News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

A folding MacBook seems to be in the works for late 2025 early 2026. Supposedly a year ahead of schedule. Amphenol is said to be dealing with the hinge.

That’s FOMO. And it’s real.

If I had sold out and switched companies LQMT would be at the $4 price while Signature Bank still be in the pennies.

It's the way the cookie crumbles everytime.

"LQMT increased revenues from parts sold five fold from last year’s 10Q1. In terms of reality that’s about five times the annual salary of a fast food service employee in many states across America. In terms of income, that is less than a fast food service employee’s salary, when divided by the employees on the books of LQMT." Priceless, thank you for putting things into perspective.

>"I try to present a balanced view based on the facts not on the emotions of anyone hyping or bashing LQMT. I believe I nailed it correctly. This board has had it correct past and present from potential to expectations to hope to FOMO.<" You DO NOT try to present a balanced view based on the facts... You repeatedly and intentionally try to paint a biased picture based either on your agenda or your lack of understanding of the difference between a small company involved in a hugely disruptive pioneering effort and a start-up company (as you labeled them) that you essentially portray as a reseller of squirt guns or some other commodity type scenario.... That is what the Weekly update TRYS ITS BEST TO PORTRAY and yet after 6,000 posts you already knew this after your very first post... It is a clear agenda to get others disgruntled and speaks volumes about your efforts to try your best to create sellers....

Another week passes and LQMT’s share price is down 3.79% from 0.058 cents to 0.0558 cents on extremely weak trading volumes and little interest. The same when LQMT moves up or down. LQMT is down 7% YOY.

LQMT released their 10Q this week as noted and posted by jamengual and Monroe1 on this board.

LQMT increased revenues from parts sold five fold from last year’s 10Q1. In terms of reality that’s about five times the annual salary of a fast food service employee in many states across America. In terms of income, that is less than a fast food service employee’s salary, when divided by the employees on the books of LQMT.

The bottom line! The income from parts is still not enough to pay for the salaries of LQMT employees.

Let’s see if LQMT can announce contracts and continue to increase quarterly revenues on steady basis to increase interest, volumes, liquidity and drive demand so the SP can increase five fold too, this year. 0.25 cents may not be anyone’s goal for LQMT. But it sure would put a smile on everyone’s face, while waiting.

It’s a very sad state of affairs, when LQMT executives can’t update shareholders on the website blog as to what’s going on. Crap that has nothing to do with NDA’s or anything else that requires silence. Just a bunch of lazy arse executives imo, not keeping shareholders up to date on what is going on.

In a post a week ago I posted this:

“Transparency is long overdue. It may cost too much to release a PR. But it costs very little for an executive blog comment to update all shareholders. When was the last communication of executive commentary made on the LQMT executive blog? Anyone?

Wasn’t that the purpose of the blog as stated in a PR?”

LQMT is now into its 29th consecutive month without a new contract announcement for the order of parts.

Share price is holding in the low pennies. Now holding in the mid 0.05’s. The walk back down is usually slow after a run up.

As stated a gazillion times: with anemic trading volumes the share price means BUBKIS!

Perhaps in 2025 or 2026 LQMT might succeed and if they ever do make it in 2024, all in it will be very thankful and glad that they did.

FOMO lives and is probably the main reason why anyone holds on regardless of any other opinion at this time. Not wanting to take a loss at this point may be another.

I try to present a balanced view based on the facts not on the emotions of anyone hyping or bashing LQMT. I believe I nailed it correctly. This board has had it correct past and present from potential to expectations to hope to FOMO.

Unfortunately LQMT can still hit the 02’s. Not my wish. The performance of LQMT will decide that.

No matter what anyone’s views are for LQMT going forward. The fundamentals have not changed.

There is potential for a contract announcement to correct the southerly direction LQMT has been heading for the past seven years. If anyone is looking to earn some lunch money, this year could be the time to be in LQMT. The potential I speak of is based on the commentary from TC.

There is also the cloud surrounding the ring and LQMT. Perhaps either company might be able to break through those clouds with a little sunshine.

Recently Movano shed some light last week and iterated what they have already stated their plans were for this year and beyond. A relaunch of B2C and a possible new launch of B2B this year.

LQMT has stated at least for the 10Q1, they are still in the game with consecutive quarters showing income from the ring company.

Right now the news released from both companies may help the sun to shine again in both LQMT and Movano during the next two quarters.

Would be nice to see an announcement for a high volume reoccurring order again. Could send LQMT up. Way up depending on the contract terms. I hope whatever the contract terms are, they will be better than the ones LQMT usually settles for.

My bet is on one present and one former executive who hold at least 1 million shares and I’m not talking about LL, regardless of how low the SP goes.

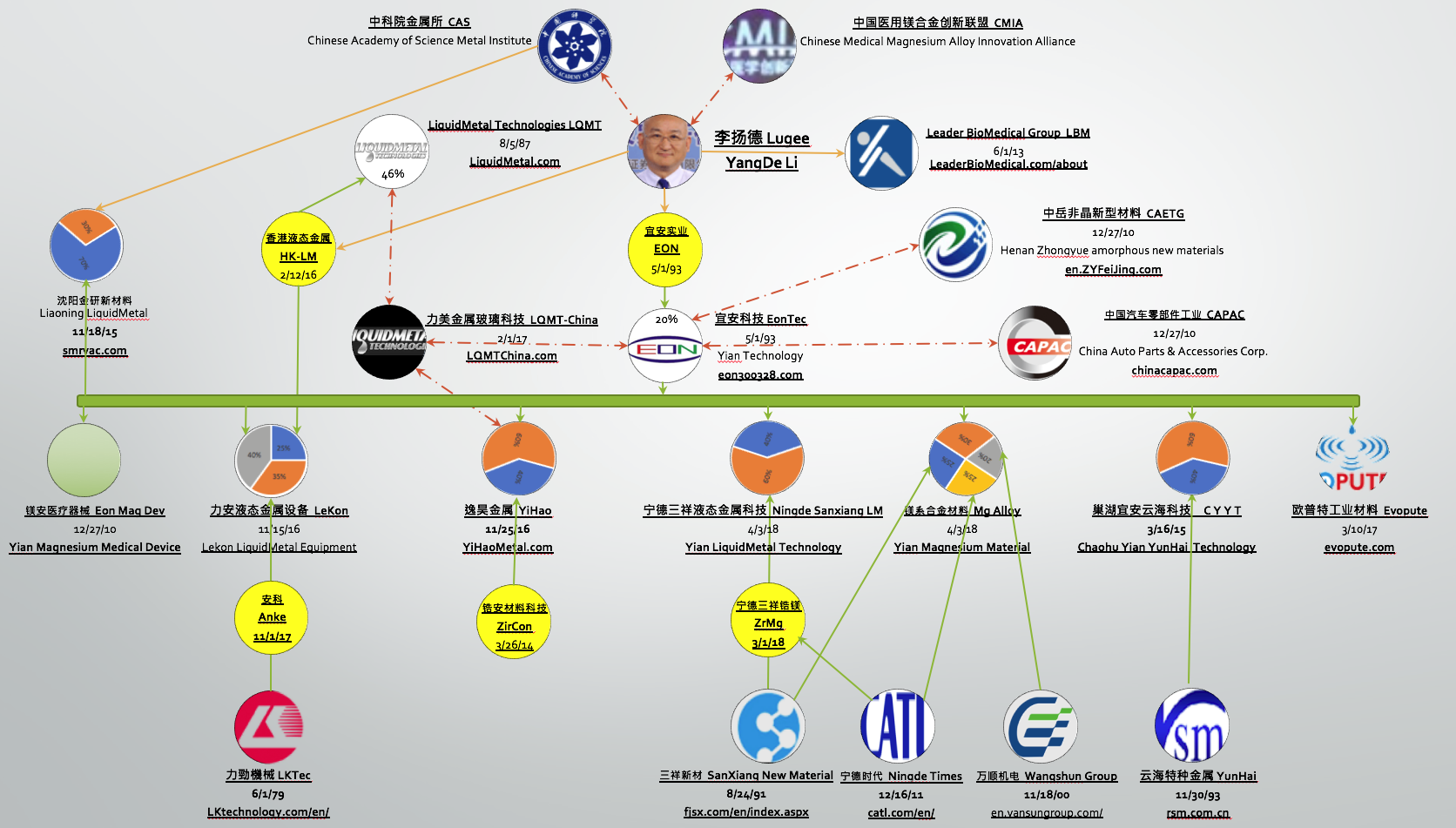

Around the globe LQMT’s partner abroad, Yian technologies, has reported continued success in manufacturing CE products such as the foldable screen and auto. Not so much in medical. Increased investment in Yian technologies has increased. And Eontec has increased sales in 2023 YOY to $165 million dollars. What they sold to achieve those sales remains a mystery as the numbers and integrity of the data cannot be verified.

Will this be the year revenues increase consistently? Only the 2nd, 3D, and 4th Q’s will tell. I’ll be pleasantly surprised if the 1st Q tics up.

Good luck to all in LQMT.

Wish TC luck.

CEO, Tony Chung, painted a rosy picture for LQMT this year during his CC, for all in LQMT. Especially for outside shareholders, I hope his picture this time, is worth more than just a thousand words to make our shares worth more than just three, four, or five cents. So far his artwork is not worth much more than last year and it’s beginning to decline in value again.

Why am I not surprised?

Good one Jay... You beat me to it and said it better than I would have...

This post is so disingenuous and a perfect example of why so many question your motives. Just like how you threw out there that all these other BMG companies are doing so much and leaving LQMT behind. I called you out on that and got a typical deflection. So please, for the good of all here, please elaborate on what portion of Eon's business is related to Liquidmetal vs all the other things they do, and have been doing for a very long time.

You also know very well there is only one parallel licensing agreement with Eon. Another intentionally misleading portion of your post and a well established pattern.

Ever since the new millenniums were born into the 21st century, this thing can go either way. Read posts 232672 and 232681.

It’s still a crapshoot and anyone should only bet what they can afford to lose.

Like an executive of LQMT once said, this can be a one off, where one contract can make a company.

Good luck.

I’ve been putting this on the sidelines for the past 6 months or so … has anything changed or is this still dead in the water? Appreciate any updates, I only hold a small position so it’s not a huge deal, but considering adding. Thank you!

Don’t quote me. I’m no expert on China’s currency, but I think Eontec, you know the one LQMT has had all of those parallel agreements with, has grossed $165 million dollars about 1.2 billion yuan. Last year.

That’s a lot of product sales. Just what the heck are they selling?

Now of course I can’t vouch for the article’s integrity. But those were the numbers.

TC, you were a part of that deal too. Perhaps you can shed some light. While you are at it. What is all of that expansion yian technology is doing with Liquidmetal in auto, consumer electronics etc., and increased $$$$ investment being clamored about?

Don’t you think LQMT shareholders should be apprised of the success of your partners abroad too? After all there are some very astute shareholders who do believe there is a strong correlation between the success of partnerships abroad.and LQMT.

Good luck to all in LQMT.

Wish TC luck.

A little more transparency might help. You think?

Put the blog to more use. What the heck. As long as you’re using and giving credit to some of the video and pictures from your partners abroad on the USA website. Would it not be a good thing to keep your shareholders apprised of what is going on with them abroad as well?

No NDA’s involved either. And they are not even competitors.

Then again, what the heck do I know? Not much.

Not only that. You could have bought LQMT back for a penny less.

What happened?

Don’t tell me it was FOMO.

If Only ...

If only I had sold LQMT and bot Signature bank (SBNY) at .03 per share! Look at SBNY now! $3.90. Unbelievable!

- Tomcat

I think those options could well turn into money, if and when LL and the CCP decide for their reasons, to make it happen. So yeah, it is a gamble, but the motives are pretty twisted.

The recorded performance is definitely consistent with those in the space that are doing their best to advance a new very innovative material with lots of advantages over others.... Amazon was essentially 'Distribution pioneering' but very, very simple pioneering compared to a new material ..... and it took Amazon about 2 decades to start getting good traction etc .... and a new material has to be at least 1,000 times more difficult than a business template innovation such as what Amazon built ... Building innovative Distribution Systems, Infrastructure and Capacity etc as a business model is pretty logical and straight-forward compared to creating a new innovative material. In order to be fair we have to put things in perspective by being educated first ....... versus just making outrageous assumptions that have no basis... Probably the best comparison we can use is the Plastics Industry.

So then those options are just a bonus and will never be a windfall most would expect. Makes a lot of sense if the high for the stock will be about 0.15 cents.

Ah jeez, we are down to a few bright informed people that can't/won't agree. Out of boredom, I would suggest. So I will weigh in too. FYI. who is 'they'? I know you are thinking in the classic sense of management of a publicly held company focused on paying it's shareholders.

I do not see that here at all, which is utterly consistent with the recorded performance of the company. "They", in my view, is LL and CCP, whose interests in acquiring the use of the brand and the IP and sitting on this company, are inconsistent with your best interests and mine. Given what has happened since 2016, and where LQMT sits today, I don't know how anyone could ignore that likelihood . Put another way, LQMT Valencia has circled the wagons and has the Chairman, the BoD, the CEO, and enough votes to do whatever they want. Paying you and me may not be on top of the list.

Come on Research.... he did a little bit of good research and just posted it ... Give him credit where credit is due....

If that is your view, which it seems to be, then you should have felt your forehead every day for not selling LQMT the day you bought it and every day since.

I don’t post on the stocks or funds. Joined the board in 2006 did not post until I saw some potential about 10 years later. This is the only penny stock I have and it was my pick against advisors advice.

And I try not to post on anything else other than LQMT and not on the BS you just posted, which has absolutely nothing to do with LQMT.

If you want to gossip just buy yourself a rocking chair and some knitting yarn.

Absolutely hilarious….I don’t enjoy having capital tied up for 10 years but you talk of 20 years waiting for LNG exports to come to fruition….that’s 1/3 of an adult life……speechless.

No pain. Just foresight. You lost your point of discussion about red, back and green.

Stay focused.

LQMT does not need to achieve profitability to rocket up the share price.

What you stated was 1+1=2 and 2+2=3. And if operating costs are kept in check profitability will be achieved. Now who in their right mind would disagree with your statement on achieving profitability? No one.

But profitability in numbers, where the revenues equate to $2 or $3 million In totality does very little for the share price. If you listen to the CC, TC was not talking about breaking $10 million in revenues or $5 million in revenues. Seeing green at 2 to 3 million dollars does zip for LQMT, even if they exceed the costs to operate.

Without future potential for many moderate contracts the endeavor to commercialize Liquidmetal remains buried in the abyss.

I can only guess, not based on history, but on foresight, that those options and TC’s purchase of shares is an indicator of higher sales and the beginning to commercialize Liquidmetal. At that point being in the green will have meaning. But even in the red the share price can rocket up on potential proof that LQMT can grow.

Not having contracts, not having real demand for LQMT’s Liquidmetal fo 29 months now is not exactly the way to achieve that goal.

It is hoped by all outside shareholders that perhaps this year like other years can be the start of that goal. Success!

There is no pain in watching a $4 dollar a share in LNG and later higher break $100 dollars a share. Just as there is no pain in seeing LQMT do as much or more.

It’s a dice roll, a hunch, a bet, and for two decades it hasn’t done very well. But going forward they still have a shot at it. That’s all it is. Yes they have made quite a few major mistakes. Perhaps now they can move forward and distance themselves from those painful mistakes that cost the company to sacrifice to stay in business. Perhaps now they have found a formula to climb out of the abyss instead of digging themselves and everyone in it another hole.

I may comment every now and then on the BS,

But my main focus is always on LQMT and wanting them to succeed. It’s not my fault if the way they operate and thier numbers don’t l

Seems it is either those looking to get cheaper and cheaper shares that devote this much time to the 'Full-Time posting Job' or those heavily invested in competing industries (threatended by the new innovations) ........ that are motivated enough to spend decades 24/7 making 4,000+ posts per stock urging others that it must be a scam, looks scary.. not up to par, can't be legit... blah, blah, blah..... What a way to spend your life...

Good one Jay21... More dots connected to wake up some others..

HMMMM....owned LNG longer than LQMT, yet not one single post ever on that board? Why the daily dedication to this perpetual lottery ticket loser but not any other stock or message board? 4600+ posts about this one though.....🤔

Wow…that’s a lot of capacity for pain! Cheniere was a long term bet on the US exporting natural gas when the terminals didn’t exist and there were very few LNG capable ships….Encana had a similar plan for exporting from BC to Japan and I was in that one. Nice ideas but it took the Ukraine war to the take the Russians out and make it happen.

Wow…that’s a lot of capacity for pain! Cheniere was a long term bet on the US exporting natural gas when the terminals didn’t exist and there were very few LNG capable ships….Encana had a similar plan for exporting from BC to Japan and I was in that one. Nice ideas but it took the Ukraine war to create the motivation.

Absolutely a very narrow minded opinion and absolutely incorrect as it applies to the growth of a company’s share price!

A company can be in the red and still rocket up to the moon!

For example:

I have owned for a long time Cheniere Energy, longer than LQMT. LNG is but one example. It was the potential for years that rocketed the share price up despite a billion in losses and annually in the red. Only recently has Cheniere Energy, entered profitability. I bought LNG way back when T. Boone Pickens was alive and offering advice.

That same potential can apply to LQMT if they ever get contracts to increase both growth in revenues, potential and operating costs. The real potential yet to be realized will be the factor that raises the share price. Breaking even on a few bucks or going into the green on the same minuscule amounts of a couple $million won’t do squat for LQMT.

Revenues of $40 million from moderate to large contracts with expenses of $45 million will! I don’t think at that point the price would be sitting at a nickel!

A whale contract would be a one off, where most long term shareholders would say goodbye.

At today’s revenues breaking even or seeing green would only increase the length of time for cash burn to run out. It will not increase the share price to where long term shareholders want it to go.

Of course I could be wrong again. Far be it from me to ever know what I am talking about.

In order to go from losing money to making money, one must go through the breakeven point. Fact of life.

Breaking even does not a $1.00 dollar make. Nor does it get the SP to even 0.50 cents.

Im good with continuing quarterly growth and larger contracts to where potential for commercializing Liquidmetal becomes a reality. Even if the costs to achieve it increases.

At that point the idea of a whale is less important. Whenever or if ever that ever happens that too will be welcomed.

I’m not good with breaking even as a one off. It does nothing for the SP and is another BS distraction from a goal to do better and succeed.

It is a round about admission of wait another year.

Until a break out order if it ever comes from the new ring large enough for a 8K announcement or a new contract with another company is announced the SP will not rise.

Notice the extremely low bar that was set for LQMT to break and even in an earlier post I stated imo, revenues of $500 thousand for a quarter would not be sufficient to move the SP up.

Now take a look at the income from all sources: $587,000 for the quarter. But as you point out the bulk of that income is from other sources, investments and rent totaling $434,000.00 dollars.

Meaning although product revenues increased over 5 fold and is very good. It is still abysmal for enticing new shareholders and the fact that no 8K has been announced adds more uncertainty that future orders from the the ring company are certain. Zero admission of a reoccurring contract due to the fact that the ring company does not have all of its ducks lined up.

Aside from that , zero communications from TC & Co., and no new contracts going into it’s 29th month is not to appealing for enticing any new speculative shareholders. In fact imo, it is keeping them away and the volumes anemic.

It may be a good strategy long term, but short term it has and will drive the SP lower.

These opinions are backed up by the facts of LQMT’s way of operating. Whether that is their intent or not, the end results are what they are as the share price walks back down very slowly.

It is another reason why I say the SP means nothing, be it at 0.02 cents or a dime.

Contracts = real interest and not interest on investments.

Good luck to you.

There is a difference between “ breaking even for the year” and “reaching breakeven by the end of the year”. The former would be great but the later may be what we get and I’m good with that as long as we start another income stream.

Breaking even is more a matter of reducing expenses and having lease/interest income than operational sale of product/royalty income, so far. Just $600K to break even is a whim....which should drive the price up nevertheless.

Off the top of my head, which doesn't mean much. LQMT is about $600,000 from breaking even for the year if income and expenses remain the same. Good but no cigar. New roll out of the ring can help make it happen as well as other endeavors mentioned in the CC.

Good luck to all in LQMT.

Wish TC luck.

For those answers, 1 (949) 635-2100

Big questions…..Is part of this total tooling? How any units are driving this $143k? ? Dollars per ring?

Overall good news …maybe better than I xpected.

$143,000 from part orders pertaining to the ring.

Appreciated, thank you.

And these prices "today" are 2013 when the article was written! Pre-covid pre-bidenomics!!

I used to drink in a bar called the Wooden Nickel. It was not the one mentioned here in the article.

An ice cold mug of beer was .50 centavos and there were better bargains in town. It was also a time

when most waited until 5 pm to take their first slug, but most assuredly, "it's got to be 5 o'clock somewhere"!!

I agree with your points of view 100%.

What today’s share price could buy you back in time.

What would a nickel buy?

Scroll down…

https://restaurant-ingthroughhistory.com/2013/07/31/what-would-a-nickel-buy/

No matter how many 'Early Adopter' companies you are working with ....... NONE of them wants any type of publicity or any bits and pieces released on what they are up to (especially since it can affect relationships with existing suppliers etc) ........ so it is pretty much always going to be like this until something is permitted to be released by the Buyer .... But that is also why the price can jump up pretty good bit when there is news .... Probably another frustrating thing to LQMT is that every time there is some type of new finding or advancement etc... they owe it to the customers to advise them ....... even customers that might have been in the process of pulling the trigger on an initial order .... Customers have nothing to loose by waiting and being sure since they already have a current supplier...

This ship was born and communist China took it for $65 million. Duh...

This is not JUST a Start-Up Company. You need to learn what you are talking about when you so effortlessly reduce the magnitude of what is actually happening when new Multi-Billion and/or Trillion Dollar Innovations / industries are in the process of being borne ...

That would mean there has to have been some kind of advancement and there has not.

However, in my opinion it would behoove the company to at least produce some general statements that indicates advancement is taking place on a somewhat regular update basis.

There are great opinions here in this ticker and most grounded in common sense which is one reason I stay fairly current. Thankfully I am not overextended

in my holdings. Seems we have a Mexican standoff of sorts happening for quite some time because of management tight lips. Why?

Unlike the plastics revolution and other innovations throughout history, I cannot think of another product that encountered such stagnancy that also was held back by international political concerns of the magnitude we witness today especially with an election coming soon that could change the sendero by a large magnitude. Probably quite a few over time because of international intrigue. (save the killing of hemp/jute sails/ropes by England who controlled the southern cotton market] [planned obsolescence]. Liquid metal amorphous tech has far reaching and very intriguing properties and attributes within the realm of defense and space uses. I daresay that there are developments continuing that cannot be divulged in these realms. Also, the need for business silence whilst products/processes are in development is good and rudimentary business policy. Handing over to competition your game plan is a sure way to bankruptcy. So what of the areas of development like the Evie ring and others that fall into the safe area for disclosure? So this may indicate it is still early in process...not what shareholders like to hear...yes, we are an impatient breed.

However, in my opinion it would behoove the company to at least produce some general statements that indicates advancement is taking place on a somewhat regular update basis. So what gives? Is there slow silent accumulation going on?

I can understand not going short when at any moment a PR could rocket the pps. I can understand the lack of aggressive buying. I can understand then the Mexican standoff situation... i think. But I cannot understand the almost complete muffling that has continued for so long unless management is just clueless or completely tech nerdy with little to no management skills. What say you?

This is not JUST a Start-Up Company. You need to learn what you are talking about when you so effortlessly reduce the magnitude of what is actually happening when new Multi-Billion and/or Trillion Dollar Innovations / industries are in the process of being borne ... Again compare it to the plastics industry and how long it took to finally roll out. This is no different... A few decades is quite normal and you continue to confuse that you (and all of us also) may have bought 20 years early but that does not mean in the least bit that LQMT or any others in this space are incompetent etc... It is the nature of the beat if you just learn a little bit about what is actually involved in pioneering efforts especially something of this magnitude.... Since you are so smart why not offer your services to LQMT and then you will really understand how little you know...

Like many start up companies, this one acting out more like a motor vehicle stalled out In traffic waiting for a tow truck to pull it off the road for twenty years to be fixed, need only to increase the potential by commercializing the IP and inking an order with a high value name brand company. They can do it in auto, medical and industrial products. LQMT does not have to sign millions of dollars in deals to get there. Once they can successfully succeed in commercializing their ip in smaller projects the marketing of the Liquidmetal brand will market itself. Both demand and hype will take care of the rest. It has worked for many companies, where market analysts over value a company’s real potential. Like a poster here recently used a word “parabolic”.

It happened at the ipo it almost happened with the LQMT/Apple debacle but not quite with the take over from China via LL.

The real problem here are the ages of those holding long term. It is why most will sell at much lower prices. Time is not on the side of most long term shareholders. And of management…I think you already stated it clearly in your opinion.

Now that said. I don’t think LL or China invested $64 million to gross $500,000.00 annually from LQMT. Or a few million in China from the same IP.

|

Followers

|

884

|

Posters

|

|

|

Posts (Today)

|

2

|

Posts (Total)

|

233328

|

|

Created

|

04/30/05

|

Type

|

Free

|

| Moderators PatentGuy1 Almosthere | |||

Liquidmetal® Technologies (ISO 9001:2008 certified) is a leading force in the research, development and commercialization of amorphous metals. Our revolutionary class of patented alloys and processes form the basis of high performance materials in a broad range of medical, military, consumer, industrial, and sporting goods products.

Discovered by researchers at the California Institute of Technology, Liquidmetal alloys’ unique atomic structure enables applications to achieve performance and accuracy levels that have not been possible before. The revolutionary class of patented materials technology redefine performance and design paradigms institutionalized by traditional materials.

As Liquidmetal Technologies controls the intellectual property rights with more than 70 U.S. patents, these high performance materials are dramatically changing the way companies develop new products.

LINKS

Featured: Automotive Pressure Sensors, 9.36 billion market by 2020

1. LiquidMetal Website

2. LiquidMetal Manufacturing Facility

3. OTC Market Report

4. Engel Liquidmetal Forum (Nov 2015)

5. ENGEL Symposium 2015

6. ENGEL Interview on Liquidmetal

PATENTS (USPTO)

1. Search Crucible Intellectual (Apple and LiquidMetal R&D)

2. Search Apple and LiquidMetal

3. Search Cross-license Patents w/Eontec

4. Search Vitreloy

5. Search Pre-grant Patents

VIDEOS

1. OMEGA Liquidmetal Bezel

2. ENGEL e-motion 110T

3. Liquidmetal Bouncing Ball

CORPORATE GOVERNANCE - BOARD OF DIRECTORS

Professor Lugee Li, Chairman

Professor Li was appointed as a member of our board of directors in March 2016 and became Chairman of our board of directors in October 2016. Professor Li is the founder, Chairman, and majority stockholder of DongGuan Eontec Co. Ltd., a Hong Kong company listed on the Shenzen Stock Exchange engaged in the production of precision die-cast products and the research and development of new materials. Professor Li founded Eontec in 1993 and has served as Chairman since that date. At Eontec, Professor Li is responsible for strategic development and research and development. Professor Li is also the founder and sole shareholder of Leader Biomedical Limited, a Hong Kong company engaged in the supply of biomaterials and surgical implants. Professor Li serves as an analyst for the Institute of Metal Research at the Chinese Academy of Sciences and serves part-time as a professor at several universities in China.

Abdi Mahamedi, Vice Chairman

Abdi Mahamedi has served on our board of directors since May 2009 and became Vice-Chairman of our board of directors in October 2016. Since 1987, Mr. Mahamedi has served as the President and Chief Executive Officer of Carlyle Development Group of Companies (“CDG”), which develops and manages residential and commercial properties in the United States on behalf of investors worldwide. At CDG, Mr. Mahamedi evaluates and supervises all of the investment activities and management personnel. Prior to joining CDG, Mr. Mahamedi founded Emanuel Land Company, a subsidiary of Emanuel & Company, a Wall Street investment banking firm, and served as a managing director for Emanuel Land Company from 1986 to 1987. In 1983, Mr. Mahamedi received his B.S.E. degree in Civil and Structural Engineering from the University of Pennsylvania, and in 1984 he received his M.S.E. degree in Civil and Structural Engineering from the University of Pennsylvania.

Isaac Bresnick

Currently serves as Legal and Regulatory Affairs Director for the Leader Biomedical Group, a private company based in Hong Kong and operating from Amsterdam, the Netherlands, and has served in that role since October 2014. At Leader Biomedical, Mr. Bresnick is responsible for the direction and management of legal affairs, regulatory affairs, quality control, and quality assurance, as well as for advising executive management of Group companies. Mr. Bresnick also currently serves as Director of AAP Joints GmbH, a private company in Berlin, Germany, and has served in that role since July 2013. Mr. Bresnick received his J.D. from the University of Connecticut School of Law in 2013, and his B.S. in Industrial Design from the University of Bridgeport in 2008. After completion of his undergraduate studies and continuing through his enrollment at UCONN Law, Mr. Bresnick worked as Senior Arrangements Designer for Electric Boat Corporation, a subsidiary of General Dynamics, from June 2008 to December 2012.

Vincent Carrubba

An experienced corporate leader and serial entrepreneur with extensive senior executive, technical and manufacturing experience. Mr. Carrubba has created and guided new products to success in the consumer goods, electronics, automotive and construction industries and has conceptualized, financed and built factories and developed new manufacturing technologies throughout Asia. From September 2014 through the present, Mr. Carrubba has served as the CEO of Admiral Composite Technologies Inc. (“Admiral”), where he has developed new technologies for environmentally responsible and innovative building materials which represent Admiral’s product lines. Mr. Carrubba has also served as Admiral’s Chairman since its inception in 2009. From September 2014 through the present, Mr. Carrubba has served as the CEO of Asia Sourcing & Communications USA Inc. and he has served as its Chairman since its inception in 2013. From 2002 through August 2014, Mr. Carrubba served as the Director of R&D for Interdynamics Inc., IDQ Holdings, where he was responsible for all R&D and QC matters, including the management of engineering, legal, patenting, regulatory, insurance and consumer relations matters. From 1989 through 1992, Mr. Carrubba designed and installed the New York Stock Exchange telecommunications and information technology systems. Mr. Carrubba has held engineering and executive positions with Xerox, General Electric, Bristol-Meyers Squibb and AT&T and he is the inventor of several patents related to telecommunications, professional tools and consumer products. Mr. Carrubba received a Bachelor of Arts degree in Engineering Science and a Bachelor of Science Degree in Mechanical Engineering from Columbia University SEAS in 1982.

Tony Chung

Mr. Chung was appointed to our board of directors in August 2017. Mr. Chung had previously served as the Company’s Chief Financial Officer from December 2008. Prior to joining the Company, Mr. Chung served as CFO at BETEK Corporation, a real estate and investment subsidiary of SK Engineering and Construction, and as CFO of Solarcity, a company providing advanced solar technology and installation services. Mr. Chung is a Certified Public Accountant and served eight years at KPMG as an Audit and Consulting Manager for several large multinational companies. He received his B.S. degree in Business Administration from the University of California, Berkeley. Mr. Chung is also an Attorney at Law and received his J.D. degree from Pacific Coast University School of Law.

| Reporting Status | U.S. Reporting: SEC Reporting |

| Audited Financials | Audited |

| Latest Report | August 4, 2020 10Q |

| CIK | 0001141240 |

| Fiscal Year End | 12/31 |

| OTC Marketplace | OTCQB |

| Market Value1 | $129,851,894 | a/o Sep 24, 2020 | |

| Authorized Shares | 1,100,000,000 | a/o Dec 31, 2016 | |

| Outstanding Shares | 914,449,957 | a/o Sep 24, 2020 | |

| -Restricted | Not Available | ||

| -Unrestricted | Not Available | ||

| Held at DTC | Not Available | ||

| Float | 487,690,350 | a/o Dec 31, 2017 | |

| Par Value | No Par Value |

| Shareholders of Record | 217 | a/o Dec 31, 2017 |

| Volume | |

| Day Range: | |

| Bid Price | |

| Ask Price | |

| Last Trade Time: |