News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

I don’t think Jtrader has a clue what he is talking about.

I saw that projection the guy made on Twitter. He based his profits off of gross margin of 7% totally forgetting (or maybe it was intentional) that there were additional operating expenses below the gross profit line which resulted in a hefty net loss for the quarter.

Which makes all his projections irrelevant.

The only reason the company’s revenues increased dramatically was that they changed their business . They do sales and installation now versus just doing sales. Frankly the gross profit on sales alone was almost the same as installation which begs the question of the need to take on all this debt to achieve the same profit ?

Now if only Bobby answered the actual questions asked of him on Twitter

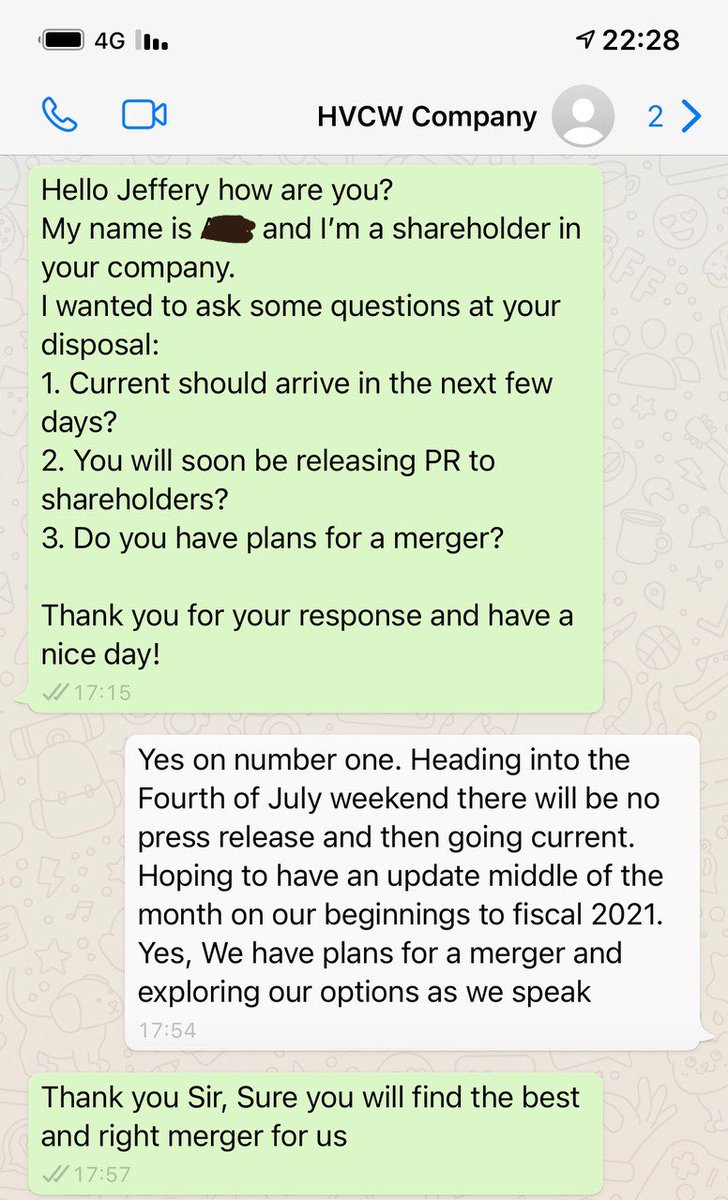

$hvcw 50b is an error - was leftover from the initial filing. Will be changed to reflect the new price.

— Bobby Tetsch (@bobby_tetsch) November 30, 2022

Courtesy of $HVCW ??J Trader?? i'd projected even higher

@JTrader444

$HVCW Updated fair market value??

I suspect revenue and profit margin to increase from here as initial growth made the last quarter margin very low. I would also predict dilution/debt conversion to stop in the coming few months.

Patience pays??

[-chart]pbs.twimg.com/media/Fi2T2OdXkAA3YXh?format=jpg&name=large[/chart]

mine are higher

Bobby T and this shit show need to get their act together

$hvcw 50b is an error - was leftover from the initial filing. Will be changed to reflect the new price.

— Bobby Tetsch (@bobby_tetsch) November 30, 2022

Will never run again, dead stock. No one trusts them. See ya wouldn't wanna be ya.

Get to buy 1s soon. Diluting all the way down it looks like.

They have their owns costs of doing business. It’s not like they are buying shells for free. They have to sit on these shells for years and sort out messes and take care of quarterly and annual filings which could add up to big dollars thru use of consultants and lawyers. Then they also have to wait several more years after shell is purchased to get all their investment out. I’m sure they have cash flow issues too from time to time.

For every successful RM they do there are failures like ABVG that just become a money pit.

They have very thick skin and seem to know what works and what doesn’t at this point in their careers.

dudes are not stupid if they could milk the sysmet for decades and not get caught...I understand your point

You can question their ethics all you want but the fact remains that they have apparently operated just within the confines of the law.

Their tweets are opinions rather than statements of facts although the supposed merger of one brothers family entertainment center into NECA at the beginning of this year was likely designed to keep interest levels in the stock/shell up while they were vetting real potential buyers.

there has to be somebody knowing someone at SEC to arrest these crooks...there cant be stealing money for 2 decades without anyone noticing

you and your brothers could really get BLAS PAUL OTCN OTCX INTL to take a vacation or something...havent you steal enough money throughout the years

If you subtract the Deferred Revenues from Liabilities, you must

also subtract A/R from Assets since they go hand in hand.

The company is still left with negative equity because they have borrowed so much money from various last resort lenders. Hopefully cash flow can keep up with the weekly repayments.

Assets = Liabilties + owners equity

Not hedging comments but analyzing their reports.

I’m not stopping you or anyone from investing. It’s your money and your choice. Go for if you think you are right.

What I am saying is that this is not the slam dunk everybody is trying to make it out to be.

It’s the way the OTC works. Most every active story stock is promoted by followers as the “best of breed” and “we know what we own” and “best CEO in the OTC” amongst other superlatives.

I say otherwise. Especially when it comes to Canouse reverse merger companies. I know Bobby T is a good salesman but even good salesmen can make bad deals when they desperately need money and banks won’t loan to them.

As usual, it’s now wait and see ….

$9M Deferred revenue is in the liability. A customer needs to have average 777 FICO score before MPS even works on the project. Sounds safe.

Assets and liabilities balance, if off by six million then the accountant did something wrong or liabilities were carried forward from a previous period.

A negative net worth isn't proper accounting.

The problem with saving the world is you should be relatively sure before speaking, but tiger is always hedging his comments just in case he is wrong. Many of his comments are uncertain and things he doesn't know for certain. So he drives buyers away without being sure

Tiger you sound smart and logical, but I can't buy/sell off your comments that really are uncertain.

Like saying we can't know for two more quarters. Which shows you don't know for certain now. .0001 or .0015. Ceo seems to be saying .0015, which is fair. .0001 is too low for the valuation.

I once tried to save the world by warning newer shareholders about the potential pitfalls of a stock they were all in love with.

It went down about 70% then in about 6 months I looked at a chart and it had gone up 10,000% with no RS.

I felt like a real asshole

Everybody is pointing to $13.8 million in assets, yet nobody is mentioning the $20.1 million in liabilities.

The company has negative net worth of $6.3 million which means at this point it is worthless , even though the stock is trading at .0005 . Even the notes on the financials say the company is worth less than zero per share.

No wonder why this stock has to get pumped so heavily. Banks won’t lend the company money and they have to rely on lenders at loan shark rates (to offset the risk) and the company’s real hope is that they can find enough “speculators” to give them money for free in exchange for shares in the Reg A.

Current shareholders will be sacrificed for the sake of future shareholders. I just don’t see it at .0015 but who knows. At .0001 they raise that $5 million immediately….it all comes down to just how bad they need the money.

That is insane growth in only 3 months (June 22-Sept 22)‼️😮

— 〽️Dawg (@Paul_Allen720) November 29, 2022

+$13.5 Milly assets!

+$16 Milly Revenue!

And at .0005/6

NO 🧠 er here! 🤪

💰💰💰💰💰 $HVCW

Modern Pro Solutions, aka $HVCW aka @bobby_tetsch 💎‼️💰💰💰 #solarpower https://t.co/thXb6bcQom

— 〽️Dawg (@Paul_Allen720) November 29, 2022

It’s all falling into place $HVCW! https://t.co/0ssNgaWuBd

— Waka Stocka Flame (@rod_harrell) November 29, 2022

revs worth more than assets $HVCW just in https://t.co/ratwg0pWjT

— mickster (@campin_robert) November 29, 2022

it will not copy

[chart]https://t.co/2QpKCJ09ZY]

[-chart]https://t.co/2QpKCJ09ZY] https://t.co/v5HkdZPt44

revs worth more than assets $HVCW just in https://www.otcmarkets.com/otcapi/company/financial-report/353746/content

it will not copy

[-chart]pbs.twimg.com/media/FiwbvBnWIAwcGxA?format=jpg&name=900x900[/chart]

just up $HVCW PUBLISH DATE TITLE PERIOD END DATE STATUS

11/29/2022 Attorney Letter with Respect to Current Information - Attorney Letter with Respect to Current Information 09/30/2022 A

https://www.otcmarkets.com/stock/HVCW/disclosure

reading yes on $HVCW revs 100mil or more , what is real worth ?????

look what we have , pps could jump 100 fold wit right words from bobby &

Pacific Energy (doing business as Modern Pro Solutions) finalized and closed on the Merger Agreement.

"We believe there is a lot of opportunity in front of us and being public will help us maximize those opportunities for the benefit of the shareholders", stated Bobby Tetsch, CEO of HVCW.

Pacific Energy Network (dba Modern Pro Solutions) is a California based parent company of several subsidiary LLC's that manage solar, roofing, HVAC, security, distribution, consulting, lead generation, marketing, sales, data, software and mortgage divisions.

Founded in 2016, PEN has quickly become one of the largest and most successful home services companies in the nation with a footprint across multiple states. With a focus on customer satisfaction and strategic business planning, PEN has grown into a multi-product business that has increased revenue year over year and expanded its reach into new markets across the United States.

For further information, please visit the Modern Pro Solutions website at

http://www.joinmps.com.

yes i did review of share structure below Authorized Shares 25,000,000,000 was 5,000,000,000 2021 & was 6,564,838,949 2022

11/09/2022

Outstanding Shares 7,704,701,400 was 3,001,563,774 2021 & was 6,564,838,949 2022

11/09/2022

but we have ah wit value over 100x's our pps closing today.

HVCW

Bid: 0.0004 Ask: 0.0006 Last: 0.0005 Chg ($): 0.00 Vol: 253.56M

in my review of share structure since 2021 increase in O/S to Outstanding Shares 7,704,701,400 was 3,001,563,774 2021 & was 6,564,838,949 2022

i say rather bullish because of company insertion $$$$$ WORTH ?????

Modern Pro Solutions Founder, Bobby Tetsch, Wins 2 Awards at the 2022 Spirit of the Entrepreneur AwardsPress Release | 11/18/2022

HVCW Announces the Merger with Pacific Energy NetworkPress Release | 08/11/2022

https://www.otcmarkets.com/stock/HVCW/news

i did review of share structure $HVCW share structure 2021 08-21-21 vs 2022 07-08-22 & 11-28-22 dilution A.S.25,000,000,000 was 5,000,000,000 2021

https://www.otcmarkets.com/stock/HVCW/security

HVCW SECURITY DETAILS

Share Structure

Market Cap Market Cap 4,622,821

11/28/2022

Authorized Shares 25,000,000,000 was 5,000,000,000 2021 & was 6,564,838,949 2022

11/09/2022

Outstanding Shares 7,704,701,400 was 3,001,563,774 2021 & was 6,564,838,949 2022

11/09/2022

Restricted 100,003,867 about the same as 2021 was 100,003,867 2021 & was Restricted 100,003,867 about the same as 2021

11/09/2022

Unrestricted 7,604,697,533 was 2,901,559,907 2021 & was 6,464,835,082 2022

11/09/2022

Held at DTC 7,228,225,533

11/09/2022

======================================================

Market Cap Market Cap

1,969,452

08/01/2022

Authorized Shares

25,000,000,000 - 07/08/2022

Outstanding Shares 6,564,838,949

07/08/2022

Restricted 100,003,867 about the same as 2021

07/08/2022

Unrestricted 6,464,835,082

07/08/2022

Held at DTC 6,088,363,082

07/08/2022

Float

Not Available

Par Value

0.0001

=====================================================

$HVCW $HVCW SECURITY DETAILS MKT CAP 3,751,955

Share Structure

Market Cap Market Cap 3,751,955

08/12/2021

Authorized Shares...5,000,000,000

07/16/2021

Outstanding Shares.3,001,563,774

07/16/2021

Restricted....................100,003,867

07/16/2021

Unrestricted..............2,901,559,907

07/16/2021

Held at DTC...............Not Available

Float...........................Not Available

Par Value..............................0.0001

https://www.otcmarkets.com/stock/HVCW/news

https://www.otcmarkets.com/stock/HVCW/financials

https://www.otcmarkets.com/stock/HVCW/disclosure

<Two years this stocks at 20 dollars or more. 1 billion market cap in 4 years>

This is the funniest thing I’ve read all day. Assuming no dilution from here on out which of course is very unlikely you are valuing the company at $154 billion minimum (7.7 billion shares x $20)

Or you think there will be a 150:1 reverse split ……

Because they can buy them back at .0005 if they want to...

Cheaper to get started with a work force trained already. Other companies trained them, we step in and hire them. When others started no work force available. No proof of concept. So hvcw should be smoother.

Two years this stocks at 20 dollars or more. 1 billion market cap in 4 years.

I don’t think you will see a reverse split for a couple of years. They need to sell the Reg A first . Who really knows if they go with .0001 or .0015?

Strange that even though Bobby T said “all parties agreed that .0001 was no longer in play” we haven’t seen documents filed that says that.

Things that make you go hmmm!

This coming year can have over 100mil in revenue.

Compare with fslr at 150, has a .46 loss for the quarter. Little upside there.

This stock has more upside than them. Risky but reward.

Loll. .0005 up. Loll

Stopp. A RS is coming. And diluting all you fools

Correct. Over 100 employees. Massive Revenue. Expanding Nationwide.

Believe or don’t believe me. I don’t care. I believe my track record of posts back up what I say.

I’m a degreed accountant with 30+ years as a Credit Manager for companies up to $200 million so I think I know a thing or two.

Don’t have a horse in the race so it’s not like I’m trying to pump anything. Just giving my honest breakdown of financials.

Spent a lot of time analyzing Canouse RM’s because I can’t believe people fall for the same crap ever single time. Have to admire Canouse/Hicks for blocking out the noise and doing on their terms. Tough way to make a living. I wouldn’t/couldn’t do it. But the fact they haven’t been disciplined yet should tell you they know how to walk that fine line.

If you think you can outsmart Canouse, then go for it!!! You may the first one.

There is no "deferred revenue". The revenue stream that is created by a lease is purchased at a discount by companies that trade equity for cash flow, and the originating company is paid. The revenue is real and immediate, but I think you know this.

They claim to have an office is Kansas City, MO.

Miracle.....a surprising and welcome event that is not explicable by natural or scientific laws and is therefore considered to be the work of a divine agency.

-Cheers!

I'm laughing at anyone who thinks tigerpac is more righteous than canhouse. Mms and close often work together to screw stockholders.

Never believe people like tiger pac have pure motives. Trust no one.

SNOW ? RU DRUNK? WESTCOAST SON. 24/7

Prepare for the run......

Deferred revenue is usually money that is paid up front in the form of deposits before the work is actually done.

The big question here is “what is the life of the contract?”

Is it three months or seven years?

Some % of customers will pay to own system and will get the tax rebates. Others will choose to lease and the leasing company will receive those rebates. Those who lease will pay over 5-7 years and revenue will be spread out over those years.

The company likely had a backlog of about 275 installations as of 9/30

(+/- 20). They will need to hire a lot of $25/hr employees to catch up on this work. Nov-Mar installations typically slow down due to weather. These guys don’t work in rain, snow or wind.

The company also doesn’t operate in a vacuum as there are many competitors within the same market all eventually trying to undercut each other to get the job until they can establish a great reputation.

I think this company needs another 2 quarters under it’s belt to see where it’s headed.

The bottom line is that any stock that previously had Canouse/Hicks involvement is structured in a way to benefit themselves first post merger. Until I see that pattern change I remain doubtful that any of these companies stocks can appreciate. This is based on several dozen experiences with Canouse reverse mergers.

Deferred revenue- we don't get paid until AR is cleared. It is a wrong statement from you.

|

Followers

|

315

|

Posters

|

|

|

Posts (Today)

|

0

|

Posts (Total)

|

35053

|

|

Created

|

09/29/14

|

Type

|

Free

|

| Moderators | |||

courtesy of $HVCW

courtesy of $HVCW

| PER IHUB MGMT |

02-07-2021

DISCLAIMER: ONLY FOR MICK

https://investorshub.advfn.com/boards/profilea.aspx?user=1012

*The Board Monitor and herewithin , are not licensed brokers and assume NO responsibility for actions,

investments,decisions, or messages posted on this forum.

CONTENT ON THIS FORUM SHOULD NOT BE CONSIDERED ADVISORY NOR SOLICITATION

AUTHORS MAY HAVE BUYS OR SELLS WITH THE COMPANIES MENTIONED IN TRADING POSTERS SHOULD DUE DILIGENT BUYING OR SELLING.

ALL POSTING SHOULD BE CONSIDERED FOR INFORMATION ONLY. WE DO NOT RECOMMEND ANYONE BUY OR SELL ANY SECURITIES POSTED HEREWITHIN.

ANY trade entered into risks the possibility of losing the funds invested.

• There are no guarantees when buying or selling any security.Any

| Volume | |

| Day Range: | |

| Bid Price | |

| Ask Price | |

| Last Trade Time: |