News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

New all-time high (eom).

HEP DART presentations 3 -7 Dec 2017

http://www.natap.org/

Pan Genotypic Direct Acting Antivirals:

Opportunity to Achieve HCV Elimination

http://regist2.virology-education.com/presentations/2017/HEPDART/50_Asselah.pdf

(my comment~Willy)

This presentation seems to validate that Mavyret holds it's own against the Gilead regimens, and perhaps in less time than Gilead's.

We can all have our opinions from reading boards, yahoo, Seeking Alpha, etc, but this is what is being distributed amoungst public health officials and world class hepatologists.

Gilead has a great program. Abbvie/ENTA's seems to be every bit as good, is shorter duration in some cases, more simple and perhaps suited towards mass use by less qualified doctors.

I know that some people are concerned about the Mavyret price being too low, but the velocity of HCV treatments is possibly changing, now due to lower prices, easier shorter treatments, and the certainty that treating earlier means avoidance of the more expensive HCC and cirrhosis issues which result in waiting.

Higher volume of treatments may offset the lower pricing. It is certainly true that the barriers of liver damage staging are being dropped.

There was a time that it made sense to await the next better treatment or the next price decrease. It doesn't appear that *new* improvements are coming, and perhaps, the prices have stabilized now; more price cuts may not be forthcoming.

ENTA’s FY2017 10-K has been filed:

https://www.sec.gov/Archives/edgar/data/1177648/000156459017024794/enta-10k_20170930.htm

I just added shares at $45.51, FWIW.

I concur that investors are ascribing no value to ENTA's wholly owned pipeline.

I thought the magnitude of today's selloff was unwarranted given my view of ENTA’s prospects for the next couple of years and beyond.

I thought the magnitude of today's selloff was unwarranted given my view of ENTA’s prospects for the next couple of years and beyond.

Some investors may have misread yesterday's press release and conflated ENTA’s guidance for FY2018 gross operating expenses with guidance for FY2018 cash burn, which was not given. (ENTA can’t give guidance for cash burn since they don’t yet know what the royalty income from ABBV will be; i.e., ABBV has not yet given guidance for Mavyret sales on which ENTA's royalties will be based.)

The exact price I paid for today's purchase does not have any intrinsic meaning—it's simply what I was able to get.

Looks like a good price so far.

Was it based on any history ?

I only trade at the close.

Thanks for your trading info.

Transcript of ENTA FY4Q17 CC:

https://finance.yahoo.com/news/edited-transcript-enta-earnings-conference-044530044.html

Nothing out of the ordinary.

I just added shares at $45.51, FWIW.

The market seems to dislike the conference call

Trend 1

Sorry but Net Income is a complete red herring for ENTA. Sure, it is "profitable" so that is comforting...but not really that useful. What really matters is the revenues, particularly the adoption of the 2nd gen product - as this translates into a long stream of royalties (100% margin). Plus that the R&D spend is kept in check & naturally that the data is promising.

If ENTA closed the R&D the Net Income figure would go parabolic..

Enanta expects that its current cash, cash equivalents and marketable securities will be sufficient to meet the anticipated cash requirements of its existing business and development programs for the foreseeable future.

Financial Guidance for Fiscal Year Ending September 30, 2018

• Research and development expense between $90 million and $110 million

• General and administration expense between $22 million and $28 million

Net income for the three months ended September 30, 2017 was $36.5 million, or $1.86 per diluted common share, compared to a net loss of $1.8 million, or $(0.09) per diluted common share, for the corresponding period in 2016.

For the twelve months ended September 30, 2017, net income was $17.7 million, or $0.91 per diluted common share, compared to net income of $21.7 million, or $1.13 per diluted common share, for the corresponding period in 2016.

source current report

ENTA FY4Q17 results:

https://finance.yahoo.com/news/enanta-pharmaceuticals-reports-financial-results-210100859.html

CC at 4:40pm ET.

Mavyret US scripts—week ending 11/10/17: #msg-136327955.

The big picture is the stock is currently moving up.

Pretty new to this. Not sure how to read it. Appreciate any assistance. Don't need details more a big picture concept. Thanks!

You must know how to read charts.

It just shows the current trend of ENTA

What does this mean?

Earnings Per Share (EPS) = 1.14

Mavyret US scripts—week ending 11/3/17: #msg-136101015.

No news that I'm aware of.

Mavyret US scripts—week ending 10/27/17: #msg-135920382.

No—still searching for an explanation.

Dew did you ever come up with an acceptable conclusion for this sale?

ABBV reduces ENTA equity stake slightly: #msg-135761339.

Mavyret will have peak annual sales of “multi-billions,” says ABBV CEO, Rick Gonzales on today's 3Q17 CC.

Mavyret 3Q17 sales (partial quarter) ~$100M: #msg-135740870.

The EDP-305 phase-1/1b data are everything investors could have wanted at this stage, IMO.

The phase-2 trial in NASH patients, which begins in 2018, will be the first test of efficacy.

ENTA reports phase-1/1b data for EDP-305:

#msg-135609371

The phase-1 portion of the trial dosed healthy volunteers; the phase-1b portion of the trial dosed patients with presumed NAFLD, based on metabolic parameters.

Dew, any thoughts on the data? Or too early?

http://ir.enanta.com/news-releases/news-release-details/enanta-pharmaceuticals-announces-positive-phase-1-ab-clinical

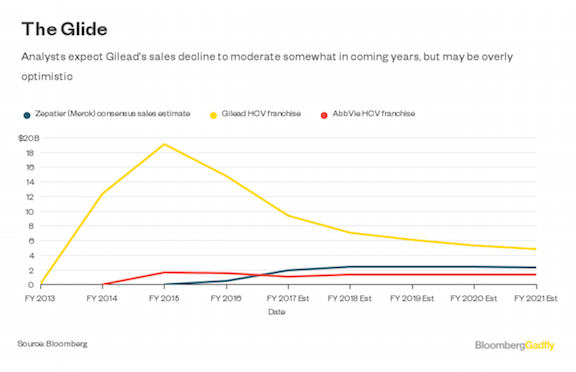

Caution: My 40% number represents patient share, not dollar share, so the numbers on the chart are not directly comparable.

Still, a 40% patient share ought to translate into a dollar share of more than 17%.

I saw it in an article recently but couldn't locate the article so I googled hep c charts and was able to find it.

Thanks. Where did you find that chart?

Judging by this Bloomberg chart, 'analyst' aren't expecting anything close to 40% so there is significant upside at 40%.

This chart suggest something closer to 17%

Note I do not know when this chart was created but I believe it being fairly recent

AASLD full-text presentations should be available at:

http://aasldpubs.onlinelibrary.wiley.com/hub/issue/10.1002/hep.v66.S1/

So is the data accessible? Or will it actually be presented Monday morning?

ENTA’s EDP-305 presentations at AASLD:

https://finance.yahoo.com/news/enanta-pharmaceuticals-present-preclinical-data-120200005.html

Yes, I think it does.

Doesn't that imply significant upside to ENTA, on that alone?

Mavyret should be able to get a 40% worldwide market share in due course (IMO). I don't know how my number compares to the consensus.

Mavyret scripts for week ending 10/13/17: #msg-135560245.

What's your low estimate guess on where market share will end up at compared to market (via enta sp) expectations? I know it is approximate but give it a shot.

(EDIT)You might be interested in AASLD abstract #205

I don't know what is permissible to post as pertains to embargo

|

Followers

|

98

|

Posters

|

|

|

Posts (Today)

|

1

|

Posts (Total)

|

3310

|

|

Created

|

03/20/13

|

Type

|

Free

|

| Moderators DewDiligence | |||

| Volume | |

| Day Range: | |

| Bid Price | |

| Ask Price | |

| Last Trade Time: |