News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Second quarter revenue totaled $28.2 million, a 19% increase over the same period in 2012

MAKO Surgical Corp. Reports Operating Results for the Second Quarter 2013

4:05 PM ET 7/30/13 | GlobeNewswire

Second Quarter 2013 Highlights

Second quarter revenue totaled $28.2 million, a 19% increase over the same period in 2012

Ten RIO(R) systems sold in the second quarter, of which eight were sold to domestic customers

A total of fifteen RIO systems sold worldwide in the first six months of 2013, increasing worldwide commercial installed base to 171 RIO systems and domestic commercial installed base to 164 RIO systems

3,274 MAKOplasty(R) procedures performed in the second quarter, a 26% increase over the same period in 2012

6,262 MAKOplasty procedures performed in the first six months of 2013, a 28% increase over the same period in 2012

MAKO Surgical Corp. (Nasdaq:MAKO), a medical device company that markets its RIO(R) Robotic Arm Interactive Orthopedic surgical platform, MAKOplasty(R) joint specific applications and proprietary RESTORIS(R) implants that together enable orthopedic surgeons to consistently, reproducibly and precisely treat patient specific osteoarthritic disease, today announced its operating results for the quarter ended June 30, 2013.

Recent Business Developments

RIO Systems - Ten RIO systems were sold during the second quarter, of which eight were sold to domestic customers and two were sold through international distributors in Italy and Turkey. The revenue associated with one RIO system sold to and customer accepted by our Italian distributor will be deferred until all revenue recognition criteria are satisfied. These ten RIO systems bring MAKO's worldwide commercial installed base of RIO systems to 171 systems and domestic commercial installed base to 164 systems as of June 30, 2013. At the end of the quarter, MAKO had 164 MAKOplasty sites worldwide. Nine MAKOplasty total hip arthroplasty, or THA, applications were sold during the quarter, six of which were sold with new RIO systems sales and three of which were sold as upgrades to existing customers with knee-only commercial systems. As of June 30, 2013, 111 RIO systems, or 65% of the worldwide commercial installed base, have the MAKOplasty THA application.

MAKOplasty Procedure Volume - During the second quarter, 3,274 MAKOplasty procedures were performed, of which 3,125 were performed at domestic sites and 577 were THA procedures. The 3,274 MAKOplasty procedures performed represent a 10% increase over the procedures performed in the first quarter of 2013 and a 26% increase over the procedures performed in the second quarter of 2012. The 577 THA procedures performed represent a 24% increase over the THA procedures performed in the first quarter of 2013 and a 106% increase over the THA procedures performed in the second quarter of 2012. The average monthly utilization per site for all MAKOplasty procedures was 7.0 procedures during the second quarter of 2013, an increase from 6.6 procedures during the first quarter of 2013. Through June 30, 2013, approximately 29,000 procedures had been performed since the first procedure in June 2006.

Clinical Research and Marketing - At the 2013 Computer Assisted Orthopedic Surgery meeting in June, three key presentations were made on MAKOplasty. First, Dr. Bryn Jones presented additional early data from the randomized controlled trial (RCT) performed at the Glasgow Royal Infirmary with the University of Strathclyde. Dr. Jones presented three-month data for the entire cohort of 139 patients highlighting accuracy, pain level, American Knee Society scores and hospital cost savings. MAKOplasty unicompartmental knee procedures results were favorable to the manually placed Biomet Oxford(R) implants in nearly all measured categories. Second, Dr. Riyaz Jinnah's group presented data on a retrospective registry review of 125 lateral uni-compartmental knee arthroplasty, or UKA, patients, 88 of which were MAKOplasty patients. At the patients' 24 month follow up appointment, the MAKOplasty lateral UKA group had a statistically significant lower revision rate, shorter average hospital stay and better alignment than the manual lateral UKA group. Lastly, Dr. Benjamin Domb's group presented data comparing acetabular cup position for a matched pair series of 50 MAKOplasty total hip procedures versus 50 manual total hip procedures. The data showed that 92% of the MAKOplasty cups were within the stricter Callanan, or Massachusetts General Hospital, safe zone, compared to 62% of the conventional cups. All results are statistically significant, and provide additional evidence of the clinical and economic benefits of MAKOplasty over manual procedures.

"We are pleased that our programs implemented in the first quarter to drive utilization and system sales are beginning to show positive business results," said Maurice R. Ferre, M.D., President and Chief Executive Officer of MAKO. "Additionally, the recently released favorable data on both knee and hip MAKOplasty provides continuing support for the clinical value proposition of our procedures."

2013 Second Quarter Financial Review

Revenue was $28.2 million in the second quarter of 2013 compared to $23.7 million in the second quarter of 2012, representing a 19% increase. The increase in revenue was primarily attributable to the recognition of revenue of 3,274 MAKOplasty procedures performed, which represents a 26% increase over the procedures performed in the second quarter of 2012, and an increase in service revenue.

Gross profit for the second quarter of 2013 was $16.8 million compared to a gross profit of $17.3 million in the same period in 2012. Gross margin for the second quarter of 2013 was 59%, consisting of a 51% margin on procedure revenue, a 62% margin on RIO system revenue and a 91% margin on service revenue. Procedure gross margin for the second quarter of 2013 was negatively impacted by an inventory valuation adjustment of $4.1 million for excess hip implant inventory related to the RESTORIS Trinity Cup and RESTORIS Metafix Femoral Stem implant system and the RESTORIS Z implant system. The valuation adjustment was primarily due to the greater than anticipated adoption of our RESTORIS PST Cup and Tapered Femoral Stem hip implant system, or RESTORIS PST implant system, which MAKO commercially launched in October 2012, as a percent of total THA procedures. In the second quarter of 2013, over 75% of the THA procedure volume was performed with the RESTORIS PST implant system.

Operating expenses were $29.6 million in the second quarter of 2013 compared to $25.8 million in the second quarter of 2012. The increase in operating expenses was primarily due to the new medical device tax, which became effective January 1, 2013, and a $2.0 million asset impairment charge for excess hip implant instrumentation associated with the RESTORIS Trinity Cup and RESTORIS Metafix Femoral Stem implant system and the RESTORIS Z implant system.

Net loss for the three months ended June 30, 2013 was $19.7 million, or $(0.42) per basic and diluted share, based on average basic and diluted shares outstanding of 46.9 million. Included in net loss for the second quarter of 2013 was a non-cash and non-operating expense of $6.9 million associated with the change in fair value of a derivative asset related to a credit facility agreement. Upon expiration of the credit facility's draw period on May 15, 2013, the derivative asset had no value resulting in a $6.9 million charge to non-operating expense in the second quarter of 2013. This compares to a net loss for the same period in 2012 of $8.5 million, or $(0.20) per basic and diluted share, based on average basic and diluted shares outstanding of 42.2 million.

Cash, cash equivalents and available-for-sale investments were $62.9 million as of June 30, 2013 compared to $73.3 million as of December 31, 2012.

2013 Six-Month Financial Review

Revenue was $53.0 million for the six months ended June 30, 2013 compared to $43.3 million for the six months ended June 30, 2012, representing a 22% increase. Revenue for the six months ended June 30, 2013 primarily consisted of $31.2 million in revenue from the sale of implants and disposables used in the 6,262 MAKOplasty procedures performed in the six months ended June 30, 2012, $14.7 million in revenue from the sale of fourteen RIO systems, ten of which included MAKOplasty THA applications, four MAKOplasty THA applications sold to existing customers, recognition of two previously deferred international commercial RIO system sales, and $7.1 million in revenue from service. In addition to the fourteen recognized RIO system sales, the revenue associated with the sale of one international commercial system including a MAKOplasty THA application was deferred until all revenue recognition criteria are satisfied.

The net loss for the six months ended June 30, 2013 was $29.3 million, or $(0.63) per basic and diluted share, based on average basic and diluted shares outstanding of 46.9 million. Included in net loss for the six months ended June 30, 2013 was non-cash and non-operating expense of $7.6 million associated with the change in fair value of a derivative asset related to a credit facility agreement, a $4.4 million non-cash inventory valuation adjustment for excess hip implant inventory and a $2.3 million non-cash asset impairment charge associated with hip implant instrumentation. This compares to a net loss for the same period in 2012 of $20.3 million, or $(0.48) per basic and diluted share, based on average basic and diluted shares outstanding of 41.9 million.

Outlook

MAKO's 2013 annual guidance of 45 to 48 RIO systems sold and 13,500 to 14,500 MAKOplasty procedures performed remains unchanged.

Conference Call

MAKO will host a conference call today at 4:30 pm ET to discuss its second quarter 2013 results. To listen to the conference call, please dial 877-843-0414 for domestic callers and 914-495-8580 for international callers approximately ten minutes prior to the start time. The participant code is 17131905. To access the live audio broadcast or the subsequent archived recording, visit the Investor Relations section of MAKO's website at www.makosurgical.com.

About MAKO Surgical Corp.

MAKO Surgical Corp. is a medical device company that markets its RIO(R) Robotic-Arm Interactive Orthopedic system, joint specific applications for the knee and hip, and proprietary RESTORIS(R) implants for orthopedic procedures called MAKOplasty(R). The RIO is a surgeon-interactive tactile surgical platform that incorporates a robotic arm and patient-specific visualization technology, which enables precise, consistently reproducible bone resection for the accurate insertion and alignment of MAKO's RESTORIS implants. The MAKOplasty solution incorporates technologies enabled by an intellectual property portfolio including more than 300 U.S. and foreign, owned and licensed, patents and patent applications. Additional information can be found at www.makosurgical.com.

Forward-Looking Statements

This press release contains forward-looking statements regarding, among other things, statements related to expectations, goals, plans, objectives and future events. MAKO intends such forward-looking statements to be covered by the safe harbor provisions for forward-looking statements contained in Section 21E of the Securities Exchange Act of 1934 and the Private Securities Reform Act of 1995. In some cases, forward-looking statements can be identified by the following words: "may," "will," "could," "would," "should," "expect," "intend," "plan," "anticipate," "believe," "estimate," "predict," "project," "potential," "continue," "ongoing," "outlook," "guidance" or the negative of these terms or other comparable terminology, although not all forward-looking statements contain these words. These statements are based on the current estimates and assumptions of our management as of the date of this press release and are subject to risks, uncertainties, changes in circumstances, assumptions and other factors that may cause actual results to differ materially from those indicated by forward-looking statements, many of which are beyond MAKO's ability to control or predict. Such factors, among others, may have a material adverse effect on MAKO's business, financial condition and results of operations and may include the potentially significant impact of a continued economic downturn or delayed economic recovery on the ability of MAKO's customers to secure adequate funding, including access to credit, for the purchase of MAKO's products or cause MAKO's customers to delay a purchasing decision, changes in general economic conditions and credit conditions, changes in the availability of capital and financing sources for our company and our customers, unanticipated changes in the timing and duration of the sales cycle for MAKO's products or the vetting process undertaken by prospective customers, changes in competitive conditions and prices in MAKO's markets, changes in the relationship between supply of and demand for our products, fluctuations in costs and availability of raw materials, finished goods (including from sole-source suppliers), and labor, changes in other significant operating expenses, slowdowns, delays, or inefficiencies in MAKO's product research and development cycles, unanticipated issues relating to intended product launches, decreases in sales of MAKO's principal product lines, decreases in utilization of MAKO's principal product lines or in procedure volume or system utilizations, increases in expenditures related to increased or changing governmental regulation or taxation of MAKO's business, both nationally and internationally, unanticipated issues in complying with domestic or foreign regulatory requirements related to MAKO's current or future products, including initiating and communicating product actions or product recalls and meeting Medical Device Reporting requirements and other requirements of the United States Food and Drug Administration, or securing regulatory clearance or approvals for new products or upgrades or changes to MAKO's current products, developments adversely affecting our actual and potential sales activities outside the United States, increases in cost containment efforts by group purchasing organizations, the impact of the United States healthcare reform legislation enacted in March 2010 on hospital spending, reimbursement, and the taxing of medical device companies, unanticipated changes in reimbursement to our customers for our products, any unanticipated impact arising out of the securities class action or any other litigation, inquiry, or investigation brought against MAKO, any negative impact from the generation or interpretation of clinical study results related to MAKOplasty, loss of key management and other personnel or inability to attract such management and other personnel, increases in costs of retaining a direct sales force and building a distributor network, unanticipated issues related to, or unanticipated changes in or difficulties associated with, the recruitment of agents and distributors of our products, and unanticipated intellectual property expenditures required to develop, market, and defend MAKO's products or market position. These and other risks are described in greater detail under Item 1A, "Risk Factors," in MAKO's periodic filings with the Securities and Exchange Commission, including MAKO's annual report on Form 10-K for the year ended December 31, 2012 filed on February 28, 2013. Given these uncertainties, undue reliance should not be placed on these forward-looking statements. MAKO does not undertake any obligation to release any revisions to these forward-looking statements publicly to reflect events or circumstances after the date of this press release or to reflect the occurrence of unanticipated events.

"MAKOplasty(R)," "RESTORIS(R)," "RIO(R)," as well as the "MAKO" logo, whether standing alone or in connection with the words "MAKO Surgical Corp." are trademarks of MAKO Surgical Corp.

Oxford(R) is a registered trademark of Biomet Orthopedics.

View dataCondensed Statements of Operations (unaudited)

(in thousands, except per share data) Three Months Ended June 30, Six Months Ended June 30,

2013 2012 2013 2012

Revenue:

Procedures $ 16,378 $ 13,018 $ 31,214 $ 24,580

Systems 8,231 8,183 14,730 14,054

Service 3,616 2,474 7,090 4,680

Total revenue 28,225 23,675 53,034 43,314

Cost of revenue:

Procedures 7,949 3,118 11,616 5,775

Systems 3,149 2,796 5,580 5,244

Service 342 451 784 832

Total cost of revenue 11,440 6,365 17,980 11,851

Gross profit 16,785 17,310 35,054 31,463

Operating costs and expenses:

Selling, general and administrative (exclusive of depreciation and amortization) 21,841 18,783 41,979 38,159

Research and development (exclusive of depreciation and amortization) 5,633 5,244 10,646 10,098

Depreciation and amortization 2,103 1,771 4,149 3,457

Total operating costs and expenses 29,577 25,798 56,774 51,714

Loss from operations (12,792) (8,488) (21,720) (20,251)

Other income (expense), net (6,936) (33) (7,613) 25

Loss before income taxes (19,728) (8,521) (29,333) (20,226)

Income tax expense - 14 15 39

Net loss $ (19,728) $ (8,535) $ (29,348) $ (20,265)

Net loss per share - Basic and diluted $ (0.42) $ (0.20) $ (0.63) $ (0.48)

Weighted average common shares outstanding -

Basic and diluted 46,935 42,161 46,870 41,927

Condensed Statements of Operations (unaudited) (in thousands, except per share data) Three Months Ended June 30, Six Months Ended June 30, 2013 2012 2013 2012 Revenue: Procedures $ 16,378 $ 13,018 $ 31,214 $ 24,580 Systems 8,231 8,183 14,730 14,054 Service 3,616 2,474 7,090 4,680 Total revenue 28,225 23,675 53,034 43,314 Cost of revenue: Procedures 7,949 3,118 11,616 5,775 Systems 3,149 2,796 5,580 5,244 Service 342 451 784 832 Total cost of revenue 11,440 6,365 17,980 11,851 Gross profit 16,785 17,310 35,054 31,463 Operating costs and expenses: Selling, general and administrative (exclusive of depreciation and amortization) 21,841 18,783 41,979 38,159 Research and development (exclusive of depreciation and amortization) 5,633 5,244 10,646 10,098 Depreciation and amortization 2,103 1,771 4,149 3,457 Total operating costs and expenses 29,577 25,798 56,774 51,714 Loss from operations (12,792) (8,488) (21,720) (20,251) Other income (expense), net (6,936) (33) (7,613) 25 Loss before income taxes (19,728) (8,521) (29,333) (20,226) Income tax expense - 14 15 39 Net loss $ (19,728) $ (8,535) $ (29,348) $ (20,265) Net loss per share - Basic and diluted $ (0.42) $ (0.20) $ (0.63) $ (0.48) Weighted average common shares outstanding - Basic and diluted 46,935 42,161 46,870 41,927

Depreciation expense for certain property and equipment was reclassified from selling, general and administrative expense to depreciation and amortization expense in the prior period's condensed statement of operations to conform to the current period's presentation. This change in presentation only affects the components of operating costs and expenses and does not affect total operating costs and expenses, revenue, cost of revenue, net loss or cash flows.

View dataCondensed Balance Sheets (unaudited)

(in thousands) June 30, December 31,

2013 2012

ASSETS

Current Assets:

Cash and cash equivalents $ 19,579 $ 61,367

Short-term investments 40,054 11,899

Accounts receivable 21,131 22,389

Inventory 21,580 25,080

Deferred cost of revenue 1,021 967

Financing commitment asset - 7,608

Prepaid and other current assets 2,678 1,972

Total current assets 106,043 131,282

Long-term investments 3,295 -

Cost method investment 4,181 4,181

Property and equipment, net 22,441 22,996

Intangible assets, net 5,771 5,657

Other assets 2,788 2,786

Total assets $ 144,519 $ 166,902

LIABILITIES AND STOCKHOLDERS' EQUITY

Current Liabilities:

Accounts payable $ 1,742 $ 2,267

Accrued compensation and employee benefits 4,861 4,298

Other accrued liabilities 7,088 8,727

Deferred revenue 9,953 9,973

Total current liabilities 23,644 25,265

Deferred revenue, non-current 769 800

Total liabilities 24,413 26,065

Stockholders' Equity:

Common stock 47 47

Additional paid-in capital 371,033 362,364

Accumulated deficit (250,924) (221,576)

Accumulated other comprehensive income (loss) (50) 2

Total stockholders' equity 120,106 140,837

Total liabilities and stockholders' equity $ 144,519 $ 166,902

Condensed Balance Sheets (unaudited) (in thousands) June 30, December 31, 2013 2012 ASSETS Current Assets: Cash and cash equivalents $ 19,579 $ 61,367 Short-term investments 40,054 11,899 Accounts receivable 21,131 22,389 Inventory 21,580 25,080 Deferred cost of revenue 1,021 967 Financing commitment asset - 7,608 Prepaid and other current assets 2,678 1,972 Total current assets 106,043 131,282 Long-term investments 3,295 - Cost method investment 4,181 4,181 Property and equipment, net 22,441 22,996 Intangible assets, net 5,771 5,657 Other assets 2,788 2,786 Total assets $ 144,519 $ 166,902 LIABILITIES AND STOCKHOLDERS' EQUITY Current Liabilities: Accounts payable $ 1,742 $ 2,267 Accrued compensation and employee benefits 4,861 4,298 Other accrued liabilities 7,088 8,727 Deferred revenue 9,953 9,973 Total current liabilities 23,644 25,265 Deferred revenue, non-current 769 800 Total liabilities 24,413 26,065 Stockholders' Equity: Common stock 47 47 Additional paid-in capital 371,033 362,364 Accumulated deficit (250,924) (221,576) Accumulated other comprehensive income (loss) (50) 2 Total stockholders' equity 120,106 140,837 Total liabilities and stockholders' equity $ 144,519 $ 166,902

View dataCondensed Statements of Cash Flows (unaudited)

(in thousands) Six Months Ended June 30,

2013 2012

Operating activities:

Net loss $ (29,348) $ (20,265)

Adjustments to reconcile net loss to net cash used in operating activities:

Depreciation 3,552 2,832

Amortization of intangible assets 884 839

Stock-based compensation 5,879 6,122

Provision for inventory reserve 4,443 95

Amortization of premium on investment securities 112 221

Loss on asset impairment 2,290 511

Provision for doubtful accounts 398 77

Issuance of stock under development agreement 389 454

Non-cash changes under credit facility 7,608 (62)

Changes in operating assets and liabilities:

Accounts receivable 860 1,692

Inventory (2,877) (11,432)

Deferred cost of revenue (54) (458)

Prepaid and other current assets (706) (2,714)

Other assets (2) (37)

Accounts payable (525) 3,776

Accrued compensation and employee benefits 563 (4,747)

Other accrued liabilities (639) (1,365)

Deferred revenue (51) 2,378

Net cash used in operating activities (7,224) (22,083)

Investing activities:

Purchase of investments (42,868) (3,160)

Proceeds from sales and maturities of investments 11,254 22,298

Acquisition of property and equipment (3,353) (3,839)

Acquisition of intangible assets (998) (65)

Net cash provided by (used in) investing activities (35,965) 15,234

Financing activities:

Payment under credit facility (1,000) -

Proceeds from employee stock purchase plan 874 844

Exercise of common stock options and warrants for cash 1,642 2,176

Payment of payroll taxes relating to vesting of restricted stock (115) (172)

Net cash provided by financing activities 1,401 2,848

Net decrease in cash and cash equivalents (41,788) (4,001)

Cash and cash equivalents at beginning of period 61,367 13,438

Cash and cash equivalents at end of period $ 19,579 $ 9,437

Condensed Statements of Cash Flows (unaudited) (in thousands) Six Months Ended June 30, 2013 2012 Operating activities: Net loss $ (29,348) $ (20,265) Adjustments to reconcile net loss to net cash used in operating activities: Depreciation 3,552 2,832 Amortization of intangible assets 884 839 Stock-based compensation 5,879 6,122 Provision for inventory reserve 4,443 95 Amortization of premium on investment securities 112 221 Loss on asset impairment 2,290 511 Provision for doubtful accounts 398 77 Issuance of stock under development agreement 389 454 Non-cash changes under credit facility 7,608 (62) Changes in operating assets and liabilities: Accounts receivable 860 1,692 Inventory (2,877) (11,432) Deferred cost of revenue (54) (458) Prepaid and other current assets (706) (2,714) Other assets (2) (37) Accounts payable (525) 3,776 Accrued compensation and employee benefits 563 (4,747) Other accrued liabilities (639) (1,365) Deferred revenue (51) 2,378 Net cash used in operating activities (7,224) (22,083) Investing activities: Purchase of investments (42,868) (3,160) Proceeds from sales and maturities of investments 11,254 22,298 Acquisition of property and equipment (3,353) (3,839) Acquisition of intangible assets (998) (65) Net cash provided by (used in) investing activities (35,965) 15,234 Financing activities: Payment under credit facility (1,000) - Proceeds from employee stock purchase plan 874 844 Exercise of common stock options and warrants for cash 1,642 2,176 Payment of payroll taxes relating to vesting of restricted stock (115) (172) Net cash provided by financing activities 1,401 2,848 Net decrease in cash and cash equivalents (41,788) (4,001) Cash and cash equivalents at beginning of period 61,367 13,438 Cash and cash equivalents at end of period $ 19,579 $ 9,437

View dataCONTACT: Investors:

MAKO Surgical Corp.

954-628-1706

investorrelations@makosurgical.com

or

Westwicke Partners

Mark Klausner

443-213-0500

makosurgical@westwicke.com

CONTACT: Investors: MAKO Surgical Corp. 954-628-1706 investorrelations@makosurgical.com or Westwicke Partners Mark Klausner 443-213-0500 makosurgical@westwicke.com

http://www.globenewswire.com/newsroom/ti?nf=MTMjMTAwNDI1MDUjOTk2Nw==

Like Cramer knows?

I like this one - got involved last year after the collapse. They don't even need to beat - just hit the numbers and hold the guidance, and the shorts will panic.

Shove it up your ass Cramer! MAKO wont dissapoint this time "skeedaddy" and I'll be happy to buy your shares!

http://www.cnbc.com/id/100900582

MAKO Surgical Corp. Schedules Second Quarter 2013 Earnings Release and Conference Call for Tuesday, July 30, 2013

FT. LAUDERDALE, Jul 15, 2013 (GLOBE NEWSWIRE via COMTEX) -- MAKO Surgical Corp. announced today that it plans to release second quarter 2013 financial results after market close on Tuesday, July 30, 2013. Maurice R. Ferre, M.D., President and Chief Executive Officer, and Fritz L. LaPorte, Senior Vice President and Chief Financial Officer of MAKO, will host a conference call to review the second quarter 2013 results starting at 4:30 pm ET on the same day. The call will be concurrently webcast.

To listen to the conference call please dial 877-843-0414 for domestic callers or 914-495-8580 for international callers and enter the passcode 17131905, approximately ten minutes prior to the start time. To access the live audio broadcast or the subsequent archived recording, visit the Investor Relations section of MAKO's website at www.makosurgical.com . Following the call, a webcast replay will be available on MAKO's website, and an audio replay will also be available by calling 855-859-2056 (404-537-3406 for international callers) and entering the passcode 17131905. Both the audio and webcast replays will be available through August 6, 2013.

About MAKO Surgical Corp.

MAKO Surgical Corp. is a medical device company that markets its RIO(R) Robotic-Arm Interactive Orthopedic system, joint specific applications for the knee and hip, and proprietary RESTORIS(R) implants for orthopedic procedures called MAKOplasty(R). The RIO is a surgeon-interactive tactile surgical platform that incorporates a robotic arm and patient-specific visualization technology, which enables precise, consistently reproducible bone resection for the accurate insertion and alignment of MAKO's RESTORIS implants. The MAKOplasty solution incorporates technologies enabled by an intellectual property portfolio including more than 300 U.S. and foreign, owned and licensed, patents and patent applications. Additional information can be found at www.makosurgical.com .

"MAKOplasty(R)," "RESTORIS(R)," "RIO(R)," as well as the "MAKO" logo, whether standing alone or in connection with the words "MAKO Surgical Corp." are trademarks of MAKO Surgical Corp.

CONTACT: Investors:

MAKO Surgical Corp.

954-628-1706

investorrelations@makosurgical.com

or

Westwicke Partners

Mark Klausner

443-213-0500

makosurgical@westwicke.com

http://www.globenewswire.com/newsroom/ti?nf=MTMjMTAwNDA0MTAjOTk2Nw==

$MAKO - What Is Missed on Intuitive Surgical's Big Miss

http://beta.fool.com/danafblankenhorn/2013/07/11/what-is-missed-on-intuitive-surgicals-big-miss/39940/

ARTICLE: Intuitive Surgical Has Its Apple Moment

http://www.thestreet.com/story/11974014/1/intuitive-surgical-has-its-apple-moment.html?cm_ven=GOOGLEN

MAKO Surgical (MAKO) Adds Scott Flora, 'Jack' Lord to Board

July 8, 2013 4:28 PM EDT

MAKO Surgical Corp. (Nasdaq: MAKO) announced that Scott D. Flora and Jonathan T. "Jack" Lord, M.D. have joined the Company's Board of Directors.

Mr. Flora is currently the President, Chief Executive Office and a director of OmniGuide Inc., a medical device company. He served as the Global Business Unit President for the surgical device division of Covidien plc, a global healthcare products company, from November 2006 until June 2011. From 1994 through 2006, Mr. Flora served in numerous positions at Smith & Nephew plc, a global medical technology company, including President and General Manager of the orthopedics reconstruction division, General Manager of the trauma and clinical therapies divisions, Senior Vice President of United States and Europe, Senior Vice President of Smith & Nephew Healthcare, and Senior Vice President of the orthopedics division. From September 2011 until January 2013, Mr. Flora served on the board of directors of Tengion, a regenerative medicine company focused on discovering, developing, manufacturing and commercializing a range of neo organs. Mr. Flora received a bachelor of science degree in marketing from Millikin University and has participated in professional development programs at Yale University, the Wharton School of the University of Pennsylvania, the Kellogg School of Management, INSEAD, and Pennsylvania State University.

Dr. Lord is currently the Chairman of the Board of Directors of Dexcom, Inc., a medical device company. He recently completed an assignment as Chief Operating Officer of the Miller School of Medicine and UHealth-University of Miami Health System, and is currently a Professor of Clinical Pathology. Dr. Lord served as the Chief Innovation Officer of the University of Miami from September 2011 to March 2012 and as the Chief Executive Officer of Navigenics, a personal genomics company, from May 2009 to December 2009. Prior to that, he was the Chief Innovation Officer and Senior Vice President of Humana, an insurance products and health and wellness services company, from 2000 to 2009. Dr. Lord is a board-certified forensic pathologist who began his medical career in the U.S. Navy and later served as chief operating officer of the American Hospital Association and several biotech companies. Dr. Lord also serves or has served as a member of a number of boards and organizations, including the Centers for Disease Control and Prevention's Advisory Committee to the Director, the National Advisory Council for Healthcare Research and Quality, which advises the U.S. Secretary of Health and Human Services, and the Joint Commission on Accreditation of Health Care Organizations. In addition to currently serving as the Chairman of Dexcom, Inc., Dr. Lord also serves as a Director at Stericycle, Inc. and Vigilant Biosciences, Inc., and serves on advisory board roles for Serco PLC (UK), Anthelio Health and Third Rock Ventures, LLC. He has earned certificates in Governance and Audit from the Harvard Business School. Dr. Lord received an M.D. from the University of Miami School of Medicine and a bachelor of science degree in chemistry from the University of Miami.

http://www.streetinsider.com/Corporate+News/MAKO+Surgical+(MAKO)+Adds+Scott+Flora,+Jack+Lord+to+Board/8482185.html

3 Disruptive Technologies Reshaping Health Care Today

http://www.fool.com/investing/general/2013/06/20/3-disruptive-technologies-reshaping-healthcare-tod.aspx

St. Mary's Students help name Morton Hospital robot R2 Knee 2

Read more: http://www.tauntongazette.com/news/x514119122/St-Marys-Students-help-name-Morton-Hospital-robot-R2-Knee-2#ixzz2VLu4GIOf

Follow us: @TauntonToGo on Twitter | TauntonToGo on Facebook

"including Senior Director of U.S. Knee Marketing, where he was responsible for directing all marketing programs and activities related to Zimmer's knee products"

MAKO Surgical Corp. Announces Addition of Senior Executive to Management Team

Read more: http://www.nasdaq.com/article/mako-surgical-corp-announces-addition-of-senior-executive-to-management-team-20130603-01072#ixzz2VDENbxJV

MAKO's Consumer Oriented Website & TV Ad.

MAKO has been running a TV ad directing potential candidates to a website called Makoplasty.com. The site appears to be focused solely for consumers as opposed to their corporate site which provides a more comprehensive overview of the company. The ad appeared on the cable channel ME-TV (Memorable Entertainment) which seems oriented to an older demographic.

After viewing the site, my personal feeling FWIW is that although it covers everything, it lacks the kind of punch that would sustain the interest of an uninitiated person. I would be interested in the observations of others on this.

Here's Why MAKO Just Popped 13%

By Steve Symington

May 28, 2013

Shares of MAKO Surgical (NASDAQ: MAKO ) rose more than 13% during Tuesday's trading after Wells Fargo analyst Larry Biegelsen upgraded the stock to "outperform" from "market perform." In addition, Biegelsen increased his price target on the stock to a range between $15 and $17 from his earlier target of $11 to $12 per share.

As it stands, and even after today's pop, this new range represents an upside of between 18% and 34% from MAKO's current price around $12.70 per share.

It's all in the hips

Remember, last October I noted that MAKO management had promised investors that their "hip 2.0 application upgrade" would be rolled out in either the third or fourth quarter of 2013. So, why did this matter?

At the time, surgeons had voiced concerns to MAKO over certain aspects of the RIO system's relatively young Total Hip Arthroplasty solution, which the company had only launched in September 2011. As Biegelsen noted with his upgrade, MAKO expects to address most of those concerns when the new hip software application is implemented in July. As a result, he states that the RIO robots "should be used for significantly more hip surgeries" going forward.

In fact, that's one of the very reasons I wrote just last week why MAKO could eventually quadruple as the company steadily increases the number of procedures performed using its robots.

Of course, it's also important to note while only 467 of the 2,988 procedures performed (or 15.6%) last quarter were hips, that still represented an 18.2% sequential increase over the previous quarter. In short, this shows that surgeons are already picking up the pace with MAKO-assisted hip replacements, despite the fact the hip 2.0 application hasn't even arrived yet.

Foolish final thoughts

However, considering that a full 65% of MAKO's 156 robots are currently equipped with the $150,000 hip add-on, there's still plenty of room for the company to boost hip procedures from current levels. This, in turn, will serve to improve MAKO's monthly per-site utilization numbers, which will only bring the company that much closer to its holy grail of sustained profitability.

When that happens, I'm convinced that long-term oriented MAKO shareholders will be rewarded handsomely for their patience.

http://www.fool.com/investing/general/2013/05/28/heres-why-mako-just-popped.aspx

Wells Fargo Upgrades MAKO Surgical (MAKO) to Outperform

May 28, 2013 7:18 AM EDT

Wells Fargo upgraded MAKO Surgical (NASDAQ: MAKO) from Market Perform to Outperform with a price target of $15-$17 (from $11-$12). Analyst Larry Biegelsen thinks new software will improved hip procedure volume.

"Based on our discussions with several prominent orthopedic surgeons, we believe that MAKO’s new hip software for its RIO robot addresses most surgeon concerns that have limited the adoption of the hip application since the hip launch in September 2011. We expect hip procedure growth and utilization to accelerate following the release of the software around July 2013. Total hip replacement procedures represent a significantly larger (4x) opportunity for MAKO than unicompartmental (uni) knee procedures which currently account for about 85% of total MAKOplasty procedures," said Biegelsen.

For an analyst ratings summary and ratings history on MAKO Surgical (NASDAQ: MAKO) click here. For more ratings news on MAKO Surgical click here.

Shares of MAKO Surgical closed at $11.22 yesterday, with a 52 week range of $10.00-$27.18.

http://www.streetinsider.com/Analyst+Comments/Wells+Fargo+Upgrades+MAKO+Surgical+(MAKO)+to+Outperform/8370825.html

What a move today! Got out @ $11.77 but will reload here in a minute!

A new shoulder application would be monumental.

One Way MAKO Surgical Could Quadruple

By Steve Symington

May 22, 2013

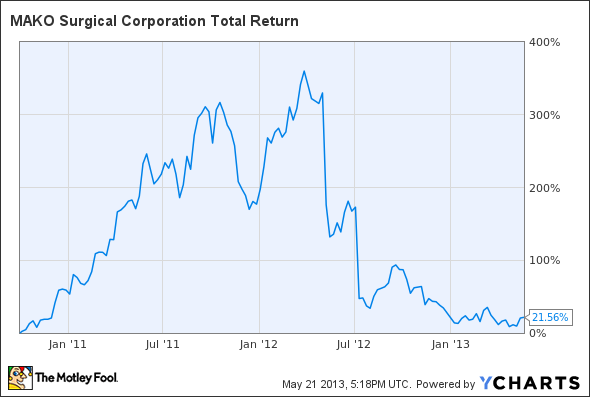

It seems an understatement to say MAKO Surgical (NASDAQ: MAKO ) has fallen hard from its March 2012 high of nearly $44 per share. To be sure, from MAKO's current price of around $11.50 per share, the stock would need to nearly quadruple for investors who bought at the peak to recoup their losses:

MAKO Total Return Price data by YCharts.

Been there, done that

The thing is, when you zoom out a bit, you can see that anyone who bought shares of MAKO a mere 18 months earlier is actually sitting on a more than 21% gain -- albeit only after enduring one heck of a ride in the meantime:

MAKO Total Return Price data by YCharts.

So what would it take for MAKO to regain its former glory?

Well, for one, remember much of that meteoric rise was the direct result of over-enthusiastic RIO system sales projections, and we all remember what happened when the company failed to live up to those expectations.

In fact, some shareholders were so furious about the ensuing drop that they filed a class action lawsuit, in which they alleged they were misled by management. Of course, I just noted yesterday one such case was dismissed thanks to MAKO's "forward-looking statements" clauses, but the damage to management's rapport with investors remains evident even after the company posted two consecutive decent quarters.

Then again, the reason investors were so excited about higher system sales in the first place wasn't the significant upfront revenue benefit, but rather the resulting long-term increase in the number of procedures. You see, each time a surgery is performed using MAKO's RIO platform, the company benefits to the tune of roughly $5,000 in recurring revenue from the sale of instruments and implants.

So what's the problem?

However, surgeons can currently only perform two different types of procedures using MAKO's system -- partial knee replacements and total hip arthroplasty.

Even then, considering that MAKO only just introduced the hip solution in September 2011, only 65% of the 156 systems currently in place are equipped to enable THA. As a result, only 467 of the 2,988 procedures performed last quarter were hip replacements. On a positive note, that did represent an 18.2% sequential increase over the previous quarter, which shows that hospitals are finally beginning to utilize MAKO's hip replacement tech on a greater scale.

Still, customers who owned MAKO's RIO robots in 2012 only performed an average of just 6.7 monthly procedures per system last year, and monthly utilization per site fell to 6.6 procedures last quarter. By contrast, consider MAKO's soft-tissue counterpart in Intuitive Surgical (NASDAQ: ISRG ) , whose customers performed around 13 procedures per month last year with each of Intuitive's da Vinci robots.

A better way

Of course, while the folks at MAKO can obviously increase the number of total procedures performed by selling new systems, that's easier said than done given the RIO's seven-figure price point. Until that growth avenue picks up more steam, then, you can bet MAKO will focus on increasing utilization.

How, then, does Intuitive Surgical manage to maintain such high monthly utilization numbers? Thanks in part to the complementary instrumental requirements of many soft-tissue surgeries, surgeons are able to perform literally dozens of different procedures using Intuitive's da Vinci platform.

That's exactly why one of the four big questions I posed going into MAKO's fourth-quarter report earlier this year revolved around whether the company had news on the development of new surgery types for the RIO. As I noted at the time, CEO Maurice Ferre did tell investors last November the company was working on a total knee replacement solution, but he also warned at the same time we shouldn't expect to see it in the near future.

Then again, when the company (mostly) answered my questions in February, management elaborated one of their "key operative priorities in 2013" was to continue collecting and analyzing user feedback and use it to "further enhance [their] product offering."

In fact, one of the yet-to-be-officially mentioned technologies that I'm waiting to hear about from MAKO is a shoulder replacement procedure. As I first noted last October, San Francisco Surgery Center Administrator Jeff Wong even stated the following in a Q&A session last August: "While we have focused exclusively on partial knee replacements up till now, we anticipate leveraging the robot for hip replacements and possibly shoulder repairs in the near future."

Call me crazy, but that doesn't seem like something one would say without at least having a conversation about it first with the minds at MAKO Surgical.

Foolish final thoughts

In the end, when MAKO eventually announces one or more new procedure types while continuing to increase the number of hip procedures performed, I see no reason why the resulting enthusiasm couldn't push the stock back near all-time highs. However, remember that this a long-term speculative bet that won't happen overnight, so, as always, patience is key to realizing big profits with this young stock.

http://www.fool.com/investing/general/2013/05/22/one-way-mako-surgical-could-quadruple.aspx

MAKO Surgical Notches Another Legal Victory

By Steve Symington

May 20, 2013

MAKO Surgical's (NASDAQ: MAKO) legal wins just keep stacking up.

Just last month, the company not only settled a trade secrets lawsuit on its own terms with competitor Blue Belt Technologies, but also resolved a patent infringement complaint it brought against U.K.-based Stanmore Implants for uncanny similarities between its own RIO System and Stanmore's Sculptor RGA.

Curiously enough, the resolution of the latter complaint ended with MAKO acquiring Stanmore's robotics technology for less than $1 million. Meanwhile, Stanmore agreed to withdraw itself from the surgical robotics market completely.

Then again, these cases were offensive moves by MAKO designed to make sure their competition would play fair. Even so, I'm sure most shareholders would agree that it would be a lot less stressful if the company hadn't needed to get involved in these legal matters in the first place.

As I noted earlier this month, however, management was also facing a courtroom challenge from other shareholders who alleged they were misled by last year's over-inflated RIO System sales projections. Of course, anyone who kept track of MAKO in 2012 remembers what happened after they missed their own lofty expectations:

MAKO Total Return Price data by YCharts

"Forward-looking statements"

Last week, however, according to a report from the South Florida Business Journal, the courts reminded shareholders the importance of owning their investing decisions.

More specifically, a Southern Florida District Court judge dismissed one of the aforementioned class action lawsuits after pointing out MAKO's "2012 sales projections were accompanied by meaningful language that cautioned investors that these 'forward-looking statements' may not be on target."

Going further, the judge elaborated by writing:

The warnings in the defendants' press releases and the referenced SEC filings warned investors of precisely what happened here: that projected system sales and procedures might be lower than projected due to the economic downturn, variable sales and a reluctance on the part of orthopedic surgeons to adopt the new technology.

What's more, the judge also ruled that comments made by management during investor conference calls were also protected as "forward-looking statements," and there exists no evidence at the time they were aware they wouldn't be able to meet their goals.

Foolish final thoughts

Of course, management's seeming ignorance was one of the very reasons fellow Fool Brian Stoffel told us last December that MAKO wouldn't remain in his 2013 portfolio, but I personally remain encouraged that the company seems to have finally adjusted investors' expectations with reality -- especially on the heels of two consecutive decent quarters.

However, regardless of how effective any given company is at selling you on its prospects, remember these businesses are run by imperfect people who may not always be able to deliver on their promises. In the end, then, don't take those monotonous Safe Harbor Statements as a time to zone out until the real conversation begins. Instead use them as a reminder that your investing decisions -- both good and bad -- are your own responsibility.

http://www.fool.com/investing/general/2013/05/20/mako-surgical-notches-another-legal-victory.aspx

Securities class action against Mako Surgical dismissed

May 17, 2013, 1:09pm EDT Updated: May 17, 2013, 1:55pm EDT

A federal judge dismissed a securities class action lawsuit against Mako Surgical Corp.

Mako Surgical President and CEO Maurice Ferre.

The complaint was filed in the Southern District of Florida in May 2012 on behalf of shareholders who claimed that officials of the Davie-based surgical robotics company (NASDAQ: MAKO) misled them concerning sales projections. The lawsuit named Mako Surgical Chairman and CEO Dr. Maurice Ferre and CFO Fritz LaPorte.

Mako Surgical’s 2012 sales guidance, released in January of that year, called for sales of 56 to 62 surgical robots. When it released its first quarter results in May 2012, the company said it sold only four and reduced its annual sales projections. Its stock dropped by 43 percent soon after.

U.S. District Judge James I. Cohn dismissed the complaint on May 15.

The judge ruled that Mako Surgical’s 2012 sales projections were accompanied by meaningful language that cautioned investors that these “forward-looking statements” may not be on target. This cautionary language wasn’t “boilerplate,” as the plaintiffs argued, because it detailed the kind of misfortunes that could cause the company to miss its projections, the judge ruled.

“The warnings in the defendants’ press releases and the referenced SEC filings warned investors of precisely what happened here: that projected system sales and procedures might be lower than projected due to the economic downturn, variable sales and a reluctance on the part of orthopedic surgeons to adopt the new technology,” the judge wrote.

Cohn also ruled that comments by Ferre and LaPorte during investor conference calls were protected as “forward-looking statements.” There were no allegations in the complaint that establish that Ferre and LaPorte had actual knowledge that the 2012 sales projections were false, the judge added.

However, the judge left the plaintiffs the option to file an amended complaint by June 5.

Officials with New York law firm Labaton Sucharow, the attorneys representing the plaintiffs, declined comment.

"Mako is pleased with Judge Cohn’s order dismissing in its entirety the putative class action against Mako," said Mako Surgical Menashe Frank said. "We are encouraged that this will further enable Mako to focus on the hospitals, doctors and patients we serve.”

Mako Surgical was represented in the case by Holland & Knight in Miami, with attorneys Louise McAlpin, Stephen P. Warren, Tracy Ann Nichols, and Allison B. Kernisky.

A shareholder derivative lawsuit, with a group of shareholders suing in place of the company, remains pending against Ferre, LaPorte and other Mako Surgical officials. The defendants filed a motion to dismiss the complaint, which also involves the 2012 sales projections.

The derivative lawsuit is also before Judge Cohn.

According to Mako Surgical’s SEC filings, the company’s board formed a special committee of two independent directors in October to review and investigate the claims raised in the derivative lawsuit. This process hasn’t been completed.

http://www.bizjournals.com/southflorida/news/2013/05/17/securities-class-action-against-mako.html?page=all

My man, hit the nail on the head!

As long as MAKO keeps delivering top notch results from their surgeries we're golden.

The only thing with that is the targeted market each is going after. Since MAKO is strictly orthopedic and ISRG is in a different niche, Im not sure how the market would react to MAKO with more bad news from ISRG. Perhaps in vague terms like robotics as a whole they may get some push from ISRG taking more heat but I dont think it is going to affect bottom line much.

That... and more bad news from ISRG camp wouldn't hurt our cause here...IMO

Im not sure there is enough "meat on the bone" yet to sustain the run we had last week to convince the markets that MAKO will continue its trek north in the very short term which if im correct is sure to entice shorts. If MAKO closes the week above the 50 dma, it may protect from heavy shorting. We need the trial results that are rumored to be extremely favorable to help MAKO find its true market value before the next Q. Any thoughts?

Me too and I took advangtage to add some more, just wanted your assessment. Carry on....

MAKO needed a correction after last weeks run, the next 2 days will tell the true tale as to this pullback. This changes nothing for me as I am generally long on my investments.

Healthy pullback or short attack? What's YO?

MAKO Surgical Given New $12.00 Price Target at Oppenheimer (MAKO)

http://www.dailypolitical.com/finance/stock-market/mako-surgical-given-new-12-00-price-target-at-oppenheimer-mako.htm

The beauty of the strong week MAKO had is that there are no gaps that need to be filled hanging overhead! MAKO BULLISH!!!!

$MAKO - SQWEEEEEEEEEEEEEEEEEZE!!!!!

MACD has crossed into positive territory, Full STO shows bullish, RSI nearing power zone. Can MAKO test 200 DMA at $13.38 next week?!

Will MAKO Surgical Reach Profitability Before 2015?

http://seekingalpha.com/article/1420801-will-mako-surgical-reach-profitability-before-2015?source=email_rt_article_title

37,973 buy at 11.23 to close, nice money moving in rather than out!

HUGE 25,000 share trade just went through @ $11.25 weeeeeeeeeeeee!!!

Small-Cap Stocks Taking Wild Swings on News: E Commerce China, Aurizon Mines, Alpha Natural Resources, Arch Coal, MAKO Surgical, Giant Interactive Group

http://www.therem.org/small-cap-stocks-taking-wild-swings-on-news-e-commerce-china-aurizon-mines-alpha-natural-resources-arch-coal-mako-surgical-giant-interactive-group/123875/

$MAKO - lessgo muthafuckas!!!!!!!!

MAKO Surgical: Burden Of Proof Still On Management

May 9 2013, 10:27

By Jake King

MAKO Surgical's (MAKO) first-quarter results did little to inspire our confidence in this battered and bruised story, but for those who truly believe in the growth prospects, MAKO looks cheap relative to expectations. The main question that needs to be answered in order to justify ownership is: Are expectations (and guidance) achievable? MAKO, which released its quarterly earnings report after the close on Tuesday, sold five RIO Systems in Q1 2013 and announced that 2,988 MAKOplasty procedures were performed, generating revenue of $24.8 million and a net loss of $0.21 per share. Revenue proved a slight beat compared to consensus estimates, while earnings were just shy of the $0.19 per share loss expected by analysts.

Since its fall from grace last year, MAKO has been, and remains, a "show me" story. We believe that management still needs to demonstrate at least two consecutive quarters of compelling results (solid meet or beat) to assuage investors' fears that expectations for long-term performance will have to be, yet again, reset. With 27% of Mako's float sold short, there's a significant community of investors who believe numbers are still too high. The results posted for Q1 aren't likely to shake their belief, or bring new long investors to the story. The burden of proof remains on management, and thus far, 2013 is off to a lackluster start. With little news flow until the next quarterly earnings report, we believe there will be continued pressure on MAKO and that potential investors will remain on the sidelines until performance improves. Furthermore, current shareholders are likely to step out in expectation of a re-entrance at lower prices, hence downside risk exists from here.

The Focus Is on Company Guidance, MAKO's Ability to Measure Up

Given MAKO's history of overstating guidance and then revising significantly, investors are focused almost exclusively on MAKO's ability to meet guidance for this year, which management reiterated alongside its quarterly results (45-48 RIO systems and 13,500-14,500 MAKOplasty procedures). The question, then, is whether the bar has been set appropriately, and whether quarterly results offer evidence that the company is on track to satisfy. With that in mind, Mako's reported RIO system sales in the first quarter appear disappointing. Even considering that sales are generally back-end loaded throughout the year, the company didn't come close to a run rate that suggests reaching guidance.

Mako reiterated 2013 guidance for 45-48 RIO system sales, but with only five new RIO placements in Q1, the company needs to average 14 RIO Systems quarterly for the next three quarters. It's certainly within striking distance (MAKO sold 15 RIO Systems quarterly in the second half of 2012), but no shoe-in. The short's argument against this precedent is that the low-hanging fruit (surgery centers that were more likely to purchase Mako's systems) has already been picked. The company's 2,988 MAKOplasty procedures performed in Q1 were a bit short of the 3,500 needed quarterly to meet guidance. Part of this, said management, was attributable to two fewer surgical days in the quarter. Again, MAKO expects MAKOplasty procedures to be a back-end loaded phenomenon (40/60 split, first half vs. second half) throughout the calendar year, although it's important to note that 2012 was an anomaly to this expectation. If 2013 plays out similarly, the current run-rate won't suffice.

Aside from meeting immediate guidance, we have three key concerns moving forward:

Practitioners that we spoke with still question the true medical need for a system like the RIO. Specialized surgeons indicated to us that they simply don't need a robot in order to perform these procedures, and that the costs don't make sense for their practices.

Along those lines, the high-volume centers that will be most lucrative to MAKO (higher procedure volume) and can afford a high-priced robotic system are the most experienced -- hence, they're the least likely to pick up a RIO System. Ironically, the lower-volume, less-experienced surgeons are the ones that most need a RIO system, and affordability for many of these centers may be out of reach.

Finally, the RIO System is not interchangeable with other implants, which locks customers in and may be creating some buyer resistance. With other systems coming to the market that allow for interchangeability, Mako is likely to face additional headwinds. Management may be able to figure this out and push through, with a strong sales and marketing campaign. But investors are likely to demand the evidence first, given the past disappointments on expectations. The competitive threat is a component of the short thesis and a key reason for MAKO's high short interest.

While we believe that Mako is within reach of its guidance for 2013, the first quarter didn't instill the confidence needed for investors to jump in en masse. We believe the Q1 results reset the "show me" story for another couple of quarters; if the company demonstrates a second quarter similar to its first, particularly in terms of RIO sales, there's more trouble on the horizon. Investors are enticed by the fact that MAKO traded at $44 in March of last year, and while the stock appears cheap relative to expectations for financial growth, the possibility that lowered expectations are still too high may keep investors away from the stock. A dip into the single digits -- which is not out of the question -- would, in our opinion, make MAKO a far more attractive comeback story. Those long the name may be wise exiting here and trying to find a better entry point in the future.GOOD LUCK WITH THAT ONE SHORTY!!!

Additional disclosure: PropThink is a team of editors, analysts, and writers. This article was written by Jake King. We did not receive compensation for this article, and we have no business relationship with any company whose stock is mentioned in this article. Use of PropThink’s research is at your own risk. You should do your own research and due diligence before making any investment decision with respect to securities covered herein. You should assume that as of the publication date of any report or letter, PropThink, LLC and persons or entities with whom it has relationships (collectively referred to as "PropThink") has a position in all stocks (and/or options of the stock) covered herein that is consistent with the position set forth in our research report. Following publication of any report or letter, PropThink intends to continue transacting in the securities covered herein, and we may be long, short, or neutral at any time hereafter regardless of our initial recommendation. To the best of our knowledge and belief, all information contained herein is accurate and reliable, and has been obtained from public sources we believe to be accurate and reliable, and not from company insiders or persons who have a relationship with company insiders. Our full disclaimer is available at www.propthink.com/disclaimer.

Time for MAKO to rock and roll! $1.00 per month and before you know it by end of summer we'll be up 50%

great point lol many bat against the rev report

MAKO Surgical Posts a Solid Quarter: Here's What Investors Need to Know

May 8, 2013 By Steve Symington

It's OK, MAKO Surgical (NASDAQ: MAKO ) shareholders; you can exhale now.

Shares of the robotic surgery specialist traded up more than 4% after the company reported earnings yesterday. For those of you who are disappointed that the stock didn't absolutely skyrocket, remember that this muted response is a heck of a lot better than the violent 37% plunge investors endured after MAKO's dismal first quarter earnings last year.

The numbers

On Monday, I noted that MAKO management desperately needed to at least meet tempered expectations to show investors they have a firm grasp on where the business is headed.

So, how did they fare?

On one hand, the company posted revenue of $24.8 million, slightly exceeding analysts' estimates, which called for sales of $24.4 million.

On the other hand, MAKO's net loss improved 18% year-over-year and came in at $9.6 million, or $0.21 per share. Unfortunately, that missed analysts' expectations of a net loss of $0.19 per share.

However, it's important to note that included in that number was "a non-cash and non-operating expense of $661,000 associated with the change in fair value of a derivative asset" related to the company's previously announced credit facility agreement with Deerfield Management. When we back out that expense, MAKO's non-GAAP loss was exactly what analysts had hoped for at $0.19 per share.

As an aside, management also told investors that they're confortable with MAKO's current cash balance, so have no intention of drawing on the costly Deerfield credit facility by the time it expires on May 15. As a result, they anticipate cash burn will increase as the inaction will invoke a $1 million "no draw fee" to Deerfield in the second quarter.

In addition, management also confirmed during the conference call that they agreed to pay approximately $1 million to Stanmore Implants to acquire the company's robotic assets as a result of last month's patent complaint resolution.

System sales

All told, five RIO systems were sold during the quarter -- this time all to domestic customers -- bringing MAKO's commercial installed base of RIO systems to 161 and with all but five here in the U.S. In addition, revenue from two previously deferred international sales was recognized this quarter after all revenue recognition criteria were satisfied.

Even better, all five of the new systems sold included MAKO's $150,000 total hip arthroplasty upgrade, while one existing customer upgraded its already-placed RIO platform with the THA add-on. As of March 31, 102 of the 156 RIO systems in place currently have the MAKOplasty THA application installed.

Procedures

A total of 2,988 MAKOplasty procedures were performed last quarter, representing a 3% sequential increase and a 30% rise from the same year-ago period.

Of those 2,988 procedures, 467 were THA surgeries. While that may seem like only a small improvement over last quarter's 395 THA surgeries, remember that it represents an 18.2% sequential increase. Considering that MAKO's hip business is still in its infancy, 467 hip procedures is more than satisfactory.

Also, remember that the company told us last quarter it would be reporting monthly utilization numbers on a per-site rather than a per-system basis to better reflect the now-material contributions from non-commercial international systems. This quarter, monthly utilization per site fell to 6.6 procedures, compared with 7.1 procedures per site in the same year-ago period. Despite the drop, however, that number still remains well within the bounds of normality.

Guidance and cash burn

Keeping in mind that the first quarter of each year tends to be MAKO's slowest, the company felt comfortable maintaining its guidance of 45 to 48 RIO systems sold and 13,500 to 14,500 MAKOplasty procedures performed in 2013.

Finally, MAKO had cash and equivalents remaining of $71 million at the end of March, compared to $73.3 million as of Dec. 31, 2012. Management also reiterated they continue to expect to throw between $22 and $27 million in the oven when all is said and done at the end of this year, so should end 2013 with around $46 million in cash on the books.

Clinical research and marketing

MAKO also highlighted the previously announced favorable results of a randomized controlled trial involving 100 patients who underwent unicompartmental knee arthroplasty procedures. More specifically, 50 of the patients had opted for MAKO's robotic solution, and 50 had received manually placed Biomet Oxford implants.

According to yesterday's press release, the trial notes "MAKOplasty resulted in significantly lower post-operative pain from day one to eight weeks post-op and it took eight weeks for Oxford patients to reach the lower pain levels that MAKOplasty patients were already reporting after six days." What's more, MAKOplasty also proved more accurate "in all dimensions measured, with statistically significant differences in four of the six dimensions."

Of course, Biomet is a privately held company, but it's safe to say that trials like this should have other publicly traded companies like Stryker (NYSE: SYK ) , Zimmer (NYSE: ZMH ) , and Johnson & Johnson (NYSE: JNJ ) sweating bullets given their competing manually placed implants. It also doesn't help their case that Johnson & Johnson in March lost its first of 10,750 lawsuits over defective metal-on-metal hip implants, but you can bet MAKO can't wait to capitalize on the fallout with its own innovative offerings.

Foolish final thoughts

In the end, MAKO shareholders are breathing a long-awaited sigh of relief after the company performed exactly as it said it would. Even so, with the stock trading more than 60% below its 52-week-high, you can bet we'll be watching closely to see whether MAKO can keep up the good work. If it can, the stock could very easily prove to be the multibagger that investors have been waiting for.

http://www.fool.com/investing/general/2013/05/08/mako-surgical-posts-a-solid-quarter-heres-what-inv.aspx

$MAKO - Nice GREEEEN finish for today!

Mako Surgical narrows Q1 loss, sales up 26%

May 7, 2013, 5:06pm EDT

Mako Surgical Corp. narrowed its losses in the first quarter as its sales grew 26 percent, but the initial stock market reaction to the news was negative.

Shares of the Davie-based manufacturer (NASDAQ: MAKO) of knee and hip replacement surgical robot were down 16 cents, or 1.5 percent, to $10.25 in post-market trading. The news was announced shortly after the market closed.

The company lost $9.6 million, or 21 cents per share, on revenue of $24.8 million in the first quarter. Analysts expected a loss of 19 cents per share. That compares with a loss of $11.7 million, or 28 cents per share, on revenue of $19.6 million in the same quarter a year ago.

Mako Surgical sold five of its Robotic Arm Interactive Orthopedic (RIO) systems in the first quarter, which was well behind the pace of the 45 to 48 sales the company projected for the entire year. It also recognized revenue from two previously contracted international RIO sales during the first quarter.

"The first quarter is typically a slower quarter for MAKO, and our first quarter results were in line with our expectations," Mako Surgical President and CEO Dr. Maurice R. Ferre stated in a news release. "The initial results of our programs designed to drive utilization and system sales are encouraging, and I remain confident in our outlook for 2013."

The increase in revenue came because more procedures were done with its equipment and the company sells parts associated with them. Procedures were up 30 percent year-over-year, but only 3 percent compared to the fourth quarter.

Mako Surgical fended off competition in April when it settled a patent infringement lawsuit against Stanmore Impacts Worldwide by agreeing to buy Stanmore’s surgical robot system for just under $1 million.

The 52-week high for Mako Surgical was $29.04 on May 8, 2012. The 52-week low was $10 on April 8.

http://www.bizjournals.com/southflorida/news/2013/05/07/mako-surgical-narrows-q1-loss-sales.html?s=image_gallery

Solid earnings report if you ask me...bottoms up!

Conf call transcript and Q&A.

link to transcript

|

Followers

|

10

|

Posters

|

|

|

Posts (Today)

|

0

|

Posts (Total)

|

203

|

|

Created

|

01/03/12

|

Type

|

Free

|

| Moderators | |||

| Volume | |

| Day Range: | |

| Bid Price | |

| Ask Price | |

| Last Trade Time: |

/sylvester%20stallone/sylvester-stallone-22-v.jpg)