News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Absolutely correct…

https://www.prnewswire.com/news-releases/movano-health-submits-exemplary-sp02-clinical-trial-results-in-key-step-towards-fda-510k-clearance-decision-302140861.html

The sp02 imo, is not a big deal. Blood pressure would be, as it would capture every one’s interest from any gender. The blood oxygen is a big deal for anyone with a pulmonary issue or contracting flu like symptoms. During a pandemic it would be a serious helpful aid.

Other than people who have pulmonary issues with blood oxygen saturation, I don’t think right now is the reason to go out and buy this product.

The blood pressure measurement would be huge. According to MOVANO, they are years away from that achievement. Presently I can see the application being successful for women if the data is accurate.

I’m sure your comments come from personal experience and movano’s own admission of not being ready to roll out much larger demand. Looks like they have the resources to get their act together long term. But as for now their stock price is in the crapper.

I think that logic is being reflected in the trading.

1500 incidents. Makes one wonder what they have been doing for LL and the gang.

I completely disagree that Research posts are annoying. They are what LQMT has led them to be. I don’t even view them as pessimistic. Just factual. I’m a long term holder as well. But let’s be real here people. They really don’t do much of anything. But there is potential for them to or we all would t be here.

Movano also launched a medical division within the company. With the hope of getting FDA thumbs up. But they can’t even deliver on the minuscule orders they’ve received so far. Still has sold out splashed on their hope page

You're very welcome, but I would prefer to share the profits!

Excellent post. Now we know why LQMT is in there predicament. It’s not their fault and had no choice. It was made for them.

I don’t feel too dumb now. No one saw this coming. Just when things were beginning to look good too.

The integrity of management at LQMT looks better now.

This should help….

https://insidepublicaccounting.com/ipa-top-500-firms/

I have a few other tickers who also reported the same predicament with Borgers. Here is one we all recognize.

https://www.msn.com/en-us/money/companies/the-sec-charges-trump-medias-newly-hired-auditing-firm-with-massive-fraud/ar-AA1o7cZx

Thank you for sharing your post of the 8K no one but you, brought up today.

O.T. Check out VZ stock 6% + in dividends.

I'm considering the alternative " Earn 5.00% APY* with a 5-month CD."

It doesn’t fit a pumper or hyper’s narrative…

https://liquidmetal.gcs-web.com/node/12016/html

So you fire first and then look for a certified accounting firm???

Whose brainchild idea was that? Does it matter?

Let’s give them more stock options.

Still think the share price can’t drop further.

I have to admit like all of the other management debacles, i never saw this coming.

Good luck to all in LQMT

Wish tc luck.

What a mess! !!

Gives me the impression that LQMT wants to shake the tree to see how much fruit falls off of the tree that floats.

Pack of Wolves going Board to Board singing their Playbook to create sellers. 22 Yrs Big Deal... becasue you bought 22 years too early? or because nobody really knows how many decades it takes to jumpstart new, eventual Trillion Dollar Innovations / Industries..... How long did Plastics take Wolve # 9 ?

I’m just curious. Between the bickering, I thought there would be some mention of the 8K report just filed that Liquidmetal no longer has an accounting firm. In addition, no first-quarter report will be filed until the new firm is adopted.

https://liquidmetal.gcs-web.com/node/12016/html

As a result of the dismissal of BF Borgers under the preceding SEC Order, the Company is in the process of engaging another Accounting Firm. Until the Company has engaged another Accounting Firm, the Company may not be able to file its financial results for the first quarter ended March 31, 2024, as well as other future SEC filings, on a timely basis. The Company shall work expeditiously to engage another Accounting Firm and go through the financial review process to ensure timely filings of SEC reports.

That's an understatement. So what was your handle in your past life on Ihub?

I can tell you from experience you come here just being born and you act like you know it all already.

I call your BS...It's been 22 years since the IPO and your estimates boggle any sane mind

Apple releasing today new products. At some point as tech advances the chances of liquid metal the company manufacturing some components goes up.

What about pencil pro?

https://www.msn.com/en-us/news/other/everything-announced-at-apple-ipad-event-oled-screens-m4-chip-pencil-pro-and-more/ar-BB1lYCz8

I call your BS...It's been 22 years since the IPO and your estimates boggle any sane mind

That might be difficult for him because he has consistently cut and posted the same boring inexperienced post about startup technologies...at least five times now.

Please add me to your Ignore list if you haven’t already.

We all know what kind if drivel all my posts are.

You haven't driveled on me yet.

okpj

Please add me to your Ignore list if you haven’t already.

We all know what kind if drivel all my posts are.

Last year around this time LQMT reported $30,000.00 in revenues from sales of all products for the first quarter.

The bar is set very low. I’m hoping LQMT can triple that this quarter.

Good luck to all in LQMT.

Wish TC luck.

Amazing how many less posts I have to go through now with my new "ignoring someone" status.

okpj

Another industry that is growing is the Smart lock industry. Currently grossing over $2.5 billion and projected to reach $10 billion by the year 2030. These locks do not fail solely due to power loss. They require repetitive mechanical movement. There are more than one manufacturer making smart locks. Enough for LQMT sales reps to explore to see if the larger companies want to invest in a prototype. A longer lasting lock would be far more competitive. There are varyious studies as to how long these locks last. A good R&D expert could prove the value for using LQMT’s IP.

Think pinions zero lubricants etc.

Time for LQMT to step up.

Good luck to all in LQMT

Wish TC luck.

A recently new use of an old material becomes a new competitor.

https://www.xometry.com/resources/materials/what-is-pla/

https://www.sciencedirect.com/science/article/pii/S0022286024007634

As an example: ConMed now uses PLA. Medical screws. It took about ten years to develop.

Its time LQMT stepped up.

Good luck to all in LQMT.

Wish TC luck.

that would be one wild swing.

i doubt this goes to infinity. and i doubt we see zero.

even half way to heaven then back half way to hell.

it would be some nice movement for a change.

the macro trend is seeing the return of manufacturing to the usa.

china is imploding while many big usa companies are packing their china bags for home sweet home.

this is right up our alley. maybe this rising tide will lift our boat.

This kills me!! Signature bank in the last 12 months. .03 to $3.25!!

Tomcat

I will be hiking and out of range. This would be a PERFECT time for LQMT to up to infinity, then down to zero.

Tomcat

Another week passes and LQMT’s share price is down 0.75% from 0.062 cents to 0.0615 cents on extremely weak trading volumes and little interest. The same when LQMT moves up or down.

LQMT has released no updates on progress.

Another boring week.

LQMT is now into its 28th consecutive month without a new contract announcement for the order of parts.

Share price is holding in the low pennies. In the 0.06’s right now. The walk back down is usually slow after a run up.

As stated a gazillion times: with anemic trading volumes the share price means BUBKIS!

Perhaps in 2025 or 2026 LQMT might succeed and if they ever do make it in 2024, all in it will be very thankful and glad that they did.

FOMO lives and is probably the main reason why anyone holds on regardless of any other opinion at this time. Not wanting to take a loss at this point may be another.

I try to present a balanced view based on the facts not on the emotions of anyone hyping or bashing LQMT. I believe I nailed it correctly. This board has had it correct past and present from potential to expectations to hope to FOMO.

Unfortunately LQMT can still hit the 02’s. Not my wish. The performance of LQMT will decide that.

No matter what anyone’s views are for LQMT going forward. The fundamentals have not changed.

There is potential for a contract announcement to correct the southerly direction LQMT has been heading for the past seven years. If anyone is looking to earn some lunch money, this year could be the time to be in LQMT.

There doesn’t seem to be much enthusiasm for the upcoming 10Q1 within two weeks. Just like the recent 10K.

There is also the cloud surrounding the ring and LQMT. Perhaps either company might be able to break through those clouds with a little sunshine.

Would be nice to see an announcement for a high volume reoccurring order again. Could send LQMT up. Way up depending on the contract terms. I hope whatever the contract terms are, they will be better than the ones LQMT usually settles for.

My bet is on one present and one former executive who hold at least 1 million shares and I’m not talking about LL, regardless of how low the SP goes.

Will this be the year revenues increase consistently? Only the 2nd, 3D, and 4th Q’s will tell. I’ll be pleasantly surprised if the 1st Q tics up.

Good luck to all in LQMT.

Wish TC luck.

CEO, Tony Chung, painted a rosy picture for LQMT this year during his CC, for all in LQMT. Especially for outside shareholders, I hope his picture this time, is worth more than just a thousand words to make our shares worth more than just three, four, five or six cents.

I have reluctantly put someone on "ignore" here for the first time. Despite some information that at times might seem valuable, I simply have had it.

Good luck to everyone.

I continue to be long with 565,000 shares, which were once over 1 million. But I am not giving up. I know the risk, and I don't need to hear repeatedly about the risks, and the negatives, that all of us here already know.

okpj

One year is definitely no big deal....

OK No problem...

4 Years gearing up for a 25 Million or 50 Million Dollar 1st order would not be uncommon.

Hey Taggingalong:

Would you, or might you be so kind to put at least one paragraph break in your posts. I like your posts, but they are always one HUGE blog of words, and I often find it hard to WANT to read them, even though I like your content.

Just a layout suggestion, even though I don't have a monopoly on the truth, unlike other posters, who post what I don't want to read, but find easier TO look at and THEN read.

Just my two cents.

Thank you,

okpj

Maybe we get a surprise early or middle of next week.

One year ago…

https://media.starrag.com/en-us/frontend/media-item/detail?id=145

Good luck to all in LQMT.

Wish TC luck.

Four years ago…

https://vimeo.com/438967135

Good luck to all in LQMT.

Wish TC luck.

Maybe think about it being a learning experience for yourself versus spewing nonsense and trying to get others to sell .... because essentially 98% of your posts are to encourage investors to sell.. Just watch and learn instead of keep spewing your ridiculous weekly saga's that are a huge joke with a situation like LQMT.

I don't post much, but I have to agree that I can't understand why Research, etc. posts. YOU (not tagalong) are annoying. Why do you insist on annoying people?

okpj

Your problem is that you are very ignorant when it comes to pioneering efforts and how many ingredients have to be in sync for the Large Scale Rollouts to begin. And again a great majority of the time it is delays and blunders caused by the early adopters who 'don't know they don't know' and have to find out for themselves thru trial and error.... And there is always so many variables in motion and colliding etc.... But as things start getting in alignment the Whale customers / early adopters start seeing the big picture and all it takes is one large rollout out and stockholders can easily see 10x / 20x your money so maybe watch and learn instead of bitch, or maybe I will watch it go down further but as long as they keep their mouth shut without spewing a bunch of nonsense then I will lean towards them having their aces lined up. If you had any sense at all you would absolutely know that your Weakly Updates are an extremely humorous indication of how little you know about pioneering new innovations... Innovators that keep their mouth shut are not out to screw people..... It is the nature of the beast .... because they have so much leverage in the things they know and have learned and for the protection of their 'early adopter customer bases' they are quietly building that they do not want to share with the world .... Maybe think about it being a learning experience for yourself versus spewing nonsense and trying to get others to sell .... because essentially 98% of your posts are to encourage investors to sell.. Just watch and learn instead of keep spewing your ridiculous weekly saga's that are a huge joke with a situation like LQMT.

Back to the nickels this morning less than 10 thousand shares trading in the midst.

Where are those huge orders?

Good luck to all in LQMT.

Wish TC luck.

A year over year update can be found in the LQMT 10K. You are not doing your DD. If I have the time I will do a comparison.

Regarding the rest of your enthusiasm. I would if LQMT traded once a year too. I agree and I’m not the first to say it. But LQMT is a boring stock to watch.

Here’s to the break out!

I think you are on to something, save all your posts for an update once a year. We would all enjoy a year over year update. Looking forward to your post May 1st 2025. Goodbye until then.

We are close to a break out, mark it down.

But again, your only purpose is to try to confuse and misrepresent things whenever possible. Why don't you just move along in your gameplan and show a chart comparison of LQMT against Amazon each day...... and then you could surely bitch about LQMT not being anywhere near where Amazon is.... That would really get to the point and show everyone how smart you are....

For Almost, Today LQMT YOY CLOSED DOWN 7.75%

For the only one who has claimed to have communications with the former CEO, LL, now Chairman of The Board.

You can thank me again anytime.

I’ll update it after the close just in case you want to review it with the chairman LL. He still talks to you via email, right?

Just for you as of now LQMT is down-14%-YOY.

Enjoy your perpetual lqmt lotto ticket and stop P*ssing on it every day. We are all in this, believing that the ticket will one day pay off.

|

Followers

|

887

|

Posters

|

|

|

Posts (Today)

|

8

|

Posts (Total)

|

232579

|

|

Created

|

04/30/05

|

Type

|

Free

|

| Moderators PatentGuy1 Almosthere | |||

Liquidmetal® Technologies (ISO 9001:2008 certified) is a leading force in the research, development and commercialization of amorphous metals. Our revolutionary class of patented alloys and processes form the basis of high performance materials in a broad range of medical, military, consumer, industrial, and sporting goods products.

Discovered by researchers at the California Institute of Technology, Liquidmetal alloys’ unique atomic structure enables applications to achieve performance and accuracy levels that have not been possible before. The revolutionary class of patented materials technology redefine performance and design paradigms institutionalized by traditional materials.

As Liquidmetal Technologies controls the intellectual property rights with more than 70 U.S. patents, these high performance materials are dramatically changing the way companies develop new products.

LINKS

Featured: Automotive Pressure Sensors, 9.36 billion market by 2020

1. LiquidMetal Website

2. LiquidMetal Manufacturing Facility

3. OTC Market Report

4. Engel Liquidmetal Forum (Nov 2015)

5. ENGEL Symposium 2015

6. ENGEL Interview on Liquidmetal

PATENTS (USPTO)

1. Search Crucible Intellectual (Apple and LiquidMetal R&D)

2. Search Apple and LiquidMetal

3. Search Cross-license Patents w/Eontec

4. Search Vitreloy

5. Search Pre-grant Patents

VIDEOS

1. OMEGA Liquidmetal Bezel

2. ENGEL e-motion 110T

3. Liquidmetal Bouncing Ball

CORPORATE GOVERNANCE - BOARD OF DIRECTORS

Professor Lugee Li, Chairman

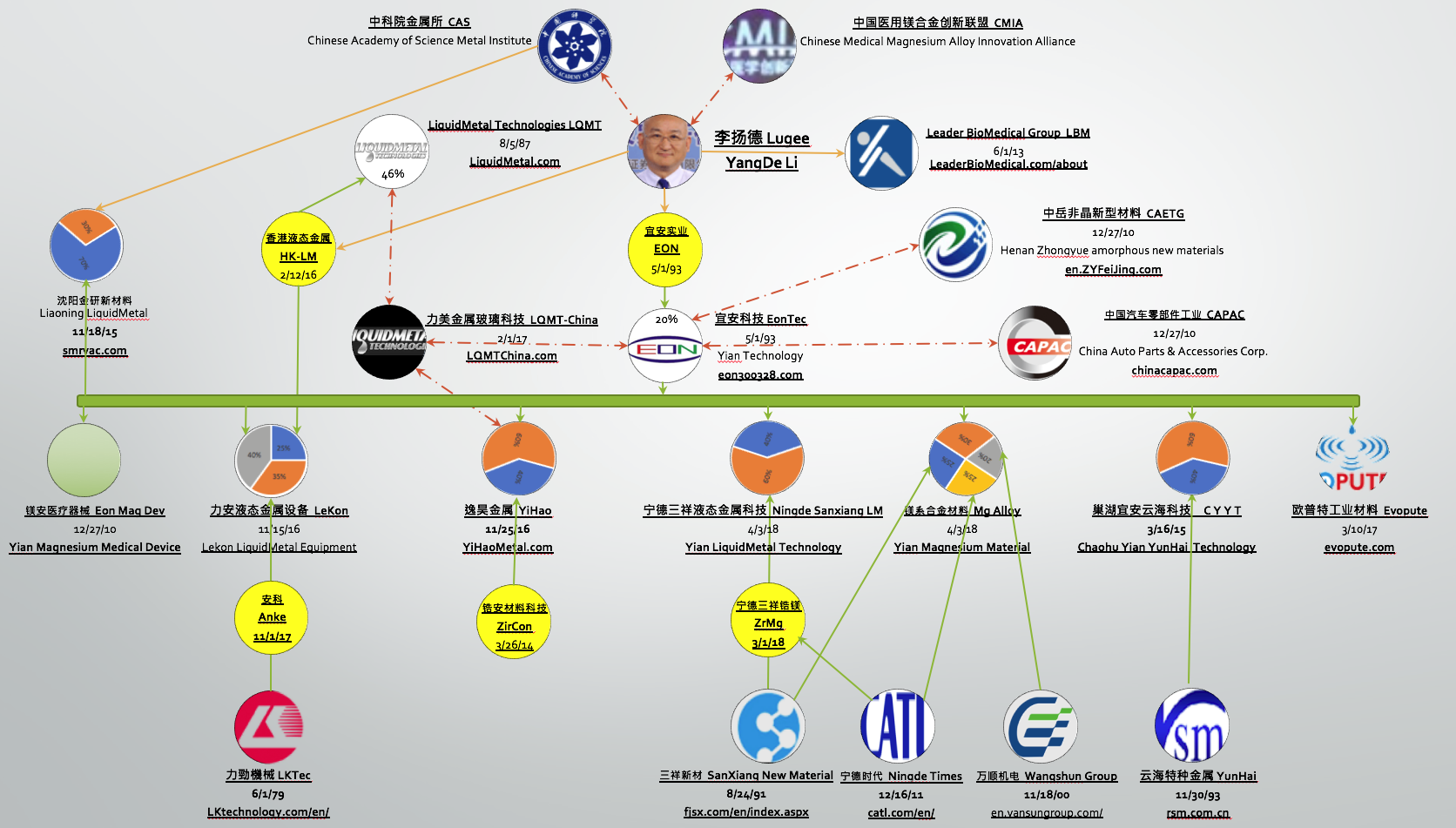

Professor Li was appointed as a member of our board of directors in March 2016 and became Chairman of our board of directors in October 2016. Professor Li is the founder, Chairman, and majority stockholder of DongGuan Eontec Co. Ltd., a Hong Kong company listed on the Shenzen Stock Exchange engaged in the production of precision die-cast products and the research and development of new materials. Professor Li founded Eontec in 1993 and has served as Chairman since that date. At Eontec, Professor Li is responsible for strategic development and research and development. Professor Li is also the founder and sole shareholder of Leader Biomedical Limited, a Hong Kong company engaged in the supply of biomaterials and surgical implants. Professor Li serves as an analyst for the Institute of Metal Research at the Chinese Academy of Sciences and serves part-time as a professor at several universities in China.

Abdi Mahamedi, Vice Chairman

Abdi Mahamedi has served on our board of directors since May 2009 and became Vice-Chairman of our board of directors in October 2016. Since 1987, Mr. Mahamedi has served as the President and Chief Executive Officer of Carlyle Development Group of Companies (“CDG”), which develops and manages residential and commercial properties in the United States on behalf of investors worldwide. At CDG, Mr. Mahamedi evaluates and supervises all of the investment activities and management personnel. Prior to joining CDG, Mr. Mahamedi founded Emanuel Land Company, a subsidiary of Emanuel & Company, a Wall Street investment banking firm, and served as a managing director for Emanuel Land Company from 1986 to 1987. In 1983, Mr. Mahamedi received his B.S.E. degree in Civil and Structural Engineering from the University of Pennsylvania, and in 1984 he received his M.S.E. degree in Civil and Structural Engineering from the University of Pennsylvania.

Isaac Bresnick

Currently serves as Legal and Regulatory Affairs Director for the Leader Biomedical Group, a private company based in Hong Kong and operating from Amsterdam, the Netherlands, and has served in that role since October 2014. At Leader Biomedical, Mr. Bresnick is responsible for the direction and management of legal affairs, regulatory affairs, quality control, and quality assurance, as well as for advising executive management of Group companies. Mr. Bresnick also currently serves as Director of AAP Joints GmbH, a private company in Berlin, Germany, and has served in that role since July 2013. Mr. Bresnick received his J.D. from the University of Connecticut School of Law in 2013, and his B.S. in Industrial Design from the University of Bridgeport in 2008. After completion of his undergraduate studies and continuing through his enrollment at UCONN Law, Mr. Bresnick worked as Senior Arrangements Designer for Electric Boat Corporation, a subsidiary of General Dynamics, from June 2008 to December 2012.

Vincent Carrubba

An experienced corporate leader and serial entrepreneur with extensive senior executive, technical and manufacturing experience. Mr. Carrubba has created and guided new products to success in the consumer goods, electronics, automotive and construction industries and has conceptualized, financed and built factories and developed new manufacturing technologies throughout Asia. From September 2014 through the present, Mr. Carrubba has served as the CEO of Admiral Composite Technologies Inc. (“Admiral”), where he has developed new technologies for environmentally responsible and innovative building materials which represent Admiral’s product lines. Mr. Carrubba has also served as Admiral’s Chairman since its inception in 2009. From September 2014 through the present, Mr. Carrubba has served as the CEO of Asia Sourcing & Communications USA Inc. and he has served as its Chairman since its inception in 2013. From 2002 through August 2014, Mr. Carrubba served as the Director of R&D for Interdynamics Inc., IDQ Holdings, where he was responsible for all R&D and QC matters, including the management of engineering, legal, patenting, regulatory, insurance and consumer relations matters. From 1989 through 1992, Mr. Carrubba designed and installed the New York Stock Exchange telecommunications and information technology systems. Mr. Carrubba has held engineering and executive positions with Xerox, General Electric, Bristol-Meyers Squibb and AT&T and he is the inventor of several patents related to telecommunications, professional tools and consumer products. Mr. Carrubba received a Bachelor of Arts degree in Engineering Science and a Bachelor of Science Degree in Mechanical Engineering from Columbia University SEAS in 1982.

Tony Chung

Mr. Chung was appointed to our board of directors in August 2017. Mr. Chung had previously served as the Company’s Chief Financial Officer from December 2008. Prior to joining the Company, Mr. Chung served as CFO at BETEK Corporation, a real estate and investment subsidiary of SK Engineering and Construction, and as CFO of Solarcity, a company providing advanced solar technology and installation services. Mr. Chung is a Certified Public Accountant and served eight years at KPMG as an Audit and Consulting Manager for several large multinational companies. He received his B.S. degree in Business Administration from the University of California, Berkeley. Mr. Chung is also an Attorney at Law and received his J.D. degree from Pacific Coast University School of Law.

| Reporting Status | U.S. Reporting: SEC Reporting |

| Audited Financials | Audited |

| Latest Report | August 4, 2020 10Q |

| CIK | 0001141240 |

| Fiscal Year End | 12/31 |

| OTC Marketplace | OTCQB |

| Market Value1 | $129,851,894 | a/o Sep 24, 2020 | |

| Authorized Shares | 1,100,000,000 | a/o Dec 31, 2016 | |

| Outstanding Shares | 914,449,957 | a/o Sep 24, 2020 | |

| -Restricted | Not Available | ||

| -Unrestricted | Not Available | ||

| Held at DTC | Not Available | ||

| Float | 487,690,350 | a/o Dec 31, 2017 | |

| Par Value | No Par Value |

| Shareholders of Record | 217 | a/o Dec 31, 2017 |

| Volume | |

| Day Range: | |

| Bid Price | |

| Ask Price | |

| Last Trade Time: |