News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

MAKO Surgical Corp. Reports Operating Results for the First Quarter 2013

4:05 PM ET 5/7/13 | GlobeNewswire

First Quarter 2013 Highlights

First quarter revenue totaled $24.8 million, a 26% increase over the same period in 2012

Five RIO(R) systems sold in the first quarter, increasing worldwide commercial installed base to 161 RIO systems and domestic commercial installed base to 156 RIO systems

2,988 MAKOplasty(R) procedures performed in the first quarter, a 30% increase over the same period in 2012

Six MAKOplasty Total Hip Arthroplasty (THA) applications sold in the first quarter, of which one was sold to an existing customer

As of March 31, 2013, 63% of worldwide commercial installed base is MAKOplasty THA enabled

MAKO Surgical Corp. (Nasdaq:MAKO), a medical device company that markets its RIO(R) Robotic Arm Interactive Orthopedic surgical platform, MAKOplasty(R) joint specific applications and proprietary RESTORIS(R) implants that together enable orthopedic surgeons to consistently, reproducibly and precisely treat patient specific osteoarthritic disease, today announced its operating results for the quarter ended March 31, 2013.

Recent Business Developments

RIO Systems - Five RIO systems were sold during the first quarter to domestic customers. These five RIO systems bring MAKO's worldwide commercial installed base of RIO systems to 161 systems and domestic commercial installed base to 156 systems as of March 31, 2013. At the end of the quarter, MAKO had 154 MAKOplasty sites worldwide. In addition, the revenue associated with two previously deferred international commercial system sales was recognized in the first quarter as all revenue recognition criteria were satisfied. Six MAKOplasty THA applications were sold, five of which were sold with the domestic RIO systems sales during the quarter and one of which was sold as an upgrade to an existing customer with a knee-only commercial system. As of March 31, 2013, 102 RIO systems, or 63% of the worldwide commercial installed base, have the MAKOplasty THA application.

MAKOplasty Procedure Volume - During the first quarter, 2,988 MAKOplasty procedures were performed, of which 2,861 were performed at domestic sites. Of the 2,988 procedures, 467 were THA procedures. The 2,988 MAKOplasty procedures performed represent a 3% increase over the procedures performed in the fourth quarter of 2012 and a 30% increase over the procedures performed in the first quarter of 2012. The average monthly utilization per site was 6.6 procedures during the first quarter of 2013. Through March 31, 2013, approximately 26,000 procedures had been performed since the first procedure in June 2006.

Clinical Research and Marketing - At the 2013 American Academy of Orthopedic Surgeons in March 2013, Dr. Mark Blyth presented the initial results of the first 100 patients from the prospective, single center, randomized controlled trial (RCT) performed at the Glasgow Royal Infirmary with the University of Strathclyde. The RCT compares the MAKOplasty unicompartmental knee arthroplasty performed with MAKO's RESTORIS MCK implants to manually placed Biomet Oxford(R) implants. MAKOplasty resulted in significantly lower post-operative pain from day one to eight weeks post-op and it took eight weeks for Oxford patients to reach the lower pain levels that MAKOplasty patients were already reporting after six days. MAKOplasty also demonstrated higher accuracy in all dimensions measured, with statistically significant differences in four of the six dimensions. Finally, a significantly higher percentage of MAKOplasty patients had "Excellent" American Knee Society Scores at three months.

Patent Infringement Actions - On April 16, 2013, MAKO agreed to settle all patent infringement actions against Stanmore Implants Worldwide Limited and affiliated entities. Under a confidential settlement agreement and an asset purchase agreement between the parties, in exchange for a cash payment to Stanmore, MAKO withdrew all legal actions against Stanmore and received Stanmore's robotic business assets and related intellectual property, as well as Stanmore's agreement to withdraw from robotics.

"The first quarter is typically a slower quarter for MAKO, and our first quarter results were in line with our expectations," said Maurice R. Ferre, M.D., President and Chief Executive Officer of MAKO. "The initial results of our programs designed to drive utilization and system sales are encouraging, and I remain confident in our outlook for 2013."

2013 First Quarter Financial Review

Revenue was $24.8 million in the first quarter of 2013 compared to $19.6 million in the first quarter of 2012, representing a 26% increase. The increase in revenue was primarily attributable to the recognition of revenue of 2,988 MAKOplasty procedures performed, which represents a 30% increase over the procedures performed in the first quarter of 2012, and an increase in system revenue and service revenue.

Gross profit for the first quarter of 2013 was $18.3 million compared to a gross profit of $14.2 million in the same period in 2012. Gross margin for the first quarter of 2013 was 74%, consisting of a 75% margin on procedure revenue, a 63% margin on RIO system revenue and an 87% margin on service revenue.

Operating expenses were $27.2 million in the first quarter of 2013 compared to $25.9 million in the first quarter of 2012. The increase in operating expenses was primarily due to an increase in sales, marketing and operations costs associated with the commercialization of the RIO system, MAKOplasty applications and RESTORIS implant systems; and an increase in general and administrative costs as MAKO continued to build infrastructure to support growth.

Net loss for the three months ended March 31, 2013 was $9.6 million, or $(0.21) per basic and diluted share, based on average basic and diluted shares outstanding of 46.8 million. Included in net loss for the first quarter of 2013 was a non-cash and non-operating expense of $661,000 associated with the change in fair value of a derivative asset related to a credit facility agreement. This compares to a net loss for the same period in 2012 of $11.7 million, or $(0.28) per basic and diluted share, based on average basic and diluted shares outstanding of 41.7 million.

Cash, cash equivalents and available-for-sale investments were $71.0 million as of March 31, 2013 compared to $73.3 million as of December 31, 2012. As of March 31, 2013, no amounts have been drawn under the credit facility agreement with affiliates of Deerfield Management Company, L.P.

Outlook

MAKO's 2013 annual guidance of 45 to 48 RIO systems sold and 13,500 to 14,500 MAKOplasty procedures performed remains unchanged.

Conference Call

MAKO will host a conference call today at 4:30 pm ET to discuss its first quarter 2013 results. To listen to the conference call, please dial 877-843-0414 for domestic callers and 914-495-8580 for international callers approximately ten minutes prior to the start time. The participant code is 58873803. To access the live audio broadcast or the subsequent archived recording, visit the Investor Relations section of MAKO's website at www.makosurgical.com.

About MAKO Surgical Corp.

MAKO Surgical Corp. is a medical device company that markets its RIO(R) Robotic-Arm Interactive Orthopedic system, joint specific applications for the knee and hip, and proprietary RESTORIS(R) implants for orthopedic procedures called MAKOplasty(R). The RIO is a surgeon-interactive tactile surgical platform that incorporates a robotic arm and patient-specific visualization technology, which enables precise, consistently reproducible bone resection for the accurate insertion and alignment of MAKO's RESTORIS implants. The MAKOplasty solution incorporates technologies enabled by an intellectual property portfolio including more than 300 U.S. and foreign, owned and licensed, patents and patent applications. Additional information can be found at www.makosurgical.com.

Forward-Looking Statements

This press release contains forward-looking statements regarding, among other things, statements related to expectations, goals, plans, objectives and future events. MAKO intends such forward-looking statements to be covered by the safe harbor provisions for forward-looking statements contained in Section 21E of the Securities Exchange Act of 1934 and the Private Securities Reform Act of 1995. In some cases, forward-looking statements can be identified by the following words: "may," "will," "could," "would," "should," "expect," "intend," "plan," "anticipate," "believe," "estimate," "predict," "project," "potential," "continue," "ongoing," or the negative of these terms or other comparable terminology, although not all forward-looking statements contain these words. These statements are based on the current estimates and assumptions of our management as of the date of this press release and are subject to risks, uncertainties, changes in circumstances, assumptions and other factors that may cause actual results to differ materially from those indicated by forward-looking statements, many of which are beyond MAKO's ability to control or predict. Such factors, among others, may have a material adverse effect on MAKO's business, financial condition and results of operations and may include the potentially significant impact of a continued economic downturn or delayed economic recovery on the ability of MAKO's customers to secure adequate funding, including access to credit, for the purchase of MAKO's products or cause MAKO's customers to delay a purchasing decision, changes in general economic conditions and credit conditions, changes in the availability of capital and financing sources for our company and our customers, unanticipated changes in the timing of the sales cycle for MAKO's products or the vetting process undertaken by prospective customers, changes in competitive conditions and prices in MAKO's markets, changes in the relationship between supply of and demand for our products, fluctuations in costs and availability of raw materials, finished goods, and labor, changes in other significant operating expenses, slowdowns, delays, or inefficiencies in MAKO's product research and development cycles, unanticipated issues relating to intended product launches, decreases in sales of MAKO's principal product lines, decreases in utilization of MAKO's principal product lines or in procedure volume, increases in expenditures related to increased or changing governmental regulation or taxation of MAKO's business, both nationally and internationally, unanticipated issues in complying with domestic or foreign regulatory requirements related to MAKO's current products, including initiating and communicating product actions or product recalls and meeting Medical Device Reporting requirements and other required reporting to the United States Food and Drug Administration, or securing regulatory clearance or approvals for new products or upgrades or changes to MAKO's current products, developments adversely affecting our potential sales activities outside the United States, increases in cost containment efforts by group purchasing organizations, the impact of the United States healthcare reform legislation enacted in March 2010 on hospital spending, reimbursement, unanticipated changes in reimbursement to our customers for our products, and the taxing of medical device companies, any unanticipated impact arising out of the securities class action or any other litigation, inquiry, or investigation brought against MAKO, loss of key management and other personnel or inability to attract such management and other personnel, increases in costs of retaining a direct sales force and building a distributor network, unanticipated issues related to, or unanticipated changes in or difficulties associated with, the recruitment of agents and distributors of our products, and unanticipated intellectual property expenditures required to develop, market, and defend MAKO's products. These and other risks are described in greater detail under Item 1A, "Risk Factors," in MAKO's periodic filings with the Securities and Exchange Commission, including MAKO's annual report on Form 10-K for the year ended December 31, 2012 filed on February 28, 2013. Given these uncertainties, undue reliance should not be placed on these forward-looking statements. MAKO does not undertake any obligation to release any revisions to these forward-looking statements publicly to reflect events or circumstances after the date of this press release or to reflect the occurrence of unanticipated events.

"MAKOplasty(R)," "RESTORIS(R)," "RIO(R)," as well as the "MAKO" logo, whether standing alone or in connection with the words "MAKO Surgical Corp." are trademarks of MAKO Surgical Corp.

Oxford(R) is a registered trademark of Biomet Orthopedics.

View data

Condensed Statements of Operations (unaudited) Three Months Ended

(in thousands, except per share data) March 31,

2013 2012

Revenue:

Procedures $ 14,836 $ 11,562

Systems 6,499 5,871

Service 3,474 2,206

Total revenue 24,809 19,639

Cost of revenue:

Procedures 3,667 2,657

Systems 2,431 2,448

Service 442 381

Total cost of revenue 6,540 5,486

Gross profit 18,269 14,153

Operating costs and expenses:

Selling, general and administrative (exclusive of depreciation and amortization) 20,138 19,376

Research and development (exclusive of depreciation and amortization) 5,013 4,854

Depreciation and amortization 2,046 1,686

Total operating costs and expenses 27,197 25,916

Loss from operations (8,928) (11,763)

Other income (expense), net (677) 58

Loss before income taxes (9,605) (11,705)

Income tax expense 15 25

Net loss $ (9,620) $ (11,730)

Net loss per share - Basic and diluted $ (0.21) $ (0.28)

Weighted average common shares outstanding --

Basic and diluted 46,804 41,694

Depreciation expense for certain property and equipment was reclassified from selling, general and administrative expense to depreciation and amortization expense in the prior period's condensed statement of operations to conform to the current period's presentation. This change in presentation only affects the components of operating costs and expenses and does not affect total operating costs and expenses, revenue, cost of revenue, net loss or cash flows.

Condensed Statements of Operations (unaudited) Three Months Ended (in thousands, except per share data) March 31, 2013 2012 Revenue: Procedures $ 14,836 $ 11,562 Systems 6,499 5,871 Service 3,474 2,206 Total revenue 24,809 19,639 Cost of revenue: Procedures 3,667 2,657 Systems 2,431 2,448 Service 442 381 Total cost of revenue 6,540 5,486 Gross profit 18,269 14,153 Operating costs and expenses: Selling, general and administrative (exclusive of depreciation and amortization) 20,138 19,376 Research and development (exclusive of depreciation and amortization) 5,013 4,854 Depreciation and amortization 2,046 1,686 Total operating costs and expenses 27,197 25,916 Loss from operations (8,928) (11,763) Other income (expense), net (677) 58 Loss before income taxes (9,605) (11,705) Income tax expense 15 25 Net loss $ (9,620) $ (11,730) Net loss per share - Basic and diluted $ (0.21) $ (0.28) Weighted average common shares outstanding -- Basic and diluted 46,804 41,694 Depreciation expense for certain property and equipment was reclassified from selling, general and administrative expense to depreciation and amortization expense in the prior period's condensed statement of operations to conform to the current period's presentation. This change in presentation only affects the components of operating costs and expenses and does not affect total operating costs and expenses, revenue, cost of revenue, net loss or cash flows.

View data

Condensed Balance Sheets (unaudited) March 31, December 31,

(in thousands) 2013 2012

ASSETS

Current Assets:

Cash and cash equivalents $ 41,469 $ 61,367

Short-term investments 28,393 11,899

Accounts receivable 15,111 22,389

Inventory 25,129 25,080

Deferred cost of revenue 759 967

Financing commitment asset 6,947 7,608

Prepaid and other current assets 2,453 1,972

Total current assets 120,261 131,282

Long-term investments 1,165 -

Cost method investment 4,181 4,181

Property and equipment, net 23,414 22,996

Intangible assets, net 5,229 5,657

Other assets 2,786 2,786

Total assets $ 157,036 $ 166,902

LIABILITIES AND STOCKHOLDERS' EQUITY

Current Liabilities:

Accounts payable $ 1,509 $ 2,267

Accrued compensation and employee benefits 2,505 4,298

Other accrued liabilities 7,702 8,727

Deferred revenue 8,622 9,973

Total current liabilities 20,338 25,265

Deferred revenue, non-current 752 800

Total liabilities 21,090 26,065

Stockholders' Equity:

Common stock 47 47

Additional paid-in capital 367,114 362,364

Accumulated deficit (231,196) (221,576)

Accumulated other comprehensive gain (loss) (19) 2

Total stockholders' equity 135,946 140,837

Total liabilities and stockholders' equity $ 157,036 $ 166,902

Condensed Balance Sheets (unaudited) March 31, December 31, (in thousands) 2013 2012 ASSETS Current Assets: Cash and cash equivalents $ 41,469 $ 61,367 Short-term investments 28,393 11,899 Accounts receivable 15,111 22,389 Inventory 25,129 25,080 Deferred cost of revenue 759 967 Financing commitment asset 6,947 7,608 Prepaid and other current assets 2,453 1,972 Total current assets 120,261 131,282 Long-term investments 1,165 - Cost method investment 4,181 4,181 Property and equipment, net 23,414 22,996 Intangible assets, net 5,229 5,657 Other assets 2,786 2,786 Total assets $ 157,036 $ 166,902 LIABILITIES AND STOCKHOLDERS' EQUITY Current Liabilities: Accounts payable $ 1,509 $ 2,267 Accrued compensation and employee benefits 2,505 4,298 Other accrued liabilities 7,702 8,727 Deferred revenue 8,622 9,973 Total current liabilities 20,338 25,265 Deferred revenue, non-current 752 800 Total liabilities 21,090 26,065 Stockholders' Equity: Common stock 47 47 Additional paid-in capital 367,114 362,364 Accumulated deficit (231,196) (221,576) Accumulated other comprehensive gain (loss) (19) 2 Total stockholders' equity 135,946 140,837 Total liabilities and stockholders' equity $ 157,036 $ 166,902

View data

Condensed Statements of Cash Flows (unaudited) Three Months Ended March 31,

(in thousands)

2013 2012

Operating activities:

Net loss $ (9,620) $ (11,730)

Adjustments to reconcile net loss to net cash used in operating activities:

Depreciation 1,759 1,378

Amortization of intangible assets 428 420

Stock-based compensation 2,938 2,721

Provision for inventory reserve 311 28

Amortization of premium on investment securities 51 128

Loss on asset impairment 265 249

Provision for doubtful accounts 117 45

Issuance of stock under development agreement 194 227

Non-cash changes under credit facility 661 -

Changes in operating assets and liabilities:

Accounts receivable 7,161 8,218

Inventory (1,284) (5,041)

Deferred cost of revenue 208 (230)

Prepaid and other current assets (481) (2,333)

Other assets - 13

Accounts payable (758) 1,344

Accrued compensation and employee benefits (1,793) (4,707)

Other accrued liabilities (1,025) (3,066)

Deferred revenue (1,399) 443

Net cash used in operating activities (2,267) (11,893)

Investing activities:

Purchase of investments (25,018) (3,160)

Proceeds from sales and maturities of investments 7,287 10,186

Acquisition of property and equipment (1,518) (2,183)

Net cash provided by (used in) investing activities (19,249) 4,843

Financing activities:

Proceeds from employee stock purchase plan 406 360

Exercise of common stock options and warrants for cash 1,270 2,026

Payment of payroll taxes relating to vesting of restricted stock (58) (81)

Net cash provided by financing activities 1,618 2,305

Net decrease in cash and cash equivalents (19,898) (4,745)

Cash and cash equivalents at beginning of period 61,367 13,438

Cash and cash equivalents at end of period $ 41,469 $ 8,693

Condensed Statements of Cash Flows (unaudited) Three Months Ended March 31, (in thousands) 2013 2012 Operating activities: Net loss $ (9,620) $ (11,730) Adjustments to reconcile net loss to net cash used in operating activities: Depreciation 1,759 1,378 Amortization of intangible assets 428 420 Stock-based compensation 2,938 2,721 Provision for inventory reserve 311 28 Amortization of premium on investment securities 51 128 Loss on asset impairment 265 249 Provision for doubtful accounts 117 45 Issuance of stock under development agreement 194 227 Non-cash changes under credit facility 661 - Changes in operating assets and liabilities: Accounts receivable 7,161 8,218 Inventory (1,284) (5,041) Deferred cost of revenue 208 (230) Prepaid and other current assets (481) (2,333) Other assets - 13 Accounts payable (758) 1,344 Accrued compensation and employee benefits (1,793) (4,707) Other accrued liabilities (1,025) (3,066) Deferred revenue (1,399) 443 Net cash used in operating activities (2,267) (11,893) Investing activities: Purchase of investments (25,018) (3,160) Proceeds from sales and maturities of investments 7,287 10,186 Acquisition of property and equipment (1,518) (2,183) Net cash provided by (used in) investing activities (19,249) 4,843 Financing activities: Proceeds from employee stock purchase plan 406 360 Exercise of common stock options and warrants for cash 1,270 2,026 Payment of payroll taxes relating to vesting of restricted stock (58) (81) Net cash provided by financing activities 1,618 2,305 Net decrease in cash and cash equivalents (19,898) (4,745) Cash and cash equivalents at beginning of period 61,367 13,438 Cash and cash equivalents at end of period $ 41,469 $ 8,693

View data

CONTACT: Investors:

MAKO Surgical Corp.

954-628-1706

investorrelations@makosurgical.com

or

Westwicke Partners

Mark Klausner

443-213-0500

makosurgical@westwicke.com

CONTACT: Investors: MAKO Surgical Corp. 954-628-1706 investorrelations@makosurgical.com or Westwicke Partners Mark Klausner 443-213-0500 makosurgical@westwicke.com

http://www.globenewswire.com/newsroom/ti?nf=MTMjMTAwMzE4MDcjOTk2Nw==

Can MAKO Surgical Beat These Numbers?

by Seth Jayson, The Motley Fool May 6th 2013 1:28AM

Updated May 6th 2013 1:30AM

MAKO Surgical (NAS: MAKO) is expected to report Q1 earnings on May 7. Here's what Wall Street wants to see:

The 10-second takeaway

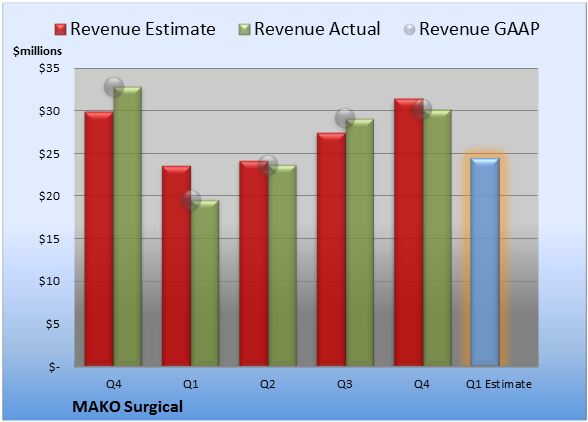

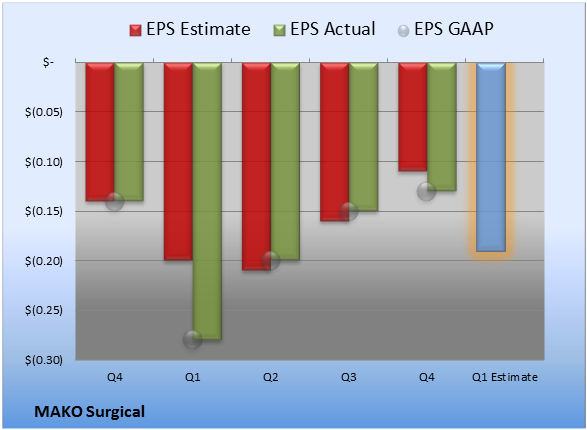

Comparing the upcoming quarter to the prior-year quarter, average analyst estimates predict MAKO Surgical's revenues will increase 24.5% and EPS will remain in the red.

The average estimate for revenue is $24.4 million. On the bottom line, the average EPS estimate is -$0.19.

Revenue details

Last quarter, MAKO Surgical booked revenue of $30.2 million. GAAP reported sales were 8.1% lower than the prior-year quarter's $32.9 million.

Source: S&P Capital IQ. Quarterly periods. Dollar amounts in millions. Non-GAAP figures may vary to maintain comparability with estimates.

EPS details

Last quarter, EPS came in at -$0.13. GAAP EPS were -$0.13 for Q4 versus -$0.14 per share for the prior-year quarter.

Source: S&P Capital IQ. Quarterly periods. Non-GAAP figures may vary to maintain comparability with estimates.

Recent performance

For the preceding quarter, gross margin was 67.0%, 110 basis points worse than the prior-year quarter. Operating margin was -19.6%, 250 basis points worse than the prior-year quarter. Net margin was -19.0%, 200 basis points worse than the prior-year quarter.

Looking ahead

The full year's average estimate for revenue is $125.9 million. The average EPS estimate is -$0.51.

Investor sentiment

The stock has a five-star rating (out of five) at Motley Fool CAPS, with 1,202 members out of 1,247 rating the stock outperform, and 45 members rating it underperform. Among 272 CAPS All-Star picks (recommendations by the highest-ranked CAPS members), 260 give MAKO Surgical a green thumbs-up, and 12 give it a red thumbs-down.

Of Wall Street recommendations tracked by S&P Capital IQ, the average opinion on MAKO Surgical is hold, with an average price target of $17.43.

http://www.dailyfinance.com/2013/05/06/can-mako-surgical-beat-these-numbers/

Previewing MAKO Surgical's First Quarter: A Pivotal Earnings Release

May 6 2013, 15:18 by: PropThink | about: MAKO

By Ivan Deryugin

Within biotechnology and the broader healthcare sector, investor sentiment often reaches extremes. A company might be heralded as a revolution in medicine and see its stock price soar, only to have it fall as reality fails to match lofty expectations and sentiment swings to the other extreme. That's exactly what occurred with MAKO Surgical (MAKO). After climbing to well above $40 in March 2012, shares began to collapse as the company failed to meet high consensus estimates. And since then, shares have continued to slide to their current $10.65, and with over 26% of the company's float sold short, it's clear that there is ample skepticism about MAKO's ability to reach profitability. With Q1 2013 earnings to be released on May 7, traders and investors will have a fresh opportunity to see if MAKO's efforts to turn itself around are bearing fruit.

2012: What Went Wrong?

Much of MAKO's slide over the last 12 months can be attributed to 2 events: 1) A Q1 2012 miss and lowered guidance, and 2) guidance that was lowered again in Q2 2012. MAKO's original guidance for 2012 called for 56-62 RIO surgical system sales, and in Q1, the company revised that guidance downward to 52-58 system sales. Alongside a Q1 miss, that sent shares falling well over 20%, and in July 2012, MAKO provided new guidance ahead of its Q2 2012 results, which sent the stock into a 43% plunge.

In July, MAKO lowered its forecasts for growth in both sales of RIO systems and surgical procedures. The company called for 42-48 RIO system sales in 2012, versus prior guidance of 52-58, and lowered its procedure guidance to 11,000-12,000, versus prior guidance of 11,000-13,000. MAKO's forecasts implied an 18.18% cut to RIO system sales at the midpoint of guidance, and a 4.17% cut to procedures at the midpoint of guidance. On its Q2 call, MAKO spoke at length about the challenges it faced during the first half of the year, and it is important that investors understand the underlying drivers of weak performance at MAKO, and what the company has done (and is doing) to address these issues.

In the first 6 months of 2012, MAKO noticed that hospital administrators had begun to scrutinize RIO purchases more closely (and by extension, MAKOplasty hip and knee procedures as well), as well as garner more surgeon support for the systems. MAKO reiterated on its Q2 call that while it has been successful in securing surgeon support for RIO systems, in hindsight it was unprepared for the increased efforts needed to actually overcome initial hesitations about its products. To that end, MAKO announced several initiatives, including a restructuring of its salesforce to increase the levels of scientific and technical knowledge regarding clinical data for MAKO's products as well efforts to deepen relationships with surgeons across the United States, and continued to make enhancements to its product line, both in terms of hardware and software.

Framing the Quarter: 4 Key Elements

MAKO's Q1 will be a pivotal quarter for the company, not only in terms of preserving/repairing management's credibility, but in terms of competition and capital as well. To that end, there are 4 key elements to this quarter that investors need to pay attention to.

1. Consensus estimates: Ahead of MAKO's Q1 results, consensus estimates call for a loss of 19 cents/share on revenue of $24.82 million. MAKO must, at a minimum, meet these estimates, or provide clear and convincing arguments as to why a miss should not be interpreted as a sign of structural weakness.

2. Reaffirming guidance: MAKO provided guidance for the year ahead during alongside its year-end 2012 earnings, and for 2013, MAKO expects to sell 45-48 RIO systems (flat to +6.67% Y/Y), and perform 13,500-14,500 MAKOplasty procedures. Given that MAKO has revised guidance downward several times in 2012, this is perhaps the most important element to this quarter. Expectations have fallen sharply, with Mizuho noting that over the past 7 months, consensus estimates have fallen by nearly 50% as sentiment regarding MAKO has soured. Another cut to guidance would further damage the credibility of MAKO's management team, despite the multiple steps taken to turn the company around.

3. Competition: Historically, MAKO's primary competition has come from traditional surgical companies, such as Stryker (SYK), Zimmer Holdings (ZMH), and Johnson & Johnson (JNJ) [Intuitive Surgical (ISRG) is more of peer than a competitor, given that its da Vinci systems are designed for different indications than those of MAKO]. However, in recent months, a new competitor has emerged: privately held Blue Belt Technologies. For the time being, it does not seem that Blue Belt has weakened MAKO's market position. However, the threat remains, and MAKO is likely to come under pressure in addressing how it plans to defend itself against stronger competition, particularly if the company's Q1 results come in below consensus or guidance is lowered.

4. Capital resources: MAKO ended 2012 with $73.266 million in cash & investments, and although MAKO is debt free, it continues to burn capital, with $27.303 and $30.292 million of cash burn in 2011 and 2010 respectively. MAKO forecast that it will see operating cash burn of $22 to $27 million in 2013, which will bring MAKO's balance of cash & investments below $50 million at the midpoint. And, should MAKO's Q1 results come in below expectations, or if guidance is yet again lowered, the company may see cash burn reach the upper end of its forecasted range. With sustained profitability currently estimated to begin only in 2015, the possibility exists that MAKO will need to raise capital before that occurs, and the company's Q1 performance and updated guidance for 2013 should clue in investors as to whether or not the company will need fortify the balance sheet in the near- to medium-term.

We believe that it's best to remain on the sidelines until MAKO reports its Q1 results. While we're always interested in picking up a turn-around story while it's still on the cheap, there remains a major element of risk coming into the Q1 results. If MAKO disappoints, the stock will tumble yet again as confidence in managements' foresight and ability to improve its competitive position erodes. But given the stock's high short interest and low expectations, if the quarter exceeds -- or even meets -- expectations, we expect a significant rally from MAKO. In that case, the company will see a near-term overhang removed with guidance finally set appropriately. The potential for short positions to unwind rapidly following an earnings meet (or beat) will serve as a tailwind and squeeze, we suspect, MAKO back to the high-$12 range.

MAKO's May puts present an attractive hedging opportunity for investors with a bullish bias and a desire to hedge against downside risk. MAKO's May $12.50 puts are currently trading at $2.10 per contract, and when combined with MAKO's closing price of $10.65 on May 3, the net cost to enter the position is $12.75. At that level, losses are capped at less than 2%, creating an inexpensive hedging opportunity. Although MAKO would need to rally nearly 20% for the trade to break even, such a move is not outside the realm of possibility given prevailing expectations and sentiment for the last few months.

Additional disclosure: PropThink is a team of editors, analysts, and writers. This article was written by Ivan Deryugin. We did not receive compensation for this article, and we have no business relationship with any company whose stock is mentioned in this article. Use of PropThink’s research is at your own risk. You should do your own research and due diligence before making any investment decision with respect to securities covered herein. You should assume that as of the publication date of any report or letter, PropThink, LLC and persons or entities with whom it has relationships (collectively referred to as "PropThink") has a position in all stocks (and/or options of the stock) covered herein that is consistent with the position set forth in our research report. Following publication of any report or letter, PropThink intends to continue transacting in the securities covered herein, and we may be long, short, or neutral at any time hereafter regardless of our initial recommendation. To the best of our knowledge and belief, all information contained herein is accurate and reliable, and has been obtained from public sources we believe to be accurate and reliable, and not from company insiders or persons who have a relationship with company insiders. Our full disclaimer is available at www.propthink.com/disclaimer.

http://seekingalpha.com/article/1406431-previewing-mako-surgical-s-first-quarter-a-pivotal-earnings-release?source=email_rt_article_title

MAKO Surgical Corp. Schedules First Quarter 2013 Earnings Release and Conference Call for Tuesday, May 7, 2013

Apr 25, 2013 17:47:44 (ET)

FT. LAUDERDALE, Apr 25, 2013 (GLOBE NEWSWIRE via COMTEX) -- MAKO Surgical Corp. announced today that it plans to release first quarter 2013 financial results after market close on Tuesday, May 7, 2013. Maurice R. Ferre, M.D., President and Chief Executive Officer, and Fritz L. LaPorte, Senior Vice President and Chief Financial Officer of MAKO, will host a conference call to review the first quarter 2013 results starting at 4:30 pm ET on the same day. The call will be concurrently webcast.

To listen to the conference call please dial 877-843-0414 for domestic callers or 914-495-8580 for international callers and enter the passcode 58873803, approximately ten minutes prior to the start time. To access the live audio broadcast or the subsequent archived recording, visit the Investor Relations section of MAKO's website at www.makosurgical.com . Following the call, a webcast replay will be available on MAKO's website, and an audio replay will also be available by calling 855-859-2056 (404-537-3406 for international callers) and entering the passcode 58873803. Both the audio and webcast replays will be available through May 14, 2013.

About MAKO Surgical Corp.

MAKO Surgical Corp. is a medical device company that markets its RIO(R) Robotic-Arm Interactive Orthopedic system, with specific applications for partial knee resurfacing and total hip replacement, and proprietary RESTORIS(R) Family of Implants for orthopedic procedures called MAKOplasty(R). The RIO is a surgeon-interactive tactile surgical platform that incorporates a robotic arm and patient-specific visualization technology, which enables accurate, consistently reproducible bone resection for accurate insertion and alignment of RESTORIS knee and hip implants. The MAKOplasty solution incorporates technologies enabled by an intellectual property portfolio including more than 300 U.S. and foreign, owned and licensed, patents and patent applications. Additional information can be found at www.makosurgical.com .

"MAKOplasty(R)," "RESTORIS(R)," "RIO(R)," as well as the "MAKO" logo, whether standing alone or in connection with the words "MAKO Surgical Corp." are trademarks of MAKO Surgical Corp.

CONTACT: Investors:

MAKO Surgical Corp.

954-628-1706

investorrelations@makosurgical.com

or

Westwicke Partners

Mark Klausner

443-213-0500

makosurgical@westwicke.com

http://www.globenewswire.com/newsroom/ti?nf=MTMjMTAwMzAxNjMjOTk2Nw==

MAKO Surgical Now Covered by WallachBeth Capital (MAKO)

Posted by: Masoud Bidgoli Posted date: April 22, 2013 In: Analyst Articles - US, Investing

Equities research analysts at WallachBeth Capital initiated coverage on shares of MAKO Surgical (NASDAQ: MAKO) in a research note issued to investors on Monday, ARN reports. The firm set a “hold” rating and a $12.00 price target on the stock.

A number of other analysts have also recently weighed in on MAKO. Analysts at Mizuho upgraded shares of MAKO Surgical from a “neutral” rating to a “buy” rating in a research note to investors on Tuesday, April 9th. They now have a $14.00 price target on the stock, up previously from $12.00. Finally, analysts at Canaccord Genuity cut their price target on shares of MAKO Surgical from $13.00 to $12.00 in a research note to investors on Wednesday, February 27th. They now have a “hold” rating on the stock.

Seven equities research analysts have rated the stock with a hold rating and four have given a buy rating to the stock. MAKO Surgical has a consensus rating of “Hold” and a consensus target price of $16.71.

Shares of MAKO Surgical (NASDAQ: MAKO) opened at 10.73 on Monday. MAKO Surgical has a 52 week low of $10.00 and a 52 week high of $42.98. The stock’s 50-day moving average is currently $11.55. The company’s market cap is $500.0 million.

MAKO Surgical (NASDAQ: MAKO) last issued its quarterly earnings data on Tuesday, February 26th. The company reported ($0.13) earnings per share (EPS) for the quarter, meeting the consensus estimate of ($0.13). The company had revenue of $30.28 million for the quarter, compared to the consensus estimate of $30.80 million. During the same quarter in the previous year, the company posted ($0.14) earnings per share. The company’s revenue for the quarter was down 8.0% on a year-over-year basis. On average, analysts predict that MAKO Surgical will post $-0.52 earnings per share for the current fiscal year.

MAKO Surgical Corp. (NASDAQ: MAKO) is a medical device company that markets its robotic arm solution and orthopedic implants for orthopedic procedures called MAKOplasty.

http://www.mideasttime.com/mako-surgical-now-covered-by-wallachbeth-capital-mako/11907/

MAKO Surgical Corp Started at Hold by WallachBeth

Apr 22, 2013 01:09:47 (ET)

(END) Dow Jones Newswires

April 22, 2013 01:09 ET (05:09 GMT)

MAKO Surgical Started at Hold by WallachBeth Capital >MAKO

Apr 21, 2013 12:38:12 (ET)

(END) Dow Jones Newswires

April 21, 2013 12:38 ET (16:38 GMT)

MAKO Neutralizes the Competition: Is the Stock a Buy?

http://www.fool.com/investing/general/2013/04/16/mako-neutralizes-the-competition-but-is-it-a-buy.aspx

Mako to Acquire Stanmore Robotic Assets in Patent Settlement

http://www.bloomberg.com/news/2013-04-16/mako-to-acquire-stanmore-robotic-assets-in-patent-settlement-1-.html

And snagging Stanmore's Sculptor and all robotic IP for a steal if the analyst reports of under $1M hold true. That's what a strong patent portfolio and defense of it will get you.

Clinching its market share further!

MAKO Surgical Corp. and Stanmore Implants Worldwide Ltd. Announce MAKO's Purchase of Stanmore Sculptor Robotic Guidance Arm

8:04 AM ET 4/16/13 | GlobeNewswire

MAKO Surgical Corp. (Nasdaq:MAKO) and Stanmore Implants Worldwide Ltd. today announced that MAKO has agreed to settle all patent infringement actions and acquire certain assets of Stanmore related to its Sculptor Robotic Guidance Arm (RGA) business.

On March 19, 2013, MAKO filed complaints against Stanmore with the U.S. International Trade Commission and the U.S. District Courts of the Northern District of California and the District of Massachusetts collectively alleging infringement of MAKO intellectual property by the Sculptor RGA.

Under the confidential settlement and asset purchase agreements between the parties, in exchange for a cash payment to Stanmore, MAKO will withdraw all legal actions and receive Stanmore's robotic business assets and intellectual property, as well as Stanmore's agreement to withdraw from robotics.

"Stanmore is pleased to have reached closure in this matter," said Michael R. Mainelli, Jr., President and Chief Executive Officer of Stanmore.

"This agreement both affirms and improves MAKO's intellectual property position in robotically assisted orthopedic surgery," said Maurice R. Ferre, M.D., President and Chief Executive Officer of MAKO. "Moreover, we are enthused about the possibility of partnering with Stanmore on potential future projects."

About MAKO Surgical Corp.

MAKO Surgical Corp. is a medical device company that markets its RIO(R) Robotic-Arm Interactive Orthopedic system, with specific applications for partial knee resurfacing and total hip replacement, and proprietary RESTORIS(R) Family of Implants for orthopedic procedures called MAKOplasty(R). The RIO is a surgeon-interactive tactile surgical platform that incorporates a robotic arm and patient-specific visualization technology, which enables accurate, consistently reproducible bone resection for accurate insertion and alignment of RESTORIS knee and hip implants. The MAKOplasty solution incorporates technologies enabled by an intellectual property portfolio including more than 300 U.S. and foreign, owned and licensed, patents and patent applications. Additional information can be found at www.makosurgical.com.

About Stanmore Implants

Stanmore Implants is a commercial-stage orthopaedic implant company focused on providing differentiated technologies designed to provide solutions for several important, yet underserved market segments. Stanmore's implant design service alongside its portfolio of orthopaedic implants draws on over 60 years' experience in providing some of the world's most successful implants in Extreme Orthopedics. Stanmore is backed by leading investors including Abingworth, Imperial Innovations and Ivy Capital and intends to seek like-minded co-investors in 2013 to further support the commercialisation and growth opportunities offered by its unique technologies and market positioning.

"MAKOplasty(R)," "RESTORIS(R)," "RIO(R)," as well as the "MAKO" logo, whether standing alone or in connection with the words "MAKO Surgical Corp." are trademarks of MAKO Surgical Corp.

CONTACT: MAKO Surgical Corp.

954-628-1706

investorrelations@makosurgical.com

http://www.globenewswire.com/newsroom/ti?nf=MTMjMTAwMjg1OTQjOTk2Nw==

MAKO Surgical and Stanmore Implants Worldwide announce that MAKO has agreed to settle all patent infringement actions and acquire certain assets of Stanmore related to its Sculptor Robotic Guidance Arm business

8:05 AM ET 4/16/13 | Briefing.com

Co announced that MAKO has agreed to settle all patent infringement actions and acquire certain assets of Stanmore related to its Sculptor Robotic Guidance Arm business. On March 19, 2013, MAKO filed complaints against Stanmore with the U.S. International Trade Commission and the U.S. District Courts of the Northern District of California and the District of Massachusetts collectively alleging infringement of MAKO intellectual property by the Sculptor RGA.

Under the confidential settlement and asset purchase agreements between the parties, in exchange for a cash payment to Stanmore, MAKO will withdraw all legal actions and receive Stanmore's robotic business assets and intellectual property, as well as Stanmore's agreement to withdraw from robotics.

WE WON!!!

Gotta love the up / down cycle $MAKO has given lately...learn to identify it and you can make a shit ton of money off of it...

The next "W" formation is underway...

MAKO Is For Growth: Seek Income And Stability Elsewhere (link back)

http://seekingalpha.com/article/1336491-mako-is-for-growth-seek-income-and-stability-elsewhere?source=email_rt_article_title

LOL...this piece was taylor made for me lol

http://www.insidermonkey.com/blog/mako-surgical-corp-mako-lions-gate-entertainment-corp-usa-lgf-among-tuesdays-top-upgrades-downgrades-112665/

MARKET TALK: Mizuho Sees Better Times Ahead for Mako Surgical

Apr 9, 2013 07:44:28 (ET)

7:44 EDT - After being nearly halved the past 7 months amid some growth concerns about robotic-surgical-equipment maker MAKO, Mizuho gets upbeat on the stock in upgrading it to buy and boosting its price target $2 to $14. "We believe that consensus 2013 estimates are achievable" while the company "still has plenty of room for growth in uni-knees, even accounting for new robotics competitors," Mizuho contends. The investment bank also thinks MAKO is unlikely to raise capital in the near-term" after selling stock in November and says MAKO is "trading at a discount to peers." Shares, inactive premarket, have fallen 18% this year. (kevin.kingsbury@dowjones.com)

(END) Dow Jones Newswires

April 09, 2013 07:44 ET (11:44 GMT)

MAKO Surgical corp Raised to Buy From Neutral by Mizuho

Apr 9, 2013 04:06:22 (ET)

(END) Dow Jones Newswires

April 09, 2013 04:06 ET (08:06 GMT)

$MAKO - MONSTER PINCHER IN THE MAKING!!!

All of it! Both iShares looking good, the institutional tab also looks good (but needs an update)...when this baby gets squeezing the release will be orgasmic!

Gabelli/Gamco or the Russel 2000?

Very interesting last 5 seconds lol

Finishing GREEN today will be a nice start to the week

It certainly has been "The Axe" here.

Once ARCA quits with their shannanigans we will go up...ARCA is notoriously keeping us down...when they are done, we will fly!

Kayla, I am sure you noticed that it was a Pittsburgh Paper.

Nice spin though.

Thanks for all of your insight over "there".

So we know the details on the injunction but the details of the settlement granting MAKO additional relief and future protections is under seal....for now. BTW Judge Cohn signed off on the permanent injunction and settlement. He's also the judge overseeing the weak class action ( Harrison et al vs MAKO) filed last July.

Gotta love Blue Belt's spin. We "resolved" the lawsuit. Yeehaw. You sure did. By having a permanent injunction filed against you (and agreeing to it), and settling the suit by agreeing to relief and protections both now and future. And all of this after vowing a fight to the death. LOL.

FORT LAUDERDALE, Fla., April 4, 2013 MAKO Surgical Corp. today announced that it has obtained an Order Granting Permanent Injunction enjoining Blue Belt Technologies, Inc. from engaging a former MAKO employee and requiring the destruction of all proprietary MAKO business information in Blue Belt's possession............The Order for Permanent Injunction was entered contemporaneous to a separate settlement agreement among Blue Belt, Mr. Gellman and MAKO, which provided MAKO with the described stipulated order, along with additional relief and future protections.

Blue Belt and Mako resolve suit

Apr 5, 2013, 1:05pm EDT

Malia Spencer

Reporter-

Pittsburgh Business Times

Email | Twitter | Google+ | LinkedIn

http://www.bizjournals.com/pittsburgh/blog/innovation/2013/04/blue-belt-and-mako-resolve-suit.html?page=all

Robotic surgical tools maker Blue Belt Technologies said Thursday it had resolved one of the two suits it faced from rival companies over its hiring practices. However, as a result the company’s Western Regional Vice President will be limited in the work he can do for the company.

Blue Belt and its Western Region Vice President Jeffrey Gellman were named in a suit filed in February by Fort Lauderdale, Fla.-based Mako Surgical Corp. Gellman previously worked for Mako and that company filed a complaint asserting breach of contract, breach of noncompete obligations, misappropriation of trade secrets and tortuous interference.

According to federal court filings granting Mako a permanent injunction and dismissing the case, from April 3 through July 31 Gellman is not allowed to actively work for Blue Belt nor is he allowed to offer services or assistance to the company in that time frame.

From Aug. 1 through Sept. 30 Gellman can work for Blue Belt “in a limited capacity” but is not allowed to work in any sales or marketing roles and can only work “with an inward-facing position” with no interaction with clients or prospective clients, according to the court order. During this time Blue Belt cannot allow Gellman to directly or indirectly assist its sales and marketing reps on any efforts for clients or prospective clients.

From August 1 through Jan. 1, 2014, Blue Belt must “implement all measures and safeguards necessary” ensuring that Gellman is “walled-off” from communication or collaboration with the company’s eastern regional sales and marketing efforts, according to the order. As of October 1 and through Jan. 1, 2014 Gellman can only work on sales or marketing for Blue Belt’s western region of the U.S.

Furthermore, the order requires that Blue Belt and Gellman hand over written certification to Mako, swearing under penalty of perjury, that any Mako information Gellman may have had has been permanently deleted and destroyed.

In a written statement Blue Belt President and CEO Eric Timko maintained that the law suit was without merit.

“At the same time, however, Blue Belt determined that is in our best interest to compete with Mako selling our new robotic technology in the marketplace, instead of competing in the courtroom, where no surgeon or patients can benefit,” he said. “We have established great momentum since officially launching NavioPFS in the United States. We fully expect to continue rapidly expanding our presence in the marketplace as more physicians and hospitals see the benefits that NavioPFS can bring to their patients and facilities at an economically friendly price point.”

Malia Spencer covers manufacturing, higher education and technology. Contact her at mspencer@bizjournals.com or 412-208-3829. You can also follow her on Twitter.

Blue Belt Technologies Resolves Lawsuit

http://www.fortmilltimes.com/2013/04/04/2599045/blue-belt-technologies-resolves.html

That was fast. So much for that vigorous defense Blue Belt was spouting off about. Lol. Stryker has one pending against Blue Belt as well.

Any further details on the civil settlement that accompanied today's injunction?

"The Order for Permanent Injunction was entered contemporaneous to a separate settlement agreement among Blue Belt, Mr. Gellman and MAKO, which provided MAKO with the described stipulated order, along with additional relief and future protections."

A great victory in MAKOs effort to protect its technology and keep it in house. Mr. Gellman tried to do a no no. Well done MAKO!

Mako Surgical Wins Court Order Against Former Employee, Competitor

Apr 4, 2013 17:38:42 (ET)

By Kristin Jones

Medical-device maker Mako Surgical Corp. (MAKO) said it has won a court order barring a former sales manager from working for a competitor, Blue Belt Technologies.

Mako had gone to court to enforce a non-competition agreement between Mako and Jeffrey Gellman, who was hired as an area vice president of sales for Blue Belt earlier this year, Mako said.

An order issued by a federal court in Florida Thursday prohibits Mr. Gellman from working for Blue Belt in any way until August 2013, and allows him to work in only a limited capacity there until 2014. Blue Belt and Mr. Gellman have also been ordered to certify that all Mako proprietary information has been destroyed.

An attorney for Blue Belt and Mr. Gellman did not immediately respond to a request for comment. Neither Mr. Gellman nor a representative for Blue Belt could be immediately reached.

Mako Chief Executive Maurice Ferre said the company was pleased with the injunction, and will work to project its investments in the field of robotically assisted orthopedic surgery.

Mako makes a surgeon-interactive robotic arm designed to allow surgeons greater prediction with a partial knee or total hip replacement procedure called Makoplasty.

Shares rose 5.1% to $11.04 in after-hours trading. Through the close, the stock was down 18% since the start of the year.

Write to Kristin Jones at kristin.jones@dowjones.com

Subscribe to WSJ: http://online.wsj.com?mod=djnwires

(END) Dow Jones Newswires

April 04, 2013 17:38 ET (21:38 GMT)

MAKO Surgical Corp. Secures Court-Ordered Permanent Injunction Against Blue Belt Technologies, Inc.

Apr 4, 2013 16:06:09 (ET)

FORT LAUDERDALE, Apr 04, 2013 (GLOBE NEWSWIRE via COMTEX) -- MAKO Surgical Corp. today announced that it has obtained an Order Granting Permanent Injunction enjoining Blue Belt Technologies, Inc. from engaging a former MAKO employee and requiring the destruction of all proprietary MAKO business information in Blue Belt's possession.

On January 30, 2013, Blue Belt announced that former MAKO sales manager Jeff Gellman had been hired as West Area Vice President of Sales. MAKO brought an action against Blue Belt and Mr. Gellman in the U.S. District Court of the Southern District of Florida to enforce the non-competition agreement between MAKO and Mr. Gellman and to prohibit the use or disclosure of MAKO's proprietary information.

By court order dated April 4, 2013, Mr. Gellman is prohibited from working for Blue Belt in any capacity until August 2013, and may only work in a limited capacity thereafter until 2014. Furthermore, both Blue Belt and Mr. Gellman have been ordered to certify under penalty of perjury that all MAKO proprietary information in their possession has been permanently purged. The U.S. District Court retained jurisdiction of the matter to ensure compliance with its order.

"MAKO is pleased with the sweeping and substantial injunctive relief we obtained on an expedited basis," said Maurice R. Ferre, M.D., President and Chief Executive Officer of MAKO. "We will remain vigilant in protecting the substantial investments made in becoming the leader in the field of robotically assisted orthopedic surgery."

The Order for Permanent Injunction was entered contemporaneous to a separate settlement agreement among Blue Belt, Mr. Gellman and MAKO, which provided MAKO with the described stipulated order, along with additional relief and future protections.

About MAKO Surgical Corp.

MAKO Surgical Corp. is a medical device company that markets its RIO(R) Robotic-Arm Interactive Orthopedic system, with specific applications for partial knee resurfacing and total hip replacement, and proprietary RESTORIS(R) Family of Implants for orthopedic procedures called MAKOplasty(R). The RIO is a surgeon-interactive tactile surgical platform that incorporates a robotic arm and patient-specific visualization technology, which enables accurate, consistently reproducible bone resection for accurate insertion and alignment of RESTORIS implants. The MAKOplasty solution incorporates technologies enabled by an intellectual property portfolio including more than 300 U.S. and foreign, owned and licensed, patents and patent applications. Additional information can be found at www.makosurgical.com .

"MAKOplasty(R)," "RESTORIS(R)," "RIO(R)," as well as the "MAKO" logo, whether standing alone or in connection with the words "MAKO Surgical Corp." are trademarks of MAKO Surgical Corp.

CONTACT: MAKO Surgical Corp.

954-628-1706

investorrelations@makosurgical.com

http://www.globenewswire.com/newsroom/ti?nf=MTMjMTAwMjc0NDMjOTk2Nw==

$MAKO - I'm going to make so much money from this play it's not even funny!

$MAKO - micro intraday squeezes going on...IMO

Are we testing the strength of the damn the shorts have built?

RELOADED!!!! $MAKO

Thx. Starbux. More so now then I was before. The price here is too enticing but it can burn either way.

Sounds like you've been a follower/shareholder for some time...looking forward to your future input

I think so, should bounce very soon. I hate AAOS week. LOL. Every year a volatile stock like MAKO gets whipsawed by every rumor. Robotic stocks. ouch. Seemed like ISRG was up $20 then down $8 today. Great news left and right for MAKO. Always a little wary of the quarter but they only need 8 bots sold to meet the avg estimate this quarter even with procedures on the low end. Sold 30 over the last two quarters. Q1 always slow. Encouraged by the chains adding. Even Hawaii's rocking a MAKO now. Finally. Lol.

Nice post! Today looked like a shake out and final short attempt IMO we be going up up and away in the near future.

Stryker follow's MAKO's lead, also files lawsuit against Blue Belt Technologies and former exec and gets said former Stryker exec banned from AAOS 2013 while seeking remedy & damages.

Stryker files lawsuit

Improved Accuracy and Decreased Pain Levels From Randomized Controlled Trial With MAKO's Robotic Arm System

8:30 AM ET 3/21/13 | GlobeNewswire

MAKO Surgical Corp., developer of human-interactive surgical robotic arm technology used to achieve accuracy in treating osteoarthritic disease, today announced the first results from a ten-year, prospective, randomized controlled trial evaluating the accuracy of unicompartmental knee arthroplasty (UKA) implant positioning, with and without robotic arm surgical assistance. Early results from this pivotal study are compelling, showing that robotic arm assisted UKA enhanced the accuracy of implant placement and decreased the levels of pain.

Performed under the guidance of orthopaedic surgeons Mark Blyth, M.D., Bryn Jones, M.D., Angus Maclean, M.D, and Iain Anthony, Ph.D., and Phil Rowe, Ph.D., at the Glasgow Royal Infirmary and the University of Strathclyde, in Glasgow, Scotland, the trial compared implant placement accuracy in patients receiving MAKO's RESTORIS MCK implants using MAKO's RIO Robotic Arm Interactive Orthopedic System to patients receiving manual placement of the Oxford Partial Knee implant from Biomet Orthopedics. One hundred patients have been enrolled in the study and randomly assigned (50 MAKO vs. 50 Oxford) to receive UKA with or without the aid of robotic arm assistance. The three-month results from 50 patients in each group also assessed early clinical outcomes such as patient reported post-operative pain levels and satisfaction. It is anticipated the trial will ultimately have 75 patients in each group. The patients will be tracked for ten years post-operatively.

"The early results are encouraging, as the data show more accurate component placement, as well as considerably lower self-reported post-operative pain levels out to six weeks," said Dr. Blyth. "The early results suggest that robotic arm assisted UKA with the RIO system greatly enhances the accuracy of implant placement, which can be achieved with only minimal deviation from the pre-operative plan."

Poor implant positioning in UKA is associated with suboptimal functional outcome following surgery; however, robotic arm technology for UKA provides pre-operative surgical planning for more accurate and minimal bone resection (excision of part of the bone), and intra-operative joint balancing for improved post-operative function and kinematics.

The primary endpoint of the clinical study is to validate the intra-operative implant alignment values recorded by the RIO system and to compare the accuracy of this implant positioning using robotic arm assistance with that achieved using conventional instrumentation in a randomized cohort. Among the secondary endpoints, the trial also examines early post-operative pain, and initial results show a reduction in patient reported post-op pain, which persists for almost 90 days following surgery. This ongoing trial will assess patient clinical, psychological and functional outcomes pre-operatively and at three months, one year, two years, five years and ten-years post-operatively.

"We are very happy with the early results for this randomized clinical trial, as it demonstrates the effectiveness of our RIO system and MAKOplastyPartial Knee Resurfacing as a minimally invasive surgical option for patients with early to mid-stage osteoarthritis," said Maurice R. Ferre, M.D., president and chief executive officer of MAKO. "Results also suggest that robotic arm assisted surgery for UKA may improve recovery with regard to less pain immediately following the procedure. We believe these early results underscore the importance of accuracy and precision in UKA surgeries, and the benefits that MAKOplasty can provide surgeons and their patients."

About MAKOplasty

MAKO's RIO Robotic Arm Interactive Orthopedic System coupled with its proprietary RESTORIS family of implants, enable surgeons to perform MAKOplasty for knee resurfacing and total hip arthroplasty. The RIO system overcomes limitations of conventional arthroplasty by providing auditory, visual and tactile guidance that, when integrated with the touch and feel of the surgeon's skilled hand, provide consistently reproducible precision in partial knee resurfacing and total hip replacements. This advanced treatment option is designed to relieve pain and restore range of motion for adults living with osteoarthritis and other degenerative hip diseases.

About MAKO Surgical Corp.

MAKO Surgical Corp. is a medical device company that markets its RIO Robotic-Arm Interactive Orthopedic system, with specific applications for partial knee resurfacing and total hip replacement, and proprietary RESTORIS Family of Implants for orthopedic procedures called MAKOplasty. The RIO is a surgeon-interactive tactile surgical platform that incorporates a robotic arm and patient-specific visualization technology, which enables accurate, consistently reproducible bone resection for accurate insertion and alignment of RESTORIS knee and hip implants. The MAKOplasty solution incorporates technologies enabled by an intellectual property portfolio including more than 300 U.S. and foreign, owned and licensed, patents and patent applications. Additional information can be found at www.makosurgical.com.

Forward-Looking Statements

This press release contains forward-looking statements regarding, among other things, statements related to expectations, goals, plans, objectives and future events. MAKO intends such forward-looking statements to be covered by the safe harbor provisions for forward-looking statements contained in Section 21E of the Securities Exchange Act of 1934 and the Private Securities Reform Act of 1995. In some cases, forward-looking statements can be identified by the following words: "may," "will," "could," "would," "should," "expect," "intend," "plan," "anticipate," "believe," "estimate," "predict," "project," "potential," "continue," "ongoing," or the negative of these terms or other comparable terminology, although not all forward-looking statements contain these words. These statements are based on the current estimates and assumptions of our management as of the date of this press release and are subject to risks, uncertainties, changes in circumstances, assumptions and other factors that may cause actual results to differ materially from those indicated by forward-looking statements, many of which are beyond MAKO's ability to control or predict. Such factors, among others, may have a material adverse effect on MAKO's business, financial condition and results of operations and may include the potentially significant impact of a continued economic downturn or delayed economic recovery on the ability of MAKO's customers to secure adequate funding, including access to credit, for the purchase of MAKO's products or cause MAKO's customers to delay a purchasing decision, changes in general economic conditions and credit conditions, changes in the availability of capital and financing sources for our company and our customers, unanticipated changes in the timing of the sales cycle for MAKO's products or the vetting process undertaken by prospective customers, changes in competitive conditions and prices in MAKO's markets, changes in the relationship between supply of and demand for our products, fluctuations in costs and availability of raw materials and labor, changes in other significant operating expenses, slowdowns, delays, or inefficiencies in MAKO's product research and development cycles, unanticipated issues relating to intended product launches, decreases in sales of MAKO's principal product lines, decreases in utilization of MAKO's principal product lines or in procedure volume, increases in expenditures related to increased or changing governmental regulation or taxation of MAKO's business, both nationally and internationally, unanticipated issues in complying with domestic or foreign regulatory requirements related to MAKO's current products, including initiating and communicating product actions or product recalls and meeting Medical Device Reporting requirements and other required reporting to the United States Food and Drug Administration, or securing regulatory clearance or approvals for new products or upgrades or changes to MAKO's current products, developments adversely affecting our potential sales activities outside the United States, increases in cost containment efforts by group purchasing organizations, the impact of the United States healthcare reform legislation enacted in March 2010 on hospital spending, reimbursement, unanticipated changes in reimbursement to our customers for our products, and the taxing of medical device companies, any unanticipated impact arising out of the securities class action or any other litigation, inquiry, or investigation brought against MAKO, loss of key management and other personnel or inability to attract such management and other personnel, increases in costs of retaining a direct sales force and building a distributor network, unanticipated issues related to, or unanticipated changes in or difficulties associated with, the recruitment of agents and distributors of our products, and unanticipated intellectual property expenditures required to develop, market, and defend MAKO's products. These and other risks are described in greater detail under Item 1A, "Risk Factors," in MAKO's periodic filings with the Securities and Exchange Commission, including MAKO's annual report on Form 10-K for the year ended December 31, 2012 filed on February 28, 2013. Given these uncertainties, undue reliance should not be placed on these forward-looking statements. MAKO does not undertake any obligation to release any revisions to these forward-looking statements publicly to reflect events or circumstances after the date of this press release or to reflect the occurrence of unanticipated events.

"MAKOplasty(R)," "RESTORIS(R)," "RIO(R)," as well as the "MAKO" logo, whether standing alone or in connection with the words "MAKO Surgical Corp." are trademarks of MAKO Surgical Corp.

Oxford(R) is a registered trademark of Biomet Orthopedics

Collier WB, Engh CA, McAuley JP, et al. Factors associated with the loss of thickness of polyethylene tibial bearings after knee arthroplasty. J Bone Joint Surg Am 2007;89:1306.

CONTACT: Media Contacts:

Amy Cook

925.552.7893

amycook@amcpublicrelations.com

Sue Siebert

954.628.0804

ssiebert@makosurgical.com

http://www.globenewswire.com/newsroom/ti?nf=MTMjMTAwMjU1MDcjOTk2Nw==

Mar 19, 2013, 5:57pm EDT

Mako Surgical files patent infringement lawsuits against rival Stanmore

http://www.bizjournals.com/southflorida/news/2013/03/19/mako-surgical-files-patent.html?ana=yfcpc

Mako Surgical President and CEO Dr. Maurice R. Ferre

MAKO Surgical Announces Patent Enforcement Actions Against Stanmore Entities

3/19/2013 5:59 PM ET

Medical device maker MAKO Surgical Corp. (MAKO) said Tuesday that it has filed complaints against Stanmore Implants Worldwide, Ltd. of Elstree, United Kingdom and Stanmore Inc. of Plymouth, Massachusetts with the U.S. International Trade Commission, and the U.S. District Courts of the Northern District of California and the District of Massachusetts collectively alleging infringement of three patents by Stanmore.

The patents at issue relate to computerized orthopedic surgical devices and software, and the patent infringement actions are directed at Stanmore's computerized orthopedic surgery guidance systems, including Stanmore's Sculptor Robotic Guidance Arm.

by RTT Staff Writer

For comments and feedback: editorial@rttnews.com

http://www.rttnews.com/story.aspx?ID=2080111

MAKO Surgical Corp. Showcases Pioneering MAKOplasty(R) Treatment Options for Total Hip Replacement and Partial Knee Resurfacing Surgeries at AAOS 2013 Annual Meeting

Mar 18, 2013 09:05:07 (ET)

CHICAGO, March 18, Mar 18, 2013 (GLOBE NEWSWIRE via COMTEX) -- MAKO Surgical Corp. , the leader in robotic arm assisted partial knee and total hip arthroplasty worldwide, today announced that it will showcase its MAKOplasty Total Hip Arthroplasty (THA) and Partial Knee Resurfacing applications at the American Academy of Orthopaedic Surgeons 2013 Annual Meeting (AAOS), March 20-23 at McCormick Place in Chicago. During the meeting, orthopedic surgeons will deliver presentations and provide hands-on demonstrations in MAKO's booth #212.

MAKOplasty THA is the company's latest application for its RIO Robotic Arm Interactive Orthopedic System, which will be highlighted by the company during the meeting. The RIO system overcomes limitations of conventional arthroplasty surgeries by providing auditory, visual and tactile guidance that, when integrated with the touch and feel of the surgeon's skilled hand, provides consistently reproducible precision in total hip and partial knee surgeries. MAKO's robotic arm assisted THA may result in a reduction in complications associated with conventional hip replacement surgery.

"With total hip replacement using MAKO robotic-arm assistance, I am a better surgeon because I perform 95 percent of my operations with the implants always in the correct position," said Lawrence Dorr, M.D., clinical professor of orthopedics at Keck School of Medicine at University of Southern California in Los Angeles. "This is better than the Harvard data, which showed 47 percent of the implants in the correct position. Even in my own practice, the MAKO robotic-arm assistance provides me with greater precision compared to when I perform the hip replacement using my experience only. Every patient who comes to me expects me to give him or her a precise operation. My consistent results allow me to fulfill the trust the patient puts in me," said Dr. Dorr.

"Knowing I have an accurate hip reconstruction gives me confidence I have minimized the risks for impingement and its consequent complications of dislocation, pain and accelerated wear. I also believe I have optimized the chance for durability of the hip replacement of 30 years," continued Dr. Dorr.

Hip replacement with MAKO's robotic-arm assistance builds upon the proven benefits of MAKOplasty Partial Knee Resurfacing, developed as an advanced treatment option designed to relieve pain for adults living with early to mid-stage osteoarthritis that has not yet spread to all three compartments of the knee. The use of the RIO system in MAKOplasty partial knee resurfacing leads to implant component placement that is two to three times more accurate than manual techniques. Studies also show that patients with bicompartmental MAKOplasty have improved function over those with total knee replacement surgery, and that these MAKOplasty patients demonstrate better post-operative range of motion and quadriceps strength compared to total knee arthroplasty.

"The MAKOplasty procedure with the RIO system for THA and partial knee resurfacing not only improves accuracy and reproducibility in surgery, it improves my patients' recovery," said Robert C. Marchand, M.D., a partner at South County Orthopedics in Wakefield, R.I., and one of the presenters in MAKO's booth during the AAOS 2013 Annual Meeting. "With partial knee resurfacing for example, I am able to use the RIO system to create an anatomical model of the patient's knee and develop a patient specific plan for optimal implant positioning based on the patient's individual anatomy. The RIO provides feedback and guidance, thereby preventing me from removing bone form outside the specified plan, and it allows for accurate implant placement. Our patients recover more quickly compared to conventional techniques and their post-operative range of motion is improved as well."

Additional studies describing the clinical success using MAKO's RIO system and its RESTORISfamily of implants when performing MAKOplasty procedures are beginning to appear in peer-reviewed journals, and a body of growing clinical data continues to be presented at academic meetings worldwide. In a recent oral presentation of a multi-center trial, the authors presented key results regarding the accuracy of robotic arm cup placement in total hip procedures, and reported 87 percent were positioned in an acceptable range. This compares favorably to data from a recently published Massachusetts General Hospital (MGH) study, which evaluated 1,823 hips receiving manual total hip arthroplasty, which reported 47 percent of cups were placed in an acceptable rage. Mal-positioning of acetabular cups in conventional hip replacement surgery may lead to impingement and implant wear that can cause dislocation. Nearly 300,000 primary hip replacement surgeries are performed annually in the United States using conventional technique.

Another multi-center study of MAKOplasty partial knee cases using RESTORIS MCK onlay medial unicompartmental implants, found very low two year post-operative revision rates of 0.4 percent, compared to two year revision rates reported at 4.0 percent and 4.4 percent respectively in the Swedish and Australian registries.

As of December 31, 2012, approximately 23,000 MAKOplasty procedures have been performed worldwide.

About MAKO Surgical Corp.

MAKO Surgical Corp. is a medical device company that markets its RIO Robotic-Arm Interactive Orthopedic system, with specific applications for partial knee resurfacing and total hip replacement, and proprietary RESTORIS Family of Implants for orthopedic procedures called MAKOplasty. The RIO is a surgeon-interactive tactile surgical platform that incorporates a robotic arm and patient-specific visualization technology, which enables accurate, consistently reproducible bone resection for accurate insertion and alignment of RESTORIS knee and hip implants. The MAKOplasty solution incorporates technologies enabled by an intellectual property portfolio including more than 300 U.S. and foreign, owned and licensed, patents and patent applications. Additional information can be found at www.makosurgical.com .

Forward-Looking Statements