News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

June to the moon

Or

Moon in June

Can you guys all just keep to being humble and stop turning this into Reddit?

No one cares who has been posting things firms already read and don't share. No one is a moron or and idiot. No one will get credit for being the most "right" because everyone here is looking at this wrong one way or another.

I'm going to share something as I have had success with listening, and sharing what I can that is goodwill to share given I spend more sweat equity sharing what I don't have to for never getting any return from strangers on a message board.

I usually have some guy tell me he was here longer and I'm wrong and I took all this time just to condense things for you to tie together.

So here's a bit of information from the 336 page PDF report online from the examiner of 'Lehman' (the global parent and its focus on how it consolidated its balance sheet as well as legally did it's infamous accounting "Repo105")... If you think that this isn't all a private and public sector coordinated intentional process playing out to bring new litigation and cross-jurisdictional practices out while the first global "crisis" took place on both paper and the early 80's to 2000's internet connected financial world.... maybe think this whole time the unwinding is being done very carefully but also rolling out at privately coordinated stages as the internet (undersea fiber cables, satellites, software, hardware, data centers etc) in 2024 is more equipped to handle cross-jurisdictional movement of assets, transactions, accounting that works in connected worldwide counterpaties, inter-company cross-jurisdictional entities rolled onto one US based parent balance sheet?

This is something to think about. You are not all wrong, but being convinced you are right enough to call people Reddit level bs back and forth. You should know being humble is lucrative. Being internet "right" will get you nowhere.

Now someone will go ahead and say but mellon that's Lehman! Not Fannie Mae!

You really need to study more if that's how you're going to think of this all.

Repo105 (used to make US Treasuries, Agency Fannie and Freddie securities/bonds 'disappear')

I will leave this for you all to consider a narrow scope of this and calling others idiots for trying to grasp something results from an argument one of you started - Do you want to make money? Or do you want to fight?

If we keep it to sharing insight we can hive mind better results for all investors. No one cares who thinks they are "right"... in the end what a waste of time.

Don't make this Reddit. Work together.

-Mellon

Careful about what you are optimistic about. Sure he can make plans and offer a consent decree but it could be a multi-year process with milestones and achievement requirements and guarantees for affordable housing. Shareholders could still get screwed for many years.

Here’s another example of failure lawsuit with no reference of the Regulator breaking the law.

UNITED STATES COURT OF FEDERAL CLAIMS

Wazee Street Opportunities Fund IV LP,

Filed 04/03/23

Quote: "This lawsuit does not challenge the foregoing arrangement made in

September 2008. While Plaintiffs do not concede that all the measures taken in September 2008 were justified or necessary, they are not here to challenge the placement of Fannie and Freddie into conservatorship at the height of the financial crisis, or the original deal struck by Treasury and FHFA at that time." End of Quote. Page 7

The lawyers are focused on the third amendment net worth sweep. By Public Law the whole contract is illegal, the contract is illegal based on the United States is not permitted to charge a commitment fee to be paid by the enterprises.

Link: https://storage.courtlistener.com/recap/gov.uscourts.uscfc.37252/gov.uscourts.uscfc.37252.30.0.pdf

Pagliara thinks that is the deadline for any Biden action based on what he heard 5 months ago. Since then he seems to be less optimistic of anything happening. I still am optimistic. Capital plans are coming next month

who said fhfa is not an independent agency? fhfa claims so.

why is calabria, the stupid shit is trying to be relevant after what so much damage he did?

Sounds good to me. Make it so Number One.

Going up Monday morning 🌄,🛹🌵🇺🇸

Great comment by Glen. He might be finally reading what Rodney has been saying.

So if FHFA is not an independent agency then how does the SPSPA work? The government just signs deals with itself now?

— Fanniegate Hero (@DoNotLose) April 26, 2024

Do we have clearance to lift off from conservatorship?

Clarence, I appreciate you taking the time to understand our situation.

Below find a link to a letter I sent to

FINANCIAL SERVICES

Committee

Committee Members

118th CONGRESS

Violations by the Federal Housing Finance Agency (FHFA) violating of the Charter Act, and the Federal Housing Enterprises Financial Safety and Soundness act of 1992 (FHEFSSA); Both as amended by the HOUSING AND ECONOMIC RECOVERY ACT OF 2008, (HERA). The Charter Acts are Fannie Mae and Freddie Mac's enabling statutes. FHEFSSA and HERA are regulatory statutes, governing the companies' regulators. All are laws passed by Congress.

https://investorshub.advfn.com/boards/read_msg.aspx?message_id=172987595

Do we have clearance Clarence ?

Clarence said, Quote: “ “…because FHFA exceeded its statutory conservator authority…”.

That’s the confusion, Conservator AND Regulator are entirely two different positions. The attorney’s DID NOT CHALLENGE the Authority of the Regulator. Justice Breyer told the plaintiffs how to win. The plaintiffs are focused on the contract SPSPA lost dividends and never challenged the FHFA Director as breaking the Law.

Barron4664

09/20/23 9:36 AM

Post #768746 on Fannie Mae (FNMA)

The problem is not with the rulings of the courts. The problem is and always has been that the plaintiffs attorneys have only challenged the “Actions of the Conservator” such as the NWS or other provisions of SPSPA which is a contract. 4617f bars courts from questioning the actions of a conservator. As it should. None of the 15 + years worth of court cases have challenged the action of the FHFA as regulator or Treasury with respect to the statutes that actually matter. The charter act, safety and soundness act, chief financial officer act, etc. To get a takings or an illegal exaction verdict, you have to show that the gov broke the laws. The actions of the conservator cant break a law. But if you go before a judge and say the SPSPA is bad and the gov stole our companies and limiting the argument to the specifics of the SPSPA agreement and the amendments you get 15 years of no results. Had they brought before Lamberth in 2013 any statutory claim involving the actual statutes with regard to the GSEs, then this probably would have ended a long time ago. It almost seems that the plaintiff attorneys have operated as some type of controlled opposition to run the statute of limitations out. A conspiracy. How can 15 years go by and nobody filed a court case based on the charter act. It is like Ray Epps, after 2.5 years, now he gets indicted for 1 count misdemeaner. With GSEs, we get a little victory for Hamish Hume. Look how great the attorneys are, they are fighting hard for us.” End of Quote

THE ATTORNEYS DID NOT CHALLENGE THE CONSERVATORSHIP! THE ATTORNEYS ASKED THE COURTS TO RULE ON THE ILLEGAL CONTRACT, SPSPA: JUSTICE BREYER TOLD THEM HOW TO WIN!

UPMOST IMPORTANT: JUSTICE BREYER: Quote: “Thank you. I think in reading this you could, with trying to simplify as much as possible, do you -- the shareholders' claim as saying we bought into this corporation, it was supposed to be private as well as having a public side, and then the government nationalized it. That's what they did. If you look at their giving the net worth to Treasury, it's nationalizing the company. Now, whatever conservators do and receivers do, they don't nationalize companies. And when they nationalized this company, naturally they paid us nothing and our shares became worthless. And so what do you say?” End of Quote, page 12

The link may not work anymore, the above statement was made and recorded in the transcript.

Link: https://www.supremecourt.gov/oral_arguments/argument_transcripts/2020/19-422_3e04.pdf

June is soon ;)

“…Administrative Procedures Act... None of the litigation made any claims of violation of these acts.”

But the Collins plaintiffs brought at least three different APA claims.

On page 13 of the published Collins v Mnuchin en banc decision, the court explains that Counts I, II, and III were all brought under various parts of the Administrative Procedures Act. Count I survived, and SCOTUS later reviewed it.

On page 13 the court specifies that Count I was brought under the APA, specifically 5 U.S.C. 706(2)(C) et seq., “…because FHFA exceeded its statutory conservator authority…”.

CFPB could just follow what you guys did at FHFA and Net Worth Swindle the equity of the banks they are supposed to regulate.

— Guido da Costa Pereira (@GuidoPerei) April 26, 2024

wasn't scotus case all about apa? i recall reading it a lot. if you are correct in saying that hamish and other plaintiff attorney's were misleading the shareholders and not doing it right and intentionally, they can be sued even if they were not paid by shareholders other than berkowitz: public statements of theirs, filing a class action on other's behalf, it is the same thing that they filed against fhfa : breach of trust. has anyone reached out to hume who may be fume ing if correct that he got caught? of course if you are right. remember hume and his team will make like 300 million in fees from class action if my memory serves it right. not a chump change when shareholders lost everything : $1500 down to $0.40 in last 16 years of their filing frivolous lawsuits and we know in the letter agreement signed it says that all lawsuits must end before end of c ship and hume and his team continues with lawsuits.

You see when I say green then it's green

Yes, the low volume is actually

a good sign for next week, and

for weeks to come

The volume dried up for the past 2 days. Possible sharp up trends next week.

You are about the most ridiculously negative poster to ever haunt

the messageboards...hardly anything you say has credibility, it's like

you're just spouting off printed troll stuff for only one reason, to irritate

others, you never cite any foundation for your opinions, something is

seriously wrong with you outlook

Nothing bad happening here, Fannie and Freddie getting ready

to give us an unusually spectacular week next week

We cannot seem to breakthrough $1.46 Captain Tutt. Do something will ya ?

I’ll stick with $libtrs

It may be $SANDRA

We need more buying volume Captain Tutt.

Once she hits $444 my new license plate is $OBAMA

Gotta give the man credit where credit is due

Used to be red on Friday. Now I say it's green

$Freddie Mac's mortgage portfolio rose at annualized rate of 3.2% in March,

bringing its balance to $3.496 $Trillion the $GSE said on Thurs.

$Single-family $Refinance $Loan $Purchases and guarantee volume was $3.9B in

March, representing 15% of total single-fam mortgage.

Booom ! Freddie Mac mortgage portfolio increases at 3.2% annual rate in Marchhttps://t.co/LVFcNOro0e

— Cmdr Ron Luhmann (@usnavycmdr) April 25, 2024

Federal Home Loan Mortgage Corporation

(FMCC) | By: Liz Kiesche, SA News Editor

Glad you have come to your senses.

Great decision to dump JPS.

Commons to the MOON $444/SHARE 🚀🚀🚀

A layman making a comparison: Net Worth 2008-2023.

Notwithstanding that today's Balance Sheet (once the S.E.C. fixes their Financial Statement fraud with the $125B worth of SPS LP increased for free as of December 2017, and its offset with reduction of Retained Earnings account, absent from their Balance Sheets), is comprised of:

- $316B SPS LP outstanding.

- $-216B Accumulated Deficit Retained Earnings accounts, and account that absorbs the future (unexpected) losses, which is what the Capital ratios are for (Retained Earnings is Core Capital). So much for "rehabilitation".

Capital Stocks DO NOT absorb losses (reduction). They just offset a negative Retained Earnings account, so the Net Worth remains with positive balance.

Regarding their Net Worth, today's $125B NW has been built with the $125B SPS LP increased for free since December 2017, absent from the Balance Sheet. Thefore, out of $125B Net Worth, $0 corresponds to the Common Stocks and $0 corresponds to the JPS.

Your comparison of Net Worth 2008-2023 is another plan of deception, in order to conceal the reality of Fanniegate, with your boss Tim Pagliara involved for sure:

I have been involved in every aspect of this issue at the highest levels for 9 years. Source

With respect to capitalization, I am not a regulatory lawyer. I am a litigator....That's being watched by a number of sophisticated lawyers...

The ongoing Common Equity Sweep not only is seen in the Income Statement posted yesterday.

Net Income

Less the amount of SPS LP increased for free (10% and NWS dividends on SPS before)

= Net Income Attributable to common shareholders

Thus, close to $0 EPS every quarter.

It's also seen in the other Financial Statement, the Balance Sheet, if it wasn't because it's missing both the $125B SPS LP increased for free, and its offset with $125B reduction of Retained Earnings account (Financial Statement fraud).

Fannie Mae: There is always $121B SPS LP, when the real SPS LP oustanding as of December 31, 2023, including the one scheduled to be increased on March 31 that must show up as well, is $199B.

Freddie Mac: The SPS LP stuck at $73B every quarter, when the real SPS LP outanding, including the one scheduled to be increased on March 31, is $120B.

As we can see in the Adjusted Net Worth activity table:

Another capital distribution, restricted, we consider that this Common Equity is held in escrow, in compliance with the exception "for Recap" in the Restriction on Capital Distributions (CFR 1237.12) and also with the FHFA-C's Rehab power: Put FnF in a sound and solvent condition, related to Capital levels.

Because this payment existed and we are just legalizing. Carry out thanks to the FHFA-C's Incidental Power (Any action authorized by this section, in the best interests of FnF or the Agency): 3rd phase: "Just joking. Zing!"

This is what the FHFA is interested in.

Sandra Thompson continues to peddle the lie about capital requirements met with "$125B Capital Reserve" (amount of Net Worth above the Capital Stock) that she sees on the Balance Sheet, in her written testimony in Congress last week. Enough reason to fire her for cause, because the FHEFSSA and her own ERCF state otherwise (they are met either with Core Capital, Total Capital, CET1 or Tier 1 Capital)

By the way, once adjusted for the Financial Statement fraud mentioned, the Capital Reserve =$0 (All the Net Worth is SPS)

The FHFA Director doesn't have authority to break the Charter Act with the CRT operations.

Let alone to set up a parallel Housing Finance System with them, called "GSE Reform".

CRT is only authorized the UST with its portion (Capital Magnet Fund) of the 4.2 bps allocated to two Affordable Housing Funds managed by HUD and the UST. Source.

The CRT is a normal bond used as an excuse to make FnF pay interests, that began with a steep 5% - 6% rate, which looked like the fraud in early conservatorship with their 30-year zero coupon callable MTNs, where FnF paid an outstanding rate when they were redeemed soon after being issued.

Now, they include arrangements in these back-end CRT "Bonds" (after FnF had carried out foreclosure prevention actions to bail out these CRT investors), and thus, it serves at the will of a random FHFA director whether he requires the payment of claims or not (Utility Model).

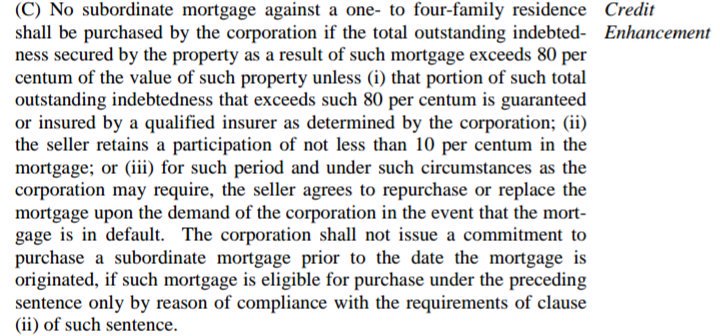

On the other hand, the PMI required to borrowers with LTV >80%, and today's Commingled Securities (Catastrophic-Loss Reinsurance or resecuritizations) 100% insured by other guarantors against default, are authorized CRT operations (number 1 and number 3 in the clause Credit Enhancement of the Charte Act, respectively)

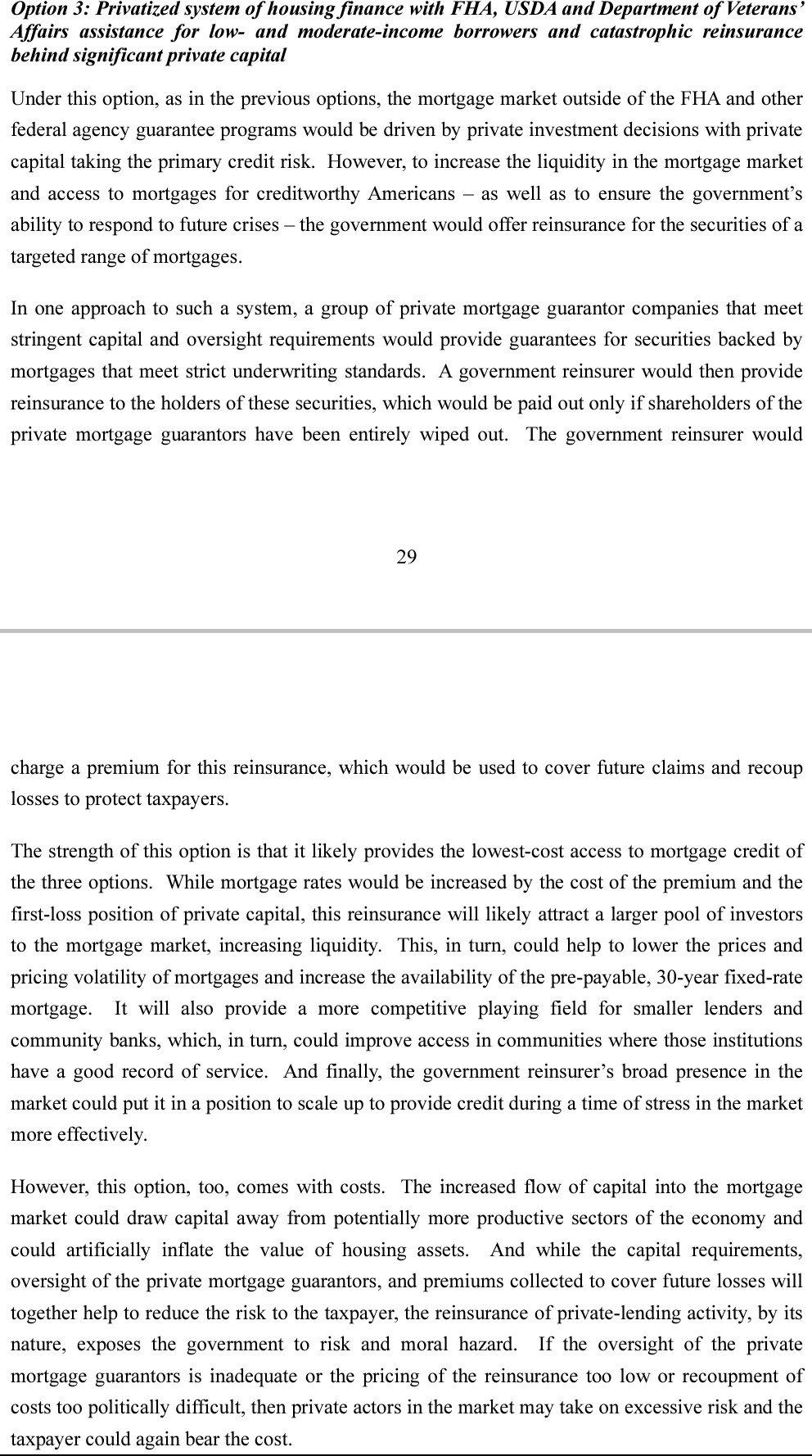

It's precisely, the Commingled Securites or Catastrophic-Loss Reinsurance, a new product for the 3-option Privatized Housing Finance System revamp, chosen by the UST in 2011 for the release from conservatorship, at the request of the Dodd-Frank law, because the option 3 is a Government Catastrophic-Loss Reinsurance and this product enables it:

This product can be used for a private Catastrophic-Loss Reinsurance as well, and then, we would be in the option 1 or 2.

It wasn't created to make FnF reinsure each other's UMBSs. Currently a pilot program, but, at some point, it has to be announced one of the 3 options.

This product was unveiled by Freddie Mac in June 2022 (Source. Notice how it's written that it began with a price of 50 bps. One week later, the FHFA changed it for 9.375 bps to better reflect the 2011 UST plan we are bound for, and not the ill-conceived Mnuchin's 2019 Plan with a Government Explicit Guarantee on MBSs)

It isn't the same a MBS with Govt Catastrophic-Loss Reinsurance and a MBS with Govt Explicit Gtee. In the first one, the credit risk is covered by private guarantors. It's activated once it files for bankruptcy.

Today, the MBS is guaranteed by FnF and there is only a cheap UST backup of FnF upon negative Net Worth. That's it. The "MBS with a Govt Implicit Gtee" is an attempt to conceal the reality of a UST backup of FnF.

The FHFA has a tendency to deviate from the normal course and it corrects itself, or, sometimes, it needs help.

The PLMBS was a product not authorized in this clause (Unlawful. Lack of credit enhancement operation) and it was one of the reasons for the conservatorships.

This time, the rogue FHFA can't be authorized to break the law again at its will, regardless that JPM, the Mnuchin Treasury Department and Mike Bloomberg (included in his electoral manifesto posted yesterday) love the CRTs. Barred in FnF.

The grounds for a Housing Finance System revamp ("GSE Reform") was initiated by FHFA's DeMarco, in light of the 2011 UST plan for the release, that included g-fee hikes, Basel framework for capital requirements: "capital standards that cover the risk as if it was held by the banks" (Mel Watt attempted to deviate from this course in his proposed Capital Rule, and he was corrected by Calabria),...., that would end up with the removal of the most privilege of all: the Charter's UST backup of FnF (Charter revoked).

ST TRIES TO OVERSHADOW DEMARCO AS MASTERMIND OF REFORM

— Conservatives against Trump (@CarlosVignote) April 25, 2024

In her written testimony.

DeMarco(written testimony, May 2011)unveiled the preps of a Privatized Housing Finance Sys revamp, chosen for the release by the UST in a Report to Congress 3 mths earlier: g-fee hikes,...#Fanniegate https://t.co/mgjrPMllgX pic.twitter.com/TDKYNXTug4

I see him responding to those I blocked because I consider them government stooges and not shareholders. Don't mind responding to shareholders with views different from mine. But there's no point in engaging those who argue that the government does no wrong.

— Rick Nagra (@RickNagra) April 25, 2024

No they didnt lose. The APA doesnt apply to the actions of a conservator under HERA. APA deals with rule making. I contend that the FHFA as regulator violated the APA when it allowed the FHFA as Conservator to sell to treasury a new novel investment product consisting of senior shares with an illegal commitment fee or charge in the form of a variable liquidation preference based on the amount of money leant from the Government’s treasury. This is a magical commitment fee whose form can change with the stroke of a pen. The statutory APA requirements for such a new investment product are written in the Safety and Soundness act of 1992. Well to continue the theme. The corrupt plaintiff Attorneys, or as FFF likes to say the dumb attorneys didn’t bother to bring an APA claim based on the actual laws that matter, choosing instead to play in the HERA actions of a Conservator sandbox. You know the actions that Congress bared the Courts to review? What a great idea, let’s ignore all the laws governing the GSEs and FHFA and instead focus all our efforts for 16 years on the actions of FHFA as Conservator. Now the Statute of limitations has run out. Better hope Crazy Carlos is right.

Which plan is that? Also, the way that reads is the only thing left to do is reach the needed capital reserves? Hopefully the enterprise regulatory capital framework can get fixed and made more realistic. In the meantime they are incredibly efficiently stacking cash so we will all be getting paid multiples for our shares once we are free.

Go and ask your dad to come and speak on this board. He has more rights than you as an investor in you..

The APA does not apply to the actions of the conservator; the SPSPA the contract Court threw that out.

The APA applied to the actions of the Regulator the Lawyers failed and never applied the Law! The argument in the courts “pay me my dividends.” The SCOTUS basically said we will not be an arbitrator in such matters of contract. Go figure!

We lost the APA (Administrative procedures act) in SCOTUS.

Not helpful?? What gives you the right to tell Barron to keep quiet? Go back to your seeking garbage and print more on how the common shareholders will be forever wiped out. You’re a hypocrite.

Barron is the one who brought it to the attention of this board. The Federal statutes are the Charter Act, the Safety and Soundness Act of 1992, as amended by HERA, and Administrative Procedures Act, and potentially the Chief Financial Officers Act. None of the litigation made any claims of violation of these acts.

So now we get to see if they mean what they say and if the 2022-2026 strategic plan is serious

Didn’t seem to impact Freddie

Yeah, we've a housing crisis.

|

Followers

|

2331

|

Posters

|

|

|

Posts (Today)

|

29

|

Posts (Total)

|

802383

|

|

Created

|

07/14/08

|

Type

|

Free

|

| Moderators not one red cent ~NORC~ stockprofitter Ace Trader EternalPatience jeddiemack FOFreddie | |||

Fannie Mae (the Federal National Mortgage Association, or FNMA) is a government-sponsored enterprise (GSE) in the U.S. that was established in 1938. Its main purpose is to provide liquidity, stability, and affordability to the U.S. housing market. It does this by purchasing mortgages from lenders (like banks), packaging them into mortgage-backed securities (MBS), and selling those securities to investors. This process ensures that lenders have more capital to issue new home loans, helping more Americans get access to homeownership.

| Volume | |

| Day Range: | |

| Bid Price | |

| Ask Price | |

| Last Trade Time: |