News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

tim howard today

"Midas–I want to address your question: “If a capital raise in light of all [the negative actions against Fannie and Freddie that Treasury has taken in the past] would be possible without a senior-to-common exchange, why would it not be possible with one? I can’t understand why outside investors would consider all of the above to be okay, but would see a senior-to-common exchange (which doesn’t affect these investors at all) as the final straw.”

I’ll start by repeating that a capital raise by Fannie and Freddie ISN’T possible as long as Treasury’s senior preferred stock and liquidation preference remain on their books. So where we seem to be in disagreement is over whether the way in which Treasury eliminates the seniors and the liquidation preference will make a difference in the companies’ capital-raising ability (and stock price).

My analysis of this question starts with the facts we know: that Fannie has 5.867 billion of fully-diluted shares of common stock outstanding (assuming conversion of the warrants by Treasury), Freddie has 3.234 billion of fully-diluted shares of common outstanding, and that as of yesterday the companies’ weighted average common stock price was $1.53. Assuming sustainable combined annual earnings of $25 billion, Fannie and Freddie’s weighted average annual earnings per share are $2.75, making their current P/E ratio just 0.56, compared with about 25 times earnings for the average common stock in the S&P 500.

Why is Fannie and Freddie’s combined P/E so low? Almost certainly it’s because the only way existing (or new) common stockholders ever will get the rights to the companies’ earnings or assets is if Treasury cancels the net worth sweep (which will kick in again after Fannie and Freddie achieve full capitalization), redeems or cancels the senior preferred, and eliminates its liquidation preference. A 0.56 P/E on the companies’ $25 billion in annual earnings is the market telling us it thinks there is little chance of any of these things happening on terms favorable to common shareholders.

Treasury can change that, if it wishes. I agree with you that all of its past actions that were prejudicial against and unfair to Fannie and Freddie will have a long-lasting and possibly permanent impact on how high the companies’ P/E can be. But I also believe that how Treasury behaves toward Fannie and Freddie in the future can, and will, make a significant difference in how far above the current 0.56 times earnings, and towards the 25 times earnings multiple of the S&P 500, Fannie and Freddie’s P/E can go.

I don’t know what Treasury wants to do with, and about, Fannie and Freddie, and it’s possible that it doesn’t either. But I do think it’s true that the negative actions of prior Treasuries against the companies in the past–forcing FHFA to place them in conservatorship while still adequately capitalized, encouraging FHFA to maximize the amount of senior preferred they had to draw by loading up their income statements with anticipatory, estimated, or overly conservative non-cash expenses, then proposing the net worth sweep just as many of those non-cash charges were about to reverse and become income–were taken because Treasury (and the Financial Establishment) intended to replace the companies with some secondary market mechanism more to their liking. That’s no longer on the table. Virtually everyone now agrees that Fannie and Freddie have the best business model for the functions they were chartered to perform. For that reason, if Treasury does implicitly agree that its past actions with respect to the companies did not have the effect it had hoped for, and unwinds the most damaging elements of those activities (the net worth sweep, the seniors and the liquidation preference), I believe the market would be inclined to put a much higher value on Fannie and Freddie’s future earnings. If, on the other hand, Treasury converts the seniors to common, that would be an unmistakable affirmation that its prior anti-shareholder policies towards the companies have not changed at all, and in that instance I don’t know why their P/E would move any higher than it is now (indeed, it likely would move lower).

Again, I’m not predicting what Treasury will do, whether in this administration or a future one. But I am saying that if Treasury decides one of its objectives is to maximize the value of its current ownership in Fannie and Freddie (via conversion of the warrants), it should do so by canceling, rather than converting, the seniors."

Oh wow. No worries. We are next.

https://finance.yahoo.com/news/these-stocks-ripped-even-higher-than-gamestop-in-the-meme-rally-165649464.html

I think you broke one of your own rules. As for the MMs - you can call them whatever you like, just no need to post it over and over again. this trade is frustrating enough without additional irritants.

It makes you ask yourself, how dumb am i ?

There are three rules of posting etiquette

1. if something is not nice, don’t post it.

2. if something is nice, post it.

3. if something you don’t like is posted, ignore it and move on to something helpful.

I think the sherwin-williams reference is

Very accurate for what the MM’s are

Doing to us. Maybe we should name them

The SW MM’s will be less irritating for you.

lol

There are three rules of comedy.

1. if something is funny, repeat it until it's not.

2. if something isn't funny, repeat it until it is.

3. if something isn't funny, repeat it until it is.

I think the sherwin-williams gag is well beyond #3

Find other companies on the Dow that have a lifetime c-ship with no chance of ending along with a rubber stamped net worth sweep memorialized by the supreme court in a 9-0 ruling and one that is mired in lawsuits they cannot possibly win due to the nature of the judiciary. I'll wait.

Dow closes at 40,000 and F&F are sucking air!

End of day Sherwin Williams strikes again.

it was 9-0. They are all complicit.

Based on what metric should this stock be above $1.60? Better, give some reasons to support how it's even sustaining these levels? There's literally nothing happening on any front to propel this stock.

Alito - since DAY ONE has looked to me like the kid who got beat up on the playground

and now hates the world and it comes out in his decisions - his revenge

little has been useful ---- some brought hope - and courts shut it down?

didn’t alito wrote the gse verdict, openly giving green light to allow the steal? the best revenge would be to ignore his verdict and let him know.

https://www.cnbc.com/2024/05/17/supreme-court-alito-trump-stop-the-steal-flag.html

Fairy represents the next designation to be used in progression LGBTQ+.....soon to come, LGBTQF+!

Why angel and not a fairy?

Oh wow. I’m looking forward to seeing $1.62 print right about now. Can someone help me out ? I’ll be your best friend. Besties forever. Cross my heart hope to die. Oh wow.

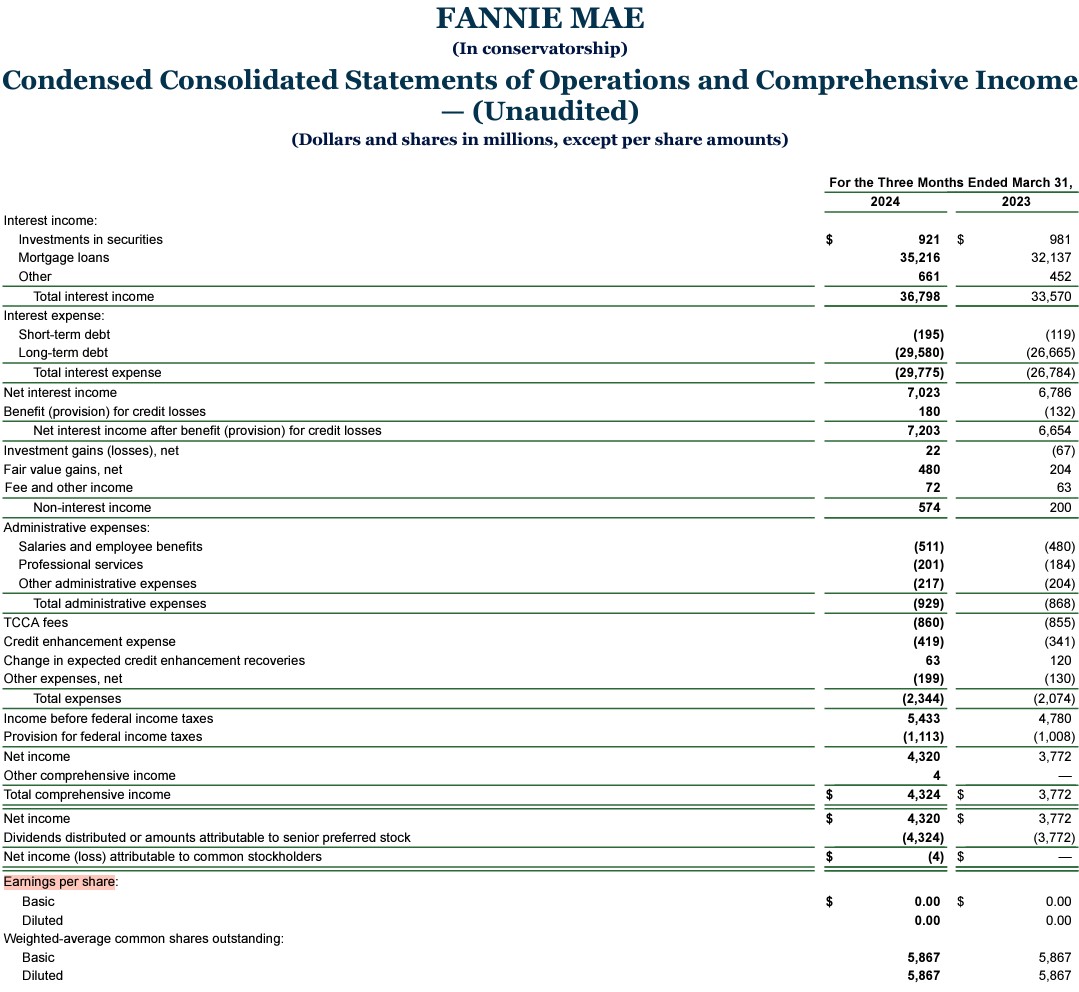

Besides, the EPS isn't calculated with Net Income, but the Net Income Attributable to Common Shareholders, after subtracting the compensation to Preferred Stocks, like dividends or today's SPS LP increased for free in the same amount as the Net Worth increase (Comprehensive Income), in the absence of dividends.

Thus, either the PER (TTM) is extremely high because FnF are posting almost $0 EPS, or NA when it's negative or $0 EPS.

Timothy Howard states that the stocks trade at a "minuscule P/E".

He attempts to conceal the ongoing Common Equity Sweep.

EPS at the bottom of the image.

1. SUIT UP

2. LOAD UP

3. SHUT UP

4. DON'T LOOK BACK

Then u know how I feel about KTCarneyPsKnownots. All useless info. All just strive to screw commons, no logic just agenda over and over to create norms and this synthetic logic about GSE past and future.

no one cares when mnuchin hand in it, go away , this is fnma board

HE argues (with logic I do not follow) that the GOV is better off - cash wise by CANCELLING SP/LP

YES

And any increase above 79.99 would be done in some fashion that allows them to NOT move DEBT over to US Books ----e.g. a promise to sell 20% of their shares within x days to John Q Public

I assume

too much bs : give them another 300 billion, 95% ownerhip, commons to $0.05, reverse split, bankruptcy, restrucuring, give moelis billions in fee. read and believe what you want to. no reporter is covering it, so everyone is hungry for anything. lol.

Rick you did it!! We’re now at $1.605 great job!

We cannot seem to breakthrough $1.60 for some strange reason. We need more warp power Scotty. Full thrusters ahead. Fire phasers and full photon torpedoes Mr. Sulu. Uhura open all hailing frequencies to the whales. Calling all whales. Spock stop jerking off every 7 years and pay attention to the incoming whales.

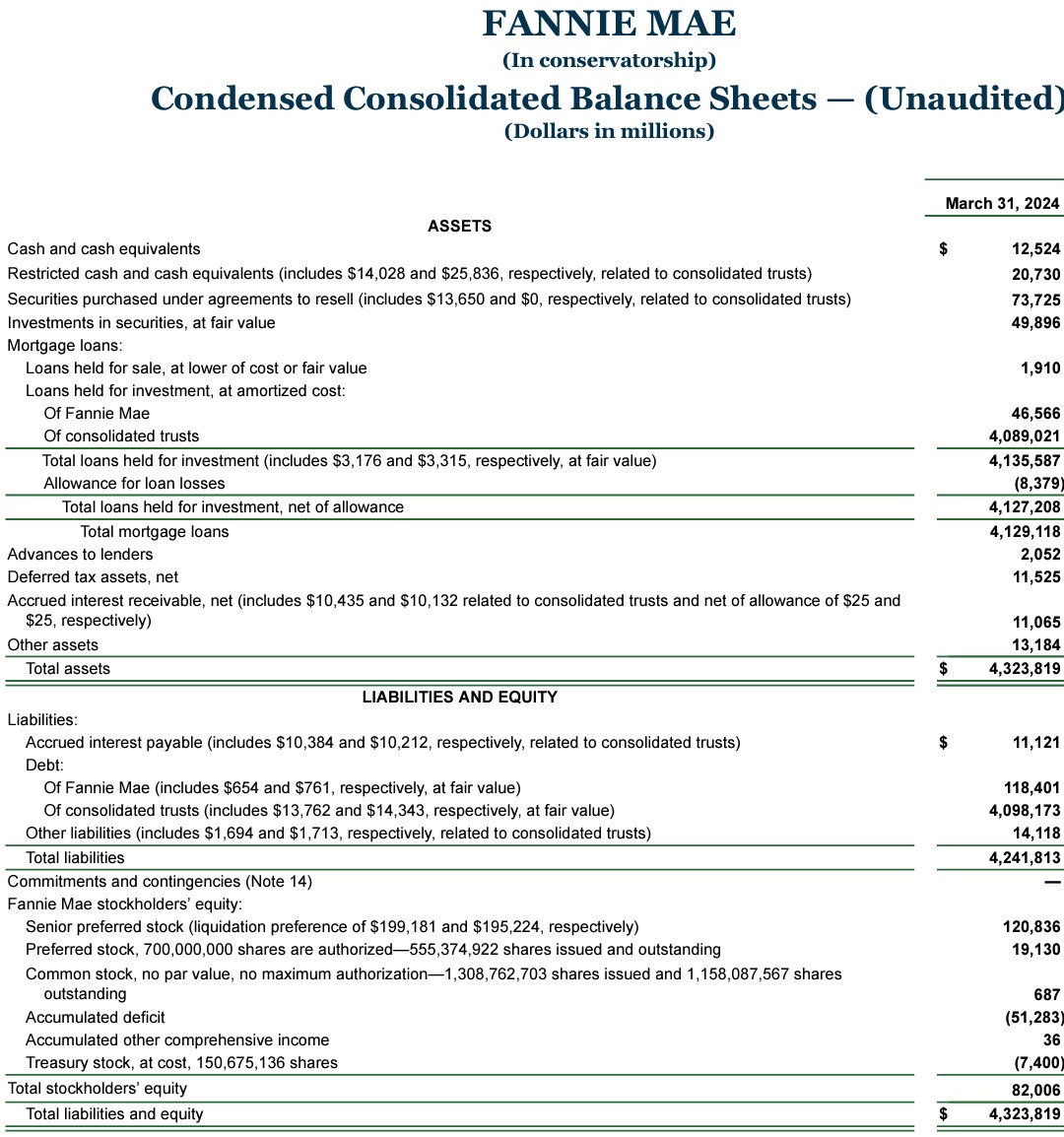

Timothy Howard should be ashamed for having repurchased $7.4B of $FNMA.

FIRST.

It's recorded on the balance sheet as Treasury Stock, a contra-equity account.

It reduces the common stock par value when calculating the core capital.

This reduction of the core capital was one of the reasons of the Conservatorships for Critically Undercapitalized enterprises. (Freddie Mac too)

We have to wonder if this is another reason why the Capital metrics are calculated "upside down", that is, beginning with the Net Worth and subtracting the SPS, instead of the sum of its components, where we would see what I've mentioned of Treasury Stock reducing the Core Capital, and people would begin to wonder who is the crackpot that repurchased common stocks in the market, in congressionally-chartered private corporations. Clearly, this isn't part of its Public Mission.

SECOND

He also aimed to boost his EPS Target Bonus, (buybacks aren't recorded in the shares outstanding to calculate the EPS).

Additionally, accounting fraud to boost his EPS Target Bonus was the reason why he was abruptly expelled from Fannie Mae in 2006, the company had to restate the financial statements of the prior years and pay a $400 million fine, as stated in the 300-page report by the OFHEO and also the SEC, portraying him as the sole boss of a corrupt organization and sole responsible of the lack of controls.

This is a fact. Other theme is that, in 2012, he was acquitted of all charges by a DC court, due to lack of evidence that he had the intent to commit fraud. And we wonder why on earth do we have Federal Agencies with enforcement action if later a low profile judge sets everything aside, and we don't know if there was a Fanniegate deal with the DOJ behind.

sure, they will also evaluate the risk factors for their new investment in terms of how much capital to allocate, and at what valuation. SPS conversion will be a risk factor to consider when putting together the financial models.

— Alec Mazo (@Alec_Mazo) May 16, 2024

SPS cramdown to own 95%+ at 10-12x p/e on…

Interesting angel in 24 months?

Tim Howard's comment on Treasury's options to monetize its stake in Fannie/Freddie. The math should be obvious to everyone:

— Alec Mazo (@Alec_Mazo) May 16, 2024

1. Warrants exercised, seniors written off: 80% of $250-$300bn market caps is $200bn-$240bn upon organic release from conservatorship in 24 months at 10-12x… pic.twitter.com/fSpbw7t4QL

Shhh! It's part of the secret sauce.

Don't you know!

LOL

What is going on with Lamberth? What happened to Libor?

So what’s taking (no pun intended) so long to unscramble the c-ship?

FNMFO has volume today with new 52 week high. Something is definitely going on here but no one tells me anything. At least the real time quotes are back now. CNBC app is the best. I was getting tired of being 15 minutes late for everything.

Rip Van Winkle Wakes Up On Monday

https://www.globenewswire.com/news-release/2024/05/15/2882266/0/en/OTC-Markets-Group-Introduces-Overnight-Trading.html

Thank you

Seems the logic from HOWARD ---- that it is better for GOV to cancel v convert - is shaky ?

logic seems - the conversion causes a ton of shares at low price - (maybe even beating up on WTS if done first)

That makes sense on its face - BUT

If Gov moves from the 79.9% (via WT 4:1) to some higher percent by converting SP to common and then does reverse splits and then does the WT conversion - I think the GOV gets all that it wants?

What am I missing

I want the GOV to kill the SP/LP

As noted for two years - I do not want the WT conversion but if the PPS at 1B is 80-100 or so - then I can live - WELL - with 20-25 a share for my current penny shares . Summary - kill the SP as prices in dollars by the LP --- and go ahead and exercise for say 80-120B cash to Treasury over several years at 25 a share

To exercise the warrant, maybe need to consult with Lamberth first.

Plaintiffs proved at trial that FHFA’s agreeing to the Net Worth Sweep was an “arbitrary and unreasonable” violation of stockholders’ reasonable expectations under their shareholder contracts.

BOOM. New evidence against Timothy Howard never commented before.

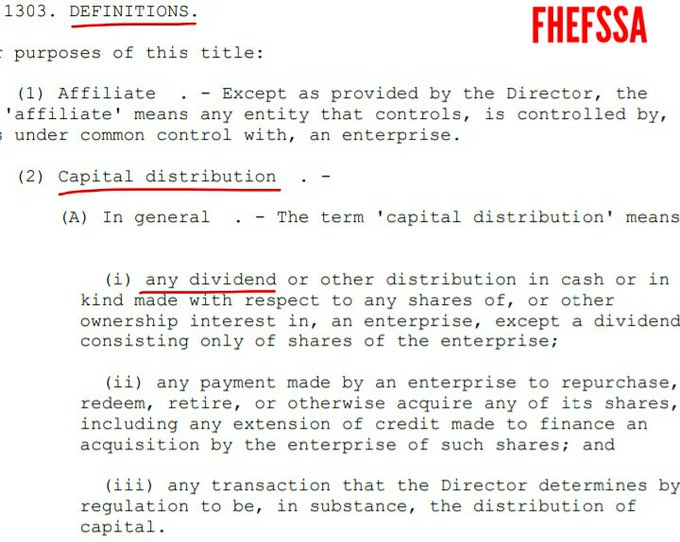

Remember that he is required to pay us Punitive Damages, for going to the Supreme Court as Amicus Curiae, to repeat a dozen times that "the SPS are non-repayable securities", when it's precisely the paydown of the SPS the only capital distribution authorized in this amendment inserted by HERA in the FHEFSSA.

Why doesn't he mention the capital distributions that are really restricted? Dividends, today's SPS LP increased for free and the Lamberth rebate.

I will add a comment not posted ever before, about his assertion: "SPS, non-repayable securities" not written anywhere, because that was a feature of the company Resolution Trust Corporation (RTC), owned by the government, created for the bailout of the FHLBanks in 1989 and their small and regional banks, in what is known as the savings and loans (S&L) crisis.

It was also set up Resolution Funding Corp (RefCorp), fully owned by the FHLBanks (Equity holders) for their bailout and a $30B RefCorp obligation that only paid interests, which doesn't mean that the FHLBanks only had to pay interests stated by the FHFA below.

A 10% interest rate at the time, with a 0.299% spread over Treasuries GAO report-. It was Sandra Thompson who tapped the maximum $30B authorized by law (Who does that?), just when she arrived at the FDIC in 1990 and later, both DeMarco (sole Accountant GAO after the expulsion of PwC. Then, UST) and ST, decided to pay only interests ($300mll annuity), not the principal of the obligation as clearly stated in their Separate Account statutory wording:

.jpeg)

They changed the payment of the principal of Refcop obligation, for "an obligation to pay interests", as we can read in this press release.

The obligation (security) only paid interests. The FHLBanks had to pay interests and principal of the Refcorp obligation. Isn't it clear?

Resolution Funding Corp (RefCorp) invested in RTC, which, in turn, invested in Public-Private Partnerships with Wall Street. What can go wrong?

This is why FSOC requested to Congress last Friday another fund for the resolution of the non-bank mortgage servicers.

Yellen, FSOC Chair, and Sandra Thompson (FSOC member) have become addicted to these "resolution funds" that end up in Public-Private Partnerships with Wall Street and it's when the manufactured crises become very profitable and useful for "loss-mitigation options for borrowers" and the politicians' dream to put a name on (Obama's programs, etc.)

As we can read in the FSOC press release of May 10th (mortgage servicers don't own the mortgages, so they can't carry out loss-mitigation activities without an express authority of the owners of the mortgages):

The fund should be designed to facilitate operational continuity of servicing, including loss-mitigation

Separate Account? I don't know what that is.

I am not a regulatory lawyer but a litigator (another attorney for Berkowitz, David Thompson)

Today is Friday - May 17

A Day to Dazzle

for Fannie and Freddie

Lol. Put it on ignore :) like the rest of us

Roaring Kitty has joined us in this play. Look closely at the note pad in this meme he posted. 🤑

— Roaring Kitty (@TheRoaringKitty) May 16, 2024

You’re right math is off not 386%

$1.99 (52 week high) is a 342.22% increase of 0.45 on June 12, 2023 the day JOoa0ky prophesied

"Commons are going to sink... Sell out now while you still can..."

Link to prophecy: https://investorshub.advfn.com/boards/read_msg.aspx?message_id=172114484

Market still prices it like a coin flip on FNMAS

Karen, your math is off.

Meh... a nickel ... it beats nothing, sure ... and all we need is 1,200 more trading days of nickel gains to get back to about where FnF were before the whole $hithouse went up in flames 😁 At the rate we've been going of 1 or 2 of those trading days every month or so we'll be there in no time ....

Good day. Must say. 🤑

Fannie mae

Houlihan Lokey is dying to hear from you. Fire up that resume, list your vast client and deal experience, and those cracker jack analytical financial statement skills. Don't forget to include your market and industry trend experience, recommendations from prior clients and stakeholders, and for Christ's sake don't forget to add your iHub posts to your portfolio. I'm sure they'll be just as impressed as we all are here. Then move on to Howard's blog and post a detailed critical analysis of where and how he's clueless.

Advice to Common Shareholders to sell their shares at the absolute bottom 11 months ago just before a 386% return. Continues to give out advice!

Quote: JOoa0ky Monday, June 12, 2023,

"Commons are going to sink... Sell out now while you still can..."

Do you have any dignity at all lady??

Link: https://investorshub.advfn.com/boards/read_msg.aspx?message_id=172114484

|

Followers

|

2309

|

Posters

|

|

|

Posts (Today)

|

0

|

Posts (Total)

|

797492

|

|

Created

|

07/14/08

|

Type

|

Free

|

| Moderators not one red cent ~NORC~ stockprofitter Ace Trader Patswil jeddiemack FOFreddie | |||

| Volume | |

| Day Range: | |

| Bid Price | |

| Ask Price | |

| Last Trade Time: |