News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Church & Dwight -- >>> The 6 Key Metrics of Church & Dwight

By Adam Levy

May 15, 2013

http://beta.fool.com/adamlevy/2013/05/15/the-6-key-metrics-of-church-dwight/34421/?source=eogyholnk0000001

Last year, Church & Dwight (NYSE: CHD) CEO Jim Craigie focused on six key metrics he wanted to improve throughout the year. He called the initiative “fix the six.” After a successful 2012 saw the company’s stock climb 20%, shares have nearly added another 20%.

Most of this success can be attributed to Craigie’s initiative last year to fix the six. The company has kept it up so far in 2013. Here’s how the six stack up in the company’s most recent earnings report.

Organic revenue growth

Organic sales improved 2% in the most recent quarter. This comes on top of a record high 8.4% sales growth in the same period last year. The driving force behind the organic sales expansion was all volume, which increased 2.4%. 40 basis points were lost to negative product mix and pricing.

Once again, the company is growing much faster internationally than domestically. Organic sales improved 5.2% outside the U.S., with great success in Mexico, the U.K, and Australia.

The international market has huge potential for Church & Dwight as it currently derives just 20.7% of its revenue from outside the United States. Comparatively, Procter & Gamble (NYSE: PG) derives more than 60% of its revenue from abroad.

P&G has been rapidly expanding into emerging markets in the last decade, and now Church & Dwight is working to catch up. Its strong revenue growth abroad is a great sign that the company can compete with the market leader as it continues its international expansion.

Margins

Church & Dwight continued to improve its margins in the first quarter of 2013. For the first quarter the company reported gross margin of 44.9%, a 110 basis point expansion from the first quarter of 2012. That number, however, still remains well below its competitors, Procter & Gamble and Colgate-Palmolive, which both sport gross margins over 50%.

Still, the company is on a path to reach those levels. The company recently completed a new laundry detergent production plant that increased productivity, and has had a positive effect on gross margin.

The company also gained gross margin advantages from better than expected sales of its high-margin personal care brands as well as faster than expected cost savings on its Avid Health acquisition.

As a result, the company expects gross margin to continue to expand in 2013 by 25 to 50 basis points as opposed to its previous guidance of flat.

Operating margin, the third metric of the six, increased 100 basis points year-over-year to 20.7% - a company record. That significantly outperformed P&G’s operating margin of 16.5% last quarter, and is better than every single one of P&G’s previous four quarters.

So, where Church & Dwight still lags the competition in gross margins, the company makes up for it with lower operating expenses. Which brings me to the next metric …

Overhead costs

Church & Dwight currently has the highest revenue per employee of any company in the consumer packaged goods space. SG&A costs contracted 20 basis points last quarter compared to the year prior to 13.1% of sales. The Avid acquisition helped keep that number low, as it added sales with minimal overhead.

Comparatively, Procter & Gamble’s SG&A costs expanded 40 basis points last quarter as a percentage of net sales. P&G’s high overhead costs are typically about one-third of its sales.

The ability of Church & Dwight to operate efficiently is one of its greatest strengths, and it looks like that trend will continue for some time.

Market share

The company’s eight “power brands” performed very well in the first quarter with 7 out of 8 expanding market share.

Three factors contributed to the success. First, the company reinvested some of its increased profits from its value brands into increased marketing support. Marketing support expanded by 30 basis points last quarter, and is typical of the kind of marketing force Craigie has used recently to expand market share.

Second, the company has introduced several new products, mostly capitalizing on underserved niche markets. These products not only serve a market with practically no competition, they also have the added benefit of high margins. Examples include single dose cold sore treatments, toothbrushes that play One Direction songs, super high concentrated laundry detergent, and adult toys from its Trojan brand.

And the last factor is the company’s ability to increase distribution. The company has worked closely with key retailers to expand shelf space for its products, which helps increase visibility, and minimize out of stocks.

As the company continues to support its most profitable brands with expanded marketing efforts, generate new products, and improve distribution, market share ought to continue growing.

Earnings

Earnings, while not exactly an afterthought, is simply a result of the company’s focus on the first five metrics. With the growth in sales, margins, market share, and reduction in overhead costs, earnings improved more than analysts expected.

In fact, this seems to be the trend, as Church & Dwight has beaten analysts estimates for 9 straight quarters. Last quarter, the company reported earnings of $0.76 per share, $0.04 better than analysts’ expectations.

For the year, the company expects to grow earnings 14% to $2.79 per share, but I wouldn’t be surprised if the company eeks out a few cents more. The first quarter was fantastic, and analysts currently expect a penny more.

The company has plenty of opportunities to continue its fantastic growth of the past few years, and with Jim Craigie’s focus on these six metrics I expect that to continue.

Strong international sales will fuel revenue expansion as the company improves margins and reduces overhead. Meanwhile, the company will continue expanding market share of its power brands in the States through increased marketing spend and the introduction of new products. All this ought to lead to further earnings growth, which means a good return for investors.

<<<

Craft Brew Alliance -- >>> 3 Stocks To Take Advantage Of Craft Beer's Popularity

May 12 2013

by: Kapitall

includes: BREW, SAM, TAP

http://seekingalpha.com/article/1428071-3-stocks-to-take-advantage-of-craft-beer-s-popularity?source=yahoo

Business relationship disclosure: Business relationship disclosure: Kapitall is a team of analysts. This article was written by Emily Smykal, one of our writers. We did not receive compensation for this article (other than from Seeking Alpha), and we have no business relationship with any company whose stock is mentioned in this article.

This list provides a closer look at some of the biggest names in the American craft beer industry - companies selling popular brands such as Redhook Ale, Samuel Adams and Blue Moon

According to the Brewers Association, the entire US beer market as of 2012 was worth roughly $99 billion and grew by 1% over the previous year. This amounted to 200,028,520 barrels of beer (where 1 barrel = 31 US gallons).

As reported on Kapitall Wire, craft brewers made strong gains within the beer industry, growing 17 by dollars and 15% by volume, versus 15% by dollars and 13% by volume in 2011.

And the craft brewing market experiences healthy rates of openings and low rates of closures. According to the Brewers Association, 409 breweries opened and just 43 closed as of March 18, 2013. Overall in 2012 there were 2,347 craft breweries, microbreweries and brewpubs in operation.

Craft brewers are also expanding into foreign markets. 2012 saw an increase in export volume of craft beer of 72% over 2011, with an approximate value of $49.1 million.

The List

Technically, a craft brewer is any brewery producing 6 million barrels of beer or less per year, where an alcoholic beverage industry member (who is not a craft brewer) owns or controls less than 25% of the craft brewery.

The somewhat loose definition of a craft brewer means beers produced by certain well known and publicly traded names fall into the category, allowing the average investor to make a play in the craft beer market even if the stock they are buying is not a craft brew company itself.

The list below includes more detailed financial data for three big players in the craft brewery industry.

For an interactive version of this chart, click on the image below. Analyst ratings sourced from Zacks Investment Research.

The demand for craft brews is on the rise - are these names poised to lead the trend? Use this list as a starting point for your own analysis.

1. Craft Brew Alliance, Inc. (BREW): Produces craft-brewed beers. Brands include Redhook Ale Brewery, Widmer Brothers Brewing, Kona Brewing Co, Omission Beer.

Market cap at $140.50M, most recent closing price at $7.43.

P/E: 61.54, Forward P/E: 29.63

PEG: 3.08

Total Debt/Equity: 0.12

52-Week High: -15.47%

BREW has produced great gains over the last month, but dropped about 50 cents on Thursday after reporting first quarter losses on slumping beer shipment. Chief executive Terry Michaelson reconfirmed expectations that revenues and earnings in 2013 would exceed 2012 levels. "The company said growth would be driven by stronger sales of Kona, Redhook and Omission brands, along with a new Redhook label called Game Changer and a new Square Mile cider. New packaging also is planned."

BREW has a higher than average projected earnings growth rate over the next 5 years (20.0%). This is higher than competitors such as ABV (projected EPS growth over next 5 years at 7.74%) and TAP (projected EPS growth over next 5 years at 4.80%).

Based on conventional valuation ratios, BREW looks cheap relative to industry peers. The stock's PEG ratio stands at 3.08, while its Price/Cash ratio stands at 30.2. Even on a Price to Free Cash Flow basis the stock looks cheap, with a ratio of 38.11, compared to FMX (P/FCF ratio at 47.86) and ABV (P/FCF ratio at 63).

At the end of 2012, BREW reported its brands would become available in European and Asian markets thanks to an exclusive distribution agreement with CraftCanTravel, the US market's first full service exporting company focusing on American craft beer. Distribution is currently taking place in countries including China, Hong Kong, Japan, Holland, Ireland and the United Kingdom.

2. Boston Beer Co. Inc. (SAM): Produces and sells alcohol beverages primarily in the United States, Canada, Europe, Israel, the Caribbean, the Pacific Rim, and Mexico. Craft brands include Samuel Adams, with 50+ seasonal and small batch varieties.

Market cap at $1.87B, most recent closing price at $145.22.

P/E: 34.11, Forward P/E: 26.71

PEG: 3.41

Total Debt/Equity: 0

52-Week High: -15.18%

When comparing valuation ratios to industry averages, SAM looks expensive. The stock's Price / Free Cash Flow ratio stands at 270.94, much higher than BREW (P/FCF ratio at 38.11), BUD (P/FCF ratio at 24.66) and TAP (P/FCF ratio at 17.13).

Short sellers think there's more downside to the stock, especially when comparing short float to industry averages. SAM short float stands at 18.78%, which is equivalent to 16.52 days of average trading volume. As an example, this is much higher than FMX (short float at 0.12%, representing 0.67 days of trading volume) and BUD (short float at 0.33%, representing 1.14 days of trading volume). Competitor BREW, while still lower, comes closer with a short float at 3.03%, equivalent to 10.35 days of average trading volume.

SAM has placed a large emphasis on seasonal brews, and The Motley Fool explains how their most recent earnings report demonstrated that this strategy is not always foolproof. Sales of the company's spring varieties fell below expectations, yet SAM has already moved on to summer ale, spending an additional $7.2M on advertising and selling.

Despite a downgrade from Credit Agricole on Thursday May 9, their target price of $170 (up from their previous target of $165) represents a 17% upside from current levels. Williams Capital also downgraded shares to market perform but increased targets from $130 to $150 (3.29% potential upside from most recent closing price). Meanwhile, USB did Boston Beer no favors when it increased their target price from $117 to $143, a -1.5% potential downside from recent closing price.

Looking beyond the traditional craft brewer:

Molson Coors Brewing Company (TAP) is one of the world's largest brewers by volume, and does not fit the traditional model of a craft brewer. However, TAP clearly recognizes the great potential in controlling craft beer names, as reported by Bloomberg. TAP currently produces Blue Moon, a popular Belgian-style beer that has been expanded to include over a dozen different varieties. And the company created a division to help develop and acquire more craft brands, called Tenth & Blake Beer Co., which has recently had discussions with at least 20 craft brewers. As the company's well known Miller Lite label continues to lose market share, more craft beers may help give the stock a much needed boost.

3. Molson Coors Brewing Company: Distributes beer brands. Craft brands include Blue Moon and its varieties, Batch 19, Third Shift Amber Lager, Colorado Native.

Market cap at $9.03B, most recent closing price at $49.49.

P/E: 20.45, Forward P/E: 11.61

PEG: 4.26

Total Debt/Equity: 0.59

52-Week High: -6.65%

TAP has recorded a weak performance over the last month, returning -1.23% since 4/8/13. The stock is falling behind companies like Compania Cervecerias Unidas S.A. and Anheuser-Busch InBev , which returned 1.82% and 0.78% respectively, during the same time period.

The company has reported disappointing earnings growth over the last year, with EPS falling by -32.84%, lower than industry peers such as SAM (EPS growth over the last year at -7.93%) and ABV (EPS growth over the last year at -13.49%). Yet VCO, BREW and FMX reported even lower rates, at -40.53%, -73.83% and -81.54% respectively.

And TAP has a lower than average projected earnings growth rate over the next 5 years (4.80%). This is significantly below analyst projections for FMX (projected EPS growth over next 5 years at 12.59%) and CCU (projected EPS growth over next 5 years at 10.90%).

On Wednesday, Zacks analysts wrote "Overall, we are encouraged with the company's strong brand portfolio, continuous innovation and cost-saving initiatives... However, the slow recovery of U.S. economy and uncertainties in Europe undermine Molson Coors' growth prospects and profitability." It gave the brewer a $53 target price and restated its neutral rating on the stock. Analysts at Nomura are more optimistic. They raised their target price from $55.00 to $61.00 in a research note to investors on Tuesday, April 9th. Goldman also increased target price to $63.00 per share from $47.00. This respectively represents 7.09%, 11.13% and 27.29% upside from the current prices.

*All accounting data sourced from Google Finance, EPS data sourced from Yahoo! Finance, all other data sourced from Finviz.

<<<

McDonalds, Church & Dwight -- >>> Don’t Make Investing Too Complicated

By Matthew Luke

May 10, 2013

Tickers: ABT, ABBV, BEAM, CHD, MCD

http://beta.fool.com/whichstockswork/2013/05/10/dont-make-investing-too-complicated/33940/?source=eogyholnk0000001

If I could send a message back in time to my younger self, I would only need to use four words, “Keep it simple, Stupid!” This is great advice for life in general, but especially good advice when investing one’s own money. How much better would my stock portfolio would look today if I had realized this when I first began investing!

Sometimes we as investors can fall into the trap of associating complexity with a good investment. The more complicated an investment however, the more things can go wrong. Often it is simplicity that can be most consistently associated with good long-term investing. If I could have taught my younger self this lesson, I may have looked for investments that resembled these four:

Simple Liquor

Before October 2011, the simple company now known as Beam (NYSE: BEAM) was part of the overly-complex golf equipment, home products, security products and liquor conglomerate, Fortune Brands. Fortune Brands was a company with such a diversity of product-types that it actually hurt the company as a possible investment. Current and potential investors were unable to properly value a company that sold everything from golf shoes and sink faucets to pad locks and bottles of bourbon. Fortune Brands was a great example of needless complexity getting in the way of investors making a lot of money.

Since selling and spinning-off its various unrelated divisions, the renamed Beam has become a much simpler company and a much better investment opportunity. Previously a very bourbon-centric company, Beam has made many small accretive acquisitions in the past few years to give it greater exposure to the fast-growing liquor categories such as flavored vodka and Irish whiskey, as well its Skinnygirl brand, which has become one of the fastest-growing liquor brands in the United States. Times have been so good for Beam lately that they are currently facing supply problems with their Maker’s Mark brand due to a surge in overseas demand. While supply problems are never good, being supply constrained because your product is so incredibly popular is high-quality problem to have. If only more complicated companies saw the benefits that simplicity brings to a business.

Simple Consumer Goods

Consumer goods have always been a pillar of safe long-term investing. Toothpaste, deodorant, soap, laundry detergent; these are the types of relatively simple products that are some of life’s necessities, bought in good economic conditions and bad. And Church & Dwight (NYSE: CHD) has been one of the consumer goods industry’s best preforms over the past 10 years.

The management team has done an excellent job over the past decade of transforming Church & Dwight from a mostly single-brand company (Arm & Hammer) into a company with 7 ‘Power Brands’ that now occupy the No. 1 position in their respective product categories (and an 8th Power Brand that is also doing very well for itself). Current and a century of past management teams also have an impressive record of returning money to shareholders. This month, company management declared their 449th regular quarterly dividend, or just over 112 years of uninterrupted dividend payments.

Simple Healthcare

Abbott Laboratories (NYSE: ABT) is another good example of a company that simplified its complicated investment thesis by breaking itself up into two separate companies. In January, Abbott Laboratories completed the separation of AbbVie (NYSE: ABBV), which comprises Abbott’s old drug discovery pharmaceuticals division. Abbott Laboratories itself was left with the company’s medical device, diagnostics and nutritionals divisions.

Although the newly-separated AbbVie’s share price has outperformed Abbott Laboratories thus far post-split, Abbott Laboratories’ business should be the more consistent and faster-growing of the two going forward. Trying to discover the next multi-billion dollar blockbuster drug is a tall order for any pharmaceuticals company. And AbbVie currently has very little in the development pipeline to fuel future growth (as well as the patent expiration of Humira coming in 2016). For Abbott Laboratories though, long-term growth prospects are clearly visible with its exposure to emerging market countries such as China and India. This is particularly true for Abbott’s nutritionals division, which now makes up about 30% of Abbott’s sales and includes high-growth emerging market product categories such as baby formula.

Simple Fast Food

McDonald’s (NYSE: MCD) is a much simpler company than some give it credit for. Although many consider McDonald’s to be a global restaurant operator, an argument can be made that McDonald’s is actually a fairly simple real estate operator.

When we think of McDonald’s, we probably think of the almost 70 million customers served every day, the 119 countries of operations, the nearly 2 million worldwide employees that need to be managed or all of the food that needs to be sourced for each of its 33,000 worldwide restaurant locations. All of that all sounds like a rather complicated business undertaking. That is until you consider that approximately 82% of those 33,000 locations are operated by franchisees. The serving, operating, managing and sourcing are actually being done by the franchisees of McDonald’s.

Under the franchise model, McDonald’s Corporation functions much like a landlord; signing tenants (franchisees) to 20-year lease (franchise) agreements. Each month McDonald’s collects monthly rent payments from their franchisees for the use of the lands and buildings that McDonald’s owns. McDonald’s also collects royalty fees and advertising fees from its franchises (12% and 4% of restaurant sales respectively). While the sales of each individual McDonald’s restaurant can vary from time to time, McDonald’s is able to predictably expect the exact same fixed-amount of rent payments 12 times a year, every year, for the next 20-years. And at the end of the 20-year agreement, McDonald’s is able to renegotiate the contract again for even higher rent payments, starting the whole process over again.

Lessons of Foolish Youth

If there is one thing I wish I had learned earlier in my youth, it is that investing need not be the complicated endeavor some make it out to be. While there is certainly money to be made investing in complicated companies with complex business models, there is also money to be made investing in simple companies with simple business models. A very good lesson to learn, even if it took a little while to learn it.

<<<

B&G Foods -- >>> B&G Foods Acquires TrueNorth Brand

May 13, 2013

By Zacks Equity Research

http://finance.yahoo.com/news/b-g-foods-acquires-truenorth-153002773.html

Packaged food company, B&G Foods, Inc. (BGS) recently acquired the TrueNorth brand from DeMet’s Candy Company. With the growing importance of nutritious snacking, TrueNorth is a healthy addition to B&G Foods’ snacks portfolio.

TrueNorth are bite sized nut clusters made of roasted nuts, with a taste of sea salt and sweetness and thus offer a healthy option for mid meal snacking. TrueNorth comes in three varieties namely Almond Pecan Crunch, Chocolate Nut Crunch and Cashew Crunch.

B&G Foods’ snacks portfolio also includes New York Style, Old London, JJ Flats and Devonsheer brands which were acquired in Oct 2013.

New York Style offers several baked products such as Mini Bagel Crisps, Pita Chips, Original Bagel Crisps, and Panetini Italian Toast. Old London, on the other hand, offers a huge variety of Melba products, such as Melba Toasts and Melba Rounds. In addition, Old London markets snacks under the names Devonsheer and JJ Flats.

B&G Foods focuses on small brands that have strong margins and generate less than $100 million in sales. Most of the time, these are smaller brands from large food companies, which have limited competition. B&G Foods’ investments in these brands help to generate huge free cash flow and ensure profitability in the long run.

B&G Foods carries a Zacks Rank #2 (Buy).

Some other consumer staple stocks that are worth a look include Flower Foods Inc. (FLO) carrying a Zacks Rank #1 (Strong Buy) and H. J. Heinz Company (HNZ) and J&J Snack Foods Corp. (JJSF) holding a Zacks Rank #2 (Buy).

<<<

J&J Snack Foods -- >>> J&J Snack Foods: Boring Company, Great Value

May 13 2013

by: Finance For Yuppies

about: JJSF, includes: CAG, K, LNCE

http://seekingalpha.com/article/1431951-j-j-snack-foods-boring-company-great-value?source=yahoo

BUSINESS DESCRIPTION

J&J Snack Foods Corporation (JJSF) sells a variety of branded and private label baked goods and food items. Soft pretzels made under the Super Pretzel and related brands are the company's flagship product and contributed 18% of the firm's revenues in 2012. Frozen juices are a declining (13% revenue) portion of the firm's business. Churros are an increasingly important part of the company's operations. Handheld "dough enrobed" product sales have almost tripled their sales (6%) over the last year largely due to the successful integration of Conagra Foods (CAG) handheld food division. Baked goods including Mrs. Good Cookie and Country Home brands, in addition to private label brands, are JJ's largest single division with 32% of sales. JJ's frozen beverage sales (16%) are primarily derived from the sale of ICEE and Slush Puppy brand drinks via 87,000 machines that it also sells and maintains (7%). The company recently acquired organic pretzel maker Kim & Scotts gourmet pretzels for $7.9m and churro maker California Churro for $24 million. JJ's products are distributed via supermarkets, restaurants, and food service companies.

INVESTMENT THESIS:

Shifting product distribution mix. Increasingly the company is shifting its product mix toward higher margin churros, pretzels, and Icee sales. In addition, JJ recently to changed its sales mix to favor retail and restaurant distribution over the price sensitive food service channel which currently accounts for 62.7% of sales. The retail distribution outlet yields higher operating margins of 12.2% versus 10.4%. In addition, in its FQ2 conference call, management mentioned a more aggressive shift to restaurant sales which are currently only approximately $20m of the company's sales, but which management has stated it can double to quintuple over the next five years.

Pristine balance sheet leaves room for financial engineering. Management has recently undertaken changes to its balance sheet that should be accretive to shareholders. Currently JJ has $188m in cash and securities on its balance sheet. Management has indicated that it will seek additional income with this cash by investing in mutual funds with an average yield of 4%. In addition, the board authorized a 500k share repurchase. With a .9% dividend yield that only costs approximately $12.6m a year in cash, estimated capital spending of only $30m in 2013, a cost of repurchase of $37m at current price levels, the company will only utilize $79.6m in cash versus an estimated $55 in free cash flow in 2013.

High probability of acquisitions. JJ's management has consistently proven that it has the ability to acquire small firms, integrate them into its distribution network, and then rapidly scale them. After Hostess' bankruptcy, JJ was one of the companies mentioned as a prospective bidder. However, the company is highly methodical about its acquisitions and will only acquire firms that fit its distribution channels and that are complementary to existing goods, thereby driving synergies. Given the company's cash balance and several instances where management has indicated it wants to pursue a substantial acquisition, it should only be a matter of time before a new acquisition is announced.

International avenues for growth. At present, the company primarily operates in the U.S. with only 2.3% of sales and 2.5% of its assets located outside the U.S., primarily in Mexico and Canada. However, international sales have been growing at an annual growth rate of over 10.8% a year (2012). The company already has dedicated sales teams and distribution centers in Canada that it can utilize to further expand its negligible footprint. Churro sales in particular could benefit from international expansion as these markets already accounted for 1/3 of JJ's total churro sales in 2012.

Valuation

The company is extremely undervalued on a DCF basis and fairly valued on a comparable basis. I used an equity risk premium of 10%, a terminal growth rate of 2%, and a WACC of 6.9%. I held 2013 income at consensus earnings of $3.41 a share, increased revenues in 2014-18 by 7% a year (which is half of the firm's 14% compound annual growth rate over the last 5 years), decreased COGS by .5% to 68.5% of sales in 2014-2015 and 67% in 2016-2018, and increased SG&A by 6% a year to reflect some SG&A leverage from greater scale. I then added back the company's $188m in cash. The resulting DCF produces a $104.68 price estimate.

On a comparable basis the company is in-line with its peers on virtually every metric. The firm's closest comp Snyder's-Lance, Inc. (LNCE) has approximately half the net margins but significantly higher income growth. Conversely, the firm's largest comp Kellogg (K) has substantially more debt as a percentage of capitalization, a comparable growth rate and margins, but a lower valuation. Therefore although the company is smaller and faster growing than the majority of its peers, I believe that the company is fairly valued on a conservative interpretation of comparables. Taking an average of the company's value on a comparable basis which is approximately the current stock price of $75.91 and the DCF value of $104.68, results in a target price of $90.29.

Comps

(click to enlarge)

INVESTMENT RISKS:

JJ's customer base is highly concentrated with its top 10 customers accounting for 43% of 2012 sales and one customer account for 8% of sales. A loss or reduction in SKU allocations from a major customer could significantly diminish the firm's revenues. Increases in the price of commodities, namely fuel and flour, can have an extremely negative impact on the company's profitability. Although the company engages in some hedging activity, a prolonged rise in prices coupled with a weak retail pricing environment could result in lower earnings. The company's founder and CEO is 70 years old. The remainder of the management team also has significant experience, but the founder's death could materially impact the firm's operations.

RECOMMENDATION & PRICE TARGET: Buy as the firm is undervalued on a DCF basis. Blended Price Target: $90.59, Current Price: $75.91, Potential Upside: 18.90%

<<<

Whole Foods - PE is 36 -- >>> Whole Foods Crafts New High

By Zacks Equity Research

May 9, 2013

http://finance.yahoo.com/news/whole-foods-crafts-high-140002602.html

Buoyed by strong second-quarter fiscal 2013 earnings, shares of Whole Foods Market, Inc. (WFM) recorded a new 52-week high of $103.72 yesterday, before closing at $102.19, and rising approximately 11.6% year to date. Based on the current price, Whole Foods is 3.6% below the Zacks Consensus average analyst price target of $106.

Moreover, it currently trades at a forward P/E of 35.6x, a 68.1% premium to the peer group average of 21.2x. Additionally, the company’s long-term estimated EPS growth rate is 17.9%, higher than the peer group average of 11.9%.

Whole Foods’ second-quarter fiscal 2013 earnings of 76 cents a share beat the Zacks Consensus Estimate of 73 cents, and surged 19% from 64 cents earned in the prior-year quarter as shoppers flocked to the grocery chain. The Austin, Texas-based company, which will undergo a two-for-one stock split later this month, also raised its earnings-per-share projection.

Management now envisions earnings between $2.86 and $2.89 per share, portraying a year-over-year jump of 13% – 15%, up from a range of $2.83 – $2.87 forecasted earlier.

Whole Foods continues to project an escalation of 10% – 11% in total sales for fiscal 2013 on the back of an expected 6.7% – 7.5% rise in comparable-store sales and 6.5% – 7.2% growth in identical-store sales.

Moreover, the company stated that for the first 3 weeks of the third quarter, comparable-store sales are witnessing healthy trends and are up 9.4%.

Zacks Rank for Whole Foods

Currently, Whole Foods carries a Zacks Rank #4 (Sell) as the comparable and identical store sales growth trend is softening. Consequently, Whole Foods narrowed the range of comparable and identical store sales growth for the fiscal year.

However, there are certain other stocks that warrant a look, such as Flowers Foods, Inc. (FLO), which holds a Zacks Rank #1 (Strong Buy) and is expected to continue with its upbeat performance. Other stocks that should be merited are J&J Snack Foods Corp. (JJSF) and The Hain Celestial Group, Inc. (HAIN), both of which sport a Zacks Rank #2 (Buy).

<<<

Compania Cervecerias Unidas, Beer Sector -- >>> Another M&A Candidate: Beer

By Federico Zaldua

May 8, 2013

Tickers: BUD, CCU, SAB

http://beta.fool.com/za0696fede/2013/05/08/another-ma-candidate-beer/33453/?source=eogyholnk0000001

The beer industry, as a part of the consumer goods industry, has a tendency towards consolidation. The reason is simple: the more share of the market a company owns, the lower its fixed costs per unit of volume sold are. Hence, your margins soar as your share of the market increases.

AB InBev (NYSE: BUD) and its owners (the Brazilian trio led by Jorge Paulo Leman) know this very well. They have consolidated the industry while making their company's margins increase for over twenty years. AB InBev is the masters of the universe in the art of cutting costs and gaining market share through acquisitions. Still, there are some markets where they do not rule. Some of those markets are dominated by their biggest competitor, SABMiller (LSE: SAB), and others are ruled by independent local companies. This companies are prone to being acquired by giants such as AB InBev or SAB Miller. Let's take a look at a company that will surely be acquired at some point in time.

I think might be the giant's next target

Compania Cervecerias Unidas (NYSE: CCU) is the company that practically owns the beer market in Chile (its market share is above 90%). Besides this, the company also enjoys a 23% market share in Argentina, its second biggest market by volume. The company is efficiently managed and could provide AB InBev or SABMiller with one market that they cannot access on their own (barriers to entry are huge when a player has such a high share of the market). The deal could actually make more sense for SABMiller since the company doesn't have a sizable business in Argentina, where AB InBev rules the beer business with a +75% market share.

CCU (as the company is known in its country) is doing great. During the first quarter, volumes went up 9.7% Year over Year (YoY), and 3.0% YoY excluding the acquisition of Manantial in Chile and Uruguay (soft drinks). Moreover, consolidated revenues increased 8% YoY due to higher volumes, but with 1.5% lower average prices YoY.

Most importantly, trading at 2013 17.5x P/E and 9.2x EV/EBITDA, the company doesn't seem awfully expensive. AB InBev trades at 2013 12.9x EV/EBITDA, while SABMiller trades at an expected 15.4x EV/EBITDA.

I think CCU is a great target for bigger brewers looking to gain new monopolies: it trades at reasonable multiples and it would give those beer giants the possibility of selling parts of the company they might not want (such as the wine division CCU controls). Across Latin America, AB InBev and SABMiller have been distributing different markets between themselves. While Colombia and Peru are almost completely controlled by SABMiller, Argentina, Bolivia, Uruguay and Paraguay belong to AB InBev. Chile is the only market within the region that these two giants cant control. I would make a bet that it will not be long until one of these two cash-rich global brewers make a compelling offer for CCU. After all, interest rates will not stay at zero forever, and cheap long term financing is always key for any multi-billion dollar deal (CCU's current market capitalization is $5.3 billion).

<<<

Church & Dwight, Hormel, Campbell Soup -- >>> 3 Great Consumer Staples Stocks Flying Under The Radar

By Robert Ciura

May 7, 2013|

Tickers: CPB, CHD, HRL

http://beta.fool.com/rciura/2013/05/07/3-great-consumer-staples-stocks-flying-under-the-r/33652/?source=eogyholnk0000001

Most income investors are well-aware of the benefits of dividend investing. Those quarterly checks provide stability and guaranteed returns in an era of high-frequency trading, geopolitical unrest, and volatile markets.

The consumer staples sector in particular is a haven for those who enjoy receiving solid dividend yields. However, while most investors are fully aware of the market’s biggest consumer staples giants, there are a few stocks with much smaller market values, below $15 billion, that might be flying under your radar.

Three great consumer staples companies

Church & Dwight (NYSE: CHD) manufactures and markets a wide range of personal care, household, and specialty products under the Arm & Hammer brand name, as well as others. The company flies under the wings of its mega-cap consumer staples giant peers, but the company’s solid brands and steady operating performance make it worthy of consideration in its own right.

The company has a spectacular track record of distributing profits to shareholders via dividends. The company recently declared its 449th consecutive quarterly dividend payment.

Of course, this long streak of dividend payments can’t be sustained without the underlying operating performance to back it up, which is an area of strength for Church & Dwight that continued during the first quarter. The company reported nearly 13% growth in net sales and 15% earnings per share growth during the first three months of the year versus the same period in 2012.

Hormel Foods (NYSE: HRL) has a market capitalization of $11 billion and a dividend yield of about 1.6%. Hormel was founded in 1891, and has since sold its flagship Spam and Hormel Chili to consumers. However, the company has broadened its product portfolio over the years. The company holds the Jennie-O brand, and earlier this year announced the acquisition of the Skippy peanut butter line.

Hormel has reported steady operating performance, indicative of its solid brands and diversified product portfolio. Recently, the company reported fiscal first-quarter sales of $2.1 billion, representing 4% growth year over year. This was largely attributable to a 2% increase in volumes as opposed to the first quarter of 2012.

Moreover, Hormel has an enviable dividend track record: the company has provided investors an astounding 47 consecutive years of dividend increases.

Campbell Soup (NYSE: CPB) is a $15 billion dollar company with a dividend yield in excess of 2.5%. The company has a long operating history that stretches back more than 140 years. Campbell offers consumers its namesake soup products, as well as a diversified portfolio, including the Pepperidge Farm and V8 brands. Although revenues and earnings were basically flat in 2012 versus 2011, Campbell did come through with a dividend increase.

In February, the company offered investors a solid quarterly report. Sales grew 10% during the second quarter to $2.33 billion. In addition, the company reported that its adjusted earnings per share increased 8% during the first half of the year.

The Foolish bottom line

These stocks provide the best of what the consumer staples sector has to offer: reliable sales and profits, as a result of products that are sold no matter the condition of the broader economy. In turn, investors also receive those quarterly dividend payments that are so valuable to income investors.

It’s worth noting that each of these stocks carries a trailing price-to-earnings ratio that is near or exceeds 20 times, a level that is above the P/E ratio on the broader market. The S&P 500 Index currently trades for roughly 18 times earnings, meaning these stocks are slightly more expensive than the broader market.

However, these companies have smaller market capitalizations than their juggernaut competitors and predictable business models that justify their higher valuations.

In addition, Hormel, Church & Dwight, and Campbell have extremely long histories of paying (and raising) payouts to shareholders. For investors interested in the consumer staples sector who are bored with the usual suspects, these under-the-radar, high-quality companies are worth a closer look.

<<<

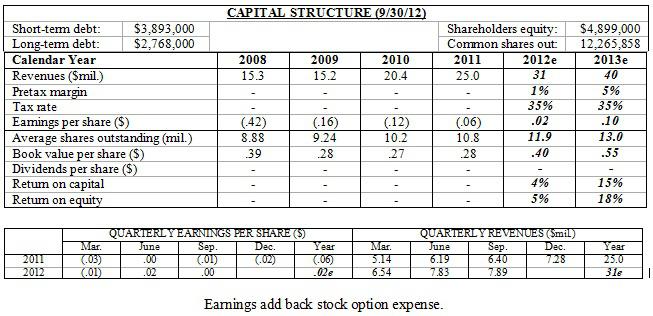

Reeds -- >>> Revenue summary by quarter (see below) -

Q1-2013 revs were up approx 3-4% from last quarter, but up 24% YOY. Revs were flat during in the 2nd half of 2012, and in the March 25 conf call Chris explained that private label revenues from a single customer in Q4-2012 were lower than anticipated, plus some Kombucha was returned due to earlier batches having conservative shelf life dating. He also said the Kombucha rollout has involved a high level of promotions.

But Chris projected that by late 2013 the run rate for Kombucha should be approaching $7-8 mil per year (approx 30,000 cases/month). In addition to the original 4 flavors, and the additional 4 flavors announced in February, there are several more flavors in the works and also new brighter labels are now on the Kombuchas. He also said that 3 significant new private labels will contribute in 2013 (one was announced April 23).

Significantly, Chis also said that many stores that have said yes to Kombucha will start carrying it in the April/May period when they do their annual re-configuration of products carried.

Revenue summary by quarter -

Q1-2013 -- 8.0 - 8.1 mil (approx)

____________________________

Q4-2012 -- 7.8 mil

Q3-2012-- 7.888 mil

Q2-2012 -- 7.831 mil

Q1-2012 -- 6.539 mil

_____________________________

Q4-2011 -- 7.282 mil

Q3-2011 -- 6.4 mil

Q2-2011 -- 6.2 mil

Q1-2011 -- 5.1 mil

______________________________

Q4-2010 -- 6.0 mil

Q3-2010 -- 5.5 mil

Q2-2010 -- 4.9 mil

Q1-2010 -- 4.0 mil

___________________________

Revenues by year -

2012 - 30 mil

2011 - 25 mil

2010 - 20.4 mil

2009 - 15.2 mil

___________________________

Reeds -- >>> Reed's Inc. 1st Quarter 2013 Revenues Increase 24%

Press Release: Reed's, Inc.

http://finance.yahoo.com/news/reeds-inc-1st-quarter-2013-123000478.html

LOS ANGELES, CA--(Marketwired - May 7, 2013) - Reed's, Inc. (NYSE MKT: REED), maker of the top-selling sodas in natural food stores nationwide, today announced its revenues for its first quarter ended March 31, 2013, and its earnings release date of May 14, 2013.

Revenues for the first quarter of 2013 increased 24% to over $8 million from $6.5 million in the first quarter of 2012. Chris Reed, Founder and CEO, stated, "This is our fourth year of significant growth. Our revenue goals for this first quarter were exceeded and indicate the strength of our continued growth momentum. This is an exciting year unfolding as we continue to expand revenues with our core brands of Reed's Ginger Brews and Virgil's Natural Sodas. Our new Reed's Culture Club Kombucha line of live probiotic cultured teas continues to roll out and gain acceptance. In addition, we continue to develop significant new private label production opportunities. We anticipate continued strong growth for the rest of 2013."

The Company will conduct a conference call @ 4:15PM EST on May 14th to discuss its 2013 first quarter results and outlook for the future. To participate in the call, please dial the following number 5 to 10 minutes prior to the scheduled call time (866) 240-5139. International callers should dial (713) 481-0091.

A replay will be available within a few days after the conference call in the investor relations section of the Company's website at: http://www.reedsinc.com/investor-relations/.

About Reed's, Inc.

Reed's, Inc. makes the top-selling natural sodas in the natural foods industry sold in over 13,000 natural food markets and supermarkets nationwide. Its six award-winning non-alcoholic Ginger Brews are unique in the beverage industry, being brewed, not manufactured and using fresh ginger, spices and fruits in a brewing process that predates commercial soft drinks. The Company owns the top-selling root beer line in natural foods, the Virgil's Root Beer product line, and the top-selling cola line in natural foods, the China Cola product line. In 2012, the Company launched Reed's Culture Club Kombucha line of organic live beverages. Other product lines include: Reed's Ginger Candies and Reed's Ginger Ice Creams. In 2009, Reed's started producing private label natural beverages for select national chains. Reed's products are sold through specialty gourmet and natural food stores, mainstream supermarket chains, retail stores and restaurants nationwide, and in Canada, as well as through private label relationships with major supermarket chains.

<<<

Tobacco Sector -- >>> 3 High Dividend Paying Stocks Worth Watching

By Madhu Dube

May 6, 2013

Tickers: MO, LO, RAI

http://beta.fool.com/madhudube/2013/05/06/3-high-dividend-paying-stocks-to-own/33109/?source=eogyholnk0000001

One of the major benefits of owning a stock from a maturing industry is that they pay good dividends. There are many companies that provide a good dividend yield, but my preference is companies that have a significant share of the maturing industry and are innovative, either in marketing or in product offerings.

I have picked three such companies from the tobacco industry -- Lorillard (NYSE: LO), Altria (NYSE: MO), and Reynolds American (NYSE: RAI) -- which are known for providing a dividend yield of more than 5%.

Company

5-Year Annual Average Dividend Yield

Lorillard

5.4%

Altria

6.5%

Reynolds American

6.5%

Betting on e-cig

Lorillard recently reported better than expected first-quarter results. It posted net sales of $1.58 billion, a growth of 3.3% year over year. Its operating profit was $438 million against analysts' estimate of $418 million. The company witnessed higher profitability because of a favorable pricing environment. In the traditional cigarette division, its prices increased 2.9%.

Lorillard also saw good response from the e-cigarette market. Its Blu e-cig generated retail sales of around $250 million. Lorillard is continuously expanding its geographic presence. Currently, this product is available in around 80,000 stores in limited stock-keeping units (SKUs). This provides an opportunity for further expansion into new markets in the form of adding more SKUs to the current stores. Considering this, the e-cig business looks on track to become a $1 billion business in 2013.

The company is also planning to launch a new rechargeable e-cig kit, which is expected to cost almost 50% less than traditional e-cig kits. This might dent profitability in the short run as the company will spend much in developing appeal for this product, but in the long run this will result in better sales.

Cashing with the retailers

Altria's first-quarter results gave a clear picture of the cigarette industry, where volumes are declining but profitability is increasing because of the better pricing environment and lower promotional spending. The company experienced a cigarette volume decline of 5.2%; however, this weak volume was offset by better pricing, which resulted in first-quarter profit of $1.38 billion.

It reported an increase of 4.9% per pack in net cigarette pricing. One of the positive catalysts for investors is the increasing market share of Marlboro. It currently has 43.6% market share, up 1% from the fourth quarter.

Additionally, the company is testing its Marlboro Leadership Price Two (MLP 2) program in Michigan and South Carolina. Under this program, retailers will have to increase the price by $0.10 per pack from the standard rate, and they will get $0.15 per pack in promo support from the company. The current MLP program gives retailers promo support of $0.20, but under this new program, retailers will increase prices, making it beneficial for them as well.

This will also improve profitability for the company and will lead to better acceptance of the higher prices by consumers. This will provide a platform for the company to increase prices in future. The company is currently testing this program in select locations to gauge consumer reaction.

Milking the cash cows

Reynolds experienced the highest volume decline of 8.7% in its first quarter among the three companies discussed. However, it reported improved profitability because of a 4% increase in net pricing. Strong quarterly pricing since the fourth quarter of 2011 has resulted in increased profitability despite high promotional spending.

Its top two brands, Camel and Pall Mall, are increasing market share, which is a good sign for the company in the midst of slowing volumes. Its Camel brand's market share is now 8.5%, up 0.1% year over year because its menthol version is gaining traction. Its Pall Mall brand has 9% market share, up 0.5% year over year due to better performance from the newly launched Pall Mall White and Pall Mall Black blends.

In the small but fast-growing e-cigarette market, sales of its Vuse brand will be expanded across many geographic locations this year. This provides a significant opportunity for the company, as it will have the advantage of launching its product in this category sooner than its largest competitor, Altria.

I don't think Reynolds will have any issue in providing dividends to investors in the long run, looking at share gain by top brands and opportunities in the e-cig market. I would recommend buying this stock for dividend seeking investors.

Harsh times, high profit

All these companies experienced declining cigarette volumes in the first quarter, but improved pricing should help these companies generate good profitability in future. Lorillard's should see an upside due to its growing Blu e-cig and its buyback program. Altria's should experience an upside as well from its new MLP program, which will improve its profitability.

Reynolds has faced the largest decline in volume, but its top brands, Camel and Pall Mall, which contribute to more than 50% of sales, are gaining market share. Its Vuse brand is also expected to gain traction once the company starts a complete rollout in the U.S.

There is no obvious issue which would cause the companies to reduce their dividend yield, so, for dividend-seeking investors, all three of these stocks are worth a watch.

Altria has been the best-performing stock of the past 50 years, but as the number of smokers in the U.S. continues to steadily decline, is Altria still a buy today? To find out whether everyone’s love-to-hate dividend stock is a savvy investment choice or a hazard to your portfolio, simply click here now for access to The Motley Fool's premium research report on the company.

<<<

Reeds -- >>> Reed's, Inc. Secures New Foodservice Private Label Partner

Press Release: Reed's, Inc.

Apr 23, 2013

http://finance.yahoo.com/news/reeds-inc-secures-foodservice-private-123000926.html

LOS ANGELES, CA--(Marketwired - Apr 23, 2013) - Reed's, Inc. (NYSE MKT: REED), maker of the top-selling sodas in natural food stores nationwide, announced today that it has secured a new agreement to produce a line of private label branded beverages for one of the largest foodservice distributors in the country.

Chris Reed, Founder and CEO of Reed's, Inc., commented, "Our unique production and flavor-crafting capabilities continue to attract interest from some of the largest supermarkets and foodservice corporations in the US. We are building some very exciting new relationships that we hope to leverage with our branded products. The margin dollars we gain from this new partnership will be reinvested into building more brand recognition for our Reed's, Virgil's and Reed's Culture Club Kombucha line of beverages."

About Reed's, Inc.

Reed's, Inc. makes the top-selling natural sodas in the natural foods industry sold in over 13,000 natural food markets and supermarkets nationwide. Its six award-winning non-alcoholic Ginger Brews are unique in the beverage industry, being brewed, not manufactured and using fresh ginger, spices and fruits in a brewing process that predates commercial soft drinks. The Company owns the top-selling root beer line in natural foods, the Virgil's Root Beer product line, and the top-selling cola line in natural foods, the China Cola product line. In 2012, the Company launched Reed's Culture Club Kombucha line of organic live beverages. Other product lines include: Reed's Ginger Candies and Reed's Ginger Ice Creams. In 2009, Reed's started producing private label natural beverages for select national chains. Reed's products are sold through specialty gourmet and natural food stores, mainstream supermarket chains, retail stores and restaurants nationwide, and in Canada, as well as through private label relationships with major supermarket chains.

<<<

Reeds -- >>> Reed's Inc. Announces Year-End 2012 Results

Press Release: Reed's Inc

http://finance.yahoo.com/news/reeds-inc-announces-end-2012-203534782.html

LOS ANGELES, CA--(Marketwire - Mar 25, 2013) - Reed's, Inc. ( NYSE MKT : REED ), maker of the top-selling sodas in natural food stores nationwide, today announced the financial results for its fiscal year ending December 31, 2012.

Financial Highlights for the Quarter:

•Revenues increased 20% to $30 million in 2012, compared to 2011.

•Gross profit increased 23% to $9.1 million in 2012.

•Earnings before non-cash items and finance costs (modified EBITDA) increased to $1 million during 2012. (See EBITDA table at end of this release for further non-GAAP information).

•Net loss for the 2012 fiscal year was $524,000 compared to a loss of $941,000 a year earlier.

•Working capital at December 31, 2012 was $2.3 million, as compared to $2.7 million at December 31, 2011.

Operational Highlights:

•Introduced our Culture Club Kombucha in July 2012 and increased distribution into a minimum of 800+ new retailers throughout the US and into select Whole Foods.

•Volume of branded Reed's and Virgil's products shipped grew at a rate of 20% over last year

•Expanded network of DSD distribution in numerous key regions increasing sales through this distribution channel by approximately 50%.

•Expanded distributor sales by over 30% by partnering in marketing efforts and focusing on sales support for distributors.

•Secured three new private label brand contracts with some of the largest retailers in the US

"2012 represents another solid year of growth here at Reed's," stated Chris Reed, Founder and CEO at Reed's Inc. "We have introduced an entirely new product line in our Culture Club Kombucha while we also expanded sales and distribution channels for our Reed's Ginger Brew and Virgil's branded products. Our EBITDA positive results have enabled us to fund our product rollouts and increased promotional spend without the requirement of additional equity or debt financing. We expect 2013 to be a great year."

James Linesch, Chief Financial Officer, stated, "Our strong business model is producing continually improving results in key areas. Our branded product revenues continue to increase at strong organic growth rates, while we also improved our gross margins. During 2012, our direct gross margin percentage, before promotional discounts, improved by an average of about 2%. Recurring general & administrative costs, before one-time costs, increased by less than 10% in 2012 while sales and gross profit contribution increased at over twice that rate, indicating improved economies of scale. Sales and marketing costs in 2012 were approximately 10% of net revenues, the same as in 2011. Our organizational structure is healthy and we have excellent brands that we are promoting in effective ways.

Linesch continued, "Our fourth quarter losses were primarily due to continued production challenges on our kombucha, resulting in higher unallocated plant costs, and to lighter than expected private label revenues from one customer. We have addressed the production issues surrounding our kombucha in our current quarter and we anticipate increased margin contribution going forward. Our underlying business is stronger than ever, however, and we feel that we have laid the foundation for improved financial performance in 2013."

The Company will conduct a conference call @ 4:15PM EDT on March 25th to discuss its 2012 fiscal year end results and outlook for the future. To participate in the call, please dial the following number 5 to 10 minutes prior to the scheduled call time (866) 578-1005. International callers should dial (713) 481-0091.

A replay will be available within a few days after the meeting in the investor relations section of the Company's website at: http://www.reedsinc.com/investors/.

About Reed's, Inc.

Reed's, Inc. makes the top-selling natural sodas in the natural foods industry sold in over 13,000 natural food markets and supermarkets nationwide. Its six award-winning non-alcoholic Ginger Brews are unique in the beverage industry, being brewed, not manufactured and using fresh ginger, spices and fruits in a brewing process that predates commercial soft drinks. The Company owns the top-selling root beer line in natural foods, the Virgil's Root Beer product line, and a top-selling cola line in natural foods, the China Cola product line. In 2012, the Company launched Reed's Culture Club Kombucha line of organic live beverages. Other product lines include: Reed's Ginger Candies and Reed's Ginger Ice Creams. In 2009, Reed's started producing private label natural beverages for select national chains. Reed's products are sold through specialty gourmet and natural food stores, mainstream supermarket chains, retail stores and restaurants nationwide, and in Canada, as well as through private label relationships with major supermarket chains.

<<<

Reeds -- >>> 8 Healthy Sodas

Sure, soda is unhealthy, but we all crave it now and again. These healthy sodas will give you a better bang for your buck.

BY EMILY MAIN

http://www.rodale.com/healthy-soda-0?cm_mmc=MSN-_-14%20Foods%20You%20Should%20Never%20Eat-_-Slideshow-_-8%20healthy%20sodas

We've said it before and will probably say it a hundred times more: Soda is toxic stuff. Not only is most of it full of diabetes-inducing high-fructose corn syrup, but drinking too much of the bubbly stuff has also been linked to an increased risk of heart attack and stroke. It contains genetically modified ingredients (GMOs) and phosphates, preservatives that have been linked to kidney disease and accelerated aging. Obviously, not something you want as part of a regular diet. But at some point, we all crave something fizzy, and that's no reason to reach for a toxic can of kidney-killing GMO water.

We looked high and low for healthy soda alternatives, free of the worst offenders in traditional sodas, such as GMOs or artificial caramel coloring that can be contaminated with carcinogens. Nor do any of our healthy sodas come bottled in cans, which are normally lined with hormone-disrupting bisphenol A. Some do contain cane sugar, a less-processed sugar that still should be consumed in moderation, and others are flavored with other sweeteners to avoid, but they're all far better alternatives to what's lurking in most soda cans. Next time a soda craving strikes, try one of these eight healthy sodas.

Steaz Sparkling Green Tea

Put down the Diet Coke! If you need an afternoon caffeine fix, grab a Steaz Green Tea soda instead. In addition to the fact that green tea is loaded with antioxidants, this no-cal soda alternative is sweetened with stevia and erythritol, a natural sugar alcohol. It's also fortified with vitamin B12, which helps improve your mood, your energy levels, and mental fog.

www.steaz.com

Reed's Light Extra Ginger Brew

Ginger ale, or ginger beer depending on who you're talking to, is a fantastic home remedy for nausea, upset stomachs, and even sore muscles, but 99 percent of what the big companies pass off as ginger ale contains tons of sugar and little to no real ginger. Not so with Reed's ginger brews, which contain the most ginger of any brand out there. And the company has just introduced a new "light" variety that, at just 55 calories per bottle, is sweetened with honey and stevia.

Virgil's Root Beer

Also from the purists at Reed's, Virgil's Root Beer is root beer made the way nature intended, by brewing a combination of herbs and spices naturally, rather than concocting a chemistry experiment of artificial flavorings, dyes, and additives. The ingredients list reads like the gatherings of a world traveler —anise from Spain, vanilla from Madagascar, molasses from the U.S., and balsam oil from Peru—and will get you off that artificial canned stuff forever. However, good as it is, this soda won't win you any favors with your waistline. At 160 calories per serving and 42 grams (g) of sugar, make it a weekly indulgence.

Bionade

This German brand may be hard to find, but it's worth it if you can get it. A naturally fermented drink made from malt and water, just like beer, this nonalcoholic soda has just 60 calories and 14 g of sugar per bottle, and it's certified organic. The sodas come in decidedly grown-up flavors like elderberry, lychee, ginger-orange, and herb, all invented by a former beer brewer. The sodas are so popular in Europe the company even rejected a takeover by Coca-Cola.

www.bionade.com

Oogave

Oogave is one of few certified-organic soda brands out there, and the line includes an honest-to-goodness organic cola alternative for people who love Coke or Pepsi. The company also has other cool flavors like strawberry-rhubarb and mandarin-key lime, the best organic alternative to Sprite or 7-Up. All the company's sodas contain half the sugar (24 g) that conventional sodas and other cane-sugar-sweetened sodas do. Plus, none of their products exceeds 100 calories per bottle.

www.thirstmonger.com

GT's Enlightened Organic Raw Kombucha

Not technically a soda, we had to throw in kombucha simply because it's so good and so good for you. Kombucha is tea that's been fermented with a probiotic culture, similar to the way vinegar is made, and the end product is low in sugar and full of healthy bacteria that aid digestion and even ward off infections. Fizzy like a soft drink, kombucha is much less sweet; these products contain just 4 g of sugar per bottle and only 60 calories. Try the slightly tart original kombucha or the fruitier citrus or ginger flavors.

www.synergydrinks.com

Hot Lips Soda

Made to "worship the magnificent fruits and berries" of the Pacific Northwest, this fruit soda is another winner, with the brand's lineup even changing with the seasons based on what's locally available—apples and pears in the fall and raspberries, blackberries, strawberries, and other berries in spring and summer. Some of the fruits are even organic. The company takes fruit, cooks it, adds water and cane sugar then bottles it, with much of the fiber-rich pulp intact, and carbonates it. Unlike a lot of so-called natural sodas, Hot Lips sodas contain organic lemon juice as a preservative, rather than ascorbic or citric acid, both of which can be derived from genetically modified corn and soy. For the healthiest Hot Lips drinks, grab the cranberry or pear sodas, neither of which has any added sugar.

Cranberry: 155 calories; Pear: 122 calories

www.hotlipssoda.com

Fizzy Lizzy

All Fizzy Lizzy sodas are nothing more than carbonated water combined with actual fruit juice, with a little vitamin C added for extra nutrition. The makers don't add sugar of any kind, so all the sugars in their sodas are naturally occurring. For the lowest-calorie options, go with the cranberry soda—just 100 calories per bottle and 22 g of sugars—or the grapefruit—also 100 calories with 25 g of sugar. Or give their award-winning pineapple soda a try, maybe mixed with some coconut water for a faux piña colada.

www.fizzylizzy.com

<<<

Reeds -- >>> Reed's Inc. Announces the Launch of Four New Flavors of Reed's Culture Club Kombucha

Press Release: Reed's, Inc

Feb 28, 2013

http://finance.yahoo.com/news/reeds-inc-announces-launch-four-133000217.html

LOS ANGELES, CA--(Marketwire - Feb 28, 2013) - Reed's, Inc. ( NYSE MKT : REED ), maker of the top-selling sodas in natural food stores nationwide, announced today that they have added four new flavors to their new Reed's Culture Club Kombucha line. The flavors are Pomegranate Ginger, Passion Mango Ginger, Cabernet and Coconut Water Lime.

Chris Reed, Founder, Chairman and CEO of Reed's Inc., stated, "We continue to have a great response to our initial four flavors of Kombucha and many requests are coming in from retailers around the country for more variety of flavors. Our first flavors were very inspired, with nouveau flavor combinations like Hibiscus Grapefruit Ginger Kombucha. In this new round of flavor development, we were compelled to be even more inventive, resulting in our new Coconut Water Lime Kombucha -- the first marriage of the fast growing coconut water and Kombucha beverage categories. Our new Cabernet Kombucha was inspired by our customers telling us they are using our Kombucha as a wine substitute. Since our third quarter 2012 launch, we have emerged as a clear front-runner in the competitive Kombucha category, establishing ourselves as the number two player. Our sights are clearly set to be number one."

About Reed's, Inc.

Reed's, Inc. makes the top-selling natural sodas in the natural foods industry sold in over 13,000 natural food markets and supermarkets nationwide. Its six award-winning non-alcoholic Ginger Brews are unique in the beverage industry, being brewed, not manufactured and using fresh ginger, spices and fruits in a brewing process that predates commercial soft drinks. The Company owns the top-selling root beer line in natural foods, the Virgil's Root Beer product line, and the top-selling cola line in natural foods, the China Cola product line. In 2012, the Company launched Reed's Culture Club Kombucha line of organic live beverages. Other product lines include: Reed's Ginger Candies and Reed's Ginger Ice Creams. In 2009, Reed's started producing private label natural beverages for select national chains. Reed's products are sold through specialty gourmet and natural food stores, mainstream supermarket chains, retail stores and restaurants nationwide, and in Canada, as well as through private label relationships with major supermarket chains.

<<<

Reeds -- >>> Q4 2012 revenue projection

Q4 - Dec 2012 -- at least 7.742 mil

Q3 - Sept 2012 -- 7.888 mil

Q2 - June 2012 -- 7.831 mil

Q1 - Mar 2012 -- 6.539 mil

Q4 - Dec 2011 -- 7.282 mil

Reeds -- >>> Reed's Inc. Announces Record Revenues of $30 Million for 2012

Press Release: Reed's, Inc

Tue, Feb 26, 2013

http://finance.yahoo.com/news/reeds-inc-announces-record-revenues-133000233.html

LOS ANGELES, CA--(Marketwire - Feb 26, 2013) - Reed's, Inc. ( NYSE MKT : REED ), maker of the top-selling sodas in natural food stores nationwide, announced today that annual revenues for 2012 increased 20% to more than $30 million.

Chris Reed, Founder, Chairman and CEO of Reed's Inc., stated, "Our Kombucha launch in 2012 continues to dominate our marketing efforts. It is not unusual for individual store sales of our Kombucha to exceed the sales of all our other products combined. We're working hard to expand these early successes to our full account base. Branded products continue fueling our expansion, growing at 20% for the fourth quarter and the early part of 2013. We expect full year 2013 to be just as strong, if not stronger for our core brands of Reed's Ginger Brews and Virgil's premium sodas.

Our private label business grew 23% for the year 2012. We have recently secured new private label contracts that will continue to fuel growth and drive incremental revenue for 2013. With the launch of new Reed's Culture Club Kombucha we have now diversified our business into three large revenue growth streams; Reed's Culture Club Kombucha, Reed's and Virgil's premium soda and private label. We are confident that our directional strategy will ensure that 2013 growth will outpace our performance in 2012."

About Reed's, Inc.

Reed's, Inc. makes the top-selling natural sodas in the natural foods industry sold in over 13,000 natural food markets and supermarkets nationwide. Its six award-winning non-alcoholic Ginger Brews are unique in the beverage industry, being brewed, not manufactured and using fresh ginger, spices and fruits in a brewing process that predates commercial soft drinks. The Company owns the top-selling root beer line in natural foods, the Virgil's Root Beer product line, and the top-selling cola line in natural foods, the China Cola product line. In 2012, the Company launched Reed's Culture Club Kombucha line of organic live beverages. Other product lines include: Reed's Ginger Candies and Reed's Ginger Ice Creams. In 2009, Reed's started producing private label natural beverages for select national chains. Reed's products are sold through specialty gourmet and natural food stores, mainstream supermarket chains, retail stores and restaurants nationwide, and in Canada, as well as through private label relationships with major supermarket chains.

<<<

>>> Study - All Plastics Are Bad for Your Body

A test of hundreds of plastic products reveals that nearly all, under varying circumstances, contain chemicals that interfere with your body's hormones.

By Emily Main

http://www.rodale.com/chemicals-plastic

Never mind the number...new research shows any kind of plastic can leach chemcials into your food.

It used to be that people who just couldn't break the plastic habit to go plastic-free could at least rely on certain types of plastics, usually those labeled #2, #4, or #5 in the triangle of arrows on the bottom, because those plastics weren't made using bisphenol A or phthalates, the two chemicals in plastic that are known to interfere with the way your body produces and handles estrogen. But a study published in the journal Environmental Health Perspectives concludes that there really are no "safe" plastics, thanks to all the chemicals, additives, and processing aids that go into making plastic products. In a test of nearly 500 chemical containers, the authors discovered that nearly all exhibited some kind of estrogenic activity.

THE DETAILS: The authors purchased 455 plastic products designed to hold food (including plastic bags and baby bottles) that were made from all different types of plastic. Some of the plastics tested, such as high-density polyethylene (#2 in the recycling triangle) and polypropylene (#5 in the recycling triangle), are considered safer plastics because, prior to this study, they hadn't been shown to leach chemicals. Some of the other plastics, such as corn-based plastics and newer so-called "BPA-free" plastic resins, were also tested. All the plastics were filled with substances mimicking food and then subjected to three types of stress—microwave heating, moist heat similar to what they might be exposed to in a dishwasher, and UV light (simulating a water bottle left in a car during the day or a baby bottle being subjected to UV sterilization).

The researchers were able to measure some type of estrogenic chemical leaching from roughly 95 percent of all the plastics tested, including 100 percent of the food wraps and 98 percent of the plastic bags. Even when the plastics were unstressed and just exposed to various solutions, they still leached estrogenic chemicals. And some of the baby and water bottles labeled "BPA free" showed greater estrogenic activity than polycarbonate bottles, which are made from BPA. When they were subjected to stress, the amount of leaching largely depended on what was in the packaging. For instance, some of the highest levels of leaching occurred in plastics containing saline solution when they were put in the microwave; saline is intended to mimic vegetables or other foods with a high water content. But baby bottles containing ethanol, which is intended to mimic milk and other foods with a higher fat content, leached more when exposed to UV light than they did when they contained a saline solution.

WHAT IT MEANS: There really aren't any "safer" plastics, and it's hard to predict which ones will leach estrogenic chemicals into your food. As this study shows, different plastics containing different types of foods will leach chemicals at different levels. That's largely because there are so many steps and additives in the plastic-making process, says George Bittner, PhD, professor of biology at the University of Texas in Austin and lead author of the study. "A plastic item can subsist of anywhere from five to 20 chemicals, some of which are additives, which are incorporated within the plastic polymer but not bound to the structure," he says. Both the materials that make up the plastic resin and the additives can leach out of plastics, says Bittner, who's also the CEO of CertiChem, the lab that tested the plastics in this study, and a consultant for PlastiPure, a company that works with plastic manufacturers to produce estrogenic-chemical-free plastics. You also have mold-release agents and colorants that are used to make or decorate the plastics, adds Mike Usey, CEO of PlastiPure, and those colorants tend to be highly estrogenic.

"We're not testing in a way that the industry has traditionally done this," Usey says. "We're not identifying specific chemicals, finding those, and then substituting another chemical. We're looking at the entire product." And that's where the industry has largely failed at keeping estrogenic chemicals out of products. He uses the example of baby bottles, which were once commonly made with BPA-based polycarbonate plastics. After parents started to demand BPA-free bottles, the industry switched to two primary alternatives, PETG and PES—hard, clear plastics that do not contain BPA. However, "we've done quite a few tests, and the level of estrogenic activity that we have found under certain conditions, especially under UV light, has been higher than with polycarbonate," Usey says. And, he adds, it's hard to pinpoint the source of the estrogenic activity without knowing the exact makeup of the plastic and any processing aids, additives, or colorants used in the final product. "Since the health effects [of estrogenic chemicals] occur at such a low level, it doesn’t take much for something to be highly estrogenic," he adds.

Usey and Bittner don't think people should eliminate plastics from their lives entirely. "I think plastics are great—they just need to be made safer," Usey says. Bittner adds, "Consumers should request from the stores where they buy plastics that those stores start supplying them with plastics that are free of estrogenic activity."

Until that happens, you can purge your home of estrogenic chemicals by adopting a plastic-free life:

• Revamp your food storage. Glass, ceramic, and stainless steel are great food-storage materials that can go from stove to fridge to freezer easily.

• Buy less processed food. Most processed foods in the grocery store come in some form of plastic packaging. Buying fresh vegetables and ingredients in bulk (which you can package in your own plastic-free containers) will help you avoid most of it.

• BYO… You may already carry a reusable mug and reusable shopping bags to eliminate some plastics, but take the next step and start carrying reusable produce bags, too, when you shop. Like other forms of plastic, those flimsy plastic produce bags can leach hormone-disrupting chemicals into your berries and broccoli, and they're hard to recycle once they're contaminated with food. You can find regular and organic cotton produce bags online at Ecobags.com.

<<<

>>> 10 Food Label Lies

Don’t spend extra money buying into marketing hype and misinformation. Look for food claims and labels you can trust.

By Emily Main

http://www.rodale.com/10-food-label-lies

Truth in Labeling?

With the economy still keeping our wallets clamped shut, no one wants to feel duped at the checkout counter. Yet, savvy food marketers have managed to tap into all our concerns over food safety and purity, labeling their products with words in phrases that, at best, are pointless, and at worst, are illegal. Here are 10 of the most deceptive marketing claims out there that make processed foods and factory-farmed meats appear much healthier than they really are.

No added growth hormones

The lie: Usually, you’ll see this claim in ads for chicken, turkey, or even pork, along with milk and beef labels. Why is it misleading? The U.S. Department of Agriculture doesn’t allow farmers to feed hormones to poultry or pork. In fact, if you read the fine print, any poultry or pork product that is advertised as “hormone free” must legally be accompanied by the disclaimer “Federal regulations prohibit the use of hormones.” Producers of those meats use antibiotics instead, which speed growth in the same way as hormones; the USDA calls this “increasing feed efficiency.” Even when you see this label on beef or dairy products—products where hormones are legally allowed—it hasn’t been verified by a third party, so you're really taking the food marketer's word for it.

To get the real thing: Buy certified organic meat and dairy, which are free of both added growth hormones and antibiotics, and organic poultry products. Or, buy from small farmers whom you can ask about how they raise and medicate their animals.

Natural