News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

AMZN, AAPL, TEVA - >>> Warren Buffett's 3 Biggest Winners in the First Half of 2020: Are They Still Buys Now?

Winning stocks for the Oracle of Omaha were few during the first six months of the year.

Motley Fool

by Keith Speights

Jul 5, 2020

https://www.fool.com/investing/2020/07/05/warren-buffetts-3-biggest-winners-in-the-first-hal.aspx

Warren Buffett ranks as one of the greatest investors of all time. But the billionaire's investments didn't fare well in the first half of 2020. Buffett's Berkshire Hathaway (NYSE:BRK.A) (NYSE:BRK.B) shares fell 21% in the first six months of the year. Most of the stocks in Berkshire's investment portfolio were down as well.

However, there some stocks in the group that delivered impressive returns. Here are Warren Buffett's three biggest winners in the first half of 2020 -- and whether or not they're still great stocks to buy for investors who aren't yet legends.

1. Amazon.com

Buffett readily acknowledges that he has been a fan of Amazon.com (NASDAQ:AMZN) for a long time but didn't buy the stock. It took the prodding of one of his trusted investment managers to add the e-commerce giant to Berkshire's portfolio last year. Buffett is undoubtedly happy with the purchase: Amazon was his biggest winner in the first half of the year with a 49% gain.

Like most stocks, Amazon's shares slid during the coronavirus-fueled market sell-off that began in late February. However, investors realized pretty quickly that Amazon's business was actually booming as a result of the COVID-19 pandemic as consumers increasingly shopped online.

It didn't seem to matter too much to investors that Amazon's profits were squeezed somewhat as the company's pandemic-related costs rose. Many of the products with a spike in demand generate low margins. Amazon also is spending a lot more on wages and bonuses, personal protective equipment, and is even investing $300 million to build a COVID-19 testing lab for its employees.

2. Teva Pharmaceutical

Earlier in his career, Buffett was known as a by-the-book value investor. His training under another legendary investor, Benjamin Graham, might have made Teva Pharmaceutical (NYSE:TEVA) look like an attractive value stock. And the drugmaker's value was unlocked quite a bit in the first six months of 2020 as Teva's shares jumped 25%.

Teva's revenue fell in 2019. However, the company posted a 5% year-over-year revenue jump in the first quarter. That's pretty impressive considering that Teva continues to face declining sales for its former top-selling multiple sclerosis drug Copaxone and a challenging U.S. generic drug market.

Buffett has always maintained a long-term perspective, though. He led Berkshire to invest in Teva when it wasn't performing very well. It's likely that he viewed the pharma stock as dirt cheap considering the potential growth in the generic and prescription drug markets over the next couple of decades as the world's population ages.

3. Apple

Apple (NASDAQ:AAPL) ranks as Berkshire's top holding, by far. Buffett said in an interview with CNBC earlier this year that Apple is "probably the best business I know in the world." It's also one of his best-performing stocks, with Apple shares vaulting 24% higher in the first half of the year.

The company closed its Apple stores across the world temporarily in response to the COVID-19 pandemic. Apple stock plunged more than 30% during the overall market meltdown. But it roared back as investors realized the impact on the company's business should only be temporary.

Apple also benefited from several moves. It launched a new 13-inch MacBook Pro. The company unveiled 12-month no-interest installment payment plans for all of its devices. Apple also confirmed a highly anticipated shift to using its own chips in its Mac computers.

Are they buys now?

My view is that two of Buffett's three biggest winners of the first half of 2020 are still good picks, but one isn't.

I'm not a big fan of Teva. Some stocks are cheap for a season, while some are cheap for a reason. I think the latter is the case for Teva. The drugmaker still has a massive debt load even after paying down some of its debt. Its solid Q1 results were likely boosted largely by individuals stocking up on prescription drugs during the early part of the COVID-19 pandemic -- a temporary effect. Teva claims some promising new products. But it also has plenty of headwinds.

On the other hand, I really like both Amazon and Apple. Amazon continues to have strong growth prospects in e-commerce and cloud hosting. I suspect the company will also become a major player in healthcare. Apple should see stronger sales as it rolls out 5G iPhones. The company's services business is another solid growth driver. My hunch is that Amazon and Apple could be two of Buffett's biggest winners not just in 2020 but over the next 10 years.

<<<

>>> Meet the Stock Buffett Has Spent $7 Billion Buying Over the Past 2 Years

There hasn't been a more attractive stock on the Oracle of Omaha's radar.

by Sean Williams

Jul 30, 2020

https://www.fool.com/investing/2020/07/30/meet-the-stock-buffett-has-spent-7-billion-buying.aspx

In recent years, Berkshire Hathaway (NYSE:BRK.A) (NYSE:BRK.B) CEO Warren Buffett has taken a lot of flak for his investment style. More specifically, Buffett's unwillingness to chase after innovative tech stocks has left his company to underperform the benchmark S&P 500. Some folks have even implied that the Oracle of Omaha has lost his touch.

But a quick look at Berkshire Hathaway's performance under Buffett shows that his steadfastness in long-term investing is exactly what's made his company so successful. Since 1965, Berkshire Hathaway's per-share market value has risen by 2,744,062%. Put another way, a $100 investment back in 1965 would have been worth more than $2.7 million as of the end of 2019. When coupled with the fact that Buffett is up more than $50 billion on his company's stake in Apple, it's somewhere between premature and wrong to suggest he's lost his touch.

Buffett has been gun-shy about putting his company's record cash hoard to work

What has been odd, though, is Buffett's unwillingness to deploy his capital over the last 4.5 years. Although he and his team did spend more than $10 billion over the past couple of weeks by acquiring natural gas transmission and storage assets from Dominion Energy, as well as by purchasing 33.9 million shares of Bank of America stock, Berkshire's cash hoard is still, presumably, near its record high of $137 billion.

The Oracle of Omaha has made a habit over the past five decades of regularly acquiring brand-name businesses with entrenched economic moats. This has resulted in Berkshire Hathaway owning about five dozen companies, including well-known names like insurer GEICO, railroad operator BNSF, and confectioner See's Candies.

However, since the buyout of Precision Castparts in January 2016, Buffett has predominantly sat on his hands. Many investors -- myself included -- have taken this lack of participation as a signal that equities aren't a good value.

But there has been one stock to catch the Oracle of Omaha's eye. It's a stock that Buffett sank close to $1 billion into in 2018, nearly $5 billion into in 2019, and has acquired approximately $1.6 billion of just during the first quarter of 2020. And it's not Apple or Bank of America, if that's what you're thinking.

Instead, the real Apple of Buffett's eye is (drum roll) Berkshire Hathaway.

That's right, Buffett can't stop repurchasing his own stock.

This is the real apple of Buffett's eye

Believe it or not, Buffett and his right-hand man Charlie Munger went approximately five years without repurchasing a single share of Berkshire Hathaway stock between 2013 and 2018. That's because a rule was in place that disallowed buybacks if Berkshire Hathaway's stock was any higher than 20% above its book value. For years, Berkshire was regularly valued between 30% and 60% above its book value, thereby disallowing Buffet and Munger from pulling the trigger on share buybacks.

Then things changed in 2018. A new repurchase program structure was laid out that allowed Buffett and Munger to rebuy Berkshire Hathaway stock as long as two criteria were met:

There would need to be at least $20 billion in cash and cash equivalents on the company's balance sheet; and Buffett and Munger must agree that Berkshire Hathaway's stock is trading at a sizable discount to its intrinsic value.

The best aspects of these new criteria are that they eliminate any sort of time constraints that might be associated with a rigid line-in-the-sand book value metric and they allow two great money managers to do what they do best: buy value when they see it.

Clearly, this dynamic duo has seen opportunity of late. Berkshire Hathaway is currently trading at 25% above its book value, a level that was last consistently seen in 2012.

By repurchasing Class A and B shares, Buffett and his team are driving down the number of outstanding shares of the company. This usually has a positive impact on earnings per share (since there are fewer shares to divide net income into), and it can make a company more fundamentally attractive.

Yes, Berkshire Hathaway is an attractive investment opportunity

But these repurchases are about far more than just helping to pump up Berkshire Hathaway's earnings per share. They're about recognizing the real value that lies in these shares.

Though Buffett's company has underperformed in 2020, it has exceptionally strong tie-ins to the health of the U.S. and global economies. A quick peek under Berkshire's hood shows that a vast majority of the company's investment portfolio is tied up in Apple, bank stocks, and consumer staples. These are all companies/industries/sectors that benefit when the economy is running on all cylinders. Buffett emphatically proclaimed during his company's virtual shareholder meeting in May that investors should "never bet against America." This series of buybacks over the past two years supports that thesis.

To add to this point, Berkshire Hathaway has five dozen owned subsidiaries that also have cyclical tie-ins -- some of which have near-guaranteed cash flow. Berkshire Hathaway rarely invests in the utility sector, but subsidiary Berkshire Hathaway Energy owns quite a few energy-generating and natural gas-transmitting assets. These are businesses you can count on to deliver in virtually any economic environment.

With Berkshire Hathaway valued at levels last seen eight years ago and Buffett still very much in control of the big decision making, it looks to be every bit the value that the Oracle of Omaha perceives it to be.

<<<

>>> Berkshire's energy unit to buy Dominion Energy's gas transmission, storage business

Reuters

July 5, 2020

https://finance.yahoo.com/news/berkshires-energy-unit-buy-dominion-193311697.html

(Reuters) - Warren Buffett's Berkshire Hathaway Inc <BRKa.N> said on Sunday it agreed to buy Dominion Energy Inc's <D.N> natural gas transmission and storage business for $4 billion in cash, expanding its energy operations while allowing Dominion to focus on its utilities operations.

Berkshire's energy unit, Berkshire Hathaway Energy, is buying Dominion Energy Transmission, Questar Pipeline and Carolina Gas Transmission; 50% of the Iroquois Gas Transmission System, and 25% of the Cove Point liquefied natural gas facility in Maryland.

The transaction includes more than 7,700 miles (12,390 km) of natural gas storage and transmission pipelines and about 900 billion cubic feet of gas storage.

Berkshire Hathaway Energy will also assume $5.7 billion of Dominion's debt, giving the transaction a $9.7 billion enterprise value. It expects a closing in the fourth quarter, pending regulatory approvals.

"We are very proud to be adding such a great portfolio of natural gas assets to our already strong energy business," Buffett said in a statement.

The transaction does not include Dominion's interest in the Atlantic Coast Pipeline.

Dominion and Duke Energy Inc <DUK.N> announced separately on Sunday they would cancel that project, saying delays and uncertain costs threatened its economic viability.

<<<

>>> Bill Ackman Gives Up on Warren Buffett

If Berkshire Hathaway isn’t spending on investments, why get tied up in the stock?

Bloomberg

By Tara Lachapelle

May 27, 2020

https://www.bloomberg.com/opinion/articles/2020-05-27/bill-ackman-gives-up-on-warren-buffett-and-berkshire-hathaway?srnd=premium

If Bill Ackman is suggesting he can do better himself, others may be feeling that way, too.

What’s Berkshire Hathaway Inc. without its deals? Perhaps not worth owning. That’s the calculation Bill Ackman seems to have made in choosing to exit his stake in Warren Buffett’s company, and who can blame him?

Ackman, the widely followed hedge fund manager, disclosed Wednesday that his firm, Pershing Square Capital Management, sold a short-lived stake in Buffett’s Berkshire Hathaway, an investment that was valued at nearly $1 billion. It’s a telling move from a shareholder who seemed to be all in on Berkshire just weeks ago — perhaps until a normally sanguine Buffett signaled that he was feeling far less certain about how the U.S. recovers from this crisis relative to the many others he’s witnessed in the past.

When Ackman first bought Berkshire shares last summer, he said he was expecting Buffett to spend some of the company’s $100 billion of “excess cash” on large acquisitions and stock repurchases. (Weren’t we all.) That hasn’t happened, even before Covid-19 struck. Still, on March 23 as the virus took hold, Ackman told Bloomberg TV that he added to his Berkshire stake as part of a “recovery bet” on the U.S. economy that involved exiting short positions and using the proceeds to increase certain equity holdings. “We are all long,” Ackman said on air. “No shorts, you know, betting on the country.” Yes, betting on the country the way Buffett was expected to.

What’s changed since then is Buffett’s outlook. Even as Berkshire sits on $137 billion of cash, and as the pandemic would seem to have created cheap buying opportunities, Buffett is selling stocks and avoiding acquisitions. “The cash position isn’t that huge when I look at the worst-case possibilities,” he said during Berkshire’s virtual shareholder meeting earlier this month, leaving his listeners’ mouths agape — maybe Ackman included.

Cash Conundrum

As Warren Buffett allows Berkshire Hathaway's cash to accumulate, investors like Bill Ackman are looking elsewhere for better returns

If Buffett isn’t spending, Ackman will. Pershing Square’s managers suggested during a conference call with their own investors Wednesday that they can put money to work faster than Buffett at this stage, which is why it doesn’t make sense to have funds tied up in the stock even though they still see Berkshire as a strong company. It’s hard to argue against that thinking. Buffett’s ability to continuously convert the company’s insurance float and cash into high-return deals and fruitful stock picks has long underpinned Berkshire as an investment. Otherwise, it’s just a collection of sturdy but slow-growing businesses that represent a cross-section of the U.S. economy at a time when the economy isn’t looking so good, as Buffett himself says.

Shares of Berkshire are down 18% this year, compared with a 7% loss for the S&P 500 Index. That under-performance also isn’t new: The stock has trailed behind the benchmark index for the last decade, as the market recovered vigorously from one crisis, then recently plunged back into another. While Buffett says that he still thinks “nothing can stop America,” his actions are making it harder to believe him. And at almost 90 years old, he’s coming dangerously close to leaving his successor stuck with so much cash that it’s less a blessing than a curse.

Berkshire Loses Its Luster

Shares of Warren Buffett's Berkshire Hathaway have lagged behind the broader market over the last 10 years:

Berkshire still has a very devoted shareholder base. But it’s a group that looks a lot like Buffett himself: graying, male, not long from retirement. At last year’s shareholder meeting — the real-life one in Omaha — what was evident from looking out at the some 40,000 enthusiastic attendees was that Berkshire needs to work on courting younger investors. Given his deal-making hiatus and Berkshire’s under-performance, they may not have the same fascination with Buffett and his company as his loyal followers do. If even Ackman is saying, in so many words, “With respect, Mr. Buffett, we can do better,” certainly others are starting to feel that way, too.

Then again, it would take just one big, splashy purchase for people to say that Buffett’s got his groove back. That’s probably how he’d prefer to hand off the company, too.

<<<

>>> Opinion: Warren Buffett has lost at least $7 billion from his last 3 big investments

MarketWatch

May 23, 2020

By Howard Gold

https://www.marketwatch.com/story/warren-buffetts-recent-track-record-is-really-really-bad-2020-05-21?mod=mw_more_headlines

Berkshire Hathaway’s recent track record is really, really bad

Last week I wrote that this was the end of the Warren Buffett era as Berkshire BRK.A, +0.45% BRK.B, -0.00% underperformed the S&P 500 SPX, +0.23% over the entire 2009-2020 bear market. Even Buffett himself recommends investors buy the S&P.

Many Buffett fans responded by saying don’t count Buffett out yet because when (not if) the market tanks again, he’ll have more than $130 billion in cash to scoop up bargains. My MarketWatch colleague Mark Hulbert noted that top advisers often come back from losing streaks to post big gains.

So, what have the nearly 90-year-old Buffett and his 96-year-old business partner Charlie Munger done for us lately? Based on Berkshire’s SEC filings, three of Buffett’s biggest recent investments—Kraft Heinz KHC, +0.80% , Occidental Petroleum OXY, -0.84% , and airline stocks—have lost at least $7 billion altogether out of an investment of roughly $10 billion in each.

To my knowledge, this is the first time anyone has reported that figure. (Berkshire did not respond to my emailed questions by deadline.)

Heinz debacle

In 2013 Berkshire and private equity firm 3G Capital paid $23.2 billion to buy H.J. Heinz Co., and two years later Heinz bought Kraft Foods Group for $54 billion. Kraft Heinz Co. stock moved closely with the S&P for a couple of years. Then, after hitting an all-time closing high above $93 in February 2017, it began a long decline.

Last year Berkshire wrote down its investment by $3 billion, while Kraft Heinz took a $15 billion write-off on its Kraft and Oscar Mayer brands. In February, even before the market selloff began, Fitch Ratings and S&P Global Ratings downgraded Kraft Heinz to junk status. Meanwhile, in 2018 and 2019, 3G sold millions of shares (it still has a big stake) as Berkshire held firm. As of March 31, Berkshire’s Kraft Heinz shares were worth about $8 billion, around $2 billion less than what it paid for them.

When the deal was struck, The New York Times called it “a big bet on conventional staples of the American cupboard, even as consumers are shifting away from processed foods.”

Millennials just aren’t in to the iconic brands Buffett enjoyed as a boy.

“I made a mistake in the Kraft purchase in terms of paying too much,” Buffett told CNBC last June. No kidding.

Occidental Petroleum

Just two months later, in August, Berkshire completed a $10 billion investment in Occidental Petroleum, which helped Oxy win a bidding war against oil giant Chevron CHV, -1.06% to buy Anadarko Petroleum for $38 billion. The deal made Occidental the biggest player in the U.S.’s Permian Basin, the world’s highest producing oilfield.

Berkshire got 100,000 preferred shares, which gave it first dibs on dividend payments if things went south. That’s exactly what happened less than six months later. After the recent collapse in crude, Occidental cut dividends on its common stock by 86%. But it still owes Berkshire a hefty 8% annual dividend on the preferred shares, which Occidental has paid out in depreciated common stock rather than cash.

On Wednesday, Occidental common shares changed hands below $15, about one third the $44 a share at which it traded when the deal closed. As of March 31, Berkshire had lost about $500 million on the common stock it owned, but the April dividend payment doubled Berkshire’s common share holdings, cutting its paper loss in half.

We couldn’t determine a current price for the preferred shares of Occidental, which don’t trade regularly. The accumulation of those preferred dividends over time, whether in cash or common stock, could soften the blow of an investment that at best looks like a masterpiece of bad timing.

Not one, not two, not three, but four

And then there were the airlines. From mid-2016 through early 2017, Berkshire bought tens of millions of shares in the four largest U.S.-based carriers—American Airlines Group AAL, -1.92% , Delta Air Lines DAL, -2.02% , Southwest Airlines LUV, -2.46% , and United Airlines UAL, -1.70%

The price tag was north of $9.3 billion, by my calculations.

But when coronavirus hit, airline stocks plummeted, and by the time Berkshire dumped them all in April, they were worth about $4.3 billion, assuming all shares were sold on the SEC filing dates. That amounts to a stratospheric loss of $5 billion. Add all these losses together and you have at least a $7 billion hit to Berkshire, not including any decline in value on the Oxy preferred shares it owns.

Buffett has had some bad luck. Who could have foreseen COVID-19? But the problems with Occidental happened soon after the deal closed and there have been big clouds hanging over energy stocks for years. Buffett also waited until April to dump airline stocks, near the bottom.

Even more troubling, after he bought a stake in USAir in 1989, he complained the investment had “soured before the ink dried on the check.”

“Investors have regularly poured money into the domestic airline business to finance profitless (or worse) growth,” he wrote to shareholders in 1992.

As recently as 2007, he noted that “a durable competitive advantage [in the airline industry] has proven elusive ever since the days of the Wright brothers.” Even in 2013, he called airlines “a death trap for investors.”

So, he didn’t heed his own warnings, then went out and bought not one airline, but four? After all these mishaps and losses, who would want to bet a single share of Berkshire Hathaway stock that Warren Buffett is going to return to his former glory?

<<<

>>> Warren Buffett Sold Phillips 66 -- Here's Why I'm Holding (and May Buy More)

Berkshire Hathaway sold its remaining stake in Phillips 66. I don't plan to follow Buffett's move.

Motley Fool

Jason Hall

May 20, 2020

https://www.fool.com/investing/2020/05/20/warren-buffett-sold-phillips-66-heres-why-im-holdi.aspx

This quarter's Berkshire Hathaway (NYSE:BRK.A) (NYSE:BRK.B) 13-F filing with the Securities and Exchange Commission -- the document that discloses the company's massive stock portfolio holdings at the end of the prior quarter -- surprised a lot of investors. We already knew that Buffett sold Berkshire's stake in the major airlines, but we didn't know what the Oracle of Omaha bagged with his elephant gun. Turns out, not much of anything: Berkshire was by far a net seller in the quarter.

One of the stocks that Buffett unloaded in the quarter was Phillips 66 (NYSE:PSX). Not only is Phillips 66 a personal holding, but it's also the oil stock I've touted the most as being worth buying in the coronavirus crash. And despite Buffett's decision to move on from my favorite oil stock, I'm not changing my view. To the contrary: It's still on my radar as a company I'm interested in buying more of.

From the biggest shareholder to a steady seller

Warren Buffett seems to have an occasional infatuation with Phillips 66 that started before it was even a stand-alone company. In 2008, Buffett invested billions in ConocoPhillips (NYSE:COP), but at the time it was an integrated oil and gas company, not the independent producer we know it as today, resulting from the 2012 spinoff of Phillips 66 as a separate company.

Berkshire sold off all of ConocoPhillips soon after the spinoff, but kept most of the 27 million shares of Phillips 66 it got. Buffett regularly touted Phillips 66's management team as being one of the best in the business, lauding its wonderful job managing capital. It does so in two ways Buffett loves seeing from companies he invests in: buying back shares, and paying (and increasing) a great dividend.

Buffett's love affair with the company peaked in the summer of 2016, when Berkshire owned 15% of Phillips 66. The heat of summer's passion faded, and Berkshire became a net seller of the company's stock almost every quarter, finally unloading its shares completely by the end of this past March.

Reading the tea leaves

Without getting too deeply into trying to read Buffett's mind, we can see that the Berkshire portfolio has substantially reduced its exposure to the energy industry over the past few years. I think it's likely that this is intentional. As a sector, the oil and gas industry has been a terrible investment over the past decade, and it's reasonable to conclude that Buffett, along with portfolio managers Todd Combs and Ted Weschler, have found other, more compelling investment ideas outside the oil patch.

The bottom line is that with the exception of Phillips 66, Buffett's biggest oil investments have not done well. Even the sweetheart deal with Occidental Petroleum (NYSE:OXY) could be a loser if that company ends up filing for bankruptcy.

Either way, that's a lot of guessing at reasons why Buffett is selling that may or may not be correct. Moreover, it really doesn't matter why. Buffett and the other Berkshire managers aren't managing your stock portfolio.

How Phillips 66 has done since Buffett started selling

Berkshire sold the last of its Phillips 66 shares last quarter, but it was the portfolio-management equivalent of washing the dregs out of your teacup. The company sold 227,436 shares to bring its holding to zero; at one point, Berkshire had owned more than 80 million Phillips 66 shares.

Since Berkshire started selling, Phillips 66 has been a solid investment. The coronavirus crash has cratered its stock price and erased a massive portion of its gains, but at the peak in late 2019, Phillips 66 investors had enjoyed more than 60% in total returns since Buffett started selling. That was actually a little better than the market as a whole, as illustrated by the SPDR S&P 500 ETF Trust (NYSEMKT:SPY):

That past performance doesn't make Phillips 66 a buy, but it's a reminder that it's steadily been one of the best investments in oil and gas. That solid performance is a product both of the parts of the oil and gas business it operates in that give it some durable advantages, and of how well its management team has proven able to navigate oil markets.

Why it's a buy today

As a starting point, Phillips 66 isn't an oil producer. That part of the business stayed with ConocoPhillips when the two split, and that's proven a big benefit. Oil prices have spent the past eight years going through extreme volatility, with two massive price crashes that have hit the stand-alone producer far more than the integrated midstream, refining, and petrochemicals producer.

To the contrary, while low prices have weighed on ConocoPhillips, Phillips 66's advanced refineries have unlocked more profits when U.S. oil is cheaper than overseas crude. It's not only been a better investment than the producer, it's outperformed the market:

Next, Phillips 66 also counts on natural gas for its fastest-growing businesses in the midstream and chemicals segments. Natural gas demand hasn't been hit nearly as hard as oil, because it's used more for electricity production and as a feedstock to make things like plastics -- think bleach and hand-sanitizer bottles -- and fertilizers. So while the refining and fuel marketing segments will struggle for much of 2020, this weakness will be partly offset by its other segments.

The business is holding up well enough, along with a rock-solid balance sheet, that the board of directors made the call just last week to maintain the quarterly dividend, while other oil giants have had to cut their payouts.

Lastly, the oil crash has turned Phillips 66 into an absolute bargain. Shares have recovered from the bottom, but are still down more than 30% this year. Considering the company's ability to weather the current environment, and that its segments should prove some of the quickest to profit from the eventual recovery in oil demand, it's absolutely worth buying now -- even if Buffett and Berkshire have moved on.

<<<

>>> Wow! Buffett Sold 19 Stocks in the First Quarter

Despite a mountain of cash, the Oracle of Omaha and his team were busy sellers during the record-breaking market sell-off.

Motley Fool

Sean Williams

May 21, 2020

https://www.fool.com/investing/2020/05/21/wow-buffett-sold-19-stocks-in-the-first-quarter.aspx

Despite a record first-quarter loss for Berkshire Hathaway (NYSE:BRK.A)(NYSE:BRK.B), there's little denying that Warren Buffett is one of the greatest investors of our time. He's created close to $400 billion in value for Berkshire's shareholders over many decades, and he's handily outperformed the S&P 500 (inclusive of dividends) by more than 2,700,000% since 1964.

As a general rule, when Warren Buffett buys or sells a stock, Wall Street and retail investors tend to pay close attention. That's why the filing of Form 13F with the Securities and Exchange Commission last Friday, May 15, was so anticipated.

The Oracle of Omaha has been a busy bee in 2020

Form 13F provides a snapshot of what asset managers with more than $100 million under management owned as of the end of the previous quarter (in this case, March 31, 2020). Put another way, it's a means of seeing what the brightest minds on Wall Street were up to during the fastest bear market correction in history.

For Buffett, who was sitting on a near-record $128 billion in cash to enter 2020, the expectation was that he would be an active buyer with the market in a serious downdraft. However, Berkshire Hathaway's 13F showed quite the opposite, with a total of 19 stocks (yes, nineteen) either being pared down or completely sold out of during the first quarter.

Keep in mind the Oracle of Omaha has been a busy bee in the weeks subsequent to the end of the first quarter. We've seen some modest bank stock selling, along with Buffett completely exiting positions in all four major airlines. But since none of these transactions occurred prior to the March 31 cutoff, they're not being accounted for in the latest 13F filing. We'll see this activity accounted for when Berkshire releases its second-quarter snapshot in mid-August.

Buffett sold a lot of stocks in the first quarter

What did Buffett sell, exactly? Here's the full rundown, listed in descending order by total shares sold:

Goldman Sachs (NYSE:GS): 10,084,571 shares sold

Sirius XM: 3,857,000

JPMorgan Chase: 1,800,499

Synchrony Financial: 675,000

American Airlines Group: 591,000

Liberty Global: 481,000

DaVita: 470,000

Teva Pharmaceutical Industries: 460,000

General Motors: 319,000

Travelers Companies (NYSE:TRV): 312,379

Liberty Sirius XM Group: 240,000

Phillips 66 (NYSE:PSX): 227,436

Axalta Coating Systems: 194,000

Verisign: 137,132

Liberty Latin America: 84,062

Suncor Energy: 70,000

Southwest Airlines: 6,500

Biogen: 5,425

Amazon: 4,000

This selling activity is not the hallmark of a passive investor

The first thing that stands out about a vast majority of this selling is that it's very weird and not what we're used to seeing from a historically passive investor.

Don't get me wrong, some of this selling was deliberate, as I'll touch on in a moment. But as an example, it's unusual to see Buffett's company selling 5,425 shares of Biogen and 70,000 shares of Suncor Energy after adding both names to the portfolio during the sequential fourth quarter. Berkshire Hathaway typically builds up new positions over many quarters, so to see token pare-downs during a period where valuations appeared to be improving significantly, and following their initial addition in Q4 2019, is rather odd.

One possible explanation for these multiple small sales is that Buffett may not have been behind many of them. Rather, we might be seeing the effects of Todd Combs and Ted Weschler exerting more direct control over Berkshire's investment portfolio. Combs and Weschler are Buffett's famed "investing lieutenants" who control a percentage of the company's investable assets.

Though it gets tougher each year to identify exactly what stocks Buffett specifically added to his company's investment holdings, this selling activity is not his hallmark.

Some stock sales were clearly deliberate

However, some of this selling was deliberate and expected. For instance, Berkshire Hathaway has been telegraphing for about two years now that it would be parting ways with integrated oil and gas giant Phillips 66, and it wound up doing exactly that during the first quarter. As a reminder, Buffett invested $10 billion into Occidental Petroleum last year to aid with Occidental's purchase of Anadarko. With Buffett seemingly choosing a new horse in the oil industry, it all but sealed Phillips 66's fate in Berkshire's portfolio.

Likewise, Buffett and his team said goodbye to insurance giant Travelers. After selling nearly all of Berkshire's stake in the company during the fourth quarter, the writing was on the wall that Travelers would be getting the boot. Though Travelers remains profitable, lower yields will likely hurt its interest-earning capacity on its float (i.e., the difference between premium collected and claims paid) for the foreseeable future.

Another move that appeared deliberate was the significant paring down in Goldman Sachs. In just two quarters, Berkshire has gone from owning in excess of 18 million shares to just 1.92 million. It's no secret that Goldman Sachs is a cyclical financial services company that tends to do its best when the U.S. and global economy are firing on all cylinders.

With the outlook for mergers and acquisitions fairly bleak at the moment, Buffett and his team may simply view other opportunities in the financial sector as more attractive.

<<<

>>> Opinion: Dud stock picks, bad industry bets, vast underperformance — it’s the end of the Warren Buffett era

MarketWatch

May 16, 2020

By Howard Gold

https://www.marketwatch.com/story/dud-stock-picks-bad-industry-bets-vast-underperformance-its-the-end-of-the-warren-buffett-era-2020-05-14?siteid=bigcharts&dist=bigcharts

The chairman of Berkshire Hathaway seems to prefer the S&P 500 to his own company’s stock

Who is the Greatest of All Time? Michael or LeBron? Willie or the Babe? Aretha or Ol’ Blue Eyes?

When it comes to investing, Warren Buffett, chairman of Berkshire Hathaway BRK.B, -0.98%, is unquestionably the greatest who ever lived, posting an extraordinary record over more than five decades. From 1965 through 2018, Berkshire racked up a 20.5% compound annual return, more than double that of the S&P 500 SPX, +0.39%, including dividends.

Buffett also is a beloved multibillionaire in an age when the superrich are vilified. His homespun wisdom and Midwestern humility have made him the most sacred of all cows to a business media hungry for wit and personality. His paeans to free-market capitalism, along with his Democratic politics, haven’t hurt him with that group, either.

Read:Warren Buffett’s ‘outdated view’: One longtime fan is considering dumping his entire Berkshire stake

But now, after profoundly underperforming the S&P 500 throughout the entire 11-year bull market, it’s fair to ask whether Buffett is still, well, Buffett. Even at the company’s virtual annual meeting, held in Omaha on May 2, some questions by shareholders, curated by CNBC’s Becky Quick, struck this listener as unusually sharp.

At times, Buffett seemed uncomfortable amid PowerPoint slides and the absence of his longtime friend and business partner, Charlie Munger, who didn’t make the trip. His bullish comments about America seemed oddly discordant while a pandemic ravages our economy.

Meanwhile, intimations of mortality hung over the proceedings. Munger is 96 and Buffett turns 90 in August. The two, Buffett said, “are not going any place voluntarily, but we probably will go someplace involuntarily before that long.” Then he quickly added, “Charlie’s in good health, incidentally. I’m in good health.”

Questions put to Buffett

No wonder shareholders asked about how Berkshire will fare without Buffett and Munger at the helm.

The right question, however, is how Berkshire is doing with them. Consider:

• From March 9, 2009, the last bear market low, through Feb. 19, 2020, the recent bull market peak, Berkshire‘s Class B shares surged 396%. Sounds impressive, but Berkshire trailed the SPDR S&P 500 ETF Trust SPY, +0.46% and Vanguard Total Stock Market Index ETF VTI, +0.60% by more than 100 percentage points, after dividends were reinvested. (So far in 2020, Berkshire stock has lost nearly 25%, lagging those index ETFs by more than 10 percentage points.)

• As of March 31, Berkshire had more than $130 billion in cash, earning almost nothing. Yet even amid the coronavirus crash, Buffett and Munger haven’t spent any of it on the big deals that made them famous. Buffett attributed that to the Federal Reserve’s multitrillion-dollar intervention, which dwarfed whatever Berkshire could do.

• Berkshire won’t spend any cash to pay a dividend, while it’s happy to collect dividends from the companies it owns. Even a modest dividend yield would have helped Berkshire shareholders narrow the gap with the S&P 500 over the past 11 years.

• Berkshire’s operating businesses are doing well and throw off tons of cash. But this mishmash of insurance, consumer products, energy, utilities and railroads just doesn’t have the growth that forward-looking investors now demand. As oil prices are likely to stay depressed for some time, the energy business’ prospects are particularly grim.

• Several recent investments, like Kraft Heinz KHC, +1.38%, Occidental Petroleum OXY, +0.43% and airline stocks (which Berkshire sold in April) have been duds, and it’s hard to imagine what would propel those stocks higher. Apple AAPL, -0.59%, the largest of Berkshire’s equity investments, is among the few technology stocks in an investment portfolio so full of blue-chip banking names it could almost be a financial sector ETF.

I emailed those questions to Berkshire but got no response by deadline.

Index fund versus Berkshire stock

Buffett himself acknowledged how tough it will be for Berkshire to beat the S&P 500 from here on. “Berkshire is about as sound as any single investment can be,” he told the annual meeting, “but I would not want to bet my life on whether we beat the S&P 500 over the next 10 years.”

“In my view, for most people, the best thing to do is to own the S&P 500 index fund,” he said, echoing past statements.

“I would make no promise to anybody that we will do better than the S&P 500. But what I will promise them is that I’ve got 99% of my money in Berkshire.”

But not apparently his heirs’ money. “I haven’t changed my will and it directs that my widow would have 90% of the funds in index funds,” he said.

Follow the money — the future money. Warren Buffett is saying, almost in so many words, that an S&P 500 index fund is a better investment now than Berkshire Hathaway’s stock. There simply aren’t many new tricks this 90-year-old can learn, especially when growth investing, indexing and trillions of dollars of Fed buying power have stolen much of Berkshire’s thunder.

More than anyone else, he must know he’s had a marvelous run but that the curtain is coming down on the Buffett era. These days, even on Broadway, the show won’t go on.

<<<

>>> Tracking Warren Buffett's Berkshire Hathaway Portfolio - Q1 2020 Update

Seeking Alpha

May 17, 2020

John Vincent

Long only, value, special situations, fund holdings

https://seekingalpha.com/article/4348288-tracking-warren-buffetts-berkshire-hathaway-portfolio-q1-2020-update

Summary

Berkshire Hathaway's 13F stock portfolio value decreased from ~$242B to ~$176B this quarter.

Their largest three holdings are at ~57% of the entire portfolio.

Berkshire Hathaway reduced Goldman Sachs stake to a minutely small position during the quarter. They also sold their large stake in the big-four airlines last month.

This article is part of a series that provides an ongoing analysis of the changes made to Berkshire Hathaway’s 13F stock portfolio on a quarterly basis. It is based on Warren Buffett’s regulatory 13F Form filed on 05/15/2020. Please visit our Tracking 10 Years Of Berkshire Hathaway's Investment Portfolio article series for an idea on how his holdings have progressed over the years and our previous update for the moves in Q4 2019.

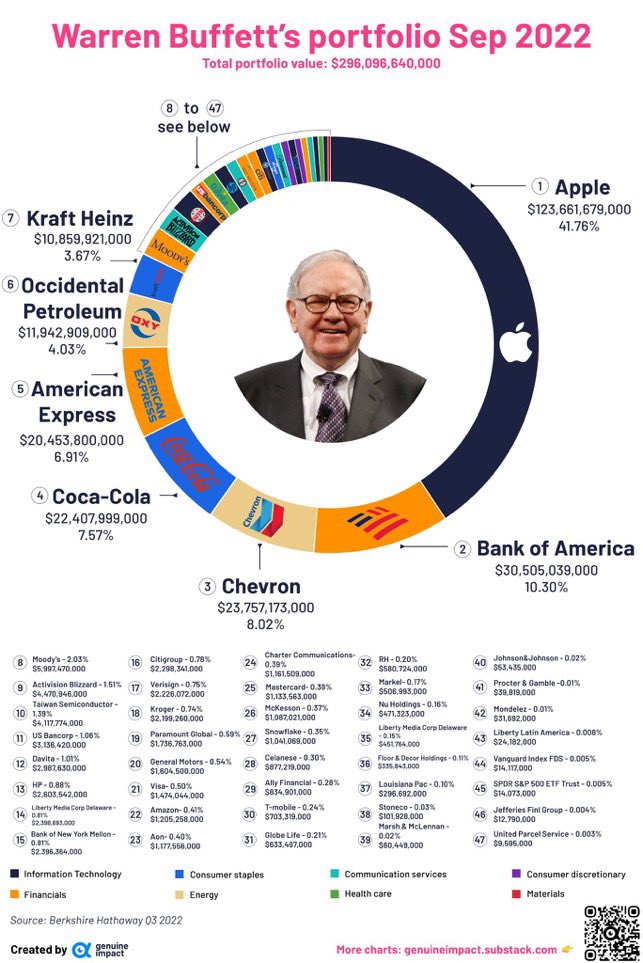

During Q1 2020, Berkshire Hathaway’s (BRK.A) (BRK.B) 13F stock portfolio value decreased ~28% from $242B to $176B. The top five positions account for more than two-thirds of the portfolio: Apple Inc., Bank of America, Coca Cola, American Express, and Wells Fargo. There are 47 individual stock positions many of which are minutely small compared to the overall size of the portfolio.

Warren Buffett’s writings (pdfs) are a treasure trove of information and are a very good source for anyone starting out on individual investing.

Note: In Q1 2020, Berkshire Hathaway repurchased ~5.5M Class B Equivalent Shares for a total outlay of ~$1.2B. The average price paid was ~$215. Book Value as of Q1 2020 was ~$153 per share. So, the repurchase happened at ~140% of Book Value. The Class B shares currently trade at ~$169.

New Stakes:

None.

Stake Disposals:

Phillips 66 (PSX) and Travelers Companies (TRV): These two minutely small stakes were disposed during the quarter.

Stake Increases:

Delta Air Lines (DAL): DAL was a very small 0.19% position in Q3 2016. The stake saw a whopping ~850% increase in Q4 2016 at prices between $39 and $52. There was a ~20% increase in Q2 2018 at prices between $49 and $56 and that was followed with a ~8% increase in Q1 2019 at ~$49.50. This quarter also saw a marginal increase. The stock currently trades at $19.19.

Note: The entire ~11% of the business stake was disposed at ~$22 last month. This is compared to their overall cost-basis of ~$44 - lost around half their investment over a holding period of just over three years.

PNC Financial (PNC): The 0.50% PNC stake was established in Q3 2018 at prices between $134 and $146 and increased by just over one-third next quarter at prices between $110 and $140. The stock is now at $97.25. Q1 2019 also saw a ~5% stake increase and that was followed with a similar increase this quarter.

United Continental Holdings (UAL): A minutely small 0.18% UAL position as of Q3 2016 saw a huge ~540% increase in Q4 2016 at prices between $52.50 and $76. 2018 had seen a ~22% selling at prices between $63 and $98. It currently goes for $19.92. This quarter also saw a minor increase.

Note: The entire ~8% of the business stake was disposed at ~$28 last month. This is compared to their overall cost-basis of ~$55 - lost around half their investment over a holding period of just over three years.

Stake Decreases:

Goldman Sachs (GS): GS is now a minutely small 0.17% of the portfolio stake. It was established in Q4 2013. Berkshire received $5B worth of warrants to buy GS stock during the financial crisis (October 2008) at a strike price of $115 (43.5M shares) that was to expire October 1, 2013. Buffett exercised the right before expiry to start this long position. Recent activity follows: Q3 2018 saw a ~40% stake increase at prices between $220 and $243 while last quarter there was a ~35% selling at prices between $197 and $232. This quarter saw another ~85% selling at prices between ~$135 and ~$250. GS currently trades at ~$172. Their overall cost-basis was ~$127 per share.

JPMorgan Chase (JPM: The ~3% JPM stake was established in Q3 2018 at prices between $104 and $119 and increased by ~40% next quarter at prices between $92 and $115. There was another ~20% stake increase in Q1 2019 at prices between $97 and $107. The stock currently trades at ~$86. There was a ~3% trimming this quarter.

DaVita Inc. (DVA): DVA is a 1.65% of the portfolio position that was aggressively built over several quarters in the 2012-13 timeframe at prices between $30 and $49. The stock currently trades at ~$79 compared to Berkshire’s overall cost-basis of ~$45 per share. This quarter saw minor trimming.

Note: Berkshire’s ownership stake in DaVita is ~30%.

Verisign Inc. (VRSN): VRSN was first purchased in Q4 2012 at prices between $34 and $49.50. The position was more than doubled in Q1 2013 at prices between $38 and $48. The buying continued till Q2 2014 at prices up to $63. The stock currently trades at ~$217 and the position is at 1.31% of the portfolio (~10% of the business). This quarter saw minor trimming.

Southwest Airlines (LUV): LUV is a ~1% portfolio stake purchased in Q4 2016 at prices between $38.50 and $51 and increased by ~10% in the following quarter at prices between $49.50 and $59. Q2 2018 saw another ~20% stake increase at prices between $50 and $57. The stock is now at ~$24.

Note: The entire ~10% of the business stake was disposed at ~$30 last month. This is compared to their overall cost-basis of ~$42 - lost ~30% of their investment over a holding period of just over three years.

General Motors (GM): GM is a 0.88% of the 13F portfolio position that was first purchased in Q1 2012 at prices between $21 and $30. By Q3 2017, the position size had increased by around six-times (10M shares to 60M shares). Q4 2017 saw a reduction: ~17% selling at prices between $40.50 and $46.50. There was a ~38% stake increase in Q4 2018 at prices between $30.50 and $38.50. The stock currently trades at $22.63. Overall, Berkshire’s cost-basis on GM is ~$32. Last quarter saw a ~3% stake increase while this quarter there was marginal trimming. Berkshire controls ~5.2% of the business.

Liberty SiriusXM Group (LSXMA) (LSXMK): The tracking stock was acquired as a result of Liberty Media’s recapitalization in April 2016. Shareholders received 1 share of Liberty SiriusXM Group, 0.25 shares of Liberty Media Group and 0.1 shares of Liberty Braves Group for each share held. Berkshire held 30M shares of Liberty Media for which he received the same amount of Liberty SiriusXM Group shares. There was a ~40% stake increase in Q2 2017 at a cost-basis of ~$40 per share and the stock is currently at $31.44. This quarter saw marginal trimming.

Note: LSXMA/LSXMK is trading at a significant NAV-discount to the parent’s (SIRI) valuation.

Amazon.com (AMZN): AMZN is a 0.59% of the portfolio stake established in Q1 2019 at prices between $1500 and $1820 and increased by ~11% next quarter at prices between $1693 and $1963. The stock currently trades at ~$2410. There was marginal trimming this quarter.

Sirius XM Holdings (SIRI): The 0.37% SIRI stake was purchased in Q4 2016 at prices between $4.08 and $4.61. Q2 2017 saw selling: ~20% reduction at prices between $4.70 and $5.50. The stock is currently at $5.34. This quarter saw minor trimming.

American Airlines (AAL): AAL stake was first purchased in Q3 2016. The original purchase was at prices between $28 and $39 and doubled in Q4 2016 at prices between $36.50 and $50. The stock is now at ~$9. There was a ~3% trimming in Q2 2018 and a similar reduction next quarter. Last two quarters saw minor trimming.

Note: The entire ~10% of the business stake was disposed at ~$11 last month. This is compared to their overall cost-basis of ~$40 - lost around 75% of their investment over a holding period of just over three years.

Liberty Global PLC (LBTYA) (LBTYK): The position was established in Q4 2013 at prices between $37.50 and $44.50 (adjusted for the 03/2014 stock-split) and increased in the following two quarters at prices between $38.50 and $46. The three quarters thru Q1 2016 had also seen a combined ~30% increase at prices between $30 and $50. Q2 2016 saw a ~17% further increase at prices between $27 and $39. The stock is now at $21.36 and the stake is at 0.25% of the 13F portfolio. This quarter saw marginal trimming.

Axalta Coating Systems (AXTA): AXTA is a small 0.24% of the portfolio stake established in Q2 2015 at prices between $28 and $36 and increased by ~16% the following quarter at prices between $24.50 and $33.50. The stock currently trades at $19.70. Berkshire owns ~10% of the business. This quarter saw marginal trimming.

Teva Pharmaceuticals (TEVA): TEVA is a very small 0.22% of the portfolio stake established in Q4 2017 at prices between $11.20 and $19.33 and more than doubled next quarter at prices between $16.50 and $22. The stock currently trades at $11.21. This quarter saw marginal trimming.

Synchrony Financial (SYF): SYF is a 0.18% of the portfolio position purchased in Q2 2017 at prices between $26.50 and $34.50 and increased by ~20% the following quarter at prices between $28.50 and $31.25. The stock is now at $16.54. This quarter saw a ~3% trimming.

Note: Synchrony is the private label credit-card business split-off from GE that started trading in August 2014 at ~$23 per share.

Suncor Energy (SU): The 0.13% SU stake was purchased in Q4 2018 at prices between $26 and $40. Last quarter saw a ~40% stake increase at prices between $29 and $33. The stock is now well below those ranges at ~$16. There was marginal trimming this quarter.

Note: Suncor Energy has had a roundtrip in the portfolio. It was a 0.48% position purchased in Q2 2013 at prices between $27 and $32. That stake was disposed during Q2 & Q3 2016 at prices between $25.50 and $29.

Biogen Inc. (BIIB) and Liberty LiLAC Group (LILA) (LILAK): These two minutely small positions (less than ~0.10% of the portfolio each) saw marginal trimming this quarter.

Kept Steady:

Apple Inc. (AAPL): AAPL is currently the largest 13F portfolio stake by far at ~36%. It was established in Q1 2016 at prices between $93 and $110 and increased by ~55% the following quarter at prices between $90 and $112. Q4 2016 saw another ~275% increase at prices between $106 and $118 and that was followed with a stake doubling in January 2017 at prices between $116 and $122. There was another ~23% increase in Q4 2017 at prices between $154 and $176 and that was followed with a ~45% increase in Q1 2018 at prices between $155 and $182. Since then, the activity has been minor. The stock currently trades at ~$308.

Note: Berkshire’s overall cost-basis on Apple is ~$141 per share. They have a ~5.6% ownership stake in the business.

Bank of America (BAC): Berkshire established this large (top three) ~11% of the portfolio position through the exercise of Bank of America warrants. The warrants had a strike price of $7.14 compared to the current price of $21.44. The cost to exercise was $5B and it was funded using the $5B in 6% preferred stock they held. There was a ~30% stake increase in Q3 2018 at prices between $27.75 and $31.80 and a marginal increase next quarter. Q2 2019 also saw a ~4% stake increase.

Note: Berkshire’s overall cost-basis is ~$13 and ownership stake is 10.7%.

American Express (AXP) and Coca Cola (KO): These two very large stakes were kept steady during the last ~6 years. Buffett has said these positions will be held “permanently”. Berkshire’s cost-basis on AXP and KO are at around $8.49 and $3.25 respectively and the ownership stakes are at ~17.6% and ~9.4% respectively.

Wells Fargo & Co. (WFC): WFC is Buffett’s fifth-largest stake at 5.28% of the 13F portfolio. It is a very long-term stake. Recent activity follows: last year saw a ~25% selling at prices between $43 and $55. Berkshire’s cost-basis is at ~$24.50 and their ownership stake is 8.4%. The stock currently trades at $23.36.

Kraft Heinz Co. (KHC): KHC is currently a fairly large position at 4.59% of the portfolio. Kraft Heinz started trading in July 2015 with Berkshire owning just over 325M shares (~27% of the business). The stake came about because of two transactions with 3G capital as partner: a ~$4B net investment in 2013 for half of Heinz and a ~$5B investment for the acquisition of Kraft Foods Group in early 2015. Berkshire’s cost-basis on KHC is ~$30 per share compared to the current price of $29.20.

Moody’s Inc. (MCO): MCO is a ~3% of the 13F portfolio stake. It is a very long-term position and Buffett’s cost basis is $10.05. The stock currently trades at ~$251. Berkshire controls ~13% of the business.

US Bancorp (USB): The 2.60% USB stake has been in the portfolio since 2006. The original position was tripled during the 2007-2009 timeframe. It was then kept relatively steady till Q2 2013 when ~17M shares were purchased at prices between $32 and $36. H1 2018 had seen a ~16% increase at prices between $49 and $58 and that was followed with a ~25% increase in Q3 2018 at prices between $50 and $55. The stock is now at $30.68 and Berkshire’s cost-basis is ~$38. They control ~10% of the business. Q4 2018 and Q2 2019 also saw minor increases.

Bank of New York Mellon Corp (BK): BK is a 1.53% of the 13F portfolio stake. The bulk of the original position was purchased in Q2 2012 at prices between $19.50 and $25. Recent activity follows: 2017 saw a ~180% increase at prices between $43.50 and $55 while 2018 saw another one-third increase at prices between $44.50 and $58.50. The stock currently trades at ~$32. Berkshire’s cost-basis on BK is ~$46 per share and ownership stake is ~10%. For investors attempting to follow, BK is a good option to consider for further research.

Charter Communications (CHTR): CHTR is a 1.35% of the portfolio position. It was established during the last three quarters of 2014 at prices between $118 and $170. In Q2 2015, the position was again increased by ~42% at prices between $168 and $193 and that was followed with another ~21% increase the following quarter at prices between $167 and $195. The stock currently trades at ~$503 compared to Berkshire’s cost-basis of ~$178. The six quarters thru Q4 2018 had seen a combined ~25% selling at prices between $250 and $395 and that was followed with a ~20% reduction in Q1 2019 at prices between $285 and $366. Q2 2019 also saw a ~5% trimming.

Occidental Petroleum (OXY) and RH Inc. (RH): These were the two new positions in Q3 2019. Both were increased last quarter. The 0.32% of the portfolio OXY stake was purchased at prices between $42 and $53 and increased by ~150% last quarter at prices between $37 and $44. The stock currently trades at ~$14. The 0.15% of the portfolio RH position was established at prices between $119 and $174 and increased by ~40% last quarter at prices between $165 and $242. It is now at ~$155. Berkshire controls ~9% of the business.

Note: Berkshire also has warrants to purchase 80M shares of OXY at $62.50 per share. That came about as part of a $10B funding deal (perpetual preferred stock with 8% annual dividend) done in May last year. The dividend was paid in common stock rather than cash last month.

Store Capital (STOR): The 0.19% STOR stake was established in Q2 2017 in a private placement transaction at $20.25 per share. The stock is now at $17.15.

StoneCo Ltd. (STNE): STNE is a 0.18% position purchased in Q4 2018 at ~$21 per share compared to the current price of ~$22.

Note: Berkshire has a ~11% ownership stake in StoneCo. In October 2018, WSJ reported that Berkshire had invested ~$300M each in two Fintech’s – India’s Paytm and Brazil’s StoneCo (STNE). The Paytm investment was made in August 2018 while the STNE purchase was following its IPO in October 2018.

Restaurant Brands International (QSR): QSR is a 0.19% of the 13F portfolio position established in Q4 2014 at prices between $35 and $42. The stock currently trades at $51.42. It started trading in December 2014 following a merger/rename transaction between Tim Hortons and Burger King Worldwide.

Note: Berkshire’s stake in the business is ~4.2%.

Costco Wholesale (COST), Globe Life (GL), Johnson & Johnson (JNJ), Mondelez International (MDLZ), M&T Bank (MTB), MasterCard Inc. (MA), Kroger Company (KR), Procter & Gamble (PG), SPDR S&P 500 Index (SPY), United Parcel Service (UPS), Vanguard S&P 500 Index (VOO), and Visa Inc. (V): These are very small positions (less than ~0.5% of the portfolio each) were kept steady this quarter.

Note 1: Since November 2015, Warren Buffett is known to own ~8% of Seritage Growth Properties (SRG) at a cost-basis of $36.50 in his personal portfolio. It currently trades at $6.92. SRG is an REIT spinoff from Sears that started trading in July 2015.

Note 2: Berkshire Hathaway also has a 225M share position in BYD Company at a cost-basis of ~$1 per share (~$2 per share in terms of ADRs – BYDDY). The ADR currently trades at $11.20.

The spreadsheet below highlights changes to Berkshire Hathaway’s 13F stock holdings in Q1 2020:

<<<

>>> Eight Stocks Give Warren Buffett A Headache (They're Not Airlines)

Investor's Business Daily

MATT KRANTZ

05/14/2020

https://www.investors.com/etfs-and-funds/sectors/sp500-stocks-give-warren-buffett-big-headache-they-are-not-airlines/?src=A00220&yptr=yahoo

Warren Buffett finally bailed out on S&P 500 airline stocks. But his portfolio is still full of stocks giving him giant headaches.

Berkshire Hathaway (BRKB) this year lost $1 billion or more, and at least 20%, on eight of its 47 U.S.-listed public holdings like financials Bank of America (BAC) and Wells Fargo (WFC) plus consumer staples stock Coca-Cola (KO). This is according to an Investor's Business Daily review of Buffett's latest holdings data from S&P Global Market Intelligence and MarketSmith. Only stocks primarily listed on U.S. exchanges were included.

Big losses in the famed Buffett portfolio persist even after he unloaded massive airline losers. And it's showing the dangers of chasing after value-priced stocks — the ones Buffett tends to prefer — in this coronavirus market. Learn how to find breakaway growth-stock winners instead on Leaderboard.

Shares of Berkshire Hathaway are down 22% just this year alone, dragged down by a host of lagging stocks. The S&P 500 is only down 13% and the growth-focused Nasdaq 100 is up 2.6%. Buffett alone lost $21.8 billion this year on his 16% stake in the company. No other top individual owner has lost anywhere near that much on an S&P 500 stock this year.

No wonder Berkshire just posted the largest-ever loss by an S&P 500 company.

Warren Buffett Snared By S&P 500 'Value Trap'

Much of Buffett's pain centers around his tilt toward S&P 500 value stocks. It's ironic as "cheap" stocks are supposed to offer safety in downturns with dividends and stability. But that's not happening in the coronavirus stock market.

The Vanguard Value ETF (VTV) is down a crushing 22% this year, nearly identical with Berkshire Hathaway's drop. But growth stocks are faring much better as they are showing more resilience in the coronavirus-inflicted world. The Vanguard Growth ETF (VTV) is down just 1.2% this year.

What's hurting the value stocks group? Exactly the kinds of stocks investors want nothing to do with in a pandemic.

S&P 500 Financials: Still A Pain Point

A trio of financials are now handing Berkshire Hathaway its biggest losses.

Berkshire Hathaway is down $13.6 billion just on one stock this year: Bank Of America. The bank's brutal 41% drop this year hurts as Berkshire Hathaway owns nearly 11% of the company. Wells Fargo is down even more: 58%. That's wiped nearly $11 billion from Berkshire's portfolio. And then there's American Express (AXP), off 37%, costing the portfolio nearly $7 billion.

Now that Buffett sold his airline stocks, the financials are Buffett's biggest problem. Six of Berkshire's worst eight losses are all financials. Savvy investors can actually make money betting against banks Buffett owns, like Wells Fargo.

Berkshire Hathaway holds 17 publicly traded financials. That's more than any other sector in the portfolio, says S&P Global Market Intelligence. And Berkshire Hathaway's public holdings in financial stocks account for a third of his portfolio. In contrast, the financials sector accounts for just 13% of the S&P 500 and just 19.5% of S&P 500 value indexes.

Being heavy on S&P 500 financials is a big drag for Buffett and other value investors. The Financial Select Sector SPDR ETF (XLF) is down 33% this year. That's the second-worst loss of the 11 sectors after only the energy sector's 40% wipeout. And that's saying something.

Not Even Coke Is Giving Buffett A Smile

Consumer staples are supposed to shine in recessions. Packaged foods gain popularity when money's tight. One 69-year-old actually scored more than $100 million on Campbell Soup stock this year. The Consumer Staples Select Sector SPDR ETF (XLP) is down this year 9.4%, holding up better than the S&P 500.

But no such luck with Buffett's favorite consumer staples stock: Coca-Cola. The beverage maker is down twice that of the sector, 21%, this year. Buffett owns 9% of the company so the drop bubbles into a $4.6 billion loss this year.

And unlike other consumer staples companies seeing bumps in their business, Coke's earnings are predicted to fall 11% this year, says S&P Global Market Intelligence. No wonder it sports a low 66 IBD Composite Rating. Compare that with the 99 Composite Rating of rival beverage maker, Monster Beverage (MNST), which is a growth stock. Monster shares are up 2.5% this year.

Certainly, value stocks might return to favor — one day. Large value stocks returned an average 10.37% annually since 1928, says Index Fund Advisors. That edges slightly past the 9.77% annualized gain of the S&P 500.

But do you and Buffett want to bet on them returning anytime soon?

Warren Buffett's Costliest Mistakes This Year

Most big losses are from S&P 500 financials

Company Ticker % Of Company Owned By Berkshire Sector YTD Stock % Ch. Berkshire's YTD Loss ($ Billion) Composite Rating

Bank of America (BAC) 10.9% Financials -40.7% $13.6 42

Wells Fargo (WFC) 8.4% Financials -58.1% $10.8 6

American Express (AXP) 18.8% Financials -37.3% $7.0 62

Coca-Cola (KO) 9.3% Consumer Staples -20.6% $4.6 66

U.S. Bancorp (USB) 10.0% Financials -50.3% $4.5 21

JPMorgan Chase (JPM) 2.0% Financials -39.7% $3.3 44

Bank of New York Mellon (BK) 10.0% Financials -35.4% $1.6 61

General Motors (GM) 5.2% Consumer Discretionary -41.4% $1.11 56

<<<

>>> Warren Buffett: Berkshire has dumped its airline stocks, 'world has changed' because of coronavirus

by Alexis Keenan

Yahoo Finance

May 2, 2020

https://finance.yahoo.com/news/warren-buffett-berkshire-has-dumped-all-of-its-airline-stocks-says-world-has-changed-001242589.html

Warren Buffett has gotten Berkshire Hathaway (BRK-A, BRK-B) out of the airline business.

During a virtual address to shareholders for the company’s annual shareholders meeting Saturday, the chairman and CEO called Berkshire’s recent purchase of roughly 10% of four of the world's largest airlines — including American (AAL), United (UAL), Delta (DAL) and Southwest (LUV) — an “understandable mistake.”

But the company has sold out of its entire interest in the airlines, worth at least $4 billion. In doing so, the Oracle of Omaha admitted to a rare investment misstep, one that’s he pinned on the coronavirus crisis hammering the global economy.

“The world changed for airlines,” the influential investor said at the meeting.

“It turned out that I was wrong about that business because of something that was not in any way the fault of four excellent CEOs,” Buffett said of COVID-19’s shock to air travel — adding that there was “no joy” in managing those companies right now.

“But the companies we bought were well managed. They did a lot of things right. It’s a very, very, very difficult business because you’re dealing with millions of people every day and if something goes wrong for 1% of them, they are very unhappy,” Buffett added.

Prior to stay at home orders put in place across the U.S. on March 1, the Transportation Safety Administration reported scanning nearly 2.3 million passengers, — a number consistent with the prior year’s approximate 2 million passengers, per day.

Yet fast forward to April 3, the agency scanned 129,763 passengers, and that number continues to decline. Buffett said he doubts whether the flying public, or even himself, will be willing to travel as frequently as they had by plane before the virus outbreak.

“People have been told not to fly. I’ve been told not to fly for a while. I’m looking forward to flying. I may not fly commercial but that’s another question,” Buffett remarked.

While he expressed hope that he could be wrong, Bufftett said the airline business changed in a major way, most obviously in the level of debt the companies will need to carry in order to stay alive.

The four companies will each need to borrow $10 to 12 billion, and in some cases will need to rely on stock sales, which will take away from their upside, he said.

“I don't know whether two or three years from now that as many people will fly as many passenger miles as they did last year, “ Buffett said. “They may and they may not, but the future is much less clear to me about how the business will turn out through absolutely no fault of the airlines themselves.”

<<<

Berkshire - >>> Everyone Needs To Calm Down About Buffett Being Quiet

Seeking Alpha

Apr. 20, 2020

https://seekingalpha.com/article/4338575-everyone-needs-to-calm-down-buffett-being-quiet

Summary

Recap what Buffett actually did during '08-'09 and expand upon the possible reasons why.

The really big move he made was actually buying the rest of Burlington Northern Santa Fe, which occurred in November '09.

Comparing BRK's balance sheet: cash as a percent of equity is twice as high now versus '08-'09.

Why I'm long BRK.B for the first time in my career: trading at the lowest P/BV and P/TBV ratios since the mid-90s.

Introduction:

Recently there has been a litany of articles asking the same essential question: why haven't we heard or seen anything from Warren Buffett investing in companies as we did back in the fall of 2008? In my mind, I always remember THE big move he made was in buying the rest of Burlington Northern Sante Fe [BNSF], announced in November of 2009. However, when I would point this out to people on FinTwit, the responses I received mostly listed off other famous moves he made during the fall of 2008 and ignored the magnitude of the BNSF deal that came later. For the first time in my investing career, I have long exposure to Berkshire Hathaway (BRK.B), so I decided to take a deeper look into comparing BRK's actions between then and now.

The Great Financial Crisis:

If you run a search for articles about the deals Buffett made during the Great Financial Crisis [GFC], then you'll turn up a number discussing his October 2008 preferred and warrants deal with Goldman Sachs (GS). You'll also find discussions mentioning his General Electric (GE) investment, also comprised of a preferred and warrants transaction. You might even find one like this referencing his investment in Swiss Re (OTCPK:SSREF) from March of 2009, which is rarer since it clearly isn't consequential to the 'Buy America' mythos that was attached to his actions, in large part due to his October 2008 Op-Ed in The New York Times. You'll even find articles declaring his preferred and warrant deal with Bank Of America (BAC), as his "Masterpiece" investment from this GFC period. That statement is interesting on its own since the BAC investment didn't even occur until the fall of 2011! Generally, though you don't see people refer to his acquisition of BNSF in anything close to the same light, and usually not at all.

Berkshire Hathaway Buys Out Burlington Northern for $26B - CBS NewsSource

One of the interesting things in researching this article is that the patterns of Buffett's style emerge clearly. Despite owning numerous businesses outright, we probably all fall victim to thinking of Buffett more as a traditional equities portfolio manager, than the leader of a financial and industrial conglomerate. Reviewing the actions he took during the GFC, I would separate these transactions into three bucket types: 1.) merger finance, 2.) distressed finance, 3.) business investment. Here's the list that I compiled with major transactions that occurred during this period:

The merger finance deals might be the most interesting because they often are sited as major moves made by Buffett during this period, but as you can see by the announcement dates, they were very early in the decline process of the market. You also see his propensity for doing preferred securities to reduce his risk profile, but it does remind me of how early on Merger Arbitrage was an important part of Buffett's investment strategy. Over time, the strategy became crowded out with more professionals employing it which narrowed the spreads. Now, Buffett has turned to financing mergers rather than just playing the price spread.

If Buffett started out the GFC period just by financing mergers, then you can clearly see in the chart above how that changed in the fall of 2008. The GS and GE deals were of the second type I mentioned, but interestingly they too occurred at a point that turned out to be early in the acceleration phase to the downside. Only the Swiss Re deal looks well timed in hindsight. What all three of those investments have in common are more than just preferred securities, either convertible to equity or attached with warrants. They are also all finance deals, and by that, I mean that these were companies that were all in trouble due to their financial leverage. In fact, I would argue that they were all effectively insolvent at this point. That's a discussion for another much longer article perhaps someday. I would add that I'd like everyone to consider not so much which firms failed, but why the few firms that survived were spared.

Buffett has been quiet so far, but right now Charlie Munger is talking about why BRK is going to wait and see. Here's a quote ascribed to Munger from this recent article:

"Warren wants to keep Berkshire safe for people who have 90% of their net worth invested in it. We're always going to be on the safe side. That doesn't mean we couldn't do something pretty aggressive or seize some opportunity. But basically we will be fairly conservative. And we'll emerge on the other side very strong."

All of those points should have been true in 2008 as well, but why did Buffett get active with three financial companies in the heart of the GFC? I like to say 'your answer here is probably your bias.' In my case, my bias is that I believed BRK itself was effectively insolvent too. Buffett's motive wasn't just about saving GS and GE, it was about saving BRK and its significant financial exposure through its GEICO unit as well. Years later Buffett himself provides the key clue in this interview in 2018:

What we all learned in that particular panic is that we're all dominoes. And we're all very close together.

Consider this concept when you think of that Op-Ed he wrote on October 16, 2008. Buffett is a master of presentation. He often has argued for higher ethical standards and board diversification in corporate America yet does little in this regard in his own backyard. Maybe I'm being too critical of him in this regard, but I personally value what people do over what they say. Bottom line, I think there's a compelling argument for why BRK made those financial investments in the heat of the GFC, and they had a lot more to do with BRK's own financial well being than just the opportunity to increase returns. If you think of it in this manner, then the reasons behind BRK's lack of action to date makes more sense. Essentially, it's not the same setup. Despite the severe economic declines we're all facing as a nation right now, the risk of a total financial system collapse is not comparable in my opinion. In pure numbers, the GDP impact will be worse in these quarters. However, back then the financial system was carrying magnitudes greater leverage than it is currently, and it was loaded with significantly inferior assets collateralized by collapsing real estate values. We were weeks away from complete societal collapse. The commercial paper market had essentially shut down. That's how grocery store shelves go empty. I have not had the same concerns this time despite the panic stocking behavior people have unfortunately succumbed too.

Comparing the GFC to our Current Period:

There were other investments than the ones I've mentioned so far in 2008. Buffett bought a stake in BYD Company Limited (OTCPK:BYDDF) in September of 2008. He also increased his exposure to USG Corporation (USG), but these were all in the 300 million type size outlays. I've tried to focus on the multi-billion dollar plus deals because that's the size that really moves the needle for a conglomerate the size of BRK. We also need to consider how BRK's balance sheet was entering the GFC and today's environment to fairly gauge their motives for the moves they have and haven't made.

In the above chart, I've added the cash, equity, and the level of industrial debt from BRK's balance sheet. When looking at those few items from the balance sheet, (yes, this is not all encompassing obviously), but in terms of the amount of cash as a percentage of total equity, BRK clearly has entered this period with considerably more of a safety net and flexibility than during the GFC. Only if we consider the level of net industrial debt/capital ratio does BRK's current standing look slightly inferior to back then. I chose to use only industrial debt versus the financial as well, because, to be honest, the complexity would require another article in itself. You can also see that the deal sizes as a percentage of cash tend to occur around similar levels.

Finally, of course, it should stand out massively that the BNSF deal was a galaxy in comparison to any of the others in terms of capital deployed. It effectively matched all of the other deals combined. He also received a lot of criticism for the deal at the time, with many suggesting he was overpaying for the railroad business. Below is a chart with the trailing EV/EBITDA multiples for the three remaining primary American freight railroad companies: CSX Corp. (CSX), Union Pacific Corp. (UNP), and Norfolk Southern Corp. (NSC). I've drawn in the approximate point of when BRK announced the acquisition. There were points in the future when the multiple went lower, but that was more to do with the growth in EBITDA than a reduction in the long term outlooks for the businesses. Point is that Buffett certainly did not pay any sort of a significant premium for this business, and now the market rewards these businesses with essentially a 50% greater multiple range.

In summary, it was the BNSF deal that deployed significantly greater capital resources than any of the other more heralded Buffett deals from that period. It was also made eight months after the low in the market of March 2009, and over a year after the financially distressed deals with GS and GE. In other words, give BRK some time before getting all upset about the lack of news. If history is a guide here, then we really shouldn't expect any business type acquisitions to be made until at least the end of this year or early 2021. That assumes that we're not making a new low in the future.

Summary & Valuation:

To conclude, I would argue that many of the deals Buffett made during the GFC were not done so for opportunity, but instead out of necessity. The real big business move was made by acquiring BNSF well after the lows had been made. Considering the greater financial flexibility that BRK has today versus then, Buffett is remaining quiet because he doesn't have to invest out of necessity. It also is nearly impossible to get valuable businesses not in distress to sell at these levels. The time to strike will likely be in the future after stocks have somewhat recovered, and everyone has a better sense of what the other side of the economic valley is going to look like.

At the start of this article, I also mentioned that for the first time ever in my investing career, I am a holder of BRK.B common stock. This is a complicated business with large exposures over various parts of the economy. I'm not going to go into a long summary of why I like this and that etc... Instead, I'd point the reader towards two key features: 1.) Yes, BRK has a lot of cash to deploy, and bluntly Buffett is often able to buy great businesses for less than other suitors. That's the benefit of just assimilating managements versus replacing them. You can often strike deals that cost shareholders less to complete in the near term. 2.) The price to book and tangible book values of BRK is at or below their respective lows since the mid-'90s.

Thus, the stock is trading cheaper on these all encompassing metrics than it did in the GFC when I have just argued that Buffett made those investments out of necessity to save his own business from financial collapse as well. If I'm not going to own it now, then I should just take the ticker off my screen.

I hope everyone is safe, healthy and happy out there.

<<<

Pearls of wisdom from the Oracle -