News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

After a very rough run, Nabors Industries (NBR -3.5%) has bounced nicely over the past few sessions. Scotia Howard Weil is using the opportunity to get out, downgrading the stock to Sector Perform from Outperform.

Yep....this has been one hell of a ride for sure no surf ATM machine here for sure bro!!!

Yep....this has been one hell of a ride for sure no surf ATM machine here for sure bro!!!

This ticker is going to hit 30% before the EOW if it keeps going at this rate!

$NBR Nabors Industries Ltd

http://pamphletshop.com

Nabors Industries Ltd. [$NBR] due diligence

bullish

weekly golden cross

$NBR

DD Notes ~ http://www.ddnotesmaker.com/NBR

##### recent news/filings ~ source: finance.yahoo.com

Mon, 16 Jun 2014 19:14:18 GMT ~ The Reluctant Rockstar

read full: http://seekingalpha.com/article/2270983-the-reluctant-rockstar?source=yahoo

*********************************************************

Fri, 06 Jun 2014 04:16:39 GMT ~ [$$] Oil-Driller Nabors Ignores Vote on Directors

[at The Wall Street Journal] - A majority of votes cast by shareholders of Nabors Industries rejected all three members of the board's compensation committee, but the drilling company chose to disregard the rebuke.

read full: http://online.wsj.com/articles/oil-driller-nabors-industries-ignores-vote-on-directors-1402012181?ru=yahoo?mod=yahoo_itp

*********************************************************

Thu, 05 Jun 2014 10:00:29 GMT ~ NABORS INDUSTRIES LTD Files SEC form 8-K, Change in Directors or Principal Officers, Submission of Matters to a Vote

read full: http://biz.yahoo.com/e/140605/nbr8-k.html

*********************************************************

Wed, 04 Jun 2014 21:41:00 GMT ~ Nabors Expands Its Board, Appointing Dag Skattum as a Director

[CNW Group] - Nabors Expands Its Board, Appointing Dag Skattum as a Director

read full: http://finance.yahoo.com/news/nabors-expands-board-appointing-dag-214100431.html

*********************************************************

Wed, 04 Jun 2014 21:40:00 GMT ~ Nabors Expands Its Board, Appointing Dag Skattum as a Director

[PR Newswire] - HAMILTON, Bermuda, June 4, 2014 /PRNewswire/ -- Nabors Industries Ltd. (NBR) today announced that its Board of Directors has expanded the Board to eight members from the current seven and subsequently appointed Dag Skattum to fill the newly created vacancy. Mr. Skattum currently serves as Managing Director of one thousand & one voices, a family-backed investment firm focused on Sub-Saharan African Investments, a position he has held since 2013. Previously, Mr. Skattum served as Partner of TPG, a leading global private investment firm, based in London from 2007 until 2013. He began his career at JP Morgan, where he worked in London and New York from 1986 until 2007, serving most recently as Managing Director and Co-head of Global Mergers and Acquisitions.

read full: http://finance.yahoo.com/news/nabors-expands-board-appointing-dag-214000528.html

*********************************************************

##### chart ~ source: stockcharts.com

##### company info ~ source: otcmarkets.com

Link: http://www.otcmarkets.com/stock/NBR/company-info

Ticker: $NBR

OTC Market Place: Not Available

CIK code: 0001163739

Company name: Nabors Industries Ltd.

Company website: http://www.nabors.com

Incorporated In: Bermuda

##### extra dd links

Edgar filings: http://www.sec.gov/cgi-bin/browse-edgar?action=getcompany&CIK=0001163739&owner=exclude&count=40

Latest filings: http://www.otcmarkets.com/stock/NBR/filings

Latest financials: http://www.otcmarkets.com/stock/NBR/financials

Latest news: http://www.otcmarkets.com/stock/NBR/news - http://finance.yahoo.com/q/h?s=NBR+Headlines

Major holdings: http://data.cnbc.com/quotes/NBR/tab/8.1

Insider transactions (1): http://finance.yahoo.com/q/it?s=NBR+Insider+Transactions

Insider transactions (2): http://www.secform4.com/insider-trading/NBR.htm

Insider transactions (3): http://www.insidercow.com/history/company.jsp?company=NBR

RegSho: http://www.regsho.com/tools/symbol_stats.php?sym=NBR&search=search

DTCC: http://search2.dtcc.com/?q=Nabors+Industries+Ltd.&x=10&y=8&sp_p=all&sp_f=ISO-8859-1

Spoke company information: http://www.spoke.com/search?utf8=%E2%9C%93&q=Nabors+Industries+Ltd.

Corporation WIKI: http://www.corporationwiki.com/search/results?term=Nabors+Industries+Ltd.&x=0&y=0

WHOIS: http://whois.domaintools.com/http://www.nabors.com

Alexa: http://www.alexa.com/siteinfo/http://www.nabors.com#

Corporate website internet archive: http://web.archive.org/web/*/http://www.nabors.com

Short Sales: http://www.otcmarkets.com/stock/NBR/short-sales

Insider Disclosure: http://www.otcmarkets.com/stock/NBR/insider-transactions

Research Reports: http://www.otcmarkets.com/stock/NBR/research

Historical Prices: http://finance.yahoo.com/q/hp?s=NBR+Historical+Prices

Basic Tech. Analysis: http://finance.yahoo.com/q/ta?s=NBR+Basic+Tech.+Analysis

Company Profile: http://finance.yahoo.com/q/pr?s=NBR+Profile

Key Statistics: http://finance.yahoo.com/q/ks?s=NBR+Key+Statistics

Industry: http://finance.yahoo.com/q/in?s=NBR+Industry

Insider Roster: http://finance.yahoo.com/q/ir?s=NBR+Insider+Roster

Income Statement: http://finance.yahoo.com/q/is?s=NBR

Balance Sheet: http://finance.yahoo.com/q/bs?s=NBR

Cash Flow: http://finance.yahoo.com/q/cf?s=NBR+Cash+Flow&annual

Market Watch: http://www.marketwatch.com/investing/stock/NBR

Bloomberg: http://www.bloomberg.com/quote/NBR:US

Morningstar: http://quotes.morningstar.com/stock/s?t=NBR

Bussinessweek: http://investing.businessweek.com/research/stocks/snapshot/snapshot_article.asp?ticker=NBR

Barchart: http://www.barchart.com/quotes/stocks/NBR

OTC Short Report: http://otcshortreport.com/index.php?index=NBR

Investopedia: http://www.investopedia.com/markets/stocks/NBR/?wa=0

http://www.pennystocktweets.com/stocks/profile/NBR

##### last known share structure ~ source: otcmarkets.com

Market Value: $8,283,823,170 a/o Jun 19, 2014

Shares Outstanding: 297,444,279 a/o May 05, 2014

Float: Not Available

Authorized Shares: Not Available

Par Value: 0.001

##### business description ~ source: otcmarkets.com

DD Notes ~ http://www.ddnotesmaker.com/NBR

Earnings updates

Revenue and rig hours increased in the United States of America Offset by a sharper than expected seasonal drop in Canada

http://www.earningsimpact.com/Transcript/82725/NBR/Nabors-Industries-Ltd----Q2-2013-Earnings-Call

Goldman Sachs Downgrades Nabors (NBR) to Buy

http://www.streetinsider.com/Downgrades/Goldman+Sachs+Downgrades+Nabors+%28NBR%29+to+Buy/8488789.html

Goldman Sachs downgraded Nabors (NYSE: NBR) from Conviction Buy to Buy with a price target of $19.50 (from $22.00). The change follows a Q2 earnings warning issued by Nabors yesterday.

"We are disappointed by the new guidance as we were confident that NBR would meet our forecast of $119mn in EBIT. We were expecting the company's manufacturing and logistics business to report about $6mn in EBIT, but we believe most likely that business returned a loss, which would explain perhaps half of the miss. The remainder of the miss was probably in the pressure pumping business, owing to inclement weather in Canada and the US Rockies," said analyst Waqar Syed.

Goldman cut its 2013/14 EPS estimate to $0.82/$1.37 from $1.04/$1.85. 2013/14 EBITDA was cut 5% & 9%, respectively.

Shares of Nabors closed at $16.00 yesterday, with a 52 week range of $12.75-$18.24.

Nabors Announces First Quarter 2013 Results

Tuesday , April 23, 2013 16:02ET

HAMILTON, Bermuda, April 23, 2013 /PRNewswire/ -- Nabors Industries Ltd. (NYSE:NBR) today reported its financial results for the first quarter of 2013. Adjusted income derived from operating activities was $149.6 million, compared to $315.5 million in the first quarter of 2012 and $149.8 million in the fourth quarter of 2012. Operating cash flow (EBITDA) was $423.0 million for the first quarter compared to $563.2 million and $427.0 million, respectively, in the first and fourth quarters of last year. Net income from continuing operations was $97.2 million ($0.33 per diluted share), compared to $142.6 million ($0.49 per diluted share) in the first quarter of 2012 and $129.3 million ($0.44 per diluted share) in the fourth quarter of 2012. Operating revenues and earnings from unconsolidated affiliates for this quarter totaled $1.58 billion, compared to $1.82 billion in the comparable quarter of the prior year and $1.60 billion in the fourth quarter of 2012. First quarter results included a gain on the sale of a large portion of marketable securities net of charges related to the previously disclosed CEO employment contract restructuring. The quarter's results also benefited from a lower effective tax rate, principally attributable to the settlement of a long outstanding tax dispute.

Tony Petrello, Nabors' Chairman, President & CEO, commented, "Operating income and cash flow were essentially flat compared to the fourth quarter, as improved results in Production Services coupled with the seasonal peak in Canada were offset by a sharp decline in Completion Services and more moderate declines in our U.S. and International drilling operations. The anticipated seasonal trough in Completion Services was exacerbated by the slow restart of activity following the holidays and the series of late winter storms across the areas where a majority of our operations are located. Despite the slow start, we expect our performance to improve later this year as we begin to restore operating leverage across our Production Services and drilling operations."

"Our initiatives to streamline and consolidate our operations are reflected in an enhanced reporting format beginning this quarter. This format reflects the way in which we now analyze our businesses and provides better visibility into the cash contribution of each of our segments."

To facilitate historical comparisons, the Company will post a downloadable Excel worksheet with three years of reformatted results to its website at www.nabors.com.

DRILLING & RIG SERVICES

In the Company's Drilling & Rig Services business line, revenues were essentially flat with the fourth quarter at $1.1 billion, as were operating cash flow and income at $356.7 and $137.3 million, respectively. Aggregate rig activity increased sequentially from 346 to 352 rigs, while daily per rig margins declined approximately $153 to average $11,987.

U.S. Drilling

Improved results in the Gulf of Mexico coupled with seasonally higher results in Alaska mostly offset the anticipated sharp decline in the U.S. Lower 48 portion of this segment. Revenues for the quarter were $484.8 million, generating $184.9 million in operating cash flow and $77.6 million in operating income. The U.S. Lower 48 rig count bottomed in mid-February at 165 rigs and has since increased by 16 to 177 rigs, three of which are recently deployed PACE(®)-X rigs. An additional two PACE(®)-X rig commitments were secured during the quarter, bringing the total number of PACE(®)-X contract awards to 19 since the beginning of 2012 and the total number of contract awards for new rigs to 23 during the same period. This segment expects to see even lower results in the second quarter as the Alaska winter season winds down and spot market pricing impacts on revenue become fully realized in the U.S. Lower 48 operations. Activity in the Gulf of Mexico is gradually improving, although seasonally weak activity is expected from June through October due to hurricane season. The new 4,600 horsepower deepwater platform rig we are building is in the final stages of commissioning after which it will be used for training until its planned mobilization later in the year. The recent passage of favorable tax legislation in Alaska is expected to spur plans for new activity, with Nabors in line to be a major beneficiary. Activity should begin later this year and increase for at least two or three years. Regaining lost market share in the U.S. Lower 48 is a priority and should result in increasing operating leverage as rig count is restored, especially since a large portion of the fleet has already been renewed at spot market rates.

Canada Drilling

The first quarter represented the customary seasonal peak in Canada, although results were short of expectations and historical highs as customers curtailed plans and concluded projects earlier than usual, despite favorable weather. Cash flow constraints continue to limit this market, with little upside expected until natural gas prices improve or LNG export timing becomes more visible. Despite the challenging market, a new rig was recently deployed under a term contract, and two deep capacity rigs have been readied for a recent award. Inquiries for rigs to drill in support of anticipated LNG exports have increased and Nabors is well positioned to capitalize on these opportunities.

International Drilling

Sequential results were down slightly in our International operations, as startup and unfavorable rig move costs offset the initial contribution of the increase in rig activity which was comprised of one land and 2.4 offshore rigs. Extraordinary and unanticipated cost issues offset a number of recent positive developments. Among the more significant issues are excessive costs in Iraq and Yemen, higher labor costs in the Middle East and North Africa, delays in restarting rigs in Algeria and lower activity in certain Latin American countries. These issues are beginning to dissipate and should be gradually extinguished over the intermediate term.

A number of positive developments are emerging. Availability of high specification rigs is becoming limited in the Middle East region, and rates are improving significantly as contracts renew. The Company has received incremental inquiries for a large number of high-specification rigs, with more anticipated in the near future. The number of available rigs in this class is insufficient to meet this prospective demand, causing the Company to anticipate significant demand for new or upgraded rigs. Nabors is well suited to meet new build requirements, and also owns the majority of the rigs eligible for upgrading. The Company recently received awards for the startup of two existing offshore platform rigs in Latin America, resumed operations with one of its idle jackups in the Arabian Gulf, is restarting rigs in Algeria and is achieving improvements in Iraq and Yemen. The impact of these developments should begin to be reflected in second-half results.

Rig Services

Sequential results in Rig Services improved with seasonally strong activity in Alaska oilfield hauling and construction more than offsetting lower results in Canrig. Fewer capital equipment shipments and reduced rental and field services activity in Canrig were in line with the lower levels of land rig activity and reduced new build construction in the U.S. and Canada. The second quarter is expected to show lower results with the end of winter activity in Alaska, despite some improvement in Canrig.

COMPLETION & PRODUCTION SERVICES

In the Company's Completion & Production Services business line, revenues decreased to $513.7 million compared to $544.2 million in the fourth quarter. This decrease resulted in a significant decrease in both segment EBITDA and operating income, which were $97.8 million and $43.8 million, respectively. The lower results were attributable to lower seasonal utilization in Completion Services, resulting in suppressed margins due to higher unrecovered costs. This more than offset the increase in Production Services as it recovered from its seasonally weak fourth quarter.

Completion Services

First quarter results in the completion services segment were even weaker than expected with the slow restart of activity exacerbated by the recent series of late winter storms. While industry activity is improving modestly, the competition for each incremental project is still intense. Modest improvement is expected in the second quarter as utilization and margins recover, although the potential for continued pricing pressure exists.

Production Services

This operation saw a modest improvement sequentially, with improving activity in the U.S. and seasonally high activity in Canada, despite a slow start to the year in the U.S. following the late fourth quarter stall in activity and difficult weather in its northern districts. Modest improvement is anticipated in the second quarter on higher expected activity in the U.S., even though the recent release of a large number of rigs by a major operator in multiple areas has disrupted the market and seasonality will weaken Canada results. Longer term, the outlook for this segment remains promising as the population of oil and liquids wells continues to grow.

Summary

Mr. Petrello summarized the results and outlook, "We remain focused on our goal of improving our performance, both financially and operationally. Our financial position remains solid despite lower operating cash flow and over $200 million in cash outflows during the quarter for semi-annual interest payments, a technology acquisition and other less significant one-time expenditures. Operationally, we continue to set records across numerous areas, and develop and adopt numerous performance enhancing technologies.

"We believe technology differentiation will be increasingly relevant in the future and will consist of both increased automation of the surface-based rig functions, and ultimately the downhole drilling processes. Nabors has all of the relevant resources under one roof to be a leader in this effort. To date we deployed three of our new PACE(®)-X series of rigs and are approaching completion of our sophisticated deepwater platform rig. All of these rigs incorporate the latest performance-enhancing technology, most of which is produced by Canrig. Our U.S. Lower 48 customers are increasingly incorporating pad drilling capability into their requirements and we continue to invest in not only new pad capable rigs but also in the retrofitting of our existing fleet. Pad drilling is expanding rapidly and is a differentiator over the near term. Nabors pioneered pad drilling in the 1970s and has the largest complement of the industry's pad-capable rigs, particularly walking style rigs.

"The near term remains challenging across all of our markets. Although cost issues are beginning to abate internationally, North American contract renewal and spot rates remain under pressure across all classes of rigs and all regions, as we have articulated since last summer. Despite these challenging conditions, we are encouraged by the increasing visibility of a meaningful improvement in our results later this year."

http://www.knobias.com/story.htm?eid=3.1.4abaa723304b81a83843877f5279dbd8455d2f6a62a44d53026278a83a5b9f95

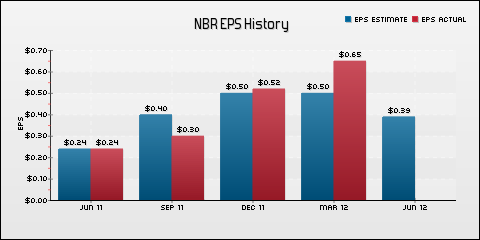

NBR: Q1 EPS 33c vs 65c Beats 28c Est

Tuesday , April 23, 2013 16:30ET

QUARTER RESULTS

Nabors Industries Ltd (NBR) reported Q1 results ended March 2013. Q1 Revenues were $1,660.96M; -9.83% vs yr-ago; BEATING revenue consensus by +1.24%. Q1 EPS was 33c; -49.23% vs yr-ago; BEATING earnings consensus by +17.86%.

Q1 RESULTS Reported Year-Ago Y/Y Chg Estimate SURPRISE

---------- ------------ ------------ ---------- ------------ ----------

Revenues: $1,660.96M $1,842.01M -9.83% $1,640.69M +1.24%

---------- ------------ ------------ ---------- ------------ ----------

EPS: 33c 65c -49.23% 28c +17.86%

---------- ------------ ------------ ---------- ------------ ----------

NBR: Q4 EPS 9c vs 26c Misses 29c Est

Tuesday , February 19, 2013 16:26ET

QUARTER RESULTS

Nabors Industries Ltd (NBR) reported Q4 results ended December 2012. Q4 Revenues were $1,627.10M; -2.81% vs yr-ago; MISSING revenue consensus by -1.92%. Q4 EPS was 9c; -65.38% vs yr-ago; MISSING earnings consensus by -68.97%.

Q4 RESULTS Reported Year-Ago Y/Y Chg Estimate SURPRISE

---------- ------------ ------------ ---------- ------------ ----------

Revenues: $1,627.10M $1,674.12M -2.81% $1,658.94M -1.92%

---------- ------------ ------------ ---------- ------------ ----------

EPS: 9c 26c -65.38% 29c -68.97%

---------- ------------ ------------ ---------- ------------ ----------

FY RESULTS Reported Year-Ago Y/Y Chg Estimate SURPRISE

---------- ------------ ------------ ---------- ------------ ----------

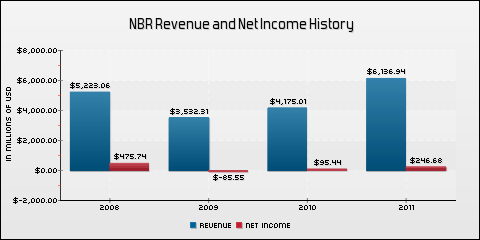

Revenues: $6,751.39M $6,136.94M +10.01% $6,876.96M -1.83%

---------- ------------ ------------ ---------- ------------ ----------

EPS: 56c 83c -32.53% $1.73 -67.63%

---------- ------------ ------------ ---------- ------------ ----------

Potential Takeover Targets: Morgan Stanley Report

http://www.cnbc.com/id/100398632?__source=yahoo|headline|quote|text|&par=yahoo

Nabors Industries Ltd. (NBR) Higher after Activist Investor Files 13D

Nabors Industries Ltd. (NYSE: NBR) is moving higher after Pamplona Capital disclosed a 8.82%, or 25,602,322 share, stake in the company in a 13D, saying they are increasingly concerned about the underperformance of the stock.

From the filing:

"The Reporting Persons initially acquired beneficial ownership of the Common Stock of the Issuer for investment purposes because they believed the Issuer's Common Stock represented an attractive investment opportunity. The Reporting Persons have become increasingly concerned about the underperformance of the Common Stock relative to its peer group and the market, the Issuer's problems experienced with achieving various aspects of its strategic plan and its declining market share. The Reporting Persons have substantial experience in the Issuer’s lines of business and have had constructive discussions with the Issuer's management. The Reporting Persons believe they have valuable insights to contribute to the development of the business and intend to have further discussions with management, the Board of Directors of the Issuer, other shareholders of the Issuer and other relevant parties relating to the Issuer's business, operations, strategy, future plans, corporate governance and related matters."

Jefferies Downgrades Nabors (NBR) to Underperform

http://www.streetinsider.com/Downgrades/Jefferies+Downgrades+Nabors+%28NBR%29+to+Underperform/7945279.html

Jefferies downgraded Nabors (NYSE: NBR) from Hold to Underperform with a price target of $13.00 (from $15.00), citing a lack of recovery in U.S. land market share, risk to dayrates and lower pressure pumping outlook.

The firm comments, "We lack confidence that NBR can recover significant market share in U.S. land, see some risk to our flat dayrate outlook and lower our pressure pumping outlook for '13. With disposals pushed out, streamlining or other sources of cash are harder to count on. In short we think NBR shares are at risk despite 12-month underperformance and despite apparent asset value support. We reiterate our preference within land drilling for HP (NYSE: HP)."

Nabors Secures $1.5 billion Five-Year Unsecured Revolving Credit Facility

Press Release: Nabors Industries Ltd.

HAMILTON, Bermuda, Nov. 29, 2012 /PRNewswire/ -- Nabors Industries Ltd. (NYSE: NBR) today announced the closing of an unsecured revolving credit facility with an aggregate principal amount of $1.5 billion, comprised of a US dollar-denominated loan facility of up $1.45 billion and a Canadian dollar-denominated loan facility of up to $50 million. The duration of the facility is five years. The terms of the new facility are substantially the same as the $750 million credit facility established in September 2010 and the $700 million credit facility established in April 2011, both of which were terminated contemporaneously with the establishment of the new facility. A Canadian $50 million unsecured revolving loan facility was also terminated contemporaneously with the establishment of the new facility. The new facility includes an accordion feature that would allow the Company to add lenders and increase the aggregate principal amount up to $1.95 billion. Interest margins and undrawn fees are based upon the Company's senior unsecured credit ratings. When drawn, US dollar-denominated borrowings under the facility will bear interest, at the Company's option, at either (a) one, two, three or six months LIBOR, or (b) the higher of the prime commercial rate of Citibank, N.A., the Federal Funds Rate plus ½ of 1%, or one month LIBOR plus 1.05%, in each case plus the applicable margin. Based upon the Company's current credit ratings, the interest margin and undrawn fees under option (a) would be 130bps and 20bps, respectively, and 25bps and 20 bps under option (b). The interest mechanism for any loans denominated in Canadian dollars is similar. The Company fully and unconditionally guarantees the obligations of its subsidiaries that are the borrowers under the credit facility.

Citigroup Global Markets Inc., Mizuho Corporate Bank Ltd. and HSBC Bank USA, N.A. acted as joint lead arrangers and bookrunners. The other lenders participating in the facility are HSBC Bank Canada, Morgan Stanley Bank, N.A., PNC Bank, National Association, Bank of America, N.A., Bank of Tokyo-Mitsubishi UFJ, Ltd., Wells Fargo Bank, N.A., Compass Bank, Sumitomo Mitsui Banking Corporation, Arab Banking Corporation, Grand Cayman Branch, and U.S. Bank National Association.

Anthony Petrello, Nabors' Chairman and Chief Executive Officer, commented, "We are pleased to announce this new credit facility, which extends our credit facility maturity by three years to 2017. We appreciate the support and confidence of the lenders partnering with us in the new facility and welcome the Bank of Tokyo-Mitsubishi UFJ, Wells Fargo Bank, Compass Bank, Sumitomo Mitsui Banking Corporation, Arab Banking Corporation and U.S. Bank as new participants."

The Nabors companies own and operate approximately 521 land drilling rigs throughout the world and approximately 607 land workover and well servicing rigs in North America. Nabors' actively marketed offshore fleet consists of 40 platform rigs, 12 jackup units and 4 barge rigs in the United States and multiple international markets. In addition, Nabors is one of the largest providers of hydraulic fracturing, cementing, nitrogen and acid pressure pumping services with approximately 805,000 hydraulic horsepower currently in service. Nabors also manufactures top drives and drilling instrumentation systems and provides comprehensive oilfield hauling, engineering, civil construction, logistics, and facilities maintenance and project management services. Nabors participates in most of the significant oil and gas markets in the world.

Nabors Industries Ltd. (NBR)

By Zacks Equity Research | Zacks – Fri, Nov 2, 2012 1:00 AM

Based upon the number of near-term challenges, we are maintaining our Underperform recommendation on Nabors Industries Ltd. (NBR) shares. The land-drilling contractor is facing headwinds in the pressure pumping market on the back of collapsing prices and lower utilization. The recent weakness in the North American onshore rig count has also been a negative.

As usual, we remain concerned about weak natural gas fundamentals, which are likely to limit the company's ability to generate positive earnings surprises. Nabors' fairly debt-heavy balance sheet also remains an issue.

Considering these factors, we see Nabors as a risky bet from which ordinary investors should exit or avoid. This is corroborated by our $12 price objective, which is based on a 2013 P/E multiple of 7.8X.

http://finance.yahoo.com/news/nabors-industries-ltd-nbr-050004462.html

Nabors' 3Q2012 EPS Equals $0.42 from Continuing Operations, Excluding a $0.20 per Diluted Share, Non-Cash Ceiling Test Impairment

HAMILTON, Bermuda, Oct. 23, 2012 /PRNewswire/ -- Nabors Industries Ltd. (NYSE: NBR) today announced its results for the third quarter and nine months ended September 30, 2012. Adjusted income derived from operating activities was $225.5 million for the third quarter, compared to $269.3 million in the third quarter of 2011 and $230.4 million in the second quarter of this year. Excluding the Company's portion of its NFR affiliate's third quarter ceiling test impairment, which amounted to a pre-tax charge of approximately $96.3 million, or ($0.20) per diluted share, net income from continuing operations was $123.6 million, or $0.42 per diluted share. This compares to $132.5 million, or $0.45 per diluted share, in the third quarter of 2011 and $109.7 million, or $0.38 per diluted share, in the second quarter of this year when all non-cash charges are excluded. Third quarter GAAP net income from continuing operations was $65.8 million, or $0.22 per diluted share, compared to $87.2 million, or $0.30 per diluted share, in the third quarter of 2011 and a net loss of $98.7 million, or ($0.34) per diluted share, in the second quarter of this year.

Operating revenues totaled $1.77 billion in the current quarter, compared to $1.61 billion in the third quarter of last year and $1.74 billion in the second quarter of this year. For the nine months ended September 30, 2012, adjusted income derived from operating activities was $777.1 million, compared to $654.4 million in 2011. Net income from continuing operations for the first nine months of 2012 was $422.2 million, or $1.45 per diluted share, compared to $297.9 million, or $1.02 per diluted share, in 2011. Year-to-date GAAP net income from continuing operations was $109.8 million, or $0.38 per diluted share, compared to $252.6 million or $0.86 per diluted share in 2011.

The quarter's results reflect the receipt of $25.3 million in contract termination payments in the Company's US Lower 48 and International operations, of which $6.7 million, or $0.02 per diluted share, would have been received in future periods extending as far as December 2013. They also reflect a lower effective tax rate, a portion of which (approximately $5.5 million, or $0.02 per diluted share) was attributable to favorable return-to-provision tax adjustments in multiple jurisdictions.

Tony Petrello, Nabors' Chairman and CEO, commented, "These results reflect improved operational performance in our US land well servicing, International and Canada operations. Unfortunately, a sharper than anticipated drop in US land drilling activity, the seasonal hurricane pause in the Gulf of Mexico, further seasonal slowing in Alaska, and reduced shipments in Canrig essentially offset those improvements. Net income also benefitted from a meaningful reduction in our effective tax rate, which we expect to be ongoing.

"The quarterly exit rates in US land drilling activity, along with the seasonal slowdown in well servicing and pressure pumping utilization, signal a significantly weaker fourth quarter followed by a modest uptick in the first quarter with the seasonal improvement in Alaska and Canada.

"Our initiatives to reduce leverage and improve financial flexibility are beginning to yield meaningful results, with third quarter operating cash flow of $495 million exceeding capital expenditures by approximately $247 million. We also achieved an $80 million reduction in accounts receivable despite a $30 million increase in revenues, primarily attributable to an improvement in DSO (days sales outstanding). This improvement in cash generation contributed to funding the redemption of $275 million in maturing notes, $120 million in semi-annual interest payments and approximately $250 million in capital expenditures, while effecting a $159 million reduction in net debt during the quarter. We will continue to diligently manage capital expenditures and working capital and expect to further reduce net debt. Proceeds from any potential asset sales will accelerate this progress.

"We continue to streamline our business through a conversion from our historical business unit structure into two lines of business, Nabors Completion & Production Services (NCPS) and Nabors Drilling & Rig Services (NDRS). The consolidation of our US well servicing and pressure pumping operations into NCPS is progressing under a matrix organizational structure. The NCPS management team has been established down to the local operations level, while the integration of support functions and facilities is ongoing. The impact of these improvements will become more meaningful over the next few quarters, although it will be obscured by the fourth and first quarter seasonal weakness that characterizes these services, as well as the macro issues discussed below. As a first step in the formation of our NDRS business line, we recently began the consolidation of our US Offshore and Alaska operations into our US Lower 48 business group.

Drilling & Rig Services

"Sequential operating income for this line of business was essentially flat at $184.6 million, compared to the $186.2 million posted in the second quarter. Improving results in Canada and International essentially offset the adverse effects of declining activity in US Lower 48 land drilling, slower US Offshore activity during hurricane season, seasonally low activity in Alaska, and reduced shipments in Canrig. During the quarter, we averaged 13 fewer rigs working at 364 rig years, with the financial effects being substantially offset by a $657 increase in average margins bringing the third quarter average to $12,351 per rig day. Approximately $200 of this increase was attributable to the portion of the lump sum contract termination payments that represent margins that would have been earned in future periods.

"Operating income in our US Lower 48 operations was $114.9 million, approximately $11.6 million lower than the second quarter, with a lower average rig count of 193.8 rigs, partially offset by an $852 increase in average margins at $12,030 per rig day. This included $40 per rig day in early termination margins that are attributable to future periods. As we anticipated, last quarter our customers reduced second half spending significantly compared to the first half in order to stay within budget in light of reduced cash flows from weaker natural gas and liquids pricing. This reduction led to third quarter activity declines and will further depress fourth quarter results. Our rig count declined by 35 rigs in the quarter, with one-half of those rigs concentrated with four large customers who curtailed their programs as contracts expired. Sixteen of our 35 rigs received early termination payments totaling $16 million in third quarter income, with only $0.7 million of this amount attributable to future periods. These combined effects caused our rig count to decline disproportionately, as compared to the industry, and it currently stands at 175 rigs on revenue.

"We deployed seven new rigs this quarter, all with long-term contract commitments. Additionally, we have secured three incremental long-term contract commitments for our new generation PACE(®)-X rig. This brings to nine the number of PACE(®)-X rigs we have yet to deliver through the first half of 2013, all with long-term contracts. Our new generation PACE(®)-X rigs represent a step change in pad drilling efficiency and mobility. Nabors pioneered pad drilling and has developed the PACE(®)-X rig to more efficiently address the evolving demand for multi-row, multi-well pad configurations. Customer response to the new offering is encouraging and we expect to attract additional contracts. There is a significant increase in demand for rigs with pad drilling capability, particularly in the shale plays. With the delivery of these nine PACE(®)-X rigs our US Lower 48 operations alone will have 93 pad-capable rigs, with our other drilling operations possessing another 79 pad rigs.

"Looking forward, our customers are indicating a resumption of more normal activity as they initiate their 2013 budgets. This should improve utilization relative to current levels and possibly moderate pricing pressure, although a number of new rigs continue to enter the market with lower rates and shorter contract durations.

"Operating income in our International operations was $30.3 million, compared to $16.4 million in the second quarter. This included an early contract termination payment of $8.8 million, of which $6.0 million would have been earned in future periods. Rig activity was 119.2 rigs, two rigs less than the prior quarter, which saw four rigs temporarily idled in Algeria that should return to work around the end of this year. Margins improved by nearly $1,340 to $12,299 per rig day, including $547 representing the future portion of the early termination payments. The absorption of higher labor costs in certain Middle East countries, the temporarily idled Algeria rigs, and the need to perform some deferred contractual rig upgrades will dampen the pace of improvement in this unit for the next several quarters. Longer term, we remain focused on improving results at a modest pace.

"Our drilling operations in Canada experienced a large increase in income as they emerged from the second quarter, despite a wetter-than-usual start to the third quarter. Operating income was $22.9 million, compared to a loss of $3.7 million in the second quarter, and $1.3 was million higher than the same quarter last year. Rig activity increased sequentially by 14 to average 34 rigs operating in the third quarter, while margins improved significantly to average $13,439, an increase of $3,513 per rig day over the second quarter. As is the case in the US Lower 48, customer cash flow constraints are limiting growth in activity. Nonetheless, we anticipate our fourth quarter to show moderate improvement and the first quarter to increase modestly again. We are also deploying a new 1,500 horsepower rig with a pad drilling moving system under a five-year contract for a key customer.

"As anticipated, our US Offshore operations experienced a modest loss in the third quarter as many of our shallow-water customers suspended their work programs for hurricane season. We anticipate some recovery in the fourth and first quarters, but the shallow-water platform market is still plagued by increased regulatory requirements that are limiting activity.

"In Alaska, results were down seasonally as expected at $4.0 million, compared to second quarter results of $8.9 million and first quarter results of $27.4 million. This market has become highly seasonal due to the reduced level of year-round drilling work being conducted in the legacy North Slope fields where steeply progressive tax rates limit reinvestment. We expect the fourth quarter to decline further, but anticipate a sharp rebound in the first quarter with what promises to be another active exploratory drilling season. There continues to be a high level of optimism that the Alaska legislature will modify the tax structure for operators, which would spur a significant increase in activity over time. Longer term, a number of strategic projects are planned in new areas where tax incentives are already in place, but these are characterized by long lead times and would likely not commence for another two to three years.

"Our Other Rig Services entities saw lower results as our Alaska trucking and construction businesses slowed seasonally and Canrig experienced a moderate slowdown in rentals and domestic shipments, mirroring other land rig equipment manufacturers. Although Canrig's capital equipment backlog has decreased recently, in line with slower North American rig construction, recent international orders are partially offsetting the decrease.

Completion & Production Services

"During the quarter, operating income in our Completion & Production Services business line was $80.0 million, up from the $74.7 million realized in the second quarter. The majority of this increase came from higher average rates in well servicing, augmented by a small improvement in pressure pumping margins to 13.1 percent, compared to 12.3 percent in second quarter. We anticipate the usual seasonally lower results in the fourth and first quarters.

"Operating income attributable to the US well servicing and fluids management operations was $32.8 million for the quarter, up $4.2 million compared to the second quarter. While rig and truck hours were essentially flat to down slightly, higher average rates for both generated most of the increase. Rates and utilization have flattened and certain markets are becoming increasingly competitive, especially in the fluids management portion of this business. We expect seasonally lower activity through late first quarter, followed by a resumption of activity as our customers indicate higher spending levels and the population of maintenance-intensive oil wells continues to increase at a robust pace.

"In our Pressure Pumping operations, operating income increased modestly to $47.2 million compared to $46.1 million in the second quarter. The outlook remains challenging across all regional markets as most of our long-term contract crews are now working at minimum activity levels and spot-market rates remain under pressure. Some competitors are bidding work at what appears to be near breakeven cash flow levels. Given the status of the spot market, we recently idled another crew in the Permian basin bringing our number of stacked frac spreads to six.

"Although we may see a small increase in industry utilization in the new year, the amount of excess capacity will likely limit any upside potential for the foreseeable future. Meanwhile, we continue to focus on cost and efficiency, particularly relating to logistics and storage functions which have been centralized into our corporate procurement and logistics group. Inventory turns have increased significantly and material costs are improving.

"In summary, the near-term market for most of our services is challenging. Macro worries are still prevalent, and the lower levels of customer spending and seasonal constraints in North America are adversely affecting all areas of our operations. While we anticipate some increase in customer spending levels at the beginning of the new year, which will improve utilization moderately, it is not likely to absorb sufficient capacity to restore pricing momentum. That will come with a more meaningful increase in demand for rigs and other services, which can occur for a number of reasons, with improving gas prices having the greatest impact.

"Nonetheless, we believe our quality asset base, diverse product lines and geography, global infra-structure and talented employee base uniquely position us as opportunities arise, particularly in the expansion of unconventional resource development. Meanwhile, we will diligently continue to improve our balance sheet quality, streamline our business and achieve higher levels of operational excellence."

Financials continued at:

http://www.knobias.com/story.htm?eid=3.1.b0ef234fdfa77e0f83c4a2bd9c6aa1115034f2072920db774fff58e532cbce0f

NBR: Q3 Adj EPS 42c vs 45c Beats 36c Est

Tuesday , October 23, 2012 16:30ET

QUARTER RESULTS

Nabors Industries Ltd (NBR) reported Q3 results ended September 2012. Q3 Revenues were $1,674.12M; +1.90% vs yr-ago; MISSING revenue consensus by -2.34%. Q3 EPS was 26c. Adjusted Q3 EPS was 42c; -6.67% vs yr-ago; BEATING earnings consensus by +16.67%.

Q3 RESULTS Reported Year-Ago Y/Y Chg Estimate SURPRISE

---------- ------------ ------------ ---------- ------------ ----------

Revenues: $1,674.12M $1,642.95M +1.90% $1,714.30M -2.34%

---------- ------------ ------------ ---------- ------------ ----------

EPS: 26c N/A N/A N/A N/A

Adj EPS: 42c 45c -6.67% 36c +16.67%

---------- ------------ ------------ ---------- ------------ ----------

Nabors Tells SEC Fracking Isn’t a Risk to Water Supplies

By David Wethe - Sep 27, 2012 2:09 PM MT

http://www.bloomberg.com/news/2012-09-27/nabors-tells-sec-fracking-isn-t-a-risk-to-water-supplies.html?cmpid=yhoo

Nabors Industries Ltd. (NBR), the world’s largest onshore rig contractor, said hydraulic fracturing doesn’t pose a major risk to underground water supplies in response to questions from the U.S. Securities and Exchange Commission.

Publicly available fracking studies, including the Environmental Protection Agency’s 2004 report, haven’t “substantiated a material risk” of drilling fluids spilling into other areas, Hamilton, Bermuda-based Nabors said in a July 27 letter to the SEC made public in a filing today.

The SEC has reviewed filings and asked companies such as Nabors, Halliburton Co. (HAL) and SandRidge Energy Inc. (SD) to answer questions about fracking operations, a technique that blasts water, sand and chemicals into underground rock to unlock hydrocarbons. The SEC said possible risks to comment on include spillage and fracking fluids seeping underground.

Nabors told the SEC the biggest risk it faces related to fracking comes from the threat of increased regulations.

“Increased regulation of hydraulic fracturing could result in reductions or delays in drilling and completing new oil and natural-gas wells, which could adversely impact the demand for fracturing and other services,” the company said.

The SEC has completed its review of Nabor’s filings, the company said.

NBR 3Q earnings 10-23-12 AMC

Nabors Industries Ltd. Third Quarter 2012 Earnings Conference Call Invitation

Monday , September 24, 2012 07:00ET

HAMILTON, Bermuda, Sept. 24, 2012 /PRNewswire/ -- Nabors Industries Ltd. (NYSE: NBR) invites you to join Anthony G. Petrello, Chairman and Chief Executive Officer, Wednesday, October 24, 2012 at 10:00 a.m. Central Time for a discussion of operating results for the third quarter 2012. Nabors will release earnings after the market closes on Tuesday, October 23, 2012.

Date: October 24, 2012

Time: 10:00 a.m. CT (11:00

a.m. ET)

Dial-in-number(s):

Domestic: (877) 941-1427

International: (480) 629-9664

Conference ID: 456291

Please call ten minutes ahead of time to ensure proper connection. The conference call will be recorded and available for replay for one week, beginning at 1:00 p.m. Central Time on October 24, 2012. To hear the recording, please call (877) 870-5176 domestically or (858) 384-5517 internationally and enter conference ID 4562916.

Nabors will have a live audio webcast of the conference call available on its website at www.nabors.com. Navigate to the Investor Relations page and then select Events Calendar to join the webcast. An electronic version of the earnings release and supplemental presentation will also be available to download from the website.

Sinopec, Nabors to Replace YPF Frankenstein Rigs, Official Says

By Pablo Gonzalez - Sep 6, 2012 10:48 AM MT

http://www.bloomberg.com/news/2012-09-06/sinopec-nabors-to-replace-ypf-frankenstein-rigs-official-says.html?cmpid=yhoo

YPF SA (YPFD), Argentina’s biggest energy company, signed contracts with oil services providers including Nabors Industries Ltd. (NBR) and China Petroleum & Chemical Corp. (386) to rent 14 drilling rigs for its shale exploration program, a YPF official briefed on the matter said.

The contracts, awarded through private auctions, will increase the number of rigs used by the Buenos Aires-based company by 47 percent from the first half of 2012, the YPF official said.

Starting next year, YPF will add 10 more rigs annually to reach the 1,200-well a year target pledged by Chief Executive Officer Miguel Galuccio in the company’s five-year business plan on Aug. 30, the official said. Galuccio also introduced a $37.2 billion investment plan until 2017 seeking to boost oil and gas output by 29 and 23 percent, respectively.

YPF should accelerate plans to rent additional rigs so the company can stop using outdated, inefficient rigs from the 1970s, known internally as Frankensteins, the YPF official said.

The one- to three-year rental accords will cost an average $10 million a rig each year, he said. YPF will invest $70 million in the second half of 2012 to rent the equipment in addition to $150 million for its 30 existing rigs, he said.

YPF will offer incentives to oil services companies to produce rigs in Argentina, the official said, declining to elaborate.

“Each drilling rig cost between $18-20 million, so, if we will need 50, it makes sense,” he said.

Cost Reductions

YPF will be able to reduce well costs that average 60 percent more than U.S. expenses with better equipment, the official said.

Besides Nabors, the world’s largest land-rig drilling contractor, and China’s Sinopec, the other companies that signed contracts for the 14 rigs are Italy’s Trevi Group SpA, Estrella International Energy Services Ltd. (EEN), Venver SA, Emepa SA, Lupatech SA (LUPA3)’s San Antonio Internacional Ltda., and DLS Drilling Logistics and Services Corp., the YPF official said.

“We do not comment on any customer matters unless initiated or approved by the customer as a matter of policy,” Denny Smith, a Nabors spokesman, said in an e-mailed response from Houston.

Sinopec, Trevi

Sinopec signed two contracts, according to the YPF official. One of the rigs is working in the Vaca Muerta shale formation in Argentina’s Neuquen province and the other is scheduled to arrive from China next month, the official said. Trevi will send three rigs in March 2013, he said.

Alejandro Di Lazzaro, a spokesman for YPF in Buenos Aires, didn’t immediately respond to telephone calls or an e-mail. A Sinopec official in Argentina declined to comment. Trevi- Petreven Argentina President Ruben Moleon didn’t respond to telephone calls and e-mails seeking comment.

The Vaca Muerta region in southern Argentina is estimated to hold at least 23 billion barrels of oil in resources, according to a survey by Ryder Scott.

Estrella Vice President Luis Aviles didn’t respond to a telephone call or e-mail. Emepa spokesman Marcos Aguilera didn’t reply to telephone calls or e-mails. Venver General Manager Cristina Ojeda didn’t respond to an e-mail seeking comment.

DLS, a part of Archer Ltd. (ARCHER), the Norwegian oilfield services provider based in Hamilton, Bermuda, didn’t respond to telephone calls and e-mails seeking comment. San Antonio didn’t respond to e-mails and telephone calls.

Nabors Lowered to Underperform

By Zacks Equity Research |

http://finance.yahoo.com/news/nabors-lowered-underperform-222431115.html

Based upon the number of near-term challenges, we have lowered our recommendation on onshore contract driller Nabors Industries Ltd. (NBR) to Underperform from Neutral.

Barbados-based Nabors conducts oil, gas and geothermal land drilling operations and is the largest land-drilling contractor in the world. It is also one of the largest land well servicing companies and workover contractors in the U.S. The company offers a number of ancillary wellsite services, including oilfield management, engineering, transportation, construction, maintenance, well logging, and other support services in select domestic and international markets.

We are concerned about the weakness in Nabors’ pressure pumping business. Deterioration in pricing and utilization, coupled with the spike in costs, is likely to adversely impact the company’s second half results. The depressed North American onshore rig count has also been a negative.

As usual, we remain worried about weak natural gas fundamentals, which are likely to limit the company’s ability to generate positive earnings surprises. The glut in domestic gas supplies still exists, with storage levels remaining well above their benchmark levels.

This will continue to weigh on natural gas prices in the near-to-medium term. Nabors – the largest North American land drilling contractor ahead of Patterson-UTI Energy Inc. (PTEN) – remains particularly exposed to this situation since its business in the region is heavily biased to gas drilling.

Nabors’ relatively weak balance sheet in this severe credit-constrained environment (debt-to-capitalization ratio of approximately 45%) is also a cause for concern. Over the last few years, the company kept adding debt to its balance sheet for a fleet recapitalization program.

Considering these factors, we see Nabors as a risky bet from which ordinary investors should exit. Our new long-term Underperform recommendation is supported by a Zacks #5 Rank (short-term Strong Sell rating).

(Let's say I was ordinary? What then? ;)

NBR:Breakout territory

currently 15.89 +.68 on 7.4m (above ave volume)

(open gap at up Aug-03-2012 13.62 to 13.73)

Support/Resistance

Type Value Conf.

resist. 22.64 2

resist. 20.84 2

resist. 19.68 4

resist. 17.70 3

resist. 17.32 2

resist. 16.98 2

resist. 16.11 2

resist. 15.40 2

supp 14.90 5

supp 13.92 25

supp 12.86 10

Nabors: Positive Catalysts Will Create Upside For Medium- To Long-Term Investors

http://seekingalpha.com/article/769411-nabors-positive-catalysts-will-create-upside-for-medium-to-long-term-investors?source=yahoo

August 1, 2012 | by: Kedar Special Situations |

NBR After declining 50% over the last year, 3Q12 will present a great opportunity to take a long position in Nabors (NBR) for those investors looking to profit from NBR's turnaround in FY2013.

Long: Nabors Industries

Current share price: $13.90

Potential Return: $ 6 to $ 10 per share with a short term $1-$2 downside

Market Capitalization: $4.2B

Cash: $460M; Total Debt: $4.7B

Leverage: 2.1x; Interest Coverage: 8x

Shares Outstanding: 290M

Gross Margin: 35%; Operating Margin:12%

Tangible BVPS:$16.30; 2013 Forward P/E: Approximately 5x

Sector: Basic Materials; Industry: Oil & Gas Drilling & Services

Trading timeline: 15-18months; Important time: 3Q-2012

Main Catalyst: Ongoing Divestitures, Management changes, Changes in NBR bylaws in addition to Sector M&A; turnaround in International and offshore operations, deleveraging of balance sheet and realignment to business leading to better company valuation; Fundamentally undervalued

How might I trade: Start a tracking position and build it up through 3Q12.

Thesis

Nabors Industries' restructuring catalysts present a compelling opportunity for investors looking to benefit from investing in a stock that has fallen more than 50% over the last year. The downtrend in the share price is caused by a mix of certain events - some firm specific while some arising due to macro economic and political headwinds. On a macro level, NBR's exposure to the natural gas industry has been a negative. The downfall in natural gas prices led to depletion charges in NBR E&P properties, negatively impacting earnings. Furthermore, business in Alaska has also been on a downtrend due to delay in expected tax laws. However NBR seems to be regaining its footing in Alaska and seems to be trending back to 2008/09 revenue numbers. The macro impact was further exacerbated by the occurrence of the BP oil spill in the Gulf in FY10 that negatively impacted the drilling industry by increasing regulatory risk leading to significant potential cost increases. In addition to the macro headwinds, the Arab uprising in the Middle East and the political unrest in Latin America has been a negative for NBR. 50% of NBR's international business is exposed to North Africa & Middle East while 38% of international exposed to Latin America. On the factors specific to NBR, concerns that the firm was overexposed to the gas industry, in addition to the negative publicity from shareholder lawsuits related to the $100M payout controversy regarding the then CEO, Eugene Isenberg created doubts in the minds of shareholders leading to the major sell-off.

Despite the negative factors, I am convinced that NBR will make a good investment for medium- to long-term investors. My conviction is borne out of certain ongoing hard and soft catalysts that are in play. One is the ongoing restructuring that NBR has been undergoing, which includes realignment of NBR business into two reportable segments. This should lead to better future valuation for the firm. Another is the ongoing divestiture of $600M-$800M in non-core and Oil & Gas (O&G) assets, 33% of which is already been completed. The proceeds are intended to go towards deleveraging the balance sheet. Then there are the recent management appointments and changes to NBR's bylaws that include removal of the former CEO and declassification of the board. If industry consolidation were to occur, then the change in bylaws coupled with recent restructuring of the business and new management changes may signal a potential future sale of the company. The sale thesis is further supported by the strategy implemented by the new management, which includes a change in revenue mix and creation of a better hedged revenue model, where drilling is complemented by well servicing operations, and rig exposure is now majorly focused on drilling for oil & gas liquids. Adding to the upside is the turnaround in Alaskan and international operations created by restructuring and calm in the Middle East & North African political climate. The restructuring efforts are obvious from the reported data over the last 25 quarters where NBR is finally reporting a turnaround in its 1H12 revenue and operating earnings. Furthermore, competitive analysis and some of the parts analysis shows that the firm remains fundamentally undervalued. The ongoing catalysts should close the gap between the current valuation and NBR's fair value over the next 12 months creating substantial upside for shareholders.

Business Overview

Nabors Industries is a land drilling contractor with significant exposure to horizontal drilling as per management remarks in 2Q12. As recently as 1Q12, NBR started reporting as two different segments, Contract Drilling Services and Completion & Production Services.

Segments -

Contract Drilling - Simply put, this segment consists of Rigs that are deployed around the world to drill for Oil, Gas and Gas liquids. Rigs usually work under either long-term contracts, which last of 1-3 years or under day work contracts. Long-term contracts have recently shrunk from 1-3 years to 6-9 months. The demand for contracts is driven by commodity costs that directly impact cash flows and demand from oil & gas majors who are NBR clients. Contract Drilling segment contains six sub segments; U.S. Lower 48 land drilling (27% of total revenue, 40% of total Operating income, 26% operating margin); U.S. Offshore (4%; 2.4%; 11%); Alaska (3.4%; 8.5%; 44%); Canada (11%; 8.5%; 26%) and International (17%; 6.5%; 6.9%). The other rig services is about 13% of total revenue, 9% of total operating income and 12.3% operating margin. Despite pressure on the drilling industry, NBR reported QoQ increase in revenue and operating income in 2012, which speaks to management's efforts to slowly restructure the business by reigning in costs, selling non-core assets and creating best-available revenue opportunities for the deployed assets. Although margins per rigs have increased sequentially in 2Q12 for the U.S. lower 48 and offshore segments, the Canadian and Alaskan segments have reported a marginal decline due to seasonal factors and weather coming into play. Despite major headwinds, NBR's operating income and revenue have reported QoQ increase for 2012 and the firm has been able to withstand Marco pressures - a positive for shareholders.

Completion and Production Services - This segment consists of pressure pumping services and oil well services. The firm added pressure pumping services to this segment in 2010 and this segment has grown to 33% of the total revenue. QoQ, the segment was up in terms of both revenue and operating income. Operating margins for the segment are seeing a turnaround in 2012, increasing from the lows of 7% in 2009/2010 to approximately 14% in 1H12. Well services, part of C&P, provides a good hedge to NBR's revenue model, especially with pressure pumping business coming under pressure. In the 2Q12 conference call, NBR acknowledged that despite pressure pumping business reporting a decline, the segment reported higher QoQ revenue as demand for servicing wells has increased. The growth of this segment due to current restructuring in E&P industry, which is expected to create higher demand for NBR's well servicing segment, provides a good revenue hedge thereby positively impacting NBR's shareprice.

Rig Exposure

A lot has been made of NBR's rig exposure. Of the total NBR rigs, which include well-servicing, offshore and onshore rigs, approximately 65% of rigs are exposed to the U.S. Another 15%-20% have exposure to Canada and the rest are international. Within the U.S., the rig exposure looks decently well hedged. Of the total deployed rigs as of 2Q12, about 130 have exposure to oil, 36 are exposed to dry gas, 41 exposed to gas liquids and 3 rigs for other purposes. NBR has deployed 11 new rigs in 2Q12. In Canada, NBR is divesting certain assets since they do no complement its services business in the region. Internationally, 50% of rig exposure is to Middle East and North Africa. As has been noted earlier, despite reported decline in the pressure pumping segment expected to report decline in 2H12, the growing well services business provides a good hedge. Moreover, management has stated that offshore operations have reported decent demand and are expected to see a pickup in the activity in 4Q12, after the hurricane season. Data mentioned by the management indicates that concerns regarding NBR's rig exposure may be overblown. With the revenue and margin numbers finally turning a corner and NBR's hedged exposure to the oil & gas drilling still largely not discounted in the share price, it might be a good time to investors to look at the firm.

MAJOR CATALYST -

Divestitures to de-lever Balance sheet - The implementation of the new divestiture strategy followed the 2H11 appointment of the new CEO and the lead director to the board. Management declared that it intended to divest Oil & Gas (O&G) operations and certain non-core assets to raise $600M -$800M. According to the firm, the cash generated from this sale will be used to directly pay down debt and de-lever the balance sheet. Since the announcement, the firm has already raised $154M in proceeds from the sale of certain O&G assets. According to NBR, another $225M-$325M divestitures of O&G properties including those in Eagle Ford are in process but slightly delayed due to its partner, Geo Resources recently getting a buyout offer from Halcon. Despite the delay, what's positive for NBR shareholders is that Geo's buyout affirms valuations for NBR assets in the region. Divestiture related to non-core assets, which include properties in Canada and Alaska are expected to raise another $300-$400M. O&G properties in Canada are said to be in the same region as that of Nexen Inc, which is currently being bought out by China's COONC for $15B. Additionally, certain offshore rigs are being currently evaluated for sale. Assuming a 6.5% weighted average coupon on the debt and a 25% tax rate (higher than median tax rate since 2006), a reduction in the debt of $1B should add approximately $0.22 to the EPS. With a P/Ex of 9.5, the debt reduction might add $1.50 to $2.50 to NBR's share price. Additionally, NBR took $198M in impairment charges for FY11, $100M related to the compensation of former CEO and $98M related to assets. NBR has also recorded depletion expense over the years related to its O&G properties. However, with the divestiture of its O&G assets, reversal of $100M CEO compensation and sale of certain older offshore rigs, NBR should be able to add $3.50 to $4.50 per share, assuming 25% tax rate and a P/Ex of approximately 9.5x.

Potential turnaround in International operations - According to NBR data, international rig exposure excluding well-serving operations constitutes 26% of the total NBR rigs. Of this, more than 50% is exposed to North Africa and Middle East. This sector has seen marginal decline in revenue from $1.3B in 2008 to $1.1B in 2011. This represents a decline from 25% of the total revenue to 16%. Furthermore, operating margins for the business has significantly declined from 30% in 2008 to 7% as of 1Q12. The decline in the operating margins despite only a marginal decline in revenue does speak to the rising costs. NBR admitted in 2Q12 that it was forced to increase salaries and pay one-time compensation to workers in countries such as Saudi Arabia. Furthermore, certain contracts for which NBR won the rights were cancelled due to political reasons in countries such as Algeria. Another reason for cost increases could be a decline in drilling activity that could have also resulted in higher fixed costs for the firm. These governmental dictates to raise salaries or cancel contracts might be due to recent Arab uprising in the Middle East and political instability in the North African nations. However, with elections being held and the political climate somewhat stabilizing, I believe that international operation should show marginal improvement in the business and add to NBR's bottom-line in 2H13. Another segment, U.S. Offshore, which constitutes only 4% of total revenue reported negative operating margins in 2011. Certain rigs related to offshore drilling are currently under consideration to be sold. Certain industry reports have indicated a comeback in the offshore drilling market. This was confirmed by NBR, which stated in 2Q12 call that they saw better performance from their offshore segment (operating revenue improved from (1.1M) in 2Q11 to $10M in 2Q12) and believe the business will pick up post hurricane season in 4Q12. It should also be noted that after accounting for seasonality in the business, the firm is reporting a turnaround in its segments in 1H12 after reporting major declines since FY09 and FY10. This segment along with the turnaround in international operation remains largely undiscounted and should create shareholder upside.

Management changes and Business Realignment may signal better valuation and future Sale - After the controversy over CEO payout in 2011, which subsequently led to shareholder litigation, there are certain noticeable changes in the ranks of NBR. First among them is the removal of Eugene Isenberg who earlier was supposed to be paid $100M and later chose to forgo the payment due to shareholder lawsuits. The person replacing him is the current CEO and former deputy chairman of the board, Mr. Anthony G. Petrello who has been historically known as a hands-on manager with intense focus on operations - the kind of leadership that NBR currently needs. Another noticeable promotion was of John Yearwood, who was promoted as the lead director in 2011. He is the former CEO of Smith International where he was instrumental in successfully negotiating and completing the sale of Smith to Schlumberger in 2010. Prior to that he spent 27 years with Schlumberger in numerous operations management and staff positions throughout the world including as President and in financial director positions. In addition to make certain noticeable changes to the management and the Board, NBR also made changes to its bylaws where is decided to declassify its board. Moreover, NBR adopted a shareholder rights plan on July 17, 2012, which is set to expire on July 16, 2013. Although the management is not opposed to an offer, the firm is opposed to someone acquiring NBR shares without paying a control premium. This action speaks to management's belief that firm is currently undervalued firm. New management's decision to report operations in two distinct segments to potentially unlock value is a proof that it is determined to execute the strategic initiative and create better shareholder value in an event of an offer. In addition to reporting in two different segments, the company also recently appointed new management teams for the two divisions making them fully functional. As noted earlier, NBR's increasing balanced revenue mix also makes it attractive, both as an investment and as a target. Given the new management, current strategic initiatives and a potential consolidation in the industry, shareholders should benefit even if NBR chooses to remain a standalone company and an eventual sale does not go through.

Fundamentally Undervalued - NBR has $460M in cash and $4.7B in debt on its balance sheet. Despite the debt, NBR is leveraged 2.4x while its interest coverage ratio is 8.0x. Of the total $4.7B in debt, only $275M are due until 2018 while NBR's $1.4B credit facility of which $490M is still available is due in September, 2014. Firm has $1B available in total liquidity, which should help alleviate any liquidity concerns - a major issue with capital intensive business. For the first time in 2H of 2012, the firm generated more operation cash flow than it spent on Capex demonstrating management's commitment to rein in costs and increase its cash flow. Looking at approximately 25 quarters of data, the year-over-year operating margins, both for the Drilling as well as Completion & Production Services have started to move up again toward the 2007 highs. This is a result of management's effort to slowly restructure the company whose share price is weighed down by Oil & Gas pricing pressure as well as from 2011 controversy surrounding NBR's CEO. After performing valuation on the company, the shares can be valued at $22.50 to $24.00 per share by the end of 2013.

The $22.50 valuation is derived by assuming that the firm only pays off $500M in debt instead of $1B, only generates $1.50 in EPS in 2013 instead of industry estimates of $2.20 while reporting $2B in 2013 EBITDA. I have used 2013 EBITDAx of 5.15x, 2013 EV/REVx of 1.39x and 2013 P/Ex of 9.5x.

Breaking the firm down and performing SOTP analysis yields $24.15. This assumes a 2013 P/REVx of 1.39 and 2013 P/EBITx of 7.2 for Drillers while 0.95x and 2.78x respectively for Completion & Production services. Moreover, if NBR becomes a takeover targets due to above mentioned catalysts, a modest 15% takeover premium for NBR yields an average price of $26 per share.

Assuming that Pressure pumping decreases by another 10% and U.S. lower 48 by 5% in 2013 while all other segments increase by a modest 3%, I still come up with a 2013 EPS of $1.9. Assuming an industry estimated forward P/Ex of 9.5x, that still yields a price of approximately $18.00.

With current share price trading at $13.90, the shares still offers a 30% margin of safety to investors who are pessimistic about a major NBR turnaround. As the above mentioned catalysts play out, I believe that investors will benefit.

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours

NBR has $460M in cash and $4.7B in debt on its balance sheet. Despite the debt, NBR is leveraged 2.4x while its interest coverage ratio is 8.0x. Of the total $4.7B in debt, only $275M are due until 2018 while NBR's $1.4B credit facility of which $490M is still available is due in September, 2014. Firm has $1B available in total liquidity, which should help alleviate any liquidity concerns - a major issue with capital intensive business. For the first time in 2H of 2012, the firm generated more operation cash flow than it spent on Capex demonstrating management's commitment to rein in costs and increase its cash flow.

Looking at approximately 25 quarters of data, the year-over-year operating margins, both for the Drilling as well as Completion & Production Services have started to move up again toward the 2007 highs. This is a result of management's effort to slowly restructure the company whose share price is weighed down by Oil & Gas pricing pressure as well as from 2011 controversy surrounding NBR's CEO. After performing valuation on the company, the shares can be valued at $22.50 to $24.00 per share by the end of 2013.

The $22.50 valuation is derived by assuming that the firm only pays off $500M in debt instead of $1B, only generates $1.50 in EPS in 2013 instead of industry estimates of $2.20 while reporting $2B in 2013 EBITDA. I have used 2013 EBITDAx of 5.15x, 2013 EV/REVx of 1.39x and 2013 P/Ex of 9.5x.

Breaking the firm down and performing SOTP analysis yields $24.15. This assumes a 2013 P/REVx of 1.39 and 2013 P/EBITx of 7.2 for Drillers while 0.95x and 2.78x respectively for Completion & Production services. Moreover, if NBR becomes a takeover targets due to above mentioned catalysts, a modest 15% takeover premium for NBR yields an average price of $26 per share.

Assuming that Pressure pumping decreases by another 10% and U.S. lower 48 by 5% in 2013 while all other segments increase by a modest 3%, I still come up with a 2013 EPS of $1.9. Assuming an industry estimated forward P/Ex of 9.5x, that still yields a price of approximately $18.00.

With current share price trading at $13.90, the shares still offers a 30% margin of safety to investors who are pessimistic about a major NBR turnaround.

NBR: Q2 Adj EPS 38c vs 23c Meets 38c Est

Tuesday , July 24, 2012 16:09ET

QUARTER RESULTS

Nabors Industries Ltd (NBR) reported Q2 results ended June 2012. Q2 Revenues were $1,737.11M; +27.33% vs yr-ago; MISSING revenue consensus by -0.40%. Q2 EPS was (25c). Adjusted Q2 EPS was 38c; +65.22% vs yr-ago; MATCHING earnings consensus.

Q2 RESULTS Reported Year-Ago Y/Y Chg Estimate SURPRISE

---------- ------------ ------------ ---------- ------------ ----------

Revenues: $1,737.11M $1,364.21M +27.33% $1,744.05M -0.40%

---------- ------------ ------------ ---------- ------------ ----------

EPS: (25c) N/A N/A N/A N/A

Adj EPS: 38c 23c +65.22% 38c 0.00%

---------- ------------ ------------ ---------- ------------ ----------

Nabors 2Q 2012 EPS Equals $0.38, Excluding Non-cash Charges

HAMILTON, Bermuda, July 24, 2012 /PRNewswire/ -- Nabors Industries Ltd. (NYSE: NBR) today announced its financial results for the second quarter and first six months of 2012. The Company posted adjusted income derived from operating activities of $230.4 million for the current quarter which compares to $177.5 million in the second quarter of 2011 and $321.2 million in the first quarter of 2012.

Net income from continuing operations, excluding certain non-cash charges, was $109.7 million ($0.38 per diluted share) compared to $70.9 million ($0.24 per diluted share) in the second quarter of 2011 and $188.9 million ($0.65 per diluted share) in the first quarter of 2012. Operating revenues and earnings from unconsolidated affiliates totaled $1.7 billion in the current quarter compared to $1.4 billion in the second quarter of last year and $1.9 billion in the first quarter of this year.

For the six months ended June 30, 2012, adjusted income derived from operating activities was $551.6 million compared to $385.1 million in the first six months of 2011. Net income from continuing operations for the first six months of 2012 was $298.6 million ($1.03 per diluted share) compared to $165.4 million ($0.57 per diluted share) in 2011. Operating revenues and earnings from unconsolidated affiliates totaled $3.6 billion for the first six months of 2012 compared to $2.7 billion for the first six months of 2011. Net income from discontinued operations for the current quarter was $24.7 million ($0.09 per diluted share), reflecting gains realized upon the sale of our remaining E&P operations in Colombia.

Including the $293.0 million ($0.72 per diluted share) of non-cash charges incurred in the quarter, GAAP net income from continuing operations was a loss of $98.7 million ($0.34 per diluted share). The largest of these charges was $145.5 million, representing the Company's portion of impairments to the reserve valuation in its NFR Energy joint venture as a result of the quarterly ceiling test, which applies the 12-month trailing average natural gas price. The balance of the non-cash charges consisted of $75.0 million from elimination of the intangible asset value of the Superior Well Services trade name, $46.2 million in asset retirements, and goodwill elimination of $26.3 million in our International and US Offshore operations.

Tony Petrello, Nabors' Chairman and CEO, commented, "Second quarter results, while short of our expectations in Pressure Pumping and International operations, illustrate the capacity of long-term contracts to limit downside exposure and sustain healthy levels of operating cash flow in weakening market conditions. As we saw with falling natural gas prices in the first quarter, the second quarter drop in prices for crude oil and natural gas liquids is further constraining customer cash flow and spending. These spending reductions, combined with the entry of newly built rigs without term commitments, are resulting in an increasingly competitive land rig market. The near term impact is diminished by our term contract coverage, but that mitigation dissipates with time. Fortunately, the longer term outlook for our business remains promising as expanded shale development will require continued drilling to offset decline rates, leading to higher demand for our services.

"Our Pressure Pumping and International segments notwithstanding, our second quarter results were in line with or modestly ahead of our expectations. The best sequential performance came from our US Well-servicing operations where we mitigated the impact of a declining Northeast market by quickly reducing costs and repositioning excess equipment into more active areas. The majority of our shortfall was in Pressure Pumping where lower revenues and higher costs disproportionately affected margins. Similarly, our International unit also fell short of expectations with startup delays and significantly higher costs.

Drilling & Rig Services

"Operating income in Drilling and Rig Services decreased by approximately $80.8 million sequentially with the sharp seasonal decline in results in Canada and Alaska combined with a decrease in our International results.