News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

https://www.fhfa.gov › Pages › publ...

FHFA Announces Final Rule Amending the Enterprise Regulatory Capital ...

ERCF @1.5% that Mansinger speaks of. Interesting.

8/14 is deadline for comments period, then FHFA will review comments, decide what changes to make and then request comments again before implementing those changes, as I said this is 5 years project for sandra dumdum

Agreed, when you see the ERCF being modified, that’s when you’ll know that the Government has all of its ducks in a row and release is imminent! That’s when you hope to have your positions full for lift off??

After 2Q & ERCF 8/14-Release@1.5%(105B)+70B to be raised

August is summer recess for congress. That's perfect time for release after modifing ERCF to 2.5% on $7 Trillions. Gov can release with $105B plus $70B to be raised to meet 2.5%. SPS+10% paid+ $30B extra can be used to buy back 30% of warrant (30% of 79.9%). Another 70% of warrant ($70B) can be returned to GSE to use $7B per year for 10 years for low/mid income housing for downpayment.

Common to $20-$40 & JPS to par.

Only way, Democrats can win in 2025 if they do above. Otherwise, new Republican government will have different priority.

By mistake Warren Buffett spill the bins when asked about banking problem. That means, Gov is already talking to Warren Buffett about recap.

As I see it, the only way for the Government to maximize their investment and not increase tax payers liabilities is to forgive the SPS and cancel the liquidation preference and then over time cash in on the remaining warrants after a percentage is used to recap and release the GSE’s. They can do one or the other but not both. Then the JPS will receive what they deserve and the commons will receive the price appreciation that they deserve. The taxpayers will have no liability and the companies will be fully funded.

Dont get your hopes up. Here is why the Waze (and Fisher) en banc petition to court of appeals in federal circuit has 0.00% odds in my view. To win an en banc petition, you need to win a majority of the circuits judges. In all of the GSEs litigation history, not one democratic judge has ever sided with shareholders (about 15 conservative judges did). This circuit has 12 judges made up of 4 republicans and 8 democrats. Not only that, 2 of the republican judges already ruled against shareholders when they joined the majority 3-0 takings opinion written by a (now retired) obama judge. So that leaves 10 judges left, 8 being democratic appointed. Even if the remaining 2 conservative judges agree with shareholders, you need a total of 5 of the remaining 8 democratic appointed judges to break party lines and overturn their fellow obama appointed colleagues ruling. Its just not happening.

There is a reason shareholders decided to appeal straight to a conservative SCOTUS where they thought they had better odds than appealing en banc to a liberal circuit first. They knew it was a waste of time. So as you can see, yes the takings cases are dead.

Thank you

Keep us posted - please - on WAZEE ----- en banc can be a life saver (but yes it is very rare but here the issue is seriously large and disconcerting and there may be other judges who want to hear the case and weigh in for those reasons?)

Please re read your first sentence

After 5+ decades of being ruled by Unelected Bureaucrats in DC, Americans and their businesses are ready for the SCOTUS to start reining in the 4th Branch.

So after Bureaucratic rule - we now move to singular uncontrolled - judicial kings

If Courts forced - -? not sure how ? - Congress to do its job ---- we could agree !!

But if Courts - here 9 people with no election and lifetime appointments -- become KING and QUEEN and a ROYAL COURT --- I do not see how the transition is better and can be worse

FOR FNMA right now - we want a strong Court FINALLY --- yes FINALLY - doing something for us --- but overall - such singular power in one address and nine people is frightening

Congressional power of the purse

See - there is something we can clearly agree

While insanely dysfunctional !! --- Congress is the PLACE - to fund and to write clear language

We then can disagree on what is worse - 9 Judges being the final say on TONS of key issues or 1000 administrators

For now - with a 6-3 super conservative SCOTUS - seems CHEVRON loses

I can but will not argue here the logic - superior logic IMO - of CHEVRON v the new stuff which scares me in its massive concentration of power in one address --- but we can agree Congress is the place to write clear laws and control the appropriations (as BO learned on the tiny reinsurance by insurance companies in ACA for money "forgiven to the lower income" by hospitals -- AS PER THE LAW -- but never line item appropriated by congress - SO BO lost in court - as he should have

You state the below as FACT - 100% - over and over

Yes - the capital now is say 100B ----- but if the below is true as FACT - copied and pasted

commons are destroyed.

preferred are going to face value.

I THEN HAVE TO ASK

Why not in 2018

Why not in 2019

Why not in 2020

Why not in 2021

Why not in 2022

Why not in 2023 so far

that’s what I thought, “I recognize, however, that arguments from me won’t cause FHFA to change”

imo, they don't even glance at the comments let alone embracing the feedback or reading them and understanding them.

If Biden delays recap/release, the next administration after him will gladly collect the $100 billion - and most likely use the money for something else than reducing the racial gap in homeownership.

Howard can't post anything without making it a marathon novel

Response to FHFA Pricing RFI

jtimothyhoward - Jun 5

Yesterday evening I submitted my response to FHFA’s May 15 “Fannie Mae and Freddie Mac Single-Family Mortgage Pricing Framework Request for Input” though the agency’s website.

This RFI discusses how the transition to the Enterprise Regulatory Capital Framework, or ERCF, this year has affected the companies’ guaranty fees (which are too high) and return on capital (which is too low). The RFI asks for public input on ten “topics,” but only the final one can fix the problems FHFA identifies: “Should risk-based pricing be calibrated to the ERCF?” I believe FHFA’s current leadership understands that the answer is “no,” but wants the industry to tell them this in their responses to the RFI, to provide political cover for lowering a capital requirement set by a predecessor Director, which nearly everyone thinks is excessive.

My RFI response makes the case for why and how the capital required of Fannie and Freddie should be reduced to no more than 2.5 percent of total assets. I recognize, however, that arguments from me won’t cause FHFA to change; the arguments that do will have to come from key stakeholders within the mortgage finance industry that FHFA knows and respects. To that end, I have submitted my response well before the August 14 deadline, to give other potential commenters ample opportunity to review it thoroughly, and draw from it whatever they may find useful in preparing their own submissions.

My response appears in full below.

On May 15, the Federal Housing Financing Agency (FHFA) issued a request for input (RFI) “soliciting comment on [Fannie Mae and Freddie Mac’s] single-family pricing framework and the goals and policy priorities that FHFA, as conservator and regulator of the Enterprises, should pursue in its oversight of the pricing framework.”

This RFI appears to be a response to criticism from the mortgage industry of the changes made by FHFA to Fannie and Freddie’s loan-level price adjustment (LLPA) grids, effective May 1, through which it lowered the LLPAs on certain higher-risk mortgages to improve their affordability, then offset the cost of those decreases by raising LLPAs on many lower-risk mortgages. In its RFI, FHFA defended these non-risk-based offsets by citing the impact of the transition in 2022 to the Enterprise Regulatory Capital Framework (ERCF) on the companies’ return on capital, noting: “Given the substantial amount of capital required to be held by the Enterprises on new mortgage acquisitions as a result of the ERCF, the Enterprises are not currently earning commercially reasonable aggregate returns on new single-family mortgage acquisitions. FHFA estimates that the Enterprises are generally earning mid-single digit returns on equity on aggregate new single-family mortgage acquisitions.”

While FHFA does not say this outright, it is evident that Fannie and Freddie are not now able to meet either of the two most critical imperatives of their charters: setting guaranty fees on their higher-risk loans at levels that are affordable to the borrowers who typically take them out, or earning “commercially reasonable aggregate returns” on their capital. To aid FHFA in resolving this dilemma, its RFI “seek(s) input on the process for setting the Enterprises’ single-family upfront guarantee fees, including whether it is appropriate to continue to link upfront guarantee fees to the ERCF, set risk-based upfront guarantee fees for both Enterprises, and set a minimum threshold for an Enterprise’s return on capital.”

Taking these in reverse order:

Minimum return on equity capital

The one parameter for Fannie and Freddie’s return on equity (ROE) over which FHFA has full control is the target ROE they build into their credit guaranty pricing models. And while I and other commenters may have opinions about what that percentage should be, the only opinions that matter are those of the investors who will be asked to provide the new capital required for the companies to ultimately exit conservatorship, or raise new equity during periods of stress if necessary. The financial advisers of FHFA, Fannie and Freddie are in the best positions to determine what this competitive market ROE is, and FHFA must seek, and heed, their advice.

FHFA also must distinguish between target and realized returns on equity. While the former can be controlled by FHFA, the latter are unknowable when guaranty fees are set, because they depend on the degree to which actual mortgage prepayments and credit losses—the key determinants of credit guaranty profitability—diverge from the medians for these variables produced within the pricing models. Once set, guaranty fees cannot be changed, making targets for realized returns on equity a futile exercise.

Finally, FHFA should not “hard-wire” different target (or maximum or minimum) ROEs for specific loan products or characteristics. Company managements should be permitted to decide on relative rates of return for different subsets of mortgage loans in real time and based on market conditions, subject to the constraint of neither significantly exceeding nor falling short of the target total ROE over a given time period (no shorter than one quarter). FHFA as regulator and supervisor should review and provide feedback on managements’ choices in this area—and sanction them for noncompliance if appropriate—but not micro-manage them.

Upfront versus ongoing guaranty fees

The mix between the upfront (or loan-level) and ongoing components of the guaranty fees Fannie and Freddie charge on their mortgage-backed securities (MBS) is not a significant contributor to the economic challenges the companies or their borrowers are facing.

Both Fannie and Freddie set target total fees for the MBS they guarantee. After the portion of the total fee to charge as an LLPA has been determined, those LLPAs are valued, in basis points, using the expected prepayment rates generated in the pricing models (and assumed in setting the ongoing fee). The only difference in the two components is that an LLPA has a known dollar value at the time it is charged, whereas the dollar amount of an ongoing fee depends on the realized prepayment rate—the faster an MBS repays, the lower the dollar amount of the ongoing fee, and vice-versa. This asymmetry in prepayment sensitivity has the potential to make a larger proportion of upfront fees on higher-risk loans an effective hedge, since greater credit losses typically (but not always) occur during times of falling home prices and lower interest rates, hence faster mortgage prepayments. Yet the impact on total credit guaranty profitability of overweighting LLPAs on higher-risk loans is not certain, and in any event decisions on LLPA weighting should be left to management.

The answer to “should upfront guaranty fees be eliminated” is straightforward. If FHFA means eliminate them entirely, total guaranty fees would fall by an equivalent amount, and move the companies’ achievable ROE even further below a competitive market return. And if FHFA means “replace upfront fees with an equivalent amount of ongoing fees,” as noted above this would not make a notable difference either to the companies or to borrowers of affordable housing loans.

Link to Enterprise Regulatory Capital Framework

With Fannie and Freddie’s “commercially reasonable” ROE determined by the market, and no meaningful economic distinction between the upfront and ongoing components of their guaranty fees, the remaining avenue of inquiry in FHFA’s RFI that might provide it with a path for simultaneously reducing the companies’ guaranty fees on affordable housing loans and giving them a realistic chance of earning a market return on their capital is “whether it is appropriate to continue to link upfront [and total] guarantee fees to the ERCF.”

Here the answer clearly is “no.” FHFA’s risk-based capital standard for Fannie and Freddie never has been truly risk-based, and the ERCF literally is not risk-based at all; as detailed below, more than all of its 4 percent-plus required “risk-based” capital is the product of a layering of unrealistic assumptions, minimums, cushions, buffers and add-ons. FHFA at some point must replace the ERCF with a true risk-based capital standard, but in the short term it can significantly reduce the companies’ capital requirements, with no compromise to the goal of achieving an exceptionally high degree of safety and soundness, by removing the most arbitrary and damaging of the non-risk-based elements of the ERCF.

History of FHFA’s risk-based capital requirements

Over the past five years, FHFA has proposed three risk-based capital standards for Fannie and Freddie—the June 2018 standard, the May 2020 preliminary ERCF, and the December 2020 final ERCF. Each of them appeared, to one degree or another, to have been engineered to produce a desired percentage result, which over time became higher and higher, even as the results of the companies’ Dodd-Frank severely adverse stress tests were improving markedly. (To avoid noncomparability, the discussion below uses total assets as a common denominator for all capital percentages. FHFA’s May 2018 standard expressed Fannie and Freddie’s required capital as a percentage of total assets and off-balance sheet guarantees, which at September 30, 2017 were 1.04 times their combined total assets, while the final ERCF expressed capital in terms of a complex measure called “adjusted total assets,” which at June 30, 2020 was 1.09 times Fannie and Freddie’s combined total assets; the results of the Dodd-Frank stress tests are given as percentages of total assets.)

The average risk-based capital requirement for Fannie and Freddie produced by the 2018 standard was 3.37 percent of the companies’ total assets at September 30, 2017. This was considerably higher than would have been predicted by the results of the 2017 Dodd-Frank tests, which was a loss of $35 billion, or 66 basis points of total assets, without a valuation reserve on deferred tax assets (and $100 billion, or 1.87 percent, with such a reserve). Yet a quick review of the structure of this standard revealed the main reason for the difference: unlike the FHFA and commercial bank Dodd-Frank stress tests (or episodes of severe stress in actuality), FHFA’s 2018 capital standard did not consider guaranty fees on loans that remained outstanding during the stress test as absorbing any credit losses, thus greatly overstating the losses to be covered by capital. FHFA called this feature “conservative.”

In two years, the risk-based capital required of Fannie and Freddie by the 2018 standard had fallen considerably, to 2.42 percent of total assets as of September 30, 2019. Some of this decline was the result of improvements in the credit quality of new mortgages being guaranteed by Fannie and Freddie, but most resulted from non-risk-based anomalies in the standard. And by then, incoming FHFA Director Mark Calabria had not only announced his intention to promulgate a new capital standard for Fannie and Freddie, but also signaled, well before that standard was proposed, what he thought the companies’ required capital percentage ought to be, saying in an interview on Fox Business, “I think our objective over time is that you have capital levels at Fannie and Freddie that are comparable to other large financial institutions,” and that 4.5 percent capital was “kind of in the neighborhood of where we’re looking at.”

When the ERCF was first proposed, Calabria had added a 1.5 percent “prescribed leverage buffer amount” to the 2.5 percent minimum capital requirement of the 2018 standard, bringing total required minimum capital to 4.0 percent. He also changed the structure of the risk-based standard to bring Fannie and Freddie’s average required risk-based capital as of September 30, 2019 up to 4.13 percent of total assets, or 3.85 percent of the “adjusted total asset” measure he preferred. After receiving criticism that his 4.0 percent minimum capital requirement (which he also applied to “adjusted total assets”) should not be above the risk-based percentage, Calabria’s response in the final December 2020 standard was not to reduce the minimum, but to add more non-risk-based elements to the risk-based component, raising it to 4.65 percent of total assets (or 4.27 percent of adjusted total assets) at June 30, 2020—nearly double the 2.42 percent required of the companies by the June 2018 capital standard just nine months earlier. Neither Fannie nor Freddie needed any initial capital to survive FHFA’s Dodd-Frank severely adverse stress tests run in 2021.

A true risk-based standard

The concept of a true risk-based capital standard is simple. It is based on a stress test, in which a company’s book of credit guarantees is subjected to a simulated environment of falling home prices (and interest rates) of some specified amount. In Fannie and Freddie’s case, FHFA has chosen a replication of the stress environment of the Great Financial Crisis, in which average home prices nationwide fell by more than 25 percent peak to trough. The stress test is run on a liquidating book of business, which is conservative, because in an actual stress environment a company would at a minimum be replacing its runoff with new business, at equal or higher guaranty fees and with minimal losses in their initial years. The stress test reveals the amount of initial capital required to survive it, and to produce the full risk-based capital requirement an amount is added to account for model risk, operational and other risks, and provide a “margin of safety”—although not so much as to override the risk-based sensitivities of the standard. Typically, a minimum capital, or leverage, standard is then set so that the risk-based standard is binding on the company most of the time.

With the ERCF, this capital setting process was reversed. Director Calabria began with a pre-determined minimum capital requirement of 4.0 percent, then engineered the risk-based requirement to produce a result that first was close to (in the preliminary proposal) and then above (in the final standard) that minimum percentage.

It is possible, however, to use historical and current data to approximate the amount of initial capital Fannie and Freddie would require to survive the stress they experienced during the Great Financial Crisis, were it to occur again. In its June 2018 capital proposal, FHFA said that the credit loss rate of Fannie’s 2007 single-family book of business “using current acquisition criteria”—that is, without the Alt A loans, interest-only ARMs and risk layering that resulted in over half of that book’s losses—would have been only 150 basis points through September 30, 2017. Using the pattern of Fannie’s actual credit losses, this would translate into a cumulative loss rate of about 115 basis points after the first five years of stress (at which point, during the crisis, Fannie’s revenues were again sufficient to absorb all current-year credit losses). In 2022, Fannie and Freddie’s average single-family net guaranty fee (total guaranty fee less TCCA fees paid to Treasury and 7.8 basis points of average administrative expenses) was 39.4 basis points. As going concerns, and without any business growth, an average net guaranty fee of 39.4 basis points would produce 197 basis points of cumulative net guaranty fee income in five years—far more than required to cover 115 basis points of cumulative stress losses over the same period, with no need to touch capital. The companies’ recent Dodd-Frank stress test results support this analysis.

It thus is not an exaggeration to say that more than all of the “risk-based” capital required of Fannie and Freddie by the ERCF at March 31, 2023—4.07 percent of total assets, or 3.70 percent of adjusted total assets—is a non-risk-based cushion of some sort, whether from highly conservative assumptions, imposed minimums, or add-ons. FHFA therefore has choices as to which of the non-risk-based aspects of the ERCF it can eliminate or pare back, in an amount sufficient to materially lower overall guaranty fees, permit efficient cross-subsidization between lower-risk and higher-risk loans, and allow Fannie and Freddie to earn market returns on the much lower, but still very conservative, amount of capital they will be required to hold. The four most significant elements of conservatism (or unrealism) in the ERCF, and their sources and degrees of conservatism, are addressed briefly below.

Ignoring guaranty fee absorption of credit losses

Fannie and Freddie’s single-family stress tests are run on a liquidating book of business. Fannie has put out data that enables us to track the prepayment rates of its December 31, 2007 single-family mortgage book that experienced the stress of the Great Financial Crisis. (Freddie has not published comparable data.) Were Fannie and Freddie’s combined $6.51 trillion single-family books at March 31, 2023 to experience these same stress prepayment rates, their 39.4 basis-point average net guaranty fee would produce approximately $132 billion as those books liquidated over their lives. That equates to 175 basis points of the companies’ $7.54 trillion in combined total assets at March 31, 2023, and none of those fees are considered as absorbing credit losses in the ERCF version of the stress test (nor are any multifamily guaranty fees). Counting no guaranty fees as absorbing credit losses in a stress test is equivalent to assuming a 100 percent prepayment rate. That is not “conservative;” in a stress test, it is indefensible.

A conservative approach to the stress test would be to speed up the prepayment rate on Fannie’s 2007 single-family book from its observed average of 20.9 percent per year to, say, 25.0 percent per year. But even this still would produce $115 billion in net guaranty fees, or 153 basis points of the companies’ March 31, 2023 total assets. If the loss-absorbing value of these guaranty fees is ignored, it must, at a minimum, be acknowledged in assessing the merits or validity of any other elements of conservatism added to the risk-based standard.

Stress capital buffer

A similar point about ignored guaranty fees applies to the stress capital buffer, which the ERCF also refers to as a “going concern buffer.” This buffer is 75 basis points of adjusted total assets (79 basis points of total assets for Fannie and 86 basis points for Freddie at March 31, 2023), and its intent is “to ensure that the Enterprise would, in ordinary times, maintain regulatory capital that could be drawn down during a financial stress and still be regarded as a viable going concern after that stress.”

The concept of a going concern buffer is a valid one, but the ERCF misapplies it. If Fannie and Freddie are to be capitalized so as to remain going concerns—and they should be—then the ERCF needs to reflect the fact that their required capital has been determined on the basis of a liquidating book, without the replacement business a going concern will have. In an analysis I did of Fannie’s 2008-2012 stress experience, the company needed almost 100 basis points less initial capital to survive a going concern stress test compared with a liquidating book stress test, because the going concern stress period lasted only five years (until going-concern annual revenues exceeded annual losses), rather than thirty. And of course in a going-concern stress test guaranty fees must count as offsets to credit losses, since those fees will be there. Stating this point somewhat differently, because Fannie and Freddie’s risk-based capital requirement is based on a liquidating book of business, it already has a “stress capital buffer” built into it. There is no justification for a second one.

Capital minimums for lower-risk loans

The application in the ERCF of a minimum capital requirement of 1.6 percent to all loans, no matter how little credit risk they have, is not only unjustified (in light of all of the other conservative elements in the standard), it is particularly damaging to Fannie and Freddie’s abilities to assist low- and moderate-income homebuyers through cross-subsidization.

Without this minimum, the guaranty fees on the companies’ lowest-risk mortgages would have expected returns much higher than their overall target ROE, and those excess returns could be used to (invisibly) cross-subsidize higher-risk loans. But a capital minimum of 1.6 percent raises the required ROEs on lower-risk loans to the point where virtually all of the possibilities for effective cross-subsidization disappear. Cross-subsidization works very well when there is a close relationship between mortgage credit risk and required capital: the overall level of guaranty fees is reasonable, and a moderate degree of overpricing of lower-risk loans generates surplus fees that can be deployed to reduce the fees on certain higher-risk loans by significant amounts. But all of the non-risk-based cushions in the ERCF (including this minimum) cause guaranty fees on the lowest-risk loans to be set very high to begin with, which makes raising them further to cross-subsidize higher-risk loans much more likely to be perceived, and criticized, as happened with FHFA’s recent LLPA changes.

Stability capital buffer

The stability buffer is a non-risk-based, undisguised, capital penalty on Fannie and Freddie for doing more than a minor amount of business. It increases their capital by 5 basis points of adjusted total assets “for each percentage point of market share exceeding the threshold of 5 percent of total residential mortgage debt outstanding.” The stability buffer added 104 basis points of total assets (or 99 basis points of adjusted total assets) to Fannie’s capital requirement, and 71 basis points of total assets (66 basis points of adjusted total assets) to Freddie’s, as of March 31, 2023.

Fannie and Freddie are the only two companies in America who guarantee the credit of conventional residential mortgages. Their guaranty makes residential mortgages attractive to contractual investors like mutual funds, pension funds and insurance companies, who lack the ability to manage the credit risk of individual mortgages but are well suited to manage the interest-rate risk of 30-year fixed-rate mortgages in MBS because they do not use leverage; the sources of their funding are stable and predictable. The main alternative to a contractual investor managing the interest-rate risk of a Fannie or Freddie-guaranteed MBS is a commercial bank holding an unsecuritized mortgage in its portfolio. For at least the past three decades, FDIC data show that banks’ serious delinquency and default rates on residential mortgages average about triple those of Fannie and Freddie, and periodically many banks fail because of funding 30-year fixed-rate mortgages and other long-term assets with short-term consumer deposits and purchased funds—most recently, Silicon Valley Bank, Signature Bank and Republic Bank. It simply is incorrect to assert that higher “market shares” of Fannie and Freddie increase systemic risk, and must be discouraged by imposing a capital penalty linked to their size. The misnamed “stability capital buffer” in fact encourages the opposite outcome.

Recommendation

Fannie Mae and Freddie Mac’s guaranty fees—particularly on loans to affordable housing borrowers—are far too high, and their current and prospective returns on equity are far too low, for one blatantly obvious reason: their “risk-based” capital required by the ERCF is in no sense risk-based. At some point, FHFA must scrap the overly complex ERCF, and start over in a way that deals with the original weaknesses of the 2018 standard (including not counting guaranty fees as offsets to credit losses, using current rather than original loan-to-value ratios to determine risk-based capital, and treating credit-risk transfer securities too generously). But in the short term, the two critical problems FHFA identifies in this RFI of unaffordable guaranty fees on higher-risk loans and an insufficient return on Fannie and Freddie’s capital can be solved quickly and simply if FHFA changes the ERCF to:

Eliminate the 1.5 percent prescribed leverage buffer in Fannie and Freddie’s minimum capital requirement, reducing it to the 2.5 percent in FHFA’s 2018 capital proposal, and

In the risk-based standard, eliminate the stability capital buffer and the 1.6 percent capital minimum, and if necessary lower the stress capital buffer by enough to reduce Fannie and Freddie’s required risk-based capital to or below the 2.5 percent minimum, leaving more than enough of the ERCF’s remaining conservatism and cushions in place to ensure an unquestionably high level of safety and soundness for taxpayers.

Already saw that and i have said in the past This is going to be a 5 year project for Dumb Sandra

There is a new post on Howard on Mortgage Finance, titled “Response to FHFA Pricing RFI.”

In the post Tim reproduces his submission to the FHFA website yesterday evening in response to its May 15 “Fannie Mae and Freddie Mac Single-family Mortgage Pricing Framework Request for Input,” and includes a brief introduction.

The post can be found here: howardonmortgagefinance.com

There is a new post on Howard on Mortgage Finance, titled “Response to FHFA Pricing RFI.”

In the post Tim reproduces his submission to the FHFA website yesterday evening in response to its May 15 “Fannie Mae and Freddie Mac Single-family Mortgage Pricing Framework Request for Input,” and includes a brief introduction.

The post can be found here: howardonmortgagefinance.com

As per JPS holders "No" They will say only commons that are held by todays JPS will get a dividend other commons will not. lol

5 cent common if released would eventually be worth a lot more especially if a dividend started paying again. Do I have this right?

I don't think the path of recap/release started in 2019 under Trump can be abandoned by Biden. Biden has not reinstated the NWS. Since 2019, FnF have built $100 billion in book equity. The old claim that FnF's business model is "flawed" (pseudo-argument for NWS looting) is no longer tenable today. At best, Biden can delay the release, but he can no longer stop it, nor can any other Democratic administration after him.

ok Even if you are correct, show us this from Biden CBO, Biden FHFA, Biden Treasury or Biden NEC????

Anything anything anything....?????

So you think Biden is going to use Trump reports. Ok sounds good. May be kite flying is better for you as well.

Another argument against an equal conversion/equal haircut on JPS/SPS is that the JPS are senior to commons. If there were a haircut on JPS, commons would become worthless. (This was the case with AIG, where there was a 10% haircut on JPS, and commons became worthless.). Otherwise, the seniority of JPS relative to commons would not be taken into account.

On the other hand, commons becoming worthless is not desired by the government. After all, it wants to monetize its common holdings. Even if treasury held two trillion common shares worth 0 cents after an equal SPS/JPS conversion, the total value of this position would still be zero:

This is because 2 trillion x 0 = 0

By contrast, two trillion shares of common stock x 5 cents yields the desired $100 billion.

KThomp19 wrote several times: If commons were worth even one cent, JPS would be worth par.

Here's a paper from CBO that shows the administration doesn't plan to take a haircut on JPS, even if there will be a haircut on its SPS:

https://www.cbo.gov/system/files/2020-08/56496-GSE.pdf

(Page 13 to page 14)

Redemption of Shareholders’ Claims in CBO’s Model

CBO’s model incorporates the judgment that in scenarios in which the GSEs’ common-stock sale did not raise enough funds to redeem the full face value of both the senior preferred and junior preferred shares, the Treasury would take a reduction (known as a haircut) in the value of its senior preferred stake before requiring junior preferred shareholders to do so. 30 That outcome would be inconsistent with the priority of interest between junior and senior preferred shares. But it recognizes that changing the GSEs’ commitments to junior preferred shareholders would be difficult outside a receivership scenario, in which the Treasury, as owner of the senior preferred shares, also owned the GSEs’ common stock (through its warrants).

-------------------

I wonder how this reconciles with your equal haircut/equal conversion calculations for JPS and SPS here:

https://investorshub.advfn.com/boards/read_msg.aspx?message_id=172037422

When it comes to investing it does not really matter what has happened except in so far as laying out the facts in order to determine what will happen. In this case the government is recapping and releasing these companies administratively and since fhfa is now political will do it under Biden.

Commons are dilutable and since the spspa liq pref exceeds the market cap of their post restructured equity valuation — are akin to toilet paper.

Jps have dilution protection and are worth face outside of receivership.

Plan accordingly. Gold plated diapers.

This is correct. And at this point not only have they not done their homework, but if you hear from them on this board then they are actively rejecting thoughtful conversation and advice in the replies to their posts

There is no problem with property rights transferred to the conservator momentarily to fulfill its mandate, otherwise a two-third shareholder vote would still be necessary and we would have voted NO on every action taken by the FHFA, for the sake of voting NO and mess around. Get it now?

The hedge fund managers and company have turned into Shareholder Rights advocates to draw the attention and later pitch their flawed calculations and judicial diatribe based on cover-ups of the law and financial concepts.

But the defense of the Shareholders Rights in companies under conservatorship is ill-conceived, because the conservatorship status is just for that, the transfer of powers and rights by the management and equity holders, and our rights are well preserved by the conservator, who now, acting on our behalf as a momentary transfer implies, it owes us fiduciary duties: it isn't to act in our best interests like a trustee, but all others: loyalty, confidentiality, accounting, act with honesty, duty of care (prudent decisions), etc. Judge Sweeney just talked about "fiduciary duty" in singular to target only the one of our best interests (dividend payments, etc)

None of them is satisfied during this phony conservatorship, with the conservator allowing that our names and number of stocks be unveiled to the hedge funds as parties in the illegal Class Action in the Lamberth court and where the DOJ is a party too. Soon after the phony trial ended last year, the short interest on FMCC increased 120% and the shareholders like me, were targeted by the brokerage firms to sign a Lending Agreement for our stocks, that popped up every time I logged in.

A different thing is our economic interests in FnF that remains intact, which is reflected in the stock valuation currently discounting all the financial fraud in the enterprises as seen in their mafia Balance Sheets with $296.5B SPS still outstanding, of which $103B are missing in the Balance Sheets (financial statement fraud), the phony conservatorship showing $-193 billion of core capital together, $-216B in their Retained Earnings accounts which is the account that has to absorb future losses ($-113B officially posted by FnF in their balance sheets. $-216 is with the adjustment for the offset with the $103B SPS increased for free, that reduces the RE account), $0 EPS every quarter since day one and the Warrant to purchase 79.9% common stock at $0.00001 per stock.

And the JPS, more of the same, because they currently discount the time period to resume the dividend payments at a 6% discount rate and for that, it's necessary to meet, at least, 25% of the Capital Buffers per Table 8: Payouts. With $400B capital shortfall together, you tell me the estimated fair value today.

This is why one of the 8 Securities Law violations is stock price manipulation because, under the Separate Account account, the common stocks would have been trading at PER 14 times all along and the battered JPS would have fetched their par value in mid 2022, the estimated date of resumption of dividend payments.

Net Worth is NOT what meets the capital requirements.

Another attorney with his calculations. Familymang:

Fannie have a net worth of $64b but needs a minimum leverage requirement of 2.5% ($114b) to exit cship, which means $50b needs to be raised today from outside investors

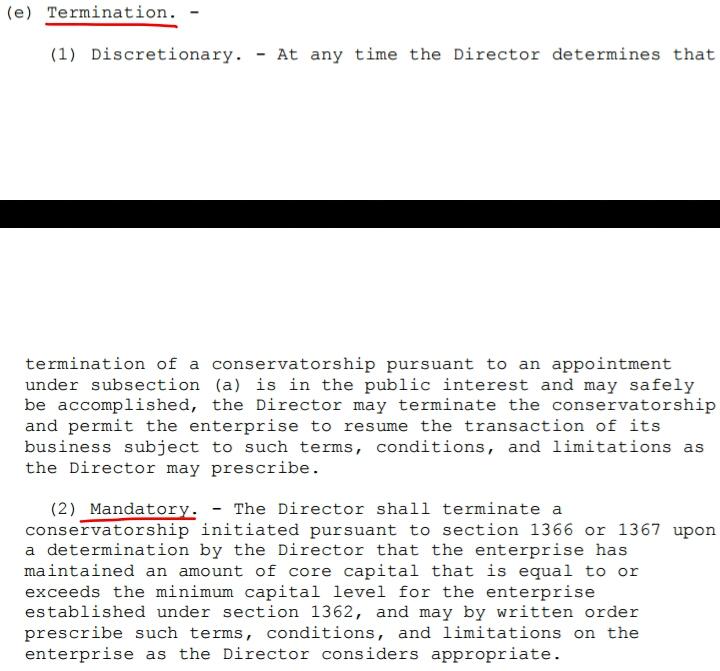

the core capital is equal to or exceeds the minimum capital level

$103B Net Worth is the $103B SPS missing on their balance sheets.

$103B SPS built since they were allowed to retain capital in September 2019. So, no regulatory capital is built because these gifted SPS carry an offset that reduces the Retained Earnings (core capital). As a consequence, the C.C. remains stuck at $-193 billion every quarter, concealed with the financial statement fraud mentioned with these SPS that are missing. All a big lie and you help them providing the cover-up and blessing.

Not only you cheer up the fact that the Net Worth that corresponds to the JPS holders and common shareholders is $0, but also you peddle the narrative contending that the current balance sheet in FnF stays as is, with a total $296.5B SPS outstanding and $301B cash syphoned off to Treasury as illegal dividend.

But there is more! You pitch the Consent Decree, which is a Conservatorship 2.0 and the closest status to a Utility Model sought-after by the plotters.

FnF are governed by the Charter Act and so will be once they resume independent operations with the end of the Conservatorships.

The Capital Rule shows $400B capital shortfall over Min Leverage capital requirement.

The Stress Test is a different thing and it takes into consideration the current balance sheet with the SPS mentioned.

in the meantime - Fannie & Freddie now have $103.1 BILLION net worth

and could be Consent Decree RELEASED tomorrow with ZERO mkt IMPACT

STRESS TESTS have ALREADY SHOWN the GSEs can handle ANY STORM

Serious decisions are based on rational considerations. Unfortunately, I have not heard the latter from those who make these claims. If they claim JPS are doomed, then commons would certainly be worthless because they rank lower in the capital stack. Anyone who claims that commons are superior to JPS has not done their homework. It's just affect driven blather.

Someone said jrs sell off tomorrow.

Are you serious?

Thank you.

This board is the only place I can get my DD.

It is too much to keep up with.

I check in occasionally.

I've been here since the beginning.

I always felt that the Government ripped us off, they broke laws, & always hoped that justice would return.

I know the Government doesn't care about the law.

I appreciate you stating your position & it comforts me.

That's all I can really ask for.

Thank you & the other responders.

GLTA.

GOVT destroyed Fannie-Mae and Freddie-Macs value

Catman does not want to talk about the GOVT going out of its way to destroy Fannie and Freddies corporate value.

You have to want to restore these companies value not just blow out hot air about it.

You start by eliminating Mnuchin / Calabria phony liquidation preference they created out of thin air. That will restore HUGE value to both companies. Then its on to the next step.

What a piece of work that guy is.

Justice Neil Gorsuch had concerns about the Chevron Doctrine Deference in 2016:

"No. 14-9585, Gutierrez-Brizuela v. Lynch

GORSUCH, Circuit Judge, concurring.

There’s an elephant in the room with us today. We have studiously

attempted to work our way around it and even left it unremarked. But the fact is

Chevron and Brand X permit executive bureaucracies to swallow huge amounts of

core judicial and legislative power and concentrate federal power in a way that

seems more than a little difficult to square with the Constitution of the framers’

design. Maybe the time has come to face the behemoth."

Thank you, kinda what I thought. There's way to much information for me to decipher.

I'll just keep holding.

Thanks.

loot children’s education fund that one saved with hard work so as to self fund their child’s education. sick. or should have just stick it to govt, they are forgiving 400 billion in student loans.

spend spend spend..

https://www.gao.gov/products/gao-23-106201

"You should also pity all the investors of the The Growth Fund of America like my kids 529 plan who were investors in the GFA via the Commonwealth of Virginia 529 Plan. GFA were very large investors of GSE common and preferred as the GSEs sold new JPS in April and May of 2008"

don't listen , lot of bull here. answer is no one knows.

Someone said jrs sell off tomorrow.

Are you serious?

Buy both commons and jps.

I don't have a clue,

Commons, buy, sell or hold.

Please.

Thank you.

Everyone should get to blow up a hedge fund once ... Just call it a mulligan. Lolololol

https://www.reuters.com/article/us-hedgefunds-ackman-gotham-idUSTRE69D2OH20101014

The clown Ackman dropped his case? No way! Lololol

That's exactly why I'm here.

https://www.cnn.com/2022/04/21/investing/bill-ackman-sells-netflix-stock/index.html

https://finance.yahoo.com/news/bill-ackman-lost-7-7-222837178.html

He's almost as good as Cramer... Lolol

It was a very simplistic section, as if judges don't know when they are paying interest and/or when they're receiving dividends.

I don't buy that simpleton excuse: "I didn't know" coming from a University grad judge.

FNMA

Pagliara dropped his case. Berkovitz abandoned the ship. Not much confidence shown by leaders of jps.

Meanwhile, Bryndon Fisher continues to fight.

Yeah. The takings cases have largely been dismissed and have died. Ackman dropped his. What is left is a 4th down 0.01 seconds left play action pass play 99 yards away from the endzone for one of the worst teams in football against one of the best where a touchdown only ties the game

No big surprise there. I feel bad for Bradford and the PagMan.

Sell JPS, Litigation Date has passed, Court stuff Familymag et al pumps is BS.

Strong Sell JPS

Are you suggesting there aren't any takings cases still alive?

Jr Preferred BIG SELL OFF TOMORROW!

Are you suggesting there aren't any takings cases still alive?

Wazee?

Kelly?

What is the highest court in the land where all lower courts must defer to precedent?

Where do all lower court decisions ultimately have potential to appeal?

JPs Sell Off Tomorrow. Paid JPS Pumpers Going Crazy With Usual Propaganda Over Weekend…

JPS Strong Sell

Took the Sacketts, 16 YEARS to try to build their Retirement House not on but near the Lake:

"CASE STORY

In 2007, Chantell and Mike Sackett started to build a home on land they own near Priest Lake, Idaho. Then officials from the Environmental Protection Agency showed up unannounced and demanded the Sacketts stop construction, kicking off a 16-year legal battle that reached the Supreme Court twice."

https://pacificlegal.org/case/sackett-v-environmental-protection-agency/

Here's some pictures of the land:

https://www.flickr.com/photos/pacificlegalfoundation/sets/72177720301408375/

|

Followers

|

2301

|

Posters

|

|

|

Posts (Today)

|

3

|

Posts (Total)

|

793298

|

|

Created

|

07/14/08

|

Type

|

Free

|

| Moderators not one red cent ~NORC~ stockprofitter Ace Trader Patswil jeddiemack FOFreddie | |||

| Volume | |

| Day Range: | |

| Bid Price | |

| Ask Price | |

| Last Trade Time: |