = 16p a share

Best case 40 MMBO @60US$ @50% post farm out @ 400 bopd per well = 21p a share

Worst case 25 MMBO @60US$ @50% post farm out @ 100 bopd per well = 7.7p a share

Obviously those are just rough and ready bag of the fag packet calculations and there are other possible scenarios.......but I think it gives a good idea of where valuations can be post the flow test being carried out successfully.

I absolutely think PetroChina will farm in - they will not pay cash, they will drill x number of development wells for their farm in 50%.

At the current 5p level and with Gazelle-1 to come, and MATD having cash left over to develop Heron-1 into a producer if so needed.......its cheap if you ask me.

Apologies for any errors.....just bashing from figures around.

17 September 2019

Petro Matad Limited

('Petro Matad' or the 'Company')

Red Deer-1 exploration well results and operational update

Petro Matad Limited, the AIM quoted Mongolian oil explorer, announces the drilling and logging results of the Red Deer-1 exploration well located in the south of Block XX and an operational update for Heron-1 and Gazelle-1 in the north of Block XX, eastern Mongolia.

Red Deer-1 has been drilled with Daton Petroleum Engineering and Oilfield Service LLC's Rig DXZ1 to a total depth of 2000 metres. No hydrocarbon bearing zones were identified during drilling and this has been confirmed with wireline logs. The well will therefore be plugged and abandoned.

The Lower Tsagaantsav primary reservoir target was encountered at 1632 metres, 30 metres shallower than the pre-drill prognosis, and comprised a thick interval of good quality sandstones interbedded with claystones. Drilling gas values remained low throughout with no increase and no significant oil shows observed upon entering the reservoir target. Petrophysical analysis of the wireline log data has confirmed the absence of hydrocarbons. Analysis of drilling gas data suggests the presence of potential source rocks shallower in the drilled section, but the absence of significant oil shows indicates that these source rocks are not fully mature for hydrocarbon generation in the vicinity of the Red Deer prospect.

Well abandonment operations are now beginning and upon completion the rig will move out and the well site will be restored to its pre-drill condition. The well was drilled on budget with total cost under $4 million.

In the northern part of Block XX, at Heron-1 the casing operation has been completed and the well has been temporarily suspended. Mobilisation of testing equipment will commence shortly and testing operations are forecast to begin in early October and to be completed during the month. DQE's Rig 40105 has been moved from Heron-1 to the Gazelle-1 well site where it is in process of being rigged up. Spud of Gazelle-1 is anticipated before the end of September.

Commencement of testing operations on Heron-1 and drilling operations at Gazelle-1 will be the subject of future announcements.

Mike Buck, the CEO of Petro Matad said:

"While the results of the Red Deer-1 well are disappointing, it was the first well to b

At this juncture, if I compare what SOCO had in Mongolia (SOCO sold the producing field to PetroChina who currently own it) - it seems we have better reservoir than SOCO found.

Heron-1 has found more gross potential oil pay/net oil pay than a lot of the SOCO producing wells found.

Read through the SOCO news releases......and expect similar from MATD in the coming months and years as they take Block XX into becoming the next producing field in Mongolia with the Heron discovery.

https://www.socointernational.com/news_70

https://www.socointernational.com/news_60

https://www.socointernational.com/news_46

https://www.socointernational.com/news_35

https://www.socointernational.com/news_31

Enjoy.......given what SOCO found, what MATD have found with Heron-1 - its looking very rosy for Heron !!!!!!

yes! im looking forward to it! finally they get a strike

The link said £ .45 still a substancial rise.

PetroChina wells produce on average at up to 200 bopd. These are all pumped wells.

It will be interesting to see the flow rates from Heron-1, will they match the 200 bopd of the PetroChina wells ? or will it be better than that given the better porosity and permeability ?

From 13 minutes 10 seconds in for MATD.

https://total-market-solutions.com/2019/09/10/malcy-talks-oil-gas-xiv/

.

.

https://www.upstreamonline.com/incoming/1847833/petro-matad-in-mongolia-oil-strike

Petro Matad in Mongolia oil strike

London-listed explorer hoping for commercial flows from discovery amid talks with PetroChina for possible early development Steve Marshall

9 Sep 2019 07:29 GMT Updated 9 Sep 2019 14:04 GMT

Share:

Petro Matad has hit oil pay with the Heron-1 exploration well sunk on its Block XX in eastern Mongolia.

The probe, which was earlier stalled by land use issues after being spudded in July this year, encountered a 77-metre gross interval of potential oil reservoir after being drilled to a total depth of 2960 metres into the primary target in the Lower Tsagaantsav reservoir, the London-listed company said in a statement.

It stated the reservoir interval, which included both oil and gas shows, was “very similar” to productive reservoirs found in wells at the T19-46 oilfield immediately to the north in PetroChina-operated Block XIX in the landlocked East Asian country.

The well, which was drilled as an appraisal to the latter oilfield, had a pre-drill resource estimate of 25 million barrels of mean prospective recoverable resources.

Casing of the well is now being carried out ahead of a testing effort that is likely to require a further rig to be brought in.

Petro Matad chief executive Mike Buck said the test is aimed at delivering commercial oil flow rates so the company can move into the exploitation phase at the discovery once its exploration licence on the tract expires in July 2020.

“We have already been in dialogue with PetroChina with a view to using its existing field infrastructure to develop the find so that we can move into early production, contingent on commercial flows,” Buck told Upstream.

He added that commercialising the discovery would enable it to retain the block so that it could continue to appraise further possible finds on the acreage.

The well was drilled by DQE International’s rig 40105 that will now suspend it and then be mobilised to drill the Gazelle-1 hole in the same block, one of three Mongolia tracts wholly owned and operated by Petro Matad.

The Gazelle prospect lies roughly five kilometres west of Heron-1 and has been estimated to hold mean recoverable prospective resource potential of 13 million barrels.

Petro Matad aims to spud the Gazelle-1 well by the end of September targeting a structure that is on trend with a pair of oilfields operated by PetroChina to the north, with a 50% to 65% chance of success for the probe, according to Buck.

The company is meantime also drilling the Red

Thanks for the extra information.

Mike seems confident, going for Velociraptor as the 4th well........the biggie in Block V.

.......He revealed the fourth and final well of the campaign will target a prospect dubbed Velociraptor - named after a dinosaur in the Jurassic Park movies - in its Block V in the west of the country that has prospective resource potential of as much as 200 million barrels............

https://www.upstreamonline.com/incoming/1847833/petro-matad-in-mongolia-oil-strike

Petro Matad in Mongolia oil strike

London-listed explorer hoping for commercial flows from discovery amid talks with PetroChina for possible early development Steve Marshall

9 Sep 2019 07:29 GMT Updated 9 Sep 2019 14:04 GMT

Share:

Petro Matad has hit oil pay with the Heron-1 exploration well sunk on its Block XX in eastern Mongolia.

The probe, which was earlier stalled by land use issues after being spudded in July this year, encountered a 77-metre gross interval of potential oil reservoir after being drilled to a total depth of 2960 metres into the primary target in the Lower Tsagaantsav reservoir, the London-listed company said in a statement.

It stated the reservoir interval, which included both oil and gas shows, was “very similar” to productive reservoirs found in wells at the T19-46 oilfield immediately to the north in PetroChina-operated Block XIX in the landlocked East Asian country.

The well, which was drilled as an appraisal to the latter oilfield, had a pre-drill resource estimate of 25 million barrels of mean prospective recoverable resources.

Casing of the well is now being carried out ahead of a testing effort that is likely to require a further rig to be brought in.

Petro Matad chief executive Mike Buck said the test is aimed at delivering commercial oil flow rates so the company can move into the exploitation phase at the discovery once its exploration licence on the tract expires in July 2020.

“We have already been in dialogue with PetroChina with a view to using its existing field infrastructure to develop the find so that we can move into early production, contingent on commercial flows,” Buck told Upstream.

He added that commercialising the discovery would enable it to retain the block so that it could continue to appraise further possible finds on the acreage.

The well was drilled by DQE International’s rig 40105 that will now suspend it and then be mobilised to drill the Gazelle-1 hole in the same block, one of three Mongolia tracts wholly owned and operated by Petro Matad.

The Gazelle prospect lies roughly five kilometres west of Heron-1 and has been estimated to hold mean recoverable prospective resource potential of 13 million barrels.

Petro Matad aims to spud the Gazelle-1 well by the end of September targeting a structure that is on trend with a pair of oilfields operated by PetroChina to the north, with a 50% to 65% chance of success for the probe, according to Buck.

The company is meantime also drilling the Red Deer-1 well in the southern part of the block that was spudded last month and has mean recoverable prospective resource potential of 48 million barrels of oil.

The well is being drilled using rig DXZ1 supplied by Daton Petroleum Engineering and Oilfield Service but has been delayed due to equipment-related issues, with drilling results due in mid-September.

Buck said progress with the well has been in line with expectations and “there have been no surprises” in terms of the stratigraphy of the targeted structure, adding that this was “positive”.

“We thought we understood the geology here and that has been borne out,” he said.

He revealed the fourth and final well of the campaign will target a prospect dubbed Velociraptor - named after a dinosaur in the Jurassic Park movies - in its Block V in the west of the country that has prospective resource potential of as much as 200 million barrels.

The company will thus be returning to the block where it came up dry with the Snow Leopard-1 well drilled last year, although Buck said this probe also demonstrated there was a working petroleum system in the tract.

He said there was additional prospectivity of around 200 million barrels on either side of the prospect that could potentially double resources in the event of a discovery.

“The block has larger high-impact prospects that we hope can build on what we have going on in the east where we hope to generate early production revenue from possible discoveries,” he said.

However, the drilling campaign could be extended with further wells as Petro Matad would be keen to use the rig to drill more than one prospect in the east, he added.

He admitted though “we are still scratching our heads” over prospectivity in the company’s Block IV in the west where the Wild Horse-1 well drilled last year came up dry but showed source rocks exist.

Petro Matad has recently gained a two-year extension of the exploration period for blocks IV and V to July 2021.

Thanks to Malcy's Blog

Sept 9, 2019

https://www.malcysblog.com/2019/09/oil-price-hurricane-petro-matad-iog-reabold-touchstone-range-and-finally/

Petro Matad

The company announces that at Heron-1 TD of 2,60m has been reached with gross reservoir intervals appearing to be very similar to the productive reservoirs found immediately to the north in block XIX. Casing is now underway and discussions have taken place with the testing contractor to determine how quickly kit can be mobilised to the location. The timescale should be within one month and hopefully a great deal less, as the company are keen to get a flow rate and to get stimulation of the well underway.

The primary target was encountered at 2,803m some five metres shallower than expected which I am told is a good sign as was the predominantly sandstone interbedded with shales and siltstones found slightly deeper. The company are ‘encouraged and the well is better than expected’ and in my call with CEO Mike Buck this morning he was clearly delighted, particularly with the porosity and permeability in the formation a pleasant surprise.

Petro Matad is only up 5% today which is a touch parsimonious but to be fair puts it up at or near recent peaks and the market knows that they are also drilling the Red Deer well at the moment. Recent speculation about that well is just that, after some slight delays due to kit on site the bit is only ‘close to objective depth’ but should reach TD in mid September before logging.

The rig will shortly move off this site and move to drill the Gazelle-1 well which it should spud in late September which means that there is still plenty of excitement due for the company. Should Heron go on and be the success that it seems they will be able to kick on with plans to make the next steps of the operation to start producing commercial hydrocarbons from Mongolia, which they thoroughly deserve, after all some of us have been waiting a long time for this moment…

Heron-1 has been drilled to a total depth of 2960 metres

September 9, 2019

Petro Matad Limited ("Petro Matad" or "the Company"), the AIM quoted Mongolian oil explorer, provides the following update on the Heron-1 well in Block XX, eastern Mongolia.

Mike Buck, the CEO of Petro Matad said:

"The results of the Heron-1 well are encouraging. Along with the well and wireline logging data being consistent with our pre-drill prognosis, there is also evidence of zones with better than expected porosity/permeability characteristics. The well will now be tested and we are pushing the contractor to mobilise equipment as quickly as possible. Further updates will be provided in due course."

Heron-1 has been drilled to a total depth of 2960 metres .... the gross reservoir interval in Heron-1 appears to be very similar to the productive reservoirs found in oil wells immediately to the north in Block XIX.

Read More at:

https://www.londonstockexchange.com/exchange/news/market-news/market-news-detail/MATD/14218048.html

https://www.malcysblog.com/2019/09/oil-price-hurricane-petro-matad-iog-reabold-touchstone-range-and-finally/

Petro Matad

The company announces that at Heron-1 TD of 2,60m has been reached with gross reservoir intervals appearing to be very similar to the productive reservoirs found immediately to the north in block XIX. Casing is now underway and discussions have taken place with the testing contractor to determine how quickly kit can be mobilised to the location. The timescale should be within one month and hopefully a great deal less, as the company are keen to get a flow rate and to get stimulation of the well underway.

The primary target was encountered at 2,803m some five metres shallower than expected which I am told is a good sign as was the predominantly sandstone interbedded with shales and siltstones found slightly deeper. The company are ‘encouraged and the well is better than expected’ and in my call with CEO Mike Buck this morning he was clearly delighted, particularly with the porosity and permeability in the formation a pleasant surprise.

Petro Matad is only up 5% today which is a touch parsimonious but to be fair puts it up at or near recent peaks and the market knows that they are also drilling the Red Deer well at the moment. Recent speculation about that well is just that, after some slight delays due to kit on site the bit is only ‘close to objective depth’ but should reach TD in mid September before logging.

The rig will shortly move off this site and move to drill the Gazelle-1 well which it should spud in late September which means that there is still plenty of excitement due for the company. Should Heron go on and be the success that it seems they will be able to kick on with plans to make the next steps of the operation to start producing commercial hydrocarbons from Mongolia, which they thoroughly deserve, after all some of us have been waiting a long time for this moment…

Heron-1, results of drilling and wireline logging

Petro Matad Limited ("Petro Matad" or "the Company"), the AIM quoted Mongolian oil explorer, provides the following update on the Heron-1 well in Block XX, eastern Mongolia.

Heron-1 has been drilled to a total depth of 2960 metres with the top Lower Tsagaantsav reservoir, the primary target for the well, encountered at 2803 metres, 5 metres shallower than the pre-drill prognosis. The formation drilled from 2803 to 2880 metres was predominantly sandstone interbedded with shales and siltstones. Oil and gas shows were recorded over this interval and on the basis of the drilling data, the gross reservoir interval in Heron-1 appears to be very similar to the productive reservoirs found in oil wells immediately to the north in Block XIX.

Wireline logs have been acquired and analysis of these data supports the interpretation of a 77 metre gross interval of potential oil reservoir. Within this interval the logs also define three zones with a total gross thickness of 22 metres (14 metres net) exhibiting better porosity and permeability characteristics than is generally seen within the Lower Tsagaantsav at this depth including in the nearby wells in the T19-46 oil field in Block XIX. Overall, the reservoir quality and oil saturations indicated on the wireline logs are sufficiently encouraging that casing will now be run in preparation for a testing programme.

The casing operation is now underway and discussions with the testing contractor have commenced to determine how quickly the testing equipment can be mobilised to the Heron-1 location. The contract requires 30 days notice to be given but the contractor has advised that an earlier start is possible depending on the status of its other activities. Once the well has been suspended DQE's drilling rig will move to the Gazelle location with a view to spudding Gazelle-1 before the end of September.

Mike Buck, the CEO of Petro Matad said:

"The results of the Heron-1 well are encouraging. Along with the well and wireline logging data being consistent with our pre-drill prognosis, there is also evidence of zones with better than expected porosity/permeability characteristics. The well will now be tested and we are pushing the contractor to mobilise equipment as quickly as possible. Further updates will be provided in due course."

interesting,i hit the ask but got some filled in the 9s and the rest in 10s

added this morning

Petro Matad Limited, the AIM quoted Mongolian oil explorer, announces its unaudited interim results for the six months ended 30 June 2019.

Financial Summary

The Group posted a loss of USD 4.41 million for the six-month period ended 30 June 2019, which compares to a loss of USD 6.65 million for the comparable period in 2018. The Company's cash balance at 30 June 2019 was USD 16.12 million (USD 3.79 million in cash and USD 12.33 million in Financial Assets), which compares to a cash balance of USD 15.55 million (USD 12.54 million in cash and USD 3.01 million in Financial Assets) on 30 June 2018.

Following the two successful placings in 2018, no new fund raises have been undertaken in 2019 as the Company's cash resources are sufficient to fully meet the costs of the planned 2019 drilling programme.

Operational Update

The Heron 1 exploration well in the Tamsag Basin of Block XX spudded with the DQE International 40105 rig on 19 July 2019. Land permits for Heron (and Gazelle) have been received and drilling operations continue towards a planned total depth (TD) of 3,050 metres. The well is an appraisal of the T19-46 oil field immediately to the north in Block XIX and is targeting a prospect with 25 MMbo of Mean Prospective Recoverable Resource. The Company expects to be in a position to announce the results of the drilling and logging of the well during the week commencing 9 September 2019.

The Gazelle 1 exploration well will follow Heron 1 after a six-kilometre rig move and will take approximately 35 days to drill and log. The planned TD is 2,500 metres and the Gazelle Prospect has an estimated Mean Prospective Recoverable Resource of 13 MMbo. Gazelle 1 is located updip of Petro China's T19-46-1 oil well on the western flank of the Tamsag Basin which is the primary source kitchen for the fields in Block XIX.

The Red Deer 1 exploration well in the Asgat Sag Basin of Block XX spudded with the Daton Petroleum Engineering and Oilfield Service LLC rig, DXZ1, on 4 August 2019. The well is targeting a prospect with 48 MMbo of Mean Prospective Recoverable Resource. Drilling operations continue towards the planned TD of 2,100 metres. Results from the drilling and logging of the well are expected to be completed by mid-September 2019.

In the event of a discovery in one or more of the 2019 exploration wells, the Company will bring in a separate rig for testing. A call-off testing contract has been signed, which ensures testing operations, if warranted, can commence soon after discovery.

The Company successfully obtained two-year PSC extensions for Blocks IV and V, as was announced on 26 June 2019.

Further operational updates will be provided in due course.

|

Followers

|

17

|

Posters

|

|

|

Posts (Today)

|

0

|

Posts (Total)

|

1028

|

|

Created

|

09/06/10

|

Type

|

Free

|

| Moderators | |||

Petro Matad is the parent company of a group focused on oil exploration, as well as future development and production in Mongolia. The Group's principal asset is the Production Sharing Contract (PSC) over Matad Block XX, a petroleum block with an area of 14,250km2 in the far eastern part of Mongolia, near the Chinese border.

Petro Matad Limited's shares were admitted to trading on AIM, London Stock Exchange, on May 1st, 2008. The company's largest shareholder is Petrovis LLC, the largest importer and distributor of petroleum products in Mongolia. The company is the first substantially Mongolian owned company to have its shares admitted to trading on any major international stock exchange.

Since 2006, Petro Matad has carried out extensive exploration on Block XX. This has consisted of re-processing previous data and undertaking programmes of 2D and 3D seismic surveys. Petro Matad is now ready to advance to the next stages of exploration on Block XX and early stage exploration and appraisal of Blocks IV and V.

It is intended that exploration will primarily be carried out by applying modern data processing and interpretation techniques to geophysical information, acquiring additional geophysical data and then, subject to future financing, undertaking drilling programmes where warranted.

Capital structure

The Company’s issued share capital consists of 333,258,252 Ordinary Shares of par value USD$0.01. The Company does not hold any Ordinary Shares in Treasury.

In so far as the Company is aware, the percentage of the Company’s issued share capital that is not in public hands is 34.18%.

The Company is aware of the below shareholders who hold 3% or more of the Company’s issued share capital.

| Number of ordinary shares | Percentage of share capital | |

|---|---|---|

| Petrovis Matad Inc. | 94,684,262 | 28.41168 |

| Janchiv Oyungerel | 13,267,946 | 3.98128 |

| Tuya Danzandarjaa | 11,694,427 | 3.50912 |

| Forestberries LLC | 11,000,000 | 3.30074 |

http://stockcharts.com/c-sc/sc?s=PRTDF&p=D&b=5&g=0&i=0&r=9476

| New Year's Day | Closed | Closed | Closed | |

| Jan. 15 | Martin Luther King Jr. Day | Closed | Closed | Closed |

| Feb. 19 | Presidents Day/Washington's Birthday | Closed | Closed | Closed |

| March 29 | Maundy Thursday | Open | Open | Early close (2 p.m.) |

| March 30 | Good Friday | Closed | Closed | Closed |

| May 27 | Day Before Memorial Day | Open | Open | Early close (2 p.m.) |

| May 28 | Memorial Day | Closed | Closed | Closed |

| July 3 | Day Before Independence Day | Early close (1 p.m.) | Early close (1 p.m.) | Early close (2 p.m.) |

| July 4 | Independence Day | Closed | Closed | Closed |

| Sept. 3 | Labor Day | Closed | Closed | Closed |

| Oct. 8 | Columbus Day | Open | Open | Closed |

| Nov. 12 | Veterans Day (Observed) | Open | Open | Open |

| Nov. 22 | Thanksgiving Day | Closed | Closed | Closed |

| Nov. 23 | Day Before Thanksgiving | Early close (1 p.m.) | Early close (1 p.m.) | Early Close (2 p.m.) |

| Dec. 24 | Christmas Eve | Early close (1 p.m.) | Early close (1 p.m.) | Early Close (2 p.m.) |

| Dec. 25 | Christmas Day | Closed | Closed | Closed |

| Dec. 31 | New Year's Eve | Open | Open | Early Close (2 p.m.) |

| Volume | |

| Day Range: | |

| Bid Price | |

| Ask Price | |

| Last Trade Time: |